ABSTRACT

In September 2014, Alibaba went public in the United States through the largest IPO (initial public offering) in history, raising $21.8 billion and elevating the company’s value to $218.7 billion. The successful listing of Alibaba, the world’s largest online and mobile commerce enterprise, has attracted a lot of attention to investment strategy; in particular, the dual-class share structure of Internet enterprises designed to protect the control rights of company founders and the promotion of enterprise IPO have become a focus for international scholars. Based on the IPO case of Alibaba Group, this paper studies the dual share system of Alibaba with regards to three aspects: theoretical analysis, case analysis and financial index analysis. First, it introduces the literature relevant to the dual share system. It then takes Alibaba as a case study in order to analyse the reasons for the success of its IPO, and studies the impact of the dual share system on this IPO. Finally, it analyzes the effect and influence of the dual share system on IPO with regards to four dimensions of financial performance. Through the discussion in this paper, we hope to provide better ideas and suggestions for companies planning an external IPO.

Introduction

In recent years, our way of life has changed due to the development of Internet enterprises. ‘B2B’, ‘B2C’, ‘O2O’ and similar concepts have infiltrated our lives, allowing us to feel the Internet industry around us. China has been the world’s largest online retail market for eight consecutive years since 2013. In 2014, jd.com, Alibaba and other Chinese Internet companies went public in the US, which became a focus for lively media discussions. What is the difference between these Internet enterprises and traditional enterprises that attract media attention? Why do so many scholars pay particular attention to the ‘equity’ and corporate governance models of these IPO companies?

Emerging enterprises such as Alibaba, JINGdong, Google and Facebook are innovating the traditional institutional capital-oriented corporate governance paradigm. Instead of the traditional ‘one share, one right’ shareholding structure, they have chosen the new dual shareholding structure. The founders of these Internet companies were not major shareholders at the time of their IPO, which constitutes a significant difference from companies in other industries. The biggest difference between Internet enterprises and enterprises in traditional industries is the former’s wide range of services, which can be directly provided to a whole country and even the whole world. Therefore, Internet enterprises need a large amount of capital injection during their period of rapid development in order to meet the rapid expansion of their scale. However, these enterprises are generally founded by highly-educated, talented entrepreneurs and forward-looking computer professionals; these founders tend to have a high level of professional knowledge and skills and good management ability, but also a relative lack of capital.

Taking Alibaba Group as an example, this paper explores the transformation of corporate ownership structure in the new era and studies the impact of the dual-class ownership structure on IPO and long-term development by clarifying the organizational structure and mechanism of Alibaba’s ‘partnership system’. This paper has selected Alibaba as the research subject for three main reasons. First, Alibaba is a representative of China’s emerging industries, with high popularity and influence; its complete elements will allow us to study the impact of the special ownership structure of emerging enterprises on IPO. Secondly, the Alibaba partnership system is a typical dual share structure. Alibaba has adopted this partnership system in order to break through the restrictions of having the same shares and the same rights; the company chose to give up IPO in the Hong Kong Stock Exchange and move to the New York Stock Exchange in the United States, which has special significance for the analysis of the dual share structure. Finally, Alibaba’s achievements largely depend on the investment of venture capital and the strategic coordination of Ma Yun’s founding team. The analysis of the partnership system is helpful for exploring the significance of dual-class ownership structure in terms of the corporate governance of emerging enterprises.

Moving on from market regulation, equity and deep analysis of human capital formation, this paper then analyzes the aspects of internal human capital and the equity capital dynamics of the Alibaba partnership system, as well as the system’s financial performance in terms of profit ability, growth ability, and risk control ability by using concrete data and chart analysis. It illustrates the positive effect of Alibaba’s dual-class share system on corporate financial performance and the positive promotional effect of the system on the innovation of ownership structure, the allocation of control rights, the promotion of corporate governance efficiency and the acceleration of the company’s IPO listing.

The innovation of this article lies in the following three main aspects. The first is the analysis of the Alibaba partnership system in terms of external supervision, internal human capital and equity capital. The system was analysed in three ways: both inside and outside were taken into consideration; the USES comparison method was used; and the objective was comprehensively analysed in terms of its macroscopic environment and microscopic inner form. For equity capital and human capital, detailed data and charts were used for logical, complete, clear and detailed analysis. Secondly, the financial performance of the Alibaba partnership system was analysed in terms of profit ability, growth ability and risk control ability, using nearly ten years of financial index data. We considered the dual share both before and after the implementation of financial indicators and the index both before and after the listing; we also selected typical Internet companies such as Amazon and compared the relevant data. Thirdly, using tables, line charts were analysed and described; this is a more intuitive and effective system for using data to demonstrate the Alibaba partnership system’s ability to play a positive role in the enterprise’s financial performance. It also illustrates the system’s configuration for equity structure, control of innovation, promotion of efficiency of corporate governance etc., which have a positive financial effect. Through our analysis of the dual-class share system of Alibaba – which is a typical Internet enterprise – Internet technology companies with a booming development momentum can learn from both Alibaba’s selection of corporate ownership structure and its arrangement of control rights. The research is in line with the current Internet boom and thus has strong timeliness and practical reference significance.

Literature review

In September 2014, Alibaba was successfully listed in the New York Stock Exchange in the United States. On the day of the listing, Alibaba’s stock price soared and its market value reached US$ 231.4 billion, surpassing Facebook and becoming the world’s second largest Internet company after Google. Ma Yun, the executive chairman of Alibaba’s board of directors, was newly ranked as the richest man in China. A frequently-asked question pertaining to the listing in the United States is that of why Alibaba chose to list in the United States.

Investor protection hypothesis is another important viewpoint for scholars studying the motivation for an overseas listing. The main theory of this hypothesis is that, due to the different history of capital market development in different countries, the capital markets in more developed countries have already formed a sound market transaction system and a sound legal protection system. For enterprises, this plays a role of supervision and standardization, including supervision of enterprises to ensure they achieve maximum transparency in information disclosure, as well as protection of rights and interests for investors. In contrast, investor protection in most developing countries is very weak, which can cause investors to lose confidence and increase financing costs. Benos and Weisbach (Citation2004) showed that the desire to protect shareholders’ rights in order to facilitate access to the equity market was one of the main reasons for companies to cross-list in the United States. Doidge (Citation2004) found that the premium of voting rights for non-US companies listed on US exchanges was much lower than that for non-US listed companies, indicating that listing in the US improved the protection of minority shareholders, thus reducing private control interests. Abdallah (Citation2005) showed that enterprises from countries with imperfect capital market systems and inadequate investor protection tend to list publicly in capital markets with developed capital markets, sound trading systems and strict supervision mechanisms in order to satisfy their desire for greater financing.

Jensen and Mecking (Citation1976) elaborated principal-agent problems based on their study of the separation of ownership and control rights, marking the maturity of the research on the first type of agency problems between shareholders and managers in corporate governance and the emergence of principal-agent theory. Based on the perspective of control structure and the private income of control, Doidge (Citation2005) found that the controlling shareholders of IPO companies in the United States had significantly reduced their shareholdings and that 26% of companies were changing their control rights. Furthermore, it has been disclosed that more than 20 partners, including Ma, hold about 10% of Alibaba; under the Alibaba partnership system, the shareholders can take up five out of the nine seats on the joint control board of directors, which puts the company’s operating decision-making firmly in the hands of the partner organizations. To sum up, apart from investor protection and market segmentation, the most important reason for Alibaba to list publicly in the United States instead of Hong Kong was the ‘partnership system’ adopted by Alibaba, namely the dual-class share structure.

Alibaba IPO list introduction

Alibaba, in the story of domestic Internet enterprises, is regarded as a myth of e-commerce. It was founded in Hangzhou by 18 people, headed by Ma Yun, and incorporated in December 1998 in the Cayman Islands. Its first website was Alibaba.com, an English-language global wholesale trade market. Its membership reached 500,000 in 2000. In 2002, it became the world’s first business website with more than one million members and made a cash profit of six million yuan. In 2005, it entered into a strategic partnership with Yahoo! and became the largest Internet company in China. Since 2008, in order to adapt to the external market environment and the needs of the group’s operation and development, Alibaba has combined its business and platform and built an integrated online business ecosystem. On 19th September 2014, Alibaba Group was officially listed on the New York Stock Exchange under the stock symbol ‘BABA’, with an offering price of $68 per share. Alibaba’s main businesses include Taobao.com, Tmall, Juhuasuan, AliExpress, Alibaba International Marketplace, 1688, Ali Mom, Ali Cloud Computing, Alipay, Cainiao Network and Ant Financial. Taobao and Tmall have developed into the world’s largest C2C and B2C platforms, and Alipay has become the largest third-party transaction platform in China. In November 2019, Alibaba Group was officially listed on the Hong Kong Stock Exchange, issuing 500 million new shares, or about US$ 13 billion, making it the world’s largest Hong Kong-based IPO in 2019 and the largest public offering in Hong Kong since 2011. In the latest Fortune Global 500 list, released on 2 August 2021, Alibaba Group ranked 63rd in the world and first among Chinese Internet companies, with an annual revenue of US$ 109.48 billion, up by 41% year on year. Relevant major developments of Alibaba are shown in .

Table 1. Major events of Alibaba’s development.

Analysis of Alibaba IPO case

Impact of dual-class share structure

The protection of the founders’ right of control plays an important role in maintaining the stability of the management, giving a role to entrepreneurship and improving the market competitiveness of the enterprise. Most Chinese Internet companies choose to go public in the United States largely because it can maintain dual-class shares and effectively protect the control of the company’s founders.

Dual-class share structure refers to a corporate share structure in which the shares have different voting rights. Dual share structure can be compared with single share structure; it breaks through the principle of ‘the same share, the same right’. In this kind of shareholding structure, two types of voting rights, high and low, are usually set up, so that control is firmly in the hands of the founders. Dual-class share structure is an effective means of controlling a company by separating share rights and control rights. It is generally believed that the advantages of this structure are as follows: it can effectively guarantee control by management over a long period of time, reduce the cost of acquiring this control, enable a role for human capital and allow the long-term development of the company. is the changes of Alibaba's shareholding structure before and after listing.

Table 2. Changes in Alibaba’s equity structure before and after listing.

Dual-class share structure first appeared in the United States, originating from International Silver Company in 1898. The original intention of this structure was to maintain control over the company during its continuous expansion by the founding shareholders and senior managers. Through the issuance of shares with different voting rights, founding shareholders can control class A shares with higher voting rights, while the issuance of class B shares with lower voting rights means that class A shareholders can simultaneously obtain equity financing and retain control rights, that is, control the majority of voting rights using lower cash flow.

In July 2013, Alibaba had to apply for an IPO to the Hong Kong Stock Exchange; at the same time, it began its Hong Kong Stock Exchange IPO plan and expected to be listed in the Hong Kong Stock Exchange by October. However, in the end, Alibaba chose to move to a New York Stock Exchange IPO in the United States the following year. The motivation behind Alibaba’s decision was its self-created Lakeside partnership system, which was essentially a separation of cash flow rights and control rights, in line with the economic essence of dual share structure, and constituted a special form of dual share structure. is the content of Alibaba Partner system.

Table 3. The specific content of the Alibaba partnership system.

The Alibaba Group’s Lakeside partnership system means that the company governance structure can implement its business strategy more effectively. Internal decisions also greatly improve efficiency, ensuring that the core founding team can devote their attention to developing convenient Alibaba trading networks around the world. In this way, Alibaba’s vision of simultaneous development of all kinds of Internet businesses can be realized; the management is not distracted by trying to maintain control of the company, meaning that the company can achieve positive economic benefits.

The influence of institutional investors

Arugaslan (Citation2004) put forward the viewpoint of split shares, pointing out that compared with the traditional ‘one share, one vote’ system, the dual-class share structure can accelerate the capital liquidity of the company and generate more attraction from investors. He observed the IPO process of Google Inc., which had adopted a dual-class share structure, and concluded that this type of structure can give the founder team more control with less equity, meaning that investors will not be willing to invest in the company and the phenomenon of founder dictatorship will occur. Claessens, Djankov, and Lang (Citation2000) proposed that shareholders with controlling shares in a company can use equity crossing and pyramid equity to separate control rights and cash in the company. The Alibaba partnership system plays a background role to Ma Yun’s entrepreneurial team and Yahoo! in terms of control. For Internet enterprises, the initial stage involves testing the relevant early technologies and establishing research and development teams, which means that they need a large amount of start-up capital. Start-up enterprises can only obtain sufficient venture capital through financing from venture capital institutions. In the initial stage, Alibaba conducted a total of four large-scale financing projects, the history of major venture capital investments is shown in .

Table 4. Main venture investment history of Alibaba.

As can be seen from the above table, the development process of Alibaba went through a start-up stage, rapid development stage, initial stage of listing and stable operation stage. Alibaba had venture capital investment for all four stages. Goldman Sachs and other venture capital institutions made the first angel investment of 5 million yuan in Alibaba at its start-up stage. Later, SoftBank also saw the potential of Alibaba in the future development of China’s Internet industry, provided US$ 20 million and helped the company through difficulties during the trough of the Internet from 2001 to 2003, which enabled Alibaba to enter the stage of rapid development following the start-up stage. At this point, the human capital of Ma Yun and other entrepreneurial teams played an important role in the development of Alibaba. Venture capital institutions only provided funds and related value-added services; it was Ma Yun’s entrepreneurial team who controlled the operation and development of the company. When Alibaba entered the stage of rapid development, SoftBank, Fidelity and other venture capital institutions financed the company with US$ 82 million. Alibaba, during the previous rounds of investment in the Taobao and eBay war, had been unable to make earnings and was anxious to cash out; at this time, Yahoo! came into the picture. Yahoo! paid US$ 1 billion and handed over Yahoo! China for this investment. Although Yahoo! is still the largest shareholder at this time, control is in the hands of Ma’s team.

In the early stage, in addition to SoftBank, Yahoo! investors such as Blocks and Ali Management bought part of the shares and made considerable profits. The secondary market provided more investors and a dilution of shareholders. SoftBank become Alibaba’s largest shareholder, but showed no interest in becoming involved in the company’s operation and management; they left this to the Ma management team. Alibaba raised four rounds of venture capital before going public. SoftBank participated in the second and third round of venture capital investment. Fidelity and others participated in the first three rounds of investment; starting from the third round of financing, some early venture capital institutions cashed out. During the fourth round – with the introduction of Yahoo! – in addition to SoftBank, the venture capital institutions that had participated in the first three rounds all cashed out. Venture capital institutions invested in stages, generally according to Alibaba’s development, in order to control risks and prevent themselves from becoming trapped. In this way, the supervision of Ma Yun and other management members could also be strengthened to restrain their behaviour. Entrepreneurs such as Ma will only be motivated to work hard if their companies have good prospects for the next round of investment. SoftBank, Fidelity and other venture capital institutions made multiple rounds of investment in Alibaba, in stages. In addition to spreading risk and constraining the entrepreneurs’ behaviour, the ultimate purpose of this process was to promote Alibaba’s listing and realize cash and return.

Before Alibaba went public, SoftBank and Yahoo! were the main venture capitalists involved in the company’s financing. When Yahoo! invested in Alibaba, it signed a deal with Ma Yun’s team that gave Alibaba the right to buy back Yahoo!‘s 50% stake if the company went public by 2015; it also gave Yahoo! the right to dispose of the stock itself. Listing and buyback are common exit strategies for venture capital. However, when Alibaba first asked to buy back Yahoo!‘s shares, Yahoo! turned down the offer, which, despite all the incentives and tax breaks involved, was nothing compared to the returns from Alibaba’s Taobao and Alipay listings. The realization of the Alibaba listing was the best exit path for venture capital institutions. SoftBank and other institutions made several rounds of investment; the ultimate goal was to promote Alibaba to go public in order to obtain high returns.

Corporate governance effect

In the 1960s, the American economist Schulz established the theory of human capital. In his view, human capital was a kind of capital reflecting on workers: the sum of the value of all knowledge, skills, working ability and health quality held by workers. Gompere et al. (Citation2006) used the personal satisfaction hypothesis to analyse the reasons why founder shareholders adopted the dual-class share structure; they believed that founders considered not only economic benefits but also other factors, such as the realization of personal self-worth, when choosing an ownership structure. Therefore, this paper focuses on an analysis of human capital in Alibaba’s corporate governance.

Ma Yun’s human capital

Ma Yun was the first entrepreneur to develop e-commerce applications in China and remain exclusive to the Internet field. He was also the first entrepreneur in mainland China to appear on the cover of Forbes, an authoritative financial magazine in the United States. In October 2000, he was rated by the World Economic Forum as one of the world’s 100 ‘Future Leaders’ for 2001. Ma Yun and his team were the first to create China’s Internet business model; he is considered ‘the Chinese person who has created the world’s best site’ and is seen as the most original model for the business idealist and doer. His creative concepts and works in the field of Internet commerce have enriched the business content and behaviour of global and Chinese business people, and contributed a classic site for global business at the end of the 20th century: Alibaba.com.

Ma Yun’s life and rich entrepreneurial experience lay the foundation for his key human capital. Although his previous three entrepreneurial experiences ended in failure, he accumulated a lot of experience and lessons for the future establishment of Alibaba. The lesson Ma learned from his first startup (Haibo Translation) was not to choose a startup project blindly. However, this entrepreneurial experience consolidated and improved Ma’s English skills, which facilitated his expansion into the international market and collaboration with international partners. Ma Yun’s personal development experience is shown in .

Table 5. Ma Yun’s personal development.

Alibaba’s board of directors and management

As can be seen from the above , the characteristics of the board members of the company are as follows:

Table 6. Members of Alibaba’s board.

First, there is a high level of loyalty. Since the establishment of the partnership system of Alibaba in 1999, Ma Yun, Joseph Tsai, Kim Kardashian, Peng Lei and other founders have worked for Alibaba with little change. They follow Ma Yun in loyalty to Alibaba, abide by the partnership contract, maintain a sincere and heartfelt regard for Ali, and have been excellent partners to Ma. It is due to the careful management of these directors that Alibaba has achieved their breakthroughs and achievements. This valuable spirit has been inherited throughout Alibaba. Alibaba’s shareholder structure is stable and the company’s internal governance is good. Alibaba partners now have a total of 38 people who have been with the company for a long time. About 90% of the team, 35 people in total, have worked at Alibaba for more than ten years. There are 19 people, about 50%, who have served for nearly 20 years.

Secondly, Alibaba values strong professional quality. The founder of Alibaba, Ma Yun, has bold and novel ideas, a highly practical ability and an adventurous spirit; his boldness is beyond doubt. Zhang Yong is responsible for the implementation and operation of Alibaba’s various domestic and foreign businesses, which have led to the successful transformation of Alibaba and the completion of the worldwide logistics network Cainiao. This has not only solidified Alibaba’s market in China, but also opened up markets abroad. The group has made a great contribution to the progress of the global enterprise.

The directors of the company also hold other positions. Ma serves on the board of directors of SoftBank and the Global Management Economics Forum and is president of the local Chambers of Commerce, the Assistant Secretary-General of the United Nations and a Special Advisor to the United Nations Conference on Trade and Development on Youth Entrepreneurship and Small Business. This shows that Ma Yun has a strong personal ability and high professional quality. Tung Chee-hwa is also the founding chairman of the non-profit Hong Kong-based US-China Exchange Foundation. Jerry Yang sits on Yahoo!’s board of directors. It can be seen that the directors of Alibaba are able to handle not only the internal governance problems of their own company, but also the operation and financial problems of other companies, as well as serving as members of international organizations. This is sufficient to demonstrate the coping ability and outstanding coordination ability of the Alibaba directors. Gilson (Citation1987) stated that under the dual-class share structure, if a company is in the process of rapid development, the management will be more actively committed to expanding the market share and so minority shareholders will not have to concern themselves with the agency problems caused by the founders control of the company and the infringement of their own interests. Therefore, the dual-class share structure can effectively motivate the management.

To sum up, good quality level, strong resistance to pressure and excellent management, organization and coordination abilities play a far-reaching decisive role in the daily operation, financial situation and long-term existence of the enterprise. The most successful action taken by Ma was to choose these excellent talents as his board members, meaning that Alibaba successfully achieved their IPO on the New York Stock Exchange.

The impact of the dual-class share structure on Alibaba’s performance

Through its design, Alibaba’s dual-class share system has realized the company’s founding team and management team’s control over the company, in contrast to the minority shares. It is precisely because of the implementation of this system that the company has continuously improved its financial performance and promoted a successful IPO. Dimitrov and Jain (Citation2006) studied American enterprises that changed from a single share structure to a dual share structure between 1979 and 1998, finding that the change of ownership structure was conducive to the improvement of enterprise value and that the return rate of shareholders tended to reach 23% in the fourth year after the change. If the enterprise issued additional shares, the return rate could be as high as 52%. Cox (Citation2017) was the first to classify the IPO of dual-class shares and single-class shares according to the ability of managers and the growth of enterprises; he used this to test the long-term differences in the operation and return performance of enterprises. Through research and analysis, it has been found that if the management ability of managers is relatively high and the company has a high growth, the IPO performance of dual-class share structure enterprises will be better than that of single share structure enterprises in the same situation. If the management ability of managers is low and the company’s growth is poor, the performance of listed companies with single share structure will be better than that of listed companies with dual share structure. Lauterbach and Yafeh (Citation2011) studied Israeli enterprises that converted from single-class share structure to dual-class share structure between 1990 and 2000, concluding that the corporate performance and corporate value of enterprises that had converted to dual-class share structure were better than those of enterprises with single-class share structure during the same period. Myers and Majlu (Citation1984) found that in the process of company operation, with the continuous increase of shares held by shareholders, their supervision over the management was also strengthened, which can reduce inaction by the management and help the enterprise to develop in a good direction. Nuesch (Citation2016) studied Swiss-listed companies between 1990 and 1999 in order to analyse the external financing needs of enterprises, finding that if enterprises needed external financing, dual-class share structure would be conducive to the improvement of corporate performance, but not vice versa. Gilson (Citation1987) stated that management could be effectively incentivized under the dual-class share structure system. During the process of a company’s rapid development, the management will pay adequate attention to the expansion of market share, meaning that minority shareholders do not have to concern themselves with agency problems caused by the control of the founder, which would endanger their own interests.

Therefore, as a new form of corporate governance, it is necessary to evaluate this system’s financial performance and test its governance effect. The ultimate purpose of corporate governance is to allocate the rights and obligations of all parties through system design in order to ensure that the management and operation of the enterprise is more effective. Corporate governance should protect the interests of shareholders and other stakeholders. First of all, for better or worse, a system needs to ensure that the enterprise profits; if there is no profit, the profit essence of the enterprise ceases to exist and the company will lose the meaning of its existence. Profitability is also important to the development of the enterprise; an enterprise’s profit ability is the most representative and important in terms of financial performance measurement standards. Secondly, enterprises need to maintain the growth of profits and assets for continuous growth, which is also an important dimension for measuring the effectiveness of the dual-class share system. Only with the growth of profits and assets can companies invest more funds into market development and business expansion, thus achieving greater development. A system should also ensure that the cash flow of the enterprise can be effectively maintained, which forms the basis of the whole mechanism and the development of the company. Only when cash flow can be self-renewed can the enterprise continuously create value. In addition, the measurement and control of corporate risk is an important reflection of the governance ability of an enterprise. If an enterprise does not control risk well, it will be easily exposed to external environmental threats and risks regardless of its profitability. Therefore, in order to measure the governance efficiency of the system, it is necessary to analyse its ability to obtain cash, ensure profitability, conduct risk control and develop growth ability.

Profitability analysis

For Alibaba, whether it adopts dual-class share structure or other forms of governance, the most fundamental mission is to achieve the growth of corporate profit. If there is no profit, the profit essence of the enterprise will no longer exist, and the significance of its existence will be lost. Profitability is also an important ability relating to the development of the enterprise. This paper reflects the profitability of Alibaba using multiple profit indicators in order to evaluate the effect of Alibaba’s dual-class share structure more effectively.

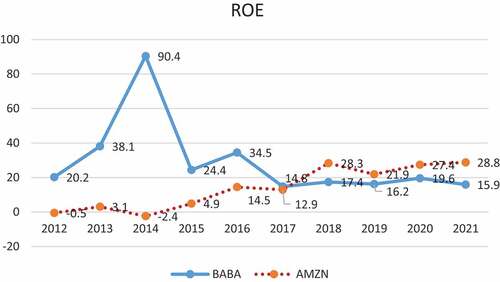

Return on equity (ROE) is an important financial index for measuring the efficiency of shareholders’ funds. It calculates the return on investment for a company’s common shareholders by dividing the net income after tax, after deducting preferred stock dividends and special income, by shareholders’ equity. It can be seen from and that Alibaba’s return on equity showed very strong growth from 2012 to 2014; the decline from 2014 to 2017 was due to the large amount of funds obtained from Alibaba’s listing. When compared with the return on equity for Amazon, the industry leader, from 2012 to 2017, Alibaba’s ROE is much higher, especially since Amazon’s growth rate is very slow compared to Alibaba’s. This shows that the return on equity has maintained a very good growth momentum following the implementation of the dual-class share system. It can be concluded from the above that the profitability of Alibaba is still maintaining this growth momentum under the dual-class share system and that the profit level is much higher than the average level of the industry. This is inseparable from the fact that the founding team and management have absolute control over the company since the proposal of Alibaba’s dual-class share system, which reduces the intervention of major shareholders and other investors in the normal production and operation of the company. After 2010, Alibaba acquired professional e-commerce branch companies, subdivided Taobao’s Tmall and Juhuasuan and invested in the film and television industry, enriching their business in multiple industries and at multiple levels, and opening up new profit growth points for Alibaba. This is also an important reason for the company’s successful IPO valuation of more than US$ 21 billion. During this process, Ali’s dual-class share system has made irreplaceable contributions to the fields of technology, public relations and sales, among others. It has also become more convenient for Alibaba’s management in terms of maintaining the orderly and steady operation of all business, which has become the fundamental guarantee for the company’s profitability improvement.

Figure 1. Analysis of Alibaba’s return on equity (%).

Table 7. Profitability analysis of Alibaba.

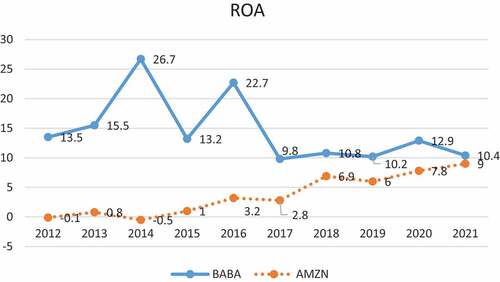

Return on assets (ROA) is the return on total assets (shareholders’ equity plus liabilities). It measures the efficiency of a company’s generation of profits from shareholders’ equity and liabilities. It can be seen from that the overall change in the trend of return on assets and return on equity for Alibaba is the same, showing very strong growth from 2012 to 2014 and a temporary fluctuation from 2014 to 2017 due to the huge amount of funds obtained from the listing, which became stable after 2017. However, when compared with the industry leader Amazon’s return on assets from 2012 to 2021, Alibaba’s return on assets is far higher. This shows that the implementation of Alibaba’s dual-class stock ownership makes the company’s return on shareholders’ equity relatively stable, and its business ability has greatly improved compared with the situation under the single-class stock ownership structure; this is consistent with the research results of Lauterbach and Yafeh (Citation2011) and Cox (Citation2017).

Figure 2. Analysis of Alibaba’s return on assets (%).

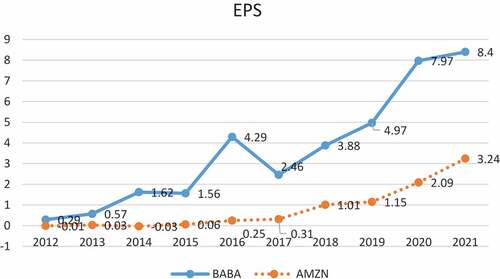

Earnings per share (EPS) is the ratio of a company’s total profit after taxes to its total common equity and reflects how much money shareholders can make per share. It can be seen from that Alibaba’s EPS has a larger growth range than Amazon’s EPS; in particular, since 2013, Alibaba’s EPS has been much higher than that of Amazon. Following this change and the implementation of the dual-class share system, the entrepreneurial management team was significantly less constrained by venture capital institutions, Alibaba’s profitability was further strengthened and the company entered a stage of rapid development. Based on all the above indicators, it can be seen that Alibaba’s profitability has been significantly improved following the implementation of the dual-class share system.

Figure 3. Earnings per share analysis of Alibaba.

Growth ability analysis

Enterprise needs to maintain the growth of profits and assets in order to grow. The partnership system is also an important dimension of the effectiveness of profits and asset growth; it allows a company to spend more money on market development, business development etc., leading to further development. For this paper, we have selected two financial indicators for the Alibaba dual share system following the growth ability analysis.

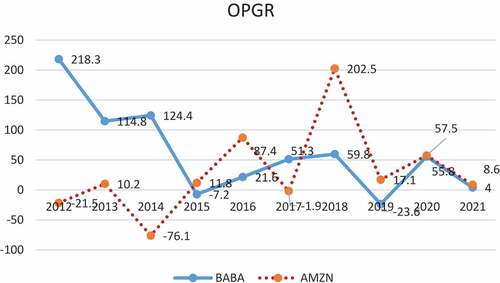

Operating profit growth rate (OPGR), also known as sales profit growth rate, is the percentage of an enterprise’s operating profit growth amount for the current year from the total operating profit of the previous year, which reflects the annual operating profit growth rate. Net capital growth rate (NCGR) is the percentage of the increase in net assets for the current period from the total net assets of the previous period, which reflects the annual growth rate of the net assets of the enterprise.

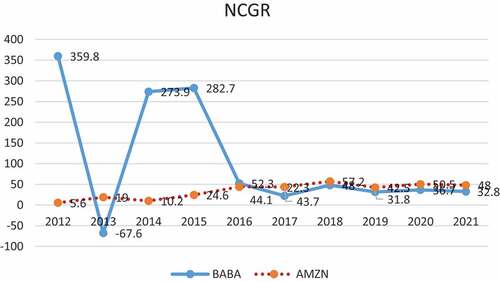

It is not difficult to see from that following a decline in the operating profit of Alibaba in 2012, there was an increase in 2013; after another brief decline in 2014, the overall trend of growth shows that the the profit growth rate was basically positive. It was only in 2018 that there was further negative growth, due to a financial crisis. It is this profit growth that has attracted investors’ funds. Although Alibaba’s net worth appeared to show negative growth prior to 2013, the remaining years of net asset growth rate have all been positive; the 2013–2015 net assets growth rate was far higher than that of Amazon after Alibaba implemented its dual share system. Following a short period of management adjustment, the operation management of the whole company has been greatly improved. To sum up, we can see that Alibaba’s growth ability has significantly improved following the implementation of the dual-class share system and that it is still in a rapid growth period. Alibaba’s growth is consistent with the overall environment of the industry, but it is clearly better than the leading enterprises in the industry. This shows that since the implementation of the dual-class share system in Alibaba, the entrepreneurial management team has been more focused on enterprise operation and thus Alibaba has had better growth ability, which is consistent with the research conclusions of Gilson (Citation1987).

Figure 4. Analysis of Alibaba’s operating profit growth rate (%).

Figure 5. Analysis of Alibaba’s net asset growth rate (%).

Enterprise growth ability and risk control ability require enterprise managers with a comprehensive grasp of all aspects of the enterprise. For Alibaba, because the number of partners on the board is capped, the business management team can be fully absorbed by dual share system enterprises in terms of talent. The experts in the field of comprehensive coordination will be able to improve the development of the enterprise as they have a comprehensive grasp on keeping the growth of the enterprise in its best state. This partnership system can avoid the restrictions brought about by the ownership structure, meaning that the entrepreneurial management team of Alibaba can maintain actual control over the enterprise, fully absorb and utilize the ability and expertise of the enterprise’s internal business experts through the dual share system and thus keep the enterprise in a good state of development. Meanwhile, supervision from venture capital institutions will help the partnership team to become more standardized in the management of the enterprise and achieve better preliminary work for decision-making on major issues, thus reducing mistakes.

Analysis of earning ability

The dual share system, first of all, ensures that enterprises can effectively maintain cash flow. This is the basis for the development of the whole mechanism and company; only cash flow can update itself. The enterprise cannot continuously recharge itself if the dual share system cannot guarantee basic stable cash flow, meaning that the dual share system will has no effect or function. Therefore, it is necessary to analyse Alibaba’s ability to obtain cash.

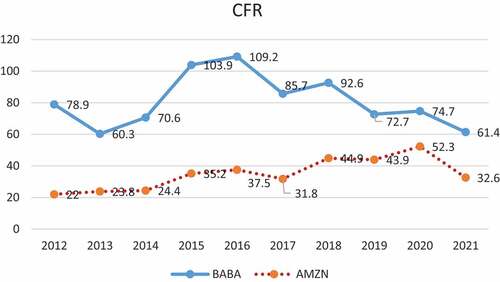

Cash flow ratio (CFR) is the ratio of earnings before interest, income taxes, depreciation and amortization (EBITDA), divided by the sum of interest or principal and interest. It reflects the ability of a business to generate enough cash from its operations to pay its debts and meet its commitments. The higher the cash flow ratio, the better the solvency of the enterprise; the lower the ratio, the worse the short-term solvency. From , it can be seen that the cash flow ratio index of Alibaba decreased slightly in 2012 and then showed a steady upward trend from 2013 to 2016, indicating that Alibaba’s cash creation ability improved steadily amid fluctuations from 2013 to 2016. In the process of establishing and implementing the dual-class share system of Alibaba, effectively improving the cash flow of the enterprise, the ability to obtain cash was also enhanced.

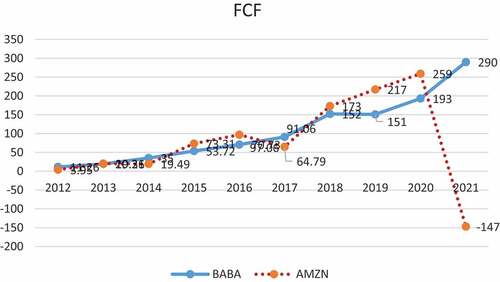

As shown in , Free cash flow (FCF), the cash a business can withdraw at will, is the most flexible cash flow for a business because it is not subject to depreciation, depletion or amortization. Over the long term, free cash flow should be a good proxy for a company’s actual profitability. As can be seen from , when compared with Amazon’s free cash flow level, Alibaba’s overall level was higher, steadily increasing from 2012 to 2021. Based on the above analysis, following the implementation of the dual-class share system, Alibaba’s cash flow has steadily and continuously increased; both its growth rate and its data for the same period are much higher than the industry average, indicating that Alibaba has a strong ability to obtain cash. Alibaba’s ability to create cash depends on effective management under the dual-class share system, as well as the excellent professional financial experts among the partners, who are able to formulate and implement effective financial and cash payment systems based on the company’s cash and business characteristics. In the process of the rapid development of the company, the management has focused on the expansion of market share, meaning that minority shareholders do not have to concern themselves with agency problems resulting from control by the founders, which would endanger the shareholders’ own interests (Gilson Citation1987). For example, in the above analysis of Alibaba’s human capital, it can be seen that among the partners, Chongxin Tsai, Yong Zhang and Wei Wu are all financial personnel with strong professional abilities. They have high financial qualifications and a rich experience accumulated from long-term work in large enterprises and firms. They are familiar with the company’s financial system and have lengthy experience in capital market investment and financing businesses. They can supervise Alibaba’s financial system and effectively guarantee the stability and growth of the company’s cash flow.

Figure 6. Analysis of Alibaba’s cash flow ratio (%).

Figure 7. Alibaba’s free cash flow analysis.

Risk control capability analysis

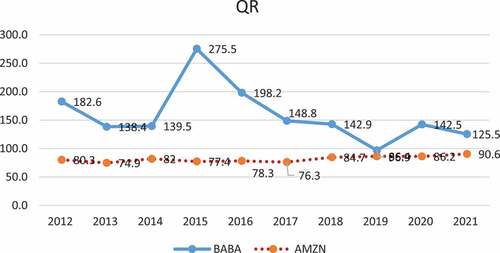

Every enterprise in the process of development will be faced with operational risk and financial risk. The ability to control risk is an important reflection of the strength of an enterprise’s high-level management. It can keep the business risk and financial risk relatively stable, and control this risk at a level suitable for the enterprise, which will help improve its profitability and improve its development level. In this paper, current ratio and quick ratio have been selected in order to explore Alibaba’s risk control ability. Current ratio (LR) is the ratio of a company’s current assets (including quick assets and inventory) divided by current liabilities, which reflects the company’s short-term solvency. Quick ratio (QR) is the percentage of quick assets and current liabilities of an enterprise, which reflects its quick solvency.

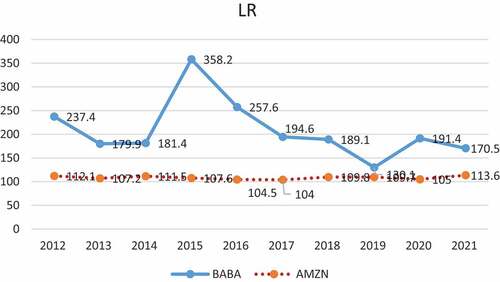

It can be seen from that the overall change in the trend for Alibaba’s current ratio and quick ratio has been consistent, showing a downward trend from 2012 to 2013 and gradually increasing after 2013, which would have given confidence and assurance to shareholders and investors and allowed the company to make preparations for its profit accumulation and listing in 2014. Alibaba’s operational and financial risks are in line with its own development speed and strategic layout. Due to the implementation of its dual-class share system, the management has a strong ability to control and grasp the company’s risk. Alibaba’s current ratio and quick ratio have been consistently higher than Amazon’s, which indicates that Alibaba has stronger short-term and long-term solvency, more stable operation and better development. Through the above analysis, we can see that Alibaba’s debt levels under the dual share system have effectively promoted the company’s own development speed and strategic layout; in terms of growth and stability, the company has shown better performance than Amazon. The enterprise’s risk control ability is increasing, and as the shareholders’ own shares also continue to increase, their supervision over the management is also increasing (Myers and Majlu Citation1984). Alibaba’s dual shareholding system performance depends on the management; the effective management of enterprises is inseparable from the partnership with excellent professional financial workers, who can, based on the company’s financial situation, collaborate fully with management on the communication and coordination around the planning and layout of state-owned enterprises, ascertain a reasonable capital budget with parties in the company and control the operational and financial risk of the enterprise so that it can achieve orderly development under certain conditions.

Figure 8. Analysis of Alibaba’s current ratio (%).

Figure 9. Analysis of Alibaba’s quick ratio (%).

Based on the above analysis, it can be concluded that Alibaba stands out among the industry in terms of its profitability, growth ability, earning ability and risk control ability following its implementation of a dual-class share system. The company has made progress year by year and its corporate governance effect has improved. The success of the company’s IPO in 2014 has provided the most powerful support. By implementing a dual share structure, the company has ensured that its most familiar and professional talents will maintain the mastery of corporate strategy, that the management of the enterprise will always enjoy dynamic and timely adjustment and robustness of persistence and that the talents among the field of professionals will be able to cooperate with each other and play to their own advantages and professional knowledge, having a good handle on the development of enterprises. Through this process, the agency cost of the enterprise is reduced, the profitability, development ability and cash ability of the enterprise are increased and the operation risk of the enterprise is effectively controlled, meaning that the enterprise will continue to maintain an excellent level within the industry. Alibaba’s dual-class share system promotes the orderly operation of the whole company, which is also an important factor in Alibaba’s IPO listing. The management of the dual-class share system is worth learning from for others in the industry; it achieves positive governance effects.

Implications of the case

Theoretical implications

From human capital theory to equity theory, this paper has comprehensively and thoroughly analysed the innovative institutional reasons for the dual share system of Alibaba; the performance analysis, including the profit ability, growth ability and risk control ability through specific data and graph table analysis, illustrates that the Alibaba dual share system has played a positive role in the enterprise’s financial performance. This shows that Alibaba’s partnership system has had a positive financial effect on the innovation of ownership structure and control rights allocation and the promotion of corporate governance efficiency, which involves the application, integration and innovation of corporate governance and financial performance analysis theory in specific cases. In the paper, we have found that this new ownership structure can guarantee Internet companies mastery over a minority stake in terms of control over the company, ensure stable improvement of operating performance and help people to address concerns about the rights of company ownership structure and the configuration of innovation, allowing them to focus on the important role of human capital in the allocation of corporate control and governance.

Practical implications

China does not allow dual-class share listings except in Hong Kong; some European and American capital markets have also already set out restrictions on dual-class share structures. This paper has studied the impact of dual-class share structure on the performance of Alibaba, conducted financial performance analysis through specific financial indicators, intuitively and powerfully explained and tested the effect of its ownership structure and control rights allocation innovation and provided a reference for measuring and evaluating the governance mechanism of control rights and ownership structure innovation. On the one hand, because Alibaba has influence not only in China but also throughout the world, its case study can provide a reference for the selection of equity structure by rapidly developing Internet companies. On the other hand, among these enterprises, the successful listing of Alibaba is largely due to the influence of the dual-class share structure. It is this structure that has the most obvious effect on the company’s performance and the most innovative value. As such, having studied Alibaba as a dual share structure through a typical enterprise analysis and summing up the pros and cons from the case study, we come to the conclusion that the momentum of vigorous development of current Internet companies for a company’s equity structure selection and control can be used for reference, and that if China introduced this shareholding structure, it would have a strong timeliness and practical significance.

Limitations and future suggestions

This paper has only used Alibaba’s listing on the New York Stock Exchange following its dual-class share structure as the subject of its case study. The case itself has a certain particularity, so the universality of the conclusions and suggestions still need to be tested and improved by multiple case studies and even empirical analysis. The existence of the dual structure was the main factor allowing Alibaba to achieve a New York Stock Exchange IPO, as it created a steady stream of value and a basic guarantee of its own development, but we cannot therefore arbitrarily believe that Alibaba’s various achievements in recent years have solely been due to the existence of the dual share structure; we can only say that the dual ownership structure is one of the aspects. Furthermore, due to the difficulty of collecting relevant information prior to Alibaba’s IPO, this paper was limited to theoretical research on dual-class share structure and Alibaba’s listing on the New York Stock Exchange; there is still room for an in-depth experience summary and supporting evidence.

Following up on the basis of the existing research, we will further expand the scope of the study of Chinese use of the dual ownership structure to other listed companies, such as Baidu, JingDong (JD), Poly (BDDU) and Beauty is Superior (JMEI), in order to carry out further research. We will research their development situation, financial situation and company performance, compared them to the results of this paper and existing research conclusions, in order to achieve a more universal conclusion. If possible, we will use larger sample data and financial analysis to conduct an empirical test of the impact of dual-class ownership structure on a company; we expect to find more powerful proof and draw better conclusions for the reference of subsequent researchers.

Conclusion

The dual-class share structure has a positive influence on the development of a company. Through our analysis of the implementation effect of Alibaba’s partnership system, it can be seen that the effectiveness of Alibaba’s partnership system is as follows: first, it guarantees the absolute control right of Ma Yun’s founder team, improves the corporate governance model and improves the efficiency of corporate governance; secondly, it protects the legitimate rights and interests of founders or important managers, avoids the infringement of their human capital and stimulates their exclusive investment into this human capital and enthusiasm for entrepreneurship and innovation; and thirdly, it ensures the implementation of the diversification strategy by the enterprise. Under the dual-class share structure, Alibaba continues to expand its business scale, steadily improving its business conditions and strengthening its risk control ability, which improves its profitability and development ability in the long term and helps the company to maintain its core competitiveness in the industry. The dual-class share structure has played a positive role in Alibaba’s future development and company value and promoted its smooth listing on the New York Stock Exchange.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Shuai Shao

Shuai Shao is in the final year of his PhD studies in Finance and Management at SOAS, University of London. His research interests are Fintech, peer to peer lending platforms and SMEs studies. His paper ‘Behavioural Aspects of China’s P2P Lending’ has been published in the European Journal of Finance. He holds a Master of Science degree in Management from Warwick Business School.

References

- Abdallah, A. 2005. “Cross-Listing, Investor Protection, and Disclosure: Does It Make a Difference? The Case of Cross-Listing versus Non-Cross-Listing Firms.” Working Paper.

- Arugaslan, O. 2004. “Why are Dual Class Shares Unified?” Western Michigan University.

- Benos, E., and M. S. Weisbach. 2004. “Private Benefits and Cross-Listings in the United States.” Emerging Markets Review 5 (2): 217–240. doi:10.1016/j.ememar.2004.01.002.

- Claessens, S., S. Djankov, and L. Lang. 2000. “The Separation of Ownership and Control in East Asian Cor-Porations.” Journal of Financial Economics 58 (1–2): 81–112. doi:10.1016/S0304-405X(00)00067-2.

- Cox, J. S. 2017. “Managerial Ability, Growth Opportunities, and IPO Performance.” Managerial Finance 43 (4): 488–507. doi:10.1108/MF-07-2016-0218.

- Dimitrov, V., and P. C. Jain. 2006. “Recapitalization of One Class of Common Stock into Dual-Class: Growth and Lo-Ng Run Stock Returns.” Journal of Corporate Finance 12 (2): 342–366. doi:10.1016/j.jcorpfin.2004.10.002.

- Doidge, C. 2004. “U.S. Cross-Listings and the Private Benefits of Control: Evidence from Dual-Class Firms.” Journal of Financial Economics 72 (3): 519–553. doi:10.1016/S0304-405X(03)00208-3.

- Doidge, C. 2005. “What is the Effect of Cross-Listing on Corporate Ownership and Control?” Working Paper.

- Gilson, R. J. 1987. “Evaluating Dual Class Common Stock: The Relevance of Substitutes.” Virginia Law Review 73 (5): 807–844. doi:10.2307/1072967.

- Gоmреre, Р., J. Іѕhіі, and Аnd А. Меtrісk. 2006. “Соrроrаtе Gоvеrnаnсе аnd Equіtу Prісеѕ.” Quаrtеrlу Journal of Economics 118: 107–155.

- Jensen, M., and W. Mecking. 1976. “Theory of the Firm: Managerial Behavior, Agency Cost and Ownership Structure.” Journal of Financial Economics 21 (3): 305–360. doi:10.1016/0304-405X(76)90026-X.

- Lauterbach, B., and Y. Yafeh. 2011. “Long Term Changes in Voting Power and Control Structure Following the Unification of Dual Class Hares.” Journal of Corporate Finance 17 (2): 215–228. doi:10.1016/j.jcorpfin.2010.09.005.

- Myers, S. C., and N. S. Majlu. 1984. “Corporate Financing and Investment Decisions WhenFirms Have Information That Investors Do Not Have.” Journal of Financial Economics 2 (13): 187–221. doi:10.1016/0304-405X(84)90023-0.

- Nuesch, S. 2016. “Dual-Class Shares, External Financing Needs, and Firm Performance.” Journal of M-Anagement & Governance 20 (3): 525–551. doi:10.1007/s10997-015-9313-5.