ABSTRACT

The push for decarbonization is dampening resource prospects in nations with undeveloped oil and gas. It is critical to reduce greenhouse gas (GHG) emissions from the petroleum sector, but there are equity issues related to requiring a shift away from oil and gas before development gains are made, especially in countries that have contributed very little to historical emissions. We review the prospects for five emerging producers to produce oil and gas at the lowest emissions intensity while achieving their economic and environmental goals. We find they lack the required capacity for stringent emissions management and to manage transition risks. The low-carbon pathway presents its own challenges with plans that lack national specificity and offer no substitute to the fiscal potential of the petroleum sector, and a lack of supportive technical assistance and finance. A just transition (JT) approach in these countries will not be about reskilling as they move away from a petroleum dependent economy, but instead about engaging with citizens to break the mould of petroleum-led development expectations and defining the new pathway for development. These countries will require support for transition planning that ensures that any oil and gas production minimizes GHG emissions, and limits the risk of economic lock-in, to invest in broad-based benefits and in a credible shift to a low-carbon economy. Inadequate international support risks leaving some countries behind, or to essential changes being contested in the transition.

Key policy insights

Emerging producers are not yet dependent on the petroleum sector, and are broadly energy poor, climate vulnerable, lower income countries.

These countries hold high aspirations for the petroleum sector to address their development needs.

The growing consensus that there should be no new oil and gas projects creates perceptions by emerging producers of injustice around the transition and could result in change being contested or some countries being ‘left behind’.

A just transition approach for these countries will minimize the oil and gas resource curse and its economic lock in, to ensure the sector is developed with broad societal benefits that do not increase national emissions.

1. Introduction

Despite the persistent resource curse risks and growing vulnerability to climate impacts they face, many countries in the Global South seek to extract what rents they still can from the petroleum sector,Footnote1 buoyed by the hope these revenues will transform their economies. New (and aspiring) producer countries share those ambitions for their petroleum sector, but they also express a desire to develop their resources more responsibly than legacy producers have, to build more resilient and sustainable economies and to avoid the resource curse.

However, an international norm is emerging in the Global North that no new oil and gas projects should be sanctioned in order to contain global warming – in effect leaving the remaining carbon budget to legacy producers. On equity grounds, new producers should have priority in producing their oil and gas, provided they can produce it at a lower emissions intensity than legacy producers. International finance and technical assistance are required to enable them to produce without a net increase in their national emissions, while ensuring broad-based benefits, and to chart a nationally-defined path to a low carbon economy.

This paper reviews the policy dilemmas facing aspiring and new oil and gas producers in a warming world. It focuses on five countries, ranging from frontier exploration plays to early producers, and considers the policy implications for the broader set of producers participating in a peer-to-peer government network called the New Producers Group (NPG).Footnote2 While the development and climate literature have focused on the prospects for decarbonizing established producers, the needs and vulnerabilities that shape the decision-making environment of emerging producers have received little attention. The immediate challenge for the countries in this study is to integrate decarbonization investments into their resource extraction plans to minimize the growth in their greenhouse gas (GHG) emissions while still meeting their development needs. We investigate the application of a just transition (JT) framework in this context. In the Discussion section, the paper provides a profile of five emerging producers by income levels, energy needs, emissions intensity, and climate vulnerability, and discusses the prospects of their petroleum sectors in a warming world. It also reviews the challenges they face in pursuing the pathways that are, in principle, available to them: decarbonizing the petroleum sector, extracting development benefits from the sector, and implementing low carbon pathways. Finally, the paper examines levers to improve outcomes in these pathways.

2. Data and method

Over the last decade, the NPG developed a trust-based environment in which bureaucrats can share their policy challenges – acknowledging resource constraints and limitations. This produced valuable qualitative data. Our thematic, inductive data analysis draws from the interpretative epistemology of hermeneutics (Geertz, Citation1973), to discover the horizon of meaning of actors and the associated values and ideas that matter to them (Marcel, Citation2001).

Most insights on policy maker views highlighted in the Discussion section are drawn from a two-week virtual training event in June–July 2021, attended by 91 officials from petroleum, energy, planning, finance, and environment agencies in Suriname, Guyana, Uganda, Lebanon, and Somalia. The goal of the training was to build an intra-governmental understanding on the intersection points between petroleum, energy, and climate goals. Country selection was therefore based on the breadth of their proposed delegations rather than national context.

Participants were given written preparatory course work. Each agency responded to a questionnaire about explicit and implicit policy assumptions, notably regarding petroleum and carbon prices over time and domestic energy demand. They detailed energy policy and plans; the state of the national petroleum sector and any expected growth; Nationally Determined Contributions (NDCs); and any dependence on conditional finance and treatment of the petroleum sector therein.

The authors collected data on the views of officials as they moderated or participated in plenary sessions and country-focused workshops. During the workshops, the authors recorded projected slides responses given by officials to framing questions around policy assumptions; objectives; stakeholder mapping; information needs across agencies; and general technocratic needs. Additional data was drawn from Zoom multiple choice polls given during plenary sessions to capture policy priorities and challenges of all participants. Limitations include aggregated poll data results (mixing country and agency type) and inconsistent sampling.

Eleven semi-directional interviews with training participants before the course provided additional data. Respondents were selected to produce a cross-agency sampling from each country, but Suriname was overrepresented with 6 respondents. Interviews aimed to capture expectations of the petroleum sector, perceptions of the energy transition, and assessments of government coordination. Questions included, for example, ‘Do your NDCs take into consideration your petroleum sector’s growth?’ and ‘What do you expect from the oil and gas sector?’

Broader insights about the priorities and challenges of new and emerging producers were also gathered from the participation of officials from the 26 NPG member countries in a series of virtual discussions, including: ‘Fostering Resilience’ in 2020 (Marcel, Citation2020); ‘Forging a New Path’ in 2021; the Annual Meeting of member countries in 2021; a hybrid event at COP26 in Glasgow (Commonwealth Secretariat, Citation2021); and an in-person meeting in Cape Town in October 2022. This data informs the analysis throughout the study. The comments cited herein are non-attributed, unless otherwise agreed.

3. Results

Despite increased investment in oil and gas following the Russian war in Ukraine, the global push for decarbonization has significantly dampened long-term resource prospects, especially in nations with undeveloped oil and gas. Calls are multiplying to stop new fossil fuel projects to meet the 1.5°C global warming limit target. Development banks have curtailed financing of new petroleum projects, which disadvantages low-income prospective producers and favours legacy producers who have already extracted resource rents and can self-finance projects. The withdrawal of Western technical assistance for the governance of the sector is particularly detrimental to new producers, which have limited financial and human resources and immature regulatory and policy frameworks.

To avoid favouring legacy producers in the distribution of the remaining carbon budget, McGlade and Ekins (Citation2015) proposed to curb costlier production first. But as Kartha et al. (Citation2018) point out, this ignores equity issues and risks advancing inequitable pathways. Perceptions of inequity also risk creating barriers to international cooperation on climate and encouraging prospective producers to proceed with projects without plans to mitigate or abate emissions. The Just Transition (JT) literature proposes principles to equitably curb production, which recognize the need for wealthy, high-emitting nations to end their oil and gas production first (Calverley & Anderson, Citation2022; Muttitt & Kartha, Citation2020). However, JT scholars have not discussed how these equity considerations might leave room for countries starting to produce because, as Calverley and Anderson point out, there is no room in the carbon budget for new oil and gas projects of any kind.

Halting new rather than legacy projects is based on practical and not equity grounds. In equity terms, the distribution of the carbon budget should favour least-developed countries with energy gaps that bear little responsibility for the climate crisis and have not benefitted from petroleum rents or energy for growth. But practically speaking, production cuts (and not additions) are needed, and large legacy producers are unlikely to cede ground to new producers (Green & Pye, Citation2022). There is, however, a growing body of evidence to suggest that new oil and gas projects can be designed more readily to minimize GHGs than retrofitting legacy assets (Gargett et al., Citation2019; World Oil, Citation2023). This opens a new pathway for emerging producers if they can develop net zero projects (Scope 1 & 2) by producing oil and gas at the lowest emissions intensity and offsetting residual, hard-to-abate sector emissions with nature-based solutions in their country. These emerging producers should not have to bear the burden of abating Scope 3 emissions in consuming countries.

This pathway is not without obstacles. First, there are capacity challenges. Most emerging producer governments lack the oversight capacity for stringent emissions management and the ability to integrate the sector’s emissions within a national Paris Agreement-aligned transition plan. Without support, they will struggle to overcome the many obstacles associated with gas-to-power projects and the lock-in risks associated with gas infrastructure.

Second, the resource curse points to the disappointing outcomes of extractives-led development, including corruption, authoritarianism, and economic stagnation (Ross, Citation2015; Sachs & Warner, Citation1995) – even in countries that have not yet produced rents (Cust & Mihalyi, Citation2017). This prompted Pye et al. (Citation2020) to suggest that an equitable distribution of production rights based on income and historic benefits would be unlikely to give developing countries the benefits they hoped for. We find that a deep change is necessary in public and political expectations around the transformative potential of the sector to avoid repeating mistakes made before and to increase interest in nationally fit-for-purpose transition plans. Opening the civic space for national dialogue (Okpanachi et al., Citation2022; Shehabi & Al-Masri, Citation2022) around rent distribution and transition plans offers a better chance of countering the resource curse and charting a JT.

The low-carbon pathway, often presented as the necessary gateway to development, is not without obstacles. Shifts to low-carbon energy involve complex socio-economic, environmental, and technical transformations (Abram et al., Citation2022; Jenkins et al., Citation2018), as well as challenges to vested interests. Nationally specific transition plans are needed to illuminate any promising sectors. Such transformations also require much greater deployment of technology, investments, and finance in the Global South (Steckel et al., Citation2017). Development assistance on clean energy deployment has been forthcoming, but investments in climate adaptation and clean energy have been insufficient. Significantly for low-income countries, clean energy deployment alone does not replace the fiscal potential of the petroleum sector.

A JT approach in these countries will not be about reskilling as they move away from a petroleum dependent economy, but instead about meeting basic needs first, and developing towards a low carbon economy in a manner that minimizes lock-in to carbon and emissions growth. This development path may include the integration of renewable energy (RE) plus gas for domestic energy needs and petroleum exports for fiscal needs. JT will also mean engaging with citizens in transition planning, so community needs are addressed and the outsized expectations regarding petroleum are reduced.

4. Discussion

4.1. Unpacking the decision-making environment of emerging producers

4.1.1. Country profiles

Most of the member countries of the NPG fall within the lower end of the income spectrum.Footnote3 Uganda and Somalia are in the low-income group, Lebanon in the lower-middle group, and Guyana and Suriname in the upper-middle group (World Bank, Citation2023). Many countries in the NPG have high external debt stocks in relation to gross national income – notably Lebanon (381% in 2021, World Bank) and Somalia (67% in 2021, World Bank) – which was exacerbated during the COVID-19 pandemic. Suriname has struggled with high food and energy prices following the war in Ukraine and is reliant on an Extended Fund Facility from the IMF.

NPG countries have petroleum sectors at different stages of development, and this is reflected in our cases. With Guyana’s small population of nearly 800,000 and crude production at 340,000 b/d in 2022 (set to increase to 810,000 b/d by 2027 and 1–1.2 mmb/d by 2030 [DPI, Citation2022, January 29]), the influx of revenue will dwarf its small economy. Its GDP grew by 20% from the previous year in 2021 (World Bank, national accounts data). It will become a rentier state, with an economy in which rent accrued from foreign sources plays a major role (Beblawi & Luciani, Citation1987). First oil production is expected in 2025 in Uganda, with peak production to reach 230,000 b/d. In simple terms, it will have a quarter of Guyana’s rent to meet the needs of an economy approximately 8 times the size of Guyana’s pre-production and a population 50 times larger (at 45 million people). In Suriname, five commercial discoveries are being appraised. Production levels are expected to be significantly smaller than Guyana’s, but with a small population and economy on par with its neighbour, the rent would impact the economy. In Lebanon and Somalia there are no commercial discoveries, though there is active exploration drilling in Lebanon.

Most emerging producers have low access to electricity, except in the Caribbean. The percentage of the population with electricity access is 36% in Somalia and 41% in Uganda (World Bank, SE4ALL, 2019 data). Many NPG countries rely on dirty, bottom-of-the-barrel imported petroleum products, such as heavy fuel oil (HFO) and diesel. For example, 67% of Guyana’s and 52% of Suriname’s energy needs are met with these carbon-intensive fuels that consume foreign exchange (Caricom, Citation2018; Suriname Energy Authority, Citation2021). All NPG countries already do (or plan to) export their oil and gas production, though many have stated their ambitions to retain a share of their expected new production for domestic use. This includes Guyana and Suriname for associated gas, and Uganda for oil (and Timor-Leste, Mozambique, and Tanzania for natural gas). Uganda has over half of its electric grid mix covered by renewable energy (RE) (IEA, Citation2020c), but, like Somalia, it relies heavily on biomass for its final energy consumption, with negative impacts on health and forest cover (IEA, Citation2021b).

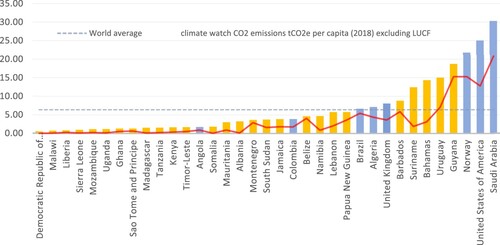

Several members of the group that are producing (or will soon produce) petroleum have large areas of forest that act as carbon sinks, notably Suriname and Guyana. Collectively, the 27 NPG countries are home to six percent of the world’s population (World Bank (Citation2021), 2016 data, Author calculations), but their total emissions are estimated at 1.4 percent of global GHGs and their oil and gas sectors account for less than one percent of total petroleum production emissions (Author calculations, Climate TRACE data). Per capita GHGs in the African and Asia Pacific NPG countries are dwarfed by established oil and gas producers in the Global North, as shown in . By comparison, NPG countries are more affected by climate change and produce relatively lower levels of total GHG (CO2e) emissions per capita.

Figure 1. Total GHG and CO2 emissions per capita for NPG countries and other selected countries, 2020 (tCO2e).

Source: Authors’ calculations using Climate TRACE data (https://www.climatetrace.org/). Notes: Climate Trace data for all GHG (in tonnes Co2e) emissions per capita* for 2020, for NPG countries and other selected countries. * the data exclude (i) maritime and (ii) forest and land use emissions.

However, if NPG countries follow in the footsteps of those with the largest GHG footprints, their contribution to global emissions would rise – especially countries with large reserves, such as Guyana (and Mauritania and Mozambique). For example, if Guyana’s production rises to a projected 1.2 mb/d by 2030, that oil could add 2–3 million tonnes CO2 equivalent in GHG to the atmosphere from extraction to final use.Footnote4 But set in a global context, the emissions impact of new producers starting from a low base would be very small. As demonstrated by Moss and Kincer (Citation2020), the hypothetical tripling of natural gas-generated electricity to serve one billion people in Sub-Saharan Africa would be equivalent to 0.62% of annual global GHG emissions.

At a national level, however, building out the oil and gas sector as planned would have a significant impact on emissions trajectories. For reference, Angola’s oil production of 1.37 mb/d accounts for one-third of national emissions, with hydropower providing 58% of the country’s electricity.Footnote5 Already, new producers can see a growth in their emissions: after Guyana’s oil production reached 74 kb/d in 2020, national emissions rose 6% from the previous year.Footnote6 However, if Guyana substituted its use of HFO and diesel with cleaner alternatives it could offset that increase in emissions. The data for projected emissions under different scenarios for sector build out and domestic energy mixes are lacking and would be of high value to policymakers.

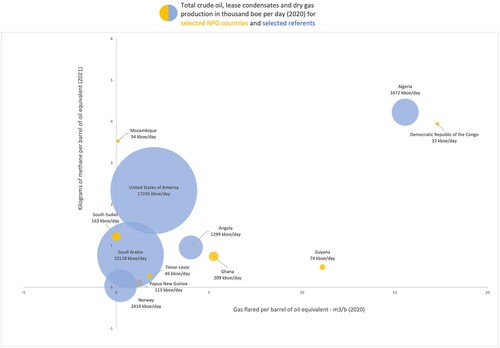

Another way to compare the relative impacts of different countries’ oil and gas climate footprints is by their emissions intensities. There is significant variance across countries (: Lavaux et al., Citation2022; Masnadi et al., Citation2018), including among new producers (in yellow on ). However, as new entrants facing headwinds in the development of their sector, they will need to position themselves at the lowest emissions intensity near Norway on , with zero routine flaring and near zero methane leakage.

Figure 2. Flaring and methane intensity of oil and gas producers in the NPG and selected referent countries.

Sources: Authors’ calculations using Skytruth data for gas flaring; EIA 2020 data for crude oil and lease condensate production; EIA 2019 data for dry gas production, except Norway, PNG, Saudi Arabia; EIA 2020 data for USA; IEA (Citation2022) 2021 data on methane emissions from oil and gas production. Note: PNG and Timor-Leste calculated as an equal proportion of 34 ‘other Asia-Pacific’ countries.

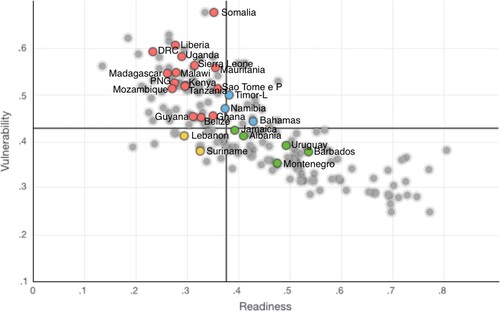

Vulnerability to climate impacts is broadly high across the group, as shown in . The countries in the upper left quadrant are the most vulnerable to climate impacts and present a low level of readiness to address them. Communities face the greatest impacts (Thomas & Twyman, Citation2005) and governments lack the means to ease them. As low-income and/or small economies, countries in this quadrant have had little influence on the commitments that the high emitters make. All NPG countries in the production phase or with significant discoveries are in this quadrant (except Suriname); the countries have yet to access significant finance for clean development, climate mitigation, and adaptation, except for Guyana, which received Norwegian funding for its REDD + programme until 2015 – a programme that suffered from corruption (Palmer & Bulkan, Citation2010) but was effective in protecting forest cover (Roopsind et al., Citation2019). As a producer, Guyana could fund its REDD + programme but external finance would make the government accountable for the performance of its forest management. Uganda’s expected oil revenues will not be on a scale to cover either development or adaptation needs.

Figure 3. Vulnerability and readiness to climate change across the member countries of the NPG, 2019.

Source: Authors’ adaptation from Notre Dame Global Adaptation Initiative.

4.1.2. Assessing petroleum prospects in NPG countries

In an influential publication, the IEA outlined the massive challenges involved in capping warming at 1.5°C in its 2050 road map. One conclusion is that, to meet this climate target, there is no room for new oil and gas development beyond projects committed to in 2021 (IEA, Citation2021a). This would leave no room for NPG countries at the exploration stage to enter the market.

Most international oil companies have set net-zero emissions targets by 2050, causing portfolio reassessments. Flaring, maturity, and long export routes increase project emissions, making North American, Middle Eastern, and major liquified natural gas (LNG) projects more attractive (Wood Mackenzie, Citation2020). Higher oil and gas prices since the war in Ukraine led to an increase of 12% of global upstream capital expenditure in 2023 from the previous year (Kimani, Citation2023), but the bulk of this investment is directed to basins with existing discoveries offering ‘advantaged barrels’ – lower cost, lower emissions production that can be delivered quickly. As both supermajors and exploration companies turn away from riskier exploration, the prospects for the sector dims significantly in NPG countries such as Lebanon, and especially Somalia where there is no active drilling.

Trading rules are also evolving, and the climate intensity of oil and gas supplies is becoming a new benchmark. The European Commission’s carbon border adjustment mechanism introduces a levy on imports of natural gas that do not meet EU carbon intensity standards. Trading platforms are using carbon intensity as a variable in crude price formulation (Rushforth, Citation2021). Some NPG countries could be advantaged in carbon-costed trading systems compared to legacy producers with assets that have fugitive methane emissions (super-emitters include Turkmenistan, Russia, the United States, Iran, Kazakhstan, and Algeria [Lavaux et al., Citation2022]) or those that require GHG-intensive enhanced recovery methods in older reservoirs (Lavaux et al., Citation2022; Masnadi et al., Citation2018).

Countries with strong Environmental, Social, Governance (ESG) oversight that can enact and enforce emissions control measures during petroleum operations should be more attractive to investors, though Papua New Guinea, Ghana, and Timor-Leste’s better-than-industry-average emissions intensities (; Masnadi et al., Citation2018) indicate that new producers with the right operators and technical assistance can outperform high-income countries.

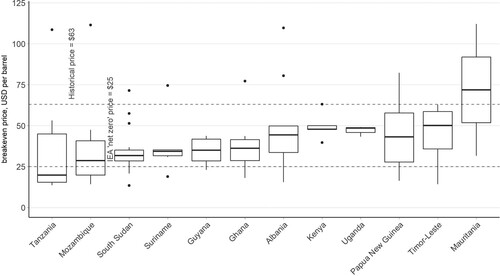

While the NPG countries can reduce their emissions intensities to compete with legacy producers, the cost associated with immature extraction, processing, and transport infrastructure poses economic challenges. Costs remain major determinants of oil and gas investment decision making. illustrates the sensitivity to price of various NPG countries, with most above the IEA ‘net zero’ price of $25/b but below the historical price of $63/b.

Figure 4. Break-even price range aggregated at the country level for selected NPG countries.

Source: Author calculations using Rystad Ucube data. Note: The horizontal line in each box indicates the median cost; the ends of the box are one quartile away from the median; the ends of vertical lines show projects that are at the 5 and 95 percentile away from the median; dots indicate outliers. Investor hurdle rate assumed to be 10%. The historical price is the average real price over last 50 years.

4.2. Available NPG development pathways

4.2.1. Minimizing emissions from the petroleum sector

Opportunities exist for technologies and practices to deliver significant GHG reductions throughout supply chains (Gordon, Citation2022), and new producers can position themselves at the lowest end of the emission intensity spectrum. New producers do not yet have significant infrastructure and can ‘build better’ rather than deploying efforts to retrofit decarbonization. Minimizing value chain emissions will be a condition of entry and endurance for traded oil and gas. While the whole sector will need to shrink to meet the goals of the Paris Agreement, producers who cut their emissions can credibly argue that their resources should be prioritized over higher-emitting ones as a share of the remaining carbon budget (IEA, Citation2020a).

Achieving ‘Zero Routine Flaring and Venting’ needs to be a key focus area. Flaring and venting can account for as much as 40% of the carbon intensity of production (Masnadi et al., Citation2018) and 95% of flared volumes could be avoided (IEA, Citation2021c). Methane is a more powerful pollutant than carbon dioxide, with over 80 times higher warming impact over 20 years (IPCC, Citation2021). The IEA finds that a 70% reduction in methane emissions is possible with today’s technology and policies, and over 40% could be done at no net cost (IEA, Citation2021d). As Mitchell et al. (Citation2022) showed, NPG countries have a unique opportunity to design, operate, monitor, and certify their operations at near zero methane emission levels – leapfrogging mature producers.

The second focus area is the use of RE in petroleum operations. Historically, the huge amounts of energy used to extract, process, and transport oil and gas has been provided by diesel, fuel oil, and natural gas. Replacing this with RE can reduce the emissions intensity of operations up to 80–90%.Footnote7 The Ugandan EACOP project will rely on hydroelectricity to power pumping stations and solar energy to heat the pipeline carrying Ugandan waxy crude. In Suriname, energy planners are interested in developing offshore wind to power platforms, which would offer cross-training of workforces and provide surplus electricity to meet domestic needs.

Despite national pledges and commitments, evidence to date demonstrates that delivery on these mitigation efforts above is not easily realized. For most NPG countries and indeed in the five countries studied, robust regulatory and legal frameworks to enshrine and implement emission-reduction policy objectives are not in place. Many do not have legal requirements on flaring, venting, methane, and effective mechanisms for reporting or dealing with non-compliance (including flaring penalties). NPG officials also stated they lack the technical and commercial expertise, personnel, analytic tools, and funds to effectively monitor and independently measure emissions. NPG officials require, for example, the capacity to understand and benchmark the emissions profile of a project.

Many governments with gas want to direct a share of their production for the domestic market. While the relative emissions of domestic versus export are not currently a driver, domestic gas consumption can be far less emission intensive than importing petroleum products and LNG (which must be shipped and re-gasified). When NPG countries import oil and gas it can increase emissions by creating additional processing steps and lengthening distances traveled. In other words, domestic use carries a different national climate burden (Gordon, Citation2022). However, diverting gas to domestic markets is hindered by numerous obstacles related to timing, finance, markets, regulations, and infrastructure (Mitchell et al., Citation2022). It would be extremely challenging to overcome these obstacles without support from international public finance and technical assistance, and even difficult with that support. The outlook is country-specific, but a mixture of incentives and penalties is generally required to establish domestic gas markets and build out new infrastructure. Domestic gas needs to be commercially yet affordably priced. Infrastructure debt is also risky given uncertainty related to the revenue streams required for repayment.

In Suriname and Guyana, there is no option but to find a productive use for the gas produced to prevent flaring. In both countries, the volumes of associated gas are greater than reservoir reinjection needs, and they must make plans to consume or export the gas or slow/halt oil production. Consuming this gas could displace HFO in the energy mix and avoid more emissions-intensive LNG exports, but the above barriers to developing the gas must be overcome. This issue appears to have contributed to delaying the final investment decision in Suriname (Smith, Citation2023).

One of the most important but underused mechanisms to minimize emissions is the government’s thorough review and approval of a company’s field development plan (FDP). This includes demonstrating how technology has been leveraged, for example, in the use of zero-bleed controls and pumps, solar or electric motors (instead of diesel or gas engines), ‘green’ completions, concentrated solar heat and steam, vapour recovery units, and leak detection and repair systems. Effective FDP reviews also involve engaging operators early, clear FDP procedures, coordination among agencies, sourcing technical expertise, setting revenue expectations, and managing political pressures. NPG governments identified capacity gaps in this area.

Another major barrier to minimizing emissions stems from the desire to commence production as fast as possible (fast-tracking). Rapid revenue streams are attractive to oil companies and the political leadership, especially considering transition risks. But fast-tracking can undermine systemwide improvements. Whilst an oil field can be brought to production in less than five years, associated gas development can take twice as long. Fiscal (and political) pressures work against delaying oil production while domestic markets and infrastructure are developed for associated gas. In Ghana, associated gas handling was not included in the fast-track development window. Extending the timeline could have avoided a decision once production started to either shut in production and forego revenues while domestic markets and infrastructure were developed or allow flaring (with only modest penalties in place). As a result, oil production continued with gas flaring. Developments of various discoveries in Guyana are being fast-tracked, which raises risks of similar failure to deal with gas and flaring.

4.2.2. Generating development gains from the petroleum sector

NPG governments view the petroleum sector as a key driver of economic growth and a means of funding their transition, but officials at the training demonstrated limited understanding of how to manage the risks associated with this sector, including the resource curse and lock-in risks. To avoid miscalculations, NPG countries must resist the urge to speed up licensing, offer excessive fiscal incentives, relax regulations, or invest too heavily in the nascent industry (Manley et al., Citation2021).

Wang and Lo (Citation2021) suggest that shifting attitudes towards the transition is necessary to address public expectations that spillover benefits will come from oil and gas development. While civil servants in the training acknowledged that the energy transition is happening ‘whether our country likes it or not’, public and political expectations about petroleum investment, and the revenues and economic opportunity it will create, remain high. Long-standing aspirations of maximizing fiscal revenues and generating long-term economic growth through linkages with the petroleum sector require re-examination through national-level dialogues.

Expectations are high for petroleum revenues to fuel national prosperity, as demonstrated by a poll of training participants from all five countries, who all cited ‘poverty reduction and investment in growth’ as the most important contribution of the oil and gas sector to national development.Footnote8 Interviews with Lebanese and Somali participants confirmed these sentiments drive hope even in NPG countries without discoveries. In Guyana, revenues will transform the economy, but it is an outlier in the NPG in terms of the scale of revenues to the size of the economy. In Suriname, the 2020 oil discovery came just in time, according to a Ministry of Finance official interviewed, as the country was facing a budgetary crisis that led to an IMF bailout. Oil and gas production, with its associated revenues, are viewed as a ‘hallelujah moment’, commented Dave Abeleven of Suriname’s Energy Authority. In NPG forums, where political economy issues are rarely discussed, there is nevertheless an acknowledgement of resource curse risks when revenues flow. Officials emphasized the need to ensure the use of oil and gas resources is not wasted but instead builds long-term prosperity and resilience.

Some NPG countries, notably Uganda, hope to use oil and gas to grow domestic industrial value chains, but historical practice shows little evidence of linkages extending beyond carbon-intensive industries. NPG countries are increasingly interested in lateral linkages that leverage the petroleum sector to develop skills, goods, and infrastructure outside the sector (Marcel et al., Citation2016), including the green economy and reducing vulnerability to oil and gas price volatility, as demonstrated in the low-carbon growth plans presented by the last two administrations in Guyana (Co-operative Republic of Guyana, Citation2021).

The track record of development outcomes from the extractives sector has often been disappointing, especially where pre-existing institutional capacities were low (Lahn & Bradley, Citation2016; Stevens et al., Citation2015). Overspending, inflation, declining agricultural competitiveness, and economic vulnerability to volatile international oil and gas prices are common symptoms of an extractives-led development pathway (Lahn & Bradley, Citation2016). Emerging producers have not escaped some of these traps, and their fiscal revenues have tended to be smaller and take longer to materialize than was forecast at discovery, leading to disappointment and public debt (Mihalyi & Scurfield, Citation2020).

Carbon risks, including lower and more volatile revenues and the potential loss of export markets, compound the concern for resource curse risks (Pye et al., Citation2020). NPG countries must not be overly optimistic about the landscape. Agencies surveyed on their planning assumptions in June 2021 expected crude oil prices to increase for 10–15 years, with some even projecting prices to keep rising until 2040 or 2050. The Carbon Tracker Initiative estimates that revenues in Ghana, Guyana, Senegal, and Uganda could fall 50 percent short of expectations over the next two decades (Coffin et al., Citation2021).

4.2.3. Implementing low carbon development pathways

The JT literature highlights the need for a shift to low carbon energy that does not worsen existing inequalities or leaving ‘anyone behind’ (Abram et al., Citation2022; Jenkins et al., Citation2016; McCauley & Heffron, Citation2018). The NPG countries in this study face several challenges in transitioning to low carbon energy.

The literature and development actors focused on JT anticipate that RE will meet the growing energy needs of lower-income countries and form the basis of their low carbon transition (Quitzow et al., Citation2019). While there is considerable potential for increasing the use of RE in the countries under study, their expansion is limited in countries without geothermal or hydro resources, such as Somalia and Lebanon. Increasing the use of wind and solar power requires the development of grid infrastructure, storage, or natural gas (Mutiso & Auth, Citation2021). Shifting the energy mix requires integrated energy planning, which was found to be lacking in this study. Immediate challenges make it difficult to develop cohesive energy policies, as exemplified by the case of Lebanon, where recent economic and political crises have had a debilitating impact on planning. Countries facing such challenges naturally prioritize less expensive strategies (both economically and politically).

As noted in Section 1, Suriname and Guyana are carbon sinks, and preserving their forest cover and biodiversity is a critical element of their low-carbon transition. Meanwhile, Uganda (and to a lesser extent Somalia) are grappling with deforestation. The countries under study seek climate finance to fund the projects outlined in their NDCs. Despite a large amount of private and public capital currently seeking green investment projects internationally (Prag, Citation2021; Stoll et al., Citation2021), the overwhelming majority of private finance flows inward to advanced economies (Bhattacharya et al., Citation2020). Moreover, access to climate finance from international funds, which is meant to help developing countries mitigate emissions and adapt to climate change, requires high thresholds and unrealistic government requirements.Footnote9 The use of Environmental, Social, and Governance (ESG) criteria to screen investments, which is intended to encourage transition funding, often penalizes high-risk NPG countries that are most in need of investments but have weak market structures, immature financial services, and inadequate incentive structures in regulatory frameworks. Ameli et al. (Citation2021) refer to this as the ‘climate investment trap’. As they point out, the IEA’s net-zero pathway does not account for the higher weighted-average costs of capital for low carbon investments in Africa and Central and South America, resulting in an overly optimistic transition scenario for NPG countries. As mentioned in Section 4.1.1, the COVID-19 pandemic and the war in Ukraine have left both low- and middle-income countries with debts that threaten to delay climate action. Radical efforts are needed to redirect capital flows for mitigation and adaptation to high-need, high-risk regions and support the development of enabling environments for investments (ibid).

Another challenge for low-carbon pathways is energy affordability. Large-scale RE projects or switching consumers from wood fuel to LPG can involve higher prices for end-users. Policymakers must consider subsidies to support low carbon projects and/or other incentives for investors. Typically, the government bears the cost, which could increase public debt. There is, therefore, a reluctance to take on more debt for projects that could attract climate finance. However, in Guyana, oil revenues can support investment gaps in clean energy, adaptation, and low-carbon growth.

5. Policy implications

Governments need to assess pathways that can best achieve their goals, which they identified primarily as environmental (e.g. preserving forest cover; biodiversity; improving air quality; climate pledges) and economic (e.g. government revenue; access to cleaner, reliable, and affordable energy; raising national income levels; economic growth and job creation; sustainable debt; resilience in the transition). While these governments often look to the petroleum sector to achieve their economic goals, they require more modelling and risk assessment capacity to determine the likelihood or margin of success in an increasingly carbon-constrained world. Countries without discoveries or active exploration programmes are relying on a petroleum sector that presents poor economic prospects. Eighty percent of officials from a broad sample of exploration, development, and production stage countries surveyed in a Zoom poll in October 2021 indicated their country had no vision for a non-oil economic development pathway. Evidently, these countries need to consider more options. Countries with credible petroleum-led development prospects also need to identify low-carbon sectors that can achieve their economic and environmental goals, as oil and gas are only steppingstones in their development path; but they lack country-specific economic insights.

Countries contemplating the petroleum pathway need to assess the risks it poses to their various environmental goals, i.e. to either manage them or to set a different course. The only way to achieve the aforementioned climate goals in a petroleum pathway is to design a lowest-emissions – and even better, net-zero – petroleum sector. These countries need estimates of lifecycle emissions from their oil and gas sector, so as to mitigate and offset these emissions, and to set realistic climate targets. Suriname, Uganda, and Guyana committed to net-zero emissions by 2050. However, during training sessions, it was apparent that national GHG emission targets were often established by the governments in these countries without input from petroleum or energy agencies. These agencies viewed the targets as infeasible without mitigation and offset measures. Conversely, environmental planners lacked essential data on energy demand growth and the GHG emissions generated by petroleum production.

A Somali official commented during the NPG 2021 Annual Meeting that ‘the “how” of the transition is difficult. The international community must come up with a plan to support middle and lower-income countries in the transition’. International climate assistance, policy support, and capacity development are lagging (OECD, Citation2019a) and this is holding back planning in low-carbon growth. Most G7 technical assistance programmes for the petroleum sector have also been withdrawn, which increases resource curse risks for countries already in oil and gas production. Assistance programmes are needed to support holistic transition planning, including a review of all available pathways and an assessment of how oil, gas, and low-carbon developments can best be combined to help achieve climate mitigation goals, and the development of a decarbonized (Scope 1 & 2) petroleum sector.

Finance is the other necessary lever. Climate finance is not reaching high-risk countries. Wong (Citation2022) argued for a co-benefits approach that addresses climate and sustainable development concomitantly in fragile countries, though it is contested (Buchholz & Rübbelke, Citation2021). Transition finance offers an adaptive approach for development partners to address the evolving financial needs of countries undergoing transition in the Global South (OECD, Citation2020), but it has focused on supporting high emitting, fossil fuel dependent countries, not on small emitters avoiding or offsetting new emissions. Countries with abatable emissions resulting from heavy fuel oil (HFO) or biomass consumption are unlikely to receive transition support when they develop oil and gas. Access to finance would likely improve with national plans that demonstrate a verifiable transition pathway, but many countries will find it easier to turn to petroleum revenues to fund their transition. Gina Griffith from the Surinamese environmental regulator NIMOS explained that her

greatest hope is that oil money will be used to, first, make sure we diversify and we don’t have to stay dependent on that oil revenue, and two, invest a big part of it in our biodiversity and the environmental management of our resources and our forests.

NPG countries hoping to secure finance or technical assistance to develop gas-to-power projects are finding fewer available avenues to do so. Most countries contributing development finance have pledged to no longer fund oil and gas projects abroad – including the US, Europe, and the UK (and China and Japan for coal) though they continue to finance and offer implicit or explicit subsidies to their own national petroleum production (Attia & Bazilian, Citation2021; Dyson et al., Citation2021; IMF, Citation2022; US Treasury, Citation2021). The African Development Bank stands alone among multilateral development banks (MDBs) in its willingness to finance gas projects (Bloomberg, Citation2021), but it is restricted without co-financiers to match funds.

6. Conclusion

This study examines the energy, economic, and environmental challenges facing emerging petroleum producers, including Guyana, Suriname, Uganda, Lebanon, and Somalia. Our findings are drawn from interviews and training sessions with government officials, along with country-level analysis. We find that these countries are guided by environmental concerns, access to clean energy, and preparing for a clean energy transition, but also by priorities that clash with international development and climate priorities, including meeting fiscal and energy needs with oil and gas projects. These countries lack the support needed to make a just transition (JT) towards a low-carbon economy, including country-specific low-carbon pathways, foreign investment, and development finance and assistance in developing low-emission petroleum projects and transition pathways. Low capacity in these countries hinders their ability to oversee low-emission projects and presents avoidable climate risks. Development partners aiming for a JT should support the transition goals of emerging petroleum producer countries. This includes a number of options, such as using export revenues to fund low-carbon growth; displacing more polluting HFO or biomass with natural gas or LPG; incentivizing clean energy to grow in the energy mix; and offsetting GHG emissions from the petroleum sector with nature-based solutions.

Government officials from the Global South often express frustration with the inequity of their energy ambitions being cut short by a climate crisis they did not meaningfully contribute to. The expansion of oil and gas investments in the Global North following the war in Ukraine heightens these sentiments. At a meeting of senior NPG officials in October 2022, an exercise involved them writing their ‘biggest worry’ on the wall. Responses included: ‘Having stranded assets while energy poverty persists’; ‘Remain(ing) where we are for another 30–40 years’; ‘Africa will continue to allow the developed world to dictate its energy policy’; ‘As a global society, we will not find the unity that is required to map the future’.

In this context, the transformations required for a global clean energy transition risk being contested. At the international level, the formation of climate policies within OECD countries and MDBs has not been sufficiently participatory. There has been a failure to adequately engage with the perceptions by emerging producers of injustice around the transition. This may result in change being contested or some countries being ‘left behind’. Political messaging at a national level around the risks inherent to petroleum development in a warming world, or the impacts of the transition, has not created a public perception of a JT, nor has there been a redefinition of societal interests that would build reform coalitions (Meadowcroft, Citation2011; Wang & Lo, Citation2021). While JT examines how to reskill workers for low-carbon sectors, emerging producers continue to train nationals for the petroleum value chain, sustained by optimism about that sector’s ability to meet their development needs. There is value in further shaping and operationalizing the JT concept in emerging producer countries – especially countries that are not currently fossil-fuel dependent – with a view to a national-level definition of a fit-for-purpose transition pathway. This approach will minimize oil and gas’ resource curse and lock in and ensure the energy sector develops with an eye to broad societal benefits that do not increase national GHG emissions.

Acknowledgements

The authors are grateful to Patrick Heller and Glada Lahn for their thoughtful contributions to earlier versions of this article, to Chris Aylett and David Manley for producing interesting figures, and to Kirsten Jenkins and the anonymous reviewers for their time and their valuable comments, which helped us to improve the quality of the manuscript.

Additional information

Funding

Notes

1 In this article, the terms petroleum sector and oil and gas sector are used interchangeably.

2 The NPG is a non-profit voluntary association of governments from 26 countries that are new to the oil and gas sector. The overriding objective is to enable countries to develop more robust strategies to manage their natural resources, build sustainable economies, and navigate energy transitions. The community of practice is co-organized by the Natural Resource Governance Institute and the Commonwealth Secretariat.

3 The list of member countries is available on https://www.newproducersgroup.online. Membership fluctuates with country engagement. At the time of conducting this research, membership included Montenegro and Albania, but not Senegal.

4 On the basis of Carnegie’s estimate for ‘light, well managed oil’, including an offsite emissions credit, 475 kg CO2 equivalent per barrel (Carnegie Endowment for International Peace). With high flaring, this could be 750 kg CO2e/barrel and thus 328.5 million tonnes of GHGs.

5 Climate TRACE emissions data for 2019; OPEC (Citation2019) for production data; IEA (Citation2021b) data for share of hydro in 2018. Emissions data for Angola and Guyana do not include forestry and land use.

6 Author calculations, Climate TRACE emissions data for 2020, EIA data for production in 2020.

7 By using energy from the power grid, emissions from the Norwegian Johan Sverdrup field were reduced by 80–90% compared to a standard development relying on gas turbines (Equinor, Citation2023).

8 The multiple-choice question included these options: Revenues for poverty reduction and investment in growth and prosperity; Revenues to service debt; Support for industrialization; Local content & employment; Better access to energy; Downstream industries; Other benefits.

9 These requirements include demonstrating a track record in the sector and a cumbersome accreditation process that can last longer than electoral cycles (Akintunde, Citation2021; Bhattacharya et al., Citation2020).

References

- Abram, S., Atkins, E., Dietzel, A., Jenkins, K., Kiamba, L., Kirshner, J., Kreienkamp, J., Parkhill, K., Pegram, T., & Santos Ayllón, L. (2022). Just transition: A whole-systems approach to decarbonization. Climate Policy, 22(8), 1033–1049. https://doi.org/10.1080/14693062.2022.2108365

- Akintunde, I. (2021). COP26: Untying the climate funding knot. The World Today. https://www.chathamhouse.org/publications/the-world-today/2021-10/cop26-untying-climate-funding-knot

- Ameli, N., Dessens, O., Winning, M., Cronin, J., Chenet, H., Drummond, P., Calzadilla, A., Anandarajah, G., & Grubb, M. (2021). Higher cost of finance exacerbates a climate investment trap in developing countries. Nature Communications, 12(1), 4046. https://doi.org/10.1038/s41467-021-24305-3

- Attia, B., & Bazilian, M. (2021, November 4). Why banning financing for fossil fuel projects in Africa isn’t a climate solution. The Conversation. https://theconversation.com/why-banning-financing-for-fossil-fuel-projects-in-africa-isnt-a-climate-solution-169220

- Beblawi, H., & Luciani, G. (1987). The Rentier state. Routledge.

- Bhattacharya, A., Calland, R., Averchenkova, A., Gonzalez, L., Martinez-Diaz, L., & Van Rooij, J. (2020, December). Delivering on the $100 billion climate finance commitment and transforming climate finance, independent expert group on climate finance, United Nations. https://www.un.org/sites/un2.un.org/files/100_billion_climate_finance_report.pdf

- Bloomberg. (2021, November 4). Natural gas key to Africa’s energy security says AfDB’s Adesina. https://www.bloomberg.com/news/articles/2021-11-04/natural-gas-key-to-africa-s-energy-security-says-afdb-s-adesina

- Buchholz, W., & Rübbelke, D. (2021). Overstraining international climate finance: When conflicts of objectives threaten its success. International Journal of Climate Change Strategies and Management, 13(4/5), 547–563. https://doi.org/10.1108/IJCCSM-06-2021-0071

- Calverley, D., & Anderson, K. (2022). Phaseout pathways for fossil fuel production within Paris-compliant carbon budgets.

- Caricom. (2018). Guyana energy report card. https://energy.caricom.org/reports-2/

- Carnegie Endowment for International Peace. Oil-climate index. http://oci.carnegieendowment.org/

- Climate TRACE. https://www.climatetrace.org

- Co-operative Republic of Guyana. (2021). ‘Local content policy for the development of Guyana’s petroleum economy; A policy guidance for managing Guyana’s petroleum resources to enhance the local workforce, supply chains and business environment for transforming the economy and well-being of Guyanese’. Revised Draft – February 2021. https://nre.gov.gy/wp-content/uploads/2021/02/LCP-for-the-Development-of-Guyanas-Petroleum-Economy-Revised-Draft-02.11.2021-updated.pdf

- Coffin, M., Dalman, A., & Grant, A. (2021). Beyond petrostates: The burning need to cut oil dependence in the energy transition. Carbon Tracker Institute.

- Commonwealth Secretariat. (2021, November 10). Forging a new path towards an equitable and just energy transition. COP Side Event. https://www.newproducersgroup.online/event/cop26-side-event-climate-change-and-new-petroleum-producing-countries/

- Cust, J., & Mihalyi, D. (2017). The presource curse. Finance & Development, 54, 4. https://www.imf.org/external/pubs/ft/fandd/2017/12/cust.htm

- DPI. (2022, January 29). In four years, Guyana expects oil revenues twice the size of its 2022 Budget. https://dpi.gov.gy/in-four-years-guyana-expects-oil-revenues-twice-the-size-of-its-2022-budget/

- Dyson, M., Engel, A., Odom, C., & Shwisberg, L. (2021, December). Headwinds for US gas power: 2021 update on the growing market for clean energy portfolios’. Rocky Mountain Institute. https://rmi.org/wp-content/uploads/2021/12/clean_enery_portfolios_brief_2021.pdf

- EIA. https://www.eia.gov

- Equinor. (2023). https://www.equinor.com/energy/johan-sverdrup

- Gargett, P., Hall, S., & Kar, J. (2019, December 6). Toward a net-zero future: Decarbonizing upstream oil and gas operations. McKinsey & Company. https://www.mckinsey.com/industries/oil-and-gas/our-insights/toward-a-net-zero-future-decarbonizing-upstream-oil-and-gas-operations

- Geertz, C. (1973). The interpretation of culture. Basic Books.

- Gordon, D. (2022). No standard oil: Managing abundant petroleum in a warming world. Oxford University Press.

- Green, F., & Pye, S. (2022). No new fossil fuel projects! The norm we need [Conference presentation]. Fossil fuel supply & climate policy conference, September 26, Oxford, United Kingdom.

- IEA. (2020a). Putting gas flaring in the spotlight. https://www.iea.org/commentaries/putting-gas-flaring-in-the-spotlight

- IEA. (2020c). World energy outlook 2020. https://www.iea.org/reports/world-energy-outlook-2020

- IEA. (2021a). Net zero by 2050. https://www.iea.org/reports/net-zero-by-2050

- IEA. (2021b). Tracking SDG7, the energy progress report 2021. https://iea.blob.core.windows.net/assets/b731428f-244d-450c-8734-af19689d7ab8/2021_tracking_SDG7.pdf

- IEA. (2021c). Curtailing methane emissions from fossil fuel operations. https://www.iea.org/reports/curtailing-methane-emissions-from-fossil-fuel-operations

- IEA. (2021d). Methane emissions from oil and gas. https://www.iea.org/reports/methane-emissions-from-oil-and-gas

- IEA. (2022). Global methane tracker 2022. https://www.iea.org/reports/global-methane-tracker-2022

- IMF. (2022, July 29). Surging energy prices in Europe in the aftermath of the war: How to support the vulnerable and speed up the transition away from fossil fuels. Working Paper No. 2022/152. https://www.imf.org/en/Publications/WP/Issues/2022/07/28/Surging-Energy-Prices-in-Europe-in-the-Aftermath-of-the-War-How-to-Support-the-Vulnerable-521457

- IPCC. (2021). Sixth assessment report. https://www.ipcc.ch/report/ar6/wg1/downloads/report/IPCC_AR6_WGI_Chapter_07.pdf

- Jenkins, K., McCauley, D., Heffron, R., Stephan, H., & Rehner, R. (2016). Energy justice: A conceptual review. Energy Research & Social Science, 11, 174–182. https://doi.org/10.1016/j.erss.2015.10.004

- Jenkins, K., Sovacool, B. K., & McCauley, D. (2018). Humanizing sociotechnical transitions through energy justice: An ethical framework for global transformative change. Energy Policy, 117(2018), 66–74. https://doi.org/10.1016/j.enpol.2018.02.036

- Kartha, S., Caney, S., Dubash, N. K., & Muttitt, G. (2018). Whose carbon is burnable? Equity considerations in the allocation of a “right to extract”. Climatic Change, 150(1-2), 117–129. https://doi.org/10.1007/s10584-018-2209-z

- Kimani, A. (2023, January 20). Upstream spending to rise to $485 billion in 2023. OilPrice.Com. https://oilprice.com/Energy/Crude-Oil/Upstream-Spending-To-Rise-To-485-Billion-In-2023.html

- Lahn, G., & Bradley, S. (2016). Left stranded? Extractives-led growth in a carbon-constrained world. Chatham House. https://www.chathamhouse.org/sites/default/files/publications/research/2016-06-17-left-stranded-extractives-bradley-lahn-final.pdf

- Lavaux, T., Giron, C., Mazzolini, M., D’Aspremont, A., Duren, C. D., Cusworth, D., Shindell, D., & Ciais, P. (2022, February). Global assessment of oil and gas methane ultra-emitters. Science, 375(6580), 557–561. https://doi.org/10.1126/science.abj4351

- Manley, D., Heller, P., & Cust, J. (2021). Oil-rich countries’ responses to energy transition: Managing the decline. In P. Cameron, X. Mu, & V. Roeben (Eds.), The global energy transition: Law, policy and economics for energy in the 21st century (pp. 25–48). Hart Publishing.

- Marcel, V. (2001). The constructivist debate; Bringing hermeneutics (properly). In Conference paper, International Studies Association. https://www.researchgate.net/publication/303287054_The_Constructivist_Debate_Bringing_Hermeneutics_Properly_In

- Marcel, V. (2020). Fostering resilience in emerging oil producers. Briefing paper, Chatham House, December, https://www.chathamhouse.org/2020/12/fostering-resilience-emerging-oil-producers

- Marcel, V., Tissot, R., Paul, A., & Omonbude, E. (2016). A local content decision tree for emerging producers. Chatham House. https://www.researchgate.net/publication/332028319_A_Local_Content_Decision_Tree_for_Emerging_Producers

- Masnadi, M., El-Houjeiri, H., Schunack, D., Li, Y., Englander, J., Badahdah, A., Monfort, J.-C., Anderson, J., Wallington, T., Bergerson, J., Gordon, D., Koomey, J., Przesmitzki, S., Azevedo, I., Bi, X., Duffy, J., Heath, G., Keoleian, G., McGlade, C., … Brandt, A. (2018). Global carbon intensity of crude oil production. https://doi.org/10.1126/science.aar6859.

- McCauley, D., & Heffron, R. (2018). Just transition: Integrating climate, energy and environmental justice. Energy Policy, 119, 1–7. https://doi.org/10.1016/j.enpol.2018.04.014

- McGlade, C., & Ekins, P. (2015, January 8). The geographical distribution of fossil fuels unused when limiting global warming to 2°C. Nature, 517(7533), 187–190. https://doi.org/10.1038/nature14016

- Meadowcroft, J. (2011). Engaging with the politics of sustainability transitions. Environmental Innovation and Societal Transitions, 1(1), 70–75. https://doi.org/10.1016/j.eist.2011.02.003

- Mihalyi, D., & Scurfield, T. (2020). How did Africa’s prospective petroleum producers fall victim to the presource curse? Policy Research Working Paper No. 9384. World Bank.

- Mitchell, B., Marcel, V., Gordon, D., & Ogeer, N. (2022). Minimising greenhouse gas emissions in the petroleum sector: The opportunity for emerging producers. African Development Bank. https://www.afdb.org/en/documents/minimising-greenhouse-gas-emissions-petroleum-sector-opportunity-emerging-producers

- Moss, T., & Kincer, J. (2020, August 7). What happens to global emissions if Africa triples down on natural gas for power?’ Blog, Energy for Growth Hub. https://www.energyforgrowth.org/blog/what-happens-to-global-emissions-if-africa-triples-down-on-natural-gas-for-power/

- Mutiso, R., & Auth, K. (2021, March 21). Sub-saharan Africa needs fair access to global carbon budget. World Economic Forum. https://www.weforum.org/agenda/2021/03/genuine-climate-justice-means-allowing-sub-saharan-africa-to-access-to-global-carbon-budget/

- Muttitt, G., & Kartha, S. (2020). Equity, climate justice and fossil fuel extraction: Principles for a managed phase out. Climate Policy, 20(8), 1024–1042. https://doi.org/10.1080/14693062.2020.1763900

- New Producers Group. https://www.newproducersgroup.online/

- Notre Dame Global Adaptation Initiative (ND-GAIN). https://gain.nd.edu/our-work/country-index/rankings/

- OECD. (2019a). Aligning development co-operation and climate action: The only Way forward. OECD Publishing. https://www.oecd-ilibrary.org/sites/b7ae8707-en/index.html?itemId=/content/component/b7ae8707-en

- OECD. (2020). Transition finance ABC methodology: A user’s guide to transition finance diagnostics. OECD Development Policy Papers, No. 26. OECD Publishing. https://doi.org/10.1787/c5210d6c-en.

- Okpanachi, E., Ambe-Uva, T., & Fassih, A. (2022). Energy regime reconfiguration and just transitions in the global south: Lessons for West Africa from Morocco’s comparative experience. Futures, 139, 102934. https://doi.org/10.1016/j.futures.2022.102934

- OPEC. (2019). Angola facts and figures. https://www.opec.org/opec_web/en/about_us/147.htm

- Palmer, J., & Bulkan, J. (2010). Legitimacy of public domain forest taxation, and combatting corruption in forestry. International Forestry Review, 12(2), 150–164. 15. https://doi.org/10.1505/ifor.12.2.150

- Prag, A. (2021, April 20). Greening the recovery from COVID-19: How sustainable will it be? OECD environment focus. OECD. https://oecd-environment-focus.blog/2021/04/20/greening-the-recovery-from-covid-19-how-sustainable-will-it-be/

- Pye, S., Bradley, S., Hughes, N., Price, J., Welsby, D., & Ekins, P. (2020). An equitable redistribution of unburnable carbon. Nature Communications, 11(1), 3968. https://doi.org/10.1038/s41467-020-17679-3 https://www.nature.com/articles/s41467-020-17679-3

- Quitzow, R., Thielges, S., Goldthau, A., Helgenberger, S., & Mbungu, G. K. (2019). Advancing a global transition to clean energy – the role of international cooperation. Economics: The Open-Access, Open-Assessment E-Journal, 13(1), https://doi.org/10.5018/economics-ejournal.ja.2019-48

- Roopsind, A., Sohngen, B., & Brandt, J. (2019). Evidence that a national REDD+ program reduces tree cover loss and carbon emissions in a high forest cover, low deforestation country. Proceedings of the National Academy of Sciences, 116(49), 24492–24499. https://doi.org/10.1073/pnas.1904027116

- Ross, M. L. (2015). What have we learned about the resource curse? Annual Review of Political Science, 18(1), 239–259. https://doi.org/10.1146/annurev-polisci-052213-040359

- Rushforth, J. (2021, June 17). Carbon Intensity in Crude Valuation. NPG Webinar. https://www.newproducersgroup.online/event/carbon-intensity-in-crude-valuation/

- Sachs, J. D., & Warner, A. M. (1995). Natural resource abundance and economic growth. National Bureau of Economic Research.

- Shehabi, A., & Al-Masri, M. (2022). Foregrounding citizen imaginaries: Exploring just energy futures through a citizens’ assembly in Lebanon. Futures, 140, 102956. https://doi.org/10.1016/j.futures.2022.102956

- Skytruth. https://viirs.skytruth.org/apps/heatmap/flarevolume.html#

- Smith, M. (2023, February 24). Suriname’s oil boom may not materialize until 2027. OilPrice.Com. https://oilprice.com/Energy/Crude-Oil/Surinames-Oil-Boom-May-Not-Materialize-Until-2027.html

- Steckel, J. C., Jakob, M., Flachsland, C., Kornek, U., Lessmann, K., & Edenhofer, O. (2017). From climate finance toward sustainable development finance. Wiley Interdisciplinary Reviews: Climate Change, 8(1). https://doi.org/10.1002/wcc.437

- Stevens, P., Lahn, G., & Kooroshy, J. (2015). The resource curse revisited. Research Paper, Chatham House, August 4, https://www.chathamhouse.org/2015/08/resource-curse-revisited

- Stoll, P. P., Pauw, W. P., Tohme, F., & Grüning, C. (2021). Mobilizing private adaptation finance: Lessons learned from the green climate fund. Climatic Change, 167(3–4). https://doi.org/10.1007/s10584-021-03190-1

- Suriname Energy Authority. (2021, October 12). Presentation to IHS seminar.

- Thomas, D., & Twyman, C. (2005). Equity and justice in climate change adaptation amongst natural-resource-dependent societies. Global Environmental Change, 15(2), 115–124. https://doi.org/10.1016/j.gloenvcha.2004.10.001

- US Treasury. (2021). Guidance on fossil fuel energy at the multilateral development banks. August. https://home.treasury.gov/system/files/136/Fossil-Fuel-Energy-Guidance-for-the-Multilateral-Development-Banks.pdf

- Wang, X., & Lo, K. (2021). Just transition: A conceptual review. Energy Research & Social Science, 82, 102291. https://doi.org/10.1016/j.erss.2021.102291

- Wong, C. (2022). Climate finance and the peace dividend, articulating the co-benefits argument. In C. Cash & L. A. Swatuk (Eds.), The political economy of climate finance: Lessons from international development. International Political Economy Series. Palgrave Macmillan.

- Wood Mackenzie. (2020). Are the majors transitioning out of sub-saharan Africa? Insight, August.

- World Bank. Sustainable energy for all (SE4ALL). https://openknowledge.worldbank.org/handle/10986/17138

- World Bank. (2021). World development indicators. https://databank.worldbank.org/

- World Bank. (2023). Country and lending groups. https://datahelpdesk.worldbank.org/knowledgebase/articles/906519-world-bank-country-and-lending-groups

- World Oil. (2023, February 16). Shell begins oil production at first GOM deepwater platform with new design. https://worldoil.com/news/2023/2/16/shell-begins-oil-production-at-first-gom-deepwater-platform-with-new-design/