ABSTRACT

A mid-century net zero target creates a challenge for reducing the emissions of emissions-intensive, trade-exposed sectors with high cost mitigation options. These sectors include aluminium, cement, chemicals, iron and steel, lime, pulp and paper and petroleum refining. Available studies agree that decarbonization of these sectors is possible by mid-century if more ambitious policies are implemented soon. Existing carbon pricing policies have had limited impact on the emissions of these sectors because their marginal abatement costs almost always exceed the tax rate or allowance price. But emissions trading systems with free allowance allocations to emissions-intensive, trade-exposed sectors have minimized the adverse economic impacts and associated leakage. Internationally coordinated policies are unlikely, so implementing more ambitious policies creates a risk of leakage. This paper presents policy packages a country can implement to accelerate emission reduction by these sectors with minimal risk of leakage. To comply with international trade law the policy packages differ for producers whose goods compete with imports in the domestic market and producers whose goods are exported. Carbon pricing is a critical component of each package due its ability to minimize the risk of adverse economic impacts on domestic industry, support innovation and generate revenue. The revenue can be used to assist groups adversely impacted by the domestic price and production changes due to carbon pricing and to build public support for the policies.

Key policy insights

A country with a mid-century net zero GHG emission target likely will need to implement more ambitious mitigation policies soon for emission-intensive sectors such as aluminium, cement, chemicals, iron and steel, lime, pulp and paper and petroleum refining.

More ambitious mitigation policies are likely to vary by country and be implemented at different times, creating a risk of leakage due to industrial production shifts to other jurisdictions.

More ambitious mitigation policy packages, compatible with international trade law, that a country can implement to reduce emissions from these sectors with minimal risk of leakage are available but differ for producers whose goods compete with imports in the domestic market and those whose goods are exported.

Carbon pricing is a critical component of each package due its ability to minimize the risk of adverse economic impacts on domestic producers, support innovation and generate revenue.

1. Introduction

The Paris Agreement objective is to hold the increase in global average temperature to well below 2°C above pre-industrial levels and pursue efforts to limit the increase to 1.5°C above pre-industrial levels. Meeting this objective requires that global CO2 emissions be reduced to at least net zero about mid-century along with significant reductions in emissions of other greenhouse gases (GHGs). Over 135 countries have a net zero target, over 90% of them with a mid-century or earlier date. Countries will need to implement more stringent mitigation policies to achieve their targets.Footnote1

Although international coordination of mitigation policies offers economic benefits, policies are likely to vary by country, be implemented at different times and at different levels of ambition. International coordination is inhibited by various factors including the disparate interests of countries that import or export emissions-intensive, trade exposed (EITE) goods. The risk of production shifts to jurisdictions with less costly regulations (leakage) deters unilateral implementation of more stringent mitigation policies.

Carbon pricing – a carbon tax or GHG emissions trading system (ETS) – encourages implementation of emission reductions whose cost per tCO2e reduced is lower than the tax rate or allowance price. Carbon pricing policies, especially ETSs, can be designed to reduce emissions by EITE sectors with minimal risk of production shifts. In such ETSs, regulated EITE sources receive free allowances, which gives them an incentive to reduce emissions but limits the total compliance cost and incentive to shift production to other jurisdictions.Footnote2

EITE sectors with high mitigation costs, such as aluminium, cement, chemicals, iron and steel, lime, pulp and paper and petroleum refining, account for 24–34% of global emissions (Bashmakov et al., Citation2022).Footnote3 A net zero target will require development of new technologies and transformation of the production facilities of those sectors. To provide sufficient time for those developments more ambitious mitigation policies for those sectors need to be implemented soon.

Various policies have been proposed to reduce emissions by these EITE sectors. Since the products of these sectors are internationally traded, any policy must comply with international trade law. Trade law provisions differ for imports and exports, so domestic producers whose goods compete with imports (import-competing) in the domestic market, and producers whose goods are exported, require different policies.

This paper presents policy packages a country can implement to increase the ambition of its policies for EITE sectors. Each package includes one or more policies proposed in the literature together with carbon pricing. Carbon pricing to minimize the risk of adverse economic impacts is a critical component of each package. Carbon pricing also generates revenue the government can use to assist groups adversely impacted by domestic price and production changes.

Since carbon pricing is a key component of each package, the paper first establishes its ability to fulfil the projected role. Sections 2 through 4 discuss carbon pricing, its advantages and limitations and evidence of its effectiveness in reducing emissions and supporting innovation. More ambitious mitigation policies for these EITE sectors that a country can implement on its own with minimal risk of leakage are presented in section 5. Collection and use of carbon pricing revenue are discussed in section 6, while section 7 concludes.

2. Carbon pricing – key features: advantages, limitations, and international coordination

Carbon taxes and GHG ETSs have been used since 1990 and 2005 respectively (World Bank, Citation2022). With a carbon tax, the government sets a carbon price but the resulting emission reductions are uncertain while with an ETS the government sets an aggregate emissions limit whose carbon price is uncertain (Pollitt, Citation2016).Footnote4,Footnote5 Stavins (Citation2022) reviews carbon taxes and ETSs in theory and in practice. The performance of different policies, including carbon taxes and GHG ETSs, is assessed by Peñasco et al. (Citation2021).

A carbon tax or allowance price imposes a cost per tCO2e on regulated emissions. This increases the prices of goods and services in proportion to their GHG emissions intensity and encourages consumers to shift to less emissions intensive alternatives (Bertoldi, Citation2022).Footnote6,Footnote7 In practice features such as exemptions and multiple rates lead to debate as to whether a specific tax is a carbon tax (Haites, Citation2018).Footnote8 Carbon pricing is becoming more prevalent (Dubash et al., Citation2022) with 35 carbon taxes and 33 ETSs collectively covering almost 23% of global GHG emissions in effect by January 2022.Footnote9 A tax or ETS can be designed to apply to a wide range of emissions sources. In practice, a tax or ETS typically covers between 10% and 80% of a jurisdiction’s GHG emissions with agricultural, forestry, chemical process and non-CO2 emissions being the most common exemptions (Khan & Johansson, Citation2022; World Bank, Citation2022). Several jurisdictions have an ETS and one or more carbon taxes that apply to different sources. These jurisdictions rarely attempt to coordinate these tax rates and allowance prices.

The main advantage of carbon pricing is flexibility; it encourages the regulated sources to implement emission reductions whose cost per tCO2e is lower than the tax rate or allowance price. It leaves the choice of mitigation measures to affected sources. In addition taxes and auctioned allowances generate revenue for the government, which can be used to address distributional impacts, as discussed in Section 6.

The limitations of carbon pricing instruments are that they:

Provide limited incentive to implement higher cost (cost per tCO2e higher than the tax or allowance price) mitigation technologies, such as renewable energy (Bertoldi et al., Citation2005; Lilliestam et al., Citation2021), or more costly measures to abate industrial process emissions (Bataille, Citation2020). The incentive to implement higher cost measures depends on the level of the carbon price, the entity’s discount rate and its expectations concerning the future tax rate/allowance price and future costs of mitigation measures (Vogt-Schilb et al., Citation2018).

Have limited impact on long-term mitigation investments (Fuss et al., Citation2018) and adoption of mitigation measures in situations where decisions are relatively insensitive to pricesFootnote10 such as recycling, household energy efficiency investments (Bertoldi et al., Citation2005), transportation choices, and urban planning (Creutzig et al., Citation2011, Citation2016).

Progressive emission reductions require tax rate increases or ETS cap reductions over time, taking into account technological and socio-economic changes as well as other policies that reduce emissions or mitigation costs. This creates an implicit strategy of implementing progressively higher cost mitigation measures over time. Relying solely on a carbon pricing policy to achieve a mid-century net zero target is not advisable because it would defer implementation of the high cost mitigation measures until lower cost measures have been exhausted and thus reduce the time available to reduce the emissions of sectors with high cost mitigation measures.

Climate impacts are the same regardless of where the GHG emissions occur while mitigation costs differ across both regions and countries. This creates the potential for significant economic benefits through international coordination of carbon pricing (Hoel, Citation1992), including options such as (1) a minimum price with each country keeping the proceeds (Parry et al., Citation2021; Weitzman, Citation2014); (2) a common price for all countries with financial transfers (Budolfson et al., Citation2021)Footnote11; and (3) a common price for a group of countries with tariffs on imports from other countries (Nordhaus, Citation2015).

Nominal tax rates and allowance prices, in practice, vary widely across jurisdictions; in 2021, large increases in allowance prices occurred in several jurisdictions (World Bank, Citation2022).Footnote12 There is no evidence of any efforts by policymakers to harmonize carbon taxes across country boundaries, which would in any case be politically and technically difficult (Pollitt, Citation2016). Historically ETSs across countries have been linked, which reduces allowance price differences (Mehling & Haites, Citation2009), mainly through limited acceptance of Kyoto Protocol credits, but that has become much less common since 2014 (Haites, Citation2016).

3. Evidence of the effectiveness of carbon pricing on GHG emission reductions

Assessing the effectiveness of a specific tax or ETS is challenging because emissions usually are subject to multiple mitigation policies, and the direct and indirect impacts of other policies and exogenous factors such as economic conditions and fossil fuel prices (Koch et al., Citation2014). In addition, the tax rate or allowance price changes over time.

Overlapping policies affect taxes and ETSs differently. The tax rate does not change but the emissions subject to the tax are affected by the other policies. With an ETS, emission reductions due to other policies contribute to compliance with the cap and so reduce the allowance price. ETSs have introduced mechanisms, such as a minimum price and market stability reserve, to limit the effect of other policies on the allowance price (Bocklet et al., Citation2019).

Recent analyses of multiple carbon pricing instruments find that despite their variability they have a statistically significant effect on emissions (Köppl & Schratzenstaller, Citation2022). Assessments of the performance of individual taxes and ETSs are summarized by Hoppe et al. (Citation2021). The most extensive literature relates to the EU ETS – the oldest and until 2021 the largest ETS – and British Columbia’s tax which has a broader scope and covers more emissions than earlier European taxes.Footnote13

3.1. Impacts of the EU ETS

An extensive ex post literature concludes that the EU ETS reduced emissions with no statistically significant adverse impacts on competitiveness or leakage (Haites et al., Citation2018). Analyses of specific EITE sectors – aluminium, cement, and steel – likely to be particularly vulnerable to foreign competition, find no adverse impacts (Boutabba & Lardic, Citation2017). Dechezleprêtre et al. (Citation2022) detects no carbon leakage by installations of multinational corporations subject to the EU ETS. Data on the embodied carbon of trade flows – whether the embodied emissions of imports increase or those of exports fall – for goods subject to the EU ETS also reveal no leakage (Naegele & Zaklan, Citation2019).

Most of the emissions reductions are due to relatively low-cost measures that can be implemented quickly, such as fuel switching (Edenhofer et al., Citation2011) and/or energy efficiency improvements (Löschel et al., Citation2019). Power and heating sources reduced emissions more than industrial sources – at approximately 4%/year vs 0.2%/year – faced with more costly options.Footnote14 Studies that attempt to attribute a share of the reductions achieved to the ETS compared to business-as-usual estimate its contribution at 3–9% with one estimate of 28% (Borghesi & Verde, Citation2019).

3.2. Impacts of the BC carbon tax

British Columbia’s carbon tax covers approximately 70% of the province’s GHG emissions and took effect on 1 July 2008 at CAD 10/tCO2.Footnote15 The tax increased at a rate of CAD 5/tCO2 per year for the next five years, then remained at CAD 30/tCO2 until April 2019 before increasing by CAD 5/tCO2 annually to CAD 50/tCO2 on 1 April 2022. Studies find that the tax reduced per capita/household gasoline use (Haites et al., Citation2018 for review), as well as residential natural gas use (Xiang & Lawley, Citation2019) and diesel consumption (Bernard & Kichian, Citation2019). Urban households reduced gasoline consumption more than rural households because they have more transportation options (Lawley & Thivierge, Citation2018).

All of these studies are based exclusively or primarily on the initial five years of rising tax rates and each covers only some of the emissions subject to the tax. Erutku and Hildebrand (Citation2018) find that the impact began to diminish after the tax rate was frozen. A recent analysis for 2008–2016 finds the tax reduced transport emissions but did not lead to a statistically significant reduction in aggregate CO2 emissions (Pretis, Citation2022).

With respect to the impact on industry, the carbon tax induced shifts in employment from more to less carbon-intensive industries with a small statistically significant increase between 2007 and 2013 (Carbone et al., Citation2020) and wage reductions in adversely impacted sectors (Yip, Citation2018, Citation2020). Although cement exports were reduced (Thivierge, Citation2020) there was no negative impact on GDP (Bernard & Kichian, Citation2021) due in part to the redistribution of tax revenue to firms and households.

4. Impact of carbon pricing on innovation

Documenting the innovation stimulated by a mitigation policy is challenging, particularly with multiple jurisdictions implementing policies. Innovation may occur any time after a policy is proposed by any jurisdiction and may happen anywhere. Innovations may originate with regulated entities, their suppliers, or independent academic, government or industry researchers. Innovation in response to a mitigation policy varies by policy type (Jaffe et al., Citation2002) and stringency (Aghion et al., Citation2016). Industrial sources that engage in R&D shifted their research activities towards a technological change (innovation and deployment of new technology) when covered by the EU ETS (Calel & Dechezleprêtre, Citation2016). Pricing policies encourage adoption of lower cost mitigation measures which requires marginal technology changes, rather than more radical, higher cost or potentially transformational innovation (Calel, Citation2020).Footnote16 While there is evidence that carbon pricing stimulates innovation, there is no consensus on the impact of pricing policies on emissions.

5. Carbon pricing and a mid-century net zero target

As of November 2021, 135 countries have adopted a net zero target, with a mid-century or earlier date for more than 90% of the countries (Rogelj et al., Citation2021). A mid-century net zero target poses a challenge for mitigation of emissions by EITE sources. Given a national net zero target this discussion assumes that EITE sectors have access to zero emissions electricity.Footnote17

Studies of options to reduce emissions by EITE sectors vary in terms of their geographic coverage, from global (van Sluisveld et al., Citation2021) to Europe (Marcu et al., Citation2021), Sweden (Nurdiawati & Urban, Citation2021) orthe US (Hasanbeigi et al., Citation2021). Although the sectoral coverage varies as well, all of the studies agree that decarbonization is possible by mid-century if more ambitious policies are implemented soon (Bashmakov et al., Citation2022).

The literature on policies to reduce the emissions of EITE sources shows support for a mix of policies, notably to include RD&D and commercialization of new technologies, carbon pricing, contracts for differences,Footnote18 other subsidies, product/consumption charges, product standards, tradable performance standards (TPS),Footnote19 and a carbon border adjustment mechanism (CBAM) (Bataille et al., Citation2018; Grubb et al., Citation2022; Nilsson et al., Citation2021).

Since the products of these EITE sources are traded, policy choice is constrained by international trade law.Footnote20 Trade law requires that a country’s treatment of ‘like’ imports may not discriminate on the basis of their country of origin or process or production methods. Providing rebates of mitigation costs on exported goods creates a risk that one or more importing countries will subject them to countervailing duties. Thus policies will differ for import-competing and export sectors.Footnote21,Footnote22

A package of policies that includes carbon pricing performs better than a carbon pricing policy on its own due to the existence of multiple market failures (Dubash et al., Citation2022). Carbon pricing can reduce the size of the rebound effect associated with most mitigation policies (Freire-González, Citation2020) with an ETS being more effective than a carbon tax (van den Bergh, Citation2011). An ETS with free allowances is part of most packages because of its demonstrated capacity to minimize leakage.

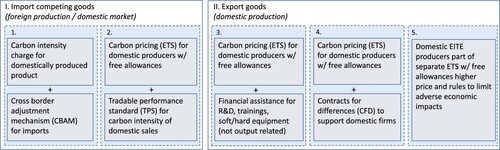

outlines possible policy packages for EITE sectors that a country could implement with minimal risk of adverse economic impacts.

Figure 1. Five possible policy packages for countries depending on production and sales of EITE goods.

Possible policy packages for EITE sectors that a country could implement with minimal risk of adverse economic impacts are illustrated in . All options consider carbon pricing as part of the policy package. If a country is a net importer of an EITE good (I), a product charge based on emissions intensity can be levied on sales by domestic producers (a product specific carbon tax) with an equivalent carbon border adjustment (CBAM) for imports (1)Footnote23,Footnote24 or a tradable performance standard can be instituted for domestic sales of a good (domestically produced or imported) with domestic producers covered by ETS with free allowance allocation (2).Footnote25 If a country is net exporter of a good (II), financial assistance to domestic firms not tied to the level of export sales for R&D support, assistance for new/modernized plants, and worker training (3), or procuring goods with prices above market price from domestic firms e.g. using contracts for differences (4) can be considered to support low carbon development. Domestic producers of export goods in policy packages 3 and 4 are subject to an ETS and receive free allowances. Producers of EITE exports could be moved into a separate ETS with rules designed to ensure a higher allowance price while protecting international competitiveness (5).Footnote26

Effective mitigation policies have economic impacts. They increase the prices of emissions-intensive goods to induce changes in consumption, production and trade volumes with impacts on employment and economic activity domestically and in other countries.Footnote27 Revenue generated by the carbon pricing in each policy package can fund domestic adjustments to cushion adverse impacts, for example through policies such as worker retraining and support for lower production levels.

6. Distributional effects of carbon pricing policies

The revenue raised by carbon pricing policies affects socio-economic groups differently and how that revenue is spent influences those distributional effects (Steenkamp, Citation2021). In practice, the use of carbon pricing revenue varies widely by jurisdiction. Some treat it as general revenue while others distribute it to firms and low income households and fund environmental projects and low carbon technologies to build public support for the policy (Raymond, Citation2019; World Bank, Citation2022).Footnote28

The most widely studied effect is the direct impact of a carbon tax on household income. Typically it is regressive in developed countries and progressive in developing countries (Koh et al., Citation2021; Köppl & Schratzenstaller, Citation2022). Governments can redistribute tax revenue to low income households or implement other changes to taxation and transfer systems to achieve desired distributional outcomes and avoid adverse impacts (e.g. Bertoldi, Citation2022; Budolfson et al., Citation2021).Footnote29

Even if a carbon tax is progressive, it increases prices for fuels, electricity, transport, food and other goods and services, an impact that adversely affects the most vulnerable. Thus, carbon taxes may not be suitable for developing countries with a limited capacity to effectively collect taxes and distribute the revenue to low income households (Steinebach & Limberg, Citation2022).

Distributional impacts typically have not been a significant issue for ETSs, in part due to relatively low allowance prices. Equity across participants, especially EITE sources, generally is addressed through free allowance allocations. Impacts of ETSs on household incomes, with the exception of electricity prices, have been too small to be a concern. Some ETSs are designed to limit electricity price increases (Petek, Citation2020) or use some revenue for bill assistance to low-income households (RGGI, Citation2019).

Carbon pricing can reduce employment and/or wages in large emissions-intensive sources so economic impacts differ across communities depending upon their mix of emissions-intensive industries (Yip, Citation2018, Citation2020). This may also be the case between urban and rural areas (Creutzig et al., Citation2020).

7. Conclusions

A mid-century net zero target creates a challenge for reducing the emissions of EITE sectors that have high marginal mitigation costs, notably in aluminium, cement, chemicals, iron and steel, lime, pulp and paper and petroleum refining industries. Available studies agree that decarbonization is possible by mid-century if more ambitious policies are implemented soon.

More ambitious mitigation policies for EITE sectors are likely to vary by country, be implemented at different times and differ in ambition. Thus a country wishing to accelerate the decarbonization of these EITE sectors should design its mitigation policies to minimize the risk of leakage due to production shifts to different jurisdictions with less costly policies. To comply with international trade law policy packages for import-competing and export sectors will need to differ.

A country can implement policy packages on its own to reduce emissions by its EITE sectors. Since a country imports or exports the products of several EITE sectors a variety of policy packages for different sectors is likely. Carbon pricing is a critical component of each package due its ability to minimize the risk of adverse economic impacts, to support innovation and to generate revenue.

Policy packages for import-competing goods include:

A product charge based on emissions intensity levied on sales of domestic goods and an equivalent carbon border adjustment mechanism (CBAM) for imports; and

A tradable performance standard for domestic sales of a good (domestic or imported) together with an ETS with free allowance allocations for domestic producers.

Policy packages for export goods, that minimize the risk of countervailing duties imposed by importers, include an ETS with free allowances for domestic producers plus financial assistance not tied to the level of export sales. Examples of such financial assistance are R&D support, or support for new/modernized plants, for worker training or government purchases of low carbon products whose costs exceed the market price using contracts for differences. Alternately EITE producers of export goods could be moved into a separate ETS with provisions designed to ensure a higher allowance price while protecting international competitiveness.

Effective mitigation policies shift consumption and production patterns to reduce emissions. The impacts of those shifts, such as a plant closure, can be large or abrupt for specific income groups or regions. Carbon pricing revenue can be used to assist groups or regions adversely impacted by the domestic impacts of mitigation policies and to build public support for the policies.

Supplemental Material

Download MS Word (42.9 KB)Acknowledgments

The authors express their appreciation for the constructive comments on earlier drafts provided by six anonymous reviewers as well as valuable suggestions from the editor, Jan Corfee-Morlot. Thanks to Renée van Diemen and the Technical Support Unit (TSU) of the Assessment Report 6 (AR6) IPCC Working Group 3 (Mitigation), where the idea of this manuscript emerged in the writing process of the AR6.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 The term ‘country’ is used to mean a country, jurisdiction, region or state depending upon the context.

2 Non EITE sources must buy allowances.

3 The focus of the paper is EITE industrial sectors with marginal abatement costs well above the prevailing tax rate/allowance price. There is no accepted term for these sectors. Together with some transportation and agricultural sources they are sometimes called ‘hard to abate’ sectors. EITE is also a broader term in that it covers some industrial sectors with marginal abatement costs lower than the prevailing tax rate/allowance price. The paper uses the term EITE with the understanding that the focus is industrial sectors with relatively high marginal abatement costs.

4 Several ETSs include price stability mechanisms such as a price floor and/or ceiling. Information on ETS designs is available from ICAP (Citation2021) while World Bank (Citation2022) provides comparative information on all taxes and ETSs.

5 Two ETS designs are common (Haites et al., Citation2018). One imposes a cap on specified emissions (sources and gases), distributes (free or by auction) tradable allowances (usually for 1 tCO2e) roughly equal to the cap and requires the designated sources to remit allowances equal to their verified emissions. The second uses an emissions intensity (baseline or performance standard) and activity level (current or historic) to create an emissions budget for each participant. If its actual emissions are less than its budget a participant receives credits for the difference while a participant with excess emissions must purchase credits for compliance. The EU ETS and Korea use the first design while China and Canada use the second.

6 A fuel tax increase or fossil fuel subsidy removal raises the prices of fossil fuels and so reduces GHG emissions. But the price changes are rarely proportional to the carbon content which leads to inefficient, even perverse, adjustments. A few subsidies, such as those for CO2 sequestration, are based on the reductions achieved but most, such as those for energy efficiency or renewable energy, are not proportional to the reductions achieved.

7 Consumer responses to taxes on gasoline and diesel, like a carbon tax on these fuels, are to consume less by travelling less, shifting modes and switching to more efficient vehicles. Fuel taxes are not included in most lists of carbon taxes (World Bank, Citation2022) because they are not proportional to the carbon content, but they are a component of the effective carbon price faced by consumers (OECD, Citation2021). Carbon taxes are more effective than energy taxes at reducing emissions.

8 Norway taxes CO2 emissions in petroleum activities on the continental shelf at a higher rate than emissions from fossil fuels consumed onshore. Ireland imposes a lower tax on solid (coal) than liquid and gaseous fuels.

9 The EU ETS – 30 countries – and RGGI – 11 US states – cover multiple jurisdictions. Carbon taxes cover 5.2% of global emissions while ETSs cover 16.5%.

10 Decisions with a low price elasticity. The longer term price sensitivity (price elasticity) may be higher. Decisions also may be affected by principal-agent problems such as landlords’ reluctance to make efficiency investments when tenants pay the energy bills.

11 Bataille et al. (Citation2018) notes that the conclusion that optimal climate policy implies a unique carbon price around the globe is valid only if unlimited transfers among countries are possible to compensate for differences in abatement costs and welfare effects. Further key references see Supplementary Material 1.

12 Finland, France and some Canadian provinces lowered fuel taxes when their carbon taxes were introduced so their real carbon tax rates are lower than the nominal rates. Emission reductions depend upon the real, rather than the nominal, tax rate. Various policies affect the relationship between the nominal and real tax rates over time.

13 Runst and Thonipara (Citation2020) estimates the impact of the Swedish carbon tax on residential CO2 emissions between 2001 and 2016 and Andersson (Citation2019) estimates its impact on transport emissions between 1990 and 2005. Governments rarely publish data on taxed emissions so evaluations rely on other sources, or proxies such as gasoline sales, for emissions data. Typically they cover only a share of the taxed emissions. Abatement costs and hence emission reductions due to a tax likely differ by sector so a reduction estimated for one sector is evidence that the tax has had an impact but may not be a good estimate of its overall effect.

14 Calculated from EU ETS compliance data by sector for the period 2013 through 2019.

15 Agriculture emissions are not covered. Electricity generation is virtually GHG emissions free so the tax does not affect the price of electricity.

16 van den Bergh and Savin (Citation2021) and Lilliestam et al. (Citation2022) debate the evidence supporting the findings presented in Lilliestam et al. (Citation2021).

17 Decarbonization of the electricity supply may occur prior to or concurrent with decarbonization of the EITE sectors.

18 Financial compensation for the marginal costs of low-carbon production compared to business as usual production.

19 TPS do not explicitly put a price on carbon nor limit amount of emission allowances.

20 Mitigation policies apply to sources while trade law applies to goods. Links between EITE sources and the internationally traded goods they produce must be established. This has already been done in the case of the EU ETS where the free allowance allocation to an installation is based on its production of specified emissions-intensive goods. So the links between ‘goods’ and ‘sources’ are clear.

21 Sectors can be classified as part of the policy development process. For example an import competing good could be defined as one whose consumption exceeds domestic production and whose exports are less than X% of production while an export good is one whose production exceeds domestic consumption and whose imports are less than Y% of consumption.

22 In practice it is unlikely that a country will be able to classify every traded good produced by EITE sectors as an import-competing or export good. Countries are likely to classify goods differently just as their definitions of sectors eligible for free allowances differ. And classifications are likely to change over time.

23 See Böhringer et al. (Citation2022) for a summary of the challenges involved in implementing a CBAM.

24 Proposals in the EU’s Fit for 55 Package indicate an incremental shift toward package 1 for producers of aluminum, cement, electricity, fertilizers and iron and steel (European Commission, Citation2021). Free allowances to producers of these goods under the ETS would be phased out between 2026 and 2035 and imports would be subject to an equivalent border adjustment. Requiring EU producers to purchase allowances has the effect imposing an emissions intensity charge on the goods they produce.

25 A similar package could be implemented with a maximum emissions standard, but the tradable performance standard creates stronger incentives to reduce the good’s emissions intensity and it raises fewer potential trade law problems.

26 In addition to free allowances based on current output and a market stability reserve, the ETS for these installations could include a minimum and maximum price (Flachsland et al., Citation2020) and periodic reviews to ensure compliance costs do not exceed a specified share, such as 5%, of production costs.

27 Adversely affected exporters may challenge the policies under international trade law and/or implement retaliatory trade measures. A number of countries that export the specified goods to the EU have expressed concerns with respect to its CBAM proposal (Acar et al., Citation2022; Eicke et al., Citation2021; Lim et al., Citation2021).

28 Revenue raised through carbon taxes and ETSs is used differently (Carl & Fedor, Citation2016; Marten & van Dender, Citation2019; World Bank, Citation2022). About 40% of carbon tax revenue is treated as general revenue and most of the balance is used to offset the burden of the tax while about 80% of ETS auction revenue is earmarked for environmental objectives. EU member states are required to use ETS auction revenues to support energy efficiency, renewable energy supply and energy poor households.

29 Equal per capita distribution – carbon dividends – is sometimes proposed.

References

- Acar, S., Aşıcı, A. A., & Yeldan, A. (2022). Potential effects of the EU’s carbon border adjustment mechanism on the Turkish economy. Environment, Development and Sustainability, 24(6), 8162–8194. https://doi.org/10.1007/s10668-021-01779-1

- Aghion, P., Dechezleprêtre, A., Hémous, D., Martin, R., & Van Reenen, J. (2016). Carbon taxes, path dependency, and directed technical change: Evidence from the auto industry. Journal of Political Economy, 124(1), 1–51. https://doi.org/10.1086/684581

- Andersson, J. J. (2019). Carbon taxes and CO2 emissions: Sweden as a case study. American Economic Journal: Economic Policy, 11(4), 1–30. https://doi.org/10.1257/pol.20170144

- Bashmakov, I. A., Nilsson, L. J., Acquaye, A., Bataille, C., Cullen, J. M., de la Rue du Can, S., Fischedick, M., Geng, Y., & Tanaka, K. (2022). Industry. In P. R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, & J. Malley (Eds.), IPCC, 2022: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press. https://doi.org/10.1017/9781009157926.013

- Bataille, C., Guivarch, C., Hallegatte, S., Rogelj, J., & Waisman, H. (2018). Carbon prices across countries. Nature Climate Change, 8(8), 648–650. https://doi.org/10.1038/s41558-018-0239-1

- Bataille, C. G. F. (2020). Physical and policy pathways to net-zero emissions industry. WIRES Climate Change, 11(2), e633. https://doi.org/10.1002/wcc.633

- Bernard, J.-T., & Kichian, M. (2019). The long and short run effects of British Columbia’s carbon tax on diesel demand. Energy Policy, 131, 380–389. https://doi.org/10.1016/j.enpol.2019.04.021

- Bernard, J.-T., & Kichian, M. (2021).The impact of a revenue-neutral carbon Tax on GDP dynamics: The case of British Columbia. The Energy Journal, 42(3), 205–223. https://doi.org/10.5547/01956574.42.3.jber

- Bertoldi, P. (2022). Policies for energy conservation and sufficiency: Review of existing policies and recommendations for new and effective policies in OECD countries. Energy and Buildings, 264, 112075. http://doi.org/10.1016/j.enbuild.2022.112075

- Bertoldi, P., Rezessy, S., & Bürer, M. (2005). Will emission trading promote end-use energy efficiency and renewable energy projects. Proceedings of ACEEE summer study on energy efficiency in industry, 2005. https://www.eceee.org/static/media/uploads/site-2/library/conference_proceedings/ACEEE_industry/2005/Panel_4/p4_1/paper.pdf

- Bocklet, J., Hintermayer, M., Schmidt, L., & Wildgrube, T. (2019). The reformed EU ETS - intertemporal emission trading with restricted banking. Energy Economics, 84, 104486. https://doi.org/10.1016/j.eneco.2019.104486

- Böhringer, C., Fischer, C., Rosendahl, K. E., & Rutherford, T. F. (2022). Potential impacts and challenges of border carbon adjustments. Nature Climate Change, 12(1), 22–29. https://doi.org/10.1038/s41558-021-01250-z

- Borghesi, S., & Verde, S. (2019). A literature-based assessment of the EU ETS. Florence school of regulation, European university institute. Florence. https://doi.org/10.2870/97432

- Boutabba, M. A., & Lardic, S. (2017). EU emissions trading scheme, competitiveness and carbon leakage: New evidence from cement and steel industries. Annals of Operations Research, 255(1-2), 47–61. https://doi.org/10.1007/s10479-016-2246-9

- Budolfson, M., Dennig, F., Errickson, F., Feindt, S., Ferranna, M., Fleurbaey, M., Klenert, D., Kornek, U., Kuruc, K., Méjean, A., Peng, W., Scovronick, N., Spears, D., Wagner, F., & Zuber, S. (2021). Climate action with revenue recycling has benefits for poverty, inequality and well-being. Nature Climate Change, 11(12), 1111–1116. https://doi.org/10.1038/s41558-021-01217-0

- Budolfson, M., Dennig, F., Errickson, F., Feindt, S., Ferranna, M., Fleurbaey, M., Klenert, D., Kornek, U., Kuruc, K., Méjean, A., Peng, W., Scovronick, N., Spears, D., Wagner, F., & Zuber, S. (2021). Protecting the poor with a carbon tax and equal per capita dividend. Nature Climimate Change, 11, 1025–1026. https://doi.org/10.1038/s41558-021-01228-x

- Calel, R. (2020). Adopt or innovate: Understanding technological responses to cap-and-trade. American Economic Journal: Economic Policy, 12(3), 170–201. https://doi.org/10.1257/pol.20180135

- Calel, R., & Dechezleprêtre, A. (2016). Environmental policy and directed technological change: Evidence from the European carbon market. Review of Economics and Statistics, 98(1), 173–191. https://doi.org/10.1162/REST_a_00470

- Carbone, J. C., Rivers, N., Yamazaki, A., & Yonezawa, H. (2020). Comparing applied general equilibrium and econometric estimates of the effect of an environmental policy shock. Journal of the Association of Environmental and Resource Economists, 7(4), 687–719. https://doi.org/10.1086/708734

- Carl, J., & Fedor, D. (2016). Tracking global carbon revenues: A survey of carbon taxes versus cap-and-trade in the real world. Energy Policy, 96, 50–77. https://doi.org/10.1016/j.enpol.2016.05.023

- Creutzig, F., Agoston, P., Minx, J., Canadell, J. G., Andrew, R. M., Le Quéré, C., Peters, G. P., Sharifi, A., Yamagata, Y., & Dhakal, S. (2016). Urban infrastructure choices structure climate solutions. Nature Climate Change, 6(12), 1054–1056. https://doi.org/10.1038/nclimate3169

- Creutzig, F., Javaid, A., Koch, N., Knopf, B., Mattioli, G., & Edenhofer, O. (2020). Adjust urban and rural road pricing for fair mobility. Nature Climate Change, 10(7), 591–594. https://doi.org/10.1038/s41558-020-0793-1

- Creutzig, F., McGlynn, E., Minx, J., & Edenhofer, O. (2011). Climate policies for road transport revisited (I): Evaluation of the current framework. Energy Policy, 39(5), 2396–2406. https://doi.org/10.1016/j.enpol.2011.01.062

- Dechezleprêtre, A., Gennaioli, C., Martin, R., Muûls, M., & Stoerk, T. (2022). Searching for carbon leaks in multinational companies. Journal of Environmental Economics and Management, 112, 102601. https://doi.org/10.1016/j.jeem.2021.102601

- Dubash, N. K., Mitchell, C., Boasson, E. L., Borbor-Cordova, M. J., Fifita, S., Haites, E., Jaccard, M., Jotzo, F., Naidoo, S., Romero-Lankao, P., Shlapak, M., Shen, W., & Wu, L. (2022). National and sub-national policies and institutions. In P. R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, & J. Malley (Eds.), IPCC, 2022: Climate Change 2022: Mitigation of Climate Change. Contribution of Working Group III to the Sixth Assessment Report of the Intergovernmental Panel on Climate Change. Cambridge University Press. https://doi.org/10.1017/9781009157926.015

- Edenhofer, C., Alessi, M., Georgiev, A., & Fujiwara, N. (2011). The EU emissions trading system and climate policy towards 2050. https://www.ceps.eu/ceps-publications/eu-emissions-trading-system-and-climate-policy-towards-2050-real-incentives-reduce/

- Eicke, L., Weko, S., Apergi, M., & Marian, A. (2021). Pulling up the carbon ladder? Decarbonization, dependence, and third-country risks from the European carbon border adjustment mechanism Energy Research & Social Science, 80, 102240. https://doi.org/10.1016/j.erss.2021.102240

- Erutku, C., & Hildebrand, V. (2018). Carbon tax at the pump in British Columbia and Quebec. Canadian Public Policy, 44(126), 131. https://doi.org/10.3138/cpp2017-027

- European Commission. (2021). Proposal for a regulation of the European Parliament and of the Council Establishing a carbon border adjustment mechanism. https://eur-lex.europa.eu/legal-content/EN/TXT/?uri=CELEX:52021PC0564

- Flachsland, C., Pahle, M., Burtraw, D., Edenhofer, O., Elkerbout, M., Fischer, C., Tietjen, O., & Zetterberg, L. (2020). How to avoid history repeating itself: The case for an EU emissions trading system (EU ETS) price floor revisited. Climate Policy, 20(1), 133–142. https://doi.org/10.1080/14693062.2019.1682494

- Freire-González, J. (2020). Energy taxation policies can counteract the rebound effect: Analysis within a general equilibrium framework. Energy Efficiency, 13(1), 69–78. https://doi.org/10.1007/s12053-019-09830-x

- Fuss, S., Flachsland, C., Koch, N., Kornek, U., Knopf, B., & Edenhofer, O. (2018). A framework for assessing the performance of cap-and-trade systems: Insights from the European Union emissions trading system. Review of Environmental Economics and Policy, 12(2), 220–241. https://doi.org/10.1093/reep/rey010

- Grubb, M., Jordan, N. D., Hertwich, E., Neuhoff, K., Das, K., Bandyopadhyay, K. R., van Asselt, H., Sato, M., Wang, R., Pizer, W. A., & Oh, H. (2022). Carbon leakage, consumption, and trade. Annual Review of Environment and Resources, 47(1), 753–795. https://doi.org/10.1146/annurev-environ-120820-053625

- Haites, E. (2016).Experience with linking greenhouse gas emissions trading systems. Wiley Interdisciplinary Reviews: Energy and Environment, 5(3), 246–260. https://doi.org/10.1002/wene.191

- Haites, E. (2018). Carbon taxes and greenhouse gas emissions trading systems: What have we learned? Climate Policy, 18(8), 955–966. https://doi.org/10.1080/14693062.2018.1492897

- Haites, E., Maosheng, D., Gallagher, K. S., Mascher, S., Narassimhan, E., Richards, K. R., & Wakabayashi, M. (2018). Experience with carbon taxes and greenhouse Gas emissions trading systems. SSRN Electronic Journal. 109–182. https://doi.org/10.2139/ssrn.3119241

- Hasanbeigi, A., Kirshbaum, L. A., Collison, B., & Gardiner, D. (2021). Electrifying U.S. industry: A technology- and process-based approach to decarbonization. Renewable Thermal Collaborative. https://www.renewablethermal.org/electrifying-us-industry/

- Hoel, M. (1992). International environment conventions: The case of uniform reductions of emissions. Environmental and Resource Economics, 2, 141–159. https://doi.org/10.1007/BF00338240

- Hoppe, J., Grubb, M., Patt, A., & Hinder, B. (2021). The impact of mitigation policies on GHG emissions, proximate drivers, and low-carbon technologies: A review of empirical ex-post evidence. Zenodo. https://doi.org/10.5281/zenodo.5562910

- ICAP. (2021). Emissions trading worldwide: Status report 2021. International Carbon Action Partnership. https://icapcarbonaction.com/en/icap-status-report-2021

- Jaffe, A. B., Newell, R. G., & Stavins, R. N. (2002). Environmental policy and technological change. Environmental and Resource Economics, 22(1/2), 41–70. https://doi.org/10.1023/A:1015519401088

- Khan, J., & Johansson, B. (2022). Adoption, implementation and design of carbon pricing policy instruments. Energy Strategy Reviews, 40, 100801. https://doi.org/10.1016/j.esr.2022.100801

- Koch, N., Fuss, S., Grosjean, G., & Edenhofer, O. (2014). Causes of the EU ETS price drop: Recession, CDM, renewable policies or a bit of everything?—New evidence. Energy Policy, 73, 676–685. https://doi.org/10.1016/j.enpol.2014.06.024

- Koh, J., Johari, S., Shuib, A., Matthew, N. K., & Siow, M. L. (2021). Impacts of carbon pricing on developing economies. International Journal of Energy Economics and Policy, 11(4), 298–311. https://doi.org/10.32479/ijeep.11201

- Köppl, A., & Schratzenstaller, M. (2022). Carbon taxation: A review of the empirical literature. Journal of Economic Surveys, 1–36. https://doi.org/10.1111/joes.12531

- Lawley, C., & Thivierge, V. (2018). Refining the evidence: British Columbia’s carbon tax and household gasoline consumption. The Energy Journal, 39(2), 147–171. https://doi.org/10.5547/01956574.39.2.claw

- Lilliestam, J., Patt, A., & Bersalli, G. (2021). The effect of carbon pricing on technological change for full energy decarbonization: A review of empirical ex-post evidence. WIRES Climate Change, 12(1). https://doi.org/10.1002/wcc.681

- Lilliestam, J., Patt, A., & Bersalli, G. (2022). On the quality of emission reductions: observed effects of carbon pricing on investments, innovation, and operational shifts. A response to van den Bergh and Savin (2021). Environmental and Resource Economics, 83(3), 733–758. https://doi.org/10.1007/s10640-022-00708-8

- Lim, B., Hong, K., Yoon, J., Chang, J.-I., & Cheong, I. (2021). Pitfalls of the EU’s carbon border adjustment mechanism. Energies, 14(21), 7303. https://doi.org/10.3390/en14217303

- Löschel, A., Lutz, B. J., & Managi, S. (2019). The impacts of the EU ETS on efficiency and economic performance – An empirical analyses for German manufacturing firms. Resource and Energy Economics, 56, 71–95. https://doi.org/10.1016/j.reseneeco.2018.03.001

- Marcu, A., Mehling, M., & Cosbey, A. (2021). Border carbon adjustments in the EU: Issues and options. European Roundtable on Climate Change and Sustainable Transition (ERCST). https://ercst.org/border-carbon-adjustments-in-the-eu-issues-and-options/.

- Marten, M., & van Dender, K. (2019). The use of revenues from carbon pricing (OECD taxation working papers, No. 43). OECD Publishing. https://doi.org/10.1787/3cb265e4-en

- Mehling, M., & Haites, E. (2009). Mechanisms for linking emissions trading schemes. Climate Policy, 9(2), 169–184. https://doi.org/10.3763/cpol.2008.0524

- Naegele, H., & Zaklan, A. (2019). Does the EU ETS cause carbon leakage in European manufacturing? Journal of Environmental Economics and Management, 93, 125–147. https://doi.org/10.1016/j.jeem.2018.11.004

- Nilsson, L. J., Bauer, F., Åhman, M., Andersson, F. N. G., Bataille, C., de la Rue du Can, S., Ericsson, K., Hansen, T., Johansson, B., Lechtenböhmer, S., van Sluisveld, M., & Vogl, V. (2021). An industrial policy framework for transforming energy and emissions intensive industries towards zero emissions. Climate Policy, 21(8), 1053–1065. https://doi.org/10.1080/14693062.2021.1957665

- Nordhaus, W. (2015). Climate clubs: Overcoming free-riding in international climate policy. American Economic Review, 105(4), 1339–1370. https://doi.org/10.1257/aer.15000001

- Nurdiawati, A., & Urban, F. (2021). Towards deep decarbonisation of energy-intensive industries: A review of current status, technologies and policies. Energies, 14(9), 2408. https://doi.org/10.3390/en14092408

- OECD. (2021). Effective carbon rates 2021 - Pricing carbon emissions through taxes and emissions trading. OECD Publishing. https://doi.org/10.1787/0e8e24f5-en

- Parry, I., Black, S., & Roaf, J. (2021). Proposal for an international carbon price floor among large emitters (2021/001. Staff Climate Note). International Monetary Fund. https://www.elibrary.imf.org/view/journals/066/2021/001/066.2021.issue-001-en.xml

- Peñasco, C., Anadón, L. D., & Verdolini, E. (2021). Systematic review of the outcomes and trade-offs of ten types of decarbonization policy instruments. Nature Climate Change, 11(3), 257–265. https://doi.org/10.1038/s41558-020-00971-x

- Petek, G. (2020). Assessing California’s climate policies—Electricity generation. 1–32 pp. https://autl.assembly.ca.gov/sites/autl.assembly.ca.gov/files/CalifLAO-ElectricityEmissions.pdf

- Pollitt, M. F. (2016). A global carbon market? (Working Paper 1608). Energy Policy Research Group, University of Cambridge. https://www.eprg.group.cam.ac.uk/wp-content/uploads/2016/03/1608-PDF.pdf

- Pretis, F. (2022). Does a Carbon Tax Reduce CO2 Emissions? Evidence from British Columbia. Environmental and Resource Economics, 83(1), 115–144. https://doi.org/10.1007/s10640-022-00679-w

- Raymond, L. (2019). Policy perspective: Building political support for carbon pricing—Lessons from cap-and-trade policies. Energy Policy, 134, 110986. https://doi.org/10.1016/j.enpol.2019.110986

- Regional Greenhouse Gas Initiative (RGGI). 2019. The investment of RGGI proceeds in 2017. pp. 1–46. https://www.rggi.org/sites/default/files/Uploads/Proceeds/RGGI_Proceeds_Report_2017.pdf

- Rogelj, J., Geden, O., Cowie, A., & Reisinger, A. (2021). Net-zero emissions targets are vague: Three ways to fix. Nature, 591(7850), 365–368. https://doi.org/10.1038/d41586-021-00662-3

- Runst, P., & Thonipara, A. (2020). Dosis facit effectum why the size of the carbon tax matters: Evidence from the Swedish residential sector. Energy Economics, 91, 104898. https://doi.org/10.1016/j.eneco.2020.104898

- Stavins, R. (2022). The relative merits of carbon pricing instruments: Taxes versus trading. Review of Environmental Economics and Policy, 16(1), 62–82. https://doi.org/10.1086/717773

- Steenkamp, L.-A. (2021). A classification framework for carbon tax revenue use. Climate Policy, 21(7), 897–911. https://doi.org/10.1080/14693062.2021.1946381

- Steinebach, Y., & Limberg, J. (2022). Implementing market mechanisms in the Paris era: The importance of bureaucratic capacity building for international climate policy. Journal of European Public Policy, 29(7), 1153–1168. https://doi.org/10.1080/13501763.2021.1925330

- Thivierge, V. (2020). Carbon pricing and competitiveness pressures: The case of cement trade. Canadian Public Policy, 46(1), 45–58. https://doi.org/10.3138/cpp.2017-074

- van den Bergh, J., & Savin, I. (2021). Impact of carbon pricing on low-carbon innovation and deep decarbonisation: Controversies and path forward. Environmental and Resource Economics, 80(4), 705–715. https://doi.org/10.1007/s10640-021-00594-6

- van den Bergh, J. C. J. M. (2011). Energy conservation more effective with rebound policy. Environmental and Resource Economics, 48(1), 43–58. https://doi.org/10.1007/s10640-010-9396-z

- van Sluisveld, M. A. E., de Boer, H. S., Daioglou, V., Hof, A. F., & van Vuuren, D. P. (2021). A race to zero - Assessing the position of heavy industry in a global net-zero CO2 emissions context. Energy and Climate Change, 2, 100051. https://doi.org/10.1016/j.egycc.2021.100051

- Vogt-Schilb, A., Meunier, G., & Hallegatte, S. (2018). When starting with the most expensive option makes sense: Optimal timing, cost and sectoral allocation of abatement investment. Journal of Environmental Economics and Management, 88, 210–233. https://doi.org/10.1016/j.jeem.2017.12.001

- Weitzman, M. L. (2014). Can negotiating a uniform carbon price help to internalize the global warming externality? Journal of the Association of Environmental and Resource Economists, 1(1), 29–49. https://doi.org/10.1086/676039

- World Bank. (2022). State and trends of carbon pricing 2022. https://openknowledge.worldbank.org/handle/10986/37455

- Xiang, D., & Lawley, C. (2019). The impact of British Columbia’s carbon tax on residential natural gas consumption. Energy Economics, 80, 206–218. https://doi.org/10.1016/j.eneco.2018.12.004

- Yip, C. M. (2018). On the labor market consequences of environmental taxes. Journal of Environmental Economics and Management, 89, 136–152. https://doi.org/10.1016/j.jeem.2018.03.004

- Yip, C. M. (2020). The ins and outs of employment: Labor market adjustments to carbon taxes. ins_and_outs_of_employment.pdf (chimanyip.com)