Abstract

The growth of the salmon aquaculture industry has attracted an increasing number of investors. Investors are conscious of economic consequences of climate change for the salmon farming companies, hence their demand for climate-related financial disclosure has increased. This study discusses potential climate-related financial impacts imposed on the salmon aquaculture production as identified by the Task Force on Climate-related Financial Disclosure (TCFD). We use data from 2016 to 2021 available on the Carbon Disclosure Project (CDP) platform, and we show to what extent salmon aquaculture companies disclose their climate-related risks. We find that when the demand of investors for climate-related financial disclosure increases, more firms tend to comply with their requests, while based on the CDP’s evaluation system, the firms perform better in minimizing their carbon impact. We argue that when salmon aquaculture companies publish their climate-related financial disclosure, they ensure transparency for their investors and secure a smooth transition into a low carbon economy.

Introduction

Over the past decades, aquaculture has been the world’s fastest-growing food production industry (Smith et al., Citation2010), with an annual growth of 7% (FAO, Citation2016). Global production has increased from around 14.9 million tonnes in 1995 to 82.1 million tonnes in 2018 (FAO, Citation2020). The increase in production has been possible due to substantial technological innovation, which led to productivity growth and lower production costs. As a result, aquaculture has become an economically competitive food production (Asche, Citation2008; Asche, Roll, Sandvold et al., Citation2013; Bergesen & Tveterås, Citation2019; Kumar & Engle, Citation2016). Overall, modern aquaculture has developed into a technologically advanced and profitable industry.

As fish farming technology has improved, the salmon-producing industry has matured and consolidated. The increased use of advanced technology has made the industry more capital intensive. This drove companies to seek for external financing, hence many were publicly listed. Today 26 companies engaged with salmon farming are traded on the Oslo Stock Exchange (OSE), one of the major seafood stock exchanges. The market value of these companies is around 368 billion Norwegian Kroner (€36.8 billion). As Sikveland et al. (Citation2021) showed, return on assets (ROA) has increased for publicly listed companies between 2001 and 2014. As a result, they become more attractive to investors. Thus, they are also responsible to meet investors’ demands to keep them satisfied.

Aquaculture production is a biological production that is subject to severe economic consequences due to the uncertain nature of climate-change (Asche, Citation2008; Asche et al., Citation2017, Citation2022). The success of the industry has led to a number of studies investigating price volatility as a consequence of climate change (Asche et al., Citation2017, Citation2019), but so far, little attention has been paid to the potential financial impacts from climate change. Misund (Citation2017) argues that common and industry-specific risk factors can impact aquaculture firms’ returns. Listed salmon aquaculture firms have a responsibility toward their investors to tackle such risks and cannot ignore them.

Financial climate-related risks are usually identified as either physical or transition risk (TCFD, Citation2017). Physical risks are defined as the risks related to economic damages that come as a result of the effect of climate change (Bovari et al., Citation2018; Dafermos et al., Citation2017, Citation2018; Dietz et al., Citation2016; TCFD, Citation2017). For instance, farmed salmon is kept in pens and if pens are destroyed as a result of extreme weather, salmon can escape, causing major financial consequences. Transition risks are linked to the risk of the firms as a result of market shocks and policy implications related to transitioning into a low-carbon economy (Battiston et al., Citation2017; Dafermos et al., Citation2018; Leaton, Citation2011; Stolbova et al., Citation2018; TCFD, Citation2017). In salmon aquaculture, transition risks are mainly related to policies and regulations. A large amount of the supplies of the Norwegian salmon aquaculture industry is exported to a diverse market (Asche et al., Citation2013; Straume, Citation2017), hence a substantial increase in the carbon tax can impact air cargo and increase price volatility (Asche et al., Citation2019).

Climate-related risks are expected to cause turmoil not only for the salmon aquaculture sector, but also across various sectors outside the food production industry. Companies across sectors are becoming aware of the financial risks associated with climate change and are looking to become climate resilient to maintain future profitability. Investors, lenders, and other stakeholders also become more aware of climate-related risks and their demands for climate resilience and adaptation increase. Climate-related financial disclosures are key in reassuring investors and other stakeholders regarding climate risks. Therefore, over the recent years organizations such as the Carbon Disclosure Project (CDP) and the Task Force for Financial Disclosures (TCFD) were created to promote the importance of reporting on climate-related risks. Such disclosures assist investors, stakeholders, and other market participants to gain a better understanding of the industry’s challenges related to climate change as well as support their future investment decisions. A standardized framework, such as the one provided by the TCFD, can also assist financial risk managers to understand and identify the risks their companies face. It is however important to note that disclosures are crucial to maintain transparency, but they are not to be seen as an indicator of good financial performance per se. They are an indication that the underlying company is tackling climate-related financial risks while considering stakeholders’ demands.

In the literature on business studies and finance there are theories that are often used to explain the relationship between companies, their stakeholders, and society. This study is compatible with theories such as the legitimacy theory, signaling theory, and stakeholder theory. In line with the legitimacy theory, organizations must ensure that they carry out activities in accordance with societal boundaries and norms (Deegan et al., Citation2002). Based on Patten (Citation2002) and their definition of legitimacy theory, if there is a large scale environmental disaster incident in a salmon-producing company (e.g., disease outbreak) then other companies also respond by increasing the amount of environmental disclosures in their annual reports even though the incident itself was directly related to one company. There are also significant information asymmetries concerning climate-related risks between corporate insiders and directors and other stakeholders, such as investors. Disclosing climate-related financial risk can reduce such asymmetries in the access to information, as discussed in the literature on signaling theory (e.g. Connelly et al., Citation2011). Nygård (Citation2020) found that sustainability reports contribute to reduce the information gap between managers and shareholders. By gaining access to information on the company they are invested in, investors and other stakeholders can impact decisions regarding the operations and finances of that company. According to the stakeholder theory, a company is responsible to meet all the demands from their stakeholders (Parmar et al., Citation2010). Therefore, if the investors’ demands for climate-related financial disclosure increase, the company is responsible to disclose its exposure on climate-risk.

In this study, we discuss climate-related risks specific to the salmon industry and explore to what extent some of the publicly listed firms have been implementing climate-related financial disclosures. Next, we investigate the role of TCFD and CDP in increasing responses from the companies. There are other initiatives that also attempt to quantify sustainability matters such as the Global Reporting Initiative (GRI),Footnote1 and specific to the aquaculture industry, the Aquaculture Stewardship Council (ASC).Footnote2 These initiatives help companies understand the outward impacts of their unsustainable practices which in turn helps them become more sustainable and impacts their willingness to report on their climate risks. We will not explain further the specifications of these initiatives as this study focuses only on the TCFD and CDP. Furthermore, we will only focus on investors’ demands regarding climate-related financial disclosures and not on other stakeholders. This is because we collect publicly available data from the CDP platform which is an investor-driven global disclosure system. The outcome of this study is applicable to salmon aquaculture firms, as well as their investors and other stakeholders, but also policy-makers and regulators.

In Section “Climate-related risks conceptualization” we divide the climate-related risks into physical and transition, and discuss the ones relevant to the Norwegian salmon aquaculture industry. In Section “Climate-related financial disclosure,” we explain the role of TCFD and CDP and the specifics of climate-risk financial disclosures for salmon aquaculture firms, as well as the main potential financial impacts they can face. In Section “Results” we analyze the publicly available reports obtained from the CDP platform. Section “Discussion” presents a discussion of the outcomes.

Climate-related risks conceptualization

Salmon farming production is a biological practice that interacts with its surrounding environment. It can therefore be vulnerable to potential financial impacts as a consequence of climate-related risks. A set of studies raising the environmental challenges of the salmon farming industry were selected and will be discussed (Asche et al., Citation1999, Citation2009; Smith et al., Citation2010). To facilitate the discussion around climate-related risks, the studies raising the environmental challenges of the aquaculture industry will be categorized according to physical and transition risks.

Physical risks

There are physical and biological risks associated with the salmon farming industry’s practices. Since salmon is farmed in open cages it can be exposed to a number of climate-related risks (Asche et al., Citation2018). The major ones are large-scale disease outbreaks (Abolofia et al., Citation2017; Asche et al., Citation2021; Fischer et al., Citation2017; Torrissen et al., Citation2013), pollution through feed waste (Asche, Citation2008; Asche et al., Citation1999), and algal blooms. Climate change can potentially worsen the impacts of these risks. The change in water temperature, increasing precipitation, raise in sea-levels, frequent storm surges and other extreme weather events are some of the climate-related risks that can financially impact the salmon aquaculture industry.

Sea cages, where salmon is kept, are an open system of stock cultivation. If storms are stronger than expected, they can destroy the cages the salmon is kept in, and it can escape, resulting to unexpected losses for the farmers (Olaussen, Citation2018). Salmon escaping from the sea cages is not something unfamiliar to the farmers and the relevant authorities and therefore they manage to keep the escapes under control without them causing large losses (Pincinato et al., Citation2021). Nevertheless, the farmers and the relevant authorities must consider the added risk from climate change. It is possible that salmon escaping becomes more frequent and the farmers are no longer able to control its potential outcome. Storm surges can also destroy materials and installations exposing the industry’s firms to severe economic consequences. Given that the installations are a valuable asset for the salmon farming practice, it being destroyed can significantly decrease stockholders’ equity.

Chronic physical risks, e.g. increase in water temperature, can impose long-term changes that will demand climate adaptation from the industry’s underlying firms (De Silva & Soto, Citation2009). Specifically, the dynamics of salmon lice are depending on the water temperature, and they are characterized by annual oscillations in parasite abundance (Jansen et al., Citation2012). For instance, salmon thrives between 9 and 14 degrees, hence instability in water temperature, can cause a disease outbreak, potentially impacting the mortality rate of salmon as well as increasing production costs as a result of necessary treatment processes, e.g. medicine and vaccines (Asche et al., Citation1999; Torrissen et al., Citation2013). Abolofia et al. (Citation2017) found that lice parasitism alone produced 436 million US dollars in damages to the Norwegian industry in 2011. Algal bloom which is linked to an increased concentration of nutrients in the sea, known as eutrophication is also an existing threat to the salmon industry, since it can be the cause of diseases spreading (Asche et al., Citation1999). It is a biological risk for the salmon aquaculture production and as for storm surges, such events can become more frequent with the imposed risk of climate change. Norwegian coastal waters are particularly vulnerable to an increase in the frequency of toxic algal bloom (Edwards et al., Citation2006). As a consequence of diseases spreading, the industry’s firms must invest sufficient funds into research (Asche, Citation2008). To be able to do this, the firms must hold a required capital amount. All physical risks related to the salmon aquaculture industry can potentially increase costs and expenses. Therefore, a so-called sustainable food production such as salmon aquaculture industry cannot afford ignoring these risks and their potential financial impacts.

Transition risks

Climate change and its impacts are receiving increased political attention. It is then sensible to expect that the political scene regarding matters related to climate change is changing. The impacts from climate change are enormous and the scientific world has been urging politicians to act immediately on the climate (IPCC, Citation2022). However, the long inactivity from politics has now emphasized the urgency for “new” relevant policy implementations that ensure a smooth transition into a low-carbon economy. What if a “smooth transition” is no longer possible? To be more specific, the urgency to save our planet can result in ill-considered decisions. Abate et al. (Citation2016) argued that stricter environmental regulations in developed countries have contributed to lower growth rates. For instance, in Norway, environmental concerns regarding the exponential growth of the Norwegian aquaculture production drove the authorities to restrict the licenses for new production (Asche et al., Citation2017; Hersoug et al., Citation2019). Asche et al. (Citation2019) argued that such restrictive regulations can result in the stagnation of the industry’s production growth, causing an increase in salmon price volatility. This can have severe consequences for the producers (farmers) and other market participants such as investors, whose aim is to maintain profitability at a minimum cost. Implementing policies without consulting the relevant industry can have undesirable outcomes. Operating based on a holistic approach is vital for creating policies and regulations that consider the industry’s environmental challenges without harming the farmers and jeopardizing the production (Osmundsen et al., Citation2017).

The key for the industry (or any industry) to maintain its profitability is the trust from its stockholders. In return, it must ensure the protection of the stockholders’ equity. Therefore, it is vital for the industry’s firms to be prepared for transitioning into a low-carbon economy. Otherwise, the costs will increase, potentially resulting in high losses, so that many shareholders will pull out if they have not yet. If stockholders sell a large number of shares from a publicly traded firm, it is likely to cause the value of the firm’s stock to fall. Listed Norwegian aquaculture firms have high liquidity buffers, but using it as a risk reduction measure is costly (Sikveland et al., Citation2021; Sikveland & Zhang, Citation2020), which can have adverse effects on returns. This in turn can reduce the stocks’ value. Moreover, considering that the salmon market offers hedging opportunities for investors through the Fish Pool futures exchange for salmon, Ewald et al. (Citation2022) found a correlation between the shares prices and longer salmon futures contracts. This implies that the salmon stock market reflects on the salmon market risk, hence, climate-related risks associated with salmon aquaculture companies are likely to impact salmon prices. To avoid these, the salmon industry firms have a responsibility toward their stakeholders to maintain their growth and reputation. The TCFD (Citation2017) recommendations argue that the key to achieve this are the financial risk managers. They are required to have sufficient knowledge about climate-related risks associated with the transition into a low-carbon economy. This knowledge is important for developing trustworthy climate-related financial disclosures as well as managing the exposure into climate-related risks (TCFD, Citation2017).

Transitioning to a low-carbon economy does not appear to be a smooth transition for the salmon aquaculture industry. The transition risks associated with the industry are various and challenging. An increase in the carbon tax, bringing farms inland or demand closed containment to improve sustainability, importing soybeans from South America despite the procedure causing deforestation, are some of the challenges the salmon industry is facing and must overcome to attain a smooth transition.

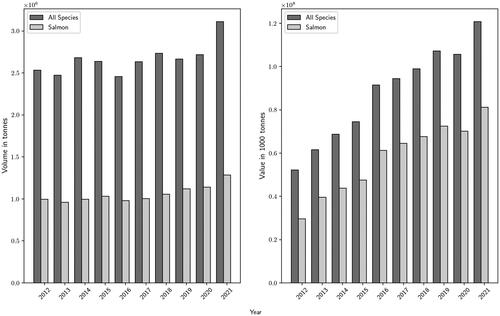

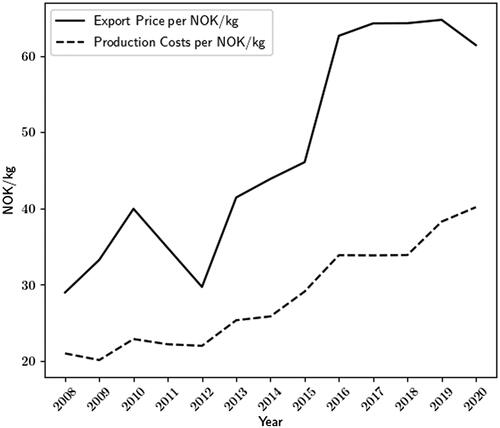

An increase in the carbon tax can severely impact the salmon aquaculture industry. shows that at the end of 2021, salmon represented approximately 40% of the quantity of all seafood species exported from Norway and 60% of the value. The increasing trend of the export volume of salmon verifies that it is a significant species for the export growth of the Norwegian seafood industry. Around 20% of salmon exported from Norway is shipped with air carriers; hence, if the Norwegian authorities are raising concerns relating to the carbon emissions of air transport, an increase in the carbon tax on air cargo is a likely policy measure. If the cost of delivering their product to their consumers rises, salmon producers are forced to either raise prices and face lower demand, or accept lower profit margins. shows the development of the annual export prices and production costs for salmonFootnote3 from 2008 to 2021. It is evident that both the annual export prices and production costs have been increasing over this period. Even though the production costs for Norwegian farmed Atlantic salmon are increasing, they are low compared to other competitor countries (e.g., Chile, Faroe Islands) (Iversen et al., Citation2020). Climate-related risks can increase production costs, causing an increase in prices and volatility which in turn creates distress for the investors (Oglend & Sikveland, Citation2008).

Figure 1. Comparison of the Volume in Metric Tonnes and Value in 1000 Tonnes of salmon and all species exported from Norway from 2012 to 2021. Source: Norwegian Seafood Council (Citation2022).

Figure 2. Salmon Export Price and Production Costs (including delivery costs) measured in NOK/kg. Source: Norwegian Directorate of Fisheries (Citation2022).

One of the biggest critiques of the salmon farming industry is the feeding practice. In the early years of salmon aquaculture production the farmers used fish meal and fish oil to feed the salmon. Later, it became clear that this feed practice was not sustainable mainly because a lot of the fish meal and fish oil came from wild-caught fish. Because of the rapid growth of the salmon aquaculture industry, more fish meal and oil were required to feed the salmon and therefore more wild-caught fish was required which then led to over-fishing wild fish populations (Tveteras & Asche, Citation2008). Researchers in collaboration with salmon fish feed manufacturers substituted fish meal and fish oil with plant-based protein sources, mainly soy (Egerton et al., Citation2020). Therefore, most of the ingredients used for feeding salmon are now plant-based. Although this transition into plant-based feed is seen as an improvement in terms of implementing a sustainable feeding practice, it also comes with a number of environmental concerns. Given that soy is mainly grown in South America, having to grow more of it raises concerns relating to the unprecedented deforestation in the Brazilian Amazon forest (Dou et al., Citation2018; Sun et al., Citation2018). These concerns are valid, especially considering that importing countries (e.g., Norway) are gaining environmental benefits as well as maintaining production growth, while the exporting countries (e.g., Brazil) suffer environmental losses. As a response, certification programs for sustainable aquaculture have been developed with a focus on restricting the global trading of soybeans (Luthman et al., Citation2019). The Norwegian salmon aquaculture industry set a goal together with their soy suppliers in Brazil to become 100% deforestation and conversion-free. Their goal was achieved in February 2022 and has set an important example for other food production industries. On the other hand, the demand for growing soy has been increasing not only for feeding salmon but also for feeding humans. Solberg et al. (Citation2021) argued that yeast produced from nonfood resources such as wood can serve as a high-quality protein source for farmed fish. They found that there is indeed potential for use in commercial production but the present costs of producing yeast from lignocellulosic biomass may still be too high, and there is a need to develop more efficient processes for economic utilization (Solberg et al., Citation2021). Such findings emphasize on the importance of research and innovation developments within the salmon aquaculture industry. Research and development are capital intensive and therefore the salmon aquaculture industry must be financially prepared to invest in projects that promote a more sustainable food production.

Government regulations and policies can also drive the need for investing in research and innovation (Asche & Smith, Citation2018). Given the binding government regulations and environmental challenges in sea-based salmon aquaculture, the rapid growth once observed has now been limited (Abate et al., Citation2016; Bjørndal & Tusvik, Citation2019). Technological developments on land-based farming have changed the potentials of the aquaculture industry as well as the cost of production. Bjørndal and Tusvik (Citation2019) found that although land-based salmon farming is early in development, if successful, it can potentially have an important impact on the dynamics of the salmon market. Investing in land-based salmon farming projects is important to further investigate to which extent it can support the salmon aquaculture production. An additional reason for dedicating part of the salmon aquaculture research to land based farming, is that several political parties, e.g., in Denmark and North America, propose to forbid net pen farming. Such proposals aim to prevent salmon escape incidents that spread parasites and pathogens to wild stocks (Bailey & Eggereide, Citation2020; Olaussen, Citation2018). The salmon aquaculture production must be prepared to implement new developments to remain a successful food production industry. Attitudes toward innovation, levels of investment and social norms influence adoption of technological, organizational and informational practices (Lebel et al., Citation2021). Moreover, policies that explicitly ban or limit the adoption of new technologies could undermine aquaculture’s green potential (Asche et al., Citation2022).

It has become clear that a “good” reputation for a food production industry is closely linked to sustainability. Being prepared to transition into a low-carbon economy is vital for being considered a successful industry. Salmon aquaculture is heavily dependent on changes in regulations and therefore it must be prepared to tackle climate-related risks or its successful reputation will be jeopardized. Assessing climate-related risks should be set as the main priority for the industry. Therefore, the question to be asked is: are the salmon aquaculture industry’s underlying companies addressing potential climate-related financial impacts?

Climate-related financial disclosure

Task force on climate-related financial disclosures (TCFD)

The Financial Stability Board (FSB)Footnote4 established the TCFD to assess climate-related risks and opportunities that assist investors, lenders, insurance writers, and other stakeholders. The role of the TCFD is to provide a standardized framework on climate-related financial disclosure so that it helps market participants understand climate-related risks. The prospect of creating a climate-related financial disclosure framework is to be singular instead of a regime, and accessible to various organizations across sectors.

The framework is based on a set of recommendations. These recommendations aim to support a company to develop a regular procedure when disclosing climate-related risks. They are based on four key features: First, the framework must be adaptable by organizations in different industries (e.g., financial services, agriculture). Second, it ought to be recorded in the files of every organization that follows the TCFD recommendations. Next, it is designed based on a “Scenario Analysis” approach. Specifically, potential hypothetical climate-related scenarios are set to happen in the future and the aim is to assess whether the underlying organization is resilient to these scenarios. Last, the framework focuses on risks and opportunities related to the transition into a low-carbon economy. The climate-related opportunities fall outside the scope of this study and therefore will not be thoroughly discussed but only mentioned.

The structure of the TCFD (Citation2017) recommendations is based on four thematic areas, that represent the core elements of how firms operate: governance, strategy, risk management, and metrics and targets. These recommendations integrated into the financial disclosure framework, create the information that will assist investors and other stakeholders to understand how to assess climate-related risks and opportunities. Since these recommendations are applicable to organizations across sectors and jurisdictions, the TCFD (Citation2017) provided supplemental guidance in developing these disclosures for both the financial and non-financial sectors. In this study, we will only focus on the Non-Financial sector recommendations that are relevant for the salmon aquaculture industry.

Financial impacts

The first step in assessing the potential climate-related financial impacts is to acknowledge and understand the physical and transition risks related to the salmon aquaculture industry. To derive the financial impacts associated with these risks, the TCFD (Citation2017) identified four major climate-related financial impact categories: Revenues, Expenditures, Assets and Liabilities, and Capital and Financing. All four categories are highly relevant for the salmon aquaculture production.

It is evident from and that there are various financial impacts that could potentially affect the financial stability of the salmon aquaculture industry. Physical risks, presented in , can mainly impact the revenues of a company, and destroy its installations which in turn will increase insurance premiums and costs. describes in detail possible transition risks of the salmon aquaculture industry and their potential financial impacts. Policy implementations associated with transition risks can also have a major impact on the revenues of a company, increase its costs and cause changes in supply and demand. Requirements for technological developments and innovations can also impact the demand for salmon, highlight the industry’s research and development requirements and emphasize on the importance of climate adaptation to minimize costs. Climate change brings instability to the market and that can reduce the demand and the revenues. Gaining a reputation of being a non- sustainable food production, or a food production that is not willing to transition and adapt to a low-carbon economy, can decrease the demand for salmon which in turn can reduce a company’s revenues.

Table 1. Examples of physical climate-related risks and Potential Impacts concerning aquaculture.

Table 2. Examples of Transition climate-related risks and Potential Impacts concerning aquaculture.

The response to the climate-related risks is depending on the industry’s firms’ cost structure (TCFD, Citation2017). A firm with lower production costs is more resilient to changes that can impact its cost structure, unlike a firm with a high-cost structure. By disclosing its cost structure, a firm better informs its investors about their investment potential. With the discussion around climate-related risks strengthening, investors will start demanding disclosure of capital expenditure plans and the level of debt or equity required for funding these plans. Disclosing these plans allows investors to understand how flexible the salmon aquaculture firms to re-invest their capital, as well as how willing the capital markets are to fund firms that are significantly exposed to climate-related risks. The salmon aquaculture production is an industry that can be severely exposed to climate-related risks because it is a food production practice highly dependent on its surrounding environment. Debt and equity structures should also be disclosed as they can also be impacted from climate-related risks. A firm’s ability to raise new debt or refinance existing debt is important to maintain investors’ trust. It shows certain flexibility to handle climate-related issues. Operating losses, asset write-downs, and the need to raise new equity for required investments, can cause changes in capital and reserves. The transparency that comes with climate-related financial disclosure is the key for the industry’s firms to prove their resilience to their stockholders.

TCFD recommendations

Investors’ demand for better climate-related financial disclosures has increased (Hahn et al., Citation2015). The number of firms across sectors that are pursuing financial disclosures upon investors’ requests is on the rise (Reid & Toffel, Citation2009). The TCFD (Citation2017) suggests that the fear of potential climate-related financial impacts can drive companies to conduct regular climate-related financial disclosures. Task Force’s aim is to provide a standardize framework with sufficient information and instructions that will assist financial risk managers in constructing better climate-related financial disclosures. presents the major TCFD (Citation2017) recommendations to be followed when creating climate-related financial disclosures. These recommendations are created with the purpose to be easily adaptable across various sectors including the salmon aquaculture industry. They can be seen as suggested steps the financial risk managers of a company should follow when creating climate-related financial disclosures. The recommendations aim to provide a holistic approach for constructing climate-related financial disclosures as well as emphasize the benefits of such disclosures for investors, and other stakeholders.

Table 3. Task force recommendations.

Carbon Disclosure project (CDP)

The Carbon Disclosure Project (CDP) was established in 2003 as an investor-led nonprofit initiative, and it began surveying large firms regarding their carbon-related risks and strategies. The main objectives of the CDP are twofold: to inform risk managers about the concerns of investors over climate-related risks and to inform investors about the climate-related risks the firms are exposed to (Stanny & Ely, Citation2008). To maintain the first objective, the CDP developed a questionnaire by translating the TCFD recommendations into actual disclosure questions and a standardized annual format. The CDP provides investors with a unique platform where the TCFD framework can be brought into real-world practice. The questionnaire is distributed to a range of firms across sectors with high market value. To achieve the second objective, the CDP decided to make the responses of individual firms publicly available online and produce reports with accumulated responses.

Considering that answering the CDP questionnaire is voluntary, the response rate has been rising gradually. Several studies indicate that an increasing number of firms submit the CDP questionnaire (Lewis et al., Citation2014; Luo et al., Citation2012; Stanny & Ely, Citation2008; Wegener et al., Citation2013). The number of Global 500 firms responding increased from 221 in 2003 to 403 in 2013 (Depoers et al., Citation2016) with the respondent firms accumulating more than 10% of the total global emissions (EU Technical Expert Group, Citation2019). As a result, the CDP holds the largest database on GHG emissions in the world (Reid & Toffel, Citation2009). The success of the CDP is driven by the investors who support it.

The companies’ decision to implement a regular practice on their reporting has enabled the CDP to influence corporate governance and climate-related financial disclosure. The CDP has obtained critical mass over the last years and it is considered the leading reporting initiative for firms worldwide. It signals a positive reputation for the firms who choose to report on the CDP platform. The CDP created a “Status Report” where they disclose the status of the reporting for each company publicly on their platform. They also developed an internal score system. It measures the comprehensiveness of disclosure, awareness and management of climate-related risks and best practices associated with environmental leadership, such as setting ambitious and meaningful targets. The details of the CDP Scores are presented on . The CDP internal scoring system is used to drive investment decisions toward a low-carbon and resilient economy. Even for low-scoring companies, choosing to report shows respect to investors’ demands as well as commitment to lower their GHG emissions. The companies that do not report on the CDP platform despite investors’ requests, indicate weaknesses in their governance and risk management strategies (Sullivan & Gouldson, Citation2012).

Table 4. Explanation of the CDP scores.

The main report on the CDP platform is the climate change report. This is in accordance with the TCFD (Citation2017) recommendations. In addition to this report, the CDP added the forest and the water security reports. The forest report is targeting firms that are inclined to measure and manage forest-related risks. Forest-related risks are relevant for organizations and industries, whose practices can cause deforestation and forest degradation. The main objective of this report is for companies to show their commitment to restore the forests. There are four forest-related reports: Cattle Products, Palm Oil, Soy, and Timber. Palm Oil and Soy are the main relevant ones for the salmon aquaculture industry and the ones we will focus on in this study. The aim of the water security report is to disclose whether firms are doing enough to tackle water pollution. The Carbon Disclosure Project (Citation2017) reported that many firms underestimate the risks related to water pollution with only 28% of the disclosing firms acknowledging any water-related risks in their practice. Climate-related financial disclosure allows stakeholders to access more information on strategies that mitigate climate change as well as assist companies to improve the disclosure of their actions that contribute to the reduction of GHG emissions (de Faria et al., Citation2018).

Climate-related financial disclosures for the salmon industry

The physical and transition climate-related risks presented in and are specific to the salmon aquaculture industry and can be seen as guidance for creating climate-related financial disclosures for individual companies. In this study, we discuss industry specific climate-related financial disclosures without focusing on individual companies. This is because the TCFD recommendations (see ) are constructed based on sectors (e.g. Agricultural, Food and Forest Products Group in the case of salmon producers) and not for individual companies. However, the climate-related financial disclosures are to be submitted by individual companies. By reporting in a common framework, i.e. the CDP’s industry-specific questionnaire, the differences in sustainability between the companies can be captured by the internal scoring system of the CDP (see ).

Assessing the impacts of climate-related risks for firms in the salmon aquaculture industry involves a number of interactions and tradeoffs among the climate-related aspects of chemical and biological pollution, disease outbreaks, unsustainable feeds and competition for coastal space (Carballeira Brana et al., Citation2021), complicated by maintaining production sufficient to meet the rising demand for blue food (Naylor et al., Citation2021). Disclosures in the salmon aquaculture industry should focus on qualitative and quantitative information related to both the industry’s policy and market risks in the areas of GHG emissions, as well as the industry’s opportunities around increasing food. The salmon-producing companies should provide evidence of their efforts to reduce GHG emissions, pollution, disease outbreaks, high fish mortality rates and unsustainable feeds. Also they must provide information on how they improve sustainability through adequate environmental monitoring, location of farms, reduction and exploitation of wastes as well as how the chemicals are being used to ensure the growth and continuity of salmon aquaculture production. The companies must also disclose the impacts that physical and transition risks had on salmon production. They should also report opportunities that capture shifts in both business and consumer trends toward consuming salmon, as well as processes and services that produce lower emissions, are less chemical-intensive, and use sustainable feeding while maintaining adequate food security.

Results

In this study, we utilized the public information available on the CDP platform. We collected publicly available data on all three types of CDP reports: climate change, forest, and water security, for seven Norwegian salmon aquaculture companies with the highest market cap. The analysis is in line with the content and converge of the firms’ responses to the CDP questionnaires.

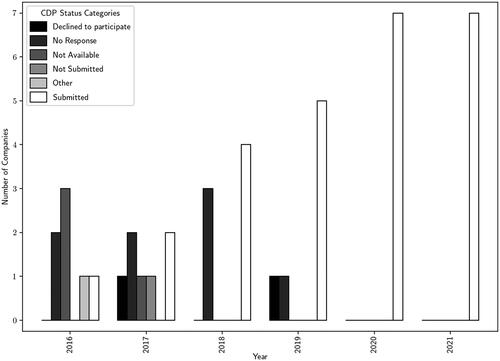

It is evident from that all seven firms have been requested to disclose their climate-change reports from 2016 to 2021. This could be because physical and transition risks of the salmon aquaculture industry have been receiving increasing attention from investors. Their demands for climate-related financial disclosures and transparency have increased. From the results demonstrated in , the firms are not obliged to respond to the investors’ requests and hence some firms “Decline to participate.” In 2016, 3 out of 7 firms chose not to publicly disclose their climate change reports but only make them available for the investors who have requested them (see for explanation). Over the years the number of companies submitting their climate change reports on the CDP platform has increased. In fact, in 2020 and 2021 all seven companies have submitted their climate change reports. This can be because discussions about sustainability and sustainable food practices increased, raising awareness for consumers, investors, and other stakeholders. Therefore, it is important for the salmon aquaculture companies to publish their climate-related financial disclosures, because it emphasizes their willingness to respond to investors’ demands, tackle climate-related risks, and lower their GHG emissions.

Figure 3. Salmon Aquaculture Firms CDP Status Results for the Climate Change report from 2016 to 2021. Source: Carbon Disclosure Project (Citation2022).

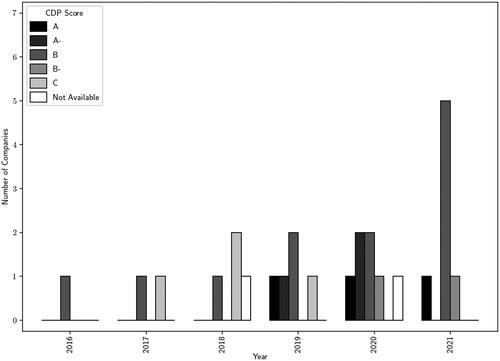

presents the corresponding CDP Scores of the companies that submitted the CDP climate change report from 2016 to 2021. Given that number of companies submitting their climate change reports have increased over the period from 2016 to 2021 (see ), the corresponding CDP scores have on average also become better. The first A was granted in 2019 which is an improvement from 2018 where the average score was C. In 2020, when all the companies submitted their reports, they on average managed to seal an “Awareness Level” about the requirements of lowering GHG emissions, with two of them taking this awareness up to the “Management level,” and the last two up to the “Leadership level” (see ). All the companies made their CDP scores publicly available in 2021 with B as the average score. It is the first year that all companies submitted the climate change report and also maintained a sufficient score. These results are encouraging for the future of the salmon aquaculture industry. They can be seen as proof that the increased demands from investors to submit climate-related financial disclosures, lower GHG emissions, and adapt more sustainable practices, have a positive impact on the industry’s companies.

Figure 4. Salmon Aquaculture Firms CDP Scores from 2016 to 2021. Source: Carbon Disclosure Project (Citation2022).

In we see that from 2016 to 2021, institutional investors have increasingly requested the salmon aquaculture firms to disclose the CDP forest report. The number of companies submitting the report has also increased from 2016 to 2021. In 2020 when all seven companies were requested to submit the forest report, three of them responded. In 2021 also three companies submitted the forest report, but six were requested to do so. presents the scores for the two types of forest-related reports we focus in this study: Palm Oil and Soy. It is evident from the results that the Soy forest report is the one mostly reported since it is quite relevant for the salmon aquaculture industry. For the Palm Oil report we notice that most companies responded after the deadline and therefore have the status of “Not Scored.” In 2021, all three companies which submitted their forest reports, were given an average score of B. The link between the salmon aquaculture’s feeding practice and soy production is what mainly drives investors to request disclosure of forest-related risks.

Table 5. Salmon Aquaculture Firms CDP Status on Forest Report from 2016 to 2021.

Table 6. Salmon aquaculture firms CDP results on forest report.

presents the number of companies which were requested to disclose the CDP Water Security Report and their responses. It is evident that the water security report is not requested as much as the climate and forest reports from investors. However, it appears that in 2021, 6 out of 7 companies were requested to disclose the CDP water security report with only one of them submitting it. This shows that the relevance of the water security report is increasing for the salmon aquaculture companies and the investors appear to believe that it does. The responses of the companies in the upcoming years will clarify investors view on the industry’s responsibility on water pollution.

Table 7. Salmon aquaculture firms CDP results on water security report.

Discussion

Physical and transition climate-related risks have been receiving increasing attention from investors over the last years. While the impacts of climate change worsen, investors’ expectations will continue to increase. A fast-growing food production industry such as salmon aquaculture has a responsibility to identify and tackle climate-related risks to protect its growth, secure transparency for its investors and other stakeholders, and smoothly transition into a low-carbon economy. To secure these, organizations such as the TCFD and CDP have been founded to encourage climate-related financial disclosures.

We discussed the potential climate-related risks, physical and transition, that are likely to financially impact the salmon aquaculture companies. Policies and regulations play a significant role in maintaining and supporting the sustainability of the industry but are not always successful. We argue that the policy makers should implement a holistic approach by consulting the salmon producers when constructing policies and regulations. Companies on the other hand, need to be prepared for the possibility of new regulation concerning climate-related risks. For instance, the growing discussions on climate-related financial disclosures have resulted in some countries, such as the United Kingdom (UK),Footnote5 to implement a new legislation that will require some companies to disclose climate-related financial information. This, or other regulatory changes could be implemented in Norway too, so Norwegian salmon producers must be prepared to make the necessary adjustments.

The results from the publicly available CDP reports are compatible with the increased investors’ demands for transparent and accurate climate-related financial disclosure. The number of firms disclosing their climate, forest, and water-security CDP reports has sharply increased between 2016 and 2021. The most important, and largely reported one is the climate report. We found that in 2020 and 2021 all seven companies submitted the CDP climate report, and were granted a B score on average. This shows that the salmon aquaculture companies are working to tackle their carbon and climate risks, while responding to the investors’ requests. Although this cannot necessarily be interpreted as good financial performance for the companies, it is a step forward toward not only transparency, but also climate change awareness and willingness to do better in terms of their own environmental impacts.

The second most important report is the CDP forest report. This report is divided into four forest-related risks, of which we only focus on the ones relevant to the salmon aquaculture industry: Palm Oil and Soy. We found that in 2021, out of six companies that were requested to submit the report, three of them submitted and were given a B score on average for the soy forest report. This was the highest number of companies reporting on their soy forest report within the predefined time requirements of the CDP. Soy is the main source of feeding for the salmon aquaculture production and it has been accused of causing deforestation. It is also a plant-based raw material that can be consumed by humans. This makes the choice of soy an unsustainable feeding practice and causes major criticism for the salmon aquaculture industry. We argue that this attracts investors’ attention and increases their demands for disclosure and as long as it remains controversial, the companies have an ethical responsibility to be transparent about it.

The third report is the CDP water security report that aims to decouple growth from depletion of water resources and capitalize a water secure economy. While this report was introduced back in 2010, it was only in 2018 that the first salmon aquaculture company was requested to submit it. The number of salmon aquaculture companies requested to report increased since 2018 with the number significantly rising in 2021 when six out of seven companies were asked to report. However, only one company submitted. This indicates that the salmon aquaculture industry does not consider that its practices cause water pollution. Considering that 6 out of 7 companies were requested by their investors to submit the water-security report, it is likely that more companies will submit this report in the future. This expectation stems from the fact that disclosing climate- and forest-related risks improved substantially upon investors’ demands.

The results from this study are relevant for salmon aquaculture companies, investors and other market participants, as well as policy makers. As climate change is increasingly discussed in politics, business, media and academia, investors have also become more aware of the issue. We verify that a large and growing number of investors are increasingly expecting salmon producers to respond to their demands and adapt to climate change. Therefore, they impose pressure on the companies to disclose the climate-related risks and financial impacts. The salmon-producing companies have a responsibility toward their investors, society and the environment to report on their climate-related risks and environmental impacts. The establishment of the CDP and the TCFD played a significant role in promoting climate-related financial disclosures. They increased awareness within the firms and thus lead financial risk managers to develop dynamic strategies to tackle climate-related financial impacts and integrate these strategies into the risk management process of the company. As a result, firms set more ambitious goals to become more competent in disclosing climate-related risks, as well as maintain their climate resilience and lower environmental footprints.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 An independent, international organization established in 1997 that helps businesses take responsibility for their climate-related impacts, by providing them with the standards for sustainable reporting.

2 An independent, international non-profit organization established in 2010 that promotes certified responsibly farmed seafood and aims to reduce the environmental impacts of aquaculture.

3 The production costs are per kg produced salmon and rainbow trout because companies produce both species and it is not possible for the Norwegian Directorate of Fisheries to separate the costs.

4 The Financial Stability Board (FSB) is an international body that monitors and makes recommendations about the global financial system.

References

- Abate, T. G., Nielsen, R., & Tveterås, R. (2016). Stringency of environmental regulation and aquaculture growth: A cross-country analysis. Aquaculture Economics & Management, 20(2), 201–221. https://doi.org/10.1080/13657305.2016.1156191

- Abolofia, J., Asche, F., & Wilen, J. E. (2017). The cost of lice: Quantifying the impacts of parasitic sea lice on farmed salmon. Marine Resource Economics, 32(3), 329–349. https://doi.org/10.1086/691981

- Asche, F. (2008). Farming the sea. Marine Resource Economics, 23(4), 527–547. https://doi.org/10.1086/mre.23.4.42629678

- Asche, F., Anderson, J. L., Botta, R., Kumar, G., Abrahamsen, E. B., Nguyen, L. T., & Valderrama, D. (2021). The economics of shrimp disease. Journal of Invertebrate Pathology, 186, 107397. https://doi.org/10.1016/j.jip.2020.107397

- Asche, F., Eggert, H., Oglend, A., Roheim, C. A., & Smith, M. D. (2022). Aquaculture: Externalities and policy options. Review of Environmental Economics and Policy, 16(2), 282–305. https://doi.org/10.1086/721055

- Asche, F., Guttormsen, A. G., & Nielsen, R. (2013). Future challenges for the maturing Norwegian salmon aquaculture industry: An analysis of total factor productivity change from 1996 to 2008. Aquaculture, 396–399, 43–50. https://doi.org/10.1016/j.aquaculture.2013.02.015

- Asche, F., Guttormsen, A. G., & Tveterås, R. (1999). Environmental problems, productivity and innovations in Norwegian salmon aquaculture. Aquaculture Economics & Management, 3(1), 19–29. https://doi.org/10.1080/13657309909380230

- Asche, F., Misund, B., & Oglend, A. (2019). The case and cause of salmon price volatility. Marine Resource Economics, 34(1), 23–38. https://doi.org/10.1086/701195

- Asche, F., Oglend, A., & Selland Kleppe, T. (2017). Price dynamics in biological production processes exposed to environmental shocks. American Journal of Agricultural Economics, 99(5), 1246–1264. https://doi.org/10.1093/ajae/aax048

- Asche, F., Roll, K. H., Sandvold, H. N., Sørvig, A., & Zhang, D. (2013). Salmon aquaculture: Larger companies and increased production. Aquaculture Economics & Management, 17(3), 322–339. https://doi.org/10.1080/13657305.2013.812156

- Asche, F., Roll, K. H., & Tveteras, R. (2009). Economic inefficiency and environmental impact: An application to aquaculture production. Journal of Environmental Economics and Management, 58(1), 93–105. https://doi.org/10.1016/j.jeem.2008.10.003

- Asche, F., Sikveland, M., & Zhang, D. (2018). Profitability in Norwegian salmon farming: The impact of firm size and price variability. Aquaculture Economics & Management, 22(3), 306–317. https://doi.org/10.1080/13657305.2018.1385659

- Asche, F., & Smith, M. D. (2018). Induced innovation in fisheries and aquaculture. Food Policy. 76, 1–7. https://doi.org/10.1016/j.foodpol.2018.02.002

- Bailey, J. L., & Eggereide, S. S. (2020). Indicating sustainable salmon farming: The case of the new norwegian aquaculture management scheme. Marine Policy, 117, 103925. https://doi.org/10.1016/j.marpol.2020.103925

- Battiston, S., Mandel, A., Monasterolo, I., Schütze, F., & Visentin, G. (2017). A climate stress-test of the financial system. Nature Climate Change, 7(4), 283–288. https://doi.org/10.1038/nclimate3255

- Bergesen, O., & Tveterås, R. (2019). Innovation in seafood value chains: The case of Norway. Aquaculture Economics & Management, 23(3), 292–320. https://doi.org/10.1080/13657305.2019.1632391

- Bjørndal, T., & Tusvik, A. (2019). Economic analysis of land based farming of salmon. Aquaculture Economics & Management, 23(4), 449–475. https://doi.org/10.1080/13657305.2019.1654558

- Bovari, E., Giraud, G., & Mc Isaac, F. (2018). Coping with collapse: A stock-flow consistent monetary macrodynamics of global warming. Ecological Economics, 147, 383–398. https://doi.org/10.1016/j.ecolecon.2018.01.034

- Carballeira Brana, C. B., Cerbule, K., Senff, P., & Stolz, I. K. (2021). Towards environmental sustainability in marine finfish aquaculture. Frontiers in Marine Science, 343, 62. https://doi.org/10.3389/fmars.2021.666662

- Carbon Disclosure Project. (2017). Harnessing the power of purchasing for a sustainable future. Technical Report.

- Carbon Disclosure Project. (2022). Scores. https://www.cdp.net/en/scores

- Connelly, B. L., Certo, S. T., Ireland, R. D., & Reutzel, C. R. (2011). Signaling theory: A review and assessment. Journal of Management, 37(1), 39–67. https://doi.org/10.1177/0149206310388419

- Dafermos, Y., Nikolaidi, M., & Galanis, G. (2017). A stock-flow-fund ecological macroeconomic model. Ecological Economics, 131, 191–207. https://doi.org/10.1016/j.ecolecon.2016.08.013

- Dafermos, Y., Nikolaidi, M., & Galanis, G. (2018). Climate change, financial stability and monetary policy. Ecological Economics, 152, 219–234. https://doi.org/10.1016/j.ecolecon.2018.05.011

- De Silva, S. S., & Soto, D. (2009). Climate change and aquaculture: Potential impacts, adaptation and mitigation. Climate change implications for fisheries and aquaculture: Overview of current scientific knowledge. FAO Fisheries and Aquaculture Technical Paper, 530, 151–212.

- Deegan, C., Rankin, M., & Tobin, J. (2002). An examination of the corporate social and environmental disclosures of bhp from 1983–1997: A test of legitimacy theory. Accounting, Auditing & Accountability Journal, 15(3), 312–343. https://doi.org/10.1108/09513570210435861

- Depoers, F., Jeanjean, T., & Jérôme, T. (2016). Voluntary disclosure of greenhouse gas emissions: Contrasting the carbon disclosure project and corporate reports. Journal of Business Ethics, 134(3), 445–461. https://doi.org/10.1007/s10551-014-2432-0

- Dietz, S., Bowen, A., Dixon, C., & Gradwell, P. (2016). ‘Climate value at risk’ of global financial assets. Nature Climate Change, 6(7), 676–679. https://doi.org/10.1038/nclimate2972

- Dou, Y., Silva, R. F. B. d., Yang, H., & Liu, J. (2018). Spillover effect offsets the conservation effort in the amazon. Journal of Geographical Sciences, 28(11), 1715–1732. https://doi.org/10.1007/s11442-018-1539-0

- Edwards, M., Johns, D., Leterme, S., Svendsen, E., & Richardson, A. (2006). Regional climate change and harmful algal blooms in the Northeast Atlantic. Limnology and Oceanography, 51(2), 820–829. https://doi.org/10.4319/lo.2006.51.2.0820

- Egerton, S., Wan, A., Murphy, K., Collins, F., Ahern, G., Sugrue, I., Busca, K., Egan, F., Muller, N., Whooley, J., McGinnity, P., Culloty, S., Ross, R. P., & Stanton, C. (2020). Replacing fishmeal with plant protein in Atlantic salmon (salmo salar) diets by supplementation with fish protein hydrolysate. Scientific Reports, 10(1), 1–16. https://doi.org/10.1038/s41598-020-60325-7

- EU Technical Expert Group. (2019). Report on Climate-related disclosures.

- Ewald, C.-O., Haugom, E., Kanthan, L., Lien, G., Salehi, P., & Størdal, S. (2022). Salmon futures and the fish pool market in the context of the capm and a three-factor model. Aquaculture Economics & Management, 26(2), 171–191. https://doi.org/10.1080/13657305.2021.1958105

- FAO. (2016). The state of world fisheries and aquaculture 2016. Contributing to food security and nutrition for all, 200. FAO.

- FAO. (2020). The state of world fisheries and aquaculture. FAO.

- Faria, J. A. d., Andrade, J. C. S., & Silva Gomes, S. M. d (2018). The determinants mostly disclosed by companies that are members of the carbon disclosure project. Mitigation and Adaptation Strategies for Global Change, 23(7), 995–1018. https://doi.org/10.1007/s11027-018-9785-0

- Fischer, C., Guttormsen, A. G., & Smith, M. D. (2017). Disease risk and market structure in salmon aquaculture. Water Economics and Policy, 03(02), 1650015. https://doi.org/10.1142/S2382624X16500156

- Hahn, R., Reimsbach, D., & Schiemann, F. (2015). Organizations, climate change, and transparency: Reviewing the literature on carbon disclosure. Organization & Environment, 28(1), 80–102. https://doi.org/10.1177/1086026615575542

- Hersoug, B., Mikkelsen, E., & Karlsen, K. M. (2019). “Great expectations” – Allocating licenses with special requirements in Norwegian salmon farming. Marine Policy, 100, 152–162. https://doi.org/10.1016/j.marpol.2018.11.019

- IPCC. (2022). Climate Change 2022: Impacts, Adaptation, and Vulnerability. Cambridge University Press.

- Iversen, A., Asche, F., Hermansen, Ø., & Nystøyl, R. (2020). Production cost and competitiveness in major salmon farming countries 2003–2018. Aquaculture, 522, 735089. https://doi.org/10.1016/j.aquaculture.2020.735089

- Jansen, P. A., Kristoffersen, A. B., Viljugrein, H., Jimenez, D., Aldrin, M., & Stien, A. (2012). (1737). Sea lice as a density-dependent constraint to salmonid farming. Proceedings of the Royal Society B, 279(1737), 2330–2338. https://doi.org/10.1098/rspb.2012.0084

- Kumar, G., & Engle, C. R. (2016). Technological advances that led to growth of shrimp, salmon, and tilapia farming. Reviews in Fisheries Science & Aquaculture, 24(2), 136–152. https://doi.org/10.1080/23308249.2015.1112357

- Leaton, J. (2011). Unburnable carbon–Are the world’s financial markets carrying a carbon bubble? Carbon Tracker Initiative, 6–7. http://www.carbontracker.org/wp-content/uploads/2014/09/Unburnable-Carbon-Full-rev2-1.pdf (Investor Watch, 2011).

- Lebel, L., Jutagate, T., Thanh Phuong, N., Akester, M. J., Rangsiwiwat, A., Lebel, P., Phousavanh, P., Navy, H., Navy, H., Soe, K. M., & Lebel, P. (2021). Climate risk management practices of fish and shrimp farmers in the Mekong region. Aquaculture Economics & Management, 25(4), 1–23. https://doi.org/10.1080/13657305.2021.1917727

- Lewis, B. W., Walls, J. L., & Dowell, G. W. (2014). Difference in degrees: CEO characteristics and firm environmental disclosure. Strategic Management Journal, 35(5), 712–722. https://doi.org/10.1002/smj.2127

- Luo, L., Lan, Y.-C., & Tang, Q. (2012). Corporate incentives to disclose carbon information: Evidence from the CDP Global 500 report. Journal of International Financial Management & Accounting, 23(2), 93–120. https://doi.org/10.1111/j.1467-646X.2012.01055.x

- Luthman, O., Jonell, M., & Troell, M. (2019). Governing the salmon farming industry: Comparison between national regulations and the ASC salmon standard. Marine Policy, 106, 103534. https://doi.org/10.1016/j.marpol.2019.103534

- Misund, B. (2017). Financial ratios and prediction on corporate bankruptcy in the Atlantic salmon industry. Aquaculture Economics & Management, 21(2), 241–260. https://doi.org/10.1080/13657305.2016.1180646

- Naylor, R. L., Kishore, A., Sumaila, U. R., Issifu, I., Hunter, B. P., Belton, B., Bush, S. R., Cao, L., Gelcich, S., Gephart, J. A., Golden, C. D., Jonell, M., Koehn, J. Z., Little, D. C., Thilsted, S. H., Tigchelaar, M., & Crona, B. (2021). Blue food demand across geographic and temporal scales. Nature Communications, 12(1), 1–14. https://doi.org/10.1038/s41467-021-25516-4

- Norwegian Directorate of Fisheries. (2022). Statistikk fra akvakultur [Aquaculture statistics]. https://www.fiskeridir.no/English/Aquaculture/Statistics

- Norwegian Seafood Council. (2022). Open reports [Åpne rapporter]. https://seafood.no/markedsinnsikt/apne-rapporter/

- Nygård, R. (2020). Trends in environmental CSR at the oslo seafood index: A market value approach. Aquaculture Economics & Management, 24(2), 194–211. https://doi.org/10.1080/13657305.2019.1708996

- Oglend, A., & Sikveland, M. (2008). The behaviour of salmon price volatility. Marine Resource Economics, 23(4), 507–526. https://doi.org/10.1086/mre.23.4.42629677

- Olaussen, J. O. (2018). Environmental problems and regulation in the aquaculture industry. insights from norway. Marine Policy, 98, 158–163. https://doi.org/10.1016/j.marpol.2018.08.005

- Osmundsen, T. C., Almklov, P., & Tveterås, R. (2017). Fish farmers and regulators coping with the wickedness of aquaculture. Aquaculture Economics & Management, 21(1), 163–183. https://doi.org/10.1080/13657305.2017.1262476

- Parmar, B. L., Freeman, R. E., Harrison, J. S., Wicks, A. C., Purnell, L., & De Colle, S. (2010). Stakeholder theory: The state of the art. Academy of Management Annals, 4(1), 403–445. https://doi.org/10.5465/19416520.2010.495581

- Patten, D. M. (2002). The relation between environmental performance and environmental disclosure: A research note. Accounting, Organizations and Society, 27(8), 763–773. https://doi.org/10.1016/S0361-3682(02)00028-4

- Pincinato, R. B. M., Asche, F., & Roll, K. H. (2021). Escapees in salmon aquaculture: A multi-output approach. Land Economics, 97(2), 425–435. https://doi.org/10.3368/le.97.2.425

- Reid, E. M., & Toffel, M. W. (2009). Responding to public and private politics: Corporate disclosure of climate change strategies. Strategic Management Journal, 30(11), 1157–1178. https://doi.org/10.1002/smj.796

- Sikveland, M., Tveterås, R., & Zhang, D. (2021). Profitability differences between public and private firms: The case of Norwegian salmon aquaculture. Aquaculture Economics & Management, 2021, 1–25. https://doi.org/10.1080/13657305.2021.1970856

- Sikveland, M., & Zhang, D. (2020). Determinants of capital structure in the norwegian salmon aquaculture industry. Marine Policy, 119, 104061. https://doi.org/10.1016/j.marpol.2020.104061

- Smith, M. D., Roheim, C. A., Crowder, L. B., Halpern, B. S., Turnipseed, M., Anderson, J. L., Asche, F., Bourillón, L., Guttormsen, A. G., Khan, A., Liguori, L. A., McNevin, A., O’Connor, M. I., Squires, D., Tyedmers, P., Brownstein, C., Carden, K., Klinger, D. H., Sagarin, R., & Selkoe, K. A. (2010). Sustainability and global seafood. Science, 327(5967), 784–786.

- Solberg, B., Moiseyev, A., Hansen, J. Ø., Horn, S. J., & Øverland, M. (2021). Wood for food: Economic impacts of sustainable use of forest biomass for salmon feed production in Norway. Forest Policy and Economics, 122, 102337. https://doi.org/10.1016/j.forpol.2020.102337

- Stanny, E., & Ely, K. (2008). Corporate environmental disclosures about the effects of climate change. Corporate Social Responsibility and Environmental Management, 15(6), 338–348. https://doi.org/10.1002/csr.175

- Stolbova, V., Monasterolo, I., & Battiston, S. (2018). A financial macro-network approach to climate policy evaluation. Ecological Economics, 149, 239–253. https://doi.org/10.1016/j.ecolecon.2018.03.013

- Straume, H.-M. (2017). Here today, gone tomorrow: The duration of Norwegian salmon exports. Aquaculture Economics & Management, 21(1), 88–104. https://doi.org/10.1080/13657305.2017.1262477

- Sullivan, R., & Gouldson, A. (2012). Does voluntary carbon reporting meet investors’ needs? Journal of Cleaner Production, 36, 60–67. https://doi.org/10.1016/j.jclepro.2012.02.020

- Sun, J., Mooney, H., Wu, W., Tang, H., Tong, Y., Xu, Z., Huang, B., Cheng, Y., Yang, X., Wei, D., Zhang, F., & Liu, J. (2018). Importing food damages domestic environment: Evidence from global soybean trade. Proceedings of the National Academy of Sciences of the United States of America, 115(21), 5415–5419. https://doi.org/10.1073/pnas.1718153115

- TCFD. (2017). Recommendations of the task force on climate-related financial disclosures.

- Torrissen, O., Jones, S., Asche, F., Guttormsen, A., Skilbrei, O. T., Nilsen, F., Horsberg, T. E., & Jackson, D. (2013). Salmon lice–impact on wild salmonids and salmon aquaculture. Journal of Fish Diseases, 36(3), 171–194. https://doi.org/10.1111/jfd.12061

- Tveteras, S., & Asche, F. (2008). International fish trade and exchange rates: An application to the trade with salmon and fishmeal. Applied Economics, 40(13), 1745–1755. https://doi.org/10.1080/00036840600905134

- Wegener, M., Elayan, F. A., Felton, S., & Li, J. (2013). Factors influencing corporate environmental disclosures. Accounting Perspectives, 12(1), 53–73. https://doi.org/10.1111/1911-3838.12007

- Wri, W. (2011). Greenhouse Gas Protocol Corporate Value Chain (Scope 3) accounting and reporting standard. World Resources Institute and World Business Council for Sustainable Development.