Abstract

The Asian region has passed a long and rocky road during the past several decades to establish itself as the second leading regional biotech market globally. China has become the second largest pharmaceutical market while Japan holds a strong second position as the global hub for medical devices development and innovation. Pharmaceutical expenditure continues to outpace real GDP growth in most of these countries. The trend is likely to be continued for a decade ahead, driven by a myriad of factors ranging from aging populations, rapidly growing welfare and increased citizen expectations raising demand for novel medicines and technologies. Satisfaction of these unmet needs in terms of supply is coming from the large multinational companies in wealthier among these societies. Domestic born and largely state-owned manufacturing industries continue to play a crucial role in an array of middle-income countries. Global biotech hub of Singapore is hosting over 1.5 times more headquarters of large pharmaceutical companies than Beijing, Tokyo, Shanghai and Hong Kong combined together. Japanese Takeda, Astellas, Daiichi Sankyo and Otsuka and Chinese Sinopharm, Guangzhou Pharmaceuticals Corporation, SPH and Yunnan Baiyao are now enlisted in leading Top 25 pharmaceutical companies rankings as per their annual net revenues in 2020–2021. Global industry landscape is evolving with ever more Asian companies obtaining the sharp innovative competitiveness leading development of cutting-edge medical technologies. Asian societies demand for pharmaceuticals and medical services continue to be characterized with unmet needs and striving to increase supply capacities. Financial obstacles of affordability of life saving medicines to the ordinary citizens shall be gradually overcome with an array of reimbursement strategies and extended insurance coverage policies. Observing the broad landscape throughout Asian region, we may witness that optimism in terms of domestic real GDP growth and consecutive biotech industry forecasts remains firmly rooted in years to come. Biosimilars are not a focus of the paper.

Asian landscape in economic development

The Asian Region which consists of East and South-East Asia has been accelerating to become an engine of global manufacturing industry. This historical four-and-a-half decade's old trend began since Deng Xiaoping’s reforms of Chinese mainland policies in the late 1970s were adopted at the height of Cold War Era. Contemporary Asian region, alongside its many demographics and socioeconomic hurdles, experiences unseen progress in terms of building welfare societies. Typical mainstream economic theory distinguishes among the developed countries and regions of Japan, South Korea, Taiwan, Singapore, and Australia and emerging economies of India, Thailand, Indonesia, Malaysia, Vietnam, Bangladesh, the Philippines. China is being classified as middle-income nation and India is about to enter middle-income countries in per capita terms. Yet this is largely misleading because both are ultimate players in the global arena: China being by far the second largest economy in the world and India being the seventh largest one according to the International Monetary Fund.

Asian large economies either preferably industry-based or service-based ones have created each in their own unique terms large surpluses and gains expanding budgetary shares devoted to the health spending. Next to public one, private out-of-pocket expenditure growth has been bold and straightforward for many years and continues to grow further. Continuously expanding affordability line for medical goods and services among Asian citizens in rich coastal and urban regions has been clearly associated with higher living standards and broader societal demand for innovative medical technologies. Current estimates say that from 2010 share of 24% middle-class citizens in these societies shall jump as high as 65% in 2030Citation1. This profound change in most of the region’s nations with partial exceptions of Laos, Myanmar or CambodiaCitation2, will have a profound and lasting impact to attracting both domestic and foreign investment in pharmaceuticals and medical device manufacturing industriesCitation3. A good hint for understanding the changing landscape is comparison of health technology investment growth rates Asia vs U.S. during the previous five-year cycle: 43.9% versus 17.8% Composite Annual Growth Rates; CAGR (2014–2018)Citation4 ().

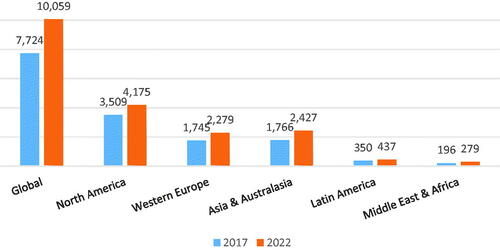

Graph 1. Health care spending (USD billion). Source: The Economic Intelligence Unit.

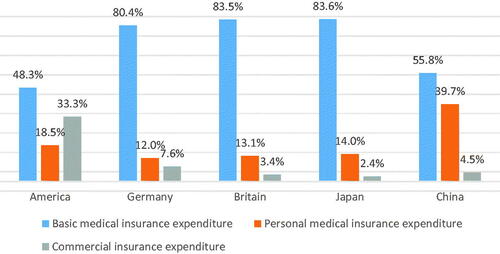

Graph 2. Comparison of the proportion of residents' medical payment.

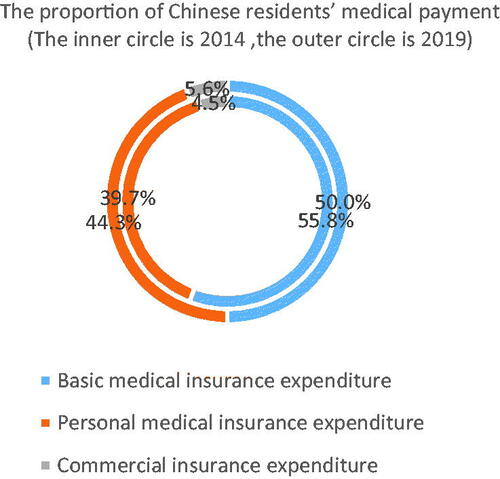

Graph 3. Comparison of the proportion of Chinese residents' medical payment. Source: Based on data from the World Health Organization Committee, the World Bank, the National Health Commission, the National Medical Security Administration, and the People's Bank of China.

Global pharmaceutical companies and foreign direct investment in Asia

The standard pathway for entering these markets for a foreign-born manufacturer, typically one based in Western Europe, Israel or North America was to purchase or negotiate a business deal with a domestic venture with certain influence. This coupling of cutting-edge biotechnology capability with strong domestic supply of skilled and educated labour force, was the driving force behind many success stories throughout this vast region. Asia Pacific pharmaceutical market being the second largest in the world after North America now in middle 2021, continues to increase its lead over Western Europe being third ranked regionCitation5. To describe the forefront of change in a picturesque manner, McKinsey Global Institute claims in its 2020 report: “Over the past decade, $1 of every $2 in new investment made worldwide went to Asian firms. In fact, $1 of every $3 in global investment went to China.” When we observe the presence of three major world economic regions in the G5000 list of the world’s largest companies by revenue, Asia headquartered firms now accounts for 43%, while Europe has 25% and North America (US and Canada) has 24% of the G5000Citation6. Overall regional health expenditure growth across Asian countries consolidates around 7% annually which by far exceeds the one both in Western Europe and North America. European Union’s average growth rate is estimated to be 3.9%Citation7 until 2024Citation8, while North America’s 5.4%. Projected total Asian market value should reach US$2.4 trillion in 2022. Given the prevailing revenue streams from branded medicines in comparison to generics, a large-scale survey of leadership of pharmaceutical manufacturers has shown that 39% of them still see Japan as the core market as opposed to 22% claiming the same for Chinese oneCitation9. Another exploration encircled a total of 509 life science and biotechnology executivesCitation10, approximately at 10% level representation of sectors across the China, India, Indonesia, Japan, Malaysia, the Philippines, Singapore, Bangladesh, South Korea, Thailand and Vietnam. Estimates grounded in this research claim that emerging market pharmaceutical spending should have risen up from US$249 billion in 2015, up to US$375 billion in 2020Citation11.

It is crucial to understand that pharmaceutical expenditure historical trends and future projections across Asia are far exceeding healthy real GDP growthCitation12 mostly ranging 5–% even today. Expanding populations, rising life expectancy coupled with sedentary life style and blossoming of NCDs are driving the need for medicines. State-owned health insurance funds and private insurance funds as payers seem set to increase their budgetary spending further. Despite the fact that riches regional markets such as Japan, South Korea and Singapore are largely saturated, most of this growth shall be driven by unmet medical needs among the emerging Asian markets. Convenient example are pain relief drugs with Asian segment comprising only 9% share globally while being home to 60% of world population. Growing awareness of therapeutic options available among the patients and prescribing physicians alike is coming with expanding affordability line and far more generous reimbursement coverage in many countries of the region. So this analgesics landscape is now rapidly changing for the betterCitation13. Across Asia here is a widespread ambition to build upon a comprehensive insurance coverage leading to the universal access to healthcare. Even far less wealthy countries are facing numerous challenges, like Indonesia and the Philippines who are making bold steps forward in this directionCitation14. Wealthier OECD Asian country members have far more ambitious development goals in their focusCitation15. Some surprising strategic initiatives come from Malaysia with an attempt to establish itself as a global pioneer in the expansion of halal pharmaceutical products, such as vaccines not derived from pigs. This particular market should have reached over US$130bn valuable sales worldwide by 2021Citation16.

Some peculiarities of South-East Asian ASEAN markets

ASEAN (The Association of Southeast Asian Nations) countries are mostly net importers of pharmaceuticalsCitation17. This is particularly evident given the emphasis on Active Pharmaceutical Ingredients(APIs) market. So far Singapore remains the only one capable of new drug development in terms of essentially innovative APIs. Unlike most of remaining nine ASEAN countries both China and IndiaCitation18 remain highly capable of independent manufacturing of APIs and intermediary pharmaceutical technology productsCitation19. More specifically Eastern China coastal regions specialize in small molecule targeted medicines such as those indicated in oncology and autoimmune diseasesCitation20. South China provinces are more involved with biologicals manufacturing. Most of country specific features of the development of pharmaceutical legislation and national developmental pathways in this arena are closely explained in recent WHO’s 2018 reportCitation21. Furthermore, there is pretty weak domestic competition in the ASEAN markets. Just like with drugs, ASEAN as a whole remains a net importer of medical devices. Vietnam, one of the most dynamic economies of an entire region, is a typical case that currently imports 90% of medical equipment from foreign manufacturers, out of which 55% comes from Japan, Germany, the US, China and SingaporeCitation22.

There are some peculiarities in domestic markets which might surprise an investor or market researcher coming even from the richest of OECD nations. For example, Chinese digital technology in treatment utilization among medical professionals, including clinical physicians, is exceptionally high. Even 94% of healthcare professionals in China use digital health apps, while the average value measured was 78% in a total of 15 countries including the U.S. and selected Asian nationsCitation23. The Asian Federation for Pharmaceutical Sciences (AFPS) founded 2007 has been one of several multilateral agencies largely facilitating the development of pharmaceutical research across ASEAN and East AsiaCitation24. Asia Pacific countries have adopted and implement the PIC/S GMP guide while ASEAN nations created a Mutual Recognition Agreement (MRA) and agreed to use the PIC/S GMP as basis for the MRACitation25. Sri Lanka regulatory developments are a convenient example of these changesCitation26. Thailand on the other hand is the case of a country with rather advanced public and private pharmaceutical sectorCitation27. Thai’s exceptionally large-scale tourism and medical tourism revenue streams have been constrained by Corona pandemics. Thus, the National Board of Investors has created a comprehensive strategy in an attempt to establish Thailand as the core biomedical technology hub for this region of Asia.Citation28 The foremost healthcare and medical industry hub has a large number of state of-the-art medical facilities,a fast-growing number of foreign patients,world-class medical facilities, premium healthcare specialists, high quality medical care, affordable price of medical treatment and large medical devices market for domestic and foreign investors. Harmonization of Good Manufacturing Practice criteriaCitation29 and introduction of regular international inspectionsCitation30 is greatly contributing to the mutual quality assurances in terms of pharmaceutical technology and fostering further trade of medicines among ASEAN nationsCitation31. This is ever more important given India’s global prestige in generic medicines manufacturing and China’s huge domestic manufacturing sector. Both of these large-scale markets have strong inner regulatory frameworksCitation32 and are capable to afford exporting pharmaceuticals with significantly lower wholesale and retail prices in comparison to small and medium enterprises typical for ASEAN nationsCitation33 ().

Table 1. Percentage of healthcare professionals who currently use any digital health technology or mobile health apps.

Consequences of widespread population ageing

There is a widespread population ageing across the Asian nations with very few young nations remaining such as Cambodia, whose under-15 population is estimated as 31% of general population. Yet for the most of this huge region, welfare consolidation and growth of purchasing power of an average citizen will be significantly constrained with consequences of third demographic transition. The leading case is Japan so far which has historically achieved welfare economy as early as of the 1960s. It was followed by the Newly Industrialized Asian Tiger Economies (South Korea, Singapore, Taiwan, SAR Hong Kong) during the 1980s, and ultimately mainland Chinese transformation becoming clearly visible mostly since the early 2000s. China will clearly be the fastest ageing large nation as we approach middle of XXI century. All of these issues related to the “Silver Cunami,” which is also known as Population Aging or Third Demographic Transition. are clearly presenting a fiscal sustainability challenge given the shrinking of work force and an ever increasing portion of retired and senior citizens. Yet at the same time these changes create a window of opportunity for Big Pharma and medical device industries. Extended longevity of Asian nations is coupled with expensive to treat chronic non-communicable diseases. NCDs in return drive the societal demand for hospital, outpatient and home-born medical care and rapid expansion of prescription medicines marketCitation12.

Responsible cost containment strategies

Various complex and comprehensive cost containment strategies are being developed across the region tailored to the national needs. Japanese Government’s Health Technology Assessment 2018 reform goes far seeking evidence for value-driven medical careCitation15. It is consistent in requesting reliable cost-effectiveness from manufacturers so that their medicines could obtain generous Japanese reimbursement under the national universal health insurance coverage scheme. Other important pharmaceutical policy initiatives such as Sakigake designation, foster the domestic innovation and first-ever global launches of cutting-edge innovative medicines in JapanCitation34. An array of domestic strategies has been adopted while reliance on cost-effectiveness analysis and annual price revisions of high budget impact drugs exceeding certain thresholds in sales, are among the most prominent innovations. Various risk-sharing agreements with multinational pharmaceutical manufacturers providing access to the expensive medicines to the vulnerable patient groups, despite Japanese lavish reimbursement policies are among others. It is crucial to emphasize that Japanese intellectual property protection in terms of brand name drugs patent life cycle of 20 + 5 years is exceptionally generous one. It allows the innovative pharma companies to harvest their revenue streams and compensate for the huge research and development costs they had during the product early life cycle stages. On the other hand, recent Japanese Pharmaceutical and Medicinal Device Agency PMDA being part of the Ministry of Health, Labor, and Welfare (MHLW) has a goal of 80% of generic substitution of brand name medicines following the patent expiry. These strategies to contain pharmaceutical budgetary bill had slow progression for many years due to traditional preference for quality by Japanese consumersCitation35 ().

In 2019, China's basic medical insurance system covers a population of 1.354 billion, with a population coverage rate of 96.7%. However, the coverage of basic medical insurance is broad but not deep, and residents' diverse medical insurance needs cannot be met. In 2014, the proportion of personal expenditure in Chinese residents' medical expenditure was about 39.7%, which is still higher than that of other developed countries, and this figure rose to 44.3% in 2019. China’s out-of-pocket rate of residents is still high. China as well has been rapidly expanding its insurance coverage policies both in spreading them across vast layers of population and extending the value of premiums in terms of services and drugs being provided to the ordinary citizens. There are also policies taking place among wealthiest of Asian economies to tackle “the drug lag” which refers to postponed, heavily delayed arrivals of most innovative medicines from the US and big EU5 markets to AsiaCitation36. This fact is now the object of thorough attention by the policy makers and such lags have been already substantially shortened in South Korea and Japan. China has accepted the challenge and this struggle has just beganCitation37. Some breakthrough achievements are visible in marketing approvals of top profile blockbuster drugs in oncology and autoimmune disease area.

Asian comprehensive digitalization in medicine

Asian technology hubs show the capacity to become crucial drivers of ongoing digitalization in medicineCitation38. The medical technology market in the Asian region has reached anticipated $133 billion in 2020. Generally speaking, medical devices are still not widely in use across the ASEAN nations’ hospitals and outpatient care which offers huge space for growth and market expansionCitation39. There is picturesque landscape of the healthcare startups across Asia: India (32%), China (22%), Singapore (11%), Japan (8%)Citation40. Yet one should not forget that Japan remains the fastest-growing medical technology market in the Asian region. Its decades-long history of high-tech innovations accompanied with strong engineering capabilities makes it home to the top medtech players. Particular strength of Japanese medical device innovation, driven by its own unmet needs is medical care for the elderly and associated solutions in robotics. Particular strength of Chinese rapidly growing R&D investment in this sector refers to the Artificial Intelligence application in E-health and clinical medicine. Exemplary breakthrough innovation was the pioneering global case of 5 G-network mediated robotic neurosurgery being conducted on a patient in Chinese PLA General Hospital in Beijing while surgeon Ling Zhipei was running real-time surgical intervention from South China's Hainan ProvinceCitation41.

Medical equipment manufacturing

South-East Asia offers a significant room of opportunity for medical equipment imports, given its growing demand and affordability. Public health spending exceeding 51%, private insurance market ranging up to 12% (Exception of Indonesia with 25%) and huge out-of-pocket private spending are frequently generating risk of catastrophic health care expenditure. This myriad of factors has driven many consecutive regional governments to adopt sets of reforms increasing public health spending. This largely refers to renewal and imports of hospital medical technology for diagnostics, treatment and rehabilitation. Background of such responsibility is immense social spending coming out of a boomerang effect. Hospital intensive care admissions of patients suffering from advanced or end stages of many intractable diseases ranging from mental disorders to cancer might be prohibitively expensive. Obviously, the cost of work absenteeism and opportunity cost of premature mortality and loss of working ability began to play a prominent role on the agenda of regional ministries of health and public health insurance fundsCitation42 ().

Table 2. The pharmaceutical industry is growing rapidly in Southeast Asia.

Market size of the medical devices market in the Asia has been steadily growing from approximately 67.5 billion U.S. dollars in 2016 up to $88.6 billion in 2020Citation43. Total estimated value by one of the leading multinational consultancies claims that an overall value of entire healthcare market in Asia reached $486.72 billion peak, back in 2019 just prior to Pandemics occurrenceCitation44. Exemplary case depicting the developments are remote patient monitoring systems. This segment of Asian market has witnessed a CAGR (composite annual growth rate) of 12.9% during the most of 2018–2023 period. Strong growth of demand for home-based monitoring devices is another notable feature of the entire regionCitation45. This trend has been largely driven by aging population, shrinking nursing and physician work force disposable and the need for cost-containment via avoidance of inpatient hospital care wherever possible. Gradual weakening of traditional family care giving across Asia is largely due to low fertility rates and less adult children being capable of taking care about their elderly parents. Another convenient landscape for observation is Asian surgical device market. One can notice that in this arena CAGR is estimated to endure at stable 4.6% over 2018–2026. Furthermore, Official Japanese e-Stat reports an average 2019 households spending on medical treatments at JPY 36,063. In the same fiscal 2019, Japanese families where spending approximately JPY 78,000 for medical servicesCitation46. Such expenditures coupled with ever growing burden of noncommunicable diseases (NCDs) will only drive the consumption higher. Such evolving demand for pharmaceuticals and medical devices due to expensive chronic NCDs such as diabetes or cancer is particularly prominent in China where almost 290 million of citizens are diagnosed with either one of the NCDs.

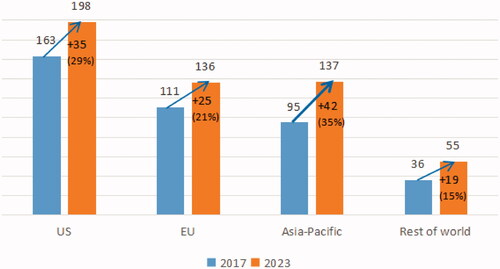

Over the foreseeable time horizon in future, Asia will inevitably become the most important growth engine of the medical technology market worldwide. Probably the most striking estimate is the one telling us that Asian entire medical device market is anticipated to reach value of up to 3,718.71 million in 2028. These dynamics should be driven by slightly slower post-Corona CAGR of 7.1% during the methodologically reliable forecasts covering 2021–2028 time horizonCitation47. Over the 2018–2023 observed period Asia has surpassed Europe becoming the second-largest regional market. Over these six years Asia continues to serve as major engine of global medtech market growth, contributing even 35% to the total incremental growthCitation48. In February 2021, 14 months since Corona pandemics was declared, it has reached an approximate value of $150 billion and an average CAGR of 9% being thus the most dynamic among leading global regions of medtech developmentCitation49 ().

Graph 4. Medtech, market size by region. Source: Health Research International.

Post-pandemic recovery pace among Asian nations

We may claim with solid grounds in evidence that most of Asian economies, with notable exceptions of IndiaCitation50 and Indonesia, have been spared the worst of the economic impact from the pandemic. Asia’s GDP growth of 6.8% in 2021 and forecasted 4.7% in 2022 are a testimony of such a landscape. Yet consequences of Corona-triggered global economic crisis have indeed been profound and may achieve an endurable impactCitation51. Throughout the vast APPAC region many governments have endorsed an array of emergency policies to provide relief from Pandemics attributable economic consequences. This refers largely to the traditional supply chains in pharmaceuticals, medical consumables and equipment, falling apart due to imposed international trade barriers. For the first time ever, Japanese and Chinese governments adopted blanket approval for the reimbursement of online medical consultations costs. The same was applicable to the medical insurance pay outsCitation52. There were other adaptive policy responses elsewhere out of which some are clearly here to remain for years. Typically, telehealth services had their widespread dissemination and promotion of services seen for the first time during the Pandemics. Yet as the time passes by the focus of India’s Ministry of Health and Family Welfare is shifting towards their core problem of NCDs. These same technologies are being used to secure access to essential telemedicine services for traditionally underserved rural populationsCitation53.

Smart hospitals construction and development presents another challenge and a room of opportunity and is beginning to be embraced by an array of regional Asian governments. In these unfolding developments, rapid pace of innovation and capability of substantial investment remains largely reserved for mainland ChinaCitation54, Hong Kong SARCitation55, Taiwan and South KoreaCitation56 so far. East Asia appears to heavily dominate the body of research evidence on smart hospitals since the early 2010s and continues with the same trendCitation57. Probably a very picturesque case revealing the movement of global innovation frontier towards Asia is related to the recent breakthrough in 5 G network mediated remote robotic surgery. Deep brain stimulation (DBS) implant was successfully implanted at the optimal target site in a patient suffering from Parkinson's disease. This was conducted at the First Medical Center of the Beijing-based PLAGH. The surgeon coordinated the operation from Department of Neurosurgery of PLAGH's Hainan Hospital situated in Sanya City, manipulating the surgical instruments 3,000 kilometres away from BeijingCitation58. These and many other technological breakthroughs throughout the entire Region are largely driving the ever-expanding demand for advanced medical care equipment. Singapore’s government adopted a strategy to make Singapore the pharmaceutical and medical device innovation hub of South-East Asia. Thailand’s and South Korea’s government continue large scale investment into the hospital sector in order to foster medical tourism competitiveness. These and ASEAN nations’ joint healthcare investment strategies are among the crown examples of such long term commitments driving the ever increasing demand for both domestic manufactured and imported cutting edge hospital technologiesCitation59.

Unfolding geo-economic developments largely affecting healthcare industries

Probably some of the most tempting milestone event for entire region is the adoption of RCЕP AgreementCitation60. RCEP refers to the regional comprehensive economic partnership, which is proposed in response to the development of economic globalization and regional economic integration. In order to strengthen regional economic integration, some countries have implemented "zero" tariffs, opened their markets to each other, and worked closely with each other to seek cooperation and development. On 15 November 2020, the world’s largest trade deal in terms of Gross Domestic Product – the “Regional Comprehensive Economic Partnership” (RCEP) – was signedCitation61. It has encircled a total of 15 countries, namely: China, Japan, South Korea, Australia and New Zealand + 10 ASEAN nations (Brunei, Cambodia, Indonesia, Laos, Malaysia, Myanmar, the Philippines, Singapore, Thailand, and Vietnam). It refers to a population size of 2.1 billion people and approximately 30% of the world’s GDP. For consumers and companies that rely on imported raw materials and components from countries in the region, the cost is greatly reduced due to the removal of tariffs and non-tariff barriers. Consumers will be able to buy high-quality and cheap products from countries in the region. The "threshold" for enterprises to enter countries in the region will be greatly reduced. Investors from countries in the region can obtain a certain period of stay and enjoy visa convenience. Personal travel abroad is more convenient and cheaper. The threshold for domestic workers to go abroad for employment will also be lowered. There are indications of an upcoming harmonization of pharmaceutical and medical device legislation and drug marketing approval and reimbursement pathwaysCitation62. If this is going to happen it may facilitate access of both domestic and external industry players across the borders in ways that were hard to imagine only few years ago. Yet the process appears to take time and real-world impact is difficult to forecast. Intellectual property protection laws will certainly become tighter and tax policies appear to become much more stringent compared to the historical standardsCitation63. Belt and Road Initiative (BRI) alongside its many naval trade routes, has its own regional consequences for the national health systems across Asia. We should not forget that Indonesia was its second point of public announcement back in 2013. The United Nations Development Policy and Analysis Division (DPAD) UN DESA’s has declared that BRI is aligned with the purposes and principles of the UN Charter and 2030 Agenda for Sustainable Development”Citation64. Introduction of the concept of “Health Silk Road”Citation65 focused on health and sustainable development together was another major milestoneCitation66. ASEAN as the oldest regional integration movement in the region remains exceptionally important for the spreading of domestic and foreign-investment driven innovation and manufacturing capacities in various fields of biotech industry. Yet one should understand that degree of legal integration within the ten countries of this alliance lags inclusive of pharmaceutical technology and hospital accreditation standards, still lags behind similar processes in the European Union and North AmericaCitation67.

Conclusive remarks

The vast Asia – Pacific region has passed a long and rocky road during the past several decades to establish itself as the second leading regional biotech market globally. China has become the second largest pharmaceutical market after the US while Japan still holds a strong second position as the global hub for medical devices development and innovation. It is also home to the strongest national medical equipment manufacturing sector in Asia. As the most important part of India's pharmaceutical industry, generic drugs are known as the "World Pharmacy." According to data from the International Government Benchmarking Association (IGBA), among the top five countries in the global generic drug penetration rate, India ranks first with a penetration rate of 97%. At present, India has 60,000 generic drug brands in 60 treatment categories and is the world's largest generic drug supplier, accounting for 20% of the global supply. Seven of the top 15 generic drug companies in the world belong to India. India holds a remarkable foothold on generic medicines manufacturing and probably strongest global presence among all the regional nations. Clearly pharmaceutical expenditure upward dynamics continues to outpace real GDP growth in most of these countries. Trend is likely to be continued for a decade ahead of us driven by a myriad of factors ranging from aging populations, rapidly growing welfare and increased citizen expectations raising demands for novel medicines and technologies. Satisfaction of these unmet needs in terms of supply is coming from the large multinational companies (Big Pharma) in wealthier among these societies. Domestic born and largely state-owned manufacturing industries continue to play a crucial role in an array of countries ranging from China to Vietnam. Growth is largely built on previous success stories. Probably the most striking case is the global biotech hub of Singapore hosting over 1.5 times more headquarters of large pharmaceutical companies than Beijing, Tokyo, Shanghai and Hong Kong combined together, inclusive of Takeda itself. State support has played pivotal role itself like was the case with South Korea’s establishment of cluster of biomedical industry centers in SeoulCitation68 or the Chinese 14th Five-Year Plan giving large emphasis on grand scale biotech capacity developmentCitation69. If we observe the Top 50 pharma companies 2020 ranking as per their annual revenues, we shall easily observe Japanese Takeda, Astellas, Daiichi Sankyo and Otsuka among the top 25Citation70. One step beyond, the Top 25 pharmaceutical companies in 2021, involve even four Chinese brands such as Sinopharm, Guangzhou Pharmaceuticals Corporation, SPH and Yunnan BaiyaoCitation71. It Is obvious that global industry landscape is evolving with more and more Asian companies obtaining the sharp innovative competitiveness among the cutting-edge medical technologies. For the medium term Asian societies demand for pharmaceuticals and medical services is going to be largely characterized with unmet needs and striving to increase supply capacities. The so-called “drug lag” in access to the expensive novel drugs such as monoclonal antibodies or targeted oncology agents shall remain substantial, particularly outside Japan, Korea, SAR HongKong and Singapore. These financial obstacles of affordability of life saving medicines to the ordinary citizens shall be gradually overcome with an array of reimbursement strategies and extended insurance coverage policies. Medical equipment markets will remain largely fragmented and dominated by domestic supply in most of mainland India, China and ASEAN. High-end medical robotics and advanced imaging diagnostics equipment exports will remain dominated by Japan and Korea in the mid-term. Observing the broad landscape throughout Asian region, we may witness that optimism in terms of domestic real GDP growth and consecutive biotech industry forecasts remains firmly routed in years to come.

Transparency

Declaration of funding

No funding was received to produce this article.

Declaration of financial/other relationships

No potential conflict of interest was reported by the author.

Peer reviewers on this manuscript have no relevant financial or other relationships to disclose.

Acknowledgements

Underlying research efforts behind this Editorial have been partially funded through Grant Em-CEAS of The Science Fund of the Republic of Serbia and Grant OI175014 of the Ministry of Education Science and Technological Development of the Republic of Serbia.

References

- Kohli HS, Sharma A, and Sood A, editors. Asia 2050: realizing the Asian century. New Delhi: SAGE Publications India; 2011. p. 1.

- Patel R, Patel A, Gohil T. Regulatory requirement for the approval of generic drug in Cambodia as per ASEAN Common Technical Dossier (ACTD). Int J Drug Reg Affairs. 2018;6(2):67–71. http://ijdra.com/index.php/journal/article/view/245

- Jakovljevic M, Lamnissos D, Westerman R, et al. Future health spending forecast in leading emerging BRICS markets in 2030-health policy implications. 2021. DOI:https://doi.org/10.21203/rs.3.rs-666830/v1

- Galen Growth Asia. Healthtech investment report. 2018. Available from: https://blog.galengrowth.com/ht-funding-fy-2018.

- Santillan VE. Asia pacific and its impact on the global pharmaceutical industry. 2019. Available from: https://ispe.org/pharmaceutical-engineering/ispeak/asia-pacific-and-its-impact-global-pharmaceutical-industry.

- McKinsey Global Institute. The future of Asia: decoding the value and performance of corporate Asia. New York: McKinsey Global Institute; 2020.

- Statista. Market growth forecast for certain pharmaceutical markets between 2019 and 2024. 2021.

- Statista, 2021. Projected global pharmaceutical market growth between 2019 and 2024, by region. Available from: https://www.statista.com/statistics/299702/world-pharmaceutical-market-growth-by-region-forecast/

- L.E.K. Special report: expanding into Asia-Pacific – life sciences opportunities and strategies for success. L.E.K. Consulting LLC; 2019. Available from: https://www.lek.com/insights/life-sciences-expansion-apac

- CPhI Southeast Asia report: executives call for track-and-trace schemes. 2020. Available from: https://cleanroomtechnology.com/news/article_page/CPhI_Southeast_Asia_Report_Executives_call_for_track-and-trace_schemes/161924.

- Kakkar V, Saini K. Outlook for Asian pharmaceutical industry. 2020. Available from: http://www.pharmabiz.com/NewsDetails.aspx?aid=121681&sid=21.

- Jakovljevic M, Timofeyev Y, Ranabhat CL, et al. Real GDP growth rates and healthcare spending–comparison between the G7 and the EM7 countries. Global Health. 2020;16(1):1–13.

- ACHEON Working Group; Kim Y-C, Ahn JS, Calimag MMP, et al. Current practices in cancer pain management in Asia: a survey of patients and physicians across 10 countries. Cancer Med. 2015;4(8):1196–1204.

- Ranabhat CL, Atkinson J, Park MB, et al. The influence of universal health coverage on life expectancy at birth (LEAB) and healthy life expectancy (HALE): a multi-country cross-sectional study. Front Pharmacol. 2018;9:960.

- Jakovljevic M, Sugahara T, Timofeyev Y, et al. Predictors of (in) efficiencies of healthcare expenditure among the leading Asian economies–comparison of OECD and non-OECD nations. RMHP. 2020;13:2261–2280.

- Ramli N, Amin N, Zawawi M, et al. Healthcare service: halal pharmaceutical in Malaysia, issues and challenges. Malaysian J Consum Fam Econ. 2018;20(S1):101–111.

- Lane EJ. Pharma market bets on ASEAN in focus ahead of economic pact. 2015. Available from: https://www.fiercepharma.com/manufacturing/pharma-market-bets-on-asean-focus-ahead-of-economic-pact.

- Ghosh PK. Novel active pharmaceutical ingredients from India: the actors-part-I. MGM J Med Sci. 2021;8(1):73.

- Yu PK. China's innovative turn and the changing pharmaceutical landscape. U Pac L Rev. 2019;51:593.

- Site selection for life sciences companies: Asia – KPMG. 2020. Available from: https://home.kpmg/ch/en/home/insights/2020/07/site-selection-for-life-sciences-companies-in-asia.html.

- How pharmaceutical systems are organized in Asia and The Pacific. Geneva: World Health Organization/Organisation for Economic Co-operation and Development; 2018.

- Vietnam’s medical devices industry: key market entry considerations. 2021. Available from: https://www.vietnam-briefing.com/news/vietnams-medical-devices-industry-key-market-entry-considerations.html/.

- Future Health Index 2019 Transforming healthcare experiences; Philips' fourth annual Future Health Index, based on a survey of 15,000 individuals and more than 3,100 healthcare professionals in 15 countries. Available from: https://images.philips.com/is/content/PhilipsConsumer/Campaigns/CA20162504_Philips_Newscenter/Philips_Future_Health_Index_2019_report_transforming_healthcare_experiences.pdf.

- The Asian Federation for Pharmaceutical Sciences (AFPS). Available from: https://www.afps2007.org/.

- Santillan VE. Asia Pacific and its impact on the global pharmaceutical industry. Available from: 2019. https://ispe.org/pharmaceutical-engineering/ispeak/asia-pacific-and-its-impact-global-pharmaceutical-industry.

- Thambavita D, Galappatthy P, Jayakody RL. Regulatory requirements for the registration of generic medicines and format of drug dossiers: procedures in Sri Lanka in comparison with selected regulatory authorities. J of Pharm Policy and Pract. 2018;11(1):1–8.

- Thavorn J, Klongthong W, Watcharadamrongkun S, et al. The impact of wisdom and pharmaceutical care on the corporate identity of Thai pharmacy retail stores. J Asian Fin Econ Business. 2021;8(1):317–326.

- Pattharapinyophong W. The opportunities and challenges for Thailand in becoming the medical tourism hub of the ASEAN region. J Manage Sci Suratthani Rajabhat Univ. 2019;6(1):1–16.

- Jabeen S, Sridhar S, Balamuralidhara V. Drug recall procedure in ASEAN countries. Res J Pharm Technol. 2019; 12(12):6041–6048. https://rjptonline.org/HTMLPaper.aspx?Journal=Research%20Journal%20of%20Pharmacy%20and%20Technology;PID=2019-12-12-72

- Quet M, Pordié L, Bochaton A, et al. Regulation multiple: pharmaceutical trajectories and modes of control in the ASEAN. Sci Technol Soc. 2018;23(3):485–503. https://doi.org/https://doi.org/10.1177/0971721818762935

- Hock SC. Harmonization of GMP inspection and benefits to ASEAN economic community. 2021. Available from: https://globalforum.diaglobal.org/issue/march-2021/harmonization-of-gmp-inspection-and-benefits-to-asean-economic-community/.

- Tongia A. The drug regulatory landscape in the ASEAN region. 2018. Available from: https://www.raps.org/news-and-articles/news-articles/2018/1/the-drug-regulatory-landscape-in-the-asean-region.

- Wong J, Chan S. China's emergence as a global manufacturing Centre: implications for ASEAN. Asia Pacific Business Rev. 2002;9(1):79–94.f.

- Kondo H, Hata T, Ito K, et al. The current status of sakigake designation in Japan, PRIME in the European Union, and breakthrough therapy designation in the United States. Ther Innov Regul Sci. 2017;51(1):51–54.

- Jakovljevic MB, Nakazono S, Ogura S. Contemporary generic market in Japan–key conditions to successful evolution. Exp Rev Pharmacoecon Outcomes Res. 2014;14(2):181–194.

- Hashimoto J, Ueda E, Narukawa M. The current situation of oncology drug lag in Japan and strategic approaches for pharmaceutical companies. Drug Information J. 2009;43(6):757–765.

- Li X, Yang Y. The drug lag issue: a 20-year review of China. Invest New Drugs. 2021;39(5):1389–1310.

- Hall R. The most exciting region in Asia for pharma and medical devices. 2017. Available from: https://www.lifescienceleader.com/doc/the-most-exciting-region-in-asia-for-pharma-and-medical-devices-0001.

- Hidayati N, Almasdy D, Putra AS. Global trade and health: an Indonesian perspective on the Asean medical device directive policy. BKM J Commun Med Public Health. 2021;37(1):1–6.

- Competition and profitability of pharmaceuticals in Asia. 2016. Available from: https://aseanup.com/competition-profitability-pharmaceuticals-asia/.

- First remote surgery in China conducted using 5G technology. https://www.globaltimes.cn/content/1142340.shtml.

- Munir Z. A Pharma Playbook for Success in Southeast Asia. 2016. https://www.bcg.com/publications/2016/pharma-playbook-success-southeast-asia.

- Statista Research Department. Market size of the medical devices market in the Asia/Pacific region from 2016 to 2020(in billion U.S. dollars). 2016. Available from: https://www.statista.com/statistics/717156/asia-pacific-region-medical-devices-market-size/.

- Asia-Pacific $486.72Bn Healthcare Industry Outlook, 2019. Cell therapy to emerge as leading market across regenerative medicine. ResearchAndMarkets.com, 2019. Available from: https://www.businesswire.com/news/home/20190320005277/en/Asia-Pacific-486.72Bn-Healthcare-Industry-Outlook-2019–-Cell-Therapy-to-Emerge-as-Leading-Market-Across-Regenerative-Medicine–-ResearchAndMarkets.com.

- Asia Pacific remote patient monitoring systems market share, size 2021 global statistics, growth factors, industry trends, competition strategies, revenue analysis, key players, regional analysis by forecast to 2024. 2021. Available from: https://www.newschannelnebraska.com/story/43737119/Asia%20Pacific%20Remote%20Patient%20Monitoring%20Systems%20Market%20Share,Size%202021%20Global%20Statistics,%20Growth%20Factors,%20Industry%20Trends,%20Competition%20Strategies,%20Revenue%20Analysis,%20Key%20Players,%20Regional%20Analysis%20by%20Forecast%20to%202024.

- Asia-Pacific general surgical devices market – growth, trends, COVID-19 impact, and forecasts (2021–2026). Available from: https://www.mordorintelligence.com/industry-reports/asia-pacific-general-surgical-devices-marke.

- Asia-Pacific Medical Devices Market – Industry Trends and Forecast to 2028; https://www.databridgemarketresearch.com/reports/asia-pacific-medical-devices-market.

- Agarwal A, Then F, Wu K. The rise and rise of Medtech in Asia. 2018. Available from: https://www.mckinsey.com/industries/pharmaceuticals-and-medical-products/our-insights/the-rise-and-rise-of-medtech-in-asia#.

- Burton P. Medtech’s Post-COVID paradigm in APAC. 2021. Available from: https://pharmaboardroom.com/articles/medtechs-post-covid-paradigm-in-apac/.

- Gauttam P, Patel N, Singh B, et al. Public health policy of India and COVID-19: diagnosis and prognosis of the combating response. Sustainability. 2021;13(6):3415.

- Krstic K, Westerman R, Chattu VK, et al. Corona-triggered global macroeconomic crisis of the early 2020s. IJERPH. 2020;17(24):9404.

- APAC healthcare sector opportunities grow as economies recover. 2021. Available from: https://www.business-sweden.com/insights/articles/APAC-healthcare-sector-opportunities/.

- Ganapathy K, Nukala L, Premanand S, et al. Telemedicine in camp mode while screening for noncommunicable diseases: a preliminary report from India. Telemed J E Health. 2020;26(1):42–50.

- Zhang H, Li J, Wen B, et al. Connecting intelligent things in smart hospitals using NB-IoT. IEEE Internet Things J. 2018;5(3):1550–1560.

- Ho CW-L, Caals K, Zhang H. Heralding the digitalization of life in post-pandemic East Asian societies. J Bioeth Inq. 2020;17(4):657–661. "

- Park J, Kim M. 2013, October. A study on the potential needs and market promotion of smart health in Korea. 2013 International Conference on ICT Convergence (ICTC). IEEE. p. 824–825.

- Rasoulian-Kasrineh M, Sharifzadeh N, Tabatabaei S-M. Smart hospitals around the world: a systematic review. 2021. Available from: https://www.researchsquare.com/article/rs-258174/latest.pdf. https://doi.org/https://doi.org/10.21203/rs.3.rs-258174/v1

- Yun G, Zhaoyi P, Qingqing C. China performs first 5G-based remote surgery on human brain. 2019. Available from: https://news.cgtn.com/news/3d3d774d7945444e33457a6333566d54/index.html.

- ASEAN investment report 2019 – FDI in services: focus on health care. Jakarta: ASEAN Secretariat; 2019.

- Chakraborty D, Chaisse J, Xu QIAN. Is it finally time for India's free trade agreements? The ASEAN “present” and the RCEP “future”. AsianJIL. 2019;9(2):359–391.

- Xi K. Asia-Pacific: world’s largest trade deal’s pharma impact too early to tell. 2020. https://pharmaboardroom.com/articles/asia-pacific-worlds-largest-trade-deals-pharma-impact-too-early-to-tell/.

- Shimizu K. The ASEAN economic community and the RCEP in the world economy. J Contemp East Asia Stud. 2021;10(1):1–23.

- Zhang Q, Fan Y. Comparative analysis of the tax burden level of RCEP countries. J Front Soc Sci Technol. 2021;1(6):35–41.

- UN DESA. Jointly building the “belt and road” towards the sustainable development goals. Available from: https://www.un.org/en/desa/jointly-building-%E2%80%9Cbelt-and-road%E2%80%9D-towards-sustainable-development-goals.

- Cao J. Toward a health silk road: China’s proposal for global health cooperation. China Q Int Strategic Stud. 2020;06(01):19–35. Available from: https://doi.org/https://doi.org/10.1142/S2377740020500013

- Tilman H, Ye Y, Jian Y. Health Silk Road 2020: a bridge to the future of health for all. 2021. Available from: https://papers.ssrn.com/sol3/papers.cfm?abstract_id=3830380.

- Ramesh T, Saravanan D, Khullar P. Regulatory perspective for entering global pharma markets. Pharma Times. 2011;43(9):15–20.

- Danieles A. South Korea to build a biomedical cluster in Seoul. 2016. https://clustercollaboration.eu/news/south-korea-build-biomedical-cluster-seoul.

- Schmid RD, Xiong X. Biotech in China 2021, at the beginning of the 14th five-year period (“145”). Appl Microbiol Biotechnol. 2021;105(10):3971–3915.

- Pharma 50: the 50 largest pharmaceutical companies in the world. Available from: https://www.drugdiscoverytrends.com/pharma-50-the-50-largest-pharmaceutical-companies-in-the-world/.

- Pharma 25 2021 Ranking. Available from: https://brandirectory.com/rankings/pharma/.

- Chongsuvivatwong V, Phua KH, Yap MT, et al. Health and health-care systems in Southeast Asia: diversity and transitions. Lancet. 2011;377(9763):429–437.