ABSTRACT

Environmental state debates focus on the governance and steering functions of politics. Concurrently, many states stand out as large global owners and investors in carbon industries. Via various investment vehicles, states control around half of all global oil and gas reserves as well as other carbon assets. We know very little, however, about where these states are invested; how they conduct their carbon investment; and what possibilities and constraints carbon-owning states have to decarbonise. Yet, these aspects – the geography, investment profiles and domestic state carbon capital dependence – are key to assess the possibilities and limitations of climate action states as carbon owners have. Based on new fine-grained firm-level data, we deliver conceptual and empirical insights into all three issues. Our intervention fills an important gap in our knowledge about the environmental state, while drawing the attention of researchers and policymakers to a blind spot, but also to transformation potentials of the carbon-owning state in the following decade.

Introduction

The state is back – at least if we believe the cascading emergence of new research programmes, journal articles, books, and public discussions on issues like the ‘new’ state capitalism (Alami and Dixon Citation2023), the ‘rebirth’ of industrial policy (Aiginger and Rodrik Citation2020), the ‘striking back’ of the state in development (EBRD Citation2020), or the recent expansion of state-led investment (Babic et al. Citation2020). In times of global crisis and transition, policymakers and scholars are re-discovering the transformative potential of state power (Allen et al. Citation2021). The environmental state is also part of this revival. Notwithstanding diagnoses about the decline of the environmental nation-state (Mol Citation2016), discussions about ‘greening the state’ (Meadowcroft Citation2012, Duit et al. Citation2016) and its concomitant transformative potentials are in full swing (Hatzisavvidou Citation2020, Hausknost Citation2020, Eckersley Citation2021). Defined as a ‘set of institutions and practices dedicated to the management of the environment and societal – environmental interactions’ (Duit et al. Citation2016, p. 5), the environmental state is today widely regarded as one, if not the key actor to potentially propel fundamental and rapid sustainable transformation on a global scale (Eckersley Citation2004, Johnstone and Newell Citation2018, Hausknost and Hammond Citation2020, Koch Citation2020).Footnote1

The discussion about the capacities and tools states can use to mitigate climate change covers a broad range of topics, from more technical suggestions like ‘greening’ the mandate of central banks (Dikau and Volz Citation2021), to demands such as a comprehensive global state intervention for a rapid transition (Bromley Citation2016), or the combination of state power with other mechanisms to enforce such transitions (Newell and Simms Citation2021). Summarising the different ‘faces’ of the environmental state, Duit (Citation2016) paradigmatically describes its four main tasks as administrative, regulating, redistributive, and knowledge-producing. All four are explicitly framing the state as governing environmental risks: the state oversees market processes and addresses ‘problems related to the market’s externalisation of environmental costs’ (Duit Citation2016, p. 69). By this logic, the environmental state is separated from markets, which it regulates and shapes towards sustainability. In other words, the existing discussions display a strong governance-centred understanding of the environmental state in tackling issues of climate change and decarbonisation.

In this paper, we extend such a governance-centred understanding by introducing one key aspect of the environmental state that has so far been mostly overlooked, namely the state as carbon owner. States not only regulate and govern markets, but they are also, crucially, owners, shareholders, investors, and lenders. In short, states are also market actors themselves (Clark et al. Citation2013, Babic et al. Citation2017). As such, many states have gained a strong financial position in the global political economy in recent years. States like Norway, China, France, and the United Arab Emirates are able to move global markets with their (dis-)investment decisions in the sectors they are heavily engaged in. Furthermore, states as owners still control more than half of global oil and gas reserves, produce more than half of global fossil fuels, and are still responsible for roughly 40 percent of investment into the sector (Alkadiri and Ewers Citation2020, Manley and Heller Citation2021). These numbers have not changed significantly in the last decade, despite a growing urgency and awareness of the looming climate catastrophe (Hults et al. Citation2012). It is more urgent than ever to scrutinise this neglected side of the environmental state, also because state carbon ownership stands in crass contrast to the normative self-understanding of the environmental state as driver of sustainability. This raises the question of how states can, as fossil fuel and carbon owners, decarbonise in a meaningful way.

This paper delivers two contributions to tackle this question. First, we refine the notion of the environmental state conceptually by going beyond its governance-related characteristics. While we concur with the environmental state literature that states have ‘classical’ governance instruments to mitigate climate change at their disposal, we argue that globalisation introduced another important but under-appreciated dimension of the environmental state. By becoming large-scale, fossil-fuelled corporate owners, many resource-rich states are now in a position in which their investment or disinvestment decisions have a direct and measurable impact on humanity’s global carbon footprint.Footnote2 This impact makes it the more important to develop a comprehensive understanding of the state as carbon owner. Our paper contributes the first conceptual outline of this understudied but crucial aspect of the environmental state.

Second, we map for the first time today’s landscape of the state as global owner of carbonised corporate equity. Existing research on the issue mainly scrutinised national oil companies (NOCs) as large and important state-owned fossil-fuel producers. However, states as owners are invested in all types of climate-damaging assets, and at different levels of ownership and control. Different states also vary across these dimensions. Drawing on recent (2021) fine-grained, firm-level state carbon ownership data from the ORBIS database, we analyse the geographical spread, the investment profiles and the domestic decarbonisation potentials of major carbon-owning states. Our results show that carbon state capital is owned by a few large states as owners; that majority ownership (and hence rather ‘illiquid’ capital) is predominant; and that decarbonisation potentials depend on a set of factors which we integrate into a heuristic for building decarbonisation strategies. Our empirical results also add to the notion that research on the environmental state should go beyond Europe and ‘the West’ as many states as owners are indeed not Western states (see also Death Citation2016). With these findings, we extend the literature on the environmental state in a significant way. This will enable future research to build on the insights generated here, and to develop concrete strategies for decarbonising the state as a global owner – for example by studying concrete cases and regions that appear prominently in our results.

Our contribution is drawing on a practice that Robyn Eckersley describes as ‘critical problem-solving’, which ‘is geared to identifying the ‘next best transition steps’ with the greatest transformational potential towards ecological sustainability’ (Eckersley Citation2021, p. 245). The approach aims to reconcile a critical stance towards issues of global justice and power relations with practicable suggestions for enabling the transformation towards an ecologically viable human future. This paper uncovers for the first time, which states as owners have the capacity and power to drastically reduce carbon emissions via their investment decisions. It also conceptualises possible strategies and discusses the viability and problems of such an approach to accelerate the energy transition. By taking such a global perspective, we go beyond the nation-state centric emphasis on the (im)possibilites of transforming the capitalist state towards sustainability (see, e.g. Hausknost Citation2020) and scrutinise the possibilities of decarbonising the state as global owner.

The following section discusses the existing literature on the governance-aspects of the environmental state and proposes a conceptual extension to integrate the rise of states as large carbon owners. The third section explains the methodological and data considerations relevant for this study. The fourth section analyses for the first time where and how states as global owners are invested in various high-carbon-emitting industries, and delineates different investment profiles and decarbonisation potentials of states as owners. The fifth section provides a conclusion and proposes the next steps of a broader research agenda on the state as carbon owner.

Governing the environmental state

The existing work on the environmental state is extensive and highly differentiated. Since the 1990s, various conceptual, normative, and empirical work has highlighted different aspects of the ‘environmental’, ‘green’, or ‘sustainable’ state (see, e.g. Dryzek et al. Citation2002, Mol Citation2002, Eckersley Citation2004, Christoff Citation2005, Meadowcroft Citation2005, Duit Citation2016). Its broad applicability in different research traditions makes the environmental or green state ‘a generic concept with different meanings’ (Hildingsson et al. Citation2019, p. 911). Nevertheless, the common denominator of existing studies can be summarised as analysing the potentials and limitations of the nation-state to bring about environmental protection and sustainability (Bailey Citation2020; see also Eckersley Citation2004, Christoff Citation2005, Hausknost Citation2020). States can, in other words, reach environmental goals by adapting and expanding the governance of environmental issues. Such green governance has many layers, of which the first and most basic one relates to rule-setting and environmental regulation. States create laws and provisions that rule out certain environmentally harmful practices and penalise offenders (Dryzek et al. Citation2002). This can, for example, be done by setting up new state institutions that engage in developing environmental policy innovations, or by instructing existing state apparatuses to follow newly established rules (Meadowcroft Citation2012). Such rule-setting targets in practice especially corporations and other economic entities that engage in environmental degradation through their business operations (see, e.g. Bromberg Citation2016).

Second, environmental state governance can and does incentivise different actors to change their behaviour to meet environmental targets set by the state. Incentivising actors goes beyond mere regulation, as states actively nudge other societal agents to adapt and work towards environmental and climate goals. Such incentives can concern citizens, for example by promoting environmental values (Barr Citation2003), or by creating financial incentives for consumers to abandon non-sustainable technologies and behaviours (Curtin et al. Citation2017). But also economic actors are being targeted by the environmental state, for example through incentive structures like emissions trading, environmental taxes, or other certification schemes (Meadowcroft Citation2005).

A third aspect of the governance-perspective on the environmental state is its interventionist side. Environmental states can and do engage in directly influencing society and markets to achieve desired outcomes. As an example, Hildingsson et al. (Citation2019) describe the intervention in industrial relations and industrial governance as a major environmental state tool for rapid decarbonisation. This goes beyond mere incentivising but represents a (temporary) market intervention for environmental goals. Another relevant tool are monetary policies and their re-designing to reflect more than simply price stability, but also climate change risks (Knaggård and Pihl Citation2015; see also Dikau and Volz Citation2021).

Each of these three aspects is key to understanding the governance-related elements of the modern environmental state. At the same time, the relationship between state power and the economy differs per aspect: while the regulating aspects of the environmental state operate within arm’s length from the economy, the incentivising aspect brings both a step closer. Environmental states that purposefully incentivise and nudge corporate actors into sustainable behaviour are overstepping such arm’s length principles. Finally, interventionist environmental states in some cases even cross the boundary between states and markets to directly influence and engineer desired sustainable outcomes, for example by manipulating or steering markets directly. The argument we develop in the following takes this one step further: how can we think about environmental states that themselves become market actors?

Beyond governance: rethinking the environmental state

As the burgeoning literature on the ‘new’ state capitalism demonstrates, states have been rising as global owners and investors in recent decades (Babic Citation2021, Alami et al. Citation2022). This rise does not only pertain to so-called emerging economies but is a global phenomenon (Babic et al. Citation2020, Kim Citation2022). Phenomena like the steady growth of the assets managed by SWFs from under USD 1tn. in 2000 to over USD 9tn. in 2021 exemplify this trend (SWFI Citation2019, Norrestad Citation2021). This establishment of states as market actors challenges classical political economy differentiations between states and markets as two distinct social spheres (see, e.g. Schwartz Citation2018). Importantly, much of this increasing state ownership is concentrated in carbon-intensive industries and firms such as in National Oil Companies (NOCs) (de Graaff Citation2012). NOCs and other SOEs hence play an outstanding role for potentially cutting global CO2 emissions (Hults et al. Citation2012). Likewise, also other state-owned vehicles such as SWFs regularly generate discussions about their (potential) role in mitigating climate change (Richardson Citation2011). Due to the global rise of state capital, today these large carbon-emitting state-owned vehicles are not only restricted to ‘typical’ statist economies like China but are to be found in many other places such as France, Qatar, and Norway (Babic et al. Citation2020). In this paper, we focus on the consequences of this rise for the environmental state: what does it mean for environmental state studies when states themselves become relevant global owners of carbon assets?

We propose to introduce the state as an owner as an important extension of the environmental state discussion. States as owners are a qualitatively different category from the three discussed elements and represent a fourth, so far under-theorised aspect of the environmental state. Even the most interventionist characteristics of the environmental state still concern its governance-functions and do not capture the fact that states become market actors themselves. Interventionist arguments like in Hildingsson et al. (Citation2019, p. 909), for example, explicitly refer to the role of the state not as owning, but as ‘govern[ing] industrial decarbonisation’ (emphasis added). Others like Allan et al. (Citation2021, p. 11) echo this difference between governance and ownership by suggesting ‘that opposition to green industrial policies might come from within the state itself as state-owned coal plants and government agencies with substantial investments in such enterprises object to and strive to block policies that reduce the value of these assets’. Similarly, monetary policy interventions for environmental state reasons are often described in terms of adapting governance mechanisms and their underlying logics (van ‘t Klooster Citation2021). Hence, even the more interventionist aspects of the environmental state discussion have to be differentiated from the role of the state as owner of carbon assets itself.

State ownership constitutes a fourth major aspect of the environmental state discussion and extends it. depicts the distance of the environmental state from the economy it is supposed to govern for the discussed aspects, with the state as owner on the right end of the spectrum.

Figure 1. Different aspects of the governance of the environmental state. The distance of states to markets decreases from left to right.

Different from other forms of environmental state governance, carbon state ownership is shaped by a fundamental tension: the state is supposed to decarbonise an aspect of the economy where it itself is invested in. In cases where whole political economies are highly dependent on for example state-led fossil fuel production (like in many Gulf states), this tension grows even stronger (see section four). However, state ownership of carbon assets also presents a major potential for decarbonisation which is not primarily accessible via regulation or other classical forms of environmental governance. Disentangling the different roles that are often subsumed under the category of the environmental state makes it possible to precisely locate potentials of greening the state, and to suggest strategies to achieve this goal. In the following, we first operationalise state carbon ownership, before turning to distinguish different possible decarbonisation strategies.

Conceptualising state carbon ownership

Being an owner puts states in the position to directly address issues of decarbonisation instead of indirectly regulating other actors. However, state ownership and its decarbonisation are not one-dimensional concepts: ownership structures can be relatively complex, and state ownership is a multifaceted phenomenon if we consider the varying motivations, forms, and effects that govern state-led equity investment (Haberly and Wójcik Citation2017, Alami and Dixon Citation2022). For the purposes of this paper, we understand state ownership of carbon assets as all types of fully state-owned entities holding shares in firms that are located in carbon industries.Footnote3 This ownership grants states as owners a certain degree of control over their invested firms – depending on, among others, the size of the ownership stake (Cubbin and Leech Citation1983, Berle and Means Citation1991). To map the global extent of this phenomenon, we deliberately refrain from distinguishing between different ownership types like voting and cashflow rights; or between different ownership patterns potentially influencing control (La Porta et al. Citation1999). Accordingly, we also do not take into account non-ownership factors that potentially influence corporate governance and control (Gillan Citation2006). We hold that these and other factors play a role for proposing decarbonisation strategies in concrete case studies, whereas our analysis lays the groundwork for such strategy-building across different corporate governance systems. To ensure comparability of different states as carbon owners, we hence resort to a conservative understanding of the relation between ownership and control: state control over its owned carbon assets rises, ceteris paribus, with a higher ownership stake (see also Babic et al. Citation2020). Existing scholarship acknowledges that ownership and operational control do not always go hand in hand in SOEs; but emphasises that ownership levels are a useful control proxy for comparative and theory-building purposes (Cuervo-Cazurra et al. Citation2014, Musacchio et al. Citation2015).

Our operationalisation has three implications for the potential decarbonisation of these assets. First, states that own more carbon assets, ceteris paribus, also control a larger amount of assets representing decarbonisation potential. Hence, the absolute size of a state as carbon owner matters for global decarbonisation efforts in two ways: first, we can determine which states invest how much in carbon assets to simply see and compare the geographies of large and small states as carbon owners. Second, we can distinguish between domestic investment, which is hard to decarbonise because it is tied to national (energy) security (see third point below); and transnational investment, which is theoretically easier to decarbonise since it is often employed to gain a return on investment. This argument is an important addition to the environmental state literature, which tends to focus on the national scale in comparing green transition potentials of states that differ vastly in their absolute contribution to global warming (see, e.g. Sommerer and Lim Citation2016). By taking carbon ownership and its control into account, we shift the debate towards the global stage and the absolute decarbonisation potentials relevant for a global green transition. We adopt this perspective when we analyse the state as a global carbon owner in the subsection ‘Geography: Where do states own carbon capital?’ below.

Second, the focus on ownership levels allows us to distinguish between different investment profiles that influence decarbonisation strategies. An elementary distinction is the one between so-called financial, i.e. profit-oriented, and more controlling profiles (Babic et al. Citation2020, Babic Citation2021). The former takes place in the form of portfolio investment, which usually does not amount to 10 percent of a company’s ownership stakes, and hence does not lead to corporate control.Footnote4 The latter takes the form of majority ownership by the owning state, which amounts, ceteris paribus, to corporate control.Footnote5 By aggregating the various ownership ties a state creates at the national level, we can establish whether a state tends, on average, to a financial or control profile. Such a distinction of investment profiles is useful to determine how liquid – and thus potentially re-investable – fossilised state capital is. Within the political economy literature, portfolio equity investment is generally understood as more liquid and ‘impatient’ than foreign direct investment, which is regarded as a more long-term form of investment, often in ‘physical’ assets (Linsi and Schaffner Citation2019, p. 852). In our distinction, states that invest predominantly through financial means could divest and redirect this liquid capital better (e.g. towards low-carbon assets) than states whose main carbon investment is invested via controlling stakes. The portfolio ratio – i.e. the relation of the sum of portfolio (financial) investment to other (controlling) investment – is thereby an important indicator of decarbonisation potential. We utilise this insight on the control-portfolio distinction and ownership profiles in the analysis subsections ‘Investment profiles: How do states own carbon capital?' and 'Carbon dependence: What are the potentials for decarbonising states as owners?’.

This differentiation leads to our third point, which is the role state ownership of carbon capital plays for domestic politics. Whereas portfolio and liquid investment might be easier to ‘get rid of’, states that own majority stakes in carbon assets also have, ceteris paribus, more control over those assets. Theoretically, this could mean that control profiles give states more leeway in effective decarbonisation if this is politically desired. However, a focus on the domestic political role of state carbon ownership nuances this aspect: many states rely on carbon (utility) ownership for reasons of energy security or are dependent on the revenues from this investment (Hanson Citation2009). State carbon entities are also a cornerstone of economic development in world regions like the Gulf states (Yom Citation2011, Young Citation2020). Carbon assets like large oil and gas firms are means of survival for many regimes rather than easy decarbonisation targets due to the corporate control states possess over them. This means that the relative size of the state carbon sector compared to the size of the domestic economy plays a major role in determining decarbonisation potentials. As we argue in the analysis below, different states have not only different levels of state carbon ownership, but also varying degrees of dependence on this resource. This means that we can differentiate between varieties of domestic state carbon capital dependency across countries. State carbon ownership can make up a higher or lower share of a country’s economy, and hence influence the economic and political stakes involved in decarbonisation. We apply this argument in the analysis in subsection, ‘Carbon dependence: What are the potentials for decarbonising states as owners?’.

Conceptualising decarbonisation

Similarly to state ownership, decarbonisation is an umbrella term for a range of different practices aimed at reducing the ecological footprint of humanity. At its core, decarbonisation implies the lowering and elimination of greenhouse gases emitted through economic activities, mostly by removing fossil fuels from primary energy production (see also Wimbadi and Djalante Citation2020). Different from micro-level questions of how to physically replace or remove carbon, the more governance-related aspects of decarbonisation deal with how states (and other actors) can steer or propel decarbonisation efforts (see, e.g. Allan et al. Citation2022). States as owners and investors have powers in addition to governance instruments, which is their ownership of capital stored in carbon firms. As corporate and asset owners, states can in theory decide what to do with this investment – again, depending on the ownership levels and control they realise in these firms (see preceding section).

In this paper, we distinguish between three ideal-typical modes of state carbon capital decarbonisation. The first is simple divestment, i.e. the selling off of (stakes in) carbon assets. This occurs most often in cases where states own small stakes in companies and other assets that can technically be sold off quickly. A typical example of this would be the Norwegian SWF GPF-G which recently decided to disinvest from oil and gas exploration altogether (Arvin Citation2021). Such investment withdrawal can in the long run lead to underfunding of carbon industries and the decline of their political legitimacy (Rosenbloom and Rinscheid Citation2020, p. 2). However, the immediate effectiveness of disinvestment is often rather low: disinvestment is often done for portfolio stakes (like in the Norwegian case), which are too small to be of broader significance; and carbon assets that are sold off can be picked up again, for example by private equity interested in maximally exploiting these climate-damaging assets (Christophers Citation2021). One way of boosting effectiveness is to increase the scale of divestment, which large owners like SWFs can potentially do.

A second means of decarbonisation is to redirect carbon investment into renewable energy sources. This can occur when firms decide to sell off fossil assets and replace these with non-carbon assets (e.g. by re-investing the money from the carbon sell-off). States that are large (or maybe even the largest) shareholders in carbon firms can employ this strategy to preserve the invested value while also decarbonising. An example of this is the Danish utility SOE Ørsted. The firm managed to sell off almost its entire carbon assets within a decade and used the revenues to decrease the carbon intensity of its power generation massively since 2010 (Ørsted Citation2019). Although this strategy is effectively reducing the carbon intensity of an SOE’s balance sheet, it faces similar constraints as the divestment strategy: sold-off carbon assets can be bought up by other investors – in the case of Ørsted it was even another state-owned vehicle, Energinet, which bought the disinvested oil and gas infrastructure in 2017. Nevertheless, state-led large-scale investment redirection can have a triple positive effect on decarbonisation through stripping investment from carbon assets, delegitimising their business models, and creating knowledge and possibly economies of scale for alternative energy sources. In addition, redirection can be combined with smart ways of phasing out carbon assets that avoid the worst polluting ramifications (Rosenbloom and Rinscheid Citation2020).

Phasing out is then also a third possibility for states to decarbonise. This means holding on to carbon ownership, stopping production successively and letting the remaining assets ‘strand’. While this is arguably the most effective strategy of ‘real’ decarbonisation, it is also the most difficult and problematic from an economic and political standpoint (Mayer and Rajavuori Citation2017). States as owners receive returns from their carbon investment, which they would lose if they phase out production. In addition, many states are also dependent on these revenues for maintaining political stability. This implies that we should expect phase-out strategies rather in cases where the dependence on carbon revenues and economic viability are lower. For example, French state-invested utility Engie started to divest from its coal business with some plants being fully shut down, such as the Hazelwood coal facility in Australia in 2017 (Paul Citation2016). However, many other formerly Engie-owned coal plants were either turned into gas or biomass plants or sold to owners that further exploited the assets (Boudreau Citation2021). Despite the difficulty of phasing out, it remains the single most powerful strategy for states as owners to reduce global CO2 emissions effectively and rapidly. summarises these three ideal-typical strategies.

Table 1. Different ideal-typical state carbon capital decarbonisation strategies.

We emphasise that these strategies are ideal-typical and will in reality be rather combined than executed in their pure form. For analytical reasons, it is however crucial to recognise the different levels of feasibility and effectiveness of each strategy. We complement this conceptual lens in the following analysis by providing a descriptive exploration of new firm-level state carbon capital data. The next section discusses our database and methodological issues, while the analysis section below proceeds with a first examination of the state as global carbon owner. This quantitative exercise is complemented by a discussion of different aspects of state carbon investment, which reveal different potential divestment strategies for the next decade.

Data and methods

We draw on firm-level ownership data from Bureau van Dijk’s ORBIS database from August 2021. ORBIS is a frequently used and well-explored large-scale database for international political economy research (Vitali et al. Citation2011, Garcia-Bernardo et al. Citation2017, Haberly and Wójcik Citation2017) and contains detailed information on (state) ownership relations relevant for our analysis. We extracted information on 7.680 global ownership relations, where a state or state-owned entity is invested in a company from a carbon industry.Footnote6 We checked and cleaned the raw data to create a dataset that contains information on the sender states, the target firms and their location, and various financial information on the target firms (such as operating revenue, current and total assets, number of employees).Footnote7

The elementary unit of this dataset is a state ownership tie. This relation consists of an owning state on the sending side, and an invested firm on the receiving end of this tie. The owning state (sender) is conceptualised as any fully state-owned vehicle that invests in fossil-fuel companies. The invested firm (target) is conceptualised as any carbon company that receives equity investment from a state-owned vehicle, and which ends up in an ownership stake for this vehicle. We aggregate each of these senders and targets on the national level to provide a meaningful overview of the existing ownership relations. This means that we do not differentiate between different vehicles investing in fossil fuel companies (such as SOEs, SWFs, and the like), but between the level of ownership and control the investing (state-owned) vehicle exerts via its investment. This differentiation allows us to measure precisely how strong and deep states are invested in particular carbon firms. This approach does not automatically assume how specific state-owned vehicles invest – for example, that SWFs typically invest small stakes via portfolio investment – but rather looks at how states as owners actually invest, independently of which type of vehicle they use to do so. Such an approach is bolstered by recent work in the field of (cross-border) state investment (see Carney Citation2018, Babic et al. Citation2020).

Not every created tie is the same – both in terms of the ownership level and control the tie grants the owning state, as well as regarding the value of the invested firm. Put simply, a majority ownership stake in a large oil multinational is different from a portfolio stake in a medium-sized domestic coal mine. To account for these differences, we calculate the weight of a tie by multiplying the ownership stake held by the state (between 0 and 1) with the operating revenue of the target firm (in USD).Footnote8 This is a common method of estimating the value of ownership ties in political economy research using large datasets (see Vitali et al. Citation2011, Garcia-Bernardo et al. Citation2017, Babic Citation2021). By assigning a weight to each ownership tie, we can analyse the global extent of state carbon ownership based on granular firm-level data. This improves the precision and quality of our data compared to standard macroeconomic measurements like balance of payments data between states (Linsi and Mügge Citation2019).

Analysis

We now turn to the analysis which builds on the conceptual ideas developed above. To give a first descriptive overview of the state as global carbon owner, we focus on three fundamental questions: first, where is state carbon ownership concentrated in the global political economy? For this, we analyse the distribution of state carbon ownership when aggregated at the national level, corresponding to the idea of states as carbon owners. Second, we ask how states own carbon capital – i.e. which investment profiles prevail in which cases, and what does this tell us about possible decarbonisation strategies? Third, we zoom in on the domestic level and ask what decarbonisation potentials different groups of states hold, depending on the significance of carbon state ownership for the whole economy. Taken together, these questions provide a comprehensive initial analysis upon which further research can build in developing decarbonisation strategies for concrete cases.

Geography: where do states own carbon capital?

The bulk of state investment in carbon companies is located domestically. This is no surprise. Large fossil-fuelled utility firms have historically been the backbone of domestic energy supply in most developed economies. In addition, many oil-rich countries such as Mexico and Saudi Arabia established large state-owned companies in the twentieth century, which still dominate domestic markets. At the same time, some states also became transnational carbon owners. The most common example is China, whose national oil companies have been creating transnational ownership and board interlock ties for almost two decades (de Graaff Citation2020). Both aspects are important to understand the geographical spread of the state as carbon owner within the global political economy.

Considering the entire sample (domestic and transnational ties), we see the following distribution of carbon state capital ().

Table 2. Top 10 states as fossil-fuel hosts and owners.

China’s overarching position stems from two factors, namely the size of its economy in combination with large-scale state ownership in key industries, such as energy production (Naughton and Tsai Citation2015). Fossil fuels played and still play a major role in China’s development trajectory. Today, China’s economy is responsible for about a quarter of total global greenhouse gas emissions (O’Meara Citation2020). The strong grip of the state on a large share of these emissions is also expressed in the massive state ownership concentration we see here. State-owned giants like CNPC or Sinopec are relevant in this respect, as is ownership of automobile and truck firms, steel producers, or smaller stakes via investment funds in multinational fossil firms like Shell and BP.

The rest of the top 10 owners have most of their fossilised ownership located domestically. Both lists only differ with regards to two states – Norway as large owner, and Germany as large host. In the Norwegian case, its rather small economy and a traditionally ‘closed’ market for foreign investment (Lie Citation2016) stand in contrast to its powerful SWF that invests large sums outside its own borders. As for the rest, large fossil-fuel owners and producers like Saudi Arabia (e.g. Saudi Aramco) or Mexico (e.g. PEMEX), and simply large economies like India (e.g. IndianOil) dominate the global landscape of states as owners.

If we look at transnational ties only, we see a strong reduction in investment volume, but also a clear shift among the top owners ().

Table 3. Top 10 states as transnational carbon state capital hosts and owners.

Transnational investment ties indicate a slightly different interest of the investing state than domestic investment. While the latter is often employed to maintain a (historically grown) grip on domestic energy security, the former is part of a state’s outwards strategy to capture profits, know-how, market shares, and other relevant assets in the global economy (Babic Citation2021). States like Norway or Kuwait, but also Canada and Sweden use investment in carbon capital in this sense. Especially the Norwegian share is dominant, with over 51 percent of all transnationally invested carbon state capital. This adds up to over 73 percent of all Norwegian state carbon investment. Some transnational owners like Singapore or Canada also show quite high percentages of their total investment being located overseas ().

Table 4. Share of carbon state capital invested cross-border.

For states that own large parts of their carbon investment domestically, potentially effective phase-out decarbonisation strategies will be difficult to realise (see section 4.3). Redirective decarbonisation strategies (see ) are particularly relevant for transnationally invested (portfolio) state carbon capital. This type of investment is often employed to gain a return on investment and can hence theoretically be redirected into other assets that provide this function. States like Singapore, Canada, and the United States steer large sovereign and pension funds that often are invested with smaller stakes in carbon firms, which provides a major potential for redirective strategies.

Investment profiles: how do states own carbon capital?

Despite this potential for decarbonisation, only slightly more than 8 per cent of all carbon state capital is financial investment via portfolio stakes in our dataset. Against this, almost 78 per cent is in majority ownership and hence represents mostly non-liquid capital. For global decarbonisation efforts, this is suboptimal, as most carbon assets are ‘stuck’ in large company stakes. This also increases the likelihood of incurring enormous losses through so-called ‘stranded assets’ (Caldecott Citation2017), as existing majority ownership positions expose states to future non-performance of carbon assets following climate change adaptation measures.

At the same time, the potential for divestment from portfolio stakes is unevenly distributed. States have different ownership profiles, with some having their carbon capital located predominantly in majority (control profile), and others in portfolio or non-controlling stakes (financial profile). In our sample, 49.5 percent of states have a control profile, whereas 18 percent have a financial profile, and 32.4 percent have a mixed profile, with most of their ownership stakes being located between the other two strategic profiles. Such a distribution is slightly less skewed towards control profiles and implies that around a fifth of all states in our sample mostly rely on portfolio, i.e. potentially liquid carbon investment. Among the top 10 owners, Norway displays by far the largest potential here, followed by Kuwait and India ().

Table 5. Investment profiles of the top 10 states as fossil owners.

The portfolio ratio represents the relation of the sum of portfolio investment to the remaining investment forms. We can see that only Norway shows a clear positive relation, reflecting the fact that three quarters of Norwegian carbon state capital is likely liquid capital. This may be similar in hybrid cases where most state capital is located in neither portfolio nor controlling stakes, as is the case for Russia and France. Here, most (carbon) state capital is invested via so-called ‘golden shares’ that retain a veto possibility for the state but do not amount to full corporate control. In the French case, the state-owned agency administering these shares has been analysed considering state financialisaton. The French state has been likened to a holding company in this respect (Coutant Citation2014). This means that carbon state ownership between portfolio and controlling investment needs to be scrutinised towards its de facto liquidity in case studies, which can determine the exact room for manoeuvre for different states as owners.

In sum, different investment profiles of states as owners point to varying degrees of decarbonisation difficulty and varying decarbonisation strategies. States with financial profiles will have fewer problems with divestment and even redirection strategies than those with control profiles. For states with mostly golden shares, a strategy of pushing the firm management to divest and redirect carbon investment into renewable assets is a viable decarbonisation strategy (see discussion section below). For the large group of states with control profiles, highly effective phase-out strategies are one clear decarbonisation pathway, ceteris paribus. To gauge this potential correctly, it is however important to understand the overall weight of carbon investment vis-à-vis the domestic economy – and consequently domestic politics. We turn to this in the next section.

Carbon dependence: what are the potentials for decarbonising states as owners?

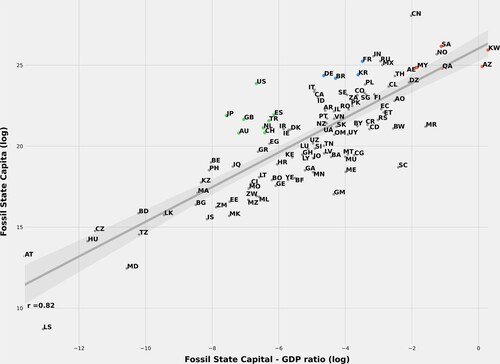

In line with the global perspective taken in this paper, we focus on presenting a global overview of the relative decarbonisation potentials of states as owners within their domestic political economy. This concerns first the absolute size of state carbon investment in combination with the relative size of this investment compared to domestic GDP (). This comparison allows us to gauge whether high-profile owners are also able to divest more easily given the relation of this investment to their total GDP.

Figure 2. Relation between total carbon state ownership (y-axis) and the ration between this ownership and GDP (x-axis). Both axes are logarithmic for representational reasons.

Unsurprisingly, both factors correlate strongly, with large-scale fossil owners also being quite dependent on these carbon investments. For illustration purposes, we pick examples from three different groups that can serve as examples of different political situations states as owners face. First, the red-coloured examples () represent strong cases of dependence on carbon state capital. Some of those states, like Kuwait and Azerbaijan, own carbon state capital in excess of their current GDP, as can be seen in . This implies not only a general dependence on oil revenues of the economy, but a strong political dependence of the state as an owner on said income and assets. In cases like Kuwait this dependence extends to the whole political system, which has been described as ‘popular rentierism’ (Yom Citation2011), whereby the legitimacy of ruling elites is upheld and bolstered by fossil revenues. This type of carbon capital-owning state is less likely to engage in large-scale and rapid divestment efforts for a range of factors, from short-term economic considerations to the question of bare political survival of ruling elites. Cases like Norway, whose SWF profitability and hence national income also still depend on fossil fuels, are more flexible in this regard as most of its investment is rather liquid capital (see previous section).

A second relevant type of owners are states that are, based on GDP, less dependent on fossil ownership, but still have significant stakes in carbon firms (examples coloured in blue, ). Those states as owners are economically and often also politically less dependent on their carbon portfolios. Rapid decarbonisation steps are not likely to lead to political breakdown and can at the same time make a real difference on the global scale if we take owners like South Korea, Germany, or France into focus. In addition, the rapid decarbonisation of domestic energy production and consumption could propel technological innovation in renewables and grant these (often industrial) countries first-mover advantages in green industries. While those economies are hence still largely dependent on fossil fuels for their industrial development, the state as owner has more leeway and incentives to decarbonise than states from the red group.

A third example are the green states (), which display relevant amounts of state carbon ownership but lower state carbon capital-GDP ratios. States like the US, Japan, or the UK still own significant stakes in carbon capital, for example through pension fund investment or utility firms. At the same time, neither the domestic economy nor their political system hinges on the state as carbon owner. In this respect, decarbonisation efforts would be much easier and faster implementable than in some of the more dependent ‘petrostates’ above. In addition, developed OECD states like the mentioned ones do have more decarbonisation leeway as falling CO2 emissions for the US and EU over the last decade exemplify (Hickel and Kallis Citation2020, p. 477).

Discussion: building decarbonisation strategies

In combination with our conceptual considerations, our empirical results provide us with a first descriptive mapping of the state as global carbon owner. We discuss three key implications of this analysis and how these can contribute to the broader goal of decarbonising states as owners.

First, our analysis delivers elementary insights into how to start building concrete decarbonising strategies. We incorporate the three discussed dimensions into an analytical heuristic, which can serve as a tool for such strategy-development ().

Figure 3. Analytical heuristic for analysing state decarbonisation strategies.

Based on our findings, we argue that only such an integrated approach that takes all three dimensions seriously represents a viable path towards concrete and viable decarbonisation strategies. The example of Norway illustrates this: with a high carbon state capital-to-GDP ratio, we would classify the decarbonisation potential of the Norwegian state as low (box 3 of ). At the same time, most of this investment is in transnational portfolio stakes, which makes most of Norway’s carbon state capital liquid and hence potentially open for rapid decarbonisation (boxes 1 and 2). Similar points apply to virtually all states as carbon owners. We hold that such a heuristic needs to be applied on a case-to-case basis, where different states will need to be studied either in single or comparative case studies (Levy Citation2008). Our empirical results provide a mapping of the different states as owners, their investment profiles, and their domestic decarbonisation potentials. Case-oriented work needs to study the interplay of these and other dimensions in determining concrete strategies that go beyond our general mapping and suggestions.

Our second discussion point then also expands on this interplay with other dimensions of decarbonisation governance. Specifically, we suggest that the focus on the state as carbon owner needs to be complemented by the agency options provided by other environmental state apparatuses and functions. The conceptual extension of the environmental state literature we argued for in section 2.1 (see ) is not a one-way street: once the extension to include ownership of carbon assets is established as a relevant category, we can recursively ask how this dimension of the environmental state can interact with the other governance-centred aspects to build effective decarbonisation strategies. In terms of regulation, states can enact ambitious decarbonisation goals that apply to state-owned entities solely. In this way, strenuous and long-winded conflicts with other private actors can be avoided. As an example, states can mandate their sovereign funds to decarbonise at a faster pace; or they can mandate their state-owned utility firms to prioritise environmental over profit goals without having to deal with resistance and delay by non-state actors. Furthermore, states can incentivise their own entities (as well as others) to decarbonise by leveraging their ownership position in firms. They can, for example, use their control position in utility firms to build green mobility infrastructure as public goods, where private actors would not be willing or able to invest (Sunio et al. Citation2021). Furthermore, states could take over the financial risks for their firms involved in decarbonising or developing green assets, and in this way de-risk rapid green transitions of state-owned entities (see also Gabor Citation2021). On the intervention side, states could propel the rapid decarbonisation of their state-owned entities by massive investment and hence turn these firms into ‘green’ national champions. Finally, states could also force the firms in which they hold a veto stake (or are the largest shareholder) to adopt more ambitious decarbonisation goals and to veto regressive ‘brown’ projects by management. summarises these potential cross-fertilisations between state ownership and other environmental state dimensions.

Table 6. Possible interplay of state ownership with other environmental state dimensions.

Third, our results also point to a major limitation of our study that needs to be addressed in future research. To build effective and smart decarbonisation strategies, we need to differentiate between carbon investment that ‘needs to go’ – e.g. the exploration and production of fossil fuels – and investment that can be transformed over time – e.g. the production of pesticides or cars, which both still rely heavily on fossil fuels, but where low-carbon alternatives technically exist. Our analysis takes a broad view on the state as carbon owner and includes all carbon assets where states currently hold ownership positions in. Such a perspective has the benefit of delivering a global status quo overview, while at the same time being limited by not considering possible temporal changes in these assets (i.e. through low-carbon alternatives). We think that it is important to add such a more dynamic perspective to the groundwork conducted in this paper. One possibility of doing so would be to introduce a fourth box to that classifies state carbon ownership according to its transition potential. This would allow for a more fine-grained analysis along sectoral lines and improve the policy-relevance of developed decarbonisation strategies.

Conclusion: towards decarbonising states as owners

Decarbonising the state as owner is one of the key challenges in the ongoing global sustainability transition. States do not only govern and regulate carbon investment, but they themselves engage in such investment forms. Existing accounts have not paid sufficient attention to this important dimension of the environmental state, which will only increase in its relevance in a post-Covid world that is looking more ‘statist’ than the preceding era of neoliberal globalisation (Gerbaudo Citation2021). We argue that a perspective extending the classical environmental state literature as adopted in this paper can help us to disentangle conceptually the state as carbon owner, and to help us in identifying empirical pathways to better understand this specific state role. Our empirical analysis sets up and analyses a granular firm-level database on the state as a carbon owner and describes three major dimensions of this phenomenon. Taken together, all three dimensions provide important groundwork in the form of a conceptual and empirical starting point for decarbonising the state as an owner. Necessarily, the analysis provided here is limited as it represents only the first step in a much broader effort to better understand the extent, strategies, and decarbonisation potentials of carbon-owning states, and to embed these insights into broader analytical and strategic considerations of a rapid and equitable global decarbonisation (see, e.g. Paterson Citation2021).

One such key aspect is to push forward the debates about the role of state carbon ownership in governing low-carbon transitions (Prag et al. Citation2018). There is a long-standing public debate about whether public or private ownership of carbon assets is more conducive to decarbonisation, connected to the normative demand of a re-nationalisation of critical assets to ensure just and rapid green transitions (see, e.g. Bozuwa and Skandier Citation2019, Lamperti et al. Citation2019). New research suggests that for sectors like electricity generation, state ownership increases investment into renewable energy sources compared to private firms (Steffen et al. Citation2022). State ownership can, in well-designed cases, be the superior decarbonisation instrument for different sectors (Benoit et al. Citation2022). At the same time, this can vary across sectors and the context is crucial: earlier studies have found that, for example, US state policies to increase the sale of renewable energy were less effective for state-owned utilities than for private ones (Delmas and Skandier Citation2011, p. 2274). Similarly, research shows how multi-level state ownership of coal plants in China can create opposition to decarbonisation from within the state and state-owned firms (Nahm and Urpelainen Citation2021). The conceptual and empirical work conducted in this paper contributes to these discussions by bringing in the state as an owner of different kinds of carbon assets. While many studies focus on large and well-known SOEs and utility firms, our analysis extends this aspect and brings portfolio, and thus theoretically liquid, carbon investment into the discussion. The question of state ownership in the green transition goes beyond specific types of SOEs, but involves a range of instruments and strategies, which need to be considered as we argue in this paper. The likelihood of successful decarbonisation is of course also dependent on the broader ecosystem of low-carbon governance, which needs to include a range of other important decarbonising instruments such as a ‘renewal of welfarism’ (Bailey Citation2015, p. 809) along sustainable lines.

Regarding future work, two key tasks are central from our perspective. The first will be to distinguish between carbon state capital that is potentially substitutable with green alternatives, and other state capital that is not. Here, existing approaches to distinguish sustainable from non-sustainable investment in general are an important starting point for further theory development (Krahé Citation2021). Such differentiated analyses also need to outline better which aspects of fossil state investment are easier to decarbonise than others, for instance with regards to incumbent (state) actors. Existing research already put the issue of fossil incumbency high on the priority list of sustainability research, which can be extended to specifically focus on the state and state elites as incumbent owners (Newell and Johnstone Citation2018). The second task will be to further theorise and empirically scrutinise the changing patterns of carbon ownership and what those imply for rapid decarbonisation strategies. Recent research suggests that the ‘old’ model of the publicly listed carbon company is slowly being replaced by other forms of private and state equity (Christophers Citation2021, Citation2022). This is an important development that shifts carbon capital away from big oil multinationals into, among others, the hands of NOCs and other state-owned vehicles. Since these vehicles are on average less transparent than their (publicly) listed counterparts, future research needs to establish the consequences of this shift theoretically and empirically. Better understanding the waning profitability of oil majors (see, e.g. Hager Citation2021) in combination with the insights on the state as carbon owner generated here is a key task for future research on effective global decarbonisation strategies.

Supplemental Material

Download MS Word (49.6 KB)Acknowledgements

We would like to thank Basil Bornemann, Louison Cahen-Fourot, Malcolm Fairbrother, Tobias Gumbert, Sandy Brian Hager, Daniel Hausknost, Peter Newell, Mat Paterson, two anonymous reviewers as well as the participants of the DVPW 2021, ISA 2022 and SASE 2022 conferences, the SECO research seminar at Roskilde University and the EPOSS seminar participants for valuable feedback on previous versions of this paper. This project has received funding from the European Research Council (ERC) under the European Union’s Horizon 2020 research and innovation program (grant agreement number 758430).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Milan Babić

Milan Babić is Assistant Professor of Global Political Economy at Roskilde University and member of the SWFsEUROPE project at Maastricht University. He is affiliated with the CORPNET research group at the University of Amsterdam. His work deals with foreign state investment and the transformations of the global political economy in the transition from a neoliberal toward a post-neoliberal global order. His work has appeared in Review of International Political Economy, International Affairs, Business & Politics, International Studies Review, Geopolitics, and The International Spectator, among others. His book The Rise of State Capital (Agenda) will be published in 2023.

Adam D. Dixon

Adam D. Dixon is Associate Professor of Globalization and Development at Maastricht University. He is principal investigator of the European Research Council research project Legitimacy, Financialization, and Varieties of Capitalism: Understanding Sovereign Wealth Funds in Europe (SWFsEUROPE). His research focuses on globalization, development, state capitalism, and the political economy of sovereign wealth funds. He is the author of Sovereign Wealth Funds: Between the State and Markets (Agenda, 2022), The New Frontier Investors: How Pension Funds, Sovereign Funds, and Endowments are Changing the Business of Investment Management and Long-Term Investing (Palgrave Macmillan 2016), The New Geography of Capitalism: Firms, Finance, and Society (Oxford University Press 2014), Sovereign Wealth Funds: Legitimacy, Governance, and Global Power (Princeton University Press, 2013), and an editor of Managing Financial Risks: From Global to Local (Oxford University Press 2009).

Notes

1 We refer here to the transformative potential of the environmental state, which has to be differentiated from both the normative claim that it should drive sustainability transitions (Eckersley Citation2004) as well as the empirical claim that it does drive them (Sommerer and Lim Citation2016). We thank an anonymous reviewer for pointing this out to us.

2 However, divestment does not necessarily lead to decarbonisation if the new owner exploits the resource. We discuss this in the following section.

3 We explain what we count as carbon industries in the next section as well as in the appendix.

4 See the study of (He et al. Citation2016), who follow the UNCTAD definition of state control beginning at 10 percent of owned shares.

5 For a discussion of different thresholds for corporate control see appendix.

6 By ‘carbon industry’ we refer to firms whose business model either directly (e.g., oil exploration firms) or indirectly (e.g., car manufacturers, pesticide producers) relies on large-scale CO2 emissions. We use different NACE2 and NAICS industry codes to determine which firms belong in this category. See appendix for a list and further information.

7 See the appendix for the specific cleaning steps and further information on the created dataset.

8 For a discussion of alternative measures of firm size, see appendix.

References

- Aiginger, K. and Rodrik, D., 2020. Rebirth of industrial policy and an agenda for the twenty-first century. Journal of industry, competition and trade, 20 (2), 189–207.

- Alami, I., Babic, M., Dixon, A.D., Liu, I., 2022. Special issue introduction: what is the new state capitalism? Contemporary politics, 28 (3), 245–263.

- Alami, I., and Dixon, A.D., 2022. "Expropriation of capitalist by state capitalist": organizational change and the centralization of capital as state property. Economic geography, 98 (4), 303–326.

- Alami, I., and Dixon, A.D., 2023. Uneven and combined state capitalism. Environment and planning A: economy and space, 55 (1). doi:10.1177/0308518X211037688.

- Alkadiri, R. and Ewers, B., 2020. Preparing national oil companies for a new energy landscape. Boston Consulting Group. https://www.bcg.com/publications/2020/strategies-for-being-an-environmentally-conscious-oil-company.

- Allan, B., Lewis, J.I., and Oatley, T., 2021. Green industrial policy and the global transformation of climate politics. Global environmental politics, 21 (4), 1–19.

- Allen, P., Konzelmann, S.J., and Toporowski, J., eds. 2021. The return of the state. S.l: Agenda Publishing.

- Arvin, J., 2021. Norway’s trillion-dollar wealth fund sold the last of its investments in fossil fuel companies. Vox. https://www.vox.com/22256192/norway-oil-gas-investments-fossil-fuel.

- Babic, M., 2021. State capital in a geoeconomic world: mapping state-Led foreign investment in the global political economy. Review of international political economy: online first.

- Babic, M., Fichtner, J., and Heemskerk, E.M, 2017. States versus corporations: rethinking the power of business in international politics. The international spectator, 52 (4), 20–43.

- Babic, M., Garcia-Bernardo, J., and Heemskerk, E.M., 2020. The rise of transnational state capital: state-Led foreign investment in the 21st century. Review of international political economy, 27 (3), 433–75.

- Bailey, D., 2015. The environmental paradox of the welfare state: the dynamics of sustainability. New political economy, 20 (6), 793–811.

- Bailey, D., 2020. Re-Thinking the fiscal and monetary political economy of the green state. New political economy, 25 (1), 5–17.

- Barr, S., 2003. Strategies for sustainability: citizens and responsible environmental behaviour. Area, 35 (3), 227–40.

- Benoit, P., et al., 2022. Decarbonization in state-owned power companies: lessons from a comparative analysis. Journal of cleaner production, 355, 131796.

- Berle, A.A., and Means, G.C., 1991. The modern corporation and private property. New Brunswick: Transaction Publishers.

- Boudreau, C., 2021. When companies go green, the planet doesn’t always win. Politico. https://www.politico.com/news/2021/03/30/companies-green-planet-doesnt-always-win-478460 (March 30).

- Bozuwa, J. and Skandier, C., 2019. Shifting ownership for the energy transition in the New green deal: a transatlantic proposal. In: Mathew Lawrence, ed. Roadmap to a green new deal. London: CommonWealth UK, 14–21.

- Bromley, P.S., 2016. Extraordinary interventions: toward a framework for rapid transition and deep emission reductions in the energy space. Energy research & social science, 22, 165–71.

- Caldecott, B., 2017. Introduction to special issue: stranded assets and the environment. Journal of sustainable finance & investment, 7 (1), 1–13.

- Carney, R.W., 2018. Authoritarian capitalism. sovereign wealth funds and state-owned enterprises in east Asia and beyond. Cambridge: Cambridge University Press.

- Christoff, P.A., 2005. Out of chaos, a shining star? toward a typology of green states. In: John Barry, and Robyn Eckersley, eds. The state and the global ecological crisis. Cambridge, MA: MIT Press, 25–52.

- Christophers, B., 2021. The End of carbon capitalism (as We knew It). Critical historical studies, 8 (2), 239–69.

- Christophers, B., 2022. Fossilised capital: price and profit in the energy transition. New political economy, 27 (1), 146–159.

- Clark, G.L., Dixon, A.D., and Monk, A.H.B., 2013. Sovereign wealth funds. legitimacy, governance, and global power. Princeton: Princeton University Press.

- Coutant, H., 2014. The state as a holding company? The Rise of the Agence Des Participations de l’Etat in the French Industrial Policy.

- Cubbin, J. and Leech, D., 1983. The effect of shareholding dispersion on the degree of control in British companies: theory and measurement. The economic journal, 93 (370), 351–369.

- Cuervo-Cazurra, A., et al., 2014. Governments as owners: state-owned multinational companies. Journal of international business studies, 45 (8), 919–42.

- Curtin, J., McInerney, C., and Gallachóir, B.Ó., 2017. Financial incentives to mobilise local citizens as investors in low-carbon technologies: a systematic literature review. Renewable and sustainable energy reviews, 75, 534–47.

- Death, C., 2016. The green state in Africa. New Haven, CT: Yale University Press.

- de Graaff, N., 2012. The hybridization of the state–capital nexus in the global energy order. Globalizations, 9 (4), 531–45.

- de Graaff, N., 2020. China Inc. goes global. transnational and national networks of China’s globalizing business elite. Review of international political economy, 27 (2), 208–33.

- Delmas, M.A. and Montes-Sancho, M.J., 2011. U.S. state policies for renewable energy: context and effectiveness. Energy policy, 39 (5), 2273–88.

- Dikau, S. and Volz, U., 2021. Central bank mandates, sustainability objectives and the promotion of green finance. Ecological economics, 184, 107022.

- Dryzek, J.S., et al., 2002. Environmental transformation of the state: the USA, Norway, Germany and the UK. Political studies, 50 (4), 659–82.

- Duit, A., 2016. The four faces of the environmental state: environmental governance regimes in 28 countries. Environmental politics, 25 (1), 69–91.

- Duit, A., Feindt, P.H., and Meadowcroft, J., 2016. Greening leviathan: the rise of the environmental state? Environmental politics, 25 (1), 1–23.

- EBRD. 2020. Transition report 2020-21: the state strikes back. European Bank for Reconstruction and Development. https://www.ebrd.com/news/publications/transition-report/transition-report-202021.html.

- Eckersley, R., 2004. The green state: rethinking democracy and sovereignty. Cambridge, MA: MIT Press.

- Eckersley, R., 2021. Greening states and societies: from transitions to great transformations. Environmental politics, 30 (1-2), 245–265.

- Gabor, D., 2021. The wall street consensus. Development and change, 52 (3), 429–59.

- Garcia-Bernardo, J., et al., 2017. Uncovering offshore financial centers: conduits and sinks in the global corporate ownership network. Scientific reports, 7 (1), 6246.

- Gerbaudo, P., 2021. The great recoil: politics after populism and pandemic. First edition hardback. London: Verso Books.

- Gillan, S.L., 2006. Recent developments in corporate governance: an overview. Journal of corporate finance, 12 (3), 381–402.

- Haberly, D. and Wójcik, D., 2017. Earth incorporated: centralization and variegation in the global company network. Economic geography, 93 (3), 241–66.

- Hager, S.B., 2021. A requiem for carbon capitalism? Capital as Power. https://capitalaspower.com/2021/10/a-requiem-for-carbon-capitalism/ (October 26).

- Hanson, P., 2009. The resistible rise of state control in the Russian oil industry. Eurasian geography and economics, 50 (1), 14–27.

- Hatzisavvidou, S., 2020. Inventing the environmental state: neoliberal common sense and the limits to transformation. Environmental politics, 29 (1), 96–114.

- Hausknost, D., 2020. The environmental state and the glass ceiling of transformation. Environmental politics, 29 (1), 17–37.

- Hausknost, D., and Hammond, M., 2020. Beyond the environmental state? The political prospects of a sustainability transformation. Environmental politics, 29 (1), 1–16.

- He, X., Eden, L., and Hitt, M.A., 2016. The renaissance of state-owned multinationals. Thunderbird international business review, 58 (2), 117–29.

- Hickel, J. and Kallis, G., 2020. Is green growth possible? New political economy, 25 (4), 469–86.

- Hildingsson, R., Kronsell, A., and Khan, J., 2019. The green state and industrial decarbonisation. Environmental politics, 28 (5), 909–28.

- Hults, D.R., Thurber, M.C., and Victor, D.G., eds. 2012. Oil and governance: state-owned enterprises and the world energy supply. Cambridge, New York, UK: Cambridge University Press.

- Johnstone, P. and Newell, P., 2018. Sustainability transitions and the state. Environmental innovation and societal transitions, 27, 72–82.

- Kim, K., 2022. Locating New ‘state capitalism’ in advanced economies: an international comparison of government ownership in economic entities. Contemporary politics, 28 (3), 285–305.

- Knaggård, Å. and Pihl, H., eds. 2015. The green state and the design of self-binding. In Karin Backstrand and Annica Kronsell, eds. Rethinking the green state: environmental governance towards climate and sustainability transitions. London: Routledge, 209–224.

- Koch, M., 2020. The state in the transformation to a sustainable postgrowth economy. Environmental politics, 29 (1), 115–33.

- Krahé, M., 2021. From system-level to investment-level sustainability. An epistemological one-way street. Brussels: Académie royale de Belgique. Chaire SFPI. https://www.academieroyale.be/Academie/documents/Opinio_SFPI_numerique31253.pdf.

- Lamperti, F., et al., 2019. Green finance: the macro perspective. Vierteljahrshefte Zur Wirtschaftsforschung, 88 (2), 73–88.

- La Porta, R., Lopez-De-Silanes, F., and Shleifer, A., 1999. Corporate ownership around the world. The journal of finance, 54 (2), 471–517.

- Levy, J.S, 2008. Case studies: types, designs, and logics of inference. Conflict management and peace science, 25 (1), 1–18.

- Lie, E., 2016. Context and contingency: explaining state ownership in Norway. Enterprise & society, 17 (4), 904–30.

- Linsi, L. and Mügge, D.K, 2019. Globalization and the growing defects of international economic statistics. Review of international political economy, 26 (3), 361–83.

- Linsi, L. and Schaffner, F., 2019. When Do heuristics matter in global capital markets? The case of the BRIC acronym. New political economy, 24 (6), 851–72.

- Manley, D. and Heller, P.R.P., 2021. Risky Bet. National oil companies in the energy transition. Natural Resource Governance Institute. https://resourcegovernance.org/sites/default/files/documents/risky-bet-national-oil-companies-in-the-energy-transition.pdf.

- Mayer, B. and Rajavuori, M., 2017. State ownership and climate change mitigation. Carbon & climate law review, 11 (3), 223–33.

- Meadowcroft, J., 2005. Environmental political economy, technological transitions and the state. New political economy, 10 (4), 479–98.

- Meadowcroft, J., 2012. Greening the state. In: P. Steinberg, and S Van Deveer, eds. Comparative environmental politics. Cambridge, MA: MIT Press, 63–88.

- Mol, A., ed., 2002. The environmental state under pressure. Amsterdam: JAI.

- Mol, A., 2016. The environmental nation state in decline. Environmental politics, 25 (1), 48–68.

- Musacchio, A., Lazzarini, S.G., and Aguilera, R.V., 2015. New varieties of state capitalism: strategic and governance implications. Academy of management perspectives, 29 (1), 115–31.

- Nahm, J. and Urpelainen, J., 2021. The enemy within? green industrial policy and stranded assets in China’s power sector. Global environmental politics, 21 (4), 88–109.

- Naughton, B. and Tsai, K.S., eds. 2015. State capitalism, institutional adaptation, and the Chinese miracle. Cambridge: Cambridge University Press.).

- Newell, P. and Johnstone, P., 2018. The political economy of incumbency: fossil fuel subsidies in global and historical context. In: Jakob Skovgaard, ed. The politics of fossil fuel subsidies and their reform. Cambridge: Cambridge University Press, 66–80.

- Newell, P. and Simms, A., 2021. How did we do that? Histories and political economies of rapid and just transitions. New political economy, 26 (6), 907–922.

- Norrestad, F., 2021. Assets under Management (AUM) of Sovereign Wealth Funds (SWFs) Worldwide from 2008 to 2021. Statista. https://www.statista.com/statistics/1267499/assets-under-management-of-swfs-worldwide/.

- O’Meara, S., 2020. China’s plan to cut coal and boost green growth. Nature, 584 (7822), S1–3.

- Paterson, M., 2021. ‘The End of the fossil fuel age’? Discourse politics and climate change political economy. New political economy, 26 (6), 923–36.

- Paul, S., 2016. France’s Engie to shut Australia’s dirtiest power plant. Reuters. https://www.reuters.com/article/australia-power-engie-idUKL4N1D4102.

- Prag, A., Röttgers, D., and Scherrer, I., 2018. State-owned enterprises and the low-carbon transition. OECD Environment Working Papers 129.

- Richardson, B.J., 2011. Sovereign wealth funds and the quest for sustainability: insights from Norway and New Zealand. Nordic journal of commerical law, 2, 1–27.

- Rosenbloom, D. and Rinscheid, A., 2020. Deliberate decline: an emerging frontier for the study and practice of decarbonization. WIREs Clim Change, 11, e669.

- Ørsted. 2019. Taking Action to Stay within 1.5(C. https://orsted.com/en/insights/white-papers/taking-action/orsteds-transformation.

- Schwartz, H.M., 2018. States versus markets: understanding the global economy. London: Bloomsbury.

- Sommerer, T. and Lim, S., 2016. The environmental state as a model for the world? An analysis of policy repertoires in 37 countries. Environmental politics, 25 (1), 92–115.

- Steffen, B., Karplus, V., and Schmidt, T.S., 2022. State ownership and technology adoption: The case of electric utilities and renewable energy. Research policy, 51 (6), 104534.

- Sunio, V., et al., 2021. The state in the governance of sustainable mobility transitions in the informal transport sector. Research in transportation business & management, 38, 100522.

- SWFI. 2019. Chart of the day, sovereign wealth fund assets under management. https://www.swfinstitute.org/news/76389/chart-of-the-day-sovereign-wealth-fund-assets-under-management.

- van ‘t Klooster, J., 2021. The ECB’s conundrum and 21st century monetary policy: how European monetary policy can be green, social and democratic. transformative responses to the crisis series. Finanzwende.

- Vitali, S., Glattfelder, J.B., and Battiston, S., 2011. The network of global corporate control. PLoS ONE, 6 (10), 6.

- Wimbadi, R.W. and Djalante, R., 2020. From decarbonization to low carbon development and transition: a systematic literature review of the conceptualization of moving toward net-zero carbon dioxide emission (1995–2019). Journal of cleaner production, 256, 120307.

- Yom, S.L., 2011. Oil, coalitions, and regime durability: the origins and persistence of popular rentierism in Kuwait. Studies in comparative international development, 46 (2), 217–41.

- Young, K.E., 2020. Sovereign risk: gulf sovereign wealth funds as engines of growth and political resource. British journal of middle eastern studies, 47 (1), 96–116.