ABSTRACT

This paper explores the processes behind legitimacy building and its role in new path creation and the path transformation or the ‘de-locking’ of an established industry. We use a mixed-methods approach and focus on the emergence of ‘New Space’ or Space 2.0 in the UK, a new-to-the-world industry, with radically different products and/or conventions. Legitimation of new product categories is essential to enable future adoption by regulators and consumers. Our findings suggest that this is not a linear process but involves interlayering, or complex feedback loops, between three distinct types of legitimacy building: regulatory, normative, and cognitive. Failure in some of these feedback loops, for example, problems with altering regulatory legitimacy, would prevent the formation of new industrial pathways with significant implications for the development of new-to-the-world and new-to-region industries.

1. Introduction

New industries emerge in response to rapid technological and process innovations and digitalisation, that is transforming existing industries at an unprecedented rate. Economic geography, and regional studies, have emphasised the role of multi-scalar actors, institutions, and agents of change in processes of new industry emergence (Breul et al. Citation2021; Bryson and Ronayne Citation2014; Frenken and Boschma Citation2007; Grillitisch et al. Citation2018), highlighting the links between regional economic diversification, relatedness, and pre-existing capabilities (Boschma et al. Citation2017; Salder et al. Citation2023).

‘New Space’, or Space 2.0, is the new private-sector space industry, led by space entrepreneurs or ‘Astropreners’. Space 2.0 produces very different products to Space 1.0 which is public sector led and commenced with the space race between the then USSR and the U.S (Fahey, Citation2019; Pelton, Citation2019; Pyle Citation2019). The private sector led Space 2.0 industry is new-to-the-world, new-to-the-UK and new to UK regions (Binz and Gong Citation2021). Space 2.0 involves new firm creation, diversification of existing Space 1.0 firms, a new geography and policy environment, and related legitimation processes. Its technologies focus on developing ‘faster, better and cheaper access to Space’ and include small satellites, satellite mega-constellations, and new launch vehicles (Quintana Citation2017). Space 2.0 represents the emergence of a new industrial pathway, built on existing national assets that are combined with the creation of new assets and supported by new legitimation processes. In countries such as the UK and US, Space 1.0 created an industrial pathway based on large incumbent companies such as Airbus Defence and Space UK with a conservative approach to innovation focusing on government-funded contracts (Billing and Bryson Citation2019). Space 2.0 is the outcome of a new path creation process, with a very different set of technologies, mix of firms and products. Space 2.0 emerged partly built on existing assets, resources and competencies of established companies and institutions involved in Space 1.0, and partly involved the creation of new assets and firms. These transformative shifts were closely intertwined with intricate processes of legitimacy building.

This aligns with the recent focus in the literature on the importance of legitimacy building required for the emergence of new industries (Benner Citation2024; Blažek, Kadlec, and Květoň Citation2023; Gong Citation2020; Hassink et al. Citation2019; Jolly and Hansen Citation2021; Kogler et al. Citation2023; Sotarauta and Grillitsch Citation2023). Legitimacy can be ascribed to different kinds of entities, including individuals, organisations, business models, industries, and technologies (Markard, Wirth, and Truffer Citation2016). In organisational management, legitimacy is defined as ‘a generalized perception or assumption that the actions of an entity are desirable, proper, or appropriate within some socially constructed system of norms, values, beliefs, and definitions’ (Suchman Citation1995 573). An industry’s legitimacy depends on how well its products, processes and services are aligned with the institutional order in that sector or region and at that specific time (Binz and Gong Citation2021).

Industry legitimacy is not an ‘automatic’ outcome of an industry’s increasing market presence or success, but instead a result of organisational and ‘system-level’ agency, responsible for new path creation and overcoming institutional barriers (Binz et al. Citation2016; Gong Citation2020; Isaksen et al. Citation2019; Markard, Wirth, and Truffer Citation2016). Organisational and system-level agency involves different stakeholders (including innovators, investors, and regulators) and institutions, working at different spatial scales. Legitimacy building is an essential process for new ventures, technologies or industries since it mobilises their access to resources, regulatory support, and consumer acceptance, necessary for survival and growth (Bergek, Jacobsson and Sandén Citation2008; Markard, Wirth and Truffer Citation2016; Zimmerman and Zeitz Citation2002). Legitimacy is particularly important when a new sector introduces a radically different product category compared to existing products and/or conventions; resistance and lock-in must be overcome. Legitimation of new product categories is essential to enable their future adoption by regulators and consumers (Bork et al. Citation2015).

There are three different types of legitimacy: (i) cognitive – the degree to which the products/companies/pathways of a new industry are understood; (ii) normative – the degree to which an industry conforms with societal values and beliefs; and (iii) regulatory – the degree to which an industry is compliant with formal rules, laws, and regulations (Markard, Wirth, and Truffer Citation2016). To date, the literature on these three types has been theoretical with limited empirical research undertaken on understanding them in practice, the role of different actors in their development and how the three types interact.

This paper examines the inter-related processes behind the development of these three types of legitimacy and their role in the emergence of Space 2.0, to highlight the interlayering and complex interactions that exist within legitimation processes. This is a multi-scalar and multi-actor process requiring new forms of legitimation given the uncertainty related to an industry with radically different products and/or conventions (Billing and Bryson Citation2019; Rusten, Bryson, and Aarflot Citation2007). In this paper, we develop a comprehensive analytical framework to explore legitimacy building and new path development comprising five distinct elements.

To test the applicability of our proposed framework and to study the emergence and legitimacy building of Space 2.0 we adopt a mixed-methods approach. We use quantitative data on the spatial distribution of space firms and employment to explore the evolving geography of the UK space sector. In addition, the analysis is informed by 80 in-depth interviews which investigated legitimacy building processes for this new sector and its emerging spatial footprint. Interviewees are drawn from an expert pool across the Space 2.0 supply-chain and policy environment including manufacturers, subcontractors, operators, and government organisations.

We have three main findings. First, we highlight how the emergence of a new industry is a dynamic multi-actor process, which consists of five key elements. The fifth element involves iterative interactions between normative, cognitive, and regulatory legitimacy building processes, which have influenced the emergence of Space 2.0. Second, we found that the emergence of Space 2.0 was dependent on the simultaneous de-locking of existing normative and cognitive legitimacy that supported satellite supply and demand, as well as launch technologies, in Space 1.0. Third, we highlight that industrial formation requires a combination of multi-scalar processes based on the configuration of cognitive, normative, and regulatory legitimacy and this might be a translocal process.

We make three contributions to debates in economic geography and regional studies on new industry emergence. First, we build an analytical framework based on established concepts (legitimacy plus de-locking plus regional/sub-national aspects) to help us understand legitimacy building with a particular reference to the space sector. This framework reconciles the conceptual confusion that existed regarding the evolution of legitimation pathways and the ways in which different types of legitimation processes are expected to support the emergence of new industries (Gong Citation2020; Hassink, Isaksen, and Trippl Citation2019; Jolly and Hansen Citation2021). Secondly, our paper showcases the role multi-scalar actors play in emerging industry legitimation, highlighting interactions between regional, national, and international institutions. These roles have been under-identified so far and yet play a critical role in industry emergence. Third, we undertake the first in-depth analysis of the emergence of Space 2.0 in the context of legitimacy building. Examining the legitimation processes that led to Space 2.0 is important given the increasing dependence of socioeconomic functions on satellites (including communication, navigation, and earth observation), as well as the commonalities of the sector with the evolution of other advanced manufacturing sectors (Billing and Bryson Citation2019).

This is a study of one sector; however, the study does highlight that this type of sector development process is complex as it involves a bundle of five elements. The balance between elements might be different in other contexts, but the paper alerts scholars, and policymakers, to the need to explore these five processes. There are policy lessons here and lessons for other sectors on the dynamic process of legitimacy building and the configuration of different actors and processes. Specific policies may be designed to target the development of legitimacy building to support the emergence of new industries.

The paper has five parts. First, we discuss the relevant economic geography and regional studies literature on emerging industries and position our paper by developing a framework for understanding legitimacy building processes. Second, we introduce the case study and methodological approach. Third, we examine regional data on the sector’s employment and establishment counts, identifying trends in the emergence and regional distribution of Space 2.0 in the UK. We then apply our new analytical framework to understand how the complex interlayering of three distinct, but linked, types of legitimacy – normative, cognitive, and regulatory influenced the development of Space 2.0. Finally, we conclude the paper and outline future avenues for research.

2. Industrial path development, agency, and legitimacy

Conceptually, we develop an analytical framework that integrates five different elements. Our point of departure is the literature on the trajectories of new industrial path development, which clarifies how path development processes may take multiple forms (Blažek and Kveton Citation2021; Grillitsch et al. Citation2018; Isaksen et al. Citation2019). These include, but are not limited to: (i) ‘new path creation’ - the emergence of new industries based on new technologies, business models or social innovation; (ii) ‘unrelated path diversification’ – diversification into a new industry based on unrelated variety; (iii) ‘path branching’ – diversification into a new industry based on related variety; (iv) ‘path upgrading’ – transition of companies within a given industry into higher value-added activities; (v) ‘path extension’ – incremental innovation in existing industries (Blažek, Kadlec, and Květoň Citation2023). These trajectories may require varying degrees of ‘de-locking’ or overcoming lock-in, which can be deliberate and intentional (designed interventions to break path or switch location) or chance and accidental (unpredictable external shocks and random events break an old trajectory and launch a new path) (Abdres et al. Citation2023; Martin and Sunley Citation2006; Martin Citation2014). Lock-in can refer to technological lock-in, as well as, being locked into pre-existing routines, norms, business models and regulatory regimes. Emerging sectors are often the outcome of a mixture of these path development processes. For example, a new industry may include both established firms that have diversified from other industries through a path branching process and new start-ups born from unrelated knowledge and resources (Lee and Fong Citation2019). An additional dimension refers to the distinction between industries that are ‘New-to-the-World’ (NTW) versus ‘New-to-a-Region’ (NTR) (Binz and Gong Citation2021).

The second element of our analytical framework relates to the geography of new industrial path development (Martin Citation2010; Martin and Sunley Citation2006; Plechero et al. Citation2020). On the one hand, the location of newly emerging industries may be less constrained since sector-specific institutions would not yet influence locational decisions (Boschma Citation1997; Hassink, Isaksen, and Trippl Citation2019). On the other hand, the emergence of new industries is often dependent on pre-existing local assets and institutions (Salder and Bryson Citation2019). Thus, the ‘location of emerging industries is not a random process and varies from industry to industry’ (Hassink, Isaksen, and Trippl Citation2019, 1637). Both approaches are useful in explaining the emergence and location of new industries; some firms emerge in locations benefiting from existing industrial paths, and others are more footloose and emerge in other geographical settings.

The third element of our analytical framework concerns the preconditions that influence the development of new industries, including the presence of dense regional networks and structures, a combination of different knowledge bases, a vibrant entrepreneurial culture, and a concentration of innovative firms (Jolly, Grillitsch, and Hansen Citation2020; Rusten and Bryson Citation2010). Our understanding of the relevance of regional strengths to path development comes from the regional innovation system (RIS) literature. The RIS literature highlights the need for considering multiple types of actors to understand the development of industries and regions (Jolly et al. Citation2020). These include firm actors, but also ‘facilitating’ or ‘intermediary’ actors (including universities, educational facilities, business development organisations, industry organisations, cluster organisations, science parks and incubators). Additionally, there are ‘public policy actors’ which may affect the development of new industrial paths by promoting new ideas and designing/implementing supportive policies to address lock-in (Blažek and Květoň Citation2022).

The fourth element are microlevel processes that drive transformations and reconfigurations of innovation systems, including two forms of agency (firm/organization or system) exercised by several types of actors (Gardner and Bryson Citation2021; Hassink et al. Citation2019). Agency is a form of social engagement and refers to actions or interventions of an individual or set of actors, and the intended and unintended outcomes of such actions. Isaksen et al. (Citation2019) and Hassink et al. (Citation2019) distinguished between firm- and system-level agency. Firm-level agency includes individuals engaged in firm-level actions such as startup formation (Grillitsch et al. Citation2022; Isaksen et al. Citation2019). Blažek and Květoň (Citation2022) argue that ‘organizational-level agency’ is a more suitable term than ‘firm-level agency’, since the actors involved are not limited to firms (Blažek and Květoň Citation2022, 1484). System-level agency can be understood as ‘agency directed beyond the boundaries of one’s own organisation’ (Blažek, Kadlec, and Květoň Citation2023, 7). These actions shape the innovation system either territorially, sectorally, or technologically (Benner Citation2024). Firms can engage in both organisational-level agency, but also in activities corresponding to system-level agency (Benner Citation2024).

The inclusion of both types of agency in our analytical framework addresses a call by Hassink et al. (Citation2019) to employ a multi-scalar and multi-actor approach to comprehend regional industrial path development. This helps avoid the narrow conclusion that regional industrial path development is a technology-driven and firm-led process (Blažek, Kadlec, and Květoň Citation2023). Agency can be constructive or destructive in relation to structures, since it can create new institutions or destroy existing ones (Benner Citation2024). Grillitsch et al. (Citation2022) combines firm and system-level agency with a typology of three outcomes: (i) innovative entrepreneurship (i.e. breaking with established patterns of doing things and working towards the establishment of new ones), (ii) institutional entrepreneurship (initiating processes that contribute to the creation of new institutions or the transformation of existing ones) and, (iii) place-based leadership (launching interactive work that crosses organisational boundaries and enhances various stakeholder engagement in the development process. All these activities can lead to ‘both intended and unintended consequences and changes’ (Blažek and Květoň Citation2022, 1485), which to Benner (Citation2024) warrants further research to fully understand.

One function of organisational-level and system-level agency is building, maintaining, or disrupting the legitimacy of sectors and technologies (Benner Citation2024; Vanchan, Mulhall, and Bryson Citation2018). This paper focuses on the macro – micro dynamics of legitimacy building, and this is the fifth element of our analytical framework. As such, we adopt a granular approach that distinguishes between three different types of legitimacy: (i) cognitive; (ii) normative; and (iii) regulatory. These three types of legitimacy are taken from Markard et al. (Citation2016) and based on works from Aldrich and Fiol (Citation1994) and Suchman (Citation1995).

We aim to highlight the critical role of all three types of legitimacy in overcoming some of the liabilities related to newness and the reworking of existing supply, demand, and governance conventions (Billing and Bryson Citation2019). For an industry to form, pioneers must create a knowledge base that eventually becomes credible as new conventions, including regulations, are established, and accepted. The knowledge base, or the degree to which the products/services (including new technological capabilities) are understood, represents a form of cognitive legitimacy, and the degree to which these are credible and conform with conventions, societal values and beliefs is understood as normative legitimacy. Normative legitimacy is achieved through processes intended to create new forms of consumer demand and must be enabled by some type of supportive institutional environment including regulatory legitimation. Regulatory legitimacy includes compliance with formal rules, laws, and regulations as well as the financial systems expectations and conventions, for example, rules/conventions related to providing insurance cover. Creating new forms of consumer demand and developing a knowledge base of new products/services, typifies institutional entrepreneurship, including related forms of legitimisation, that help create supportive narratives around a newly emerging socio-technical configuration (Binz and Gong Citation2021, 608). These processes are all supported by the wider systemic environment or ‘system-level agency’, including supporting actors (government, consultants, investors, universities). These actors might be co-located within a regional cluster (agglomerations with supporting infrastructure) or located elsewhere, but still accessible, for example, through temporary clustering (Henn and Bathelt Citation2015).

These three types of legitimacy are mutually supportive with alterations in normative forcing regulatory changes or vice versa, and technological development that is cognitive altering demand and challenging existing conventions. This is not a linear process, and the legitimation process can commence at any point in this trilogy of processes. Alternatively, all alterations in normative, regulatory, and cognitive legitimacy building might occur simultaneously. Once established, legitimacy is path-dependent and is a resource in its own right, and a route to acquiring other critical resources including access to finance (Vestrum, Rasmussen, and Carter Citation2017). To Binz et al. (Citation2016, 3) ‘legitimacy is actively built up through the interplay of different actor groups in the early stage of a new technology and industry’. It is a social construct that highlights the importance of cultural support and endorsement from different stakeholders to emerging industries in overcoming the ‘liability of newness’ (Jolly and Hansen Citation2021). This legitimation process includes adjustments to consumer demand and behaviours, regulations, and existing routines. We suggest that system-level and organisational-level agency are enablers of normative, cognitive, and regulatory legitimacy for Space 2.0.

3. Case selection and research methods

The approach chosen to illustrate and validate our conceptual framework is based on a case study design of the emergence of Space 2.0 in the UK. Our focus is on the UK upstream space sector or suppliers of space technology (spacecraft, launch equipment, satellites) as opposed to the ‘downstream’ which includes providers of satellite-enabled services (imaging, climate monitoring, navigation, and communications). Legitimation processes were expected to have played an important role in explaining the emergence of Space 2.0 given the risks related to the privatisation of space and the development of mass-produced satellites. The selection of this unique sector responds to Benner’s (Citation2024, 3) claim that ‘methodologically, the research agenda could benefit from empirical diversification’.

The origin of Space 1.0 lies in the 1950–71 rocket programme, developed as a product of 20th-century conflicts. Manufacturers of Space 1.0 products relied upon government and military procurement contracts for the design and fabrication of bespoke satellites. This industry then evolved to include more standardised commercial communication satellites. Communication satellites are the largest (size of a double-decker bus), heaviest, and most expensive satellites (Satellite Applications Catapult Citation2014). Usually, they operate in the geostationary band (35786 km above earth), which is the most expensive orbit into which to launch a satellite. As a result, the cost of failure is high and the incentives for disruptive innovation are low, and the preference is for proven technology (Billing and Bryson Citation2019). These satellites have low margins and limited demand with, on average, four orders per manufacturing company, per year. Space 2.0 reflects a revolutionary transition from the existing space industry in response to processes of legitimacy building. A new market for less durable, low mass and size (usually under 1,200 kg), and cheaper satellites emerged to provide real-time global imaging, security for the advanced data economy, navigation, and broadband connectivity. These satellites are usually launched in low earth orbit and come with reduced launch costs.

The country focus of this analysis is deliberate as despite cancelling its rocket launch programme in 1971, the UK has remained a leading international manufacturer of spacecraft and highly complex payloads, with strengths in high-end navigation systems, satellite communications and more recently small satellites (National Space Strategy Citation2021). These existing national assets, have supported the emergence of UK Space 2.0 firms in recent years, focused on developing faster, better, and cheaper access to space. Their emergence has been enabled by processes of legitimacy building, supported by organisational and system-level agency. This includes investment by the UK government in critical infrastructure, such as the new UK spaceport (Spaceport Cornwall), from which Virgin Orbit attempted its launch of the first orbital space mission from the UK and Europe, on the 9th January 2023.

To gain insights into the legitimacy processes that led to the emergence of Space 2.0 in the UK, we deployed a mixed-methods approach. Quantitative and qualitative data was integrated into a framework where the quantitative exploration set the background for the qualitative research that focussed on legitimacy building processes. First, regional data on employment and firm counts was used to identify trends in the emergence and geography of Space 2.0. This initial analysis confirmed that a new path creation process was on-going that required investigation given the sector’s wider societal significance. Regional data from the Office for National Statistics’ Business Register and Employment Survey and UK Business counts was explored. The former is a representative survey of 80,000 enterprises providing employment information by Standard Industrial Classification (SIC − 2007 revision) whilst the latter is an excerpt of the Inter-Departmental Business Register (IDBR), which is a registry of firms covering more than 90% of UK economic activity. The SIC codes included 30.3: Manufacture of air and spacecraft and related machinery; 33.16: Repair and maintenance of aircraft and spacecraft and 51.22: Space Transport. These codes ensured that the analysis focused on firms involved in Space 2.0. The complexity of operations within Space 2.0 suggests that solely focusing on these SIC codes would underestimate the size and importance of this sector. This is preferred to including related SIC codes, such as engineering or satellite telecommunication providers, which would skew the analysis by incorporating satellite broadcasters and consultancy services. Industry and employment dynamics were examined for Great Britain and sub-national geographies between 2010 and 2018.

Quantitative and qualitative insights were combined to obtain a more complete picture of the evolution, legitimation processes and dynamics of Space 2.0. Eighty in-depth interviews with participants (Appendix 1) from across the space sector were conducted to explore processes of legitimacy building and the emergence of Space 2.0. The interviews were conducted between November 2014 and July 2015. A stratified form of purposive sampling was deployed with the cases selected from the UK Space Directory (profiles and functions of UK satellite manufacturers). This sample was stratified by firm size (number of employees) and function. Two groups of manufacturing firms (28) were represented: (i) prime satellite manufacturers, who design satellites, configure procurement, and manage the final integration of components; and (ii) subcontractors, who supply materials, hardware components, and subsystems. This stratified approach helped to ensure maximum diversity of research participants. Additionally, operators and satellite application providers (30), and government organisations and regulators were interviewed (22).

The number of participants was flexible around the data needs of the research, with recruitment only ending when it was apparent that new data would not significantly add to theory development. The interviews ranged in length from thirty to ninety minutes and were semi-structured, consisting of a set of prearranged questions. These questions were divided into three parts: (1) background/product questions, (2) organisation and governance of production, and (3) regulation. Data collection was undertaken concurrently, with four stages of analysis (transcription, description, classification, and coding) ensuring any knowledge gaps were addressed. Initially, the research gap we set out to address and theories from the literature provided a set of codes. The analysis was not confined to these preliminary codes, as inductive codes were identified as new themes were observed. The interviews were treated in a confirmatory manner to test our conceptual perspective. New codes emerged as ‘sub-categories’ of the preliminary codes and identified new themes. There were several revisions to the coding, as their reliability was tested after being applied to multiple transcripts and checking for consistencies. These revisions did not involve removing codes from the coding manual but merging some categories (four in total) where appropriate.

The activities of Space 2.0 actors from beyond the UK are outside the scope of this study but the industry beyond the UK contributed to building legitimacy for Space 2.0 within the UK. UK Space 2.0 cannot be isolated from the global setting as activity elsewhere shapes outcomes in other places. The actions of companies located beyond the UK impacted on legitimacy building for UK Space 2.0, specifically in the context of launch, as the UK’s launch capability is not yet fully established, but also in the shift towards the development of a private sector-led space age.

4. The emergence of space 2.0 and the evolving geography of the UK space sector

Space 2.0 emerged partly built on existing assets, resources and competencies of established companies and institutions involved in Space 1.0, and partly involving the creation of new assets and firms. These transformative shifts were closely intertwined with intricate processes of legitimacy building.

The emergence of Space 2.0 in the UK was underpinned by all three types of legitimacy-building processes. These resulted from a series of strategic interventions, culminating in institutional and innovative entrepreneurship that ultimately drove transformative changes within the space industry (Grillitsch et al. Citation2022). The tangible outcome of this evolution was the birth of a novel sector known as Space 2.0, characterised by a noticeable uplift in the number of firms operating in the upstream space domain and reduction in the size of the average space business. Employment in the sector shows sign of flux in pre-existing regional clusters whilst firm data also document the emergence of vibrant new regional clusters (Appendix 2).

At the national level, the sector experienced relatively slow employment growth (4% total between 2010–2018) whilst at the same time, the number of firms grew by 150% from 1,075 to 2,695. This highlights a significant reduction in the size of firms with average employment per firm at 92 in 2010 and 38 employees in 2018. This is indicative of the transition from Space 1.0 with larger firms, dependent on heritage and vertically integrated production processes, to Space 2.0, with smaller, less vertically integrated firms specialising in smaller sized products or satellite components.

Space 2.0 has an uneven regional geography with the North West and South West accounting for the largest number of jobs in 2010 (37% of the sector’s total jobs) whilst the South East had the largest number of space firms with 235 (22% of total firms). Between 2010 and 2018, the North West lost jobs but more than doubled its number of space businesses. On the other hand, the East Midlands experienced an increase of 60% from 13,150 to 21,000 (accounting for the largest number of jobs in the sector, 20% of the sector’s total) whilst falling behind the national growth rate in number of businesses.

Tracking Space sector growth between 2010 and 2018 shows a mixture of path dependence and the emergence of new clusters. Employment data suggests that growth primarily occurred in relatively strong regions such as the East Midlands (moving from 13% to 20% of the sector’s jobs). These changes in the East Midlands region reflect the influence of a regional alignment of actors and institutions intended to support the growth of a well-established sector in the region. Leicester University emerged as a global leader in satellite technology, facilitating knowledge exchange via temporary and proximate clustering. This has since been reinforced by the commitment to build a £75million Space Park by a partnership involving the University of Leicester, Leicester City Council, and the Leicestershire Enterprise Partnership. This park will be ‘a significant global hub for businesses, researchers, academia and innovation’ (UKSA Citation2019). Firm data on the other hand show that new space businesses were split between pre-existing clusters (i.e. the South East) and new clusters such as Wales that doubled its share of total space firms from 60 in 2010 to 300 in 2018. This is an example of newly emerging industries being less constrained in their locational decisions since sector-specific institutions do not yet influence locational decisions (Boschma Citation1997; Hassink, Isaksen, and Trippl Citation2019). In Wales, this was based around photonics, secure communications, and software systems (Gov.Wales Citation2019).

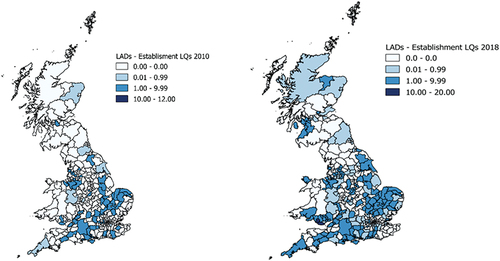

To track the local specialisation of the sector, we turn to Location Quotients (LQ).Footnote1 LQs provide a comparison of employment and/or the number of firms in an area compared to the national average. Higher concentrations (LQs >1) indicate specialisation of an area in the Space sector whilst LQs < 1 suggest that a local area does not have a significant concentration of Space sector activity. LQs take into consideration the size of local economic activity, providing insight into relative concentration or dispersion and the importance of the sector.

Our firm data allows us to map establishment LQs (Appendix 3) in Local Authority Districts that offer greater geographical granularity compared to regions. These maps highlight the increase in business population and the geographical expansion associated with the emergence of Space 2.0. In 2010, 65 Local Authority Districts (LADs) had LQs greater than one whilst in 2018 this figure had almost doubled to 128. Most of this growth occurred at pre-existing locations or at LADs bordering established clusters, benefitting from localised spillovers. The exception is the emerging cluster southwest of Glasgow.

Consequently, we see that Space 2.0 was partly built on existing assets, resources and competencies of established companies and institutions involved in Space 1.0, and partly involved the creation of new assets and firms. These transformative shifts were closely intertwined with intricate processes of legitimacy building. The next section explores the legitimacy building process that led to the emergence of Space 2.0.

5. Legitimacy building

The section distinguishes between different legitimation processes and explores the inter-related processes behind the development of three types of legitimacy: normative, cognitive, and regulatory. We approached our analysis by applying an analytical framework comprising of five distinct but related elements. The first and second element concerns the diverse trajectories of new industrial path development and geographical aspects of new industrial path development. These were explored in the previous section, which tracked space sector growth between 2010 and 2018 to highlight a mixture of path dependence and the emergence of new clusters.

The third element of our analytical framework addresses the preconditions associated with the birth and evolution of emerging industries. This encompasses factors like the presence of regional networks and a diverse knowledge infrastructure. The fourth element highlights the importance of micro-level processes that drive transformations and reconfigurations within innovation systems: organisational-level and system-level agency. The fifth and final component of our analytical framework, is dedicated to exploring the macro – micro dynamics of legitimation within the context of industrial path development. The next sections explore the macro – micro dynamics of three types of legitimacy building: normative, cognitive, and regulatory. This is a multi-scalar and multi-actor process influenced by the presence of regional networks, associated knowledge infrastructure (the third element of our analytical framework) and organisational-level and system-level agency (the fourth element of our analytical framework). All five elements of our analytical framework interact and have enabled Space 2.0 to emerge as a distinct and new space industry.

6. Normative legitimacy

Normative legitimacy is the degree to which an emerging industry conforms with societal values and beliefs – addressing challenges and needs. It represents the standards by which an institution is judged. This is where social values and beliefs come in. One reading of Space 2.0 is that Space 1.0 was based on a set of values linked to national security (military) combined with space as a place for scientific research. It became a place for large business (expensive satellites). Space 1.0 was exclusionary. Space 2.0 challenged the links between space, military and science and highlighted that space had much wider societal relevance. This then shifts from an exclusionary to inclusionary set of values – space for all. This shift in values from Space 1.0 which was focussed on enabling a very narrow set of national priorities to one in which Space 2.0 results in a type of democratisation of space as Space 2.0 broadens access.

Changes at the firm-level (both consumers and producers), in the context of the emergence of Space 2.0, were in response to new technological solutions. One important alteration behind the emergence of Space 2.0 was the reduction in launch costs that occurred over the last ten years. Formed in 2002, the American launch company SpaceX has been at the forefront of this shift, by dramatically reducing costs with innovations in reusable rocket technology, off-the-shelf components, and in-house production of 70% of their spacecraft (reducing dependency on expensive suppliers). SpaceX charges $4,653 per kilogram to launch a telecommunications satellite into orbit while traditional aerospace companies charge up to $39,000 per kilogram (Fernholz Citation2014). The emergence of more affordable launch options opened the market for smaller-scale satellite manufacturers, who innovated in miniaturisation and the standardisation of production processes to reduce product costs. This is an example of organisational-level agency.

Facilitating or intermediary actors had an important role to play, this included universities. The best example of the impact of universities on legitimising 2.0 technologies in the UK is ‘SSTL’. In 1970, academics at the University of Surrey experimented with creating satellites using off-the-shelf components. In 1981 their first satellite, UoSAT-1, was launched by NASA demonstrating the proof of concept that relatively small, sophisticated, and inexpensive satellites could be built rapidly, but still form a powerful communications network. This paired with the realisation that many launch rockets had spare payload capacity that could be used to launch micro-satellites. This led to the formation of Surrey Satellite Technology Ltd (SSTL), a spin-out company established by the University that was eventually acquired in 2008 by EADS, the European aerospace and defence company. SSTL was behind the development of a ‘new space race’, based on the principle of the smaller the satellite the better. Thus, the origins of the revolution in satellite design and related supporting legitimacy building that were fundamental to the emergence of Space 2.0 are based in the UK, whilst supportive and enabling innovations in launch occurred in the US. SSTL developed and tested the technology and facilitated alterations in normative and subsequently regulatory legitimacy that led to the emergence of a new industrial pathway – Space 2.0. In this new space economy, small firms and satellites could succeed. SSTL continues to function as an independent UK company with its own brand and distinctive approach to the design and launch of satellites benefitting from enhanced links with the University of Surrey.

The outcome of this process of legitimacy building was the development and market acceptance of a new product – smaller satellites – that were positioned in lower orbits reducing risks and launch costs. These smaller satellites could be launched into Low-Earth orbit because of innovations in lower-cost ground antenna systems capable of satellite tracking, as well as, advanced digital coding systems, enabling enhanced transmission capabilities and the use of new spectrum frequencies. It is significant that these satellites can operate in Low-Earth orbit (400 km to 1,200 km above Earth), since the lower altitude allows for improved latency and accuracy of signals travelling between the Earth and the satellites (Quintana Citation2017). The combination of these disruptive innovations has led to new firm formation (focussed on the production of smaller satellites) and facilitated alterations in normative and regulatory legitimacy.

Cost-effective launch solutions and the increasing affordability of mass-producing thousands of small satellites enabled and encouraged new venture formation. Manufacturers of smaller satellites that have formed in response to disruptive innovations include three UK firms: SSTL (established 1985), AAC Clyde Space (established 2005) and Oxford Space Systems (established 2013). These three firms are now established global market leaders accounting for 40% of the global total of satellites with dimensions as small as 10x10x10 centimetres. These firms focus on producing ‘hundreds of thousands of identical satellites per year’, which is very different from the ‘tens of large, bespoke satellites’ produced per year by Space 1.0 manufacturers (Quintana Citation2017). These satellite constellations are financed by new privately UK funded operators, such as Avanti and One Web, who aim to build networks of up to a thousand low earth satellites. The global coverage of mega-constellations promises ‘always on’ broadband, imagery, and tracking information. Smaller satellites have reduced capacity but lower launch costs including launch from non-equatorial locations. Lower costs reduce financial risks encouraging innovation that is path changing creating opportunities to overcome the type of technological lock-in that was associated with Space 1.0 (Billing and Bryson Citation2019). With Space 1.0 satellites ‘you have to manage risk more closely, use older, special components’ (M.Prime2a). The lifetime of these smaller satellites is much reduced because of greater atmospheric drag. The shift in normative legitimacy was towards market acceptance of lower cost smaller satellites that need to be replaced more frequently, increasing the market size, and leading to new firm formation and the creation of new firm and sector routines and conventions. This increase in the size of the space industry then resulted in enhanced political attention leading to alterations at the ‘system-level’ (changes to the wider systemic environment or system-level agency). Alterations in regulatory legitimisation then reinforced the normative legitimacy that the firms were building through their disruptive innovations,

An example of system-level agency was the development of the UK Space Innovation Strategy (2010) by Government, academia, and business stakeholders. This aligned with the creation of the UK Space Agency and the subsequent formulation of a National Space Policy (2015), both focussing on the delivery of new satellite-enabled applications. This had a significant impact on the extent to which Space 2.0 product categories (or technologies) are considered appropriate to be adopted on a large-scale. Since the 2010 Space Innovation Growth Strategy, the UK government has committed to increasing R&D expenditure on emerging space technologies, doubling national funding for space programmes and technologies to £550 m. This financial support has been part of the ‘renaissance’ of the UK Government’s interest in the UK space sector since 2012. These grants enabled Space 2.0 firms to develop rapidly. Without grants the firms ‘limited’ financial resources would have restricted growth, since borrowing from private-sector lenders to support innovation came with expectations of ‘very high returns on investment’ (Interview_SystemsManufacturer1a). These government grants are justified by expected rates of return from future tax payments and the contributions to the ‘public good’ from satellite-enabled applications. This example is evidence of where public policy actors drive system-level agency, related to the building of normative legitimacy.

There is thus a shift in motivation of those working behind Space 2.0 that reflects this alteration in normative legitimacy. There is a two-way process at work here. On the one hand, developments in smaller satellites signposted that this shift in legitimacy was possible. Thus, the conditions for Space 2.0 emerged that were then, on the other hand, reflected back on alterations in values. One could argue that the first innovators challenged the normative legitimacy that underpinned Space 1.0 and the outcome was the development of a new normative legitimacy that underpinned Space 2.0. The ‘space for all’ value required an alteration in the cost structure – this was a two-way process.

7. Cognitive legitimacy

The knowledge base or the degree to which these disruptive innovations and their commercial possibilities have become understood (cognitive legitimacy) is based on the crafting of narratives around a newly emerging socio-technical configuration (Binz and Gong Citation2021). These narratives have been created by organisational and system-level agency undertaken by supportive external actors. These actors might be co-located within a regional cluster (agglomerations with supporting infrastructure) or located elsewhere, but still accessible, for example, by temporary clustering (Henn and Bathelt Citation2015). For example, Universities played a central role in developing cognitive legitimacy, through generating expert and related knowledge. This knowledge is ‘tapped into’ through technical papers, conference presentations and professional licencing agreements (Interview_DataApplications4). There is significant cross-over between normative and cognitive legitimacy here, since the knowledge gained contributes to both disruptive innovation, as well as understanding the societal impacts of the emerging socio-technical configuration. UK satellite firms often interact with universities, which are not always within close proximity, since they are chosen by specialism and expertise. For example, one firm “deals with about six or eight universities (Interview_DataApplications2).

Inter-firm exchanges were another key driver behind the cognitive legitimacy building process that led to Space 2.0. Interactions and collaborations with other firms maximised the resources available to Space 2.0 firms. At the same time, technological innovations have become accepted by producers and consumers through discussion and debate in regional clusters. The primary example in the UK is the Harwell space cluster, situated south of Oxford. Harwell is the location for 110 space 2.0 companies and the Catapult Satellite Applications Centre; the Rutherford Appleton Laboratory research and test facility; ESA’s ECSAT centre; and ESA’s space business incubator (which supports start-up companies with funding and workspace). This concentration of satellite organisations provides networking opportunities for co-located companies and for firm representatives visiting this cluster. This networking facilitates engagement with political networks involved in influencing the reconfiguration of regulatory legitimacy, as well as building cognitive legitimacy. Network formation is supported by opportunities for frequent face-to-face meetings and the exchange of ‘tacit’ knowledge. Additionally, geographic proximity increases the chance of ‘unexpected and spontaneous encounters’ (Bathelt and Turi Citation2011 525). These chance encounters are particularly valuable for start-up companies leading to increasing return effects.

Alternative opportunities for discussion and debate occur via events organised by the Satellite Applications Catapult Centre and the UK Space Agency. These organisations are responsible for annual and often monthly Space 2.0 meetings and conferences. These events vary in purpose and participant composition but generally serve as platforms for exchanging knowledge, generating ideas, forming new relationships, and creating and projecting legitimacy. For example, the 2019 UK Space Conference held in Newport (Wales) facilitated multi-actors to exchange ideas, share plans, develop relationships, and seek inspiration to thrive in the new space age. Meanwhile, the Catapult hosts a monthly coffee morning (‘Satuchino’) for engaged individuals or organisations who use satellite technology or data. These events are a specific type of temporary clustering (Henn and Bathelt Citation2015 105). The bringing together of industry actors and encouraging face-to-face interactions, supports the formation of new networks and strengthens existing ties facilitating institutional work that supports cognitive, normative, and regulatory legitimacy building processes. These events also present firms and individuals with opportunities to generate interest in their products, as well as the chance to integrate with other delegates and form networks with actual or potential customers and collaborators. Consequently, attending networking events is a strategic investment with Space 2.0 companies expecting new business opportunities to be identified. This is supported by virtual networking opportunities created by social media platforms, such as LinkedIn; the ‘Knowledge Transfer Network’ (KTN) site and the ‘UK Space Directory’ are virtual tools used to support networking by individuals involved in Space 2.0. These types of virtual clustering activities are particularly valuable for smaller, resource-constrained firms.

8. Regulatory legitimacy

The emergence of Space 2.0 was dependent on alterations in regulations that followed the disruptive innovations made by SSTL. Prior to these changes ‘new space’ players were locked out of the industry and lacked regulatory legitimacy. One example of significant regulatory change was the 2018 UK Space Industry Act, which enabled spaceflight to occur from the UK. This is the first significant step towards establishing a UK launch market for Low-Earth orbit satellites. In addition to the regulatory framework being in place, a list of potential UK spaceports was identified. A UK Spaceport would support potential cost savings, the avoidance of export control barriers, and would simplify the logistics for the launch of smaller satellites made in the UK. It would reduce time to launch as currently ‘operators wishing to launch satellites weighing more than 50 kg often need to wait between six and nine months to secure a launch contract’ (Quintana Citation2017). These changes have led to the emergence of launch operators in the UK (for example, Reaction Engines, Skyorra, Orbex) as well as, attracting manufacturers of smaller satellites.

The development of spaceports across the UK is part of a government strategy to capture 10% of the global space market by 2030 and this is enabled by alterations in regulatory legitimacy. Seven spaceport locations in the UK have been identified, but only one was operational by early 2023. The UK’s northern latitude location makes it an ideal launch location for satellites that require a polar orbit or sun-synchronous orbit; rockets launched from the UK are able to overcome the boost that comes from the Earth’s rotation as this reduces the further a launch site is located from the equator. Space 2.0 has provided an opportunity for the UK to capitalise on its geography to establish spaceports and this locational advantage includes the country’s long coast line and new spaceflight laws. The UK Government has developed new approaches to regulating and licencing new launch vehicles that are intended to ensure that the country will have three operational spaceports by the end of 2023. This process was one in which Space 1.0 in the UK experienced a process of de-locking through regulatory, normative, and cognitive legitimacy building. This was part of the institutional entrepreneurship required to support a newly emerging socio-technical configuration – Space 2.0 – and was part of system-level agency transformation. Prior to the emergence of Space 2.0, the UK had no locational advantage in launch, but processes related to cognitive legitimacy supported alterations in normative legitimacy that were facilitated by supportive regulatory legitimacy. All this is behind the emergence of a new UK regional geography of Space 2.0. This is an example of an unintended consequence.

In other cases, alterations in regulations are behind firm-level innovations. For example, the 1967 Outer Space Treaty (OST) is the principal treaty for regulating activities in outer space and outlines the core principles guiding UN member states in relation to their actions in space. One of the key principles of the OST is the registration of space objects. All satellites intended for launch must first be registered and allocated an orbital slot (if a geostationary satellite) and coordinated radio frequency spectrum. Additionally, a space licence is required before a satellite can be launched, and these are awarded by National Space Agencies. In the UK, as part of the licencing process, operators are required to obtain minimum liability insurance of €60 million. This protects the satellite operator and the UK ‘against the financial consequences of damages caused to a third party’ (Montpert Citation2011:283). In this instance, regulation lags firm-level innovation reflecting a tension between cognitive and normative legitimacy; for satellite mega-constellations (up to a thousand satellites) such insurance costs are unaffordable. Consequently, the UK Space Agency is considering new approaches to licencing mega-constellations. Any change to this form of regulatory legitimacy would represent a dramatic alteration further facilitating Space 2.0 pathway creation, altering the wider framework conditions supporting the industry, and encouraging changes in cognitive and normative legitimacy.

Another example of building regulatory legitimacy was the government's financial support for Space 2.0. This overlaps with the example of the UK Space Innovation Strategy (2010) referred to in the normative legitimacy section. Here the government is both nudging innovation through alterations in regulations and funding regimes and this then is an attempt to grow the market, but these nudges also cross over and are facilitated by regulatory change. Much of this funding was targeted at producers to encourage innovation. Government intervention is all about prioritisation based on trade-offs that are also underpinned (or distorted) by politics, and thus this is then reflected in this cross-over between these two types of legitimacy. One cannot be isolated from the other. There are different possible trajectories here: i) regulatory change intended to nudge behaviour – space port regulations and insurance; and ii) stimulate innovation that then might need regulatory change at some time in the future.

The application of our analytical framework to exploring the emergence of Space 2.0 has shown all five processes worked together to enable Space 2.0 to emerge as a distinct and new space industry. For example, technological innovation occurred supported by government-funded research that was initially undertaken in universities (third element). These innovations were based around developing new technological solutions and then engaging in proof-of-concept activities (fourth element) that led to alterations in normative legitimacy (fifth element). This challenged the dominance of large satellites highlighting that new markets could form around an alternative technological solution. Consumers became interested in smaller satellites, as they began to understand their commercial possibilities reflecting a change in normative legitimacy. All this is framed within a regulatory structure in which initially regulations linked to Space 1.0 prevented the further development and adoption of smaller satellites. There was then a ‘system-level’ shift in response to more bottom-up processes, as infrastructure investment and regulatory change, including the introduction of supportive regional policy (fourth element) (Salder, Bryson, and Clark Citation2023). New pathways need to be permitted and enabled rather than discouraged and this involves alterations in all three forms of legitimacy. This process of legitimacy configuration and reconfiguration was complex and multi-scalar, with multiple feedback loops between different forms of agency that were shaping or facilitating alterations in normative, cognitive, and regulatory legitimacy.

9. Discussion and conclusion

This paper provides the first in-depth analysis of the emergence of Space 2.0 in the context of legitimacy building. This is important given the increasing dependence of socioeconomic processes on satellite-enabled applications (including communication, navigation, and earth observation). The emergence of Space 2.0 in the UK represents the creation of a new industrial pathway, partly based on existing established collections (path-branching) of regional assets, which have shaped or contributed to making the market for smaller and less expensive satellites. Once this new approach had acquired legitimacy then Space 2.0 could unfold with the establishment of many new firms involved in satellite and component production. It is important to appreciate that these new Space 2.0 firms would have been excluded from participating in Space 1.0 products – they had no legitimacy in the Space 1.0 industry. Space 1.0 continues to produce large telecommunication satellites, whilst Space 2.0 is a new layer of firms and products on to the UK space industry representing the emergence of a novel industrial pathway.

Legitimation processes played an important role in explaining the emergence of Space 2.0 given the risks related to the privatisation of space and the development of mass-produced satellites. This paper distinguishes between different legitimation processes and explores the inter-related processes behind the development of three types of legitimacy (normative, cognitive, and regulatory We have developed a comprehensive analytical framework comprising five distinct elements (). Our starting point is rooted in the literature concerning the diverse trajectories of new industrial path development (Grillitsch & Sotarauta Citation2020). The second component of our analytical framework focuses on the geographical aspects of new industrial path development, examining how location and spatial factors influence these trajectories. The third element addresses the preconditions associated with the birth and evolution of emerging industries. This encompasses factors like the presence of regional networks and a diverse knowledge infrastructure. The fourth element highlights the importance of micro-level processes that drive transformations and reconfigurations within innovation systems: organisational-level and system-level agency. The fifth and final component of our analytical framework, is dedicated to exploring the macro – micro dynamics of legitimation within the context of industrial path development. The application of this framework to exploring the emergence of Space 2.0 has shown that each component was important, but that all five processes worked together to enable Space 2.0 to emerge as a distinct and new space industry. A summary of this analytical framework and the abstract processes that are revealed via a study of Space 2.0 is presented below ().

Table 1. Analytical framework and the abstract processes that are revealed via a study of Space 2.0.

This paper makes three contributions. Our first contribution is to recognise that the emergence of a new industry is a dynamic multi-actor process, which consists of five key elements. The fifth element involves iterative interactions between normative, cognitive, and regulatory legitimacy building processes, that de-locked Space 1.0 and enabled the emergence of Space 2.0 through facilitating alterations in the characteristics of demand and supply. The case of Space 2.0 highlights the importance of focussing initially on actor-orientated and contingent aspects of industry formation and to then frame this within an account of how consumer demand is reconfigured resulting in an alternative technological solution being rendered legitimate. For industrial path development alterations in normative-related legitimacy are essential as these support further alterations in cognitive and regulatory legitimacy. This is a complex process in which alterations in regulatory legitimacy may facilitate changes in normative and cognitive legitimacy or alterations in regulatory legitimacy follow-on from disruptive innovation. It is not a linear process but involves interlayering, or complex feedback loops, between these three distinct types of legitimacy building. Further sector and country studies are required to explore differences in this interlayering by industry, country, and region. The failure of some of these feedback loops, for example problems with altering regulatory legitimacy, would prevent the formation of a new industrial pathway.

Our second conceptual contribution is that the emergence of Space 2.0 was dependent on the simultaneous de-locking of existing normative and cognitive legitimacy that supported satellite supply and demand, as well as launch technologies, in Space 1.0. Both de-locking processes required alterations in regulatory legitimacy. Understanding industry formation must acknowledge the role legitimacy de-locking and legitimacy building plays as part of a co-evolutionary innovation process in which the emergence of Space 2.0 required changes to occur in an interacting population of stakeholders and for new stakeholders to join the emerging new industry. This interacting population included suppliers of small satellites and their consumers, ground station networks and launch systems including spaceports. The key point here is that the emergence of Space 2.0 required co-evolutionary alterations in the legitimacy building processes of interacting industries: satellite design and fabrication, launch technologies and downstream or providers of satellite-enabled services. Nevertheless, the term de-locking needs to be used with care as this does not imply that the legitimisation processes that evolved to support Space 1.0 have been replaced by those that have evolved to support the emergence of Space 2.0. Space 1.0 continues to exist based around military and large communication satellites whilst Space 2.0 reflects the creation of a new democratised or more inclusive space market segment. Thus, de-locking of Space 1.0 enabled the emergence of Space 2.0, but this process did not destroy Space 1.0, but led to a diversification of the space industry and this had important regional implications.

Our third conceptual contribution is to highlight that industrial formation requires a combination of multi-scalar processes based on the configuration of cognitive, normative, and regulatory legitimacy and this might be a translocal process. The actual configuration, or sequence, will be sector specific. For Space 2.0, one university played a critical role in the generational technological shift that was required to de-lock Space 1.0 and to establish the foundations for Space 2.0. It is noteworthy that this de-locking required support from NASA highlighting that the emergence of Space 2.0 in the UK involved actors located in different national jurisdictions. Developing a more granular understanding of industry-related legitimation processes is important, since it will help inform policy interventions intended to support new emerging industries.

Further research is required to explore the role legitimacy building plays in the emergence of new industries. Processes of legitimacy building, specifically focussed on the transformation or the ‘de-locking’ of an established industry, may differ by sector, country, and region. Therefore, more comparative studies of these processes are required that would include research on de-locking in emerging economy settings and on industrial sectors that are not as tied to government as Space 1.0 and Space 2.0. This would involve identifying other emerging industries, which have undergone processes of ‘de-locking’ either as a result of external pressures (necessity de-locking) or as the outcome of new opportunities (e.g. technological advancements). In addition, a comparison of the legitimation processes between mature (but contested) and emerging industries is required to explore sector-based differences in the inter-layering of processes involved in forming normative, cognitive, and regulatory legitimacy.

Acknowledgements

We are grateful to Bram Timmermans for handling the editorial review of this article and for his guidance on the four rounds of revisions. The constructive comments from the reviewers challenged us to refine and develop our argument. The research was undertaken with funding from the Economic and Social Science Research Council (ESRC) (ES/J50001X/1). We thank the interviewees and the participants at the stakeholder events who gave their time to discuss this topic; without them the research would not have been possible.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 LQs are defined as the ratio between the local and the national share of an industry.

References

- Aldrich, H. E., and C. M. Fiol. 1994. “Fools Rush In? The Institutional Context of Industry Creation.” The Academy of Management Review 19 (4): 645–670. https://doi.org/10.2307/258740.

- Andres, L., J. R. Bryson, H. Bakare, and F. Pope. 2023. “Institutional Logics and Regional Policy Failure: Air Pollution as a Wicked Problem in East African Cities.” Environment & Planning C Politics & Space 41 (2): 313–332.

- Bathelt, H., and P. Turi. 2011. “Local, Global and Virtual Buzz: The Importance of Face-To-Face Contact in Economic Interaction and Possibilities to Go Beyond.” Geoforum 42 (5): 520–529. https://doi.org/10.1016/j.geoforum.2011.04.007.

- Benner, M. 2024. “System-Level Agency and Its Many Shades: Path Development in a Multidimensional Innovation System.” Regional Studies 58 (1): 238–251. https://doi.org/10.1080/00343404.2023.2179614.

- Bergek, A., S. Jacobsson, and B. A. Sandén. 2008. “Legitimation’ and ‘Development of Positive externalities’: Two Key Processes in the Formation Phase of Technological Innovation Systems.”Technology Analysis and Strategic Management 20 (5): 575–592.

- Billing, C. A., and J. R. Bryson. 2019. “Heritage and Satellite Manufacturing: Firm-Level Competitiveness and the Management of Risk in Global Production Networks.” Economic Geography 95 (5): 1–19. https://doi.org/10.1080/00130095.2019.1589370.

- Binz, C., and H. Gong. 2021. “Legitimization Dynamics in Industrial Path Development: New-To-The-World versus New-To-The Region Industries.” Regional Studies. https://doi.org/10.1080/00343404.2020.1861238.

- Binz, C., S. Harris-Lovett, M. Kiparsky, D. L. Sedlak, and B. Truffer. 2016. “The Thorny Road to Technology Legitimation—Institutional Work for Potable Water Reuse in California.” Technological Forecasting and Social Change 103:249–263. https://doi.org/10.1016/j.techfore.2015.10.005.

- Blažek, J., V. Kadlec, and V. Květoň. 2023. “The Role of Assets and Variegated Constellations of Organizational-And System-Level Agency in Regional Transformation.” European Planning Studies 1–22. https://doi.org/10.1080/09654313.2022.2163155.

- Blažek, J. and V. Květoň. 2021. “From coal-mining to data-mining: The role of leadership in the emergence of a regional innovation system in an old industrial region.” In Handbook on city and regional leadership, edited by M. Sotarauta and A. Beer, 168–186. Cheltenham: Edward Elgar.

- Blažek, J., and V. Květoň. 2022. “Regionalization of the SWAT+ Model for Projecting Climate Change Impacts on Sediment Yield: An Application in the Nile Basin.” Regional Studies 42. ht tps://d oi.org/1 0.1080/0034/3404/ 2022/2054976.

- Bork, S., J. P. Schoormans, S. Silvester, and P. Joore. 2015. “How Actors Can Influence the Legitimation of New Consumer Product Categories: A Theoretical Framework.” Environmental Innovation and Societal Transitions 16:38–50. https://doi.org/10.1016/j.eist.2015.07.002.

- Boschma, R. A. 1997. “New Industries and Windows of Locational Opportunity: A Long-Term Analysis of Belgium.” Erdkunde 51 (1): 12–22. https://doi.org/10.3112/erdkunde.1997.01.02.

- Boschma, R., L. Coenen, K. Frenken, and B. Truffer. 2017. “Towards a Theory of Regional Diversification: Combining Insights from Evolutionary Economic Geography and Transition Studies.” Regional Studies 51 (1): 31–45. https://doi.org/10.1080/00343404.2016.1258460.

- Breul, M., C. Hulke, and L. Kalvelage. 2021. “Path Formation and Reformation: Studying the Variegated Consequences of Path Creation for Regional Development.” Economic Geography 97 (3): 213–234. https://doi.org/10.1080/00130095.2021.1922277.

- Bryson, J. R., and M. Ronayne. 2014. “Manufacturing Carpets and Technical Textiles: Routines, Resources, Capabilities, Adaptation, Innovation and the Evolution of the British Textile Industry.” Cambridge Journal of Regions, Economy & Society 7 (3): 471–488. https://doi.org/10.1093/cjres/rsu018.

- Fahey, C. 2019. Space 2.0 Regulating Growth in the Space Industry, Available from: https://www.scl.org/articles/10494-space-2-0-regulating-growth-in-the-space-industry.

- Fernholz, T. 2014 What It Took for Elon Musk’s SpaceX to Disrupt Boeing, Available from: https://qz.com/281619/what-it-took-for-elon-musks-spacex-to-disrupt-boeing-leapfrog-nasa-and-become-a-serious-space-company/.

- Frenken, K. and R. Boschma. 2007. “A Theoretical Framework for Evolutionary Economic Geography: Industrial Dynamics and Urban Growth as a Branching Process.” Journal of Economic Geography 7 (5): 635–649.

- Gardner, E. C., and J. R. Bryson. 2021. “The Dark Side of the Industrialisation of Accountancy: Innovation, Commoditization, Colonization and Competitiveness.” Industry and Innovation 28 (1): 42–57. https://doi.org/10.1080/13662716.2020.1738915.

- Gong, H. 2020. “Multi-Scalar Legitimation of a Contested Industry: A Case Study of the Hamburg Video Games Industry.” Geoforum 114:1–9. https://doi.org/10.1016/j.geoforum.2020.05.005.

- Gov.Wales. 2019 Lift off for Wales’ first UK Space Conference, Available from:https://gov.wales/lift-wales-first-uk-space-conference.

- Grillitsch, M., B. Asheim, and H. Nielsen. 2022. “Temporality of Agency in Regional Development.” European Urban and Regional Studies.2 29 (1): 107–125.

- Grillitsch, M., B. Asheim, and M. Trippl. 2018. “Unrelated Knowledge Combinations: The Unexplored Potential for Regional Industrial Path Development.” Cambridge Journal of Regions, Economy & Society 11 (2): 257–274. https://doi.org/10.1093/cjres/rsy012.

- Grillitsch, M., and M. Sotarauta. 2020. “Trinity of Change Agency, Regional Development Paths and Opportunity Spaces.” Progress in Human Geography 44 (4): 704–723. https://doi.org/10.1177/0309132519853870.

- Hassink, R., A. Isaksen, and M. Trippl. 2019. “Towards a Comprehensive Understanding of New Regional Industrial Path Development.” Regional Studies 53 (11): 1136–1645. https://doi.org/10.1080/00343404.2019.1566704.

- Henn, S., and H. Bathelt 2015 Knowledge Generation and Field Reproduction in Temporary Clusters and the Role of Business Conferences. Geoforum, 58:104–113.

- Isaksen, A., S. E. Jakobsen, R. Njøs, and R. Normann. 2019. “Regional Industrial Restructuring Resulting from Individual and System Agency.” Innovation: The European Journal of Social Science Research 32 (1): 48–65. https://doi.org/10.1080/13511610.2018.1496322.

- Jolly, S., M. Grillitsch, and T. Hansen. 2020. “Agency and Actors in Regional Industrial Path Development. A Framework and Longitudinal Analysis.” Geoforum 111:176–188. https://doi.org/10.1016/j.geoforum.2020.02.013.

- Jolly, S., and T. Hansen. 2021. “Industry Legitimacy: Bright and Dark Phases in Regional Industry Path Development.” Regional Studies 56 (4): 630–643. https://doi.org/10.1080/00343404.2020.1861236.

- Kogler, D. F., A. Whittle, K. Kim, and A. Lengyel. 2023. “Understanding Regional Branching: Knowledge Diversification via Inventor and Firm Collaboration Networks.” Economic Geography 99 (5): 471–49.

- Lee, Y., and E. A. Fong. 2019. “The Impact of Diversifying and de Novo Firms on Regional Innovation Performance in an Emerging Industry: A Longitudinal Study of the US Ethanol Industry.” Industry and Innovation 26 (7): 769–794. https://doi.org/10.1080/13662716.2018.1531747.

- Markard, J., S. Wirth, and B. Truffer. 2016. “Institutional Dynamics and Technology Legitimacy–A Framework and a Case Study on Biogas Technology.” Research Policy 45 (1): 330–344. https://doi.org/10.1016/j.respol.2015.10.009.

- Martin, R. 2010. “Roepke Lecture in Economic Geography: Rethinking Regional Path Dependence: Beyond Lock-In to Evolution.” Economic geography 86 (1): 1–27.

- Martin, R. 2014. “Path Dependence and the Spatial Economy: A Key Concept in Retrospect and Prospect.” In Handbook of Regional Science, edited by M. M. Fischer and P. Nijkamp, 609–629. Berlin: Springer.

- Martin, R., and P. Sunley. 2006. “Path dependence and regional economic evolution.” Journal of Economic Geography 6 (4): 395–437. https://doi.org/10.1093/jeg/lbl012.

- Montpert, P. 2011. “Space Insurance.” In Contracting for Space: Contract Practice in the European Space Sector, edited by L. J. Smith and I. Baumann, 283–290. Farnham: Ashgate.

- National Space Strategy, 2021 Available from: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/1020617/national-space-strategy.pdf.

- Pelton, J. N. 2019. Space 2.0: Revolutionary Advances in the Space Industry. Switzerland: Springer.

- Plechero, M., M. Kulkarni, C. Chaminade, and B. Parthasarathy. 2020. “Explaining the Past, Predicting the Future: The Influence of Regional Trajectories on Innovation Networks of New Industries in Emerging Economies.” Industry and Innovation 28 (7): 1–23. https://doi.org/10.1080/13662716.2020.1780419.

- Pyle, R. 2019. Space 2.0: How Private Spaceflight, a Resurgent NASA, and International Partners are Creating a New Space Age. Dallas: BenBella Books.

- Quintana, E. 2017. “The New Space Age: Questions for Defence and Security.” The RUSI Journal 162 (3): 88–109.

- Rusten, G., and J. R. Bryson. 2010. “Placing and Spacing Services: Towards a Balanced Economic Geography of Firms, Clusters, Social Networks, Contracts and the Geographies of Enterprise.” Tijdschrift voor Economische en Sociale Geografie 101:248–261. https://doi.org/10.1111/j.1467-9663.2009.00584.x.

- Rusten, G., J. R. Bryson, and U. Aarflot. 2007. “Places Through Products and Products Through Places: Industrial Design and Spatial Symbols as Sources of Competitiveness.” Norsk Geografisk Tidsskrift - Norwegian Journal of Geography 61 (3): 133–144. https://doi.org/10.1080/00291950701553889.

- Salder, J., and J. R. Bryson. 2019. “Placing Entrepreneurship and Firming Small Town Economies: Manufacturing Firms, Adaptive Embeddedness, Survival and Linked Enterprise Structures.” Entrepreneurship & Regional Development 31 (9–10): 9-10, 806–825. https://doi.org/10.1080/08985626.2019.1600238.

- Salder, J., J. Bryson, and J. Clark. 2023. “The Decoupling Effect and Shifting Assemblages of English Regionalism: Economic Governance, Politics and Firm-State Relations.” Environment & Planning C Politics & Space. 0 (0). https://doi.org/10.1177/23996544231206821.

- Satellite Applications Catapult. 2014 Small is the New Big, Available from: https://sa.catapult.org.uk/wp-content/uploads/2018/12/Small-is-the-new-Big.pdf. Accessed 22, 2022

- Sotarauta, M., and M. Grillitsch. 2023. “Path Tracing in the Study of Agency and Structures: Methodological Considerations.” Progress in Human Geography 47 (1): 85–102. https://doi.org/10.1177/03091325221145590.

- Suchman, M. C. 1995. “Managing legitimacy: Strategic and institutional approaches.” The Academy of Management Review 20 (3): 571–610. https://doi.org/10.2307/258788.

- UKSA 2019 Space Park Leicester, Available from: http://www.ukspa.org.uk/members/space-park-leicester.

- Vanchan, V., R. Mulhall, and J. Bryson. 2018. “Repatriation or Reshoring of Manufacturing to the U.S. and UK: Dynamics and Global Production Networks or from Here to There and Back Again.” Growth and Change 49 (1): 97–121. https://doi.org/10.1111/grow.12224.

- Vestrum, I., E. Rasmussen, and S. Carter. 2017. “How Nascent Community Enterprises Build Legitimacy in Internal and External Environments.” Regional Studies 51 (11): 1721–1734. https://doi.org/10.1080/00343404.2016.1220675.

- Zimmerman, M. A. and G. J. Zeitz. 2002. “Beyond Survival: Achieving New Venture Growth by Building Legitimacy.” Academy of Management Review 27: 414–431.

Appendix 1

Interview Codes (to anonymise the firm names)

Appendix 2

UK space sector: employment and firm counts

Appendix 3

Maps Establishment LQs 3,- 3