?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Enthusiasm for crowdfunding’s ability to fill gaps in the provision of entrepreneurial finance continues among academics, policymakers and practitioners. In this, increasing attention has been paid to the geography of crowdfunding. This work has provided important evidence on various spatial influences on the location of platforms and campaigns and on their eventual success. In this paper, we take a rare look at the geography of the supply of crowdfunds. Specifically, our concern is with equity crowdfunding. Drawing on a hand collected data set, combining data on investments and on investors’ locations, we explore spatial influences on the extent of crowdfunding investment beyond commonly explored issues of distance.

1. Introduction

Academics and policymakers have enthusiastically embraced crowdfunding as an alternative source of external finance for entrepreneurial ventures (Gierczak et al., Citation2016). Drawing upon ideas from microfinancing (Armendáriz de Aghion and Morduch, Citation2000) and crowdsourcing (Afuah and Tucci, Citation2012), crowdfunding is the effort of collecting smaller amounts of money from a larger crowd via the Internet (Mollick, Citation2014). As a totem of the digital revolution (Brüntje and Gajda, Citation2016), it is positioned as a means to leverage the “wisdom of the crowd”, allowing would-be entrepreneurs to raise funds through distributed networks of investors, pre-customers or “fans”.

A key aspect of all forms of crowdfunding is the virtual connection between entrepreneurs and potential funders. This has allowed commentators to attach to it the notion of the “democratization of finance” (Cumming et al., Citation2021; Harrison, Citation2013); a term that is used to describe the “broadening and deepening of access to the capital market for ordinary, moderate income individuals and households” (Erturk et al., Citation2007, p. 554). In this, much is made of the idea of distributed networks of funders. While not quite “footloose”, crowdfunding is much less rooted in place than the traditional forms of external finance open to entrepreneurs (Agrawal et al., Citation2015; Guenther et al., Citation2018; Tang et al., Citation2020). As Langley and Leyshon (Citation2017, p. 1031) observe, “… [c]rowdfunding has the potential to challenge established notions of the ‘right place’ by appealing over the heads of traditional audiences for investment … Indeed, it may be that the crowdfunding economy has the ability to bring together geographically distributed funders and fundraisers according to the logic of the internet’s ‘long tail’. Those with shared interests who are separated by physical distance may create online ecologies”.

However, even in these online ecologies it appears that “geography still matters” (Agrawal et al., Citation2010, p.1). In exploring the spatial aspects of crowdfunding, existing empirical work has largely considered the places in which funding campaigns are situated (Gallemore et al., Citation2019) or the simple distance of funders from the location of the crowdfunding venture (Agrawal et al., Citation2011). Here, in broad terms, the evidence indicates that the most successful crowdfunding campaigns are concentrated in large cities (Baeck et al., Citation2014; D’Ambrosio and Gianfrate, Citation2016; Langley and Leyshon, Citation2017) and that distance continues to matter to funders (Agrawal et al., Citation2015; Dubois and Gromek, Citation2018; Guenther et al., Citation2018; Lin and Viswanathan, Citation2015; Mollick, Citation2014). Just as successful crowdfunding campaigns have been shown to cluster, with the spatial clustering of projects largely explained by “the pre-existing geographic distribution of population and economic activity” (Breznitz and Noonan, Citation2020, p. 1069), so too might we expect funders to be unevenly distributed across space and that features of their location will be explanatory. In short, we anticipate that the spatial distribution of crowd-funders will be “spiky” and that this spikiness will be more than a simple function of the relative location of fundraising campaigns. For instance, recent work has suggested that local levels of religiosity (Di Pietro and Masciarelli, Citation2021), immigration and immigrant diversity (Di Pietro, Citation2021) influence entrepreneurs’ ability to draw investment from the local crowd.

We believe that this manuscript is an early attempt to explore the spatial characteristics of the online ecologies of crowdfunding by looking at the geographic characteristics of supply. That is, our interest is in the places that contribute most to crowdfunding campaigns. While some past work has looked at the influence of context on the fortunes of particular crowdfunding campaigns (e.g., Josefy et al., Citation2017), remarkably little attention has been given to contextual influences on the pervasiveness of crowdfunding generally (Lewis et al., Citation2021; Schwienbacher, Citation2019). Indeed, much of the research on the behaviour of crowd-funders continues to treat them as spatially dispersed individuals whose only salient spatial feature is their distance from the fundraising ventureFootnote1. In contrast, this manuscript seeks to provide early evidence on attributes of places that relate to the intensity of participation in crowdfunding projects and to address the “lack of attention to the contingent composition of crowdfunding as an economic entity” (Langley, Citation2016, p. 308).

In developing our theoretical framework, we draw parallels with the diffusion of innovation literature’s emphasis on the cosmopolite (Rogers, Citation2003). Crowd-funders are not merely funders, they are also early adopters of an innovative means of venture funding. As innovation adopters, funders face significant uncertainty resulting from broad information asymmetries, with limited opportunities to reduce information asymmetries through traditional means (e.g., tightly-specified contracts, pre-investment screening, or post-investment monitoring) (Mochkabadi and Volkmann, Citation2020). Here, information challenges are twofold: funders must seek to reduce information asymmetries related to both projects and to the mechanics and risks of funding through a novel online platform. Paralleling the importance of access to cosmopolitan networks in the diffusion of innovation literature, we anticipate that sociodemographic and economic features of locations may represent variable connectedness and signal the legitimacy of new technologies. In this way, features of funders’ locations may serve to ameliorate information asymmetries and encourage participation.

While the term “crowdfunding” captures considerable variety in approachesFootnote2, equity crowdfunding may be closest to traditional conceptions of entrepreneurial finance (Block et al., Citation2018). Indeed, the policy community explicitly positions it as a means to “increase … job creation and economic growth by improving access to the public capital markets for emerging growth companies” (Jumpstart Our Business Startups Act, Citation2012, p. 1, emphasis added). It is consciously distinguished from the institutionalized financing practices of established organizations such as banks and venture capital firms, and discussed as an alternative form of financing in the digital economy (Baeck et al., Citation2014; Langley and Leyshon, Citation2017). Following this, equity crowdfunding is our focus. Specifically, we draw on data regarding investments made through Companisto, a German crowdfunding platform. We supplement this with hand collected data from a variety of sources that provide pertinent information on the characteristics of funders’ locations. Our aim is to increment knowledge of the geography of financing of smaller firms, beyond considerations of distance. This is a subject that has historically received limited attention (Hall, Citation2013; Pollard, Citation2003).

Consistent with previous findings, we observe a negative relationship between the distance of investors to campaign offices and various indicators of investment levels. However, beyond distance, we identify several spatial characteristics that associate with increased levels of investment. Borrowing from the literature on the diffusion of innovation (Rogers, Citation2003), we interpret these variables as increasing investors’ ability to attenuate important information asymmetries. Specifically, our analyses suggest that regional connectedness and the intensity of science and technology activities within a region are positively related to the amount and number of investments in crowdfunding campaigns that flow from that region. Our analyses control for various other spatial attributes of regions and campaigns that may be thought to influence investment.

The manuscript contributes to the current discussions on the understanding the different ecologies (Langley et al., Citation2020) of crowdfunding by focusing on the supply of equity-based funds. The current literature on the geography of crowdfunding is skeptical of the promise of a “flat world” in crowdfunding contributions and investment. It recognizes that where entrepreneurs are located “matters” (Breznitz and Noonan, Citation2020; Gallemore et al., Citation2019; Lin and Viswanathan, Citation2015). This manuscript focuses on the location of investors and tries to identify, beyond distance, what spatial characteristics of investors’ locations influence the likelihood of investing in entrepreneurial firms.

The paper is organized as follows. In section 2, we present the theoretical background and our hypotheses, followed by details account of methodology and variables in section 3. Section 4 presents the results followed by the concluding remarks.

2. Background

As Mason (Citation2010, p. 167) observes, “geographical considerations generally attract little consideration in studies of entrepreneurial finance”. In this way, for instance, the literature on small firms’ access to finance has typically treated them as “placeless entities” (Pollard, Citation2003, p. 440), with fund-seeking and fund-raising apparently insensitive to spatial influences. Yet, financial systems are intrinsically spatial (Leyshon, Citation2000; Martin, Citation1999). Most obviously, in systems characterized by both the demand for and supply of capital, the simple geographic distance between actors is likely to implicate costs. And, in this vein, past studies have demonstrated “spatial price discrimination” in small firm lending (Degryse and Ongena, Citation2005), but with evidence that these concerns may be ameliorated by new technologies (DeYoung et al., Citation2011; Petersen and Rajan, Citation2002).

Beyond distance considerations, research has less frequently considered features of the geography of demand, or of the places in which finance seekers and finance providers – typically borrowers and lenders – are co-located. To this end, numerous geographically contingent factors (including varying financial regulations and accounting practices, the value of assets, the availability of talent, and the extent of social and financial networks) are likely to influence the experiences of entrepreneurs seeking funds (Pollard, Citation2003). In addition to “external” influences, entrepreneurs’ place-specific expertise molds their networks and further influences their interactions with financial systems (Hall, Citation2013; Pollard, Citation2003). This simultaneous relationship between knowledge and space shapes geographies of financial practices (Lee, Citation2011) and these, ultimately, affect the processes and outcomes of securing external financing for businesses (Hall, Citation2013). The reciprocal relationship between the geography of venture capitalists and hubs of innovative firms is a prominent example of the space sensitivity of finance (Clark, Citation2005; Gompers and Lerner, Citation1999; Mason and Harrison, Citation1995). In summary, and despite some sense that advancements in information and communication technologies may reduce the “tyranny of distance”, empirical research is broadly consistent in demonstrating that small firms’ financing outcomes continue to be affected by their locations (e.g., Alessandrini et al., Citation2008; Bellucci et al., Citation2013; Langley, Citation2016; Lee and Brown, Citation2017; Lee and Luca, Citation2019; Pike and Pollard, Citation2010; Powell et al., Citation2002).

The influence of geography is also apparent in the nascent crowdfunding literature. Despite taken-for-granted assumptions concerning the enabling role of crowdfunding platforms in bypassing the liability of location, evidence suggests that the geography of crowdfunding is nonetheless uneven and impacted by “digital and place-based clustering” (Langley and Leyshon, Citation2017, p. 1034). As collaboration between crowdfunding platforms and mainstream financial organization such as venture capitalists increases, it seems likely that crowdfunding, similar to other forms of financing, will become increasingly space-sensitive (Gallemore et al., Citation2019; Langley and Leyshon, Citation2017). Signs of an uneven distribution of crowdfunding activity for small and innovative firms are becoming apparent. Crowdfunding platforms are typically located in financial hubs, alongside agglomerations of knowledge and expertise (Baeck et al., Citation2014; Langley, Citation2016; Langley and Leyshon, Citation2017). Not surprisingly, most successful campaigns are also launched within the large cities (Dubois and Gromek, Citation2018; Langley, Citation2016; Mollick, Citation2014) characterized by more diverse and sophisticated sources of human capital (Florida, Citation2002). Also, proximity to “like-minded” individuals encourages entrepreneurs with successful crowdfunding campaigns to relocate (Noonan et al., Citation2021). This research, however, is not concerned with the spatial distribution of crowdfunding platforms and campaigns, but with that of the funders and, more specifically in this case, investors.

The goal of this research is to contribute to a better understanding of the geographic influences on participation in equity crowdfunding by investors. That is, our interest is in the context of regions that are characterized by relatively greater crowdfunding investment activity, an area that is understudied (Giudici et al., Citation2013). We speculate that, after controlling for differences in the characteristics of projects and structural differences between regions, features that serve to reduce the information asymmetries associated with investing through the novel medium of crowdfunding will associate with higher relative investor participation. We anticipate that features of the investors’ locations help them to, more and less, discount both the information opacity concerning projects and the information opacity concerning the mechanism of investment through a crowdfunding platform.

To reduce information asymmetries, individual investors rely on knowledge and information they currently hold or can readily acquire. Prior research has explored crowd investors’ concerns with the quality of ventures (Ahlers et al., Citation2015; Mollick, Citation2014), investigating the relationship between propensities to invest and, inter alia, the quality of presented materials, the frequency and detail of campaign updates, the age of investee businesses, the equity stake offered, the disclosed financial statements, and proposed exit routes (e.g., Ahlers et al., Citation2015; Block et al., Citation2018; Mollick, Citation2014). Other work has noted the crowd’s attention to the quality of the human capital, proxied by the education of the members or the size of management boards (Ahlers et al., Citation2015), and with individuals’ social capital (Giudici et al., Citation2013; Lin et al., Citation2013; Mollick, Citation2014).

However, simple proximity is likely to be an important way of reducing uncertainty by increasing the likelihood of interacting with individuals and groups who are familiar with either the project or the principals. Certainly, distance appears to be an important factor in the probability of participating in crowdfunding projects (Dubois and Gromek, Citation2018; Gallemore et al., Citation2019; Giudici et al., Citation2013). Even as technologies and regulations permit more distant investment, the probability of investing still appears to be an inverse function of distance. Indeed, recent work suggests that local biases in equity crowdfunding increase with the size of individual investments. Of course, proximity effects are likely to be about more than simple Euclidean distance between funders and projects. For instance, research indicates that investment decisions are influenced by fellow investors. Potential investors gain additional information from an investment opportunity by observing early investors’ decisions or may seek to reduce risks by simply imitating the behaviours of prominent investors. In this way, colocation forces become reinforcing, underpinned by socio-spatial influences on fundraising and funding (Dejean, Citation2019; Kromidha and Robson, Citation2016; Vismara, Citation2016).

The key issue is investors’ preference for projects that are “familiar” or that may be rendered familiar. It is well established in the broader investment literature that investors’ information-driven behaviour (Massa and Simonov, Citation2006) leads to investments in stocks that are familiar or where familiarity is inexpensively acquired. In short, “[f]amiliarity breeds investments” (Nofsinger, Citation2005, p. 68). The role of familiarity is evident in investors’ preferences for things that are relevant to their geography, relevant to their profession, or well-known brands (Massa and Simonov, Citation2006). In the case of equity crowdfunding, familiarity lowers the costs (time and money) associated with reducing information asymmetries and provides more opportunity to acquire tacit knowledge about the businesses and the entrepreneurs (Estrin et al., Citation2018). A preference for the familiar is likely to be compounded by the relatively higher costs of due diligence, evaluation and monitoring that attach to the smaller investments that are typical in a crowdfunding setting (Ahlers et al., Citation2015).

The role of distance in rendering familiarity is well-established in the research on traditional forms of financing. The existence of a “home bias” is evident when investing in public companies (Massa and Simonov, Citation2006; Mondria and Wu, Citation2010; Nofsinger, Citation2005). Not surprisingly, “home bias” also influences investment behaviour in more informationally opaque smaller and newer firms. One might also infer the importance of proximity from widespread evidence on the concentration of venture capital investors and venture capital-backed firms (Bengtsson and Ravid, Citation2009; Chen et al., Citation2010; Fritsch and Schilder, Citation2008; Mason and Harrison, Citation1995; Sorenson and Stuart, Citation2001). Distance has also been shown to play a similar role in bank financing, albeit somewhat ameliorated by digital technologies (Alessandrini et al., Citation2008; Bellucci et al., Citation2013; Degryse and Ongena, Citation2005; Lee and Brown, Citation2017; Lee and Luca, Citation2019). In the case of crowdfunding, one might anticipate that the digital revolution will further reduce distance-related information costs. Nevertheless, the associated costs of gathering tacit knowledge about the business and monitoring post-investment performance continue to be lower for local investment opportunities (Agrawal et al., Citation2015; Dubois and Gromek, Citation2018; Giudici et al., Citation2013; Guenther et al., Citation2018; Lin and Viswanathan, Citation2015). Indeed, some evidence suggests that even more sophisticated investors, who are presumably better at due diligence and at assessing venture quality, are sensitive to distance (Guenther et al., Citation2018). Simply, colocation enables the investors to gather information about the market, the business, and the entrepreneur in a less costly manner. This is particularly important when set against the small size of the typical investment in a crowdfunding campaign. Following these arguments, and as segue to our main concerns, we hypothesise that:

H1:

Both the propensity and intensity of investments will be negatively related to the distance between the location of the project and the location of investors.

The notion of “connectivity” is firmly entrenched in the literature on industrial clusters, supplementing local buzz with global pipelines that link firms in the cluster to important sources of novel knowledge and information (Bathelt et al., Citation2004). In much the same way, the diffusion of innovation literature affords “connectedness” a central role (Rogers, Citation2003), where individuals are more likely to adopt innovations as their connectedness to the outside world increases through social engagement, contact with change agents, and exposure to mass media. More prosaically, recent work has emphasized the importance of physical connectivity (i.e., “the diffusion of transport networks”) to the growth of cross-border investment (Chen and Lin, Citation2020), with the proliferation of direct flights, the growth in liner shipping and the expansion of high-speed rail leading to a substantial increase in international investment activity.

We extrapolate from observations on the importance of connectivity for the flow of ideas, funds and, ultimately, innovations, to argue that better connectivity, or connectedness, will associate with greater participation in equity crowdfunding. That is, all things being equal, places that are better connected will more likely be home to individuals investing in crowdfunding projects. Here we see connectivity as both a physical attribute – the extent to which people and “things” flow to and from the place – and a digital attribute – the extent to which the individuals located in the place engage in digital commerce.

In this way, connectivity is likely to foster familiarity, to expose residents to new ideas and new technologies, and, through these, to reduce the information asymmetries and perceived risks associated with crowdfunding. In many ways, this echoes recent conversations around the central role of cities in regional development; in particular their function in innovation processes and as nodes in global networks, modulating broad capital flows (Clark et al., Citation2018). Residence in a central location is likely to provide access to more diverse resources and to allow individuals to build more sophisticated localized social capital (Laursen et al., Citation2012), better placing them to evaluate markets and the prospects of innovative projects. The connectedness of a region increases investors’ abilities to search for information and decrease the costs of acquiring information about projects and their markets. Therefore, we propose that:

H2:

Higher local connectivity will positively associate with the propensity and intensity of engagement in crowdfunding investment.

Beyond connectivity, the likelihood of participating in equity crowdfunding will be moderated by perceptions of compatibility and complexity (Rogers, Citation2003). Compatibility is concerned with the consistency of crowdfunding activity with the values, experiences and needs of potential investors. Complexity is concerned with how easily potential investors find it to understand and use the technology involved. In other words, a key aspect of investing through crowdfunding is understanding the innovative online mechanisms through which evaluation, financial transactions, and future monitoring routines become possible. Here we view investment through a crowdfunding platform as an innovative approach to entrepreneurial finance (Block et al., Citation2018), and investors (or those who conduct due diligence but decide not to invest) as early adoptersFootnote3 of this innovation. As early adopters, investors must demonstrate a higher tolerance for risks, an ability to mitigate uncertainties, have more extensive and diverse expert networks, and be characterized by greater financial resources and financial literacy (Rogers, Citation2003). Importantly, there is ample evidence in the literature on smart cities (Kourtit and Nijkamp, Citation2012) or cities and innovation (Shearmur, Citation2012) to suggest that many of these aspects have territorial bases.

We believe that a key indicator of the relative compatibility and complexity of crowdfunding technologies for individuals may be found in the pervasiveness of digital technologies, in particular the internet, at the regional level. To the extent that e-shopping has been historically a predominantly urban phenomenon (Farag et al., Citation2006), individuals located in cities may be more likely to have had more experience with technologies analogous to crowdfunding platforms, both directly and through social networks. Investment through crowdfunding often requires that individuals assess the risks and prospects of the projects based on information that is presented solely online. Potential investors must mitigate both the information opacity surrounding investment projects, and also the information asymmetry concerned with the technical transaction of online crowd investing. In other words, investors need to be literate enough to understand the mechanism of investing through an online platform, evaluate the associated risks, and communicate with other investors. The pervasive use of information technologies would allow members of the crowd to seek information and evaluate options at a lower cost. Therefore, it is expected that more pervasive local use of the Internet would lead to a higher proportion of individuals who are motivated and capable to try to invest through crowdfunding platforms. Accordingly, we hypothesize that:

H3:

Higher local internet use will positively associate with the propensity and intensity of engagement in crowdfunding investment.

The issue of compatibility extends beyond the pervasiveness of e-commerce in a region. Rogers, (Citation2003) early adopters are typically technically literate and rely upon a technology “buzz” created by likeminded individuals in extensive (and local) social networks. Homophily, the tendency to have ties with similar people, may create a more (or less) supportive environment around experimentation and the adoption of new technology (Rogers, Citation2003). However, while the adoption of equity crowdfunding as a means of investment requires some degree of familiarity with this specific technology, it is also likely to be enhanced by location within a technically sophisticated milieu, more generally. In this way, familiarity can be supported through shared practices of experimentation and risk taking, allowing potential investors to learn from the signaling behaviour of their peers (Vismara, Citation2018). Following this, we hypothesize that in regions with a higher proportion of individuals working with new technologies, the adoption of crowdfunding as a means of investment will be facilitated by an atmosphere of shared experience and related expertise. To this end, we suggest that:

H4:

Higher local technology familiarity will positively associate with the propensity and intensity of engagement in crowdfunding investment.

The theoretical framework laid out above is concerned with spatial factors that would affect the ability of the potential investors to mitigate the information asymmetry pertinent to crowdfunding projects and processes of crowdfunding investment. Of course, other factors will bear on investors’ likelihood of investing and these, in turn, may be sensitive to space. For instance, individuals’ wealth or the dynamics of the financial sector in their regions are likely to influence degrees of risk tolerance and attitudes towards new financial technologies. In addition, projects are inevitably heterogeneous and differences in their quality will relate to the probability of successful fundraising (Ahlers et al., Citation2015; Mollick, Citation2014). We seek to control for these influences in our modeling. The specific proxies and our data choices are outlined in the Methodology section that follows.

3. Methodology

The empirical work of this study models the following equation:

Where is the amount of investment, the number of investors, or the number of investments from location

in campaign

(in this way we investigate 3 different dependent variables);

is the distance of campaign

’s office from

;

captures investors’ location-specific characteristics;

is the set of the variables that control for the quality of the project; and,

is a set of variables that capture the structural business and demographic characteristics of the region c.

3.1. Data

Data for analyzing the spatial characteristics of crowd-equity investments are drawn from multiple sources. Our principal source is Companisto. Companisto is a Berlin-based equity crowdfunding platform that provides easily accessible and detailed information on projects, the location of investors, and the date and amount of investments. The platform has been active since 2012 and, as of May 2019, more than 96 thousand investors from 92 counties had participated in 119 rounds of investmentsFootnote4. From this perspective, Companisto is one of the leading European-based equity crowdfunding platformsFootnote5.

Data on each campaign was hand-collected by the research team. Data collected in this phase recorded the characteristics of each campaign, such as the money sought, stage of the development of the firm, and various other characteristics of the firm, (including location, industry, business age, size of the management team, use of proceeds, patent, export activities, and sales turnover). In the second stage, a web crawler was developed to collect further information on each investmentFootnote6. Data collected at this stage include the name (or nickname) of investors, the campaign in which the funds were invested, the amount and date of the investment, and the location of the investors.

In the final phase, data on the spatial characteristics of investors’ locations were collected. While initial analysis indicated that investments were made from more than 4 thousand cities and more than 90 countries, the amount or frequency of investments in some of these locations was small. Accordingly, we ranked cities on the basis of the total investment amount. We focus our analyses on the eighty-eight cities that had total investments of more than €50,000. The investments made in these cities comprise 64% of total investments. Since most data on spatial characteristics were available at NUTS2, the corresponding NUTS2 was determined for each location. Our eighty-eight cities belong to 38 NUTS2 regions. Investors in these NUTS2 regions invested in Companisto campaigns around 39 thousand times, with a total investment value of €26.64 million. Regions in this data are located in Germany, Austria, Switzerland, Belgium, as well as the city of London, UKFootnote7. In a small number of cases, we were unable to attribute the investment to a NUTS2 region, with the investor location only available at the country level. In these instances, the amount or number of investments was distributed over the regions of that country proportional to the size of known investments from region in campaign

. As robustness check, the analyses were run without this adjustment, setting those observations as missing. The results did not change.

In the final phase, the coordinates of the investor cities and the project offices were collected to calculate the distance between the head office of campaign and region

. Further information on the source of data and on the characteristics of the regions, collected from multiple sources, are presented in Appendix 1.

3.2. Dependent variables

As noted, we investigate three dependent variables. The first dependent variable is the amount invested in campaign from region

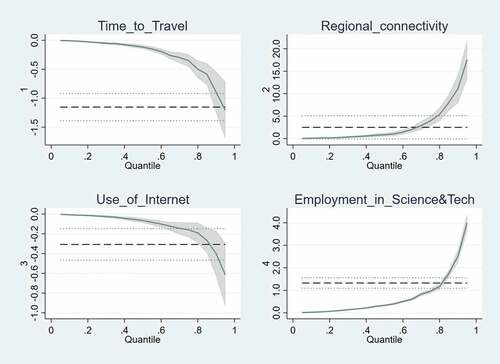

in €000s. Unsurprisingly, the data are right skewed. Importantly, OLS assumptions were violated. Accordingly, we employ Generalized Linear Modelling (GLM) to estimate the equationFootnote8. As a robustness check, controlling for the influence of outliers and observing the estimates for higher values of investments, this equation was also estimated by quantile regression. The results of the glm estimation, quantile regression at the median, and the graph of changes in coefficients of quantile regressions are presented in Panel (a) and (b) and .

Figure 1. Coefficients of variables of interest- quantile regression of amount of investment (T. Euros).

Table 1. Estimation results.

The second and third dependent variables are the number of investors and the number of investments in campaign from region

. These two variables are different since some investors invest in specific campaigns several times. However, we did not anticipate a substantial difference between the two models. Given the count and right skewed nature of the variables, we model them using a negative binomial specification.

The units of analyses are therefore the amount of investment, number of investors, and number of investments from region in campaign

. The results of the estimations are presented in , panel (c) and (d). All the models were estimated with STATA 15.

3.3. Independent variables

Distance in this research is estimated by travel between a project firm’s office and the coordinates of the given investor’s region. To do this, we use the STATA module georoute (Weber and Péclat, Citation2018), to calculate the travel distance in kilometers and hoursFootnote9. While both measures were added to the dataset, we only use hours in the analyses due to inevitable collinearity issues.

Regional connectivity, consistent with the second hypothesis, is proxied by the share of annual road freight transport by regions of loading in national road freight transport (measured in ’000 tons). Since it is likely that larger regions will have more extensive roads networks and, consequently, have a higher share of loading (i.e., connectivity becomes a simple proxy for population and not physical connectivity), the index is adjusted by the region’s share of national population.

Consistent with hypothesis 3, we measure the pervasive use of the Internet using the percentage of the regional population that purchased goods online in the past 12. Unfortunately, these data were only available at the NUTS1 level and enter our models as such.

To proxy for general technology familiarity, we record the percentage of individuals working in science and technology sectorsFootnote10. In addition, we calculated the location quotient (LQ)Footnote11 for ICT. However, as with our two measures of distance, our two measures of broad technology familiarity were predictably collinear. In this case, only the latter is included in our main models.

3.4. Control variables

In building our models we capture a variety of control variables with a view to ameliorating concerns over omitted variables bias that are common in work of this kind. Specifically, we control for both project- and regional-level factors that are likely to bear upon our various measures of the volume of investment.

At the project-level, control variables related to the characteristics of the campaigns and entrepreneurs are included. The empirical literature on the influence of project characteristics on campaign success is reasonably well established (e.g., Anglin and Pidduck, Citation2022; Lukkarinen et al., Citation2016; Mollick, Citation2014). Here, we begin by controlling for the amount of money sought at the beginning of the campaign. Some campaigns had limited goals. That is, the total amount of investment cannot exceed the campaign goal. This follows past work that suggests that the motivation of investors may be reduced after a project has met its financial goals (Kuppuswamy and Bayus, Citation2018).

In addition, following the literature on traditional forms of investing, we anticipate that firm age will influence investment activity; with the longer trading records and more readily available information of older businesses providing greater assurance to potential investors. We also control for investors revealed preference for innovation (Johan and Zhang, Citation2020) by identifying whether campaign firms held patented or had patent applications that were current at the time of the investment.

At the level of the project, we attempt to capture some element of the social capital influences on investing. Previous studies have demonstrated that higher levels of social capital – from family and friends (Agrawal et al., Citation2015), through a social network such as Facebook (Mollick, Citation2014), and internally within crowdfunding platforms (Butticè et al., Citation2017; Colombo et al., Citation2015) – increases the likelihood of campaign success. Unfortunately, information on the social contacts of the entrepreneur or entrepreneurial team is limited on the platform. However, we employ a binary variable, equal to 1 if the entrepreneurs disclosed contact information on Facebook, Twitter, LinkedIn, or Xing. This indicates their use of important social networking sites and is likely to signal a commitment to building and maintaining social capital. As an alternative approach, we constructed a further variable by calculating the number of social network contacts that were shared as well as the number of comments that was exchanged in the platform. Both approaches yielded broadly similar results.

Finally, Companisto identifies the primary industrial classification of the campaigning firm. To aid interpretation, we then aggregate these classifications into 5 categories: E-commerce and online services; Electronics; Food and beverages; Information Technology solutions; and others. The analysis also includes a campaign year control and dummy variable that indicates where firms sought loans rather than investments.Footnote12

Some additional project-level variables were also captured. These included the stage of the development of the firm, the intended use of proceeds, whether the firm exports, the management team size, disclosed revenue, and the percentage of shares offered. However, in preliminary modeling, none of these variables proved significant predictors of our dependent variables. With a view to parsimony and to aid interpretability they are not reported here. In addition, we tested whether the language of the campaign (English or German) associated with our investment variables. However, language proved to be collinear with year; from 2012, fewer campaigns were presented in German. Accordingly, we elected to prefer year in our models, since it also controls for the popularity of crowdfunding platforms.

Turning to regional level influences; intuitively, one anticipates that the simple “size” of a location will correlate with the availability of human and financial resources. Accordingly, we use measures of both population and economy size. For the former, we use the natural log of the population of the region. For the latter, we use per capita Gross Value added (GVA). However, per capita GVA is curvilinearly related to the dependent variables. Moreover, the squared value of per capita GVA is highly correlated with per capita GVA. Accordingly, to allow us to observe the non-linearity but avoid collinearity problems, we enter per capita GVA as 3 dummy variables representing the 2nd, 3rd and 4th quartiles of per capita GVA in the 38 regions, with the 1st quartile acting as the reference category. (See Appendix 1). Several other variables were initially included in the model to proxy for employment and education, such as, the percentage of employed individuals and the percentage of individuals with tertiary education. However, inclusion of these variable creates multicollinearity problem, as education and employment statistics were highly correlated with per capita GVA and population size. This, of course, is not unexpected, (Florida, Citation2005). Accordingly, only the measures of population and per capita GVA were retained in the models.

Our models also include a measure for localized trust. Giudici et al (Citation2013) distinguish between an individual’s personal social capital and the social capital that is inherent to the location in which they reside. They report a significant positive relationship between an entrepreneur’s personal social capital and the probability of reaching funding goals, but a not significant coefficient for territorial social capital. However, “[t]rust affects the fraction of returns that investors can retain in their successful investment outcomes” (Bottazzi et al., Citation2016, p. 2288), and therefore increases the probability of investment in ventures. To this end, Lederman et al. (Citation2002, pp. 509–510) explain “ … that communities with stronger ties among its members are better equipped to organize themselves to overcome the free-rider problem of collective action”. Following this rationalization, we introduce an adjusted “incident rate” as a proxy for trust. The incident rate is calculated by the sum of the number of vehicular thefts, intentional homicides, burglaries of private residential premises, and robberies, divided by the total number of these crimes in the corresponding country. This method accounts for the different practices of crime reporting among countries. However, to account for the effect of population density, the incident rate is adjusted by the share of the population of the corresponding region from its country population.

Business structural differences (other than employment in IT sectors) are measured by calculating LQs for the financial sector and manufacturing. LQs for financial sectors (except insurance and real estate sectors) and manufacturing are calculated at NUTS2 in relation to the relevant national employment. The LQ of financial services allows us to control for the possible effect of an active financial services market on the intensity of crowdfunding investment. While investment-activity in regions may associate with more investment through crowdfunding, it is also possible that individuals are drawn to crowd equity investing when there are relatively fewer opportunities to engage in traditional forms of investment. In the calculations of LQs, we use industry classifications from NACE Rev.2.

Other structural variables were initially considered in our preliminary modeling. However, these proved to be highly collinear with the other key variables. For example, we aimed to measure population diversity in the regions by the percentage of foreign-born individuals. However, this measure is highly correlated with per capita GVA.

4. Results

4.1. Descriptive statistics

As noted, the sample consists of 4,352 investments made from 38 regions in 98 campaigns between 2012 to 2018. Panel (a) of presents the descriptive statistics for our dependent variables. Means and standard deviations of the dependent variables illustrate the right-skewed nature of the data distribution and confirm that the choice of analytical techniques. In addition, this panel includes the mean and standard deviation of travel time by road in hours from the home city of the investor to the city of the campaign’s office. A minimum value of zero indicates that both the investors and the campaign are located in the same city.

Table 2. Descriptive statistics.

Panel (b) gives summary statistics for the region-level variables employed in our analysis. The value of shares of loading and the incident rate in a region naturally vary between 0 and 1. However, after adjusting for relative population, maximum values may be above 1.

Panel (c) reports the summary statistics for campaign-level variables. Although not explicitly reported in the table, approximately 80% of businesses were early stage of development, around 6% were at growth phase, and about 14% were at the seed phaseFootnote13. For analysis purposes, we use the natural log transformation of business age to account for the right skew in the data. The most common sectors for projects include E-commerce and online services, Electronics, IT solutions, and Food and Beverages. Given the relative rarity of other industries (e.g., media, textiles, cosmetics, and chemical products), we combine these into a single category. This group, “Others”, represents 20% of firms. Only 16.3% of the firms had registered patents, while 7% of had at least one ongoing patent application at the time of the campaign. Most firms, around 76%, elected to place no upper limit on the amount of funds they were seeking. In other words, entrepreneurs could continue to raise funds after they had reached their campaign goals but had time remaining on the duration of the campaign.

4.2. Multivariate analysis

reports the results of GLM estimations for (a) the investment amounts in €000s, (b) quantile regression at the median for investment amounts in €000s, (c) negative binomial estimation of the number of investors, and (d) for the number of investments. For both the GLM and Quantile regressions we exclude highly influential outliers from the analyses.

Consistent with the first hypothesis, and with the findings of previous research, simple distance is negatively associated with all dependent variables. Here we measure distance as the “time to travel” from investors’ regions to campaign offices. As expected, our results indicate that the investments from more distant regions are smaller and involve fewer investors. Importantly, this holds while controlling for key regional economic indicators, such as GVA, the concentration of financial sectors, and the concentration of individuals who are active in science and technology. That is, distance matters and is not simply a function of regional size, wealth or sectoral relatedness. Given that most platforms are located in large cities, and most campaigns are launched from large cities (Mollick and Robb, Citation2016), the importance of a local bias suggests that more affluent regions and big cities would continue to dominate equity crowdfunding activity. In this light, the “democratizing” effects of equity crowdfunding are likely to be much more limited than early commentary assumed. Reinforcing this notion, the quantile regression graph for “time to travel” shows that, not surprisingly, distance becomes more influential as investment amounts increase, but is relatively unimportant in the bottom quintile of investments.

Turning to hypothesis 2, which was concerned with “connectivity”, our measure of physical regional connectivity, adjusted loading share, is significant in explaining variations in the amount and frequency of investment from regions. In other words, regions that act as hubs for the transportation of goods are more likely to be home to crowdfunding investors and to be the source of higher amounts of crowdfunding investment. Importantly, this holds over-and-above the effect of distance to campaign and after controlling for population effects and industrial structure. In short, to borrow a metaphor (Bathelt et al., Citation2004), while “local buzz” may be an important source of investment, investment may also be achieved through “pipelines” flowing from well-connected places.

However, while physical connectivity seems to promote investment from a region, our measure of digital connectivity performs in contrast to our expectations. Specifically, the percentage of individuals (within a region) who used the Internet to order goods online in the past 12 months is negatively associated with investment in the campaigns; whether measured as amount invested, number of investments or number of investors. Hypothesis 3 positioned the relative incidence of online shopping as an indicator of digital connectivity and a signal of familiarity with the technologies used in crowdfund investing. In this way, we were consistent with what the literature on the spatial characteristics of online shopping has termed the “innovation-diffusion” hypothesis (e.g., Beckers et al., Citation2018). In its initial conception (Anderson et al., Citation2003, p. 421), this simply held “that urban populations are most likely to adopt e-retail because they are better educated and more likely to use the Internet actively for other purposes”. As our descriptive statistics indicate, the proportion of individuals engaging in online shopping is high in all the regions where we observe investment activity. As anticipated by Anderson et al. (Citation2003), the technology of online shopping has diffused beyond urban settings, at least in developed countries (cf. Song, Citation2021). In this way, online shopping is likely to be an outdated measure of digital connectivity and familiarity. Rather, consistent with an “efficiency hypothesis”, individuals may be more inclined to buy online in areas that have less direct access to a variety of goods and services (Kirby-Hawkins et al., Citation2019). In other words, this measure is likely to be an inverse proxy of the diversity of the locally available goods rather than the pervasive use of the internet for searching or the familiarity with key technologies.

Following this, to provide an alternative test for hypothesis 3, we add the LQ for IT sector. However, given the collinearity with the percentage of individuals who work in science and technology, we remove the latter from the supplementary analysis. After removing the percentage of individuals who are employed in science and technology sectors, the LQ for IT has a positive and statistically significant relationship with the investment amount and frequency. Moreover, online ordering becomes not significant in two of the four models. Indeed, online ordering is positive and significant in a Negative Binomial regression of the number of investors (see appendix 2 for these supplementary analyses). It is also worth recalling that online shopping is measured at the NUTS1 level, providing less fine regional data than other variables.

The fourth hypothesis investigates the influence of a highly educated workforce on the propensity and intensity of engagement in crowdfunding investment. Consistent with our hypothesis, a higher percentage of employment in science and technology within a region is a positively associated with the frequency of investments or number of investors. Moreover, the effect is more pronounced at higher values of investments ().

Beyond our hypotheses, our control variables behave much as anticipated. For instance, population and GVA are both positively associated with the amount and frequency of investment. That is, more populated and wealthier regions are more likely to be home to equity crowdfunding investors. We also note a significant negative association between the adjusted crime rate and investment in a crowdfunding campaign in the quantile regression at the median (panel b of ). Recall, that we envisaged this variable as an indicator of “trust” or social cohesion. However, this variable is not significant in the other models. Further investigation of the graph of the coefficient of incident rateFootnote14 indicates that the negative trend is visible for larger investment amounts only: an issue of intensity rather than propensity. In terms of business structure, regions with a higher proportion of employment in manufacturing and financial services are less likely to contribute to equity crowdfunding. Finally, our campaign-level variables confirm expectations, such that patenting activity and campaign ambitions are positively associated with investment activity.

4.3. Robustness checks

reports Variance Inflation Factors (VIFs) associated with our analyses. The VIFs do not suggest multicollinearity problems in any of the models reported in , with all values smaller than 10.

Table 3. Variance inflation factors.

Given the continued importance of “distance”, it is possible to interpret our findings simply as a function of the colocation of campaigns and investors in innovative, “connected” places, full of highly educated and skilled people – more evidence of Florida’s (Citation2002) geography of talent. However, since our results indicate that other spatial considerations “matter” even after controlling for distance, we became interested in whether our hypotheses hold after removing the effect of local investment activity. Much of the prior literature suggests that the majority of initial investment is from local sources, often family, friends, and the entrepreneurs themselves. However, our interest was in how spatial considerations influenced investment activity beyond these “localization” effects. For this reason, we re-estimated our models having excluded investments from the city in which the campaign firm is located. Our results do not change. There are clear spatial influences on equity crowdfunding investment that go beyond simple considerations of distances between investors and entrepreneurs.

5. Concluding remarks

Crowdfunding’s “manifesto” emphasizes its ability to channel crowd resources to entrepreneurial firms that might otherwise be left behind by traditional financial institutions. In this positive view (Gallemore et al., Citation2019), access to finance for entrepreneurs for the commercialization of innovation is more inclusive (Mollick and Robb, Citation2016; Stevens et al., Citation2015). Critics, however, question the evenness of crowdfunding ecologies and, thus, their inclusiveness. As Gallemore et al. (Citation2019) suggest “[i]n principle, crowdfunding is a knowledge sector, subject to agglomeration economies and information-sharing benefits” (p.1393) and therefore, bound to be affected by “the intersection of digital network and place-based clusters” (Langley and Leyshon, Citation2017, p. 1032). The clustering of successful campaigns in traditional hubs of innovation and finance (Shiri M Breznitz and Noonan, Citation2020) indicates that the geography of crowdfunding is “spikey”. Moreover, “campaigns” location shapes their fortunes” (Gallemore et al. Citation2019, p.1399). Importantly, this spatial unevenness is not only the effect of a home bias in investment (Agrawal et al., Citation2014; Lin and Viswanathan, Citation2015; Mollick, Citation2014). Rather, recent studies suggest that other spatial factors may be at work. For instance, past work has shown that the success of crowdfunding campaigns may be influenced by, inter alia, urbanization and affluence (Gallemore et al., Citation2019), population and economic activities (Shiri M Breznitz and Noonan, Citation2020), cultural similarities (Burtch et al., Citation2014), or gender and racial differences (Kleinert and Mochkabadi, Citation2021; Younkin and Kuppuswamy, Citation2018).

Our interest in this research, however, was not with successful campaigns, but with the source of money. We were interested to understand, beyond any home bias, what spatial factors might explain the supply of crowdfunds. Our findings also suggest that investment follows a spiky pattern. Considering investors in crowdfunding as early adaptors of an innovative financial intermediary, we draw from Rogers’s, (Citation2003) diffusion of innovation theory to link the spatial characteristics of places with the ability to mitigate information asymmetries attendant upon investment through crowdfunding platforms.

Our results suggests that regions that are more physically connected are more likely to be home to investors. However, counter to our expectations, we observe a negative effect of digital connectivity, as proxied by online shopping. We rationalized this in terms of an “efficiency” hypothesis (Kirby-Hawkins et al., Citation2019), in which higher rates of online shopping indicate access to fewer and less sophisticated goods and services. In this way, online shopping is a poor proxy for connectedness, but an inverse indicator of the likelihood of directly encountering new products and services.

We had also envisaged internet usage as an indicator of technological familiarity and a means to reducing technology uncertainties in the process of investing. As an alternative test of this hypotheses, we explored the effect of relative employment in ICT. Here, the LQ of regional ICT employment was positive and significant.

In line with other studies, we also observe that distance matters. However, it is intriguing to note that distance is not a significant predictor of investment at low levels of investment. Moreover, when we removed investments that are from the city of the entrepreneurs, the effects of our other spatial influences are unchanged. Spatial influences, beyond the distance between investors and investees, shape the supply of crowdfunds. Indeed, although positioned as a control variable, we observe that more populated and more affluent regions are more likely to be sources of funds.

Of course, these results do not entail that crowdfunding investment does not contribute to increased inclusiveness in financial markets. However, the concentration of successful campaigns in large, affluent cities is mirrored by a concentration of investors in similar (not always the same) places. These places are typically innovative, sophisticated, and connected. Given this, it seems naïve to assume that “ordinary [people] will be able to go online and invest in entrepreneurs that they believe in”Footnote15 and that crowdfunding, left to its own devices, will democratize either the demand or supply of entrepreneurial finance.

Certainly, our research is not without limitations. We have only considered one equity platform, in Germany. The strong presence of creative and digital industries in Berlin, the headquarter of Companisto, made this city a major player in crowdfunding activities (Langley et al., Citation2020). Unfortunately, we are unable to investigate investor motivations and it may be that the these are influenced by the sorts of ventures Companisto attracts. In this vein, it is also unfortunate that the research could not control for the effect of different types of campaigns. For example, we might speculate that green tech start-ups would receive funding from regions with similar environmental concerns. However, the low number of observations in specific industries does not allow us to explore this.

Acknowledgement

The authors are thankful to Dr. Farid Seifi for his invaluable technical assistance.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. Of course, beyond spatial considerations, recent funder-level analyses identify heterogeneity in the preferences and attitudes of funders (e.g., Brent and Lorah, Citation2019; Wallmeroth, Citation2019).

2. With the most common types being equity, rewards-based, donation-based and debt.

3. Rogers (Citation2003) classifies the adaptors of innovative products and mechanisms into five categories: Innovators, early adaptors, early majority adaptors, Late majority adaptors, and laggards. Given the newness of crowd equity platforms; we think the current investors are the innovators and early adaptors of the system.

5. https://www.eu-startups.com/2017/11/top-10-equity-based-crowdfunding-platforms-in-europe/ (Accessed 30 April, 2019).

6. The data used for the analysis was collected on date 18/12/2018. Campaigns for developing real estate ventures were excluded.

7. No other region in the UK met our threshold of inclusion.

8. To identify the appropriate family and link function, the data was fitted with EasyFit 6.5. The glm method with gamma family and link function power(4) is used for estimation.

9. Georoute connects to the HERE Application Programming Interface (API) (https://developer.here.com to retrieve distances).

10. We use https://ec.europa.eu/eurostat/cache/metadata/Annexes/htec_esms_an3.pdf to categorise industries.

11. LQ measures the relative concentration of employment in each sector based on the regional and reference location.

12. We recognise that there is variation in the regional measures across time, however, we used the most recent and available data within the timeframe of the study. We could not observe substantial differences in structural measures where they were available, therefore, we content ourselves with a series of cross-section modeling. We thank the editor for bringing this to our attention.

13. This categorisation is taken directly from Companisto and is age-based.

14. Available upon request.

15. From President Obama’s speech (5 April 2012) on crowdfunding signing the JOBS ACT. The authors replace “Americans” with people.

https://obamawhitehouse.archives.gov/blog/2016/06/08/promise-crowdfunding-and-american-innovation

References

- Afuah, A., and C.L. Tucci. 2012. “Crowdsourcing as a Solution to Distant Search.” Academy of Management Review 37: 355–375.

- Agrawal, A., C. Catalini, and A. Goldfarb. 2010. Entrepreneurial Finance and the Flat-World Hypothesis: Evidence from Crowd-Funding Entrepreneurs in the Arts.

- Agrawal, A.K., C. Catalini, and A. Goldfarb. 2011. The Geography of Crowdfunding. National Bureau of Economic Research.

- Agrawal, A., C. Catalini, and A. Goldfarb. 2014. “Some Simple Economics of Crowdfunding.” Innovation Policy and the Economy 14: 63–97. doi:10.1086/674021.

- Agrawal, A., C. Catalini, and A. Goldfarb. 2015. “Crowdfunding: Geography, Social Networks, and the Timing of Investment Decisions.” Journal of Economics & Management Strategy 24: 253–274.

- Ahlers, G.K., D. Cumming, C. Günther, and D. Schweizer. 2015. “Signaling in Equity Crowdfunding.” Entrepreneurship Theory and Practice 39: 955–980.

- Alessandrini, P., A.F. Presbitero, and A. Zazzaro. 2008. “Banks, Distances and Firms’ Financing Constraints.” Review of Finance 13: 261–307.

- Anderson, W.P., L. Chatterjee, and T.R. Lakshmanan. 2003. “E-Commerce, Transportation, and Economic Geography.” Growth and Change 34: 415–432.

- Anglin, A.H., and R.J. Pidduck. 2022. “Choose Your Words Carefully: Harnessing the Language of Crowdfunding for Success.” Business Horizons 65: 43–58. doi:10.1016/j.bushor.2021.09.004.

- Armendáriz de Aghion, B., and J. Morduch. 2000. “Microfinance Beyond Group Lending.” Economics of Transition 8: 401–420.

- Baeck, P., L. Collins, and B. Zhang. 2014. Understanding Alternative Finance. The UK Alternative Finance Industry Report 2014. Nesta.

- Bathelt, H., A. Malmberg, and P. Maskell. 2004. “Clusters and Knowledge: Local Buzz, Global Pipelines and the Process of Knowledge Creation.” Progress in Human Geography 28: 31–56.

- Beckers, J., I. Cárdenas, and A. Verhetsel. 2018. “Identifying the Geography of Online Shopping Adoption in Belgium.” Journal of Retailing and Consumer Services 45: 33–41. doi:10.1016/j.jretconser.2018.08.006.

- Bellucci, A., A. Borisov, and A. Zazzaro. 2013. “Do Banks Price Discriminate Spatially? Evidence from Small Business Lending in Local Credit Markets.” Journal of Banking & Finance 37: 4183–4197. doi:10.1016/j.jbankfin.2013.06.009.

- Bengtsson, O., and S.A. Ravid. 2009. ”The Importance of Geographical Location and Distance on Venture Capital Contracts.” SSRN Electronic Journal. doi:10.2139/ssrn.1331574. Available at SSRN 1331574.

- Block, J., L. Hornuf, and A. Moritz. 2018. “Which Updates During an Equity Crowdfunding Campaign Increase Crowd Participation?” Small Business Economics 50: 3–27. doi:10.1007/s11187-017-9876-4.

- Bottazzi, L., M. Da Rin, and T. Hellmann. 2016. “The Importance of Trust for Investment: Evidence from Venture Capital.” The Review of Financial Studies 29: 2283–2318. doi:10.1093/rfs/hhw023.

- Brent, D.A., and K. Lorah. 2019. “The Economic Geography of Civic Crowdfunding.” Cities 90: 122–130. doi:10.1016/j.cities.2019.01.036.

- Breznitz, Shiri M., and D.S. Noonan. 2020. “Crowdfunding in a Not-So-Flat World.” Journal of Economic Geography 20: 1069–1092. doi:10.1093/jeg/lbaa008.

- Brüntje, D., and O. Gajda. 2016. “Crowdfunding in Europe. State of the Art in Theory and Practice.”

- Burtch, G., A. Ghose, and S. Wattal. 2014. “Cultural Differences and Geography as Determinants of Online Prosocial Lending.” Mis Quarterly 38: 773–794.

- Butticè, V., M.G. Colombo, and M. Wright. 2017. “Serial Crowdfunding, Social Capital, and Project Success.” Entrepreneurship Theory and Practice 41: 183–207. doi:10.1111/etap.12271.

- Chen, H., P. Gompers, A. Kovner, and J. Lerner. 2010. “Buy Local? The Geography of Venture Capital.” Journal of Urban Economics 67: 90–102.

- Chen, M.X., and C. Lin. 2020. “Geographic Connectivity and Cross-Border Investment: The Belts, Roads and Skies.” Journal of Development Economics 146: 102469. doi:10.1016/j.jdeveco.2020.102469.

- Clark, G.L. 2005. “Money Flows Like Mercury: The Geography of Global Finance.” Geografiska Annaler: Series B, Human Geography 87: 99–112.

- Clark, J., J. Harrison, and E. Miguelez. 2018. “Connecting Cities, Revitalizing Regions: The Centrality of Cities to Regional Development.” Regional Studies 52: 1025–1028. doi:10.1080/00343404.2018.1453691.

- Colombo, M.G., C. Franzoni, and C. Rossi-Lamastra. 2015. “Internal Social Capital and the Attraction of Early Contributions in Crowdfunding.” Entrepreneurship Theory and Practice 39: 75–100. doi:10.1111/etap.12118.

- Cumming, D., M. Meoli, and S. Vismara. 2021. “Does Equity Crowdfunding Democratize Entrepreneurial Finance?” Small Business Economics 56: 533-552.

- D’Ambrosio, M., and G. Gianfrate. 2016. “Crowdfunding and Venture Capital: Substitutes or Complements?” The Journal of Private Equity 20: 7–20.

- Degryse, H., and S. Ongena. 2005. “Distance, Lending Relationships, and Competition.” The Journal of Finance 60: 231–266.

- Dejean, S. 2019. The Role of Distance and Social Networks in the Geography of Crowdfunding: Evidence from France. Regional Studies.

- DeYoung, R., W.S. Frame, D. Glennon, and P. Nigro. 2011. “The Information Revolution and Small Business Lending: The Missing Evidence.” Journal of Financial Services Research 39: 19–33.

- Di Pietro, F. 2021. “Leveraging Regional Immigration and Immigration Diversity for Financing Crowdfunding Projects.” Regional Studies, Regional Science 8: 291–301.

- Di Pietro, F., and F. Masciarelli. 2021. “The Effect of Local Religiosity on Financing Cross-Regional Entrepreneurial Projects via Crowdfunding (Local Religiosity and Crowdfinancing).” Journal of Business Ethics 178: 1–15. doi:10.1007/s10551-021-04805-4.

- Dubois, A., and M. Gromek. 2018. “How Distance Comes into Play in Equity Crowdfunding.” In The Rise and Development of FinTech (Open Access), edited By Teigland et al., 376–389. Routledge.

- Erturk, I., J. Froud, S. Johal, A. Leaver, and K. Williams. 2007. “The Democratization of Finance? Promises, Outcomes and Conditions.” Review of International Political Economy 14: 553–575. doi:10.1080/09692290701475312.

- Estrin, S., D. Gozman, and S. Khavul. 2018. “The Evolution and Adoption of Equity Crowdfunding: Entrepreneur and Investor Entry into a New Market.” Small Business Economics 51: 425–439.

- Farag, S., J. Weltevreden, T. Van Rietbergen, M. Dijst, and F. van Oort. 2006. “E-Shopping in the Netherlands: Does Geography Matter?” Environment and Planning: B, Planning & Design 33: 59–74.

- Florida, R. 2002. “The Economic Geography of Talent.” Annals of the Association of American Geographers 92: 743–755.

- Florida, R. 2005. Cities and the Creative Class. New York: Routledge.

- Fritsch, M., and D. Schilder. 2008. “Does Venture Capital Investment Really Require Spatial Proximity? An Empirical Investigation.” Environment & Planning A 40: 2114–2131.

- Gallemore, C., K.R. Nielsen, and K. Jespersen. 2019. ”The Uneven Geography of Crowdfunding Success: Spatial Capital on Indiegogo.” Environment and Planning A: Economy and Space 51: 1389–1406. doi:10.1177/0308518X19843925, 0308518X19843925.

- Gierczak, M.M., U. Bretschneider, P. Haas, I. Blohm, and J.M. Leimeister. 2016. “Crowdfunding: Outlining the New Era of Fundraising.” In Crowdfunding in Europe, 7–23. Springer.

- Giudici, G., M. Guerini, and C. Rossi Lamastra. 2013. ”Why Crowdfunding Projects Can Succeed: The Role of Proponents’ Individual and Territorial Social Capital.” Available at SSRN 2255944.

- Gompers, P.A., and J. Lerner. 1999. What Drives Venture Capital Fundraising?. National bureau of economic research.

- Guenther, C., S. Johan, and D. Schweizer. 2018. “Is the Crowd Sensitive to Distance?—how Investment Decisions Differ by Investor Type.” Small Business Economics 50: 289–305.

- Hall, S. 2013. “Geographies of Money and Finance III: Financial Circuits and the ‘Real Economy.” Progress in Human Geography 37: 285–292.

- Harrison, R. 2013. “Crowdfunding and the Revitalisation of the Early Stage Risk Capital Market: Catalyst or Chimera?” Venture Capital 15: 283–287. doi:10.1080/13691066.2013.852331.

- Johan, S., and Y. Zhang. 2020. “Quality Revealing versus Overstating in Equity Crowdfunding.” Journal of Corporate Finance 65: 101741. doi:10.1016/j.jcorpfin.2020.101741.

- Josefy, M., T.J. Dean, L.S. Albert, and M.A. Fitza. 2017. “The Role of Community in Crowdfunding Success: Evidence on Cultural Attributes in Funding Campaigns to “Save the Local Theater.” Entrepreneurship Theory and Practice 41: 161–182.

- Jumpstart Our Business Startups Act, 2012. H. R.

- Kirby-Hawkins, E., M. Birkin, and G. Clarke. 2019. “An Investigation into the Geography of Corporate E-Commerce Sales in the UK Grocery Market.” Environment and Planning B: Urban Analytics and City Science 46: 1148–1164.

- Kleinert, S., and K. Mochkabadi. 2021. “Gender Stereotypes in Equity Crowdfunding: The Effect of Gender Bias on the Interpretation of Quality Signals.” The Journal of Technology Transfer 1–22. doi:10.1007/s10961-021-09892-z.

- Kourtit, K., and P. Nijkamp. 2012. “Smart Cities in the Innovation Age.” Innovation: The European Journal of Social Science Research 25: 93–95.

- Kromidha, E., and P. Robson. 2016. “Social Identity and Signalling Success Factors in Online Crowdfunding.” Entrepreneurship & Regional Development 28: 605–629.

- Kuppuswamy, V., and B. L. Bayus. 2018. “Crowdfunding Creative Ideas: The Dynamics of Project Backers.” In The Economics of Crowdfunding, 151–182. Cham: Palgrave Macmillan.

- Langley, P. 2016. “Crowdfunding in the United Kingdom: A Cultural Economy.” Economic Geography 92: 301–321.

- Langley, P., S. Lewis, C. McFarlane, J. Painter, and A. Vradis. 2020. “Crowdfunding Cities: Social Entrepreneurship, Speculation and Solidarity in Berlin.” Geoforum 115: 11–20. doi:10.1016/j.geoforum.2020.06.014.

- Langley, P., and A. Leyshon. 2017. “Capitalizing on the Crowd: The Monetary and Financial Ecologies of Crowdfunding.” Environment & Planning A 49: 1019–1039.

- Laursen, K., F. Masciarelli, and A. Prencipe. 2012. “Regions Matter: How Localized Social Capital Affects Innovation and External Knowledge Acquisition.” Organization Science 23: 177–193.

- Lederman, D., N. Loayza, and A.M. Menéndez. 2002. “Violent Crime: Does Social Capital Matter?” Economic Development and Cultural Change 50: 509–539. doi:10.1086/342422.

- Lee, R. 2011. “Spaces of Hegemony? Circuits of Value, Finance Capital and Places of Financial Knowledge.” In The SAGE Handbook of Social Geographies, edited by Agnew and Livingstone, 185–202. London: SAGE.

- Lee, N., and R. Brown. 2017. “Innovation, SMEs and the Liability of Distance: The Demand and Supply of Bank Funding in UK Peripheral Regions.” Journal of Economic Geography 17: 233–260. doi:10.1093/jeg/lbw011.

- Lee, N., and D. Luca. 2019. “The Big-City Bias in Access to Finance: Evidence from Firm Perceptions in Almost 100 Countries.” Journal of Economic Geography 19: 199–224. doi:10.1093/jeg/lbx047.

- Lewis, A.C., A.M. Cordero, and R. Xiong. 2021. “Too Red for Crowdfunding: The Legitimation and Adoption of Crowdfunding Across Political Cultures.” Entrepreneurship Theory and Practice 45: 471–504.

- Leyshon, A. 2000. Money and Finance. A Companion to Economic Geography, edited by Sheppard and Barnes, 432, Blackwell Publishing Ltd.

- Lin, M., N.R. Prabhala, and S. Viswanathan. 2013. “Judging Borrowers by the Company They Keep: Friendship Networks and Information Asymmetry in Online Peer-To-Peer Lending.” Management Science 59: 17–35.

- Lin, M., and S. Viswanathan. 2015. “Home Bias in Online Investments: An Empirical Study of an Online Crowdfunding Market.” Management Science 62: 1393–1414.

- Lukkarinen, A., J.E. Teich, H. Wallenius, and J. Wallenius. 2016. “Success Drivers of Online Equity Crowdfunding Campaigns.” Decision Support Systems 87: 26–38. doi:10.1016/j.dss.2016.04.006.

- Martin, R. 1999. The new economic geography of money (Chap. 1). In R. Martin (Ed.), Money and the space economy. New York: Wiley.

- Mason, C. 2010. “Entrepreneurial Finance in aRegional Economy“. Venture Capital 12: 167–172. doi:10.1080/13691066.2010.507033.

- Mason, C.M., and R.T. Harrison. 1995. “Closing the Regional Equity Capital Gap: The Role of Informal Venture Capital.” Small Business Economics 7: 153–172.

- Massa, M., and A. Simonov. 2006. “Hedging, Familiarity and Portfolio Choice.” The Review of Financial Studies 19: 633–685.

- Mochkabadi, K., and C.K. Volkmann. 2020. “Equity Crowdfunding: A Systematic Review of the Literature.” Small Business Economics 54: 75–118.

- Mollick, E. 2014. “The Dynamics of Crowdfunding: An Exploratory Study.” Journal of Business Venturing 29: 1–16. doi:10.1016/j.jbusvent.2013.06.005.

- Mollick, E., and A. Robb. 2016. “Democratizing Innovation and Capital Access: The Role of Crowdfunding.” California Management Review 58: 72–87.

- Mondria, J., and T. Wu. 2010. “The Puzzling Evolution of the Home Bias, Information Processing and Financial Openness.” Journal of Economic Dynamics & Control 34: 875–896.

- Nofsinger, J. 2005. The Psychology of Investing.(2. Painos). New Jersey: Pearson Education, Inc.

- Noonan, D.S., S.M. Breznitz, and S. Maqbool. 2021. “Looking for a Change in Scene: Analyzing the Mobility of Crowdfunding Entrepreneurs.” Small Business Economics 57: 685–703. doi:10.1007/s11187-020-00418-9.

- Petersen, M.A., and R.G. Rajan. 2002. “Does Distance Still Matter? The Information Revolution in Small Business Lending.” The Journal of Finance 57: 2533–2570.

- Pike, A., and J. Pollard. 2010. “Economic Geographies of Financialization.” Economic Geography 86: 29–51.

- Pollard, J.S. 2003. “Small Firm Finance and Economic Geography.” Journal of Economic Geography 3: 429–452.

- Powell, W.W., K.W. Koput, J.I. Bowie, and L. Smith-Doerr. 2002. “The Spatial Clustering of Science and Capital: Accounting for Biotech Firm-Venture Capital Relationships.” Regional Studies 36: 291–305. doi:10.1080/00343400220122089.

- Rogers, E.M. 2003. Diffusion of Innovations. 5th ed. London: Simon and Schuster, Inc.

- Schwienbacher, A. 2019. “Equity Crowdfunding: Anything to Celebrate?” Venture Capital 21: 65–74. doi:10.1080/13691066.2018.1559010.

- Shearmur, R. 2012. “Are Cities the Font of Innovation? A Critical Review of the Literature on Cities and Innovation.” Cities 29: S9–18. doi:10.1016/j.cities.2012.06.008.

- Song, Z. 2021. “The Geography of Online Shopping in China and Its Key Drivers.” Environment and Planning B: Urban Analytics and City Science 49 (1): 259–274.

- Sorenson, O., and T.E. Stuart. 2001. “Syndication Networks and the Spatial Distribution of Venture Capital Investments.” The American Journal of Sociology 106: 1546–1588.

- Stevens, R., N. Moray, and J. Bruneel. 2015. “The Social and Economic Mission of Social Enterprises: Dimensions, Measurement, Validation, and Relation.” Entrepreneurship Theory and Practice 39: 1051–1082.

- Tang, L., R. Baker, and L. An. 2020. “The Success of Crowdfunding Projects: Technology, Globalization, and Geographic Distance.” Economics of Innovation and New Technology 31: 1–22. doi:10.1080/10438599.2020.1838412.

- Vismara, S. 2016. “Equity Retention and Social Network Theory in Equity Crowdfunding.” Small Business Economics 46: 579–590.

- Vismara, S. 2018. “Information Cascades Among Investors in Equity Crowdfunding.” Entrepreneurship Theory and Practice 42: 467–497.

- Wallmeroth, J. 2019. “Investor Behavior in Equity Crowdfunding.” Venture Capital 21: 273–300. doi:10.1080/13691066.2018.1457475.

- Weber, S., and M. Péclat. 2018. “A Simple Command to Calculate Travel Distance and Travel Time.” The Stata Journal 17: 962–971.

- Younkin, P., and V. Kuppuswamy. 2018. “The Colorblind Crowd? Founder Race and Performance in Crowdfunding.” Management Science 64: 3269–3287.