ABSTRACT

Chinese monetary and financial authorities have been among the pioneers in promoting green finance. This article investigates the use of one specific monetary policy tool, namely window guidance, by the Peoples’ Bank of China (PBC) and the China Banking Regulatory Commission (CBRC) to encourage financial institutions to expand credit to sustainable activities and curb lending to heavy-polluting industries. ‘Window guidance’ is a relatively informal policy instrument that uses benevolent compulsion to ‘guide’ financial institutions to extend credit and allocate lending in line with official (government) targets. We investigate window guidance targets for the period 2001–2020 and find that ‘green’ targets were included by the CBRC from at least 2006 and by the PBC from 2007 to discourage lending to carbon-intensive and polluting industries and/or to increase support to sustainable activities. In 2014, both authorities stopped discouraging lending to carbon-intensive/polluting industries through window guidance. Sustainable objectives were subsequently also removed from the PBC's list of window guidance priority sectors at the start of 2019, ending the practice of green window guidance in China. Sustainability-enhancing window guidance targets were replaced and formalized through new ‘Guidelines for Establishing the Green Financial System’, reflecting efforts to move away from controls-based towards market-based policy instruments. Based on this analysis, the article draws four lessons for the design of green finance policies for other countries that seek to enhance sustainable finance and mitigate climate change and related risks.

Key policy insights

The Chinese experience of using window guidance to direct bank lending to support national sustainability targets and goals shows how the instrument can be successfully used in financial markets that are at an early stage of financial market development.

The efficacy of window guidance and other directed bank-lending policies is likely to diminish as financial markets mature and direct monetary policy instruments become less powerful.

When window guidance is used, it should be linked to clear criteria of success, the achievement of which should be monitored.

Green window guidance should be embedded in a broader framework of green finance policies, as well as climate and environmental policies.

While today's framing and language on sustainable finance policy in China focuses increasingly on market-based instruments, the Chinese experience of using window guidance offers valuable lessons for other emerging economies in Asia and beyond with financial systems dominated by banks.

1. Introduction

China has been one of the pioneers in developing green finance. Greening growth and steering the Chinese economy towards a more sustainable development path has been an important objective for Chinese government agencies for almost two decades. Achieving this goal necessitates a shift of investment away from carbon- and resource-intensive and highly polluting industries towards more sustainable, greener industries. China's leadership has made clear that it expects the financial sector to play a central role in financing and supporting this transition. China's green financial governance policies, including prudential supervisory and green finance guidelines, have received considerable attention in China and internationally over the last decade. However, little is known about how Chinese monetary and financial regulatory agencies have informally guided credit towards more sustainable investment through a process of credit allocation, known as ‘window guidance’. Window guidance, also known as ‘moral suasion’ and ‘jawboning’, is a translated term of the Japanese expression and can be defined as a ‘policy [that] uses benevolent compulsion to persuade banks and other financial institutions to stick to official guidelines’ (Geiger, Citation2008). Window guidance was initially adopted by the People's Bank of China (PBC), the country's central bank, in the late 1990s (Geiger, Citation2008). Window guidance has also been employed by the China Banking Regulatory Commission (CBRC) (Ma & Spencer, Citation2004), the primary banking regulator.Footnote1 Window guidance, as an instrument to promote green lending while discouraging investment in environmentally harmful activities, has been listed as an important instrument in the PBC and CBRC's set of policy instruments employed to contribute to the Chinese government's objective of greening the economy. A thorough understanding of this ‘green window guidance’, which – analogous to the definition of window guidance provided above – can be defined as a policy that uses benevolent compulsion to persuade financial institutions to extend additional credit to sustainable sectors, companies or activities or away from heavy-polluting ones, is important for deriving lessons for the design of green finance policies in China and elsewhere.

Within the broader literature on the role of central banks and financial regulators in addressing environmental risks and greening the financial system to support the transition to low carbon development (e.g. Alexander & Fisher, Citation2019; Campiglio et al., Citation2018; Dikau & Volz, Citation2019, Citation2021; Durrani et al., Citation2020; Robins et al., Citation2021; Setyowati, Citation2023; Volz, Citation2017), this paper focuses on one specific policy instrument for scaling-up sustainable finance. Previous research on the promotion of green finance and sustainable development in China has primarily focused on the green regulatory policies and credit guidelines that Chinese financial authorities have rolled out (e.g. Volz, Citation2019; Wang, Citation2018; Zadek & Chenghui, Citation2014), but has largely overlooked how informal guidance has been used for the same objective. Concerning the greening of monetary policy, contributions focus on proposals for the alignment of different instruments, usually in the European context (Dafermos et al., Citation2021; Matikainen et al., Citation2017; Schoenmaker, Citation2021; Van ’t Klooster & van Tilburg, Citation2020) and, in the context of the PBC, on repos, the Medium Term Lending Facility, and their collateral eligibility criteria (Chen et al., Citation2019; Fang et al., Citation2020; Macaire & Naef, Citation2021). The literature discussing window guidance in China, on the other hand, has focused on its effectiveness in controlling the growth of lending by commercial banks (Angrick & Yoshino, Citation2020; Beggs & Deer, Citation2019; Bell & Feng, Citation2013; Fukumoto et al., Citation2010; Geiger, Citation2008; He, Citation2014), but it has not addressed the sustainable finance dimension of window guidance. Moreover, the role of the CBRC as the country's primary banking regulator has been largely ignored by the literature on window guidance in China, even though it has included various credit-guiding policies in its policy reports, as shown by this article.

Against this backdrop, this article investigates how the PBC and the CBRC selected their window guidance targets with the aim of guiding credit towards green investment and away from harmful activities in order to promote sustainable investment and growth. Based on a detailed analysis of the PBC and the CBRC's policy reports, we examine window guidance targets for the period 2001–2020. The changes of sustainable window guidance targets are discussed against the background of bigger economic policy trends and developments in China. To the best of our knowledge, this article is the first that examines the role of window guidance in greening bank lending in China.

Our principal finding is that both institutions, the PBC and the CBRC, framed their qualitative window guidance to encourage banks to lend to specific priority sectors and refrain from extending credit to others. The qualitative targets of both institutions’ window guidance policies are diverse and include a large and changing variety of national, social and economic priority industries and regions over the last few decades. Importantly, between 2006 and 2019, targets included different sustainability-related objectives, confirming that both institutions actively pursued what we call ‘green window guidance’. In 2014, however, the PBC and CBRC stopped discouraging lending to high energy-consuming and polluting industries. Subsequently, at the start of 2019, green finance was removed from the list of PBC targets and priority sectors, and the green dimension of window guidance was effectively closed, while the PBC continues to use the instrument for the prioritization of other not explicitly green sectors and activities.

The phasing out of the green targets of window guidance occurred against the backdrop of a push towards the formalization of comprehensive sustainable finance and climate risk-related financial policy in China. In September 2016, the PBC, along with the CBRC and five other governmental agencies, issued the Guidelines for Establishing the Green Financial System, which provide a comprehensive policy framework that has the aim of mobilizing and incentivising investment in green sectors, while restricting credit flows to polluting industries (PBC et al., Citation2016). The implementation of the new guidelines, along with the phasing out of green window guidance targets, reflect a transition towards the formalization of ‘green monetary policy’. A greater emphasis on financial markets in financing green investments is also in line with the general shift from controls- to market-basedFootnote2 monetary policy since the 2010s (Beggs & Deer, Citation2019).

Moreover, we discuss the calibration of window guidance targets against the background of the major economic, structural and environmental trends in China. While the inclusion of guidance targets to allocate credit away from heavy, energy-consuming and polluting industries coincided with a persistent reduction of air pollution, the abandoning of these targets in 2014 coincided with a delayed and most likely unrelated (due to lags from lending to economic activity) stagnation or even slight increase of pollution from 2016 to 2017. Furthermore, renewable energy, energy saving and the low carbon economy were consistently emphasized as qualitative targets for credit flows while the Chinese economy experienced an unprecedented rise in new investment in clean energy that transformed China's energy mix. In contrast, abandoning the targets coincided with a significant decline of annual investment in renewable energy. While these observations do not imply a causal relationship, they provide the context in which green window guidance was employed in China.

Based on the analysis of China's experience with green window guidance, the article draws four lessons. First, the Chinese experience shows how directed lending through window guidance can be framed to address the reallocation of capital towards green economic activities, even though it is difficult to isolate the effect. Second, the efficacy of window guidance and other directed controls-based lending policies is likely to diminish as financial markets mature and bank lending becomes less dominant. Third, when window guidance is used, it should be linked to clear criteria of success, the achievement of which should be monitored. Authorities should also monitor potential distorting, unwanted side effects. Forth, green window guidance should be embedded in a broader set of green finance policies, prudential risk-focused frameworks, as well as general climate and environmental policies. Overall, the Chinese experience shows how green window guidance can be used in a policy effort to align the financial system with climate and other sustainability goals, but that such policies need to be adapted to the specific context in which they are used.

The article is structured as follows. Section 2 outlines the methodology and data that we use. Section 3 provides an overview of the broader sustainable finance policy landscape in China. Subsequently, Section 4 presents the empirical investigation of window guidance as a tool for greening the lending of Chinese banks, and an assessment of the development of green window guidance targets. Section 5 discusses policy implications for the promotion of sustainable finance and mitigation of climate change-related and environmental risks through direct instruments. Section 6 concludes.

2. Methodology and data

The article is based on an in-depth analysis of government documents, including regulations, policy reports and sustainable finance action plans. The empirical analysis is based on the review of the Annual Reports of the CBRC from 2006 to 2016 and the Quarterly Monetary Policy Reports of the PBC from Q1 2001 to Q3 2020. We then conducted a comprehensive desk-research and a content analysis of the selected reports to identify and analyse the PBC and CBRC's account of ‘window’ or ‘credit guidance’ with regard to the inclusion or exclusion of factors relevant for directly supporting green sectors or restricting credit to heavy-polluting and energy intensive industries. The collected data sets were analysed using qualitative methods of content analysis, grounded theory and discourse analysis (Hajer & Versteeg, Citation2005). The data were analysed to identify emerging themes and key ideas (Tavory & Timmermans, Citation2014). We also conducted anonymous, unstructured interviews with six current and former officials and policymakers from the PBC and the CBRC/CBIRC as well as seven market experts in this area to verify our findings and interpretation.

Any study of this kind comes with limitations. First, while the findings on the inclusion, and later exclusion, of sustainability window guidance targets from the policy reports of the CBRC and PBC do reflect the broader developments of the Chinese economy and sustainability agenda, they provide an imperfect account of policy action. This study therefore does not allow for an assessment of policy impact or a quantitative evaluation of the effect of the changing calibration of window guidance on green and non-green financial flows. Instead, we conduct a stock-take and investigate the overall changing calibration, framing and role that window guidance has played in the instrument toolbox of the PBC and CBRC, as well as in the context of China's evolving sustainable finance policy agenda.

Second, the focus of the study is on window guidance by the PBC and CBRC. There are potentially other policies with a similar effect implemented by the same or other financial authorities in China that are not described in this study, making it difficult to isolate the effect of green window guidance.

Finally, the study investigates ‘window’ or ‘credit guidance’ activities that are labelled as such by the PBC and CBRC. We do not consider other indirect policies and instruments that are not explicitly labelled as ‘window guidance’ (窗口指导) or ‘credit policy guidance’ (信贷政策引导). Therefore, the analysis and results of this article are based on the PBC and CBRC's identification and description of relevant policies, leaving open the possibility that the annual and quarterly policy reports that the study is based on omitted or overemphasized certain aspects of actual policy implementation.

3. Sustainable finance policy in China

Efforts in China to introduce sustainability objectives into the financial system, as well as the first policy initiatives by the PBC and other financial authorities, date back to the 1980s (Zadek & Chenghui, Citation2014). Important milestones (see Table A1 in the Supplementary Material) include the joint issuance of the ‘Opinions on Implementing Environmental Protection Policies and Regulations to Prevent Credit Risks’, along with the Green Credit Policy in 2007 by the PBC, the CBRC and the Ministry of Environmental Protection (MEP), which also foreshadowed the wider inter-agency cooperation that was to come. The Green Credit Policy aimed at setting incentives for banks to include environmental compliance, as well as environmental and social (E&S) risk assessment, as criteria to be considered in the loan origination process (IISD, Citation2015). The CBRC has since been active in guiding banks towards assessing environmental standards in the credit review process and is furthermore tasked with enhancing E&S risk management practices (Aizawa & Yang, Citation2010).

Furthermore, banks were required to cease lending to firms blacklisted by the MEP for environmental violations, as well as to projects that violate other green regulation (Shen et al., Citation2013). Wang (Citation2018) characterized the overall approach of Chinese authorities, among them the PBC and the CBRC, as a ‘top-down’ approach, in which macroprudential and monetary policy play key roles and which differs significantly from the Western ‘bottom-up’ approach in which a central role is attributed to the private sector. It is important to emphasize that Chinese monetary and financial authorities have a significant level of control over the financial system, which differs substantially from the Western market-based oversight system.

Over the past decade, a focus of authorities has been the development of a classification (in other jurisdictions known as a ‘taxonomy’) of ‘sustainable’ investments with the aim of encouraging the development of green financial products. Building on the 2007 Green Credit Policy, the CBRC published its Green Credit Guidelines in 2012 (CBRC, Citation2012), thereby introducing a first definition of green loans, which included 12 sectors and activities, including renewable energy, green transportation and green building (NGFS, Citation2019). In 2015, the PBC was the first central bank to establish a green bond standard by issuing the Green Bond Endorsed Project Catalogue (PBC, Citation2015).

The PBC played a central role in developing a green financial information system, a taxonomy of sustainable activities and new green financial products, providing financial institutions with channels for debt financing to support green projects (PBC, Citation2016). Overall, the PBC has played a central role in mainstreaming green finance in China. The incorporation of climate-related and environmental risks on the prudential and credit level has been a target of policy initiatives, supported through the PBC's Green Finance Committee. In this context, the PBC has also incorporated green finance into its macroprudential framework in order to incentivise the scaling up of green finance (Wang, Citation2018).

Apart from a prudential view of climate change and related risks, Chinese sustainable finance polices have also focused on scaling up of green finance. These policy initiatives of the last decades can also be attributed to the central government's economic development goals with sustainability objectives and low-carbon development having been included in China's Twelfth (2011–2015) and Thirteenth (2016–2020) Five-Year Plans (Ho, Citation2018).

The ‘Guidelines for Establishing the Green Financial System’, which were released by the PBC, along with the CBRC and five other governmental agencies in 2016, describe a comprehensive plan that utilizes market- and controls-based policy instruments to further scale up sustainable investment (PBC et al., Citation2016). A strong emphasis lies on the establishment of a formal framework to enable green lending. Furthermore, the guidelines stress the role and development of securities markets and other market-based instruments for supporting green investment. Nonetheless, direct monetary policy instruments in the form of green refinancing operations for green loans are also included in the guidelines, complimented by a broader system of controls over the financial system outside of the PBC and CBRC's direct remit (Pearson et al., Citation2020).

4. Window guidance and the promotion of green finance

Despite its importance as a central element of Chinese monetary policy, there has been little analysis of the qualitative targets of window guidance in general, and on how these targets have been continuously changed to reflect national priorities, including the aim of enhancing sustainable growth, in particular. To fill this gap, we conduct a detailed analysis of the PBC's and the CBRC's policy reports for the periods 2001–2020 and 2006–2016, respectively. In the following, we review the use of window guidance by the PBC and CBRC and examine how sustainability targets were included.

4.1. The PBC's window guidance targets

To analyse the qualitative targets of the PBC's window guidance, and specifically the presence of sustainability-related targets, we investigate the central banks’ Quarterly China Monetary Policy Reports since 2001. The reports offer insights into how window guidance targets have been communicated by the PBC, and how the PBC values window guidance relative to other instruments. The reports also list the qualitative guidance targets the PBC has provided to financial institutions. The qualitative targets of the PBC's window guidance are referred to in the reports both as ‘window guidance’ (窗口指导) or ‘credit policy guidance’ (信贷政策引导) (usually mentioned in the context of the ‘structural guiding role of credit policy’ (和信贷政策的结构引导作用)). Independently of how its guidance efforts are labelled and translated, all investigated quarterly reports by the PBC provide a similar level of detail on the targets of its positive and negative credit guidance. Window or credit guidance is described by the PBC as one of its major instruments of monetary policy in the last decade and is therefore also discussed as a separate instrument in Section Two of each report.

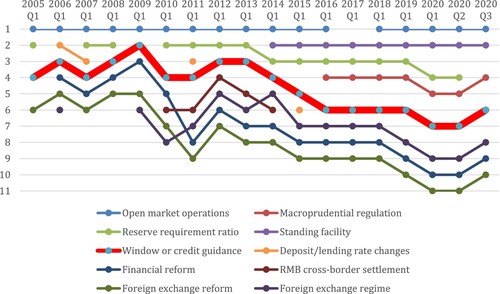

illustrates the qualitative targets of the PBC's window guidance. The green bars in the upper part of the figure denote an inclusion of positive targets, while the red bars in the lower part of the figure denote the inclusion of a negative target in a quarterly report. From the first quarter of 2007 until the first quarter of 2019, the PBC regularly included positive targets for green lending. Negative targets were included regularly between the first quarter of 2007 and the third quarter of 2014, with the exemption of only five quarters.

Figure 1. Inclusion of positive green and negative non-green window guidance targets in the PBC's quarterly reports’, 2005 Q1-2020 Q2.

Over time, the discussion of window or credit guidance has moved further back in the listing of instruments in the PBC's quarterly monetary policy reports (Table A2 in the Supplementary Material). While window guidance was discussed as the PBC's third or fourth instrument in its monetary policy toolbox until 2014, it has since moved to position six or seven, indicating a loss of priority or emphasis of the PBC's guidance operations ().

Figure 2. Relative position of the section on window or credit guidance in the PBC's quarterly reports’ monetary policy section, 2005–2020. Note: See Table 2A for details.

Note: Policy instruments that occurred irregularly are not included. Source: Compiled by authors based on the PBC’s quarterly monetary policy reports.

A central finding is that the PBC stressed the calibration of its credit and window guidance policy to enhance sustainable investment and discourage credit towards environmentally harmful activities (See Figure 1 and columns 4 and 5 of Table A2 in the Supplementary Material for more detail). The targets of the PBC's positive green guidance have varied since 2010. From Q1 2007 until Q1 2013, the PBC usually included one or two specific sustainability targets, such as ‘efforts for energy savings’, ‘emissions reduction’ or ‘environmental protection’. In Q2, Q3 and Q4 of 2013, the PBC did not list positive green window guidance targets, but began in Q1 2014 to include a more general ‘green’ category in its guidance targets in the form of ‘green and environment-friendly areas’ or simply ‘green finance’. A more general green target continued to be included until Q4 2018, although with several disruptions (Q4 2014-Q4 2015, Q2 2016, Q4 2016-Q1 2017, Q1 2018). With regard to negative window guidance, the PBC discouraged lending to ‘heavy energy-consuming and highly polluting industries’ from Q1 2007 until Q2 2014 and included the target in almost every quarter, but stopped including it in the fourth quarter of 2014 (potentially linked to considerations concerning a possible growth-sustainability trade off, further discussed below). In the quarterly reports since Q4 2018, the PBC has not included any positive green or negative heavily polluting targets in the outline of its window guidance operations.

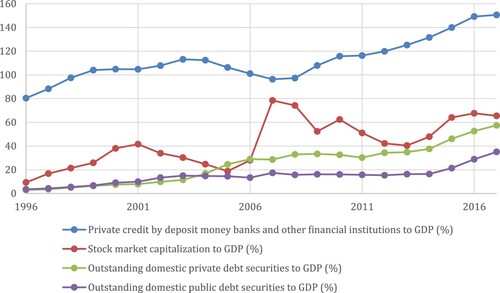

Although it is no longer used in a green calibration, our empirical investigation shows that for the time being, window guidance remains a central qualitative instrument for the allocation of credit to priority sectors and regions – at least for the PBC – with no indication for its abandonment. Despite the rapid development of financial markets in China since the 1990s, bank lending continues to dominate the Chinese financial system (Tobin & Volz, Citation2019), as shown in . Yet, the experience with window guidance in Japan suggests that this instrument may become less effective in influencing how credit is allocated by banks in China going forward (Angrick & Yoshino, Citation2020; Fukumoto et al., Citation2010; Rhodes & Yoshino, Citation1999). The role of financial markets, as well the financial system in which the PBC operates in today, have been compared to the environment in which the Bank of Japan (BOJ) effectively operated in the 1980s and 1990s (Angrick & Yoshino, Citation2020; Fukumoto et al., Citation2010). Fukumoto et al. (Citation2010) argue from a Japanese perspective that since China is expected to see steady progress in its financial market infrastructure and financial liberalization, the historical transition of the role and effectiveness of window guidance in Japan could offer lessons on how progress in financial liberalization could diminish the effectiveness of window guidance in China over time, thereby making interest rate policy more important as a monetary policy instrument. However, it is important to point out that the literature on the BOJ's window guidance primarily focuses on its impact on quantitatively restricting the overall amount of credit, while our analysis of Chinese window guidance focuses on the changing selection of qualitative targets.

Figure 3. Total finance as percentage of GDP, 1996–2017. Source: Compiled by authors with data from the World Bank Financial Development Index database.

Theoretically, the effectiveness of window guidance in controlling the quantity or allocation of credit is bound to diminish when bank lending gives way to capital markets and non-bank-based lending. Therefore, the process of financial market development and liberalization in China, which has seen security and stock markets expand (), may be expected in the future to undermine the effectiveness of window guidance as a credit control instrument by opening up alternative channels for companies to obtain funds. However, for now, the Chinese financial system remains heavily dominated by bank lending, allowing Chinese supervisory agencies to exert significant control over financial flows through the regulation and allocation of bank lending. Furthermore, even if window guidance becomes less effective, there are also other relevant instruments that the Chinese authorities have used and can use in the future to exert and increase control over the financial system, including through direct control of financial institutions independently of financial regulation and supervision (e.g. Bai et al., Citation2020; Chen & Rithmire, Citation2020; Pearson et al., Citation2020; Petry, Citation2020).

4.2. The CBRC's window guidance targets

Similar to the account of the PBC's policy practice, the CBRC Annual Reports give insights into the institution's qualitative credit and window guidance targets. We investigate these targets for the period between 2006 and 2016 (around the time of the merger with CSRC, CBRC stopped publishing annual reports), with regard to how the CBRC described the role of this guidance in promoting green finance. The language used by the CBRC in its reports on its window guidance activities is often vague. Our analysis of the targets in the English annual reports of the CBRC, therefore, includes all accounts of guidance targets that are not associated with formal policy instruments, are informal and can hence be characterized as providing window guidance. Nonetheless, the CBRC's ambition to informally guide credit can be clearly identified in the reports.

Similarly to the PBC's practice of using ‘window guidance’ and ‘credit guidance’ interchangeably, in only 5 of the 11 reports under review does the CBRC refer to its credit guiding activities directly under the label ‘window guidance’ (Table A3 in the Supplementary Material). However, all 11 reports list detailed qualitative lending targets, regions and sectors for informal credit guidance. It is again possible to identify trends in the CBRC's guidance practice. First, from 2006 until 2013, the CBRC remained committed to employing negative window guidance with the aim of encouraging banks to extend less credit to ‘high pollution, energy consuming and resource dependent industries’ and sectors (Columns 3 and 4 of Table A3 in the Supplementary Material). However, mirroring similar observed patterns in the PBC's guidance targets, after 2013, the CBRC stopped its negative guidance through which it had induced banks to ease lending to polluting industries. Second, the CBRC's negative guidance preceded its positive guidance and promotion of green credit. While no positive green target sectors were yet included in 2006, the CBRC began in 2007 to list ‘green credit’ as a positive target for bank lending for the first time. Between 2007 and 2016, the CBRC's positive green guidance became more comprehensive and detailed. Until 2011, it focused mainly on ‘environmentally-friendly activities’, the ‘low carbon economy’ and ‘energy-saving and emission reduction projects’, but included more detailed sectors from 2012 onwards and encouraged financial institutions to increase lending for ‘new energy vehicles’ and renewable energy in general.

4.3. Interpretation and economic contextualization of the development of green window guidance targets

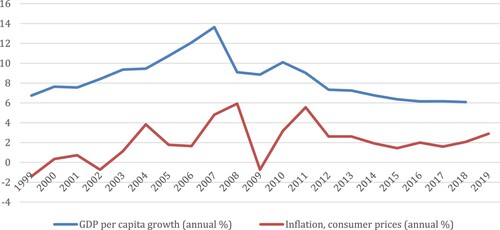

The analysis shows that in their reports, both the PBC and the CBRC describe an extensive use of informal credit or window guidance to allocate credit to sustainable priority sectors and away from heavy polluting industries. Furthermore, the informal interviews with policymakers and market participants also suggest that green window guidance has played a role. While not insinuating a causal relationship, these findings on the changing calibration of window guidance should be discussed against the background of broader economic, financial and environment-related changes that took place in China over the last two decades. The practice of green window guidance was introduced by the CBRC in 2006 and by the PBC in 2010, at a time when China experienced continuous rapid growth and severe and worsening environmental problems. While China's growth model since the late 1970s had been highly successful, it was also highly carbon intensive and polluting, and the positive effects on welfare from strong GDP growth were partially offset by the increase in air pollution and environmental damages (Day, Citation2005; Edmonds, Citation1998; World Bank, Citation1997, Citation2001, Citation2007). The short-term trade-off between growth and environmental protection that many developing and emerging markets are confronted with is well known, and it can be argued that China, in the context of an initially limited ability to achieve growth at low environmental costs, paid a significant environmental price for achieving rapid growth. The welfare-reducing side-effects of rapid growth were taken increasingly seriously in the late 1980s and 1990s, and led to the elevation of the National Environmental Protection Bureau to the status of a ministry in 1998 (Bramall, Citation2008). By the mid-2000s, when China achieved GDP per capita growth rates well above 10% (), growth was deemed sufficiently high and the adverse environmental impacts threatening enough to public health and political stability to justify interventions such as the introduction of negative window guidance targets by the CBRC to restrict financial flows to highly polluting sectors. However, the unwillingness of policymakers to sacrifice too much growth for carbon emission reductions and environmental protection continued. In the 12th Five Year Plan for the period 2010–2015, the Chinese government made a reduction in carbon intensity dependent on achieving at least 8% annual GDP growth during the time period in question (Qiu, Citation2011).

Figure 4. Inflation, consumer prices and GDP per capita growth (annual %) in China, 1999–2019. Sources: Compiled by authors with data files from the World Bank national accounts data, OECD National Accounts, International Monetary Fund and International Financial Statistics and data files.

While high economic growth rates arguably provided the CBRC and the PBC with the policy space to introduce and then expand positive and negative window guidance targets, in 2014, both the PBC and the CBRC abandoned their negative window guidance targets. This adjustment took place against the background of declining GDP per capita growth below 7% for the first time since 1999 (). Furthermore, the Chinese economy increasingly relied again on a more carbon-intensive economic structure between 2002–2009 (Guan et al., Citation2014) and, in the context of slowing economic growth after 2007 and sub-8% growth after 2012, window guidance targets that could have been perceived as impeding rapid economic growth were abandoned.

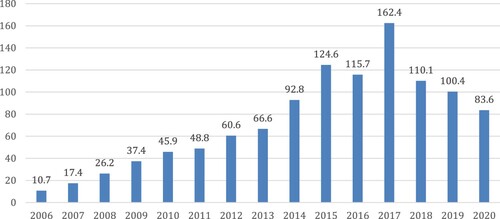

While the last published report of the CBRC from 2016 still includes positive green window guidance targets, the PBC included these for the last time in Q4 2018 and has since refrained from describing window guidance as a tool for the allocation of credit to green sectors. Although the PBC's positive targets had included the ‘transformation of the energy mix’ and ‘clean energy’ in its positive window guidance, the shift in focus first away from the mitigation of credit flows to carbon intensive industries and later the termination of positive guidance occurred against the background of a broader policy change that negatively affected the renewable energy sector in China. In June 2018, the Chinese government began to phase out subsidies for most of its solar projects and subsequently reduced feed-in tariffs and limited subsidies for new solar generation, a sector that had boomed under extensive subsidies (Hook & Hornby, Citation2018). Furthermore, while the PBC and CBRC abandoned the inclusion of green window guidance targets on clean energy, Chinese annual new investment in renewable energyFootnote3 also shrank considerably to US$ 100.4bn in 2019 and decreased further to US$ 183.6bn in 2020 from the peak of US$ 162bn in 2017 (). This 49% decline of investment from the peak occurred in the context of an economy with the highest wind and solar power capacities worldwide which at the same time, is also the most polluting one and remains the world's biggest builder of new coal-fired power stations (Hook, Citation2019). While there is no clear causal relationship, the changing calibration of window guidance coincided with other policy measures that ultimately resulted in a reduction in investment in renewable energy.

Figure 5. New clean energy investment in China in billion US$, 2006–2020. Data: Compiled by authors with data from Bloomberg New Energy Finance.

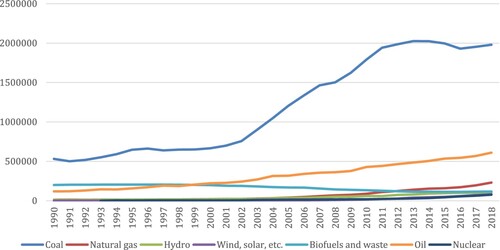

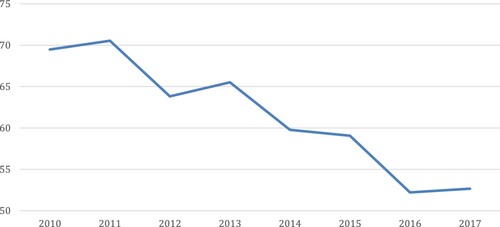

Prior to the COVID-19-related economic slowdown in 2020, there had already been signs of a renewed and increasing interest in coal in China – the world's biggest producer and consumer of coal – and policymakers had begun prioritizing low costs for power as a stimulus measure in response to overall slower economic growth, as reflected in lower coal prices and the building of new coal-fired power stations that challenged the credit guidance-deprived renewable energy sector (Hook, Citation2019). In the context of the COVID-19 crisis, stabilizing the economy became the highest political priority. Furthermore, there have been some indications of a de-prioritization of environmental protection, climate change and a transition towards cleaner energy in the face of the economic shock and pressure to stimulate the economy. Importantly, the emphasis of the central government on decarbonizing the economy – which recently culminated in President Xi Jinping's commitment for China to hit peak emissions before 2030 and achieve carbon neutrality by 2060 – stands in contrast to the determination of provincial governments to prop up growth by all means. It has been noted that in 2020, China's local governments approved plans for new coal power plant capacity at the fastest rate since 2015, and the construction of new coal power plant capacity that had been approved in the first half of 2020 exceeded the one from 2018 and 2019 combined (Hale & Hook, Citation2020). While new coal plants are used by regional and provincial governments as a means to stimulate their economies, the policy change follows a five-year period in which China tried to reduce its dependence on the heavily polluting commodity (ibid.). China's energy mix continues to be heavily dominated by coal, making up over 60% in 2018 (). The announcement in June 2020 by the PBC and others of an updated ‘Green Bonds Endorsed Projects Catalogue’, which excludes ‘clean coal’ from the universe of eligible financing projects, can be seen as an important counter-effort to dry up funding for new coal-fired powerplants.

Figure 6. Total primary energy supply (TPES) by source in kilotonnes of oil equivalent (ktoe) in China, 1990–2018. Source: IEA, World Energy Balances 2020.

Another important explanation for the phasing out of green window guidance by both the PBC and the CBRC is the increasing formalization of green finance policies and efforts to move away from controls-based towards market-based financial policy instruments. While green window guidance was partly abandoned, financial authorities introduced new policies that restricted lending to polluting industries. Importantly, the 2016 Guidelines provide a comprehensive policy framework that has the aim of mobilizing and incentivising more investment in green sectors, while restricting investment in polluting sectors. The guidelines also include greening re-lending operations by the PBC, specialized guarantee mechanisms and other measures (PBC et al., Citation2016). The implementation of the new guidelines, along with the phasing out of green window guidance targets, indicate a transition towards the formalization of green monetary policy. A greater emphasis on financial markets in financing green investments is also in line with the general shift from controls- to market-based monetary policy since the 2010s (Beggs & Deer, Citation2019).

In summary, the changes in window guidance targets are reflected by broader environmental and economic developments in China, as well as a formalization of green finance policies that have replaced direct credit allocation tools. While we are not in a position to assess the impact of green window guidance policies, the analysis shows that these were well-embedded in the changing calibration of the broader policy sphere in China along with national economic priorities.

5. Policy lessons

Direct monetary policy instruments as well as general credit controls have dominated financial policy in many developing and emerging market economies in the past. While there has been a trend towards financial liberalization over the last decades, some central banks and supervisors continue to rely on controls and direct instruments – especially when financial market development is at an early stage and does not permit the effective use of market-based instruments. In the context of implementing the Paris Agreement and promoting sustainable finance, controls-based financial policy frameworks have been extended by some to include sustainability objectives. The Chinese window guidance framework provides an example for this as it was originally introduced to control bank lending and credit growth, and to direct credit towards priority sectors, but had been augmented to also include sustainability considerations.

The Chinese use of financial controls offers several policy implications and lessons that are particularly relevant in an emerging market context where credit control instruments are utilized.Footnote4 First, the Chinese experience shows how the PBC and CBRC included window guidance as a key directed lending instrument for reallocating capital towards green economic activities. While it is difficult due a lack of data and the informal nature of the instrument to comprehensively assess the efficacy and scale of impact of green window guidance in China, our investigation shows that both the PBC and CBRC described the instrument as a central tool for the scaling up of green lending. In this context, it is important to stress that a plethora of other policies, financial guidelines and regulations have been introduced to also affect these flows over the past two decades. The timing and calibration of the instrument also reflects the broader policy developments in China that enhanced investment in renewable energy and coincided with reductions in air pollution. Window guidance, together with other investment-shaping policy measures, is featured in the policy reports as the CBRC and PBC's main contribution to the implementation of the high-level economic policy objectives of the government. As shown, the calibration of window guidance targets has been in line with the major economic, structural and environmental trends in China. The use of guidance targets to allocate credit away from heavy, energy-consuming and polluting industries occurred while China was experiencing a reduction of air pollution, which occurred in the context of targeted subsidies, an energy sector reform, and the 2015 revised Environmental Protection Law (Zhao et al., Citation2015). The abandoning of these targets in 2014 was part of a broader policy change that led to a (delayed) stagnation (or slightly increasing) of pollution from 2016 to 2017 (). The consistent emphasis on renewable energy, energy saving and the low carbon economy as a window guidance target for credit flows accompanied an unprecedented rise in new investment in clean energy that transformed China's energy mix (), and that, once the targets were abandoned, was and is correlated with a significant decline of investment in renewable energy (). Overall, the Chinese experience suggests that the calibration of window guidance reflected the broader policy developments in China and could, together with other green finance policies, have had a positive effect on greening investment and promoting specific sustainable sectors of the economy.

Figure 7. PM2.5 air pollution, mean annual exposure (micrograms per cubic meter) in China, 2005–2017. Data: Compiled with data from the World Bank.

Second, the efficacy of window guidance and other directed lending policies declines over time, proportional to the transition from bank-dominated to market-facilitated lending as the primary channel for credit flows. The experience with window guidance in Japan (Cargill et al., Citation1997; Fukumoto et al., Citation2010) shows the processes that may render this instrument less effective in the future in China. The process of financial market development and liberalization in China will arguably undermine the effectiveness of window guidance as a credit control instrument by opening up alternative channels for companies to obtain funds.Footnote5 As the financial system evolves, a system of controls needs to be supplemented with more market-based instruments. Window guidance and other directed lending tools are relatively blunt tools and may be most appropriate for central banks and supervisors who oversee less developed financial markets and have less sophisticated monetary and prudential policy frameworks. This is reflected by the use of comparable direct monetary policy instruments by other Asian central banks, including Bangladesh Bank, the State Bank of Vietnam and the Reserve Bank of India, to enhance sustainable finance (Dikau & Volz, Citation2019).

Third, when window guidance is used, it should be linked to clear criteria of success, the achievement of which should be monitored. In particular, it is vital to also monitor the impact of the instrument on the financial and, specifically, credit market, where it could potentially lead to distorting side effects if banks extend credit based on guidance targets instead of solely based on an underlying credit analysis.

Fourth, green window guidance will have to be embedded in a broader set of green finance policies (as well as climate and environmental policies). Green window guidance should be complemented, as done in China, by other tools to enhance sustainable finance. The 2016 ‘Guidelines for Establishing the Green Financial System’, outline a plethora of tools and instruments, some which have worked along window guidance for years, while others are being newly implemented. It will be necessary to adjust window guidance to the specific context and changes in financial markets as other instruments become more relevant.

Furthermore, as the international debate shows, the adjustment of central bank collateral frameworks to take climate and environmental risks or broader sustainability criteria into account can be a useful tool for central banks that rely primarily on indirect monetary policy instruments (e.g. Oustry et al., Citation2020). On the financial risk side, prudential policy and risk management tools have to play a key role in addressing and mitigating climate and environmental risks. Pricing-in these risks will also contribute to the greening of financial flows when, for example, transitions risks in assets connected to heavily polluting and/or fossil fuel industries are accounted for. The Guidelines, as described above, have a particular focus on the risk channel and include various proposals for prudential instruments as well as risk management practices of financial institutions, including for stress testing, green bond definitions and disclosure requirements.

6. Conclusions

In conclusion, our empirical investigation has revealed that both the PBC and the CBRC have extensively used window and credit guidance as an informal instrument to encourage financial institutions to structure their portfolios according to national priorities. Furthermore, this research shows that green positive guidance, as well as sustainability-enhancing negative guidance, have played a central and constant role among the comprehensive targets that are outlined by the PBC quarterly and, in the past, by the CBRC annually. With regard to negative guidance, both the PBC and the CBRC ceased their long-practiced tradition of discouraging financial institutions to lend to high-energy, high-pollution industries by 2014, while positive sustainability targets were phased-out by the PBC at the start of 2019.

Overall, our analysis of the changing nature of window guidance targets and findings on the termination of green window guidance reflect a transition in Chinese financial policy away from controls-based towards market-based instruments. The end of negative informal window guidance as well as of positive guidance coincide with the introduction of numerous formal green regulations and guidelines since at least 2010, in a process that can be interpreted as the mainstreaming of green finance policies in prudential policies.

The Chinese experience offers important lessons for central banks and supervisors in countries with less developed financial systems and strong reliance on banking lending, which may utilize or therefore even rely primarily on direct monetary policy instruments and controls. First, the Chinese experience shows how directed lending through window guidance can be framed to address the reallocation of capital towards green economic activities, even though it is difficult to isolate the effect. Second, the efficacy of window guidance and other directed lending policies is likely to diminish as financial markets mature. Third, when window guidance is used, it should be linked to clear criteria of success, the achievement of which should be monitored. Authorities should also monitor potential distorting, unwanted side effects. Fourth, green window guidance should be embedded in a broader set of green finance policies, prudential risk-focused frameworks, as well as general climate and environmental policies. Overall, the Chinese experience suggests that green window guidance can be utilized as an instrument to help align the financial system with climate and other sustainability goals, but that such policies need to be fitted to the specific context in which they are used.

Supplemental Material

Download MS Word (62.8 KB)Acknowledgements

The authors acknowledge support from the Grantham Research Institute on Climate Change and the Environment, at the London School of Economics, and the ESRC Centre for Climate Change Economics and Policy (CCCEP) (ref. ES/R009708/1). Ulrich Volz would like to acknowledge financial support provided by the UK's Economic and Social Research Council (ESRC) and the National Natural Science Foundation of China (NSFC) through the Newton Fund research project ‘Developing financial systems to support sustainable growth in China – The role of innovation, diversity and financial regulation’ (ESRC: ES/P005241/1, NSFC: 71661137002). The authors would like to thank three anonymous referees and the editors of Climate Policy for tremendously helpful comments on the manuscript, as well as participants at conferences at the Bank of Japan and the Chinese University of Hong Kong, and at the GRASFI Workshop on Climate Finance in Asia and Australasia for very helpful feedback on presentations of earlier versions of this paper.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 The CBRC was merged with the China Insurance Regulatory Commission (CIRC) in 2018 to form the China Banking and Insurance Regulatory Commission (CBIRC).

2 We differentiate between ‘market-based’ financial systems where companies principally raise finance through capital markets (bond and equity markets) and ‘bank-based’ financial systems where banks provide most financing to companies. As illustrated in Figure 4, China has a bank-based financial system.

3 Renewable energy and green transportation are responsible for the majority of the green credit in China (Choi & Heller, Citation2021; Escalante et al., Citation2020).

4 However, it is important to point out that there have also been advanced economy examples for the utilisation of window guidance, albeit usually not involving the central bank (e.g. Ohls, Citation2017).

5 However, as discussed above, there is a broader system of controls in China through which market-based financial flows could also be controlled.

References

- Aizawa, M., & Yang, C. (2010). Green credit, Green stimulus, green revolution? China’s mobilization of banks for environmental cleanup. The Journal of Environment & Development, 19(2), 119–144. https://doi.org/10.1177/1070496510371192

- Alexander, K., & Fisher, P. G. (2019). Central banking and climate change. Working Paper published by the Research Network for Sustainable Finance.

- Angrick, S., & Yoshino, N. (2020). From window guidance to interbank rates – Tracing the transition of monetary policy in Japan and China. International Journal of Central Banking, 16(3), 279–316.

- Bai, C.-E., Hsieh, C.-T., Song, Z., & Wang, X. (2020). Special deals from special investors. Becker Friedman Institute China, Working Paper, 39.

- Beggs, M., & Deer, L. (2019). Remaking monetary policy in China: Markets and controls, 1998–2008. Palgrave Macmillan.

- Bell, S., & Feng, H. (2013). The rise of the People’s Bank of China: The politics of institutional change. Harvard University Press.

- Bramall, C. (2008). Chinese economic development. Routledge. https://doi.org/10.4324/9780203890820

- Campiglio, E., Dafermos, Z., Monnin, P., Ryan-Collins, J., Schotten, G., & Tanaka, M. (2018). Climate Change challenges for central banks and financial regulators. Nature Climate Change, 8(6), 462–468. https://doi.org/10.1038/s41558-018-0175-0

- Cargill, T. F., Hutchison, M. M., & Itō, T. (1997). The Political economy of Japanese monetary policy. MIT Press.

- CBRC. (2012). Notice of the CBRC on issuing the green credit guidelines.

- Chen, H., Chen, Z., He, Z., Liu, J., & Xie, R. (2019). Pledgeability and asset prices: Evidence from the Chinese corporate bond markets. Working paper published by the National Bureau of Economic Research. https://doi.org/10.3386/w26520

- Chen, H., & Rithmire, M. (2020). The rise of the investor state: State capital in the Chinese economy. Studies in Comparative International Development, 55(3), 257–277. https://doi.org/10.1007/s12116-020-09308-3

- Choi, J., & Heller, T. (2021). The potential for scaling climate finance in China. Climate Policy Initiative. https://www.climatepolicyinitiative.org/wp-content/uploads/2021/02/The-Potential-for-Scaling-Climate-Finance-in-China-1.pdf

- Dafermos, Y., Gabor, D., Nikolaidi, M., Pawloff, A., & van Lerven, F. (2021). Greening the Eurosystem collateral framework. Report published by the New Economics Foundation.

- Day, K. A. (2005). China’s environment and the challenge of sustainable development. Routledge. https://doi.org/10.4324/9781315497693

- Dikau, S., & Volz, U. (2019). Central banking, climate change, and green finance. In J. Sachs, W. T. Woo, N. Yoshino, & F. Taghizadeh-Hesary (Eds.), Handbook of green finance (pp. 81–102). Springer.

- Dikau, S., & Volz, U. (2021). Central bank mandates, sustainability objectives and the promotion of Green finance. Ecological Economics, 184, 107022. https://doi.org/10.1016/j.ecolecon.2021.107022

- Durrani, A., Rosmin, M., & Volz, U. (2020). The role of central banks in scaling up sustainable finance – What do monetary authorities in the Asia-pacific region think? Journal of Sustainable Finance & Investment, 10(2), 92–112. https://doi.org/10.1080/20430795.2020.1715095

- Edmonds, R. L. (1998). Studies on China’s environment. The China Quarterly, 156, 725–732. https://doi.org/10.1017/S0305741000051316

- Escalante, D., Choi, J., & Larsen, M. L. (2020). Green banking in China – Emerging trends: With a spotlight on the Industrial and Commercial Bank of China (ICBC). Climate Policy Initiative. https://www.climatepolicyinitiative.org/wp-content/uploads/2020/08/Green-Banking-in-China-Emerging-Trends-1.pdf

- Fang, H., Wang, Y., & Wu, X. (2020). The collateral channel of monetary policy: Evidence from China. Working Paper published by the National Bureau of Economic Research. https://ideas.repec.org/p/pen/papers/20-008.html

- Fukumoto, T., Higashi, M., Inamura, Y., & Kimura, T. (2010). Effectiveness of window guidance and financial environment – in light of Japan’s experience of financial liberalisation and a bubble economy. Bank of Japan Review. Bank of Japan.

- Geiger, M. (2008). Instruments of monetary policy in China and their effectiveness: 1994–2006. UNCTAD Discussion Paper, 187. United Nations Conference on Trade and Development.

- Guan, D., Klasen, S., Hubacek, K., Feng, K., Liu, Z., He, K., Geng, Y., & Zhang, Q. (2014). Determinants of stagnating carbon intensity in China. Nature Climate Change, 4(11), 1017–1023. https://doi.org/10.1038/nclimate2388

- Hajer, M., & Versteeg, W. (2005). A decade of discourse analysis of environmental politics: Achievements, challenges, perspectives. Journal of Environmental Policy & Planning, 7(3), 175–184. https://doi.org/10.1080/15239080500339646

- Hale, T., & Hook, L. (2020). China expands coal plant capacity to boost post-virus economy. Financial Times. https://www.ft.com/content/cdcd8a02-81b5-48f1-a4a5-60a93a6ffa1e

- He, W. P. (2014). Banking regulation in China: The role of public and private sectors. Palgrave Macmillan.

- Ho, V. E. H. (2018). Sustainable finance & China’s Green credit reforms: A test case for bank monitoring of environmental risk. Scholarly Paper published by the Social Science Research Network, No. ID 3124304. https://doi.org/10.2139/ssrn.3124304

- Hook, L. (2019). Climate change: How China moved from leader to laggard. Financial Times. https://www.ft.com/content/be1250c6-0c4d-11ea-b2d6-9bf4d1957a67

- Hook, L., & Hornby, L. (2018). China’s solar desire dims. Financial Times. https://www.ft.com/content/985341f4-6a57-11e8-8cf3-0c230fa67aec

- IISD. (2015). Greening China’s financial system. Report published by the International Institute for Sustainable Development. https://www.iisd.org/system/files/publications/greening-chinas-financial-system.pdf

- Ma, J., & Spencer, M. (2004). China: Selective tightening and soft-landing. Deutsche Bank Global Markets Research, Emerging Markets.

- Macaire, C., & Naef, A. (2021). Impact of Green Central Bank collateral policy: Evidence from the People’s Bank of China. Working Paper #812 published by the Banque de France. https://publications.banque-france.fr/sites/default/files/medias/documents/wp812.pdf

- Matikainen, S., Campiglio, E., & Zenghelis, D. (2017). The climate impact of quantitative easing. Grantham Research Institute on Climate Change and the Environment, London School of Economics and Political Science. https://www.lse.ac.uk/granthaminstitute/wp- content/uploads/2017/05/ClimateImpactQuantEasing_Matikainen-et-al-1.pdf

- NGFS. (2019). A call for action. Climate change as a source of financial risk. First comprehensive report. Network for Greening the Financial System, Banque de France. https://www.ngfs.net/sites/default/files/medias/documents/ngfs_first_comprehensive_report_-_17042019_0.pdf

- Ohls, J. (2017). Moral suasion in regional government bond markets. Bundesbank Discussion Paper, 33/2017. Bundesbank. https://ssrn.com/abstract=3083988

- Oustry, A., Erkan, B., Svartzman, R., & Weber, P.-F. (2020). Climate-related risks and Central Banks’ collateral policy: A methodological experiment. Banque de France Working Paper, 790. Banque de France. https://publications.banque-france.fr/en/climate-related-risks-and-central-banks-collateral-policy- methodological-experiment

- PBC. (2015). China green bond endorsed project catalogue (2015 edition). Peoples Bank of China, Green Finance Committee of China Society for Finance and Banking.

- PBC. (2016). The People’s Bank of China annual report 2015.

- PBC, MOF, NDRC, MEP, CBRC, CSRC & CIRC. (2016). Guidelines for establishing the green financial system.

- Pearson, M., Rithmire, M., & Tsai, K. S. (2020). Party-state capitalism in China. Harvard Business School, Working Paper 21-065, 47.

- Petry, J. (2020). Financialization with Chinese characteristics? Exchanges, control and capital markets in authoritarian capitalism. Economy and Society, 49(2), 213–238. https://doi.org/10.1080/03085147.2020.1718913

- Qiu, J. (2011). China unveils green targets. Nature, 471(7337), 149–149. https://doi.org/10.1038/471149a

- Rhodes, J. R., & Yoshino, N. (1999). Window guidance by the Bank of Japan: Was lending controlled? Contemporary Economic Policy, 17(2), 166–176. https://doi.org/10.1111/j.1465-7287.1999.tb00672.x

- Robins, N., Dikau, S., & Volz, U. (2021). Net-zero central banking: A new phase in greening the financial system. Grantham Research Institute on Climate Change and the Environment and Centre for Climate Change Economics and Policy, London School of Economics and Political Science, and Centre for Sustainable Finance, SOAS, University of London. https://www.lse.ac.uk/granthaminstitute/wp-content/uploads/2021/03/Net-zero-central-banking.pdf

- Schoenmaker, D. (2021). Greening monetary policy. Climate Policy, 21(4), 581–592. https://doi.org/10.1080/14693062.2020.1868392

- Setyowati, A. B. (2023). Governing sustainable finance: Insights from Indonesia. Climate Policy, 23(1), 108–121. https://doi.org/10.1080/14693062.2020.1858741

- Shen, B., Wang, J., Li, M., Li, J., Price, L., & Zeng, L. (2013). China’s approaches to financing sustainable development: Policies, practices, and issues. Wiley Interdisciplinary Reviews: Energy and Environment, 2(2), 178–198. https://doi.org/10.1002/wene.66

- Tavory, I., & Timmermans, S. (2014). Abductive analysis: Theorizing qualitative research. University of Chicago Press.

- Tobin, D., & Volz, U. (2019). The development and transformation of the financial system in the People’s Republic of China. In U. Volz, P. J. Morgan, & N. Yoshino (Eds.), Routledge handbook of banking and finance in Asia (pp. 15–38). Routledge.

- Van ’t Klooster, J., & van Tilburg, R. (2020). Targeting a sustainable recovery with green TLTROs (preprint). Positive Money. https://doi.org/10.31235/osf.io/2bx8h

- Volz, U. (2017). On the role of central banks in enhancing green finance. Inquiry Working Paper, 17/01. UN Environment Inquiry into the Design of a Sustainable Financial System.

- Volz, U. (2019). Fostering green finance for sustainable development in Asia. In U. Volz, P. J. Morgan, & N. Yoshino (Eds.), Routledge handbook of banking and finance in Asia (pp. 488–504). Routledge.

- Wang, Y. (2018). China’s green finance strategy: Much achieved, further to go. Sustainable Finance Leadership Series, Grantham Research Institute on Climate Change and the Environment, London School of Economics and Political Science.

- World Bank. (1997). Clear water, blue Sky.

- World Bank. (2001). China – Air, land, water.

- World Bank. (2007). Costs of pollution in China.

- Zadek, S., & Chenghui, Z. (2014). Greening China’s financial system – An initial exploration. International Institute for Sustainable Development (IISD) and the Development Research Center of the State Council.

- Zhao, X., Yin, H., & Zhao, Y. (2015). Impact of environmental regulations on the efficiency and CO2 emissions of power plants in China. Applied Energy, 149, 238–247. https://doi.org/10.1016/j.apenergy.2015.03.112