Abstract

Background

US commercial health plans have been found to vary in how they cover specialty drugs indicated for a range of diseases. In this study, we examined patients’ access to hemophilia A (HemA) treatments across a set of large commercial health plans.

Objective

To examine variation in health plans’ coverage policies for HemA treatments.

Methods

We reviewed HemA treatment coverage policies (current as of August 2019) issued by 17 commercial health plans primarily using the Tufts Medical Center Specialty Drug Evidence and Coverage Database. We categorized policies as: covered without conditions (coverage consistent with the FDA label); covered with conditions (conditions on coverage beyond the FDA label); broader coverage (coverage for a broader patient population than the FDA label); and mixed (conditions on coverage beyond the FDA label in one way, but coverage was broader than the FDA label in another).

Results

We identified 296 coverage policies for 26 HemA treatments, including 15 short half-life factor VIII (FVIII) products, five extended half-life FVIII products, three bypassing agents, two desmopressin products, and emicizumab. We classified 36% of policies as coverage without conditions, 50% as covered with conditions, 7% as broader coverage, and 7% as mixed. Plans applied conditions on coverage with different frequencies: two did not apply conditions in any policies; ten applied conditions in ≥50%; four applied conditions in <40%. One plan did not publish coverage policies for any HemA products. Conditions on coverage most often related to bleeding frequency (36%), although specific requirements varied. Plans applied step therapy protocols in 17% of policies.

Conclusions

How health plans covered HemA treatments varied. Plans added conditions on coverage beyond the FDA label roughly half the time. Conditions most often related to bleeding frequency. Variable coverage affects patients’ access to treatment, and potentially has clinical implications on disease management and disease progression.

Introduction

Hemophilia A (HemA) is a rare, inherited bleeding disorder caused by deficiency of factor VIII (FVIII), an essential blood-clotting protein, and affects one of every 5,000–10,000 male live birthsCitation1. Mild disease severity is defined as having a factor level of >0.05–0.40 IU/ml, moderate as 0.01–0.05 IU/ml, and the severe form as <0.01 IU/mlCitation2.

Treatment has generally involved infusing the patient with FVIII replacement products. Treatment can be episodic (in response to a bleeding episode) or prophylactic (to prevent bleeding episodes)Citation3. Of particular concern for prophylactic treatment, the average half-life of factor concentrates can range from approximately 12 h in short half-life products (SHL) to 18 h in extended half-life (EHL) products resulting in intravenous dosing multiple times a weekCitation4. Patients can develop allo-antibodies (inhibitors) against exogenous FVIII, nullifying the therapeutic value of the factor replacement therapy. The incidence of these inhibitors can be as high as 30% in severe patients, and 3–13% in mild or moderate patientsCitation5.

Other available treatments include desmopressin acetate, which induces the release of endogenous FVIII, bypassing agents (BPAs) (e.g. recombinant activated FVII or activated prothrombin complex concentrate), which circumvent the blood clotting steps that require FVIII, and emicizumab, which is a bispecific monoclonal product that mimics the activity of FVIII by bridging factors IXa and X. For patients with inhibitors, immune tolerance therapy (ITT) (regular administration of factor concentrate) can “reset” a patient’s immune response so that it does not interfere with the function of exogenously introduced FVIII.

HemA results in a large economic burden for patients, their families, and the health care systemCitation6,Citation7. The average annual direct and indirect costs of treating patients with HemA is estimated to be greater than $230,000, with even higher estimated costs of $978,955 for patients with inhibitorsCitation8.

Research has identified variation in US commercial health plan coverage policies for specialty drugs that treat a range of diseasesCitation9,Citation10. However, whether there is similar variability in how plans cover HemA treatments is unclear.

We examined patients’ access to HemA treatments across a set of large commercial health plans. Our findings may help the hemophilia community understand variation in coverage that may affect patients’ access to treatment.

Methods

We identified HemA treatments from the National Hemophilia Foundation’s clinical guidelines (Appendix A)Citation11. We examined treatments indicated for prophylaxis, episodic therapy, or both.

Next, we identified coverage policies for HemA treatments from the Tufts Medical Center Specialty Drug Evidence and Coverage (SPEC) databaseCitation12, which contains information on 17 large commercial health plans (11 national plans, six regional plans) which cover specialty drugs (Appendix B)Citation13. The included plans comprise >150 million covered lives (ranging between 2.5–14.5 million covered lives per plan), which account for >60% of commercially covered lives. For hemophilia treatments not in SPEC, we identified coverage policies from the websites of the same 17 plans. Included coverage policies were current as of August 2019.

We benchmarked HemA treatment coverage to the treatment’s FDA label indication (Appendix A), designating coverage as “coverage without conditions” if the populations covered by the plan and approved by FDA were the same, “covered with conditions” if the plan covered for a narrower patient population than the FDA label, “broader coverage” if the plan covered for a broader patient population than the FDA label, and mixed if the plan covered for a narrower patient population than the FDA label in one way, but a broader population in another. We recorded coverage differences for patients with and without inhibitors.

We categorized coverage conditions as: patient subgroup requirements, which required patients to meet certain clinical criteria (e.g. recent experience of ≥2 bleeding episodes); or step therapy protocols, which required patients to first fail an alternative treatment.

Results

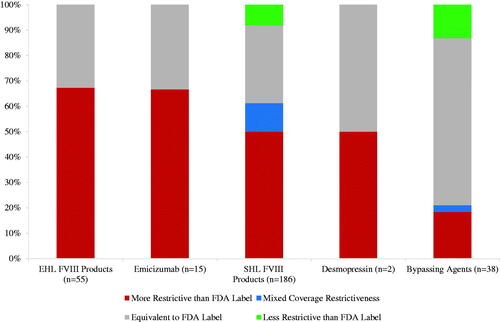

We identified 296 coverage policies; 186 for SHL FVIII products, 55 for EHL FVIII products, 38 for BPAs, 15 for the non-factor product, emicizumab, and two for desmopressin.

We classified 36% (106) of policies as covered without conditions, 50% (148) as covered with conditions, 7% (20) as broader coverage, and 7% (22) as mixed. Of the 42 policies categorized as broader coverage or mixed, 25 covered perioperative use (prevention of bleeding related to surgical procedures) for products not approved for this use, and 16 covered prophylactic use for products approved only for episodic use. On one occasion, a plan covered a BPA for acquired HemA (an off-label use).

Of policies classified as coverage with conditions or mixed, plans most frequently imposed patient subgroup requirements (141/170 policies, 83%). These requirements most often related to bleeding frequency (107/141, 76%) and typically varied by disease severity. For example, for FVIII products, one plan imposed no additional requirements on patients with severe disease, but required patients with mild or moderate disease to have experienced ≥2 spontaneous joint bleeds. Another plan issued FVIII policies that imposed no additional requirements on patients with severe disease, but required patients with mild to moderate disease to have experienced one of the following: a bleed into a joint; a bleed into the central nervous system; or ≥4 bleeds into soft tissue.

The second most common patient subgroup requirement denied coverage for perioperative use (24/141 policies, 17%), even when the product was approved for this application.

Health plans imposed step therapy protocols in 30% (51/170) of policies with additional coverage conditions. Plans tended not to define “treatment failure”, but those that did described patients’ failure to meet clinical goals (e.g. patients experienced a continuation of spontaneous bleeds). Two plans often required patients with mild disease to first fail desmopressin (i.e. experienced bleeding episodes) before granting coverage of FVIII products. Forty-one step therapy protocols required that patients first fail a single treatment, five required patients fail two treatments, and another five required patients fail ≥3 treatments. Of the 51 step therapy protocols, 10 (20%) required patients fail prior therapy with some specific brands within a treatment class; 41 (80%) required that patients fail a treatment from a particular class, but did not specify the brand.

Variation across health plans

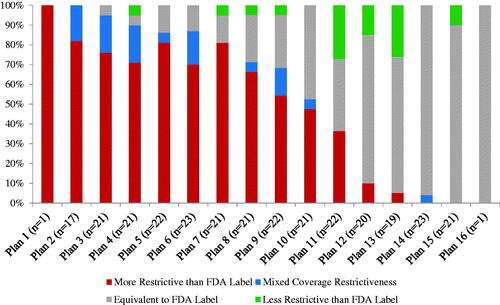

Sixteen health plans issued publicly available coverage policies for HemA treatments. One plan issued no policies for the included drugs. Some plans issued more policies than others; 12 issued policies for ≥20 treatments, while two issued a policy for a single treatment.

Some plans applied coverage conditions beyond the FDA label more often than others (). Two plans did not impose additional coverage conditions in any policies. Of plans that applied additional coverage conditions, ten did so in at least half of their policies, while four did so in fewer than half of their policies.

Figure 1. Coverage variation across health plans (n = 296 coverage policies across 16 health plans). Numbers in parentheses refer to the number of policies issued by each health plan. One plan did not issue policies for the included products.

Variation across HemA treatments

Health plans covered some HemA treatment classes more restrictively than others (). Plans applied coverage conditions in more than half of their policies for SHL FVIII products (114/186 policies, 61%), EHL FVIII products (37/55 policies, 67%), and the non-factor product (10/15 policies, 67%). Plans imposed additional coverage conditions in 21% (8/38) of BPA policies.

Figure 2. Coverage variation across treatment classes (n = 296 coverage policies across 16 health plans). Number in parentheses refers to the number of policies issued for all treatments in the class. EHL, Extended half-life; FVIII, Factor VIII; SHL, Short half-life.

Plans most often applied additional coverage conditions for newer HemA treatments, the non-factor product, emicizumab (10/15 policies, 67%), and EHL FVIII products (37/55 policies, 67%). For emicizumab, ten plans imposed patient subgroup requirements (60% of which were bleeding related) and four plans additionally imposed step therapy protocols. For example, one plan required that patients with mild hemophilia fail desmopressin acetate, patients with FVIII inhibitors fail a BPA, and patients without FVIII inhibitors fail a FVIII product, before gaining access to emicizumab.

For the five EHL FVIII therapies, plans most often applied patient subgroup requirements (30/37 EHL FVIII policies with imposed restrictions), which were typically bleeding related requirements before prophylactic use (25/30 policies with patient subgroup requirements). Some plans additionally applied step therapy protocols (16/37 policies with imposed restrictions) for both prophylactic and on-demand use: eight policies required failure of SHL FVIII products, three policies required failure of desmopressin, and four policies required failure of both SHL FVIII products and desmopressin before granting access to an EHL FVIII product.

Discussion

Health plans applied coverage conditions beyond HemA products’ FDA labels more than half the time. This finding suggests that, on average, commercial health plans cover HemA treatments more restrictively than drugs for other orphan diseases, for which research has found plans impose coverage restrictions roughly one third of the timeCitation14. This may be explained by the large number of available HemA treatments, which is not generally the case for orphan diseases. The availability of multiple therapeutic options allows plans to prioritize enrollee’s access to certain treatments over others. However, inappropriately applied coverage conditions can negatively impact disease management and health outcomes if they affect patients’ timely access to optimal therapy as well as disregard physicians’/patients’ treatment choice. For example, some plans imposed coverage restrictions by the number of joint bleeds. Increased bleeding into joints resultant from suboptimal or delayed treatment can cause irreversible damage leading to pain and hemophilic arthropathy, thus compromising patients’ health-related quality of life (HRQoL)Citation15.

Our study demonstrates that the largest US commercial health plans cover HemA treatments differently. Important consequences of this finding include that hemophilia patients enrolled in different plans have unequal access to treatments, and that physicians must tailor their treatment choices not only to a patient’s clinical needs, but also to the patient’s health insurance.

It is unclear why different health plans cover the same treatments differently. One reason may be that some plans adhere more closely to treatment guidelines than others. For instance, the National Hemophilia Foundation Medical and Scientific Advisory Council (MASAC) recommends that desmopressin be used for patients with mild HemACitation11. We found that two health plans required that patients with mild HemA first fail desmopressin before gaining coverage for FVIII products; however, other plans did not impose the same requirement. It may also be that some plans took a lead from clinical trial inclusion criteria when applying conditions on coverage. The most common coverage condition was that patients had experienced a particular number of bleeding episodes over a specified period of time, a typical clinical trial inclusion criterion for these products. It was notable, however, that plans varied in their application of bleeding requirements.

The identified differences in health plan decision-making may be explained by plans being able to afford different levels of spending, or that plans may have different contracting arrangements with manufacturers, which give rise to differences in their coverage requirements. One potential explanation for additional coverage requirements imposed on emicizumab for patients without inhibitors is that some plans may not have updated their coverage policies following FDA’s extension of emicizumab’s label to include patients without inhibitors in late 2018Citation16.

Our findings provide insight into how health plans may cover future HemA treatments, including gene therapies. A key study finding is the variation in health plans’ patient access criteria, which may be the case in plans’ policies for a future HemA gene therapy. Indeed, research has found that plans impose varied coverage conditions for the two available gene therapies, onasemnogene abeparvovec for spinal muscular atrophy, and voretigene neparvovec for inherited retinal disease, with plans having different disease severity requirements and age of eligibility criteriaCitation17.

Future research should build on this study in various ways. First, research that examines the consistency of health plan coverage requirements with available treatment guidelines and clinical trial inclusion criteria would be valuable. Understanding how plans formulate coverage policies would help the hemophilia community to better understand the reasons underpinning their access to care. Second, future research should examine how plans' use of coverage conditions (patient subgroup restrictions or step therapy protocols) affects product utilization and HemA patients’ health outcomes. Third, future research should also evaluate how providing HemA treatment coverage information to patients aids them in their selection of the most appropriate health plan.

Our study has a number of limitations. First, not all health plans issued a coverage policy for each treatment. Second, our findings may not generalize to other commercial plans or to public payers (e.g. Medicaid). Third, we did not account for appeals that patients can file in response to coverage denials. Fourth, we did not account for cost-sharing requirements. Fifth, we did not evaluate the clinical appropriateness of coverage conditions, e.g. by comparing them with clinical guidelines.

Conclusion

For HemA treatments, plans applied coverage conditions that go beyond the FDA label. These conditions often related to bleeding frequency, although specific requirements varied. Variation in coverage policies has important consequences for the hemophilia community’s access to established and emerging therapies, and potentially has clinical implications for patients regarding disease management and disease progression.

Transparency

Declaration of funding

This study was funded by Genentech.

Declaration of financial/other interests

No potential conflict of interest was reported by the author. Peer reviewers on this manuscript have no relevant financial or other relationships to disclose.

Acknowledgements

None stated

References

- National Hemophilia Foundation. Fast Facts. About Bleeding Disorders. 2020. Available at https://www.hemophilia.org/About-Us/Fast-Facts. [Accessed May 4, 2020].

- World Federation of Hemophilia. Mild Hemophilia (Revised November 2012). 2020. Available at: http://www1.wfh.org/publication/files/pdf-1192.pdf. [Accessed September 24, 2020].

- Centers for Disease Control and Prevention. Hemophilia. Treatment of Hemophilia. 2020. Available at https://www.cdc.gov/ncbddd/hemophilia/treatment.html. [Accessed May 4, 2020].

- Tiede A. Half-life extended factor VIII for the treatment of hemophilia A. J Thromb Haemost. 2015;13(Suppl 1):S176–S9.

- Witmer C, Young G. Factor VIII inhibitors in hemophilia A: rationale and latest evidence. Ther Adv Hematol. 2013;4(1):59–72.

- Dalton DR. Hemophilia in the managed care. Am J Manag Care. 2015;21(suppl 6):S123–S130.

- Brown TM, Lee WC, Joshi AV, et al. Health-related quality of life and productivity impact in haemophilia patients with inhibitors. Haemophilia. 2009;15(4):911–917.

- Zhou Z-Y, Koerper MA, Johnson KA, et al. Burden of illness: direct and indirect costs among persons with hemophilia a in the United States. J Med Econ. 2015;18(6):457–465.

- Chambers JD, Wilkinson CL, Anderson JE, et al. Variation in private payer coverage of rheumatoid arthritis drugs. J Manag Care Spec Pharm. 2016;22(10):1176–1181.

- Chambers JD, Anderson JE, Wilkinson CL, et al. Variation in the coverage of disease-modifying multiple sclerosis drugs among US payers. Am J Pharm Benefits. 2017;9(5):155–159.

- National Hemophilia Foundation. MASAC recommendations concerning products licensed for the treatment of hemophilia and other bleeding disorders (Revised February 2020). 2020. Available at: https://www.hemophilia.org/sites/default/files/document/files/259_treatment.pdf. [Accessed May 8, 2020].

- Chambers JD, Kim DD, Pope EF, et al. Specialty drug coverage varies across commercial health plans in the US. Health Aff. 2018;37(7):1041–1047.

- National Association of Insurance Commissioners. Accident and health policy experience report. 2019. 2018. Available at: https://www.naic.org/prod_serv/AHP-LR-19.pdf. [Accessed August 24, 2020].

- Chambers JD, Panzer AD, Kim DD, et al. Variation in US private health plans' coverage of orphan drugs. Am J Manag Care. 2019;25(10):508–551.

- Knobe K, Berntorp E. Haemophilia and joint disease: pathophysiology, evaluation, and management. J Comorb. 2011;1:51–59.

- Food and Drug Administration. FDA approves emicizumab-kxwh for hemophilia A with or without factor VIII inhibitors. 2020. Available at: https://www.fda.gov/drugs/drug-approvals-and-databases/fda-approves-emicizumab-kxwh-hemophilia-or-without-factor-viii-inhibitors. [Accessed May 8, 2020].

- Chambers JD. Large health gains, but challenges for health care payers. What can we expect from gene therapies? In: 12th annual conference of the israeli society for pharmacoeconomics and outcomes research. Herzliya; 2019.

Appendix A. List of hemophilia A treatments

Appendix B. Commercial health plans included in the specialty drug evidence and coverage (SPEC) database

1. Aetna Inc.

2. Anthem Inc.

3. Blue Cross Blue Shield Massachusetts

4. Blue Cross Blue Shield Michigan

5. Blue Cross Blue Shield New Jersey

6. Blue Cross Blue Shield North Carolina

7. Blue Cross Blue Shield Tennessee

8. Carefirst Inc.

9. Centene Corporation

10. Cigna

11. EmblemHealth

12. Guidewell (Florida's Blue Cross and Blue Shield)

13. Health Care Service Corporation

14. Highmark Inc.

15. Humana Inc.

16. Independence Health Group

17. UnitedHealth Group

Note. Health plans listed in alphabetical order. Three of the largest 20 health plans were excluded because they only offered Medicare/Medicaid coverage (n = 2) or did not make their policies publicly available (n = 1).

Source: 2016 Accident and Health Policy Experience Report. Market Share Reports for the Top 125 Accident and Health Insurance Groups and Companies by State and Countrywide. Page 295. Available from https://www.naic.org/prod_serv/AHP-LR-16.pdf