ABSTRACT

It has been widely recognized that platforms utilize their editorial capacity to transform the industries they intermediate. In this paper, we examine the intermediary role of the leading audio streaming platform – Spotify – on the recorded music industry. Spotify is often called the ‘new radio’ for the influence it has on breaking songs and artists, and for the role it plays in music discovery and consumption. Our purpose is to determine whether Spotify is leveling the playing field or entrenching hierarchies between major labels and independent labels. We attempt to answer this question through a longitudinal analysis of content owners (major labels or ‘indies’) and formats (albums, tracks, or playlists) promoted by Spotify through its global Twitter account: @Spotify. As a carefully curated venue for corporate speech @Spotify provides a window into continuities and changes in Spotify’s corporate strategy. By using @Spotify as a proxy through which to track patterns of promotion between the years 2012 and 2018, this paper offers a novel empirical examination of how Spotify is shaping the consumption of music, and in turn the structure of the recording industry. In doing so, we provide evidence for speculating about the future of the recorded music industry in a platform era.

Introduction

Borrowed from industry, the term ‘platform’ connotes neutrality (Gillespie, Citation2010). In recent years, however, there has been growing critical and academic interest in the social and cultural impacts of platforms (van Dijck et al., Citation2018) and platformization (Helmond, Citation2015). Recent work has also recognized the critical shaping influence platforms have over the industries they enter and the commodities they exchange. In the creative industries this has been referred to as the ‘platformization of cultural production’ (Nieborg & Poell, Citation2018, p. 4276).

The recorded music industry is commonly cited as the first cultural industry to have been disrupted by the twin forces of digitalization and the internet (Hesmondhalgh & Meier, Citation2018).Footnote1 Prominent music and cultural industry scholars have examined change and continuity in the digital music industry from various perspectives over the years (Baym, Citation2011; Leyshon, Citation2001; Morris, Citation2015; Rogers, Citation2013; Wikström, Citation2013). However, to-date there has been a lack of empirical research into how streaming platforms might be influencing the structure of the industry: in particular, the balance of power between major and independent (‘indie’) record labels. Moreover, there has also been little research on how changes in consumption habits precipitated by streaming – such as the much-discussed shift from albums to playlists – may be influencing this balance (though see Aguiar & Waldfogel, Citation2018).

In what follows, we examine the intermediary role of the leading audio streaming platform – Spotify. Spotify is often called the ‘new radio’ for the influence it has on breaking new songs and artists, and for the important role it plays in music discovery and consumption (Peoples, Citation2015; Resnikoff, Citation2016). Our purpose is to determine whether Spotify is leveling the playing field or entrenching hierarchies between major labels and independent labels. We attempt to answer this question through a longitudinal study of content owners (major labels or ‘indies’) and formats (albums, tracks, or playlists) promoted by Spotify through its global Twitter account: @Spotify. By using @Spotify as a proxy through which to track patterns of promotion between the years 2012 and 2018, this paper offers a novel empirical examination of how Spotify is shaping the consumption of music, and in turn the structure of the recording industry. In doing so we provide evidence for speculating about the future of the recorded music industry, and the cultural industries more generally, in a ‘platform society’ (van Dijck et al., Citation2018).

Background context

For much of the twentieth century, broadcast radio was the dominant vehicle through which popular recording musicians reached their audience and listeners discovered new music. While video and television had become key promotional media by the 1990s, ‘it has largely been radio play’, wrote Keith Negus in his classic Producing Pop (Citation1992,, p. 101), ‘which has encouraged retailers to stock recordings and consumers to purchase them.’ However, much of the music that found its way onto the airwaves and into the stores has been music owned and distributed by the major label system. The major record groups – currently Universal Music Group, Sony Music Entertainment, and Warner Music Group – have long dominated commercial radio – a legacy of payola, radio’s risk averse programing practices, and the high costs of ‘plugging’ records. While college radio stations and public broadcasters continue to expose listeners to a much more diverse array of artists and styles, independent musicians and record labels (or ‘indies’) have faced a considerable structural disadvantage in promoting their content through commercial radio (Hendy, Citation2000; Kruse, Citation2003).

As a result, although indies account for the vast majority of employment and music releases (WIN, Citation2018), as one US study concluded, independent labels ‘are left to vie for mere slivers of (radio) airtime’ (Thomson, Citation2009). This structural disadvantage and resulting imbalance has long been a matter of significant concern for scholars (Chapple & Garofalo, Citation1977; Malm & Wallis, Citation1984). While we should not exaggerate conflict between the majors and indies, nor accept uncritically ‘the romance of independence’ (Negus, Citation1992, p. 16), independent labels have played a crucial role in the history of recorded music (Chapple & Garofalo, Citation1977). Indies are considered the source of musical innovation and disruption, as they are ‘supposedly more in touch with the rapid turnover of styles and sounds characteristic of popular music at its best’ (Hesmondhalgh, Citation1999, p. 35).

With the rise of digital content distribution and listening models, some predicted the arrival of a new era, when artists could connect directly with listeners and independent record companies could compete more equitably with major labels (Lam & Tan, Citation2001). Soon, however, a host of new aggregators, online retailers and platforms managed to insert themselves in between musicians and their fans (Galuszka, Citation2015; Prey, Citation2015). Music industry scholars have described this as a process of ‘reintermediation’ (Leyshon, Citation2014; Young & Collins, Citation2010).

Audio streaming platforms have since become a mainstream means through which to consume music in many parts of the world (IFPI, Citation2019).Footnote2 With the rise in popularity of streaming, there is a growing body of research that explores the impact of streaming platforms on artists (Marshall, Citation2015), the economics of the music industry (Nordgård, Citation2016), taste (Webster, Citation2019) and recorded music itself (Negus, Citation2019). There has also been much speculation in academic and industry circles over what this shift in music consumption means for the distribution of power between the major record labels, independent labels, and their artists (Baym, Citation2011; Burkart, Citation2014; Marshall, Citation2015; Wikström, Citation2013; WIN, Citation2018). For some, the promise of streaming is that it frees music distribution and discovery from the stranglehold of the major labels – giving more space to independent artists and independent record labels as listeners explore the ‘long tail’ of a platform’s catalogue (Anderson, Citation2007).

More recently, there has been increased attention on how streaming platforms are utilizing their editorial capacity to transform the industries they intermediate (Morris & Powers, Citation2015). Much of this attention has been on Spotify and its promotion of playlists (Bonini & Gandini, Citation2019). While listeners, record labels, brands and other third parties can all create their own playlists on Spotify, Spotify-owned playlists are the most visible and most followed playlists on the platform. The 35 most followed playlists on Spotify (as of January 2019) are all Spotify-owned playlists; as are 99 of the top 100 playlists. The top Spotify-owned playlist – the algorithmically generated ‘Today’s Top Hits’ has a larger audience than any US radio station (Music Business Worldwide, Citation2018). In turn, research has confirmed the crucial importance of Spotify-owned playlists on artists’ careers (Aguiar & Waldfogel, Citation2018).

Spotify claims that the growing visibility and importance of its own playlists is a natural outgrowth of its data-driven, listener-centred model (United States Securities and Exchange Commission, Citation2018). Critics, however, see it otherwise. They point to design decisions – visible through Spotify’s interface – which serve to promote Spotify-owned playlists, while demoting third party playlists and other formats such as albums and tracks (Packer, Citation2016; Pelly, Citation2017). Scholars have pointed out that by unbundling the recording industry’s primary sales format – the album – and re-bundling content in the form of playlists, Spotify assumes control over the way music is consumed (Bonini & Gandini, Citation2019).

Despite the importance of this topic to the music industry ecosystem, to-date there have been few empirical studies exploring whether – or how – streaming platforms are using their central intermediary role. Are platforms like Spotify driving listeners to their editorial content (ie. playlists)? In turn, how might this be impacting the balance of power between majors and indies? There has been little research assessing whether platforms use their own playlists to promote more content from major labels or from independent labels, and whether or not this has changed over the previous years.

For this project, we were interested in tracking and examining continuities and changes in both the proportion of major to indie label content and the format of the content (albums, tracks, or playlists) that Spotify promotes. However, this type of analysis is difficult to do through the Spotify platform itself – both because the platform is personalized for each user and because Spotify does not provide an archive of tracks, albums or playlists that have been uploaded, deleted, or altered over the years. To solve this problem, we needed to identify a proxy that could help us to identify broader historical patterns in the promotion of content owners and formats. We selected Spotify’s global Twitter account – @Spotify – for this purpose.

Twitter as a proxy

As both a corporation and a content platform, Spotify presents itself and promotes its content through various channels not limited to its own platform. This includes the company’s global Twitter account (@Spotify). Although the original idea of Twitter was to provide personal status updates, it quickly became a marketing communication channel (Vargo, Citation2016). Spotify was an early bird in the microblogging Twittersphere. It joined the platform in November 2008, only a year and a half after the launch of Twitter. As of April 2020, the Twitter account @Spotify has 3.4M followers. Furthermore, since 2008 @Spotify has tweeted 31.3 K tweets; demonstrating the company’s clear interest in the Twittersphere, both as a marketing communication channel and as a strategic space to engage with the music community.Footnote3

Twitter’s leading position on the web gives the company a key brokerage role in the networked communication flows affecting a wide range of human activities, from political campaigns (Tumasjan et al., Citation2011), to disaster responses (Houston et al., Citation2015). As a consequence, researchers have used Twitter data to study a wide range of computer-mediated communication aspects, such as the characteristics of influential users in social network sites (Dubois & Gaffney, Citation2014; Esteve Del Valle & Borge, Citation2018a), the interplay between social media and political polarization (Conover et al., Citation2011; Esteve Del Valle & Borge, Citation2018b), or the online behavior of journalists and politicians (Brems et al., Citation2017), among others.

Despite the massive use of Twitter by musicians, record labels, and music festival attendees, research using Twitter data as a proxy to study the music industry is still in its infancy. The bulk of research comes from the music information retrieval industry (MIR) community (Hauger et al., Citation2013; Moore et al., Citation2014; Farrahi et al., Citation2014; Zangerle et al., Citation2014). For example, Kim et al. (Citation2014) used the dataset #nowplaying to build a predictive model to study the association between the listening behavior of Twitter users and Billboard rankings. Their results show that the number of daily tweets about a specific song and artist is predictive of Billboard rankings, thus revealing that music listening behavior on Twitter is positively associated with general music trends. However, while previous research has shown the potential of using Twitter data to study a wide range of computer-mediated communication aspects affecting multiple societal actors (politicians, companies, journalists, etc), research using Twitter data to better understand the changing music industry is (unexpectedly) still very slim. Furthermore, we are not aware of any study attempting to use Twitter as a proxy to understand platform intermediation.

In this research, Spotify’s global Twitter account is used not only as an object of study, but as both a data source and as a method. In so doing, we follow Rogers’ digital methods approach (Citation2009, Citation2013) which uses the epistemology of the internet – its online groundedness – as methodological basis ‘in an effort to conceptualize research which follows the medium, captures its dynamics, and makes grounded claims about cultural and societal change’ (Rogers, Citation2009, p. 8).Footnote4 In this way we use the data collected from @Spotify as a proxy to make sense of Spotify’s intermediary role in the music industry. In the next section, we elaborate on how we use Twitter data from Spotify’s global Twitter account (@Spotify) as a proxy to track patterns in both the proportion of major to indie label content and the format of the content that Spotify promotes over a longer period of time.

Methods

Testing @Spotify as a proxy for Spotify

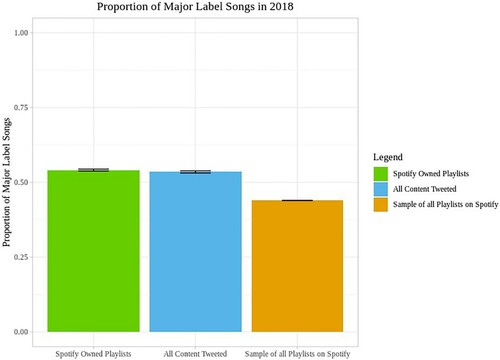

In order to test whether Spotify’s Twitter account is a good proxy, we gathered two large random samples of playlists from Spotify that were available on the platform in the final year of our data collection (2018). The first sample was a random set of 500 Spotify-owned playlists (i.e., playlists curated by Spotify). The second dataset of 1001 playlists was a random sample of all the playlists that were available on the Spotify platform in 2018: it included playlists curated by listeners, by record labels, by artists and other third parties, as well as by Spotify.Footnote5 Both samples were large enough to have sufficient statistical power to be able to compare them to the share of major label content in the playlists that were promoted on Spotify’s global Twitter account in 2018 (see ).

Table 1. Descriptive statistics of playlists from Spotify.

We started by classifying the record labels in our datasets into two categories: major labels and independent labels. This was not an easy methodological step: While ‘indie’ has long been a poorly defined construct (Fonarow, Citation2006; Hesmondhalgh, Citation1999), the dividing line between major and independent record labels has only become more blurred in recent years (Galuszka & Wyrzykowska, Citation2018). In the physical era, a major label distribution deal would have – for many – disqualified a label from defining themselves as ‘indie’ (see Fonarow, Citation2006). Today, the criteria of independent distribution is more difficult to apply as music is distributed through multiple channels and involves aggregators that are sometimes owned by a major record label (Galuszka & Wyrzykowska, Citation2018).

Following the rationale of the Worldwide Independent Network (WIN) which states that ‘measuring music industry market share by copyright ownership continues to be the most legitimate method’Footnote6 we decided to use copyright ownership of a track – instead of distributor – to categorize tracks. To do so we created a list of all the record labels owned by one of the ‘Big Three’ major record companies: Universal, Warner, and Sony. We then queried the names of these three major record companies in the labels retrieved from the Spotify playlists and created a dummy variable which indicated if a song belonged to a major record company (1) or not (0).

Next we compared the sample of 500 Spotify-owned playlists to the content that Spotify promoted through its global Twitter account in 2018. Our reasoning was that Spotify’s Twitter account could be used as an effective proxy to identify changes over time if the major-indie label proportion of content in the Spotify playlists and other content promoted through @Spotify in 2018 was similar to the proportion in the sample taken from Spotify in that same year.

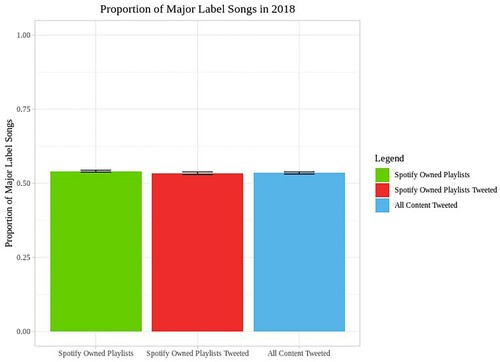

In (below) we can see that our sample of 500 random Spotify-owned playlists contains a percentage of major label content of 54.1%, which is very close to the percentage of major label content on the Spotify-owned playlists that Spotify promoted through its global Twitter account (53.41%) in 2018. Furthermore, when we compare the major label proportion in these 500 playlists to all the content that Spotify promoted through Twitter (including albums, tracks and playlists) that same year, we see that major label content makes up 53.49% of this content. Again, this is nearly identical to the percentage of major label content found on Spotify-owned playlists promoted through @Spotify and to the percentage found on the 500 Spotify playlists randomly collected from the platform in 2018. This therefore confirmed our expectation that @Spotify provides an effective proxy to understand Spotify’s historical patterns of promotion.

Figure 1. Proportion of major label songs in sample of Spotify-owned playlists, tweeted Spotify-owned playlists, and all content tweeted by Spotify in 2018.

Scraping Twitter

As we now had confidence in using @Spotify as a proxy to track changes over time, we began to scrape the @Spotify account from 1 January 2012 and 31 December 2018.Footnote7 Spotify promotes playlists, albums, tracks, extended plays, podcasts, artists, videos, and concerts via its @Spotify account. We decided to only analyze tweets that promoted playlists, albums and tracks as these were the main formats, and because we were interested in contributing to debates about whether Spotify is actively pushing listeners towards consuming music through playlists (Hu, Citation2018; Iqbal, Citation2019).

We employed the Python script ‘Twitterscraper’Footnote8 to scrape the tweets from Spotify’s global Twitter account. In total we collected 5,624 tweets (2012–2018). We extracted from the content of these tweets the links to the Spotify albums, tracks and playlists.Footnote9 Using Python software we extracted the format that a link contained (an album, a track or a playlist) and the identification number in the link.Footnote10 We then utilized the identification number to extract the data from the Spotify Application Programming Interface (API).Footnote11

Next, we preprocessed the data retrieved from the @Spotify account. First, we recategorized as ‘tracks’ a few ‘albums’ that contained only one song. Second, following the regulations established by the Recording Academy for the Grammy Awards – which mandates that an ‘album’ contains at least 5 tracks (The Recording Academy, Citation2016) – we filtered out all albums with less than 5 tracks.

Results

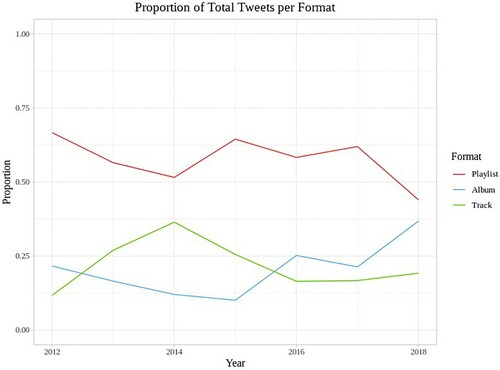

We were first interested in determining the format that Spotify promotes most often through its Twitter account. After collecting every tweet promoting albums, tracks and playlists from the beginning of 2012 until the end of 2018, it became clear that @Spotify promotes playlists more heavily than it does both albums and individual tracks (see and ).

Figure 2. Proportion of total tweets on Spotify’s global Twitter account @Spotify per format in the years 2012–2018.

Table 2. Descriptive statistics of data promoted on Spotify’s global Twitter account (2012–2018).

For Spotify listeners this is likely not surprising. Upon logging in to Spotify one immediately encounters a wide selection of playlists. Indeed, the playlist has become the central form of music curation on Spotify (Prey, Citationin press). However, previous studies and reports have tended to frame this as a gradual and inevitable ‘progression of music consumption trends’ whereby ‘playlists are becoming more and more dominant in the music industry as streaming services gain traction’ (‘Playlists Overtake … ’, Citation2016). Spotify too claims that it is just following listeners: that the growing centrality of its own playlists is a natural outgrowth of its data-driven, listener-centred model (United States Securities and Exchange Commission, Citation2018).

However, our study complicates this simple story of the rise of the playlist. Our analysis of @Spotify shows that Spotify has been actively and consistently promoting playlists over other ways of consuming music at least since 2012. Rather than a gradual move towards playlists, Spotify has been heavily promoting the playlist format on Twitter during the entire seven-year period that we analyzed. Spotify thus appears to be leading rather than merely following listeners. Spotify’s own data further supports this point: Playlist consumption accounts for just over 30 percent of listening time on the platform (United States Securities and Exchange Commission, Citation2018) while on @Spotify, well over 50% of tweets have promoted playlists.

However, in the final year of our analysis (2018) the percentage of tweets promoting playlists suddenly dipped below 50% for the first time, while the percentage of tweets promoting albums grew to almost 37%. It remains to be seen whether we are entering a ‘post-playlist’ era, as some commentators have speculated (Hu, Citation2018), or if this is just a brief respite in the slow death of the album (Negus, Citation2015).

While it is clear that Spotify has promoted playlists more heavily over this period, we were also interested in determining who the curators or owners of these playlists are. Are these mainly Spotify-owned playlists or are they playlists curated by third parties – such as the major record labels? This brings us to our next question: Whose playlists does Spotify promote through its Twitter account?

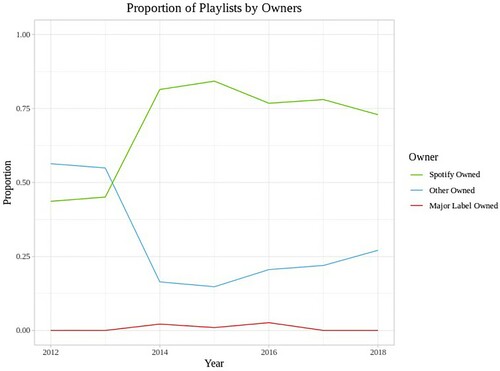

Perhaps not surprisingly, the results of our analysis of all the playlists promoted through @Spotify between the years 2012–2018 shows a clear preference for playlists created by Spotify over third-party playlists (see below).

Figure 3. Curators or owners of playlists promoted on Spotify’s global Twitter account @Spotify from 2012 until 2018.

However, the promotion of Spotify-owned playlists appears to have not always been a strategic priority for the company. Prior to 2014 Spotify promoted playlists by third parties more often than their own playlists. Furthermore, the shift towards promoting Spotify-owned playlists appears to be the result of a sudden change in strategy rather than a gradual transition. Our Twitter data shows that sometime in 2014 Spotify began to heavily promote its own playlists in place of third-party playlists.

Interestingly, this transition followed a key purchase: In 2013, Spotify acquired a playlist curation startup called ‘Tunigo’. For the authors of Spotify Teardown (Citation2019) this marks the beginning of Spotify’s ‘curatorial turn’ (Eriksson et al., Citation2019, p. 61). While Spotify Teardown describes how this strategic turn to curation was implemented over a period of years as Spotify began filling globally advertised positions for ‘Music Editor/Playlist Curator’, Spotify’s global Twitter account foreshadows this and provides us with a roadmap for what was to come. @Spotify reveals that already by 2014 Spotify had shifted from promoting playlists to promoting Spotify-owned playlists.

Of course, third parties have continued to build their own playlists on Spotify’s platform, and listeners have continued to listen to these playlists. Spotify revealed in its SEC filings that user-generated playlists accounted for approximately 36% of monthly content hours on the platform (United States Securities and Exchange Commission, Citation2018). Included in this category are playlists created by the major labels. Our interest in investigating how platform intermediaries such as Spotify may impact the dominance of the major label system resulted in our decision to separately analyze tweets promoting playlists curated by the three major labels. This revealed a point of significant interest: during the entire seven-year period that we analyzed, @Spotify has almost completely ignored playlists curated by Universal, Sony and Warner (see above).

Nevertheless, the fact that Spotify heavily promotes Spotify-owned playlists instead of, for example, major label-owned playlists – tells us nothing about the major-to-indie proportion of these playlists. Spotify-owned playlists contain a mix of major label artists and independent artists. Therefore, we were interested in determining who owns the content that makes up the playlists, albums, and individual tracks that Spotify promotes through @Spotify. While we had already looked at Spotify tweets for 2018 in order to test our use of Twitter as a proxy, we wanted to see if there have been any changes in the proportion of major to indie label content that has been promoted since 2012.

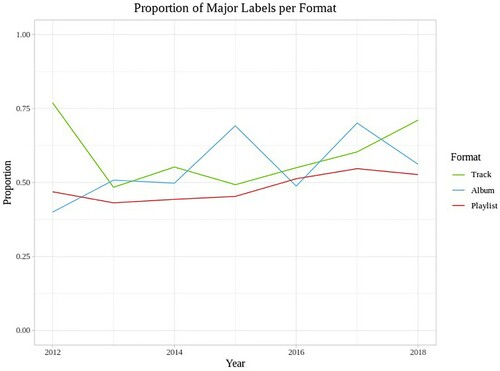

The graph below (see ) provides a somewhat more complicated picture of trends in the promotion of major label content over the years 2012–2018. While there has been a gradual increase in the percentage of major label content on the playlists tweeted through @Spotify, and of major label tracks since 2015, the promotion of major label albums has fluctuated significantly over this time period. Still, in recent years there appears to be a positive trend in the promotion of major label content through all three formats.

Figure 4. Proportion of major label content per format promoted on Spotify’s global Twitter account @Spotify (2012–2018).

When we compare both the collected tweets and our sample of 500 Spotify playlists to our random sample of 1001 Spotify playlists (which includes playlists curated by listeners, by record labels, by artists and other third parties, as well as by Spotify) – we find that this random sample of all playlists has a significantly lower percentage of major label content. Indeed, only 43.93% of the content on these playlists is content owned by one of the major record companies (See below). Again, the percentage of major label content on the Spotify-owned playlists was 54.1%, and 53.49% of all the content tweeted by @Spotify was major label content. Whether this indicates that Spotify as a ‘gatekeeper’ is helping the major label system to maintain their historical dominance, or if this signifies a shift towards more promotional parity between majors and indies is a more complicated question that we will discuss below.

Figure 5. Proportions of major label songs in random sample of Spotify-owned playlists, all content tweeted, and a random sample of all the playlists on Spotify from 2018.

Discussion

As a sociotechnical feature common to many platforms, playlists reveal the politics of ‘selection’ (van Dijck et al., Citation2018) – a key mechanism through which platforms such as Spotify attempt to create platform dependence. For musicians and record labels, there is a growing dependency on Spotify-owned playlists (Iqbal, Citation2019). Research has confirmed the crucial importance of Spotify-owned playlists for artists’ careers (Aguiar & Waldfogel, Citation2018).

However, rumblings of discontent are emerging as the major record labels become increasingly dependent on Spotify-owned playlists. According to a report published by Deutsche Bank, the three major labels are ‘upset’ with the share of major label content that Spotify is including in its curated playlists (Sandoval, Citation2018). While the report is not clear about precisely what this share is, and what the major labels would consider to be a ‘fair’ share, our analysis of Twitter research provides some interesting insights. Slightly more than 50% of the content of the playlists that Spotify promotes through @Spotify, and over 50% of our random sample of all Spotify-owned playlists available in 2018 is content owned by major record labels. This is more major label content than is found in our sample of all playlists available on Spotify in 2018: just over 40% of the content on this random list of playlists is content owned by one of the major record companies. This seems to indicate that Spotify exhibits a bias towards major label content, relative to what listeners and other third parties are promoting through the playlists they create.

However, perhaps this is not the right comparison to make. We get a very different picture if we instead compare the percentage of major label content on Spotify-owned playlists and tweeted content to the major labels’ dominance of radio (consistently over 80 percent according to one multi-year US study – see Thomson, Citation2009), or to Sony, Universal and Warner’s combined 69.2 percent market share of global recorded music revenues in 2018 (Mulligan, Citation2019). Indeed, one source quoted in the Deutsche Bank report complained that ‘the major labels stand to marginally lose share’ because of Spotify-owned playlists (Sandoval, Citation2018). This is because, in comparison to commercial radio playlists and record store retail space, Spotify-owned playlists leave considerably more room for independent label content. What is more, the three major record companies have put considerable effort into building their own playlists brands through which to promote their roster. Yet, as discussed in the Results section, these playlists have been almost invisible on Spotify’s global Twitter account, receiving almost no promotion during the period of our analysis.

Thus, while Spotify is often called the ‘new radio’ for the influence it has on breaking new songs and artists, and for the important role it plays in music discovery and consumption, this study suggests that Spotify is proving to be a more difficult medium than commercial radio for the major labels to push their content through. Whether this means that Spotify is leveling the playing field and making it easier for independent record labels to get their music out is another question. However, there is some evidence that the shift towards streaming has benefited independent labels: A recent report reveals considerable gain in market share by the independent music sector in relation to the major labels (WIN, Citation2018).

Nevertheless, as our collection and analysis of Spotify tweets has revealed, the major label share of all the content promoted through @Spotify has increased since 2012. It is here that we can most clearly see the advantage of using Twitter as a proxy to reveal longitudinal trends. Our Twitter data seems to indicate a gradual ‘return’ of the major labels over the past seven years. While Spotify appears to be leveling the playing field in comparison to commercial radio, we should not assume that this trend will continue into the future.

This may be because – while artists and labels are increasingly dependent on Spotify – Spotify at the same time remains heavily dependent on the three major label groups. While Netflix is often cited as a model for Spotify to follow, the recorded music industry is much more consolidated than the television industry. If the largest major – Universal Music Group – decided to remove its content from Spotify, or to refuse to grant it a license to use its content in new markets, the platform would be in serious trouble. As Spotify admits in the ‘Risks Related to Our Business’ section of its 2018 SEC filings:

… If we fail to obtain these licenses, the size and quality of our catalog may be materially impacted and our business, operating results, and financial condition could be materially harmed. (United States Securities and Exchange Commission, Citation2018, p. 15)

However, while Spotify may be feeling pressure from the major labels to promote more of their content, they are at the same time being pressured by financial investors to reduce their content costs. The bulk of Spotify’s revenues are paid to rights holders – most prominently, record labels. Reports suggest that the major labels (Universal, Warner & Sony) receive between 52% and 54% of the net revenue generated by their artists on the platform, while independent record labels are paid between 50% and 52% (Ingham, Citation2018a; Sandoval, Citation2018). One result of these high content costs is Spotify is struggling to achieve profitability. In the decade that it has been around, Spotify has been kept alive by venture capital and investors. However, these investors, as industry analyst Mark Mulligan (Citation2018, para.5) puts it, ‘are investing in the potential upside on a future industry changer, not a present-day industry defender.’ In other words, they are investing in dis-intermediation – in a business model which reduces, or eliminates entirely, the need to rely on content from the traditional recorded music industry.

To attract financial capital, platforms such as Spotify must attempt to transform themselves from distributors of content to producers of a unique service (see Eriksson et al., Citation2019, p. 61). Spotify-owned playlists are a central part of this strategy. By unbundling the recording industry’s primary sales format – the album – and re-bundling content in the form of playlists, Spotify assumes control over the way music is consumed. Indeed, Spotify founder and CEO Daniel Ek boasted to investors that the fact that users increasingly turn to Spotify playlists for music, is ‘a massive transformation’ that ‘puts Spotify in control of the demand curve’ (Spotify Investors, Citation2018). Playlists are thus an example of how a multi-sided platform like Spotify employs ‘curatorial power’ to advance its own interests (see Prey, Citationin press).

In recent years, Spotify has made strategic attempts to reduce its reliance on record labels – both major and independent. One controversial example has been Spotify’s use of ‘fake artists’. In the summer of 2016, Music Business Worldwide reported that Spotify was paying producers a flat fee to create tracks under fake names (Ingham, Citation2016). This content was being produced in order to fill out Spotify-owned playlists and thus reduce royalty payments to record labels. All of these tracks were found on Spotify mood playlists such as ‘Peaceful Piano’, ‘Deep Focus’ and ‘Ambient Chill’, where they generated ‘hundreds of thousands or, in many cases, millions of streams'‘ (Ingham, Citation2018b). A former Spotify insider was quoted in Variety as calling the practice ‘one of a number of internal initiatives to lower the royalties [Spotify is] paying to the major labels’ (Trakin & Aswad, Citation2017).Footnote12 As Bonini and Gandini (Citation2019, p. 8) correctly point out, power struggles between competing actors are ‘coded in’ to the playlist format.

Looking towards the future, one possibility is that Spotify will use its own playlists to steadily increase the presence of unsigned artists – or even so-called ‘fake artists’ – on its platform. However, another possibility is just as likely: that the share of major label content promoted through Spotify playlists will continue to rise to reflect increasing pressure from the major record labels. At the time of writing, Spotify is at the negotiating table with each of the three major record labels to decide on new royalty rates. While it is interesting to speculate on the results that these negotiations may have on the content and the formats that Spotify promotes, we leave the empirical examination of these possibilities open for future study.Footnote13

Conclusion

Content platforms like Spotify can be compared to Heraclitus’ river: one can never access the same platform twice. Constantly in flux from one moment to the next, Spotify churns in motion as tracks, albums and playlists are added, deleted and reconfigured. This presents researchers with a conundrum: Any analysis of the platform itself will necessarily be an analysis of the present. Spotify does not provide an archive of songs that were uploaded in 2009, or playlists that disappeared in 2019.

To solve this problem, we decided to use a proxy that could help us to identify broader historical patterns in the promotion of content and formats. We selected Spotify’s global Twitter account – @Spotify – for this purpose. It is important to point out that we are not making any claims about any effects that Spotify’s promotional tweets may have on music consumption. Instead, we argue that – as a carefully curated venue for corporate speech – @Spotify provides a window into continuities and changes in Spotify’s corporate strategy, and what we could call platform politics of selection (van Dijck et al., Citation2018).

This study determined that Spotify has been heavily promoting the playlist format since at least 2012. Spotify thus appears to be actively pushing listeners to consume music through playlists in place of other formats. Moreover, Spotify is using its editorial capacity to promote its own playlists over playlists created by the major labels and other third parties. While Spotify-owned playlists have a higher share of major label content than do playlists created by third parties, there is comparatively more room for independent music on Spotify playlists than on commercial radio playlists. Nevertheless, the major label proportion of all the content that Spotify has promoted through its global Twitter account has gradually increased in recent years. Research should investigate if this trend continues into the future.

While there is considerable debate over the meaning of the ‘indie’ moniker in a digital music world (Hesmondhalgh & Meier, Citation2014), there is also widespread recognition of the continued crucial role of independent production across the cultural industries (Bennett et al., Citation2013). Our findings are therefore not only of interest to music industry scholars. From journalism to video games to film, media content is increasingly finding audiences and advertisers on and via digital platforms (Nieborg & Poell, Citation2018). This process of ‘platformization’ (Helmond, Citation2015) appears to fundamentally transform the organization of cultural production, distribution and marketing. Spotify in particular appears to have become ‘a model for other services that use digital technology to transform the distribution of cultural goods’ (Vonderau, Citation2019, p. 4). Thus, this study has implications that extend beyond the music industry to other industries impacted by platform intermediation.

In turn, the use of Twitter as a proxy provides researchers with a window through which to witness unfolding transformations between platforms and the industries they intermediate. It can help reveal broader transformations in power relations within cultural industries, such as the recorded music industry, with important implications for cultural producers – and for culture – in a platform society.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Robert Prey

Robert Prey is an Assistant Professor at the Center for Media and Journalism Studies, University of Groningen, the Netherlands. He researches the relationship between technology, capitalism and culture. His current focus is on algorithmic recommendation systems and the interdependent processes of ‘datafication’ and ‘platformization’; in particular as they relate to music streaming platforms and the music, musicians and industry developing around them.

Marc Esteve Del Valle

Marc Esteve Del Valle is an Assistant Professor in the Centre for Media and Journalism Studies at the University of Groningen. His research and teaching interests explore the intersection between new media and social networks. The main focus of his research is on networked politics. His secondary area of research is on e-learning, especially the study of political learning processes taking place on social networking sites. More recently, he has turned to focus on understanding the relations between digital media and the public sphere.

Leslie Zwerwer

Leslie Zwerwer is a data science consultant at the Center for Information Technology, University of Groningen. She holds degrees in both Mathematics and Psychology.

Notes

1 In the decade and a half since the emergence of Napster and P2P file sharing, the global recording industry declined by 40%, from $23.8 billion in 1999 to $14.3 billion in 2014 (IFPI, Citation2019).

2 Streaming has been credited with reversing the declining fortunes of record labels. By 2018, global recorded music revenues reached $19.1 billion, becoming the largest revenue source for the global recording industry (IFPI, Citation2019).

3 A conversation one of the authors had with a Spotify Head of Content in 2019 confirmed that Spotify employs a social media team for each of its Twitter accounts. This team first decides on what to tweet and then passes these decisions on to superiors who make the final decision and offer suggestions.

4 Our gratitude to one of this paper’s reviewers for pointing this out.

5 These datasets were acquired from Chartmetric – a US-based music analytics company which collects a real-time record of playlists through Spotify’s API (see https://www.chartmetric.com/). Chartmetric provided the researchers with a random selection of playlists that appeared on Spotify in 2018. The datasets included information such as the name of each playlist, total followers, and copyright owners (ie. record label) of each track on each playlist.

6 This rationale is based on a determination of the relative risk involved: ‘distribution is interchangeable and involves only a modicum of risk, whereas investing in the creation of a copyright in the first place is the biggest risk that any artist or music entrepreneur can take’ (WIN, Citation2018, p. 7).

7 Unfortunately, technical limitations impeded us from scraping data before 2012.

8 Available at https://github.com/taspinar/twitterscraper

9 Tweets that did not mention any Spotify link were left out of the analysis.

10 For example https://open.spotify.com/playlist/37i9dQZF1DX0LpVh8OqcuH?si=PzZmbg4NRGqkt9PHxAPdmw contains a playlist with identification number 37i9dQZF1DX0LpVh8OqcuH.

11 Each format had a different data structure. To be able to parse it into one data frame we used different functions for each format.

12 Further evidence for this strategy emerged when Billboard reported in the summer of 2018 that the streaming platform was offering significant advances to a number of independent artists if they would license their music directly to Spotify (Karp, Citation2018). By paying the artist directly Spotify would be able to improve its margins, while the artist would receive much more per stream than they would if signed to a major label.

13 As one reviewer suggested, it would be very insightful to study Spotify’s Twitter behavior during previous periods of negotiations with record labels, and other major events, to assess potential impact on Spotify’s promotional decisions. While this is beyond the scope of the present paper, we hope to pursue this idea in the future.

References

- Aguiar, L., & Waldfogel, J. (2018). Platforms, promotion, and product discovery: Evidence from spotify playlists (No. w24713). National Bureau of Economic Research.

- Anderson, C. (2007). The long tail: How endless choice is creating unlimited demand. Random House.

- Baym, N. K. (2011). The Swedish model: Balancing markets and gifts in the music industry. Popular Communication, 9(1), 22–38. https://doi.org/https://doi.org/10.1080/15405702.2011.536680

- Bennett, J., Kerr, P., & Strange, N. (2013). Cowboys or indies? 30 years of the television and digital independent public service production sector. Critical Studies in Television: The International Journal of Television Studies, 8(1), 108–130. https://doi.org/https://doi.org/10.7227/CST.8.1.9

- Bonini, T., & Gandini, A. (2019). “First week is editorial, second week is algorithmic”: platform gatekeepers and the platformization of music curation. Social Media+Society, 5(4), 1–11. https://doi.org/https://doi.org/10.1177/2056305119880006

- Brems, C., Temmerman, M., Graham, T., & Broersma, M. (2017). Personal branding on Twitter. Digital Journalism, 5(4), 443–459. https://doi.org/https://doi.org/10.1080/21670811.2016.1176534

- Burkart, P. (2014). Music in the cloud and the digital sublime. Popular Music and Society, 37(4), 393–407. https://doi.org/https://doi.org/10.1080/03007766.2013.810853

- Chapple, S., & Garofalo, R. (1977). Rock ‘n’ roll is here to pay: The history and politics of the music industry. Burnham Inc Pub.

- Conover, M., Ratkiewicz, J., Francisco, M., & Gonçalves, B. (2011). Political polarization on Twitter. In Proceedings of the fifth International AAAI Conference on Weblogs and Social Media (pp. 89–96). Barcelona, Spain: Association for the Advancement of Artificial Intelligence.

- Dubois, E., & Gaffney, D. (2014). The multiple facets of influence. American Behavioral Scientist, 58(10), 1260–1277. https://doi.org/https://doi.org/10.1177/0002764214527088

- Eriksson, M., Fleischer, R., Johansson, A., Snickars, P., & Vonderau, P. (2019). Spotify teardown: Inside the black box of streaming music. Mit Press.

- Esteve Del Valle, M., & Borge, R. (2018a). Leaders or brokers? Potential influencers in online parliamentary networks. Policy & Internet, 10(1), 61–86.

- Esteve Del Valle, M., & Borge Bravo, R. (2018b). Echo chambers in parliamentary Twitter networks: the Catalan case. International Journal of Communication, 12, 1715–1735.

- Farrahi, K., Schedl, M., Vall, A., Hauger, D., & Tkalcic, M. (2014). Impact of listening behavior on music recommendation. ISMIR.

- Fonarow, W. (2006). Empire of Dirt: The aesthetics and Rituals of British indie music. Wesleyan University Press.

- Galuszka, P. (2015). Music aggregators and intermediation of the digital music market. International Journal of Communication, 9, 20.

- Galuszka, P., & Wyrzykowska, K. M. (2018). Rethinking independence: What does ‘independent record label’ mean today? In E. Mazierska, L. Gillon, & T. Rigg (Eds.), Popular music in the post-digital age: Politics, economy, culture and technology (pp. 33–50). New York: Bloomsbury Publishing.

- Gillespie, T. (2010). The politics of ‘platforms’. New Media & Society, 12(3), 347–364. https://doi.org/https://doi.org/10.1177/1461444809342738

- Hauger, D., Kepler, J., Schedl, M., Košir, A., & Tkalcic, M. (2013). The million musical tweets dataset: What can we learn from microblogs. In Proceedings of the 14th International Society for Music Information Retrieval Conference (ISMIR), Curitiba, Brazil.

- Helmond, A. (2015). The platformization of the web: Making web data platform ready. Social Media+Society, 1(2), 1–11. https://doi.org/https://doi.org/10.1177/2056305115603080

- Hendy, D. (2000). Pop music radio in the public service: BBC radio 1 and new music in the 1990s. Media, Culture & Society, 22(6), 743–761. https://doi.org/https://doi.org/10.1177/016344300022006003

- Hesmondhalgh, D. (1999). Indie: The institutional politics and aesthetics of a popular music genre. Cultural Studies, 13(1), 34–61. https://doi.org/https://doi.org/10.1080/095023899335365

- Hesmondhalgh, D., & Meier, L. M. (2014). Popular music, independence and the concept of the alternative in contemporary capitalism. In J. Bennett & N. Strange (Eds.), Media independence: Working with freedom or working for free? (pp. 94–116). Routledge.

- Hesmondhalgh, D., & Meier, L. M. (2018). What the digitalisation of music tells us about capitalism, culture and the power of the information technology sector. Information, Communication & Society, 21(11), 1555–1570. https://doi.org/https://doi.org/10.1080/1369118X.2017.1340498

- Houston, J., Hawthorne, J., Perreault, M., Park, E., Goldstein, H., Halliwell, M., & Griffith, S. (2015). Social media and disasters: A functional framework for social media use in disaster planning, response, and research. Disasters, 39(1), 1–22. https://doi.org/https://doi.org/10.1111/disa.12092

- Hu, C. (2018, November 16). Our new “post-playlist” reality. Retrieved December 18, 2019, from https://www.getrevue.co/profile/cheriehu42/issues/our-new-post-playlist-reality-138493

- IFPI. (2019, April 2). IFPI global music report 2019. Retrieved May 5, 2019, from https://www.ifpi.org/news/IFPI-GLOBAL-MUSIC-REPORT-2019

- Ingham, T. (2016, August 31). Spotify is making its own records … and putting them on playlists. Retrieved December 6, 2019, from https://www.musicbusinessworldwide.com/spotify-is-creating-its-own-recordings-and-putting-them-on-playlists/

- Ingham, T. (2018a, September 23). Spotify’s direct distribution deals: What do artists get paid? Retrieved December 5, 2019, from https://www.musicbusinessworldwide.com/spotifys-direct-distribution-deals-what-do-the-artists-get/

- Ingham, T. (2018b, August 2). Fake artists still dominate Spotify ‘chill’ playlists. Now Universal is fighting back … with Apple Music. Retrieved December 6, 2019, from https://www.musicbusinessworldwide.com/fake-artists-still-dominate-spotifys-chill-playlists-now-real-artists-are-fighting-back-with-apple-music/

- Ingham, T. (2018c, August 14). Spotify is on a collision course with the major record companies. Here’s why. Retrieved December 6, 2019, from https://www.musicbusinessworldwide.com/spotify-is-on-a-road-to-collision-with-the-record-industry-heres-why/

- Iqbal, N. (2019, April 28). Forget the DJs: Spotify playlists are the new musical starmakers. Retrieved May 6, 2019, from https://www.theguardian.com/music/2019/apr/28/streaming-music-algorithms-spotify

- Karp, H. (2018, June 06). Spotify offers managers, artists advances to license music directly to its streaming service: Exclusive. Retrieved May 6, 2019, from https://www.billboard.com/articles/business/8459616/spotify-offers-managers-artists-advances-license-music-directly-exclusive

- Kim, Y., Suh, B., & Lee, K. (2014). #nowplaying the future billboard: mining music listening behaviors of twitter users for hit song prediction. SoMeRA '14.

- Kruse, H. (2003). Site and sound: understanding independent music Scenes. Peter Lang.

- Lam, C. K., & Tan, B. C. (2001). The internet is changing the music industry. Communications of the ACM, 44(8), 62–68. https://doi.org/https://doi.org/10.1145/381641.381658

- Leyshon, A. (2001). Time–space (and digital) compression: Software formats, musical networks, and the reorganisation of the music industry. Environment and Planning A: Economy and Space, 33(1), 49–77. https://doi.org/https://doi.org/10.1068/a3360

- Leyshon, A. (2014). Reformatted: Code, Networks, and the transformation of the music industry. Oxford University Press.

- Malm, K., & Wallis, R. (1984). Big sounds from small peoples: The music industry in small countries. Constable.

- Marshall, L. (2015). ‘Let’s keep music special. F—spotify’: On-demand streaming and the controversy over artist royalties. Creative Industries Journal, 8(2), 177–189. https://doi.org/https://doi.org/10.1080/17510694.2015.1096618

- Moore, J. L., Joachims, T., & Turnbull, D. (2014). Taste space versus the world: An embedding analysis of listening habits and geography. ISMIR.

- Morris, J. W. (2015). Selling digital music, formatting culture. University of California Press.

- Morris, J. W., & Powers, D. (2015). Control, curation and musical experience in streaming music services. Creative Industries Journal, 8(2), 106–122. https://doi.org/https://doi.org/10.1080/17510694.2015.1090222

- Mulligan, M. (2018, June 12). Spotify’s new rules of engagement. Retrieved December 6, 2019, from https://www.midiaresearch.com/blog/spotifys-new-rules-of-engagement/

- Mulligan, M. (2019, March 13). Label market shares. Retrieved December 4, 2019, from http://www.midiaresearch.com/blog/2018-global-label-market-share-stream-engine/

- Music Business Worldwide. (2018, July 19). Want to get your track on a Spotify playlist? Join the queue … . Retrieved December 15, 2019, from https://www.musicbusinessworldwide.com/want-to-get-your-track-on-a-spotify-playlist-join-the-queue/

- Negus, K. (1992). Producing pop: Culture and conflict in the popular music industry. E. Arnold.

- Negus, K. (2015). Digital divisions and the changing cultures of the music industries (or, the ironies of the artefact and invisibility). Journal of Business Anthropology, 4(1), 151–157. https://doi.org/https://doi.org/10.22439/jba.v4i1.4793

- Negus, K. (2019). From creator to data: The post-record music industry and the digital conglomerates. Media, Culture & Society, 41(3), 367–384. https://doi.org/https://doi.org/10.1177/0163443718799395

- Nieborg, D. B., & Poell, T. (2018). The platformization of cultural production: Theorizing the contingent cultural commodity. New Media & Society, 20(11), 4275–4292. https://doi.org/https://doi.org/10.1177/1461444818769694

- Nordgård, D. (2016). Lessons from the world’s most advanced market for music streaming services. In P. Wikström & R. DeFillippi (Eds.), Business innovation and disruption in the music industry (pp. 175–190). Edward Elgar Publishing.

- Packer, T. (2016, November 29). Spotify’s march to monopolise playlists continues. The Daily Digest – Medium. Retrieved December 9, 2019, from https://medium.com/@ExtendedDigest/spotifys-march-to-monopolise-playlists-continues-5d27beb6ee2a

- Pelly, L. (2017, June 21). The secret lives of playlists. Retrieved May 6, 2019, from https://watt.cashmusic.org/writing/thesecretlivesofplaylists

- Peoples, G. (2015, July 8). What happens when spotify gets behind an artist? A case study of Hozier and Major Lazer. Retrieved June 25, 2017, from http://www.billboard.com/articles/business/6656722/spotify-spotlight-support-major-lazer-hozier

- Playlists Overtake Albums in Listenership, Says LOOP Study. (2016, September 22). Retrieved December 10, 2019, from https://musicbiz.org/news/playlists-overtake-albums-listenership-says-loop-study/

- Prey, R. (2015). “Now Playing. You”: Big data and the production of music streaming space (Doctoral dissertation). Communication, Art & Technology: School of Communication.

- Prey, R. (in press). Locating power in platformization: Music streaming playlists and curatorial power. Social Media + Society.

- The Recording Academy. (2016). Basic grammy guidelines. https://www.grammy.com/sites/com/files/59th_guidelines_quick_reference_guide.pdf

- Resnikoff, P. (2016, June 6). Spotify free is bigger than almost every American Radio Station. Retrieved June 24, 2017, from https://www.digitalmusicnews.com/2016/06/16/spotify-free-bigger-radio-stations/

- Rogers, J. (2013). The death and life of the music industry in the digital age. A&C Black.

- Rogers, R. (2009). The end of the virtual: Digital methods. Vossiuspers UvA.

- Rogers, R. (2013). Digital methods. MIT Press.

- Sandoval, G. (2018, July 12). The major music labels are upset that they don’t get more play on Spotify’s mega-popular playlists, says Deutsche Bank. Retrieved May 5, 2019, from https://www.businessinsider.nl/spotify-curated-playlists-labels-2018-7/?international=true&r=US

- Spotify Investors. (2018, March). Investor day - March 2018. https://investors.spotify.com/events/investor-day-march-2018/default.aspx

- Thomson, K. (2009, April 29). Same old song. Future of Music Coalition. https://futureofmusic.org/article/research/same-old-song

- Trakin, R., & Aswad, J. (2017, July 11). Spotify denies creating ‘fake artists,’ although multiple sources claim the practice is real. https://variety.com/2017/biz/news/spotify-denies-creating-fake-artists-although-multiple-sources-claim-the-practice-is-real-1202492307/

- Tumasjan, A., Sprenger, T., Sandner, P., & Welpe, I. (2011). Election forecasts with Twitter. Social Science Computer Review, 29(4), 402–418. https://doi.org/https://doi.org/10.1177/0894439310386557

- United States Securities and Exchange Commission. (2018, March 23). Form F-1 registration statement, spotify technology, S.A. Retrieved May 6, 2019, from https://www.sec.gov/Archives/edgar/data/1639920/000119312518092759/d494294df1a.htm

- van Dijck, J., Poell, T., & de Waal, M. (2018). The platform society: Public values in a connective world. Oxford University Press.

- Vargo, C. J. (2016). Toward a Tweet typology: contributory consumer engagement with brand messages by content type. Journal of Interactive Advertising, 16(2), 157–168. https://doi.org/https://doi.org/10.1080/15252019.2016.1208125

- Vonderau, P. (2019). The Spotify effect: Digital distribution and financial growth. Television & New Media, 20(1), 3–19. https://doi.org/https://doi.org/10.1177/1527476417741200

- Webster, J. (2019). Taste in the platform age: Music streaming services and new forms of class distinction. Information, Communication & Society, 1–16. https://doi.org/https://doi.org/10.1080/1369118X.2019.1622763

- Wikström, P. (2013). The music industry: Music in the cloud. Polity.

- WIN. (2018). Worldwide independent market report 2018. Worldwide Independent Network Ltd. http://winformusic.org/files/WINTEL%202018/WINTEL%202018.pdf

- Young, S., & Collins, S. (2010). A view from the trenches of music 2.0. Popular Music and Society, 33(3), 339–355. https://doi.org/https://doi.org/10.1080/03007760903495634

- Zangerle, E., Pichl, M., Gassler, W., & Specht, G. (2014). #nowplaying music dataset: Extracting listening behavior from Twitter. In Proceedings of the first international workshop on internet-scale multimedia management (pp. 21–26). ACM.