ABSTRACT

Financial transactions are part of everyday life, yet banking has largely withstood the digital transformation within most European countries. Recently, there have been initiatives that merge the digital and the financial sphere by integrating the transactions that run through established financial infrastructures into digital platforms. Large data-driven companies hereby seek access to financial transactions and try to embed payments within their platforms. This contribution discusses differing models of how tech-driven companies gain access to financial infrastructures, and how recently introduced policies engender these processes. Within Europe and the United Kingdom, banks that operate through financial infrastructures and hold most transactional data are now required by regulators to provide access to their customers’ accounts. The platformization of financial transactions is thus not purely a technical question, but it also is a remarkable example of how politically enforced changes in the materiality of data lead to reconfigurations with broader economic and social consequences. It results in the transformation of money into a form of (transactional) data and shows how the value of money and data depends on the technological underpinnings that determine the capability of their circulation. In order to understand their valuation, we need to take the material assemblages that enable their distribution into account.

1. Introduction – the (non-)digital wallet

When most people leave their homes, they think of a few things to take with them, normally including their smartphone and their wallet with their debit/credit cards and some cash. These items are essential to navigate and organize everyday life. While smartphones have already integrated several services that once required multiple devices, a separate credit or bank card or cash are still necessary for most purchases. This divide between smartphone and wallet resembles the separation of the underlying technologies that enable financial transactions.

This contribution shows how the ongoing division of the digital realm within the smartphone, and the financial sphere within the wallet, is rooted in the separation of their underlying technological foundations. While bank cards use established financial infrastructures to enable transactions, digital forms of payments developed by big players such as Apple and Facebook seek to embed transactions within platforms. However, tech-driven companies do not replace existing financial infrastructure, but they expand on them. This paper presents three models of how non-financial companies seek to gain access to the financial infrastructures in order to embed financial transactions within their data streams. It connects the importance of transactional data to ongoing processes of platformization and explains how these changes within the infrastructural materiality of monetary circulation are stimulated politically. As within the EU and the United Kingdom this process is engendered by regulatory demands, the platformization of financial transactions highlights the close entanglements of technological change, the politics of data, and everyday (financial) life.

The ambition of tech-driven companies to gain access to financial infrastructures is closely linked to the growing importance of transactional data. Thus, this contribution will also unpack the technical and political underpinning behind the very plausible claim that ‘Data is the new money, but also, money is data’ (Pardes, Citation2019). While the former is already a well-established imperative within the data economy (Fourcade & Healy, Citation2017), the latter is key to the transformation of financial services and indicates important differences between the financial and the tech industry: until now, banks have thrived on money, not data. Yet the increasing relevance of transactional data is tightly bound to the potentiality of information stored within money streams. As studies by economic anthropologist Bill Maurer have shown, ‘the value in the exchange now takes a back seat to the transactional data’, meaning that not the amount of the purchase, but the fact of the purchase itself is paramount (Maurer, Citation2012a, p. 477). As a consequence, ‘real-time payments and transaction data’ can be more readily combined with other forms of data, building a ‘richer and truer picture of the borrower’s ability to repay’, according to a description by the Bank of England (Citation2020, p. 13). The combination of different forms of data that have until now been separate thus allows for ever more substantive assessments of people’s social or economic situations. The following describes how technological changes are accompanied by fundamental shifts within the political economy of payments and banking as these spheres are pushed towards the platform model.

This contribution expands the analysis of valuation of monetary transfers (e. g. the data of transactions) enabled by new payment structures that, until now, have primarily been described for the Global South to the Global North (Maurer, Citation2012b, Citation2012c; O’Dwyer, Citation2015, Citation2019; Jain & Gabor, Citation2020). It substantiates these anthropological and cultural insights into the value of transactional data by foregrounding how transactional data handling and use are inseparable from material and technological conditions, including the performance of operations, speed, frequency and susceptibility of failure (Blanchette, Citation2011; Kaufmann & Jeandesboz, Citation2017). Building on studies that foreground the political and economic importance of infrastructures (Bernards & Campbell-Verduyn, Citation2019a; de Goede, Citation2012a, Citation2012b), the following discusses different models of how tech-driven actors gain access to financial infrastructures to embed transactional data into their platforms. The analysis sheds light on the effects of potentially transformative regulatory directives, the Second Payment Services Directive in the European Union (PSD2), and Open Banking in the United Kingdom, as other key drivers of the platformization of transactional data. This adds an important political dimension to bourgeoning literature on the platform economy that originated within the private sector and is now embraced by regulators (Langley & Leyshon, Citation2017; Plantin et al., Citation2018; Poell et al., Citation2019; van Dijck et al., Citation2018).

The following connects the differing features that enable the platformization of transactional data with an analysis of its technological implementation. The first section discusses the conceptual notions of platforms and infrastructures and connects them to politics and the economic value of financial transactions. The second section distinguishes three differing models of how tech-driven companies gain access to financial infrastructures and how they expand their platforms with the use of transactional data. Part three then argues that tech-driven actors are not the only drivers of platformization, as regulatory decisions within the EU and UK are key drivers of these models by demanding banks enable access to their customers’ accounts. Although these regulations are seen as a quiet revolution within the field of banking, they have not attracted much (critical) scholarly attention. The regulatory push that enables platformization shows how data generation and analysis is politically induced by altering the technologies that enable their circulation.

2. (Financial) infrastructures and platforms

This section discusses different strands of literature to connect the technological and material underpinnings of financial transactions to the value of their data. As in many Western countries the existing bank-based payment infrastructure is dominant, payment services such as Google Pay, Amazon Pay and Apple Pay have built their platforms on top of these existing payment systems to collect transactional data. These services offer customers the option to pay for (online) purchases without leaving their platform to execute the payment. Users thereby do not need to type in their credit card number or initiate a bank transfer themselves, but they can use different options to skip these modes of payment (e. g. by allowing the payment service to make transfers using costumer’s credit cards, or by using a pre-paid amount of money). Nevertheless, the importance of financial transactions and financial infrastructures had been recognized before the rise of platforms, as the fields of financial security and economic prediction show. Appreciating the respective materiality, forms of connectivity and economic logics that drive infrastructures and platforms is essential to understanding how platformization is connected to the relevance of transactional data.

Financial infrastructures are ubiquitous and allow the organization of financial life, facilitating payments, debt obligations or trading. Without becoming banks themselves, tech-driven companies seek access to these infrastructures and try to embed transactional data within their platforms. Acquiring and maintaining a banking license is seen as burden for tech companies due to the accompanying regulatory restraints. With the entrance of the platform model into the world of finance, financial infrastructures are not replaced, but instead platforms build and expand on infrastructural capabilities. Thomas Poell, David Nieborg and José van Dijck have provided a useful definition for this process of platformization as ‘the penetration of the infrastructures, economic processes, and governmental frameworks of platforms in different economic sectors and spheres of life’ (Citation2019, p. 5f.). Platformization in the field of banking is enabled by the use of what are termed application programming interfaces, or APIs, as a tool to penetrate financial infrastructures. As explained below, within Europe and the United Kingdom this is enabled by new regulatory demands requiring banks that operate through financial infrastructures and hold most transactional data to provide access to their customers’ accounts via APIs. This adds an important twist to insights generated by digital media and communication scholarship that have foregrounded how platforms govern (Gorwa, Citation2019): The directives of PSD2 and Open Banking embrace the platform model as a form of governance, promoting the growth of platforms in the financial sphere by regulatory means as section 3 explains in more detail.

While platforms and infrastructures are often seen as interchangeable, their conceptual distinctions help to account for the shift that is taking place within the field of transactions economics. In everyday language, the term ‘platform’ is often used synonymously with ‘infrastructure’. As Tarleton Gillespie (Citation2010) has shown in his account of the diverse etymological origins of the term ‘platform’, this claim is not meaningless, but has effects on perceptions across multiple venues for multiple audiences. Although they acknowledge the infrastructural intermediation of some platforms (Beer, Citation2013), Paul Langley and Andrew Leyshon (Citation2017, p. 19) argue against the metaphorical use of ‘infrastructure’ for platforms, asserting that ‘platforms are not utilities or conduits that simply channel circulations. Platforms actively induce, produce and programme circulations.’

In terms of their architecture, infrastructures are rather heterogeneous systems that are connected via socio-technical gateways, while platforms are programmable with a stable core system. Infrastructures’ market structures are mostly ‘administratively regulated in the public interest’, while platforms are only sometimes regulated, and are mostly private and competitive in nature. These different characteristics also resemble different temporalities: while infrastructures are established for long-term sustainability, platforms work with frequent updating (Plantin et al., Citation2018). At the same time, there are also some platforms which have infrastructural characteristics as their public implications are undeniable, including Google, Amazon, Facebook, Apple and Microsoft (van Dijck et al., Citation2018).

Central to the concept of platforms is user-generated data. As Nick Srnicek describes, ‘The platform has emerged as a new business model, capable of extracting and controlling immense amounts of data, and with this shift we have seen the rise of large monopolistic firms’ (Srnicek, Citation2017, p. 6; O’Dwyer, Citation2019, p. 141). For Langley and Leyshon, platforms are ‘particular comings together of code and commerce’ (Citation2017, p. 19). Of course, data is also generated within infrastructures, but in this model, data is the by-product of enabling flows and transactions, not the core of the business model. The next section discusses the specific value that lies within transactional data which flows along payment infrastructures and how its use as a form of memory gains new importance with the rise of platforms.

2.1. Money as memory – use of transactional data

Financial infrastructures are deeply embedded into everyday lives and they have numerous political implications. In most countries they are part of what are termed ‘critical infrastructures’, which are supposed to survive even catastrophic events (Folkers, Citation2017). The ‘critical’ implications of payment infrastructures foreground their political relevance and show that their importance is far from being reducible to the financial sector. Financial infrastructures are deeply entangled in broader political, economic and security rationales, and at the same time finance has ‘infrastructural power’ itself within market-based economic governance (Bernards & Campbell-Verduyn, Citation2019a; Braun, Citation2018). Financial infrastructures process a wide array of financial relations including credit and lending, collaterals, remittances, securities and payments. While payments are central to this analysis, several contributions have foregrounded the implications of digital credit and debt relations (Langley, Citation2014; Clarke, Citation2019; Bernards, Citation2019).

Transactions data is most valuable as it allows several conclusions to be drawn about personal life and actual behaviour. It mostly includes a timestamp, an account or credit card number, beneficiary account details, a description of the purchase and the amount. A payment statement allows even more detailed insight into the most personal information. Just to name a few examples: A monthly recurring beneficiary transaction from the same account is usually the wage and also shows the employer. Payments related to public institutions often include social security or tax identification numbers. Certain spending habits show relevant connections, for example to certain communities (religious or political), and medical spending may contain other sensitive information, such as the treatment of a specific disease.

Money and transaction data are forms of memory that were collected and stored before the evolution of information and communications technology allowed the rise of what has been called ‘big data’ (van Dijck, Citation2014). Rachel O’Dwyer (Citation2019) has provided a genealogy of how money has been used as a form of memory and how it is used to inform action. Her brief history of transactional records demonstrates how companies used transactional data as a proxy to rank, score, and classify individuals and to make predictions and decisions about future access and exclusion. While the state certainly exercised control over the supply and circulation of money in the pre-electronic era, as it does today, the ways money moves within commercial enterprises produced another layer of monetary control and access for citizens, even before electronic payments. For example, credit bureaus used transactional data (which they extracted from accounting records) to infer the creditworthiness of merchants and consumers, while department stores used these records to infer details of buyers’ purchasing habits and to influence their future purchasing behaviour. Transactional data acted as a predictive proxy for other aspects of individual or business conduct (ibid., p. 139). Hence, the surveillance and commercial use of proliferated personal data is not a new feature of the twenty-first century. As money is increasingly perceived as data, and less as a value itself, the practices of its use and exchange become more relevant. While Emily Gilbert (Citation2015, p. 361) has defined money as ‘a symbolic referent, a social system, and a material practice’ as it might acquire different values, Mareile Kaufmann (Citation2018, n. p.) has added that the same applies to digital data which seems to acquire the quality of money as it is also a ‘socio-technical system of exchange, and a material practice of calculation and analysis’. She argues that we need to understand both data and money as ‘societal and cultural practice’ whose values are determined by their exchange, accumulation and calculation. The next section describes the political implications of money’s social and cultural qualities as well as its quality as a form of memory.

2.2. The politics of financial transactions

The potential of information that lies within financial transactions has already been exploited before the rise of data-driven businesses. Within the provision of (financial) security, banks, police authorities and intelligence agencies have used transactional data to comprehend social relations. Financial transactions are regularly surveilled by banks and financial authorities as part of the fight against fraud, money laundering and terrorism financing (Amicelle, Citation2017; Wesseling et al., Citation2012).

Access to transactional data and control of payment infrastructures has political relevance and even geo-political implications, as the example of the largest global payment infrastructure shows. SWIFT, the Belgian-based Society for Worldwide Interbank Financial Telecommunications, acts as an ‘infrastructure for infrastructures’ as it enables and shapes payment networks that operate on and through it by providing secure bank-to-bank messaging. SWIFT handles about 80% of global payment traffic (Dörry et al., Citation2018). Although it presents itself as a neutral device to enable international payments, SWIFT also plays a role in the provision of security and within the geopolitics of sanctions (de Goede, Citation2012a). Through SWIFT the US can monitor all cross-border bank transfers and thereby enforce sanctions by punishing foreign banks for non-compliance, or threatening to cut them off from the basis of the global banking system – the dollar (Eich, Citation2018). The US government also has access to most of the established credit and debt data via Visa and Mastercard payment services (Arauz, Citation2019).

The case of SWIFT foregrounds the (geo-)political implications of payment infrastructures which rest on the value of data that money carries. Transactional data promise insights into economic and social relations, they are used to map networks and reveal patterns that are rendered for economic and security purposes. The next section shows how the technological underpinning for the circulation of data and/or money enables or disables their usage. Concretely, the following examines different ways in which tech-driven companies gain access to financial infrastructures to embed transactional data in their platforms. These underlying mechanisms seek to enable the frictionless experience of payments that payment services by BigTech companies want to achieve. If users can execute their payments without whipping out their credit cards or their cash, they will spend more time on the respective platforms and eventually embed their finances into their digital life.

3. Banking without banks? The platformization of financial transactions

The increasing importance of financial transactions as memory is closely entangled with a changing materiality of circulation which is enabled by platformization of financial transactions. This section describes how technology-driven companies seek to gain access to transactional data that transforms the political economy of payment platforms and data. While data is merely the by-product of (economic) circulation within the infrastructural model, the production of data is the main purpose of a platform (Srnicek, Citation2017; van Dijck et al., Citation2018). Platforms are set up with the clear aim of engendering data (re-)production, whereas infrastructures may also make financial gains by allowing the flow of money and other goods in exchange for a fee or similar economic incentives. Instead of replacing existing payment infrastructures, the platform model builds on them and thereby facilitates payments through their services. Within a platform, transactional data can thus be combined with other data streams and fed into the creation of ‘closed loops.’ Within these loops, consumers are directed to particular modes of payment or vendors because these vendors support particular modes of payment (Maurer, Citation2014). Linking transactional data to other kinds of data such as location, past behaviour and social connections enables all kinds of future value propositions, to the degree that ‘information about a monetary exchange may have a comparable or greater exchange value than the monetary token engaged in the transaction itself’ (O’Dwyer, Citation2016, n. p.).

While these practices are only just emerging in European countries, they are already happening in many places around the globe where cash and cards have been replaced by other means of payment. In China, platforms like Alipay and WeChat have developed into all-rounders which include everyday payment options and messaging applications – used by billions of consumers and deeply embedded in Chinese everyday life (Ahmed & Fong, Citation2017). The lack of dominant, pre-existing functioning credit cards or other payment infrastructures is seen as the reason why Chinese tech companies have been so successful in providing these services. Although users still need a Chinese bank account, they do not need to separately facilitate everyday payments with their bank or credit card. Instead, payment services are integrated into social platforms. The usage of information that is implied within transactional data is thus widened and combined with other kinds of data streams. The infamous Chinese social credit rating score thus ‘expands the concept of credit ratings far beyond financial metrics, to include social, political, and environmental factors both in terms of data inputs and rating outputs’ (Gruin & Knaack, Citation2019, p. 13).

In comparison to these far-reaching transitions it is noteworthy that in many European countries, including the United Kingdom, banking seems to have withstood the upheaval that digital services have brought other parts of the economy, such as travel, movies or taxis. The reason why banking has seemed immune to the digital transformation surely does not lie in the sector’s technological underdevelopment. For a long time, finance has been pushing ICT innovation to ensure financial gains, as the industry pushed the establishment of fibre technology in central hubs of financial trade to enhance millisecond-trading (Sassen, Citation2016). The everyday usage of new financial services is often prevented by shops’ reliance on established payment systems such as cash or credit cards, rooted within the dominant financial infrastructures. However, big and small tech-driven companies seek to enhance the transition towards digitalized financial within the Western world.

The following segments describe three models of how tech-driven companies secure access to transactional data that is transferred via financial infrastructures: first, the example of the Apple Card provides a model in which cooperation with an incumbent financial actor is used to secure access to payment infrastructures. Second, the example of solarisBank shows that the need of tech-driven companies to gain access to financial infrastructures has already been turned into a business model itself. Third, Facebook’s Libra has announced that it will circumvent established financial infrastructures altogether, which has been met with political and regulatory concerns. Within all three models, transactional data will be embedded within platforms that have been established. Platforms hence will not replace infrastructures but instead expand them.

3.1. The appleization of finance?Footnote1

In February 2019 two of the biggest companies of the tech and financial worlds, respectively, announced their collaboration: Apple and Goldman Sachs together launched a credit card. Although credit cards are not necessarily a revolutionary form of business, this move caught broad public attention. It seeks to bridge the divide of wallet and smartphone by enhancing the digital wallet within the smartphone. At the same time, the move expanded both parties’ core businesses as the two companies sought new revenue sources (Mickle et al., Citation2019). Although there is no fundamentally innovative feature with the new credit card, the move integrates the payments more directly into a mobile device as it seeks to connect data that is already stored on the device. The promise that comes with the card is not linked to new modes of purchasing, but rather the way (personal) finances are experienced.

While the Apple Card does not alter the means of payment – the purchase – it does seek to alter the way users handle their financial data. By embedding money as a form of data deeply into the platform, money is levelled with other kinds of data. Hence, paying for the purchase of goods or services should not be an additional step, but happen seamlessly. Tech companies often provide convenience by reducing frictions. While for users this means that the conscious step of payment and thereby direct contact with their finances is made redundant, this has new potential for data analytics. As José Ossandon (Citation2014) has shown for the data that is used for retail store credits, transactional data is captured and then leveraged at the point of sale, which acts as a ‘hub where multiple databases are practically enacted’ (p. 441).

The fact that one of the world's biggest tech companies now offers financial services raises questions about the potentially dark side of the future of money. As Arielle Pardes (Citation2019, n. p.) puts it:

Imagine how Big Tech could also change the status quo for payment security, by replacing those tired and vulnerable credit card numbers with smarter forms of authentication. Imagine, too, how all of these consumer conveniences might overshadow our suspicions about handing over the finer details of our financial lives to Big Tech. Apple says it won’t snoop on your spending, and that’s nice. But that’s not to say that the next company to issue a credit card—Google, or Facebook—won’t sell your monthly statement to the highest bidder.

3.2. Reducing banks to infrastructure

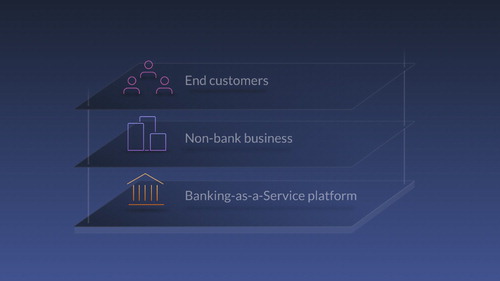

While Apple cooperates with a bank that offers the tech giant access to payment infrastructure, there are other models of how tech-driven companies can use payment infrastructures without becoming a bank themselves. This need to connect platforms to payment infrastructures has even been turned into a business model: solarisBank, the self-proclaimed ‘Tech company with a banking license’, offers banking services such as bank accounts, algorithmic scoring, transactions and even payment cards for non-bank customers. solarisBank works on a business-to-business basis, meaning it solely offers access to financial infrastructures to other businesses who then provide financial services to end users within their applications. Their services also include regulatory expertise on anti-money laundering and countering terrorism financing.

A most important feature in their business model is APIs whose role will be described in more detail below. As a means of data exchange, APIs are widely established, especially as a way of communicating between platforms and their various components and players that surround them. For solarisBank, APIs are a crucial tool for their business of providing banking infrastructure as a service. In adverts to other companies, they proclaim: ‘Build your own banking products with our API accessible banking as a service platform’ (solarisBank, Citation2020; see ). Their platform has access to financial infrastructures and enables other non-bank businesses to access the banking platform via APIs, thereby offering financial services to their (end) customers.

Figure 1. solarisBank – ‘Banking-as-a-Service platform’ – Model.

solarisBank spells out the biggest aim of their business as follows: ‘Our goal is to accelerate the transformation of the financial services industry: By making possibly every company worldwide a provider of financial services, banks will in the future act solely as the providers of infrastructure and become mostly invisible to the consumer’ (solarisBank, Citation2020). This sentence states most explicitly a possible direction within the platformization of transactional data: the reduction of banks’ role to providers of access to payment infrastructures. As will be described below, this tendency is not only enhanced by technological developments but also by new regulatory demands allowing third parties access to banks’ customer accounts.

The examples of Apple Card and solarisBank show two models in which platforms have used the intermediary space between existing established payment platforms and incumbent financial actors, a practice that Bill Maurer has described as ‘riding the rails’ of existing (public) infrastructures (Maurer, Citation2014). Within these two models, banks remain in place as providers of access to financial infrastructures while the non-financial companies provide the platform that costumers use. The next section describes another model that circumvents established financial infrastructures altogether by using distributed ledger technologies such as blockchain. This model gained prominence lately when another Big Tech company announced their plans to launch a new digital currency.

3.3. New financial infrastructures?

In 2019, Facebook announced the launch of its currency ‘Libra’ which caught wide attention as it was heralded as a fundamental challenge to the established financial system. At the time of writing, Libra has not materialized and it is still unclear if it will take the shape as was introduced in the Libra white paper (Libra, Citation2019). Recent developments indicate that Facebook's initial ambitions have been ‘scaled back’ and that they increasingly seek to complement national currencies (Popper & Issac, Citation2020).

Still, as Facebook claims that Libra's mission is to be ‘a simple global currency and financial infrastructure that empowers billions of people’ it is worth taking a moment to discuss its underlying model. Libra seeks to fulfil its claim of providing a financial infrastructure by coupling its new cryptocurrency with a blockchain-based payment and contract system (Bernards & Campbell-Verduyn, Citation2019b). By creating a new digital currency based on blockchain technology it would circumvent banks altogether, with the ambition of ‘turn[ing] Facebook into a platform that people never need to leave, and to create the conditions under which Facebook is the internet for as many people as possible’ (Beer, Citation2019, n. p.).

Using blockchain technology as an infrastructure would circumvent established financial intermediaries and transmit the transactional data through a mechanism of distributed consensus (Rodima-Taylor & Grimes, Citation2019b). While this would in principle allow established financial infrastructures and banks to be avoided altogether, an ‘increasing tendency can be observed of blockchain-based initiatives to operate in tandem with more traditional money transfer infrastructures’ (Rodima-Taylor & Grimes, Citation2019a, p. 853). In addition to regulators’ concerns about Facebook’s plans, it is thus still unclear if Libra will succeed in circumventing established payment infrastructures altogether.

Such ambitions of creating platforms on top of established financial infrastructures, or even circumventing them altogether, pose a challenge to the providers of these systems, such as banks and other financial services providers. They could not only lose a main revenue stream, but also their direct connections to customers, and would increasingly be diminished to the role of providing financial infrastructures that enable tech companies to collect and process (payment) data. The question thus arises as to whether this is sufficient to keep incumbent financial institutions in their current position. If data-driven corporations increasingly take over the provision of payment services within their platforms, banks could be reduced to nothing more than the infrastructural substrate of their service.

As indicated above, the push towards platformization is not solely driven by technological change, but also by regulatory demand. The ability to access and transfer payments – mostly gained with a banking licence – implies several regulatory demands, such as prevention of money laundering and terrorist financing. However, European regulators do not seek to prevent change within the banking sector. Instead they aim to open the field to new, especially tech-driven services.

4. Open banking. The regulatory push for platformization

This section discusses the technological foundations on which the regulatory demands of PSD2 and Open Banking are built, and how these demands enforce the platformization of banking infrastructures via the use of APIs. Within the European Union and the United Kingdom, regulators demanded a ‘seismic shift’ within the payments landscape when they pushed incumbent financial institutions to open their data and infrastructures to third parties (Agarwal, Citation2016). These demands aim at models that are similar to those of Apple Card and solarisBank, by enforcing cooperation between financial and non-financial companies. Like the described models this opening potentially enables tech and other companies to access transactional data processed within the payment infrastructures and embed them within platforms. In 2015 the EU adopted a new directive on payment services, PSD2, which is equivalent to Open Banking in the United Kingdom. The directive came into force in January 2018 and its explicit aims are to take account of new types of payment services and to ‘promote innovative mobile and internet payment services’ (European Commission, Citation2019). Within the directive, banks are given the role of trustees to secure customer data, while at the same time they are requested to provide access to their customer data upon request. In the past, consumers who wanted to allow other services to access their accounts had to provide their login details. This changes with PSD2. The regulatory demand thus effectively ends banks’ exclusive control of their users’ payment data and control of the payment process.

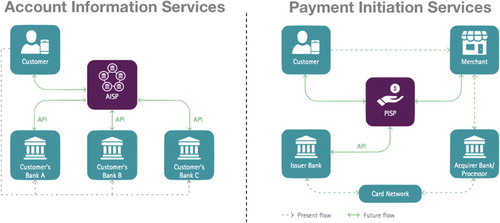

With the new payment directives, regulators govern through the infrastructures to enable market change and platformization. From a technological perspective, the demanded changes widen the scope of possible services that evolve from financial transactions and management. For this purpose, regulators have defined two differing roles for third parties that incumbent financial players need to enable: a Payment Initiation Service Provider (PISP), and/or as an Account Information Service Provider. Customers may allow the latter, an Account Information Service Provider, to receive information about their bank accounts with one or more banks, and their payments. These services might be used to organize budgets and financial planning. If the customer consents, through the PISP, they order their bank to transfer an amount to the beneficiary's account. Most of these services – payment initiation and account information – will be implemented as mobile apps or within platforms. This presents a direct alternative to a range of other payment services, such as credit cards.

Challenging the established (US-dominated) international credit card schemes was one main intention behind the new payment directive (Eroglu, Citation2019). Established credit card providers already hold an important position within the chain of financial service providers and they have already transformed from processing payments to the collection of data. Mastercard for example aggregates and analyses 65 billion transactions of 1.5 billion cardholders in 210 countries to map business and define consumer trends. From these amounts of data, they can extract spending habits and sell these insights to others. One example of their data analysis is the observation that people who stop for gas around 4 pm are likely to stop at a supermarket within the next hour and spend between 35 and 40 dollars afterwards (Mayer-Schönberger & Cukier, Citation2013) .

Figure 2. Relationships between customer, merchant and their respective banks with PSD2. Source: https://developer.ibm.com/mainframe/docs/open-banking/openbanking-psd2-in-practice-apis-and-mplbank/

4.1. Whose platform? Governing through APIs

This last section shows that while APIs, application programming interfaces, are a central means within the platformization of financial transaction, the question if banks or big tech’s platforms will be dominant in processing transactional data remains open. The new payment directive requires banks to open their APIs to third parties, thus enabling Payment Initiation Services and Account Information Services to acquire customers’ banking data. In the past, when users accessed their bank accounts, the banks sent the information from their servers to the customers’ banking mobile app, also owned by the same bank, using proprietary APIs. The new payment directive requires financial institutions to install a set of open APIs that allow any other company to send and receive API requests and thereby access their transactional data.

The regulatory push for interoperability in banking via APIs is inherently a push towards the platformization of financial services, as this kind of connectivity distinguishes infrastructures from platforms. Both systems depend on interoperability with their environments. While infrastructures ensure interoperability through standards and gateways, platforms work with APIs (Plantin et al., Citation2018). As the ongoing usage of payment infrastructures shows, and the aforementioned models of how Big Tech companies are gaining access to payment infrastructures illustrate, the two systems do not necessarily exclude one another. Instead, platforms penetrate infrastructures or try to circumvent them altogether as Facebook’s Libra seeks to do. Via APIs platforms of non-financial companies can evolve on top of payment infrastructures and embed transactional data into their platforms while banks are increasingly reduced to providing access to financial infrastructures, like the model of solarisbank shows (see ).

Incumbent financial actors are becoming increasingly aware of the potential that lies within their customers’ transactional data. Following the model of data-driven business, banks seek to use the potential of payment-based analytics and use ‘real-time transaction analysis’ to enable personalized offers and behavioural segmentation (Amoore, Citation2013). As a means to establish their own platforms, incumbent financial actors already use APIs to enable a controlled interaction between their systems and third parties, especially what are known as FinTechs (Hendrikse et al., Citation2018). FinTechs are technology-enabled innovative young companies concentrating on financial services. While FinTechs were first said to be disrupting the financial landscape altogether, cooperation with them has become a sort of middle way to enhance digital advancements within finance, without completely disrupt the established order. They also present a possible way for incumbent financial actors to defend their position as financial service providers while at the same time embracing digital change. Within this model, FinTechs provide additional services to banks’ own platforms without fundamentally challenging banks’ current status.

Regulatory demands on banks to open their APIs thus accelerates the platformization of financial infrastructures, either by allowing FinTechs to expand banks’ platforms or by allowing tech companies to embed transactional data within their platforms. By enhancing the use of APIs, the flow of transactional data is facilitated as APIs engender their exchange between different parties. However, the use of APIs is far from a neutral way of reciprocal communication because platform providers set the terms of exchange. As Plantin et al. explain for the case of Facebook, ‘APIs permit other programs to “plug in,” in order to exchange data or perform other functions; unlike electrical sockets, however, APIs create a two-way flow of data. In the language of infrastructure studies, an API is a gateway, permitting other systems to interact with Facebook to form a seamlessly interactive network’ (Citation2018, p. 303).

Further research into how Big Tech companies use APIs also shows that they present a double-edged sword. While APIs increase the functionality of a platform by promoting a mushrooming of apps that use the API to exchange data with said platform, they also create restrictions for app developers, users and researchers (Langlois & Elmer, Citation2013). Hendrikse, Bassens, and van Meeteren (Citation2018) describe similar effects for Apple’s use of APIs that creates a ‘walled garden’ which ‘effectively is a barrier or checkpoint through which Apple exclusively decides the extent to which developers can access the operating system, as well as which developers can market their apps via Apple’s platform’ (p. 166). Hence, APIs bring a proprietary interest of the platform owner into the notion of interoperability even while they seem to de-centralize and open the platform (Mackenzie, Citation2018). As discussed above, platforms thus have political implications as they enable or disable interaction and set the terms for exchange.

Taken together, PSD2 presents a remarkable case of politically enforced market liberation that favours the platform model which originated within the private sector for the governance of payment data. The regulatory reason to promote the platformization of banking assumes that incumbent financial actors will stay in the position to determine the conditions of data exchange, if they succeed in building platforms. As one member of the board of the German Bundesbank comments: ‘The new directive has secured the role of banks as the trustee of their customers’ data. Financial institutions are in charge of the procedure (…). The bank account could in this way become an ‘open platform’ around which all kinds of customer relationships evolve’ (Balz, Citation2018). As platform holders, it would be largely in the hands of the banks themselves to decide upon the openness of the API gateways to their systems. Yet, the need to provide APIs and build platforms potentially favours those who have the necessary resources, most likely big banks and Big Tech companies.

5. Conclusion and outlook

The future direction of payment systems is still open at this point. As the payment directive has already entered into force, new ways of data exchange are increasingly being used. Although it is not clear who will provide the major platforms for payments and other financial relations, the shift within the underlying materiality already affects the use and governance of these data streams. The platformization of financial transactions is not purely a technical question, but is also a remarkable example of how politically enforced changes in the materiality of data lead to reconfigurations with broader economic and social consequences. The integration of transactional data into platforms enables their combination and levelling with other kinds of data.

Linking the technological changes as well as regulatory demands with their political and economic implications is necessary to understand the scope and impact of data vocations. Adding to the overall topic of this Special Issue, this contribution shows how changes within the material underpinnings enable and prefigure the heterogeneous visions of (big) data practices (Madsen et al., Citation2016). Taking the materiality of electronic money seriously leads to a reconceptualization of its ontology and political agency, as Anna Leander (Citation2015) has emphasized. For security and policing purposes, it means that the claim to ‘follow the money’ will increasingly be replaced by ‘follow the data’, and platforms will potentially require a similar regulation to financial intermediaries (Zetzsche et al., Citation2017, p. 35f.). For commercial purposes this presents an opportunity for ever-more detailed insights into consumer behaviour.

The new importance of financial transactions and their transformation into one form of data stream also connects to wider shifts. Within the platform logic, financial streams are detected as one form of data stream, as one form of relationship between two data points, but not necessarily as the distinguishing market logic. While ‘big data strategists’ have already claimed that ‘data is in fact a new kind of capital on par with financial capital for creating new products and services’, such wide-ranging implications have yet to be established (Sadowski, Citation2019, p. 3). As this contribution has shown, broader shifts with political and economic consequences are rooted within their technological foundations. As the move from financial infrastructures to platforms prefigures how money is increasingly used as data, the materiality of data circulation renders the data as valuable in and of itself. The question remains as to when this material shift will be tangible for everyone; in other words, when the wallet and the smartphone will merge completely.

Acknowledgements

I am grateful to Rocco Bellanova, Marieke de Goede and the whole FOLLOW team, Tasniem Anwar, Anneroos Planqué-van Hardeveld, Esmé Bosma, Pieter Lagerwaard, as well as the anonymous reviewers for their constructive feedback and comments. Many thanks to Richard Thrift for proofreading the manuscript and to Mareile Kaufmann for initiating this Special Issue, her immensely helpful editorial work and patience.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes on contributor

Carola Westermeier is a postdoctoral researcher in the Department of Political Science at the University of Amsterdam. She is part of the FOLLOW project group at the Amsterdam Institute for Social Science Research (AISSR), supported by a Consolidator Grant of the European Research Council (ERC). Her research is based at the intersections of security studies, international political economy and political sociology. [Email: [email protected]]

Additional information

Funding

Notes

1 The term is borrowed from Hendrikse, Bassens & van Meeteren (Citation2018).

References

- Agarwal, S. (2016). PSD2: Payments regulation that raises a profound strategic choice for banks. https://bankingblog.accenture.com/psd2-payments-regulation-that-raises-a-profound-strategic-choice-for-banks

- Ahmed, S., & Fong, A. (2017). Cashless Society, Cached Data Are Mobile Payment Systems Protecting Chinese Citizens’ Data? The citizen lab. https://citizenlab.ca/2017/01/cashless-society-cached-data-security-considerations-chinese-social-credit-system/

- Amicelle, A. (2017). When finance met security: Back to the War on Drugs and the problem of dirty money. Finance and Society, 3(2), 106–123. https://doi.org/10.2218/finsoc.v3i2.2572

- Amoore, L. (2013). The politics of possibility: Risk and security beyond probability. Duke University Press.

- Arauz, A. (2019). The Data of Money. https://www.tni.org/files/publication-downloads/recommended_reading_-_data_of_money.pdf

- Balz, B. (2018). Ökosystemen im Zahlungsverkehr gehört die Zukunft [Payment Ecosystems are the Future], Der Bank Blog. https://www.der-bank-blog.de/oekosystemen-zahlungsverkehr-zukunft/mobile-payment/38817/

- Bank of England. (2020). Open data for SME finance: What we proposed and what we have learnt. https://www.bankofengland.co.uk/paper/2020/open-data-for-sme-finance

- Beer, D. (2013). Popular Culture and New media: The politics of circulation. Palgrave Macmillan.

- Beer, D. (2019). Facebook’s new currency is an attempt to create a platform we never leave. https://www.opendemocracy.net/en/oureconomy/facebooks-new-currency-is-an-attempt-to-create-a-platform-we-never-leave/

- Bernards, N. (2019). The poverty of fintech? Psychometrics, credit infrastructures, and the limits of financialization. Review of International Political Economy, 26(5), 815–838. https://doi.org/10.1080/09692290.2019.1597753

- Bernards, N., & Campbell-Verduyn, M. (2019a). Understanding technological change in global finance through infrastructures. Review of International Political Economy, 26(5), 773–789. https://doi.org/10.1080/09692290.2019.1625420

- Bernards, N., & Campbell-Verduyn, M. (2019b). Facebook’s Libra and the International Politics of Financial Infrastructures. E-International Relations Publishing. https://www.e-ir.info/2019/07/05/facebooks-libra-and-the-international-politics-of-financial-infrastructures/

- Blanchette, J.-F. (2011). A material history of bits. Journal of the American Society for Information Science and Technology, 62(6), 1042–1057. https://doi.org/10.1002/asi.21542

- Braun, B. (2018). Central banking and the infrastructural power of finance: The case of ECB support for repo and securitization markets. Socio-Economic Review, 107, 515. https://doi.org/10.1093/ser/mwy008

- Clarke, C. (2019). Platform lending and the politics of financial infrastructures. Review of International Political Economy, 26(5), 863–885. https://doi.org/10.1080/09692290.2019.1616598

- de Goede, M. (2012a). Speculative security: The politics of pursuing terrorist monies. University of Minnesota Press.

- de Goede, M. (2012b). The SWIFT affair and the global politics of European security. Journal of Common Market Studies, 50(2), 214–230. https://doi.org/10.1111/j.1468-5965.2011.02219.x

- Dörry, S., Robinson, G., & Derudder, B. (2018). There is no Alternative. SWIFT as Infrastructure Intermediary in Global Financial Markets. Financial Geography Working Paper Series. http://www.fingeo.net/wordpress/wp-content/uploads/2019/01/FinGeo-WP_Robinson_Swift-GPN_GR2.pdf

- Eich, S. (2018). SWIFT: A modest proposal? An alternative bank transfer network won’t be enough to counter American financial hegemony. https://www.thenation.com/article/swift-a-modest-proposal/

- Eroglu, H. (2019). How instant payments and PSD2 could pave the way to PSD3. https://bankingblog.accenture.com/instant-payments-psd2-could-pave-way-psd3

- European Commission. (2019). Payment services. https://ec.europa.eu/info/business-economy-euro/banking-and-finance/consumer-finance-and-payments/payment-services/payment-services_en#eu-rules-on-payment-services

- Folkers, A. (2017). Existential provisions: The technopolitics of public infrastructure. Environment and Planning D: Society and Space, 10(4). https://doi.org/10.1177%2F0263775817698699

- Fourcade, M., & Healy, K. (2017). Seeing like a market. Socio-Economic Review, 15(1), 9–29. https://doi.org/10.1093/ser/mww033

- Gilbert, E. (2015). Common cents: Situating money in time and place. Economy and Society, 34(3), 357–388. https://doi.org/10.1080/03085140500111832

- Gillespie, T. (2010). The politics of ‘platforms’. New Media & Society, 12(3), 347–364. https://doi.org/10.1177/1461444809342738

- Gorwa, R. (2019). What is platform governance? Information, Communication & Society, 22(6), 854–871. https://doi.org/10.1080/1369118X.2019.1573914

- Gruin, J., & Knaack, P. (2019). Not just another Shadow bank: Chinese authoritarian capitalism and the ‘developmental’ promise of digital financial innovation. New Political Economy, 3(2), 1–18. https://doi.org/10.1080/13563467.2018.1562437

- Hendrikse, R., Bassens, D., & van Meeteren, M. (2018). The Appleization of finance: Charting incumbent finance’s embrace of FinTech. Finance and Society, 4(2), 159–180. https://doi.org/10.2218/finsoc.v4i2.2870

- Jain, S., & Gabor, D. (2020). The rise of digital financialisation: The case of India. New Political Economy, 52(18), 1–16. https://doi.org/10.1080/13563467.2019.1708879

- Kaufmann, M. (2018). Digital data and value: Official risk-narratives of hacking in India and the US. Technoculture, 8.

- Kaufmann, M., & Jeandesboz, J. (2017). Politics and ‘the digital’. European Journal of Social Theory, 20(3), 309–328. https://doi.org/10.1177/1368431016677976

- Langley, P. (2014). Equipping entrepreneurs: Consuming credit and credit scores. Consumption Markets & Culture, 17(5), 448–467. https://doi.org/10.1080/10253866.2013.849592

- Langley, P., & Leyshon, A. (2017). Platform capitalism: The intermediation and capitalization of digital economic circulation. Finance and Society, 3(1), 11–31. https://doi.org/10.2218/finsoc.v3i1.1936

- Langlois, G., & Elmer, G. (2013). The research politics of social media platforms. Culture Machine. http://www.culturemachine.net/index.php/cm/article/view/505

- Leander, A. (2015). Theorising international monetary relations: Three questions about the significance of materiality. Contexto Internacional, 37(3), 945–973. https://doi.org/10.1590/S0102-85292015000300006

- Libra. (2019). White paper – an introduction to Libra. https://libra.org/en-US/white-paper/

- Mackenzie, A. (2018). From API to AI: Platforms and their opacities. Information, Communication & Society, 16, 1–18. https://doi.org/10.1080/1369118X.2018.1476569

- Madsen, A. K., Flyverbom, M., Hilbert, M., & Ruppert, E. (2016). Big data: Issues for an international political sociology of data practices. International Political Sociology, 10(3), 275–296. https://doi.org/10.1093/ips/olw010

- Maurer, B. (2012a). Late to the party: Debt and data. Social Anthropology, 20(4), 474–481. https://doi.org/10.1111/j.1469-8676.2012.00219.x

- Maurer, B. (2012b). Payment: Forms and functions of value transfer in contemporary society. The Cambridge Journal of Anthropology, 30(2), https://doi.org/10.3167/ca.2012.300202

- Maurer, B. (2012c). Mobile money: Communication, consumption and change in the payments space. Journal of Development Studies, 48(5), 589–604. https://doi.org/10.1080/00220388.2011.621944

- Maurer, B. (2014). Postscript: Is there money in credit? Consumption Markets & Culture, 17(5), 512–518. https://doi.org/10.1080/10253866.2013.850037

- Mayer-Schönberger, V., & Cukier, K. (2013). Big data: A revolution that will transform how we live, work and think. Murray.

- Mickle, T., Hoffman, L., & Rudegeair, P. (2019). Apple, Goldman Sachs team up on credit card paired with iPhone, The Wall Street Journal. https://www.wsj.com/articles/apple-goldman-sachs-team-up-on-credit-card-paired-with-iphone-11550750400

- O'Dwyer, R. (2015). When Telcos become banks: Sociotechnical control in mobile money. Proceedings of ISIS Summit Vienna, S3014. https://doi.org/10.3390/isis-summit-vienna-2015-S3014

- O’Dwyer, R. (2016). Where’s the money? http://kingsreview.co.uk/articles/wheres-the-money/#_ftn5

- O’Dwyer, R. (2019). Cache society: Transactional records, electronic money, and cultural resistance. Journal of Cultural Economy, 12(2), 133–153. https://doi.org/10.1080/17530350.2018.1545243

- Ossandón, J. (2014). Sowing consumers in the garden of mass retailing in Chile. Consumption Markets & Culture, 17(5), 429–447. https://doi.org/10.1080/10253866.2013.849591

- Pardes, A. (2019). Why the Apple Card Is the Gleaming Future of Money. https://www.wired.com/story/why-apple-card-is-gleaming-future-of-money/

- Plantin, J.-C., Lagoze, C., Edwards, P. N., & Sandvig, C. (2018). Infrastructure studies meet platform studies in the age of Google and Facebook. New Media & Society, 20(1), 293–310. https://doi.org/10.1177/1461444816661553

- Poell, T., Nieborg, D., & van Dijck, J. (2019). Platformisation. Internet Policy Review, 8(4), http://policyreview.info/concepts/platformisation. https://doi.org/ 10.14763/2019.4.1425

- Popper, N., & Issac, M. (2020). Facebook-backed libra cryptocurrency project is scaled back. https://www.nytimes.com/2020/04/16/technology/facebook-libra-cryptocurrency.html

- Rodima-Taylor, D., & Grimes, W. (2019a). International remittance rails as infrastructures: Embeddedness, innovation and financial access in developing economies. Review of International Political Economy, 26(5), 839–862. https://doi.org/10.1080/09692290.2019.1607766

- Rodima-Taylor, D., & Grimes, W. (2019b). Virtualizing diaspora: New digital technologies in the emerging transnational space. Global Networks, 19(3), 349–370. https://doi.org/10.1111/glob.12221

- Sadowski, J. (2019). When data is capital: Datafication, accumulation, and extraction. Big Data & Society, 6(1), https://doi.org/10.1177/2053951718820549

- Sassen, S. (2016). The global city: Enabling economic intermediation and bearing its costs. City & Community, 15(2), 97–108. https://doi.org/10.1111/cico.12175

- solarisBank. (2020). Homepage. https://www.solarisbank.com/en

- Srnicek, N. (2017). Platform capitalism. Polity.

- van Dijck, J. (2014). Datafication, dataism and dataveillance: Big data between scientific paradigm and ideology. Surveillance & Society, 12(2), 197–208. https://doi.org/10.24908/ss.v12i2.4776

- van Dijck, J., Poell, T., & de Waal, M. (2018). The platform society: Public values in a connective world. Oxford University Press.

- Wesseling, M., de Goede, M., & Amoore, L. (2012). Data wars beyond surveillance. Journal of Cultural Economy, 5(1), 49–66. https://doi.org/10.1080/17530350.2012.640554

- Zetzsche, D. A., Buckley, R. P., Arner, D. W., & Barberis, J. N. (2017). From FinTech to TechFin: The Regulatory Challenges of Data-Driven Finance. European Banking Institute Working Paper Series No 6.