ABSTRACT

Since the use of swap lines during the global financial crisis, the Federal Reserve is widely seen as international lender of last resort. Yet the focus on emergency liquidity assistance tends to obscure the broader significance of swap lines for US monetary governance. As this article shows, swap lines have historically played a crucial and evolving role in structuring and facilitating specific practices of offshore Eurodollar liquidity production in the interest of US monetary policy. A key contemporary example can be found in the uptake of swap lines during the Covid-19 market turmoil in early 2020: swap lines alleviated offshore dollar funding conditions to such an extent that they also triggered reverse inflows of dollar liquidity back into the US. More than simply providing a backstop to the global system, these swap interventions effectively restructured cross-border financial flows in a way that afforded the Fed greater control over domestic markets. Yet as the capacity to influence global liquidity conditions appears increasingly crucial to the Federal Reserve’s control over domestic monetary conditions, these interventions pose broader questions about its role in managing instable and evolving cross-border credit relations that link domestic and global markets.

Introduction

The global financial crisis has renewed interest in the role of central banks in stabilising the international monetary system in times of crisis (McDowell Citation2012, Helleiner Citation2014, Hardie and Thompson Citation2020). The extension of central bank swap lines by the Federal Reserve has been regarded as a significant step in the evolution of the global financial safety net (Mehrling Citation2015, Tooze Citation2018, McDowell Citation2019, Sahasrabuddhe Citation2019). More recently, swap lines also played a key role in the Federal Reserve’s response to the Covid-19 crisis (Aldasoro et al. Citation2020), solidifying the Fed’s role as de facto international lender of last resort (Helleiner Citation2014, Broz Citation2015). Based on these interventions, swap lines are generally understood as a relatively straightforward institutional development: as markets globalise, so do the backstops that central banks provide (Mehrling Citation2015, Murau et al. Citation2020).

Considering the overwhelming liquidity pressures experienced during times of crisis, it is hardly surprising that scholars have framed the actions of the Federal Reserve around the accommodation of the needs of global capital (McDowell Citation2012, Hardie and Maxfield Citation2016). Yet by reducing global liquidity to the technical problem of designing a proper market backstop, the literature tends to sidestep the broader governmental problems that confront US policymakers when seeking to maintain control over both domestic and global dollar markets. Far from existing in isolation, global or ‘offshore’ Eurodollar markets are deeply intertwined with their domestic or ‘onshore’ foundations: while individual actors such as global banks, reserve managers, and institutional investors can take positions in dollars without direct involvement of US actors, American financial institutions provide a crucial and elastic source of funding for the activities of the offshore system as a whole. As a result, US financial markets are closely interwoven with the pace and rhythm of the global financial cycle, and funding conditions in one market can easily spill over into others (Mehrling Citation2015, Rey Citation2015). This close integration raises the question: how do swap lines assist the Fed in maintaining control over instable and evolving credit relations that link domestic and global dollar markets?

Studies of the Eurodollar markets have long emphasised the role of states and technocrats in supporting financial globalisation (Strange Citation1988, Helleiner Citation1994, Kapstein Citation1994, Cohen Citation2015). At the same time, political economists have tended to ‘black box’ (MacKenzie Citation2005) the precise liquidity dynamics that entangle state and private finance in global markets, and instead attributed financial globalisation to the consequences of deregulation and liberalisation. Yet as recent studies on market-based governance show, the integration of disparate financial systems and practices required policy interventions that institutionalised and stabilised evolving credit relationships between global financial actors (Konings Citation2007, Braun et al. Citation2020, Gabor Citation2020). Drawing on this approach, this article maintains that growing entanglements between public actors and private finance highlight the crucial role of central banks in intervening on behalf of those global actors and market processes that strengthen the coherence of their policy frameworks.

The key argument advanced in this article is that swap lines restructure the macrofinancial linkages between the global and the national economy in the interest of US monetary policy. As an intervention in private market processes, swap lines inherently straddle the line between prudential and monetary policy-driven intervention: at the most basic, swap lines can protect private financial actors from destabilising losses by ensuring easy financing conditions in global markets. The gist of such international last resort lending is to provide a backstop to markets until private actors resume orderly trading (Mehrling Citation2014). Yet sometimes swap lines do more than simply support markets, and instead shape offshore interest rates directly in support of domestic monetary policy preferences. When setting rather than backstopping rates, swap lines effectively violate the Bagehotian principle of lending at a high price against good collateral.Footnote1 Instead, they come to resemble a ‘foreign open market operation’, an intervention that actively restructures offshore yields in the interests of domestic monetary policy and financial stability.

As the empirical analysis in this article shows, the link between swap lines and monetary policy is not coincidental. Already in the 1960s, the Fed used swap interventions into the newly emerging offshore Eurodollar markets to reassert control over the activities of globalising American banks. As Fed officials recognised at the time, the offshore activities of US banks were intricately connected to domestic monetary conditions as banks could repatriate offshore funding pressures back into domestic markets. Despite initial successes, these swap interventions soon ended as the Fed pivoted towards monetary tightening, and came to consider offshore dollar easing as counterproductive to the overall fight against inflation (McCauley and Schenk Citation2020). The historical experience helps us understand the role swap interventions play in managing contemporary cross-border capital flows. As the example of the Covid-19 pandemic shows, recent swap lines interventions go far beyond backstopping global markets: in early 2020, swap lines offered the Fed an effective lever to manipulate offshore yields, restructure credit flows, and pull global capital into US markets in the interests of the US financial system and US monetary policy. This suggests that the impact of the Fed’s international operations on its domestic monetary policy settings continues to be central to the Fed’s swap lending.

The article makes two central contributions. First, it brings an important monetary history of the relationship between swap lines and monetary policy to bare on the way the political economy literature has conceptualised the role of the Federal Reserve as an international lender of last resort. While the idea that the Fed uses swap lines defensively to ‘shield’ its monetary policy operations and US markets from global conditions is recognised in the literature (McDowell Citation2012, Hardie and Thompson Citation2020), what is generally underestimated is the extent to which global crisis management depends on the Fed’s recognition of strategic interests in working not just within domestic markets but also through evolving global markets. The second contribution derives from here. As recent studies have shown, central banking requires mobilising private infrastructures with oftentimes highly contingent outcomes (Walter and Wansleben Citation2019, Braun and Gabor Citation2020, Dutta Citation2020). By extending this line of analysis to the international level, this article locates the politics of swap interventions in the infrastructural problem of what makes the global dollar system ‘governable’ from the perspective of the Federal Reserve.

The analysis presented in this article is based on secondary literature, financial news, bank research notes, as well as seven interviews with economists and research analysts working in central banking, the global regulatory community, and in global banks. The interviews were conducted between July and October 2020 and are used for background information. The remainder of the article is structured as follows. The first section reviews the association of swap lines with last resort lending in the existing literature. Section 2 shows that the broader capacity of the Federal Reserve to manage the cross-border linkages between domestic and global dollar markets derives from its fundamental organising role within the dollar-centric global payments system. Drawing on these insights, the final two sections analyse the relationship between swap lines and monetary policy in the two time periods discussed.

The Federal Reserve as international lender of last resort

During the global financial crisis, the use of central bank swap lines established the Federal Reserve as a de facto international lender of last resort. From 2007-10, the Fed used swap lines to fourteen foreign central banks to extend the reach of emergency dollar liquidity assistance beyond its own monetary jurisdiction (McDowell Citation2012, Mehrling Citation2015, Sahasrabuddhe Citation2019, Carré and Le Maux Citation2020, Hardie and Thompson Citation2020). Even though the Fed had periodically relied on swap lines since 1962, they were traditionally associated with exchange rate management (Bordo et al. Citation2015). The provision of liquidity to backstop private international banking is therefore widely regarded as a fundamentally new development (Bahaj and Reis Citation2019), and credited with resolving the dollar liquidity squeeze at the heart of the global financial crisis (Tooze Citation2018).

In the literature, the Fed’s international last resort lending is defensively motivated. Economic research has shown that swap lines were effective in alleviating short-term dollar funding pressures, highlighting international banking integration and dollar exposure as key variables in swap line allocation (Aizenman and Pasricha Citation2009, McGuire and von Peter Citation2009, Goldberg et al. Citation2010, Moessner and Allen Citation2010). IPE scholars have emphasised that risks arising from the international investment positions of US financial actors prompted the Fed to intervene abroad to protect American private financial interests (Hardie and Maxfield Citation2016). These exposures were particularly significant with regard to European banking systems, highlighting the centrality of transatlantic financial conduits for the operation of the international monetary system (Tooze Citation2018, Hardie and Thompson Citation2020). Swap lines were most effective in bringing down offshore dollar funding pressures after the removal of caps on swap lending to several key counterparties in October 2008 (Carré and Le Maux Citation2020). Swap lines are thus widely regarded as a mechanism to stabilise and entrench the core of the dollar-centric international monetary order (Mehrling Citation2015, Murau et al. Citation2021).

While the crisis swap lines expired in early 2010, the Fed and five other central banks re-established a swap network during the Euro crisis.Footnote2 Reviving the practices pioneered during the crisis, the initially temporary network promised unlimited dollar liquidity to other participating central banks when needed, and was made permanent in October 2013 (Mehrling Citation2015). The post-crisis institutionalisation of swap lines is generally seen as a crucial step in the evolution of the global financial safety net (McDowell Citation2019), indicating the end of the ad-hoc ‘non-system’ (Ocampo Citation2017) that developed after the breakdown of Bretton Woods (Eichengreen Citation2009, Prasad Citation2014). Although the US has long played a critical role in international crisis management (Kirshner Citation2006, Helleiner Citation2014), it has often done so indirectly, for instance via the lending channels of the IMF (Chwieroth Citation2008). Accordingly, the global financial safety net developed as a patchwork, with earlier swap interventions intended primarily to protect international reserve positions and defend exchange rate arrangements (Bordo et al. Citation2015). The use of swap lines for international last resort lending thus is generally regarded as a qualitative shift from swap interventions ‘then’ to ‘now’—from the historical use for the stabilisation of exchange rates between official currencies in the 1960s and 1970s to contemporary emergency liquidity provisions for private finance.

Yet the clear-cut distinction between lending purposes tends to obscure our understanding of the role that swap lines play in international markets. In practice, the distinction between purposes can be hard to draw, as swap interventions targeted at offshore dollar funding pressures also affect exchange rates and interest rates. This is recognised by McDowell (Citation2012), who explicitly analyses swap lines as alleviating a variety of interrelated spillover threats. Similarly, Hardie and Thompson (Citation2020, p. 8) note that during the global financial crisis, becoming an international lender of last resort was crucial to the Fed’s ability to control domestic interest rates. As transcripts from the Fed’s Federal Open Market Committee meeting in late 2007 show, policymakers were particularly concerned that high offshore rates could drive up the Fed’s key domestic interest rate, the federal funds rate. According to Fed Chairman Bernanke, dollar funding problems in Europe had direct spillover effects onto US markets: ‘There is a shortage of dollars there early in the day, which often leads the funds rate to open high. It creates problems for our monetary policy implementation’ (FOMC Citation2007, p. 13, emphasis added).

The problem that confronted the Fed was that European banks were setting LIBOR rates early in the day in London at terms that reflected their own funding conditions, rather than those in the United States. Since LIBOR served as benchmark for US corporate loan contracts and certain US mortgages, these offshore rates directly defined funding conditions for a considerable number of firms and households in the US. The Fed’s inability to influence LIBOR directly thus impaired the pass-through efficiency of its monetary policy transmission mechanism and obstructed monetary easing (McDowell Citation2012, p. 172). Concerns about offshore dollar funding pressures increased after the collapse of Lehman Brothers in September 2008. At the time, swap lines failed to ease offshore funding conditions as swaps were both limited in quantity and tied to fluctuating market interest rates. As Carré and Le Maux (Citation2020, p. 731) show, in early October 2008, the European Central Bank paid an interest rate of above ten percent on its dollar borrowing. Dollar funding conditions only eased after the removal of limits on swap lending and a shift to fixed interest rates at OIS + 100 basis points on 13 October 2008. Within days, LIBOR-OIS spreads narrowed by about 200 basis points. As Bernanke later testified before Congress, the augmentation of swap lending terms ‘help[ed] ease conditions in global dollar markets that were spilling over into our own funding markets’ (US Congress Citation2009, p. 4). The role of swap lines in bringing down LIBOR rates can thus be understood both as a form of emergency international liquidity assistance and as a mechanism to aid the implementation of domestic monetary policy (McCauley and Schenk Citation2020).

Yet despite this implicit admission that swap lines are integral to broader questions of domestic monetary management, swap interventions are typically framed as largely reactive to market pressures outside of the US over which the Fed has little control (e.g. Hardie and Maxfield Citation2016). By conceptualising the international system as outside of the purview of central banking activities, this framing limits our understanding of the Fed’s role in the international system to merely preventing negative externalities in the form of financial spillovers. It reduces global liquidity dynamics and financial factors to a purely technical problem of financial stability and fails to develop a more comprehensive account of the governmental problems that arise out of the macrofinancial linkages between global and domestic dollar markets (Shin Citation2012). As the next section will show, what is missing is a better understanding of how swap interventions are tangled up with the Fed’s efforts to govern the economy effectively.

Cross-border flows and monetary management

The capacity of the Federal Reserve to manage cross-border linkages between domestic and Eurodollar markets derives from its fundamental organising role within the payments system. As recent studies have shown, modern finance is characterised by its essential public-private hybridity (e.g. Mehrling Citation2011, Pistor Citation2013, Hockett and Omarova Citation2016, Braun Citation2018, Ricks Citation2018). Money markets and the payment relations that underpin them are always shaped by the interaction of private market participants with public authorities (Giannini Citation2011, Knafo Citation2013, Ugolini Citation2017). How states and their central banks govern money therefore has important consequences for how power operates at the very centre of financial markets, how credit claims are negotiated, and what actors gain in importance over time.

Due to their outsized role in the payments system, central banks engage in both financial stability policy and macroeconomic management. Though formally separate, operationally these two aspects are deeply intertwined: because the transmission of monetary policy signals occurs through markets and depends on easy credit flow within the economy, central banks have found it necessary to accommodate the proliferation of increasingly instable forms of private credit creation (Murau Citation2017). Yet against the backdrop of these evolving credit and liquidity relations, central banks need to maintain control over the dynamics of ‘financial plumbing’. Securing monetary governability—defined as ‘the ability to use monetary policy instruments, such as open market operations, to achieve specific policy objectives, such as price stability’ (Braun et al. Citation2020, p. 7)—thus goes beyond simply preserving the integrity of the payments system. To enhance their ability to affect the financial institutions and processes that exist within markets, central banks proactively shape market structures by selectively supporting specific market segments, instruments, or institutions (Hockett and Omarova Citation2016, Walter and Wansleben Citation2019, Pape Citation2020). From this perspective, central bank backstops are never merely apolitical or technocratic, but central to financial management and tied up with inherently political questions about the entanglement of public authorities and private actors in the organisation of the market.

Though the public-private hybridity of finance has primarily been explored in the domestic context, it can usefully be extended to the international level (Braun et al. Citation2020). States have played a crucial role in the construction of financial globalisation, most notably by nurturing the growth of the Eurodollar markets with which they identified strategic interests (Helleiner Citation1994, Kapstein Citation1994, Konings Citation2011). The ability to sell dollar debt abroad, for instance, has afforded the United States access to a reliable stream of external financing for both its public and private debt, and is widely regarded as a key source of US structural power in global finance (Strange Citation1988, Schwartz Citation2011, Panitch and Gindin Citation2012). The growth of macrofinancial linkages that facilitate the circulation of dollars offshore has historically depended on the capacity of states and their central banks to institutionalise and stabilise cross-border credit relationships between global financial actors (Braun et al. Citation2020). To that end, states have long pursued global prudential regulatory standards or promoted private financial risk management techniques (Baker Citation2013, Thiemann Citation2014, Lockwood Citation2015). Yet whereas regulatory arrangements are best understood as putting in place an external framework for market functioning (Birk and Thiemann Citation2020), swap lines should be seen as a market-based form of intervention: their contribution to monetary management comes from their ability to productively induce private risk bearing by selectively nurturing those market processes that allow policymakers to preserve the coherence of their monetary policy and financial stability frameworks.

To substantiate this claim, we first need to account for the capacity of the Federal Reserve to affect global market processes. While the Federal Reserve is not a global central bank, the central role of the US dollar as the global key funding, investment and reserve currency nonetheless affords it a key source of influence over global credit intermediation (Mehrling Citation2015). At first glance, dollar credit intermediation can occur purely ‘offshore’ or outside of the US—for instance, when foreign investors use dollar-denominated bank accounts offered by European banks as a means of payment and buy US dollar bonds issued by non-residents outside the United States (He and McCauley Citation2012). Despite appearances, however, the Eurodollar market does not exist in isolation. Due to the centrality of the dollar, non-US residents face an inherent currency mismatch in their international operations. When foreign investors or banks make positions and accumulate liabilities in dollars rather than their domestic currency, they face a structural demand for dollar funding. Here, the ability to service debts by forcing dollar income flows in their favour becomes a core organising feature of economic activity and subjects these investors to the pace and rhythm of global dollar liquidity conditions (Bortz and Kaltenbrunner Citation2017). As global investors meet their dollar funding needs in wholesale money markets, US banks and money market funds have emerged as a structural source of global dollar supply (Aldasoro et al. Citation2019, Correa et al. Citation2020).

Collectively, these processes integrate domestic and global dollar markets, with important consequences for the reach of the Federal Reserve. For one, it affords US monetary policy a key ‘external’ dimension, as the lending capacity of US institutions in global markets is shaped by their ability to obtain easy funding in US markets. Recent studies show that just as loose US monetary policy relaxes global leverage constraints, monetary tightening in the United States leads to significant deleveraging of global financial intermediaries and the retrenchment of international credit flows (Miranda-Agrippino and Rey Citation2020). While the importance of international monetary spillovers has long been established (Calvo et al. Citation1996), they have increased in significance since the global financial crisis, as global investors increasingly search for yield across borders and fuel asset bubbles in distinct economies (Shin and Turner Citation2015). Yet as global banks and investors tap wholesale sources of funding to invest in high-yielding securities and bond markets, for instance in the United States, changes in global dollar liquidity conditions can directly spill back to those markets and disrupt domestic monetary conditions.

These macrofinancial linkages represent a distinct policy problem: as liquidity is shaped by global factors that blur the distinction between onshore and offshore markets, the coherence of national economic policy cannot be assumed (Avdjiev et al. Citation2016). As the structure of cross-border flows is increasingly integral to the functioning of wholesale and bond markets, the dynamics of the global financial cycle are both facilitated by US monetary policy and can directly feed back onto US monetary conditions. Despite their formal separation, domestic monetary policy and global financial stability concerns are thus inherently blurred: the Fed cannot respond solely to the domestic macroeconomic variables that constitute its monetary policy mandate—price stability and employment—but also needs to consider how the dynamics of global finance shape its policy space.

Here, the structural dollar funding needs experienced by globally active institutions offers the Federal Reserve a unique source of leverage over global finance: while wholesale money markets serve as an elastic source of global dollar supply for offshore markets, the Fed is the only actor that can truly alleviate the settlement constraint in the global payments system, precisely because the ultimate means of payment—central bank reserves—are its own liability (Mehrling Citation2014). Traditionally, the Fed only draws on this capacity indirectly as its standard monetary policy operations target the overnight rate to manipulate the settlement constraint within the domestic interbank market (Bindseil Citation2004). Arbitrage then connects the overnight rate to other interest rates across both domestic and global dollar markets, giving US monetary policy its broader significance for offshore dollar funding markets (Bruno and Shin Citation2015). Yet nothing prevents the Fed from transacting in other markets to influence offshore asset prices and interest rates more directly —for instance, in times of crisis, when normal arbitrage channels between markets break down.

From the perspective of financial plumbing, providing private sector liquidity offshore is as much a function to alleviate cash flow constraints as it is a mechanism to repair and support the infrastructural connections between market segments on which the transmission of interest rate signals depends. The formal distinction between last resort lending and monetary policy here reveals itself as ultimately only one of degree: last-resort-lending ‘backstops’ the market by providing an ‘outside spread’ within the bounds of which normal commercial dealing takes place (Mehrling Citation2014, p. 110). Monetary policy, by contrast, seeks to influence or set market rates directly (Ricks Citation2018). Swap lines straddle the line between prudential backstop and monetary policy-driven intervention: depending on their pricing, they can be used either to backstop or manipulate market rates directly, and thus can be used as a policy tool to protect and promote those credit channels and liquidity dynamics that allow the Fed to manage the relationship between offshore markets and domestic monetary policy preferences.

In practice, the Fed has only cautiously relied on swap lines to support its monetary policy stance. Central banks have historically struggled to square their role in offshore markets with their domestic policy mandates and have tended to opt for a more hands-off approach to international monetary management (Helleiner Citation2014). As a form of international monetary cooperation, swap lines are therefore usually defined around a shared global interest, such as exchange rate stabilisation or financial stability. Yet central banks have pursued a more activist role when confronted with the destabilising effects of new and evolving credit dynamics and liability management practices on their own economies (Altamura Citation2017, Braun et al. Citation2020), such as during the initial expansion of the Eurodollar market and since the global financial crisis. As the remainder of this article shows, during such periods of adjustment, the Fed has developed innovative ways to use swap lines as a more sophisticated intervention mechanism in support of its domestic monetary policy.

Swap lines and the early Eurodollar market

The Federal Reserve first developed a comprehensive swap network with several advanced economy counterparties in the 1960s. This early swap network is most commonly associated with exchange rate management to stabilise the Bretton Woods monetary order (McDowell Citation2017). In light of the growing US balance of payment deficit, a key interest of the US Treasury and the Fed was to forestall any run on the US gold stock and stabilise the value of the dollar against speculative attacks (Bordo et al. Citation2015). Based on the success of this initiative, in the late 1960s the Fed put in place an additional swap line with the Bank for International Settlements that was intended exclusively to manage offshore dollar yields in the emerging Eurodollar markets. Through this swap line, the Fed sought to manage the effect of US banks’ globalising funding operations on domestic monetary conditions.

The engagement of US banks with the Eurodollar markets was partly a response to the restrictive domestic credit environment. Throughout the late 1950s and early 1960s, US banks regularly found themselves starved of funds as interest rate ceilings pushed corporations to invest in financial markets directly rather than deposit their cash with commercial banks. Constrained by such regulatory caps, banks started to develop deposit alternatives to attract funding. A key innovation in this regard were negotiable Certificates of Deposits (CDs), which enabled banks to finance their operations by borrowing in the money markets directly (Konings Citation2007, p. 46). Fed policymakers soon came to regard these new liability management strategies as inflationary and found themselves caught between accommodating these practices, and thus accepting inflation, or restricting market activity with potentially adverse effects on financial stability. The dilemma was exemplified in 1966, when the Fed decided to counteract the expansion of bank liability management techniques by imposing interest rate ceilings on bank deposits and CDs. By limiting the attractiveness of bank liabilities for other money market participants, the Fed effectively incentivised money market participants to rotate out of bank liabilities and into other, more lucrative investments (Klopstock Citation1968, p. 135). As banks found themselves virtually priced out of domestic money markets, they experienced a severe credit crunch in domestic markets and instead looked to their offshore branches to accommodate the shortfall of funding. Ultimately, the Fed’s policy-induced credit crunch of 1966 pushed American banks further into the Eurodollar markets, and intensified the links between onshore and offshore markets as banks increasingly channelled funds between their branches in different jurisdictions (Burger Citation1969).

The resulting entanglements between onshore and offshore markets represented both problems and opportunities for states. While public officials saw strategic interests in internationally expanding their financial sectors, they also faced considerable ‘epistemic uncertainty’ about the nature of the incipient Eurodollar markets, and sought to develop forms of intervention that would allow them to shield domestic monetary processes from these offshore markets (Braun et al. Citation2020, p. 2). One way in which some central banks responded to these problems was by intervening in the Eurodollar markets directly. To maintain control over the foreign currency activities of their commercial banks, central banks, along with the Bank for International Settlements, began to place funds in the Eurodollar market directly (Schenk Citation2010, p. 227). Central banks would either place dollars from their FX reserve holdings directly with banks active in Eurodollar markets, or engage in temporary swaps in which they sold dollar spot against local currency and repurchased at forward rates, with transactions priced at rates that encouraged commercial banks to place Eurodollar deposits abroad. Through these transactions, central banks effectively endorsed and bolstered the Eurodollar market by pushing deposits out into the offshore market (Braun et al. Citation2020).

Unlike other central banks, however, the Fed was reluctant to intervene in the Eurodollar market: as the Fed sought to encourage its banks to keep funds within the domestic market, officials were keen not to be seen as bolstering the offshore dollar markets directly. At the same time, Fed policymakers understood that as US banks drew on Eurodollar funding for their domestic operations, they could repatriate the disruptive effects of cyclical fluctuations in Eurodollar interest rates back into domestic markets. To address this situation, Fed officials sought to deploy swap lines to delegate the placement of offshore funds to their partner institutions. For these operations, the Fed relied extensively on the BIS, the only non-central bank within its network. While the BIS was already engaging in swaps with the Federal Reserve for exchange stabilisation purposes, in 1965 the Fed established a second swap line with the BIS which was to be used explicitly for Eurodollar market interventions (McCauley and Schenk Citation2020).

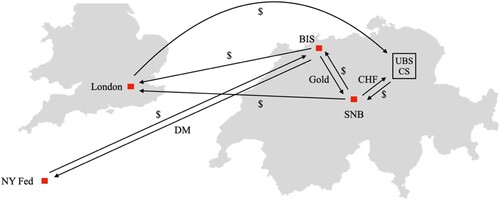

The stated motivation behind this ‘second’ BIS swap line was to smooth out interest rate fluctuations in the Eurodollar markets. As McCauley and Schenk (Citation2020, pp. 23–28) show, a key example of these operations can be found in the 1966 year-end swap operations. As policymakers were anticipating, Swiss banks were withdrawing about $400 m from the Eurodollar markets as they preferred to show Swiss Franc rather than dollars on their year-end balance sheets reports. As US banks relied on Eurodollar markets for their liquidity needs, the resulting funding shortage put upward pressure on Eurodollar interest rates. To alleviate these cash flow problems, the BIS coordinated with both the Swiss National Bank (SNB) and the Fed. In a first step, the SNB conducted large swap operations with its own commercial banks that were seeking to rotate out of dollar deposits, and channelled the dollars obtained to the BIS via a swap against gold. In a second step, the BIS then deposited these dollars back in the Eurodollar markets. To fully meet dollar cash flow needs, the BIS obtained additional funds via its second swap line with the Fed, collateralised against Deutsche Mark (). In total, the BIS obtained $360 m from the Fed and SNB (McCauley and Schenk Citation2020, p. 26). Collectively, the roundtripping of Swiss dollar deposits along with the injection of new dollar liquidity via the Fed—BIS swap line was successful in easing offshore interest rates: whereas the one-month Eurodollar rate had risen abruptly from 6.5 percent to 7.3 percent on 29 November, with other rates rising similarly, rates fell back to 6.6 percent by 12 December 1966 following coordinated interventions (Coombs Citation1967, p. 356).

Figure 1. 1966 year-end swaps and deposit operations. Source: author’s illustration based on McCauley and Schenk (Citation2020, p. 26).

The Eurodollar interventions went beyond merely backstopping offshore markets. The implicit danger that Fed officials saw was that offshore funding pressures could spill over into US markets as American banks sought to pass on the higher funding cost incurred by their offshore branches. As the fed funds rate was fluctuating between 5–6 percent at the time, Eurodollar yields of over seven percent posed a challenge to the Fed’s attempt to temporarily ease domestic monetary conditions following the policy-induced credit crunch earlier that year (McCauley and Schenk Citation2020, p. 25). A spillover of high offshore funding costs threatened to seriously undermine its control over domestic monetary policy (Klopstock Citation1968, p. 131). Just as the 1966 credit crunch had shown US banks that they could rely on their internal liquidity management to offset losses of wholesale funding in domestic money markets (Burger Citation1969, Konings Citation2007, p. 48), it demonstrated to the Fed that the entanglement of onshore and offshore dollar markets left it with little alternative but to police cross-border banking relationships directly. As a prudential intervention, the swap lines helped contain volatility in the Eurodollar markets. By targeting yields, however, rather than simply backstopping markets at a price, the swap lines effectively functioned as a foreign open market operation that restructured offshore yields in the interest of US monetary policy.

Within the central banking community, the intervention was initially seen as a success. In the following years, the Fed relied several times on the ‘second’ swap line to the BIS to influence Eurodollar market conditions, though use of the facility slowed significantly after 1969 (McCauley and Schenk Citation2020, p. 39). By that time, central bankers had grown increasingly wary of the potential of the Eurodollar markets to undermine domestic efforts at containing inflation. As debates from central banker meetings at Basel show, policymakers extensively pondered the nature of their relationship with the Eurodollar markets in the early 1970s (Altamura Citation2017, chapter 2, Braun et al. Citation2020), caught between bolstering the resilience of the market—which would soon gain in importance with the emergence of Petrodollar recycling after the 1973 oil shock (Kapstein Citation1994, p. 68, Kershaw Citation2018)—and containing its endogenous credit and inflation dynamics in the interests of domestic policy. Over the next years, the emerging policy consensus saw the gradual expansion of the Eurodollar’s backstop infrastructure as central banks settled into a more hands-off form of international monetary management (Thiemann Citation2014, Gabor Citation2016).

In summary, the Fed’s Eurodollar swap interventions were tightly linked to questions of domestic monetary policy. While bolstering the Eurodollar market itself, the Fed’s interventions were far from a benign exercise in the interest of international financial stability. The Fed’s management of cross-border integration was short-lived, conducted in relative secrecy, driven by domestic considerations, and abandoned once considered counterproductive to US monetary policy. As an intervention into private Eurodollar market processes, swap lines were not used again until the global financial crisis.

Swap lines and the contemporary Eurodollar market

Since the global financial crisis, swap lines have once again become a permanent feature of the global financial architecture. As the Fed currently only activates swap lines during times of crisis, they are generally associated with emergency liquidity assistance. Based on the experience of the 1960s, however, it is possible to ascertain their broader role in organising markets. As analysed above, the swap network of the 1960s was primarily intended to sustain the Bretton Woods monetary regime and only subsequently expanded to support Eurodollar interest rates. In similar fashion, the Fed’s twenty-first century swap lines developed from a primary instrument to backstop global dollar markets into a more sophisticated tool to manage the link between offshore and onshore markets during times of market stress. While this development was already visible during the global financial crisis, this section substantiates the point further by analysing the effect of swap lines on global and US money market rates during the Covid-19 pandemic.

In early March 2020, the onset of the pandemic saw unexpected volatility not just in short-term offshore funding markets, but in the US Treasury market itself, usually considered one of the most liquid markets in the world. Amidst the sudden contraction in market activity, the Treasury sell-off was motivated by a ‘dash for cash’ as investors were selling off even long-term treasuries in a bid to access cash to meet their income shortfalls. Foreign investors alone sold almost $300bn in Treasuries in March, half of which came from foreign official accounts as public reserve managers sought to acquire dollars to manage capital outflows and exchange rates (Setser Citation2020). Domestically, volatility in the Treasury market was heightened by the unwinding of hedge funds’ leveraged basis trades, while US dealers struggled to absorb the Treasury supply amidst bloated inventories and regulatory constraints (Schrimpf et al. Citation2020). As the US Treasury market serves as a key benchmark and strategic safe asset for the global financial system, funding dislocations in this market immediately reverberated through other short-term funding markets (Avdjiev et al. Citation2020).

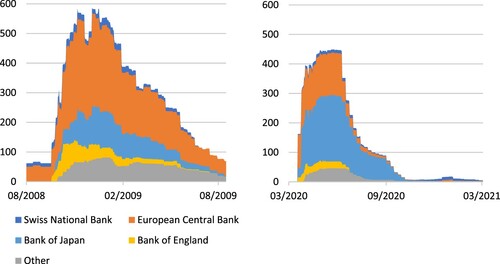

Given these problems, the Fed quickly stepped up its crisis response. Starting in early March, the Fed began to intervene in the repo market and buy Treasuries directly, with the pace of purchases accelerating significantly over the next weeks and peaking at roughly $75bn per day in late March (FOMC Citation2021, p. 17). In mid-March, the Fed added facilities for primary dealers, commercial paper, and money market funds to its emergency response, soon followed by further interventions in corporate credit, and state and municipal debt markets. At the same time, the Fed accelerated its international crisis response, most crucially by lowering the cost of its swap offerings to foreign central banks from OIS + 50 bps to OIS + 25 bps on March 15 (FOMC Citation2021, p. 15). From the end of March onwards, the uptake of swap lending effectively put a ceiling on offshore dollar funding costs. Outstanding swap amounts peaked at $449 billion in May 2020, second only to the drawings seen at the height of the global financial crisis (). In a testament to the shifting dynamics of global dollar markets, this time most of the lending did not go to Europe: in the key period from March to May 2020, the ECB only accounted for about 32 per cent of outstanding swap lines, compared to 47 per cent by the Bank of Japan. By contrast, during the global financial crisis, the ECB had accessed almost 80 per cent of swap line lending.

Figure 2. Outstanding swap amounts by counterparty during the global financial crisis and the Covid-19 pandemic, in $ billion. Source: Federal Reserve Bank of New York.

The uptake of swap lines helped lower FX swap rates in two ways: first, by allowing banks to borrow ‘outside’ dollars via their central bank, these banks can cover their own funding costs as well as increase their lending in FX swap markets, thereby passing through cheaper funding conditions to non-bank investors without direct access to a swap line (Avdjiev et al. Citation2020). Second, by providing an outside option for banks, the swap lines essentially ‘freed up’ US dealer-bank balance space on which foreign banks would otherwise rely to access dollars. This allowed dealers to lend more freely to non-banks in the FX swap market, meeting elevated demand.Footnote3 Collectively, these activities disincentivised foreigner investors from liquidating Treasuries to obtain dollar liquidity, and helped bring down stress in offshore funding markets.

Yet swap lines arguably went beyond emergency lending. By reducing swap pricing to OIS + 25 bps, the Fed was offering offshore dollar liquidity at prices well below pre-stress levels. More than simply backstopping markets, swap lines exerted broader effects on yields and lending behaviour. Effectively, the Fed moved from controlling the bounds within which offshore interest rates trade towards compressing credit spreads altogether. These interventions had significant consequences for the shape of cross-border credit relations. In normal times, offshore dollar rates generally trade at a premium to funding rates in domestic dollar markets (Mehrling Citation2015). This allows US financial institutions to take advantage of arbitrage opportunities by lending in the offshore markets.Footnote4 In April 2020, the Fed’s aggressive manipulation of offshore funding rates momentarily reversed this dynamic: by offering favourable funding conditions abroad, the Fed incentivised foreign institutions to lend dollars back into US markets. Swap lines thus managed to exert a gravitational pull that dragged down even domestic short-term funding rates.

The interplay of FX swap funding and domestic market rates can be demonstrated through an analysis of the US commercial paper (CP) market segment. Like Certificate of Deposits, CP are short-term unsecured debt instruments that are issued by banks, including foreign banks, and largely held by non-bank investors such as prime money market funds. The CP market is significant for two reasons: first, as foreign banks account for 67 percent of the overall $1tn outstanding CP in the US market, non-US banks have a significant impact on this market (Federal Reserve Citation2021, p. 56). Here, foreign banks interact with US non-banks such as prime money market funds (MMFs), which are primary lenders in significant domestic markets. Second, the CP market plays a significant role in the determination of LIBOR rates following post-2008 reforms, having replaced interbank rates as key source of unsecured global dollar funding for banks. For this reason, volatility in the CP market was the main factor behind the LIBOR-OIS spreads in early 2020, turning the market into a crucial intersection between global and domestic money markets (Eren et al. Citation2020a).

The turmoil in the CP market went through three distinct phases. During the first phase, in the last two weeks of March, prime MMFs suffered sudden outflows of about $200 billion, or 20 per cent of assets under management, as investors were withdrawing cash to meet their funding needs elsewhere (Eren et al. Citation2020b). To meet redemptions, prime MMFs were forced to liquidate large parts of their portfolios. Yet as prime MMFs sought to substitute CP for more liquid short-term assets such as Treasury bills, dealer-banks struggled to absorb the large inflow of CP amidst regulatory restrictions on their ability to expand their balance sheets (IMF Citation2020, p. 5). Dealer inventories only expanded significantly after 18 March, after the Fed announced new Primary Dealer and MMF Liquidity facilities, and lifted capital and leverage requirements associated with lending through the facilities. The temporary easing of regulatory restrictions worked in a counter-cyclical fashion by allowing dealers to expand their balance sheets and absorb greater order flows, and thus helped stabilise market liquidity conditions.Footnote5

In the following days, dealer inventories started to grow as they absorbed CP from foreign banks directly. As MMFs stopped buying, dealers started to ‘underwrite and hold’ for a spread: dealers were underwriting CP at rates up to 250 basis points, while funding themselves at the Primary Dealer Credit Facility—the Fed’s discount window facility for primary dealers that became operational on 17 March—for 25 bps (Pozsar Citation2020a, p. 2). In essence, these dealers were conducting risk-free arbitrage, borrowing low from the Fed, the safest counterparty there is, and lending at elevated market rates. They could extract such favourable terms from foreign banks because offshore dollar funding costs suggested a scramble for dollars reminiscent of the situation during the global financial crisis (Avdjiev et al. Citation2020).

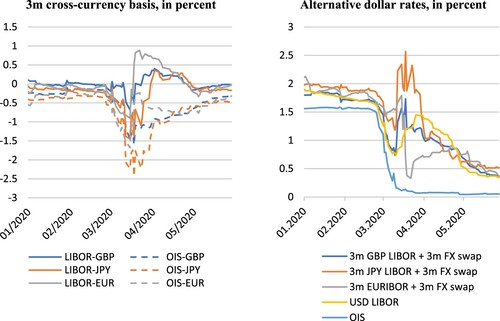

Following the Fed’s announcement on 15 March that it would lower the cost of its standing swap line network to OIS+25 bps, swap lines saw immediate and strong uptake by the Bank of Japan and ECB. On 19 March, the Fed expanded its swap lines to include all previous fourteen counterparties from the global financial crisis. To ease funding conditions further, the Fed switched from weekly to daily swap operations on 20 March, and by the end of March swap line uptake had reached critical mass to bring down cross-currency basis spreads in various currencies ().Footnote6

Figure 3. Short-term funding markets under stress. Source: Bloomberg Terminal, author’s calculations.

The second phase of CP market turmoil was characterised by the effect of swap line uptake. From early to mid-April, LIBOR-OIS spreads started to fall, and the cross-currency basis even went positive in some cases, offering a discount on dollar borrowing (Pozsar Citation2020a). At this point, funding prices started to fragment. For banks in monetary jurisdictions with access to a swap line, FX swap funding costs implied a discount on unsecured funding at LIBOR rates, whereas other banks without access to cheap outside risk-free funding still struggled with a dollar funding premium in private markets. With bank funding costs diverging within global markets, ‘something like a tug of war emerged’ between OIS-linked swap lines and interbank rates as to which one would anchor FX swap pricing, a process that eventually dragged down both LIBOR and FX swap implied funding costs significantly (Eren et al. Citation2020a, p. 4). By shaping market prices directly, the Fed’s swap lines thus prompted other market rates to fall in line.Footnote7

In the third phase, falling FX swap costs triggered inflows into prime MMFs that calmed CP rates. During the last two weeks of April, LIBOR-OIS fell by a dramatic 62 bps as foreign banks brought liquidity from offshore markets back into the domestic CP market (Pozsar Citation2020a, p. 3). Spurred by the on-going fall in the FX swap implied cost of dollar funding, foreign banks suddenly found it cheaper to raise dollars offshore in the FX swap market and then lend at LIBOR prices. Such arbitrage trades contributed to a narrowing of spreads (a reduction of LIBOR rates), and thus helped reduce stress in the CP market (Eren et al. Citation2020a). As a result, foreign banks went from being price takers to price setters within a month: as funding costs fell in the CP market and prime MMFs started to see funding inflows again, foreign banks could use cheap FX swap implied funding rates to extract favourable rates for commercial paper. Over the course of a month, this brought CP funding rates down from 250 bps to around 50 bps by the end of April (Pozsar Citation2020a).

It is possible that the effect of swap lines on domestic markets was an unintended albeit welcome by-product of international last resort lending. Unlike for the earlier time periods discussed in this article, internal documents such as Federal Open Market Committee Transcripts are not yet publicly available for 2020. Yet there are reasons to assume that Fed policymakers considered swap lines useful in addressing domestic market volatility. As Fed Chairman Powell (Citation2020, p. 4, emphasis added) highlighted during the press conference announcing swap interventions on 15 March, ‘when dollar funding pressures emerge abroad, those central banks [with access to a swap line] can contain the pressures in their jurisdictions and prevent them from impeding the flow of credit here at home.’

The Fed also appears to have favoured swap lines as intervention tool over the domestic Commercial Paper Funding Facility (CPFF). Swap lines effectively allow the Fed to sidestep private markets by lending against foreign currency collateral to foreign central banks, which in turn assume the risk of lending to private actors. The CPFF, by contrast, is a direct backstop for an unsecured funding market and potentially exposes the Fed to losses on its lending. To avoid this situation, under the CPFF the Fed provided funding via a special purpose vehicle, backed by a $10bn equity investment from the US Treasury that served as loss-absorbing capital, and priced at OIS + 110 bps for A1/P1 issuers, and OIS + 200 bps for those of a lower credit rating. The CPFF thus offered funding considerably above swap rates, and overall usage of the facility remained limited, peaking at $4.3bn after a month in operation (FOMC Citation2021, p. 29). The Fed’s clear preference for secured lending, as well as the high prevalence of foreign banks in the CP markets and its broader links to global funding markets that were already experiencing severe funding pressures, might have prompted the Fed to address short-term funding dislocations through forceful intervention in the offshore markets (Pozsar Citation2020b, p. 3).

In summary, swap lines exerted a profound influence on market dynamics. Swap lines effectively induced a form of international cross-currency arbitrage that saw highly unusual cross-border money flows in which foreign banks sourced dollars offshore via swap lines to ease dollar liquidity conditions in domestic US markets. Effectively, the Fed relied on a positive spillback as transmission mechanism to shape domestic money market conditions. Though the Fed’s aggressive interventions and the violation of the Bagehotian principle of last resort lending have been justified in terms of the unprecedented nature of the pandemic shock (Hauser Citation2021), the historical experience of the 1960s suggests an alternative interpretation: far from simply backstopping markets and compressing credit spreads, swap lines played a useful function in restructuring the feedback effects between domestic and global dollar markets.

Conclusion

Swap lines can serve a variety of purposes. Though typically associated with exchange rate management under the Bretton Woods system and last-resort-lending since the global financial crisis, this article has shown that swap lines have also played a key role in managing the cross-border links between domestic and global dollar markets. Influencing private credit relations is not merely a question of financial stability: by promoting specific credit channels and liquidity dynamics, swaps restructure cross-border flows in the broader interests of US monetary policy and secure the domestic foundations of global dollar intermediation.

The mixing of domestic and international policy concerns is not unproblematic. As the article has demonstrated, swap lines have tended to reinforce the Fed’s monetary policy stance. Conversely, swap lines were abandoned when considered counterproductive to the broader objectives of domestic monetary policy. In the late 1960s, swap line interventions into the emerging Eurodollar market were ended because they were seen as fuelling inflation. Similarly, in the 1980s the Fed abandoned swap lines for exchange rate management purposes because it feared that foreign exchange interventions would undermine the credibility of its commitment to domestic price stability (Bordo et al. Citation2015). Since the global financial crisis, emergency lending via swap lines and easy monetary policy have worked in lockstep. Yet it is not impossible to imagine a scenario in which a return of inflation prompts the Fed to hike rates without committing itself to swap lending to mitigate the effects of its policy decision on the international monetary system. Following the 2020 interventions, central bankers have already started to pose the question of ‘how to deal with market dysfunction in periods when the optimal policy response differs from that required for monetary policy purposes’ (Hauser Citation2021, p. 11).

In summary, while monetary policy considerations were usually not the primary reason for establishing swap lines, the Fed has generally proven itself unwilling to act internationally against the interests of its domestic mandate. It is precisely because swap lines always impact domestic US markets that monetary policy considerations remain integral to the broader politics of swap line lending. The unresolved dilemma is that cross-border capital flows require a degree of management, rather than just a backstop. The lack of a truly global institution responsible for the international monetary system is a long-established policy concern (Kindleberger Citation2000). In the system’s current configuration, the Fed is the only institution capable of effectively supporting the dollar-centric international order. But while the Fed has proven willing to intervene internationally to mitigate or even harness the effects of the global financial cycle on US markets, it has been less attentive to the role of its monetary policy in driving global monetary imbalances (Schwartz Citation2016). As a result of this lopsided focus, swaps have tended to reinforce existing inequalities in the global economy. The Fed’s early swap interventions bolstered the growth of transatlantic capital relations at the heart of the emerging Eurodollar market and contributed to the rise of financial globalisation and financialisation more broadly (Helleiner Citation1994, Braun et al. Citation2020). Since the global financial crisis, the Fed’s swap network has further entrenched the international monetary hierarchy expressed by cross-border capital flows. In its pursuit of monetary governability, the Fed’s selective swap lending has endorsed permissive financing conditions for financial institutions from core monetary jurisdictions, while actors from peripheral economies continue to face penalty rates in international markets in times of stress (Murau et al. Citation2021), leaving them vulnerable to short-term international capital flows (Gallagher Citation2015, Bonizzi and Kaltenbrunner Citation2018).

In light of these issues, the importance of understanding global liquidity conditions and their shifting drivers should become increasingly clear. As this article has shown, global liquidity is not just a problem of financial stability, but central to broader and deeply political questions about market organisation. As such, it presents an important fault line for monetary governance: how central banks situate themselves strategically in relation to private market activity has significant consequences for which trading activities can be done profitably and which actors gain in importance over time (Pape Citation2020). Given the central role of the dollar, the potentially conflicting interests that confront policymakers with regards to domestic and international monetary management is particularly relevant for studies of the Federal Reserve and carries broader significance for our understanding of the international monetary system.

Acknowledgements

For support and feedback on earlier versions of this paper, I thank Matthew Watson, Chris Clarke, Steffen Murau, Iain Hardie, Matthias Thiemann, Onur Özgöde, Mathis Richtmann, Mareike Beck, Dylan Cassar, Johannes Petry, Tobias Pforr and Robin Jaspert, as well as the participants of the ‘Financial Stability Research Seminar’ on 21 January 2021 and the participants of the Warwick Critical Finance Group ‘Manuscript Development Workshop’ on 18 February 2021.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Fabian Pape

Fabian Pape is a PhD Candidate in International Political Economy at the Department of Politics and International Studies, University of Warwick (UK). His research focuses on the role of the Federal Reserve in the transformation and internationalisation of US money markets.

Notes

1 While Bagehot only discusses last resort lending in a domestic context, the framework has subsequently been expanded to the international level (Kindleberger Citation2000).

2 These counterparties are the Bank of England, Bank of Canada, European Central Bank, Bank of Japan, and Swiss National Bank. The standing swap network was first agreed in November 2011.

3 Interview: economist, research department, central bank (videoconference, 28 September 2020)

4 Interview: Managing Director, research department, global bank (telephone, 23 September 2020)

5 Interview: Economist, global regulatory institution (telephone, 27 July 2020)

6 The cross-currency basis measures the spread between funding at LIBOR rates and through the FX swap market. A negative JPY/USD basis, for instance, implies a hedging cost to obtain USD against Japanese Yen in the swap market.

7 Interview: Former US Treasury economist (videoconference, 15 September 2020).

References

- Aizenman, J. and Pasricha, G.K., 2009. Selective swap arrangements and the global financial crisis: analysis and interpretation. NBER Working Paper, 14821.

- Aldasoro, I., Ehlers, T., and Eren, E., 2019. Global banks, dollar funding, and regulation. BIS Working Papers No 708: Bank for International Settlements.

- Aldasoro, I., et al., 2020. Central bank swap lines and cross- border bank flows. BIS Bulletin 34: Bank for International Settlements.

- Altamura, C., 2017. European banks and the rise of international finance. London: Routledge.

- Avdjiev, S., Eren, E., and McGuire, P., 2020. Dollar funding costs during the Covid-19 crisis through the lens of the FX swap market. BIS Bulletin, 1 April: Bank for International Settlements.

- Avdjiev, S., McCauley, R.N., and Shin, H.S., 2016. Breaking free of the triple coincidence in international finance. Economic policy, 31 (87), 409–451. doi:https://doi.org/10.1093/epolic/eiw009.

- Bahaj, S. and Reis, R., 2019. Central bank swap lines. Bank of England: Staff Working Paper No. 741.

- Baker, A., 2013. The New Political Economy of the macroprudential ideational shift. New political economy, 18 (1), 112–139. doi:https://doi.org/10.1080/13563467.2012.662952.

- Bindseil, U., 2004. The operational target of monetary policy and the rise and fall of reserve position doctrine. Working Paper Series, No. 372: European Central Bank.

- Birk, M. and Thiemann, M., 2020. Open for business: entrepreneurial central banks and the cultivation of market liquidity. New political economy, 25 (2), 267–283.

- Bonizzi, B. and Kaltenbrunner, A., 2018. Liability-driven investment and pension fund exposure to emerging markets: a minskyan analysis. Environment and planning A: economy and space, 51 (2), 420–439. doi:https://doi.org/10.1177/0308518X18794676.

- Bordo, M.D., Humpage, O.F., and Schwartz, A.J., 2015. Strained relations: US foreign-exchange operations and monetary policy in the twentieth century. Chicago: University of Chicago Press.

- Bortz, P.G. and Kaltenbrunner, A., 2017. The international dimension of financialization in developing and emerging economies. Development and change, 49 (2), 375–393. doi:https://doi.org/10.1111/dech.12371.

- Braun, B., 2018. Central banking and the infrastructural power of finance: the case of ECB support for repo and securitization markets. Socio-economic review. doi:https://doi.org/10.1093/ser/mwy008.

- Braun, B. and Gabor, D., 2020. Central banking, shadow banking, and infrastructural power. In: P. Mader, D. Mertens, and N. van der Zwan, eds. The Routledge international handbook of financialization. London: Routledge, 241–252.

- Braun, B., Krampf, A., and Murau, S., 2020. Financial globalization as positive integration: monetary technocrats and the Eurodollar market in the 1970s. Review of international political economy, 1–26. doi:https://doi.org/10.1080/09692290.2020.1740291.

- Broz, J.L., 2015. The politics of rescuing the world's financial system: the Federal Reserve as a global lender of last resort. Korean journal of international studies, 13 (2), 323–351.

- Bruno, V. and Shin, H.S., 2015. Capital flows and the risk-taking channel of monetary policy. Journal of monetary economics, 71, 119–132. doi:https://doi.org/10.1016/j.jmoneco.2014.11.011.

- Burger, A., 1969. A historical analysis of the credit crunch of 1966. Federal Reserve Bank of St. Louis Review: September.

- Calvo, G.A., Leiderman, L., and Reinhart, C.M., 1996. Inflows of capital to developing countries in the 1990s. Journal of economic perspectives, 10 (2), 123–139. doi:https://doi.org/10.1257/jep.10.2.123.

- Carré, E. and Le Maux, L., 2020. The federal reserve’s dollar swap lines and the European Central Bank during the global financial crisis of 2007–09. Cambridge journal of economics, 44 (4), 723–747.

- Chwieroth, J.M., 2008. Normative change from within: the international monetary fund's approach to capital account liberalization. International studies quarterly, 52 (1), 129–158. doi:https://doi.org/10.1111/j.1468-2478.2007.00494.x.

- Cohen, B., 2015. Currency power. Understanding monetary rivalry. Princeton, NJ: Princeton University Press.

- Coombs, C.A., 1967. Treasury and federal reserve Foreign exchange operations. Federal Reserve Bulletin, March. Washington, DC: Board of Governors of the Federal Reserve System.

- Correa, R., Du, W., and Liao, G., 2020. U.S. banks and global liquidity. International Finance Discussion Papers 1289. Washington, DC: Board of Governors of the Federal Reserve System.

- Dutta, S.J., 2020. Sovereign debt management and the transformation from keynesian to neoliberal monetary governance in britain. New political economy, 25 (4), 675–690. doi:https://doi.org/10.1080/13563467.2019.1680961.

- Eichengreen, B., 2009. Out of the box thoughts about the international financial architecture. IMF Working Paper WP/09/116. International Monetary Fund.

- Eren, E., Schrimpf, A., and Sushko, V., 2020a. US dollar funding markets during the Covid-19 crisis – the international dimension. BIS Bulletin, 12 May: Bank for International Settlements.

- Eren, E., Schrimpf, A., and Sushko, V., 2020b. US dollar funding markets during the Covid-19 crisis – the money market fund turmoil. BIS Bulletin, 12 May: Bank for International Settlements.

- Federal Reserve. 2021. Financial stability report. Washington: Board of Governors of the Federal Reserve System.

- FOMC, 2007. Conference call of the federal open market committee, 6 December. Available from: https://www.federalreserve.gov/monetarypolicy/files/FOMC20071206confcall.pdf [Accessed 25 June 2021].

- FOMC, 2021. Open market operations during 2020. Federal Reserve Bank of New York, May 2021.

- Gabor, D., 2016. The (impossible) repo trinity: the political economy of repo markets. Review of international political economy, 23 (6), 967–1000.

- Gabor, D., 2020. Critical macro-finance. A theoretical lens. Finance and society, 6 (1), 45–55.

- Gallagher, K., 2015. Ruling capital: emerging markets and the reregulation of cross-border finance. Ithaca: Cornell University Press.

- Giannini, C., 2011. The age of central banks. Cheltenham: Edward Elgar.

- Goldberg, L.S., Kennedy, C., and Miu, J., 2010. Central bank dollar swap lines and overseas dollar funding costs. NBER. Available from: http://www.nber.org/papers/w15763.

- Hardie, I. and Maxfield, S., 2016. Atlas constrained: the US external balance sheet and international monetary power. Review of international political economy, 23 (4), 583–613. doi:https://doi.org/10.1080/09692290.2016.1176587.

- Hardie, I. and Thompson, H., 2020. Taking Europe seriously: European financialization and US monetary power. Review of international political economy, 1–19. doi:https://doi.org/10.1080/09692290.2020.1769703.

- Hauser, A., 2021. From Lender of last resort to market maker of last resort via the dash for cash: why central banks need new tools for dealing with market dysfunction. Speech at Reuters, London. Available from: https://www.bankofengland.co.uk/-/media/boe/files/speech/2021/january/why-central-banks-need-new-tools-for-dealing-with-market-dysfunction-speech-by-andrew-hauser.pdf?la=en&hash=A02A833632782A87D97A1F9EFEB26205B4E8DF13 [Accessed 25 June 2021].

- He, D. and McCauley, R., 2012. Eurodollar banking and currency internationalisation. Bank for international settlements: BIS quarterly review, June.

- Helleiner, E., 1994. States and the reemergence of global finance: from Bretton Woods to the 1990s. Ithaca, NY: Cornell University Press.

- Helleiner, E., 2014. The status Quo crisis: global financial governance after the 2008 meltdown. New York: Oxford University Press.

- Hockett, R.C. and Omarova, S.T., 2016. The finance franchise. Cornell law review, 102, 1143.

- IMF, 2020. Global financial stability report, April. Washington, DC: International Monetary Fund.

- Kapstein, E.B., 1994. Governing the global economy: international finance and the state. Cambridge, MA: Harvard University Press.

- Kershaw, P.V., 2018. Averting a global financial crisis: the US, the IMF, and the Mexican debt crisis of 1976. The international history review, 40 (2), 292–314. doi:https://doi.org/10.1080/07075332.2017.1326966.

- Kindleberger, C.P., 2000. Manias, panics and crashes: a history of financial crises. 4th ed. Hoboken, NJ: Palgrave Macmillan.

- Kirshner, J., 2006. Currency and coercion in the twenty-first century. In: D. Andrews, ed. International monetary power. Ithaca: Cornell University Press, 139–161.

- Klopstock, F., 1968. Euro-dollars in the liquidity and reserve management of US banks. Federal Reserve Bank of New York: Monthly Review, July.

- Knafo, S., 2013. The making of modern finance: liberal governance and the gold standard. New York: Routledge.

- Konings, M., 2007. The institutional foundations of US structural power in international finance: from the re-emergence of global finance to the monetarist turn. Review of international political economy, 15 (1), 35–61. doi:https://doi.org/10.1080/09692290701751290.

- Konings, M., 2011. The development of American finance. New York: Cambridge University Press.

- Lockwood, E., 2015. Predicting the unpredictable: value-at-risk, performativity, and the politics of financial uncertainty. Review of international political economy, 22 (4), 719–756. doi:https://doi.org/10.1080/09692290.2014.957233.

- MacKenzie, D., 2005. Opening the black boxes of global finance. Review of international political economy, 12 (4), 555–576. doi:https://doi.org/10.1080/09692290500240222.

- McCauley, R. and Schenk, C., 2020. Central bank swaps then and now: swaps and dollar liquidity in the 1960s. Bank for International Settlements: BIS Working Papers, 851.

- McDowell, D., 2012. The US as ‘Sovereign international last-resort lender’: the fed's currency swap programme during the great Panic of 2007–09. New political economy, 17 (2), 157–178. doi:https://doi.org/10.1080/13563467.2010.542235.

- McDowell, D., 2017. Brother, can you spare a billion?: the United States, the IMF, and the international lender of last resort. New York: Oxford University Press.

- McDowell, D., 2019. Emergent international liquidity agreements: central bank cooperation after the global financial crisis. Journal of international relations and development, 22, 441–467.

- McGuire, P. and von Peter, G., 2009. The US dollar shortage in global banking and the international policy response. Bank for International Settlements: BIS Working Papers, 291.

- Mehrling, P., 2011. The New lombard street: how the Fed became the dealer of last resort. Princeton, NJ: Princeton University Press.

- Mehrling, P., 2014. Why central banking should be re-imagined. Bank for International Settlements: BIS Papers No 79.

- Mehrling, P., 2015. Elasticity and discipline in the global swap network. International journal of political economy, 44 (4), 311–324. doi:https://doi.org/10.1080/08911916.2015.1129848.

- Miranda-Agrippino, S. and Rey, H., 2020. U.S. monetary policy and the global financial cycle. The review of economic studies, 87 (6), 2754–2776. doi:https://doi.org/10.1093/restud/rdaa019.

- Moessner, R. and Allen, W.A., 2010. Central bank co-operation and international liquidity in the financial crisis of 2008-2009. BIS Working Paper, No. 310, 1–89. doi:https://doi.org/10.2139/ssrn.1631791.

- Murau, S., 2017. Shadow money and the public money supply: the impact of the 2007–2009 financial crisis on the monetary system. Review of international political economy, 24 (5), 802–838. doi:https://doi.org/10.1080/09692290.2017.1325765.

- Murau, S., Pape, F., and Pforr, T., 2021. The hierarchy of the offshore US-dollar system: on swap lines, the FIMA repo facility and special drawing rights. GEGI Study, Global Development Policy Center, Boston University. February.

- Murau, S., Rini, J., and Haas, A., 2020. The evolution of the Offshore US-dollar system: past, present and four possible futures. Journal of institutional economics, 16 (6), 767–783.

- Ocampo, J.A., 2017. Resetting the international monetary (Non)system. Oxford: Oxford University Press.

- Panitch, L. and Gindin, S., 2012. The making of global capitalism: the political economy of American empire. London: Verso Books.

- Pape, F., 2020. Rethinking liquidity. A critical macro-finance view. Finance and society, 6 (1), 67–75.

- Pistor, K., 2013. A legal theory of finance. Journal of comparative economics, 41 (2), 315–330. doi:https://doi.org/10.1016/j.jce.2013.03.003.

- Powell, J., 2020. Transcript of Chair Powell’s Press conference call. Federal Reserve: 15 March.

- Pozsar, Z., 2020a. Singularity Global Money Notes #30. Credit Suisse: 14 May 2020.

- Pozsar, Z., 2020b. U.S. dollar libor and war finance. Global Money Notes #29. Credit Suisse: 14 April 2020.

- Prasad, E.S., 2014. The dollar trap: how the U.S. dollar tightened Its grip on global finance. Princeton, NJ: Princeton University Press.

- Rey, H., 2015. Dilemma not trilemma: the global financial cycle and monetary policy independence. Cambridge, MA: NBER.

- Ricks, M., 2018. Money as infrastructure. Columbia business law review, 3, 757.

- Sahasrabuddhe, A., 2019. Drawing the line: the politics of federal currency swaps in the global financial crisis. Review of international political economy, 26 (3), 461–489. doi:https://doi.org/10.1080/09692290.2019.1572639.

- Schenk, C., 2010. The decline of sterling. Managing the retreat of an international currency, 1945–1992. Cambridge: Cambridge University Press.

- Schrimpf, A., Shin, H.S., and Sushko, V., 2020. Leverage and margin spirals in fixed income markets during the Covid-19 crisis. BIS Bulletin, 2 April: Bank for International Settlements.

- Schwartz, H.M., 2011. Subprime nation: American power, global capital, and the housing bubble. Ithaca, NY: Cornell University Press.

- Schwartz, H.M., 2016. Banking on the FED: QE1-2-3 and the rebalancing of the global economy. New political economy, 21 (1), 26–48. doi:https://doi.org/10.1080/13563467.2015.1041480.

- Setser, B., 2020. Did the dollar's position as the leading reserve currency help hold treasury yields down this spring? Follow the money. Council on Foreign Relations. Available from: https://www.cfr.org/blog/did-dollars-position-leading-reserve-currency-help-hold-treasury-yields-down-spring [Accessed 25 June 2021].

- Shin, H.S., 2012. Global banking glut and loan risk premium. IMF economic review, 60 (2), 155–192. doi:https://doi.org/10.1057/imfer.2012.6.

- Shin, H.S. and Turner, P., 2015. What does the new face of international financial intermediation mean for emerging market economies? In: B.D. France, ed. Financing the economy: new avenues for growth. Paris: Banque de France, 25–36.

- Strange, S., 1988. States and markets. London: Continuum.

- Thiemann, M., 2014. In the shadow of basel: how competitive politics bred the crisis. Review of international political economy, 21 (6), 1203–1239. doi:https://doi.org/10.1080/09692290.2013.860612.

- Tooze, A., 2018. Crashed: how a decade of financial crises changed the world. New York: Allen Lane.

- Ugolini, S., 2017. The evolution of central banking: theory and history. London: Palgrave.

- US Congress, 2009. Economic and budget challenges for the short and long term, 111th Congress, 1st Sess., Washington, DC, 3 March.

- Walter, T. and Wansleben, L., 2019. How central bankers learned to love financialization: the fed, the bank, and the enlisting of unfettered markets in the conduct of monetary policy. Socio-Economic Review. doi:https://doi.org/10.1093/ser/mwz011.