ABSTRACT

The growth models approach (GMA) has become increasingly prominent in Comparative Political Economy over the last years. While it has originally been developed for advanced economies, there is a growing number of applications for developing countries. This raises the question of how readily transferable the GMA concepts are to the peripheral capitalist experience. This paper explores the analytical building blocks for an extension of the GMA to developing economies from post-Keynesian-structuralist perspective. It argues that in a developing country context supply-side considerations will be more important and build on structuralist theory to understand the ‘real’ constraints in the developing countries' growth process. It uses Minskyan theory to understand how currency hierarchy creates financial causes for international economic stratification. As a consequence, the role of the state is more crucial than in advanced economies, but at the same time states are more vulnerable. This paper concludes by reflecting on the key concepts of GMA, finance-led, export-led and state-led growth in the light of developing economies and identifying neoliberal as well developmentalist versions of these.

Introduction

The growth models approach (GMA) has become increasingly prominent in Comparative Political Economy (CPE) over the last years (Baccaro and Pontusson Citation2016). It was developed as a response to the Varieties of Capitalism (VoC) approach and builds on post-Keynesian (PK) analyses of demand regimes (Bhaduri and Marglin Citation1990, Lavoie and Stockhammer Citation2013). It develops a demand-side-oriented analysis of trajectories for capitalist economies that gives prominence to distributional conflict and allows for systemic instability. It has highlighted the emergence of debt-driven as well as export-driven growth models. This analytical framework has been developed specifically for advanced economies in the period before the Global Financial Crisis (GFC), but recently there have been some applications of GMA to developing countriesFootnote1 (Nölke Citation2018, Schedelik et al. Citation2021, Akcay et al. Citation2021, Mertens et al. Citation2022). Akcay et al. (Citation2021) apply GDP growth decompositions to several developing countries to analyse whether they follow debt-led or export-led growth models. Schedelik et al. (Citation2021) and Mertens et al. (2021) synthesise GMA and existing CPE analyses of developing economies. Based on selected country studies, they use an inductive approach to identify ideal types. Ramiro Fernandez et al. (Citation2018) critically discuss extensions of the VoC approach to developing countries and counterpose a dependency interpretation, but they do not engage with GMA.Footnote2 These contributions raise the question how readily the GMA concepts and its analytical framework can be transposed to developing countries. Are their experiences and economic structures sufficiently similar? Is their position in the world economy different? How do the core GMA concepts have to be modified to fit the developing country experience?

Developing countries differ structurally from advanced economies in that they are technologically lagging; they are typically characterised by large labour reserves (in a non-capitalist or informal sector), which impact wage growth in advanced sectors; they are sectorally disarticulated in that many intermediate and capital goods need to be imported, thus sectoral spillovers are weak and specific balance of payment constraints often arise. Finally, they have illiquid financial markets, credit rationing is more common (in particular for the informal sector). As consequence exchange rates tend to be volatile and firms and the government have to rely on foreign exchange (FX)-denominated borrowing from abroad. While some developing countries, variably referred to as newly industrialising, semi-peripheral, mid-income or emerging economies (which section 8 relates to state policies), have over some periods experienced high growth rates, overall developing economies (including most emerging markets) have not converged to the income levels of advanced economies (Johnson and Papageorgiou, Citation2020). They specialise in exporting commodities and low-tech manufacturing goods (UNCTAD Citation2021). They also experience more volatile growth, i.e. more pronounced boom–bust cycles (Pritchett Citation2000). An economic foundation of GMA needs to be able to account for these stylised facts.

This paper aims to clarify the macroeconomic concepts and mechanisms relevant to a growth model analysis for developing countries.Footnote3 Its contribution is to fuse insights from PKE and Latin American structuralism and to provide a synthetic framework as a macroeconomic basis for extending GMA analysis to countries of the periphery. PKE is already informing GMA analyses for advanced economies, but not comprehensively so. GMA has mostly used Kaleckian approaches to distribution and growth, while other PK insights, in particular Minskyan theory of financial instability and role of the state in Keynesian theory are underexplored (Stockhammer Citation2022). PKE offers valuable contributions for our understanding of peripheral economies, but it is not enough. Its treatment of the supply side of the economy is not suited for developing economies. It needs to be complemented by structuralism, which offers an analysis of developing economies based on structural differences between core and peripheral economies and the resulting growth dynamics. As exports of developing economies are typically low or medium tech, their growth tends to be weaker than that of advanced economy exports. It suggests that international trade will perpetuate income differences. We argue that PKE and structuralism are complementary. Structuralism (at least in its traditional form) has a focus on production and trade. The PK theory of finance, which highlights the emergence of financial instability, can be extended to explain financial cycles and financial peripheralisation in developing economies and thereby fill gaps in the structuralist approach. On the financial side currency hierarchies emerge, which are expressed in higher interest rates in the periphery but also in pro-cyclical capital flows. Capital flight during a financial crisis will make it more difficult for states in developing economies to play a stabilising role. A PK-structuralist synthesis identifies specific financial as well as productive mechanisms that give rise to a stratification of the global economy. This explains the persistence of differences in income levels as well as larger volatility in growth in the periphery.

For GMA to apply to developing economies, first, supply-side factors (if different ones from those analysed by the VoC) namely the structural specificities of developing economies have to be considered more systematically. Second, the asymmetries in the international economy and the insertion into the global economy play a more prominent role. Third, the previous two points have implications for the potential role of the state for growth and the catching-up process. To enable development, strategic state intervention (in the form of industrial policy, balance of payment management and demand management) will be required. The state potentially has a more important role for late developers, however, states are also in a worse position. The colonial heritage, commodity dependence and financial subordination negatively impact state capacities for developing countries. The analysis requires a re-consideration of central concepts in GMA, namely export-led growth, finance-led growth and the role of the state. A structuralist development strategy includes a form of export orientation (for industrial sectors to grow) and a development of finance (in particular domestic financial deepening). Thus different types of export-led and finance-led growth need to be distinguished, depending on the extent they support domestic industrial upgrading or expose the country to external financial vulnerabilities. Thus neoliberal as well as developmentalist versions can exist and state-led growth deserves more attention.

Two limitations of the scope of the paper need to be clarified. First, as the main argument of this paper is that the macroeconomic analysis of GMA needs to be extended for application to developing economies, it analytically counterposes advanced and developed economies. Thereby it runs the danger of downplaying variation among developing economies, which differ by size (and thus leverage they have with respect to multinational firms that seek market access), by the level of development (developing economies vs. emerging markets), by the specifics of their colonial legacies and along a whole set of other dimensions. This paper operates at a high level of abstraction and uses the juxtaposition to clarify economic mechanisms that are unique or particularly relevant in the peripheral experience such as to derive conceptual conclusions for GMA. Second, many of the arguments presented in this paper could also be explored in the context of advanced economies, in particular the southern European economies. That is beyond the scope of this paper.

This paper is structured as follows. Section 2 presents the GMA. Section 3 introduces PKE and Section 4 structuralism. Section 5 presents core and periphery polarisation based on production and trade. Section 6 analyses how currency hierarchy and financial flows along PK lines can lead to international stratification. Section 7 discusses the role of the state. Section 8 reconsiders core concepts of GMA. Section 9 concludes the paper.

Growth models: the state of the debate and applications to the periphery

The GMA builds on post-Keynesian Economics (PKE) to understand the growth and political economy dynamics in advanced economies. Since this publication by Baccaro and Pontusson (Citation2016), it has had a substantial impact in the field of CPE, which seeks to explain the differences in institutions and economic performance across countries (Hassel and Palier Citation2021, Baccaro et al. Citation2022). The field used to be dominated by the VoC approach which emphasises supply-side factors such as labour relations system and financial structures as sources of comparative advantage. Since the GFC criticism of the VoC approach has intensified and Baccaro and Pontusson (Citation2016) build on PK analyses of demand regimes and growth models (Bhaduri and Marglin Citation1990, Lavoie and Stockhammer Citation2013) to propose a distinction between export-led (Germany), consumption-led (UK) and some intermediate cases (Sweden and Italy). It uses PKE to provide a macroeconomic basis that focuses on the demand side, allows for demand effects of changes in income distribution and for instability of the growth process. Baccaro and Pontusson go beyond the PK approach in that they combine it with a political economy analysis of (sectoral) producer groups associated with the different growth models in a Gramscian notion of a historic bloc. Their ambition is broader than PKE: explaining national political economies, whereas PKE discusses demand regimes, i.e. a specific economic feature of these national political economies. That is reflected in a shift in terminology from ‘demand regimes’ to ‘growth models’.

GMA has since been extended in various directions and offers a richer analysis of social and political aspects of GMs and considers forces emanating from the international sphere (Schwartz and Blyth Citation2022), but the macroeconomic core and in particular the centrality of the export-led vs. debt or consumption-led growth models distinction remains at the centre (Baccaro et al. Citation2022).Footnote4 Some case studies append the growth models to include FDI-led growth or commodity-driven growth (Ban and Adascalitei Citation2022, Sierra Citation2022), but that is without a general reconceptualisation of the growth models and their identification.

The PK demand regime analysis on which GMA builds stems from attempts to build macroeconomic Marx–Keynes synthesis models that clarify when wage-led (Kaleckian) or profit-led (Marxian) demand regimes arise (Bhaduri and Marglin Citation1990). This framework has subsequently given rise to a rich empirical literature that tries to econometrically identify distribution-led demand regimes (e.g. Hein and Vogel Citation2008, Stockhammer et al. Citation2009, Onaran and Galanis Citation2014). While the demand regimes analysis at first focussed on distribution as the core explanatory variable, financial factors have since gained prominence. For example, Stockhammer and Wildauer (Citation2016) document that for many countries (the debt-driven growth models) the growth in house prices and borrowing has become a major driver of growth (see also Hein Citation2012).

As of now, the GMA framework is shaped by the boom period before the GFC, for which it was originally developed. The distinction between debt-driven and export-driven growth models has been particularly useful for that period and to understand the origins of the GFC. However, the question arises whether these concepts can form a general framework for CPE. From a PKE perspective, we note two shortcomings of the GMA. First, the treatment of finance in GMA is highly uneven. A core feature of PKE is a distinct theory of financial instability and financial cycles (see Section 3), which is not captured in most versions of GMA. Second, the treatment of the state does not correspond to the potentially critical role of government policies in PKE. For example, Hübscher and Sattler (Citation2022) subordinate fiscal policy to the growth model. Thus conceptually, the state is not considered as playing an independent role in determining the growth model. Kohler and Stockhammer (Citation2022b) highlight that PK macroeconomics allows for a richer variety of potential demand drivers and empirically demonstrates that differences in housing cycles and fiscal policy have played a key role in explaining differences in growth performance since the GFC.

From a developing country perspective, two other shortcomings stand out. First, GMA only offers a casual treatment of the supply side. In part, this may be due to a desire to contrast with the exclusive supply-side focus of VoC, in part because, arguably, in the pre-GFC period the main differences between advanced country experiences were not along supply-side lines nor were these the source of instability. However, the neglect of the supply side is a conceptual weakness for a comprehensive approach, which is all the more important for the analysis of developing economies. Section 5 will take the structuralist approach as the starting point for an analysis of peripheral economies. Second, there is a question whether the treatment of the relation of national growth models to the international regime does justice to the particular challenges developing countries experience. This includes both the international production and the financial system. Section 6 will draw on a Minsky approach to currency hierarchy to address the financial aspect of this.

While GMA so far has mostly been used to analyse advanced economies, there is a growing number of applications to developing economies.Footnote5 Akcay et al. (Citation2021) stay close to the analytical framework of Hein and Mundt (Citation2013). Based on an analysis of GDP growth decompositions (into private consumption, investment, net exports and government consumption) and sectoral balances (i.e. the extent to which households, business and the state are accumulating debt) for eight developing economies they find, for the post-GFC period, that Argentina, Brazil and India are domestic demand-led with high public debt, South Africa and Turkey (private) debt-led demand regimes and China, Mexico and Russia having forms of export-led growth. Compared to the pre-GFC period, they report a shift towards domestic demand-led regimes whereas advanced economies moved towards export-led regimes.

Tan and Coran (Citation2022) and Sierra (Citation2022) are two case studies on China and Latin American countries respectively. Both extend the GMA to suit the cases. Tan and Conran argue that China had a hybrid of an export-led growth model in the coastal area and a state-led model in the interior. These are in an uneasy balance, with one dominating at different periods, but both having different regional and distributional implications. Shifts in the balance are often the result of external developments, such as East Asian crisis or the GFC. Tan and Conran (Citation2022) also highlight tensions between the two. Sierra (Citation2022) analyses the Latin American experience as a case of commodity-driven growth, without fully clarifying how that would be identified, and explores the political obstacles to a regime shift, namely the role of elites associated with commodity exports.

Nölke (Citation2018), Schedelik et al. (Citation2021), Mertens et al. (2021) take some inspiration from GMA, but are strongly rooted in institutional analysis. Closer to the structuralist focus, Nölke (Citation2018) counterposes dependent and state-permeated models, which represent different strategies to deal with developing economies subordinate role in the world economy. ‘Whereas [dependent market economies] embrace foreign economic integration wholeheartedly, [state permeated economies] put a strong premium on national control and long-term stability’ (Nölke Citation2018, p. 279). The Visegrad countries are used to illustrate the former; China and India for the latter. Brazil is analysed as a less successful intermediate case.

More eclectically, Schedelik et al. (Citation2021) propose to group countries along the two axes of open/protected economies and exhibiting positive/negative institutional complementarities, which results in dependent, state-permeated, hierarchical and patrimonial models. While they have positive references to GMA, analytically their categories are only weakly related. Mertens et al. (Citation2022) is the most ambitious attempt to synthesise previous comparative capitalisms research and the GMA. It offers a growth decomposition analysis as well as an institutional analysis for major emerging economies (with a focus on China, Brazil and India). It distinguishes between wage-based (Brazil) and debt-based (South Africa) consumption-led growth, commodities-based (Brazil, Indonesia) and manufacturing-based (Korea) export-led growth; and FDI-based (Mexico) and domestically-based (China) investment-led growth (Mertens et al. 2021, Table 2). We will return to these categories in Section 7. They note that emerging economies differ from advanced economies in that investment is a more important growth component, international dynamics (FDI flows, commodity prices cycles) are more important, the embeddedness of economic actors in the political sphere differs and some emerging markets display a high degree of internal heterogeneity.

This paper relates positively to all of these but goes beyond them. Compared to Akcay et al., we highlight the specific structures and positions of peripheral economies; compared to Tan and Conran and Sierra our reconsideration of GMA is more conceptual; compared to Mertens et al. we seek to reconsider the applicability of the widely used GMA categories more explicitly.

Post-Keynesian economics

Keynesian economics was a response to the protracted (European) economic problems of the 1920s and the Great Depression of the 1930s in the global north. Post-Keynesians interpret Keynes’ work as a break from neoclassical theory and tie PKE back to classical political economy and a class analytical approach. Thus PKE builds on but goes beyond Keynes.Footnote6 It rejects methodological individualism and instead bases its analysis on social norms, conventions and social structures, in particular the class structure of a society. Keynes argued that in the face of fundamental uncertainty people rely on simple behavioural rules (often called heuristics). These will involve social comparisons and norms and may be abandoned in times of crisis. This can lead to herding behaviour during booms and abrupt changes in times of crises. Income distribution and power relations play an important role in PKE. Income distribution is regarded as based on the bargaining power of labour and the market power of firms. An important feature of PK economic models is that working-class households have a higher propensity to consume than households with capital incomes.

The macroeconomic core of PKE is the theory of effective demand and involuntary unemployment. This asserts that changes in economic growth are (mostly) driven by demand factors, i.e. spending decisions, rather than on slowly changing supply-side factors like technology or the flexibility of product and labour markets. Investment spending (arguably the most important variable driving the business cycle) depends on non-rational factors (‘animal spirits’) and financial factors like credit availability. Autonomous expenditures, such as private investment or government spending, will lead to a multiplier process that generates income.Footnote7 PK theory of money and finance emphasises the emergence of endogenous (systemic) financial instability. PKE also posits that supply will, at least in advanced economies, respond to demand pressures, which give rise to path-dependent growth.

PK theory of financial instability and financial crises is in particular associated with the work of Hyman Minsky, the pioneer of the Financial Instability Hypothesis (Minsky Citation1986). One feature of the Minskyan approach is to analyse businesses and households, as well as banks, in terms of their liabilities. Investment (whether in productive capacity or in financial assets) usually requires additional liabilities (such as loans). Leverage will typically increase in the course of a boom, which creates the seeds for overindebtedness and busts. Assets differ in their degree of risk and liquidity and riskier assets have to provide higher interest rates. Importantly the risk premia will change over the business cycle. During the boom, the business outlook will become more optimistic and thus risk premia will decline; during a crisis, when investors panic, there will be a flight to safe and liquid assets and thus the interest rates will increase sharply (in Keynes this is the increase in the liquidity preference). Minsky’s approach is important for understanding advanced economies as it helps understand the systemic and cyclical nature of financial booms and busts as well as their severity. But Minsky’s theory also has important implications for developing economies and their position in the international financial hierarchy (see Section 6).

PKE argues that supply-side factors, in particular technology and consequently productivity growth, will respond to some extent to demand pressures. In other words, technological progress is induced rather than exogenously given. While at any point in time, there will be specific supply-side constraints to growth (say, a given stock of factories or a given set of production technologies), but these constraints are over longer periods elastic: investment spending leads in an increase in productive capacity and high demand growth will be conducive to technological progress (e.g. Dutt Citation2006, Fazzari et al. Citation2020 for more formal discussions of these themes).Footnote8 The important implication of induced technological progress is that it gives rise to a path-dependent growth process rather than one with demand-induced short-run fluctuation around a supply-side-determined growth trend. This means that recessions leave long-lasting scars and recoveries will be weaker after severe crises rather than stronger (Cerra and Saxena Citation2008). Thus countercyclical policies not only stabilise the business cycles but also improve long-term growth.

Keynesianism has an elaborate theory of the impact of government activity, in particular of fiscal and monetary policy, on economic growth. At the core of that is the concept of the fiscal multiplier, which posits that in economies with unemployment, i.e. in particular in a recession, deficit-financed government spending will have positive impact on the private sector with substantial second-round effects. Thus fiscal multipliers in a crisis are expected to be substantially above one. The impact of monetary policy, nowadays mostly performed via interest policy, is asymmetric over the business cycle in that higher interest rates during a boom will slow down growth, but during a crisis, in particular a financial crisis when a flight to safety has set in, interest rates will be insufficient to ignite growth. PKE, however, has little to say on what determines actual economic policies. Thus, while PKE analytically provides the basis for a notion of state-led growth via fiscal policy as a driver of growth, it does not offer a theory to understand when state-led growth will materialise as a growth model.

Latin American structuralism

Latin American structuralismFootnote9 was informed by the peripheral experience of the 1930s, where Latin American countries, due to the breakdown in world trade, experienced a form of import-substituting industrialisation. It formed in the 1950s and 60s around CEPAL with Raul Prebisch the leading proponent. Structuralists build on Keynesian insights, adapt them in the light of the challenges faced by peripheral economies and offer an institutionally and historically motivated approach that emphasises the colonial legacy of the periphery. It questions liberal orthodoxy in particular as regards the benefits of international trade. At the core of this approach are differences in the internal economic structures in developing economies and in advanced economies, which result in differences in how they relate to the international economy. The interaction of these different economies gives rise to processes of divergence that prevent developing countries from achieving the (per capita) income levels of advanced economies; i.e. they fail to converge. First, developing countries typically have a dual economy with a large non-capitalist sector (agriculture or the informal sectors), which provides a pool of hidden unemployment, and a more advanced (capitalist) sector. Second, developing countries are technologically lagging and thus need to import advanced machinery, in particular capital goods. This, third, leads to a disarticulation of the economy in the sense that spillovers between sectors are limited as key products have to be imported. Fourth, as a consequence, the main export goods will be either commodities or low-tech industrial goods. Fifth, this need for imports leads to a particular constraint in terms of foreign exchange as capital goods, which are essential for the growth process, need to be imported. As will be discussed in more depth in Section 5, these stylised facts will lead to forces of divergence in the world economy.

Structuralism has influenced, but is distinct from, dependency theory and world systems theory. The latter has occasionally overshadowed the former, thus a clarification will be helpful. Following Kay (Citation1989), we regard structuralism as an economic theory that takes as starting point structural differences between the economies of advanced and developing countries and aims to derive specific policy suggestions for development; dependency theory as a political economy approach that builds on structuralist economics but is more concerned about political and social dynamics and is often more sceptical about state abilities to foster development. World System Theory pushes the divergence argument further and ascribes primacy to the world system and thus sees limited scope for states. Thus there is a substantive difference between World System Theory, dependency theory and structuralism in particular regarding the role of the state. This paper builds on structuralism and is consistent with dependency theory.

Structuralism is consistent with PKE and the two are complementary in that their main focus is on developing and advanced economies respectively. Theoretically, both are based on a (non-Marxist) class-analytic political economy approach. Both share a scepticism about the social efficacy of the market mechanism and an emphasis on the potential of state intervention. There are differences in emphasis: PKE has a focus on the demand side of the economy whereas structuralism has much more focus on the supply side. As the following section discusses in more depth, structuralism elaborates its supply-side considering constraints that are particularly relevant for developing countries. In line with its demand side focus, PKE has a more elaborate theory of finance, which is important for developing countries (Section 5). Not all post-Keynesians and structuralists would necessarily agree that a PK-structuralist synthesis is desirable (or possible), but a substantial number of contemporary structuralist-inspired authors such as Taylor (Citation2004), Vernengo (Citation2006), Ocampo et al. (Citation2009), Porcile and Yajima (Citation2019) move in a similar direction.

‘Real’ causes of divergence: technological capabilities and export dynamics

The structuralist starting point is in the differences in economic structures between developing and advanced economies (Prebisch Citation1950; for formal discussions, see Blecker Citation1996 and Cimoli et al. Citation2010). As these structural differences are on the supply side,Footnote10 it may at first seem at odds with the Keynesian focus on demand-led growth, however, structuralists derive the implications of these structural differences for demand formation and analyse specific demand constraints. Supply-side differences matter, because they give rise to different demand dynamics. Developing countries typically have large hidden unemployment in agriculture or informal employment. Thus economic growth will not necessarily lead to general wage growth, which breaks part of the induced technological progress mechanism in PKE. They are technologically behind the advanced economies, which mean that they cannot produce up-to-date capital goods (machinery) themselves, but have to import them. This means a foreign exchange shortage (rather than domestic demand) can constrain the growth process and technological progress.Footnote11

At the core of the structuralist research program is the assertion that the interaction of core and peripheral economies will result in divergent dynamics that lead to asymmetric outcomes of international trade. Starting from the stylised facts that developing economies need to import capital goods. The balance of payment represents a specific constraint as it directly impacts the growth of the economy. Structuralists highlight two ‘real’ (i.e. production and trade-related) mechanisms that can give rise to divergence. The first is developed in Thirlwall’s balance of payment constraint growth model (Thirlwall Citation1979, Citation2019). The current account equilibrium requires that the value of imports equal the value of exports. If we abstract from capital flows and assume a given exchange rate, exports will depend on the growth rate of demand, which in turn will depend on the rate of economic growth of the trade partners (here: developed economies). Imports, on the other hand, will depend on the growth of domestic growth. Thus the equilibrium growth rate of the developing country will depend on the growth rate of the centre times the export elasticity over the import elasticity (an export elasticity is the change in exports induced by a change in economic growth in the trade partner).Footnote12 That simple statement will be correct for any country (if the current account is balanced). However, advanced economies typically export high-tech manufacturing goods, which have a relatively high-income elasticity, i.e. as income increases, the demand for high-tech manufacturing goods will increase dynamically; developing countries export primarily commodities, agricultural and low-tech manufacturing, which typically have low-income elasticities, i.e. the demand for these goods is less dynamic than economic growth. Thus this simple model suggests divergence between centre and periphery as developing economies would need to grow faster than advanced ones for convergence, but that will be ruled out by the different values of export and import elasticities (Dutt Citation2002). The Thirlwall model has been used to develop a growth theory (see Blecker Citation2016 for a critical survey), however, as it sidesteps capital flows and exchange rate movements, it is better regarded as a useful illustration of how equilibrium growth between regions with different degrees of development can differ rather than a comprehensive growth model.

The second mechanism focuses on price developments, namely on the terms of trade (export prices relative to import prices). This had been a major concern for the early structuralists, who argued that the terms of trade were shifting at the expense of developing countries (the so-called Prebisch-Singer hypothesis).Footnote13 In part, this is due to the demand dynamics of exports and imports discussed above, in part due to the higher market power of firms in the global north.Footnote14 These movements of the terms of trade would take place over long periods, and indeed, this seems to be the case. However, in recent debates on commodity dependence, the focus has shifted to a medium-term time horizon and documented that commodity prices exhibit periods of sustained growth as well as decline, i.e. they have a cyclical nature. This cycle is longer (20–50 years) than the regular business cycle and referred to as ‘commodity super cycle’ (Erten and Ocampo Citation2013). In the upswing, they will outperform industrial goods and fall more strongly during the downturn. This means that commodity dependence can have positive effects on the upswing of the long cycle; thus peripheral countries will be tempted into commodity exports for extended periods. However, over longer periods commodity dependence will not come with industrial upgrading, but trap countries in a medium-income position.

The arguments presented here are macroeconomic. They complement the literature on global value chains, which highlights how production processes get sliced and organised in different countries and under different organisational forms, which typically come with siphoning off profits to the centre (Gereffi et al. Citation2005; Milberg and Winkler, Citation2013). This literature highlights that sustained growth requires an effective linking of local firms to global value chains. The global value chains literature is comparatively micro (and meso) economic and indeed often is more focussed on explaining interfirm and supply relations than on macroeconomic outcomes. The main implication of the structuralist divergence for GMA is that it has to account for commodity dependence and the extent to which technological developments trap economies in a low equilibrium due to the properties of its export sectors.

Financial causes of divergence: currency hierarchy and capital flows

While structuralist theory (developed in the financially relatively stable Bretton Woods era) has its focus on ‘real’ factors, financial factors feature prominently in PKE. PKE also provides an analysis of financial factors that structure the international political economy: the theory of currency hierarchies (de Paula et al. Citation2017, Bortz and Kaltenbrunner Citation2018). We will present a version that highlights Minskyan features. One part of the structural differences between developing and advanced economies is that the former have weaker, less liquid financial markets.

PK theory of a hierarchy of money posits that financial instruments further down from the apex require higher rates of return. In the sphere of international finance this means that the currencies of different countries occupy different places in the hierarchy. Usually, a single currency or limited number of currencies plays the role of international top currencies, which serve as ‘safe assets’ of the international system. These need to be widely available and have liquid markets. Conversely, currencies at the bottom of the hierarchy will be more volatile and have (assets with) higher interest rates. Such a hierarchy is self-reinforcing. As top currencies have low-interest rates (in the international context), financial actors will want to issue debt in this currency and thus will need liquidity in this currency. The higher interest rates and exchange rate volatility create a disadvantage for the peripheral business sectors.

The theory of currency hierarchy also has important dynamic implications, which brings us to the issue of financial instability. As interest rates are lower in centre currencies, there is an incentive to borrow in FX. During a boom when debt ratios are rising, for developing countries this typically means that foreign-denominated debt will rise (the inability of developing countries to issue domestic currency-denominated debt is often referred to as ‘original sin’).Footnote15 This FX-denominated debt poses important challenges for developing countries as financial flows have a pronounced cyclical pattern. In times of a boom, finance will flow in (resulting in an appreciation of the currency); in times of financial crises, when a ‘flight to safety’ sets in, financial flows will move out of the developing country towards the centre. These capital flows are pro-cyclical both with respect to the domestic economy (i.e. amplifying the domestic boom) and with respect to the international (or US) financial cycle (i.e. importing the international cycle). Thus two types of vulnerabilities arise. First, a financial cycle that emerges from the interaction of domestic activity (say, an investment boom) and international capital flows arise. The capital flows (pro-cyclical with respect to domestic growth) amplify the boom, but reverse sharply when the economy slows down (e.g. Kohler Citation2019, Kohler and Stockhammer Citation2022a). This pattern is akin to the one of the East Asian financial crisis, where the booms in developing countries were based on sound fundamentals (i.e. high productivity and export growth), attracted capital inflows and with the sudden stop and sharp depreciation the real debt burden increased (as debt was in foreign currency, but income in domestic currency, which had just become devalued) and led to sharp recession (Arestis and Glickman Citation2002).

Second, financial globalisation exposes developing economies to the global, i.e. US centred, financial cycle. A shock in the centre will lead to a flight to safety and capital flow reversal from the developing economies for reasons unrelated to the developing economies themselves. This is the type of dynamics that is emphasised in the work of Helene Rey (Citation2013) and is illustrated in the immediate aftermath of the GFC but also in the spring 2020 at the onset of the covid crisis. Aldasoro et al. (Citation2020) highlight that these two cycles have different periodicities, with the global financial cycles being shorter than the domestic financial cycles cum capital inflows.

This has important implications for both states and firms in developing economies. For both, it means that when they need it most, they face difficulties in external financing. For the state that means that they are limited in their ability to perform their stabilisation role (countercyclical budget deficits to stabilise demand in a recession).Footnote16 But governments, aware that a sharp devaluation will cause a debt crisis for business and that a devaluation will be perceived as a sign of weakness, try to stabilise the exchange rate, which typically involves austerity policies. For firms, this reinforces pro-cyclical growth dynamics. Firms face easier access to foreign credit during the boom and in the crisis, credit constraints are biting and the real debt burden will increase because of devaluation. The two put together mean that the cyclical dynamics will be more pronounced in the periphery.

The state: more important, yet weaker

The previous sections have shown how a PK-structuralist approach analyses private sector dynamics and offers simple and plausible real as well as financial mechanisms that will give rise to divergent performance of centre and peripheral economies. Actual economies are mixed economies and states can shape economies. PKE and structuralism are part of long-standing tradition in economic theory and history that emphasises the potential of the state to shape economic development. This goes back to List and Gerschenkron’s emphasis on the role of the state for late developers (Gerschenkron Citation1962, Allen Citation2017, Chapter 6, Weiss and Hobson Citation1995). Following the success of East Asian economies, the concept of the developmental state became widely used. Developmental states typically entail industrial policy and management of international trade and creating financial institution to enable the growth of strategic sectors. This is flanked by education policies and infrastructure projects (e.g. Amsden Citation1989, see Haggard Citation2018 as an overview). This suggests a notion of state-led growth, which is currently absent from GMA.

At the same time, state capacities are more limited in peripheral economies. A major part of this is the colonial legacy. Colonialism meant the destruction of indigenous state structures and the building of extractive institutions,Footnote17 which included authoritarian states, but also highly unequal land ownership structures, which generated powerful interest groups that use the state to extract rents (from commodity exports) rather industrialisation. This is reflected in the political economy literature on patrimonial or predatory states (Evans Citation1989, Kohli Citation2004) and the resource curse. It is probably no coincidence that the first non-European area to industrialise was Japan, which had not been colonised. European economies industrialised with internationally and internally strong state, often based on capitalist involvement in state elites (Tilly Citation1990, Vries Citation2015, Chapter 1).

There are also contemporary political and economic forces that constrain state activities. US hegemony and World Bank and IMF conditionality are important parts of that. That is epitomised in the Washington Consensus that effectively outruled developmental policies (except for education). The state also faces multinational corporations that are larger and more powerful than domestic capital. These political factors are reinforced by financial factors. Peripheral states have only a limited ‘monetary sovereignty’. Their currencies have a subordinate role in the international financial systems; its financial systems are weak. They tend to face capital outflows during crises, which makes state intervention more difficult when it is needed most, and put pressure on them to pursue pro-cyclical austerity policies.

Short, in peripheral countries the state has an important role in enabling development, but at the same time they have more limited state capacities. Actual states and their policies differ widely. It is useful to think of them on predatory to developmental spectrum and there is an extensive literature on country studies, with the contrast between the African, Latin American and East Asian frequently used, with east Asian cases on the development side, African ones on the predatory one and Latin America intermediate (e.g. Evans Citation1989). The reasons for the Asian success story feature the far-reaching land reforms that disempowered rentier elites (Kay Citation2002) and relatively and autonomous state that was nonetheless socially embedded with good links to business groups (Evans Citation1989, Kohli Citation2004). State policies were thus crucial in the emergence of an intermediate layer of economies that have variably been referred to as semi-periphery, newly industrialising countries, mid-income countries or emerging economies.

Reconsidering GMA’s core concepts: neoliberal and developmentalist growth models

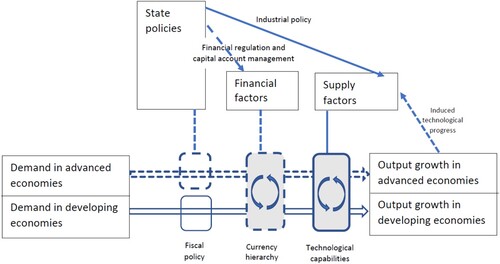

The previous sections have analysed the forces of cross-country divergence that will emerge from international trade and international finance. summarises this graphically. PKE focuses on advanced economies; its main mechanisms are represented in broken lines. As regards the interaction of advanced and peripheral economies, financial factors give rise to a currency hierarchy that impacts the growth path (through financial flows, interest rates and the exchange rate) in advanced and developing economies. Supply is regarded as adjusting in the medium term. Structuralism focusses on developing economies; its main mechanisms are depicted as solid lines. It highlights supply-side factors such as technological capabilities that impact, e.g. the export elasticities and thus the interaction of growth (and its volatility) in the centre and the periphery. The state has a direct impact on demand but also shapes the supply side (via industrial policy) and the financial sector (via capital account management and financial regulation). This section will reconsider the central concepts of the extant growth models literature in the light of the circumstances of developing economies.

Figure 1. Post-Keynesian and structuralist mechanisms for core-periphery divergence.

Key concepts of GMA like export-led and finance-led growth models are now mostly used descriptively. In the original PK analyses, this was done with a critical undertone. In Lavoie and Stockhammer (Citation2013), export-led and finance-led growth models are analysed as part of a neoliberal regime. The Fordist period is analysed as a (statist and) wage-led growth model. Neoliberalism has, through a series of policy measures, transformed the institutional basis, but still exhibits wage-led demand regimes (in large economies). Thus increasing inequality does not itself generate growth, but additional stimulation via financialisation or exports is needed. Moreover, PK analysis highlighted the inherent instability in both growth models: finance-led growth models rely on growing household debt, export-led growth models on increasing international trade imbalances. In the context of developing economies, neoliberalism took the form of the Washington Consensus (e.g. Rodrik Citation2006), which involved capital account liberalisation, free trade and a restriction of state activities.

To highlight potential pitfalls in growth model identification, it will be useful to outline a structuralist development strategy. Such a strategy would involve selective protectionism (import restrictions and export support), it would involve state spending on infrastructure and education; use of development banks to support (selective) private investment; a management of the capital account, in particular restrictions of capital inflows, and of the exchange rate (to support exports and discourage import of consumption goods). Depending on the relative weights of these ingredients, a structuralist growth model may exhibit features of export-led growth or of a finance-led model if development banks succeed in enabling large-scale (private) investment; or they may constitute a distinct state-led growth model. Thus there are different versions of export and finance-led growth models. thus reconsiders the core concepts of GMA for developing economies in the light of different development strategies.

Table 1. Two faces of growth models.

First, export-led growth takes on a somewhat different meaning for developing economies because of the specific supply-side context. While in advanced economies, an export-led strategy is often associated with domestic demand restraint and free-riding on external demand (say the case of Germany), for developing countries industrialisation and growth of manufacturing will almost by definition require export orientation (as domestic markets will often be too small).Footnote18 Export-led growth thus may take on a more positive meaning, if it is based on industrial goods as export growth will to some extent be necessary condition for upgrading. These might be called Kaldorian exports.Footnote19 The east Asian and Chinese experience is an illustration of this. However, not every export orientation will lead to upgrading. Export-led growth based on commodities in line with developing countries’ comparative advantage is not in general linked to upgrading (and might be called Ricardian exports). But this is amplified by political economy effects of the resource curse in commodity-dependent economies (as discussed in Sierra Citation2022). An important distinguishing line between ‘good’ and ‘bad’ export-led growth is the extent to which there are spillovers to other productive sectors, i.e. to what extent exports lead to productivity growth in other sectors.

There are two closely related concepts to the neoliberal version of export-led growth. FDI-led growth is used by Bohle and Regan (Citation2021) for Ireland and Hungary. They mostly analyse the politics of this hypothesised growth model. They regard investment and productivity growth as driven by FDI. Closely related, Nölke and Vliegenthart (Citation2009) proposed the term ‘dependent market economy’ for central and eastern European economies. They lean more heavily on VoC and identify them via the strong share of FDI for investment and productivity growth and transnational control of corporate governance (in the context of institutional complementarity). Both Bohle and Regan and Nölke and Vliegenthart analyse only successful cases and do not provide general criteria of identification. In particular, they presuppose MNC-internal transfer of technology and investment and consequently sectoral or aggregate productivity growth is driven by FDI.Footnote20 However, FDI does not necessarily lead to economic growth (or productivity growth): it can crowd in or crowd out domestic investment (Misun and Tomsik Citation2002, Menzinger Citation2003, Agosin and Machado Citation2005).

Second, there is an ambiguity about the role of finance and thus ‘finance-led’ growth. Debt-driven growth models will have a stronger international dimension in peripheral countries (indeed they also had a strong international dimension in advanced economies), but these are amplified by FX-denominated debt and by the fact that capital inflows are likely to be more cyclical. And indeed many developing countries have experienced boom–bust cycles driven by volatile capital inflows. However, weak (domestic) financial sectors and high-interest rates (in line with the currency hierarchy argument) are a substantial constraint for growth in many developing countries. Thus a successful development strategy would have to provide (additional) credit to domestic firms and to those sectors that are to be grown strategically. Thus a structuralist strategy would also come with some growth of the financial sector. Therefore we need a distinction between production-oriented finance and speculative or consumption-oriented finance (e.g. Samarina and Bezemer Citation2016). The basic distinguishing line is, first, to what extent finance-led growth leads to business investment vs. to what extent it leads to consumption growth, and, second, to what extent finance-led growth comes with external vulnerabilities (i.e. high level of FX debt and of short-term FX liabilities).

Third, state-led growth will have to be considered for developing economies, where ‘state-led growth’ denotes policies in the spirit of a Keynesian and developmental state.Footnote21 The concept of state-led growth has not been elaborated in GMA. This presumably is due to the pre-GFC context in which GMA was developed. Kohler and Stockhammer (Citation2022b) hint at a demand-oriented notion of state-led growth to explain differences in performance across advanced economies since the GFC. Tan and Coran (Citation2022) use the term (for the interior parts of China) and identify government infrastructure investment as the key variable. For developing economies state-led growth will have a strong supply-side dimension and presumably would cover state investment, state-sponsored financial institutions such as development banks and industrial policy. In contrast, the widely used practice of identifying growth models via GDP growth decomposition uses government consumption as the key measure of aggregate demand attributable to the state. This is essentially a measure of government employment and is neither adequate to capture state-led growth from the demand side nor from the supply side. Establishing the concept of state-led growth will thus require a reconsideration of how growth models are identified empirically.

While the exposition in is derived from our theoretical discussion, it has close relatives in the applied literature. Nölke’s distinction between market-permeated and state-permeated development models comes close to the neoliberal vs. developmentalist growth models. Interestingly, some of the extant empirically oriented literature has in fact, if undertheorised, made steps towards similar classification. Mertens et al. (Citation2022) distinguish commodity-based and manufacturing-based export-led models, which are similar to our Ricardian and Kaldorian exports; and they differentiate between FDI-based and domestically-based investment-led growth. The terminology is rather different here, but the main example of domestically-based investment-ledFootnote22 growth is China and analysed by Mertens et al. as state-led, thus bringing it close to state-led growth in . Akcay et al. distinguish between domestic demand-led economies that are based on private debt growth and those based on public debt growth. They mention potential macroeconomic differences between the two (public debt can have countercyclical effects; private debt tends to be pro-cyclical), but do not develop this is into a systematic theory of different growth models, nor do they consider the supply-side dimension. Short, the juxtaposition in can be regarded as a theoretical framing of existing empirical classifications.

Conclusions

This paper has asked whether GM analysis is applicable to countries in the global south and how it would need to be adapted. The macroeconomic basis of GMA for peripheral economies needs to be able to account for persistent differences in income levels and higher growth volatility. We have argued that PKE and structuralism are complementary. Structuralism highlights how different economic and productive structures in peripheral economies can lead to divergent growth trajectories that trap them in commodity and low-tech exports with weak growth potentials. PKE highlights financial instability and offers an explanation of the emergence of currency hierarchies. Financially peripheral economies will be exposed to capital inflows which exacerbate economic instability.

Our analysis thus identifies ingredients for an extension of GMA to developing economies as well as conceptual challenges for GMA. It will have to take supply-side factors and an economy’s position in the international productive and financial pecking order more seriously than it currently does. First, external economic factors will be more important than advanced economies. An analysis thus should start with identifying the position of a country in both productive and financial structures. This includes questions about the leading export sectors and the respective growth prospects, the technological sophistication of these. One key question here is the issue of commodity export dependence. Commodity dependence will have cyclical dynamics as primary commodities will have higher price volatility than industrial goods and, specifically, will often exhibit strong cycles. Second, is the question of integration into the international financial system. This involves questions of the extent of foreign currency-denominated debt and how sensitive the country is to financial inflows and international financial shocks. Third, the question of state capacities. More so than in centre countries the question is about what states can do (as opposed what is politically feasible). As a result, GMA needs to consider a broader set of potential growth models, in particular, the possibility of state-led growth and it needs to analyse the links between demand and supply factors more explicitly. Export-led and finance-led growth models may exist in neoliberal as well developmentalist incarnations.

Acknowledgements

Earlier versions of the paper have been presented at the The Second Workshop of the Growth Models in the Global South Studies Network and the International Political Economy Research Group at KCL. This paper has benefited from comments by Guen Anzolin, Bruno Bonizzi, Alexandre de Podesta Gomes, Karsten Kohler, Ian Lovering, Christian May, Andreas Nölke, Özlem Onaran, Michael Schedelik, Esra Ugurlu and two anonymous referees. The usual disclaimers apply.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Engelbert Stockhammer

Engelbert Stockhammer is Professor of International Political Economy at the Department for European and International Studies at King's College London, UK.

Notes

1 The terms developing economy, peripheral economy and global south are used synonymously.

2 They refer to dependency theory rather than structuralism. However, as Ramiro Fernandez et al. complement their analysis of divergent forces in the world economy with an emphasis on state involvement, implying that effective state policy can substantially counteract divergent forces, this is a minor difference. Different from Ramiro Fernandez et al. this paper situates the argument explicitly in the debate around the GMA.

3 It thus complements Stockhammer (Citation2022), which provides a PK foundation for GMA for advanced economies.

4 Much of the GMA work identifies growth models by means of a decomposition of GDP growth into its constituent components (i.e. consumption, investment and net exports), but Kohler and Stockhammer (Citation2022b) point out that this can give misleading interpretations for the post-GFC period. PK macroeconomics suggests a more careful distinction between movement in the key growth drivers and the demand regimes that mediate their economic impact (Stockhammer and Onaran Citation2022, 61–64).

5 The following discussion focuses on the literature that explicitly builds on GMA. There is a wider literature on the CPE of developing economies (among others Schneider Citation2009, Carney Citation2016), which devotes little attention to questions of demand formation.

6 An overview of PKE for political economists can be found in Stockhammer (Citation2022). See Lavoie (Citation1992) as an introduction and King (Citation2002) for a history of PKE.

7 An important difference to standard economics is that PKE does not pose a universal market clearing process for all markets. In particular, in the labour market wage flexibility will not usually cure involuntary unemployment: a wage cut in a recession (i.e. in response to unemployment) will lead to a reduction in consumption expenditures as wages are the main source of income for most households. This mechanism is at the core of the wage-led demand regime.

8 Specific forms of induced technological progress include learning by doing and various forms of economies of scale such as network effects and spill overs.

9 We will use the term ‘structuralism’ for Latin American structuralism. Dutt (Citation2019) highlights that there was also a European and American structuralism (including Singer, Myrdal and others). The distinction is not important for the argument of this paper. Kay (Citation1989) and Fischer (Citation2015) give overviews; Prebisch (Citation1950), Furtado (Citation1965) and essays in CEPAL (Citation2016) are seminal contributions; Ocampo et al (Citation2009) is a recent text book.

10 The structuralist analysis can also be read as giving specific reasons why the supply-side effects postulated by PKE may not materialise in developing economies.

11 These arguments are in principle relevant for any countries and often gives rise to divergent growth paths and poverty traps. Thus some analyses of the Euro crisis build on structuralist arguments (e.g. Storm and Naastepad Citation2015, Gräbner et al Citation2020).

12 More formally: assume imports (M) depend on domestic GDP (Y) and exports (X) depend on world demand (YW). We abstract from exchange rate and price changes. Thus the import and investment functions are M= m0 + eYMY and X = x0 + eYXYW. The balance of payment equilibrium is M=X. When that holds, we get the equilibrium GDP Y* = (x0- m0) + (eXY/eMY)YW. Thus the growth of our country differs from world growth by the ratio of the export to import elasticities. If the import elasticity is larger than the import elasticity (eXY<eMY), the domestic growth will be below world growth Y* <YW.

13 This argument was often connected to a theory of ‘unequal exchange’. Note that the first argument does not involve such unequal exchange.

14 Differences in market power could be regarded as a third mechanism. The corporate sector is monopolistic in advanced economies and the labour is better organised in advanced than in developing countries. This means that firms will be better positioned to increase prices in the case of import price shocks and workers to push for higher wages than their counterparts in developing countries. As a result of these different market structures (and in particular of the large informal reserve army), productivity gains in the south may be passed on as lower prices and realised in the north. Note that the market power of firms and the organisation of labour will have developed not primarily with respect to developing countries, but rather of evolutions of competitive (intra-capitalist) dynamics within the north and the countervailing power of labour (i.e. domestic northern class struggle), but it will have strong indirect impact on the periphery.

15 Hausman and Panizza (Citation2010, p. 21) conclude ‘the domestic bond market is still not a venue through which to borrow from foreigners in local currency’. Recent increases in external debt are dominated by increases of private debt (UNCTAD Citation2020, p. 6).

16 Note that this is the opposite of the US experience during the GFC, when demand for US government bonds increased and capital flew to the USA despite the fact that the USA was the origin of the GFC.

17 Acemoglu et al. (Citation2001) distinguish between settler colonies and extractive colonies with the former replicating European participatory institutions and the latter implementing extractive institution. Acemoglu et al. restrict the extractive institutions to the state and do not analyse private sector extractive institutions or class relations.

18 That was recognized early on by CEPAL who advocated Latin American economic integration to enlarge markets. In theory an export-led strategy based on Thirlwall’s law would involve balanced current accounts (as the current account equilibrium holds in that model), but in practice (e.g. east Asia) it typically came net export surpluses.

19 The wording is from Schwartz (Citation2000), who distinguishes between Kaldorian and Ricardian growth strategies for late developers.

20 FDI is defined by ownership. Thus ‘FDI inflows’, despite the ‘I’ standing for investment, does not constitute investment in the macroeconomic sense. FDI coincides with actual investment in the case of greenfield investment, but in the case of mergers and acquisitions FDI occurs without macroeconomic investment.

21 One could argue that neoliberalism is also state led in the sense that deregulation policies are implement by states. In this sense any growth model may be state led. We use the term in a narrow sense to summarise a set of developmentalist or Keynesian policies.

22 It is notable, that GMA has not considered investment-led growth. This probably reflects the context in which GMA was developed (the pre-GFC boom), but from an history of thought and developmental perspective this is odd. Growth theory of different stripes would have high investment rates as a core feature of high growth and successful development. In neoclassical theory investment would be high because of rates of time preference, in Marxist theories because of high profitability, in Keynesian theory because of animal spirits and available credit. Thus theories differ as to the ‘why’, but agree that high investment is crucial. And the east Asian tigers (and China) indeed had high investment to GDP ratio. Within GMA only Mertens et al. (2021) explore investment led growth. This absence is reinforced by the frequent use of GDP growth decompositions in GMA. In advanced economies, investment is only about one fifth of GDP and thus does not show as a major growth contributor. However, they do potentially matter for developing economies, which, certainly in the East Asian cases had much higher growth and investment rates. However, growth accounting understates the importance of investment as it creates new productive capacity and embodies technological progress.

References

- Acemoglu, D., Johnson, S. and Robinson, J.A., 2001. The colonial origins of comparative development: an empirical investigation. American Economic Review, 91 (5), 1369–1401.

- Agosin, M., and Machado, R., 2005. Foreign direct investment in developing countries: does it crowd in domestic investment? Oxford Development Studies, 33 (2), 149–62.

- Akcay, Ü, Hein, E., and Jungmann, B. 2021. Financialisation and macroeconomic regimes in emerging capitalist economies before and after the Great Recession, Working Paper, No. 158/2021, Hochschule für Wirtschaft und Recht Berlin, Institute for International Political Economy (IPE), Berlin.

- Aldasoro, I., et al. 2020. Global and domestic financial cycles: variations on a theme. BIW Working Paper 864.

- Allen, R.C., 2017. Industrial revolution: A very short introduction. Oxford: Oxford University Press.

- Amsden, A., 1989. Asia's next giant: South Korea and late industrialization. Oxford: Oxford University Press.

- Arestis, Philip, and Glickman, Murray, 2002. Financial crisis in Southeast Asia: dispelling illusion the Minskyan way. Cambridge Journal of Economics, 26 (2), 237–260.

- Baccaro, L., Blyth, M., and Pontusson, J., 2022. Introduction: rethinking comparative capitalism. In: L. Baccaro, M. Blyth, and J Pontusson, eds. Diminishing returns: The New politics of growth and stagnation. Oxford: Oxford University Press, 1–50.

- Baccaro, L., and Pontusson, J., 2016. Rethinking comparative political economy: the growth model perspective. Politics and Society, 44 (2), 175–207.

- Ban, C. and Adascalitei, D., 2022. The FDI-led growth models oft he east-central and south-eastern European periphery. In: L. Baccaro, M. Blyth and J. Pontusson, eds. Diminishing returns: The new politics of growth and stagnation. Oxford: Oxford University Press, 189–211.

- Bhaduri, A., and Marglin, S., 1990. Unemployment and the real wage: the economic basis for contesting political ideologies. Cambridge Journal of Economics, 14, 375–93.

- Blecker, R., 1996. The new economic integration: structuralist models of North–South trade and investment liberalization. Structural Change and Economic Dynamics, 7 (3), 321–45.

- Blecker, R.A., 2016. The debate over “Thirlwall’s law”: balance-of-payments-constrained growth reconsidered. European Journal of Economics and Economic Policy: Intervention, 13 (3), 275–290.

- Bohle, D., and Regan, A., 2021. The comparative political economy of growth models: explaining the continuity of FDI-led growth in Ireland and Hungary. Politcs and Society, 49 (1), 75–106.

- Bortz, Pablo, and Kaltenbrunner, Annina, 2018. The international dimension of financialization in developing and emerging economies. Development and Change, 49 (2), 375–393.

- Carney, R.W., 2016. Varieties of hierarchical capitalism: family and state market economies in east Asia. The Pacific Review, 29 (2), 137–163.

- CEPAL. 2016. ECLAC economic thinking. Selected texts (1948–1998). United Nations. Available from: https://www.cepal.org/en/publications/40881-eclac-thinking-selected-texts-1948-1998.

- Cerra, V., and Saxena, S., 2008. Growth dynamics: the myth of economic recovery. American Economic Review, 98 (1), 439–457.

- Cimoli, M., Porcile, G., and Rovira, S., 2010. Structural change and the BOP constraint: why did Latin America fail to converge? Cambridge Journal of Economics, 34, 389–411.

- De Paula, L., Fritz, B., and Prates, D., 2017. Keynes at the periphery: currency hierarchy and challenges for economic policy in emerging economies. Journal of Post Keynesian Economics, 40 (2), 183–202.

- Dutt, A., 2002. Thirlwall’s Law and uneven development. Journal of Post Keynesian Economics, 24 (3), 367–90.

- Dutt, A., 2006. Aggregate demand, aggregate supply and economic growth. International Review of Applied Economics, 20 (3), 319–36.

- Dutt, A., 2019. Structualists, structures, and economic development. In: A Nissanke, and J. A Ocampo, eds. The palgrave handbook of development economics. Palgrave, 109–141.

- Erten, B., and Ocampo, J., 2013. Super cycles of commodity prices since the mid-nineteenth century. World Development, 44, 14–30.

- Evans, P., 1989. Predatory, developmental, and other apparatuses: A comparative political economy perspective on the Third World state. Sociological Forum, 4, 561–587.

- Fazzari, S., Ferri, P., and Variato, A., 2020. Demand-led growth and accommodating supply. Cambridge Journal of Economics, 44 (3), 583–605.

- Fischer, A., 2015. The end of peripheries? On the enduring relevance of structuralism for understanding contemporary global development. Development and Change, 46 (4), 700–732.

- Furtado, C., 1965. Development and stagnation in Latin America: A structuralist approach. Studies in Comparative Development, 1, 159–175.

- Gereffi, G., et al., 2005. The governance of global value chains. Review of International Political Economy, 12 (1), 78–104.

- Gerschenkron, A., 1962. Economic backwardness in historical perspective. Cambridge. Massachusetts: Belknap Press of Harvard University Press.

- Gräbner, C., et al., 2020. Is the Eurozone disintegrating? macroeconomic divergence, structural polarisation, trade and fragility. Cambridge Journal of Economics, 44 (3), 647–669.

- Haggard, S., 2018. Developmental states. Cambridge: Cambridge University Press.

- Hassel, A., and Palier, B., 2021. Growth and welfare in advanced capitalist economies. How have growth regimes evolved? Oxford: Oxford University Press.

- Hausmann, Ricardo, and Panizza, Ugo. 2010. “Redemption or Abstinence? Original Sin, Currency Mismatches and Counter-Cyclical Policies in the New Millenium,” CID Working Papers 194.

- Hein, E., 2012. The macroeconomics of finance-dominated capitalism and its crisis. Cheltenham: Edward Elgar.

- Hein, E. and Mundt, M., 2013. Financialisation, the financial and economic crisis, and the requirements and potentials for wageled recovery. In: M. Lavoie and E. Stockhammer, eds. Wage-led growth. An Equitable Strategy for Economic Recovery. London: Palgrave Macmillan, 153–186.

- Hein, E., and Vogel, L., 2008. Distribution and growth reconsidered – empirical results for six OECD countries. Cambridge Journal of Economics, 32, 479–511.

- Hübscher, E., and Sattler, T., 2022. Growth models under austerity. In: L. Baccaro, M. Blyth, and J Pontusson, eds. Diminishing returns: The new politics of growth and stagnation. Oxford: Oxford University Press, 401–419.

- Johnson, P., and Papageorgiou, C., 2020. What remains of cross-country convergence? Journal of Economic Literature, 58 (1), 129–75.

- Kay, C., 1989. Latin American theories of development and underdevelopment. London: Routledge.

- Kay, C., 2002. Why East Asia overtook Latin America: agrarian reform, industrialisation and development. Third World Quarterly, 23 (6), 1073–1102.

- King, J., 2002. A history of post Keynesian economics since 1936. Cheltenham: Edward Elgar.

- Kohler, K., 2019. Exchange rate dynamics, balance sheet effects, and capital flows. A Minskyan model of emerging market boom-bust cycles. Structural Change and Economic Dynamics, 51, 270–283.

- Kohler, K., and Stockhammer, E., 2022a. Flexible exchange rates in emerging markets: shock absorbers or drivers of endogenous cycles? Industrial and Corporate Change, doi:10.1093/icc/dtac036.

- Kohler, K., and Stockhammer, E., 2022b. Growing differently? financial cycles, austerity and competitiveness since the global financial crisis. Review of International Political Economy, 29 (4), 1314–41. doi:10.1080/09692290.2021.1899035.

- Kohli, A., 2004. State-Directed development: Political power and industrialization in the global periphery. Cambridge: Cambridge University Press.

- Lavoie, M., 1992. Foundations of post-Keynesian economic analysis. Aldershot: Edward Elgar.

- Lavoie, M., and Stockhammer, E., 2013. Wage-led Growth: Concept, Theories and policies. In: M. Lavoie and E. Stockhammer, eds. Wage-led growth. An Equitable Strategy for Economic Recovery. London: Palgrave Macmillan, 13–39.

- Menzinger, J., 2003. Does foreign direct investment always enhance economic growth? Kyklos, 56 (4), 493–510.

- Mertens, D., et al. 2022. Moving the center: growth models in emerging capitalist economies. Manuscript.

- Mertens, D., et al., 2022. Moving the center: Adapting the toolbox of growth model research to emerging capitalist economies. IPE Working Papers, 188/2022.

- Milberg, W., and Winkler, D., 2013. Outsourcing economics. Global value chains in capitalist development. Cambridge: Cambridge University Press.

- Minsky, H., 1986. Stabilizing an unstable economy. New Haven: Yale University Press.

- Misun, J., and Tomsik, V., 2002. Dows foreign direct investment crowd in or crowd out domestic investment? Eastern European Economics, 40 (2), 38–56.

- Nölke, A., 2018. Dependent versus state-permeated capitalism: two basic options for emerging markets. International Journal of Management and Economics, 54 (4), 269–282.

- Nölke, A., and Vliegenthart, A., 2009. Enlarging the varieties of capitalism: The emergence of dependent market economies in East Central Europe. World Politics, 61, 670–702.

- Ocampo, J.A., Rada, C., and Taylor, L., 2009. Growth and policy in developing countries. A structuralist approach. New York: Columbia University Press.

- Onaran, Ö, and Galanis, G., 2014. Income distribution and growth: a global model. Environment and Planning, 46 (10), 2489–2513.

- Porcile, G., and Toshiro Yajima, G., 2019. New structuralism and the balance-of payments constraint. Review of Keynesian Economics, 7 (4), 517–536.

- Prebisch, R., 1950. The economic development of Latin America and its principal problems. New York: United Nations.

- Pritchett, L., 2000. Understanding patterns of economic growth: searching for hills among plateaus, mountains, and plains. World Bank Economic Review, 14 (2), 221–50.

- Ramiro Fernandez, V., Ebenau, M., and Bazza, A., 2018. Rethinking varieties of capitalism from the Latin American periphery. Review of Radical Political Economics, 50 (2), 392–408.

- Rey, H., 2013. Dilemma, not trilemma. The global financial cycle and monetary policy independence. Available from: https://www.kansascityfed.org/publicat/sympos/2013/2013Rey.pdf. Jackson Hole.

- Rodrik, D., 2006. Goodbye Washington consensus, hello Washington confusion? A review of the world bank's economic growth in the 1990s: learning from a decade of reform. Journal of Economic Literature, 44 (4), 973–987.

- Samarina, A., and Bezemer, D., 2016. Do capital flows change domestic credit allocation? Journal of International Money and Finance, 62, 98–121. doi:10.1016/j.imonfin.2015.12.013.

- Schedelik, M., et al., 2021. Comparative capitalism, growth models and emerging markets: The development of the field. New Political Economy, 26 (4), 514–526.

- Schneider, B.R., 2009. Hierarchical market economies and varieties of capitalism in Latin America. Journal of Latin American Studies, 41 (3), 553–575.

- Schwartz, H.M., 2000. States versus markets: The emergence of a global market. 2nd ed. Basingstoke: Palgrave.

- Schwartz, H.M., and Blyth, M., 2022. Four galtons and a Minsky: growth models from an IPE perspective. In: L. Baccaro, M. Blyth, and J Pontusson, eds. Diminishing returns: The new politics of growth and stagnation. Oxford: Oxford University Press, 98–115.

- Sierra, J., 2022. The politics of growth model switching: why Lain America tries, and fails, to abandon commodity-driven growth. In: L. Baccaro, M. Blyth, and J Pontusson, eds. Diminishing returns: The new politics of growth and stagnation. Oxford: Oxford University Press, 189–212.

- Stockhammer, E., 2022. Post-Keynesian macroeconomic foundations for comparative political economy. Politics and Society, 50 (1), 156–87. Available from: https://journals.sagepub.com/doi/full/10.117700323292211006562.

- Stockhammer, E., and Onaran, O., 2022. Growth models and post-Keynesian macroeconomics. (with O. Onaran). In: L. Baccaro, M. Blyth, and J. Pontusson, eds. Diminishing returns: The new politics of growth and stagnation. Oxford: Oxford University Press, 53–73.

- Stockhammer, E., Onaran, Ö, and Ederer, S., 2009. Functional income distribution and aggregate demand in the Euro area. Cambridge Journal of Economics, 33 (1), 139–159.

- Stockhammer, E., and Wildauer, R., 2016. Debt-driven growth? Wealth, distribution and demand in OECD countries. Cambridge Journal of Economics, 40 (6), 1609–1634. doi:10.1093/cje/bev070.

- Storm, S., and Naastepad, C.W.M., 2015. Europe’s hunger games: income distribution, cost competitiveness and crisis. Cambridge Journal of Economics, 39 (3), 959–986.

- Tan, Y., and Conran, J., 2022. China’s growth models in comparative and international perspective. In: L. Baccaro, M. Blyth, and J. Pontusson, eds. Diminishing returns: The new politics of growth and stagnation. Oxford: Oxford University Press, 143–166.

- Taylor, L., 2004. Reconstructing macroeconomics. Structuralist proposals and critiques of the mainstream. Cambridge: Mass: Harvard University Press.

- Thirlwall, A.P., 1979. The balance-of-payments constraint as an explanation of international growth rates differences. Banca Nazionale de Lavoro Quarterly Review, 32, 45–53.