Abstract

A growing body of literature suggests that an economic case may exist for investment in large-scale climate change mitigation. At the same time, however, investment is persistently falling well short of the levels required to prevent dangerous climate change, suggesting that economically attractive mitigation opportunities are being missed. To understand whether and where these opportunities exist, this article contrasts macro-level analyses of climate finance with micro-level bottom-up analyses of the scale and composition of low-carbon investment opportunities in four case study developing world cities. This analysis finds that there are significant opportunities to redirect existing finance streams towards more cost-effective, lower-carbon options. This would mobilize substantial new investment in climate mitigation. Two key explanations are proposed for the failure to exploit these opportunities. First, the composition of cost-effective measures is highly context-specific, varying from place to place and sector to sector. Macro-level analyses of climate finance flows are therefore poor indicators of the micro-level landscape for low-carbon investment. Specific local research is therefore needed to understand the opportunities for cost-effective mitigation at that level. Second, many opportunities require enabling governance arrangements that are not currently in place. Mobilizing new low-carbon investment and closing the ‘climate finance gap' therefore requires attention to policy frameworks and financing mechanisms that can facilitate the exploitation of cost-effective low-carbon options.

Policy relevance

The importance of increasing investment in climate mitigation, especially in developing nations, is well established. This article scrutinizes four city-level studies of the scope for cost-effective low-carbon investment, and finds that significant opportunities are not being exploited in developing world cities. Enabling governance structures may help to mainstream climate considerations into investments by local actors (households, businesses and government agencies). While climate finance distributed through international bodies such as the Green Climate Fund may not always be a suitable vehicle to invest directly in disaggregated, local-level measures, it can provide the incentives to develop these governance arrangements.

1. Introduction

1.1. The climate finance gap

The economic benefits of early action to mitigate climate change have been well established (Doniger, Herzog, & Lashof, Citation2006; IPCC, 2014; Stern, Citation2006) and a more recent body of work suggests that a significant level of climate change mitigation is economic even on private terms (IEA, Citation2015; Somanathan et al., Citation2014). The International Energy Agency (IEA), for example, finds that fuel savings alone could more than pay for the new energy infrastructure needed to stay within 2 °C of warming (IEA, Citation2015). Moreover, a growing body of evidence finds that the wider impacts of climate mitigation are overwhelmingly positive and substantially enhance the case for action (Clark et al., Citation2014; Stern, Citation2015; Thurston, Citation2013; Ürge-Vorsatz, Danny Harvey, Mirasgedis, & Levine, Citation2007), although more analysis is needed (Tompkins et al., Citation2013).

Levels of investment in mitigation, however, are falling well short of what is required to prevent dangerous climate change. McKinsey (Citation2010), the IEA (Citation2013, Citation2014, Citation2015), and others (GEA, Citation2012; McCollum et al., Citation2013; WEF, Citation2013) estimate that between US$ 500 billion and US$ 1.6 trillion of low-carbon investment is required each year if dangerous climate change is to be avoided, but total low-carbon investment was only US$ 331 billion in 2013 (Buchner et al., Citation2014). There is therefore a significant climate finance gap.

Closing this gap may be most challenging in the developing world. The Intergovernmental Panel on Climate Change (IPCC, 2014) notes that many developing countries lack the institutional structures and technical capabilities needed to identify and implement low-emission development strategies, particularly given that other development priorities are competing for scarce financial resources (see Held, Charles, & Eva-Maria, Citation2014; Kato, Jane, Pieter, & Randy, Citation2014; Pauw, Citation2014). However, if an economic case for climate change mitigation exists, it may also be strongest in developing world cities. In 2014, developing nations accounted for more than half of global infrastructure spending (PWC, Citation2014). Cities are major recipients of this investment due to both historical infrastructure deficits and rapid economic and population growth: developing world cities are expected to be home to 5.2 billion people in 2050 (WHO, Citation2014). Redirecting business-as-usual investment towards low-carbon options in these contexts could therefore make a major contribution towards global mitigation efforts.

In this analysis, a bottom-up approach is adopted to assess the economic case for climate change mitigation in the cities of Johor Bahru in Malaysia, Lima–Callao (hereafter Lima) in Peru, Palembang in Indonesia and Kolkata in India. The results provide insights into two issues: the scale of the economic case for climate change mitigation at the local level compared with global assessments, and the current allocation of low-carbon investment compared with the cost-effective measures identified at the local scale. By highlighting these issues, this article documents unrealized opportunities to mobilize new resources for mitigation, reveals patterns that can help identify where the biggest barriers and opportunities lie, and offers insights on the governance structures that could a play a role if these barriers are to be overcome and the investment opportunities exploited.

This article is structured as follows. Section 2 provides an outline of our current understanding of the landscape of low-carbon investment. In Section 3, key descriptive statistics for the four case-study cities are presented. Section 4 outlines the methods, data sources and assumptions underpinning each city study. In Section 5, the results of the city-scale studies are presented and compared. In Section 6 the implications of these results for climate policy are discussed, particularly the interventions that are likely to be required at the local level if new forms of low-carbon investment are to be unlocked. Finally, Section 7 offers conclusions and policy recommendations.

2. The landscape of climate finance: A top-down perspective

Existing and future climate flows have been investigated by a number of authors (see Ampri et al., Citation2014; Bowen, Campiglio, & Tavoni, Citation2014; Clapp, Ellis, & Corfee-Morlot, Citation2012; Jakob et al., Citation2014; Jürgens et al., Citation2012; Kirkman, Seres, & Haites, Citation2013; Olbrisch, Haites, Savage, Dadhich, & Shrivastava, Citation2011). A challenge only very recently addressed has been the lack of a common set of guidelines and definitions to ensure consistency between estimates (World Bank, Citation2015). Therefore, existing estimates vary widely according to data availability, the focus of the study and researchers’ particular definitions of climate finance. Notably, even the term ‘climate finance’ itself is disputed: it can be narrowly used to refer to transfers of ‘new and additional financial resources’ from developed to developing countries, or more widely to refer to all financing channelled to climate mitigation and adaptation.

Arguably the most comprehensive review of recent climate finance flows is produced by the Climate Policy Initiative (CPI), whose estimates include all finance towards ‘emission reductions, climate resilience, and enabling environment projects' (Buchner et al., Citation2012, Citation2013, Citation2014). In other words, the CPI adopts a wide definition of climate finance encompassing total investment in low-carbon measures by the public and private sector, plus public framework expenditures such as policy design costs and capacity-building programmes. However, this assessment largely excludes household-level investment in low-carbon measures (for example, the purchase of more efficient appliances or retrofitting buildings) due to the complexity of data collection, and public revenue support (for example, the revenue from carbon credits or feed-in tariffs) due to the risk of double-counting (Falconer & Stadelmann, Citation2014).

Numbers from the CPI show that the total amount of climate finance was US$364 billion in 2011, US$359 billion in 2012 and US$331 billion in 2013. Compared to the estimates above, these data suggest that there is a persistent gap between current climate finance flows and the levels of investment required to prevent dangerous climate change (Buchner et al., Citation2014). Moreover, the analysis shows that low-carbon investments secure finance primarily from domestic rather than international sources. In 2013, 74% of global low-carbon investment originated in the country in which it was spent and 90% of the total level of private investment was spent in the country of origin (Buchner et al., Citation2014). This ‘home bias’ suggests that climate finance is not necessarily flowing to the most cost- or carbon-effective measures globally. This underscores the importance of providing economic evidence on the low-carbon investment opportunities available around the world, of increasing investors’ awareness of these opportunities, and of building local-level capacities to mobilize investment and deliver low-carbon measures.

According to Buchner et al. (Citation2012, Citation2013, Citation2014), the electricity sector has been the dominant recipient of low-carbon investment. They find that renewable electricity investments comprised 85% of all mitigation expenditure in 2011, 76% in 2012 and 78% in 2013. The dominance of this sector raises questions about whether commercially attractive opportunities for low-carbon investment in other sectors of the economy are being exploited, whether the electricity sector offers the most cost-effective mitigation options, and whether adequate enabling governance structures for low-carbon investment exist outside of the electricity sector.

These stylized facts provide a broad outline of the landscape for low-carbon investment on an international scale. The analysis presented below provides a means to compare the current flows of climate finance against opportunities for cost-effective mitigation in four case studies. This highlights the scope to redirect investment towards climate-friendly options, and thereby scale-up global climate finance.

3. The case studies

Studies of the economically attractive opportunities for low-carbon investment were conducted for the cities of Kolkata in India, Lima in Peru, Palembang in Indonesia and Johor Bahru in Malaysia (Colenbrander, Gouldson, Sudmant, & Papargyropoulou, Citation2015a, Citation2015b; Gouldson, Colenbrander, et al., Citationin press). These four cities were selected based on research funding opportunities and on local interest in the methodology and outputs. While by no means representative of developing world cities, the four case studies do represent both upper middle-income nations (Peru and Malaysia), and lower middle-income nations (Indonesia and India), and both tier 1 megacities (Lima and Kolkata) and tier 2 cities (Johor Bahru and Palembang).

4. Methods, data sources and assumptions

The methodology for each city study comprised three key stages:

An evaluation of recent trends (from 2000) in energy use, energy bills and carbon emissions, and an assessment of the impacts of these trends continuing for the next decade (to 2025);

An analysis of the potential costs, benefits and emissions savings from a large number of low-carbon measures that could be applied in different sectors of the city and in the regional electricity grid; and

An aggregation of the results to develop the economic case for investment in these options at scale in different sectors of the city over the coming decade.

Each study focused on the region under the influence of a specified municipal authority or authorities, so that the study area was defined by metropolitan boundaries. This meant that any low-carbon measures associated with longer distance travel and trade fell outside the scope of the research. Temporally, each study focused on energy use and trends in the period from 2000 to 2014, including both fuels directly consumed (Scope 1 emissions) and electricity produced outside municipal boundaries but consumed within the city (Scope 2 emissions), taking into account the carbon intensity of grid electricity and network and grid losses. Due to lack of reliable data, the studies did not include emissions from industrial processes, embedded emissions or energy from goods and services consumed in the city but produced elsewhere.

Trends in energy use in each city between 2000 and 2014 were calculated drawing on primary data from government agencies, industry sources and academic literature. These baselines were used to determine historical emissions and energy expenditure. Business-as-usual baselines through to 2025 were developed for each study based on the extrapolation of trends between 2000 and 2014, taking into consideration economic growth, population growth, changes in energy use and energy demand, major planned projects within the city, changing consumer behaviour and changing levels of efficiency. Projections were made independently for each sector in order to provide a detailed picture of the composition and levels of current and future energy use and emissions. Apart from planned investments, it was assumed that emissions patterns through to 2025 would reflect the patterns developed in each city over the period 2000–2014. The data inputs and resulting baselines were reviewed and refined by stakeholder workshops in each city.

In analysing the economic case for low-carbon investments, each study focused narrowly on the direct private costs and benefits of a wide array of low carbon measures. While this approach does not consider indirect social and environmental costs, the narrow analysis reflects the reality that a strong, direct economic case needs to be demonstrated before public investors will consider the wider impact of any potential investments. The net present value (NPV), scope for deployment and emission reduction potential of each measure were calculated drawing on data in academic and grey literature, and through consultations with stakeholder groups. The NPV reflects the capital costs, operating costs and fuel savings of each measure over its lifetime. The mitigation potential of each measure (at realistic levels of deployment) was based on calculations of the renewable energy generated, energy use avoided or waste emissions prevented in comparison with business-as-usual levels through the period to 2025.

Measures were considered to be economically attractive on commercial terms if they generate a positive NPV over their lifetime with a real discount rate of 5%. While in reality the expected return will vary based on the characteristics of the investor, the investment and the context, these parameters effectively exclude less economically feasible options. For reference, the IEA (Citation2015) adopts a high discount rate of 10% and low discount rate of 3%.

The measures considered in this analysis include only those available at the time of research and the costs of these measures are held constant. This approach probably overestimates the future costs of measures that will benefit from technological learning that would reduce the costs and improve the effectiveness of the measures over time (Köhler, Grubb, Popp, & Edenhofer, Citation2006). The importance of path dependencies and innovation, which are expected to significantly improve the economic case for mitigation analysis over time, are highlighted in the discussion.

Full details of the methodology used in these studies, including data sources and lists of participants in stakeholder panels, are detailed, Gouldson, Colenbrander, et al. (in press) and Colenbrander et al. (Citationin press-a, Citationin press-b).

4.1. The use of city-scale MAC curves

Marginal abatement cost (MAC) curves present information on the cost and carbon effectiveness of mitigation measures in a simple graphical form. MAC curves have been widely used to support decision-making in the fields of energy, water and waste management (see, for example, ESMAP, Citation2012; Kesicki & Ekins, Citation2012). However, their relative simplicity can create issues and care is required to ensure, for example, that transaction and policy-implementation costs are properly accounted for in MAC curves, that the effect of interactions between measures is analysed, that unintended consequences from the timing of measures are assessed and that cost uncertainties are properly modelled (Kesicki & Ekins, Citation2012; Vogt-Schilb & Hallegatte, Citation2014; Kesicki & Strachan, Citation2011).

In this analysis, extensive efforts have been undertaken to address these concerns. To ensure that transaction and policy-implementation costs were fully included, extensive consultation with industry, multiple levels of government and local experts was undertaken to examine the key assumptions underpinning the analysis. Although concerns about their use remain, we argue that MAC curves continue to have value in providing a relatively accessible illustration of the landscape of opportunities for investment in climate mitigation. We therefore present some of our results in the form of MAC curves while fully recognizing their limitations.

5. Results

5.1. Economically attractive abatement opportunities by city

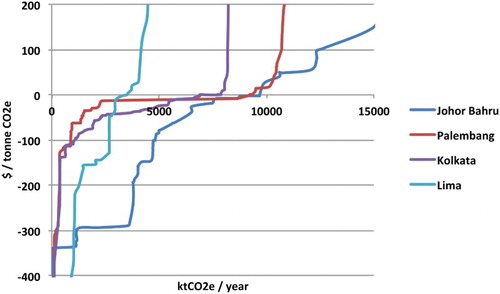

The NPV of the range of economically attractive mitigation options available in each city is presented in . This equates to the area under the x-axis for each MAC curve in . These results include only mitigation options directly within the city and therefore the electricity sector is not included here, as the grids generally serve a wider region ().

FIGURE 1 Marginal abatement cost curve for each city (including the residential, commercial, industry, transport and waste sectors)

TABLE 1 Key city statistics in 2014

TABLE 2 An overview of the economically attractive mitigation potential by city

Comparing the results across cities, two key findings are evident. First, significant cost-effective abatement opportunities are available in each city, with the total NPV ranging from US$ 521 million in Kolkata to US$ 1.9 billion in Johor Bahru (the composition of these investment is explored in the discussion). These investments would achieve potential carbon savings ranging from 3.2 MtCO2e in Lima to 9.4 MtCO2e in Johor Bahru by 2025.

Second, there is significant variation among cities with respect to the scale of opportunities. In terms of the total value of economically attractive low-carbon investments available per capita, Kolkata shows significantly less potential than Lima or Palembang, and dramatically less potential than Johor Bahru. This may reflect different levels of lock-in as in Kolkata many projects were made prohibitively expensive by the need to replace or remove existing infrastructure. Alternatively, the large mitigation potential in the fast-growing cities of Johor Bahru and Palembang suggests that it may be cheaper for cities to climate-proof new projects than to retrofit or replace existing infrastructure.

5.2. Economically attractive abatement opportunities by sector

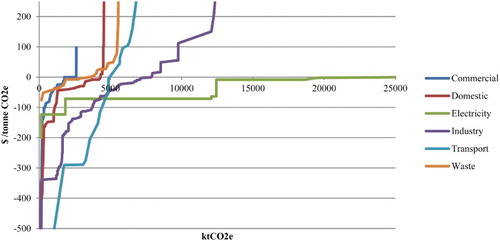

In the following table, economically attractive low-carbon investment opportunities are presented by sector for the four cities ().

TABLE 3 Value of cost-effective investment by sector

The commercial and waste sectors seems to offer relatively limited opportunities for economically attractive mitigation, suggesting that opportunities may already have been realized, or that, in relative terms, limited opportunities exist. The scope for economically attractive mitigation investments in the domestic, electricity, industry and transport sectors is more compelling for climate policy makers and large-scale investors, with potential cost-effective abatement valued between US$ 863 million and US$ 2.1 billion.

Investments in the electricity sector offer the largest potential for emissions savings (indicated by the intercept with the x-axis), but the transport sector offers the largest economic returns (indicated by the area under the x-axis) (). This suggests either that the most cost-effective opportunities in the electricity sector have been exploited, or that low-carbon investments in this sector are not particularly economically attractive. Each of the domestic, industry and commercial sectors account for 15% or more of the total value of cost-effective abatement and combined with the transport sector these sectors account for 75% of the total value of cost-effective mitigation opportunities in the cities analysed.

FIGURE 2 Marginal abatement cost curves by sector

6. Discussion

6.1. The characteristics of the investment opportunity

These results reveal that a wide range of low-carbon measures are economically attractive in all four of the cities studied, and across a variety of sectors. Exploiting these opportunities would mobilize an additional US$ 19.4 billion in climate finance, and avoid an estimated 23.9 MtCO2e being produced, between 2015 and 2025.

Two specific findings are worth highlighting. First, relative to the size of the local economy, climate mitigation has the greatest economic potential in Palembang and Johor Bahru. While recognizing our small sample size, this result tentatively suggests that mid-sized industrial cities with rapidly increasing populations, energy demand and emissions typically have substantial potential for cost-effective mitigation. These cities offer uniquely large opportunities to realize the economic and carbon savings from mainstreaming climate considerations. For example, green building standards, high-efficiency air conditioners, Euro IV vehicle standards and best practices in the cement industry generate large economic returns as well as carbon savingsFootnote1.

By comparison, megacities such as Lima and Kolkata have established, energy-inefficient infrastructure and (particularly for Lima) the path dependencies associated with urban sprawl and high dependence on motor vehicles. Although economic opportunities exist, these factors may reduce the economic case for climate change mitigation because retrofitting or replacing high-carbon infrastructure is typically more costly and less effective than integrating climate considerations into the design and construction phases (see Ürge-Vorsatz et al., Citation2007).

If opportunities for cost-effective mitigation are greatest in cities similar to Johor Bahru and Palembang, this suggests that there are huge opportunities to redirect investments towards lower-carbon options over the coming decade. Projections show that future emissions growth will be concentrated in Asia (IEA, Citation2014) and that most urbanization will occur in second-tier cities over coming decades (Phdungsilp, Citation2009), that is, in cities that are more similar to Johor Bahru and Palembang than Kolkata or Lima. The removal of energy subsidies in Indonesia and Malaysia, and the rapid development of carbon trading markets in China, will further enhance the economic case for urban climate action, and thus the scope to mobilize new investment in mitigation.

Second, these results suggest that, at least in the case-study cities, the largest opportunities to unlock new climate finance are in the domestic, industrial and transport sectors. This is in striking contrast to current trends in low-carbon investment. In 2012, for example, 76% of climate finance was invested in renewable energy (Buchner et al., Citation2013), a sector where only 19% of the cost-effective abatement opportunity is found in the city-level analysis. At the same time, 22% of 2012 climate finance went to ‘energy efficiency’ (10%) and ‘other mitigation measures’ (12%); these are areas where 79% of the value of cost-effective abatement opportunities was found by the city-level economic assessments. This disconnection partially reflects the relative difficulty of tracking low-carbon investments in the domestic, commercial, industrial and transport sectors, where investments often have modest capital requirements and are privately made (Buchner et al., Citation2014). It also demonstrates the importance of small and disaggregated investments, and the need for further ground-level research, business models and programs that aggregate and coordinate small investments, and a broadened concept of climate finance that includes measures that are climate-relevant but not solely climate-related (Clapp et al., Citation2012), such as investments that promote modal shifts in transport (World Bank, Citation2015).

However, the discrepancy between the opportunities for and the allocation of climate finance also highlights the need to mainstream climate considerations into policy in developing country cities. This approach could ensure that finance from households, businesses and government agencies is channelled into cost-effective lower-carbon options, such as solar water heating, more efficient air conditioners and hybrid vehicles. While these measures may entail higher upfront costs, they will more than pay for themselves over their lifetime while reducing emissions relative to business-as-usual trends. These small-scale investments collectively generate massive economic and carbon savings, but due to their size and the absence of recoverable collateral, are not generally the sorts of investments favoured by commercial banks, insurance companies or sovereign wealth funds, for example. This underscores the importance of governance arrangements and policy frameworks that can drive the low-carbon transition.

Future research will be needed to provide a more complete picture of these important aspects of climate finance policy and practice. Analysis included only four developing world cities, and looked only at the time period to 2025, two notable limitations. This analysis should therefore be seen as a starting point and call for further research assessing climate finance opportunities from the ground level.

6.2. Implications for climate policy

Mobilizing large-scale low-carbon investment from diverse actors will require the development of enabling governance structures at the local level (UNEPFI, Citation2014). Decision-makers must recognize that policy interventions need to be carefully tailored to the opportunities available in a specific context. Different categories of climate change projects present different issues and challenges, and accordingly demand different models for support. In broad terms, attention needs to be paid to the financial characteristics of the investment opportunity at hand, existing policy frameworks (including information, regulatory and economic instruments) and the institutional structures available for implementation and governance, among other issues (UNEPFI, Citation2014).

Realizing the opportunities outlined above will require a whole series of discrete investments. Some are large investments that can be financed as distinct entities using, for example, special purpose vehicles that attract and disburse public and private finance in the form of debt or equity. Project, municipal and green bonds, for instance, could mobilize large amounts of private investment for climate-friendly public transport infrastructure. Others may be financed by organizations themselves, either through their own balance sheet or through bank lending. This would probably be the dominant source of financing for the large energy-efficiency opportunities in the industrial sector. Other low-carbon measures may need to be financed, in whole or in part, by private individuals. These individuals would then bear the marginal cost of more energy-efficient vehicles and appliances, for example, but will also recoup the associated savings over the life time of the investment.

With respect to financing sources, the reality is that governments will need to rely on the private sector to provide much of the necessary capital (Aghion, Hepburn, Teytelboym, & Zenghelis, Citation2014), using public finance to catalyse, incentivize and de-risk the flow of private finance. The private sector not only has more significant resources available for investment, particularly in a time of shrinking public budgets, but is also often widely perceived as bringing additional efficiency, managerial capabilities and operational power to projects (Whitley & Ellis, Citation2012). Policymakers will therefore need to consider how to ensure appropriate risk-adjusted returns to mobilize additional private finance, and how to redirect existing financing streams into less carbon-intensive options. Relevant policy instruments could include carbon pricing schemes, mandatory energy efficiency standards for buildings or vehicles, renewable energy quotas, capacity-building programmes, initiatives to raise awareness and green public procurement policies. By mainstreaming low-carbon goals into private investment in this way, public decision-makers can break business-as-usual path dependencies and stimulate low-carbon innovation in technologies, policies and practices (Aghion et al., Citation2014).

Institutional investors also suggest that the public sector has a role to play in packaging investments at an appropriate scale and duration, and in providing long-term policy certainty and alignment with wider policy goals (IIGCC, Citation2014; Sullivan, Citation2011). Indeed, aggregating a large number of small investments can cause relatively high transaction costs. Energy service companies and other intermediaries (ESCOs) offer one way of doing this. However, while theoretically attractive, ESCOs have often struggled to get to scale and to deliver on their objectives. There are a number of common issues (see UNEPFI, Citation2014), such as the difficulty of attributing cost savings to a particular energy efficiency-related investment or for ESCOs to obtain third-party financing from banks and other lenders. There is accordingly a need for institutional innovations if governments hope to direct investment from pension funds, sovereign wealth funds and the like to the kinds of opportunities outlined above.

It is particularly important that municipal authorities consider overall financing requirements at the early stages of urban planning to ensure that the most financially attractive projects are not cherry-picked, leaving a series of other less economically attractive projects that can only be financed by government (Sullivan, Citation2011). By taking an integrated approach, governments can also look at the cross-subsidization of investment needs. They may be able to reduce the total amount of upfront capital required and to generate long-term revenue streams that can be used to fund less financially attractive options, for example, using revolving funds to invest in energy-efficient buildings (see Gouldson, Kerr, et al., Citation2015).

There is an urgent need for future research to provide a more complete picture of the scope for investment in economically attractive low-carbon measures at the ground level. Although this analysis included only four developing world cities, and considered only the time period to 2025, it identified substantial opportunities that are not being exploited. Equally critically, the findings must be communicated to diverse audiences including a range of levels and sectors of government, private businesses, civil society organizations and households. This kind of work can thus help to catalyse substantial new flows of low-carbon investment.

7. Conclusions and policy recommendations

The results from four city-level economic assessments suggest that significant opportunities for economically attractive climate finance exist across cities in the developing world. Fast-growing cities appear to present the largest scope for economically attractive climate mitigation investments. However, many of the most significant opportunities in terms of economic and carbon savings are relatively small-scale investment prospects in the commercial, domestic, industrial and transport sectors. Delivering these measures will often require politically challenging policy reforms or innovative financing mechanisms, tailored to the project, city and sector. Local development priorities, the financial characteristics of specific investment opportunities and the existence of institutions capable of coordinating and administering finance at the local level are just some of the key considerations. Public decision-makers can direct financial flows from households, businesses and institutional investors towards cost-effective low-carbon options, thereby mobilizing substantial new investment in mitigation. If replicated on a global scale, this could largely bridge the climate finance gap. There is therefore an urgent need for local-level analysis of economic opportunities for climate action in order to inform the design of specific policy interventions, as well as to complement and contextualize global assessments of the scope and case for climate action.

Supplemental data

Supplemental data for this article can be accessed here [10.1080/14693062.2015.1104498].

Acknowledgements

We would like to extend our gratitude to each of these organizations and to our research partners in each city.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1. For specific examples of investment opportunities in these cities, please see Colenbrander et al. (in press-a, in press-b) and Papargyropoulou, Gouldson, Colenbrander, and Sudmant (in press).

Related Research Data

References

- Aghion, P., Hepburn, C., Teytelboym, A., & Zenghelis, D. (2014). Path dependence, innovation and the economics of climate change. San Francisco: CPI .

- Ampri, I., Falconer, A., Wahyudi, N., Rosenberg, A., Bara, M., Ampera, A. T., … Wilkinson, J. (2014). The landscape of public climate finance in Indonesia – executive summary. Jakarta: Indonesian Ministry of Finance ; Climate Policy Initiative. Retrieved from CPI website:http://climatepolicyinitiative.org/publication/landscape-of-public-climate-finance-in-indonesia-3

- Bowen, A., Campiglio, E., & Tavoni, M. (2014). A macroeconomic perspective on climate change mitigation: Meeting the financing challenge. Climate Change Economics, 5, 1440005. doi: 10.1142/S2010007814400053

- Buchner, B., Angela, F., Hervé-Mignucci, M., & Trabacchi, C. (2012). The landscape of climate finance. San Francisco: Climate Policy Initiative.

- Buchner, B., Hervé-Mignucci, M., Trabacchi, C., Wilkinson, J., Stadelmann, M., Boyd, R., … Micale, V. (2013). The landscape of climate finance. San Francisco: Climate Policy Initiative

- Buchner, S., Stadelmann, M., Wilkinson, J., Mazza, F., Rosenberg, A., & Abramskiehn, D. (2014). The landscape of climate finance. San Francisco: Climate Policy Initiative.

- Clapp, C. J., Ellis, J. B., & Corfee-Morlot, J. (2012). Tracking climate finance: What and how? Paris: Organization for Economic Cooperation and Development/International Energy Agency. Retrieved from OECD website: http://www.oecd.org/env/climatechange/50293494.pdf

- Clark, L., Jiang, K., Akimoto, K., Babiker, M., Blanford, G., Fisher, K., … Krey, V. (2014). Assessing transformation pathways. In O. Edenhofer, et al. (Eds.), Climate change 2014: Mitigation of climate change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change (pp. 413–510). Cambridge: Cambridge University Press.

- Colenbrander, S., Gouldson, A., Sudmant, A., & Papargyropoulou, E. (in press-a). Exploring the economic case for early investment in climate change mitigation in middle-income countries: A case study of Johor Bahru, Malaysia. Environmental Science and Policy. Climate and Development

- Colenbrander, S., Gouldson, A., Sudmant, A., & Papargyropoulou, E. (in press-b). The economic case for low carbon development in rapidly growing developing world cities: A case study of Palembang, Indonesia. Energy Policy. doi:10.1016/j.enpol.2015.01.020

- Doniger, D., Herzog, A., & Lashof, D. (2006). An ambitious, centrist approach to global warming legislation. Science 314, 764–765. doi:0.1126/science.1131558

- ESMAP. (2012). Planning for a low carbon future: Lessons learned from seven country studies (Knowledge series 011/12). Washington, DC: Energy Sector Management Assistance Program; The World Bank.

- Falconer, A., & Stadelmann, M. (2014). What is climate finance? Definition to improve tracking and scale up climate finance. Venice: CPI. Retrieved from the CPI website: http://climatepolicyinitiative.org/wp-content/uploads/2014/07/Brief-on-Climate-Finance-Definitions.pdf

- GEA. (2012). Global energy assessment: toward a sustainable future – summary. Vienna: International Institute for Applied Systems Analysis (IIASA). Retrieved from the IIASA website: http://www.iiasa.ac.at/web/home/research/Flagship-Projects/Global-Energy-Assessment/GEA-Summary-web.pdf

- Gouldson, A., Colenbrander, S., Sudmant, A., McAnulla, F., Kerr, N., Sakai, P., … Kuylenstierna, J. (in press). Exploring the economic case for low carbon cities. Global Environmental Change. doi:10.1016/j.gloenvcha.2015.07.009

- Gouldson, A., Kerr, N., McAnulla, F., Hall, S., Colenbrander, S., & Sudmant, A. (2014). The economics of low carbon cities: Kolkata, India. London: The Centre for Low Carbon Futures. Retrieved from http://www.climatesmartcities.org/sites/default/files/3710%20Kolkata%20Full%20Report%20Oct%202014%20v12.pdf

- Gouldson, A., Kerr, N., Millward-Hopkins, J., Freeman, M., Topi, C., & Sullivan, R. (2015). Innovative financing models for low carbon transitions: Exploring the case for revolving funds for domestic energy efficiency programmes. Energy Policy, 86, 739–748. doi:10.1016/j.enpol.2015.08.012.

- Gupta, S., Harnisch, J., Barua, D. C., Chingambo, L., Frankel, P., Garrido Vázquez, R. J., … Massetti, E. (2014). Cross-cutting investment and finance issues. In O. Edenhofer, R. Pichs-Madruga, Y. Sokona, E. Farahani, S. Kadner, K. Seyboth, … J. C. Minx (Eds.), Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change (pp. 1207–1246). Cambridge: Cambridge University Press.

- Held, D., Charles, R., & Eva-Maria, N. (2014). Climate governance in the developing world. Cambridge: John Wiley & Sons.

- IIGCC (2014). 2014 Global investor statement on climate change. Retrieved from IIGCC website: http://www.iigcc.org/publications/publication/2014-global-investor-statement-on-climate-change

- International Energy Agency. (2013). World energy outlook. Paris: IEA. Retrieved from http://www.worldenergyoutlook.org/publications/weo-2013/

- International Energy Agency. (2014). World energy outlook 2013 – Executive summary. Paris: IEA. Retrieved from http://www.iea.org/Textbase/npsum/WEO2013SUM.pdf

- International Energy Agency. (2015). Energy technology perspectives 2015. Paris: International Energy Agency.

- Jakob, M., Steckel, J. C., Klasen, S., Lay, J., Grunewald, N., Martínez-Zarzoso, I., … Edenhofer, O. (2014). Feasible mitigation actions in developing countries. Nature Climate Change, 4, 961–968. doi:10.1038/nclimate2370

- Jürgens, I., Amecke, H., Boyd, R., Buchner, B., Novikova, A., Rosenberg, A., … Vasa, A. (2012). The landscape of climate finance in Germany. Berlin: Climate Policy Initiative. Retrieved from CPI website: http://climatepolicyinitiative.org/wpcontent/uploads/2012/11/Landscape-of-Climate-Finance-in-Germany-Full-Report.pdf

- Kato, T., Jane, E., Pieter, P., & Randy, C. (2014). Scaling up and replicating effective climate finance interventions. Paris: OECD.

- Kesicki, F., & Ekins, P. (2012). Marginal abatement cost curves: A call for caution. Climate Policy, 12, 219–236. doi:10.1080/14693062.2011.582347

- Kesicki, F., & Strachan, N. (2011). Marginal abatement cost (MAC) curves: Confronting theory and practice. Environmental Science & Policy, 14, 1195–1204. doi: 10.1016/j.envsci.2011.08.004

- Kirkman, A., Seres, S., & Haites, E. (2013). Renewable energy: Comparison of CDM and Annex I projects. Energy Policy, 63, 995–1001. doi: 10.1016/j.enpol.2013.08.071

- Köhler, J., Grubb, M., Popp, D., & Edenhofer, O. (2006). The transition to endogenous technical change in climate-economy models: A technical overview to the innovation modeling comparison project. The Energy Journal, 1, 17–55. doi:10.5547/ISSN0195-6574-EJ-VolSI2006-NoSI1-2

- McCollum, D., Nagai, Y., Riahi, K., Marangoni, G., Calvin, K., Pietzcker, R., … van der Zwaan, B. (2013). Energy investments under climate policy: A comparison of global models. Climate Change Economics, 4, 1340010. doi:10.1142/S2010007813400101

- McKinsey and Company. (2010). Impact of the financial crisis on carbon economics - GHG cost curve V2.1. New York: McKinsey and Company. Retrieved from http://www.mckinsey.com/~/media/McKinsey/dotcom/client_service/Sustainability/cost%20curve%20PDFs/ImpactFinancialCrisisCarbonEconomicsGHGcostcurveV21.ashx

- Olbrisch, S., Haites, E., Savage, M., Dadhich, P., & Shrivastava, M. K. (2011). Estimates of incremental investment for and cost of mitigation measures in developing countries. Climate Policy, 11, 970–986. doi:10.1080/14693062.2011.582281

- Papargyropoulou, E., Gouldson, A., Colenbrander, S., & Sudmant, A. (in press). The economic case for low carbon waste management in rapidly growing cities in the developing world: The case of Palembang, Indonesia. Journal of Environmental Management. doi:10.1080/14693062.2014.953906

- Pauw, W. P. (2014). Not a panacea: Private-sector engagement in adaptation and adaptation finance in developing countries. Climate Policy, 15 (5), 1–21.

- Phdungsilp, A. (2009). Comparative study of energy and carbon emissions, Fifth Urban Research Symposium 2009. Retrieved July 5, 2014, from http://siteresources.worldbank.org/INTURBANDEVELOPMENT/Resources/336387-1256566800920/6505269-1268260567624/Phdungsilp.pdf

- PWC. (2014). Capital project and infrastructure spending Outlook to 2025. London. Retrieved from PWC website: https://www.pwc.se/sv_SE/se/offentlig-sektor/assets/capital-project-and-infrastructure-spending-outlook-to-2025.pdf

- Somanathan, E., Sterner, T., Sugiyama, T., Chimanikire, D., Dubash, N. K., Essandoh-Yeddu, J., … Zylicz, T. (2014). National and sub-national policies and institutions. In O. Edenhofer et al., (Eds.), Climate change 2014: Mitigation of Climate change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change (pp. 1141–1206). Cambridge and New York, NY,: Cambridge University Press.

- Stern, N. (2006). Stern review: The economics of climate change (Vol. 30). London: HM treasury.

- Stern, N. (2015). Why are we waiting? The logic, urgency, and promise of tackling climate change. Cambridge, MA and London: MIT Press.

- Sullivan, R. (2011). Investment-grade climate change policy: Financing the transition to the low-carbon economy. London: Institutional Investors Group on Climate Change.

- Thurston, G. D. (2013). Mitigation policy: Health co-benefits. Nature Climate Change, 3, 863–864. doi:10.1038/nclimate2013

- Tompkins, E. L., Mensah, A., King, L., Long, T. K., Lawson, E. T., Hutton, C. W., … Bood, N. (2013). An investigation of the evidence of benefits from climate compatible development. Working Paper. Sustainability Research Institute, Leeds University.

- UNEPFI. (2014). Demystifying private climate finance. Geneva: UNEPFI.

- Ürge-Vorsatz, D., Danny Harvey, L. D., Mirasgedis, S., & Levine, M. D. (2007). Mitigating CO2 emissions from energy use in the world's buildings. Building Research & Information, 35(4), 379–398. doi: 10.1080/09613210701325883

- Vogt-Schilb, A., & Hallegatte, S. (2014). Marginal abatement cost curves and the optimal timing of mitigation measures. Energy Policy, 66, 645–653. doi: 10.1016/j.enpol.2013.11.045

- Whitley, S., & Ellis, K. (2012). Designing public sector interventions to mobilise private participation in low carbon development: 20 questions toolkit (Working paper 346). London: Overseas Development Institute. Retrieved January 23, 2015, from http://www.odi.org/sites/odi.org.uk/files/odi-assets/publications-opinion-files/7660.pdf

- WHO. (2014). Urban population growth. Retrieved May 15, 2015, from http://apps.who.int/gho/data/node.main.URBPOP?lang=en

- World Bank. (2015). Common principles for climate mitigation finance tracking. Washington, DC: World Bank. Retrieved from http://www.worldbank.org/content/dam/Worldbank/document/Climate/common-principles-for-climate-mitigation-finance-tracking.pdf

- World Economic Forum (WEF). (2013). The green investment report: the ways and means to unlock private finance for green growth. Geneva: World Economic Forum. Retrieved from WEF website: http://www3.weforum.org/docs/WEF_GreenInvestment_Report_2013.pdf