?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This paper investigates the joint and separate effects of Environmental (E), Social (S), and Governance (G) scores on bank stability. Using a sample of European banks operating in 21 countries over 2005–2017, we find that the total ESG score, as well as its sub-pillars, reduces bank fragility during periods of financial distress. This stabilizing effect holds strongly for banks with higher ESG ratings. These results are confirmed by a differences-in-differences (DID) analysis built around the introduction of the EU 2014 Non-Financial Reporting Directive (NFRD). Our evidence also reveals that, in times of financial turmoil, the longer the duration of ESG disclosures, the greater the benefits on stability. Finally, we show that the ESG–bank stability linkages vary significantly across banks’ characteristics and operating environments. Our findings are robust to selection bias and endogeneity concerns. Overall, they support the regulatory effort in requiring an enhanced disclosure of non–financial information.

1. Introduction

The global financial and European sovereign debt crises renewed the interest on firms’ engagement in Corporate Social Responsibility (CSR).Footnote1 The recent literature on its effectiveness in enhancing firms’ performance is rich, although results tend to be mixed (e.g. Lee and Faff Citation2009; Margolis, Elfenbein, and Walsh Citation2009; Oikonomou, Brooks, and Pavelin Citation2012; Albertini Citation2013; Dixon-Fowler et al. Citation2013; Friede, Busch, and Bassen Citation2015). In addition, only a few studies focus on risk (Luo and Bhattacharya Citation2006; Bouslah, Kryzanowski, and M’Zali Citation2018) and for banks these typically examine single CSR aspects, such as the environmental dimension (Gangi et al. Citation2019) and governance (Berger, Imbierowicz, and Rauch Citation2016; Anginer et al. Citation2018).

Two main views explain the relationship between CSR and risk (Bouslah, Kryzanowski, and M’Zali Citation2018)Footnote2: (i) the risk mitigation; and (ii) the overinvestment view. The former derives from a risk management argument based on the stakeholder theory and the value created by moral capital (Godfrey, Merrill, and Hansen Citation2009; Luo and Bhattacharya Citation2006). The latter originates from the agency theory and focuses on opportunistic managerial behaviour: managers may improve sustainability scores for the sake of their own reputation as responsible social citizens (Barnea and Rubin Citation2010). The two views offer opposite predictions: negative in the risk mitigation view, by decreasing the probability of adverse events firms obtain greater resilience during shocks (such as a crisis and an economic downturn); and positive in the overinvestment view due to managerial entrenchment.

In recent years, banks have increasingly perceived sustainability as a means to increase their reputation, and also to promote trust and credibility (Schultz, Castelló, and Morsing Citation2013; Park, Lee, and Kim Citation2014). Whether this ultimately mitigates the effect of the financial crisis has not yet been tested in the banking literature. In this study we conjecture that the channel through which this may occur is via bank stability, measured by default risk.

This paper provides three main contributions to this stream of literature. First, despite several studies have addressed the relationship between CSR and firm risk, ours is the first to consider the European banking sector and to use a market-based measure of default risk (Distance to Default). The focus on Europe is especially relevant, since many countries in this region pioneered sustainability practices, with EU banks leading compared to those headquartered elsewhere (Ho, Wang, and Vitell Citation2012). In addition, from a regulatory perspective, major steps have been taken to enhance disclosures on non–financial information and diversity.

In 2014 the EU adopted the Non-Financial Reporting Directive (2014/95/EU) that required certain large companies, including banks, to disclose information on the way they operate and manage social and environmental challenges. More recently, the EU has demonstrated a strong commitment to step up efforts to addressing these issues.Footnote3 In addition, in October 2020, the European Banking Authority (EBA) issued a discussion paper on the management and supervision of ESG risks for credit institutions and investment firms (EBA Citation2020). In November 2020, the European Central Bank announced, after a public consultation, that banking stress tests that will be held in 2022 will also include consideration of climate-related risks (ECB Citation2020). Similar initiatives are currently under way also outside the European Union or are even developed at the global level by the banking industry itself. For example, the Climate Biennial Exploratory Scenario (CBES) in the UK, that assesses the resilience of the financial system to climate risks (Bank of England Citation2021a)Footnote4; and the ‘Principles for Responsible Banking’, that are a voluntary framework ensuring that banks’ strategy and practice align with the vision society has set out for its future in the UN Sustainable Development Goals and the Paris Climate Agreement. The Principles are currently signed by 235 banks from 69 countries, representative of 60 trillion USD total assets.

Our second contribution to the literature is that we use the whole set of information provided by Environmental, Social and Governance (ESG) scores as a proxy for CSR performance (Chang, Kim, and Li Citation2014; Eccles, Ioannou, and Serafeim Citation2014; Kim, Li, and Li Citation2014; Sassen, Hinze, and Hardeck Citation2016). ESG scores are aggregate variables resulting from weighting several heterogeneous indexes: Environmental (E), that includes sustainable use of resources, emissions and innovation in reducing environmental footprints; Social (S), that comprises for example, job satisfaction, workplace health and safety, diversity, equality and human rights; and Governance (G) activities, that includes for example compliance with best practices, equal treatment of shareholders, integration of non–financial objectives in strategic and managerial decisions.

Thirdly, this paper explores the relationship between ESG scores and bank stability over a relatively long period (2005–2017) that covers the global financial sub-prime and European sovereign debt crises. By means of an interaction term, confirmed by the results of a series of robustness checks based on alternative measures, we verify whether the effect on bank stability is affected by the economic cycle. To our knowledge, this is the first study to provide a similar evidence.

We postulate that the ESG–bank stability linkage may reward higher scores, especially during crisis times. This expectation is tested using a differences-in-differences (DID) framework built around the introduction in 2014 of the EU’s Non-Financial Reporting Directive. Additionally, the relatively long-time span allows us to investigate the impact of the duration of ESG disclosures for each entity: this is the first empirical evidence on this measure of banks’ ESG commitment. Finally, by adopting a heterogeneous cross–country sample of European banks, we can assess whether the ESG–bank risk relationship is driven by other firms’ characteristics (e.g. size) and a different operating environment (financial system orientation and per-capita income levels).

Our empirical results show that, when considering aggregated ESG scores, engagement in CSR practices is associated with higher stability (i.e. lower default risk) during crises years. It also seems to encourage more prudent banking activities, fostering more stable relationships with the financial community and enhancing reputation. These aspects are crucial in mitigating the potential adverse impact of negative events that typically occur during a crisis. We also find that all ESG sub–pillars participate to this association: the development of environmental technologies and processes optimizing the use of resources; the fair treatment of the workforce; banks’ responsibility to produce quality goods and services integrating the customers’ health, safety, integrity and data privacy; a bank’s capacity to guarantee equal treatment of all shareholders and promoting anti-takeover devices. Thus, bank management strategies that combine these practices seem able to mitigate bank instability during financial slowdowns. Our results are robust to selection bias and endogeneity concerns. In addition, we show that the stabilizing effect observed in crisis years holds strongly for banks with higher ESG scores, through a differences-in-differences setting. We also find that the longer the duration of ESG disclosures, the greater are the benefits, implying that both the level and the commitment of a bank’s engagement matter, even if disclosures become mandatory.

Interestingly, our evidence indicates that the composite ESG score exerts a different impact on financial stability depending on banks’ characteristics and on differences in the operating environment. More specifically, we observe that only the largest European banking groups subject to the EBA’s stress tests experience improvements in financial stability during crisis periods. Finally, we find that ESG strategies are more beneficial in more bank–oriented financial systems and in countries with higher per-capita income levels.

In terms of policy, our results support the European regulatory commitment on mandatory disclosures on non–financial reporting for larger entities: how to improve such benefits and extend them also to smaller institutions are open questions for both policy-makers and academic research.

The remainder of the paper is organized as follows. Section 2 reviews the literature and formulates our hypotheses. Sections 3 describes the empirical methodology, the sample and the variables used. Section 4 discusses the main results. Additional analyses and robustness checks are presented in Section 5. Finally, Section 6 concludes and offers some policy implications.

2. Literature review and hypotheses development

Over the past two decades, CSR received a growing interest from researchers, practitioners, and regulators. Most published empirical studies focused on its role in terms of enhanced performance, assessing its impact within and outside firms and measuring its multi–dimensional components. Evidence is not definitive and is subject to several methodological difficulties (Margolis, Elfenbein, and Walsh Citation2009). Most empirical works tend to use proxies that typically focus only on one aspect, such as employee satisfaction (Edmans Citation2011, Citation2012; Edmans, Li, and Zhang Citation2014); environmental protection (Dowell, Stuart, and Yeung Citation2000; Konar and Cohen Citation2001); corporate philanthropy (Masulis and Reza Citation2015; Liang and Renneboog Citation2016); or consumer satisfaction (Luo and Bhattacharya Citation2006; Servaes and Tamayo Citation2013). Only recently, research begun to exploit the greater level of cross–firm and industry data availability and scope offered by ESG disclosure scores (Liang and Renneboog Citation2017).

Many studies analyse the implications of sustainable practices primarily within non–financial corporations (Santis, Albuquerque, and Lizarelli Citation2016; Godfrey et al. Citation2020). Yet, several works have emphasized that the role played by banks in allocating capital and fostering economic growth should encourage more research (Beck, Demirgüç-Kunt, and Levine Citation2010; Levine Citation2005), beyond financial performance. Despite a growing body of evidence points to the positive impact of sustainable practices on banking profitability (Wu and Shen Citation2013; Cornett, Erhemjamts, and Tehranian Citation2016; Gangi et al. Citation2019; Nizam et al. Citation2019; among others), whether and how ESG activities affect bank risk remains a fundamental and open question.

To the best of our knowledge, there are no published studies on this topic in a broader ESG context and with a focus on bank stability or risk-taking. Existing papers examine only one ESG aspect: for example, Anginer et al. (Citation2018) find that a subset of corporate governance (shareholder friendliness) leads to higher stand-alone and systemic risks, especially for larger banks or with stronger safety nets, while Gangi et al. (Citation2019) argue that more environmentally engaged banks exhibit less risk. Given this gap in the literature and the importance of the issue, a key contribution of this paper is hence to link bank stability and all ESG dimensions by searching for robust evidence of a risk reduction channel, in the specific context of financial crises. Moreover, we aim at providing findings that are robust from issues of reverse causality and endogeneity, that frequently affect the analysis of CSR effects on risk and performance (Bénabou and Tirole Citation2010).

The theoretical literature on the link between CSR and risk provides two main views. The ‘risk mitigation view’, within the stakeholder theory, posits that greater investments in CSR act as insurance for firms that create moral capital or goodwill among stakeholders (Godfrey Citation2005; Godfrey, Merrill, and Hansen Citation2009; El Ghoul and Karoui Citation2017). This may prove to be a considerable advantage during periods of financial turmoil and economic decline. Instead, the ‘overinvestment view’ considers CSR investments as a waste of resources and implies a positive association with firm risk derived from managerial entrenchment. Managers may seek to overinvest in CSR for their private benefit or personal reputation (Barnea and Rubin Citation2010), or to gain support from activists (Cespa and Cestone Citation2007). Closely connected with the risk mitigation view, one should also consider the risk implications of the relationship between social performance and expected returns (Bouslah, Kryzanowski, and M’Zali Citation2018), through the effects of idiosyncratic risk in asset pricing (Boutin-Dufresne and Savaria Citation2004; Lee and Faff Citation2009), hence predicting a negative relationship between CSR and risk.Footnote5

If CSR is associated with a perceived lower risk from market participants, this should also lower the cost of capital, reduce agency and asymmetric information issues (El Ghoul et al. Citation2011) and reduce capital constraints hence leading to better access to finance (Cheng, Ioannou, and Serafeim Citation2014). Additionally, CSR has also been found to enhance bank earnings quality (García-Sánchez and García-Meca Citation2017). In the non–financial sector, CSR activities seem to reduce losses in market shares for high levels of leverage (Bae et al. Citation2018), to be negatively correlated with stock price crash risks (Kim, Li, and Li Citation2014) and to improve credit ratings (Attig et al. Citation2013): similar effects may be present also in the banking industry. Finally, sustainability may be used strategically by managers as a risk mitigating tool towards adverse consequences of negative events (Godfrey, Merrill, and Hansen Citation2009; Attig et al. Citation2013; McCarthy, Oliver, and Song Citation2017). Consistently, recent evidence underlines an insurance-like role of sustainable practices during the global financial crisis (Lins, Servaes, and Tamayo Citation2017), especially against idiosyncratic risk (Godfrey, Merrill, and Hansen Citation2009).

We hypothesize that higher ESG scores may be associated with more prudent and sustainable banking activities, reducing the overall risk. Moreover, this effect should be stronger when negative events occur, especially during crisis years: benefits for companies from CSR engagement strongly emerge when unexpected declines in trust occur. Consistently with recent findings on non-financial enterprises (Lins, Servaes, and Tamayo Citation2017), we conjecture a positive role played by ESG scores in enhancing market trust and stability for banks during financial turmoil. Our prediction is based on the moral capital theory, which sees CSR as an insurance-like strategy for shareholders value maximization, by mitigating stakeholders’ conflict in the event of a crisis (Bouslah, Kryzanowski, and M’Zali Citation2018).

H1. Banks with higher ESG scores are less risky, especially during a financial crisis.

Most studies focus on proxies related to one ESG dimension (Berger, Imbierowicz, and Rauch Citation2016; Anginer et al. Citation2018; Gangi et al. Citation2019). We differentiate our study from previous research by examining the ESG–bank risk linkage disaggregating all its components. Due to the heterogeneity of CSR activities, reflected also in ESG measurement methodologies (Liang and Renneboog Citation2017),Footnote6 there are significant interconnections across its components (Galbreath Citation2013). Nonetheless, the existing literature has suggested that each pillar of ESG should play a significant role on banks’ stability.

In general, one could anticipate a weak link between the Environmental pillar and banks, in contrast with non–financial firms. Evidence from the latter shows that environmentally pro–active corporations experience a reduction in perceived riskiness from investors (Feldman, Soyka, and Ameer Citation1997) and that environmentally–friendly activities are associated with better stakeholder engagement (Cheng, Ioannou, and Serafeim Citation2014). Bouslah, Kryzanowski, and M’Zali (Citation2013) argue that on one side this effect arises from reduced compliance costs for environmental regulations (less likely to impact banks), but also from improved image and loyalty of key stakeholders (potentially holding also in the banking sector). Gangi et al. (Citation2019) document a robust negative association between environmental friendliness of banks and their risk. The authors argue that there are direct and indirect effects at work derived from different channels on the costs or stability of funding: the lending channel, operational efficiency, reputation, and loyalty of customers. Furthermore, environmental performances directly link to stakeholder confidence by strengthening the moral dimension of firms, and thus enhanced reputation (Godfrey Citation2005). Therefore, in line with the moral capital theory, we explore environmental banks practices role in restoring trust during exogenous confidence downturns, such as financial crises.

H2. Environmental activism reduces bank risk-taking, especially during a financial crisis.

With reference to the Social component, we expect that more attention on the improvement of human rights and employee relations and generally promoting workforce conditions and morale, could encourage a better culture and more effective screening and monitoring of loans, ultimately reducing banks’ overall risks. However, this risk-mitigating effect may not be as explicit as financial derivatives in shielding banks from market shocks (Buston Citation2016). A positive link between workforce-related social aspects and stability is advanced by several scholars (see Bauer, Derwall, and Otten Citation2007 in terms of commitment, loyalty and cost of litigation; Kane, Argote, and Levine Citation2005 on cooperation and trust). Bouslah, Kryzanowski, and M’Zali (Citation2018), argue that firms with higher social performance have also higher moral capital, turning into a higher valuation of performance from stakeholders. Additionally, most interactions with stakeholders occur through incomplete contracts, that an exogenous shock may jeopardize. Therefore, high social capital during a crisis could mitigate this concern (Lins, Servaes, and Tamayo Citation2017), leading to superior bank stability. For our purposes, high social engagement enhances bank stability by strengthening stakeholder trust and market participants confidence.

H3. Bank instability is inversely related to the level of social engagement, especially during a financial crisis.

Concerning Governance, the link with stability is generally consistent with regulation and supervision (Dell’Atti et al. Citation2017). Several banking crises have been associated, at least partially, with poor governance or conduct of management (Dowling Citation2006). However, this link is not always confirmed empirically (Stulz Citation2016). The extensive literature survey on the relationship between governance and bank risk-taking provided by Berger, Imbierowicz, and Rauch (Citation2016) and Anginer et al. (Citation2018) shows how relevant and complex is this relationship. The latter document how a shareholder-friendly governance increases both stand-alone and systemic risks in banks, and this behaviour is different than in non–financial firms due to the presence of explicit and implicit safety nets. Similarly, a greater shareholder orientation seems to be associated with greater losses during the crisis (Beltratti and Stulz Citation2012; Leung, Song, and Chen Citation2019). Mollah and Liljeblom (Citation2016) find that banks with more powerful CEOs performed better and reduced their asset risk during the sovereign debt crisis than during the credit crisis, despite accepting higher insolvency risk. Their results also suggest that board independence is associated with greater bank solvency.

According to the stakeholder view, the governance pillar should be positively associated with bank stability due to the lower incentive to pass–through risks (Kirkpatrick Citation2009). Stakeholder-oriented corporate governance may be pivotal in strengthening social purposes and boosting bank moral capital. In this paper, we explore the relevance of stakeholder-oriented corporate governance in enhancing bank resilience, during a period of lack of trust, such as the global financial crisis. However, the relationship between governance and bank stability is particularly complex to disentangle. Gaganis et al. (Citation2020) explore in detail this issue for a large cross-country sample, concluding that the positive impact of corporate governance on bank stability emerges when macroprudential policies increase. The role of these policies appears particularly strong in reducing the likelihood and severity of financial crises.

H4. Fair governance practices positively affect bank stability, especially during a financial crisis.

As discussed in the introduction, CSR engagement does not fall outside the scope of regulation: particularly in recent years regulators have been pushing for more controls and action on sustainable finance and banking. In 2014 the EU adopted the Non-Financial Reporting Directive (NFRD), that emphasized the importance of disclosure requirements for firms to include environmental and other non-financial performance; in 2018 the European Commission published an action plan that sets out an EU strategy on sustainable finance and a roadmap for future work across the financial system (EC Citation2018). In 2021, the EC also adopted a broad set of measures aimed at fostering the funding of sustainable activities and achieve climate neutrality by 2050 (EC Citation2011).

Literature on the consequences of such norms on banks is scant. Chen et al. (Citation2018) investigate firms’ reaction to China’s 2008 requirement to disclose CSR activities, documenting an increasing of firm sustainable engagement at the expense of performances. Grewal, Riedl, and Serafeim (Citation2019), by examining the equity market reaction to passage of the EU 2014 NFRD, show a negative association for EU firms. The documented reaction appears to be less negative for firms with higher pre-directive non-financial performance and non-financial disclosure levels.

In a recent study, Jackson et al. (Citation2020) find that the effect of mandatory social responsibility behaviour led to a significant increase in the CSR engagement in firms operating in 24 OECD countries, although this did not translate in lower corporate irresponsibility. Similarly, a pilot study by Fiechter, Hitz, and Lehman (Citation2020) provide evidence that EU firms increased their CSR activities immediately after the adoption of the 2014 EU NFRD, thus confirming that, at least in Europe, regulation was the right institutional answer to stakeholders’ recent call for more corporate socially responsible behaviour. Specifically, the EU Parliament, adopted a mandatory ‘comply or explain’ approach which obliges firms to identify and justify any areas of non-compliance.

In this paper, we rely on the structural importance of the 2014 EU NFRD and aim at testing whether more ESG engaged banks were affected differently by the directive compared to others. We expect therefore to find two possible consequences; (i) an increase in compliance costs for banks, which negatively affect their performance (Chen et al. Citation2018); (ii) a rewarding effect for banks more engaged in ESG practices, which is reflected by a positive impact on their performance (Bouslah, Kryzanowski, and M’Zali Citation2018), consistently with the moral capital theory framework.

H5: The EU 2014 Non-Financial Reporting Directive (NFRD) rewarded banks more engaged in CSR practices.

3. Methodology and data

3.1. Empirical strategy

Our methodology consists of two steps. In the first step, we empirically investigate the relationship between CSR engagement (proxied by ESG scores) and bank stability in a setting that is robust to potential endogeneity issues. We follow Wintoki, Linck, and Netter (Citation2012) using the improved system version of the generalized method of moments (GMM) estimator proposed by Blundell and Bond (Citation1998) and built on the work of Arellano and Bover (Citation1995). Moreover, to better control for the issue of reverse causality, we run the instrumental variables (IV) two-stage least squares (2SLS) regression estimator (see Section 5).

Banks with better financial performance could be simultaneously more stable and more inclined to invest in CSR strategies (Bénabou and Tirole Citation2010; Chih, Chih, and Chen Citation2010). The consistency of the system GMM model depends on the assumption that the error term is not autocorrelated and on the validity of the instruments used. Two specification tests are reported. The first is the Hansen test of overidentifying restrictions, which examines the validity of the instruments by analysing the sample analogue of the moment conditions used in the estimation procedure. The second test examines the hypothesis of no autocorrelation in the error term. The presence of first-order autocorrelation in the differenced residuals does not imply that the estimates are inconsistent; however, the presence of second-order autocorrelation does.

We employ the two-step system GMM estimator (or linear dynamic panel data) with Windmeijer corrected standard errors.Footnote7 Lagged non-binary explanatory variables are used to address endogeneity. Second and higher-order lags and differences of the dependent variable are used as instruments to avoid the endogeneity concern occurring from the inclusion of the lagged dependent variable. In all specifications the number of instruments employed is smaller than the group under investigation (Roodman Citation2009). The lagged dependent variable is treated as endogenous while all the remaining explanatory variables are exogenous. We use the following equation for the model:

(1)

(1) where the one-year Merton’s Distance to Default (DTD) is the stability measure of bank i at time t (the year in progress), that we employ as a market-based measure following Hassan, Khan, and Paltrinieri (Citation2019) and Anginer et al. (Citation2018).

We collect probability of default (PD) data from Bloomberg and we estimate Distance to Default as the inverse standard normal cumulative distribution function of the PD (Jessen and Lando Citation2015). The higher are DTD values, the lower is the risk of bank default.Footnote8 To mitigate the effects of outliers, the dependent variable is winsorized at the 1% of each tail.

In line with previous research (Galbreath Citation2013; Kim, Li, and Li Citation2014; Crifo, Forget, and Teyssie Citation2015; Sassen, Hinze, and Hardeck Citation2016; among others), we proxy the CSR engagement (our target variable) through ESG scores. We have different variables of interest (see Section 3.3), because we also disaggregate ESG scores om pillars and constituents (e.g. emissions, environmental product innovation, human rights, shareholders, etc.). Each target variable is interacted with the crisis years dummy (D_CRISIS), that equals 1 during the global financial and European sovereign debt crises periods (2008–2012) and 0 otherwise (2005–2007 and 2013–2017).Footnote9 This econometric approach allows us to verify whether ESG scores’ effect on bank stability depends on economic cycles (Lins, Servaes, and Tamayo Citation2017).Footnote10

Moreover, consistently with studies examining the relationship between CSR and firm risk (Bouslah, Kryzanowski, and M’Zali Citation2013; Sassen, Hinze, and Hardeck Citation2016; Gupta and Krishnamurti Citation2018), we control for additional variables that may affect bank stability, both bank-specific (namely size, capitalization, credit risk, efficiency, profitability, liquidity, income diversification, ECB’s unconventional liquidity injections proxied by the Very Long–Term Refinancing Operations, VLTROsFootnote11), and country-specific (industry concentration, economic growth, strength of capital regulation and supervision).

Table defines our variables, data sources and expected signs. To mitigate the effect of outliers, accounting-based control variables (SIZE, ETA, LLR_GL, CIR, ROAE, CASH_TA, and DIV) are winsorized at the 1% level on both tails.

Table 1. Variable definitions and expected relationships vs bank stability.

Standard errors are clustered at the bank-level. Finally, c is a constant term, the variable vi is the unobserved bank-specific-effect and µit is the idiosyncratic error.

The second step involves exploiting the effects of the Non-Financial Reporting Directive (NFRD), issued in late 2014 (Directive 2014/95/EU), in a differences-in-differences (DID) setting. All banks in our sample are listed, with more than 500 employees, so they were affected by the NFRD, yet they differ in their CSR engagement at the time of enforcing the directive.

More specifically, the NFRD requires certain large public-interest entities to disclose their performance on a range of non-financial dimensions alongside their accounts, on a ‘comply or explain’ basis. These dimensions, despite being labelled differently (‘respect for human rights’ or ‘diversity on board of directors’), are all within the scope of ESG scores. Therefore, having only firms within the scope of the directive in our sample (EU-based large listed banks that are those for which consistent ESG scores are available), allows us to further analyse the relationship between ESG and bank stability by comparing their performance before and after 2014, and in particular focus on the behaviour of entities that already achieved higher ESG scores before the Directive.

This represents the ideal setting to investigate our fifth hypothesis (H5), both an ordinary least square (OLS) and a panel data with and without fixed-effects models, over the period 2012–2017:

(2)

(2) where the dummy D_SHOCK representing the introduction of the NFRD that takes value 1 for post-treatment years (2015–2017) and 0 otherwise. The dummy D_TREATED takes value of 1 for banks above average values of ESG scores in the year of the shock (2014) and 0 otherwise, and D_SHOCK*D_TREATED represents their interaction. Therefore, the coefficient of D_SHOCK*D_TREATED is our target variable. We further control for a set of bank and country characteristic, as well for the same fixed effects employed in our baseline model (see Equation (1)).

To address the potential bias arising from treated and control groups heterogeneity (banks above or below average values of ESG scores), we employ a propensity score matching (PSM) procedure (Rosenbaum and Rubin Citation1983). This procedure requires the following steps. To identify the control group, we first run a logit model to calculate propensity scores of being a high-ESG bank, employing all non-binary bank-level control variables (SIZE, ETA, LLR_GL, CIR, ROAE, CASH_TA, and DIV) and including bank fixed-effects (Bhandari and Javakhadze Citation2017) for the period before the introduction of the Directive (2012–2014). We then match, without replacement, each treated bank to a control bank using the Nearest Neighbour matching (see e.g. Chang et al. Citation2019). Finally, we run the DID regression on the resulting matched sample and carry out a battery of robustness checks, as detailed in Section 5.

3.2. Sample description

The analysis focuses on banks headquartered in European countries, with data available from Thomson Reuters’ Refinitiv on ESG scores (our variable of interest), both at composite and individual levels during the period 2005–2017 (the last data available).Footnote12 These scores are designed to transparently and objectively measure a company’s relative ESG performance, commitment and effectiveness across 10 main themes (emissions, environmental product innovation, human rights, shareholders, etc.) based on company–reported information (e.g. annual reports, non-governmental organizations websites, and media outlets). The database provides ESG scores data on approximately 1,000 companies (mainly U.S. and European) as of 2002.

These criteria significantly restrict our sample, despite the Heckman two-step model confirms the absence of sample selection bias (see Section 5). Firstly, non–financial disclosures became mandatory in 2014 and only for large firms (Directive 2014/95/EU). Additionally, firms can decide not to report ESG scores to Thomson Reuters’ Refinitiv database.Footnote13 Finally, since Thomson Reuters does not specify the reason for missing values on ESG scores, it would be biased to compare banks that do not disclose this information with those that do.

The final sample consists of 84 banks that cover 21 European countries belonging to Eastern (5), Western (6), Northern (6) and Southern (4) Europe (Table A3). All banks are listed. In addition, half of our sample banks are included in the EBA’s stress tests for large banks. We concentrate on Europe for the following reasons. Firstly, ESG is particularly relevant in this area: according to the literature, European companies lead if compared to others (Ho, Wang, and Vitell Citation2012). Secondly, the European Union passed the Directive 2014/95/EU fostering the role of non-financial information disclosure of firms. Finally, there is limited research linking ESG to risk within the EU.

The data collected are year-end observations over a relatively long period (2005–2017) that includes the global financial and European sovereign debt crises. By means of an interaction term, we investigate whether the effect on stability depends on economic and/or financial conditions. Data is available only yearly: we are therefore unable to conduct the analysis with higher frequency.

3.3. Measurement of ESG variables

ESG terminology first appeared in the United Nations Principles for Responsible Investment (PRI) and then in several companies’ CSR reports (Davis and Stephenson Citation2006). Although there is no univocal identification of this concept yet, ESG scores have already been extensively used by consulting firms, financial advisors, and asset managers. Bassen and Kovacs (Citation2008) argue that ESG scores monitoring and disclosures play a key role in developing CSR strategies and allow investors to assess firms’ risks and opportunities. Therefore, ESG scores are currently the leading proxies of CSR engagement (Liang and Renneboog Citation2017).

The granularity of information provided by Thomson Reuters’ Refinitiv database allows us to extend the analysis beyond the overall composite score, including its three pillars as well as their individual components. Table A1 in the Appendix summarizes the taxonomy of ESG scores, their definition, calculation, and weights used for computation accordingly to Thomson Reuters’ methodology. All ESG scores range between 0 and 1, with higher values indicating stronger performance in sustainability practices.

To verify H1, on the joint effects of Environmental, Social, and Governance scores on bank stability, we use the ESG composite score (ESG). It captures a balanced view of the banks’ performance in the three areas (ENV, SOC, and GOV) through an explicit weighted combination of a series of firm-specific indicators that proxy results towards sustainability practices. We hypothesize a positive relationship with our dependent variable (DTD): higher total ESG scores are expected to be linked with more prudent banking activities (especially due to a long-term perspective and a stakeholder-based view) and decrease bank risk.

Since each ESG dimension bears its own identity (Oikonomou, Brooks, and Pavelin Citation2012; Bouslah, Kryzanowski, and M’Zali Citation2013), our analysis is repeated by breaking down composite scores, firstly into its three pillars and then into its sub-components (see the Appendix for further details), to avoid confounding the effects of individual dimensions (Griffin and Mahon Citation1997; Johnson and Greening Citation1999).

The second target variable is the Environmental score (ENV), resulting from the weighted average of three constituents: Resource Use; Emissions and Innovation. Based on our second hypothesis (H2), we expect a positive sign, because banks may be (or perceived) less risky if they integrate environmental issues in their lending policies (Goss and Roberts Citation2011), by excluding borrowers more exposed to changes in environmental regulation; could improve their operational efficiency (Fiordelisi, Marques-Ibanez, and Molyneux Citation2011; Clarkson et al. Citation2015; Gangi et al. Citation2019); through improvements in their reputation (Ruiz, García, and Revilla Citation2016; Aramburu and Pescador Citation2017), or not being associated with controversial firms. We expect this relationship to hold also when performing the baseline model on the three distinct components at the same time.

To test for H3, we focus on the Social score (SOC), based on the following four indicators: Workforce; Human rights; Community and Product Responsibility. We expect a positive sign on both the total SOC score and its four constituents. This because lending and investing activities could provide greater stability, if loans are granted, assets are selected and portfolios are monitored through strengthened processes (Allen, Carletti, and Marquez Citation2011), including those pertaining to the Social dimension, especially the workforce and product responsibility.

To verify H4, we concentrate on the Governance score (GOV) and its three constituents: Management; Shareholders and CSR Strategy. We again hypothesize a positive relationship with our dependent variable (Dowling Citation2006; Dell’Atti et al. Citation2017): improved corporate governance should represent a key tool in managing risks and maintaining stability. In general, these positive relationships should strengthen during periods of distress, such as the global financial and the European sovereign debt crises. For this reason, we interact each target variable with a crisis–specific dummy variable.

3.4. Descriptive statistics

Table reports the summary statistics and tests for differences in means between the crisis and non-crisis periods for all variables, excluding the VLTROs dummy. As expected, during the crisis years the Distance to Default significantly decreased, reaching the average value of 2.688 over the period 2008–2012 compared to 2.898 in the normal years. The ESG score (ESG), as well as each of its pillars (ENV, SOC, and GOV) show a decline during the crisis. The average mean of the composite score decreases (from 61.1% to 59%), mainly driven by the negative change displayed by the GOV pillar (from 54.3% to 51%). We argue that during the crisis, banks could be more focused on financial strength or profitability, rather than sustainability, consistently with Cornett, Erhemjamts, and Tehranian (Citation2016).

Table 2. Summary statistics.

About bank-specific characteristics, CIR and ROAE are the variables showing the most significant changes over the sample period, followed by SIZE and DIV. Operational efficiency worsened during the crisis years (due to the decline in operating income): the CIR grew from 65% to 69.4% and, simultaneously, the ROAE decreased from 8% to 4.5%. The variable SIZE grew moderately from 9.052 in the non-crisis period to 9.069 in the crisis period: possibly this is the result of consolidation processes occurring as a by-product of bank rescues. At the same time, the mean DIV decreased from 10.90% to 9.80%, indicating a lower capability of exploiting diverse income sources during crisis years.

With reference to macroeconomic factors, only GDP growth (GDP_GRW) and the supervisory strength (SUP_PWR) varied significantly. More specifically, GDP_GRW exhibited a considerable decline in crisis years (0.20%) compared to the non-crisis period (2.40%), due to the expected hoarding effect of the contraction in demand. Similarly, SUP_PWR decreased significantly (from 10.08 to 9.91), corroborating the European Commission’s call for strengthening banking supervision after it showed a limited effectiveness in ensuring bank stability.

The difference in means between the two sub-periods, reveals that, with only a few exceptions (namely size, cash to total assets, strength of capital regulations and market concentration), all variables (including our target ones) show a statistically significant difference during crisis years. Table A2 in Appendix shows that although most pairwise correlation coefficients are statistically significant, the magnitudes are relatively low.

4. Main results

4.1. Baseline analysis

Table reports the results of the baseline model described in Equation (1) for our sample banks over the period 2005–2017. This model is based on a two-step system GMM estimator and includes the Hansen test, Hansen p-value (confirming the validity of the instruments) and AR(2) – second-order autocorrelation tests (confirming that there is no second order serial correlation in the error terms). We use alternatively, as target variables, the composite ESG score (column I) and its constituents (columns II, III, and IV).

Table 3. Baseline model.

Each variable of interest (ESG, ENV, SOC, and GOV) is interacted with the dummy crisis (D_CRISIS) to verify whether the contribution of ESG strategies to bank stability varies over time. We also include control variables related to bank–specific and country–specific factors.

Focusing on the results for the total ESG score, column (I) of Table displays a significant relationship with our dependent variable (Distance to Default), but only when interacted with the dummy crisis and showing the expected positive sign. In other words, we find that the overall engagement in sustainability practices has explanatory power for stabilization during periods of financial distress, as hypothesized (H1) and consistently with the moral capital theory. This implies that banks with higher ESG scores seem less prone to insolvency during periods of financial distress. In line with Peloza (Citation2006), engaging in sustainability practices encourages more prudent banking, fosters more stable relations with the financial community and enhances reputation.

Our results confirm the ‘risk mitigation view’, deriving from the stakeholder theory, seeing CSR as an insurance-like mechanism towards stakeholders (Godfrey Citation2005; Godfrey, Merrill, and Hansen Citation2009; El Ghoul and Karoui Citation2017). The same holds true when we look at the individual constituents of ESG scores (columns II, III, and IV of Table ): only in times of crisis, each ESG pillar (ENV, SOC, and GOV) is explanatory over bank stability, supporting our hypothesis (H2, H3, and H4).

With reference to the ENV–stability linkage, Table shows that environmentally-active banks benefit in terms of stability during crisis periods (Ducassy Citation2013). This outcome is broadly in line with previous studies (e.g. Feldman, Soyka, and Ameer Citation1997; Bouslah, Kryzanowski, and M’Zali Citation2013; Cheng, Ioannou, and Serafeim Citation2014; Gangi et al. Citation2019). For example, Feldman, Soyka, and Ameer (Citation1997) found that engagement in environmental practices implies a reduction in perceived riskiness from investors. Cheng, Ioannou, and Serafeim (Citation2014)‘s results suggest that environmentally–friendly activities are associated with better stakeholder engagement. Gangi et al. (Citation2019) show that banks should assume environmental responsibility not only to generate spillover benefits to the community, but also to achieve their own strategic goals and address the pressures of strengthening regulatory requirements. We find that SOC positively affects bank stability only during crisis year. A possible explanation for this result is that more active lending and monitoring activities due to increased employee satisfaction should strengthen stability.

Finally, a significant and positive sign is found also for GOV, but again only during times of crisis. Previous studies find more shareholder-oriented banks incurred greater losses (Anginer et al. Citation2018) especially during the crisis (Beltratti and Stulz Citation2012). However, unlike Anginer et al. (Citation2018), our evidence suggests that improved corporate governance seems to provide benefits in terms of stability. Our results are therefore in line with literature exploring the link between stakeholder-oriented governance and bank stability (Dell’Atti et al. Citation2017; Leung, Song, and Chen Citation2019).

Overall, our findings on ESG target variables show that, during periods of financial distress, the integration of ESG practices into banks’ internal processes seems to be beneficial in reducing bank fragility.

However, bank stability is also related to other bank- or country-specific factors. Table shows that the proxies for bank capital (ETA), asset quality (LLR_GL), income diversification (DIV) and ECB’s unconventional liquidity injections (D_VLTRO) are relevant.

As expected, the ETA and LLR_GL variables show a positive and a negative sign, respectively. Overall, we find that banks that are more capitalized and with a sound asset quality tend to be more stable. For DIV and D_VLTRO, the negative sign prevails, suggesting that increasing diversification reduces bank stability. Indeed, diversification is not always beneficial for banks, for instance when it extends to businesses or geographical areas poorly understood by managers or when activities, despite diverse, remain highly correlated. Moreover, the negative sign for D_VLTRO means that the ECB unconventional liquidity injections seem to have contributed to a lower stability for banks that obtained them. This result confirms those of Tabak, Fazio, and Cajueiro (Citation2012), who find that banks with more liquidity appear farther from the stability frontier. Such evidence is intuitively reasonable since high levels of liquidity may encourage banks to put in place risk-taking behaviour that can determine a decrease in their resilience (although the contrary may be also true, see e.g. Bias, Heider, and Hoerova Citation2016).

With reference to macroeconomic factors, Table reveals statistically significant coefficients only for the variable targeting supervisory powers (SUP_PWR) at the country level, but the sign is not as expected (negative rather than positive), implying a decrease in bank stability. We therefore find that the strength of supervision is limited in ensuring bank stability. Although this result confirms recent findings in the literature (Chiaramonte, Poli, and Oriani Citation2015), it should be interpreted with caution. In other words, instead of signalling that more supervisory power lowers stability, the variable is more likely supportive of the recent European effort in fostering improvements in supervision, especially after 2011 and above all through the creation of a banking union.

Finally, as expected, we find a significant negative sign for the crisis dummy (D_CRISIS). However, this result should be read jointly with the interaction term. Considered alone, the financial crisis dummy suggests that financial turmoil leads to a generalized reduction in the distance-to-default (i.e. worsening stability). But ESG scores (including individual pillars), during the same years (i.e. the interaction term) invert this trend through an increase in the distance-to-default. The magnitude of the latter effect is stronger than the former (for the overall ESG score and the Social and Governance pillars), or slightly smaller (for the Environmental pillar).

4.2. Tests for disentangled ESG components

We re-estimate our baseline model using, as target variables, the following ESG components: Resource Use score, Emission score, and Environmental Innovation score for the first pillar ENV; Workforce score, Human Rights score, Community score, and Product Responsibility score for the second pillar SOC; and finally, Management score, Shareholders score, and CSR Strategy score for the pillar GOV (see Table A1 in Appendix). Due to multicollinearity issues across sub-components of the same ESG pillar, we centred them with their averages. Results are presented in Table .

Table 4. Estimation results for disentangled ESG score components.

We find that the ESG–bank stability linkage is mainly driven by the following four sub-components: Environmental Innovation score, Workforce score, Product Responsibility score, and Shareholders score. These are significant only when interacted with the dummy crisis, showing a positive relationship with our proxies for bank stability. One possible empirical channel could be through lending if banks with higher ESG scores are those that account more for environmental and social components in their loan origination and pricing policies (see e.g. Chen et al. Citation2020; Zhou et al. Citation2021). It is reasonable to expect that on average such banks will benefit in terms of more stability (i.e. less risk) in a credit-driven financial crisis.

We find that the beneficial effects of sustainability practices on bank stability, occur only during periods of financial distress, and is attributable to a variety of factors. These include: the development of new environmental technologies and processes that optimize the use of resources; the fair treatment of the workforce; the banks’ responsibility to produce quality goods and services integrating the customer’s health, safety, integrity, and data privacy; the banks’ ability to guarantee equal treatment of shareholders and to enforce anti-takeover devices. All these findings reinforce the expectations included in our hypothesis (H2, H3 and H4), adding more insights to the categories of ESG scores that appear more strongly associated to financial stability of banks during financial crisis.

4.3. Effects of the 2014 EU non-financial reporting directive

We also examine the impact of the EU NFRD of 2014 for banks with higher or lower ESG scores, in a DID regression model. Our sample includes European countries (Norway, Russia, Switzerland) outside the geographical scope of the NFRD. Additionally, some countries (Denmark, France) implemented comparable regulations before 2014. Therefore, we performed the DID setting excluding Russia, Switzerland, France, Norway, and Denmark. Other countries (i.e. Greece, Finland, Luxembourg, and Sweden) implemented more restrictive thresholds based on the number of employees, total assets and/or net turnover, however, they all applied the NFRD to listed companies. Since our sample is entirely constituted by listed banks, with more than 500 employees the comparability of results is ensured.

Panel A of Table shows the result of the logit model employed to calculate propensity scores through non-binary bank-level controls and bank fixed-effects. Panel B confirms that there are no significant differences between targets and their matches in our sample. In other words, our methodological approach allows us to conduct our DID comparison on control banks that are very similar to treatment banks, reducing individual differences and the related potential bias. Finally, Panel C shows the results of the DID, confirming the robustness of our baseline results. More specifically, they confirm that the stabilizing effect of ESG scores is present for banks with higher levels of ESG ratings after the reform of 2014, consistently with our H5.

Table 5. Effects of the 2014 EU non-financial reporting directive.

The results of the DID model support the recent increasing effort of European regulators towards a mandatory enhanced disclosure of non-financial information. More specifically, we interpret the results of the DID regression considering the moral capital theory (Bouslah, Kryzanowski, and M’Zali Citation2018). It is reasonable to assume that since the introduction of the NFRD, banks’ stakeholders and shareholders have recognized the higher moral capital accumulated by high-ESG banks, which by creating relational wealth among stakeholders, reduce uncertainty on future cash flows and improve market-based stability measures.

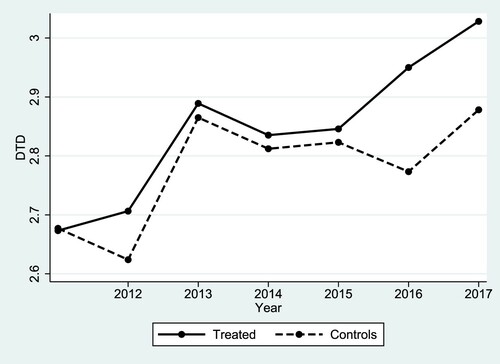

Figure in the Appendix shows that, in absence of the shock occurred in 2014, the trend for the bank stability measure (DTD) is similar for both the treatment and the control groups, hence providing visual support to the parallel trends assumption. The robustness of this finding is furtherly checked in the following section on a relevant subsample of countries.

5. Additional analyses and robustness checks

To strengthen the validity of our findings, we run a set of further analyses and robustness checks. Firstly, accounting for the ESG score level as well as the duration of ESG disclosures, in Table we test two-step system GMM regressions using alternatively, as variables of interest, the ESG rating level (columns I) and the number of years of the bank’s ESG disclosure (ESG_Nyears, columns II). For ESG rating levels we split our sample in two groups: below or above the sample mean of the ESG score. Each target variable is interacted with the dummy crisis. This approach allows us to test if previous results were prone to the non-random introduction of the legislative shock (Directive 2014/95/EU). We confirm the stabilizing effect of ESG scores in periods financial distress for banks with higher ESG scores, whereas for the subsample with lower ESG scores statistical significance is weak. In addition, we find that, in times of financial turmoil, the longer the duration of ESG disclosures, the higher are the benefits in terms of bank stability. Therefore, it seems that stability benefits from both a greater and a longer engagement in ESG activities.

Table 6. Accounting for ESG disclosure duration and ESG score level.

To control for the sample selection bias originated by the criteria used to create our sample banks (see Section 3.2), we also run the Heckman (Citation1978)‘s two-step method (Wu and Shen Citation2013; Shen et al. Citation2016; McGuinness, Vieito, and Wang Citation2017) as follows. In the first step (Panel A of Table ) we estimate the decision equation using a multinomial probit model, whose parameters are used to calculate the Inverse Mills Ratio (IMR), where the dependent variables are dummies (D_ESG) equal to 1 from the year in which a bank of our sample started to be involved in ESG practices and 0 before. The second step (see Panel B of Table ) employs the IMR as the additional explanatory variable in the performance equation, in our case the stability regression (Li and Prabhala Citation2007). Results stress the strength and unbiasedness of our baseline regression and confirm the significant and positive role of our ESG target variables in supporting bank stability only during financial crisis.

Table 7. Heckman two-step estimation results.

Moreover, we verify the robustness of results to potential endogeneity bias stemming from reverse causality, omitted variables and measurement error. For instance, companies with better financial performance or more stable, may be inclined to engage more in CSR (Bénabou and Tirole Citation2010; Chih, Chih, and Chen Citation2010). Our results may be sensitive to the measures used for both bank stability and the ESG scores. We alleviate these concerns using both the instrumental variables (IV) two-stage least squares (2SLS) estimator (Table ) and the two-step system GMM model based on an alternative definition of bank stability (Table ) and ESG scores (Table ).

Table 8. IV 2SLS estimation results.

Table 9. Baseline model with an alternative bank stability measure.

Table 10. Baseline model with an alternative ESG score definition.

For the IV 2SLS, in the first stage we estimate the goodness, as an instrument for our target variable, of the political orientation of each country (Hasan et al. Citation2018). The dummy variable Political_orient is equal to 1 for firms headquartered in countries that voted for democrats or progressive political parties and 0 otherwise. The rationale behind the selection of this instrument is that democrats or progressive political parties are more likely to exert pressure on firms to adopt green and sustainable practices, while republican or conservators are not. Therefore, political orientation of a country should be correlated with CSR (Cheung 2016; Hasan et al. Citation2018) but is unlikely to have a significant effect on bank risk. To obtain the information about the country political orientation in Europe, we employ the Chapel Hill Expert Survey (CHES) database (Polk et al. Citation2017).

As shown in Panel A of Table , these are all positively and significantly correlated with all instrumented target variables. The Cragg-Donald F-test statistics are all higher than the critical value of 16.38, with p-values smaller than 0.01 in all specifications. The weak instrument hypothesis test (i.e. testing for the relevance of the IV in the first stage) and the higher F-test (lower p-values) indicate a rejection of the null: our IVs are strongly correlated with our endogenous variables, supporting their validity. In the second stage (Panel B of Table ), the coefficients of our target variables (ESG, ENV, SOC, GOV) are all positive and statistically significant during financial turmoil, confirming our baseline findings (Table ).

Adopting only one market-based risk indicator (the distance to default) could be considered as a partial view on our target relationship. Hence, we perform our estimations using as dependent variable the Z-score (Panel A of Table ), as well as its individual components (Panel B) as in Lepetit et al. (Citation2008); Doumpos, Gaganis, and Pasiouras (Citation2015).

The Z–score is a widely used and reliable accounting-based alternative bank stability measure (Beck and Laeven Citation2006; Demirgüç-Kunt and Huizinga Citation2010;Bartholdy and Justesen Citation2020, among others), calculated as the sum of equity to total assets (ETA) and return on average assets (ROAA), scaled by the three–year standard deviation of ROAA. Data for its computation is collected from Thomson Reuters and it measures the number of standard deviations that profits can fall before a bank fails (Beck and Laeven Citation2006). Higher Z–score values indicate a lower probability of insolvency and thus greater bank stability. Since the Z–score is highly skewed, we use its natural logarithm (Laeven and Levine Citation2009). Table shows how results are consistent with our main findings.

We further test the consistency of our results using an alternative ESG score definition, provided by a different provider (Bloomberg), in a two-step system GMM setting. The alternative ESG variables (BESG, BENV, BSOC and BGOV) are built with a different methodology: the focus is on the level of transparency of information disclosed by reporting entities. In Table , model (I) refers to BESG, the score capturing the overall score, model (II) on BENV (carbon emissions, climate change effects, pollution waste disposal, renewable energy and resource depletion), model (III) on BSOC (supply chain, discrimination, political contributions, diversity, human rights and community relations), and model (IV) on BGOV (cumulative voting, executive compensation, shareholders’ rights, takeover defence, staggered boards and independent directors). We find again support for our baseline findings.

Since our analysis relies on a heterogenous cross–country sample of European banks, we further test its robustness by performing several additional analyses in our baseline econometric setting on specific sub-samples, to assess whether the ESG–bank risk linkage varies significantly due to banks’ characteristics or different operating environments.

As shown in Table , we find that only the largest European banking groups subject to the periodic EBA stress testing exercise show the association between stability and ESG scores during crisis periods. This result is supportive of the European regulatory effort towards both listed and larger entities (including banks) in enhancing non-financial disclosures.

Table 11. Baseline model for different sub-samples.

Our evidence also indicates that, in times of crisis, ESG strategies play a beneficial role for financial stability only in bank-oriented financial systems, where systemic risks could pose a greater threat (Table ). A possible explanation is that ESG practices are of particular relevance in providing several competitive advantages, such as enhancing a bank’s reputation, which is a crucial factor in withstanding both financial turmoil and the potential lack of trust arising from it. On the other side, a market-oriented system could be able to provide market discipline more frequently and gradually through pricing effects, showing a limited response during financial turmoil.

Furthermore, we observe (Table ) that ESG scores have a positive association with financial stability only for those banks located in European countries with higher income levels based on average GDP per capita. This result could be an additional evidence on the greater sensitivity towards sustainability that is achieved at higher levels of economic development (even if we do not consider emerging countries). At the same time, richer countries engage in ESG activities sooner than others, achieving already a sufficient level to obtain stability benefits before the financial crisis hit. However, this result should be interpreted with caution since we do not investigate the cause–effect direction of this relationship.

Additionally, we run our baseline model using Country-Level Index of Financial Stress (CLIFS) and its annual variation (ΔCLIFS) as alternative measures of the financial crisis. The CLIFS index is composed by six market-based financial stress measures, aimed at capturing equities, bonds and foreign exchange co-movements during financial turmoil. The CLIFS index is provided on a monthly frequency by the ECB: we annualized it by taking the 12-month average values to adapt it to the yearly frequency of our dataset. Following Hollo, Kremer, and Lo Duca (Citation2012) and Duprey, Klaus, and Peltonen (Citation2017), the CLIFS is standardized using the empirical cumulative density function (CDF) over a 10-year window to ensure both cross-country comparability and a sufficient cover of financial stress events. Table reports the results of this additional test. The coefficients of interest ESG*CLIFS and ESG*ΔCLIFS are statistically significant and strongly positively correlated with bank stability, also when including time and country fixed effects. Overall, this additional analysis furtherly corroborates our baseline results.

Table 12. Alternative measure of the crisis: the country-level index of financial stress (CLIFS).

As we are interested in testing the effect of ESG scores on banks’ stability during financial turmoil in Europe, it is useful to disentangle if the relationship differs for: (i) the subprime crisis, which took place in 2008–2009; (ii) the European sovereign debt crisis, which took place from 2010 to 2012. To this aim, we create two dummy variables: the SUB_CRISIS, which takes the value of 1 for years 2008–2009 and 0 otherwise, and the SOV_CRISIS, which equals 1 for years 2010–2012, and 0 otherwise. Then, we interact these variables with banks’ ESG scores. Results are provided in Table .

Table 13. Subprime vs Sovereign crisis.

As expected, we find significant negative associations between ESG and DTD that seems slightly stronger during the subprime crisis, as demonstrated by the magnitude of the coefficients. This evidence could be related to fact that, by differentiating loan spreads between firms more or less exposed to environmental issues (as demonstrated by e.g. Chen et al. Citation2020), banks with higher responsibility could benefit from lower risks (see e.g Zhou et al. Citation2021), especially when the turmoil originates in the credit market.

Finally, a question arises as to whether there are potential non-linearities in our relationships of interest. Similarly to Azmi et al. (Citation2021)’s study on ESG and bank performance in emerging markets, we run several additional tests to check for potential non-linear effects during the crisis period and found no evidence of them.Footnote14 However we believe that more research is needed in this area as the differences across our data sample both in terms of time span and countries under investigation, do not allow a direct comparison.

6. Conclusions

This paper empirically investigates the joint and separate effects of environmental, social, and governance scores (ESG) on bank stability for the European banking sector. The long sample period (2005–2017) includes the global financial and European sovereign debt crises and allows us to verify whether the effect on bank stability depends on the economic cycle, while controlling for bank- and country-specific variables. We hypothesize that, during a financial crisis: (i) banks with higher ESG scores are less risky; (ii) environmental activism reduces bank risk-taking; (iii) bank instability is inversely related to the level of social engagement; (iv) fair governance practices positively affect bank stability; and (v) the EU 2014 Non-Financial Reporting Directive rewarded banks more engaged in CSR practices.

We find that both the composite ESG score and its individual pillars reduce bank fragility, with a higher impact for the social dimension. This effect emerges during crises periods and is robust to selection bias and endogeneity issues. Our evidence is supportive of the predictions of the stakeholder theory and supports the idea that moral capital creates value and resilience for firms.

When we further disentangle the components of each ESG pillar, our results show that greater effects are attributable to environmental innovation, the fair treatment of the workforce, product responsibility and the equal treatment of shareholders. We also show that the positive ESG-bank stability linkage holds especially for banks with higher ESG scores, both by splitting our sample, as well as exploiting the EU 2014 NFRD as a shock in a differences-in-differences setting. Additionally, we find that the effect is stronger the longer the duration of disclosures. These results imply that the benefits of sustainability practices are contingent on the level of a bank’s engagement in ESG practices, but also on a longer commitment.

Finally, we find that ESG ratings exert a different impact on stability depending on the characteristics of banks and their operating environments. Only the largest European banking groups seem to obtain benefits on financial stability during crisis periods. This result is supportive of the recent European regulatory requirement on enhanced non-financial disclosures enforced for public-interest institutions, including banks. We also find that, in times of crisis, ESG strategies play a beneficial role for financial stability in bank-oriented financial systems, where systemic risks may pose a greater threat, as well as in European countries with higher income levels, that could be more sensitive to sustainability issues or may have engaged in related practices earlier.

This paper provides evidence that ESG strategies could act as an insurance-like risk mitigation device for banks during periods of financial distress. A possible explanation is that engaging in environmental, social, and corporate governance practices seems to be associated with more prudent banking activities, fostering a more stable relationships with reference communities and enhancing a bank’s reputation. Hence, our findings confirm that enhancing ESG engagement in the banking sector is not only beneficial in terms of its impact on the environment and the society but is also able to strengthen the resilience of the banking sector when a financial crisis occurs.

Overall, our evidence reveals that, beyond the traditional regulatory approach, focusing on ESG issues matters in the banking sector and corroborates the proposal, advanced by the European Banking Authority, to include ESG considerations within supervisory frameworks. Additionally, integrating sustainability practices into banks’ internal processes to enhance stability should constitute an interesting suggestion also for a sound management of credit institutions.

In terms of policy implications, our results suggest that sustainability practices require strong efforts and relatively long periods of time before they provide a benefit on stability. How to improve such benefits or how to extend them to smaller institutions, are open questions for policymakers that should be addressed in future academic research.

Acknowledgements

We are grateful to the Editor Chris Adcock and two anonymous referees for their helpful and constructive comments that greatly improved the paper. We thank conference and seminar participants at the 3rd Social Impact Investment Conference (University of Rome 2019); 3rd Conference on Contemporary Issues in Banking (University of St Andrews 2019); International Workshop of Financial System Workshop of Financial System Architecture and Stability (Bayes Business School, 2020); 1st Annual Boca Corporate Finance and Governance Conference (Florida Atlantic University 2020); University of Birmingham (2020) and Kings College London (2020); and in particular, Ettore Croci, and discussants: Giovanni Ferri, Franco Fiordelisi, Yrjo Koskinen and Marcel Lukas. The paper won the best paper award at the 3rd Social Impact Investment Conference (University of Rome 2019). All remaining errors are our own.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Claudia Girardone

Claudia Girardone is Professor of Banking and Finance at Essex Business School of the University of Essex where she is Director of the Essex Finance Centre (EFiC) and the School's Director of Research. Claudia's research areas are on banking sector financial and social performance, bank corporate governance and stability, the industrial structure of banking and access to finance. She has published over 50 articles in books and peer-reviewed international journals. She is a co-author of the textbook “Introduction to Banking” (Pearson, 2015) and she is currently on the editorial board of several journals, including the Journal of Financial Economic Policy and The European Journal of Finance.

Notes

1 There is no unique definition of CSR (McWilliams and Siegel Citation2001; Hill et al. Citation2007; Dahlsrud Citation2008): the European Commission (Citation2011) defines it as ‘the responsibility of enterprises for the impact on society […] to integrate social, environmental, ethical, human rights and consumer concerns into their business operations and core strategy in close collaboration with their stakeholders’.

2 For many years, the debate in the literature around CSR was mainly theoretical and based either (i) on the shareholder view of the firm (Friedman Citation1970) that considers CSR activities as a cost; or (ii) the stakeholder view (Freeman Citation1984) that sees them primarily as an ethical obligation (see also Garriga and Melé Citation2004).

3 In 2017 the European Commission adopted detailed non-binding guidelines on the disclosure of non-financial information to improve business transparency on social and environmental matters and ensure consistency and comparability across companies (2017/C 215/01). Sustainability reporting is also at the heart of the so-called ‘European Green Deal’ that is an action plan of the European Commission with the objective to make Europe the world’s first climate-neutral continent by 2050.

4 Specifically, an online document (Bank of England Citation2021b) that summarizes the key elements of the UK 2021 biennial exploratory scenario states that: ‘The financial risks from climate change affect the safety and soundness of firms the Bank regulates and the stability of the wider financial system that it oversees. Climate-related financial risks therefore have a direct impact on the delivery of the Bank’s macroprudential and microprudential policy objectives […]’

5 Several studies find that improvements in CSR can benefit firms’ relationships with stakeholders, lower the vulnerability to reputational risks and enhance the long-term business sustainability (Becchetti, Ciciretti, and Hasan Citation2015). The commitment to CSR can be used as an alternative risk hedging and mitigation tool (Peloza Citation2006). Swanda (Citation1990), for example, views the results of moral behaviour as a capital asset and emphasizes the strategic importance of preserving and advancing a firm’s moral capital.

6 In recent years, a variety of ESG indices measuring firm-level CSR performance have been constructed using different rating methodologies (e.g., some are based on a box-ticking approach – ‘compliance’, while others are based on interpretative analysis – ‘engagement’).

7 To further assess the robustness of our results with respect to the estimation methods, we also employ a bank fixed-effects panel data regression model with clustered standard errors at the bank level and results, unreported and available upon request, are broadly confirmed.

8 For robustness, we also used an alternative market-based bank risk measure, i.e. the one-year Merton’s probability of default (PD). Results are qualitatively similar and available upon request.

9 As a robustness test, we perform our analysis also using a dummy crisis variable that ends in 2013 rather than 2012. The results are qualitatively similar and available upon request. Due to the limited number of observations, it was not feasible to divide our sample period (2005–2017) into sub-periods (pre–crisis, crisis, post–crisis).

10 As a potential alternative to the interaction term, sample splitting could bias the results due to sub-sample specific covariates that can obfuscate the treatment effect and may also reduce the number of observations. However, in an unreported test, we verify the consistency of our results by running the baseline model without the interaction term and results are broadly confirmed.

11 The VLTROs are considered the ECB’s largest liquidity injections ever, with more than one trillion Euro introduced in the Eurozone banking system in two tranches (VLTRO1 in 2011Q4, VLTROs in 2012Q1, both ended in 2015Q1).

12 Thomson Reuters’ Refinitiv is an enhancement and replacement to the Thomson Reuters’ ASSET4 ratings, which has been widely used in previous CSR studies (Cheng, Ioannou, and Serafeim Citation2014; Eccles et al. 2015; El Ghoul and Karoui Citation2017; among others). We start our sample in 2005 due to the low coverage on ESG scores in previous years.

13 The same issue occurs when collecting ESG scores data from Bloomberg database. In this case, the level of coverage is lower and, more importantly, less granular information on ESG constituents is present. However, as robustness tests, we perform our analysis also using Bloomberg as a data source: our results hold also in this setting (see Section 5). Moreover, although widely used in previous related studies on corporate social performance (e.g., Jiao Citation2010; El Ghoul et al. Citation2011; among others), it was not possible to use the Morgan Stanley Capital International (MSCI) ESG database (formerly known as Kinder, Lyndenberg, and Domini Research and Analytics Inc. (KLD) database), because, except for the most recent years, it does not provide data on European countries (Sassen, Hinze, and Hardeck Citation2016).

14 We thank an anonymous reviewer for suggesting this analysis. Results are not reported but are available with the authors.

References

- Albertini, E. 2013. “Does Environmental Management Improve Financial Performance? A Meta-Analytical Review.” Organization & Environment 26 (4): 431–457.

- Allen, F., E. Carletti, and R. Marquez. 2011. “Credit Market Competition and Capital Regulation.” Review of Financial Studies 24 (4): 983–1018.

- Anginer, D., A. Demirguc-Kunt, H. Huizinga, and K. Ma. 2018. “Corporate Governance of Banks and Financial Stability.” Journal of Financial Economics 130 (2): 327–346.

- Aramburu, I. A., and I. G. Pescador. 2017. “The Effects of Corporate Social Responsibility on Customer Loyalty: The Mediating Effect of Reputation in Cooperative Banks Versus Commercial Banks in the Basque Country.” Journal of Business Ethics 154 (3): 701–719.

- Arellano, M., and O. Bover. 1995. “Another Look at the Instrumental Variable Estimation of Error-Components Models.” Journal of Econometrics 68: 29–51.

- Attig, N., S. El Ghoul, O. Guedhami, and J. Suh. 2013. “Corporate Social Responsibility and Credit Ratings.” Journal of Business Ethics 117 (4): 679–694.