?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Despite the potential benefits of agricultural insurance in helping farmers adapt to climate risks, its uptake among smallholder farmers remains limited. This study analyses the drivers of awareness and adoption of agricultural insurance in Nigeria to better understand the adoption process. 1,080 farming households were surveyed across six agro-ecological zones in Nigeria, covering areas with different socio-economic characteristics of farmers and levels of climate risk. Data were collected through face-to-face interviews between October 2020 and February 2021. The results show that more than half of the farmers were unaware of agricultural insurance. Logit regression results show that education, herd size, access to a bank, weather information, and flood experience positively influence awareness and adoption of agricultural insurance. In addition to low awareness, the main barriers to adoption are lack of knowledge about the effectiveness of insurance, difficulty in affording insurance, and farmers’ low level of trust in insurance providers. Late payment of claims and inadequate compensation were the main challenges faced by adopters of agricultural insurance. Raising awareness and helping farmers to assess the effectiveness of agricultural insurance, as well as developing a supportive institutional environment, would help to build a well-functioning insurance market.

Key policy insights

To increase the uptake of agricultural insurance, it is first necessary to raise awareness among farmers.

Government agencies should consider monitoring and sanctioning insurance agencies and companies that fail to comply with contractual agreements to promote and ensure prompt payment of due compensation; to increase transparency of insurance providers’ performance; and to increase confidence in insurance providers.

We recommend using different premium payment methods, adjusting land policies, improving access to weather information, and increasing access to bank credit for smallholder farmers to increase farmers’ motivation to use insurance.

1. Introduction

Farmers face multiple risks from climate change; crops can be destroyed by drought, floods or new pest and disease outbreaks (IFAD, Citation2010). As a result, weather variability leads to variability in yields and thus in welfare (Chavas J.P. et al., Citation2019; Di Falco et al., Citation2014; Skees et al., Citation2001). Weather risks are particularly burdensome for smallholder farmers in developing countries, whose livelihoods are largely dependent on agricultural production (IFAD, Citation2010; Omerkhil et al., Citation2020). In addition, smallholders tend to have very limited access to formal financial services, which increases their risk of climate and extreme weather vulnerability, slow economic development and poverty (IFAD, Citation2010). The adverse effects of climate change are expected to continue, leading to production losses in the sector and jeopardizing the achievement of the Sustainable Development Goals, particularly Goal 1, ‘Eradicate extreme poverty and hunger’, and Goal 7, ‘Ensure environmental stability’ (BNRCC, Citation2011).

Agricultural insurance is one of the modern risk management strategies available to make the agricultural system more resilient. It helps farmers to insure against the impacts of climate change on yield and income variability (Di Falco et al., Citation2014; Skees et al., Citation2008, Citation2015; Skees and Barnett, Citation2004) and serves as collateral for banks in loan servicing (Nnadi et al., Citation2013). Cash payments from an insurer improve farmers’ ability to make the necessary investments to adapt or maintain their current production strategies; insurance can also facilitate adaptation when bundled with new technologies (Collier et al., Citation2009; Elabed et al., Citation2013). Insurance can have a positive impact on the resilience of crop farmers, livestock keepers, food security and household consumption (Biglaria et al., Citation2019; De Nicola, Citation2015; De Nicola & Hill, Citation2013; FAO, Citation2021; IPPC, Citation2018; Thornton & Herrero, Citation2014).

In this context, agricultural insurance reduces the risk of crop failure, as do other strategies such as reduced tillage, irrigation, new varieties, etc. Insurance encourages risk-averse farmers to adopt riskier adaptive innovations that promise higher yields and incomes. In this way, insurance can stimulate innovation and development, not just protection against crop failure (Hansen et al., Citation2017). Some studies highlight the negative impacts of using agricultural insurance, such as over-reliance on insurance that may slow the adoption of other climate risk adaptations (Collier et al., Citation2009); moreover, subsidies may not be sustainable in the long run if the majority of farmers participate in an insurance programme with them (Budhathoki et al., Citation2019). In addition, the price of premiums may increase as climate risk increases, while farmers become dependent on insurance payouts without making efforts to adapt to the changing environment; thus, agricultural insurance itself may lead to moral hazard (Tadessa et al., Citation2015; Collier et al., Citation2009; Budhathoki et al., Citation2019). However, these negative effects are usually outweighed by the positive benefits (Cole & Xiong, Citation2017).

Because of its potential benefits, agricultural insurance has been recommended and promoted by intergovernmental organizations as one of the preferred climate change adaptation strategies (ARC, Citation2023; IPCC, Citation2018; IPCC, Citation2019; Nnadi et al., Citation2013; World Bank, Citation2014). Training and technical assistance have been provided to climate change stakeholders in developing countries, such as ministries of environment and agriculture, banks, insurance companies and brokers, farmer groups, and policymakers, to enable them to design local policies that create the institutional environment for well-functioning agricultural insurance markets (ARC, Citation2023; IFPRI, Citation2014; IWMI, Citation2021).

In 2010, Nigeria formally included insurance among its agricultural climate change adaptation strategies in its Nationally Determined Contribution (UNFCCC, Citation2015). With government support, the National Agricultural Insurance Corporation (NAIC) has offered insurance with a subsidy of up to 50% of the premium (World Bank, Citation2011), with the intention of expanding insurance among Nigerians, targeting approximately 15 million smallholder farmers (NAIC, Citation2021). Despite this support to stakeholders and the potential benefits of insurance to farmers, there has been low patronage and adoption of agricultural insurance in the country (Akinola, Citation2014; Falola et al., Citation2013; Ibitoye, Citation2013; Olajide-Adedamola & Akinbile, Citation2019). Literature from other developing countries such as South Africa, Iran, Nepal and Kenya revealed a similar situation (Biglaria et al., Citation2019; Budhathoki et al., Citation2019; Elum et al., Citation2017; Jensen et al., Citation2017; Jensen & Barrett, Citation2017; Marr et al., Citation2016; Oduniyi et al., Citation2020).

Various studies examine different aspects of agricultural insurance. These include examinations of appropriate agricultural financial management in a changing climate (Daron & Stainforth, Citation2014; Turvey et al., Citation2006; Woodard et al., Citation2016; Zhu et al., Citation2018). Other studies analyse how insurance contributes to social protection (Devereux, Citation2016; Jensen et al., Citation2017), affects farmers’ welfare (Chantarat et al., Citation2017), and is used to provide subsidies to farmers (Freudenreich & Mubhoff, Citation2018; Ricome et al., Citation2017). Some studies examine how insurance contributes to reducing rural poverty (Hansen et al., Citation2018) and increase social equity (Fisher et al., Citation2018). However, less attention has been paid in the literature to farmers’ awareness and adoption of agricultural insurance and the reasons for low adoption rates (Carter et al., Citation2016; Jin et al., Citation2016; Ntukamazina et al., Citation2017).

There is a consensus in the literature that awareness of an innovation, such as insurance, is a prerequisite and the first stage of its adoption. This is based on the Awareness, Interest, Evaluation, Trial and Adoption (AIETA) processes (Daberkow & Mcbride, Citation2003). These AIETA processes are influenced by information channels as postulated by diffusion of innovation theory (Rogers, Citation2003). Farmers’ financial capabilities may also influence their adoption behaviour, highlighting the role of wealth, such as income, livestock ownership and other assets, as depicted by resource-based theory (Below et al., Citation2014). Research shows that farmers who experience climate-related natural disasters and extreme weather events are more likely to be aware of and purchase insurance. This is because, as the need and necessity to offset the effects of emerging climate-related threats such as drought and flooding increases, farmers will seek new knowledge and techniques to help them overcome these constraints, as suggested by the protection motivation theory (Floyd et al., Citation2000).

This study examines the drivers of awareness and adoption of agricultural insurance by farmers. It attempts to provide answers to four questions: i) Are farmers aware of agricultural insurance as a climate risk adaptation strategy?; ii) What are the drivers of awareness and adoption of insurance as a climate risk adaptation strategy?; iii) What are the barriers to insurance adoption perceived by non-adopters?; and iv) What are the difficulties faced by farmers who have adopted this strategy? The study places the emerging insurance market in the economic context of a developing country, using the case of Nigeria. It contributes to the general understanding of the drivers of awareness and adoption of agricultural insurance. Because many farmers in developing countries, including Nigeria, are unaware of insurance, they cannot be interested in it and do not evaluate the benefits and costs, including the reduction of uncertainty for the household. Many farmers who are aware still struggle to understand the potential welfare effects and have low levels of trust in insurance providers, which discourages them from investing in insurance. This study adds to knowledge and provides insights for policy to help in the design and implementation of agricultural insurance as a key part of climate adaptation strategies. The remainder of the paper is organized as follows. Section 2 presents the methodology, followed by Section 3 which describes the results and provides a discussion, and finally Section 4 concludes.

2. Methodology

2.1. Study area

Nigeria lies between latitudes 4° and 14° N and longitudes 2° and 15° E. Rainfall ranges from 3,000 mm annually in the south to 1,800 mm in the southwest, decreasing progressively away from the coast to 500 mm in the far north. The average maximum temperature in the northern part is about 38 °C, while frost can occur at night during the same season (Britannica, Citation2021). The country has three main dry agro-ecological zones (AEZs) in the North: the semi-arid zone, the Sudanese savannah and the Guinean savannah. It also has three other humid AEZs in the South: Swamp Forest, Mangrove and Tropical Rainforest. Rainfall is bimodal in the humid/southern part of the country and unimodal in the dry AEZs in the North (World Climate Guide, Citation2019). The country has a landmass of 923,768 km2 and agricultural land covers 68 million ha, of which 34 million ha is arable land and 28 million ha is pasture (FAO, Citation2021). Agricultural insurance policy is promoted in the country to protect smallholder farmers against natural disasters and to ensure payment of adequate compensation sufficient to keep the farmer in business (See 1.0 section of the supplementary material).

2.2. Study sampling procedure

A multistage sampling procedure was used to select respondents for the quantitative structured questionnaire survey. First, to cover the whole of Nigeria, three states (Jigawa State from the semi-arid zone; Gombe State from the Sudanese savannah and Kaduna State from the Guinean savannah) were purposively selected from the dry AEZs and another three states (Imo State from the freshwater swamp, Ogun State from the tropical rainforest and Ondo State from the mangrove zone) from the humid AEZs (). Second, 2 local government areas (LGAs) were selected from each state. Thirdly, two wards were selected from each selected LGA to include 24 wards in all, and, fourthly, 45 farming households were randomly selected from each ward, resulting in the inclusion of 1,080 households in the study sample.

Figure 1. Map of the study area.

2.3. Data collection

Primary data were collected in face-to-face interviews by the author with the help of 12 trained enumerators (village extension workers) between October 2020 and February 2021, using a pen-and-paper structured questionnaire survey of 1,080 farmers. Farm household heads were interviewed or, in their absence, their representatives. Interviews were conducted in English or local languages (mainly Hausa, Igbo and Yoruba) and translated into English. The semi-structured questionnaire consisted of questions on household head characteristics, farm and institutional characteristics, climate risks experienced in the past 10 years and agricultural insurance information. The questionnaire (See 2.0 section of the supplementary material) was pre-tested with 40 farmers and modified accordingly; the pre-tested data were not included in the main primary analysis.

Two multivariate logistic regression models were used to analyse the variables influencing: i) farmers’ awareness, and ii) their use of agricultural insurance. Multicollinearity was tested using correlation analysis; the variable ‘type of credit’ was dropped because it is highly correlated with the variable ‘access to banks’; the variable ‘land ownership’ was also dropped because it is highly correlated with ‘type of land ownership.’ In addition, the Variance Inflation Factor (VIF) was used to test for multicollinearity among the remaining variables (), and none of the coefficients are greater than the recommended threshold of 5.0 (Akinwande et al., Citation2015). Both awareness and adoption of agricultural insurance fall into two categories: aware and unaware (awareness) or adopters and non-adopters (adoption). Since the dependent variables are binary in nature, the logistic regression model is appropriate for the analysis (Stoltzfus, Citation2011). Awareness of agricultural insurance can therefore be influenced by a number of factors,

(1)

(1) Where:

= indicates the probability that the head of the farm household is aware of agricultural insurance,

is a constant,

is the residual,

are the regression estimates,

denotes the set of explanatory variables or factors expected to influence awareness of agricultural insurance as a climate change adaptation measure ( of the supplementary material).

Table 1. Perceived climate-related disaster effects across agroecological zones in the last 10 years.

Adaptation to climate change refers to the adjustment of agricultural systems in response to actual and expected climatic and non-climatic stimuli and conditions, in order to avoid or reduce associated risks or to exploit potential opportunities (IPCC, Citation2001). Household decisions on whether to insure their crops or livestock are considered within the general framework of utility or profit maximization. It is assumed that economic agents (farmers) will use agricultural insurance only if the perceived utility or net benefit of using it is significantly higher than the cost. In this context, the farmer's expected utility is not observable, but the economic agent's behaviour can be observed through the decision to insure or not to insure the crop, as used in several studies (Bryan et al., Citation2013; Di Falco et al., Citation2011; Greene & Hensher, Citation2003; Mendelsohn, Citation2000). The potential explanatory variables expected to influence the perceived benefits leading to the adoption of agricultural insurance are summarized in .

Farmer’s expected benefits from the insurance are equal to ,

(2)

(2) thus,

Where: is the unobserved or latent variable which indicates that household i chooses to adopt agricultural insurance if the expected benefits are greater than zero (> 0).

is a constant,

is the residual, are the regression estimates,

denote the set of explanatory variables or factors that influence the expected benefits as guided by the theories as shown ( of the supplementary material). The statistical software STATA (version 14) was used for the analysis.

2.4.1. Variables influencing awareness and adoption of agricultural insurance

Based on the literature review, we selected factors influencing awareness and adoption of agricultural insurance and grouped them into socio-demographic, farm and institutional characteristics and climate risk experience based on the studies. We consider awareness as a step and a prerequisite for adoption; studies show that awareness of crop insurance as a climate risk mechanism was found to be influenced by gender, farm size and high level of education (Ghazanfar et al., Citation2015; Olila & Pambo, Citation2014). Access to credit was reported in the literature to influence awareness of agricultural insurance (Ghazanfar et al., Citation2015; Hountondji et al., Citation2018). Membership in a farmers’ cooperative was also found to influence awareness of agricultural insurance (Jatto, Citation2019). Since banks are one of the intermediaries in insurance market design in the country, we considered access to banks and cooperative association as proxies for access to credit and insurance information.

Regarding the effect of socio-demographic characteristics on the adoption of agricultural insurance, female farmers were more likely to adopt livestock insurance than their male counterparts (Chand et al., Citation2016). Age was found to affect the adoption of index-based livestock insurance (Oduniyi et al., Citation2020). Education influences the adoption of livestock insurance (Abugri et al., Citation2017; Chand et al., Citation2016; Oduniyi et al., Citation2020). Chand et al. (Citation2016) and Oduniyi et al. (Citation2020) found that farming experience in livestock rearing influences the adoption of livestock-based index insurance. The number of dependents in the household influences the decision to adopt index-based livestock insurance (Oduniyi et al., Citation2020). In terms of farm characteristics, herd size influences the decision of farmers to adopt livestock insurance (Chand et al., Citation2016). It has been reported that farm size influences the use of crop insurance (Budhathoki et al., Citation2019). With regard to institutional characteristics, the adoption of weather index insurance is influenced by access to bank/credit (Amare et al., Citation2019; Bogale, Citation2015; Budhathoki et al., Citation2019; Gine et al., Citation2008). In terms of climate risk experience, moisture stress and number of flood experiences are reported to affect crop insurance use (Amare et al., Citation2019; Bogale, Citation2015; Budhathoki et al., Citation2019).

3. Results and discussion

3.1. Description of the sample

The results ( of the supplementary material) show that adopters and non-adopters differ significantly on 5 of the 9 continuous descriptive variables. For example, the average age of adopters is 50.4 years compared to 47.9 years for non-adopters, which may have an impact on farmers’ awareness and adoption of agricultural insurance. In terms of years of formal education, adopters had an average of 10.4 years of formal education, significantly higher than non-adopters (8 years). Education plays an important role in understanding written information from banks, insurance brokers and agents, and in assessing the potential benefits of using agricultural insurance (Amare et al., Citation2019), which may influence farmers’ awareness and decision to use agricultural insurance. Agricultural insurance adopters have an average cultivated area of 4.5 ha, which is significantly higher than the 3.3 ha of non-adopters. The average number of livestock is 234 for adopters compared to 28 for non-adopters, and the average annual non-agricultural income is $123.2 for adopters compared to $83.7 for non-adopters. Higher livestock numbers and farmer incomes may provide farmers with the financial capacity to purchase insurance premiums, as the resource-based theory postulates (Below et al., Citation2014).

Table 2. Awareness and adoption of agricultural insurance (N = 1,080).

On the other hand, adopters and non-adopters differed significantly on 7 of the 10 categorical descriptive variables ( of the supplementary material). 89.58% of adopters are members of farmer groups, which is significantly higher than non-adopters (82.06%) who are not group members. Members of farmer groups are able to insure their farm on a collective basis, as provided by the Insurance Act (NAIC, Citation2017). This may facilitate the use of insurance among farmer group members. In addition, 94.79% of adopters own farmland, which is significantly higher than 60.04% of non-adopters who own farmland. On the other hand, 71.87% of the non-adopters were involved in off-farm livelihood activities. Farmers also differ in their access to agricultural extension services and credit. Agricultural insurance adopters have less access to extension services. 76.04% of adopters have access to extension services compared to 83.08% of non-adopters. This may have implications for the awareness and use of agricultural insurance as a reliable source of agricultural information for smallholder farmers in developing countries (Bryan et al., Citation2013). Conversely, in terms of access to credit, 65.62% of adopters have access to credit, which is statistically higher than 28.60% of non-adopters. Similarly, there is a significant difference in the type of credit used, with 66.67% of adopters having access to formal credit compared to 41.03% of non-adopters having access to formal credit. This may have implications as all formal agricultural credit is required by law in the country to be insured (NAIC, Citation2017), which may increase the ability of farmers to purchase insurance, as postulated by resource-based theory and experimented in India (Cole et al., Citation2013). In addition, most (88.47%) of agricultural insurance adopters have access to weather information, which is significantly higher than 69.75% of non-adopters. Furthermore, adopters have experienced more floods than non-adopters. Experienced farmers may be more proactive in insuring their farms against anticipated climate extremes, as suggested by the theory of protection motivation (Floyd et al., Citation2000).

Table 3. Awareness and adoption of agricultural insurance across agroecological zones.

3.2. Perceived climate-related disaster effects, awareness and adoption of agricultural insurance

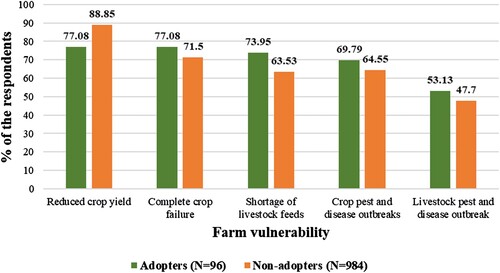

shows the proportions of farmers who experienced climate-related natural disasters in the last 10 years. The result shows that a higher proportion of agricultural insurance adopters experienced events that made their farms more vulnerable than non-adopters, with the exception of crop yield losses. The experience of climate-related natural disasters may lead farmers to adopt insurance, as suggested by the theory of protection motivation.

Figure 2. Perceived impact of climate-related disasters in the last 10 years.

shows that more farmers in dry AEZs perceive climate-related disaster effects on their farms than in humid AEZs. The most affected farmers were in semi-arid zones and the least in mangrove zones. This may be due to the frequency of droughts in the dry AEZs and the drought resilient ecosystem services provided by the mangrove AEZ.

The results in show that 48.6% of the farmers surveyed are aware of agricultural insurance as a climate change adaptation strategy. Thus, more than half of the farmers are not aware of agricultural insurance as a climate risk measure. Studies (Ankrah et al., Citation2021; Elum et al., Citation2017; Olajide-Adedamola & Akinbile, Citation2019) reported low awareness of agricultural insurance products as climate risk adaptation in Nigeria, Ghana and South Africa.

shows the distribution of awareness and adoption of agricultural insurance among farmers in the dry AEZs and the humid AEZs. In the dry AEZs, more farmers in the Sudanese savannah are aware of insurance and have a higher adoption rate than farmers in the semi-arid and Guinean savannah zones, which may be due to the incidence of drought in these zones. In the humid AEZs, more farmers in the tropical rainforest zone are aware of insurance and have a higher rate of adoption than farmers in the swamp forest and mangrove zones, probably due to the incidence of flooding in these zones and buffer ecoservices received from the Swamp forest and Mangrove AEZs. This pattern indicates the importance of awareness raising, as the results showed that the adoption of agricultural insurance increases as farmers’ awareness increases.

3.3.1. Determinants of awareness of agricultural insurance

The results in show the explanatory variables for awareness and adoption of agricultural insurance. The socio-demographic characteristics of household heads are found to influence awareness. For example, an increase in the age of farmers increases the likelihood of awareness of agricultural insurance. This may be due to the changes observed over time and the high perceived risks that lead them to seek available adaptation strategies. Farmers’ awareness of agricultural insurance also increases significantly with years of schooling (p < 0.01). Educated farmers are more likely to consult different institutions that promote agricultural insurance as an adaptation option and to understand written information about insurance products (Ghazanfar et al., Citation2015; Hountondji et al., Citation2018).

Table 4. Respondent awareness and adoption of agricultural insurance (N = 1,080).

In terms of farm characteristics, unexpectedly, farmers with small farms and non-livestock owners are more likely to be aware of agricultural insurance (p < 0.05). This may be due to their high vulnerability to climate risks, which leads them to seek new knowledge that will help them overcome these constraints, as suggested by the protection motivation theory. However, Olila and Pambo (Citation2014) reported a positive relationship between farm size and awareness of agricultural insurance in Kenya, although the result was not significant. As herd size increases, farmers are more likely to be aware of agricultural insurance (p < 0.10).

One possible reason is that farmers with large numbers of animals may find it difficult to manage their livestock because of climate risks, leading them to seek ways to minimize expected severe losses. Another plausible reason is that large herds may serve as a proxy for wealth, giving the farmer access to a variety of information sources and the ability to pay for insurance. In addition, the loss due to illness/disaster may be much higher than for farmers with smaller herds.

Regarding the effect of institutional characteristics, farmers who are members of a group, farmers with access to banks and farmers, and farmers with access to weather information are more likely to be aware of agricultural insurance. Most farmers receive information on agricultural innovations, new government policies and programmes during group meetings. Ibitoye (Citation2013) reported that 66% of farmers learn about agricultural insurance during farmers’ cooperative meetings. Thus, Jatto (Citation2019) reported the positive effect of cooperative membership on agricultural insurance awareness in Nigeria. Furthermore, the agricultural insurance market policy provides subsidies to support smallholder farmers who collectively insure their farms within a group (NAIC, Citation2017). In terms of access to banks, banks are intermediaries in the agricultural insurance market arrangement that bring farmers into contract with the NAIC (Olubiyo & Hillan, Citation2005). These banks provide loans that give farmers the financial ability to purchase insurance premiums. The positive effect of access to banks is consistent with the findings of Ghazanfar et al. (Citation2015), who reported a significant effect of credit availability on insurance awareness among farmers in Pakistan. The positive effect of access to weather information is that it helps farmers to know the expected climate risk, which leads them to seek proactive measures (Hountondji et al., Citation2018). Regarding the effect of climate risk experience on awareness of agricultural insurance, farmers who experience flood incidences are more likely to be aware of agricultural insurance. Flood incidence leads farmers to seek ways to make their farming business more resilient, and other ex-post management strategies that will keep them in business.

3.3.2. Determinants of the adoption of agricultural insurance

For the insurance adoption model, socio-demographic characteristics were found to influence the adoption of agricultural insurance by farmers. An increase in years of schooling significantly increases the likelihood of adoption (p < 0.05). Education plays a role in reducing cognitive failure, which is a psychological phenomenon that can affect an individual's willingness to spend their limited income to cover risks (Amare et al., Citation2019). The positive effect of education on agricultural insurance adoption is consistent with various studies (e.g. Abugri et al., Citation2017; Amare et al., Citation2019; Bogale, Citation2015; Chand et al., Citation2016; Oduniyi et al., Citation2020).

With regard to farm characteristics, farmers with statutory land tenure are more likely to use agricultural insurance than farmers with customary land tenure. This may be because legal land tenure is more secure than customary land tenure. This security of tenure allows farmers to make larger investments (Jianjun et al., Citation2015), and their own land can be used as collateral to access credit. In addition, farmers with large numbers of livestock are more likely to adopt agricultural insurance (p < 0.01). Livestock is a proxy for wealth that makes farmers financially capable, as explained by the resource-based theory. On the other hand, a large number of livestock requires a huge investment and running costs, which leads farmers to secure the investment by taking out agricultural insurance. Farmers with small herds may find it uneconomical to insure their livestock. Our findings on the positive effect of legal type of land tenure and herd size are consistent with Chand et al. (Citation2016).

In terms of institutional characteristics, access to extension services reduces the likelihood that the farmer will take out agricultural insurance (p < 0.05). Although the marginal effect is very small, this unexpected result may be partly explained by the fact that farmers who had access to extension services were more likely to be informed about different climate risk management strategies and therefore could choose from a greater variety of different risk diversification and mitigation options (Arshad et al., Citation2016; Barrett et al., Citation2001; Bryan et al., Citation2009; Budhathoki et al., Citation2019). Another possible reason is that extension organizations and agents, or some of them, were not involved in promoting agricultural insurance to farmers in the country. Insurance agents and brokers, banks and extension agents are the intermediaries responsible for bringing farmers into a business relationship with NAIC within the provisions of relevant laws, rules and regulations (Olubiyo & Hillan, Citation2005). In addition, farmers with access to banks are more likely to adopt agricultural insurance (p < 0.01). According to the resource-based theory, the ability to adopt depends on one's wealth and assets; in other words, farmers demand more security for their investments as their wealth increases (Marr et al., Citation2016). Another plausible reason is that access to credit helps farmers improve their financial capacity to pay insurance premiums (Amare et al., Citation2019). Moreover, poor people have a lower capacity to build capital for climate risk management and risk transfer, except through credit (Tadesse et al., Citation2015). The findings of this study are consistent with the literature (e.g. Budhathoki et al., Citation2019; Arshad et al., Citation2016; Tadesse et al., Citation2015; Abugri et al., Citation2017; Bogale, Citation2015). Farmers with access to weather information are more likely to use agricultural insurance (p < 0.01). This is likely because knowledge of expected weather and climate extremes leads farmers to prepare for expected climate risks (Hill et al., Citation2013).

Regarding the effect of climate risk experience, farmers who have experienced floods and droughts are more likely to purchase agricultural insurance (p < 0.05). This is explained by the protection motivation theory, which states that when a farmer experiences a threat in the environment in which he operates, he seeks techniques to disrupt the threat (Floyd et al., Citation2000). This finding is consistent with studies by Amare et al. (Citation2019), Bogale (Citation2015), and Akinola (Citation2014). Amare et al. (Citation2019) explained that insurance adoption is most likely to come from farming systems where household livelihood strategies are largely exposed to weather-related risks. Bogale (Citation2015) reported that farmers under conditions of moisture stress are more likely to adopt weather index insurance.

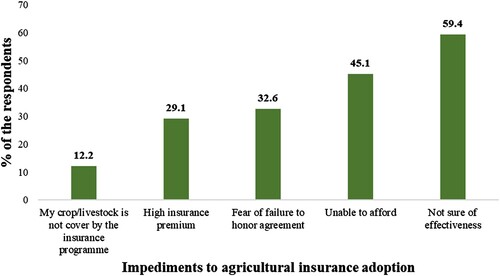

3.4. Reasons for not using agricultural insurance among those who are aware of it (N = 524)

shows the barriers to use of agricultural insurance as reported by farmers who are aware of it (48.61%). The main barrier reported by 59% of farmers is that they are not sure about the effectiveness of the insurance. This is confirmed by Ankrah et al. (Citation2021). In addition, 45% of farmers could not afford the insurance. This indicates the robustness of our inferential result, which showed the statistically significant effect of access to banks (credit) on the use of insurance, as also postulated by the resource-based theory. This is in line with Cole et al. (Citation2013), who reported that liquidity constraints are more important than education for the uptake of agricultural insurance, and further explains the experimental result that insurance uptake increases when a high cash reward is given before purchasing insurance.

Figure 3. Reasons for non-adoption given by non-adopters of agricultural insurance (N = 524).

Our results show that 32% of farmers say that the reason they do not buy insurance is because they are afraid that the insurance company will not honour the contract. This suggests that farmers’ trust in agricultural insurance companies is an important reason why farmers choose to insure their farms. This is consistent with several studies (e.g. Budhathoki et al., Citation2019; Cole et al., Citation2013; Giné et al., Citation2010; Ibitoye, Citation2013; Marr et al., Citation2016). Also, 29.10% of farmers reported that the high premium price discourages them from using agricultural insurance (consistent with, e.g. Ali et al., Citation2020; Ghazanfar et al., Citation2015; Ibitoye, Citation2013; Kong et al., Citation2011).

3.5. Difficulties faced by adopters of agricultural insurance and their views on its performance

shows how long farmers have been using agricultural insurance and their views on the performance of the strategy. The majority (75%) of farmers have used agricultural insurance in the last 5 years, another 20% in the last 10 years, and only 1% at the beginning of the last two decades. This may indicate that the strategy is following the normal process of ‘technology diffusion’ in relation to time and society, as postulated by Rogers (Citation2003). Finally, the result also shows that 54.8% of farmers rate the performance of agricultural insurance as good or very good, based on their personal assessment, while only 27.9% rate it as poor.

Table 5. Farmers’ opinions on the performance of agricultural insurance (N = 96).

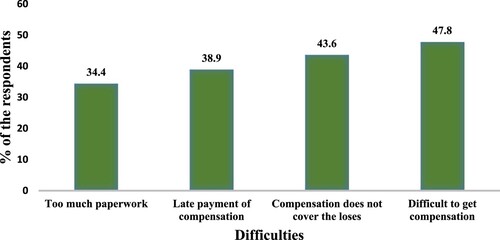

shows the reported challenges associated with agricultural insurance as a climate change adaptation strategy. These results show that 47.8% and 38.9% of farmers experienced difficulties in accessing compensation and late payment of compensation, respectively. Previous studies have also highlighted late payment of compensation as the main reason for low uptake (e.g. Ajieh, Citation2010; Broberg, Citation2019; Ghimire et al., Citation2016; Johnson et al., Citation2018; Marr et al., Citation2016). Furthermore, 43.6% of insurance users reported that compensation did not cover farmers’ losses. This implies that the objective of agricultural insurance to keep farmers in the business ex-post risk and disaster is not always achieved; therefore, the objective is defeated when compensation cannot cover the losses incurred (Ajieh, Citation2010; Nordlander et al., Citation2019). Finally, 34.5% of farmers reported that there is too much paperwork and administration during the registration and compensation application process (see similar findings from Budhathoki et al., Citation2019).

Figure 4. Difficulties encountered by users of agricultural insurance (N = 96).

4. Conclusions

This study sought to understand the drivers of awareness and adoption of agricultural insurance by farmers in Nigeria, as well as the reasons for non-adoption of the strategy and the difficulties faced by farmers who have adopted insurance. More than half of the farmers surveyed are not aware of agricultural insurance as a climate risk management strategy and only 8.9% have adopted it. In order to achieve an adoption rate of 20% (15 million smallholder farmers), as envisaged by the government in its NARF programme, awareness of agricultural insurance, understanding of the procedures involved and of the welfare effects of insurance, as well as confidence in the system, need to be increased among farmers.

Our results show that agricultural insurance campaigns can raise awareness of agricultural insurance when targeting young farmers, farmers with low levels of education, landless farmers, and those who do not have access to banks. In addition, farmers with a small number of household members, small farm sizes, and farmers without livestock should also be targeted when promoting agricultural insurance because they are particularly vulnerable. The use of cooperatives and other farmer-led groups can play a potentially important role in raising farmers’ awareness of insurance. Improving access to banks for financing climate action and access to weather information also helps to increase the use of insurance among resource-poor smallholder farmers.

Legal land tenure also helps to promote the uptake of agricultural insurance. The government should reform policies so that farmers with customary land tenure can apply for and easily obtain a certificate of legal ownership. The non-adopters also report that they could not afford insurance. Secure land tenure will allow land to be used as collateral for loans, which will increase farmers’ financial capacity to purchase agricultural insurance. In addition, subsidies are already part of the NARF programme. However, it is not entirely clear whether all farmers are aware of the subsidy and how they can benefit from it, or whether the subsidy is sufficient. Further research is needed to refine the programme and address all these issues that block uptake. Different modes of payment could be introduced, such as cash, in-kind and instalment payments, and access to micro-credit could be improved to help farmers and overcome the problem of low financial capacity.

Our results also showed that agricultural insurance products are difficult to understand, especially for populations with low literacy rates. This suggests that information on insurance products needs to be simplified to support decision-making by farmers with low levels of education. Since nearly 60% of the non-adopters indicated that they were not sure about the effectiveness of insurance products, government agencies can consider providing risk models and cost–benefit analyses that are tailored to farmers in different locations and with examples from different types of farming systems. This will help farmers to assess the risk exposure and welfare effects of agricultural insurance, as insurance may not always be the best strategy to adapt to climate risks. Extension services can also play a crucial role in disseminating information through various channels, such as training, farm visits and the media. Informal education by extension workers can help farmers to read and understand the terms and conditions of agricultural insurance policies.

A key problem associated with insurance, reported by both non-adopters and adopters, is that farmers fear that insurance companies will not honour agreements. This includes concern about as difficulties to obtain compensation and inadequate or late payouts. Some farmers have direct experience of such failures. The government and agricultural insurance companies could work together to implement policies that increase farmers’ confidence in insurance, for example by: i) reducing the challenges of meeting contractual obligations to farmers who take out insurance; ii) establishing a unit to monitor and provide information on claims payouts by insurance companies; and iii) regulating and, where necessary, sanctioning non-performing insurance companies to ensure strict adherence to contractual agreements. Finally, the government can help by providing local and farming system-specific information on the welfare effects of agricultural insurance. Taken together, these measures combined with improved institutions could help to raise awareness and confidence among adopters, while allaying the fears of non-adopters.

A limitation of the study is that it does not distinguish between the different types of agricultural insurance used by farmers. In addition, the study does not examine the costs and benefits of agricultural insurance to consumers, or consumer behavioural characteristics, including risk aversion. However, these are all important for understanding the potential welfare contributions of agricultural insurance; future research is particularly needed on the welfare effects in countries with emerging insurance markets.

Supplemental Material

Download MS Word (36.6 KB)Acknowledgements

The study acknowledges the Faculty of Tropical AgriSciences, Czech University of Life Sciences, Prague for funding the research (IGA20223113). The Abubakar Tafawa Balewa University Bauchi, Nigeria, for its oversight role in data collection, in particular the Department of Agricultural Economics and Extension headed by Professor M. H. Sani.

The research has been approved by the Board of the Faculty of Tropical Agriculture to comply with the ICJME Guidelines for the Protection of Research Participants, the Belmont Report or the Declaration of Helsinki, as appropriate.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Abugri, S. A., Amikuzuno, J., & Daadi, E. B. (2017). Looking out for a better mitigation strategy: Smallholder farmers’ willingness to pay for drought-index crop insurance premium in the Northern region of Ghana. Agriculture and Food Security, 6(1), 71–80. https://doi.org/10.1186/s40066-017-0152-2

- Ajieh, P. C. (2010). Poultry farmers’ response to agricultural insurance in delta state. Nigeria. J Agri Sci, 1(1), 43–47.

- Akinola, B. D. (2014). Determinants of farmers’ adoption of agricultural insurance: The case of poultry farmers in Abeokuta Metropolis of Ogun State, Nigeria. British Journal of Poultry Sciences, 3(2), 36–41.

- Akinwande, M. O., Dikko, H. G., & Samson, A. (2015). Variance inflation factor: As a condition for the inclusion of suppressor variable(s) in regression analysis. Open Journal of Statistics, 5(7), 754–767. https://doi.org/10.4236/ojs.2015.57075

- Ali, E., Egbendewe, Y. G. E., Abdoulaye, T., & Sarpong, D. B. (2020). Willingness to pay for weather index-based insurance in semi-subsistence agriculture: Evidence from northern Togo. Climate Policy, https://doi.org/10.1080/14693062.2020.1745742

- Amare, A., Simane, B., Nyangaga, J., Defisa, A., Hamza, D., & Gurmessa, B. (2019). Index-based livestock insurance to manage climate risks in Borena Zone of Southern Oromia, Ethiopia. Climate Risk Management, 100191. https://doi.org/10.1016/j.crm.2019.100191

- Ankrah, D. A. A., Kwapong, N. A., Dennis Eghan, D., Adarkwah, F., & Boateng-Gyambiby, D. (2021). Agricultural insurance access and acceptability: Examining the case of smallholder farmers in Ghana. Agriculture & Food Security, 10(1), 19. https://doi.org/10.1186/s40066-021-00292-y

- ARC. (2023). African Risk Capacity Strategic Framework. https://www.arc.int/arc-strategic-framework

- Arshad, M., Amjath-Babu, T. S., Kächele, H., & Müller, K. (2016). What drives the willingness to pay for crop insurance against extreme weather events (flood and drought) in Pakistan? A hypothetical market approach. Climate and Development, 8, 234–244. https://doi.org/10.1080/17565529.2015.1034232

- Barrett, C. B., Reardon, T., & Webb, P. (2001). Non-farm income diversification and household livelihood strategies in rural Africa: Concepts, dynamics, and policy implications. Food Policy, 26(4), 315–331. https://doi.org/10.1016/S0306-9192(01)00014-8

- Below, T. B., Schmid, J. C., & Sieber, S. (2014). Farmers’ knowledge and perception of climatic risks and options for climate change adaptation: A case study from two Tanzanian villages. Regional Environmental Change, 15(7), 1169–1180. https://doi.org/10.1007/s10113-014-0620-1

- Biglaria, T., Maleksaeidi, H., Eskandari, F., & Jalali, M. (2019). Livestock insurance as a mechanism for household resilience of livestock herders to climate change: Evidence from Iran. Land Use Policy, 87, 104043. https://doi.org/10.1016/j.landusepol.2019.104043

- BNRCC. (2011). National adaptation strategy and plan of action on climate change for Nigeria (NASPA-CCN). Prepared for the Federal Ministry of Environment Special Climate Change Unit http://csdevnet.org/wp-content/uploads/NATIONAL-ADAPTATION-STRATEGY-ANDPLAN-OF-ACTION.pdf

- Bogale, A. (2015). Weather-indexed insurance: An elusive or achievable adaptation strategy to climate variability and change for smallholder farmers in Ethiopia. Climate and Development, 7(3), 246–256. https://doi.org/10.1080/17565529.2014.934769

- Britannica. (2021). Climate of Nigeria. https://www.britannica.com/place/Nigeria/Climate

- Broberg, M. (2019). Parametric loss and damage insurance schemes as a means to enhance climate change resilience in developing countries. Climate Policy, 20, 1–11. https://doi.org/10.1080/14693062.2019.1641461

- Bryan, E., Deressa, T. T., Gbetibouo, G. A., & Ringler, C. (2009). Adaptation to climate change in Ethiopia and South Africa: Options and constraints. Environmental Science & Policy, 12(4), 413–426. https://doi.org/10.1016/j.envsci.2008.11.002

- Bryan, E., Ringler, C., Okoba, B., Roncoli, C., Silvestri, S., & Herrero, M. (2013). Adapting agriculture to climate change in Kenya: Household strategies and determinants. Journal of Environmental Management, 114, 26–35. https://doi.org/10.1016/j.jenvman.2012.10.036

- Budhathoki, N. K., Lassa, J. A., Pun, S., & Zander, K. K. (2019). Farmers’ interest and willingness to pay for index-based crop insurance in the lowlands of Nepal. Land Use Policy, 85, 1–10. https://doi.org/10.1016/j.landusepol.2019.03.029

- Carter, M. R., Cheng, L., & Sarris, A. (2016). Where and how index insurance can boost the adoption of improved agricultural technologies. Journal of Development Economics, 118, 59–71. https://doi.org/10.1016/j.jdeveco.2015.08.008

- Chand, S., Bhattarai, M., Kumar, A., & Saroj, S. (2016). Status and determinants of livestock insurance in India: A micro-level evidence from Haryana and Rajasthan. Indian Journal of Agricultural Economics, 71(3), 335–346.

- Chantarat, S., Mude, A. G., Barrett, C. B., & Turvey, C. G. (2017). Welfare impacts of index insurance in the presence of a poverty trap. World Development, 94, 119–138. https://doi.org/10.1016/j.worlddev.2016.12.044

- Chavas J.P., D. F., Adinolfi F, S., & Capitanio, F. (2019). Weather effects and their long-term impact on the distribution of agricultural yields: Evidence from Italy. European Review of Agricultural Economics, 46(1), 29–51. https://doi.org/10.1093/erae/jby019

- Cole, S., Giné, X., Tobacman, J., Townsend, R., Topalova, R., & Vickery, J. (2013). Barriers to household risk management: Evidence from India. American Economic Journal: Applied Economics, 5(1), 104–135. https://doi.org/10.1257/app.5.1.104

- Cole, S. A., & Xiong, W. (2017). Agricultural insurance and economic development. Annual Review of Economics, 9(1), 235–262. https://doi.org/10.1146/annurev-economics-080315-015225

- Collier, B., Skees, J., & Barnett, B. (2009). Weather index insurance and climate change: Opportunities and challenges in lower income countries. The Geneva Papers on Risk and Insurance - Issues and Practice, 34(3), 401–424. https://doi.org/10.1057/gpp.2009.11

- Daberkow, S. G., & Mcbride, W. D. (2003). Farm and operator characteristics affecting the awareness and adoption of precision agriculture technologies in the US. Precision Agriculture, 4(2), 163–177. https://doi.org/10.1023/A:1024557205871

- Daron, J. D., & Stainforth, D. A. (2014). Assessing pricing assumptions for weather index insurance in a changing climate. Climate Risk Management, 1, 76–91. https://doi.org/10.1016/j.crm.2014.01.001

- De Nicola, F. (2015). Handling the weather: Insurance, savings, and credit in West Africa. World Bank Policy Research Working Paper No. 7187, San Diego, CA.

- De Nicola, F., & Hill, R. V. (2013). Interplay among credit, weather insurance and savings for farmers in Ethiopia, presentation at the American Economic Association Meetings.

- Devereux, S. (2016). Social protection for enhanced food security in sub-Saharan africa. Food Policy, 60, 52–62. https://doi.org/10.1016/j.foodpol.2015.03.009

- Di Falco, S., Bozzola, M., Adinolfi, F., & Capitanio, F. (2014). Crop insurance as a strategy for adapting to climate change. Journal of Agricultural Economics, 65(2), 485–504. https://doi.org/10.1111/1477-9552.12053

- Di Falco, S., Veronesi, M., & Yesuf, M. (2011). Does adaptation to climate change provide food security? A micro-perspective from Ethiopia. American Journal of Agricultural Economics, 93(3), 825–842. https://doi.org/10.1093/ajae/aar006

- Elabed, G., Bellemare, M. F., Carter, M. R., & Guirkinger, C. (2013). Managing basis risk with multiscale index insurance. Agricultural Economics, 44(4-5), 419–431. https://doi.org/10.1111/agec.12025

- Elum, Z. A., Modise, D. M., & Marr, A. (2017). Farmer’s perception of climate change and responsive strategies in three selected provinces of South Africa. Climate Risk Management, 16, 246–257. https://doi.org/10.1016/j.crm.2016.11.001

- Falola, A., Ayinde, O. E., & Agboola, B. O. (2013). Willingness to take agricultural insurance by cocoa farmers in Nigeria. International Journal of Food and Agricultural Economics, 1(1), 97–107. https://doi.org/10.22004/ag.econ.156837

- FAO. (2021). Nigerian demographics. http://www.fao.org/faostat/en/#country/159

- Fisher, E., Hellin, J., Greatrex, H., & Jensen, N. (2018). Index insurance and climate risk management: Addressing social equity. Development Policy Review, 37, 581–602. https://doi.org/10.1111/dpr.12387

- Floyd, D. L., Prentice-Dunn, S., & Rogers, R. W. (2000). A meta-analysis of research on protection motivation theory. Journal of Applied Social Psychology, 30(2), 407–429. https://doi.org/10.1111/j.1559-1816.2000.tb02323.x

- Freudenreich, H., & Mubhoff, O. (2018). Insurance for technology adoption: An experimental evaluation of schemes and subsidies with maize farmers in Mexico. Journal of Agricultural Economics, 69(1), 96–120. https://doi.org/10.1111/1477-9552.12226

- Ghazanfar, S., Qi-wen, Z., Abdullah, M., Ahmad, Z., & Lateef, M. (2015). Farmers’ perception and awareness and factors affecting awareness of farmers regarding crop insurance as a risk coping mechanism evidence from Pakistan. Journal of Northeast Agricultural University (English Edition), 22(1), 76–82. https://doi.org/10.1016/s1006-8104(15)30010-6

- Ghimire, Y. N., Timsina, K. P., & Gauchan, D. (2016). Risk management in agriculture: Global experiences and lessons for Nepal. Nepal agricultural Research Council (NARC), Socioeconomics and Agricultural Policy Research Division. Lalitpur, Government of Nepal, Nepal.

- Giné, X., Menand, L., Townsend, R. M., & Vickery, J. I. (2010). Microinsurance: A case study of the Indian rainfall index insurance market. World Bank Policy Research working paper series, World Bank, Washington, DC.

- Gine, X., Townsend, R., & Vickery, J. (2008). Patterns of rainfall insurance participation in rural India. The World Bank Economic Review, 22(3), 539–566. https://doi.org/10.1093/wber/lhn015

- Greene, W. H., & Hensher, D. A. (2003). A latent class model for discrete choice analysis: Contrasts with mixed logit. Transportation Research Part B: Methodological, 37(8), 681–698. https://doi.org/10.1016/s0191-2615(02)00046-2

- Hansen, J., Hellin, J., Rosenstock, T., Fisher, E., Cairns, J., Stirling, C., Lamanna, C., van Etten, J., Rose, A., & Campbell, B. (2018). Climate risk management and rural poverty reduction. Agricultural Systems, 172, 28–46. https://doi.org/10.1016/j.agsy.2018.01.019

- Hansen, J. W., Araba, D., Hellin, J., & Goslinga, R. (2017). A roadmap for evidence-based insurance development for Nigeria’s farmers. CCAFS Working Paper no. 218. Wageningen, Netherlands: CGIAR Research Program on Climate Change, Agriculture and Food Security (CCAFS). www.ccafs.cgiar.org

- Hill, R. V., Hoddinott, J., & Kumar, N. (2013). Adoption of weather-index insurance: Learning from willingness to pay among a panel of households in rural Ethiopia. Agricultural Economics, 44(4–5), 385–398. https://doi.org/10.1111/agec.12023

- Hountondji, R. L., Tovignan, S., & Hountondji, P. S. (2018). Determinants of farmers awareness about crop insurance case of Ouesse District, Benin. International Journal of Progressive Sciences and Technologies (IJPSAT), 12, 37–45. https://ijpsat.ijsht-journals.org

- Ibitoye, S. J. (2013). Assessment of the levels of awareness and use of agricultural insurance scheme among the rural farmers in Kogi State, Nigeria. International Journal of Agricultural Science, Research and Technology, 2(3), 143–148. http://www.ijasrt.com/.

- IFAD. (2010). The potential for scale and sustainability in weather index insurance for agriculture and rural livelihoods. https://www.ifad.org/documents/38714170/40239486/The+potential+for+scale+and+sustainability+in+weather+index+insurance+for+agriculture+and+rural+livelihoods.pdf/7a8247c7-d7be-4a1b-9088-37edee6717ca

- IFPRI. (2014). National crop insurance programme: Challenges and opportunities. https://ccafs.cgiar.org/events/workshop-national-crop-insurance-programme-challenges-and-opportunities

- IPCC. (2001). Climate change 2001: synthesis report. contribution of working groups I, II and III to the third assessment report of the Intergovernmental Panel on Climate Change. IPCC.

- IPCC. (2018). Summary for policymakers. In: Global warming of 1.5°C. An IPCC special report on the impacts of global warming of 1.5°C above pre-industrial levels and related global greenhouse gas emission pathways, in the context of strengthening the global response to the threat of climate change, sustainable development and efforts to eradicate poverty (eds.)]. World Meteorological Organization, Geneva, Switzerland, pp. 32.

- IPCC,. (2019). Climate change and land: An IPCC special report on climate change, desertification, land degradation, sustainable land management, food security, and greenhouse gas fluxes in terrestrial ecosystems. 2019 Intergovernmental Panel on Climate Change. Electronic copies of this report are available from the IPCC website www.ipcc.ch. pp. 511

- IWMI,. (2021). Bundled solutions with seed systems, index insurance and climate information to manageagricultural risks (BICSA). https://cgspace.cgiar.org/bitstream/handle/10568/114115/BICSA%20workshop%20Report_june%202021.pdf

- Jatto, N. A. (2019). Assessment of farmer’s awareness of agricultural insurance packages: Evidence from “Farming is our pride” communities of Zamfara State, Nigeria. AGRICULTURA TROPICA ET SUBTROPICA, 52(2), 79–83. https://doi.org/10.2478/ats-2019-0009

- Jensen, N., & Barrett, C. (2017). Agricultural index insurance for development. Applied Economic Perspectives and Policy, 39(2), 199–219. https://doi.org/10.1093/aepp/ppw022

- Jensen, N. D., Barrett, C. B., & Mude, A. G. (2017). Cash transfers and index insurance: A comparative impact analysis from northern Kenya. Journal of Development Economics, 129, 14–28. https://doi.org/10.1016/j.jdeveco.2017.08.002

- Jianjun, J., Yiwei, G., Xiaomin, W., & Nam, P. K. (2015). Farmers’ risk preferences and their climate change adaptation strategies in the yongqiao district, China. Land Use Policy, 47, 365–372. https://doi.org/10.1016/j.landusepol.2015.04.028

- Jin, J., Wang, W., & Wang, X. (2016). Farmers’ risk preferences and agricultural weather index insurance uptake in rural China. International Journal of Disaster Risk Science, 7(4), 366–373. https://doi.org/10.1007/s13753-016-0108-3

- Johnson, L., Wandera, B., Jensen, N., & Banerjee, R. (2018). Competing expectations in an index-based livestock insurance project. The Journal of Development Studies, 55, 1–19. https://doi.org/10.1080/00220388.2018.1453603

- Kong, R., Turvey, C. G., He, G., Ma, J., & Meagher, P. (2011). Factors influencing shaanxi and Gansu farmers’ willingness to purchase weather insurance. China Agricultural Economic Review, 3(4), 423–440. https://doi.org/10.1108/17561371111192293

- Marr, A., Winkel, A., van Asseldonk, M., Lensink, R., & Bulte, E. (2016). Adoption and impact of index-insurance and credit for smallholder farmers in developing countries. Agricultural Finance Review, 76(1), 94–118. https://doi.org/10.1108/afr-11-2015-0050

- Mendelsohn, R. (2000). Efficient adaptation to climate change. Climatic Change, 45(3/4), 583–600. https://doi.org/10.1023/A:1005507810350

- NAIC. (2017). Nigerian agricultural insurance profile. https://cdn.cseindia.org/userfiles/agricultural-insurance-nigeria.pdf

- NAIC. (2021). Nigerian Agricultural Insurance Corporation. https://www.devex.com/organizations/nigerian-agricultural-insurance-corporation-48805

- Nnadi, F. N., Chikaire, J., Echetama, J. A., Ihenacho, R. A., & Umunnakwe, P. C. (2013). Agricultural insurance: A strategic tool for climate change adaptation in the agricultural sector. Net Journal of Agricultural Science, 1(1), 1–9. https://www.netjournals.org/pdf/NJAS/2013/1/13-020.pdf.

- Nordlander, L., Pill, M., & Martinez, R. B. (2019). Insurance schemes for loss and damage: Fools’ gold? Climate Policy, 20, 1–11. https://doi.org/10.1080/14693062.2019.1671163

- Ntukamazina, N., Onwonga, R. N., Sommer, R., Rubyogo, J. C., Mukankusi, C. M., Mburu, J., & Kariuki, R. (2017). Index-based agricultural insurance products: Challenges, opportunities and prospects for uptake in Sub-sahara Africa. Journal of Agriculture and Rural Development in the Tropics and Subtropics (JARTS), 118(2), 171–185. http://www.urn.fi/urn:nbn:de:hebis:34-2017042052372.

- Oduniyi, O. S., Antwi, M. A., & Tekana, S. S. (2020). Farmers’ willingness to pay for index-based livestock insurance in the North West of South Africa. Climate, 8(3), 47. https://doi.org/10.3390/cli8030047

- Olajide-Adedamola, F. O., & Akinbile, L. A. (2019). Inhibitors and motivators of adoption of agricultural insurance in Nigeria. International Journal of Agricultural Management and Development (IJAMAD, 9(3), 285–292. https://ageconsearch.umn.edu/record/301183/

- Olila, D. O., & Pambo, K. O. (2014). Determinants of Farmers’ awareness about crop insurance: Evidence from Trans-Nzoia County, Kenya. Selected paper prepared for oral presentation at the 8th Annual Egerton University International Conference: 26th – 28th March, 2014.

- Olubiyo, S. O., & Hillan, G. P. (2005). Assessment of the operation of agricultural insurance scheme in Nigeria. Savings and Development, 29(3), 293–312. https://www.jstor.org/stable/25830901.

- Omerkhil, N., Chand, T., Valente, D., Alatalo, J. M., & Pandey, R. (2020). Climate change vulnerability and adaptation strategies for smallholder farmers in Yangi Qala District, Takhar, Afghanistan. Ecological Indicators, 110, 105863. https://doi.org/10.1016/j.ecolind.2019.10586

- Ricome, A., Affholder, F., Gerard, F., Muller, B., Poeydebat, C., Quirion, P., & Sall, M. (2017). Are subsidies to weather-index insurance the best use of public funds? A bio-economic farm model applied to the Senegalese groundnut basin. Agricultural Systems, 156, 149–176. https://doi.org/10.1016/j.agsy.2017.05.015

- Rogers, E. M. (2003). Diffusion of innovations. 5th ed., Free Press. p. 512.

- Skees, J. R., Barnett, B. J., & Collier, B. (2008). Agricultural insurance, background and context for climate adaptation discussions. Developed for the OECD “Expert Workshop on Economic Aspects of Adaptation” held in Paris, France, April 7-8, 2008. Published by GlobalAgRisk, Inc. 1008 S. Broadway Lexington, KY 40504 859.489.6203.

- Skees, J. R., Gober, S., Varangis, P., Lester, R., & Kalavakonda, V. (2001). Developing rainfall-based index insurance in Morocco. The World Bank.

- Skess, J. R., & Barnett, B. J. (2004). Challenges in government facilitated crop insurance. In Book “China in Global Economy: Rural Finance and Credit infrastructure in China”, 172–185.

- Stoltzfus, J. C. (2011). Logistic regression: A brief primer. Academic Emergency Medicine, 18(10), 1099–1104. https://doi.org/10.1111/j.1553-2712.2011.01185.x

- Tadesse, M. A., Shiferaw, B. A., & Erenstein, O. (2015). Weather index insurance for managing drought risk in smallholder agriculture: Lessons and policy implications for sub-Saharan Africa. Agricultural and Food Economics, 3(26), 2–21. https://doi.org/10.1186/s40100-015-0044-3

- Thornton, P. K., & Herrero, M. (2014). Climate change adaptation in mixed crop-livestock systems in developing countries. Global Food Security, 3(2), 99–107. https://doi.org/10.1016/j.gfs.2014.02.002

- Turvey, C. G., Weersink, A., & Celia Chiang, S. H. (2006). Pricing weather insurance with a randomstrike price: The Ontario ice-wine harvest. American Journal of Agricultural Economics, 88(3), 696–709. https://doi.org/10.1111/j.1467-8276.2006.00889.x

- UNFCCC. (2015). Nigeria’s intended nationally determined contribution. https://www4.unfccc.int/sites/ndcstaging/PublishedDocuments/Nigeria%20First/Approved%20Nigeria’s%20INDC_271115.pdf

- Woodard, J. D., Shee, A., & Mude, A. (2016). A spatial econometric approach to designing and rating scalable index insurance in the presence of missing data. The Geneva Papers on Risk and Insurance – Issues and Practice, 41(2), 259–279. https://doi.org/10.1057/gpp.2015.31

- World Bank. (2011). Nigeria crop weather index insurance pre-feasibility study report. https://www.indexinsuranceforum.org/sites/default/files/NIGERIA_Weather_Index_Insurance_Feasibility_Study_Final%2BReport%2BEdits2%2Baccepted_0.pdf

- World Bank. (2014). Reducing the vulnerability of Azerbaijan’s agricultural systems to climate change, impact assessment and adaptation options. Published by World Bank Washington, D.C. pp. 94. http://doi.org/10.1596/978-1-4648-0184-6

- World Climate Guide. (2019). Nigerian climate: Average weather, temperature, precipitation and best time. https://www.climatestotravel.com/climate/nigeria

- Zhu, W., Porth, L., & Tan, K. S. (2018). A credibility-based yield forecasting model for crop reinsurance pricing and weather risk management. Agricultural Finance Review, 79, 2–26. https://doi.org/10.1108/afr-08-2017-0064