?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Following economic instability after the Global Financial Crisis, the financing of small and medium-sized enterprise (SME) growth and productivity has become central to UK government policy for sustainable economic development, evidenced by the establishment of the British Business Bank and Regional Investment Funds. This paper considers demand-side and supply-side failures in the contemporary UK SME finance market. Adopting mixed methods, binary logit regression analysis of the 2015 UK Small Business Survey of 15,502 SMEs is sense-checked using qualitative participatory findings from 6 SME finance support advisors. Findings confirm the importance of SME size, age, management capability and use of appropriate, timely external advice. They support the resource-based view of SME access to finance, contributing to borrower discouragement and under investment, suggesting the need for improved support to upskill entrepreneurs’ financial management and investment readiness and the concept of an ‘holistic entrepreneurial finance ecosystem’ approach to assist UK SME finance.

Introduction

A plethora of studies in recent decades report that small and medium-sized enterprises (SMEs) experience financial constraints more frequently than large firms. The premise for supporting the sector is that SMEs are the drivers for economic growth (Birch Citation1979; Lerner Citation2010; BIS Citation2013) and that financial constraints impede their competitive advantage (Beck and Demirguc-Kunt Citation2006). However, few studies have examined whether there are demand or supply-side failures, how they occur and their wider implications for theory, policy and practice. The recent proportional decline in annual UK SME demand for external finance, prior to the COVID-19 Pandemic, where employer SMEsFootnote1 demand reduced from 26% in 2010 to just 12% in 2019 (BEIS Citation2020), also illustrates the need for contemporary explanatory research. This is pertinent, given the UK government’s desire to stimulate SME growth (HM Treasury Citation2021). Furthermore, it will be helpful to take account the lessons learned from the aftermath of the late 2000s Global Financial Crisis (GFC), as they may provide useful insights into the contemporary SME financing requirements for addressing the uncertainties of the current global economic crises, relating to the Ukraine conflict, UK exit (“Brexit”) from the European Union, and post-Pandemic economic recovery.

Numerous studies have reported that SMEs are large contributors to employment generation (Birch Citation1979; NESTA Citation2009b; Ayyagari, Demirgüç-Kunt, and Maksimovic Citation2011), underpinned by the later 20th Century trend to deindustrialisation and proliferation of self-employment. SMEs facilitate flexible working practices (Owen et al. Citation2017) with the so-called “Vital 6%” of SMEs generating over half of all new employment in the last decade in the UK (NESTA Citation2009b; Anyadike-Danes and Hart Citation2017). Hence, it is not surprising that empirical studies (Armstrong et al. Citation2013; Bank of England Citation2015; Commission of the European Communities Citation2008) have reported SMEs’ importance within the UK and European Union. More recently, amidst current economic uncertainties, the role of potential high growth firm scale-up has risen high on the UK policy agenda as a means of raising productivity and international competitiveness (HM Treasury Citation2021; Anyadike-Danes and Hart Citation2017; Owen et al. Citation2020).

Parallel to this recognition, a body of theoretical literature has evolved that examined the finance gap for SMEs (Cowling Citation2010; Deakins and Freel Citation2012; Jones-Evans Citation2015). The literature discusses the importance of access to formal (supply-side) business finance, defined as funding excluding retained earnings and from informal funders, such as founders, family and friends (the “3Fs”), essential for business to scale-up and grow (North, Baldock, and Ullah Citation2013). The literature (NESTA Citation2009a; Baldock and Mason Citation2015) makes a case for contemporary SME finance escalator analysis which demonstrates recent dynamic changes in the types of finance available to UK SMEs, marking the rise of new alternative sources, such as crowdfunding and asset-based finance (Davis Citation2012; Zhang et al. Citation2016, Citation2017), whilst acknowledging that bank finance remains the main source of finance for SMEs (Owen et al. Citation2017; BEIS Citation2020).

In the aftermath of the economic turmoil of the GFC and more UK Brexit and global Pandemic, financing SME growth remains central to UK government policy for economic development and sustainability, as enshrined in the UK Government’s Build Back Better plan for growth (HM Treasury Citation2021) and the SME finance oversight support role of the British Business Bank (Van der Schans Citation2015). Since the early 2000s there has been a UK policy trend towards “picking winners” and supporting the specialist financing requirements of young potential high growth firms (Smallbone, Baldock, and Burgess Citation2002) and more established SME scale-ups (Anyadike-Danes and Hart Citation2017). However, now there is also growing awareness in the UK that access to SME finance assists economic adjustment and has the potential to play an important role in diversifying the economy (HM Government Citation2022; Levelling Up White Paper; HM Treasury & BIS Citation2011), developing greater regional growth and equality through regionally targeted SME funding (i.e., Northern Powerhouse and Midlands Engine funds) and that SMEs of all ages and stages require adequate finance to stabilise and promote more sustainable growth – whether slow or fast (BBB Citation2016). This paper provides an important contribution by considering the role of both the supply and demand-sides of UK SME access to finance.

Supply-side failure

From a theoretical perspective, the supply-side failure for businesses seeking external finance dates from the findings of the UK Macmillan Commission (Macmillan Citation1931). Subsequently, many studies continue to address the same point (Baldock and Harrison Citation2015; Hussain and Scott Citation2015). The premise is that demand is greater than the finance supplied by less formal sources such as individual business angels and more formal sources, such as banks and venture capital (VC), resulting in an estimated finance gap ranging between £250,000 and £5 m (Baldock and Mason Citation2015; Deakins and Freel Citation2012) – or what the Breedon Review (Citation2012) estimated at upwards of £84 billion in aggregate. The gap is explained, largely, due to information asymmetries between borrowers and lenders, which make effective due diligence prohibitively expensive for relatively small loans and contributes to the associated problems of moral hazard, adverse selection and agency failure (Carpenter and Peterson Citation2002; Hsu Citation2004), which may lead to supply-side failure to fund viable SMEs (North, Baldock, and Ekanem Citation2010).

Demand-side failure

However, there is now emerging evidence of SME demand failures, resulting from signalling failures (Mueller, Westhead, and Wright Citation2012) relating to SME resource limitations (Mac an Bhaird Citation2010), and financing network failures (Lerner Citation2010), which may also result in borrower discouragement (Fraser Citation2014). The chain of cause and consequence, suggests the need to consider a more holistic “financing ecosystem” approach to develop “bespoke” theory, policy and practice (Hughes Citation2009; Hwang and Horowitt Citation2012; Mazzucato and Penna Citation2014) to meet the evolving challenges faced by SMEs when seeking finance.

The evolving, complex and dynamic UK economic environment offers a unique context to examine SME finance. To this end, this paper draws on the 2015 UK Longitudinal Small Business Survey (LSBS) of 15,502 SMEs, examining the initial baseline year of data. The size of this survey enables a more robust examination of access to finance data than hitherto possible in the UK. To gain a deeper insight into the quantitative findings and to corroborate the results, we also adopt a mixed methods approach (Creswell Citation2003) by sense checking our findings with six business and finance support advisors operating in the Oxford Innovation agency network which assists UK SME growth.

The paper proceeds by examining demand and supply-side SME finance literature, followed by establishing the research questions and methodology, before presenting key findings, discussion of the theoretical and policy implications and conclusions.

Literature review – theoretical underpinning

The supply-side

The importance of SMEs has long been acknowledged in the UK, gaining traction after World War 2, and has been subject to considerable theoretical scrutiny (Berger and Udell Citation1992; Cowling Citation2010; Jones-Evans Citation2015). Since the first reporting of the business finance gap (Macmillan Citation1931), supply-side theories have dominated (e.g., Bolton Citation1971; Wilson Committee Citation1979); these mainly relate to perceived information asymmetries (IAs) between SME owner managers and finance providers. IAs are considered to be most acute at the start-up stage, when new and innovative businesses tend to lack financial information and trading track records, giving rise to agency cost (Jensen and Meckling Citation1976), moral hazard and adverse selection (Myers and Majluf Citation1984) that is mitigated through collateral or asset cover (Coco Citation2000) to demonstrate their viability and reduce perceived risk to lenders/investors (Deakins and Hussain Citation1994; Carpenter and Peterson Citation2002; Hsu Citation2004). Often the relatively small amounts of finance required by SMEs do not justify formal investors’ due diligence costs (North, Baldock, and Ullah Citation2013).

Financing (debt or equity) without rigorous checks gives rise to poor investment decisions through adverse selection (financing non-viable propositions, type I error and not financing viable proposition type II error; Deakins and Hussain Citation1994) and moral hazards in terms of poor management decisions (Hughes Citation2009), leading to loss of economic competitiveness. A further aspect of supply-side failure is the economic cycle, which affects the availability of external finance (Cowling, Liu, and Ledger Citation2012; Cowling Citation2010), evidenced during the GFC induced recession that led to the decline in the availability of both debt and equity business finance in the UK (Armstrong et al. Citation2013; North, Baldock, and Ullah Citation2013).

The finance escalator

Straddling the supply and demand-sides of entrepreneurial finance theory Berger and Udell’s (Berger and Udell Citation1998) model of decreasing opacity suggests that as businesses mature they become less opaque to investors, signalling greater viability and increasing their range of external financing options. This theory underpins the finance escalator (NESTA Citation2009a; North, Baldock, and Ullah Citation2013) which maps out the types of entrepreneurial finance available at a given time and location for businesses at different stages of their development. The interconnectedness between the age, information and viability of the firm provides a framework to evaluate SME access to sources of finance. This evolving model helps to demonstrate the role of the finance escalator for SMEs, where the financing gaps exist, and further extends explanation in terms of the specifics of the demand-side approach.

Recent analysis of the UK finance escalator (Mason Citation2017) has revealed dynamic changes in the demand and supply of SME finance post GFC. Most notable has been the rise in alternative financing such as crowd funding, accelerators, seed VCs and business angel groups for earlier stage SMEs, to fill the gap left by traditional bank (Baldock and Mason Citation2015) and asset-based finance (Davis Citation2012) which has shifted towards more mature SMEs. Whilst Zhang et al. (Citation2016) valued the UK online alternative finance markets at £3.2bn in 2015, this represented less than 3.5% of UK business bank lending in that period, suggesting that for the vast majority of UK SMEs bank finance remains the main source of external finance (BEIS Citation2017, Citation2020). Critically, the finance escalator also highlights that an increasingly complex UK SME finance market may present SME demand-side barriers, suggesting the need for a more holistic ecosystem approach which considers SME resources, knowledge and decision-making (Owen, Deakins, and Savic Citation2019).

The demand-side

Demand-side theories attempt to explain the entrepreneurial selection and approaches to external financing and provide important insight into potential demand-side failures (Levenson and Willard Citation2000). Pecking order theory (Myers and Majluf Citation1984; Hamilton and Fox Citation1998) suggests the owner-manager exhibits preference in order of self-finance, family, friends, formal debt, and equity, as most firms will seek to keep borrowing down and cede ownership as a last resort.

Pecking order has been challenged by supply-side availability such as where equity might become more readily available as a form of risk finance than debt, such as for young innovative firms (North, Baldock, and Ullah Citation2013). It is also challenged by the resource-based view (“RBV”; Barney Citation1991; Mac an Bhaird Citation2010). RBV suggests that as management experience and networking develop (Uzzi Citation1999), this can improve both the access and terms and conditions for external finance. Thus, young small firms with inexperience management teams, limited financial management skills and limited experience of accessing and assessing different types of external business finance will be less likely to successfully identify and source appropriate types and optimal sources of finance (Owen, Deakins, and Savic Citation2019).

Signalling theory (Leland and Pyle Citation1977; Mueller, Westhead, and Wright Citation2012; Ahlers et al. Citation2015) also suggests that where businesses are unable to adequately demonstrate their viability to potential investors they will be less successful in accessing external finance. Conversely, North, Baldock, and Ullah (Citation2013) recognise that where serial entrepreneurs or spin-out managers already have close ties with finance providers, so-called “soft-start” businesses are able to identify and successfully signal (i.e., through application) to obtain external finance. However, a potential downside of existing financing relationships is path dependency (Teece Citation2007). This relates to where reliance on a particular source of finance leads to overlooking other more suitable sources of external finance; an example is the dark side of relationship banking where sub-optimal borrowing may occur through soft budget constraints and high-cost loans (Bolton and Scharfstein Citation1996).

Similarly, another form of demand failure is discouraged borrower syndrome (Kon and Storey Citation2003; Fraser Citation2014) whereby viable firms do not apply for external finance because of the fear of being rejected (Armstrong et al. Citation2013; Fraser, Bhaumik, and Wright Citation2015). Kon and Storey (Citation2003) also note that firms may express financing needs, but do not apply because they do not perceive that suitable finance is available, or are cautious about investing during economic downturns. They caution that self-reported discouragement will not always indicate valid requirement and could represent wishful thinking. Nevertheless, discouragement provides a potentially useful indication of unmet latent demand over time. Discouraged borrower effect was found to be particularly prevalent in the UK in the aftermath of the GFC. This was exacerbated by a combination of SMEs’ caution to invest in uncertain markets, and poor perceptions of bank lenders in relation to rising borrowing costs and disadvantageous terms, increased expectation of rejection and a distrust of banks. Collectively, this created SME risk aversion in a recessionary market (BIS Citation2013; Cowling, Liu, and Ledger Citation2012; Bank of England Citation2015). Furthermore, Cowling et al. (Citation2016) suggest there is evidence of mismatch between SMEs perceptions and the supply of finance; as the recession passed and the cost burden of borrowing fell in the UK, SMEs have continued to exhibit discouragement, suggesting a lag in adjustment (GLA Citation2013; BEIS Citation2020).

For the UK, this evidence leads to two observations. First, many start-ups and small firms lack the management resources to successfully access external finance; they require investment readiness training in order to adequately prepare their business plan (Mason and Kwok Citation2010), and raise confidence and self-esteem to seek external finance (Owen et al. Citation2017; Owen, Deakins, and Savic Citation2019). Second, an appropriate network of financial intermediaries is required to assist SMEs in finding suitable types of finance (Cavalluzzo and Wolken Citation2005; Lerner Citation2010). Overall, the importance of a holistic approach to SME finance which considers both supply and demand-side requirements, suggests the need for a “pipeline” (Mason and Brown Citation2013) or “ecosystem approach” (Hwang and Horowitt Citation2012) that develops entrepreneurial finance skills and facilitates access to external finance; this in turn suggests a broad role for policy oversight, such as through a state investment bank (Breedon Review Citation2012; Mazzucato and Penna Citation2014). Such an approach warrants careful consideration during times of economic uncertainty, such as currently in the aftermath of UK Brexit and the Pandemic, especially to support innovation (Owen, Deakins, and Savic Citation2019) and technology-based firms in the interim period (North, Baldock, and Ullah Citation2013) - the potential high growth firms that can scale-up and address the UK’s productivity and international competitiveness needs (CMA Citation2015; Anyadike-Danes and Hart Citation2017; Owen et al. Citation2020).

In summary, SME research has suggested many theoretical and practical reasons for the barriers to their application and access to external finance, giving rise to numerous empirical studies. However, few studies provide a balanced appraisal. Drawing from past literature, the following research questions are formulated to consider the extent to which there are demand-side or supply-side failures in the UK SME finance market, their causes, and theoretical and policy implications. To achieve this, we explore three key research questions (RQs):

RQ1 – What is the extent, and what are the likely causes, of the finance gaps for UK SMEs?

RQ2 - What are the significant factors contributing to external financing outcomes?

RQ3 – What is the scope and capability of public SME finance support policy to mitigate the finance gaps?

Methodology

Given the complexity and interconnected nature of SME finance, a mixed methods approach is adopted (Creswell Citation2003). Quantitative data is drawn from the 2015 baseline UK Longitudinal Small Business Survey (LSBS), an annual CATI (computer-assisted telephone interview) survey of UK SME owner-managers. This provided a representative sample of 15,502 UK SMEs (surveyed in the second half of 2015), the largest UK SME finance survey at that time. Drawing on data for registered businesses from the UK government Inter-Departmental Business Register (IDBR, which includes all UK businesses which are registered for VAT and with pay as you earn employee records) for 2.3 m businesses, LSBS is stratified random sampled to include sufficient (20%) medium-sized businesses (50–249 employees), as well as to account for broad sector and UK “regional” (9 English regions and 3 devolved nations of Scotland, Wales and Northern Ireland) distribution. The survey is also supplemented to ensure sufficient (23%) unregistered zero employee businesses, drawn from Dun and Bradstreet’s high street data, which is also similarly stratified random sampled to account for broad sector and UK regional location to match the British business population structure estimates (representing 5.4 m at the time; BIS Citation2016)Footnote2. The data are examined for the degree of success in receiving, or discouragement from accessing, external finance in 2015.

We employ Baldock et al’.s (Baldock et al. Citation2006) two-stage approach. First, we use bivariate chi-square analysis to examine the key characteristics of SME finance seekers, successful applicants and discouraged borrowers. Second, we examine the key SME (e.g., size, age, location, sector) and management characteristics (e.g., number of managers, capabilities, external advisors) through a series of binary logit regression models (Tabachnick and Fidell Citation2013) to assess the main factors contributing to dependent variable outcomes relating to external financing overall, for different types of finance and for discouraged borrowers.

Typically, prior empirical studies on SME finance undertake linear regressions using least square-based models. However, the statistical property of the dependent variable in our study can make the outcome econometrically complicated (i.e., as it takes only 0 and 1 value, the level of debt financing of these SMEs cannot be assumed constant throughout its entire range). So, the linearity assumption, (y) is the dependent variable and

is the matrix of independent variables, is unlikely to hold. In addition, in this case the predicted value of

does not lie between 0 and 1. Thus, alternatively to model SME finance, we can use the logistic transformation:

The EquationEquation 1(1)

(1) ensures that 0< E(y|x) < 1. However, as this equation requires a nonlinear estimation technique, most studies prefer to use least square to estimate log-odds ratio as shown below which is linearization of the results by solving the EquationEquation 1

(1)

(1)

Depending on the model, is the probability of achieving funding or the probability of being discouraged from applying for external finance in the last 12 months for company i, x are the independent variables such as number of managers, capabilities, external advisors, employment size, age since established, location and sector.

Additionally, to gain deeper insights into our data findings, a participatory stakeholder approach was employed (Dart and Davies Citation2003). These qualitative in-depth extended telephone interviews, typically of over one hour’s duration, adopted a semi-structured topic guide approach. This ensured a consistent framework of enquiry about the key LSBS findings and enabled opportunity to probe on issues arising. These interviews were purposively selected with six highly experienced Oxford Innovation (OI) SME finance support advisors, drawn from across their South, West, Midlands and Northern English regional services. These advisors all undertake business and finance support to assist growth potential SMEs at start-up and scale-up stages and distressed SMEs. The qualitative interviews were used to sense-check (Creswell Citation2003) the quantitative findings and provide practitioners’ experiential explanations for finance gaps and practical policy solutions. Qualitative data interviews were transcribed, checked with the respondents for accuracy and assessed by two independent researchers to avoid individual interpretive bias (Creswell Citation2003).

Our approach has limitations, notably in relying on one large cross-sectional wave of 2015 UK SME data, which pre-dates the Pandemic. We also use selective supporting evidence from a small number of specialist SME finance advisors representing the English regions. Nevertheless, we believe that the data set is the most robust available in recent times for the UK and the advisors are from one of the UK’s leading business support agencies.

Findings

Here, we analyse the LSBS 2015 SME financing data (including for self-employed) to address our first two research questions (RQs) in order. RQ 1 explores SME finance gaps and their likely causes, with consideration for the ongoing UK SME finance market adjustments post GFC (Lee, Sameen, and Cowling Citation2015). We initially use bivariate analysis to systematically assess SME demand for external finance in relation to supply-side variations in the success rates of applications for different types of finance and whether there are variations in the success rates of different types of SMEs that indicate demand-side factors. This approach is extended to assess application discouragement. Where findings appear significant, we apply these to multivariate modelling to address RQ2 to determine which demand or supply factors are most significant to accessing finance and then to examine what factors most impact upon discouragement. We then address RQ3 by using our participatory stakeholder interviews, with six specialist Oxford Innovation (OI) SME finance advisors, to sense check our key quantitative findings and to assess the scope and capability of public SME finance support policy to mitigate the revealed finance gaps.

RQ1 Extent of SME finance gaps and likely causes – Profiling the demand and receipt of external finance

SME demand for external finance

SMEs’ choice of credit remains supply dependent, consistent with pecking order theory. After personal and family finance, commercial banks remain the dominant player when accessing external finance (Deakins and Hussain Citation1994; De Bettignies and Brander Citation2007; Cowling, Liu, and Ledger Citation2012; Lee, Sameen, and Cowling Citation2015), especially short-term borrowing. depicts the types and percentage of required finance accessed during the preceding year (to late 2015). Almost one-fifth (2,865; 19%) of SMEs surveyed had sought external finance. The main types of finance sought were bank loans and overdrafts (both 43%), leasing (35%), credit cards (22%), commercial mortgages (11%), factoring (9%), grants (7%), equity finance (6%), and peer-to-peer debt finance (4%, P2P). Overall, the vast majority of applicants (83%) received at least some fundingFootnote3, with 11% of applications still in process at the time of survey and just 6% receiving no finance. Applicants seeking credit card and leasing type loans were most successful; whilst applications for bank loans, commercial mortgages, and equity finance were less successful. The frequency of loan application was unsurprising; in the preceding year, 62% only applied once for finance (typically to a bank), 18% applied twice, 20% applied three or more times. The main reasons reported for seeking external finance were for working capital to assist cash-flow (51%), equipment and vehicles (42%), buying land and premises (15%), property refurbishment (9%), growth (7%) and R&D (3%). The median amount of external finance raised by surveyed SMEs during the last year was £100,000, with just over a quarter raising up to £25,000 and one-eighth (13%) raising over £1 m.

Table 1. Types of finance accessed and success rates in the last 12 months.

These findings corroborate earlier studies, with SMEs typically seeking short-term external finance as commercial banks are reluctant to lend for long-term due to the “lack of information” gap (Cowling, Liu, and Ledger Citation2012; Fraser Citation2014), collateral deficit (Deakins and Hussain Citation1994) and higher incidence of financial delinquency amongst SMEs (Fraser, Bhaumik, and Wright Citation2015). This leads to credit rationing amongst SMEs and prevents them from planning long-term investment, creating SME patient capital gaps (Owen, Deakins, and Savic Citation2019), long-term welfare loss for the economy and poor competitiveness internationally.

SME demand-side success characteristics

presents summary statistics for the success rates of surveyed SMEs in accessing finance according to their business and management characteristics. This reveals that application success rates have related themes which form the basis for further exploration in this paper.

Table 2. Access to finance – success rates and discouragement by business and management characteristics.

Size and age

Smaller and younger established firms are significantly (<.001 level for self-employed) less likely to achieve application success than larger and older firms. This supports prior findings that start-up and younger established firms are disproportionately affected when seeking external finance (North, Baldock, and Ullah Citation2013).

Internal resources

Firms with no partners/directors are significantly (<.01) less likely to achieve application success whilst, conversely, those with perceived “good capabilities to access finance” are significantly (<.001) more likely to achieve application success. In combination, these findings strongly support the RBV (Barney Citation1991) of the firm, indicating that larger, older, more management resource-intensive firms, endowed with collateral assets have better perceived capabilities to access external finance and are ultimately more successful in doing so.

External resources

Counterintuitively, whilst external assistance might be expected to increase the likelihood of accessing finance, SMEs that used external assistance to access finance were significantly (<.05) less likely to receive any finance. This may indicate demand-side failure in a number of ways, such as poor business performance characteristics, or a failure to find and access appropriate external assistance within a suitable time period. This may indicate a poor management resource base in relation to seeking external finance and finding suitable funding networks; a problem highlighted for small, young, firms in the study of UK innovative firms’ journeys to finance (BEIS Citation2017).

Discouragement

Another aspect of demand failure is “borrower discouragement” (Kon and Storey Citation2003; Fraser Citation2014) where potential borrowers do not seek required external finance due to fear of rejection, or perceptions of expensive or unsuitable finance availability, based on previous personal experience or lack of knowledge and information. Cowling et al. (Citation2016) estimated 2.5% of UK businesses were discouraged borrowers during the GFC in 2008, whilst Fraser (Citation2014) suggested this figure quadrupled for 2009.

The LSBS 2015 revealed 9% of SMEs with borrower discouragement. This includes 3% of SMEs (417) that had applied for some funding (316 obtaining at least some, 47 obtaining nothing and with 54 experiencing delays with unresolved applications) during the last year. The main reasons for discouragement are avoidance of additional borrower risk through over exposure to borrowing (20%), expectation of rejection (17%) and expected high cost of finance (13%). For those that had applied for finance and then become discouraged, expectations of rejection (29%) and delays taking too long in obtaining finance (14%) become increasingly important, whilst risk avoidance remains a key reason (15%).

The characteristics of SME-discouraged borrowers () are significantly related to smaller size, younger age and less resources; micro businesses (1–9 employees; <.001 level), young businesses established five or less years (<.001), SMEs with no partners or directors (self-employed; <.001) and SMEs declaring poor capabilities to access finance (<.001). Furthermore, those using external finance finders and advisors are more likely to exhibit discouragement (<.001) alongside SMEs that have a formal business plan, but do not keep it updated (<.01). Our findings are in-line with previous studies where smaller, younger SMEs, with lesser management resources and capabilities are more likely to be discouraged (Fraser Citation2014; Cowling, Liu, and Ledger Citation2012). However, what is more revealing in this empirical study is that discouragement extends beyond merely young firms; it included more established typically smaller SMEs that may be struggling and lack financial management skills, including basic business planning (Xiang, Worthington, and Higgs Citation2015). Again, this underpins the RBV perspective on access to finance (Barney Citation1991; Owen, Deakins, and Savic Citation2019). Additionally, the finding that minority ethnic-led businesses are significantly discouraged (<.001) may relate to first-generation managers, who may lack cultural and network experience and contacts to assist with accessing external finance (Smallbone et al. Citation2003).

Our data exploration reveals the causal links contributing to UK SME demand or supply-side failure to access external finance and strongly suggests that smaller and younger UK SMEs suffer from inherent demand-side failures constraining their access to external finance. This has implications for the dynamics of UK economic growth, especially where there is persistently high incidence of discouraged borrowers amongst start-ups and more established viable SMEs failing to secure external finance, leading to social and economic welfare loss.

RQ2 Significant factors – Demand or Supply Failure?

We use multivariate binary logit models to explore whether the applicants for external finance during the past 12 months received at least some finance. Using the business and management characteristics from our initial bivariate analysis, we test which factors are more likely to determine the success or failure of applications and whether these are demand or supply-side related factors.

Our basic model results (; note, provides a correlation matrix for variable relationships within the regression models), assessing whether SME applicants received at least some funding proved robust, with 85.6% accuracy. Findings were significantly different from the baseline model at <.001 level, with Nagelkerke R2 13.8% explanation of outcomes and Hosmer and Lemeshow “HL” model goodness-of-fit of .72 (<.05).

Table 3. Obtained at least some external finance in the last 12 months.

Table 4. Correlation matrix.

Our results support mainly demand-side explanations, particularly in relation to the firm’s perceived capabilities and employment size.

Internal resources

Increased self-reported perceptions of the firm’s higher level of capabilities to access finance is significantly associated with increased chances of accessing finance. Comparing firms’ perceived capabilities, those firms with poor capabilities are less likely (0.323 times) to obtain finance than those with good capabilities (<0.001); firms with average capabilities are also less likely (0.496 times) to obtain finance than those with good capabilities (<0.01). These findings make a case for increasing firm capabilities to enhance their chances of obtaining external finance.

Firm size

Increased employment size (a strong proxy indicator of increased resource base for accessing external finance) is associated with increased chances of obtaining finance. Notably, firms with zero employees are less likely (0.297 times) to obtain finance than the ones with 50 to 249 employees (<0.001). Whilst it can be argued that young small firms face supply-side shortages in finance, this evidence demonstrates a key association between firm size and improved capabilities of access to external finance. It suggests that smaller firms, even when established, may suffer demand failures due to their weaker capabilities to access finance.

Types of finance

Disaggregating the types of finance sought demonstrates that access to loan, equity, grant and leasing finance is significantly (<.01 level) improved by perceived better capabilities to access financeFootnote44. Women-led firms are significantly less likely (0.464 times) to access bank overdraft finance than their male counterparts (<0.05), supporting previous findings (IFC Citation2011) that women entrepreneurs may be disadvantaged when accessing external finance due to gender bias (Marlow and Patton Citation2005; Moro, Wisniewski, and Mantovani Citation2017); a potential supply-side failing, or a demand failing in relation to lacking confidence and being unable to adequately present their cases for finance.

Sectors

Supply-side financing deficit may affect particular sectors. The catering sector is perceived as volatile and high risk by UK banks (GLA Citation2013). SMEs in accommodation and food catering are less likely (0.337 times) to have obtained finance than those in other sectors (<0.05). When different forms of finance are disaggregated, the catering sector was particularly disadvantaged (<.05 level) when accessing bank overdraft finance.

Location

Appears significant to lenders. The more peripheral and rural areas away from large city banking and financial centres may be underserved (North, Baldock, and Ekanem Citation2010). Firms located in the Midlands (0.144 times) and North (0.16 times) of England are significantly less likely to have obtained a bank overdraft (<.05); whilst firms located in urban areas are more likely (1.899 times) to have obtained loan finance than the ones in rural areas (<.01).

Three additional models were tested to evaluate the effect of the external factors to the base model. The additional models included variables that measured: (i) the existence of an up-to-date business plan; (ii) the level of innovation of the venture; and (iii) future and past growth (in turnover and employment). This analysis highlights two equivalent points. First, the three external factors do not contribute significant impact to explain access to funding (only one variable, declining sales, was statistically significant <.1). Second, all variables that were significant in the base model were also significant in the three new models. Additionally, the coefficient signal and the odds ratios were consistent across the four models.

Borrower discouragement

Lack of confidence, networks and financial literacy negatively impact on SMEs’ success in accessing external debt and equity finance, leading to discouragement of finance seekers (Xiang, Worthington, and Higgs Citation2015). To corroborate or reject these findings, we measured borrower discouragement by establishing that SMEs had external financing requirements but did not apply for this finance in the year prior to the survey. This may be perceived as another form of demand-side failure. Results for the basic regression model () were robust, with 86.30% accuracy; implying significant difference from the baseline model at <.001 level, R-square 8% explanation of outcomes and Hosmer and Lemershow “HL” model goodness-of-fit at 0.963 (<.01).

Table 5. Discouraged from applying for external finance in last 12 months.

Findings corroborate the RBV perspective (Barney Citation1991) with smaller and younger firms, with poor management capabilities and less access to external advice being most discouraged. SMEs with perceived poor management capabilities are significantly more likely (2.634 times) to be discouraged from seeking external finance than those with good capabilities (<.001); firms with average capabilities are also more likely (1.827 times) to be discouraged than those with good capabilities (<0.01). Firms that did not seek external advice to obtain finance are more likely (1.620) to be discouraged than the ones that did. Younger SMEs established up to five years are significantly more likely (1.666 times) to be discouraged than those established for more than 20 years (<.001). In terms of size, companies with 1 to 9 employees are more likely (1.471) to be discouraged than the ones with 50 to 249 (<.001). Similarly, firms with 10 to 49 employees are more likely (1.481 times) to be discouraged than the ones with 50 to 249 (<.001).

The analysis also indicates that ethnic minority-led SMEs are significantly less likely (0.536) to be discouraged than their indigenous counterparts (<.001). These findings appear to contradict previous studies arguments that non-indigenous entrepreneurs lack confidence, cultural knowledge or experience to approach and successfully secure external finance, or may be disadvantaged by credit scoring centralised lending, which can adversely impact on the technically and financially less literate owner-managers/management teams (Smallbone et al. Citation2003; North, Baldock, and Ekanem Citation2010; Mason and Kwok Citation2010; IFC Citation2011). However, such studies are highly nuanced by ethnic group, generation and sector, suggesting for example that external financing problems are more prevalent for first generations facing language and cultural barriers. What is perhaps more evident here is that mature second-generation minority ethnic businesses (which are likely to represent the vast majority, Smallbone et al. Citation2003) may not be discouraged.

Similarly, to the funding model, we evaluated the impact of: (i) the existence of an up-to-date business plan; (ii) the level of innovation of the venture; and (iii) future and past growth (in turnover and employment) in the likelihood of a venture being discouraged. Again, all variables that were significant in the base model are also significant in the three new models. However, all three external factors seem to affect the likelihood of SME discouragement. The model evaluating having a business plan demonstrates that SMEs that kept their documentation up-to-date were more likely (1.234 times) to be discouraged (<.05) than those without a plan. Similarly, SMEs with an outdated business plan were also more likely to be discouraged (1.514 times) than those without one (<0.01). This indicates that having a business plan might well act as a discouragement through self-assessment, with prior failure to access finance leading to a lapse in keeping plans up-to-date. It could also indicate that business plans are required by advisors, who may then assess that the business does not have a viable funding case, whilst those not requiring finance may not perceive a need for a business plan.

The model assessing the impact of innovation in discouragement shows that both variables indicated that innovative SMEs are less likely to be discouraged. SMEs introducing product or service innovations are less likely (1.698 times) to be discouraged than non-innovators (<.001). Similarly, SMEs introducing process innovations are less likely (1.229 times) to be discouraged (<.01). These findings are more positively for the UK economy, since innovative SMEs are not being discouraged from seeking external finance.

The growth model reveals two key findings. First, turnover growth does not appear to explain discouragement, since the two variables measuring past and future turnover were not statistically significant. Second, past and future employment growth may explain discouragement, as they were statistically significant (<.05). SMEs with stable employment were less likely (0.748 times) to be discouraged than those increasing their number of employees in the last year (<0.05). Similarly, SMEs that reduced their number of employees were less likely (0.698 times) to be discouraged than those that increased employees (<0.05). In terms of future employment growth, our findings indicate that SMEs that expect to remain with the same number of employees are less likely (0.762 times) to be discouraged than those expecting to increase their work force (<0.05). The lack of correlation between employment and sales with regard to discouragement appears to indicate that discouraged SMEs (which are less innovative) are foregoing process innovation investment in favour of employment growth, or struggling and perceive that they are unable to provide valid investment cases. Either way, they are likely to be contributing to the UK’s lack of productivity puzzle (HM Government Citation2017).

Overall, our findings challenge the long-held view that predominantly supply-side failure deprives SMEs access to external finance, without qualifying the stage of the business operation. We observe prominent demand-side failure correlated with SMEs’ employment size. We also reveal multiple and complex RBV and management characteristics that impact on the intentions of SME owners when accessing external finance. One additional possible explanation for the demand-side failure in this case may be that the GFC has led to revision of credit scoring methodology employed by lenders, raising the hurdle for securing a loan; the higher threshold may be making it more difficult for SMEs to succeed, particularly smaller employee ones, leading to lower numbers of loan applications (North, Baldock, and Ullah Citation2013).

RQ3 The scope and capability of public SME finance support policy

In the wake of major financial and political crises, such as the GFC, the quantitative findings from the LSBS 2015 raise important questions for both SME finance policy and delivery. Our findings question the commonly held view that the SME finance gap is largely attributable to supply-side failure (Owen, Deakins, and Savic Citation2019). To further understand and corroborate these findings we consulted with six experienced business and finance advisors from the Oxford Innovation (OI) agency network, specialising in early and growth scale-up stage financing for UK SMEs. This discussion section, addresses the quantitative data’s emergent business characteristic and RBV issues across three demand centred themes where business finance advisors feel that they can make a difference; selection of finance, the role of advisors and discouragement.

Selection of finance

Interviewees experiences corroborated quantitative findings that most SMEs received at least some funding (83% applicants) over the last year. The prevalence of different sources (in order of most survey responses); bank loans, overdrafts, leasing/HP, credit cards, factoring, equity, grants and P2P debt finance was generally thought to be in line with the interviewees experiences. They reported that “The UK financing picture is changing … SMEs tend to use personal finance and banks as their first external lender and they typically have existing relationships” and this aligns with pecking order theory (Myers and Majluf Citation1984) and path dependency theory (Teece Citation2007; Owen, Deakins, and Savic Citation2019). “However, post the GFC, SMEs are increasingly finding that bank borrowing is not appropriate for various reasons such as strict terms and conditions, longer processing time, increasing lender demands for collateral, trade history, aversion to supporting innovative and risky projects.” This quote underscores similar observations of restricted and increased costs of bank lending for SMEs in the UK (Cowling, Liu, and Ledger Citation2012; North, Baldock, and Ullah Citation2013).

Respondents further noted, “there are now far more flexible alternatives to financing cash-flow and other financing needs especially through crowdfunding and P2P”. These changes highlight the evolution of the post GFC UK funding escalator (Mason Citation2017) and, for example, the ease of access for established SMEs to obtain P2P funding (e.g., from Funding Circle) as a substitute for bank lending (Mac an Bhaird et al. Citation2019). The advisors highlighted the example of the South West of England, where they reported that the volume of lending has increased through P2P with decisions being made more quickly (e.g., within 7 days) when compared to banks loan approvals. Although the survey analysis suggested that bank loans, overdrafts, leasing/HP, credit cards were accessed with far greater frequency than P2P, interviewees reported growing SME use of alternative P2P and crowdfunding financing products, supporting other UK evidence (Davis Citation2012; Zhang et al. Citation2017).

The interviewees therefore strongly supported the view that SMEs’ failure to access finance was due in part to their lack of knowledge of alternative finance. It was no surprise that the majority of finance seekers exhibit path dependency (Teece Citation2007), only going to one provider which is typically their bank. “A lot more work needs to be done to educate SME entrepreneurs on what are the appropriate sources of finance for their business, especially on particular products like mezzanine finance to improve demand for alternative products”. Furthermore, the personal circumstances of the entrepreneur are considered crucial in accessing external finance, indicating that their ability and willingness to provide personal guarantee and collateral is a key determinant to accessing bank finance or alternative types of finance. These findings are supported in previous studies (Deakins and Hussain Citation1994; Smallbone et al. Citation2003; North, Baldock, and Ekanem Citation2010; Cowling, Liu, and Ledger Citation2012). Thus, whilst these findings mainly confirm prior studies, they highlight the importance of entrepreneurial finance knowledge and the potentially critical role of external advisors, which many studies overlook (Owen, Deakins, and Savic Citation2019).

The role of advisors

We asked the advisors why SMEs using external finance support were found to be less successful (although not significantly) at accessing external finance. They suggested that often SMEs already in distress seek external assistance at a late stage that renders help less effective. Furthermore, such entrepreneurs in smaller and younger firms are more likely to need risk finance that requires highly skilled trusted advisors and connected niche financiers (e.g., public-backed mezzanine funders operated by UK Regional Investment Funds; BEIS Citation2017). Interviewees also suggest, “Already ‘distressed’ SMEs when they engage with finance finders and advisors are likely to have already struggled to raise finance … ”. This is partially supported by the greater (but not significant) likelihood of SMEs with up-to-date business plans failing to obtain finance. Furthermore, “ … .Their approach to raising funds is not necessarily ‘tactical’ or ‘strategic’ but ‘reactionary’, requiring immediate cash-injection. An example is where entrepreneurs leave it too late to access external finance, which is reflected in the ‘turnaround’ market where firms are about to go bust. This has given rise, in some cases, to the practice of ‘Pre-Pack Administration’ when an insolvent business is sold to a ‘phoenix’ company” (i.e., a business that has been set up by the existing directors before going into administration).Footnote5

A notable distinction is between “distressed” early-stage companies that engage advisors and those that do so as part of a calculated plan for growth. In the former case, success is highly unlikely and there may be other motivations driving the advisory engagement, such as administration fees, pre-pack deals (HoC Citation2016). Where SMEs are already distressed advisors are unable to fundamentally change their business plans. They often have to look at several different finance sources before getting any traction, thus requiring greater numbers of applications. Those SMEs which seek external support are also often younger and smaller business which may not have the management resource (e.g., a Financial Director) to focus on searching and accessing external funds, often with little knowledge of non-bank financing (Owen, Deakins, and Savic Citation2019).

The advisors also highlighted “crucial trust and links between firms, finance finders and advisors and potential investment providers” playing an influential role to successfully securing external finance. This supports the concept of network ties and bonds in facilitating SMEs’ accessing external finance (Uzzi Citation1999). More importantly, there is a difference between long-term relationship advisors and short-term service providers. The former is considered more effective as they can work with SME clients over a longer period, understand their needs, and provide a wider financing network which firms access. A related issue is the incentive/remuneration method for advisors which may also influence the outcome for firms;Footnote6 “Advisors tend to work at risk and have different approaches to secure their income, including retainer, success, and upfront fees”. These issues are raised in the broader access to SME support literature (Mole, North, and Baldock Citation2017) and need further exploration to see how they affect SMEs’ access to external funds.

The finding that younger firms, under five years of age, were more likely to use financial advisors, was considered to be due to their higher risk finance profiles and lack of established networks. These businesses may be unable to obtain bank finance (North, Baldock, and Ullah Citation2013) and are likely to require external expert assistance to find and make applications for grants and equity (Mason and Kwok Citation2010; Owen, Deakins, and Savic Citation2019). “For example, a young spin-out firm, which may have received public grants e.g., Smart award from Innovate UK – typically requiring matching funding – and then accessed other support e.g., Knowledge Transfer Network – may then be ready for seeking equity investment”. There is also evidence that business finance advisors can add to the “collateral value” of applications, mitigating some of the risk for lenders to an earlier stage business (Owen et al. Citation2017; OECD Citation2018).

In conclusion, LSBS 2015 findings suggest that larger businesses with stronger management resources are significantly more likely to successfully access external finance (supporting the RBV view of SME access to finance, Barney Citation1991). Larger SMEs tend to have greater management resources, greater extended networks to tap into, and use experts to prepare their business finance case, resulting in higher quality presentations/pitches which will help to mitigate information asymmetry and persuade financiers to lend (BEIS Citation2017). For younger, smaller businesses that require risk finance for growth or to overcome distress, this study sheds important new light into the crucial role of specialist finance advisors to assist with investment readiness and business plans and access to niche risk finance networks (e.g., business angels and public backed lenders) to overcome IA barriers. Critically, we progress the demand failure analysis of Owen, Deakins, and Savic (Citation2019) in finding that these advisors offer more support than typical small firms accountants (Mole, North, and Baldock Citation2017) and that where trusted established partnerships exist, this can lead to more sustainable SME financing outcomes.

Discouragement

The advisors supported the LSBS findings that younger and smaller SMEs with declared poor access to finance capabilities are less likely to succeed in accessing external finance and are more likely to exhibit borrower discouragement. This is in-line with other recent UK studies (Fraser Citation2014). The apparently contradictory finding that SMEs with business plans (even when up to date), and employment growth orientation are more discouraged from accessing external finance, may indicate the more conservative investment approaches of SMEs in times of economic uncertainty. Again, advisors were asked about the increased likelihood of discouragement with use of business advice, particularly for small employer SMEs with business plans, suggesting either their unsuitability for external finance, or the unsuitability of advice offered at the time.

Th advisors considered that the discouraged borrower firms within this sample were largely ill-prepared, in terms of financial information, management resources and entrepreneurial capital to secure external finance, or that those with up-to-date business plans were cautious low innovation firms struggling with lagged or low sales growth potential that contributes to the UK’s low productivity puzzle (BEIS Citation2017). This is underpinned by discouraged SMEs being less likely to seek advice, or previously unsuccessful applicants when they do so.

Interviewees concurred with quantitative findings that smaller and younger SMEs are less likely to obtain bank funding; due to limited finance raising experience, lack of collateral and track record, which also often limits their chances to access equity finance (North, Baldock, and Ullah Citation2013). The finding that discouragement extends to small firms with up to 49 employees, is “ … indicative of the large proportion of cautious and potentially under-performing firms, underlined by the prevalence of those with up-to-date business plans, but holding back on investment, or seeking advice on new financing alternatives to banks.”

Advisors observed that young entrepreneurs lack resources and experience, leading to inadequate business planning and ongoing business development planning. “Business plans are important for accessing external funds but … many SMEs are too busy ‘fighting fires’ in their day-to-day operations to devote the resources required”. Furthermore, “ … business plans will change over time especially for start-ups, due to pivoting of their business model and this should be expected and supported, as it can ultimately be a positive development”. A further observation was that SMEs and the lender can pull out of a deal at the “last minute” thus giving rise to trust deficit and causing discouraged affect next time round (Fraser Citation2014). Advisors agreed on the main reasons for discouragement (e.g., avoiding additional risk, fear of rejection, perceived high cost of finance and length of time and amount of hassle to obtain finance), but were surprised that time delays and excessive hassle were not higher up the list (Mac an Bhaird et al. Citation2019) alongside inability to obtain co-finance to leverage sufficient funding (Owen, Deakins, and Savic Citation2019 report grant fund matching difficulties).

Advisors also suggested that retail bankers’ cautious attitude to early-stage SMEs was also a factor. Most retail banks have a corporate policy of not lending without well-covered collateral. This supports the economic cycle view of Cowling, Liu, and Ledger (Citation2012) that post GFC bank lending has become less accessible for young, early-stage UK SMEs. Furthermore, this has become more acute in some sectors, such as hospitality, where LSBS 2015 findings suggest a potential supply-side funding gap, which may extend to banks not lending regardless of the maturity of small businesses.

Discussion and conclusions for policy and theory

Our LSBS 2015 study of UK SME access to finance demonstrates how the GFC and resultant SME bank lending policy restrictions on SMEs has disproportionally negatively impacted on younger and smaller firms’ access to external finance and contributed to their higher levels of borrower discouragement. We offer deep insights into the further adjustments to entrepreneurial finance theory and practice required to ensure that SMEs are adequately financed and supported through the current UK post-Brexit and post-Pandemic economic rebuild, which will require a significant contribution from SMEs (HM Treasury Citation2021).

Whilst we reveal that the vast majority of SME applicants receive the funding that they require, our findings demonstrate potential supply-side failure, particularly in the lack of bank and equity finance for viable early-stage SMEs, and a persistent patient capital gap for smaller SMEs, alongside locational disadvantages in more remote and rural regions (BEIS Citation2017).

However, whilst prior studies mainly focus on supply-side remedies for SME finance gaps, we also find that a major cause of UK SME finance gaps is demand-side failure. We provide significant evidence that the poorer management capability of younger and smaller SMEs is associated with demand failures and increased levels of discouragement, which are contributing to UK SME underinvestment. We also reveal that external support is underutilized and often ineffective and yet, if delivered by specialist advisors in a timely and suitable relationship financing fashion (North, Baldock, and Ekanem Citation2010), it could develop more sustainable SMEs.

The major contribution of the paper is therefore to develop the resource-based view (RBV) of SME access to finance (Barney Citation1991), by demonstrating that resource failure, due to poor financial management and finance seeking capabilities is not only strongly correlated with finance application failure, but also with borrower discouragement (Fraser Citation2014). This suggests requirements for improved business finance support to upskill entrepreneurs’ financial management, financial literacy and investment readiness. From a policy perspective, a key finding is the duality of discouragement between young and small firms that are either cautious and uncertain of their ability to raise appropriate funds that could aid growth and scale-up, or distressed and unsuited to finance. The former may grow employment, but suffer lagged sales growth (typical of the innovation “valley of death” period, Owen, Deakins, and Savic Citation2019), and may be symptomatic of process underinvestment that is contributing to the UK’s poor production puzzle.

Many of the younger and smaller SMEs that struggle to obtain external finance are poorly externally networked and fail to seek advice, or to receive adequate specialist and timely financing advice. Insufficient financial literacy to make loan applications to the current highly centralised UK banking system that has replaced relationship banking with credit scoring (North, Baldock, and Ekanem Citation2010; Cowling, Liu, and Ledger Citation2012; North, Baldock, and Ullah Citation2013), or to adequately consider and apply for alternative finance such as crowdfunding, P2P, asset and equity, is a major issue.

These findings make a case for a more “holistic entrepreneurial finance ecosystem approach” which adequately remedies the demand failures we expose and supports SME development pipelines (Mason and Brown Citation2013) and “ecosystem approaches” (Hwang and Horowitt Citation2012; Hughes Citation2009). Entrepreneurship skills development including financial management is essential to enable SMEs to access external finance. In turn this supports RBV related theory around investment readiness (Mason and Kwok Citation2010), signalling (Mueller, Westhead, and Wright Citation2012) and networking (Uzzi Citation1999) and suggests a key bridging role for external financial intermediaries and advisors (Owen, Deakins, and Savic Citation2019; Lerner Citation2010).

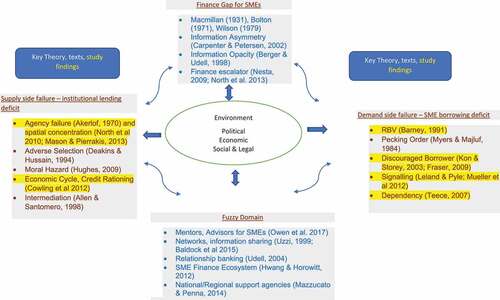

offers a summary review of how our findings fit within the emerging theoretical entrepreneurial finance ecosystem framework (Owen, Deakins, and Savic Citation2019), from a UK perspective. It presents historically reported explanations for the SME finance gap, mainly attributed to supply-side failures. We highlight where our empirical UK-based study finds support for these via bank credit rationing and the resultant reduction in patient capital supply alongside uneven regional distribution, which has significantly negatively impacted younger and smaller SMEs. However, we also highlight that, in this period where alternative finance is increasingly available, it is demand-side failure that provides a greater set of explanations. This shift has received limited attention from academics, practitioners and policymakers. We therefore develop the emerging more holistic enterpreneurial finance ecosystem approach required to address SME finance (Owen, Deakins, and Savic Citation2019) by demonstrating the critical role for specialist financial advisors to assist young, small SMEs in growth and distress financing to create more sustainable SME financing outcomes. Far more attention is required to develop holistic theoretical and policy solutions with greater focus on the “fuzzy domain” of business advice and network support extention of financial intermediation which straddles SME finance supply and demand to overcome information asymmetries.

Figure 1. Conceptualising a holistic approach to supply and demand side of SME finance.

From a policy perspective, the UK Government has consistently been committed to SME growth, with increasing concerns for improving productivity, and to facilitating this via SME investment through improving the post-GFC UK SME finance escalator (Owen et al. Citation2020). Notably, this has involved the development and oversight of supply-side debt and equity instruments through the emerging role of the British Business Bank (Van der Schans Citation2015).

Recent events affecting the UK and global financial markets relating to Brexit, the Pandemic and Ukraine crisis have led to renewed importance being attached to developing industrial policy that is inclusive of strategic support for SMEs. This has included the Treasury patient capital review, Industrial Strategy and Plan for Growth (HM Treasury Citation2021). These increase emphasis on addressing key sector and regional SME financing imbalances through the British Business Bank’s Regional Investment Funds and proposed Shared Prosperity Funds (to replace the loss of EU regional funds) and improve on long-standing supply-side failings (both sectoral and regional). However, amidst growing concerns over the UK’s relatively poor productivity, we present new evidence on an important group of young and established SME discouraged borrowers that are unlikely to increase their productivity. We find strong evidence that financial literacy, investment readiness (Mason and Kwok Citation2010) and improved financial support and intermediary services (Owen, Deakins, and Savic Citation2019) can address this to provide future SME sustainability and growth.

Now, more than ever, there is a need for the British Business Bank to step-up and play the significant overarching SME finance and support role to provide a holistic policy approach (Mazzucato and Penna Citation2014). This can deliver public-private linkages to enable private sector financiers and support agencies to deliver a more effective SME finance escalator (North, Baldock, and Ullah Citation2013). We note improvements in recent years through the British Business Bank’s introduction of regional representatives working with English Local Enterprise Partnerships (LEPs) to improve the promotion of the Regional Investment Funds and business angel investment networks (BBB Citation2022). However, more needs to be done to fund and deliver the additional specialist business support, previously delivered unevenly and inconsistently through EU competition funding via LEPs in England (Uyarra, Shapira, and Harding Citation2016). Our research demonstrates that further SME finance policy cohesion can lead to a more sustainable productive UK SME sector.

Limitations and future research applications

This paper was based on the largest survey of SME finance undertaken in the UK at the time. Nevertheless, it is limited by insufficient scale to accurately measure equity finance (which represents only 6.5% of finance seekers), but is likely to be related to more growth-oriented SMEs (North, Baldock, and Ullah Citation2013). The authors have proposed to BEIS that a national survey of UK SME early equity investment is required to fill this vital knowledge gap. Furthermore, the data presented in the paper only relate only to the snapshot cross-sectional LSBS baseline survey of 2015. Subsequent annual waves of the LSBS have confirmed the data reported here (Owen et al. Citation2017) and are starting to provide deeper insights into UK SME financing trends. However, the longitudinal data remains limited and under developed in terms of tracking SME external financing with their business performance over time and contextual comparisons between the performance of UK SMEs with different countries SME financing. Leading on form this, since banks remain the predominant form of external finance sought and used by UK SMEs, future research should explore bank policy and practice in different countries (e.g., Germany’s Sparkasse regional banks), in addition to examining the relationship between financial literacy and bank application success, to examine the merits of relationship banking and find good practice practitioner solutions to support SME lending. Finally, we believe that we have established a robust mixed methods approach which may be adopted by future researchers (albeit possibly with more supply-side interview insights) to undertake research which generates greater understanding of the operation of the SME entrepreneurial finance ecosystem.

Acknowledgments

The authors are grateful for seed funding received from the Enterprise Research Centre (ERC) and reviewer feedback from Professor Stephen Roper. We also acknowledge the free assistance provided by Oxford Innovation, a leading UK support agency for potential high growth SMEs.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. Demand for external finance has also fallen prior to the COVID-19 pandemic for self-employed, but data for UK employer SMEs is considered as a more robust measure (BEIS 2020).

2. Most broad data reported by sector, location and business size are robust to 1% significance. It should be noted that there is oversampling of medium sized enterprises and under-sampling of self-employed and micro enterprises to provide robust data scale.

3. Note, it was not possible to ascertain across all types of finance whether all funding applied for was secured. Where this was possible to check (i.e. bank loans and equity finance) over 90% of required finance was received.

4. Examination of the specific types of finance indicated robust models for all except equity where the numbers were small and the HL is .025 and the baseline model only has .1 difference and charitable/trust/grants where similarly to equity some observations fall below 50 cases. All of the models have at least 75% classification accuracy.

5. A pre-pack is an “arrangement under which the sale of all or part of a company’s business or assets is negotiated with a purchaser prior to the appointment of the administrator, and the sale contract executed on the appointment of the administrator or very shortly afterwards”. See: House of Commons Library Briefing Paper, Number CBP5035, Pre Pack Administration. 20th January 2016.

6. Fees may reduce the number of less quality businesses (a finding supported by Mole et al. Citation2017).

References

- Ahlers, G. K.C., D. Cumming, C. Gunther, and D. Schweizer. 2015. “Signalling in Equity Crowdfunding.” Entrepreneurship Theory and Practice 39 (4): 955–980. doi:10.1111/etap.12157.

- Anyadike-Danes, M., and M. Hart. 2017. The UK’s High Growth Firms and Their Resilience Over the Great Recession. Enterprise Research Centre research paper no. 62, September. Warwick University.

- Armstrong, A., Davis P E, L. Liadze, and C. Rienzo. 2013. Evaluating Changes in Banking Lending to UK SMEs Over 2001-12. Ongoing Tight Credit. NEISR Discussion Paper No.408, UK Department for Business, Innovation and Skills, BIS/13/85.

- Ayyagari, M., A. Demirgüç-Kunt, and V. Maksimovic. 2011. Small Vs. Young Firms Across the World – Contribution to Employment, Job Creation, and Growth. Policy Research Working Paper, 5631, The World Bank Development Research Group.

- Baldock, R., and R. Harrison. 2015. “Financing SME Growth in the UK: Meeting the Challenges After the Global Financial Crisis.” Venture Capital 17 (1–2): 1–6. doi:10.1080/13691066.2015.1050241.

- Baldock, R., P. James, D. Smallbone, and I. Vickers. 2006. “Influences on Small Firm Compliance Related Behaviour: The Case of Workplace Health and Safety.” Environment and Planning C 24 (6): 827–846. doi:10.1068/c0564.

- Baldock, R., and C. Mason. 2015. “Establishing a New UK Finance Escalator for Innovative SMEs: The Roles of the Enterprise Capital Funds and Angel Co-Investment Fund.” Venture Capital 17 (1–2): 59–86. doi:10.1080/13691066.2015.1021025.

- Bank of England. 2015. Trends in Lending: April. London: The Bank of England.

- Barney, J. 1991. “Firm Resources and Sustained Competitive Advantage.” Journal of Management 17 (1): 99–120. doi:10.1177/014920639101700108.

- BBB. 2016. The Business Finance Guide: A Journey from Start-Up to Growth. British Business Bank report

- BBB. 2022. Northern Powerhouse Investment Fund Interim Evaluation Report. Sheffield: British Business Bank PLC, April.

- Beck, T., and A. Demirguc-Kunt. 2006. “Small and Medium-Size Enterprises: Access to Finance as a Growth Constraint.” Journal of Banking & Finance 30 (11): 2931–2943. doi:10.1016/j.jbankfin.2006.05.009.

- BEIS. 2017. The Innovative Firm’s Journey to Finance. A Report by BMG and CEEDR, BEIS Research Paper Number 23, November. London: Crown Copyright.

- BEIS. 2020. Longitudinal Small Business Survey: SME Employers (Businesses with 1-249 Employees) – 2019. Report by UK Department for Business, Energy and Industrial Strategy, June. London: Crown Copyright.

- Berger, A N., and G F. Udell. 1992. “Some Evidence on the Empirical Significance of Credit Rationing.” The Journal of Political Economy 100 (5): 1047–1077. doi:10.1086/261851.

- Berger, AN., and DF. Udell. 1998. “The Economics of Small Business Finance: The Roles of Private Equity and Debt Markets in the Financial Growth Cycle.” Journal of Banking and Finance 22 (6–8): 613–673. doi:10.1016/S0378-4266(98)00038-7.

- Birch, DGW. 1979. “The Job Generation Process.” MIT Program on Neighborhood and Regional Change. https://ssrn.com/abstract=1510007

- BIS. 2013. Small Business Survey 2012: SME Employers. BMG report for the UK Department for Business, Innovation and Skills, April

- BIS. 2016. “Longitudinal Small Business Survey Year 1: SME Employees.” UK Department for Business, Innovation and Skills research paper 289, May.

- Bolton, J.E. 1971. “Committee of Inquiry on Small Firms.” In Cmnd. Vol. 4811. London: H.M.S.O.

- Bolton, P., and DS. Scharfstein. 1996. “Optimal Debt Structure and the Number of Creditors.” The Journal of Political Economy 104 (1): 1–25. doi:10.1086/262015.

- Breedon Review. 2012. Boosting Finance Options for Business. Report of the Industry-led Working Group in Alternative Debt Markets, March. London: Crown Copyright.

- Carpenter, RE., and BC. Peterson. 2002. “Capital Market Imperfections, High Tech Investment and New Equity Financing.” The Economic Journal 112 (477): 54–72. doi:10.1111/1468-0297.00683.

- Cavalluzzo, K., and J. Wolken. 2005. “Small Business Loan Turndowns, Personal Wealth, and Discrimination.” The Journal of Business 78 (6): 2153–2178. doi:10.1086/497045.

- CMA. 2015. Productivity and Competition: A Summary of the Evidence. Report by UK Competition and Markets Authority, July. London: Crown Copyright.

- Coco, G. 2000. “On the Use of Collateral.” Journal of Economics Survey 14 (2): 191–214. doi:10.1111/1467-6419.00109.

- Commission of the European Communities. 2008. A Small Business Act for Europe. Com(2008)394. Brussels: Commission of the European Communities.

- Cowling, M. 2010. “The Role of Loan Guarantee Schemes in Alleviating Credit Rating.” Journal of Financial Stability 6 (1): 63–71. doi:10.1016/j.jfs.2009.05.007.

- Cowling, M., W. Liu, and A. Ledger. 2012. “Small Business Financing in the UK Before and During the Current Financial Crisis.” International Small Business Journal 30 (7): 778–800. doi:10.1177/0266242611435516.

- Cowling, M., W. Lu, M. Minniti, and N. Zhang. 2016. “UK Credit Discouragement During the GFC.” Small Business Economics 47 (4): 1049–1074. doi:10.1007/s11187-016-9745-6.

- Creswell, JW. 2003. Qualitative, Quantitative and Mixed Methods Approaches. Thousand Oaks, CA: Sage.

- Dart, J. J., and R.J. Davies. 2003. “A Dialogical Story-Based Evaluation Tool: The Most Significant Change Technique.” American Journal of Evaluation 24 (2): 137–155. doi:10.1177/109821400302400202.

- Davis, A. 2012. Seeds of Change: Emerging Sources of Non-Bank Funding for Britain’s SMEs. Report by Centre for the Study of Financial Innovation, July.

- Deakins, D., and M. Freel. 2012. Entrepreneurship and Small Firms. Maidenhead: MacGraw-Hill.

- Deakins, D., and G. Hussain. 1994. “Risk Assessment with Asymmetric Information.” International international Journal of Bank Marketing 12 (1): 24–31. doi:10.1108/02652329410049571.

- De Bettignies, J E., and J A. Brander. 2007. “Financing Entrepreneurship: Bank Finance versus Venture Capital.” Journal of Business Venturing 22 (6): 808–832. doi:10.1016/j.jbusvent.2006.07.005.

- Fraser, S. 2014. Back to Borrowing? Perspectives on the ‘Arc of Discouragement’. ESRC White Paper No. 8, March

- Fraser, S., S K. Bhaumik, and M. Wright. 2015. “What Do We Know About Entrepreneurial Finance and Its Relationship with Growth?” International Small Business Journal 33 (1): 70–88. doi:10.1177/0266242614547827.

- GLA. 2013. SME Finance in London. Report by SQW and CEEDR to the Greater, November. London Authority.

- Hamilton, R T., and M A. Fox. 1998. “The Financing Preferences of Small Firm Owners.” International Journal of Entrepreneurial Behavior & Research 4 (3): 239–248. doi:10.1108/13552559810235529.

- HM Government. 2017. Industrial Strategy: Building a Britain Fit of the Future. White Paper, November. London: Crown Copyright.

- HM Government. 2022. Levelling Up the United Kingdom. February. CP604 Crown Copyright.

- HM Treasury. 2021. Build Back Better: Our Plan for Growth. CP401 London. March.

- HM Treasury & BIS. 2011. The Plan for Growth. London: Published by UK Department for Business, Innovation and Skills (BIS) and HM Treasury. March.

- HoC. 2016. “House of Commons Library.” Briefing Paper, Number CBP5035, Pre Pack Administration.January20

- Hsu, D. 2004. “What Do Entrepreneurs Pay for Venture Capital Affiliation?” The Journal of Finance 59 (4): 1805–1844. doi:10.1111/j.1540-6261.2004.00680.x.

- Hughes, A. 2009. “Hunting the Snark: Some Reflections on the UK Support for the Small Business Sector.” Innovation, Management, Policy and Practice 11 (1): 114–126. doi:10.5172/impp.453.11.1.114.