?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The sovereign debt crisis led to financial difficulties for European firms and a decline in the use of labour input. We use qualitative firm-level data for 24 European countries, collected within the third wave of the Wage Dynamics Network (WDN3) of the ESCB, to propose a cross-country analysis of the relationship between a credit shock and labour markets. We first derive a set of indices measuring difficulties in accessing the credit market for the period 2010–2013. Second, we provide a description of the relationship between credit difficulties and changes in labour input, both along the extensive and the intensive margins as well as on wages. We find strong and significant correlation between credit difficulties and adjustments along both the extensive and the intensive margin. In the presence of credit market difficulties, firms also cut wages by reducing the variable part of wages. This evidence suggests that credit shocks can affect not only the real economy, but also nominal variables.

1. Introduction

In many European countries, the early 2010s have been characterized by significant difficulties in accessing credit by firms, as well as households and governments. The global financial crisis, having originated in 2007 in the US subprime market, and the subsequent sovereign debt crisis, which hit Europe in the summer of 2011, forced European banks to considerably tighten their credit conditions for firms in many economies and for several years.

The global financial crisis and sovereign debt crisis renewed the interest for the effect of credit shocks on the real economy. Before the global financial crisis, the relationship between credit constraints and employment was investigated in the literature, analysing the link between financial development and growth (e.g. Beck & Demirguc-Kunt, Citation2006; Klapper et al., Citation2006). Following the global financial crisis, many papers focussed on the effect of credit shocks on the real economy (Acharya et al., Citation2018; Berg, Citation2018; Bottero et al., Citation2020; Cingano et al., Citation2016; Degryse et al., Citation2016), and the labour market in particular (Bentolila et al., Citation2018, June; Berton et al., Citation2018; Buera et al., Citation2015; Chodorow-Reich, Citation2014; Duygan-Bump et al., Citation2015; Hochfellner et al., Citation2016; Pagano & Pica, Citation2012; Popov & Rocholl, Citation2018). The existing literature builds primarily on linked firm-bank data and examines the impact of exogenous credit supply shocks, making use of the sticky lender–borrower relationship. Different types of financial shocks have been examined: Popov and Rocholl (Citation2018) focus on the effect of the funding shock of German savings banks during the US mortgage crisis, Chodorow-Reich (Citation2014) take advantage of the different exposures of the lenders on the syndicated market to mortgage-backed securities in the US. Acharya et al. (Citation2018) look at bank-firm relationships in Europe to analyse several outcomes including employment. Bentolila et al. (Citation2018, June) use the differences in Spanish banks’ health at the start of the Great Recession. Other papers derive local-level measures of credit supply (e.g. Greenstone et al., Citation2020). These papers typically focus on a single country, and do not analyse the heterogeneity in firms’ adjustments across countries.

This paper looks at the link between credit shocks and adjustment in labour from a European perspective, which is fundamental for the European policy makers. To do so, we use a unique, fully harmonized survey conducted in 25 European countries by the Wage Dynamics Network (WDN), a research network of the European System of Central Banks.Footnote1 The survey, which was the third one conducted by the network and thus is labelled as WDN3 in this paper, focusses on the period between 2010 and 2013 and asks firms to report both their difficulties in accessing credit and the ways of adjusting labour costs, be it through employment or through wages. We construct an index of credit difficulties which is cleaned from the impact of demand and other shocks. This index is fully comparable across firms in different countries, and we use it to analyse the intensity of credit restrictions in different EU countries. Then we relate our index of credit difficulties to firms’ labour cost adjustments. First, we find that credit difficulties were extremely heterogeneous both within and across countries. According to our estimates, in countries with low average values of the credit difficulty index, the within-country variability was also quite low. On the contrary, in the most severely hit countries (mainly Southern European and some Eastern European countries) the within-country variability was remarkably high. If we compare countries, we find that the interquartile range (the difference between the 25th and the 75th percentiles) of the distribution of our index in Austria, the country registering the lowest level of credit difficulties, was three times lower than that observed in the most severely hit countries. Second, we find that European firms hit by a credit shock report more frequently a reduction in both employment and wages than firms without financing difficulties.

We estimate that a 1 point increase in our index of credit difficulties is associated with an increase in the probability to adjust employment by close to 2 pp (over a mean probability of 16%). As the survey collects detailed information on the strategies to adjust labour costs, we can distinguish also between adjustment along the extensive (i.e. change in headcount) and the intensive margin (i.e. reduction in hours per employee). Consistently with Berton et al. (Citation2018), who focus on one Italian region, we find that credit supply shocks affected both the extensive and the intensive margin. More importantly, we find that the reduction of the intensity of the use of labour as a response to a credit shock was not confined to Italy, as found by Berton et al. (Citation2018), where the subsidized reduction of hours was widely used, but also happened in other European countries, mainly through non-subsidized reduction of hours (i.e. part-time work arrangements).

Workers are affected heterogeneously by firms’ credit difficulties. We find that the probability of an adjustment in case of an adverse credit shock was higher for temporary workers. This finding is consistent with Bentolila et al. (Citation2018, June), who focus on Spain, and Caggese and Cuñat (Citation2008), who examine the case of Italy. Firms also decreased their hiring, with a particularly significant effect on the employment opportunities of younger job-seekers. Labour market adjustment as a response to credit constraints is thus a potential explanation behind the considerable rise of youth unemployment in most European countries (see Hoynes et al., Citation2012 for the US and Verick, Citation2009 for European countries for a description of how youth unemployment developed following the financial crisis).

In addition to the adjustment in employment, we find that firms also adjust wages when they face credit difficulties. The relationship between credit shocks and wage dynamics has been less investigated so far by the literature, probably because of data constraints and because it has not been clear whether European firms have margins to adjust wages. An exception are Hochfellner et al. (Citation2016) and Moser et al. (Citation2020), who use employer-employee matched data for a sample of German firms and, by the use of different strategies, examine the impact of credit shocks on earnings, and Adamopoulou et al. (Citation2020) who focus on Italy. We find that in our sample an increase of 1 point of our credit difficulty index is associated with an increase in the probability to cut wages, by around 1pp. over an average of 14%. The impact of credit difficulties is stronger for the flexible part of workers’ compensation, whereas the impact on base wage is small and not precisely estimated. This is probably related to the institutional rigidities which prevent cuts of base wages.

We find that the effect of credit market conditions on the extensive margin of adjustment was rather similar along several firm characteristics: the interaction of the extensive margin of adjustment with firm’s size, sector and autonomy is insignificant. For firms which are neither parent nor subsidiary/affiliate we find a higher probability to adjust the extensive margin when the credit difficulty index increases. We also find that the interaction term between the credit difficulty index and the extensive margin is higher in case of domestic firms than foreign owned ones. For a given credit supply shock, the reaction of firms is show some degree of heterogeneity across European countries (controlling for differences in the economic structure, i.e. firm size and sector). The most significant differences can be detected between the Eastern European / Baltic group of countries. This suggests that the different impact of credit shocks on employment and wages can occur not only due to heterogeneity in the intensity of the shocks across countries but also due to country specific factors such as labour policy protection or wage bargaining.

Our estimation strategy is also supported by some additional exercises based on matching banks in the credit registers of France and Italy with firms in the WDN3 survey. We are aware that estimates using WDN3 are based on qualitative self-reported information, which do not allow for the identification of the effect of an exogenous credit supply shock to firms’ labour costs. Nevertheless our findings are robust as confirmed by the use of quantitative information from the credit register data. Based on these data, we construct a credit supply shock index and we show that it correlates with our survey-based measure of credit difficulties. Within this rather different setting our main results are fully confirmed.

This paper is organized as follows. Section 2 describes the main features of the WDN3 data. Section 3 explains the methodology for calculating the index of credit difficulties. In Section 4, we show how the index correlates with measures about employment and wage adjustments in our sample of firms. In Section 5, we focus on France and Italy and on a sample of WDN3 firms matched with credit register data. Last, Section 6 briefly concludes.

2. The WDN3 survey

We use firm-level survey data collected by the Wage Dynamics Network (WDN). WDN is a research network of the European System of Central Banks, dedicated to the study of the features and sources of wage and labour cost dynamics and their implications for monetary policy in the euro area. The first and the second surveys on firms’ price and wage setting practices have been carried out in 2007 and 2009. The third survey, the results of which are used in this paper, was conducted in 2014 by national central banks in 25 countries of the European Union. It covers the 2010–2013 period, and was answered by over 25,000 firms (see Izquierdo et al., Citation2017 for details).

Following the global financial crisis, several European countries have been confronted with a severe sovereign debts crisis. The latter, together with more stringent regulation about capital requirements and the related tightening of credit standards, transmitted into the second phase of the double-dip recession from the last quarter of 2011 until the first quarter of 2013 in the European Union as a whole. Firms were hit by adverse demand and credit shocks, and both types of shocks affected their strategies to adjust their labour input during 2010–2013. Therefore, the third wave of the WDN survey (WDN3) was designed specifically to differentiate by types of shock (to product demand, demand volatility, credit availability, customers’ ability to pay and supply availability) and their intensity, as well as to explore firms’ adjustment strategies during this period. Special attention was given to firms’ adjustments of labour input, wage dynamics and wage settings practices. For a more detailed description of the WDN3 survey, see Appendix 1.

This paper uses four sets of questions from the survey (see in the Appendix for the exact list of the questions).

First, we use the questions on credit availability and credit conditions. Six questions aim at capturing the taxonomy in the severity of credit constraints. They consider both the worsening in the quantity or access to credit and the costs and conditions of credit supplied by the banks. Firms were also asked to qualify the intensity of the difficulties. Both the questions on access to credit and credit conditions were asked in relation to three types of requested credit (financing working capital, financing new investments, refinance debt).

Second, a group of questions was asked on the changes in economic conditions faced by the firms during 2010–2013. Firms could choose between five symmetrical responses describing the change in level of demand, volatility of demand, customers’ ability to pay and availability of supplies (the potential answers were: strong decrease, moderate decrease, unchanged, moderate increase, strong increase). We use these questions to control for the effects of other shocks, deriving an uncorrelated measure of credit difficulties.

Third, several questions were asked on the channels of labour market adjustments used by the firms during 2010–2013. Firms were asked if they needed to significantly reduce their labour input or to alter its composition. Firms that needed to adjust their labour input were asked about the exact way of doing so (e.g. layoffs, reduction of hours, freeze of new hires, etc.). We use these questions to make a distinction between the extensive and the intensive margins of labour adjustment. Adjustment along the extensive margin is defined as individual or collective layoffs, while the intensive margin is defined as a reduction of working hours per worker (be it unsubsidized or carried out in the framework of subsidized schemes).

Finally, some questions allow us to measure the propensity of firms to adjust base and variable wages. (For a description of the answers on labour adjustment please see in the Appendix.) We combine these four sets of data and control for firm-level characteristics to examine the connection between credit shocks and labour adjustment.

3. Measuring credit difficulties using WDN3

Using the questions about credit difficulties, we construct firm-specific indices of credit constraints, comparable for 24 EU countries included in the WDN3 survey. Data for Ireland are excluded as answers about the availability of credit are not collected for this country. We focus on firms in manufacturing, trade and business services sectors (we call the latter two sectors together private services). Our final sample consists of around 19,000 firms.Footnote2 See for a description of our sample.

A look at the raw data confirms the presence of strong cross-country heterogeneity. reports the share of firms stating that the lack of credit for a given purpose, or the cost of credit was a relevant or very relevant problem. Over 40% of firms in Greece, Bulgaria, Poland and Slovenia report that credit difficulties were relevant or very relevant for their activity, but the values are also high for Italy, Spain, Portugal and Cyprus. While in Greece, Slovenia, Italy, Spain, Portugal, and Cyprus the high values are likely to reflect the impact of the sovereign debt crisis on financial intermediation, in Poland the reason may be the high share of self-financing (Strzelecki & Wyszyński, Citation2016). In Malta and Austria, on the other hand, only a minor proportion of firms faced difficulties in getting credit. Within firms, the responses about the difficulties to obtain credit for different purposes are highly correlated. This explains why the average share of firms reporting problems to obtain credit is similar for different credit types within one country.

Table 1. Share of firms in manufacturing, trade and business services, who viewed that credit access problem in 2010–2013 (as described in the credit accessibility questions) was relevant or very relevant, %.

We derive a unique comparable measure of credit difficulties across European countries. We take advantage of the high correlation between the six credit availability measures. We combine both conditions and quantity aspects of credit availability via principal component analysis (PCA).Footnote3 Before applying PCA, we remove the part of the correlation which could be due to other shocks hitting firms and affecting also their ability to access credit. To do so, we first regress our basic measures of credit restrictions on variables measuring demand and demand volatility shocks, customers’ ability to pay, the availability of supplies and firms’ characteristics, such as sector and firm size. We use the residuals of these six regressions to carry out the PCA. The descriptive statistics of the obtained components are given in . The first principal component explains 70% of the total variance in credit difficulty measures and has positive loadings of roughly similar size for all the six questions, therefore representing the overall credit difficulty for a firm.

Table 2. Principal component analysis of the credit difficulty measures.

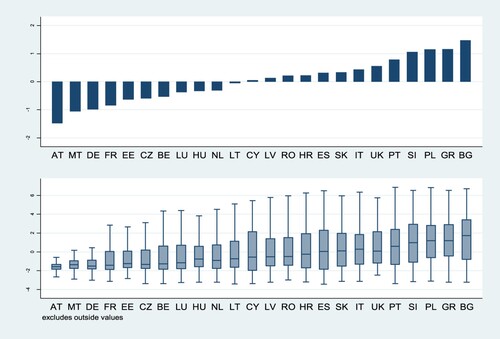

reports the average firm scores of the ‘credit difficulty index’ by country, as measured by the first principal component. Countries are ranked according to their average level of firms’ credit difficulties. The values are normalized around the average level of credit indexes for all countries. Thus, values above zero reflect above-average levels of credit difficulty. The index has a value above the whole-sample average in Italy, Spain, Portugal, Poland, Slovenia, Bulgaria and Greece. The distribution of countries by credit difficulty is quite symmetric, with a roughly similar number of countries experiencing above-average and below-average level of credit problems.

Figure 1. Country averages of credit difficulty index and box-plot analysis of firm level variation.

Note: Sample is restricted to manufacturing, trade and business service firms.

The lower graph of shows the distribution of the obtained credit difficulty indices by country, with the lower and upper borders representing the 25th and the 75th percentiles, respectively. The line in the box shows the median. In all countries, the distribution of the credit difficulty index has a long positive tail, suggesting that even in countries where a majority of the firms had no credit difficulties, quite a large minority faced financing problems. Austria and Malta are extreme cases, where over 75% of firms had the same low level of credit difficulty.Footnote4 In Poland, Slovenia, Bulgaria and Greece, the distribution of the credit difficulty index is more even. In these countries the occurrence of both the very low and the very high values of the credit difficulty indices was rare and the majority of firms had similar, relatively severe credit access problems. Overall, the figure shows the presence of high heterogeneity of credit difficulties across EU countries: the interquartile range (the difference between the 25th and the 75th percentile of the distribution) of the index of credit difficulties in Austria is around three times lower than that observed in Italy or in Greece.

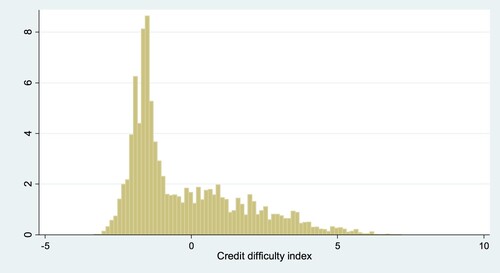

shows the distribution of the derived credit difficulty index for all countries in the sample, weighing observations to reflect total employment in the countries. The large mass in the negative interval reflects the high weight of France, Austria and Germany in the total sample of firms and rather good credit availability in these countries. The right tail is much longer and mostly positive, reflecting the overall severity of credit conditions for many firms.

Figure 2. Histogram of credit difficulty index.

Note: Sample is restricted to manufacturing, trade and business service firms. Data weighted to reflect an overall employment in the country.

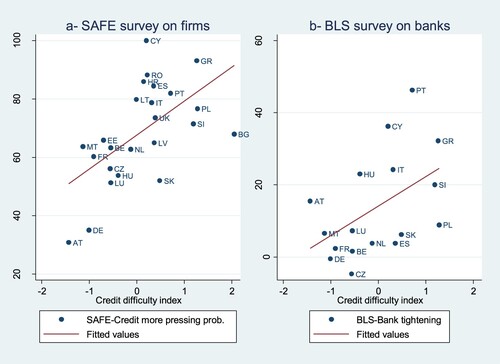

To cross-check whether our index indeed captures the credit difficulties that we intend to measure, we compare it with external data sources. For this cross-check, we first look at the Survey on the access to finance of enterprises (SAFE), conducted by the ECB and the European Commission since 2009. The SAFE Survey is comparable to the WDN3 Survey in the sense that it measures credit difficulties as perceived by the firms, and not by the banks as a supplier of credit. The SAFE survey collects data from small and medium-sized enterprises (SMEs) in Europe asking, among other things, what the most pressing problem for firms during the reference period is. , panel a, is based on the 2013 SAFE survey and refers to the same period as the WDN3. It compares the share of firms reporting at least one obstacle in obtaining a (bank) loan in the SAFE survey in 2013 (vertical axis) to the country level average of the index of access to finance from the WDN3 survey (horizontal axis). The figure confirms the high correlation between the two measures.

Figure 3. Correlations of the results of SAFE survey on firms and BLS on banks, and index of credit difficulties.

Note: Panel a: Safe survey, share of firms reporting credit availability as the more pressing problem and index of credit difficulty (mean values for each country). Panel b: BLS survey, share of banks reporting a tightening in conditions and index of credit difficulty (mean values for each country).

The ECB’s Bank Lending Survey (BLS) provides another possibility to validate our results, by looking at credit conditions from the banks’ perspective. The BLS was launched in 2003 by the ECB to enhance the Eurosystem’s knowledge of the financing conditions in the euro area. It can be seen as the European equivalent of the Senior Loan Officer Opinion Survey on Bank Lending Practices in the US. In the BLS, a sample of banks is asked every quarter about, among others, how they changed their credit standards in the previous three months for loans to non-financial enterprises. We have extended the ECB sample of the euro area countries with data from the Czech Republic, Poland and Hungary, making use of data collected and published by national central banks. For each country and every quarter, a net percentage of banks tightening (+) and loosening (−) their credit conditions is reported. , panel b reports, on the vertical axis, the average of the net percentages of tightening banks for each country during the 16 quarters over 2010Q1 to 2013Q4 (2012Q1-2013Q4 for CZ). The horizontal axis shows the first principal component from the WDN3 data. The positive correlation between the BLS-measure of credit supply conditions and the WDN3-measure of firms’ difficulties in obtaining finance, gives confidence to our interpretation of the first principal component as a measure of credit supply difficulties.

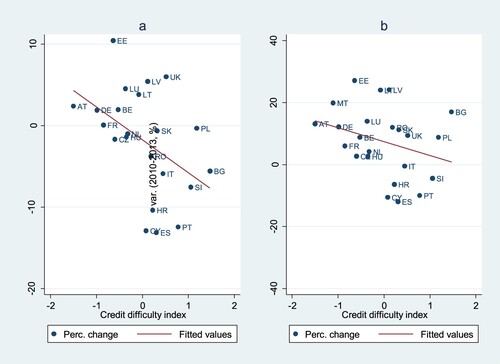

Finally, plots the correlation between our credit difficulty index and important labour market macro variables, drawn from national accounts, measuring changes in the use of labour (measured by total hours worked) and nominal hourly wages during the period 2010–2013. shows that there is a clear negative correlation between the change in employment at the macro level and our index of credit difficulties. A (weaker) negative correlation also arises between credit difficulties and nominal wage growth. This preliminary look at the aggregate data gives comfort to our interpretation of the credit difficulty index and provides a strong motivation for our micro analysis.

Figure 4. Correlations between adjustments in employment (total hours worked, panel (a) and nominal hourly wages (panel b) and index of credit difficulties).

Note: National accounts (Private sector only) and index of credit difficulty (mean values for each country).

4. Credit market access and labour adjustments: evidence from microdata

Aggregate data may hide considerable differences across firms. Thus, we look at the micro data to see whether the correlation between credit difficulties and labour adjustment is observable on the firm level and if there are any differences in terms of the type of adjustment. Furthermore, the countries analysed in this study have very different labour market institutions, which can affect the firms’ response to shocks. Therefore, it is worthwhile to look at several different channels of adjustment.

Starting with the total adjustment (question about the need to reduce labour input), adjustments along the extensive margin (i.e. if the firm undertook individual or collective layoffs) and adjustments along the intensive margin (subsidized as well as non-subsidized reductions of hours), we construct a set of dummy variables equal to 1 if firm i adjusted its labour input using a specific method of adjustment k, and zero otherwise.Footnote5 We also look at the other instruments to adjust labour input and in particular at firms that stopped new hiring and did not renew temporary job contracts. These outcomes are particularly relevant, because they help understanding the impact of the sovereign debt crisis on specific dimensions of the European labour markets, for example, the rise in youth unemployment, which could have been particularly affected by the reduction in hiring, and the segmentation between temporary and permanent job contracts.

We extend our analysis to adjustments in wages as a response to credit difficulties. Data limitations have prevented analysing this relationship until now. Based on the WDN3 survey, however, we can check whether firms adjusted base and variable wage components in response to credit shocks.

To check for a correlation between labour cost adjustments and the measures of credit market difficulties described in Section 3, we consider the following baseline specification:

(1)

(1)

where

- adj_ki is a dummy variable on k-th type of labour market adjustment for firm i (equal to 1 in case of strong or moderate decrease in the use of the method of adjustment),

- credit_difficultyi is the measure of credit constraint experienced by firm i,

- Xi is a vector of firm-level control variables, which in all models correspond to country, sector and size dummies.

The results on labour input adjustments are reported in and and those on wage adjustments in .

Table 3. Labour input adjustments and credit availability. Probit marginal effects.

Table 4. Labour input adjustments and credit availability (robustness check). Probit marginal effects.

Table 5. Labour input adjustments and credit availability, by detailed method of adjustment. Probit marginal effects.

As shown by , the index of credit market difficulty correlates positively with the probability to adjust labour input, a result which is in line with the current literature on the employment effect of credit shocks. Our findings, however, suggest that adjustments took place along both the extensive and the intensive margins, although with a somewhat higher intensity in the case of the extensive margin. In particular, we estimate an increase in the probability to adjust employment by close to 2 pp (over a mean probability of 16%) after a 1 point increase in our index of credit difficulties. This result is also robust to the inclusion of additional controls such as the share of labour costs in total costs, the share of flexible labour costs, and dummies on the degree of firm´s autonomy (parent company, subsidiary/affiliate or other), structure (single establishment or multi-establishment firm) and ownership (mainly domestic or foreign) (see ).

This result is confirmed when the methods to adjust labour input are analysed separately (). For all the methods, credit market difficulties are always positively correlated to the probability to adjust firm workforce. Results show that firms more strongly affected by credit difficulties as measured by our index tend to use individual layoffs to adjust their labour force more than collective or temporary layoffs, probably reflecting higher institutional rigidities to use these alternative methods of adjustment. Also, credit difficulties are positively associated with the freeze or reduction of new hires and the non-renewal of temporary contracts, while the impact on early retirement or temporary agency workers is more limited. On the intensive margin, firms hit by credit shocks tend to use non-subsidized reduction of hours with a higher probability. At the same time, higher credit difficulties are not significantly associated with a higher incidence of subsidized reductions of working hours, probably because the latter lead to a decline of labour costs which relaxed the financing difficulties. Subsidized reduction of working hours was available on a large scale only in a few countries during the sovereign debt crisis.

reports the marginal effect of worsening credit conditions on the probability to adjust wages. Our estimates confirm the positive correlation between credit market difficulties and the adjustment of wages, reflecting their impact on the adjustment of flexible wages (increasing this probability by almost 1 pp). By contrast, the impact on base wages is not significant, possibly showing the larger institutional rigidities to adjust base wages in European countries (on average, just 5% of European firms adjusted base wages over this period).

Table 6. Wage adjustments and credit availability, base wage and variable wage components. Probit marginal effects.

We check whether firm-specific factors, such as size, sector, ownership, structure and autonomy, affect the response of labour market variables to credit shocks. For this purpose, we include an interaction term between our index of credit difficulties and firms’ characteristics (see ). The interaction of the extensive margin of adjustment with firm’s size, sector and autonomy is insignificant, suggesting that the effect of credit market conditions on the extensive margin of adjustment was rather similar across firms of different size, sector and autonomy level. Interestingly, for firms which are neither parent nor subsidiary/affiliate we find a higher probability to adjust the extensive margin when the credit difficulty index increases. We also find that the interaction term between the credit difficulty index and the extensive margin is higher in case of domestic firms than foreign-owned ones. The results for the interaction term with the intensive margin of adjustment are not statistically significant.

Table 7. Credit availability and labour market adjustments by type of firm. Probit marginal effects.

We then look more closely at country heterogeneity. We define three geographical areas corresponding to (i) Continental Europe and UK, (ii) Eastern European and Baltic countries and (iii) Southern European countries. The grouping is based on differences in the financial sector. Firms in Continental Europe and in the UK are typically less dependent on banks for their financial needs (this is true especially for UK, see Brown et al., Citation2009) and are characterized by lower leverage (see, e.g. Bach Outlook no.2, 2014). Eastern European and Baltic countries are grouped together because their banking sectors are characterized by a large market share of foreign banks, and a considerable degree of dependence on banking finance. Finally, in the Southern European countries the banking sector suffered the most during the period 2010–2013 because of their exposure to sovereign debt risk. We interact the index of credit difficulties with area dummies to check the differences in the elasticity of employment to credit difficulties in the different areas. The results of this exercise are reported in . Interestingly, we do not find much evidence that the elasticity of employment to credit shocks was different across these areas. In particular, no significant differences are found between group (i) and (iii) in any method of labour cost adjustment, although the impact of credit difficulties on the employment adjustment in the intensive margin and flexible wage adjustment seems to be lower in the Eastern European and Baltic countries.

Table 8. Credit availability and labour market adjustments by geographical area. Probit marginal effects.

For completeness, we also provide estimates in which the credit difficulty index is interacted with country dummies (see ). We take France as baseline. The coefficients within Southern European countries are quite homogenous, the only difference being smaller effect on extensive margin in Italy. In general, some cross-country heterogeneity emerges, with no clear pattern. Some significant differences can be detected only within the Eastern European/Baltic group. Firms in Slovenia, Slovakia Poland, Lithuania and Romania tend to rely less on labour or flexible wage margins of adjustment in response to worsening credit supply conditions. The use of labour and wage adjustment margins in two Baltic countries, i.e. Latvia and Estonia, as well as Hungary, Croatia, Bulgaria does not differ significantly from the baseline. This result suggests that the heterogeneous reaction of the EU labour markets in response to the sovereign debt crisis is explained not only by the differences in the intensity of the crisis across countries, but also by country-specific factors. This conclusion is in line with the results by Mathä et al. (Citation2019) showing that strict employment protection and high centralization or coordination of wage bargaining make it less likely that firms reduce wages when facing negative shocks (irrespective of the type of negative shock).

Table 9. Credit availability and labour market adjustments by country. Probit marginal effects.

5. Robustness checks: evidence from France and Italy

Our index of credit difficulties has been calculated on qualitative data from the survey. In this section, based on French and Italian data on loans to firms we construct a quantitative index of credit supply and we test whether our results are still confirmed.

We combine the WDN3 sample with data from the credit register in the two countries, administered by the Banque de France and the Bank of Italy, respectively. The data includes all credit commitments by all banks operating in each country exceeding 25,000 euros in France and 30,000Footnote6 euros in Italy. The thresholds, which are quite similar, therefore exclude only very small companies with low credit facilities granted. Both databases include firm identifiers (tax codes) that make it possible to link firms with WDN3 data and identify their lending banks. The data have a monthly frequency. For each company-bank pair, the total credit granted at the end of the year is recovered.Footnote7

Credit register data are used to construct a quantitative index of credit supply, which can be assigned to the firms in the WDN3 sample. We consider the universe of banks in Italy and France from 2007 to 2013, i.e. before the burst of the global financial crisis and after the sovereign debt crisis. Aggregating loan data by bank, we calculate the three-year percentage change in total loans for each bank. This way we remove bank fixed effects. We then carry out the simple regression [2] to remove a time trend t, aimed at capturing aggregate common factors (e.g. credit demand).

(2)

(2)

Last, we take the residuals of [2], and in particular residuals in year 2013,. The use of residuals instead of

allows us to get a quite conservative measure of credit supply, since, for each bank, we consider how much bank’s b credit grows compared to the aggregate trend. Finally, we assign the residuals for the period 2010–2013 to each WDN3 firm. Firms have multiple bank relationships, thus, we weight each residual with the share of loans

of firm f (in the WDN3 sample) in the total amount of loans of the firm with any bank b in the register in 2009, i.e. the year preceding the survey reference period. This strategy allows us to limit the impact of possible selection bias in the firm-bank relationship in response to the global financial and/or the sovereign debt crisis. In particular we calculate the index of credit supply to firm f,

as:

(3)

(3)

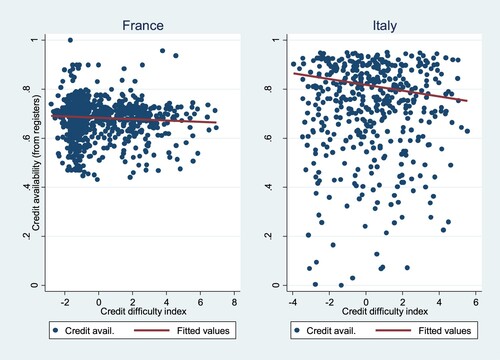

This procedure leads to an imperfect match between the two datasets and we get around 750 observations per country.Footnote8 We normalize the two indices and pool the two datasets. compares the index of credit difficulties drawn from the WDN3 survey with this measure of credit supply change. As expected, the two indices are negatively correlated.

Figure 5. Correlations between the change in credit supply and the index of credit difficulties.

Note: Credit supply (measured on credit registers and normalized between zero and one in both countries) and index of credit difficulty.

Our estimation results are reported in (the regression models also include sector and size dummies and a country dummy). The first column refers to the correlation of and our credit difficulty index, entirely based on WDN3 data: firms matched with banks with lower credit growth are more likely to report difficulties in accessing to credit and the correlation between the two indices is statistically significant.. This is an indirect validation of our approach based on qualitative self-reported information. Columns 2–5 show the estimated probabilities to reduce the extensive margin, the intensive margin, the base wage and the variable wage, respectively. The results are substantially confirmed. The correlation between credit supply and the probability to reduce labour is negative. The same holds for flexible wages, but not for base wages, as found in the examination of all countries.

Table 10. Italy and France. Alternative index of credit supply and labour market adjustments. Pooled data.

6. Conclusions

In this paper, we provide empirical evidence about a strong correlation between credit shocks and labour market adjustments in Europe during the sovereign debt crisis. We rely on WDN3 survey data, which has the advantage to offer a unique European perspective, providing comparable, harmonized results for 24 countries.

We are aware of the limits of our approach. First, the data allow us to calculate only the probability of an adjustment and not how much of the observed employment drop can be imputed to credit difficulties. Second, since we use survey data on self-reported credit difficulties and other shocks, our index of credit difficulty does not allow for a proper identification of the credit supply shock hitting the various countries, net of any demand effect. Thus, our main estimates are simple correlations between credit difficulties and firms’ labour cost adjustment strategies. Even with this limitation, our results confirm that credit shocks are important determinants of labour market fluctuations in Europe.

Second, credit market difficulties are associated not only with a decrease in employment, but also with a decline in the intensity of the use of labour in terms of hours worked. One consequence of this finding is that after large-scale shocks like the sovereign debt crisis, special attention may be needed on measures of labour market slack, other than the unemployment rate (which is a simple headcount ratio of how many people are without a job over active population).

Finally, our results suggest also that, in response to credit difficulties, base wages are quite rigid and do not adjust on average. Nevertheless, European firms reduce nominal wages by cutting the variable part of employee compensation (bonuses, performance-related premia, etc.). Thus, credit difficulties may have consequences not only on real variables but also on nominal ones (e.g. Adamopoulou et al., Citation2020; Moser et al., Citation2020; for an analysis on the impact of credit difficulties on prices, see also Duca et al., Citation2017).

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Katalin Bodnár

Katalin Bodnár is an economist in the Supply Side, Surveillance and Labour Markets Division at the European Central Bank. Her interests include labour economics and potential output.

Ludmila Fadejeva

Ludmila Fadejeva is a research economist at Latvijas Banka. Her research interests include monetary and labour economics, particularly the study of monetary policy transmission and income/wealth inequality.

Marco Hoeberichts

Marco Hoeberichts is an economist in the Economics and Research Division at De Nederlandsche Bank. His research interests I include labour economics and inflation dynamics.

Mario Izquierdo Peinado

Mario Izquierdo Peinado is Head of the Supply and Labor Market Analysis Unit at the Directorate General of Economics and Statistics of the Bank of Spain. His research interests include various labor market issues, such as wage dynamics, wage inequality and the impact of labor market institutions.

Christophe Jadeau

Christophe Jadeau is an economist at Banque de France, Engineering and Statistical Methodology Department.

Eliana Viviano

Eliana Viviano is Head of the Labour Market Division at the Economics and Research Department of the Bank of Italy. She has published both micro and macro papers on various labor market issues, such as labor market reforms, determinants of wage dynamics, methodological aspects related to the estimation of unemployment and employment rates.

Notes

1 Previous WDN surveys do not allow to make a similar analysis on the impact of credit constrains on labour cost adjustments. WDN1 survey did not include any question regarding difficulties in access to finance while WDN2, which was an update of WDN1 with small sample sizes and conducted only in 10 European countries, included merely one question regarding the extent of difficulties in access to finance for firms. Using this dataset, Fabiani et al. (Citation2015), although they focus on demand shocks, find that negative finance shocks increase the likelihood to adjust margins and costs at the firm level and once the impact of demand shocks is taken into account, financially constrained firms are more likely to adjust non-labour costs.

2 Firms’ non-response to the credit availability questions is not homogenous across countries. In the UK, almost 30% of firms in manufacturing, trade and business services sectors haven't provided answers to this block of questions. In Greece this share is 12%, followed by Hungary (9%), Latvia (9%) and Italy (8%). In the remaining of the countries the non-response rate was smaller.

3 As robustness check we derive credit difficulty index using factor analysis. The obtained results lead to the same findings. The difference in the size of the marginal effects using both measures (with standardized variance) is negligible.

4 The countries with low credit difficulties on average are characterized by a good cyclical position at the start of the sovereign debt crisis, as shown for example by their low unemployment rates. At the same time, in Austria and Malta, the low share of state-owned banks and in the latter, the high share of foreign owned banks have also likely played a role. In Austria, only a low percentage of the firms applied for a credit in the period examined in the WDN3 survey. See Stiglbauer (Citation2017) and Micallef and Caruana (Citation2017).

5 The dummy for the adjustment on the extensive margin is equal to 1 if the firm answered that individual and/or collective layoffs were used moderately or strongly, and 0 otherwise. The dummy for the intensive margin is equal to 1 if the firm answered that the decrease of hours worked per worker, either subsidized or non-subsidized, was used moderately or strongly, and 0 otherwise.

6 Prior to 2009, the Italian credit register only included loans in excess of €75,000. Companies not present in the credit register before 2009 are therefore excluded from the sample. However, this selection has an extremely limited impact since the Italian WDN3 sample mostly includes companies with at least five employees (see Izquierdo et al., Citation2017 for details), which meet the requirement for inclusion in the register.

7 When dealing with bank data one of the main problems concerns bank mergers and how to reattribute loans to firme made by the banks involved in the M&A. The data used in this paper presents the same problem and in case of merge the information related to the bank-firm match is dropped (and the firm is excluded from the sample). However, in the period under scrutiny, during which two deep financial crises occurred, merges in both countries were rather limited. Even if this potentially generate some selection bias, the type of selection induced by bank M&A is not clear and likely not correlated to labour market outcomes.

8 Most firms drop out because of errors in tax codes.

References

- Acharya, V. V., Eisert, T., Eufinger, C., & Hirsch, C. (2018). Real effects of the sovereign debt crisis in Europe: Evidence from syndicated loans. The Review of Financial Studies, 31(8), 2855–2896. https://doi.org/10.1093/rfs/hhy045

- Adamopoulou, E., De Philippis, M., Sette, E., & Viviano, E. (2020). The long run earnings effects of a Credit Market Disruption, IZA DP No. 13185.

- Beck, T., & Demirguc-Kunt, A. (2006). Small and medium-size enterprises: Access to finance as a growth constraint. Journal of Banking & Finance, 30(11), 2931–2943. https://doi.org/10.1016/j.jbankfin.2006.05.009

- Bentolila, S., Jansen, M., & Jimenez, G. (2018, June). When credit dries up: Job losses in the Great Recession. Journal of the European Economic Association, 16(3), 650–695. https://doi.org/10.1093/jeea/jvx033

- Berg, T. (2018). Got rejected? Real effects of not getting a loan. Review of Financial Studies, 31(12), 4912–4957. https://doi.org/10.1093/rfs/hhy038

- Berton, F., Mocetti, S., Presbitero, A., & Richiardi, M. (2018). Banks, firms and jobs. Review of Financial Studies, 31(6), 2113–2156. https://doi.org/10.1093/rfs/hhy003

- Bottero, M., Lenzu, S., & Mezzanotti, F. (2020). Sovereign debt exposure and the bank lending channel: Impact on credit supply and the real economy. Journal of International Economics, 103328

- Brown, J. R., Fazzari, S. M., & Petersen, B. C. (2009). Financing innovation and growth: Cash flow, external equity, and the 1990s R&D boom. Journal of Finance, 64(1), 151–185. https://doi.org/10.1111/j.1540-6261.2008.01431.x

- Buera, F., Fattal-Jaef, R., & Shin, Y. (2015). Anatomy of a credit crunch: From capital to labor markets. Review of Economic Dynamics, 18(1), 101–117. https://doi.org/10.1016/j.red.2014.11.001

- Caggese, A., & Cuñat, V. (2008, Nov.). Financing constraints and fixed-term employment contracts. The Economic Journal, 118(533), 2013–2046. https://doi.org/10.1111/j.1468-0297.2008.02200.x

- Chodorow-Reich, G. (2014). The employment effects of credit market disruptions: Firm-level evidence from the 2008–9 financial crisis. Quarterly Journal of Economics, 129(1), 1–59. https://doi.org/10.1093/qje/qjt031

- Cingano, F., Manaresi, F., & Sette, E. (2016). Does credit crunch investments down? New evidence on the real effects of the bank-lending channel. Review of Financial Studies, 29(10), 2737–2773. https://doi.org/10.1093/rfs/hhw040

- Degryse, H., De Jonghe, O., Jakovljević, S., Mulier, K., & Schepens, G. (2016). ‘The impact of bank shocks on firm-level outcomes and bank risk-taking’, Paris December 2016 Finance Meeting EUROFIDAI - AFFI. Available at SSRN: https://ssrn.com/abstract=2788512

- Duca, I., Montero, J. M., Riggi, M., & Zizza, R. (2017). I will survive. Pricing strategies of financially distressed firms. Temi di discussione (Economic working papers) 1106, Bank of Italy, Economic Research and International Relations Area.

- Duygan-Bump, B., Levkov, A., & Montoriol-Garriga, J. (2015). Financing constraints and unemployment: Evidence from the Great Recession. Journal of Monetary Economics, 75, 89–105. https://doi.org/10.1016/j.jmoneco.2014.12.011

- Fabiani, S., Lamo, A., Messina, J., & Rõõm, T. (2015). European firm adjustment during times of economic crisis, ECB Working Paper no 1778.

- Greenstone, M., Mas, A., & Nguyen, H. L. (2020). Do credit market shocks affect the real economy? Quasi experimental evidence from the great recession and ‘normal’ economic times. American Economic Journal: Economic Policy 12, 200(225). doi:10.1257/pol.20160005

- Hochfellner, D., Montes, J., Schmalz, M., & Sosyura, D. (2016). Winners and losers of financial crises: Evidence from individuals and firms, mimeo, University of Michigan.

- Hoynes, H., Miller, D., & Schaller, J. (2012). Who suffers during recessions? Journal of Economic Perspectives, 26(3), 27–48. https://doi.org/10.1257/jep.26.3.27

- Izquierdo, M., J. F. Jimeno, T. Kosma, A. Lamo, S. Millard, T. Rõõm, & E. Viviano (2017) Labour market adjustment in Europe during the crisis: microeconomic evidence from the Wage Dynamics Network survey, ECB Occasional Paper n 192.

- Klapper, L., Laeven, L., & Rajan, R. (2006). Entry regulation as a barrier to entrepreneurship. Journal of Financial Economics, 82(3), 591–629. https://doi.org/10.1016/j.jfineco.2005.09.006

- Mathä, T. Y., Millard, S., Rõõm, T., Wintr, L., & Wyszyński, R. (2019). Shocks and labour cost adjustment: evidence from a survey of European firms, ECB Working Paper Series no 2269.

- Micallef, B., & Caruana, K. (2017). Results of the 2014 Wage Dynamics Network for Malta, ECB WDN3 Country Report.

- Moser, C., Saidi, F., Wirth, B., & Wolter, S. (2020). Credit supply, firms, and earnings inequality, MPRA Paper 100371.

- Pagano, M., & Pica, G. (2012). Finance and employment. Economic Policy, 27(69), 5–55. https://doi.org/10.1111/j.1468-0327.2011.00276.x

- Popov, A., & Rocholl, J. (2018). Do credit shocks affect labor demand? Evidence for employment and wages during the financial crisis. J. Financial Intermediation, 36, 16–27. https://doi.org/10.1016/j.jfi.2016.10.002

- Stiglbauer, A. (2017). The third wage dynamics network firm survey: Country Report on Austria, ECB WDN3 Country Report.

- Strzelecki, P., & Wyszyński, R. (2016). Poland’s labour market adjustment in times of economic slowdown – WDN3 survey results, NBP Working Papers 233, Narodowy Bank Polski, Economic Research Department.

- Verick, S. (2009). Who is hit hardest during a financial crisis? The vulnerability of young men and women to unemployment in an economic downturn, IZA DP No. 4359, August 2009.

Appendix 1. The WDN3 survey

In this paper, we use so-called WDN3 survey, conducted in 2014 by national central banks in 24 countries of the European Union. This survey constitutes the main data source we use to deal with these issues. This survey is the third wave of enquiries led by the Wage Dynamics Network (WDN) of the European System of Central Banks, a research network dedicated to the study of the features and sources of wage and labour cost dynamics and their implications for monetary policy in the euro area. The first survey on firms’ price and wage setting practices has been carried out by 17 national central banks in 2007–2008. Additional questions – mainly to respondents of the first wave – have then been issued in a short second wave in 2009, in order to assess the firms’ reaction to the global financial crisis of 2007–2008.

Since late 2009, the European countries have been confronted to the sovereign debts crisis, and labour market reforms have occurred: the third wave was designed to measure the nature of shocks and the firms’ reaction during the period 2010–2013, and especially the adjustments they made in their price and wage settings practices. The harmonized questionnaire contains three main parts: the nature of the shocks (changes in demand, in accessibility of funding, costs and mainly elements of the labour costs), the adjustments on employment and wages, and the main obstacles to hiring.

Each participating national central bank was responsible for the translation of the questionnaire and for the conduct of the survey in the country. Each central bank chose both the sample computation and the data collection method for its national data, leading to a large variety of sample computation and data characteristics. More than 24,000 firms were surveyed during the year 2014: if the perimeter of sectors can differ from a country to another, the manufacturing, trade, business services and, to a lesser extent, construction are well represented across the participating countries. To improve firm comparability between countries we restrict our analysis to the three main sectors – manufacturing, trade and business services (see for detailed information on sample).

In most countries, firms with less than 5 employees were excluded from the survey: they only represent 2% of the data. 29% of firms have 5–19 employees, 24% 20–49, 25% 50–199 and 20% more than 200 employees. For all countries we only include firms with at least 5 employees.

Table A1. Survey sample by country, sector and size (firms that provided answers about credit availability).

Table A2. List of the WDN3 questions used in this paper.

Table A3. Share of firms in manufacturing, trade and business services, who reported need to reduce labour input or alter its composition; and use of labour adjustment measures by corresponding firms, %.