Abstract

Aims

The COVID-19 pandemic has claimed the lives of more than 800,000 people in the United States (US) and has been estimated to carry a societal cost of $16 trillion over the next decade. The availability of COVID-19 vaccines has had a profound effect on the trajectory of the pandemic, with wide-ranging benefits. We aimed to estimate the total societal economic value generated in the US from COVID-19 vaccines.

Methods

We developed a population-based economic model informed by existing data and literature to estimate the total societal value generated from COVID-19 vaccines by avoiding COVID-19 infections as well as resuming social and economic activity more quickly. To do this, we separately estimated the value generated from life years saved, healthcare costs avoided, quality of life gained, and US gross domestic product (GDP) gained under a range of plausible assumptions.

Results

Findings from our base case analysis suggest that from their launch in December 2020, COVID-19 vaccines were projected to generate $5.0 trillion in societal economic value for the US from avoided COVID-19 infections and resuming unrestricted social and economic activity more quickly. Our scenario analyses suggest that the value could range between $1.8 and $9.9 trillion. Our model indicates that the most substantial sources of value are derived from reduction in prevalence of depression ($1.9 trillion), gains to US GDP ($1.4 trillion), and lives saved from fewer COVID-19 infections ($1.0 trillion).

Limitations

Constructed as a projection from December 2020, our model does not account for the Delta or future variants, nor does it account for improvements in COVID-19 treatment.

Conclusions

The magnitude of economic benefit from vaccination highlights the need for coordinated policy decisions to support continued widespread vaccine uptake in the US.

Introduction

As of December 2021, the COVID-19 pandemic has claimed the lives of over 800,000 people in the United States (US), and has resulted in the most severe economic downturn since the Great DepressionCitation1,Citation2. Estimates have pegged the cost of the pandemic in the US at $16 trillion over the next decadeCitation3.

Effective COVID-19 vaccines create a broad range of societal benefits, from extending lives and avoiding hospitalizations to increasing economic output and improving quality of life by restoring unrestricted social and economic activity more quickly. As of December 2021, one vaccine, developed by Pfizer-BioNTech, has been fully approved by the US Food and Drug Administration, and two additional vaccines, developed by Moderna and Janssen, have been approved under emergency use authorization in the USCitation4–6. As of December 2021, 204.1 million Americans have been fully vaccinated, with an additional 37.8 million Americans who have received one dose of a two-dose regimen vaccineCitation7.

To assess ongoing policy discussions and investments already put into the development, manufacturing, and distribution of COVID-19 vaccines, as well as ongoing funding to increase vaccination rates, it is important to understand the societal value of COVID-19 vaccines in the US. Quantifying the magnitude of societal benefit from a vaccine provides important context for evaluating public policy proposals and new legislation, such as the Biden administration’s $1.9 trillion emergency relief plan which includes approximately $62 billion directed toward COVID-19 vaccination and testingCitation8. Using data from the Centers for Disease Control and Prevention (CDC) and published literature as inputs for a population-based economic model, we estimated the societal value of COVID-19 vaccines in the US.

Methods

To estimate the value of a COVID-19 vaccine, we modeled societal economic value gained over a 3.5-year time horizon from two primary components: (1) value from avoiding COVID-19 cases, and (2) value from resuming social and economic activity more quickly.

To estimate the societal economic value generated by a COVID-19 vaccine through these two channels, we compared the impact of the gradual introduction of COVID-19 vaccines starting at the end of 2020 (“vaccine scenario”), with a hypothetical scenario in which vaccines were never introduced (“no vaccine scenario”).

To estimate the societal economic value generated from COVID-19 vaccines, we relied on several assumptions and findings from prior analyses. We conducted a targeted review of existing CDC data, published literature, news articles, public reports, and trade press to identify the most relevant and up-to-date inputs for the economic model. Specifically, to estimate the value of COVID-19 cases avoided with a vaccine, we reviewed literature on COVID-19 case likelihoods (including hospitalizations and deaths) and healthcare costs and quality of life impacts associated with a COVID-19 infection. To estimate the value from resuming social and economic activity more quickly, we reviewed literature on the impact of the pandemic on GDP, healthcare costs associated with deferred care, depression prevalence, and excess deaths due to non-COVID-19 causes.

To minimize the risk of over-estimating COVID-19 vaccine benefits, we incorporated mutually exclusive societal value categories to reduce the risk of double-counting impacts. To address inherent uncertainty in the past and future trajectory of the COVID-19 pandemic, as well as forward-looking projections of societal value gained with COVID-19 vaccines, we conducted scenario analyses to assess the impact of changing key model assumptions on our findings. A detailed set of tables describing our model inputs, sources, and embedded assumptions is available in Supplemental Tables 1 and 2.

Value from avoiding COVID-19 cases

To estimate the number of COVID-19 cases avoided with a vaccine, we relied on epidemiology forecasts modeled by Bartsch et al. Citation9, which projected COVID-19 case counts over a 2.5-year time horizon with and without a vaccine under different efficacy, population coverage, and timing scenarios. We relied on CDC updates and published estimates from Q1 and Q2 2021 to inform base case inputs for these parameters: (1) average vaccine effectiveness of 90%Citation10, (2) 75% of Americans receiving the vaccineCitation7,Citation11, and (3) 30% of Americans exposed to COVID-19 before widespread vaccine rolloutCitation12. Although the actual percent of Americans exposed to COVID-19 at the time that vaccines became available remains uncertain, we assumed that there were four times as many actual cases than reported casesCitation13. Under our base-case assumptions, we used projections from Bartsch et al.Citation9 to estimate that approximately 150 million COVID-19 cases would be avoided in our vaccine scenario over our model’s 3.5-year period compared to our no vaccine scenario. We also included scenario analyses with a lower bound of 100 million COVID-19 cases avoided and upper bound of 200 million cases avoided consistent with varying vaccine effectiveness ranges. Among all estimated COVID-19 cases avoided, 30% of cases were assumed to be asymptomatic based on best estimates from the CDC in Q4 2020Citation14.

Across all projected cases of COVID-19 avoided with a vaccine, we estimated the economic value gained from the following three categories: (1) life years saved, (2) healthcare costs avoided, and (3) quality of life gained. Supplemental Table 1 lists the values, assumptions, and sources for the inputs used to estimate the economic value gained from these three categories. First, to estimate the value from life years saved, CDC data were used to estimate counts of avoided cases by age groupCitation15. We employed age-specific infection fatality rates (IFRs) from O’Driscoll et al.Citation16 and calculated remaining life expectancy by age group using the US Social Security Administration actuarial life tablesCitation17 to account for differences in COVID-19 mortality and life expectancies for people of various age groups when calculating years of life saved. We then applied a 3% discount rate to calculate present discounted years of life saved. We valued a life year at $150,000, as discussed below, and from the present value of life years gained, we subtracted age-specific total continued lifetime healthcare costs that would have been incurred if individuals had not died of COVID-19Citation18. Next, to estimate healthcare costs avoided, CDC estimates and published literature were used to inform the likelihood of COVID-19 hospitalization by age categoryCitation18,Citation19. We then calculated the average cost of hospitalization by using information on the cost and frequency of COVID-19 hospitalization across different insurance coverage categories (i.e. Medicare, Medicaid, private, uninsured)Citation20,Citation21. Finally, estimates of the quality of life gained from avoiding non-hospitalized symptomatic, non-critically hospitalized, and critically hospitalized COVID-19 cases within one year following infection were based on published literatureCitation22; uncertainty regarding long-term impacts from COVID-19 precluded an assessment of quality of life impact beyond one year post-infection.

Value from resuming unrestricted social and economic activity more quickly

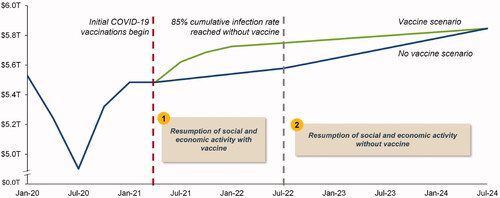

To estimate the value from restoring unrestricted social and economic activity more quickly with a COVID-19 vaccine, we estimated the difference in timing of when economic activity would begin to resume in the vaccine and no vaccine scenarios. For the vaccine scenario, we assumed resumption of social and economic activity would begin in Q2 2021 following the launch of COVID-19 vaccines in December 2020, which we observed in most areas of the US, and that a return to unrestricted social and economic activity would occur throughout 2021. For our no vaccine scenario, we assumed that a return to a near pre-pandemic state would occur after 15 months through a combination of natural immunity through infection and quarantine fatigue, paired with ongoing masking requirements. For natural immunity in the no vaccine scenario we assumed a population-level threshold of 85% cumulative exposure to COVID-19Citation23,Citation24.

To forecast the number of months until the threshold of 85% cumulative exposure would be reached without a vaccine after January 2021, we reviewed CDC COVID-19 case counts from Q3 and Q4 2020 to estimate the number of new COVID-19 cases per month without a vaccine, applying a multiplier of four to account for unreported casesCitation12,Citation13. We estimated that approximately 80 million individuals were exposed to COVID-19 by December 31, 2020, and that, on average, approximately 11 to 16 million individuals would be newly exposed to COVID-19 each month starting in January 2021 without a vaccine. Under these assumptions, we estimated that the US would reach 85% cumulative exposure between Q1 and Q3 2022 without vaccines. Based on these assumptions, our base case scenario estimated that restrictions on social and economic activity would begin to ease 15 months sooner in our vaccine scenario compared to the no vaccine scenario.

Based on the estimated difference in timing between the vaccine and no vaccine scenarios for resuming unrestricted social and economic activity, we estimated the economic value gained across the following four categories: (1) US gross domestic product (GDP) gained, (2) reduction in the prevalence of depression, (3) life years saved (non-COVID-19), and (4) healthcare costs avoided from deferred care. Findings from the targeted literature review were used to inform the calculations and assumptions for each category. The values, assumptions, and sources for these inputs can be found in Supplemental Table 2.

To estimate the value from US GDP gained, we relied on reported GDP growth projections from Goldman SachsCitation25 which evaluated forward-looking scenarios with and without COVID-19 vaccine availability. Specifically, using actual Q4 2020 nominal US GDP as a benchmarkCitation26, we applied real GDP growth rates from the Goldman Sachs forecastCitation27 to project US GDP under both scenarios. Given the inherent uncertainty in projecting long-term GDP impacts, we imposed a simplifying and conservative assumption that US GDP would converge in the vaccine and no vaccine scenarios 24 months after the 85% cumulative infection rate occurs in the no vaccine scenario (Q2 2024 in our base case) (). The US GDP gained was the difference between projected GDP in the vaccine and no vaccine scenarios.

Figure 1. US GDP projections (with and without COVID-19 vaccines). Abbreviations. GDP, gross domestic product; T, trillion; US, United States.

To estimate the value gained from depression avoided, we compared depression rates before the pandemic in 2019 to depression rates during the pandemic in 2020 using available literature to determine the increase in depression rates under social and economic restrictions across multiple depression severity categories. We assumed that depression prevalence would decrease to pre-pandemic levels by the difference in number of months it would take to resume social and economic activity in a no vaccine scenario compared with a vaccine scenario. We then used inputs from published literature to quantify the quality of life and healthcare cost impact associated with each depression severity category in order to estimate the value gained from reducing depression prevalenceCitation28–30. We used $150,000 as the value of a life year in the base case scenario as we did in other sections of our model related to quality of life.

For life years saved from reducing mortality from non-COVID-19 causes, we reviewed CDC data and published literature to estimate excess deaths not directly due to COVID-19 across multiple age categories from Q1 2020 to Q4 2020. Excess deaths were calculated as the total all-cause deaths in 2020 minus the average number of deaths per year from 2015 to 2019Citation31. We assumed, based on CDC data, that one-third of excess deaths during 2020 were not due to COVID-19Citation32. From this estimate, we projected monthly deaths avoided and life years gained from non-COVID-19 causes under a non-pandemic scenario and estimated the present value of these life years gained using $150,000 as the value of one life year and 3% as the discount rate. We subtracted the age-specific total continued lifetime healthcare costs that would have been incurred if individuals had not died from the present value of life years gainedCitation27.

Lastly, to estimate healthcare costs avoided for treating non-COVID-19 conditions, we relied on published estimates from McKinsey & CompanyCitation33 which assessed the one-year future cost impact of deferring necessary care during the COVID-19 pandemic across five common, chronic conditions: cancer, congestive heart failure, chronic obstructive pulmonary disease, diabetes, and hypertension.

Results

Value from avoiding COVID-19 cases

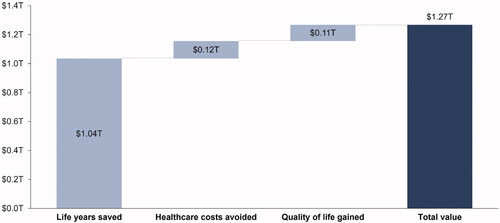

Among the 150 million total COVID-19 cases potentially avoided with vaccines, we estimated the total value from life years saved, healthcare costs avoided, and quality of life gained to be approximately $1.27 trillion across the 3.5 year time horizon ().

Figure 2. Value from avoiding COVID-19 cases. Abbreviation. T, trillion.

The largest source of value was estimated for life years gained ($1.04 trillion), resulting from approximately 815,000 deaths avoided and 7.7 million present discounted years of life saved. The total value from healthcare costs avoided was estimated to be approximately $120 billion, with a majority of the value accruing from patients covered by private insurance or Medicare. Finally, the value from quality of life gained from avoiding COVID-19 cases was estimated to be approximately $113 billion when accounting for quality of life losses up to one year post-infection for symptomatic cases.

Value from resuming unrestricted social and economic activity more quickly

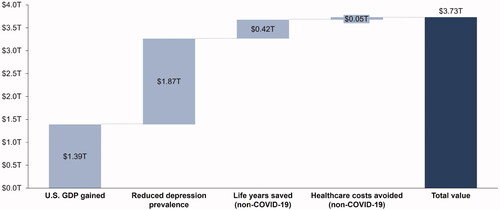

By easing restrictions on social and economic activity 15 months earlier, we estimated that the total value of COVID-19 vaccines from GDP gained, reduced prevalence of depression, life years saved (non-COVID-19 causes), and healthcare costs avoided (non-COVID-19 causes) would be approximately $3.73 trillion across the 3.5-year time horizon ().

Figure 3. Value from resuming unrestricted social and economic activity more quickly. Abbreviations. GDP, gross domestic product; T, trillion; US, United States.

The largest source of value from resuming social and economic activity 15 months earlier was due to reduced depression prevalence ($1.87 trillion), with nearly 50 million US adults estimated to have newly developed moderate-to-severe depression during the COVID-19 pandemic. We estimated that resuming unrestricted social and economic activity more quickly would also generate approximately $1.39 trillion in US GDP; this is due to businesses re-opening, increased earnings and employment, and increased productivity of the workforce when people no longer have to work from home or assist their children with online school. We found that COVID-19 vaccines would generate an additional $415 billion in value from non-COVID-19 life years saved and avoid $54 billion in non-COVID-19 healthcare costs resulting from deferred care.

Scenario analyses

To account for the inherent uncertainty in estimating total societal economic value from COVID-19 vaccines, scenario analyses were conducted with varying assumptions for the number of COVID-19 cases avoided with vaccines, impact of vaccines on resuming unrestricted social and economic activity more quickly, and value of lives saved with vaccines. The total estimated societal economic value ranged from approximately $1.83 trillion under our most conservative assumptions (COVID-19 cases avoided: 100 million; time difference between scenarios: 9 months; value per life year saved: $50,000) to approximately $9.92 trillion under our least conservative assumptions (COVID-19 cases avoided: 200 million; time difference between scenarios: 21 months; value per life year saved: $250,000) ().

Figure 4. Total societal value from COVID-19 vaccines (scenario analyses). Abbreviations. K, thousand; m, million; T, trillion.

Discussion

Vaccines are one of the most cost-effective health interventions available due to their ability to save lives, avoid treatment costs, and prevent potential long-term disabilityCitation34,Citation35. For example, by vaccinating children against diseases such as measles/mumps/rubella, hepatitis A and B, and pertussis, the US is estimated to save over $80 billion in health treatment and other costs to society in a single yearCitation36. Due to the high infection rate of COVID-19 and its impact on society as a whole, both in terms of illness and death and halting social and economic activity, COVID-19 vaccines have the potential to generate some of the largest costs savings in vaccine historyCitation37.

The findings from our analysis suggest that the availability of COVID-19 vaccines could generate approximately $5.0 trillion in total societal economic value in the US alone, or approximately 24% of 2020 US GDP. Using more versus less conservative assumptions produced a potential range of benefits from $1.83 trillion to $9.92 trillion, equivalent to approximately 9% and 47% of 2020 US GDP, respectivelyCitation38. Compared with the $16 trillion cost of the pandemic estimated over a 10-year time horizon by Cutler and SummersCitation3, our findings suggest that COVID-19 vaccines have reduced the total economic burden of the pandemic by approximately a third. Since our model’s time horizon is 3.5 years rather than the 10-year horizon used by Cutler and Summers, we are likely understating the overall benefit of COVID-19 vaccines relative to the burden of the pandemic. However, as the benefits of the vaccine are likely concentrated in this earlier period, this comparison is still meaningful. Our model suggests that the most substantial sources of societal economic value were derived from reduction in prevalence of depression ($1.87 trillion), gains to US GDP ($1.39 trillion), and lives saved from fewer COVID-19 infections ($1.04 trillion). These results are consistent with the January 2021 Economic Report of the PresidentCitation39, which estimated that accelerating vaccine availability by eight months (from September 2021 to January 2021) would save $2.4 trillion in health and economic costs. Our findings are also conservative compared to those of Thunstrom et al.Citation40, who estimated the value of lives lost and the present value of GDP lost to be $9.4 trillion and $13.7 trillion, respectively, over a 30-year horizon, in a scenario with restrictions and no vaccine. Lastly, our estimated societal economic value of COVID-19 vaccines is consistent with the findings of Acharya et al.Citation41. While we measured the benefit of COVID-19 vaccines by summing the value generated across different categories, Acharya et al.Citation41 applied an asset-pricing framework by observing stock market responses to vaccine progress and constructed a general equilibrium model to estimate the amount of wealth a representative agent would be willing to pay for a vaccine that ends the pandemic. Acharya et al.Citation41 found that the value of ending the COVID-19 pandemic is equal to 5-15% of total wealth, which, when applied to the total 2019 capital stock in the USCitation42, translates to $3.5 trillion to $10.5 trillion. This aligns with our potential range of benefits of $1.83 trillion to $9.92 trillion.

Our findings for gains to US GDP are consistent with an analysis from Q4 2020 that estimated a potential US GDP benefit of $1.1 trillion under more conservative assumptions, comparing a scenario with no vaccine for 2 years to a scenario with a vaccine becoming available to the public late in 2021Citation43. A separate analysis conducted by McKinsey and Oxford EconomicsCitation44 estimated that $0.8 trillion to $1.1 trillion in additional US GDP could be achieved by the end of 2022 in a scenario including a COVID-19 vaccine. A less conservative McKinsey studyCitation45 estimated that $5 trillion in US GDP could be gained in a scenario with virus containment compared to a scenario with virus recurrence. Lastly, MulliganCitation46 estimated that shutting down nonessential activities during the pandemic has cost $1.77 trillion in welfare per quarter, which equals $8.84 trillion over 15 months.

Our model used age-specific IFRs to compute an average COVID-19 fatality rate of 0.54% across all infections, which is consistent with generally accepted estimates from the clinical and scientific communityCitation47,Citation48. However, uncertainty regarding the true number of COVID-19 infections to date has led to uncertainty in mortality rates, with some reported IFRs ranging from 0.5% to 1.4%Citation49. Our estimated COVID-19 fatality rate of 0.54% is consistent with the estimated IFR for the adult population of 0.6% in Broughel and KotrousCitation50, as well as US state-specific IFRs ranging from 0.22% to 1.71% calculated by Irons and RafteryCitation51 using COVID-19 case, death, and testing data through March 7, 2021.

Similarly, there is uncertainty in the COVID-19 hospitalization rates across all infected cases due to the uncertainty in the true count of COVID-19 infections. Using hospitalization data by age from the literature, we calculated that 4.8% of symptomatic COVID-19 cases result in hospitalization, resulting in an overall hospitalization rate of 3.3% across symptomatic and asymptomatic COVID-19 infections. While these estimates generally align with COVID-19 hospitalization rates from Q4 2020Citation52, they are lower than other reported estimates which evaluated hospitalization rates for symptomatic cases during the first half of 2020Citation53,Citation54 and during the rise of the Delta variant in 2021Citation55.

While our model accounted for quality of life losses among hospitalized COVID-19 patients up to one year post-infection, scientific and clinical uncertainty currently prevent a robust assessment of long-term healthcare costs and quality of life impacts for patients after their initial COVID-19 infection. Early evidence suggests that between 10% to 20% of patients hospitalized for COVID-19 may need to be re-hospitalized within 60 days after discharge, primarily patients over 65 years old or with chronic conditionsCitation56. Furthermore, a subset of COVID-19 patients (termed patients with “long COVID”) may continue to experience lasting, debilitating symptoms following their initial infection over the course of several monthsCitation56–58. Longer-term relapsing or remitting COVID-19 symptoms among a subset of infected patients could lead to substantially higher healthcare costs and quality of life impacts, as suggested by Cutler and SummersCitation3 who estimated that the longer-term health impairments from COVID-19 may yield societal costs over $2.5 trillion over one year.

Our findings also highlight the high behavioral health burden from the COVID-19 pandemic, as well as the substantial value that may be generated from COVID-19 vaccines by reducing depression prevalence through restored social and economic functioning. Our estimate of $1.87 trillion in value from reduced depression prevalence is similar to previous estimates from Cutler and SummersCitation3, who estimated the one-year societal costs of mental health impairment from the COVID-19 pandemic to be approximately $1.6 trillion in the US. In our base case scenario, reduced depression prevalence is the largest source of value from resuming social and economic activity. While this finding may seem surprising when comparing to the value from GDP gained or lives saved, it is tied to the substantial increase in the prevalence of depression during the COVID-19 pandemic, with nearly 50 million US adults estimated to have newly developed moderate-to-severe depression. This outcome speaks to an important part of the burden of the pandemic that may be underemphasized and is consistent with a history of literature on the burden of depressionCitation59. However, the estimated value from reduced depression prevalence is also sensitive to the dollar value ascribed to a life year. The relative weight of the value from a reduction in depression prevalence is reduced if the value of a life year is decreased.

The results from our economic model also suggest that COVID-19 vaccines will generate approximately $469 billion in value by preventing deaths ($415 billion) and healthcare costs ($54 billion) from non-COVID-19 causes. These estimates regarding non-COVID-19 deaths are informed by prior research reported by the CDC that estimated approximately two-thirds of excess deaths in 2020 were due to COVID-19Citation32,Citation60. For findings related to non-COVID-19 healthcare costs avoided, our analysis focused on estimating costs from deferring healthcare across five common conditions and may underestimate the true long-term impact of deferred treatment, medical diagnoses, and surgeries from the COVID-19 pandemic across the broader US population.

Based on our review of various literature, for all categories relating to lives saved and quality of life impacts, we assumed a value of $150,000 for one life year in our base case scenarioCitation61–63. We chose to use the value of a life year rather than the value of a statistical life to avoid double-counting economic activity gains. While we used a baseline value of $150,000 for a life year, similar to other value assessment approaches, we examined a range of values as part of our scenario analyses.

Lastly, the value from restoring unrestricted social and economic activity more quickly with a COVID-19 vaccine is meant to account for (a) the pandemic’s effect on workers’ productivity, decreased income and spending, stay-at-home orders, and business closures (US GDP); (b) mental health deterioration due to fear of infection, loss of loved ones, and loneliness during quarantine (prevalence of depression); (c) the burden on the healthcare system due to lack of resources, in terms of personnel and hospital beds, that results in increased mortality from non-COVID-19 causes (life years saved); and (d) the delay in care for chronic conditions (healthcare costs from deferred care). While many studies analyzing the benefits of COVID-19 mitigation limit their focus to avoiding reductions in production, healthcare costs, and deathsCitation40,Citation50, we believe that overlooking the additional impacts of COVID-19 (i.e. mental health, excess deaths due to non-COVID-19 causes, and costs of deferring healthcare) would drastically understate the toll that the pandemic has taken on society as a whole, not just those who have been infected with COVID-19. For example, prior studies have reported that the effect of the pandemic on the US general public’s mental health is substantial, and this translates to quality of life reductions and higher healthcare costsCitation64,Citation65. However, even though we accounted for these additional impacts of the pandemic on society, our list is not comprehensive because we attempted to minimize the overlap of categories to reduce double-counting; therefore, our estimated economic value gained from restoring unrestricted social and economic activity more quickly likely remains conservative.

Limitations

Given the rapidly evolving landscape of scientific information related to the COVID-19 pandemic, as well as the inherent uncertainty in forecasting the value generated by novel health technologies like the COVID-19 vaccines, we generally sought conservative model inputs and reviewed alternative findings from published literature and reports to test the robustness of our results. We also attempted to incorporate the most up-do-date assumptions regarding the efficacy and coverage of COVID-19 vaccines as of December 2021. Of note, our model was constructed as a projection of vaccine and no vaccine scenarios beginning from the real-world launch of vaccines in December 2020. It therefore did not explicitly account for the Delta variant of the COVID-19 virus, which became the dominant strain in July 2021, or any future variantsCitation66. The data available and incorporated into our model was based mainly on the Alpha variant which was circulating in the US at the end of 2020 and first half of 2021Citation67. While the Delta variant is more contagious, the vaccines have so far continued to show effectiveness in preventing COVID-19 hospitalizations and deathCitation68. CDC guidelines recommend booster doses to all adults, based on studies showing that after inoculation against COVID-19, vaccine efficacy and immunity may decrease over timeCitation69. The range of cases avoided presented in our scenario analyses indirectly accounts for varying uptake of booster doses and potential waning immunity. In addition, our model did not explicitly account for potential future improvements in therapeutics and other treatments which may reduce the likelihood of death from COVID-19 infection over time.

We likely underestimated the long-term quality of life impacts and healthcare costs from avoiding COVID-19 cases. Due to scientific and clinical uncertainty of long-term healthcare costs and quality of life impacts, we focused on the quality of life effects only in the first year post-hospitalization due to COVID-19, and therefore, may understate the quality of life benefits from the vaccine. Additionally, while our estimated healthcare costs due to COVID-19 hospitalization were separated by age and insurance coverage category, we did not account for increased costs due to intensive care unit admission and ventilation; thus, these healthcare costs avoided were likely understated as well.

Additionally, we may have underestimated the full vaccine benefits generated from restoring unrestricted social and economic activity more quickly. To be conservative, we measured the benefit from reducing depression prevalence but did not account for reductions in other mental health conditions that have been exacerbated due to COVID-19, such as anxiety, substance abuse disorder, and post-traumatic stress disorder. However, reduced prevalence of depression may also reduce the prevalence of these disordersCitation33. Additionally, we assumed that those with mild depression during the pandemic incurred no quality of life reduction, and we did not account for the gains in utility experienced by the general population due to reduced health risk and reduced fear of contagion when vaccines became widely availableCitation70,Citation71. We also did not account for the potentially substantial long-term economic benefits generated by COVID-19 vaccines stemming from avoided education disruption since these benefits would overlap with the value from US GDP gained. Projections have estimated that average lost earnings resulting from the COVID-19 pandemic may reach $110 billion each year among current K-12 students, with greater learning loss impacts experienced by Black, Hispanic, Indigenous, and low-income studentsCitation72.

Lastly, we did not attempt to perform a full cost-benefit analysis for COVID-19 vaccines and instead focused on the benefits. To conduct a cost-benefit analysis, one should incorporate the costs of vaccines, which may include the manufacturing, transportation, and administration of vaccines, in addition to lost wages for those who would have to take unpaid time off to receive the vaccine.

Conclusions

Our economic analysis conservatively estimates that COVID-19 vaccines generate $5.0 trillion in overall societal economic value for the US across a 3.5-year time horizon, with scenario analyses suggesting value ranging from $1.8 trillion to $9.9 trillion. Importantly, these estimates do not capture potential benefits from reducing disruption to K-12 education. Our results highlight the substantial benefits generated from COVID-19 vaccines and the importance of coordinated US policy decisions to support rapid and widespread vaccine uptake.

Transparency

Declaration of funding

This research was funded by Janssen Pharmaceuticals, Inc.

Declaration of financial/other interests

MMF and BB are or were employees of Janssen Pharmaceuticals, Inc., which is a manufacturer of a COVID-19 vaccine. NK, ES, JL, JM, YS, and PL are employees of Analysis Group, which received consulting fees from Janssen Pharmaceuticals, Inc. The peer reviewers on this manuscript have received an honorarium from JME for their review work. A reviewer on this manuscript has disclosed that they are currently an advisor to NK on another valuation project–but one unrelated to this COVID-19 topic. The other peer reviewers on this manuscript have no other relevant financial relationships or otherwise to disclose.

Author contributions

NK, ES, MMF, BB, and PL conceived the study. All authors contributed to the study design. JL led the literature search, data collection, and analysis. All authors were involved in the interpretation of the results. JL, JM, and YS drafted the manuscript, and NK, ES, PL, MMF, and BB critically revised it. All authors have approved the final version of the manuscript.

Previous presentations

Not applicable.

Supplemental Material

Download PDF (130.5 KB)Acknowledgements

We thank Wei Wei Magnuson and John Jarvis for assistance with the literature review, data collection, and analysis, and Anupam Jena for comments on an earlier manuscript draft. Editorial assistance was provided by Shelley Batts, PhD, an employee of Analysis Group, Inc.

References

- Gopinath G. The great lockdown: Worst economic downturn since the great depression. 2020. [cited 2021 Jan 14]. Available from: https://blogs.imf.org/2020/04/14/the-great-lockdown-worst-economic-downturn-since-the-great-depression/.

- Centers for Disease Control and Prevention (CDC). United States COVID-19 cases, deaths, and laboratory testing (NAATs) by state, territory, and jurisdiction. 2021. [cited 2021 Dec 20]. Available from: https://covid.cdc.gov/covid-data-tracker/#cases_casesper100klast7days.

- Cutler DM, Summers LH. The COVID-19 pandemic and the $16 trillion virus. JAMA. 2020;324(15):1495–1496.

- US Food and Drug Administration. FDA approves first COVID-19 vaccine. 2021. [cited 2021 Aug 31]. Available from: https://www.fda.gov/news-events/press-announcements/fda-approves-first-covid-19-vaccine.

- US Food and Drug Administration. Moderna COVID-19 Vaccine. 2021. [cited 2021 Jan 19]. Available from: https://www.fda.gov/emergency-preparedness-and-response/coronavirus-disease-2019-covid-19/moderna-covid-19-vaccine.

- US Food and Drug Administration. Janssen COVID-19 Vaccine. 2021. [cited 2021 Jun 7]. Available from: https://www.fda.gov/emergency-preparedness-and-response/coronavirus-disease-2019-covid-19/janssen-covid-19-vaccine.

- The New York Times. See how the vaccine rollout is going in your state. 2021. [cited 2021 Dec 20]. Available from: https://www.nytimes.com/interactive/2020/us/covid-19-vaccine-doses.html?auth=login-email&login=email.

- Kapur S, Sarlin B. What's in the $1.9 trillion COVID bill Biden just signed? You might be surprised. 2021. [cited 2021 Jun 7]. Available from: https://www.nbcnews.com/politics/congress/what-s-1-9-trillion-covid-bill-biden-just-signed-n1260719.

- Bartsch SM, O'Shea KJ, Ferguson MC, et al. Vaccine efficacy needed for a COVID-19 coronavirus vaccine to prevent or stop an epidemic as the sole intervention. Am J Prev Med. 2020;59(4):493–503.

- Katella K. Comparing the COVID-19 vaccines: How are they different? 2021. [cited 2021 Jun 7]. Available from: https://www.yalemedicine.org/news/covid-19-vaccine-comparison.

- Gu Y. Path to normality: 2021 outlook of COVID-19 in the US. 2021. [cited 2021 Jun 7]. Available from: https://covid19-projections.com/path-to-herd-immunity/#comparison-projected-vs-actual.

- COVID Data Tracker. Trends in number of COVID-19 cases and deaths in the US reported to CDC, by state/territory. 2021. [cited 2021 Jun 7]. Available from: https://covid.cdc.gov/covid-data-tracker/#trends_dailytrendscases.

- Beusekorn MV. Study: US COVID cases, deaths far higher than reported. 2021. [cited 2021 Jun 7]. Available from: https://www.cidrap.umn.edu/news-perspective/2021/01/study-us-covid-cases-deaths-far-higher-reported.

- Centers for Disease Control and Prevention (CDC). COVID-19 pandemic planning scenarios. 2021. [cited 2021 Jun 7]. Available from: https://www.cdc.gov/coronavirus/2019-ncov/hcp/planning-scenarios.html.

- Centers for Disease Control and Prevention (CDC). Demographic trends of COVID-19 cases and deaths in the US reported to CDC. 2020. [cited 2021 May 27]. Available from: https://covid.cdc.gov/covid-data-tracker/#demographics.

- O'Driscoll M, Ribeiro Dos Santos G, Wang L, et al. Age-specific mortality and immunity patterns of SARS-CoV-2. Nature. 2021;590(7844):140–145.

- Social Security Administration. Actuarial life table. 2019. [cited 2021 Aug 31]. Available from: https://www.ssa.gov/oact/STATS/table4c6.html.

- Centers for Disease Control and Prevention (CDC). COVID-19: Hospitalization and death by age. 2020. [cited 2020 Nov 19]. Available from: https://www.cdc.gov/coronavirus/2019-ncov/covid-data/investigations-discovery/hospitalization-death-by-age.html.

- Bhatia R, Klausner J. Estimating individual risks of COVID-19-associated hospitalization and death using publicly available data. PLoS One. 2020;15(12):e0243026.

- Glied SA, Zhu B, Chakraborty O, et al. Who will pay for COVID-19 hospital care: Looking at payers across states. 2020. [cited 2021 Jan 22]. Available from: https://www.commonwealthfund.org/blog/2020/who-will-pay-covid-19-hospital-care-looking-payers-across-states.

- Sloan C, Markward N, Young J, et al. COVID-19 hospitalizations projected to cost up to $17B in US in 2020. 2020. [cited 2021 Jan 22]. Available from: https://avalere.com/insights/covid-19-hospitalizations-projected-to-cost-up-to-17b-in-us-in-2020#:∼:text=Results,through%20the%20end%20of%202020.

- Department of Health and Social Care, Office for National Statistics, Government Actuary's Department and Home Office. Direct and indirect impacts of COVID-19 on excess deaths and morbidity: Executive summary. 2020. [cited 2020 Nov 23]. Available from: https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/907616/s0650-direct-indirect-impacts-covid-19-excess-deaths-morbidity-sage-48.pdf.

- MU Health Care. COVID-19 vaccine key to reaching ‘herd immunity’. 2021. [cited Jun 7 2021]. Available from: https://www.muhealth.org/our-stories/covid-19-vaccine-key-reaching-herd-immunity.

- INTEGRIS Health. What is herd immunity? 2021. [cited 2021 Jun 7]. Available from: https://integrisok.com/resources/on-your-health/2021/may/herd-immunity.

- Hatchett R, Lipsitch M, Hatzius J. COVID-19: Where we go from here. 2020. [cited 2020 Dec 11]. Available from: https://www.goldmansachs.com/insights/pages/covid-19-where-we-go-from-here-f/report.pdf.

- US Bureau of Economic Analysis. Gross Domestic Product [NA000334Q]. 2021. [cited 2021 Jun 7]. Available from: https://fred.stlouisfed.org/series/NA000334Q.

- Sawyer B, Claxton G, Peterson-KFF Health Systems Tracker. How do health expenditures vary across the population? 2019. [cited 2021 Jan 22]. Available from: https://www.healthsystemtracker.org/chart-collection/health-expenditures-vary-across-population/.

- Ettman CK, Abdalla SM, Cohen GH, et al. Prevalence of depression symptoms in US adults before and during the COVID-19 pandemic. JAMA Netw Open. 2020;3(9):e2019686.

- Parsonage M. The economic and social costs of mental illness. 2003. [cited 2021 Jan 22]. Available from: https://www.researchgate.net/publication/308378405_The_economic_and_social_costs_of_mental_illness.

- Birnbaum HG, Kessler RC, Kelley D, et al. Employer burden of mild, moderate, and severe major depressive disorder: mental health services utilization and costs, and work performance. Depress Anxiety. 2010;27(1):78–89.

- Centers for Disease Control and Prevention (CDC). Excess deaths associated with COVID-19, weekly deaths by state and age. 2021 [cited 2021 May 27]. Available from: https://www.cdc.gov/nchs/nvss/vsrr/covid19/excess_deaths.htm.

- Rossen LM, Branaum AM, Ahmad FB, et al. Excess deaths associated with COVID-19, by age and race and ethnicity – United States, January 26-October 3, 2020 2020. [cited 2021 Jan 22]. Available from: https://www.cdc.gov/mmwr/volumes/69/wr/mm6942e2.htm.

- Coe H, Enomoto K, Finn P, et al. Understanding the hidden costs of COVID-19's potential impact on US healthcare. 2020. [cited 2020 Nov 4]. Available from: https://www.mckinsey.com/industries/healthcare-systems-and-services/our-insights/understanding-the-hidden-costs-of-covid-19s-potential-impact-on-us-healthcare.

- Rémy V, Zöllner Y, Heckmann U. Vaccination: the cornerstone of an efficient healthcare system. J Mark Access Health Policy. 2015;3(1):27041. v3.

- VoICE. Vaccines are among the most cost-effective health interventions available. 2019. [cited 2021 Jun 21]. Available from: https://immunizationevidence.org/key-concepts/vaccines-are-among-the-most-cost-effective-health-interventions-available/.

- Loria K. 7 facts about vaccines that show why they're one of the most important inventions in human history. 2015. [cited 2021 Jul 21]. Available from: https://www.businessinsider.com/why-vaccines-are-so-important-2015-2.

- Bloom DE, Cadarette D, Ferranna M. The societal value of vaccination in the age of COVID-19. Am J Public Health. 2021;111(6):1049–1054.

- Bureau of Economic Analysis. Gross Domestic Product, 4th Quarter and Year 2020 (Advance Estimate). 2021. [cited 2021 Nov 30]. Available from: https://www.bea.gov/news/2021/gross-domestic-product-4th-quarter-and-year-2020-advance-estimate.

- The White House, Council of Economic Advisers. Economic report of the President together with the annual report of the Council of Economic Advisers. 2021. [cited 2021 Jan 19]. Available from: https://www.whitehouse.gov/wp-content/uploads/2021/01/Economic-Report-of-the-President-Jan2021.pdf.

- Thunström L, Newbold SC, Finnoff D, et al. The benefits and costs of using social distancing to flatten the curve for COVID-19. J Benefit Cost Anal. 2020;11(2):179–195.

- Acharya VV, Johnson T, Sundaresan S, et al. The value of a cure: an asset pricing perspective (no. w28127). 2020. [cited 2021 Nov 30]. Available from: https://www.nber.org/system/files/working_papers/w28127/w28127.pdf.

- US Bureau of Economic Analysis. Capital Stock at Constant National Prices for United States. 2021. [cited 2021 Nov 30]. Available from: https://fred.stlouisfed.org/series/RKNANPUSA666NRUG.

- Walmsley T, Rose A, Wei D. The impacts of the coronavirus on the economy of the United States. EconDisCliCha. 2021;5(1):1–52.

- Azimi T, Conway M, Latkovic T, et al. COVID-19 vaccines meet 100 million uncertain Americans. 2020. [cited 2021 Jan 11]. Available from: https://www.mckinsey.com/industries/pharmaceuticals-and-medical-products/our-insights/covid-19-vaccines-meet-100-million-uncertain-americans.

- Smit S, Hirt M, Dash P, et al. Crushing coronavirus uncertainty: the big ‘unlock’ for our economies. 2020. [cited 2021 Jan 8]. Available from: https://www.mckinsey.com/business-functions/strategy-and-corporate-finance/our-insights/crushing-coronavirus-uncertainty-the-big-unlock-for-our-economies.

- Mulligan CB. Economic activity and the value of medical innovation during a pandemic. J Benefit-Cost Anal. 2020;27060:1–24.

- McNeil DG. The pandemic's big mystery: how deadly is the coronavirus. 2020. [cited 2021 Jan 8]. Available from: https://www.nytimes.com/2020/07/04/health/coronavirus-death-rate.html.

- Beasley D. COVID-19 fatality rate down 30% since April, study finds. 2020. [cited 2021 Jan 8]. Available from: https://www.reuters.com/article/us-health-coronavirus-fatality-idUSKBN27S39D.

- Oliver S. EtR Framework: Moderna COVID-19 vaccine. 2020. [cited 2021 Jan 8]. Available from: https://www.cdc.gov/vaccines/acip/meetings/downloads/slides-2020-12/slides-12-19/04-COVID-Oliver.pdf.

- Broughel J, Kotrous M. The benefits of coronavirus suppression: a cost-benefit analysis of the response to the first wave of COVID-19 in the United States. PLoS One. 2021;16(6):e0252729.

- Irons NJ, Raftery AE. Estimating SARS-CoV-2 infections from deaths, confirmed cases, tests, and random surveys. Proc Natl Acad Sci USA. 2021;118(31):e2103272118.

- Jha AK. COVID-19 hospitalization rates are dropping. That’s terrible news. 2020. [cited 2021 Jan 8]. Available from: https://www.washingtonpost.com/outlook/2020/12/07/covid-hospitalization-rates-dropping/.

- Ferguson N, Laydon D, Nedjati Gilani G, et al. Report 9: Impact of non-pharmaceutical interventions (NPIs) to reduce COVID-19 mortality and healthcare demand. 2020. [cited 2021 Jan 11]. Available from: https://www.imperial.ac.uk/media/imperial-college/medicine/sph/ide/gida-fellowships/Imperial-College-COVID19-NPI-modelling-16-03-2020.pdf.

- Bartsch SM, Ferguson MC, McKinnell JA, et al. The potential health care costs and resource use associated with COVID-19 in the United States. Health Aff. 2020;39(6):927–935.

- Twohig KA, Nyberg T, Zaidi A, et al. Hospital admission and emergency care attendance risk for SARS-CoV-2 Delta (B. 1.617. 2) compared with alpha (B. 1.1. 7) variants of concern: a cohort study. Lancet Infect Dis. 2021;22(1):35–42.

- Belluck P. He was hospitalized for COVID-19. Then hospitalized again. And again. 2020. [cited 2021 Jan 11]. Available from: https://www.nytimes.com/2020/12/30/health/covid-hospital-readmissions.html.

- Barber C. The problem of 'long haul' COVID. 2020. [cited 2021 Jan 8]. Available from: https://www.scientificamerican.com/article/the-problem-of-long-haul-covid/.

- Rabin RC. Some COVID survivors haunted by loss of smell and taste. 2021. [cited 2021 Jan 8]. Available from: https://www.nytimes.com/2021/01/02/health/coronavirus-smell-taste.html.

- Greenberg PE, Fournier A-A, Sisitsky T, et al. The economic burden of adults with major depressive disorder in the United States (2010 and 2018). Pharmacoeconomics. 2021;39(6):653–665.

- Woolf SH, Chapman DA, Sabo RT, et al. Excess deaths from COVID-19 and other causes, March-July 2020. JAMA. 2020;324(15):1562–1564.

- Merrill D. No one values your life more than the federal government. 2017. [cited 2021 Jan 3]. Available from: https://www.bloomberg.com/graphics/2017-value-of-life/.

- Aldy JE, Viscusi WK. Age differences in the value of statistical life: revealed preference evidence. Rev Environ Econ Policy. 2007;1(2):241–260.

- Conover C, The Apothecary. How economists calculate the costs and benefits of COVID-19 lockdowns. 2020. [cited 2021 Feb 3]. Available from: https://www.forbes.com/sites/theapothecary/2020/03/27/how-economists-calculate-the-costs-and-benefits-of-covid-19-lockdowns/?sh=259094846f63.

- Bueno-Notivol J, Gracia-García P, Olaya B, et al. Prevalence of depression during the COVID-19 outbreak: a Meta-analysis of community-based studies. Int J Clin Health Psychol. 2021;21(1):100196.

- Vindegaard N, Benros ME. COVID-19 pandemic and mental health consequences: Systematic review of the current evidence. Brain Behav Immun. 2020;89:531–542.

- Crist C. Delta becomes dominant coronavirus variant in US. 2021. [cited 2021 Oct 4]. Available from: https://www.webmd.com/lung/news/20210707/delta-dominant-us-coronavirus-variant#:∼:text=July%207%2C%202021%20%2D%2D%20The.,1.617.

- Garcia de Jesús E. Here’s what we know about B.1.1.7, the U.S.’s dominant coronavirus strain. 2021. [cited 2021 Sep 13]. Available from: https://www.sciencenews.org/article/covid-coronavirus-b117-variant-us-dominant-strain.

- Sakay YN. Here’s how well COVID-19 vaccines work against the Delta variant. 2021. [cited 2021 Sep 13]. Available from: https://www.healthline.com/health-news/heres-how-well-covid-19-vaccines-work-against-the-delta-variant.

- Centers for Disease Control and Prevention (CDC). COVID-19 Vaccine Booster Shots. 2021. [cited 2021 Dec 6]. Available from: https://www.cdc.gov/coronavirus/2019-ncov/vaccines/booster-shot.html.

- Lakdawalla DN, Doshi JA, Garrison Jr LP, et al. Defining elements of value in health Care-A Health Economics Approach: An ISPOR Special Task Force Report [3]]. Value Health. 2018;21(2):131–139.

- Cerda AA, García LY. Factors explaining the fear of being infected with COVID‐19. Health Expect. 2021;0:1–7.

- Dorn E, Hancock B, Sarakatsannis J, et al. COVID-19 and student learning in the United States: The hurt could last a lifetime. 2020. [cited 2020 Nov 23]. Available from: https://www.mckinsey.com/industries/public-and-social-sector/our-insights/covid-19-and-student-learning-in-the-united-states-the-hurt-could-last-a-lifetime.