Abstract

The capability to vary risk-taking is an important aspect of performance in organizations where behavioral adjustments are required to suit changing objectives. Incentive schemes are one way to influence risk-taking. Yet, evidence indicates incentives do not have their intended effects and may encourage excessive risk-taking. To examine this issue, we draw on compensation activation theory that proposes individual motives are activated by specific features of compensation schemes and expressed in behaviors. We extend compensation activation theory by focusing on (1) responses to a sequence of tasks designed to activate risk-taking and (2) the effects of incentive schemes on these relationships. We conducted a laboratory experiment with 173 participants who were allocated randomly to one of three bonus schemes. The linear scheme has a linear relationship between returns from risk-taking and rewards. The bonus cap scheme operates similarly up to a point where no further rewards are paid. The outcome-adjusted scheme, with a two-year hypothetical time frame, requires realized gains for the first year of investment and no losses in next year. Results support our hypotheses that these incentive schemes have differential effects on the strength and direction of relationships between risk-taking across a sequence of tasks. The linear scheme strengthens the relationships between risk-taking across sequential tasks. Conversely, the bonus cap scheme weakens the relationships between risk-taking across sequential tasks. The outcome-adjusted scheme creates variability by decreasing risk-taking when the connections between risk-taking and rewards are less salient and increasing risk-taking when connections between risk-taking and rewards are more salient. We contribute to the literature concerning compensation activation and incentives by deepening our understanding of the roles played by tasks and incentives in activation processes and by explaining the variability of risk-taking in terms of changes in connections between behavior and rewards.

Risk-taking is central to organizational activities and is especially valuable when adjusted in response to objectives (Bednarek, Chalkias, and Jarzabkowski Citation2019; Zinn Citation2019). The capability to vary behaviors is an important aspect of performance in contexts that demand change (Tett and Fisher Citation2021), are volatile (Mieg, Citation2022), or require risk-taking to achieve performance objectives (Guastello Citation2016). Incentive schemes are one way to align behaviors, including risk-taking (Deckop, Merriman, and Blau Citation2004), with organizational interests (Markoulli et al. Citation2017).

Explaining behavioral variability involves modeling interactions between individual characteristics and environmental features (Podsakoff et al. Citation2019). Compensation activation theory provides such a model by proposing that individual motives are activated by incentives that trigger their expression in behavior (Fulmer and Shaw Citation2018). Advancing theorizing about compensation activation processes is important because empirical evidence suggests incentive schemes do not function as intended (Hartmann and Slapničar Citation2015), due to insufficient attention to differences in sensitivity to rewards (Kokkinis Citation2019). Moreover, failures to do so are consequential and damaging, especially when harms associated with risk-taking are involved and when incentives are large.

Risk-taking in the finance sector is a particular concern (Brandao-Marques, Correa, and Sapriza Citation2020). Excessive risk-taking by incentivized actors in financial markets was a causal factor in the 2008 global financial crisis (Financial Stability Board Citation2009a, Citation2009b; Shaw and Gupta Citation2015; Turner Citation2009). Millions of people experienced the psychological and economic consequences of the financial crisis, and the repercussions of the recession continue (Erdem Citation2020). Indeed, the financial cost of the crisis is a present-value reduction of lifetime earnings in the US at $70,000 per person (Barnichon, Matthes, and Ziegenbein Citation2018). Yet, prior to the pandemic, Wall Street bonus payments were returning to pre-crisis levels, with the total bonus payment pool of $31.4 billion in 2017 being close to the bonus pools of $33 billion–$34 billion in 2006 and 2007 (McLannahan Citation2018), with the current situation being similar (Aratani Citation2023).

The need to promote and limit risk-taking is an organizational challenge (Pettersen Gould, Citation2021). Risk-taking creates possibilities to realize opportunities that bring benefits. Thus, a core element of work in financial services is individual risk-taking on behalf of an organization in the expectation that realized gains will be greater than losses. Doing so involves responding to sequences of tasks designed to encourage risk-taking (Fenton-O’Creevy et al. Citation2005). For example, asset managers make a series of daily investment decisions, each of which requires evaluations of risks and possible returns that have consequences for financial stability (Haldane Citation2014). Insufficient risk-taking results in under-performing assets, whereas excessive risk-taking creates harm to individual and organizational performance, finances, and reputation (Ben-David, Birru, and Prokopenya Citation2018).

Moreover, the conditions under which gains can be realized change in relation to differing objectives (e.g. risk appetite) and environmental factors (e.g. market conditions) (Angeli and Gitay Citation2015). Aligning the actions of risk-taking employees with banks’ risk appetites is therefore central to achieving organizational objectives (Wiedemann et al. Citation2023). Although incentives have the potential to shape risk-taking, their precise effects remain under-theorized (Fulmer and Shaw Citation2018). Thus, a key question to emerge from prior research is, What are the conditions that change the activation and expression of risk-taking?

To address this question, we examine risk-taking in response to a sequence of tasks that enabled us to look at changes in risk-taking under differing combinations of tasks and incentives. Each task comprised cues designed to activate competence motives that are expressed in risk-taking (Weller, Ceschi, and Randolph Citation2015). We contextualized the tasks in a hypothetical-asset-manager scenario and carried out the study in a research laboratory. We used an experimental method and randomly allocated participants to conditions with different incentives. We examined three different incentive schemes common within the UK banking sector. The linear scheme has a linear relationship between returns from risk-taking and rewards. The bonus cap scheme operates similarly up to a point where no further rewards can be gained. The outcome-adjusted scheme, with a hypothetical time frame of two years, requires realized gains for the first year of investment and no losses in the next year.

Risk-taking and its activation

The significance of risk-taking to organizations has generated a thriving research stream that seeks to explain why risk-taking varies across individuals and when situational features make risk-taking more or less likely (Shou and Olney Citation2020). Recent developments have placed incentives at the heart of theorizing about such processes. Compensation activation theory (Fulmer and Shaw Citation2018) explains how incentives activate behaviors by integrating insights from theories of fundamental social motives (Kenrick, et al. Citation2010a, Citation2010b;) and trait activation processes (Tett and Burnett Citation2003) with studies of responsiveness to pay.

Compensation activation theory (Fulmer and Shaw Citation2018) has several tenets that informed the development of our study. Two core tenets are that social motives vary at the individual level and that they are latent. The fundamental social motives framework was developed to describe a set of motives that have an evolutionary basis and drive functionally adaptive behaviors that influence survival (Kenrick, Neuberg, et al. 2010). Compensation activation theory (Fulmer and Shaw, Citation2018) refocuses the notion of fundamental social motives by considering the motives that are central to explaining workplace behaviors and are responsive to incentives. These motives include competence.

Competence motives drive the development of a reputation for mastery through the granting of status by others, the growth of self-esteem (Kenrick, et al. Citation2010a, Citation2010b), and demonstrating one’s value to a group (Cheng et al. Citation2013). Drives for competence function to support self-esteem and the associated personal and social benefits (Kenrick, et al. Citation2010a, Citation2010b). Competence motives are especially relevant to the study of risk-taking and incentives in finance services, given highly selective processes that seek out applicants with strong capabilities (St-Onge and Beauchamp Legault Citation2022). Moreover, financial services work is complex and incentives play a powerful role in attempts to shape behavior (Kirchler, Lindner, and Weitzel Citation2020). The corollary is that risk-taking is a way to express competence motives due to the perceived connections between risk-taking and rewards (Weller et al. Citation2015).

Incentives as facilitators

Compensation activation theory proposes that the alignment of incentive systems with motives activates their expression in behavior (Fulmer and Shaw Citation2018). For example, high competence motives are associated with high levels of risk-taking under variable pay conditions. This effect occurs because the incentive scheme provides a task cue, i.e. a cue associated with the nature of work itself (Tett and Burnett Citation2003). Task cues activate competence motives, and their expression in risk-taking may lead to financial gains. Such gains reinforce beliefs about competence and are personally and financially rewarding (Cadsby, Song, and Tapon Citation2007).

Compensation activation theory also proposes that people whose motives are activated exhibit stronger behavioral responses than those whose motives are not activated (Fulmer and Shaw Citation2018). Thus, the theory additionally proposes compensation schemes that interact with individual motives. This modeling corresponds with the notion of facilitators in trait activation theory (Tett and Burnett Citation2003) that is a foundational element of theorizing about compensation activation. The effects of facilitators are multiplicative such that expressing traits in behavior is more likely when a situational cue makes relevant information more salient. The reverse also occurs. Expressing a trait is less likely when a situational cue makes relevant information less salient. For example, core self-evaluations (evaluations of self-concept, capabilities, and control; (Judge, Locke, and Durham Citation1997) are associated with personal beliefs that goals can be achieved. Such beliefs are activated by variable incentives and expressed in strategic risk-taking. By contrast, fixed salary payments do not activate core self-evaluations, and no significant differences exist in strategic risk-taking between people with differing levels of core self-evaluations (Chng et al. Citation2012).

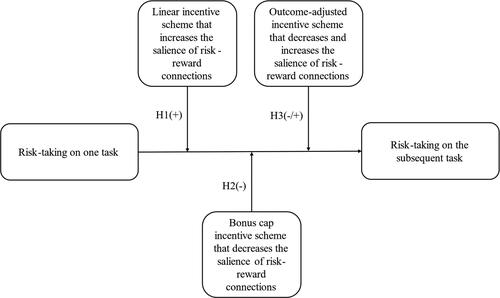

We draw on theories of compensation activation (Fulmer and Shaw Citation2018) and trait activation (Tett and Burnett Citation2003) to examine the activating features of task cues designed to trigger competence motives as they relate to risk-taking. We start by considering a commonly used incentive scheme, referred to as a linear scheme, that offers bonus payments in direct proportion to gains and rewards risk-taking in the short term (Pikulina et al. Citation2014). By considering the linear scheme from an activation perspective, we propose it provides a task cue that increases the salience of connections between risk-taking and rewards. A consequence is that risk-taking becomes greater across a sequence of tasks. As such, our first hypothesis follows.

Hypothesis 1: The positive relationship between risk-taking on sequential tasks is strengthened by a linear bonus scheme.

Of concern is that employers may deploy incentive schemes to stimulate greater risk-taking than is desirable for the public interest (Thanassoulis and Tanaka Citation2017). Hence, alternative incentive schemes have been designed. A bonus cap scheme was introduced in the UK in 2014 with the aim of reducing risk-taking. The bonus cap scheme is designed so that gains achieved from risk-taking are rewarded up to a point beyond which no further bonus payments are made. Bonus payments are intended to be limited to 100% of salary, or 200% with shareholder approval (Credit Institutions Directive Citation2013).

Taking a compensation activation perspective creates a new way to examine the functioning of the bonus cap scheme by explaining how the connections between tasks and incentives influence risk-taking. Given our interest in sequences of behavior, we propose that the bonus cap scheme weakens relationships between risk-taking on one task and risk-taking on the next task, due to the definite cut-off point for the connection between risk-taking and rewards. Thus, the bonus cap scheme highlights the possibility that more risk-taking will not lead to more rewards. Thus, our second hypothesis follows.

Hypothesis 2: The positive relationship between risk-taking on sequential tasks is weakened by a bonus cap scheme.

Incentivising variability

Incentive schemes are designed to shape behavior by rewarding the expression of certain actions while reducing the likelihood of others (Ryan and Deci Citation2020). Therefore, incentive schemes may create behavioral variability by changing the direction of a relationship between two variables, depending on the value of expressed behaviors (Tett and Burnett Citation2003). One way to encourage variability in risk-taking involves using an outcome-adjusted scheme in combination with different task cues to change the connections between risk-taking and possibilities for achieving rewards from resulting gains. Specifying a minimum return focuses attention on the low possibilities for gain (Essl and Jaussi Citation2017) and lowers risk-taking. Thus, risk-taking is not activated when a minimum return is required for an incentive to be paid out.

By contrast, risk-taking is activated when incentive schemes connect behavior with rewards (Cadsby, Song, and Tapon Citation2007; Chng et al. Citation2012). Specifically, risk-taking increases in competitive situations (Ozbeklik and Smith Citation2017), especially for people with high competence motives who are predisposed toward social comparison (Liu, Elliot, and Li Citation2021) and achieving goals (Zou, Scholer, and Higgins Citation2020). Moreover, competition activates motives that are fulfilled by risk-taking that offers the means to reach desired outcomes (Barclay, Mishra, and Sparks Citation2018). Hence, our final hypotheses follow.

Hypothesis 3a: The positive relationship between risk-taking on sequential tasks is weakened when an outcome-adjusted scheme decreases the salience of connections between risk-taking and rewards.

Hypothesis 3b: The positive relationship between risk-taking on sequential tasks is strengthened when an outcome-adjusted scheme increases the salience of connections between risk-taking and rewards.

depicts the research model.

Figure 1. The research model.

Methods and materials

Participants and procedure

Ethical approval for the study was sought and granted from the first author’s university. Participants were contacted via a behavioral research laboratory participant pool and through the offices of MSc Finance and MSc Management programs at a UK university. A total of 173 people agreed to take part. Participants were introduced to the study and asked to read introductory material that explained that the purpose of the study. Participants were informed that their involvement in the study was voluntary, and they could withdraw from the study at any time without any consequences. Everyone agreed to join the study, and they were given one hour to complete the items. The pool included 66 (38.2%) men and 107 women (61.8%). The mean age was 26.21 (range = 18–61; SD = 9.11). Participants were allocated randomly to one of three incentive schemes. Fifty-seven (32.9%) participants were in the linear scheme, 57 (32.9%) in the bonus cap scheme, and 59 (34.1%) in the outcome-adjusted scheme.

To create an incentive structure with material consequences, participants were informed that the outcomes of their asset-selection choices would be calculated on completion of the study and that they might receive a cash bonus. Participants’ bonus payments represented approximately 1/1000 of the bonus presented in the hypothetical scenario. For example, a hypothetical bonus of £10,000 yielded a real cash bonus of £10. A research fellow in the laboratory calculated the outcomes of each participant’s choices based on the probabilities described in the risk-taking tasks and using an Excel spreadsheet with a random-number generator. For example, if a participant chose an asset with an 80% probability of successful return, and if the randomly generated number fell between 0 and 0.2, the asset failed to generate a return. If the randomly generated number fell between 0.2 and 1, the asset was successful in generating a return and the appropriate cash payment was calculated. The range of payments was the £10 participation fee with no bonus to the fee plus a bonus payment of £32. The mean payment was £19.46 (SD=£5.72).

Prior to the experiment, 39 temporary and permanent employees from the same UK financial institution as the expert advisors who advised on our measures participated in a pilot study. Participants were 23 (59%) men and 16 (41%) women (mean age = 31.38, range = 20–49, SD = 7.77, mean tenure = 9.17 years, range = 0–33, SD = 7.92). We explained the purpose of the study to the participants, requested their consent, and gave them one hour to complete the measures described below and to provide feedback on the questions. Qualitative feedback suggested completing the measures as straightforward and the risk-taking tasks were a reasonable reflection of those performed by asset managers.

Measures

Young men take more risks than older men or women in a range of contexts (Josef et al. Citation2016), so we used self-report items to assess age (in years and months) and sex (1 = male, 2 = female) and included them as control variables.

Although we are interested in risk-taking in response to a task sequence, compensation activation theory assumes motives are key to the process (Fulmer and Shaw Citation2018), so we assessed competence motives using the need for achievement scale (McClelland Citation1976) to include as a control variable. Five items measured responses to statements such as ‘I take moderate risks and stick my neck out to get ahead at work or in my class’. The response range was 1 = Strongly disagree to 7 = Strongly agree. Cronbach’s alpha=.59. The reliability of the scale is moderate (Nunnally Citation1967). Therefore, we examined the relationship between need for achievement and risk-taking as supplementary analysis to be interpreted with caution.

Choices made in financial services organizations are based on probability. Thus, we controlled for understanding of probability by using four questions based on prior research (Kirchler, Lindner, and Weitzel Citation2018), and following advice from three expert advisers. A sample question is, ‘Suppose you enter a gamble involving flipping a fair coin multiple times. You will win £10 every time you see heads and lose £5 every time you see tails. If you flip the coin 10,000 times, how much do you expect to win or lose every time you flip the coin on average? a) Lose £2.50, b) Neither lose nor gain any money (£0); c) Win £2.50; d) Win £5.00.’ Scores ranged from 0 (no correct answers) to 4 (all correct answers).

Maths competence is also a prerequisite for working in the finance industry. Drawing on prior research (Kirchler, Lindner, and Weitzel Citation2018), we assessed maths competence as a control variable using four items that asked participants to add or subtract sets of three four-figure numbers (e.g. 37092 + 40111 + 97362). Participants could not use phones, calculators. or other devices to complete the sums. Scores ranged from 0 (no correct answers) to 4 (all correct answers).

To measure risk-taking, we collaborated with the same three expert advisors and drew on prior research (Charness, Gneezy, and Imas Citation2013; Dohmen and Falk Citation2011; Eckel and Grossman Citation2008; Hartmann and Slapnicar 2015). We designed a set of four tasks that presented participants with a hypothetical-asset-manager scenario. We also followed assessment guidance by measuring a specific aspect of behavioral risk-taking that is close to workplace tasks (Bran and Vaidis Citation2020). All tasks included a task cue that was designed to activate risk-taking by specifying the conditions required to achieve a financial return. Each task required participants to select one asset from a range of six assets in which to invest their portfolio. The assets varied in their risk-return characteristics, with one asset that maximized the expected return, three assets that offered different combinations of lower risks and lower returns, and two assets that offered different combinations of higher risks and higher returns. We captured riskiness by calculating the variance of the risk-return relationship. Variance is the measure of risk used in modern portfolio theory—a cornerstone of finance—that enables investors to make choices that yield the lowest risk for a given level or return, or the highest rewards for a given level of risk (Markowitz Citation1952).

The assets in each task increased the demand for risk-taking by increasing the level of risk-taking needed to achieve a bonus payment. Demands for risk-taking also increased across the four tasks. Task 1 informed participants they had just inherited £100,000 from a distant relative whom they had never met. They had to choose between six different assets to invest this money in for one year, after which they would receive the cash. Scores reflected risk and return and ranged from 0 (least risky, i.e. a sure but low-level return) to 27.56 (most risky, i.e. a high-level, low-likelihood return). The financial return was not influenced by any of the incentive schemes.

Task 2 differed from Task 1 by adding an incentive for risk-taking. Task 2 provided all participants with the same basic instruction: ‘You have been recruited as a portfolio manager for ABC Bank. You are given the responsibility of investing £100million.’ Participants chose one asset to invest their portfolio in from a choice of six. For example, asset 2 had a 5% chance of failure and a 95% chance of success. It would result in a £2,500 loss for the bank in the event of failure and a £1million gain in the event of success, yielding an expected return of .94. Asset 4 had a 15% chance of failure and an 85% chance of success. It would result in a £1million loss for the bank in the event of failure and a £2million gain in the event of success, yielding an expected return of 1.55. Asset 4 therefore offered a higher expected return than option 2. Appendix A shows the task 2 information presented to participants and the asset-choice table from which they selected one asset to invest their portfolio in.

Task 3 presented a choice of six assets with an additional demand that required a target return of £5million before a bonus could be earned. Task 4 extended the demand for risk-taking further by introducing a competitive element and stating that no bonus would be paid unless gains exceed those of John Smith, a hypothetical asset manager in a rival bank.

To assess the effects of incentives, we focused on three incentive schemes in use within UK financial institutions at the time of the study. Participants were assigned randomly to one of the three incentive schemes by the Qualtrics software that delivered the survey. Participants were then given information about their incentive scheme. Participants in the linear scheme condition were told their bonus scheme offers a linear relationship between risk-taking and rewards. For example, a £5million return earned a hypothetical £5,000 bonus and a £5 cash payment. No bonus was paid in the event of a loss. Participants in the bonus cap condition were told their incentive scheme offered a bonus that was proportional to the return achieved on the portfolio up to a maximum of £4,000. For example, a £1million return yielded a hypothetical £1,000 bonus (a £1 real payment to participants), and a £5million return yielded a maximum hypothetical bonus of £4,000 (a £4 real payment to participants). No bonus was paid in the event of a loss. Participants in the outcome-adjusted scheme condition were told their incentive scheme operated over a hypothetical time frame of two years. The bonus was proportional to the return on the portfolio for the first year of investment only if the investment did not fail in the next year. No bonus was given in the event of a loss in the current year. The probabilities of success and failure were the same in both years. We created one variable with three categories to examine the conditional effects of incentive schemes on the relationships between risk-taking across a sequence of tasks (1 = linear scheme, 2 = bonus cap scheme, 3 = outcome-adjusted scheme).

Results

Descriptive statistics and bivariate correlations are shown in .

Table 1. Descriptive statistics and bivariate correlations.

Initial examination of the data using a paired-samples T-test show risk-taking is significantly higher for tasks 3 and 4 that consist of more cues than tasks 1 and 2 (mean difference task 3 and task 1 = 8.59, t = 10.18, p<.001; mean difference task 4 and task 1 = 9.11, t = 8.71, p<.001; mean difference task 3 and task 2 = 8.53, t = 9.97, p<.001; mean difference task 4 and task 2 = 9.06, t = 9.06, p<.001).

We carried out hypothesis testing using ordinary least-squares regression analysis and subsequent examinations of conditional effects. The regression analysis shows risk-taking in response to one task was associated with risk-taking on the next task, as expected. shows the results.

Table 2. Regression of individual differences, incentive scheme, and risk-taking on subsequent risk-taking.

We tested for conditional effects by examining a series of regression equations using version 4.3 of the PROCESS macro model 1, which is suitable for multi-categorical moderators (Hayes and Montoya Citation2017; Hayes Citation2022). The tests included sex and understanding of probability as control variables because they was significant in one of the initial regression models (Becker Citation2005). shows the results of the conditional effects analysis. For this analysis, regression weights are unstandardized as recommended (Hayes Citation2022).

Table 3. Conditional effects of incentive schemes on the relationship between risk-taking on sequential tasks.

Results show the linear scheme strengthened the positive association between risk-taking on task 2 and risk-taking on task 3, and between risk-taking on task 3 and risk-taking on task 4, supporting Hypothesis 1 (task 3 analysis effect=.61, SE=.10, t = 5.92, p<.001, LLCI=.41, UCLI=.82, task 4 analysis effect=.74, SE=.11, t = 6.50, p<.001, LLCI=.52, UCLI=.96). In accordance with Hypothesis 2, the bonus cap scheme weakened the positive association between risk-taking on task 2 and task 3 compared with the linear incentive scheme (effect=.37, SE=.14, t = 2.71, p<.01, LLCI=.14, UCLI=.40). We found no significant effect of the bonus cap scheme on the association between risk-taking on task 3 and task 4.

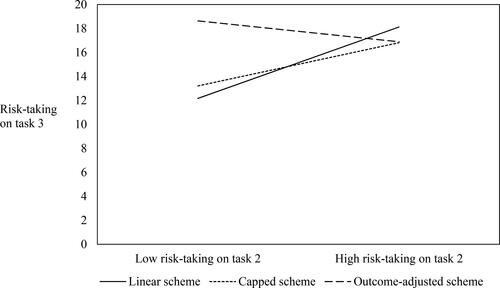

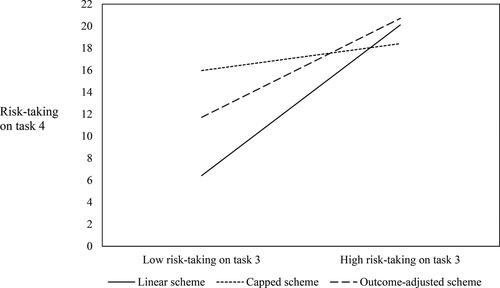

The outcome-adjusted scheme weakened the association between risk-taking on task 2 and task 3 compared with the linear scheme such that it was not significant, supporting Hypothesis 3a. Conversely, the outcome-adjusted scheme strengthened the positive association between risk-taking on task 3 and risk-taking on task 4 (effect=.49, SE=.16, t = 3.11, p<.01, LLCI=.18, UCLI=.80), supporting Hypothesis 3b. depicts the conditional effects of each bonus scheme on the relationship between risk-taking on task 2 and task 3. depicts the conditional effects of each bonus scheme on the relationship between risk-taking on task 3 and task 4.

Figure 2. The conditional effects of incentive schemes on the relationship between risk-taking on task 2 and task 3.

Figure 3. The conditional effects of incentive schemes on the relationship between risk-taking on task 3 and task 4.

Supplementary examination of the need for achievement data show it has no significant effects on risk-taking in any of the tasks.

Discussion

We hypothesized that risk-taking in response to a sequence of tasks is influenced by incentive schemes that have differential effects on the strength and direction of relationships. Results support our hypotheses and have implications for theorizing about compensation activation as well as the functioning of incentives.

We contribute to the compensation activation literature by developing understanding of the distinct role of task cues in the activation of behavior. Compensation activation theory (Fulmer and Shaw Citation2018) suggests variability in competence motives is key to explaining individual differences in response to incentive schemes. We reconsider the activation process by examining task cues as activators (Tett and Burnett Citation2003) of risk-taking as an expression of competence (Weller et al. Citation2015). The results of our study support our modeling by showing risk-taking is a consistent response to a sequence of tasks that are designed to activate such behavior. We organized the cues in tasks 1–4 so that possibilities for achieving rewards become more strongly connected with risk-taking as the sequence progressed. Participants responded to these cues with increasing levels of risk-taking. Risk-taking on tasks 3 and 4 was significantly higher than risk-taking on tasks 1 and 2.

The implication for theorizing is that task cues activate risk-taking behavior. Examining a sequence of tasks enabled us to isolate the effects of small changes in task cues on risk-taking behavior. The positive relationships between risk-taking across a sequence of tasks highlight the dynamic nature of the activation process, as has been suggested in relation to trait activation (Wille and De Fruyt Citation2014), and illustrate the activation process is sensitive to rapid situational changes (Woods et al. Citation2013). The corollary is that models of activation processes are more accurate when task cues are precisely specified and theorized as activators of behaviors that influence risk-taking.

The second implication for theorizing concerns the identification of the incentive characteristics that strengthen connections between risk-taking across a task sequence. Returning to trait activation theorizing offers an expanded view of the role incentives play in the activation process. Whereas compensation activation theory (Fulmer and Shaw Citation2018) focuses on interactions between motives and incentives that strengthen the expression of motives in behaviors, trait activation modeling refers to situational cues that interact with traits as facilitators (Tett and Burnett Citation2003). The effects of facilitators are multiplicative, and their effects can either strengthen or weaken trait-behavior relationships. By considering incentives as facilitators, we hypothesized that different schemes would have different effects.

Results supported our first hypothesis that connections between risk-taking on a sequence of tasks are strengthened when task cues designed to activate risk-taking are made more salient by the linear incentive scheme that offers increasing rewards in proportion to the gains accrued from risk-taking. Thus, we go beyond prior studies of fixed and variable pay (Chng et al. Citation2012; Cadsby, Song, and Tapon Citation2007) to focus on financial risk-taking across situations differentiated only by alterations in task cues and the conditional effects of an incentive scheme intended to make salient the rewards associated with risk-taking.

By contrast, the bonus cap scheme weakened the connections between risk-taking on a sequence of tasks, supporting our second hypothesis. The bonus cap scheme decreases the salience of the risk-return relationship by limiting possibilities for financial rewards. In this case, more risk-taking does not lead to more returns, and the bonus cap scheme reduces risk-taking. The implications for theorizing about compensation activation is that the strengthening and weakening effects of incentive schemes extend to the interactions between incentives and risk-taking across a sequence of tasks.

Third, we contribute to the literature concerned with incentives and their potential to align risk-taking behavior with organizational objectives by creating behavioral variability (Bednarek, Chalkias, and Jarzabkowski Citation2019; Zinn Citation2019). The phenomenon of variability in relationships between individual characteristics and behaviors across different situations is well established (Tett and Christiansen Citation2007). However, the occurrence of behavioral variability within situations is less well articulated (Tett, Toich, and Ozkum Citation2021). Variability in the conditional effects of incentives is similarly under-theorized. Our results shed light on the functioning of activation processes by showing how behavioral variability occurs when an outcome-adjusted scheme changes the salience of connections between behavior and rewards. Consequently, the same scheme strengthens and weakens risk-taking across a sequence of tasks.

Weakening effects occurred when the outcome-adjusted scheme made salient a change in task cue that reduced possibilities for achieving a reward. Conversely, strengthening effects occurred when the outcome-adjusted scheme highlighted the potential for gain in a competitive situation (Zou, Scholer, and Higgins Citation2020; Liu, Elliot, and Li Citation2021; Barclay, Mishra, and Sparks Citation2018). These differing conditional effects are striking given that the outcome-adjusted scheme is designed to present a stronger limitation on risk-taking than a bonus cap scheme, by focusing attention on longer-term profitability (Financial Stability Board Citation2009a, Citation2009b).

The implication for theorizing is that modeling organizational cues as facilitators and examining their effects on behavior in response to small changes in task cues develops a nuanced view that expands explanations of activation processes. Incentives are central to managerial attempts to influence behavior (Wiedemann et al. Citation2023) and contribute to financial organizations’ social responsibilities (Thekdi, Citation2016). Our study goes beyond research that shows an outcome-adjusted scheme focuses attention on loss (Essl and Jaussi Citation2017), to identify when it becomes a source of variability. We refine our understanding of when the same incentive scheme has both positive and negative effects on activation. Doing so has implications for modelling the disruption of behavioral sequences either by strengthening them or weakening them. This approach also offers possibilities for connecting individual behavior with organizational risk appetite.

Furthermore, our theorizing implies two points of traction for managers, namely, task cues and incentives, function in concert. These insights have applicability beyond risk-taking to other behaviors for which variability is an important element of performance, such as when crises require risk-taking and safety-focused behaviors to be adjusted, as we have seen throughout the COVID-19 pandemic (Qin et al. Citation2021).

Limitations and future research

The study has several limitations. Although the materials were designed by experts and pilot-tested in a relevant organization, laboratory settings do not carry the same high stakes as organizations, so risk-taking may be overestimated (Weber and Chapman Citation2005). Most participants had mathematical skills, although they are not equivalent to employees in financial services. The cash bonus payments that participants received were adjusted to account for realized outcomes, yet the payment deferral was hypothetical. Studies that involve both adjustments and real-time payment delays would deepen our understanding of how the outcome-adjusted scheme functions.

The current study also has several implications for further research. First, further examination of specific task cues is a fruitful avenue that could provide new insights concerning when and why activation occurs. In an era when flexibility and adaptation are key to success in many sectors (Park and Park Citation2019), the capability to vary behavior is a necessary element of performance and warrants attention. Second, additional study of motives would extend understanding of their role in compensation activation processes. In our study, the internal reliability of the need for achievement measure was low. Alternative approaches to conceptualizing and operationalizing competence motives, including need for achievement and other forms of competence motive, would deepen insights into the role of motives in risk-taking and other organizationally significant behaviors.

Third, continued examinations of the facilitating features of incentive schemes would provide an expanded view of their role in altering behavior in response to sequences of tasks. Incentives are significant components within organizational systems designed to shape behavior. Yet, their effects may not be as intended, as has been highlighted by the recent UK scrapping of the bonus cap scheme (Ho Citation2023). Continued efforts to develop refined activation models will enable a deeper understanding of how to stimulate behavioral variability without causing the suppression of self-expression that is personally stressful (Tett and Burnett Citation2003) or the excessive risk-taking that threatens organizations and societies (Brandao-Marques, Correa, and Sapriza Citation2020; Financial Stability Board Citation2009b, Citation2009a; Turner Citation2009). Moreover, our study was limited to one cultural context. Expanding the scope of compensation activation research to include other types of incentives and different cultural contexts would provide a more comprehensive understanding of the mechanisms that explain risk-taking and other performance-related behaviors.

Conclusion

The variability of risk-taking contributes to the attainment of individual and organizational goals by adjusting behavior in accordance with circumstantial requirements. Incentive schemes are one mechanism for changing risk-taking. By extending compensation activation theory (Fulmer and Shaw Citation2018) and examining risk-taking in response to task cues designed to activate such behavior, we develop and test a model of the interactions between risk-taking and incentives. Through findings from a laboratory study, we show the positive relationships between risk-taking on sequential tasks are strengthened when a linear incentive scheme increases the salience of connections between risk-taking and rewards. By contrast, the relationships between risk-taking on sequential tasks are weakened by a bonus cap scheme that limits possibilities for financial returns. Furthermore, an outcome-adjusted scheme changes the salience of connections between risk-taking and rewards and creates variability in risk-taking. However, such variability includes possibilities for higher levels of risk-taking than intended. The current research contributes to theorizing about the activation of behavior by extending compensation activation theory to the study of risk-taking across a sequence of tasks, examining the differing roles of task cues and incentives in the activation process, and identifying combinations of tasks and incentives that create variability in risk-taking. In so doing, we build a nuanced and dynamic model of activation that has implications for considerations of behaviors other than risk-taking, as well as the role of task cues and incentives in the process.

Acknowledgements

We are appreciative of financial support from the Bank of England that part-funded the research. We would like to thank the team of three experts from the financial sector who advised on the development of items and arranged the pilot study. In addition, we gratefully acknowledge Professor Rhona Flin, Dr Barbara Fasolo, Dr Tom Reader and Dr Niranjan Janardhanan for their helpful comments on earlier versions of this manuscript. We would also like to thank attendees at a research seminar and at the Society for Risk Analysis annual conference 2022 for their useful questions and suggestions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Data availability statement

The data that support the findings of this study are available from the corresponding author upon reasonable request.

Additional information

Funding

References

- Angeli, M., and S. Gitay. 2015. "Bonus regulation: Aligning reward with risk in the banking sector." Bank of England Quarterly Bulletin Q4. Accessed November15, 2023. https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2015/bonus-regulation-aligning-reward-with-risk-in-the-banking-sector.pdf?la=en&hash=B30E9A38C3626509539B7A3890FE3D3F15F03437.

- Aratani, L. 2023. "Average Wall Street bonuses plummeted in 2022 to $176,700." The Guardian, Accessed March 30, 2023. https://www.theguardian.com/business/2023/mar/30/wall-street-average-bonus-salary.

- Barclay, P., S. Mishra, and A. M. Sparks. 2018. “State-Dependent Risk-Taking.” Proceedings. Biological Sciences 285 (1881): 20180180. https://doi.org/10.1098/rspb.2018.0180.

- Barnichon, R., C. Matthes, and A. Ziegenbein. 2018. “The Financial Crisis at 10: Will we Ever Recover?” Federal Reserve Bank of San Francisco Economic Letter 19: 1–4.

- Becker, T. E. 2005. “Potential Problems in the Statistical Control of Variables in Organizational Research: A Qualitative Analysis with Recommendations.” Organizational Research Methods 8 (3): 274–289. https://doi.org/10.1177/1094428105278021.

- Bednarek, R., K. Chalkias, and P. Jarzabkowski. 2019. “Managing Risk as a Duality of Harm and Benefit: A Study of Organizational Risk Objects in the Global Insurance Industry.” British Journal of Management 32 (1): 235–254. https://doi.org/10.1111/1467-8551.12389.

- Ben-David, I., J. Birru, and V. Prokopenya. 2018. “Uninformative Feedback and Risk Taking: Evidence from Retail Forex Trading.” Review of Finance 22 (6): 2009–2036. https://doi.org/10.1093/rof/rfy022.

- Bran, A., and D. C. Vaidis. 2020. “Assessing Risk-Taking: What to Measure and How to Measure It.” Journal of Risk Research 23 (4): 490–503. https://doi.org/10.1080/13669877.2019.1591489.

- Brandao-Marques, L., R. Correa, and H. Sapriza. 2020. “Government Support, Regulation, and Risk Taking in the Banking Sector.” Journal of Banking & Finance 112: 105284. https://doi.org/10.1016/j.bankfin.2018.01.008.

- Cadsby, C. B., F. Song, and F. Tapon. 2007. “Sorting and Incentive Effects of Pay-for-Performance: An Experimental Investigation.” Academy of Management Journal 50 (2): 387–405. https://doi.org/10.5465/AMJ2007.24634448.

- Charness, G., U. Gneezy, and A. Imas. 2013. “Experimental Methods: Eliciting Risk Preferences.” Journal of Economic Behavior & Organization 87: 43–51. https://doi.org/10.1016/j.jebo.2012.12.023.

- Cheng, J. T., J. L. Tracy, T. Foulsham, A. Kingstone, and J. Henrich. 2013. “Two Ways to the Top: Evidence That Dominance and Prestige Are Distinct yet Viable Avenues to Social Rank and Influence.” Journal of Personality and Social Psychology 104 (1): 103–125. https://doi.org/10.1037/a0030398.

- Chng, D. H. M., M. S. Rodgers, E. Shih, and X. Song. 2012. “When Does Incentive Compensation Motivate Managerial Behaviors? An Experimental Investigation of the Fit between Incentive Compensation, Executive Core Self-Evaluation, and Firm Performance.” Strategic Management Journal 33 (12): 1343–1362. https://doi.org/10.1002/smj.1981.

- Credit Institutions Directive. 2013. “Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 on Access to the Activity of Credit Institutions and the Prudential Supervision of Credit Institutions and Investment Firms.” Official Journal of the European Union Accessed June 6, 2022. https://eur-lex.europa.eu/legal-content/EN/LSU/?uri=CELEX:32013L0036.

- Deckop, J. R., K. K. Merriman, and G. Blau. 2004. “Impact of Variable Risk Preferences on the Effectiveness of Control by Pay.” Journal of Occupational and Organizational Psychology 77 (1): 63–80. https://doi.org/10.1348/096317904322915919.

- Dohmen, T., and A. Falk. 2011. “Performance Pay and Multidimensional Sorting: Productivity, Preferences, and Gender.” American Economic Review 101 (2): 556–590. https://doi.org/10.1257/aer.101.2.556.

- Eckel, C. C., and P. J. Grossman. 2008. “Forecasting Risk Attitudes: An Experimental Study Using Actual and Forecast Gamble Choices.” Journal of Economic Behavior & Organization 68 (1): 1–17. https://doi.org/10.1016/j.jebo.2008.04.006.

- Erdem, O. 2020. After the Crash: Understanding the Social, Economic and Technological Consequences of the 2008 Crisis. Cham, Switzerland: Springer Nature.

- Essl, A., and S. Jaussi. 2017. “Choking under Time Pressure: The Influence of Deadline-Dependent Bonus and Malus Incentive Schemes on Performance.” Journal of Economic Behavior & Organization 133: 127–137. https://doi.org/10.1016/j.jebo.2016.11.001.

- Fenton-O’Creevy, M., N. Nicholson, E. Soane, and P. Willman. 2005. Traders: Risks, Decisions, and Management in Financial Markets. Oxford, U.K.: Oxford University Press

- Financial Stability Board. 2009a. "FSF Principles for Sound Compensation Practices." Accessed September 27, 2022. http://www.fsb.org/2009/04/principles-for-sound-compensation-practices-2/.

- Financial Stability Board. 2009b. "Implementation standards for the FSB. Principles for sound compensation practices." Accessed September 27, 2022. http://www.financialstabilityboard.org/2009/09/principles-for-sound-compensation-practices-implementation-standards/.

- Fulmer, I. S., and J. D. Shaw. 2018. “Individual Differences in Employee Reactions to Pay Systems: An Integrative Conceptual Review with Implications for Employees and Organizations.” Journal of Applied Psychology 103 (9): 939–958. https://doi.org/10.1037/apl0000310.

- Guastello, S. J. 2016. “The Performance-Variability Paradox: Risk Taking.” In Cognitive Workload and Fatigue in Financial Decision Making. Evolutionary Economics and Social Complexity Science, edited by S. J. Guastello, 99–107. Tokyo: Springer.

- Haldane, Andrew. 2014. "The age of asset management?". Speech at the London Business School. Accessed January 7, 2023. https://www.bankofengland.co.uk/-/media/boe/files/speech/2014/the-age-of-asset-management.pdf.

- Hartmann, Frank, and Sergeja Slapničar. 2015. “An Experimental Study of the Effects of Negative, Capped and Deferred Bonus on Risk Taking in a Multi-Period Setting.” Journal of Management & Governance 19 (4): 875–896. https://doi.org/10.1007/s10997-014-9297-6.

- Hayes, A. F. 2022. Introduction to Mediation, Moderation, and Conditional Process Analysis: A Regression-Based Approach. Third ed. New York: Guilford Press.

- Hayes, A. F., and A. K. Montoya. 2017. “A Tutorial on Testing, Visualizing, and Probing an Interaction Involving a Multicategorical Variable in Linear Regression Analysis.” Communication Methods and Measures 11 (1): 1–30. https://doi.org/10.1080/19312458.2016.1271116.

- Ho, J. K. S. 2023. “Removing Bankers’ Bonus Cap: Will This Enhance the Competitiveness of the UK Financial Market?” Capital Markets Law Journal 18 (4): 556–572. https://doi.org/10.1093/cmlj/kmad016/7252870.

- Josef, A. K., D. Richter, G. R. Samanez-Larkin, G. G. Wagner, R. Hertwig, and R. Mata. 2016. “Stability and Change in Risk-Taking Propensity across the Adult Life Span.” Journal of Personality and Social Psychology 111 (3): 430–450. https://doi.org/10.1037/pspp0000090.

- Judge, T. A., E. A. Locke, and C. C. Durham. 1997. “The Dispositional Causes of Job Satisfaction: A Core Evaluations Approach.” Research in Organizational Behavior 19: 151–188. https://doi.org/10.1037/0021-9010.83.1.17.

- Kenrick, D. T., V. Griskevicius, S. L. Neuberg, and M. Schaller. 2010a. “Renovating the Pyramid of Needs: Contemporary Extensions Built upon Ancient Foundations.” Perspectives on Psychological Science: A Journal of the Association for Psychological Science 5 (3): 292–314. https://doi.org/10.1177/1745691610369469.

- Kenrick, D. T., S. L. Neuberg, V. Griskevicius, D. V. Becker, and M. Schaller. 2010b. “Goal-Driven Cognition and Functional Behavior: The Fundamental-Motives Framework.” Current Directions in Psychological Science 19 (1): 63–67. https://doi.org/10.1177/0963721409359281.

- Kirchler, M., F. Lindner, and U. Weitzel. 2018. “Rankings and Risk‐Taking in the Finance Industry.” The Journal of Finance 73 (5): 2271–2302. https://doi.org/10.1111/jofi.12701.

- Kirchler, M., F. Lindner, and U. Weitzel. 2020. “Delegated Investment Decisions and Rankings.” Journal of Banking & Finance 120: 105952. https://doi.org/10.1016/j/jbankfin.2020.106952.

- Kokkinis, A. 2019. “Exploring the Effects of the ‘Bonus Cap’rule: The Impact of Remuneration Structure on Risk-Taking by Bank Managers.” Journal of Corporate Law Studies 19 (1): 167–195. https://doi.org/10.1080/14735970.2018.1455492.

- Liu, Z. N., A. J. Elliot, and Y. Li. 2021. “Social Comparison Orientation and Trait Competitiveness: Their Interrelation and Utility in Predicting Overall and Domain-Specific Risk-Taking.” Personality and Individual Differences 171: 110451. https://doi.org/10.1016/j.paid.2020.110451.

- Markoulli, M. P., C. I. Lee, E. Byington, and W. A. Felps. 2017. “Mapping Human Resource Management: Reviewing the Field and Charting Future Directions.” Human Resource Management Review 27 (3): 367–396. https://doi.org/10.1016/j.hrmr.2016.10.001.

- Markowitz, H. M. 1952. “Portfolio Selection.” The Journal of Finance 7 (1): 77–91. https://doi.org/10.2307/2975974.

- McClelland, D. C. 1976. The Achievement Motive. New York: Irvington.

- McLannahan, B. 2018. “Wall Street Bonuses Rise 17% to Pre-Crisis Levels.” Financial Times March 26, 2018.

- Mieg, H. A. 2022. “Volatility as a Transmitter of Systemic Risk: Is There a Structural Risk in Finance?” Risk Analysis: An Official Publication of the Society for Risk Analysis 42 (9): 1952–1964. https://doi.org/10.1111/risa.13564.

- Nunnally, J. C. 1967. Psychometric Theory. New York: McGraw-Hill.

- Ozbeklik, S., and K. Smith. 2017. “Risk Taking in Competition: Evidence from Match Play Golf Tournaments.” Journal of Corporate Finance 44: 506–523. https://doi.org/10.1016/j.jcorpfin.2014.05.003.

- Park, S., and S. Park. 2019. “Employee Adaptive Performance and Its Antecedents: Review and Synthesis.” Human Resource Development Review 18 (3): 294–324. https://doi.org/10.1177/1534484319836315.

- Pettersen Gould, K. 2021. “Organizational Risk: “Muddling through” 40 Years of Research.” Risk Analysis: An Official Publication of the Society for Risk Analysis 41 (3): 456–465. https://doi.org/10.1111/risa.13460.

- Pikulina, E., L. Renneboog, J. Ter Horst, and P. N. Tobler. 2014. “Bonus Schemes and Trading Activity.” Journal of Corporate Finance 29: 369–389. https://doi.org/10.1016/j.jcorpfin.2014.09.010.

- Podsakoff, N. P., T. M. Spoelma, N. Chawla, and A. S. Gabriel. 2019. “What Predicts within-Person Variance in Applied Psychology Constructs? An Empirical Examination.” The Journal of Applied Psychology 104 (6): 727–754. https://doi.org/10.1037/apl0000374.

- Qin, H., C. Sanders, Y. Prasetyo, M. Syukron, and E. Prentice. 2021. “Exploring the Dynamic Relationships between Risk Perception and Behavior in Response to the Coronavirus Disease 2019 (COVID-19) Outbreak.” Social Science & Medicine (1982) 285: 114267. https://doi.org/10.1016/j.socscimed.2021.114267.

- Ryan, R. M., and E. L. Deci. 2020. “Intrinsic and Extrinsic Motivation from a Self-Determination Theory Perspective: Definitions, Theory, Practices, and Future Directions.” Contemporary Educational Psychology 61: 101860. https://doi.org/10.1016/j.cedpsych.2020.101860.

- Shaw, J. D., and N. Gupta. 2015. “Let the Evidence Speak Again! Financial Incentives Are More Effective than we Thought.” Human Resource Management Journal 25 (3): 281–293. https://doi.org/10.111/1748-8583-12080.

- Shou, Y., and J. Olney. 2020. “Assessing a Domain-Specific Risk-Taking Construct: A Meta-Analysis of Reliability of the DOSPERT Scale.” Judgment and Decision Making 15 (1): 112–134. https://doi.org/10.1017/S193029750000694X.

- St-Onge, S., and M.-E. Beauchamp Legault. 2022. “What Can Motivate Me to Keep Working? Analysis of Older Finance Professionals’ Discourse Using Self-Determination Theory.” Sustainability 14 (1): 484. https://doi.org/10.3390/su14010484.

- Tett, R. P., and D. D. Burnett. 2003. “A Personality Trait-Based Interactionist Model of Job Performance.” The Journal of Applied Psychology 88 (3): 500–517. https://doi.org/10.1037/0021-9010.88.3.500.

- Tett, R. P., and N. D. Christiansen. 2007. “Personality Tests at the Crossroads: A Response to Morgeson, Campion, Dipboye, Hollenbeck, Murphy, and Schmitt (2007).” Personnel Psychology 60 (4): 967–993. https://doi.org/10.1111/j.1744-6570.2007.00098.x.

- Tett, R. P., and D. M. Fisher. 2021. “Personality Dynamics in the Workplace: An Overview of Emerging Literatures and Future Research Needs.” In The Handbook of Personality Dynamics and Processes, edited by J. F. Rauthmann, 1061–1086. Cambridge, MA: Academic Press.

- Tett, R. P., M. J. Toich, and S. B. Ozkum. 2021. “Trait Activation Theory: A Review of the Literature and Applications to Five Lines of Personality Dynamics Research.” Annual Review of Organizational Psychology and Organizational Behavior 8 (1): 199–233. https://doi.org/10.1146/annurev-orgpsych-012420-062228.

- Thanassoulis, T., and M. Tanaka. 2017. “Optimal Pay Regulation for Too-Big-to-Fail Banks.” Journal of Financial Intermediation 33 (1): 83–97. https://doi.org/10.1016/j.jfi.2017.03.001.

- Thekdi, S. A. 2016. “Risk Management Should Play a Stronger Role in Developing and Implementing Social Responsibility Policies for Organizations.” Risk Analysis: An Official Publication of the Society for Risk Analysis 36 (5): 870–873. https://doi.org/10.1111/risa.12643.

- Turner, A. 2009. “The Turner Review: A Regulatory Response to the Global Banking Crisis.” Financial Services Authority Accessed February 17. http://www.fsa.gov.uk/pubs/other/turner_review.pdf.

- Weber, B. J., and G. B. Chapman. 2005. “Playing for Peanuts: Why is Risk Seeking More Common for Low-Stakes Gambles?” Organizational Behavior and Human Decision Processes 97 (1): 31–46. https://doi.org/10.1016/j.obhdp.2005.03.001.

- Weller, J. A., A. Ceschi, and C. Randolph. 2015. “Decision-Making Competence Predicts Domain-Specific Risk Attitudes.” Frontiers in Psychology 6: 540. https://doi.org/10.3389/fpsyg.2015.00540.

- Wiedemann, A. U., C. Bouten, P. Hertrampf, V. Stein, and N. Mues. 2023. “The Risk-Related Tone from the Top: Evidence from German Regional Banks.” Journal of Risk Research: 1–20. https://doi.org/10.1080/13669877.2023.2176911.

- Wille, B., and F. De Fruyt. 2014. “Vocations as a Source of Identity: Reciprocal Relations between Big Five Personality Traits and RIASEC Characteristics over 15 Years.” The Journal of Applied Psychology 99 (2): 262–281. https://doi.org/10.1037/a0034917.

- Woods, S. A., F. Lievens, F. De Fruyt, and B. Wille. 2013. “Personality across Working Life: The Longitudinal and Reciprocal Influences of Personality on Work.” Journal of Organizational Behavior 34 (S1): S7–S25. https://doi.org/10.1002/job.1863.

- Zinn, J. O. 2019. “The Meaning of Risk-Taking–Key Concepts and Dimensions.” Journal of Risk Research 22 (1): 1–15. https://doi.org/10.1080/13669877.2017.1351465.

- Zou, X., A. A. Scholer, and E. T. Higgins. 2020. “Risk Preference: How Decision Maker’s Goal, Current Value State, and Choice Set Work Together.” Psychological Review 127 (1): 74–94. https://doi.org/10.1037/rev0000162.

Appendix A

Task 2: question example

You have been recruited as a portfolio manager for ABC Bank. You are given the responsibility of investing £100 million.

Linear incentive scheme condition

Your bonus scheme: You will be awarded a bonus proportional to the return you achieve on your portfolio, equivalent to £1000 per £1 million of return you achieve. For example, if you generate a £1 million return, you will earn a £1000 bonus. If you generate a £5 million return, you will earn a £5,000 bonus. If you make a loss, no bonus will be paid.

Bonus cap incentive scheme condition

Your bonus scheme: You will be awarded a bonus proportional to the return you achieve on your portfolio, equivalent to £1,000 per £1 million of return you achieve, up to a maximum of £4000. For example, if you generate a £1 million return, you will be paid a £1000 bonus; but if you generate a £5 million return, you will be paid a maximum bonus of £4000. If you make a loss, no bonus will be paid. The table below shows the risk-return characteristics of each asset.

Outcome-adjusted incentive scheme condition

Your bonus scheme: You will be awarded a bonus proportional to the return you achieve on your portfolio this year, only if your investment does not fail in the next year. You will receive no bonus if your investment makes a loss this year, or if it generates a positive return this year but makes a loss next year. For example, if you achieve a £5 million return this year, then you will be paid a bonus of £5000 only if it does not fail (i.e. make a loss) in the next year. The probability of success and failure for each asset in any given year is shown in the table below, and these probabilities remain the same every year.

Please select one investment asset from the following 6 assets to invest in the £100 million asset portfolio that you are managing.