?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Research on air travellers’ willingness to pay (WTP) for climate change mitigation has focussed on voluntary emissions offsetting so far. This approach overlooks policy relevant knowledge as it does not consider that people may value public goods higher if they are certain that others also contribute. To account for potential differences, this study investigates Swedish adults’ WTP for a mandatory air ticket surcharge both for short- and long-distance flights. Additionally, policy relevant factors influencing WTP for air travel emissions reductions were investigated. The results suggest that mean WTP is higher in the low-cost setting associated with short-distance flights (495 SEK/ tCO2; 50 EUR/ tCO2) than for long-distance flights (295 SEK/ tCO2; 30 EUR/t CO2). The respondents were more likely to be willing to pay the air ticket tax if they were not frequent flyers, if they were women, had a left political view, if they had a sense of responsibility for their emissions and if they preferred earmarking revenues from the tax for climate change mitigation and sustainable transport projects.

Key policy insights

A mandatory air ticket tax is a viable policy option that might receive majority support among the population.

While a carbon-based air ticket tax promises to be an effective tool to generate revenues, its potential steering effect appears to be lower for low cost contexts (short-distance flights) than for high cost contexts (long-distance flights).

Policy consistency regarding the tax base and its revenue use may increase public acceptability of (higher) air ticket taxes. Earmarking revenues is clearly preferred to tax recycling or general budget use.

Insights about the personal drivers behind WTP for emissions reductions from air travel can help to inform targeting and segmentation of policy interventions.

1. Introduction

In the current policy debate, carbon pricing mechanisms are a central strategy to steer consumption and investments towards low-carbon technologies and more sustainable practices (Baranzini et al., Citation2017; World Bank, Ecofys, & Vivid Economics, Citation2017). One sector where this approach is not very far developed, neither in terms of emissions covered nor in terms of the carbon price level, is aviation (Penner, Citation1999; Sims et al., Citation2014). To date, only a few countries (e.g. UK and Norway) have introduced direct taxes or charges on air travel, and the aviation sector even benefits from significant subsidies (Gössling, Fichert, & Forsyth, Citation2017). In the EU, intra-continental flights are covered by the EU emissions trading system (ETS). However, flights into and out of the EU are not included in the ETS, over 80% of ETS emissions allowances (EUA) are allocated for free to the aviation sector, and carbon prices under the EU ETS have been low, which means that the inclusion of air travel in the ETS has not yet resulted in a significant carbon price signal for air travel (Cui, Li, & Wei, Citation2017; Meleo, Nava, & Pozzi, Citation2016). Internationally, the ‘Carbon Offsetting and Reduction Scheme for International Aviation’ (CORSIA) that was initiated by the International Civil Aviation Organization (ICAO) aims for carbon neutral growth of the sector after 2020. However, the scheme will only cover additional emissions above the 2020 level, it will be a voluntary scheme to start with, and it will not apply to domestic flights (ICAO, Citation2016).

Driven by the lack of stringent pricing policies, a common way to address greenhouse gas emissions from air travel is to encourage voluntary carbon offsetting (Daley & Preston, Citation2009). However, considering the need to cut aviation emissions by half in order to stay within 2°C of warming by mid-century above pre-industrial levels, voluntary offsetting is an insufficient approach (Becken & Mackey, Citation2017). Emissions from aviation are projected to grow by 140% between 2013 and 2050 (Kuramochi et al., Citation2018), when the contribution of aviation to global CO2 emissions may reach 22% (Cames, Graichen, Siemons, & Cook, Citation2015). The current share of emission offsets in total emissions from air travel is negligible (Zelljadt, Citation2016), and the additionality and mitigation potential of offsetting have been questioned (Broderick, Citation2008). Another policy instrument is to tax air travel, thereby providing an incentive to travel less (Daley & Preston, Citation2009; Sims et al., Citation2014). Today, the most common way to create this incentive is air ticket taxation (Krenek & Schratzenstaller, Citation2016) since charging VAT on international flights or taxing kerosene would first require (re-) negotiations of international agreements.

A complication in the design of air ticket taxation is that there is little information about people’s willingness to pay (WTP) for such mandatory taxes. In contrast, various studies have investigated air travellers’ WTP for voluntary offsets (Brouwer, Brander, & Van Beukering, Citation2008; Choi & Ritchie, Citation2014; Jou & Chen, Citation2015; Lu & Shon, Citation2012; MacKerron, Egerton, Gaskell, Parpia, & Mourato, Citation2009). However, this information is not particularly useful for the design of air ticket taxes as there are strong indications that WTP is systematically lower for voluntary offsets than for coercive instruments (Segerstedt & Grote, Citation2016; Wiser, Citation2007).

By addressing this shortcoming, this study is the first that investigates WTP for mitigating air travel emissions based on a mandatory payment vehicle, a climate surcharge on air tickets. In doing so, the study aims to improve the valuation of mitigating air travel emissions and to increase its policy relevance. The study further adds to the existing body of work on payment vehicles by contrasting WTP in low cost contexts (short-distance flights), to that of high cost contexts (long-distance flights). Moreover, it investigates policy relevant aspects driving people’s WTP besides socio-demographic factors, including political views, flight frequency, sense of responsibility for emissions, as well as preference for earmarking revenues from carbon pricing policies. Knowing the factors that drive WTP for mitigating air travel emissions in a specific context can support the design of effective policy interventions and increase their public approval.

The specific context of this study is Sweden and its policies to address the climate impact of air travel. At the time of the study (early 2017), the introduction of a climate tax on air tickets was publicly debated in Sweden. The ticket tax was eventually introduced in April 2018. In the research informing the preceding debate and the legislative process (Andersson & Falck, Citation2017), data about the WTP of Swedes for mitigating emissions from flying was limited to people’s general WTP for offsets (Gössling, Haglund, Kallgren, Revahl, & Hultman, Citation2009). Moreover, Swedes’ WTP for climate mitigation in general had been estimated (Carlsson et al., Citation2012), but there was no evidence regarding the specific WTP for air travel emissions. Thus, with respect to Swede’s WTP for mitigating air travel emissions, the existing literature was and still is fragmented and does not provide conclusive answers to at least three questions: What is (approximately) Swedes’ WTP for the mitigation of their air travel emissions in a mandatory scheme? Is there a difference in WTP elicited between short distance flights and long distance flights? And what are the factors influencing WTP? In order to respond to these questions, empirical data was collected in a contingent valuation survey, which is presented in the following section, together with the approach for data analysis. This is followed by Section 3 which presents and discusses the results of the survey and econometric estimations. Section 4 presents policy implications and concludes.

2. Data and methods

2.1. Contingent valuation (CV) survey

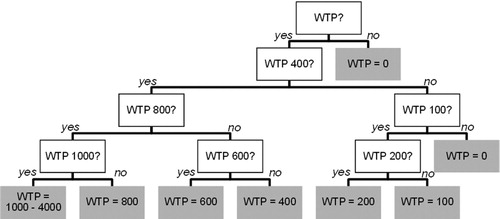

The data for this study is based on a contingent valuation survey (n = 500), which was implemented by computer-assisted web interviewing of a representative, random sample of Swedish adults in January 2017.Footnote1 All respondents went through the WTP elicitation process repeatedly in order to elicit WTP for emissions reductions with different payment vehicles (PVs), including a mandatory air ticket surcharge on short-distance flights and the same surcharge on long-distance flights.Footnote2 The order of all PVs in the survey was randomized in order to avoid bias induced by order or fatigue effects. To elicit WTP, the survey combined a simple dichotomous choice question about general WTP with an iterative bidding process for those respondents that were willing to pay in principle. Iterative bidding followed a pre-defined bidding structure (see ).

Figure 1. Pre-defined bidding structure. The numbers indicate bid values in SEK/tCO2. Grey boxes show the endpoints, i.e. the WTP values that were used for further analysis.

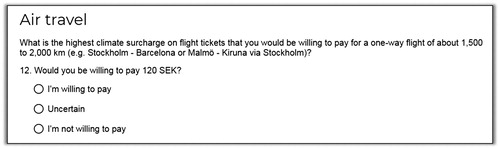

The level of bids was the same for all PVs and ranged from SEK 100–1,000Footnote3 per ton CO2, which reflects the results of previous CV studies (Brouwer et al., Citation2008; Löschel, Sturm, & Uehleke, Citation2017) and the price range of current carbon pricing schemes (World Bank, Ecofys, & Vivid Economics, Citation2016). Bid values per tCO2 were transformed to corresponding values per short-distance flight (30–300 SEK) and long-distance flight (120–1,200 SEK). This transformation assumed a carbon intensity of 171 gCO2/ pkm for the short-distance (ca. 1,750 km) example flights and 133 gCO2/ pkm for the long-distance (ca. 9,000 km) example flights. These carbon intensities are high compared to industry estimates (Andersen Resare, Citation2015), in order to partly account for greenhouse gas emissions other than CO2 that are emitted from flying (see Section C of the supplementary material for further elaboration on these carbon intensities). Because of the uncertainty connected to carbon intensity estimates, the sensitivity of WTP results to changes in the assumed carbon intensity was tested. In the WTP elicitation, no reference was made to the price of the air tickets (see text in ), since ticket prices are not fully proportionate to travel distance, and hence price-anchors would have potentially biased the results.

Figure 2. Example for WTP elicitation question. This is translated from the original survey which was conducted in Swedish.

The interpretation of WTP responses followed a conservative approach. Those who were not willing to pay in principle and those who rejected the lowest bid were considered to have a WTP of zero. For all others, the highest accepted bid was treated as their WTP. Respondents could also state that they are uncertain about a bid, which was treated as rejection in order to reduce potential hypothetical bias (Loomis, Citation2014). Respondents who indicated that their WTP was higher than the highest bid of 300 and 1,200 SEK for short- and long-distance flights respectively could freely state their maximum WTP up to a cap of four times the highest bid. This cap was chosen in order to avoid unrealistically high valuations and still make sure that most people’s values are covered, even for rather extreme results (e.g. mean WTP of 900 SEK/t and a standard deviation of >1,000 SEK/t).

Besides uncertainty recoding and capping the highest bid, further measures were taken to counteract hypothetical bias. These measures included consequentiality design (Loomis, Citation2014) of the survey (‘results of this survey are meant to inform policy reforms’), and a reminder about the opportunity cost of paying for CO2 emissions (‘don't agree to costly policies if you think you cannot afford it or if you feel that there are more important things for you to spend your money on’). Strategic bias, on the other hand, might entail that respondents systematically undervalue a good in order to avoid costly policies in the future (Venkatachalam, Citation2004). This potential bias was addressed by reminding respondents that they are asked about their personal WTP and not what they think is the right level for pricing air travel emissions in general (section D of the supplementary material contains more information about how different biases were addressed in the survey design).

Besides the elicitation of WTP, the survey also included questions about socio-demographic data, travel behaviour and policy preferences in the context of carbon pricing. The survey data is summarized in , which also includes the variable codes, means and standard deviations.

Table 1. Coding, mean and standard deviation (SD) of variables.

2.2. Econometric analysis

An econometric analysis was carried out to identify significant drivers of respondents’ general and specific WTP for a surcharge for their air travel emissions. General WTP refers to respondents’ dichotomous choice to support the surcharge or not (WTPsurcharge), while specific WTP refers to the amount respondents are willing to pay for the surcharge on a short- and long-distance flight (WTPairshort, WTPairlong). First, a simple logit regression approach was chosen to identify the significant predictors for WTPsurcharge. Second, interval regressions were carried out for WTPairshort and WTPairlong. Interval regression accounts for the fact that the data for WTPairshort and WTPairlong consists of intervals (between highest accepted and lowest rejected bid); and it is has been previously applied in a comparable context (Brouwer et al., Citation2008). Finally, an interval regression model was computed that combined WTP responses for short- and long-distance flights by using the lower of the two valuesFootnote4 as lower bound and the higher value as upper bound of respondents’ intervals (WTPaircombined). It is important to note that the WTP data were transformed to SEK/ tCO2 values in order to make the coefficients comparable across the three interval regressions.

The model specifications for these regressions were based on a literature review that was carried out to identify policy relevant factors affecting people’s views and preferences towards climate change mitigation. The review resulted in a list of variables including respondents’ air travel frequency (Brouwer et al., Citation2008), frequentfly; their political view (Hornsey, Harris, Bain, & Fielding, Citation2016), leftpolview; their sense of responsibility for their emissions (Brouwer et al., Citation2008), responsible; and their preference for earmarking revenues from carbon pricing (Kotchen, Turk, & Leiserowitz, Citation2017), earmark. For all of these variables, data was collected in the survey (see above).

In order to explore their potential explanatory power, partial correlation tests were carried out, controlling for a set of socio-demographic variables (age, female, education, hhsize, income). The tests showed highly significant partial correlations to WTPsurcharge, WTPairshort and WTPairlong for all four variables (frequentfly, leftpolview, responsible and earmark). Therefore, all four were included in the following conceptual model for regression analysis:(1)

(1) where y is WTPsurcharge, X1 to X5 are above mentioned socio-demographic characteristics, X6 is flight frequency (frequentfly), X7 is the political view (leftpolview), X8 is the sense of responsibility for one’s emissions (responsible) and X9 is the preference for earmarking of tax revenue (earmark); β1 to β9 are the corresponding coefficients, and ε is an error term. After estimating the full model (1) also a stepwise removal of variables that were below the 10% significance level (p < 0.1) was executed, both for the logit regression of WTPsurcharge and for the interval regressions of WTPairshort, WTPairlong and WTPaircombined.

3. Results and discussion

Below, first the results from WTP elicitation are presented and discussed, including differences between WTPairshort and WTPairlong, and the sensitivity of results to changes in carbon intensity of flying. Second, the econometric analysis is presented and results are discussed. Finally, contextual factors from the specific situation in Sweden are included in the discussion.

3.1. Willingness to pay for emissions from air travel

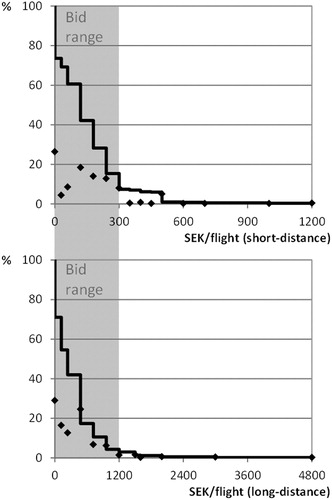

The survey shows that more than 70% of respondents had a positive WTP for their air travel emissions (see ). The distribution of positive WTP shows that the approval was highest at the first (and central) bid of the iterative bidding process (at 120/ 480 SEK per short-/ long-distance flight), indicating a potential anchoring effect. In contrast, the distribution of WTP responses above and below the central value sharply differs between short- and long-distance flights. While for short-distance flights only 13% of respondents indicated a positive WTP below the central bid, this share was 29% for long-distance flights. WTP above the central bid was, in turn, much more frequent for short-distance flights (42%) than for long-distance flights (17%).

Figure 3. WTP distribution for short- and long-distance flights. Diamonds indicate the respective shares of acceptance at given bid levels; solid lines indicate cumulative acceptance. The grey area marks the survey’s bid range. For both graphs X-axis values correspond to a range of 0–4 000 SEK/ tCO2.

This difference between short- and long-distance flights is also reflected in average WTP values. After transforming WTP values in order to receive comparable results in SEK/ tCO2, average WTP for long-distance flights turned out to be much lower than for short-distance flights (295 versus 495 SEK/ tCO2). It was shown in a two-sided t-test (t = 13.7, p < 0.001) and a Wilcoxon signed-rank test (z = 14.5; p < 0.001) that the difference between the two means of SEK 200 is statistically highly significant. This finding is in line with previous research which suggests that WTP is higher in a low-cost decision context (Blasch & Farsi, Citation2014; Diekmann & Preisendörfer, Citation2003). While bid levels per tCO2 were the same for both short- and long-distance flights, bids per flight were four times lower for short-distance flights. This influence of the absolute cost-context on WTP illustrates the importance of eliciting WTP for the same good in different cost-contexts, or making at least the cost-context explicit when reporting results.

Average WTPair_short and WTPair_long per tCO2 are at 495 and 295 SEK (ca. 50 and 30 EUR) still within the range found in previous studies, including 41 EUR for European air travellers (Brouwer et al., Citation2008), 14 EUR (21 AUD) for Australian air travellers (Choi & Ritchie, Citation2014), and 21 EUR (25 USD) in the Taiwanese context (Lu & Shon, Citation2012). The WTP values presented in are, however, conservative estimates, as respondents’ highest accepted bid was used as their maximum WTP. If, instead, the midpoints of the intervals between highest accepted and lowest rejected bid are used, WTPair_short and WTPair_long increase to 551 and 353 SEK respectively. One explanation for the comparably high WTP estimates found in this study is that it used a mandatory PV while previous studies were based on voluntary offsetting. This is in line with previous research in the context of climate change mitigation, which found that mandatory PVs are associated with higher acceptance (Segerstedt & Grote, Citation2016) and higher WTP (Wiser, Citation2007) than voluntary PVs.

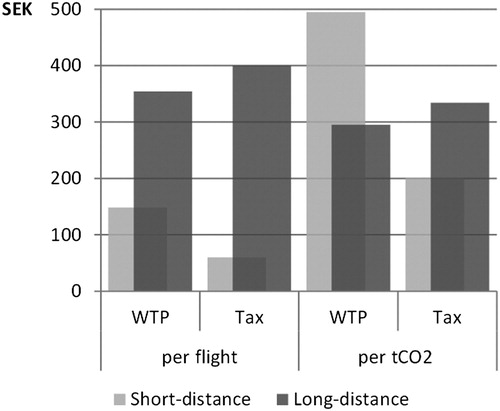

Figure 4. Juxtaposition of average WTP values and Swedish air ticket tax for short and long distance flights. The figures per ton CO2 were achieved by dividing WTP per flight and tax levels (SEK 60 short-distance and SEK 400 long-distance) by the CO2 emissions caused by the example-flights from the survey (0.3t short-distance and 1.2t long-distance).

Absolute WTP results of this study (and previous research) should be treated with due scepticism. This is not only due to the effect that framing of PVs may have, but also due to the very specific case settings of CV studies and their (often) limited sample sizes. Moreover, WTP levels for air travel emissions also depend on the assumed carbon intensity of air travel. While WTP in this study was elicited per flight (ticket), the transformation to WTP per tCO2 requires a conversion factor. This carbon intensity factor, measured in gCO2/pkm, depends among others on aircraft efficiency, capacity utilization, and assumptions about the global warming potential of air travel. The sensitivity analysis for average WTPair_short and WTPair_long presented in shows that changes in assumed carbon intensity strongly impact average WTP levels. However, the difference between WTPair_short and WTPair_long found in this study remains significant for all plausible combinations of carbon intensity.Footnote5 The finding that WTP is higher in a low-cost setting is, hence, robust to changes in (assumed) carbon intensity.

Figure 5. Sensitivity of mean WTP to changes in carbon intensity. Diamonds indicate the values used in this study. For comparison, the Swedish carrier SAS communicates average carbon intensity of 100 gCO2/pkm (Andersen Resare, Citation2015), while CO2 equivalent emissions are estimated to be higher by a factor of up to 2 (Lee et al., Citation2010).

3.2. Personal factors influencing WTP

The regression analysis revealed that the variables frequentfly, leftpolview, responsible and earmark are all significant predictors of WTP, while from the socio-demographic variables only female is a significant predictor of WTPsurcharge and income is a significant predictor of WTPairshort, WTPairlong and WTPaircombined (see ). The latter effect of income on WTP was found in many previous CV studies, also in the context of flying and emissions offsetting (Brouwer et al., Citation2008; Jou & Chen, Citation2015; Löschel et al., Citation2017). The variable female significantly increased the likelihood of being willing to pay (WTPsurcharge), which supports previous evidence for gender differences in environmental behaviour in general (Zelezny, Chua, & Aldrich, Citation2000) and in WTP for air travel emissions in particular (MacKerron et al., Citation2009).

Table 2. Results from stepwise regression of model (1).

Of the other significant variables, frequentfly is the only one with a negative sign. In the context of WTPsurcharge, this backs the recent finding that support for aviation policies is weaker among ‘aeromobile’ people (Kantenbacher, Hanna, Cohen, Miller, & Scarles, Citation2018). On the other hand, people who feel personally responsible for their own emissions tend to agree with the surcharge (WTPsurcharge). This is in line with the finding that a perception that the general public is responsible for climate change (in contrast to governments or industry) significantly increases the approval of mandatory carbon offsetting (Kantenbacher et al., Citation2018). Feeling responsible is also associated with an increase in the amount people were willing to pay, again consistent with previous research (Brouwer et al., Citation2008). It is important to note that only one quarter of respondents ranked themselves (i.e. air travellers) first or second when asked who from a group of five different actors is most responsible to reduce emissions from air travel. This closely replicates corresponding findings from a survey study at a Swedish airport (Gössling et al., Citation2009).

Besides the personal sense of responsibility, also people’s political view appears to be significant for WTP. A leftpolview is associated with a higher likelihood for WTPsurcharge. This, however, only implied a modest political polarization on the issue. While WTPsurcharge was, indeed, highest among people with a clearly left political view (82%), it was still above 50% across the whole political spectrum. A recent opinion poll found similar approval of the Swedish air ticket tax but a slightly more pronounced political polarization (Rosén & Kihlberg, Citation2018).

Finally, a preference for earmarking tax revenues for climate change mitigation or sustainable transport solutions (earmark) is positively associated with WTP. This finding is in line with previous research that earmarking is the preferred option to use revenues form carbon pricing policies (Baranzini & Carattini, Citation2017; Drews & Bergh, Citation2016; Kotchen et al., Citation2017).

3.3. Potentially influential factors from the Swedish context

In addition to personal factors influencing WTP, two key aspects of this study’s Swedish context were identified that may have influenced the results: (a) the lively public debate around a climate tax on air travel, and (b) sociocultural aspects of environmental policy making in Sweden.

First, the public debate in the context of the Swedish air ticket tax might have led to strategic behaviour among respondents. At the time of the study in early 2017 an air ticket tax had been publicly discussed and planned for by the Swedish government for several months. Therefore, the air ticket surcharge that was presented in the survey was likely a policy that was perceived by respondents as something that might actually be implemented, hence giving them an incentive to strategically undervalue emissions reductions under a mandatory surcharge. Due to this strategic bias the level of WTPair_short and WTPair_long might in fact be higher than stated by respondents.

On the other hand, there are some sociocultural particularities of Sweden, which might have led to higher WTP (than could be expected in other countries). Case or country specific social and cultural aspects are highly relevant for the acceptance of climate change policies (Alló & Loureiro, Citation2014). Sweden is a country characterized by a high trust in government (Rothstein, Citation2015), a high environmental awareness among the population, particularly with respect to climate change (EC DG Communication, Citation2017), and a strong tradition of environmental taxation (OECD, Citation2014). This implies that a government-administered tax or surcharge targeting climate change is likely to be better accepted (also at a higher tax level) in Sweden than in countries with lower trust in government, lower environmental awareness and dislike of (environmental) taxation.

4. Conclusions and policy implications

The results of this study have implications both for carbon pricing of air travel in general and for the specific policy of air ticket taxation in Sweden. The first policy relevant finding is that there is a considerable positive WTP for a mandatory surcharge on air travel emissions. Compared to voluntary offsetting, for which previous studies also found positive WTP, a surcharge or tax is a favourable instrument from a climate mitigation perspective as it actually forces people to pay. In the case of offsetting there seems to be an attitude-behaviour gap (Higham, Reis, & Cohen, Citation2016; Juvan & Dolnicar, Citation2014), which might explain the discrepancy between stated WTP and the low actual participation in the offsetting market (Zelljadt, Citation2016). This study also provides some indications for the attitude-behaviour gap, as about half of the respondents expressed positive WTP, but did not feel that it is mainly the air travellers’ responsibility to reduce emissions.

A tax that forces every air traveller to pay for the emissions has two potential climate impacts. First, it may steer behaviour away from flying. Second, it generates revenue that can be used for climate mitigation purposes. In both cases it is important that the incentive structure for different travel distances is well-designed. The new air ticket tax in Sweden is SEK 60 (EUR 6) for short-distance flights (including domestic and intra-European), SEK 250 (EUR 25) for medium-distance flights and SEK 400 (EUR 40) for long-distance flights (Swedish Tax Agency, Citation2018). If measured in SEK/t CO2 (see ), the tax is higher for the long-distance flights used in this study (ca. 330 SEK/ tCO2) than for the short-distance flights (ca. 200 SEK/ tCO2). If the aim is to steer travel behaviour away from flying, and if distance-specific WTP values are taken into consideration, it should be the other way around and the tax (per tCO2) should be higher for short-distance flights than for long-distance flights.

The air ticket tax is, however, only one policy with impact on the ticket price. In addition, the EU ETS applies to all intra-European (i.e. only short-distance) flights. The associated cost per flight has so far been negligible (<1 EUR per flight) as more than 80% of EUAs are allocated for free to the aviation sector and carbon prices under the EU ETS have been low (De Bruyckere & Abbasov, Citation2016). Moreover, also the reduced VAT rate of 6% is charged on Swedish domestic flightsFootnote6, but not on international flights. As international flights make up 80% of the passengers (and 90% of CO2 emissions) of Swedish air travel (Kamb, Larsson, Nässén, & Åkerman, Citation2016), and as VAT is not relevant for business travel, the (reduced) VAT applies only to a small fraction of flights. So, even if the EU ETS, domestic VAT and air tickets taxes are all taken into consideration, the implicit carbon price on short-distance flights likely remains much lower than the implicit carbon price on long-distance flights. Considering further that environmentally preferable substitutes, such as high-speed trains, are only viable for short-distance travels, the incentive structure of the new air ticket tax seems to be misguided.

Moreover, the overall implied carbon price level on air travel is still low. With increasing EU ETS allowance prices and decreasing free allocation, the costs per short-distance flight may increase in the future, but the risk for ‘over-charging’ short-distance flights due to overlaps between the EU ETS and the air ticket tax is limited. Carbon prices implied by the air ticket tax (< 350 SEK) and on the market for EUAs (ca. 200 SEK in September 2018) are, for instance, still far away from the level of the Swedish carbon tax of 1,150 SEK/ tCO2. The carbon tax is at the same time the most common value for the external cost of carbon used in Swedish transport planning (Trafikverket, Citation2016). Accepting the carbon tax as a valid proxy for the external cost of carbon in the Swedish context implies that WTP values found in this study are lower bound estimates for the value of air travel emissions and that existing carbon pricing policies in the aviation sector are not ambitious enough.

Accordingly, strong behavioural change is not expected and the Swedish tax is projected to reduce the number of flights only by about 3%, while annual growth until 2022 is projected to be 3.6% (Andersson & Falck, Citation2017). The main argument for keeping the Swedish tax at a relatively low level has been to avoid the risk of passengers shifting from domestic airports to airports abroad (Swedish Government, Citation2018), which was one of the reasons for abolishing the Dutch air passenger duty (Gordijn, Citation2010). The risk for demand shifts abroad is likely to be higher for long-distance flights, since air ticket taxes for these flights are higher. This is, in turn, an additional argument in favour of somewhat higher taxes on short-distance flights.

The low overall low tax level, the relatively low tax rate on short-distance flights and the risk of demand shifting to other countries suggest that the effectiveness of a tax scheme relies on the use of the revenues for climate mitigation, rather than on behavioural change. Yet, revenues from the new Swedish air ticket tax, projected to be SEK 1.8 billion per year, are programmed to go to the general budget (Andersson & Falck, Citation2017). Similarly, revenues from EU ETS auctions in Sweden are also not earmarked (Le Den, Beavor, Porteron, & Ilisescu, Citation2017). This not only reduces the effectiveness of the tax or the trading scheme, but general budget use was also the least popular option for revenue use among respondents of the survey. Respondents’ preference for earmarking was significantly associated with their WTP, which implies a wish for consistency between the tax base and the intended revenue use. These findings suggest that earmarking revenues may raise public acceptance or might enable a more ambitious pricing policy. A recent study even suggests that there is an association between the expected (direct) environmental effectiveness of a tax and the preference for environmental earmarking (Carattini, Baranzini, Thalmann, Varone, & Vöhringer, Citation2017). Hence, the strong preference for earmarking found in the Swedish case might well be explained by respondents’ low expectations for the effectiveness of the air ticket tax.

In addition to increased effectiveness, earmarking revenues would address another common criticism of the Swedish air ticket tax, namely its lack of incentives for innovation. The air ticket tax has been criticized on the grounds that, by taxing tickets rather than emissions or fuels, it does not encourage innovation. Economic modelling has shown that air ticket and fuel taxes both impact emissions, but that only fuel taxes incentivize fuel economy improvements, and that there are no clear-cut differences in welfare effects between the two (Keen, Parry, & Strand, Citation2013). The main reason for not taxing emissions, e.g. through fuel taxation, is related to international trade regimes limiting fuel taxation in aviation (e.g. European Council Directive 2003/96/EC). Earmarking of revenues may partly compensate for this by enabling the provision of funds for innovations related to, for instance, efficiency improvements and alternative fuels.

In addition to the effectiveness of air ticket taxation and its innovation potential, fairness is another important policy aspect. This study found that frequent fliers tend to have a lower WTP, which is problematic as it might be driven by free-riding, i.e. strategically understating WTP to avoid costly payments in the future (Venkatachalam, Citation2004). Frequent flyers are not only willing to pay less, but they also disproportionately use the highly subsidized aviation system (Gössling et al., Citation2017) and cause a larger amount of CO2 emissions, thereby adding further costs to society. The mismatch between frequent flyers’ lower WTP and higher impact imply that it is a large challenge to implement adequate carbon pricing policies for frequent flyers. This is a political rather than a technical challenge. There are proposals to, for instance, differentiate taxes between economy, business and first class tickets, or to introduce progressive tax rates that increase with flight frequency (Chancel & Piketty, Citation2015; Krenek & Schratzenstaller, Citation2016).

In conclusion, neither voluntary emissions offsetting, nor the inclusion of aviation in emissions trading schemes, nor the current practice of revenue use appear to be sufficient to counterbalance emissions growth from air travel. In contrast, air ticket taxes whose revenues are used for climate change mitigation appear to be a viable policy option as long as there is no ambitious international scheme in place. However, the substantial positive WTP for such a climate surcharge on air tickets also indicates that modest taxation will unlikely steer behaviour away from flying, and high tax rates and earmarking of revenues are needed in order to achieve considerable CO2 emissions reductions.

Supplemental Material

Download MS Word (85.6 KB)Acknowledgements

We thank colleagues and students at the IIIEE, Lund University, for their valuable input during survey development and testing, and we thank Prof. Luis Mundaca for critical and constructive suggestions regarding study design and interpretation of results.

Disclosure statement

No potential conflict of interest was reported by the authors.

ORCID

Jonas Sonnenschein http://orcid.org/0000-0002-8738-2704

Nora Smedby http://orcid.org/0000-0003-1433-2260

Additional information

Funding

Notes

1. The whole survey is available in Section A. of the supplementary material online; and Section B. of the supplement contains further information about the sampling process.

2. Two additional PVs, that were part of the survey but are not reported here, were a motor vehicle fuel surcharge and voluntary offsetting of transport emissions by purchasing and retiring EU emission allowances.

3. 10 SEK were about 1 EUR at the time of the study.

4. These two values were the respective midpoints of respondents’ WTP intervals for short and long distance flights.

5. The analysis did not go beyond combinations in which the carbon intensity of short distance flights was double the one of long distance flights (e.g. 75/150, 100/200 and 125/250 g/pkm respectively).

6. Note that charging reduced VAT can be regarded a subsidy, rather than a tax.

Related Research Data

References

- Alló, M., & Loureiro, M. L. (2014). The role of social norms on preferences towards climate change policies: A meta-analysis. Energy Policy, 73(Supplement C), 563–574. doi: 10.1016/j.enpol.2014.04.042

- Andersen Resare, L. (2015). CO2 emissions when flying? Retrieved from http://www.sasgroup.net/en/co2-emissions-when-flying/

- Andersson, M., & Falck, M. (2017). Skatt på flygresor (Lagrådsremiss). Stockholm: Finansdepartementet. Retrieved from http://www.regeringen.se/49c8c5/contentassets/1e6ea0359b8b4fa8a265ff4387d8eb57/skatt-pa-flygresor.pdf

- Baranzini, A., & Carattini, S. (2017). Effectiveness, earmarking and labeling: Testing the acceptability of carbon taxes with survey data. Environmental Economics and Policy Studies, 19(1), 197–227. doi: 10.1007/s10018-016-0144-7

- Baranzini, A., van den Bergh, J. C. J. M., Carattini, S., Howarth, R. B., Padilla, E., & Roca, J. (2017). Carbon pricing in climate policy: Seven reasons, complementary instruments, and political economy considerations. Wiley Interdisciplinary Reviews: Climate Change, 8(4), n/a-n/a. doi: 10.1002/wcc.462

- Becken, S., & Mackey, B. (2017). What role for offsetting aviation greenhouse gas emissions in a deep-cut carbon world? Journal of Air Transport Management, 63(Supplement C), 71–83. doi: 10.1016/j.jairtraman.2017.05.009

- Blasch, J., & Farsi, M. (2014). Context effects and heterogeneity in voluntary carbon offsetting – a choice experiment in Switzerland. Journal of Environmental Economics and Policy, 3(1), 1–24. doi: 10.1080/21606544.2013.842938

- Broderick, J. (2008). Voluntary carbon offsets: A contribution to sustainable tourism? In D. Weaver, C. Michael Hall, & S. Gössling (Eds.), Sustainable tourism futures (Vol. 15, pp. 169–199). Routledge. doi: 10.4324/9780203884256.ch10

- Brouwer, R., Brander, L., & Van Beukering, P. (2008). “A convenient truth”: air travel passengers’ willingness to pay to offset their CO2 emissions. Climatic Change, 90(3), 299–313. doi: 10.1007/s10584-008-9414-0

- Cames, M., Graichen, J., Siemons, A., & Cook, V. (2015). Emission reduction targets for international aviation and shipping. Freiburg: European Parliament. Directorate General for Internal Policies. Retrieved from http://www.europarl.europa.eu/RegData/etudes/STUD/2015/569964/IPOL_STU(2015)569964_EN.pdf

- Carattini, S., Baranzini, A., Thalmann, P., Varone, F., & Vöhringer, F. (2017). Green taxes in a post-Paris world: Are millions of nays inevitable? Environmental and Resource Economics, 68(1), 97–128. doi: 10.1007/s10640-017-0133-8

- Carlsson, F., Kataria, M., Krupnick, A., Lampi, E., Löfgren, Å, Qin, P., … Sterner, T. (2012). Paying for mitigation: A multiple country study. Land Economics, 88(2), 326–340. doi: 10.3368/le.88.2.326

- Chancel, L., & Piketty, T. (2015). Carbon and Inequality from Kyoto to Paris: Trends in the global inequality of carbon emissions (1998-2013) and prospects for an equitable adaptation fund. Paris School of Economics. Retrieved from http://www.ledevoir.com/documents/pdf/chancelpiketty2015.pdf

- Choi, A. S., & Ritchie, B. W. (2014). Willingness to pay for flying carbon neutral in Australia: An exploratory study of offsetter profiles. Journal of Sustainable Tourism, 22(8), 1236–1256. doi: 10.1080/09669582.2014.894518

- Cui, Q., Li, Y., & Wei, Y.-M. (2017). Exploring the impacts of EU ETS on the pollution abatement costs of European airlines: An application of network environmental production function. Transport Policy, 60, 131–142. doi: 10.1016/j.tranpol.2017.09.013

- Daley, B., & Preston, H. (2009). Aviation and climate change: Assessment of policy options. In S. Gössling, & P. Upham (Eds.), Climate change and aviation: Issues, challenges and solutions (pp. 347–372). London: Earthscan.

- De Bruyckere, L., & Abbasov, F. (2016). Aviation ETS - gaining altitude. Brussels: Transport & Environment. Retrieved from https://www.transportenvironment.org/sites/te/files/2016_09_Aviation_ETS_gaining_altitude.pdf

- Diekmann, A., & Preisendörfer, P. (2003). Green and greenback: The behavioral effects of environmental attitudes in Low-cost and high-cost situations. Rationality and Society, 15(4), 441–472. doi: 10.1177/1043463103154002

- Drews, S., & Bergh, J. C. J. M. v. d. (2016). What explains public support for climate policies? A review of empirical and experimental studies. Climate Policy, 16(7), 855–876. doi: 10.1080/14693062.2015.1058240

- EC DG Communication. (2017, September 15). Special Eurobarometer 459: Climate change. Retrieved from https://data.europa.eu/euodp/data/dataset/S2140_87_1_459_ENG

- Gordijn, H. (2010). The Dutch Aviation Tax; lessons for Germany? Presented at the Infraday-2010, Berlin. Retrieved from https://www.infraday.tu-berlin.de/fileadmin/fg280/veranstaltungen/infraday/conference_2010/papers_presentations/paper---gordijn.pdf

- Gössling, S., Fichert, F., & Forsyth, P. (2017). Subsidies in aviation. Sustainability, 9(8), 1295. doi: 10.3390/su9081295

- Gössling, S., Haglund, L., Kallgren, H., Revahl, M., & Hultman, J. (2009). Swedish air travellers and voluntary carbon offsets: Towards the co-creation of environmental value? Current Issues in Tourism, 12(1), 1–19. doi: 10.1080/13683500802220687

- Higham, J., Reis, A., & Cohen, S. A. (2016). Australian climate concern and the ‘attitude–behaviour gap.’. Current Issues in Tourism, 19(4), 338–354. doi: 10.1080/13683500.2014.1002456

- Hornsey, M. J., Harris, E. A., Bain, P. G., & Fielding, K. S. (2016). Meta-analyses of the determinants and outcomes of belief in climate change. Nature Climate Change, 6(6), 622–626. doi: 10.1038/nclimate2943

- ICAO. (2016). Consolidated statement of continuing ICAO policies and practices related to environmental protection – Global Market-based Measure (MBM) scheme (No. Resolution A39-3). Retrieved from https://www.icao.int/environmental-protection/CORSIA/Documents/Resolution_A39_3.pdf

- Jou, R.-C., & Chen, T.-Y. (2015). Willingness to pay of air passengers for carbon-offset. Sustainability, 7(3), 3071–3085. doi: 10.3390/su7033071

- Juvan, E., & Dolnicar, S. (2014). The attitude–behaviour gap in sustainable tourism. Annals of Tourism Research, 48, 76–95. doi: 10.1016/j.annals.2014.05.012

- Kamb, Anneli, Larsson, Jörgen, Nässén, Jonas, & Åkerman, Jonas. (2016). Klimatpåverkan från svenska befolkningens internationella flygresor. Gothenburg: Chalmers University of Technology. Retrieved from http://publications.lib.chalmers.se/records/fulltext/240574/240574.pdf.

- Kantenbacher, J., Hanna, P., Cohen, S., Miller, G., & Scarles, C. (2018). Public attitudes about climate policy options for aviation. Environmental Science & Policy, 81, 46–53. doi: 10.1016/j.envsci.2017.12.012

- Keen, M., Parry, I., & Strand, J. (2013). Planes, ships and taxes: Charging for international aviation and maritime emissions. Economic Policy, 28(76), 701–749. doi: 10.1111/1468-0327.12019

- Kotchen, M. J., Turk, Z. M., & Leiserowitz, A. A. (2017). Public willingness to pay for a US carbon tax and preferences for spending the revenue. Environmental Research Letters, 12(9), 094012. doi: 10.1088/1748-9326/aa822a

- Krenek, A., & Schratzenstaller, M. (2016). Sustainability-oriented EU taxes : The example of a European carbon-based flight ticket Tax ( FairTax: Working Paper Series No. 01). Umeå universitet. Retrieved from http://urn.kb.se/resolve?urn=urn:nbn:se:umu:diva-120832

- Kuramochi, T., Höhne, N., Schaeffer, M., Cantzler, J., Hare, B., Deng, Y., … Blok, K. (2018). Ten key short-term sectoral benchmarks to limit warming to 1.5°C. Climate Policy, 18(3), 287–305. doi: 10.1080/14693062.2017.1397495

- Le Den, X., Beavor, E., Porteron, S., & Ilisescu, A. (2017). Analysis of the use of auction revenues by the member states. Brussels: European Commission. Retrieved from https://ec.europa.eu/clima/sites/clima/files/ets/auctioning/docs/auction_revenues_report_2017_en.pdf

- Lee, D.S., Pitari, G., Grewe, V., Gierens, K., Penner, J.E., Petzold, A., & Prather, M.J. (2010). Transport impacts on atmosphere and climate: Aviation. Atmospheric Environment, 44(37), 4678–4734. doi: 10.1016/j.atmosenv.2009.06.005

- Loomis, J. (2014). Strategies for overcoming hypothetical bias in stated preference surveys. Journal of Agricultural and Resource Economics, 39(1), 34–46.

- Löschel, A., Sturm, B., & Uehleke, R. (2017). Revealed preferences for voluntary climate change mitigation when the purely individual perspective is relaxed – evidence from a framed field experiment. Journal of Behavioral and Experimental Economics, 67, 149–160. doi: 10.1016/j.socec.2016.12.007

- Lu, J.-L., & Shon, Z. Y. (2012). Exploring airline passengers’ willingness to pay for carbon offsets. Transportation Research Part D: Transport and Environment, 17(2), 124–128. doi: 10.1016/j.trd.2011.10.002

- MacKerron, G. J., Egerton, C., Gaskell, C., Parpia, A., & Mourato, S. (2009). Willingness to pay for carbon offset certification and co-benefits among (high-)flying young adults in the UK. Energy Policy, 37(4), 1372–1381. doi: 10.1016/j.enpol.2008.11.023

- Meleo, L., Nava, C. R., & Pozzi, C. (2016). Aviation and the costs of the European emission trading scheme: The case of Italy. Energy Policy, 88, 138–147. doi: 10.1016/j.enpol.2015.10.008

- OECD. (2014). OECD environmental performance reviews: Sweden 2014. OECD Publishing. doi: 10.1787/9789264213715-en

- Penner, J. E. (1999). Aviation and the global atmosphere: A special report of the intergovernmental panel on climate change. Cambridge: Cambridge University Press.

- Rosén, H., & Kihlberg, J. (2018, March 25). Stödet ökar för flygskatten – majoritet säger ja. Dagens Nyheter. Retrieved from https://www.dn.se/nyheter/politik/stodet-okar-for-flygskatten-majoritet-sager-ja/

- Rothstein, B. (2015). The moral, economic, and political logic of the Swedish welfare state. In J. Pierre (Ed.), The Oxford handbook of Swedish politics. Oxford University Press. Retrieved from http://www.oxfordhandbooks.com/view/10.1093/oxfordhb/9780199665679.001.0001/oxfordhb-9780199665679-e-41

- Segerstedt, A., & Grote, U. (2016). Increasing adoption of voluntary carbon offsets among tourists. Journal of Sustainable Tourism, 24(11), 1541–1554. doi: 10.1080/09669582.2015.1125357

- Sims, R., Schaeffer, R., Creutzig, F., Cruz-Núñez, X., D’Agosto, M., Dimitriu, D., … Tiwari, G. (2014). Transport. In Climate Change 2014: Mitigation of Climate Change. Contribution of Working Group III to the Fifth Assessment Report of the Intergovernmental Panel on Climate Change [Edenhofer, O., R. Pichs-Madruga, Y. Sokona, E. Farahani, S. Kadner, K. Seyboth, A. Adler, I. Baum, S. Brunner, P. Eickemeier, B. Kriemann, J. Savolainen, S. Schlömer, C. von Stechow, T. Zwickel and J.C. Minx (eds.)]. Cambridge University Press, Cambridge, United Kingdom and New York, NY, USA.

- Swedish Government. (2018). Regeringens proposition 2017/18:1 (The government’s budget proposal) ( p. 474ff.). Stockholm. Retrieved from https://www.regeringen.se/4a6e13/contentassets/79f6d27416794f0bb146c792e02b65fc/budgetpropositionen-for-2018-hela-dokumentet-prop.-2017181.pdf

- Swedish Tax Agency. (2018). Tax on air travel in Sweden. Retrieved from https://www.skatteverket.se/servicelankar/otherlanguages/inenglish/businessesandemployers/payingtaxesbusinesses/taxonairtravel.4.41f1c61d16193087d7f5348.html

- Trafikverket. (2016). Analysmetod och samhällsekonomiska kalkylvärden för transportsektorn: ASEK 6.0, Kap 12 Kostnader för klimateffekter [Analysis method and calculation values for cost benefit analyses in the tansport sector: ASEK 6.0, Ch 12 Costs of climate effects]. Borlänge. Retrieved from https://www.trafikverket.se/contentassets/4b1c1005597d47bda386d81dd3444b24/12_klimateffekter_a60.pdf

- Venkatachalam, L. (2004). The contingent valuation method: A review. Environmental Impact Assessment Review, 24(1), 89–124. doi: 10.1016/S0195-9255(03)00138-0

- Wiser, R. H. (2007). Using contingent valuation to explore willingness to pay for renewable energy: A comparison of collective and voluntary payment vehicles. Ecological Economics, 62(3–4), 419–432. doi: 10.1016/j.ecolecon.2006.07.003

- World Bank, Ecofys, & Vivid Economics. (2016). State and trends of carbon pricing 2016. Washington, DC: World Bank. Retrieved from http://hdl.handle.net/10986/25160

- World Bank, Ecofys, & Vivid Economics. (2017). State and trends of carbon pricing 2017. Washington, DC: World Bank Publications. Retrieved from http://hdl.handle.net/10986/28510

- Zelezny, L. C., Chua, P.-P., & Aldrich, C. (2000). New ways of thinking about environmentalism: Elaborating on gender differences in environmentalism. Journal of Social Issues, 56(3), 443–457. doi: 10.1111/0022-4537.00177

- Zelljadt, E. (2016). Offsetting in the aviation sector evaluating voluntary offset programs of major airlines. Berlin: ecologic. Retrieved from http://ecologic.eu/sites/files/publication/2016/zelljadt_2016_offset_use_in_the_aviation_sector.pdf