?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Southern European countries are widely considered a distinct type of capitalism, but they have experienced a varied growth performance, both over time and across countries. This paper investigates the growth drivers in southern Europe since the mid-1990s. We consider a broad set of potential growth drivers derived from the literature on Mediterranean capitalism and Comparative Political Economy more broadly. On the demand side, these include the role of house prices (as the main financial variable; highlighted in parts of the growth models approach); the ‘financial curse’ hypothesis (which posits that financial inflows caused house price booms and crowded out manufacturing activities); and Keynesian arguments on the impact of fiscal policy. On the supply side, these encompass the cost competitiveness argument (consistent with mainstream economics and the Varieties of Capitalism approach), research-led technological change; and neo-structuralist arguments regarding the productive capacity. We find strong evidence for the growth contributions of house prices and fiscal policy. While these findings are generally supportive of extant analysis of these economies as finance-led rather than export-led, they call for a more serious integration of house prices in growth model analysis and for a more systematic analysis of the growth impact of fiscal policy.

Introduction

While southern European countries are regarded by Comparative Political Economy (CPE) as a distinct type of capitalism (e.g. Amable Citation2003, Molina and Rhodes Citation2007), they have experienced quite different growth trajectories over the past two decades (e.g Burroni, Colombo and Regini Citation2021). Most of them experienced a boom prior to the Global Financial Crisis (GFC), but since then Greece has had a prolonged depression and Italy has stagnated, while Spain and Portugal have seen substantial growth since the Euro crisis. This raises the question of what the drivers behind these different performances are.

Within CPE, the Varieties of Capitalism (VoC) approach has focused on the institutional determinants of competitiveness, and VoC-inspired research thus tends to highlight cost competitiveness due to differing labour relations (Johnston et al. Citation2014) or on innovative capacity (Soskice Citation2022). The growth models approach (GMA), incorporating insights from post-Keynesian macroeconomics, emphasises demand factors, contrasting debt-led and export-led models (Baccaro and Pontusson Citation2016). Kohler and Stockhammer (Citation2022) highlight house price dynamics, fiscal policy and non-price competitiveness as crucial factors explaining growth. All of these are based on studies covering diverse sets of European economies, but similar themes occur in the literature focusing on ‘Mediterranean capitalism’: Burroni et al. (Citation2021b) conclude that weak innovation capacity has been more important than a lack of cost competitiveness, while noting the role of international financial inflows as a potential explanatory factor. From a GMA perspective, Baccaro (Citation2021) argues that southern European economies exhibit a peripheral form of consumption-led model, where credit creation has been central. Pérez (Citation2021) and Sebastian Dellepiane-Avellaneda, Hardiman and Las Heras (Citation2021) highlight the role of financial inflows in explaining the regiońs trade deficits, with the latter arguing that capital inflows have had a negative impact on the industrial and thus export capacity.

The contribution of this paper is that it systematically tests different arguments that have been put forward to explain the growth trajectories of Southern European countries in the last three decades. In so doing, this paper considers differences in key variables within Southern European economies rather than contrasting these economies against other European economies. This is important for both theoretical and empirical reasons. By focusing on a set of countries sharing similar historical and institutional conditions, our empirical analysis illustrates the factors that have influenced GDP growth on a set of countries with similar conditions and comparable positions in the international productive and financial hierarchies. In contrast, a more heterogenous sample, while interesting in its own right, would compare countries with different levels of development and at different positions in the international political economy, which may impact how they respond to the changes in growth drivers, i.e. effects may differ. Our findings also provide an important empirical foundation for the discussion of whether countries in a given variety of capitalism follow a similar growth model.

We consider a wide range of potential growth drivers. In addition to the cost competitiveness argument (consistent with mainstream economics and the VoC approach) and technological factors such as research and development (stressed by Burroni, Colombo and Regini Citation2021 and Soskice Citation2022), we also analyze neo-structuralist arguments regarding the productive capacity (Simonazzi et al. Citation2013, Storm and Naastepad Citation2016) and Keynesian arguments on the impact of fiscal policy. As regards financial factors we analyse house prices (highlighted in parts of GMA), and the ‘financial curse’ hypothesis, which posits that financial inflows into the booming real estate and construction sectors have eroded manufacturing capabilities (Sebastian Dellepiane-Avellaneda, Hardiman and Las Heras Citation2021). Our main findings are that house prices (which have cyclical dynamics) and fiscal policy have had a strong impact on growth. In contrast, we fail to find evidence for the impact of cost competitiveness (measured as unit labour costs, ULC) and of R&D expenditures. Nor do we find evidence for the financial curse hypothesis or that economic complexity of exports determines growth. Not only is the impact of house prices and fiscal policy statistically significant, but these two variables potentially explain around half of the actual GDP growth in Southern Europe, although with notable variability across different countries and time periods.

Methodologically we pursue a quantitative approach and build on Kohler and Stockhammer (Citation2022), but focus on Southern European countries, consider a broader set of potential growth drivers and offer panel results (due to the longer time period covered). We first present scatter plots with bivariate regression for each hypothesis, and then a multivariate panel regression to jointly consider the potential drivers. We organize the data for the five southern European countries (Greece, Portugal, Spain, Italy and France)Footnote1 into four periods, each of which represents a distinct episode: 1988–98 is the (pre-Euro) time of the European monetary system; 1999–2008 the pre-GFC boom, 2009–13 the crisis period, covering the Global Financial Crisis and the Euro crisis; and 2014–19 is the post-crisis period until the onset of the covid crisis. Thus, we have a set of long averages that allows econometric analysis to identify medium-term effects.

The paper is structured as follows. Section 2 reviews the relevant literature and distills the working hypotheses to be explored. Sections 3–8 offer binary scatter plots for house price boom and bust hypothesis, the financial curse hypothesis, the fiscal policy hypothesis, the cost competitiveness hypothesis, the research-led technological change hypothesis, and the structural hypothesis respectively. Section 9 presents the regression analysis and discussion of the results. Finally, section 10 concludes.

Working hypotheses on potential growth drivers

Southern European countries are treated as a distinct country group in most of the CPE literature. In the VoC tradition, similarities in terms of labour market institutions (organized but fragmented labour relations), and the financial sector (bank based) are highlighted (Amable Citation2003, Molina and Rhodes Citation2007), while wide-ranging state intervention is often regarded as compensating for lack of institutional coordination. Recent studies on the role of the state (Capano and Lippi Citation2021), labor market and industrial relations (Afonso et al. Citation2021) and welfare systems (Guillén et al. Citation2021) have concluded that ‘Mediterranean capitalism’ still has certain distinctive features, despite some polarization between the (modernizing) Iberian countries and (the more traditional) Greece and Italy. In the following, we present the main positions in the debate and what they imply for potential growth drivers.

In the VoC tradition competitiveness has long been at the centre, with an emphasis that it can be achieved by different means and institutional settings. For the Mediterranean VoC, a comparative advantage in certain sectors were initially identified (Amable Citation2003), but in the context of the Euro crisis it has often been argued that the uncoordinated wage bargaining systems gave rise to inflationary pressures from non-tradeable sectors that eventually undermined overall competitiveness (Johnston et al. Citation2014). In their concluding chapter, Burroni, Colombo and Regini (Citation2021) highlight three factors commonly discussed as important for explaining growth: cost competitiveness, finance and innovation. They argue that innovation, in particular research and development, has been a major factor behind the weak development, but are skeptical about the role of cost competitiveness. In a similar vein, but for a much broader country group Soskice (Citation2022) emphasizes the centrality of innovation, in particular, R&D for understanding growth trajectories. Burroni, Colombo and Regini (Citation2021) explain Southern European countries’ difficulties to compete in the international knowledge economy as a result of inadequate human capital formation, R&D investment, and innovation policies.

GMA puts demand side factors at the centre. Based on GDP growth decomposition, this has often meant contrasting consumption or debt-led models to export-led model, with Southern European economies, at least until the GFC, clearly located in the former category. Hein et al. (Citation2021) argue that many of them have shifted towards export-led models since the GFC, while Kohler and Stockhammer (Citation2022) argue that the positive trade balances Southern European countries have experienced since the GFC are a result of a reduction in imports due to contracting domestic demand amidst deep recessions rather than of increased exports. In line with the latter argument, Baccaro concludes that the Mediterranean growth model, both before and after the GFC, is ‘an unstable variant’ of what he terms ‘a peripheral consumption-led model’ (Citation2021, p. 20). The instability of southern European countries’ growth performance derives from the fact that they show a ‘tendency to accumulate foreign debt through sustained current account deficits’ (Citation2021), which in peripheral economies can only be financed temporarily. Stockhammer and Wildauer (Citation2016, Citation2018) document the centrality of rising household debt and real estate prices for southern European economies and show that household debt is largely driven by real estate prices. Given the central role fiscal policy has in Keynesian macroeconomics and the intense debates at the time of the Euro crisis of the Troika-mandated austerity policies, it is surprising how little prominence GMA has given to fiscal policy until recently. But over the past few years, some contributions based on post-Keynesian economics have included the role of fiscal policy in the GMA approach (most explicitly Kohler and Stockhammer Citation2022, but also Hein and Martschin Citation2021, Morlin et al. Citation2022, Prante et al. Citation2022).

While there is broad agreement on the resulting debt-led growth model, there is less agreement on its origin. While Baccaro and Bulfone (Citation2022) highlight (for Spain and Italy) the different political coalitions underpinning the growth models, many authors draw inspiration from international political economy arguments that place countries in their position in productive or financial hierarchies. Pérez (Citation2021) argues that financial inflows to southern Europe were strongly pro-cyclical and mostly concentrated on the real estate and construction sector. This lowered aggregate productivity growth and contributed to current account deficits (by increasing imports via debt-fueled domestic demand). Sebastian Dellepiane-Avellaneda, Hardiman and Las Heras (Citation2021) take this further and argue that financial inflows turned into a ‘financial curse’ (similar to the resource curse) that has undermined the manufacturing sector in these countries. Inspired by the neo-structuralist arguments, Simonazzi et al. (Citation2013) and Storm and Naastepad (Citation2016) argue that the position of these economies in the international division of labour traps them in low-tech exports with low-income elasticities, which makes export-led growth model impossible.

We use the extant literature to derive a broad set of hypotheses on potential growth drivers, which are summarized in . The first set of growth drivers are on the demand side and include hypotheses regarding financial factors and fiscal policy.Footnote2 The housing boom–bust hypothesis argues that housing markets experience endogenous boom bust cycles and that house prices have a substantial impact on economic growth via consumption (so-called wealth effects) and residential investment. In GMA and PKE Stockhammer (Citation2015) and Stockhammer and Wildauer (Citation2016) have made the case that the debt-driven growth model is based on house price inflation. Kohler and Stockhammer (Citation2022) argue that the GFC and the subsequent downturn should be understood as the downswing of a finance-led growth model rather than the shift away from a finance-led model. Since the GFC there has been growing research on financial cycles and house prices feature prominently as a key variable therein (e.g. Drehmann et al. Citation2012, Aikman et al. Citation2015).

Table 1. Growth drivers and working hypotheses.

The financial curse hypothesis, which originated in the critical financialization literature (thus outside the GMA; Sebastian Dellepiane-Avellaneda, Hardiman and Las Heras Citation2021, Gambarotto et al. Citation2019, Mamede Citation2020), takes as a starting point the idea that ‘the financial surpluses of the European periphery may well be responsible for its current account deficits’ (Rodrigues and Reis Citation2012, p. 191). This hypothesis argues that financial inflows contributed to Southern Europés trade deficits by reducing these countries’ export capabilities, as a result of the shift in finance and other productive resources to non-tradeable sectors. While there are some similarities between the previous and this hypothesis, as both highlight financial factors and the centrality of real estate within them, the two hypothesis differ in whether they focus on the international or the domestic arena: the financial curse hypothesis locates the origin of financial dynamics to large extent abroad (financial inflows) whereas the house price hypothesis is agnostic about the national or international origins, but highlights the (domestic) financial cycle that may be amplified by financial flows. The house price hypothesis explains domestic growth (which will typically come with current account imbalances due to import demand), whereas the financial curse argues that inflows (and housing booms) negatively affect the manufacturing base and thus exports.

The GFC and the Euro crisis have led to intense debates in economics and a reformulation of Keynesian arguments, which have only been partially incorporated into the CPE literature. Few of the early studies of GMA feature fiscal policy. Recently, several of the GMA contributions from the economics side give fiscal policy more prominence (Hein and Martschin Citation2021, Kohler and Stockhammer Citation2022, Morlin et al. Citation2022). This leads to the Keynesian fiscal policy hypothesis, which posits that fiscal policy has a strong impact on economic growth, in particular in times of recession. In the language of economics: fiscal multipliers are large. Famously Blanchard and Leigh (Citation2014) demonstrated that the IMF’s macroeconomic model had severely understated the size of the fiscal multiplier and thus the economic impact of austerity. Since then, mainstream economic policy institutions (i.e. OECD, IMF) often suggest fiscal multipliers in the order of magnitude of 2–2.5 during recession (or during times when the interest rate is close to zero) (Batini et al. Citation2014). While this is an important change in mainstream economics, it has long been part of post-Keynesian theory and policy (Arestis and Sawyer Citation2003, Allain Citation2015, Hein Citation2018).

Then there is a set of hypotheses that relate to the supply side of the economy. The VoC literature, classifies southern European countries as ‘mixed market economies’, which uncoordinated wage bargaining systems that lead to higher wage inflation (pushed by the non-tradable sectors), which led to a loss in competitiveness prior to the Euro crisis (Johnston et al. Citation2014). This informs our cost competitiveness hypothesis, wherein (unit) labour costs are a key determinant of net exports and consequently economic growth. We note that this hypothesis has been criticized by the PK analyses of demand regimes, which demonstrates that while declining ULC may have positive effects on net exports, but will have negative effects on domestic demand, namely consumption, as it will (usually) correspond to a declining wage share (Stockhammer et al. Citation2009).

This wage cost argument presupposes a given technological structure. Mainstream economics regards technological change as the main determinant of economic growth in the long term. Earlier version of (mainstream) growth theory (e.g. the Solow growth model) took technological change as exogenous, but more recent versions conceive of it as determined in particular by R&D expenditures (Romer Citation1994). Within VoC, Soskice (Citation2022) in a more general discussion of the American system of innovation, and Burroni, Colombo and Regini (Citation2021) in relation to Southern Europe, have highlighted R&D investment as important driver of growth. Thus research-led technological progress hypothesis posits that growth is driven by R&D expenditures.

Finally we consider the structuralist hypothesis, which is based on recent reformulations of Latin American structuralist arguments. It posits that the sophistication (complexity) of manufacturing determines the export dynamics and thus economic growth. Originally this was proposed for developing economies, where Hausmann et al. (Citation2007) demonstrated that the export structure (empirically proxied by the economic complexity index; Hidalgo and Hausmann Citation2009) predicts subsequent economic growth. This index has been used also by CPE researchers, e.g. Kohler and Stockhammer (Citation2022) and Burroni, Colombo and Regini (Citation2021).

The purpose of all the growth drivers in our analysis ultimately is to explain growth. However, some do so more directly than others. Among these hypotheses the ones relating to house prices, fiscal policy and research-led technical progress directly relate to economic growth. The cost-competitiveness, the financial curse and the structuralist hypothesis relate directly to export growth and which is then supposed to explain economic growth. Thus while for most hypotheses we plot the growth drivers against GDP growth, for some those three hypotheses we report plots against export growth measures.

Methodologically this paper builds on Kohler and Stockhammer (Citation2022) by assessing growth drivers. Much of the GMA literature uses GDP growth decompositions to identify growth models. This compares the relative size (of growth) of the components of GDP (that is private consumption, public consumption, investment and net exports). Among these consumption and net export typically receive most attention as their dominance can be interpretated as related to consumption-led and export-led growth models. Hein et al. (Citation2021) and Hein and Martschin (Citation2021) combine this analysis with an analysis of sectoral balance sheet positions (e.g. requiring increases in household debt for the debt-led growth model). In contrast, growth drivers denote factors that are not themselves part of GDP accounting (such as house prices or measures of fiscal policy) but are hypothesized to cause changes in GDP. Kohler and Stockhammer (Citation2022) argue that the GDP growth decompositions have proven useful for the pre-crisis period, but may give a misleading picture for periods when growth drivers don’t match GDP components unambiguouslyFootnote3.

Our approach differs from Kohler and Stockhammer (Citation2022) in that, firstly, we broaden the set of potential growth drivers; secondly, we focus on southern European economies; and thirdly, we consider a longer period, which allows to move to a panel analytical setting. We organize our data into medium-term periods that have a useful interpretation (EMS era, Euro pre-GFC, GFC & Euro crisis, post-Euro crisis periods) and use data from these periods to derive medium-term effects of the growth drivers.

Housing boom–bust hypothesis

In the growth models literature household debt has often received more attention than house prices. Baccaro and Pontusson (Citation2016) refer to the ‘consumption-led’ growth model of the UK, but have in mind debt-fuelled consumption. They note in a footnote that household debt may be driven by house prices. Hein and Mundt (Citation2013) uses the term ‘debt-led consumption boom’.Footnote4 However, most of household debt is mortgage debt and a growing literature on financial cycles highlights the centrality of house prices therein. Stockhammer and Wildauer (Citation2016) use house prices as well as household debt as explanatory variables in explaining GDP growth. Stockhammer and Wildauer (Citation2018) provide evidence that house prices have been the main driver of household debt.

Since the GFC there has been growing interest in household debt and house prices in economics. The impact of house prices on consumption is analysed as a wealth effect, which the empirical literature reports to be smaller in Europe than in the USA (Slacalek Citation2009). The recent literature on financial cycles has established that house prices (and credit growth) are key parts of the financial cycles (Drehmann et al. Citation2012). Finally, a growing theoretical and empirical literature models endogenous boom bust cycles in house prices (Dieci and Westerhoff Citation2012, Ryoo Citation2016, Gusella and Stockhammer Citation2021). Our hypothesis thus focuses on the role of house prices.

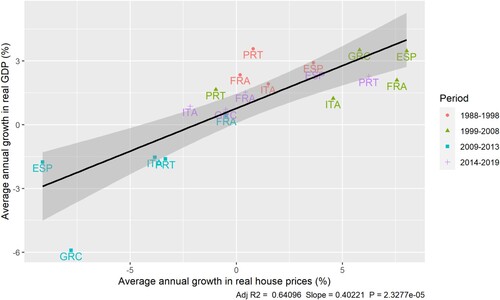

(a) plots (real) house price growth against (real) GDP growth.Footnote5 This shows that changes in real house prices are positively correlated to changes to GDP (statistically significant at the 1% level). Additionally, the crisis does not appear as a break in this sense, and the trend exists before and after the crisis. In short, the house price hypothesis seems to hold in Southern Europe.

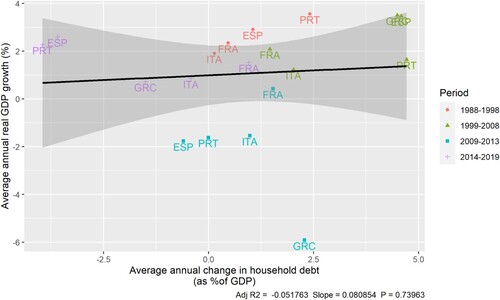

Figure 1. a: Relation between changes to house prices and GDP growth. Source: OECD. b: Relation between changes in household debt and GDP growth. Source: OECD and BIS. Note: household debt data for Greece start 1996.

In further exploration, we find a tight link between house prices and consumption as well as with investment (gross fixed capital formation), without any evidence of a break resulting from the GFC, indicating that the link between house prices and GDP and its components does not seem to have changed (see figures in supplementary material A.2.1). The elasticity of investment with respect to house prices is substantially larger than that for consumption, but since consumption represents a much larger share of GDP than investment (ca. 60% and 20% of GDP respectively), the different elasticities of consumption and investment with respect to house prices correspond to the about similar sizes of GDP growth contributions.

As parts of the GMA literature put household debt (rather than house prices) in the centre, (b) plots changes in household debt against real GDP growth. This shows a weak (and statistically insignificant) link between the two. This figure also suggests a change in the relationship between these two variables, as the post-GFC observations (in purple) show a negative relation between the two variables. Indeed, for the periods prior to 2014 the positive link is stronger (with a slope of .57; Supplementary material A.2.2). We find a similar result as regards the relation between house prices and household debt: while there was a link until 2014, the relation seems to have changed in the post-GFC period, presumably as household try to deleverage (and loan-to-value ratios are declining). In contrast house prices do maintain their impact on GDP. Thus we overall confirm the house price hypothesis.

The characterization of the pre-GFC as ‘debt-driven consumption boom’ (Hein and Mundt Citation2013) or ‘consumption-led growth’ (Baccaro and Pontusson Citation2016) is in our view misleading as it neglects the substantial impact of house prices on investment. The shift in Hein (Citation2019) and Hein and Martschin (Citation2021) to the term ‘debt-led private demand boom’ encompasses both consumption and investment and refers to household as well as corporate debt and is more appropriate, but does not put house prices at the centre. Our results suggests that ‘house price-driven growth’ is more insightful.

Financial curse hypothesis

The financial curse hypothesis posits that Southern European countries saw large inflows of capital in the pre-crisis expansion that have undermined the industrial base of these countries. Mamede (Citation2020) and Sebastian Dellepiane-Avellaneda, Hardiman and Las Heras (Citation2021) build on the literature on the resource curse or the Dutch disease to analyse the effects of the large capital inflows these countries received. They argue that the bank-based financial systems of Southern Europe transformed these inflows of capital into lending for non-tradable activities such as construction and the real estate sector. The resulting housing booms fostered pre-crisis demand growth, but shifted resources away from manufacturing and thus weakened export capabilities.

The mechanisms through which the housing boom harmed exports are not always fully specified: the transfer of resources from the tradable to the non-tradable sectors refers to capital (through the channelling of credit to the construction and real estate sectors), but also a diversion of labour in favour of these sectors (Sebastian Dellepiane-Avellaneda, Hardiman and Las Heras Citation2021, p. 11, Mamede Citation2020, p. 10). This argument explains a relative shift of resources, but requires additional assumptions to derive an absolute decline of manufacturing (only the latter gives a negative effect on exports). For absolute decline there need to be scarce resources, e.g. the loanable funds theory of finance, where the overall amount of credit is limited by saving and capital inflows or a situation of full employment.Footnote6 If there is unemployment, a credit boom with endogenous money could benefit manufacturing production.

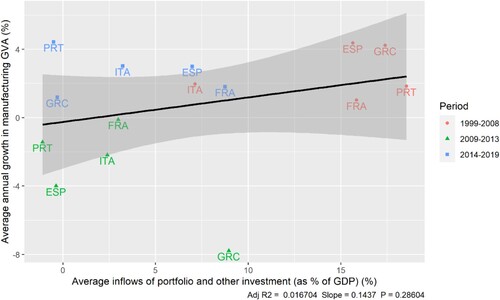

Empirically, the financial curse hypothesis posits that financial inflows lead to rising house prices, which ultimately harm Southern European countries’ export performance. Identifying the impact of (net) financial inflows on exports is difficult as net inflows must (ex post) equal net imports, but it is not clear whether inflows cause trade deficits (via fuelling a housing boom) or inflows merely finance trade deficits. Thus for investigating the financial curse hypothesis we first use gross capital inflows and second house prices (which according to the hypothesis are driven by inflows) to explain manufacturing value added and exports.

(a) plots gross financial inflows (defined as gross portfolio and other investmentFootnote7) against the manufacturing sectoŕs gross value added (GVA). The relation is positive, if not statistically significant, indicating that financial inflows have not been associated with a reduction in the absolute size of the manufacturing sector.

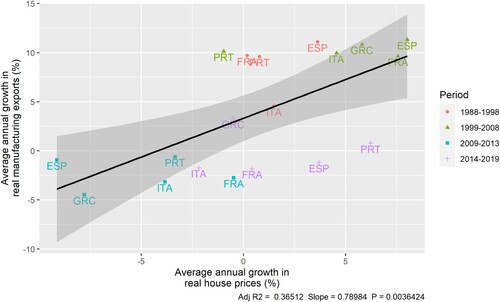

Figure 2. a: Relation between gross portfolio and other investment and the growth of manufacturing GVA. Source: OECD. Note: data on portfolio and other investment is available after 1993 for Spain, after 2002 for Greece, and after 1999 for the rest of countries. B: Relation between the growth of real house prices and real manufacturing exports. Source: OECD, AMECO and WTO. Note: HP data for Greece available from 1997.

(b) plots real house price growth against real manufacturing export growth. If the housing boom eroded Southern European countries’ export capabilities one would expect a negative relation. We find no evidence for that. The correlation between house prices growth and the growth of gross manufacturing exports is positive (statistically significant at the 1% level). This would suggest that that the house price boom (and associated growth) benefited manufacturing exports. We also test a variant where we use a country’s share of EU exports, which may control for global changes in exports dynamics (say, the rise of China). This gives a small negative correlation, but far from statistical significance (see supplementary material A.3.2). Overall, the financial curse hypothesis does not seem to hold for our sample.

Keynesian fiscal policy hypothesis

Fiscal policy has, until recently, only played a secondary role in CPE as a potential growth driver. The discussion of pre-GFC models hardly mentions fiscal policy. In analyses of post-GFC growth models perceptive discussions of different fiscal policies across European countries sit uneasily with a conceptual framework that is based on the consumption-led/export-led growth models distinction (e.g. Baccaro and Pontusson Citation2021). Post-Keynesian contributions to GMA feature fiscal policy more systematically (e.g. Hein and Martschin Citation2021, Morlin et al. Citation2022). Kohler and Stockhammer (Citation2022) make a forceful case that differences in fiscal policy have been a major determinant of growth for the post-crisis period.Footnote8 This slow inclusion of fiscal policy in CPE is in contrast to debates in macroeconomics and economic policy, where the impact of fiscal policy, or more technically the size of fiscal multipliers has been hotly contested. This is a major change as pre-GFC mainstream economics downplayed the role of fiscal policy. Much of the recent literature finds large fiscal multipliers, in particular during recessions.Footnote9 Most famously Blanchard and Leigh (Citation2014) report that IMF macroeconomic models had substantially underestimated fiscal multipliers and consequently understated the impact of austerity. Stockhammer et al. (Citation2019) provide evidence for European countries, showing that while they had responded to the GFC in a similar fashion in terms of fiscal policy, they diverge afterwards. During the Euro crisis northern countries had a relatively neutral fiscal policy, while southern European countries pursued aggressive austerity in the midst of a recession. The question is whether this argument carries over to the longer time period that we are considering and whether it can explain differences in performance across southern European countries.

Identifying the impact of fiscal policy is difficult because the observed budget deficit is an outcome of active policy decisions as well as the (passive) result of economic growth (lower growth leads to lower tax incomes and thus higher deficits). In the econometrician’s terminology there is an endogeneity problem. We use the cyclically adjusted government budget balance as measure of fiscal policy to avoid this problem. This measure, published by the World Bank as ‘structural deficit’, gives the budget balance if the economy were at normal capacity utilisation. It is expansionary when there is a deficit, and contractionary when there is a surplus. As we are interested in the impact of fiscal policy on GDP growth (i.e. changes in GDP rather than GDP levels), we focus on annual changes to the structural deficit (measured as % of GDP), the size of the impact can be interpreted as the fiscal multiplier. For ease of interpretation, we use the budget deficit rather than the budget surplus (the measures are identical, but have opposite signs).

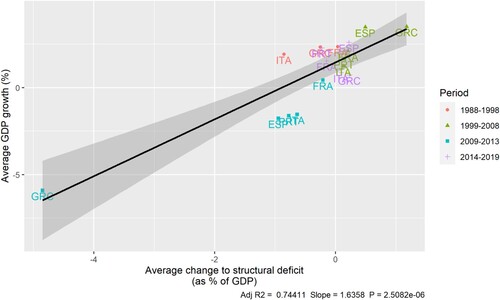

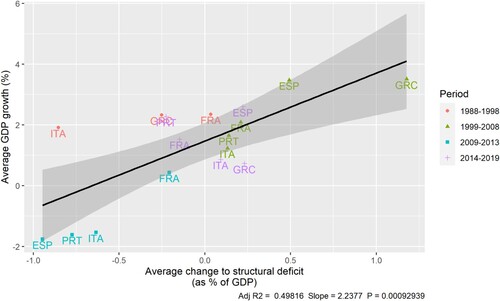

(a,b) show the scatter plot between structural (cyclically adjusted) budget deficit and growth. We find a slope of 1.64 (statistically significant at the 1% level). The plot suggests that Greece 2009–13 period may be an outlier. We thus repeat the estimation excluding that observation ((b)) and find that the relation still holds, and the slope even increases (2.26, statistically significant at the 1% level). Thus we confirm that fiscal policy is a potent growth driver and the Keynesian fiscal policy hypothesis holds.

Figure 3. a: Relation between changes to structural deficit and GDP growth (full sample). Source: OECD and World Bank. Note: Structural deficit data is available since 1988 for Greece, France and Italy, and since 1995 for Spain and Portugal. b: Relation between changes to structural deficit and GDP growth (without Greece crisis observation) Source: OECD and World Bank. Note: Structural deficit data is available since 1988 for Greece, France and Italy, and since 1995 for Spain and Portugal.

Cost-competitiveness hypothesis

For many analysts, the Eurozone crisis was symptomatic of deeper, productive imbalances within European economies, surfacing as persistent current account deficits in Southern Europe and surpluses in the European core. This coincided before the crisis with stronger increase of labour costs in southern Europe vis à vis the European core. The trade imbalances view of the Euro crisis had support by some mainstream economists (e.g. Sinn Citation2012) as well as by some heterodox economists (e.g. Lapavitsas et al. Citation2012, Cesaratto Citation2015). On the CPE side, Johnston et al. (Citation2014) get close to that position as they argue that uncoordinated wage bargaining systems in southern Europe gave rise to inflationary pressures emanating from sectors not exposed to international competition (i.e. sectors producing non-tradeable goods). All these arguments presuppose what we call the cost competitiveness hypothesis, which includes, first, that ULC are major determinants of exports (or more generally: current account positions), and second, that this also has a major impact on economic growth.

There have been various criticisms against the main thrust of this argument. Structuralists (Storm and Naastepad Citation2015a) have argued that it overstates cost competition. Other factors, in particular the sectoral structure and the technological content of exports may have a larger impact on export performance. Those favouring financial factors have argued that current account imbalances may be caused by capital inflows causing real estate booms (e.g. Pérez Citation2021). Post-Keynesians have objected to the second step of the hypothesis. They argue that while a decline in ULC may have positive export effects, it will have also have negative domestic demand effects as it usually entails a decline in the wage share, which has a negative impact of consumption (Stockhammer et al. Citation2009).

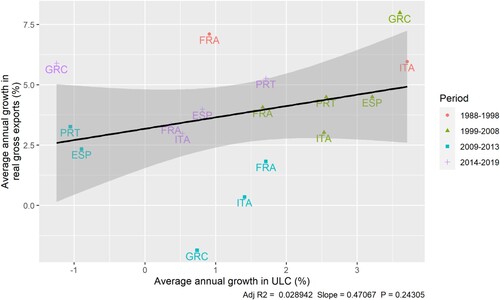

The graph 4(a) plots the growth of ULC against the growth rate of exports. There is a positive, statistically insignificant relation.

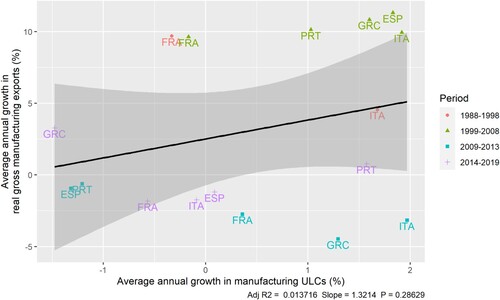

The standard measure of ULC refers to the entire economy, i.e. tradeables and non-tradeables. Thus (aggregate) ULCs may give a distorted picture as regards competitiveness if ULC in non-tradeable sectors rise faster than in tradeable sectors as is claimed by the VoC argument about uncoordinated wage bargaining. We thus also test the hypothesis focusing on manufacturing ULCs and exports ((b)). The relationship is also positive and below the usual limits for statistical significance. Overall thus we fail to find evidence for the cost competitiveness hypothesis.

Figure 4. a: Relation growth in ULCs and growth in real gross exports. Source: OECD. Note: France and Italy have ULC data for all periods, Greece, Portugal and Spain have no ULC data for the rpe-1999 period. b: Relation growth in ULCs and growth in real gross exports. Source: OECD. Note: France and Italy have ULC data for all periods, Greece, Portugal and Spain have no ULC data for the pre-1999 period.

Research-led technological change hypothesis

According to mainstream economics (e.g. the Solow growth model) technological change is the main determinant of growth in the long run. While in the original Solow model technological change was assumed to be exogenous more recent models treat it as endogenous and identify R&D expenditures as a major determinant (Romer Citation1994). National systems of innovation approach (e.g. Freeman Citation1995) takes a societal approach to innovation and highlights the linkages between different actors. The VoC approach draws on both. Soskice (Citation2022) puts innovation at the centre of his recent reformulation of VoC, and Burroni, Colombo and Regini (Citation2021) feature innovation capabilities prominently in the context of southern European economies. They offer a broader institutional analysis of national innovation systems and use R&D expenditures as the main empirical summary variable. Burroni et al also refer to the ECI, which we discuss in section 7. In GMA, which focusses on the demand side, R&D has not featured.

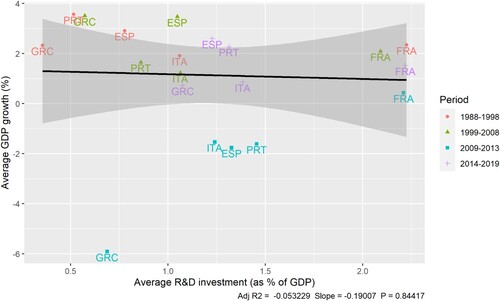

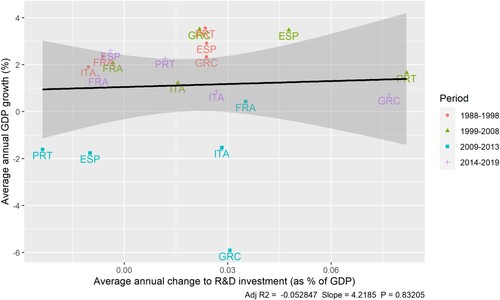

We use R&D expenditures as the main variable for the research-led technological progress hypothesis. This does not do full justice to the national systems of innovation approach, but it is fair to say that in the VoC adaptions as well as in the innovation literature R&D expenditures have taken a centre stage as an empirical indicator (e.g. Soete et al. Citation2022). The main alternative would be the number of patents, but they are considered less reliable in many cases (e.g. Kleinknecht and Reinders Citation2012). (a) reports the scatter plot for R&D expenditures (as percent of GDP) and GDP growth. We fail to find evidence of a link between R&D and GDP growth for our sample. The coefficient is negative and statistically insignificant. One could argue that it is the change in R&D expenditures (rather than its level) that are key for growth. Thus (b), a robustness check, reports the plot with the difference in R&D, with the same result: we fail to find a (positive) link. Short, the innovation induced-technological change hypothesis does not hold in our sample. R&D expenditures do not explain growth performance in southern Europe.

Figure 5 .#a: Relation between R&D investment and GDP growth. Source: OECD. NOTE: Prior to 2003 Greece only has data every 2 years. b: Relation between changes to R&D investment and GDP growth. Source: OECD. Note: Prior to 2003 Greece only has data every 2 years.

Structuralist hypothesis

Some authors (Simonazzi et al. Citation2013, Storm and Naastepad Citation2016; Grabner et al. Citation2020) argue that wage costs is only a secondary determinant of export performance. Applying a structuralist analysis to the Eurozone, they suggest that differences in the sectoral structure and (closely related) the technological content of their exports are a key cause of export growth and thus the macro-economic trajectories. Demand for low-tech exports is less income elastic that than of high-tech ones, thus the growth prospects in these sectors are weaker. Different from the research-induced technical progress hypothesis, the structuralist argument highlights the sectoral composition of exports. More specifically, more sophisticated exports have lower price-elasticities and are thus better placed to sustain export-led growth strategies. This argument has received some attention in GMA (Baccaro Citation2021, Kohler and Stockhammer Citation2022), but it has not been at its core.

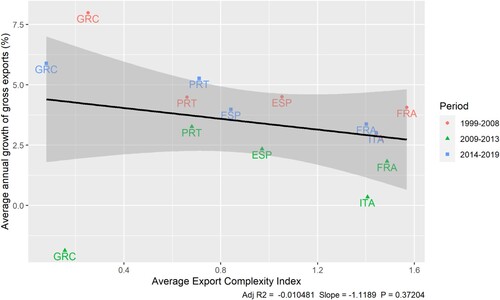

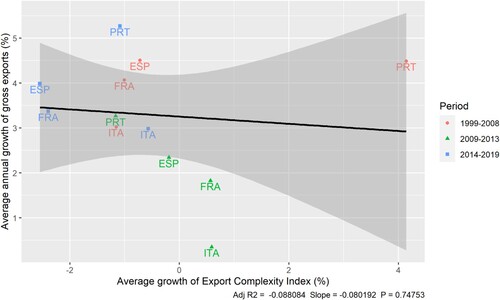

In this argument technological development is often operationalised through the Exports Complexity Index (ECI). This is a sectoral variable that measures how diversified the inputs and export destinations of export goods are (Hidalgo and Hausmann Citation2009), which has been found to explain growth in developing economies (Hausmann et al. Citation2007). What we call the structuralist hypothesis states that countries with a higher ECI should have stronger export growth. (a), plots the ECI against the growth of net exports. We find a negative relation, which is not statistically significant. It can be argued that it is the change in ECI rather than its levels that impacts exports. Thus (b) plots the growth in ECI against growth of real gross exports (without Greece).Footnote10 This reports no statistically significant relationship between the growth of ECI and the growth of real exports. Another way to operationalise the structuralist argument, based on the Thirlwall model, is to estimate export and import equations, identifying the relevant export and import elasticities and calculating the equilibrium growth rates implied by them (Thirlwall Citation1979, Citation2019). This is beyond the scope of this paper (and sensitive to the precise specification of those equations). Existing studies for European countries (Bagnai Citation2010, Table 5) suggest relatively high equilibrium growth rates for southern Europe in this model. Overall, we fail to find support the structuralist hypothesis – while it may be useful for understanding differences in trade between north and southern Europe, it does not seem to be able to explain export performance within southern Europe.

Figure 6. a: Relation between ECI and the growth of real gross exports. Source: OECD and Atlas of Economic Complexity. Note: ECI data is only available since 1995. b: Relation between growth of ECI and the growth of real exports (without Greece). Source: OECD and Atlas of Economic Complexity. Note: ECI data is only available since 1995.

A synthetic regression estimation

The two-variable scatter plots presented so far have the advantage that they are intuitive and offer a quick check for the plausibility of an alleged effect. However, they analyse effects in isolation. This section thus reports regression results that incorporate all the main variables discussed simultaneously. We estimate the following equation:

where subscripts j and t refer to country and time period. Based on the hypotheses discussed we expect the following signs: house price hypothesis

,Keynesian fiscal policy hypothesis

, wage cost competitiveness hypothesis

, research-induced technological progress hypothesis

and Structuralist hypothesis

.

Our regression of real GDP growth is a panel model using period averages (1988–98, 1999–2008, 2009–13, 2014–19) for the five southern European economies. The observations have a long differences format (similar to regressions using five-year averages or differences) and results can be interpreted as medium-term effects.

The results of this regression (as well as those of the scatterplots) have to be interpreted with caution. First, the regressions are low on degrees for freedom. Second, there are potential issues of inverse causation. Given the time span of the observations, one would expect causation in both directions for many variables. The extent of the problem differs by variable. The most vulnerable variable with respect to this is probably ULC. Arguably, higher GDP growth can lead to inflationary pressures which can translate into wage and ULC growth. There may also be an impact of GDP growth on house prices. While this impact ought to be modest over longer periods, in our sample it may exist. The structural deficit is by construction independent of GDP growth; ECI is not an obvious candidate for inverse causation. R&D may respond to the increased growth if growth comes with bottlenecks in production that motivate additional research. The estimated regression coefficients thus may be a combination of effects in both directions thus coefficients may overstate causal effects of the explanatory variable. However, even if there are inverse causation issues the analysis still contains useful information: given that we cannot exclude inverse causation, a positive (and statistically significant) relation is a necessary, but not sufficient condition for the causal mechanism to operate. Inversely, if a variable does not show substantial effects, that variable can be discarded as potential growth driver.

reports the estimation results. Specification 1 is our baseline specification with all factors considered. Among the explanatory variables HP and the structural deficit are statistically significant at the 1% level. The respective coefficients are .17 and 1.18, respectively. None of the other variables is statistically significant at conventional levels. The coefficient on house prices corresponds to the wealth effect on consumption plus the impact on investment. The point estimate of .17 is somewhat larger than most wealth effect estimates. The coefficient on the structural deficit can be interpreted as a fiscal multiplier and is in line with recent estimate that put the multiplier above 1 (and this coefficient should be free of inverse causation issues). The coefficient estimates of ULC and ECI have perverse signs (positive and negative respectively) and are not statistically significant, and neither is the coefficient sign for R&D. Specification 2 includes ECI and R&D in differences rather than levels as it could be argued that it is the change rather than the level of these variable that impact exports and thus growth. The results are very similar: R&D and ECI remain statistically insignificant, while house prices and the structural deficit remain statistically significant. Specification 3 includes country fixed effects (though the relevant F test fails to reject that these are jointly zero).Footnote11 Again, results are similar. Specification 4 includes time fixed effects. This specification controls for common time specific shocks, which include changes in the world economy. The results are qualitatively similar to the baseline specification, but coefficients for house prices and deficits are lower (.08 and 1.1, respectively). In specification 4 ULC become statistically significant (at the 10% level) with a positive sign, which is at odds with the relevant hypothesis (possible explanations include that this positive sign reflects a wage-led demand regime or that this in due to inverse causality with GDP growth causing inflationary pressures that also impact ULC growth).

Table 2. Panel regression model of GDP growth.

While many of our variables show no impact on GDP growth, our model has substantial explanatory power. To illustrate the size of the effects implied in our regression (and taking the coefficient estimates at face value), plots actual growth and the growth explained by house prices and the structural deficit, which is calculated by multiplying the actual house price and structural deficit data with the coefficients from specification 1. The figure also shows the percentage of GDP growth explained by changes in house prices and structural deficit. These two variables explain almost half of actual GDP growth between 1999 and 2019 for Southern Europe as a whole (see supplementary material A.5).Footnote12 Its explanatory power is greatest for the crisis and pre-crisis period and weaker for the post-crisis period (with 55%, 76% and 12%, respectively, explained on average across southern Europe). The fit is better for Spain and Greece than for Italy and Portugal and the explanatory power for France is weak. Thus, the model, unsurprisingly, works best for those cases with large changes in house prices or fiscal policy. However, the explanatory power for Italy and Portugal is still substantial (just below 50%).

Figure 7. Comparison of actual GDP growth and the contribution of changes in house prices and the structural deficit, Note: the contribution of house prices and structural deficit has been calculated by multiplying the actual changes in these variables by the respective coefficients of specification 1 in .

Does our research design, in particular the choice of time periods and country sample bias our results in favour of some explanatory factors? First, the fact that we organise our periods around distinct boom and bust periods does favour variables that have a cyclical pattern, such as house prices, as opposed to those which only impact long-run growth. Whether this constitutes a bias depends on what one thinks that CPE has to explain: should it explain long run growth or actual movements in growth, including cyclical dynamics. In our view CPE has to be able to analytically account for the events like the GFC or Euro crisis. Second, the fact that our sample only includes southern European countries has the advantage that there is institutional similarity across countries (and thus the pooling assumption is more likely to hold), but may understate the impact of those variables that explain differences across groups of countries. This is particularly relevant for the structuralist hypothesis, which specifically explains difference between core and peripheral countries. In fact, in a more heterogenous sample, including countries from both core and periphery of Europe, Kohler and Stockhammer (Citation2022) find that non-price competitiveness is an important growth driver (in addition to house prices and fiscal policy). Jungmann (Citation2021) for a sample of emerging economies also reports (for the post-GFC period) effects of non-price competitiveness.

By putting house price dynamics and fiscal policy at the centre stage, our research confirms the importance of demand side considerations for GMA (see also Kohler and Stockhammer (Citation2022)), but it also shifts the focus of the analysis. While debt features prominently, house price dynamics and house price cycles have not systematically been built into GMA and the housing CPE literature (e.g. Johnston and Kurzer Citation2020) is focussed on social and political implications rather than the growth impact of housing. Our findings illustrate the importance of fully incorporating housing and house price dynamics into growth models analysis.

The importance of fiscal policy as a growth driver in southern Europe not only represents a different finding to most GMA analyses and it suggests a need for GMA to reconsider its methodological approach to analysing the state’s contribution to economic growth. Much of GMA (Baccaro and Pontusson Citation2021, Hein et al. Citation2021, Mertens et al. Citation2022) uses a decomposition of GDP growth in the contribution of its demand components (government consumption, private consumption, investment and net exports) to identify export-led and debt-led demand regimes.Footnote13 This approach, in our view, misidentifies the role of the state, in particular fiscal policy. The item ‘government consumption’ essentially corresponds to wages of government employees and is a relative stable variable that does not mirror the growth impact of changes in fiscal policy over the business cycle, which is typically debt-finance and quite independent of government employment. Much of the impact of expansionary fiscal policy will show up as increases (or reduction in decreases) in private consumption, and thus a growth driver analysis (where fiscal policy is an independent variable) is required. By combining the GDP decompositions with a sectoral financial balance analysis, Hein (Citation2019) and Hein and Martschin (Citation2021) go a step in the direction suggested here, but are unable to identify the growth impact of fiscal policy.

Conclusion

Our empirical analysis has confirmed the validity of the housing cycle and fiscal policy hypothesis, while we failed to find evidence for the financial curse hypothesis, the cost-competitiveness, the research-induced technological change hypothesis and the structuralist hypothesis. This holds for the simple scatter plots as well as in a panel regression model that jointly tests all relevant variables. Our findings have important implications for understanding the variety of experiences within Mediterranean Capitalism, qualifying some of the conclusions in the extant literature. We only partially confirm Burroni et al.’s (Citation2021a) claims. We confirm the secondary role of cost-competitiveness and the importance of financial factors, but find no evidence for the centrality of research driven technological progress. The fact that none of the growth drivers related to exports (e.g. ULCs, ECI) have a statistically significant relation with GDP growth supports Baccaro’s analysis of Southern Europe as following a peripheral form of consumption-led growth rather than having transitioned to an export-led growth model. Yet our analysis suggests house prices rather than household debt as the key financial variable, as rising house prices can contribute to consumption and investment and do not always require changes in household debt. Most importantly, we add fiscal policy as a key growth driver in Southern Europe, which does not feature prominently in most VoC and GMA analysis of the region (with Pérez and Matsaganis Citation2018 and Kohler and Stockhammer Citation2022 as exceptions). What explains different growth experiences within the southern European countries? According to our findings differences in house prices and fiscal policy go a long way of explaining these.

This begs the question: what explains the difference in fiscal policy and house prices, our two main growth drivers, across countries (given their seemingly similar institutional structures) and time? The focus of this paper has been on identifying the growth drivers and their impact rather than their origin, so all we can offer here is some suggestions for future research. The institutions that feature prominently in CPE are not geared to explaining house price dynamics and fiscal policy. Fiscal policy is directly the outcome of the (domestic) political process and of the international constraints that a country faces. Fiscal policy thus will be tied to political coalitions; as regards the international constraints the size of the country and consequently the size of its sovereign debt market does influence the bargaining position of a country within Europe (a version of ‘too big to fail’; admittedly this is better in explaining the difference between Spain and Greece than that between Spain and Italy). As regards house price and debt dynamics, Baccaro and Bulfone (Citation2022) highlight the importance of political coalitions, in particular the central role of the construction and financial sectors in Spain. That is a plausible hypothesis, but the evidence marshalled so far is sketchy. Fuller (Citation2015) develops institutional measures of credit permissiveness. The resulting index is a crude measure, but the approach is promising as it focuses on institutions that influence the house price-credit link. Finally, as has been highlighted for Spain (Fernández and García Citation2017) the relation of a country’s financial sector to international finance may be important to understand the extent to which international financial players enter real estate activities in a country and thus act as a trigger or amplifier for housing bubbles. However, there is no systematic analysis of cross-country differences yet (Pérez Citation2021).

What are the implications for the growth models approach? This paper took the notion of a Mediterranean Capitalism characterized by a similar set of institutions (compared to other country groups) as starting point. Given the diversity of growth performances, this raises the question whether a variety of capitalism necessarily corresponds to a unique growth model. A growth model occurs when within a given institutional structure a limited set of growth drivers exercise a consistent influence such as to shape the growth process. The experience of the southern European countries has been shaped by fiscal policy and house prices as those two variables explain a large part of actual growth. This is not in contradiction to a peripheral consumption-led growth model, but does shed a different light on the relevant growth drivers.

What are the implications for future research in CPE? Our findings reinforce existing trends in the literature, which has begun to move away from its focus on cost competitiveness. Our results reinforce the importance of demand side considerations. This is not to downplay supply side considerations as such. These may determine potential growth, but actual growth is more driven by the demand side. However, the recent leaning towards innovation and in particular on R&D in CPE seems misplaced. For explaining the main changes in growth across countries and time in our sample the supply side clearly does not play the centre stage. The strength of GMA is in its fusion of institutional and macroeconomic analysis. Our analysis pushes this further. First, GMA has been developed during the boom preceding the GFC. For that period the export-driven/debt-driven distinction was useful for understanding country performances. But GMA needs to broaden its analysis its potential growth drivers, which may or may not form coherent growth models. Second, if one accepts the importance of aggregate demand it is hard to avoid the conclusion that GMA may be looking at the ‘wrong’ institutions. Our findings suggest that house price dynamics and fiscal policy are key to understanding economic performance in southern Europe, current institutional analysis is not geared towards that. CPE needs an institutional analysis of spending and lending.

Acknowledgements

This paper is a part of the Leverhulme grant ‘The Political Economy of growth models in an age of stagnation’ (Leverhulme RPG-2021-045). The paper has benefited from comments by Ben Tippet, Guen Anzolin, Ian Lovering and two anonymous referees. The usual disclaimers apply.

Supplemental Material

Download MS Word (857.1 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Correction Statement

This article was originally published with errors, which have now been corrected in the online version. Please see Correction (http://dx.doi.org/10.1080/13563467.2023.2213562)

Additional information

Funding

Notes

1 The inclusion of France is somewhat arbitrary as France is an intermediate case. While France shares some of the characteristics with other southern European countries, namely fragmented labour organisation and strong state interventions, it has a higher income level, a more developed financial sector and in the Euro crisis was only partially affected by the sovereign debt crisis.

2 It is not straightforward whether finance is considered a demand or supply factor. We define demand side factors that directly impact spending decisions. In that sense, say the availability of credit and the uncertainty caused by a financial crisis are on the demand side. Our hypotheses regarding finance refer in particular to financial cycles, which are on the demand side. Supply side factors are those that impact relative prices and technology.

3 GDP growth de-composition and financial balance disaggregation are based on national income and financial accounting, thus are ‘true’ by definition, but they can be misleading when used with causal interpretation. For example, after the GFC, many southern European countries experienced strong improvements in their current accounts, which in GMA framework is easily interpreted as shift towards an export-led growth model (as in Hein et al. 2021). Kohler and Stockhammer (Citation2022) argue that this is misleading: first, the improvement of net export has been driven by a sharp decline in imports rather than by a growth in exports. Second the decline in imports is (as Hein et al. 2021 agree) driven to a large extent by the sharp recession caused by the housing bust and consequent deleveraging and by austerity policies during the Euro crisis. Thus rather than a genuine export-led growth process, this experience is better characterised as a finance-led and state-led growth process in reverse.

4 In the later work Hein (Citation2019), Hein and Martschin (Citation2021), and Hein et al. (2021) this has been replaced by ‘debt-led private demand boom’ regime in order to take into account the effect of residential investment booms.

5 Full variable definitions and sources can be found in supplementary material A.0.

6 In so far as the financial curse hypothesis rests on a version of the loanable funds theory of financial markets, it is inconsistent with post-Keynesian macroeconomic theory.

7 In the Appendix (see supplementary material) we test this hypothesis by focusing only on portfolio investing, without any substantial changes to our results.

8 There are important differences in how these papers identify the impact of fiscal policy. Kohler and Stockhammer (Citation2022), like this paper, uses cyclically adjusted fiscal deficits as the variable for fiscal policy and then estimate its effects on GDP growth (in a cross country regression). This is close to a Keynesian short-run multiplier. Morlin et al. (Citation2022) use a supermultiplier framework, i.e. they treat all government expenditures as autonomous, their multiplier is long-run one that combines induced consumption as well as induced investment effects and it is calculated from a decomposition of GDP growth into different autonomous demand components. Unlike standard Keynes multipliers where deficit-finance spending is associated with a different multiplier than tax-financed expenditures, they treat all government expenditures the same. Martschin and Hein (2022) give a prominent role to fiscal policy (along side monetary policy and wage policy) in their qualitative analysis and use four measures for fiscal policy, but do not quantitatively identify the growth impact of fiscal policy (or of any of the other policy areas). Hein et al. (2021) do use GDP growth decompositions where the state sector is represented by government spending and conclude that most southern European countries have shifted post-crisis to a form of export-led growth. In further interpretation of the results, they stress the importance of austerity policies, but without offering a measure of the growth impact of austerity.

9 E.g. Auerbach and Gorodnichenko (Citation2012), De Long and Summers (Citation2012), Eggertsson and Krugman (Citation2012), Gechert et al. (Citation2019), Stockhammer et al. (Citation2019). Some of the literature refers to periods where the interest rate is at (or close to) the zero lower bound and thus monetary policy becomes ineffective. In practice this will coincide with our use of recessions (if anything southern European countries would have higher multipliers if we used ZLB).

10 The plot with Greek data (supplementary material A.4) shows a positive relationship between the two variables, but Greecés observations are clearly outliers.

11 In the baseline specification our dependent variable is in differences (real GDP growth), thus it corresponds to a country fixed effects model in (logarithmic) levels of GDP.

12 This and the following does not rely on the R2 (which is above .9 in all specifications), but compares actual growth rates across countries and across time (for our periods) with growth explained by house prices and fiscal policy.

13 We perform a GDP growth decomposition exercise in Table A.1 (in the supplementary material).

References

- Afonso, A., et al., 2021. Labor market (de)regulation and wage-setting institutions in Mediterranean capitalism. In: L. Burroni, E. Pavolini, and M Regini, eds. Mediterranean capitalism revisited: one model, different trajectories. London: Cornell University Press, 115–148.

- Aikman, D., Haldane, A.G., and Nelson, B.D., 2015. Curbing the credit cycle. The Economic Journal, 125, 1072–1109.

- Allain, O., 2015. Tackling the instability of growth: a Kaleckian-Harrodian model with an autonomous expenditure component. Cambridge Journal of Economics, 39 (5), 1351–1371.

- Amable, B., 2003. The diversity of modern capitalism. Oxford: Oxford University Press.

- Arestis, P., and Sawyer, M., 2003. Reinventing fiscal policy. Journal of Post Keynesian Economics, 26 (1), 3–25.

- Auerbach, A., and Gorodnichenko, Y., 2012. Measuring the output responses to fiscal policy. American Economic Journal – Economic Policy, 4, 1–27.

- Baccaro, L., 2021. Is there a “Mediterranean” growth model? In: L. Burroni, E. Pavolini, and M Regini, eds. Mediterranean capitalism revisited: one model, different trajectories. London: Cornell University Press, 19–41.

- Baccaro, L., and Bulfone, F., 2022. Growth and stagnation in Southern Europe. The Italian and Spanish growth models compared. In: L. Baccaro, M. Blyth, and J. Pontusson, eds. Diminishing returns: The new politics of growth and stagnation. Oxford: Oxford University Press, 293–322.

- Baccaro, L., and Pontusson, J., 2016. Rethinking comparative political economy: the growth model perspective. Politics and Society, 44 (2), 175–207.

- Baccaro, L., and Pontusson, J., 2021. European growth models before and after the great recession. In: Anke Hassel, and Bruno Palier, eds. Growth and welfare in advanced capitalist economies: How have growth regimes evolved? Oxford: Oxford University Press, 98–134.

- Bagnai, Alberto, 2010. Structural changes, cointegration and the empirics of Thirlwall's law. Applied Economics, 42 (10), 1315–1329.

- Batini, N., et al. 2014. Fiscal multipliers: size, determinants, and use in macroeconomic projections. Technical Notes and Manuals. IMF Fiscal Affairs Department https://www.imf.org/external/pubs/ft/tnm/2014/tnm1404.pdf.

- Blanchard, O.J., and Leigh, D., 2014. Learning about fiscal multipliers from growth forecast errors. IMF Economic Review, 62 (2), 179–212. doi:10.1057/imfer.2014.17.

- Burroni, L., Colombo, S., and Regini, M., 2021. Human capital formation, research and development and innovation. In: L. Burroni, E. Pavolini, and M Regini, eds. Mediterranean capitalism revisited: one model, different trajectories. London: Cornell University Press, 192–210.

- Burroni, L., Pavolini, E., and Regini, M., 2021a. Conclusion. Mediterranean capitalism between change and continuity. In: L Burroni, E Pavolini, and M Regini, eds. Mediterranean capitalism revisited. One model, different trajectories. Ithaca: Cornell University Press, 211–34.

- Burroni, L., Pavolini, E., and Regini, M., 2021b. Mediterranean capitalism revisited: one model, different trajectories. London: Cornell University Press.

- Capano, G., and Lippi, A., 2021. States’ performance, reforms and policy capacity in Southern Europe. In: L. Burroni, E. Pavolini, and M Regini, eds. Mediterranean capitalism revisited: one model, different trajectories. London: Cornell University Press, 42–66.

- Cesaratto, S., 2015. Balance of payments or monetary sovereignty? In search of the EMU’s original sin. International Journal of Political Economy, 44 (2), 142–156.

- De Long, J.B., and Summers, L.H., 2012. Fiscal policy in a depressed economy. Brookings Papers on Economic Activity, 2012 (1), 233–297. doi:10.1353/eca.2012.0000.

- Dieci, Roberto, and Westerhoff, Frank, 2012. A simple model of a speculative housing market. Journal of Evolutionary Economics, 22 (2), 303–29.

- Drehmann, M., Borio, C., and Tsatsaronis, K. 2012. Characterising the financial cycle: don't lose sight of the medium term!, BIS Working Paper 380.

- Eggertsson, G., and Krugman, P., 2012. Debt, deleveraging, and the liquidity trap: a Fisher-Minsky-Koo approach. Quarterly Journal of Economics, 127 (3), 1469–1513.

- Fernández, R., and García, C., 2017. Wheels within wheels within wheels: the importance of capital inflows in the origin of the Spanish financial crisis. Cambridge Journal of Economics, 42 (2), 331–53.

- Freeman, Chris, 1995. The ‘national system of innovation’ in historical perspective. Cambridge Journal of Economics, 19, 5–24.

- Fuller, G., 2015. Who’s borrowing? Credit encouragement vs. credit mitigation in national financial systems. Politics and Society, 43 (2), 241–68.

- Gambarotto, F., Rangone, M., and Solari, S., 2019. Financialisation and deindustrialisation in the Southern European Periphery. Athens Journal of Mediterranean Studies, 5 (3), 151–172.

- Gechert, S., Horn, G., and Paetz, C., 2019. Long-term effects of fiscal stimulus and austerity in Europe. Oxford Bulletin of Economics and Statistics, 81 (3), 647–666. doi:10.1111/obes.12287.

- Gräbner, C., et al., 2020. Is the Eurozone disintegrating? Macroeconomic divergence, structural polarisation, trade and fragility. Cambridge Journal of Economics, 44 (3), 647–669. doi:10.1093/cje/bez059.

- Guillén, A.M., et al., 2021. Southern European welfare systems in transition. In: L. Burroni, E. Pavolini, and M Regini, eds. Mediterranean capitalism revisited: one model, different trajectories. London: Cornell University Press, 149–171.

- Gusella, F., and Stockhammer, E., 2021. Testing fundamentalist-momentum trader financial cycles. An empirical analysis via the Kalman filter. Metroeconomica, 72 (4), 758–797.

- Hausmann, R., Hwang, J., and Rodrik, D., 2007. What you export matters. Journal of Economic Growth, 12 (1), 1–25. doi:10.1007/s10887-006-9009-4.

- Hein, E., 2018. Autonomous government expenditure growth, deficits, debt, and distribution in a neo-Kaleckian growth model. Journal of Post Keynesian Economics, 41 (2), 316–338.

- Hein, E., 2019. Financialisation and tendencies towards stagnation: the role of macroeconomic regime changes in the course of and after the financial and economic crisis 2007-09. Cambridge Journal of Economics, 43, 975–999.

- Hein, E., and Martschin, J., 2021. Demand and growth regimes in finance-dominated capitalism and the role of the macroeconomic policy regime: a post-Keynesian comparative study of France, Germany, Italy and Spain before and after the Great Financial Crisis and the Great Recession. Review of Evolutionary Political Economy, 2, 493–527.

- Hein, E., and Mundt, M., 2013. “Financialization, the financial and economic crisis, and the requirements and potentials for wage-led recovery”. In: M. Lavoie, and E Stockhammer, eds. Wage-led growth. London: Palgrave Macmillan, 153–186.

- Hein, E., Meloni, W.P., and Tridico, P., 2021. Welfare models and demand-led growth regimes before and after the financial and economic crisis. Review of International Political Economy, 28 (5), 1196–1223. doi:10.1080/09692290.2020.1744178.

- Hidalgo, C.A., and Hausmann, R., 2009. The building blocks of economic complexity. Proceedings of the National Academy of Sciences, 106 (26), 10570–10575. doi:10.1073/pnas.0900943106.

- Johnston, A., and Kurzer, P., 2020. Bricks in the wall: the politics of housing in Europe. West European Politics, 43 (2), 275–296.

- Johnston, A., Hancké, B., and Pant, S., 2014. Comparative institutional advantage in the European sovereign debt crisis. Comparative Political Studies, 47 (13), 1771–1800. doi:10.1177/0010414013516917.

- Jungmann, B. 2021. “Growth drivers in emerging capitalist economies before and after the Global Financial Crisis”, Working Paper, No. 172/2021, Hochschule für Wirtschaft und Recht Berlin, Institute for International Political Economy (IPE), Berlin.

- Kleinknecht, A., and Reinders, H., 2012. How good are patents as innovation indicators? evidence from German CIS data. In: M. Andersson, et al., eds. Innovation and growth: from R&D strategies of innovating firms to economy-wide technological change. Oxford: Oxford University Press, 115–27.

- Kohler, K., and Stockhammer, E., 2022. Growing differently? Financial cycles, austerity and competitiveness since the Global Financial Crisis. Review of International Political Economy, 29 (4), 1314–41. doi:10.1080/09692290.2021.1899035.

- Lapavitsas, C., et al., 2012. Crisis in the eurozone. London: Verso.

- Mamede, R.P., 2020. “Financialisation and structural change in Portugal: a euro-resource-curse?”. In: A.C. Santos, and N. Teles, eds. Financialisation in the European periphery: work and social reproduction in Portugal. London: Routledge, 64–82. chapter 4. Mamede.

- Mertens, D., et al. 2022. Moving the center: Adapting the toolbox of growth model research to emerging capitalist economies (IPE Working Papers 188/2022). Berlin School of Economics and Law, Institute for International Political Economy (IPE).

- Molina, O., and Rhodes, M., 2007. The political economy of adjustment in mixed market economies: a study of Spain and Italy. In: B. Hancké, M. Rhodes, and M. Thatcher, eds. Beyond varieties of capitalism: conflict, contradictions and complementarities in the European economy. Oxford: OUP, 223–252.

- Morlin, G., Passos, N., and Pariboni, R., 2022. Growth theory and the growth model perspective: insights from the supermultiplier. Review of Political Economy. doi:10.1080/09538259.2022.2092998.

- Pérez, S., and Matsaganis, M., 2018. The political economy of austerity in southern Europe. New Political Economy, 23 (2), 192–207.

- Pérez, S.A., 2021. Which level of analysis? Internal versus external explanations of Eurozone divergence. In: L. Burroni, E. Pavolini, and M Regini, eds. Mediterranean capitalism revisited: one model, different trajectories. London: Cornell University Press, 67–90.

- Prante, F., Hein, E., and Bramucci, A., 2022. Varieties and interdependencies of demand and growth regimes in finance-dominated capitalism: a Post-Keynesian two-country stock–flow consistent simulation approach. Review of Keynesian Economics, 10 (2), 264–290.

- Rodrigues, J., and Reis, J., 2012. The asymmetries of European integration and the crisis of capitalism in Portugal. Competition and Change, 16 (3), 188–205.

- Romer, Paul, 1994. The origins of endogenous growth. Journal of Economic Perspectives, 8 (1), 3–22.

- Ryoo, S., 2016. Household debt and housing bubbles: A Minskian approach to boom-bust cycles. Journal of Evolutionary Economics, 26, 971–1006.

- Sebastian Dellepiane-Avellaneda, Hardiman, N., and Las Heras, J., 2021. Financial resource curse in the Eurozone periphery. Review of International Political Economy, doi:10.1080/09692290.2021.1899960. Dellapiane-Avellaneda et al. (2021) for Spain.

- Simonazzi, A., Ginzburg, A., and Nocella, G., 2013. Economic relations between Germany and southern Europe. Cambridge Journal of Economics, 37 (3), 653–675.

- Sinn, H.-W., 2012. The European balance of payments crisis. CESifo Forum, 13 (Special Issue), 2–10.

- Slacalek, Jiri, 2009. What drives personal consumption? The role of housing and financial wealth. The B.E. Journal of Macroeconomics, 9, 1. doi:10.2202/1935-1690.1555.

- Soete, L., Verspagen, B., and Ziesemer, T., 2022. Economic impact of public R&D: an international perspective. Industrial and Corporate Change, 2022 (31), 1–18.

- Soskice, D., 2022. Rethinking varieties of capitalism and growth theory in the ICT era. Review of Keynesian Economics, 10 (2), 222–241.

- Stockhammer, E., 2015. Rising inequality as a root cause of the present crisis. Cambridge Journal of Economics, 39 (3), 935–58.

- Stockhammer, E., and Wildauer, R., 2016. Debt-driven growth? Wealth, distribution and demand in OECD countries. Cambridge Journal of Economics, 40 (6), 1609–1634. doi:10.1093/cje/bev070.

- Stockhammer, E., and Wildauer, R., 2018. Expenditure cascades, low interest rates or property booms? Determinants of household debt in OECD countries. Review of Behavioral Economics, 5 (2), 85–121. doi:10.1561/105.00000083.

- Stockhammer, E., Onaran, Ö, and Ederer, S., 2009. Functional income distribution and aggregate demand in the Euro area. Cambridge Journal of Economics, 33 (1), 139–159.

- Stockhammer, E., Qazizada, W., and Gechert, S., 2019. Demand effects of fiscal policy since 2008. Review of Keynesian Economics, 7 (1), 57–74.

- Storm, S., and Naastepad, C.W.M., 2015a. ‘Europe’s hunger games: income distribution, cost competitiveness and crisis,’. Cambridge Journal of Economics, 39 (3), 959–986.

- Storm, S., and Naastepad, C.W.M., 2016. Myths, mix-ups, and mishandlings: understanding the Eurozone crisis. International Journal of Political Economy, 45 (1), 46–71.

- Thirlwall, A.P., 1979. The balance-of-payments constraint as an explanation of international growth rates differences. Banca Nazionale de Lavoro Quarterly Review, 32, 45–53.

- Thirlwall, A.P., 2019. Thoughts on balance-of-payments constrained growth after 40 years. Review of Keynesian Economics, 7 (4), 554–567.