?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This article investigates the effects of the political connectedness on the business performance of private sector firms in South East Europe. This question is relevant to contemporary ideas about the importance of ‘state capture’ in the region, and the article provides a new perspective on the nature and consequences of this phenomenon. Analysis of survey data reveals that political connections tend to undermine the business performance of connected firms, with a potential negative impact on the economic development of the countries concerned. It is argued that this process is better described as ‘business capture’ rather than ‘state capture’. The terminology is important as it suggests how policies might be used to manage this issue. The negative effect on business performance is substantial, especially in service sectors and in countries of the Western Balkans. The EU member states of the region are relatively immune from the negative effects of business capture.

1 Introduction

The concept of state capture has risen up the policy and research agenda in South East Europe (SEE) in recent years. State capture has been defined in different ways, but generally refers to the existence of cosy relations between political and business elites. In particular, it refers to the way in which powerful business interests may use bribery and corruption to influence public policy in their favour. The discussion of state capture in SEE has been carried out in the context of recent experience with democratic backsliding, competitive authoritarianism, and the emergence of illiberal democracies (Kapidžić, Citation2020; Stojarova, Citation2020). In the Western Balkans, it has been linked to the reversal of democratic reforms and a reversion to more authoritarian modes of governance (Bieber, Citation2018, Citation2020). These trends are thought to be associated with links between political elites and business leaders aimed at enhancing their positions of power and privilege (Keil, Citation2018). However, relatively little attention has been paid to the economics of state capture. This is puzzling because there is a large literature exploring the business performance of politically connected firms in a number of different national contexts. This article addresses this gap by analysing the impact of political connections on business performance in SEE.

The development of the political connections of business firms has been especially important in transition and emerging economies where state institutions are weak. In the institutional haze, firms seek protection through political connections to counteract the lack of legal certainty offered by ineffective legal systems and the absence of a level playing field for doing business. Such political connectedness of firms may have either a positive or negative influence on business performance. On the positive side (for the firms involved), political connections may provide privileged access to finance, enable firms to avoid regulatory barriers, obtain licences and permits more easily than other firms, and protect against commercial corruption and mafia attentions. On the negative side, political connections may be inimical to business success, as investment decisions may be biased in favour of political interests causing a misallocation of resources. If easy access to credit is enabled by political connectedness, the resulting investments may be wasteful and inefficient. Political connections may also involve tunnelling and asset stripping of firms in favour of political sponsors.

In this article, I apply these ideas to the case of political connectedness in SEE. Following Yakovlev (Citation2006) for the Russian case and Szanyi (Citation2019) for the Hungarian case, I argue that the economic systems that have been established SEE may also be best described as examples of ‘business capture’ in which the state, and through it a dominant political elite, holds sway over the business sector and whose leading personalities are closely entangled with it. In this system, the political elite that dominates the state seeks to control the business sector through neopatrimonial networks of personal connections within and between the political and business elites.Footnote1 In rare cases in which large firms have become potentially more powerful than the state, the latter has invariably stepped in to assert its control. In order to investigate these issues, I make use of the EBRD BEEPS survey to identify the key research question concerning the impact of such political connectedness on business performance in SEE.

The next section reviews the literature on political connectedness and state capture and identifies some examples of politically connected firms in SEE. Section 3 sets out the methodology and the data sources used and presents the descriptive statistics. Section 4 presents the analysis using non-linear regression modelling incorporating interactions between political connectedness and other categorical explanatory variables. The regression model emphasises the marginal effects of political connectedness on firm performance in SEE measured through the prism of employment growth. Section 5 presents the conclusions and policy implications.

2 Political connectedness and state capture

The concept of state capture first proposed by Hellman et al. (Citation2003) can be distinguished from the classical concept of ‘regulatory capture’ (Stigler, Citation1971) as being a form of high-level corruption. It is associated with the experience of the transition in Eastern Europe, especially in the former Soviet Union. While under socialism the state influenced the economy, under state capture the business sector ‘captures’ the state. Hellman et al. (Citation2003) distinguish two ideal types of state capture, distinguished by the difference between ‘captor firms’ and ‘influential firms’. Captor firms, often newly established private businesses run by wealthy tycoons, use bribery and corrupt practices (not excluding the use of force) to buy influence among leading politicians and other state personnel. These firms are not influential in a political sense, and so have a need to use financial resources to buy protection in weak states where the rule of law is not well established. In the successor states of the former Soviet Union, the tycoon owners of such firms have often gained enormous wealth on the basis of the privatisation of state-owned natural resources companies. In contrast, influential firms gain protection from the state through their political connectedness. Influential firms may operate under continuing state ownership, or they may be new private firms with that have been established by members of the former nomenklatura – so-called ‘red capitalists’ – or they may have simply appointed serving politicians to their managing board.

More recent interpretations of state capture in Central and Eastern Europe (CEE) have questioned the prevalence of captor firms in that transition region, where the new business elite does not have access to great wealth based on natural resources. Rather than businesses capturing the state, in CEE it seems that the state, in the form of dominant political parties, has captured key parts of the business sector. Innes (Citation2014) argues that the dominant political parties in CEE economies have captured the business sector through a process of what she calls ‘party state capture’, while Szanyi (Citation2019, p. 2) calls this ‘business capture’ (in contrast to state capture). Business capture is exercised through regulatory tools including the use of selective measures favouring politically aligned businesses, and public policies are adopted that shield politically connected firms from market competition. Business capture thus establishes a patronage state, which facilitates rent-seeking by politicians and other state personnel (Szanyi, Citation2019, p. 17). In the words of Madlovics and Magyar (Citation2020) ‘[n]o longer are oligarchs or an organised underworld capturing the state, but instead a political enterprise, an “organised upperworld”, monopolises political power and captures the economy, including the oligarchs themselves.’ In such a system, the business sector is captured by a political-economic clan that operates as a ‘pyramidal patronal network’. The political leadership in such a system has the power to confiscate the property of favoured businesses if they become too powerful, while political connections provide firms with protection from the arbitrary power of lower-level bureaucrats and privileged access to business loans, credits and contracts.

2.1 Political connectedness and firm performance

The phenomenon of business capture is closely connected to political connectedness of firms. It is not unique to South East Europe, or even to transition economies in general. In a study of newly privatised firms around the world, Boubakri et al. (Citation2008) found that 35.5% out of a sample of 245 such firms had political connections, defined as having a politician or ex-politician on the company board. Such politically connected firms were found to be more prevalent in countries with lower levels of judicial independence.

Many studies of politically connected firms focus on the advantages this practice confers, such as providing protection from competitors, preferential access to finance, tax privileges, and preferential access to government subsidies and bank loans. Much of the research has been conducted in China. Several studies found that politically connected firms obtain preferential access to credit (Liu et al., Citation2018). Having political connections in the form of independent directors linked to the ruling Party shields private firms from unfavourable government intervention. Chinese private firms that foster political connections with government officials are able to grow even in a weak property rights environment (Kung & Ma, Citation2018; Wu et al., Citation2018). Easy access to credit and other preferential advantages for politically connected firms have also been observed in Taiwan (Shen & Lin, Citation2016), Indonesia, (Fu et al., Citation2017), Korea (Shin et al., Citation2018) and Malaysia (Phan et al., Citation2020).

While the above studies identify the benefits of political connections, such as easier access to bank loans, others identify the downside of such advantages in the form of over-investment and inferior efficiency and competitiveness. For example, in the early stage of transition in Russia and Eastern Europe, Vishny and Shleifer (Citation1994) argued that political connections adversely affect corporate decisions, distort incentives and lead to a misallocation of investment, and thus undermine a firm’s competitiveness. In a much-quoted 45-country study, Faccio et al. (Citation2006) showed that while politically connected firms are more likely to receive preferential corporate bailouts, they experience a lower rate of return on assets than bailed-out firms without political connections. They argue that this shows that political connections cause an inefficient allocation of capital. Boubakri et al. (Citation2008), in the study cited above, found that the economic performance of politically connected firms is significantly worse than that of politically unconnected firms. For transition economies, Ruziev and Webber (Citation2019) show that political connectedness among SMEs diverts investment loans and credits away from those without such connections, leading to an overall misallocation of resources with a negative impact on growth.Footnote2 Several Chinese studies also came to similar conclusions regarding the economic inefficiency of political connections. Ling et al. (Citation2016) showed that politically connected real estate companies with easier access to long-term bank loans than others tend to overinvest, and as a result have a lower return on assets. Shi et al. (Citation2018) shows that politically connected independent directors destroy firm value because they are ineffective in monitoring managers’ performance. Li et al. (Citation2019) identified a negative relationship between political connections and economic efficiency in Chinese renewable energy firms. There are many other examples from around the world in which political connections lead to poor company performance. For example, a negative relationship between political connectedness and firm performance has been identified in Pakistan (Saeed et al., Citation2016) and in Korea (Schoenherr, Citation2019). In the latter example, political connections enable private firms to win government contracts, which have often been executed inefficiently and at relatively high cost.

2.2 Business capture and political connectedness in SEE

Scholars of South East European politics have identified to the close linkages between the political and economic elites as a key characteristic of the political economy of the region, often referred to as ‘state capture’. Keil (Citation2018: p. 61, footnote 1) defines state capture as:

efforts by either groups or individuals in the public and private sectors to influence, manipulate and shape laws, policies, regulations, decrees and other government policies to their advantage … in which actors take control over large parts of the institutional set-up in order to push a certain policy agenda and promote their own interests.

While referring to the earlier work of Hellman et al. (Citation2003), this definition does not seem much different from that of Stigler’s ‘regulatory capture’. It defines state capture as an act of agency by the business sector to influence government policies and laws. In this article, however, I investigate the linkages between the political and economic elites through the prism of political connectedness exercised through neopatrimonial networks. Considering the economic dimensions of such connectedness between the political elite and the business elite, such linkages can be characterised as ‘business capture’ rather than state capture (Yakovlev, Citation2006; Szanyi, Citation2019) or even ‘society capture’ in the term used by Cvetičanin et al. (Citation2023) to describe the capture of social institutions beyond the business sector. Such business capture is a system in which ‘public power is exercised mainly for private gain’ (Innes, Citation2014). Another way of thinking about this is that the phenomenon of business capture that characterises CEE and SEE regions is a variant the ‘influential firms’ discussed by of Hellman et al. (Citation2003) rather than their ‘captor firms’ that were (and still are) prevalent in the former Soviet Union. Bieber (Citation2018, pp. 347–348; Bieber, Citation2020, p. 109) describes state capture as the ‘control of state resources for illicit purposes by a small elite in control of the state [which is] the leadership of the ruling parties.’ This definition is more in line with the concept of business capture which I use in this article.

Business capture is closely related to practices of clientelism and rent seeking by ruling political parties. Sotiropoulos (Citation2017) identifies typical practices of ruling parties in the region, including offering plum contracts to favoured companies who give kickbacks to the dominant party in power and the placement of party loyalists in prime positions in public enterprises both at national and local level. In addition, numerous examples of clientelism and its systematic use by ruling parties to attract votes and retain a hold on power has been documented in Croatia by Vuković (Citation2019) and in Serbia and Kosovo by Cvejić (Citation2016b, Citation2016a). The consequences of clientelism can be severe. In Croatia, the political connectedness of Agrokor, a giant agricultural and retail conglomerate, led to its downfall through excessive over-expansion and indebtedness amounting to €6 billion, or 10% of all corporate debt in the country when it collapsed in 2017 (Ivanković, Citation2017; Klepo et al., Citation2017). Pavlović (Citation2019) provides examples from Serbia of contracts between the government and private firms with confidentiality clauses that are not transparent to public view, of public procurement contracts awarded to favoured companies, and of the (mis)allocation of public funds by state agencies to politically connected firms.

The growth of clientelism in SEE has been associated with the nature of privatisation that took place in the region. In Croatia, privatisation in the 1990s transferred assets into the hands of a relatively small number of politically connected tycoons (Petričić, Citation2000). In Serbia, the privatisation process provided ample opportunities for rent-seeking bureaucrats and politicians to acquire socially owned enterprises, some of which subsequently collapse due to asset stripping, while others survived retaining their strong political connections (Ivanović et al., Citation2019; Vujačić & Petrović Vujačić, Citation2016). One well-known case was that of the businessman Miroslav Mišković who had taken part in the privatisation process in Serbia becoming owner of a large retail company, and by 2007 was ranked on the Forbes list among the world’s thousand richest people (Pavlović, Citation2020). The May 2012 elections brought to power a coalition government led by the Serbian Progressive Party (SNS). In fulfilment of voter expectations, a crackdown on corruption was initiated and Mišković was arrested in December 2012 along with eight others on charges of embezzlement in connection with the privatisation of road maintenance companies (Buckley & MacDowell, Citation2012). The Serbian Special Prosecutor for Organised Crime alleged that the suspects had gained an ‘illegal profit’. In 2016 the Belgrade High Court acquitted Mišković of the abuse-of-office charges. After various twists and turns, the defendant was found guilty of tax evasion by the Belgrade High Court and sentenced to two and a half years in prison (Stojanovic, Citation2019). Given the ability of the government to put pressure on the judiciary, this example of back-and-forth movement in a high-profile commercial law case illustrates the dominance of the political elite over even the most powerful businesses in Serbia. In North Macedonia, the process of privatisation created many politically connected firms. According to Boduszynski (Citation2010, p. 167) ‘Macedonian privatisation policy turned out to be a fiasco, with most firms sold to SDSM [the Social Democratic Union of Macedonia] insiders at “preferential” rates. The politically connected managers who acquired the larger firms and banks could also rely on their insider status to secure … loans from the unprivatised and government-controlled banks.’

Numerous other examples of political connectedness of private firms in SEE have been reported in the media and reports of international organisations. An investigation by the media group BIRN revealed the close connections between lighting companies from Serbia and Hungary and the ruling elites in both countries; it is argued that these connections enabled the companies to win contracts to provide street lighting in numerous towns and cities (Curic & Zöldi, Citation2019). In Montenegro, the former Prime Minister and his family owned a major bank and several private companies. During the 2008 financial crisis the bank was bailed out with public funds (Petričić, Citation2000). In Kosovo, companies in the quarrying sector with political ties are alleged to have gained favourable contracts in road-building programmes (KDI, Citation2018, p. 16). In Slovenia, Domadenik et al. (Citation2016) found that 16% of supervisory board members in private firms were politically connected over the period 2000–2010 and that firms with politically connected supervisory board members had lower productivity than non-connected firms.

3 Methodology

Empirically, political connectedness can be viewed as one of several determinants of a firm’s business performance alongside more standard explanatory factors such as the size, age, and sector of operation of a firm. The effect of firm size on growth has been subject of much scrutiny. Some studies have shown a positive relationship between size and growth, given that larger firms have easier access to finance and may be dominant actors in the market (Bentzen et al., Citation2012; Singh & Whittington, Citation1975). Other studies have shown a negative relationship between size and growth, which may be due to smaller firms being further away from the industry optimal size, and also due to their greater flexibility and adaptability to changes in demand (Rogers et al., Citation2010). In SEE, Banerjee and Jesenko (Citation2016) found a positive relationship between firm size and firm growth in the case of Slovenia, but they also found that this effect diminishes with size. For Croatia, Perić et al. (Citation2020) found a similar positive relationship between firm size and growth in the period since the economic and financial crisis of 2008. It is also thought that age will have a negative effect on growth, because newer firms are more likely to have arisen in response to dynamic changes in demand and to incorporate more recent technology and be more innovative than older firms (Coad et al., Citation2016; Evans, Citation1987). The effect of the sector of activity is ambiguous because the growth of firms in different sectors depends largely on the evolution of demand for different products.

The literature on political connectedness of firms in transition and emerging economies has highlighted its ambiguous effects on business performance. As shown above, previous studies have identified a range of channels through which connectedness may affect firm performance. Some of these are likely to underpin a positive effect of connectedness of growth, through channels such as privileged access to loans and public sector contracts. There may also be offsetting negative causal influences between political connectedness and firm performance, since connectedness may lead to inefficient investment decisions as well as making firms more vulnerable to asset stripping. Since either of these potential outcomes may occur, it is of interest to identify which of these two potential effects is dominant in SEE, or whether they balance each other out giving rise to an overall neutral impact of connectedness on business performance.

In this article, I take the growth of employment as an indicator of the business performance of firms in SEE. The focus on employment growth as a proxy for business performance assumes that at any point in time each firm faces more or less the same technology and, since the capital-labour ratio required to produce a unit of output will be the same for all firms, employment size reflects the level of investment in the firm. Over the relatively short period of three years, it can be further assumed that no major labour-saving changes in technology would have taken place which would affect the demand for labour.Footnote3

The model which I propose to test therefore takes the following form:

where:

employment growth = [(E in year t – E in year t-3)/E in year t-3)] (where E= number of permanent full-time employees) (continuous variable)

size = number of full-time employees in the firm in year t (continuous variable)

age = number of years since the firm was founded (continuous variable)

connected = whether the owner, CEO, top manager, or any of the board members in political position (0–1 dummy variable)

sector = manufacturing or services sector (0–1 dummy variable)Footnote4

country = country in which firm is based (0–1 dummy variable)

= individual firm

ε = disturbance term

The model explains business performance of firms, proxied by employment growth, as a function of the size of firms (measured by employment), the age of firms, the broad sector in which they operate and whether a firm has political connections. Squared terms in size and age take account of non-linearities in these two variables. Due to the skewed distribution of firms’ employment growth rates, I use the natural logarithm of the employment growth rate which has an approximately normal distribution. Since it is not possible to take a logarithm of a negative number, I shift the axis by one unit by adding 1 to the employment growth rate before taking the logarithm. Firm size and age also enter in log form, so the elasticity of employment growth with respect to size and age of firm that is relatively straightforward to determine.Footnote5 The effect of connectedness on employment growth is given by the coefficient , the effect of sector is given by the coefficient

, while the effect of individual country characteristics is given by the coefficient value

. In estimating the model in below I also allow for interaction effects between connectedness and sector, and connectedness and country.

Table 1. Descriptive statistics for main variables for selected SEE countries.

Table 2. Characteristics of politically connected firms by country, age, size and growth.

Table 3. Determinants of employment growth (dependent variable).

3.1 Data

The EBRD-World Bank Business Environment and Enterprise Performance Survey (BEEPS) provides an ideal tool to analyse the nature of political connectedness of firms and its economic effects in South East Europe. The sixth round of the BEEPS survey (BEEPS VI) was carried out in 2018–2020 and covered approximately 25,733 enterprises in 38 countries.Footnote6 This article uses data from the survey for Albania and Bulgaria and all the countries of former Yugoslavia (Bosnia and Herzegovina, Croatia, Kosovo, Montenegro, North Macedonia, Serbia and Slovenia) covering 3,466 firms, most of which were surveyed in 2019. shows the descriptive statistics of the key variables that are used in the model analysed in the next section.

Within the sample, the mean size of firms was 92 permanent full-time employees at the time of the survey, having increased from an average of 87 employees three years prior. Economic growth was proceeding apace in the region at this time (before the outbreak of the corona virus pandemic) and this is reflected in a 15% mean of employment growth over this period, or about 5% per annum on average. The variation of growth is large, with some firms shrinking and other fast-growth firms expanding at a rapid rate. Within the sample about 43% of firms are in the manufacturing sector, with the rest in various service activities including retail trade, wholesale trade, construction and other service activities. Finally, about 4.5% of the firms have political connections, defined as whether the owner, CEO, top manager, or any of the board members in political position, ranging from 2.5% in Bulgaria to 10.7% in Montenegro.Footnote7 In absolute numbers, there are 156 politically connected firms in the sample, ranging from 10 politically connected firms in the North Macedonian sample to 30 politically connected firms in the Bosnia and Herzegovina sample.

The age and size of firms varies across countries (see ). The average age of firms ranges from 16 years in Albania to 27 years in Slovenia. Politically connected firms tend to be slightly older than unconnected firms and almost twice as large. However, this pattern is not uniform. There is little difference in the age of politically connected and unconnected firms in Bulgaria, Croatia, Serbia and Slovenia. The pattern of size differences is reversed in Bosnia and Herzegovina, Croatia and Slovenia. The data also show that, on average, being politically connected appears to reduce annual employment growth of the sample firms by about 3% points.

4 Empirical analysis and results

The estimation of the model is shown in . It begins with the most parsimonious version, with three explanatory variables – size and age and connectedness of the firms, for the SEE region as a whole (model 1). Following that, the squared values of the size and age variables are added to account for non-linearities in these variables (model 2). Model 3 brings in the sector variable, allowing this to interact with connectedness to identify the separate effect of connectedness across sectors. Model 4 brings in the individual countries as explanatory variables (as 0–1 dummies) while model 5 allows for the additional interaction of country by connectedness to identify differences in the influence of political connectedness across countries. The model is estimated using ordinary least squares (OLS). The Breusch–Pagan test of heteroscedasticity is used to identify whether the OLS assumption of constant variance of the disturbance term can be rejected. Where the assumption of constant variance of the disturbance term is rejected, robust standard errors are estimated. The model is estimated using the STATA econometrics package.

The estimation of the first model shows that the natural log of employment growth is positively related to firm size and negatively related to firm age, both at a 1% level of significance. The elasticity of the natural log of (3-year employment growth+1) to firm size is 0.044, so that a 1% increase in size is associated with to an annual 4.4% increase in employment growth over three years, or 1.5% on an annual basis. Similarly, the elasticity with respect to age is 0.094, more than double the effect of size, but in the opposite direction. Overall, the estimated model shows that younger and larger are firms, the faster is their employment growth and vice versa.

The estimated model also shows that, in SEE, political connectedness has a significant negative effect on firm performance, as measured by firm’s employment growth. The effect is significant at the 10% level (bordering on the 5% level of significance). It shows that, controlling for other factors, firms that are politically connected can expect to grow at an annual rate 1.66% points slower than unconnected firms.Footnote8

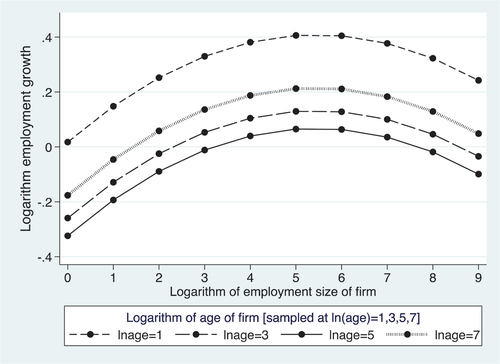

Model 2 shows the effect of adding non-linear terms for size and growth. The squared values are significant at the 1% level. In the case of firm size, employment growth increases up to a point, but for larger firms, it decreases giving rise to an inverted U-shape. The opposite is true for firm age. portrays this effect. The fastest employment growth is found in young firms aged around 3 years with a size of between around 200 employees.

Figure 1. Predicted employment growth by firm size and age .

Models 3–5 introduce interactions of connectedness with sector and country. The full effects of the interaction terms are not revealed by the simple coefficients in the main regression table. Instead, it is necessary to inspect the marginal effects and the contrasts of the predictive margins, which take into account both the interaction and the main effect together (Brambor et al., Citation2006). These are shown in the last three columns of . Row 1 shows that politically connected firms have worse business performance than unconnected firms in every version of the model. In all cases, the contrast is negative, indicating that connections lead to a slower rate of employment growth compared to unconnected firms. The estimated contrast between the growth rates of connected and unconnected firms is between −0.043 and −0.054. The latter estimate has the highest precision being significant at the 5% level. It is given by model 5, which estimates the interactions between connectedness and both sector and country, and also uses country dummies. In terms of actual employment growth, this model predicts that political connectedness reduces annual employment growth rate by 1.75% points compared to non-connected firms.

The impact of connectedness on employment growth differs across sectors. It has a significant impact in the services sector, reducing annual employment growth in that sector by 2.19% points. However, there is no effect of connectedness on employment growth in the manufacturing sector. Political connectedness in the services sector has a distinctly negative impact on business performance, in sectors such as retail and wholesale, and in construction. Examples of the negative impact of political connectedness in the construction sector have been noted above in Serbian street lighting and in Kosovan road-building activities.

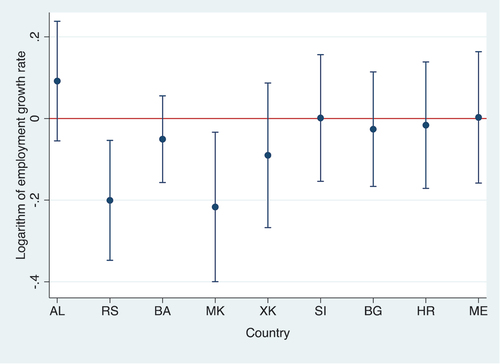

The contrasts of predictive margins of employment growth for connected firms (versus unconnected) are significant at 1% level for Serbia (−0.203,t = −2.72) and at 5% level for North Macedonia (−0.216, t = −2.31) (see also ). This suggests that political connectedness is especially important factor in firm performance in these two countries. In Serbia, being politically connected has an adverse effect on firm performance equivalent to a 6.1% point annual reduction in employment growth, while in North Macedonia the effect is equivalent to a reduction in annual employment growth of 6.5% points (see also ). Large negative effects are also observed in Bosnia and Herzegovina, and Kosovo, but these effects are not statistically significant even at the 10% level. The only case in which the effect of political connectedness has a positive impact on firm performance, Albania, also does not pass the test of statistical significance.Footnote9 It is also apparent that political connectedness has no overall impact on firm performance in the EU members states in South East Europe: Slovenia, Bulgaria and Croatia, or in the most advanced candidate state Montenegro.

Figure 2. Predicted employment growth of connected firms with 95% confidence intervals.

5 Conclusions

This article has argued that the phenomenon often referred to as ‘state capture’ in South East Europe can better be described as ‘business capture’. State capture, in its initial formulation, referred to a process by which large enterprises run by wealthy tycoons captured state institutions through means of bribery and corruption. This may have been a good characterisation of the situation in Russia following the break-up of the Soviet Union and the unruly process of privatisation that led to a massive accumulation of wealth by the new owners of large firms in the natural resources sector. However, in South East Europe, although there have been examples in which privatisation led to the emergence of wealthy tycoon capitalists, firms were never large or powerful enough to capture the state. Instead, ruling political elites have emerged in the form of powerful clientelistic political parties that dominate the state and seek to control the business sector through neopatrimonial networks. This process has been illustrated in this article through a few examples from the emerging literature on state capture in the region, and from media reports of business capture in specific sectors such as construction and retail.

The concept of business capture relates to the idea of ‘influential firms’ as opposed to ‘captor firms’ identified in the classic article on state capture by Hellman et al. (Citation2003). The idea of influential firms illustrates the way in which business capture is implemented through close ties between political actors and business firms, through the appointment of politicians to company boards, or outright ownership of firms by politicians or members of their families. Such cases have been widely observed in many emerging economies and have been studied by analysing the effect of political connections on business performance. Some researchers have argued that political connections enhance firms’ performance through privileged access to loans and state procurement contracts, while others have pointed out that political connections can lead to poor business and investment decisions, a wasteful use of resources and may damage firms’ business performance as a result. In this sense, reducing or eliminating business capture should boost an affected countries’ economic growth.

Much of the research on state/business capture, clientelism and associated democratic backsliding has been based on qualitative research and case study examples. In this article, however, I have followed the empirical literature on the impact of political connections on business performance to develop and estimate a model of business capture in SEE. The results of the model show that in this region, on average, political connections have an overall negative impact on firm performance. This effect persists through a number of functional forms of the estimated model. The model also shows that the negative impact of political connections is especially severe in the services sectors of these economies, rather than in the manufacturing sectors. Examples given above relate to the cases of Agrokor in Croatia and Delta Holdings in Serbia, both large conglomerates with a large presence in the retail sector. It also shows that the Western Balkan countries have been more adversely affected by business capture than have the EU member states in the region, with the most significant negative effects of political connectedness occurring in North Macedonia and Serbia. Noticeable negative effects are also found in Bosnia and Herzegovina and in Kosovo, but the statistical significance of the impact in these two countries is weak, while a positive but non-significant effect is found in Albania.

In sum, the article has investigated the role state/business capture in SEE and shown that, rather than states being captured by business interests, it is more often the case that the business sector is captured by the state through powerful neopatrimonial networks linked to clientelistic ruling parties. This process takes the form of political appointments to boards of private companies, or political officeholders (or members of their families) running firms as owners or managers. According to research into similar situations around the world, the effect of such political connections on business performance can be either positive or negative. The empirical analysis of political connections in this article has shown that such political connections tend to have an adverse impact on business performance in SEE. The policy implications are considerable. The focus on business capture and political connectedness suggests that public policy should emphasise support for non-connected firms, for example by supporting the entry of start-up firms. Public policy should also direct state support, and especially EU investment funds, to politically independent firms including both large independent firms and SMEs. This contrasts with the emphasis on introducing anti-corruption measures which have been the main focus of policy recommendations by those who see the problem as one of state capture rather than business capture, but which have mainly been ineffective.

Finally, the EU member states in SEE seem to be somewhat immune to the negative effects of political connectedness. While political connections persist in those countries, the more benign influences of political connectedness on business performance appear to offset the negative effects. Whether EU membership as such is responsible for this attenuation of the more pernicious effects of business capture in those countries remains to be studied in future research.

Disclosure statement

No potential conflict of interest was reported by the author.

Notes

1. Neopatrimonialism is a form of government in which personal connections and influence networks coexist with rational-legal forms of governance, and in extreme cases may form the dominant form of decision making with the aim of extracting resources from the state for private gain of politicians and government officials (see for example Bach, Citation2011).

2. This is the only other study of which I am aware that has used the BEEPS data to investigate the impact of political connectedness on business performance. However, the authors use different proxies for connectedness than I do, namely the ‘frequency of bribes and gifts’ and the ‘receipt of government contracts’. In my view, these represent imperfect measures of political connectedness compared to the one used in this study since bribes and gifts may be needed only by firms that are not politically connected (i.e. captor firms rather than influential firms defined by Hellman et al. (Citation2003), while both connected and non-connected firms may receive government contracts.

3. It should be noted that the concept of business performance is multifaceted and, were robust data available, it might be possible to widen the research to cover alternative dependent variables such as profitability and market penetration indicators. However, since such data is not readily available, I would argue that reliance on employment growth of the firm is a reasonable working proxy, especially over a short three year period.

4. The firm’s sector is based on the firm’s main activity and product or service – the services sector includes wholesale and retail trade, construction and other services activities.

5. For example, the elasticity of employment growth with respect to size is equal to .

7. In the BEEPS survey, question BMb5 asks whether the owner, CEO, top manager, or any of the board members is in a political position either in a formal political (appointed or elected) position, or another position of authority, for example in the judicial system, government bureaucratic or the military, with direct or potential influence over policy.

8. Since the employment growth is measured over three years, the coefficient on connectedness of −0.051 is divided by 3 to give an annual effect of −0.0166.

9. It should be noted that both negative and positive effects at the individual firm level, controlling for other determinants of firm performance, can be distortive of the overall allocative efficiency of the whole economy.

References

- Bach, D. C. (2011). Patrimonialism and neopatrimonialism: Comparative trajectories and readings. Commonwealth & Comparative Politics, 49(3), 275–294. https://doi.org/10.1080/14662043.2011.582731

- Banerjee, B., & Jesenko, M. (2016). The role of firm size and firm age in employment growth: Evidence for slovenia, 1996-2013. The European Journal of Comparative Economics, 13(2), 199–219.

- Bentzen, J., Madsen, E. S., & Smith, V. (2012). Do firms’ growth rates depend on firm size? Small Business Economics, 39(4), 937–947. https://doi.org/10.1007/s11187-011-9341-8

- Bieber, F. (2018). Patterns of competitive authoritarianism in the Western Balkans. East European Politics, 34(3), 337–354. https://doi.org/10.1080/21599165.2018.1490272

- Bieber, F. (2020). The rise of authoritarianism in the Western Balkans. Palgrave Macmillan.

- Boduszynski, M. P. (2010). Regime change in the Yugoslav successor states: Divergent paths towards a new Europe. The John Hopkins University Press.

- Boubakri, N., Cosset, J. -C., & Saffar, W. (2008). Political connections of newly privatized firms. Journal of Corporate Finance, 14(5), 654–673. https://doi.org/10.1016/j.jcorpfin.2008.08.003

- Brambor, T., Roberts Clark, W., & Golder, M. (2006). Understanding interaction models: Improving empirical analysis. Political Analysis, 14(1), 63–82. https://doi.org/10.1093/pan/mpi014

- Buckley, N., & MacDowell, A. (2012). Serbian tycoon arrested in graft probe. Financial Times, December 12th. https://www.ft.com/content/aa6ef120-4443-11e2-952a-00144feabdc0

- Coad, A., Segarra, A., & Teruel, M. (2016). Innovation and firm growth: Does firm age play a role?. Research Policy, 45(2), 387–400.

- Curic, A., & Zöldi, B. (2019). The illumination of Serbia, Hungarian style. Balkan Insight, June 26. https://balkaninsight.com/2019/06/26/illumination-of-serbia-hungarian-style/

- Cvejić, S. (Ed.). (2016a). Informal power networks, political patronage and clientelism in Serbia and Kosovo. SeCons.

- Cvejić, S. (2016b). On the inevitability of political clientelism in contemporary Serbia. Sociologija, LVIII(2), 239–252. https://doi.org/10.2298/SOC1602239C

- Cvetičanin, P., Bliznakovski, J., & Krstić, N. (2023). Captured states and/or captured societies in the Western Balkans. Southeast European and Black Sea Studies.

- Domadenik, P., Prašnikar, J., & Svejnar, J. (2016). Political connectedness, corporate governance, and firm performance. Journal of Business Ethics, 139(2), 411–428. https://doi.org/10.1007/s10551-015-2675-4

- Evans, D. S. (1987). The relationship between firm growth, size and age: Estimates for 100 manufacturing industries. The Journal of Industrial Economics, 35(4), 567–581. https://doi.org/10.2307/2098588

- Faccio, M., Masulis, R. W., & McConnell, J. J. (2006). Political connections and corporate bailouts. The Journal of Finance, 61(6), 2597–2635. https://doi.org/10.1111/j.1540-6261.2006.01000.x

- Fu, J., Shimamoto, D., & Todo, Y. (2017). Can firms with political connections borrow more than those without? Evidence from firm-level data for Indonesia. Journal of Asian Economics, 52, 45–55. https://doi.org/10.1016/j.asieco.2017.08.003

- Hellman, J. S., Jones, G., & Kaufmann, D. (2003). Seize the state, seize the day: State capture and influence in transition economies. Journal of Comparative Economics, 31(4), 751–773. https://doi.org/10.1016/j.jce.2003.09.006

- Innes, A. (2014). The political economy of state capture in Central Europe. Journal of Common Market Studies, 52(1), 88–104. https://doi.org/10.1111/jcms.12079

- Ivanković, Ž. (2017). The political economy of crony capitalism: A case study of the collapse of the largest Croatian conglomerate. Politička misao, 54(4), 40–60.

- Ivanović, V., Kufenko, V., Begović, B., Stanišić, N., & Geloso, V. (2019). Continuity under a different name: The outcome of privatisation in Serbia. New Political Economy, 24(2), 159–180. https://doi.org/10.1080/13563467.2018.1426563

- Kapidžić, D. (2020). The rise of illiberal politics in Southeast Europe. Southeast European and Black Sea Studies, 20(1), 1–17. https://doi.org/10.1080/14683857.2020.1709701

- KDI. (2018). State capture in Kosovo: The political economy of gravel. Kosova Democratic Institute.

- Keil, S. (2018). The business of state capture and the rise of authoritarianism in Kosovo, Macedonia, Montenegro and Serbia. Southeastern Europe, 42(1), 59–82. https://doi.org/10.1163/18763332-04201004

- Klepo, M., Bićanić, I., & Ivanković, Z. (2017). Slučaj agrokor: Kriza najveće hrvatske kompanije [The Case of Agrokor: the Crisis of the Largest Croatian Company]. Friedrich Ebert Stiftung.

- Kung, J. K., & Ma, C. (2018). Friends with benefits: How political connections help to sustain private enterprise growth in China. Economica, 85(337), 41–74. https://doi.org/10.1111/ecca.12212

- Ling, L., Zhou, X., Liang, Q., Song, P., & Zeng, H. (2016). Political connections, overinvestments and firm performance: Evidence from Chines listed real estate companies. Finance Research Letters, 18, 328–333. https://doi.org/10.1016/j.frl.2016.05.009

- Li, M., Sun, X., & Song-Turner, H. (2019). The impact of political connections on the efficiency of China’s renewable energy firms. Energy Economics, 83, 467–474. https://doi.org/10.1016/j.eneco.2019.06.014

- Liu, L., Liu, Q., Tian, G., & Wang, P. (2018). Government connections and the persistence of profitability: Evidence from Chinese listed firms. Emerging Markets Review, 36, 110–129. https://doi.org/10.1016/j.ememar.2018.04.002

- Madlovics, B., & Magyar, B. (2020). Post-communist predation: Modeling reiderstvo practices in contemporary predatory states. Public Choice, 187(3–4), 247–273. https://doi.org/10.1007/s11127-019-00772-7

- Pavlović, D. (2019). The political economy behind the gradual demise of democratic institutions in Serbia. Southeast European and Black Sea Studies, 20(1), 19–39. https://doi.org/10.1080/14683857.2019.1672929

- Pavlović D. (2020). The political economy behind the gradual demise of democratic institutions in Serbia. Southeast European and Black Sea Studies, 20(1), 19–39. https://doi.org/10.1080/14683857.2019.1672929

- Perić, M., Vitezić, V., & Perić Hadžić, A. (2020). Firm size - firm growth relationship during economic crisis. Ekonomska Misao i Praksa Dubrovnik, XXXI(1), 29–53.

- Petričić, D. (2000). Kriminal u hrvatskoj pretvorbi: tko, kako, zašto. Abakus.

- Phan, D. H. B., Tee, C. M., & Tran, V. T. (2020). Do different types of political connections affect corporate investments? Evidence from Malaysia. Emerging Markets Review, 42, 42. https://doi.org/10.1016/j.ememar.2019.100667

- Rogers, M., Helmers, C., & Koch, C. (2010). Firm growth and size. Applied Economics Letters, 17(16), 1547–1550. https://doi.org/10.1080/13504850903085043

- Ruziev, K., & Webber, D. J. (2019). Does connectedness improve SMEs’ access to formal finance? Evidence from post-communist economies. Post-Communist Economies, 31(2), 258–278. https://doi.org/10.1080/14631377.2018.1470855

- Saeed, A., Belghitar, Y., & Clark, E. (2016). Do political connections affect firm performance? Evidence from a developing country. Emerging Markets Finance and Trade, 52(8), 1876–1891. https://doi.org/10.1080/1540496X.2015.1041845

- Schoenherr, D. (2019). Political connections and allocative distortions. The Journal of Finance, 74(2), 543–586. https://doi.org/10.1111/jofi.12751

- Shen, C., & Lin, C. (2016). Political connections, financial constraints, and corporate investment. Review of Quantitative Finance and Accounting, 47(2), 343–368. https://doi.org/10.1007/s11156-015-0503-7

- Shin, J. Y., Hyun, J., Oh, S., & Yang, H. (2018). The effects of politically connected outside directors on firm performance: Evidence from Korean chaebol firms. Corporate Governance an International Review, 26(1), 23–44. https://doi.org/10.1111/corg.12203

- Shi, H., Xu, H., & Zhang, X. (2018). Do politically connected independent directors create or destroy value? Journal of Business Research, 83, 82–96. https://doi.org/10.1016/j.jbusres.2017.10.009

- Singh, A., & Whittington, G. (1975). The size and growth of firms. The Review of Economic Studies, 42(1), 15–26. https://doi.org/10.2307/2296816

- Sotiropoulos. (2017). Corruption, anti-corruption and democracy in the Western Balkans. Politicke perspektive, 7(3), 7–26.

- Stigler, G. (1971). The theory of economic regulation. Bell Journal of Economics and Management Science, 2(1), 3–21. https://doi.org/10.2307/3003160

- Stojanovic, M. (2019). Serbia convicts businessman Miskovic of tax evasion. https://balkaninsight.com/2019/03/08/serbia-convicts-businessman-miskovic-of-tax-evasion/

- Stojarova, V. (2020). Moving towards EU membership and away from liberal democracy. Southeast European and Black Sea Studies, 20(1), 221–236. https://doi.org/10.1080/14683857.2019.1709723

- Szanyi, M. (2019). The emergence of patronage and changing forms of rent-seeking in East Central Europe. Post-Communist Economies, 34(1), 122–141. https://doi.org/10.1080/14631377.2019.1693738

- Vishny, R. W., & Shleifer, A. (1994). Politicians and firms. The Quarterly Journal of Economics, 104(4), 995–1025. https://doi.org/10.2307/2118354

- Vujačić, I., & Petrović Vujačić, J. (2016). Privatization in Serbia: An assessment of the last round. Economic Annals, LXI(209), 45–77. https://doi.org/10.2298/EKA1609045V

- Vuković, V. (2019). Political economy of corruption, clientelism and vote buying in Croatian local government. In Z. Petak & K. Kotarski (Eds.), Policy-making at the European Periphery: The case of Croatia (pp. 107–124). Palgrave Macmillan.

- Wu, H., Li, S., Ying, S. X., & Chen, X. (2018). Politically connected CEOs, firm performance, and CEO pay. Journal of Business Research, 91, 169–180. https://doi.org/10.1016/j.jbusres.2018.06.003

- Yakovlev, A. (2006). The evolution of business – state interaction in Russia: From state capture to business capture? Europe-Asia Studies, 58(7), 1033–1056. https://doi.org/10.1080/09668130600926256