ABSTRACT

Many oil and gas (O&G) companies began, in recent years, to increase their renewable and low-carbon energy (R&LCE) operations – crucial for climate mitigation. In Scotland, renewable electricity generation has tripled since 2009. However, this progress remains insufficient to meet carbon reduction targets. More effective public policies are needed to accelerate this trend while meeting energy needs and retaining energy industry employment, which is essential for a just transition. This study analyzes drivers of O&G industry investment into R&LCE to understand how government intervention can steer corporate decision-making. We develop and apply a conceptual framework of drivers of decisions for such investments. We conducted semi-structured interviews with 12 individuals in strategic positions working in O&G companies in Scotland, which are exemplary of similar O&G-intensive regions in the global North. We find that the energy transition narrative within the industry mostly supports developing R&LCE projects that build on existing O&G assets and expertise, such as blue hydrogen and carbon capture and storage. Industry-wide narratives encourage investment in R&LCE across the sector, not only in companies facing the most scrutiny. The findings suggest the need to tailor public policy to increase the pressure of drivers of change, including increasing restrictions on access to financial capital for O&G, emphasizing narratives that promote R&LCE, and working to lower the costs of accessing expertise and retraining employees in R&LCE technology. Transitioning employment without job loss through retraining workers synergizes private and social interests, so an emphasis on (re)training and education for capacity building can be an immediate successful policy approach for a just transition.

Key policy highlights

Diverse factors influence O&G companies’ decision-making on R&LCE.

O&G industry perceives government support (fiscal and non-financial, like knowledge-exchange networks) is important to drive private investment in R&LCE.

Industry paradigm evolving towards a more favourable view of the energy transition.

Industry perceives the need to continue O&G production alongside emissions-reduction technology (CCS and blue hydrogen).

Key factors to facilitate the transition are individual leadership and retraining to retain employment.

1. Introduction

Energy supply is one of the most significant contributors to global GHG emissions (IPCC, Citation2023), making shifting away from fossil fuels key in addressing climate change. The oil & gas (O&G) industry is responsible for a significant fraction of greenhouse gas emissions, directly and indirectly in production and consumption. Governments have responded to climate change by implementing policies to enable and accelerate the energy transition away from fossil fuels and towards renewable & low-carbon energy (R&LCE) while meeting energy needs and retaining quality employment.

In the UK, the Climate Change Act 2008 was amended in 2019 to commit the government to reduce the UK’s carbon emissions to net zero by 2050 (BEIS, Citation2019; UK Parliament, Citation2019), with Scotland planning to achieve it by 2045 (Scottish Parliament, Citation2019). Scotland is central to the UK’s energy transition plans because it produces 82% of the UK’s O&G (Dowens, Citation2021). Renewable energy here includes that which is generated from non-exhaustible resources like wind, solar, hydro and tidal power (Fattouh et al., Citation2018; REN21, Citation2020). Low-carbon energy is defined here to include that which is generated from finite sources that emit less CO2 than traditional fossil fuels, such as blue hydrogen and nuclear, and technology that reduces the amount generated by carbon-emitters, such as Carbon Capture and Storage (CCS) at gas-fired power stations (Dickel, Citation2020; Lu et al., Citation2019). O&G companies have promoted the latter as an intermediate stage in the energy transition (Van de Graaf, Citation2018) to maintain the gas revenues, some claim, needed to pursue further R&LCE (e.g. Shell, Citation2018).

The energy transition represents opportunities for Scotland, but it also risks injustices, in part because local communities heavily reliant on the O&G industry are vulnerable to industry relocations and job losses (Hirsch, Citation2020). Since O&G reserves were first discovered and exploited in the North Sea in the 1960s and 1970s (Shepherd, Citation2015), O&G has been core to the local and regional economy (Kemp, Citation2013), with Aberdeen dubbed ‘The Oil Capital of Europe’ (Innes & Monios, Citation2018). The industry boomed throughout the 1980s and weathered several oil price slumps, including in 2015 (Shepherd, Citation2015), which led to a significant downsizing of the sector (Innes & Monios, Citation2018). Scotland’s O&G reserves were once lauded as a source of economic opportunity and strength, but their exploitation has become more contested (Evensen et al., Citation2023; Ostfeld & Reiner, Citation2020). Recently proposed developments, such as the Cambo oil field near Shetland, have triggered controversy, suggesting that O&G companies operating in Scotland might struggle to continue exploiting the resources they have relied upon for decades.

While R&LCE has long garnered the interest of O&G companies (Chaiyapa et al., Citation2018), only in recent years they have begun increasing their operations in R&LCE substantially (Pickl, Citation2019). It is generally accepted that in the early stages of R&LCE development, government support is necessary: public policies broadly understood, both financial and institutional measures, including facilitating access to expertise and networks. However, some scholars argue that this stage (the ‘valley of death’ before commercial viability) has passed (Van de Graaf, Citation2018) and that intervention (public policy) is no longer required for R&LCE technology adoption, assuming that markets will pull technology diffusion (ibid.). Government support for R&LCE in Scotland comes through numerous channels, e.g. The North Sea Transition Deal (2021) between the UK Government and OGUK and the £26 million from the Scottish Government to fund the Aberdeen Energy Transition Zone, both pledging investment in R&LCE (BEIS and OGUK, Citation2021; Scottish Government, Citation2021; BBC News, Citation2021). Further financial and practical support is available through government-affiliated industry and regulatory bodies, such as the Oil and Gas Authority (OGA, Citation2021), and institutions like the Net Zero Technology Centre (NZTC), funded by governments and industry (NZTC, Citation2021). The recent rapid progress observed in voluntary R&LCE activities (in Scotland, at least) could suggest that the private sector might have taken the lead in the transition. Given significant public investment in the energy transition, it is important to understand what motivates the industry in this transition, in order to strongly justify this public investment and design effective public policies.

To this end, we analyze the motivations of O&G companies to increase their R&LCE operations. We aim to (1) identify the diversity of factors influencing O&G companies’ decisions to increase their R&LCE operations (Factors); (2) explore to what extent O&G companies would voluntarily choose to increase such operations in the absence of public policy and law (Voluntary choice); and (3) identify the main barriers to increasing private investment from O&G companies in R&LCE, where policy can support (Barriers). Understanding the motivations of O&G companies to increase investment in R&LCE can inform more effective policy to facilitate a just energy transition and aid the exploration of a paradigm change towards an increase in such operations. To address these aims, we develop a conceptual framework of drivers or motivations for O&G companies to increase R&LCE operations and present the findings of 12 semi-structured interviews with professionals from 11 firms (global engineering, consultancy, exploration, or operating) with relevant decision-making capacities within the O&G industry in Scotland.

Many O&G companies working in Scotland have been vocal about their new operations in R&LCE, setting out targets in their public strategy documents and widely publicizing the success of their green projects (e.g. Equinor, Citation2020; Shell, Citation2018), albeit this publicity may not reflect their dominant operations. Public documents articulate the reasons for transition that companies wish to advertise. However, research suggests that there may be further, non-disclosed or implicit motivations for engaging with R&LCE (Chaiyapa et al., Citation2018). Understanding these motivations is important to advance the energy transition (Steg et al., Citation2021) and identify levers to make it more just. ‘Implicit motivations’ refer here to drivers that guide company decisions, but are not necessarily referred to outside specific circles, e.g. government or industry groups. Hereafter, ‘motivations’ refers to both implicit and advertised ones.

Previous studies that have engaged with experts on the energy industry in Scotland focused on understanding the view from government or were conducted before the shock to the energy transition induced by COVID-19 (Cowell et al., Citation2017; Hirsch, Citation2020; McEwen & Bomberg, Citation2014; Okereke & Russel, Citation2010). These studies analyzed broader carbon emissions reductions across business activities by energy-intensive companies and the role of devolution in energy. Other studies have analyzed O&G as a subsidiary sector (Hellsmark & Hansen, Citation2020; Normann, Citation2015). We build upon these studies and focus on O&G businesses that are actively engaged in the shift towards R&LCE.

2. Conceptual framework of motivations for the O&G industry to invest in R&LCE

Our research began by conducting a qualitative review of the academic literature to identify major drivers or factors discussed across the range of motivations for the O&G industry to invest in R&LCE as a voluntary environmental action (details in Appendix A). Drivers are understood here in the behavioural sense, as the conditions that motivate change. While the concept of drivers is inspired by literature on broader voluntary environmental measures (see Kolstad, Citation2011), studies specifically about the drivers and motivations for the O&G industry to increase operations in R&LCE are rare. Therefore we have synthetized these drivers from a diverse body of literature.

We structured these factors by theme to create a framework of drivers that influence decisions for O&G company investments into R&LCE (). The framework illustrates the diversity of decision-making factors a firm could consider when deciding whether to increase R&LCE operations. We divided these drivers into two categories, adapted from the classification by Okereke and Russel (Citation2010): (1) external to O&G companies, including government action, and (2) internal to O&G companies, affecting operations from within. Given our research focus on government action, we disaggregate related factors in the framework. For each driver, explains the mechanism(s) of how it can encourage R&LCE operations and indicates supporting literature.

Table 1. Drivers of increased private operations from O&G firms in R&LCE (Source: the authors).

The drivers are articulated in the framework as positive – driving R&LCE uptake intentions and decisions. In most cases, if the driver is absent, it can be inferred that it may, instead, deter investment (i.e. drivers become barriers). For example, where O&G reserves are perceived to be significant (rather than limited; driver a.), or if R&LCE operations are not perceived as profitable relative to current O&G operations (e.g. green hydrogen production; driver b.). We discuss each driver below (further details in Appendix A).

An O&G companies’ known reserves (driver a.) have been found to have an inverse relationship with its investments in R&LCE (Pickl, Citation2019). In Scotland, oil production slowed since 2009 (BP, Citation2020), and this is reflected in higher UK imports of fossil fuels (Thomas, Citation2020). Regarding relative profitability (driver b.), the wind is the largest source of electrical R&LCE (Scottish Renewables, Citation2021), which fell in cost per kilowatt-hour between 2010 and 2018, and is now competitive in many markets (IRENA, Citation2019; REN21, Citation2020). Perceptions over the relative profitability of this and other R&LCE may vary, but the trend is robust, although counteracted by the volatility of O&G prices and supply due to international events. Difficulty in accessing capital (driver c.) for traditional O&G exploration and production ventures may steer O&G companies to diversify. Public opinion (driver d.) about energy production’s contribution to climate change is becoming more prominent and may influence decisions for several reasons, including to ensure the acceptability of ongoing or new operations (Chaiyapa et al., Citation2018), meeting customer green demand (Kolstad, Citation2011) and the need for a firm to maintain their Social License to Operate (Jijelava and Vanclay, Citation2017).

Regarding government role (driver e.), companies may adopt voluntary actions to either dissuade regulators from establishing compulsory rules or to gain a competitive advantage if laws are implemented (Aguirre & Ibikunle, Citation2014; Kolstad, Citation2011; Okereke & Russel, Citation2010). Certainty of policy continuity is vital to encourage energy companies to participate in R&LCE support programmes (Aguirre & Ibikunle, Citation2014). Normative pressure from the government may have also helped to set the stage for R&LCE in Scotland, through narratives describing ‘imaginaries of an energy independent and “green” nation’ (Hirsch, Citation2020, p. 2) embedded in energy and innovation strategies, for example. Narratives and discourses are used here in the Foucaldian sense: narratives are the way people tell stories, and discourses are the broader way of thinking expressed through language. Both narratives and discourses help humans construct meaning and knowledge about the world. These are expressed and operationalized in spoken and written language (reports, strategies or laws). Lastly, strong policy networks between government, NGOs, and the energy sector can also help foster the energy transition (Cowell et al., Citation2017; McEwen & Bomberg, Citation2014).

Internally, O&G companies possess engineering and project management expertise (driver f.) that is highly transferable in many cases to R&LCE development and implementation (assets that could be repurposed), and access to the financial capital to develop and deploy R&LCE technology on a commercial scale (Peng et al., Citation2019). An O&G company’s expressions of environmental concern (driver g.) have been correlated with its willingness to invest in R&LCE (Hartmann et al., Citation2021). Finally, shareholder demands (driver h.) evolving towards greener considerations can influence firm decisions (Kolstad, Citation2011; O’Rourke, Citation2003; Van de Graaf, Citation2018).

Overall, these factors may interact to drive private action for the energy transition (York & Bell, Citation2019). Drivers internal to the firms may be affected by external drivers, including government law and policy, and the later influenced by the other external drivers (e.g. energy security, market considerations and public opinion). All drivers may combine to favour a paradigm shift within O&G companies towards more investment in R&LCE (see Appendix A).

A paradigm, first introduced by Kuhn (Citation1962/Citation2012), is a set of commonly held beliefs about how a phenomenon functions, which informs and legitimizes related work (Bakken, Citation2019). The knowledge that underlies paradigms may be factual, but it is framed to form narratives. A change in paradigm (or in discourses and narratives) does not necessarily bring about change in behaviour although it is often a key step towards it. While originally used to refer to schools of scientific knowledge, Bakken’s (Citation2019) application of paradigms to the energy industry is useful in examining how and why a shift to R&LCE is happening within O&G companies. The ‘incumbent paradigm’ (Bakken, Citation2019, p. 184) in society and the O&G industry can be interpreted as energy being essential for ensuring a good standard of living for all, and therefore that there is a moral imperative to ensure that energy comes from the cheapest sources, assumedly fossil fuels. However, this paradigm is being replaced by another one (although still lagging emerging paradigms among other actors, such as epistemic communities): that GHG emissions and the resulting climate change have large-scale social and environmental impacts, disproportionately affect poorer people, and therefore energy needs should be met with R&LCE (Bakken, Citation2019). This raises the question of how that paradigm shift is occurring in O&G companies and the influence of government action.

3. Methods

We gathered primary data from 12 semi-structured interviews with contractors and senior employees working for a range of O&G companies operating in Scotland. Semi-structured interviews are chosen because they allow researchers to gather in-depth information from a group of individuals with specialized expertise and insight, including about implicit motivations. This methodology ensures that themes are covered consistently across respondents, while also allowing them to speak freely about related topics (Gibson & Brown, Citation2009) with sufficient depth and flexibility. Also, using interviews makes this research more directly comparable with previous studies on investment in R&LCE in Scotland, which often have used a similar approach (Cowell et al., Citation2017; Hirsch, Citation2020; McEwen & Bomberg, Citation2014; Okereke & Russel, Citation2010).

3.1. Sampling and interviews

The goal of our sampling approach was to elicit views from a wide diversity of professionals in a position to reliably identify drivers of change within the O&G industry. The sensitivity of industrial decisions (sometimes confidential or politically delicate) and concern over public image are known limitations to conducting interviews in the sector (Chaiyapa et al., Citation2018). This adds remarkable value to the sample we gathered.

The Interviewees included four respondents identified via researcher contacts, and eight accessed through a thorough process of identification via an online professional network and profiles leading to 44 invitations. Potential participants were selected through a body for energy professionals and from companies in OGUK’s directory (‘Oil & Gas UK’; OGUK Citation2021), which engaged in R&LCE or looking to move into the sector in Scotland according to their public mission. Respondents included employees of medium- and large-scale operators across the business chain of O&G operations, and have various disciplinary backgrounds (see Appendix B).

Questions were articulated based on the research aims with a view to eliciting drivers from the conceptual framework. However, most questions did not mention specific drivers, to mitigate bias (see Appendix B). The interview protocol briefly described the study and asked the core interview questions and baseline demographic questions. Respondents were asked to speak to their individual perspective and opinion regarding the sector and their company.

3.3. Analysis

We transcribed all interviews and shared the transcripts with participants to allow them to correct any mistakes and withdraw any confidential information that might have been shared in error. No substantive information was changed. We then coded qualitatively the transcripts (using nVivo 12 Pro), developing a codebook with 34 themes under which the content of the interviews was categorized (DeCuir-Gunby et al., Citation2011). The codes were developed as a combination of deduction (from the conceptual framework) and induction (from the themes raised in the interviews). This allowed as much of the relevant interview content to be included in the analysis as possible.

Where a statement pertained to two or more codes, we referenced it under all that were appropriate (DeCuir-Gunby et al., Citation2011). Coding allowed us to identify common themes across participants, in addition to those that were unique to individuals. This coding was reviewed, and transcripts analyzed twice. During the first review, the codes were adjusted to better reflect the data. The second review was undertaken to enhance internal validity and reliability, by ensuring that data were analyzed consistently across the interviews.

For reporting results, quotes were selected because they reflect patterns of views across the data succinctly. Fragments in square brackets are by the authors, to abbreviate, clarify or anonymize. The views reported are not necessarily those of the authors, and can be at odds with ambitious climate policy discourses; we describe them with the aim of understanding the diversity of opinions that must be navigated in climate policy.

4. Results and interpretation

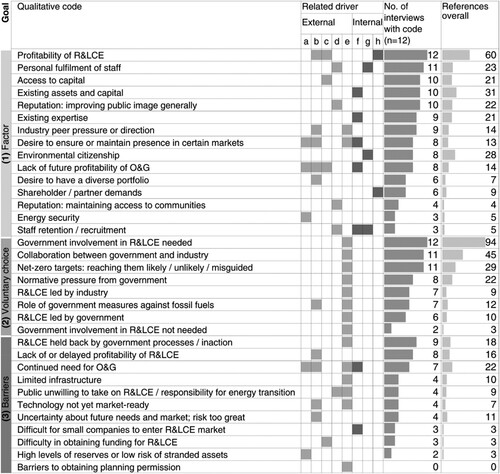

To report the results, the next subsections follow the conceptual framework, distinguishing between external and internal drivers. We associated each qualitative code with one of the three research goals, as well as with one or more driver in the conceptual framework (; columns ‘Goal’ and ‘Related driver’ respectively). We estimated how frequently each concept was mentioned in the interviews (; last two columns). All participants’ responses were considered equally.

Figure 1. Codebook and frequency results (Source: the authors). Drivers are external: (a) O&G reserves and energy security, (b) Profitability, (c) Access to capital, (d) Public opinion and reputation, (e) Government law and policy; and internal: (f) Existing expertise, capital and assets, (g) Environmental citizenship, (h) Shareholder demands. (Study) goals are those stated in the Introduction: (1) factors influencing decisions to increase R&LCE operations; (2) the role of public policy/ government involvement vis-a-vis fully voluntary choice; (3) explicit barriers to private investment.

Respondents highlighted a wide range of factors contributing to or preventing R&LCE investment, including many discussed in the literature. The most cited drivers encouraging investment, in overall mentions, were R&LCE profitability; government law and policy involvement and collaboration; access to capital; O&G companies’ existing capital and assets; and environmental citizenship and personal fulfilment. Notably uncommon at the time of the interviews, were concerns regarding energy security and shareholder demands. These may have heightened due to recent global developments in energy supply and public policy, such as the disruption in O&G provision from Russia.

In what follows, some codes are excluded as they were infrequently mentioned by participants or were given little importance. They are included in for completeness. The drivers in the following subsections are not necessarily exclusive, and quotations may be relevant to multiple themes.

Across all drivers, it transpired that a paradigm shift is occurring in the O&G industry with regards to the dominant attitude towards R&LCE. Several participants suggested that this change in narrative had become more powerful in recent years, e.g.:

[I]t became really clear in 2019, if you look at BP’s Economic Outlook from 2019, you’ll see a real key shift, […] the world all seem to go ‘Wow, this is real now, it’s not just for fun or daydreaming about anymore’, […] everybody seemed to, all at once, go ‘Yeah, this is real, let’s do something about it’, and [my employer is] part of that. (E5)

4.1. External drivers and barriers

4.1.1. O&G reserves and energy security

The interviews revealed little evidence suggesting that hydrocarbon reserves are a significant consideration – hydrocarbon levels in North Sea oil reserves were not discussed by any participants who were not prompted to consider it. When asked about the relevance of reserves to R&LCE decision-making, J10 and E11 emphasized that O&G will still be required throughout the energy transition for both traditional uses and R&LCE. As discussed later, the continued need for O&G as part of deploying R&LCE forms an important part of the new discourse within the industry.

Regarding stranded assets, some companies appeared to have worked with the assumption of being able to exploit all of their existing assets alongside R&LCE operations, and perhaps continue to do so:

[W]hen you look at the case of stranded assets, [reserves] that you’ve got on your portfolio, […] but are unlikely to ever be produced, […] in the [UK] sector we were operating [on the assumption of] 100% [of our reserves being produced]. (J10)

4.1.2. Relative profitability of R&LCE

The importance of R&LCE profitability to increase industry operations was explicitly mentioned by all interviewees: ‘[W]e definitely will not be doing projects which are not economic, that's for sure’ (H8).

Unsurprisingly, it was clear among respondents that investment in R&LCE by O&G companies depended on its profitability, relative to alternative operations (including business-as-usual). They agreed, either implicitly or explicitly, that R&LCE is an area of current and future growth, which will have ‘some tremendous winners’ (C3). While voluntary measures for R&LCE were once perceived as a cost for the O&G industry (an exercise in corporate social responsibility), views in the energy sector appear to have shifted to seeing R&LCE as an opportunity to capitalize upon (Okereke & Russel, Citation2010):

[A]ll the clients are talking about energy transition, […] offshore wind is growing […] whilst [O&G] is diminishing, […] clean energy is now our number one strategic target area. (K12)

[Independent advisors on climate change are] not saying that the economy is a zero-carbon [or] a zero-[O&G] economy, […] there is still a need, even in 2050, for [O&G] to exist. (J10)

Participants also portrayed using natural gas as ‘almost like a pseudo-energy transition’ (E11) due to its lower emissions relative to coal and oil. A transition pathway widely accepted within the O&G industry intertwines the need for hydrocarbons and R&LCE development, as follows: natural gas is useful to produce blue hydrogen and can provide revenue while the infrastructure for hydrogen is established (I9 and E11). Once the latter integrates into the energy mix and electricity production from renewable sources increases, green hydrogen production can be expanded (G7).

This use of natural gas as part of the energy transition has been criticized outside the O&G industry, with Ueckerdt et al. (Citation2021, p. 391) arguing that building hydrogen capacity at the expense of electrification through renewable sources, could risk ‘a lock-in of fossil-fuel dependency’. The consistency of the pro-hydrogen narrative among the employees interviewed, in the face of differing views outside the industry, suggests that this forms part of the new paradigm within the industry, encouraging R&LCE development while justifying continued O&G activities.

4.1.3. Access to capital

All interviewees but two discussed concerns over access to capital in the energy transition. They suggested that a threat to O&G venture funding was forcing companies to change their operations to fulfil Environmental, Social and Governance (ESG) requirements:

[W]e are linked to the big pension funds, we need to be kept that way, and you can’t do that if you’re not ethical and […] not seen to be genuinely looking to change. (D4)

The cost of capital for O&G projects, rather than its availability, may drive investment in R&LCE more notably. Capital for the latter is often cheaper (E11), and ‘more marginal [O&G] projects […] will not be developed’ (F6). This may increase investment in R&LCE on profitability grounds, should financial capital for O&G projects become too expensive.

4.1.4. Public opinion and reputation

Nearly all participants referred to the role of the public in the energy transition. Some emphasized that their employers were keen to engage with civil society to inform their strategies and activities (E5, G7 and H8). Others suggested that public perception was important for maintaining their Social License to Operate (D4, G7, I9, J10 and K12), which was considered at a national or European level, rather than with regards to relations with local communities close to energy production. Overall, this implies a very superficial approach to procedural justice (which requires inclusive representation in decision making; Santos Ayllón & Jenkins, Citation2023), but that public pressure still influences O&G companies:

[P]ublic perceptions are forcing a change of behaviour amongst the [O&G] community: for example, [a large international operator] bought its way into offshore renewables, [only] because they needed to get a green presence. (K12)

[P]eople who love the Earth and [environmental non-profit organisations], go after [large international O&G companies], but […] there is going to come a time where midsized companies will be exposed. (E11)

In parallel, participants’ references to personal fulfilment suggest an influence of social norms internalized by staff:

I’m a believer in the next generation, […] and who’s caring about them? In the current government it doesn’t feel […] like anybody [does]. But at least [my employer does]. (E5)

4.2. Governmental law and policy

All participants emphasized that government intervention is essential to facilitate investment in R&LCE by O&G companies (as represented by a high frequency of all categories of government drivers in ).

4.2.1. Restriction of carbon emissions and fossil fuel use

Perhaps unsurprisingly, measures that make high-emission activities more expensive are a major factor for O&G companies to consider R&LCE. Discussing the short term, participants focused on actions to increase energy efficiency of O&G operations. In the longer term, many suggested that expected high carbon prices influenced investment in R&LCE:

[C]arbon pricing has moved significantly within the last, […] 12, 24 months […]. It could be foreseeable that […] you’re either going to be pushed towards reducing those emissions in order to continue [towards] your planned cessation of production […], or you pull that cessation of production forward. (J10)

It is good that the government is pushing through regulation to say, ‘you have to start moving towards no local emissions’, and at the same time, encouraging the market by investing in it. If they weren’t doing that it would be too easy for profit-driven companies to just say ‘we’ll do it in the future, […] when the technology is there, and when the other more value-added opportunities aren’t there to compete against it’. (E5)

4.2.2. Support for R&LCE

Government measures to support the development, deployment, and uptake of R&LCE were considered vital. Three participants working for companies developing new R&LCE technology emphasized the particular role of government support in progressing fledgling technology due to the risk of investing in unproven technology which might not succeed (A1, J10 and K12). This aligns with the importance the private sector gives to government support for new technologies towards commercial viability (Weiss & Bonvillian, Citation2009). For smaller companies, this funding can be essential to develop and demonstrate new R&LCE and, ‘because of that demonstration, they will be able to attract investment’ (K12).

When discussing government support for more established R&LCE technology, nearly all participants stated that without it, many or all of these projects would not proceed, although they stressed that this did not mean the companies themselves were dependent on the support (G7 and H8). These two observations appear somewhat contradictory. However, they suggest a perception that government support has encouraged companies to invest in certain R&LCE projects that would not be of their interest otherwise.

All but one interviewee mentioned the importance of active collaboration between government and industry, with some emphasizing that it is critical for effective policies encouraging energy companies to maintain their presence in Scotland. A respondent suggested that the industry can do certain projects independently (such as emission reduction projects on offshore installations) triggered by carbon pricing and internal drivers alone. However, to encourage large-scale R&LCE ventures (with the potential for long-term production capacity), government support was perceived as imperative:

[Without] support from government, [the] industry would probably do nothing, […] it’s based entirely upon input from government to get the right behaviours and support the right opportunities. (J10)

[My employer]’s mantra is to try and invest in a jurisdiction [where] you know policies will be […] stable, and it’s not […] one government coming in today with one policy, and then […] the same government wakes up tomorrow, policies are changing. (E11)

4.2.3. Government discourse and networks

Institutional discourse (the narratives used in written and oral communications, conveying values and desirable goals, among others) and support for policy and information networks facilitate knowledge sharing among industry actors (Cowell et al., Citation2017; McEwen & Bomberg, Citation2014). Besides financial measures, all participants mentioned the importance of energy policy networks and consultations to encourage interest and investment. For example, regarding the NZTC in Aberdeen:

[N]ot only does it help to get the financial assistance but […] they’re building the network, […] so that we can then seek out expertise, innovation, [and] technology, to carry out these projects, because it’s all frontier really, […] it’s good that there’s the government support to […] get past that and start applying it. (E5)

[T]he trick is to push in the direction that we’ve seen over the past several years [when] conversations intensified about switching from fossil fuels to renewable generation. (F6)

4.3. Internal drivers and barriers

4.3.1. Existing expertise, capital, and assets

The firm-specific advantages to further R&LCE investment that appeared most salient were the presence of existing expertise, capital, and assets. Expecting less future O&G demand, companies are exploring the potential of converting their existing O&G assets into R&LCE facilities, and these assets may determine the type of projects in which companies invest:

[T]owards the end of the value chain of [O&G] is, what do you do with your assets that you have? […] [I]t’s very attractive to be able to [use] them for something else. And in the UK […] CCS and hydrogen are the obvious candidates. (I9)

Further, many O&G competencies were seen to be transferable to R&LCE, so specific company expertise can give a competitive advantage in certain R&LCE technology sectors, such as hydrogen:

[I]t fits with our existing skillset, all the engineering that we employ, […] the whole infrastructure of our business doesn’t really need to change much to get involved in that space, it’s very much akin to what we already do with [O&G] projects. (B2)

[I]f we look at the [numerous] people in [my employer]’s office, […] maybe [1/6] of them might have transferable skills, […] you’re looking at some real niche skills around chemicals or subsea reinjection […], so it’s not a huge amount actually. (D4)

4.3.2. Environmental citizenship

Several interviewees suggested that environmental commitments in their employers’ strategies have a material impact on day-to-day activities, including investments in R&LCE:

[My employer] is ensuring that they’re delivering per their own strategy, […] updating the parameters that they normally use to make go/no-go decisions for any investment, and including decarbonisation is a key part. (G7)

Some participants discussed how their own personal fulfilment drove them to work in the energy industry, sometimes specifically in R&LCE. This suggests that individuals’ sense of environmental citizenship and personal motivations can also steer operations:

I had always been a committed environmentalist. […] I got the opportunity to transition […] into the renewable part of the business four years ago. [T]he renewable part of [my employer] then was so small and […] like a start-up mentality. And I remember folks saying to me, ‘What are you doing? You are throwing away your education, your career, etc., for something that’s so uncertain […]’. I thought, well, these are the principles I have, this is why I came in […] and it definitely wasn’t easy for the first few years, but gradually, we’ve grown the business up, I’ve been part of shaping [it] up, I’m really privileged and humbled to be part of it from the beginning. (C3)

4.3.3. Shareholder demands

Participants rarely mentioned shareholder demands, but some implied that their influence was important to high-level business decisions (F6, G7 and I9). One participant suggested that their employer’s core business was defined by shareholders:

[I]f we did want to diversify or pivot, we would have to rewrite all of our agreements around the establishment of the company. So […] although there are options there, it’s what our investors are telling us, […] they want us to be focused on [O&G] and this is the core of our business. (I9)

5. Discussion

Our first research aim was to identify the diversity of factors influencing decision-making on R&LCE within O&G companies, of which we found a wide variety. To deploy a sufficient range of R&LCE on a large scale, it must be more profitable than O&G in the long term. Government law and policy notably influence O&G companies, particularly through fiscal measures (e.g. carbon pricing and subsidies) and non-financial support for R&LCE projects. Government discourse and networks (the narratives used in formal communications, and the platforms and other initiatives to connect experts) are also important in steering the paradigm within the industry. These facilitate sharing and accessing expertise, influence social norms, and prompt the industry to see competitive advantages in the transition.

Regarding our second aim of exploring the extent to which O&G companies would voluntarily increase R&LCE operations in the absence of public policy and law, the findings suggest that they would not invest to the same extent without such government policy. It is rational for companies to explore efficiency measures to reduce costs. Yet from the interviews, it appears unlikely that O&G companies would have pursued independently significant technological innovation or large-scale R&LCE projects (e.g. quote by E5 in subsection ‘4.2.1. Restriction of carbon emissions and fossil fuel use’). In the absence of government policies to aim to limit carbon emissions many companies would not have innovated, in line with the Porter Hypothesis (Porter & van der Linde, Citation1995). Interviewees also argued that institutional support for R&LCE (such as providing subsidies and enabling networks) has been integral to increase capacity, and it will continue to be essential throughout the transition.

The third aim sought to identify barriers to private investment in R&LCE. Our results indicate a perceived continued need for O&G production alongside emissions-reduction technology. This perception diminishes the incentives for O&G companies to invest in R&LCE. Companies are still able to access capital for O&G in accordance with ESG requirements, and the implementation of some R&LCE is intertwined with O&G, such as blue hydrogen. These two aspects lessen the perceived pressure to replace O&G production and thus contribute to justify decisions to continue O&G production.

5.1. Policy implications

The energy transition presents major opportunities also for the O&G industry, but it is deeply disruptive to their traditional work too. This potential disruption hinders this powerful group from taking a favourable position towards ambitious mitigation targets in negotiations. The emergent O&G paradigm explored in this research gives indication that negative perceptions about this disruption due to a clean energy transition are diminishing. These negative perceptions are further reduced with R&LCE innovation that fits well with existing O&G assets and expertise, such as blue hydrogen, CCS, and the use of renewable energy to reduce emissions in hydrocarbon production (like transport electrification or switching electricity sources).

In parallel, interview results regarding several drivers suggest there is an overall belief that O&G operations may continue, and that extant assets may be exploited to fund the energy transition, particularly blue hydrogen and CCS. The continued emphasis on CCS appreciated throughout the interviews highlights an emerging challenge. Based on this belief, companies are able to justify long-term O&G production, which could hamper the advance of R&LCE. This focus represents a rather narrow transition pathway, anchored in what wider evidence suggests are second- (or third-)best strategies; following IPCC (Citation2022, Citation2023) reports, CCS solutions show lower potential and higher costs to mitigate emissions in the energy sector than, e.g. energy efficiency and renewable sources. For a rapid clean energy transition to occur, there is thus a need to counteract the narrative that the transition requires a middle step via CCS and natural gas. This suggests a need for intervention to restrict O&G production while also facilitating R&LCE expansion. An emphasis on diversification, reorientation, and technological phase-out (Andersen & Gulbrandsen, Citation2020; Mäkitie et al., Citation2019) can encourage a stronger support for the leap required for fast emission reduction. Such intervention could be aided, among others, by renewed government narratives that diminish the acceptability of continued O&G production. Another barrier relates to government processes and regulations deemed to be outdated (like lengthy project approvals), which hinder private investment in R&LCE in some circumstances and may need to be revised and tailored to R&LCE.

The interview evidence also highlighted the importance of individual leadership in R&LCE initiatives within the O&G industry. Self-aware professionals may undertake activities they believe in, i.e. expanding R&LCE activities, despite colleagues in their working environment not supporting or informally disapproving of these activities due to uncertainty, risk, or different values (e.g. quote by C3 in ‘4.3.2. Environmental citizenship’). Such individuals are pivotal in the pioneering stage of innovation diffusion, arguably when innovators are subject to criticism and extra scrutiny (like in the above quote). Initiatives for social or professional recognition of individual pioneering work can help in this area. Although this stage fades out as R&LCE efforts become more normalized.

5.2. Further research

The findings point to further areas of research to better inform public policy for a just energy transition. Our results show that government support and collaboration are crucial from the perspective of the industry. The next step is to investigate the effectiveness of specific interventions to encourage deployment of R&LCE technology that is independent of O&G production (e.g. R&LCE not suited to utilizing existing O&G assets or expertise, like onshore wind, solar farms; or decentralized systems like domestic solar or electric cars for battery storage). Such technologies may need more government support than emission mitigation technologies favoured by the O&G sector such as CCS and blue hydrogen. Further diversity of perspectives can also be uncovered, such as whether the emphasis on drivers differs by firms’ level of engagement with R&LCE. Perspectives of industry representatives are also highly dynamic, they continue shifting. Understanding their evolution over time is ever more relevant in a context of rapidly evolving global narratives around energy security and sustainability, influenced by global political events, such as conflicts affecting international O&G trade and energy policy, and increasingly ambitious international agreements on climate change mitigation. Also, understanding the impact of such views on decisions, i.e. the attitude-action gap, merits further attention: actions by private firms may be preceded by a change in internal narratives (which influence intentions), so there may be a lag (or a gap) between this change and the firm acting upon it.

6. Conclusion

Our results suggest a favourable disposition within the Scottish O&G industry to increase investment in R&LCE on several levels. This is driven particularly by considerations of R&LCE profitability, utilizing existing expertise, capital and assets (notably market-based drivers), and by the personal motivations of industry workers. However, in response to the central research question, understanding the motivations of O&G companies to increase investment in R&LCE, the results also suggest that this appetite for R&LCE expansion is perceived to have largely been achieved through government intervention and, to an extent, public pressure; industry representatives perceive the government as crucial for the industry to increase R&LCE operations. Regarding two key elements of a just energy transition, while energy security (access) is not perceived as a challenge by interviewees, job loss is a known concern for communities in Scotland, and interviewees hint at the potential to transfer and retrain workers in new R&LCE operations, which in turn would avoid impacting wider employment (Scheer et al., Citation2022).

This research highlights areas where government policy could influence private investment in R&LCE: incentivizing investors to focus on non-O&G related R&LCE, facilitating training (to address concerns over continuity of employment) and access to specialist expertise, and tailoring narratives (i.e. the language used in written and oral communications) to shape the ongoing paradigm shifts through networks. In particular, industry priorities exist about skill transfer, and these align with societal priorities to avoid disruption to employment in relevant communities. Therefore, this area can be an immediate strategy where government intervention supports a transformational and ultimately just energy transition.

Supplemental Material

Download MS Word (166.5 KB)Disclosure statement

No potential conflict of interest was reported by the authors.

References

- Aguirre, M., & Ibikunle, G. (2014). Determinants of renewable energy growth: A global sample analysis. Energy Policy, 69, 374–384. https://doi.org/10.1016/j.enpol.2014.02.036

- Andersen, A. D., & Gulbrandsen, M. (2020). The innovation and industry dynamics of technology phase-out in sustainability transitions: Insights from diversifying petroleum technology suppliers in Norway. Energy Research & Social Science, 64, 101447. https://doi.org/10.1016/j.erss.2020.101447

- Bakken, B. E. (2019). Energy transition dynamics: Does participatory modelling contribute to alignment among differing future world views? Systems Research and Behavioral Science, 36(2), 184–196. https://doi.org/10.1002/sres.2578

- BBC News. (2021). Scottish government provides £26 m to help green energy transition. BBC News, June 19, 2021, sec. Scotland Business. https://www.bbc.com/news/uk-scotland-scotland-business-57539254

- BEIS. (2019). UK becomes first major economy to pass net zero emissions law. GOV.UK (blog). Retrieved June 27, 2019, from https://www.gov.uk/government/news/uk-becomes-first-major-economy-to-pass-net-zero-emissions-law.

- BEIS and OGUK. (2021). North sea transition deal. BEIS. https://assets.publishing.service.gov.uk/government/uploads/system/uploads/attachment_data/file/972520/north-sea-transitiondeal_A_FINAL.pdf

- BP. (2020). BP statistical review of world energy 2020. BP. https://www.bp.com/en/global/corporate/energy-economics/statistical-review-of-world-energy.html

- Chaiyapa, W., Esteban, M., & Kameyama, Y. (2018). Why go green? Discourse analysis of motivations for Thailand’s oil and gas companies to invest in renewable energy. Energy Policy, 120, 448–459. https://doi.org/10.1016/j.enpol.2018.05.064

- Cowell, R., Ellis, G., Sherry-Brennan, F., Strachan, P. A., & Toke, D. (2017). Energy transitions, sub-national government and regime flexibility: How has devolution in the United Kingdom affected renewable energy development? Energy Research & Social Science, 23, 169–181. https://doi.org/10.1016/j.erss.2016.10.006

- DeCuir-Gunby, J. T., Marshall, P. L., & McCulloch, A. W. (2011). Developing and using a codebook for the analysis of interview data: An example from a professional development research project. Field Methods, 23(2), 136–155. https://doi.org/10.1177/1525822X10388468

- Dickel, R. (2020). “Blue hydrogen as an enabler of green hydrogen: The case of Germany.” NG 159. Oxford Institute for Energy Studies. https://www.oxfordenergy.org/publications/blue-hydrogen-as-an-enabler-of-green-hydrogen-the-case-of-germany/.

- Dowens, J. (2021). Oil and gas production statistics 2019. Scottish Government. https://www.gov.scot/publications/oil-and-gas-production-statistics-2019/.

- Equinor. (2020). Equinor sustainability report 2020. Equinor. https://www.equinor.com/en/sustainability.html.

- Ershaghi, I. (2019). Ethical issues facing engineers in oil and gas operations. In A. E. Abbas (Ed.), Next-generation ethics: Engineering a better society (pp. 245–257). Cambridge University Press.

- Evensen, D., Whitmarsh, L., Devine-Wright, P., Dickie, J., Bartie, P., Foad, C., Bradshaw, M., Ryder, S., Mayer, A., & Varley, A. (2023). Growing importance of climate change beliefs for attitudes towards gas. Nature Climate Change, 13(3), 240–243. https://doi.org/10.1038/s41558-023-01622-7

- Fattouh, B., Poudineh, R., & West, R. (2018). The rise of renewables and energy transition: What adaptation strategy for oil companies and oil-exporting-countries? OIES Paper: MEP 19. Oxford Institute for Energy Studies, https://doi.org/10.26889/9781784671099

- García-García, P., Carpintero, Ó., & Buendía, L. (2020). Just energy transitions to low carbon economies: A review of the concept and its effects on labour and income. Energy Research & Social Science, 70, 101664. https://doi.org/10.1016/j.erss.2020.101664

- Gibson, W., & Brown, A. (2009). Working with qualitative data. SAGE Publications, Ltd.

- Hartmann, J., Inkpen, A. C., & Ramaswamy, K. (2021). Different shades of green: Global oil and gas companies and renewable energy. Journal of International Business Studies, 52(5), 879–903. https://doi.org/10.1057/s41267-020-00326-w

- Hellsmark, H., & Hansen, T. (2020). A new dawn for (oil) incumbents within the bioeconomy? Trade-offs and lessons for policy. Energy Policy, 145, 111763. https://doi.org/10.1016/j.enpol.2020.111763

- Hirsch, S. L. (2020). Governing technological zones, making national renewable energy futures. Futures, 124, 102648. https://doi.org/10.1016/j.futures.2020.102648

- Innes, A., & Monios, J. (2018). Identifying the unique challenges of installing cold ironing at small and medium ports – The case of Aberdeen. Transportation Research Part D: Transport and Environment, 62, 298–313. https://doi.org/10.1016/j.trd.2018.02.004

- IPCC. (2022). Ipcc sixth assessment report: Working group III: Mitigation of climate change. Summary for policymakers. IPCC. https://www.ipcc.ch/report/ar6/syr/.

- IPCC. (2023). Climate change 2023: Synthesis report. IPCC. https://www.ipcc.ch/report/ar6/syr/.

- IRENA. (2019). Renewable power generation costs in 2018. International Renewable Energy Agency. https://www.irena.org/-/media/Files/IRENA/Agency/Publication/2019/May/IRENA_Renewable-Power-Generations-Costs-in-2018.pdf

- Jijelava, D., & Vanclay, F. (2017). Legitimacy, credibility and trust as the key components of a social licence to operate: An analysis of BP's projects in Georgia. Journal of Cleaner Production, 140, 1077–1086. https://doi.org/10.1016/j.jclepro.2016.10.070

- Kemp, A. (2013). The official history of north sea oil and gas: Vol. I: The growing dominance of the state. Routledge.

- Kolk, A., & Pinkse, J. (2008). A perspective on multinational enterprises and climate change: learning from ‘an inconvenient truth’? Journal of International Business Studies, 39(8), 1359–1378. https://doi.org/10.1057/jibs.2008.61

- Kolstad, C. (2011). Intermediate environmental economics: International edition. Chapter 14. Voluntary Measures. Oxford University Press.

- Kuhn, T. S. (1962/2012). The structure of scientific revolutions: 50th anniversary edition. University of Chicago Press.

- Lu, H., Guo, L., & Zhang, Y. (2019). Oil and gas companies’ low-carbon emission transition to integrated energy companies. Science of the Total Environment, 686, 1202–1209. https://doi.org/10.1016/j.scitotenv.2019.06.014

- Mäkitie, T., Normann, H. E., Thune, T. M., & Sraml Gonzalez, J. (2019). The green flings: Norwegian oil and gas industry’s engagement in offshore wind power. Energy Policy, 127, 269–279. https://doi.org/10.1016/j.enpol.2018.12.015

- Marques, A. C., & Fuinhas, J. A. (2012). Are public policies towards renewables successful? Evidence from European countries. Renewable Energy, 44, 109–118. https://doi.org/10.1016/j.renene.2012.01.007

- Marques, A. C., Fuinhas, J. A., & Pires Manso, J. R. (2010). Motivations driving renewable energy in European countries: A panel data approach. Energy Policy, 38(11), 6877–6885. https://doi.org/10.1016/j.enpol.2010.07.003

- McEwen, N., & Bomberg, E. (2014). Sub-State climate pioneers: The case of Scotland. Regional & Federal Studies, 24(1), 63–85. https://doi.org/10.1080/13597566.2013.820182

- Nemet, G. F., Zipperer, V., & Kraus, M. (2018). The valley of death, the technology pork barrel, and public support for large demonstration projects. Energy Policy, 119, 154–167. https://doi.org/10.1016/j.enpol.2018.04.008

- Nilsen, T. (2017). Innovation from the inside out: Contrasting fossil and renewable energy pathways at statoil. Energy Research & Social Science, 28, 50–57. https://doi.org/10.1016/j.erss.2017.03.015

- Normann, H. E. (2015). The role of politics in sustainable transitions: The rise and decline of offshore wind in Norway. Environmental Innovation and Societal Transitions, 15, 180–193. https://doi.org/10.1016/j.eist.2014.11.002

- NZTC. (2021, March). About us: Performance. Net Zero Technology Centre. https://www.netzerotc.com/about-us/performance/

- OGA. (2021). OGA overview 2021. OGA. https://www.ogauthority.co.uk/media/7141/ukcs-a5-overview-final_web.pdf

- OGUK. (2021). Operators directory – OGUK. Oil and gas UK. 2021. https://oguk.org.uk/members-directory/operators-directory/.

- Okereke, C., & Russel, D. (2010). Regulatory pressure and competitive dynamics: Carbon management strategies of UK energy-intensive companies. California Management Review, 52(4), 100–124. https://doi.org/10.1525/cmr.2010.52.4.100

- O’Rourke, A. (2003). A new politics of engagement: Shareholder activism for corporate social responsibility. Business Strategy and the Environment, 12(4), 227–239. https://doi.org/10.1002/bse.364

- Ostfeld, R., & Reiner, D. M. (2020). Public views of Scotland’s path to decarbonization: Evidence from citizens’ juries and focus groups. Energy Policy, 140, 111332. https://doi.org/10.1016/j.enpol.2020.111332

- Peng, Y., Li, J., & Yi, J. (2019). International oil companies’ low-carbon strategies: Confronting the challenges and opportunities of global energy transition. IOP Conference Series: Earth and Environmental Science, 237(4). https://doi.org/10.1088/1755-1315/237/4/042038

- Pickl, M. J. (2019). The renewable energy strategies of oil majors – from oil to energy? Energy Strategy Reviews, 26, 100370. https://doi.org/10.1016/j.esr.2019.100370

- Porter, M. E., & van der Linde, C. (1995). Toward a new conception of the environment-competitiveness relationship. Journal of Economic Perspectives, 9(4), 97–118. https://doi.org/10.1257/jep.9.4.97

- Prno, J. (2013). An analysis of factors leading to the establishment of a social licence to operate in the mining industry. Resources Policy, 38(4), 577–590. https://doi.org/10.1016/j.resourpol.2013.09.010

- Rauter. (2022). Elite energy transitions: Leaders and experts promoting renewable energy futures in Norway. Energy Research & Social Science, 88, 102509. https://doi.org/10.1016/j.erss.2022.102509

- REN21. (2020). Renewables 2020 global status report. REN21 Secretariat. https://www.ren21.net/reports/global-status-report/.

- Rugman, A. M., & Verbeke, A. (1998). Corporate strategies and environmental regulations: An organizing framework. Strategic Management Journal, 19(4), 363–375. https://doi.org/10.1002/(SICI)1097-0266(199804)19:4<363::AID-SMJ974>3.0.CO;2-H

- Rugman, A. M., & Verbeke, A. (2000). Six cases of corporate strategic responses to environmental regulation. European Management Journal, 18(4), 377–385. https://doi.org/10.1016/S0263-2373(00)00027-X

- Santos Ayllón, L. M., & Jenkins, K. (2023). Energy justice, just transitions and Scottish energy policy: A re-grounding of theory in policy practice. Energy Research & Social Science, 96, 102922. https://doi.org/10.1016/j.erss.2022.102922

- Scheer, A., Schwarz, M., Hopkins, D., & Caldecott, B. (2022). Whose jobs face transition risk in Alberta? Understanding sectoral employment precarity in an oil-rich Canadian province. Climate Policy, 22(8), 1016–1032. https://doi.org/10.1080/14693062.2022.2086843

- Scottish Government. (2021, June 19). Delivering an energy transformation. Scottish Government. News (blog). https://www.gov.scot/news/delivering-an-energy-transformation/

- Scottish Parliament. (2019). Climate change (emissions reduction targets) (Scotland) act 2019. https://uk.westlaw.com/Document/IACBBB430FC7011E9ADBCF85583773D0E/View/FullText.html.

- Scottish Renewables. (2021). Renewable energy facts & statistics | Scottish renewables. https://www.scottishrenewables.com/our-industry/statistics

- Shell. (2018). Shell Energy Transition Report. Shell. https://www.shell.co.uk/a-cleaner-energy-future/our-response-to-climate-change/_jcr_content/par/textimage.stream/1524757699226/3f2ad7f01e2181c302cdc453c5642c77acb48ca3/web-shell-energy-transition-report.pdf.

- Shepherd, M. (2015). Oil strike north sea: A first-hand history of north sea oil. Luath Press Ltd.

- Steg, L., Perlaviciute, G., Sovacool, B. K., Bonaiuto, M., Diekmann, A., Filippini, M., Hindriks, F., Jacobbson Bergstad, C., Matthies, E., Matti, S., Mulder, M., Nilsson, A., Pahl, S., Roggenkamp, M., Schuitema, G., Stern, P. C., Tavoni, M., Thøgersen, J., & Woerdman, E., (2021). A research agenda to better understand the human dimensions of energy transitions. Frontiers in Psychology, 12. https://doi.org/10.3389/fpsyg.2021.672776

- Thiri, M. A., Villamayor-Tomas, S., Scheidel, A., & Demaria, F. (2022). How social movements contribute to staying within the global carbon budget: Evidence from a qualitative meta-analysis of case studies. Ecological Economics, 196, 107356. https://doi.org/10.1016/j.ecolecon.2022.107356

- Thomas, N. (2020, January 20). Scotland considers a future without oil and gas. Financial Times. https://www.ft.com/content/d984e6ea-2258-11ea-b8a1-584213ee7b2b

- Ueckerdt, F., Bauer, C., Dirnaichner, A., Everall, J., Sacchi, R., & Luderer, G. (2021). Potential and risks of hydrogen-based e-fuels in climate change mitigation. Nature Climate Change, 11(5), 384–393. https://doi.org/10.1038/s41558-021-01032-7

- UK Parliament. (2019). Climate change Act 2008 (2050 target amendment) Order 2019. https://uk.westlaw.com/Document/I2B734F20996311E9A309D215B5DEFD99/View/FullText.html.

- Van de Graaf, T. (2018). Battling for a shrinking market: Oil producers, the renewables revolution, and the risk of stranded assets. In D. Scholten (Ed.), In The geopolitics of renewables (pp. 97–121). Springer International Publishing AG.

- Weiss, C., & Bonvillian, W. B. (2009). Structuring an energy technology revolution. Massachusetts Institute of Technology.

- York, R., & Bell, S. E. (2019). Energy transitions or additions?: Why a transition from fossil fuels requires more than the growth of renewable energy. Energy Research & Social Science, 51, 40–43. https://doi.org/10.1016/j.erss.2019.01.008

- Zhong, M., & Bazilian, M. D. (2018). Contours of the energy transition: Investment by international oil and gas companies in renewable energy. The Electricity Journal, 31(1), 82–91. doi:10.1016/j.tej.2018.01.001