ABSTRACT

The extensive use of fossil fuels in recent decades is a well-known cause of the climate crisis. Climate action inevitably requires the strategic reorientation of industries that are part of the fossil fuel regime. International oil companies are central to this regime and possess the incumbent’s characteristic power and influence to steer this process. However, European international oil companies continue to invest in fossil fuels, even as they acknowledge the climate crisis imperative. Socio-political and economic dynamics can either reinforce the oil regime or pressure firms to take climate action. We aim to comprehensively analyse the dynamics between external socio-political and economic actors’ pressures to climate action on the one side, and the industry response on the other, from 2005 to 2019, using Geels Triple Embeddedness Framework. Drawing on a wide range of qualitative and quantitative longitudinal data (e.g. regulations, oil and renewables market trends, companies’ investments in oil, renewables, and low-carbon technologies), we characterised the pressures and responses of the different analytical categories and established three phases. The results indicate that policy pressure on the oil regime in this period lacked constancy and comprehensiveness. The Kyoto Protocol ratification produced an initial momentum that prompted some companies to invest in alternative fuels and renewables, but efforts faded after 2010. Societal calls for a transition from fossil fuels and divestments from oil companies have risen since 2017. Recent socio-economic pressures combined with policy pledges for net-zero emissions have prompted all companies to invest beyond fossil fuels. However, efforts are still marginal and additional advancements in climate policy are necessary to foster the renewables market and to promote the phase-out of oil.

Key policy insights

Europe lacks a comprehensive policy framework to support the fast deployment of available alternative fuels.

Policies need to foster the development and adoption of alternatives to petrochemical products, alongside their reduction and recycling.

Apart from supporting renewable energy and other alternatives to oil, policies also need to target the phase-out of oil and send a clear signal to companies.

1. Introduction

Limiting carbon emissions and avoiding temperature rises greater than 2°C requires phasing out fossil fuels (Rogelj et al., Citation2018). Achieving this transition inevitably demands the recreation of economic activities and social habits that have been shaped by fossil fuels (Seto et al., Citation2016; Unruh, Citation2000). International Oil Companies (IOCs) are key players in the fossil fuel regime and their decisions can have a global impact on climate mitigation efforts. IOCs possess the power and influence characteristics of incumbents: They can not only sustain and prolong the current regime, but they can also produce disruptive innovation across the industry (Turnheim & Sovacool, Citation2020; van Mossel et al., Citation2018).

How these influential companies proceed on climate depends on multiple internal and external factors (Geels & Schot, Citation2007). Companies need to transition from fossil fuels to fulfil the Paris Agreement promise of a climate-neutral world by mid-century. Previous studies have analysed oil companies’ response to climate change (Ferns et al., Citation2019; Mäkitie et al., Citation2019; Steen & Weaver, Citation2017; van den Hove et al., Citation2002), but the role of coordinated pressure from social, political, and economic actors has not been comprehensively considered (Kungl & Geels, Citation2018). Others have mapped policy developments to limit fossil fuel exploration (Gaulin & Le Billon, Citation2020; Gençsü et al., Citation2020), but without considering their impact on industry practices.

Climate, energy, and mobility policies play a crucial role in fostering the re-orientation and decision processes of IOCs. However, it is also important to understand how societies and markets evolve to fully grasp the forces of motivation and resistance towards transition (Geels & Penna, Citation2015; Kivimaa et al., Citation2021). We seek to contribute to the existing literature by comprehensively analysing the dynamics between socio-political and economic pressures and the industry response from 2005 to 2019. Comparing European IOCs’ investments against the external environment will bolster understanding about the limitations of climate policy and how to better galvanise companies’ transition from oil. Additionally, we intend to identify if the content or sequence of external pressure might have driven the kind of responses adopted by IOCs (Kungl & Geels, Citation2018).

We chose to analyse European IOCs due to their proactive discourse in improving their environmental performance (Dietz et al., Citation2020; Ferns et al., Citation2019). Some European IOCs – like Shell, BP, and Total – diversified their portfolios in the 2000s to include renewable energy and less carbon-intensive fuels. Recently, a growing number of European IOCs have also developed decarbonisation strategies to respond to climate policy pledges of net-zero emissions by 2050 (Lu et al., Citation2019). However, different pathways exist for net-zero emissions and not all align with sustainability goals. European IOCs have long abandoned the role of climate change deniers (van den Hove et al., Citation2002), but it remains unclear to what extent they have shifted their trajectory and what has spurred it (Mäkitie et al., Citation2019). Following this introduction, we present the Geels Triple Embeddedness Framework (Geels, Citation2014) and describe how we operationalise the analysis. The subsequent sections discuss our results and their policy implications.

2. Method

2.1. Conceptual framework

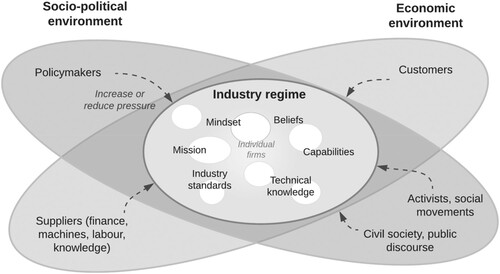

The triple embeddedness framework (TEF) developed by Geels (Citation2014) is used here to systematically analyse policy, social, and economic pressures to climate action in the oil sector and the responses they provoked from European IOCs. The TEF uses evolutionary economics, neo-institutional theory, and economic sociology to conceptualise how firms-in-industries co-evolve with their external environment. The TEF structure encompasses the industry regime (comprised of different firms), which exists in an external environment divided into the socio-political and the economic (task) environment (see ). In transitions theory, technological innovation is often treated as the main source of industry disruption; however, socio-political and economic environments feature many different actors that can also disrupt regimes and stimulate transitions (Kivimaa et al., Citation2021).

Figure 1. Conceptual framework (adapted from Geels (Citation2014)).

Geels (Citation2014) emphasises that, despite the existence of an industry regime, firms-in-industries might present different behaviours. It can take a long time to align external pressures to prompt a transition; in the meantime, the ambiguous socio-political and economy context can trigger different responses from firms (Kungl & Geels, Citation2018). As such, industry regime actors can adopt strategies that range from resisting to maintaining their core activities, to completely reinventing their business models (Geels, Citation2014; Turnheim & Sovacool, Citation2020). However, studies using the TEF framework have mostly reported uniform behaviour from firms-in-industries (Brauers & Oei, Citation2020; Kungl & Geels, Citation2018; Mühlemeier, Citation2019).

The TEF framework has been used in previous literature to analyse the transition of national energy sectors, such as the phase-out of coal in Poland (Brauers & Oei, Citation2020), Switzerland (Mühlemeier, Citation2019) and Germany (Kungl & Geels, Citation2018; Mühlemeier, Citation2019). It is also suitable for studying the oil industry regime (Geels, Citation2014). The value of the TEF for empirical research is its ability to incorporate the bidirectionality of relationships between the actors in a regime and its external environment into a longitudinal and multidimensional approach (Brauers & Oei, Citation2020; Geels, Citation2014).

2.2. Research design and case selection

The analysis looked at two dimensions: external actors’ pressure on IOCs for climate action and climate action responses from IOCs. The time frame used to capture the changes was from 2005 until 2019. We chose 2005 as the starting point due to key political developments in that year. The Kyoto Protocol, which entered into force in 2005, was the first attempt under the United Nations Framework Convention on Climate Change (UNFCCC) to get countries to commit to targets for greenhouse gases (GHG) emissions mitigation. That same year, the European Union Emissions Trading System (EU ETS) was launched and established emissions reduction targets for many sectors and industries; this included only downstream activities of oil companies (Verbruggen et al., Citation2019). Therefore, we would expect IOCs’ responses to start to emerge after 2005.

The analysis here seeks to characterise and synthesise the IOCs individual response. We consider 12 private European companies, working both downstream and upstream, that are listed in the S&P Global Platts 2020 ranking of the world’s 250 largest energy companies (). European IOCs are recognised for having a proactive climate action discourse and many have recently developed net-zero emissions strategies (Dietz et al., Citation2020; Ferns et al., Citation2019; Lu et al., Citation2019). Although most major European IOCs operate worldwide, previous studies have argued that their distinct behaviour might also be related to the socio-political context in which they operate (Levy & Kolk, Citation2002).

Table 1. Major European IOCs included in the analysis.

2.3. Data collection and analysis

presents the aspects considered for data collection, which is organised around different categories of TEF actors. The TEF offers guidance on the kinds of developments that one should look for when elaborating on actors’ influence, but the choice is not free of some level of subjectivity. In this analysis, we use a mix of qualitative and quantitative data to generate a comprehensive picture; a full list of the documents is available in Appendix A.

Table 2. Data types and sources used in the analysis.

The analysis of the socio-political pressures focused on constructing a timeline of international and European developments in policymaking (regulations, directives, and binding targets) related to climate, energy, and mobility. Additionally, we explored the Nexis Uni database for social trends in European news. Our searches combined the keywords ‘fossil fuels’ and ‘oil industry’ with the terms ‘activism’ (213 returns), ‘divestment’ (4.503 returns), and ‘transition’ (37.371 returns). The searches allowed us to capture the emergence of social movements against the oil industry. A final parameter considered the number of European parliament seats held by the Green Party. The presence of green parties approximates the importance that society assigns to environmental issues (Hartmann et al., Citation2021).

We analysed the economic environment using quantitative data on market trends for oil and renewables, primarily seeking to identify the transitional status of oil. We calculated the z-score of each variable to normalise all the numerical indicators and facilitate comparison (Mäkitie et al., Citation2019). The z-score is a numerical measurement that describes a value's relationship to the mean of a group of values. We also considered reports from IEA on the European oil sector (IEA, 2014; 2018; 2020).

We formulated the oil regime response by calculating the average values of each parameter using IOCs’ individual data. We also observed developments from industry associations’ climate change initiatives, specifically from industry association IPIECA and the Oil and Gas Climate Initiative (OGCI). IOCs’ quantitative data were retrieved from the Refinitiv databaseFootnote1; missing data were complemented with annual reports from the analysed period (173 documents), which also helped map changes in strategic orientation and decarbonisation efforts. Annual reports are reliable sources of information on organisational developments and strategic plans (Hartmann et al., Citation2021).

We analysed the annual reports using the software NVivo 11. We coded annual reports segments referring to renewable energy, climate change, or GHG emissions mitigation in the mission statement and letters of the CEO, chairman or directors. These codes were used to analyse the evolution of companies’ strategic orientation over the years. Engagement incidents with renewables and low-carbon technologies were collected using the NVivo text search function. Such engagement incidents included R&D projects, acquisitions, joint ventures, partnerships, construction of facilities, and patent registrations. We did individual searches of engagement incidents using the keywords renewable, solar, wind, biofuels, hydrogen, and carbon capture and storage (CCS) to identify engagement incidents that were then coded in respective nodes. Generic mentions of adopting or intending to develop a particular technology were not considered concrete developments. The nodes of different kinds of engagement incidents were later revised to exclude multiple mentions, resulting in a total of 330 incidents. As a final step, we analysed the GHG emission reduction targets of companies’ decarbonisation strategies.

Building on these data, we divided the analysed period into different phases. We used a timeline to organise the pressures and responses found in the different analytical categories of the TEF (socio-political and economic environments and industry regime). The quantitative data time-series allowed us to identify turning points in the trends considered for socio-political, economic, and industry regime actors. The turning points were placed in sequence in the timeline and complemented with identified developments and events (e.g. directives, social movements). The contrast of the developments in the two external – socio-political and economic environment – dimensions and the IOCs highlighted the alignment of pressures and responses or the lack thereof, allowing the establishment of three response phases. We acknowledge that this procedure inevitably requires interpretation and thus introduces a degree of subjectivity. As such, other analysts would perhaps divide the period differently.

3. Results

The results of our analysis are presented in four sub-sections below. First, we describe European and international climate policy developments that could prompt IOCs’ responses to climate change. Second, we also consider the emergence of social movements and political interest in green parties, which signal social pressure. Third, we evaluate economic pressures by analysing market developments related to oil and renewables. The final section analyses IOCs’ response to the external pressures by considering their strategic orientation, investments in renewables and oil, and efforts to mitigate GHG emissions.

3.1. The socio-political environment of European IOCs

Socio-political environments include the evolution of international and European policy and societal developments, all of which can impact industry and firm behaviours. presents a timeline containing the main policy developments and key instruments related to IOCs.

Table 3. Developments in international and European policymaking from 2005 to 2019 relevant to the oil industry.

The ratification of the Kyoto Protocol in 2005, alongside a favourable political environment in the EU, spurred a series of climate-related policies. That same year, the EU ETS was launched as a first attempt to reduce industry emissions. However, the ETS classified oil industry activities as exposed to carbon leakage, which entitled companies to free emissions allowances. The first European Climate & Energy package was agreed upon after Kyoto and established targets for 2020 that could impact the oil industry. The 2009 Renewable Energy Directive was a key development from the package and included a 10% target of renewable energy sources in transport. The Fuel Quality Directive was also launched in 2009. It introduced the binding target of GHG intensity reduction to 6% in transport fuels by 2020 (compared to a 2010 baseline). Granted, the policy gave fuel suppliers room to choose their preferred mitigation strategy. Possible avenues mentioned were biofuels, electric vehicle credits, upstream emissions reduction, or the use of other alternative fuels. Nonetheless, the two policies combined made investments in biofuels the most convenient. However, many studies have largely contested the actual ability of first-generation biofuels to reduce emissions, leading the technology to lose public and political support in the years that followed (Cadillo-Benalcazar et al., Citation2021; Puricelli et al., Citation2021).

The first policy incentives for CCS came during the same period, roughly in 2009. The Directive 2009/31/EC established a legal framework for the environmentally safe geological storage of CO2. The New Entrants Reserve 300 programme (NER 300) was also designed in 2010 to fund eight diverse demonstration projects in CCS; however, the EU ETS’ low carbon prices produced little interest in the technology (IEA, 2014; Reiner, Citation2016). The low support among the EU Member States has limited CCS development in the European context, with only one CCS pilot project having received funding (European Commission, Citation2021; Reiner, Citation2016). International organisations have provided a more supportive setting for CCS: The IEA has advocated for CCS, and IPCC scenarios since 2014 have included the technology as a possible avenue for achieving necessary deep reductions in emissions to meet ambitious climate goals (Minx et al., Citation2018; Reiner, Citation2016). Thanks to the legitimacy conferred by organisations like the IEA and the IPCC, CCS has garnered attention in decarbonisation strategies adopted by IOCs (Minx et al., Citation2018).

Initial pressure to take climate action in 2009 wavered in the years that immediately followed. European regulators’ belief in peak oil and the transition to renewables was replaced by a rise in the price of electricity, the Euro monetary crisis, and the emergence of technologies that favoured the fossil fuel industry (e.g. fracking and CCS) (Bürgin, Citation2015; Helm, Citation2014). The 2009 COP in Copenhagen and the 2011 COP in Durban also revealed a lack of international consensus and most nations neglected to follow the relatively strong European climate mitigation efforts; additionally, many nations allowed increased fossil fuel exploration along with the introduction of fracking and shale gas production (Bürgin, Citation2015; Helm, Citation2014). This impacted the European political debate, with cost-effectiveness concerns overtaking the vision of becoming an international leader in climate policy. The unfavourable context for climate action influenced the EU’s 2030 Climate and Energy Policy drafting process. No additional binding targets for the transport sector were undertaken, loosening some pressure on the IOCs. The Commission justified this choice with the weakly evidenced claim that available first-generation biofuels could contribute to decarbonising the transport sector. However, investments in biofuels were only one of the possible avenues for increasing the use of renewable energy in transport. Another similar policy that failed was the 2014 Alternative Fuels Infrastructure Directive, which required the EU Member States to devise the frameworks for developing the market for alternative fuels and energy sources and their associated infrastructure by 2025. Most Member States adopted targets that were inadequate for creating a viable network of recharging points and alternative fuel stations.

The adoption and ratification of the Paris Agreement (2015-2016) renewed the political and societal support for climate action in the EU. The number of news articles related to transition and divestment from fossil fuels in the Nexis Uni database increased by 70% after 2015. The Commission decided to restore the binding target for renewable sources in transport when adopting the 2018 Renewable Energy Directive. The target was increased to a 14% share of renewable fuels in transport by 2030, from which at least 3.5% is to be from advanced biofuels. The 2018 IPCC Report Global Warming of 1.5°C also reinforced the urgency of mitigating GHG emissions. The same year saw the emergence of social movements calling for climate action against the fossil fuel industry like Extinction Rebellion and the youth movement through Fridays for Future. Fridays for Future, and its founder Greta Thunberg, achieved worldwide attention; their constant presence in the news reinforced the urgency of the climate emergency. Pearson and Rüdig (Citation2020) describe how Fridays for Future’s school strikes across Europe might have impacted the results of elections: Green parties in 11 countries achieved double-digit votes in 2018, which signalled the growing importance of environmental issues for political agendas (Pearson & Rüdig, Citation2020). The EU Green Party also had a record increase in its number of seats in the European Parliament—from 52 to 74 in the 2019 election. This transformation of the socio-political environment culminated with the launch of the European Green Deal in December 2019, which sets Europe up to be the first climate-neutral continent by 2050.

3.2. The economic environment of IOCs

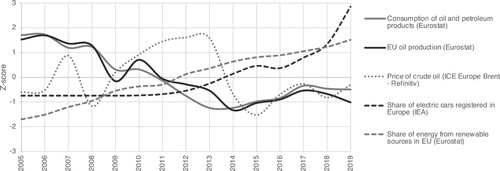

IOCs’ economic environment is characterised by two relevant trends: the European production and consumption of oil and petroleum products, and the expansion of renewable energy (). Comparing oil and renewable energy indicators reveals how much energy providers, producers and consumers responded to calls for transition. The peak in European oil consumption occurred in 2004 and faced a consistent decline until 2014. The drop in European oil demand and increased competition from the Middle East, Asia and the United States exerted significant economic pressure on the sector; as a result, fifteen European refineries shut down between 2008 and 2014 (IEA, 2014). Production levels also declined and dependence on crude oil imports peaked in 2015 with a share of 96,7% (Eurostat, 2021). Renewable energy experienced steady growth in Europe during the analysed period and accounted for 19% of European primary energy sources in 2019, but did not necessarily replace oil products. shows that oil consumption has increased in Europe since 2013 thanks to the transport sector—the sole major economic sector that has increased its emissions since the adoption of climate policy goals (EEA, Citation2021).

Figure 2. The evolution of the economic (task) environment (2005–2019).

During the analysed period, consumers exerted negligible economic pressure on IOCs, primarily due to a lack of alternatives for personal mobility. The expansion of electric cars after 2017 is one source of market pressure that represented 3% of European cars in 2019. Coming decades may see personal vehicles shift from combustion engines to electric ones, but similar alternatives are not yet readily available for other transport segments. Navigation, aviation and freight transport still require further development to adopt alternative fuels or electricity-based solutions (Bouman et al., Citation2017; Staples et al., Citation2018). Associations from the maritime and aviation sectors have moved to increase the efficiency of vessels and aeroplanes and are experimenting with alternative fuels. However, the decarbonisation of the transport sector in the analysed period was not expressive, and there is still a need for much more infrastructure and technological development. Beyond this, IOCs also have other growing markets for oil, such as petrochemical products (IEA, 2018).

Meanwhile, IOCs have mainly experienced economic pressure through the divestment movement, with 350.org as a pioneer (Ayling and Gunningham, 2017; Gaulin & Le Billon, Citation2020). Due to societal backlash, several universities became the first institutions to divest from fossil fuel companies. Many pension funds, religious organisations, financial institutions, and public bodies have followed suit (Ayling and Gunningham, 2017). Although the divestment movement first emerged as an ideological choice, its expansion after 2015 was mainly driven by financial choices. Mainstream investment portfolios started in this period to recognise renewables as an attractive economic choice. In 2017, for instance, key investor initiatives like Transition Pathway and Climate Action 100 + were founded. A joint report by IEA and Imperial College produced evidence that stock market portfolios featuring renewables in the German and French markets returned 171% against a −25% loss from fossil fuels between 2010 and 2019 (Donovan et al., Citation2020). Plantinga and Scholtens (Citation2021) also found that divestment is financially attractive, even in a market where fossil fuels will continue to lead the energy mix for some time. Despite the evidence regarding renewables’ positive performance, globally most investments were allocated to fossil fuels in 2019 (Donovan et al., Citation2020). However, this trend could reverse soon. For example, the European Investment Bank took steps in 2019 to end financial support to fossil fuel energy projects from 2022 (EIB, 2019).

3.3. The incumbents’ decarbonisation efforts

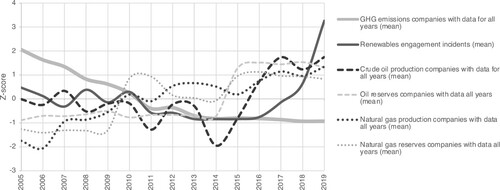

IOCs were first confronted with climate change in the 1980s, but scientific evidence was still mounting and companies downplayed the threat (van den Hove et al., Citation2002). By the time of Kyoto’s ratification, IOCs faced a completely different external environment that recognised an undeniable need to act on climate change. However, not all European IOCs started a fruitful journey towards decarbonisation after 2005. exposes three trends that are relevant for understanding companies’ response to climate change: oil production and reserves, GHG emissions, and engagement incidents with renewables (wind, solar, biofuels, and hydrogen). Analysed IOCs presented some level of action after 2005 by reducing GHG emissions (Scope 1) or engaging with renewables. However, all IOCs halted renewable energy engagement incidents by 2011 and their direct GHG emissions saw no significant drop after 2013. The increase in oil production and reserves after 2014 cemented the weakening of decarbonisation efforts. The expansion of oil production and reserves is not surprising, since IOCs’ annual reports consistently stated their belief that following decades would see a growing demand for fossil fuels.

Figure 3. The IOCs response to decarbonisation.

By 2019, all analysed IOCs had committed to GHG emission reductions in their annual reports. Many of the IOCs are members of the OGCI, an industry-led coalition of partners created in 2014 to focus on sectoral mitigation (OGCI, 2021). IPIECA, one of the most influential industry associations, also expressed their commitment to climate mitigation at COP21 in 2015 (Bach, 2017). Further, in 2020, nine of the IOCs announced net-zero emission targets for the upcoming decades. Many IOCs, including nine companies analysed here, have also declared the goal of transitioning into a low-carbon energy business. Despite these commitments, the data indicate that companies have produced marginal reductions in direct GHG emissions since 2013, with six of the twelve companies not producing reductions at all. This lack of abatement performance undermines the credibility and feasibility of net-zero targets.

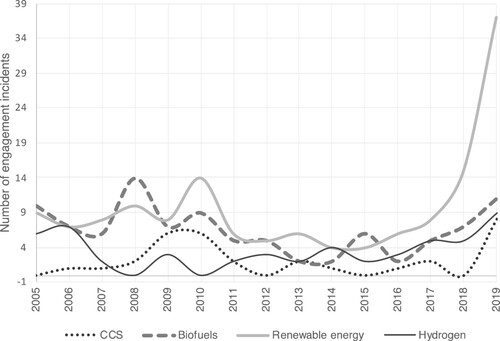

A detailed analysis of historical engagement incidents with alternative fuels, CCS, and renewable energy sources, also depicts that the engagement with low-carbon technologies has not been consistent (). Engagements with alternative fuels mainly occurred with biofuels, which reached their peak in 2008. The uncertainties surrounding the technology impacted IOCs’ engagements, which only resumed growth after 2017 with the development of second-generation biofuels. Engagement incidents with hydrogen only increased after 2016.

Figure 4. IOCs’ engagement incidents with renewables, low-carbon fuels, and CCS.

IOCs have consistently positioned CCS in geological reservoirs as a feasible solution for mitigating GHG emissions. The industry association IPIECA has supported the technology since 2003 and the OGCI has lobbied for political support to CCS (IPIECA, 2003). However, there was no consistent investment in the technology. Some pilot projects occurred between 2009 and 2010, but it took until 2019 for six IOCs to announce a new batch of demonstration projects. The most considerable controversy of CCS is that projects are only financially viable if there are high carbon prices (Reiner, Citation2016). Adopting CCS as the primary reduction strategy brings significant risks (Smith et al., 2016). Furthermore, the mitigation potential that IOCs attribute to the technology exceeds the actual potential given the development and deployment that it still requires (Reiner, Citation2016).

Renewable energy from solar and wind encompasses most IOCs engagement incidents, but IOCs support for the technologies was not constant. Initial efforts to support renewables came from BP, Shell and Total. BP exited the solar market in 2013 but decided to retain its wind business after initially considering a sale. Most incumbent actors also refrained from investments in renewables between 2011 and 2016. That trend reversed in 2017 as all companies reached unprecedented levels of engagement. It is still unknown if the rise in investments is another fad or if conditions will allow the technology to become IOCs’ preferred investment over fossil fuels.

3.4. Discussion: the dynamics between external pressures and the IOCs decarbonisation efforts

When looking at developments in socio-political and economic environments alongside IOCs’ climate actions, it is apparent that external pressure coincides with companies’ levels of action. We divided the studied period into three phases—the main events of each are listed in . Phase 1, from 2005 to 2010, is marked by the pressure from initial regulations around reducing GHG emissions and the resultant efforts from IOCs. However, a lack of continued policy pressure led companies to reduce their efforts. This stagnation characterises Phase 2, covering 2011 until 2016. Pressure from all analysed actors emerged in Phase 3 (2017–2019) and IOCs responded with the promise of a transition.

Table 4. Dynamics between the external environment and IOCs (additional pressure and climate action – green, reduction of pressure and climate action – red).

We call Phase 1 (2005–2010) ‘The Kyoto Effect’ because the political environment created by the treaty resulted in a series of EU climate policies. The pressure produced by policymakers prompted diversification in seven IOCs, but the five other incumbents had no or minimal engagement with renewables in the period. The existence of mixed signals created an ambiguous context where not all companies saw the need to act. The political setting in the period was enough motive for some companies to start diversifying their business to markets beyond oil; however, the lack of civil society pressure or available technological alternatives to combustion engines made other companies strengthen their fossil fuel dependence beliefs. Companies tend to prioritise different kinds of information according to previous experiences and manager beliefs or mindsets (Kungl & Geels, Citation2018; Pfeffer & Salancik, Citation2003). In a context that lacks significant market pressure, only a robust policy framework would make re-orientation an attractive course of action (Steen & Weaver, Citation2017).

The policies in place during Phase 1 focused on increasing efficiency and were unlikely to produce something beyond incremental change. The first targets for renewable sources in transport resulted in a limited response of drop-in biofuels. First-generation biofuels were an inadequate alternative for reducing emissions, and investments in the technology produced a false sense of progress towards sustainability. Biofuels still account for most renewable sources in transport (IEA, 2020), highlighting the meagre progress in developing other alternatives. Regulations like the Renewable Energy Directive and Fuel Quality Directive were fundamental to stimulating IOCs’ search for alternatives; however, when the limits of biofuels became clear, there was inadequate support to encourage other investments. Policies have failed to create a stable market for alternative fuels that could spur divestment from oil.

The favourable economic environment for fossil fuels and lack of solid policy incentives for renewables made most IOCs retreat from diversification during Phase 2 (2011-2016), referred to as ‘Back to business as usual’. Most companies ignored renewable energy, biofuels, or hydrogen; likewise, they presented marginal emissions reductions. The lack of social-political pressure on climate action aligned with an emphasis on economic recovery among IOCs. Facing diminished external pressure, IOCs strengthened their core business in fossil fuels rather than shifting to new business activities or sectors. The need for economic recovery might also have resulted in what Kungl and Geels (Citation2018) refer to as the ‘masking effect’, which occurs when an immediate and obvious pressure leads to an underestimation of underlying trends. In this case, the concern with an economic recovery masked the need to tackle climate change.

Phase 3 (2017-2019) presents alignment of pressure from the full range of different external environment actors, a phase that we call ‘Has the transition arrived?’. Increased societal awareness of climate change, the consolidation of fossil fuel divestment as an ethical and economically favourable choice, and the EU’s adoption of the net-zero emissions target by 2050 created an external environment that demanded IOCs’ climate response. Most companies have elaborated decarbonisation strategies for their operations, and some are even calling themselves energy companies rather than oil companies. However, IOCs’ responses should be approached with caution because the policy framework in this Phase still leaves room for expansion in oil exploration and our economies remain carbon-dependent. Moreover, the announcement of such strategies resembles IOCs’ old greenwashing strategies (van den Hove et al., Citation2002), and, importantly, our findings show that they still invest in fossil fuels. The IOCs corporate mindset is that market segments like navigation, aviation, and petrochemicals, will still need fossil fuels in the following decades. Technological developments are indeed necessary for those segments to transition, but the direction of these should not be left to IOCs. A transition from fossil fuels will inevitably create a short-term loss of profit for these companies; to ease that transition, governments need to take an active role with policy and finance (Plantinga & Scholtens, Citation2021). The scenario found in this last Phase resonates with the argument that if climate policy aims to produce a transition from fossil fuels, policies need to target the phase-out of oil in addition to increasing incentives for renewables (York & Bell, Citation2019).

The analysis presented in this study also features some limitations, and suggestions for future studies can be made. First, the boundaries of analysis could be modified by expanding the external environment beyond the European context or going deeper at the company level. On the one hand, a company-level analysis could shed light on what kinds of decarbonisation strategies are more suitable and assist in elaborating more specific policy advice. On the other hand, expanding the boundary of analysis could assist in identifying trends from markets other than Europe that IOCs might have considered when evaluating economic pressures. Secondly, apart from the IOCs considered in our analysis, many other players comprise the European oil regime. Future studies can examine those different sectoral players to uncover parallels in companies’ responses to calls for climate action. The findings discussed here also cannot be generalised. European IOCs operate in a context where a bottom-up culture enables civil society to influence policies. Different dynamics between external pressures and the IOCs regime may appear when considering other localities with large oil reserves like Saudi Arabia. Finally, the current lack of available data and indicators on IOCs’ renewable assets, for example, limited our analysis, making it impossible to accurately estimate the proportion of investments in fossil fuels and renewables.

4. Conclusion

This article analysed the dynamics between socio-political and economic pressures and the European oil sector response from 2005 to 2019. The analysis hints at how policy can encourage decarbonisation efforts within the sector and, ultimately, spur a transition from oil. Overall, the pressures on IOCs to take climate action were insufficient and lacked sequence to bring about a significant transition away from fossil fuel investment towards green energy. These missteps allowed companies to make incremental changes and ensured the stability of the old oil regime. During most of the analysed period, policies were the main source of pressure, but after 2017, economic and socio-political pressures also increased. The alignment of different external environmental actors was crucial to pushing IOCs to invest in new technologies. This contextual setting must persist to ensure companies’ transition to new markets. Climate policy can play a crucial role here by adopting stricter regulations to mitigate emissions from IOCs productive activities and by supporting a transition away from oil.

European climate policy needs to include more effective regulations to ensure the mitigation of GHG emissions from IOCs’ direct operations but also across its supply chain. The EU ETS’ provision of free emissions allowances to oil refining activities might have prevented carbon leakage, but it likely reduced the pressure on IOCs to mitigate emissions. All of the studied IOCs presented minimal direct GHG emissions reductions after 2013. However, eight IOCs have established decarbonisation strategies in 2020 that predict the achievement of net-zero emissions by 2050. Any future allocation of free emissions allowances should consider the technological developments in the sector to avoid slowing down the decarbonisation process. Even if mitigating emissions is essential, a transition from oil is the end goal. The advancement of supply-side policies for fossil fuels is another step required to ensure net-zero emissions by 2050. Policymakers can look at the case of asbestos or chlorofluorocarbons for precedents in the implementation of such measures.

The first issue that policies can target is the expansion of alternative fuels and their required infrastructure. Almost all oil consumed in Europe comes from imports; therefore, increasing the share of renewable fuel sources is also a matter of energy security. Our study reveals that biofuels were IOCs’ main avenue for increasing renewable sources. However, other alternatives are already available in the market and just need to have their deployment accelerated. IOCs are currently investing marginally in recharging points, but deploying such infrastructure cannot be left to IOCs’ alone given their market interests.

The consumption of motor fuels will likely drop with the expansion of electric vehicles and the incorporation of alternative fuels in sectors such as aviation and maritime. However, the IEA warns that replacements for petrochemical products like fertilisers, plastics, and rubbers are still greatly underdeveloped (IEA, 2018). Efforts to ban single-use plastics and adopt circular practices when developing packages and equipment can reduce the future demand for plastics. However, this represents just a share of the petrochemical products we consume, and still many others (from textiles to pharmaceuticals) need to transition to renewable sources. Policies need to support the development and adoption of alternatives in the petrochemical industry, as well as the reduction and recycling of petrochemical products.

Supplemental Material

Download MS Word (26.7 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 Available at http://www.refinitiv.com.

2 Companies position on S&P Global Platts 2020 ranking of the world’s 250 largest energy companies. Available at https://www.spglobal.com/platts/top250/rankings/2020.

3 The European Green Deal was officially adopted in January 2020 when the European Parliament voted in favour of it.

References

- Brauers, H., & Oei, P.-Y. (2020). The political economy of coal in Poland: Drivers and barriers for a shift away from fossil fuels. Energy Policy, 144, 111621. https://doi.org/10.1016/j.enpol.2020.111621

- Bouman, E. A., Lindstad, E., Rialland, A. I., & Strømman, A. H. (2017). State-of-the-art technologies, measures, and potential for reducing GHG emissions from shipping – A review. Transportation Research Part D: Transport and Environment, 52, 408–421. https://doi.org/10.1016/j.trd.2017.03.022

- Bürgin, A. (2015). National binding renewable energy targets for 2020, but not for 2030 anymore: Why the European Commission developed from a supporter to a brakeman. Journal of European Public Policy, 22(5), 690–707. https://doi.org/10.1080/13501763.2014.984747

- Cadillo-Benalcazar, J. J., Bukkens, S. G. F., Ripa, M., & Giampietro, M. (2021). Why does the European Union produce biofuels? Examining consistency and plausibility in prevailing narratives with quantitative storytelling. Energy Research & Social Science 71, 101810. https://doi.org/10.1016/j.erss.2020.101810

- Dietz, S., Gardiner, D., Jahn, V., & Noels, J. (2020). Carbon performance of European integrated Oil and Gas companies: Briefing paper. Transition Pathway Initiative, 1–26. https://www.transitionpathwayinitiative.org/publications/58.pdf?type=Publication

- EEA. (2021). EU Emissions Trading System (ETS) data viewer, viewed 5 May 2021 < https://www.eea.europa.eu/data-and-maps/dashboards/emissions-trading-viewer-1>.

- Donovan, C., Fomicov, M., Gerdes, L., & Waldron, M. (2020). Energy investing exploring risk and return in the capital markets. IEA.

- European Commission. (2021). NER 300 programme, viewed 26 april 2021 <https://ec.europa.eu/clima/policies/innovation-fund/ner300_en#tab-0-0>

- Ferns, G., Amaeshi, K., & Lambert, A. (2019). Drilling their Own graves: How the European Oil and Gas supermajors avoid sustainability tensions through mythmaking. Journal of Business Ethics, 158(1), 201–231. https://doi.org/10.1007/s10551-017-3733-x

- Gaulin, N., & Le Billon, P. (2020). Climate change and fossil fuel production cuts: Assessing global supply-side constraints and policy implications. Climate Policy 20, 888–901. https://doi.org/10.1080/14693062.2020.1725409

- Geels, F. W. (2014). Reconceptualising the co-evolution of firms-in-industries and their environments: Developing an inter-disciplinary Triple Embeddedness framework. Research Policy, 43(2), 261–277. https://doi.org/10.1016/j.respol.2013.10.006

- Geels, F. W., & Penna, C. C. R. (2015). Societal problems and industry reorientation: Elaborating the dialectic issue LifeCycle (DILC) model and a case study of car safety in the USA (1900–1995). Research Policy, 44(1), 67–82. https://doi.org/10.1016/j.respol.2014.09.006

- Geels, F. W., & Schot, J. (2007). Typology of sociotechnical transition pathways. Research Policy, 36(3), 399–417. https://doi.org/10.1016/j.respol.2007.01.003

- Gençsü, I., Whitley, S., Trilling, M., & Worrall, L. (2020). Phasing out public financial flows to fossil fuel production in Europe. Climate Policy, 20(8), 1010–1023. https://doi.org/10.1080/14693062.2020.1736978

- Hartmann, J., Inkpen, A. C., & Ramaswamy, K. (2021). Different shades of Green: Global oil and gas companies and renewable energy. Journal of International Business Studies, 879–903. https://doi.org/10.1057/s41267-020-00326-w

- Helm, D. (2014). The European framework for energy and climate policies. Energy Policy, 64, 29–35. https://doi.org/10.1016/j.enpol.2013.05.063

- Kivimaa, P., Laakso, S., Lonkila, A., & Kaljonen, M. (2021). Moving beyond disruptive innovation: A review of disruption in sustainability transitions. Environmental Innovation and Societal Transitions, 38, 110–126. https://doi.org/10.1016/j.eist.2020.12.001

- Kungl, G., & Geels, F. W. (2018). Sequence and alignment of external pressures in industry destabilisation: Understanding the downfall of incumbent utilities in the German energy transition (1998–2015). Environmental Innovation and Societal Transitions, 26, 78–100. https://doi.org/10.1016/j.eist.2017.05.003

- Levy, D. L., & Kolk, A. (2002). Strategic responses to global climate change: Conflicting pressures on multinationals in the Oil industry. Business and Politics, 4(3), 275–300. https://doi.org/10.2202/1469-3569.1042

- Lu, H., Guo, L., & Zhang, Y. (2019). Oil and gas companies’ low-carbon emission transition to integrated energy companies. Science of The Total Environment, 686, 1202–1209. https://doi.org/10.1016/j.scitotenv.2019.06.014

- Mäkitie, T., Normann, H. E., Thune, T. M., & Sraml Gonzalez, J. (2019). The Green flings: Norwegian oil and gas industry’s engagement in offshore wind power. Energy Policy, 127, 269–279. https://doi.org/10.1016/j.enpol.2018.12.015

- Minx, J. C., Lamb, W. F., Callaghan, M. W., Fuss, S., Hilaire, J., Creutzig, F., Amann, T., Beringer, T., de Oliveira Garcia, W., Hartmann, J., & Khanna, T. (2018). Negative emissions—part 1: Research landscape and synthesis. Environmental Research Letters, 13(6), 063001. https://doi.org/10.1088/1748-9326/aabf9b

- Mühlemeier, S. (2019). Dinosaurs in transition? A conceptual exploration of local incumbents in the Swiss and German energy transition. Environmental Innovation and Societal Transitions, 31, 126–143. https://doi.org/10.1016/j.eist.2018.12.003

- Pearson, M., & Rüdig, W. (2020). The Greens in the 2019 European elections. Environmental Politics, 29, 336–343. https://doi.org/10.1080/09644016.2019.1709252

- Pfeffer, J., & Salancik, G. R. (2003). The external control of organizations - A resource dependence perspective. Stanford University Press.

- Plantinga, A., & Scholtens, B. (2021). The financial impact of fossil fuel divestment. Climate Policy, 21(1), 107–119. https://doi.org/10.1080/14693062.2020.1806020

- Puricelli, S., Cardellini, G., Casadei, S., Faedo, D., van den Oever, A. E. M., & Grosso, M. (2021). A review on biofuels for light-duty vehicles in Europe. Renewable and Sustainable Energy Reviews 137. https://doi.org/10.1016/j.rser.2020.110398

- Reiner, D. M. (2016). Learning through a portfolio of carbon capture and storage demonstration projects. Nature Energy, 1, 15011. https://doi.org/10.1038/nenergy.2015.11

- Rogelj, J., Shindell, D., Jiang, K., Fifita, S., Forster, P., Ginzburg, V., Handa, C., Kheshgi, H., Kobayashi, S., Kriegler, E., & Mundaca, L. (2018). Mitigation pathways compatible with 1.5°C in the context of Sustainable development. In V. Masson-Delmotte, P. Zhai, H.-O. Pörtner, D. Roberts, J. Skea, P. R. Shukla, A. Pirani, W. Moufouma-Okia, C. Pé an, R. Pidcock, S. Connors, J. B. R. Matthews, Y. Chen, X. Zhou, M. I. Gomis, E. Lonnoy, T. Maycock, M. Tignor, & T. Waterfield (eds.), Global warming of 1.5 C (pp. 93–174). Intergovernmental Panel on Climate Change (IPCC).

- Seto, K. C., Davis, S. J., Mitchell, R. B., Stokes, E. C., Unruh, G., & Ürge-Vorsatz, D. (2016). Carbon lock-In: Types, causes, and policy implications. Annual Review of Environment and Resources, 41(1), 425–452. https://doi.org/10.1146/annurev-environ-110615-085934

- Staples, M. D., Malina, R., Suresh, P., Hileman, J. I., & Barrett, S. R. H. (2018). Aviation CO2 emissions reductions from the use of alternative jet fuels. Energy Policy, 114, 342–354. https://doi.org/10.1016/j.enpol.2017.12.007

- Steen, M., & Weaver, T. (2017). Incumbents’ diversification and cross-sectorial energy industry dynamics. Research Policy, 46(6), 1071–1086. https://doi.org/10.1016/j.respol.2017.04.001

- Turnheim, B., & Sovacool, B. K. (2020). Forever stuck in old ways? Pluralising incumbencies in sustainability transitions. Environmental Innovation and Societal Transitions, 35, 180–184. https://doi.org/10.1016/j.eist.2019.10.012

- Unruh, G. C. (2000). Understanding carbon lock-in. Energy Policy, 28(12), 817–830. https://doi.org/10.1016/S0301-4215(00)00070-7

- van den Hove, S., Le Menestrel, M., & de Bettignies, H.-C. (2002). The oil industry and climate change: Strategies and ethical dilemmas. Climate Policy, 2(1), 3–18. https://doi.org/10.3763/cpol.2002.0202

- van Mossel, A., van Rijnsoever, F. J., & Hekkert, M. P. (2018). Navigators through the storm: A review of organization theories and the behavior of incumbent firms during transitions. Environmental Innovation and Societal Transitions, 26, 44–63. https://doi.org/10.1016/j.eist.2017.07.001

- Verbruggen, A., Laes, E., & Woerdman, E. (2019). Anatomy of emissions trading systems: What is the EU ETS? Environmental Science & Policy, 98, 11–19. https://doi.org/10.1016/j.envsci.2019.05.001

- York, R., & Bell, S. E. (2019). Energy transitions or additions? Energy Research & Social Science, 51, 40–43. https://doi.org/10.1016/j.erss.2019.01.008