ABSTRACT

According to most climate mitigation scenario assessments, limiting global warming to 1.5–2°C in the long run will not be possible without the extensive deployment of carbon dioxide removal (CDR) from the atmosphere. CDR is required for drawing down and achieving net-zero CO2 emissions by mid-century. Thereafter, CO2 removals will likely need to exceed residual CO2 emissions, resulting in net negative emissions. A policy framework based on ‘carbon removal obligations’ (CROs) has been proposed to respond to concerns about the financial and fiscal viability, the lack of incentives for CDR uptake, as well as the physical and technological risks associated with any climate mitigation scenario that relies on large scale CDR. Here we propose an updated and improved CRO policy framework, consisting of two core elements: the ‘principal CRO mechanism’ obliges emitters of a tonne of CO2 to remove a tonne of CO2 at the time of maturity of the CRO. On top of this obligation, CRO holders need to pay a fee for the temporary storage of CO2 in the atmosphere. This ‘CRO pricing instrument’ is used by regulators to steer the carbon emissions and removals pathways independently. Our update suggests that markets for CDR under the CRO framework should operate independently from markets for emission reductions. We propose a blueprint for legal implementation where CROs are integrated akin to private financial borrowing and debt mechanisms. By aligning CROs with established financial systems, we leverage familiar institutional roles, seamlessly integrating climate mitigation into the core economy.

Key policy insights

The proposal applies the polluter pays principle to the costs of carbon removal from the atmosphere, whilst providing legal guarantees that the removals will materialize.

By placing climate change mitigation pricing levers in the hands of the traditional managers of financial stability, that is, central banks, better account is taken of the externality of carbon emissions as part of core economic and financial management, with the corollary that climate change mitigation response management is better integrated into the economic mainstream.

Establishing a standard for the creation of removal units by CDR projects facilitates a more efficient market by reducing transaction costs and enhancing price discovery.

Early action by government to put in place legislative measures indicating the direction of policy, and a timetable for introducing CROs, would enhance private sector confidence and engagement in the CDR project sector.

1. Introduction

Many countries – representing more than two thirds of global GDP – and numerous international corporations, have pledged to achieve net zero carbon emissions by mid-century (Black et al., Citation2021; Rogelj et al., Citation2021). However, the 6th assessment report of the Intergovernmental Panel on Climate Change (IPCC) highlights that the 1.5°C threshold will likely be surpassed already in the mid-2030s – even if immediate emission reduction measures were implemented globally (Canadell et al., Citation2021). At the current rate of greenhouse gas (GHG) emissions to the atmosphere, the remaining cumulative (RC) global carbon budgetFootnote1 to stay within an average global surface temperature increase of 1.5°C by 2100, will be consumed within the next decade, if not sooner (Lamboll et al., Citation2023). More specifically, the global RC carbon budget for a 50% likelihood to limit global warming to 1.5, 1.7 and 2°C has, respectively, reduced to 105 GtC, 200 GtC and 335 GtC from the beginning of 2023, equivalent to 9, 18 and 30 years from 2022 onwards and assuming 2022 emissions levels (Friedlingstein et al., Citation2022).

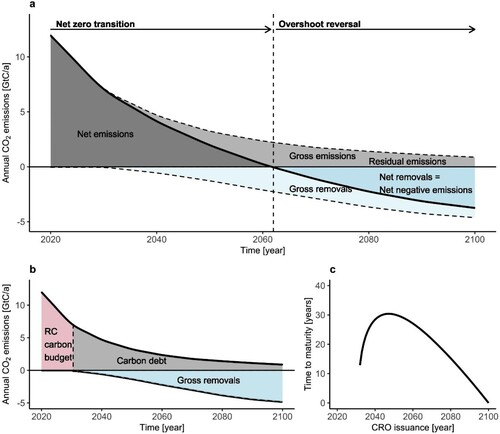

To limit warming to 1.5–2°C in the long run, most model-based assessments agree that carbon dioxide removal (CDR) from the atmosphere will be needed at large scale (Riahi et al., Citation2022). A variety of mechanisms have been proposed for this, including measures like afforestation and reforestation, and technological options such as bioenergy with carbon capture and storage (BECCS) and direct air carbon capture and storage (DACCS). Climate mitigation scenarios assessed by the IPCC foresee two different time horizons for such CDR deployment in the context of stringent climate goals: in the near to medium-term the role of CDR is to support emission reductions (ERs)Footnote2 for achieving net zero CO2 emissions by mid-century. In the long run, CDR needs to exceed residual emissions from sectors remaining hard to decarbonize (Luderer et al., Citation2018), in order to achieve net CO2 removals or net negative emissions (Gasser et al., Citation2015), as illustrated in a. Net CO2 removals reduce atmospheric carbon stocks and can induce a cooling of the planet, if other GHG emissions also decline sufficiently (Fuglestvedt et al., Citation2018). In that case, even 1.5°C can still be met by 2100 despite the temporary overshoot of the target.

Figure 1. Panel a: Elements characterizing a carbon emissions pathway. Net CO2 emissions (opaque grey area) equal gross emissions (all grey areas) minus gross removals (all blue areas). Net emissions coincide with gross emissions in the near future until carbon dioxide removal (CDR) is ramped up. When gross emissions equal gross removals, net zero CO2 emissions are achieved (vertical dashed line). Beyond net zero, gross removals exceed gross emissions, resulting in net negative emissions or net carbon removals (opaque blue area). Net emissions deplete the remaining cumulative (RC) carbon budget, whereas net removals replenish an overshot RC carbon budget. Gross emissions which remain hard-to-abate in the long-term are labelled residual emissions. ‘CDR’ is a general term which comprises gross removals and net negative emissions, or the underlying technologies and practices, depending on the context. Panel b: Elements characterizing the CRO framework. Carbon debt is generated by gross emissions once the RC carbon budget has been depleted, here around 2030. Carbon debt is compensated intertemporally by gross removals. Panel c: The repayment term structure shows the time to maturity in years as a function of the date of issuance for the profile in panel b. For an analytical definition see Bednar et al. (Citation2023).

Bednar et al. (Citation2021) address the long-term role of CDR based on a rationale of intergenerational fairness, proposing regulatory arrangements that introduce the carbon removal obligation (CRO). They argue that emitters causing the overshoot of the RC carbon budget need to remain liable for delivering the net carbon removals required to reverse the overshoot in the second half of the century. Furthermore, they contend that the price of temporary atmospheric carbon storage – comparable to temporary CO2 storage through afforestation – can be quantified and should rightfully be shouldered by emitters. In the absence of such an intertemporal mechanism that enforces the polluter pays principle (PPP), net removals would become a ‘public waste management task’, potentially imposing a huge fiscal burden on future generations on top of the growing climatic impacts (Bednar et al., Citation2019). On the other hand, fully decarbonizing the global economy before overshooting the 1.5°C warming target, would require radical measures (Grubler et al., Citation2018) which will likely not be achieved within this narrow time frame.

The CRO policy framework is appealing for a couple of reasons: first, it allows CDR-based climate change mitigation to be streamlined into the economy using the existing principle of interest-bearing financial debt. By taking this approach, emitters are not only legally obligated to ensure carbon removals, but are also mandated to make payments as long as their CO2 emissions persist in the atmosphere. In this way, the PPP is upheld and enforced (Stainforth, Citation2021). It is expected that this scheme can attract significant private capital as the basis for the robust functioning of a CDR market in the near-term. Second, CRO pricing ensures that near-term ERs and CDRs are not compromised by the possibility of net removals later in the century. In other words, it reduces the moral hazard that would likely lead to mitigation deterrence (Fankhauser & Hepburn, Citation2010) if contracting a CRO were for free. CRO pricing thus assures that – where possible – CDR is deployed in addition to, and not instead of, ERs.

This paper builds on, amends and extends the mechanisms conceptualized in Bednar et al. (Citation2021). Moreover, it provides a concrete roadmap for the implementation of the overall CRO policy framework, as proposed herein. We proceed as follows: In section 2 we revisit the scope of the principal CRO mechanism as envisaged by Bednar et al. (Citation2021). Moreover, we explain the CRO pricing instrument, for which a novel analytical model has been developed. In section 3 we begin to explore possible legal frameworks, instruments and mechanisms that might enable implementation of the CRO policy framework, so as to facilitate operationalization of a negative carbon economy. We set out conclusions in section 4.

2. The updated CRO

The CRO policy framework consists of two elements: the principal CRO mechanism and a CRO pricing instrument. The transition from the proposals in Bednar et al. (Citation2021) to that proposed in this paper with respect to these elements is demonstrated in section 2 in the Supplementary Information. Here we elaborate on the elements of the CRO policy framework, as now proposed.

2.1. Theoretical considerations

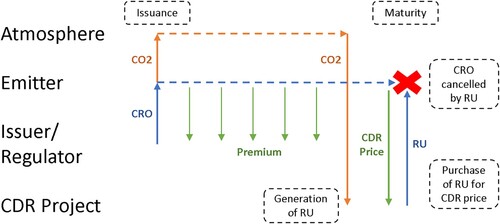

The principal CRO mechanism is executed by CRO issuing entities and dictates that for every tonne of CO2 emitted as ‘carbon debt’, a CRO is issued to the emitter. We classify emissions that exceed the RC carbon budget as this carbon debt,Footnote3 as in b. CROs in turn oblige emitters to remove an equivalent amount of CO2 upon the CRO's maturity (see ). Hence, CROs are issued at the time of emission and remain with emitters until CRO maturity. At maturity, emitters must possess removal units (Macinante & Singh Ghaleigh, Citation2022) for CRO cancellation, purchased on a CDR market or obtained via certified ‘in-house’ CDR operations. It is expected that removal units are traded competitively on a CDR market, ensuring CDR implementation at the lowest cost by capable entities at CRO maturity.

Figure 2. At the time of emission, an Issuer issues a CRO to the emitter, held until maturity. By maturity, emitters must own a removal unit (RU), generated by CDR projects and traded on a CDR market or directly generated by certified in-house operations of the emitter. The CRO is cancelled against an RU at maturity. Between issuance and maturity, emitters pay a Premium, serving to (1) reduce emitter-specific (idiosyncratic) risks, (2) guide the emissions and removals paths and (3) potentially allocate revenues towards mitigating future loss & damage or adaptation needs related to temporary atmospheric CO2 stocks. In the figure, dashed boxes indicate actions or events; green arrows denote financial flows; blue arrows represent the exchange of CROs and RUs; and orange arrows depict physical CO2 fluxes.

The CRO pricing instrument, on the other hand, encompasses the delineation and application of an apt CRO Premium, a two-stage process conducted by separate entities (elaborated in section 3). Initially, the regulator sets the CRO Base Premium (e.g. in EUR per tonne CO2) as a financial incentive to steer the emissions pathway. Subsequently, commercial CRO issuers impose emitter-specific Commercial Premiums atop this base and determine maturity profiles. Determination of these parameters aims to minimize idiosyncratic risks, as issuers remain liable for CDR deployment if CRO-holders default. Moreover, Premium payments financially compensate issuers for these risks taken. The maturity profiles and Commercial Premiums reflect the emitter's financial position: a stronger position may warrant longer maturities and potentially lower Premiums, while a weaker position might see shorter maturities and higher Premiums. This approach ensures that emitters have a clear basis for deciding whether to reduce emissions or secure CROs. The total Premium may manifest as a financial interest rate, termed originally a ‘carbon debt interest rate’ (Bednar et al., Citation2021), a periodic fee, or, at its simplest, a one-off payment by the emitter upon the CRO's issuance (illustrated in ). While c presents an idealized repayment term structure derived from a typical mitigation scenario, it is essential to understand that this aggregate pattern emerges from the combined individual maturity settings of all emitters. Due to variations in individual settings reflecting financial risk considerations, the real-world aggregate repayment trajectory might differ substantially from what current mitigation scenarios suggest.

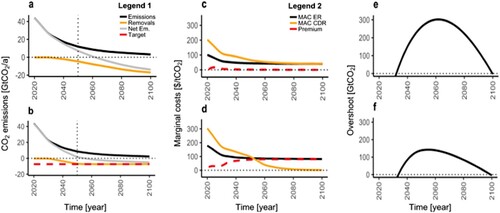

Figure 3. Climate mitigation scenarios based on a 1.5°C RC carbon budget (400GtCO2 from 2020 onwards). For the full range of scenarios see Bednar et al. (Citation2023). The left column (a, c, e) reflects a standard mitigation scenario, whereas the right column (b, d, f) illustrates a scenario where gross removals were capped at 2 GtC/a, similar to the scenario archetypes in Obersteiner et al. (Citation2018). Panels a & b: Emission profiles, including gross emissions (black), gross removals (orange) and net emissions/removals (grey). In panel b gross removals were capped at 2 GtC/a (red dashed line). Panels c & d: Present value marginal cost paths of emission reductions (ERs, black) and carbon dioxide removal (CDR, orange); as well as the present value CRO Base Premium (red dashed line). The CRO Base Premium is defined as the present value of marginal costs of ERs at issuance of the CRO minus the present value CDR price at maturity. Capping gross removals implies a larger CRO Premium in panel d than in panel c. Panels e & f: Cumulative CO2 emissions above the RC carbon budget. The upper bound for gross removals reduces the overshoot of the RC carbon budget and associated risks.

The principal CRO mechanism paired with the CRO pricing instrument defines the ERs’ marginal costs at CRO issuance and the CDR price upon the CRO's maturity: under idealized perfect foresight conditions within the CRO framework, emitters would reduce emissions until ERs’ marginal costs equate to CRO-associated marginal costs – the present value sum of future marginal removal costs and the CRO Premium. A Premium increase for a set maturity period would reduce CRO demand, resulting in fewer issued CROs and diminished removal demand at maturity, hence lowering the CDR price at maturity.Footnote4 Fewer CROs being issued implies more ERs in the near-term, and elevated ERs’ marginal costs.

The principal CRO mechanism presumes a CDR market's existence but not one for ERs. An ERs market could conceivably coexist with the CRO framework, given conditions delineated in Supplementary Information, section 2. Separation of the CDR market permits divergent marginal costs between CDR and ERs, attributed to factors like different technological learning rates (see c). This separation paves the way for individual target determination for ERs and CDR (see d), a potentially beneficial strategy for various reasons (McLaren et al., Citation2019), encompassing political factors (Geden et al., Citation2019; Geden & Schenuit, Citation2020). Target setting coupled with technological learning rate variations are elaborated upon in section 2.2 scenarios.

The principal CRO mechanism ensures that gross emissions and removals in total stay within the RC carbon budget, whereas CRO pricing plays a crucial role in determining how ERs and removals contribute over time to achieving this goal. The purpose of defining a Base Premium is thus to incentivize gross emission and removal pathways that are in line with a broader set of climate policy targets and/or risk considerations. Furthermore, revenues generated from Base Premium payments, conceptualized as compensation for temporary atmospheric CO2 storage, can be effectively allocated to mitigate loss and damage attributable to these additional temporary CO2 stocks, or to the resultant adaptation needs. This allocation contributes to the realization of intergenerational climate equity goals, aligning with suggestions posited in Bednar et al. (Citation2021).

In terms of steering emissions and removals paths, intermediate targets (Rogelj et al., Citation2019) such as achieving net zero CO2 emissions by 2050, could be induced by appropriately imposing a time dependent Base Premium. Similarly, the Base Premium can be utilized to discourage emitters from obtaining CROs that would result in exceeding a specified threshold for removals at a given CRO maturity, as depicted in b. In this manner, the Base Premium can serve as an incentive for a soft upper limit on removals. This might reduce the overshoot (f) and the associated risks, recognizing that it is still unclear whether from technological, environmental and economic perspectives CDR can be deployed at the required scale to reverse the overshoot (Fuss et al., Citation2018; Honegger & Reiner, Citation2018; Lawrence et al., Citation2018; Obersteiner et al., Citation2018). More sophisticated CRO pricing strategies could be targeted at internalizing the physical risks associated with an overshoot by quantifying the likelihood and impact of climatic feedbacks, such as the melting of ice sheets, permafrost thaw (Gasser et al., Citation2018), or other tipping points (Armstrong McKay et al., Citation2022). If such feedbacks lead to additional warming, for instance through CO2 outgassing from permafrost soils, they would put at risk the attainability of the temperature target even if cumulative emissions complied with the RC carbon budget – which the principal CRO mechanism aims to assure.

The analytical model introducing the CRO pricing mechanism is explained in a recent working paper (Bednar et al., Citation2023). One way of determining the CRO Base Premium is through modelling of the properties of the processes relevant for climate mitigation in the physical, technological and socio-economic environment, as well as the consideration of additional climate targets, such as net zero CO2 emissions by 2050. The CRO Base Premium is then derived ex-post from marginal abatement cost paths – a method which is fully compatible with the model-based practice adopted by many regulators and scientific communities to compute carbon prices, for which countless examples exist in the climate economic literature. On the basis that the assumptions underlying such numerical models are valid, the CRO Base Premium can be imposed to adjust price levels of ERs and CDR which then incentivize the preferred behaviour among emitters and the CDR industry. Realistically, an adaptive approach will be required to adjust the CRO Base Premium iteratively using model-based estimates backed by carbon market observational data, and considering other factors that determine a socially desirable mitigation pathway. The CRO Commercial Premium is determined by the issuing entities based on normal credit risk evaluations (Lando, Citation2004), which the analytical CRO model does not address.

2.2. CRO based climate mitigation scenarios

Bednar et al. (Citation2023) also set out a detailed scenario analysis based on a simple numerical model with technological change represented by ‘learning-by-doing’. Two of the scenarios are illustrated in , including a scenario where CDR is capped at 2 GtC/year (7.3 GtCO2/year) in panels b, d and f. Important conclusions for the integration of CDR into carbon policy schemes can be drawn from the scenario analysis: First, the initially high costs of CDR options like BECCS and DACCS compared to ERs is one of the frequent arguments used against CDR integration into ETSs. An ETS would require additional financial resources to cover that price gap between ERs and CDR, or else fail to stimulate innovation and early uptake of CDR (Burke & Gambhir, Citation2022; Rickels et al., Citation2021). A similar situation applies for the scenarios in , where the price of CDR exceeds that of ERs. However, according to the principal CRO mechanism, ERs at CRO issuance always compete with CDR at maturity.Footnote5 This time lag increases the competitiveness of CDR and even allows for charging a positive CRO Base Premium in almost all of the examined pathways in Bednar et al. (Citation2023), instead of the need for additional funding an ETS would have to supply. Second, allowing the price levels to diverge is not only the prerequisite for separate target setting for ERs and CDR, as in b. It also leads to a more cost-effective pathway than is achievable under a policy scheme requiring a single price. Even in the absence of additional constraints for emissions and/or removals as in a, price levels diverge due to endogenous technological change. A generalization towards sectoral CRO pricing, which considers the different learning rates and inertias in CDR portfolios, the emitting sectors as well as their abatement options, would likely further improve flexibility and cost effectiveness.

3. Legal frameworks, instruments and mechanisms for implementation

While recognizing that other approaches may be possible, this section aims to illustrate relatively straightforward legislative actions to provide for implementation of the CRO policy framework envisaged in the preceding section. In the proposed implementation scenario, central banks as regulators and commercial banks as CRO issuing entities have roles to play in the allocation/distribution of CROs to emitter entities, via mechanisms similar to those dealing with private financial borrowing and debt.

3.1. Initial discussion

Carbon debt is treated as financial debt in the balance sheets of emitters, represented by CROs. For example, each tonne of CO2 emissions equals one CRO. Like financial debt, CROs accrue interest, referenced herein as the CRO Premium. The CRO Base Premium is determined by the central bank. The CRO Commercial Premium is determined by the commercial CRO issuer bank for their customer-emitter entities based on normal credit risk evaluations, terms and conditions including collateral. CRO Premium payments might be hypothecated in part to a fund for specific future purposes,Footnote6 just as a sovereign fund might be. CROs are discharged by the CRO holder acquiring and surrendering/retiring removal units generated by a CDR project.

Elements for implementation of the proposed CRO policy framework thus include:

a legal obligation for prescribed legal entities to report their emissions;

the date when the RC carbon budget is defined to be expended (or a process to determine a temporally distributed instantaneous (TDI) carbon budget, as explained in the Supplementary Information);

emissions overshooting the RC or TDI carbon budget being defined in law as carbon debt that must be included by prescribed legal entities in their financial accounts (e.g. in the balance sheet);

carbon debt being subject to a financial CRO Premium – both for the commercial banks and the banks’ emitter-customers that are prescribed legal entities;

carbon debt being extinguished by prescribed legal entities acquiring and retiring removal units;

removal units being generated and issued by CDR projects;

provision for funds generated by CRO Base Premium payments on the commercial banks’ accounts with the central bank – and perhaps also a portion of the CRO Commercial Premium payments by the emitter entities to their issuer commercial banks – to be hypothecated against future climate change management risks; and

carbon debt not being able to be written off, but rather needing to be paid off. Thus, in the case of an insolvent emitter, any outstanding carbon debt will need to be paid off by the CRO issuing entity (i.e. commercial bank that issued it).

By treating carbon debt the same as any other business debt, the CROs on the emitter's balance sheet would need to be taken into account when considering the emitter's solvency. This underscores the need for an established marketplace for removal units to be functioning robustly, well before CROs become applicable, so that liability can be ascertained and budgeted for by emitters. There would also be other relevant regulatory provisions to be taken into account, for instance, such as the rules against insolvent trading.

Moreover, the CRO policy framework, as proposed in Bednar et al. (Citation2021), holds that ‘ … To assure its physical conservation and exert control over its aggregate level, carbon debt would initially be issued at the base rate by managing authorities – for example, Central Banks – to which commercial banks would be held liable in case of insolvent debtors’. This gives rise to two points.

First, central banks (for example, the Bank of England), control money supply and can create ‘base money’ through open market operations (e.g. buying or selling government bonds). However, for the most part, commercial banks take deposits and use these deposits to lend to borrowers (subject to central bank requirements to maintain a fractional reserve to cover depositor repayments): this increases the money supply beyond the base money issued by the central bank (see Bateman & Allen, Citation2022; McLeay et al., Citation2014). It is proposed to adapt these concepts and approach to the issuance of CROs. Thus, we propose commercial banks will issue CROs to reflect the level of a customer's emissions; they will apply their normal credit risk evaluation to set the rate of interest they charge; they will need also to maintain a reserve with the central bank to cover – not repayments – but the risk that their customer does not honour the CRO, as in such a case, that obligation falls to the commercial bank as issuer.

Second, a question arises whether the role envisaged for central banks would come within their respective mandates. In this respect, analysis shows ‘significant differences in central bank mandates’ Dikau and Volz (Citation2021), highlighting also that ‘central banking activities depend in practice not only on the formal mandate, but also its interpretation, which can be ambiguous’.Footnote7 Dikau and Volz found there is ‘a particularly strong case for central banks to respond to climate change risks as part of core macro-financial stability mandates’, however, going beyond this to use its powers to actively ‘green’ the financial system and economy, would depend on a central bank's legal mandate. They conclude that, rather than a central bank intervening to address market externalities, the preferred solution would be removing that market failure, for example, by a carbon pricing mechanism that internalizes the social cost of carbon emissions.Footnote8 These authors note that the Bank of England (BoE) under Mark Carney had accusations of ‘mission creep’ levelled against it in relation to its stance on climate risks, notwithstanding the terms in which the objectives for the BoE's Monetary Policy Committee were set out (i.e. to support the government's economic policy and objectives for growth) and Carney's support for carbon pricing Dikau and Volz (Citation2021). Thus, such concerns could be addressed through government policy and legislation, by providing for internalization of the social cost of carbon through carbon debt/CROs. Giving effect to such a government policy, the BoE (or other central bank) would not be straying far from traditional core roles of safeguarding financial stability and supporting wider economic objectives.Footnote9

A further initial observation is that, in terms of climate policy developments and, in particular, emissions mitigation policy development, the suggestions in this paper could integrate with a carbon border adjustment mechanism (CBAM) just as readily as an ETS could do. Determining the emissions, resulting from production of the relevant imported goods would be the same, irrespective of whether the mechanism to attach a price to those emissions (that is, the carbon border adjustment) was done through an ETS or by issuing CROs.

3.2. CRO framework functioning

The CRO policy framework introduces a demand side (carbon debt/CROs) and a supply side (removal units), thus intimating the formation of a market (‘CDR market’).

3.2.1. Demand side

Under the CRO policy framework, obligations to accurately measure emissions from economic activities above a minimum threshold would need to be mandatory across all sectors of the economy or, at least, all those sectors whose emissions are considered significant enough to generate carbon debt and as a result, be included in the legal framework. These measurement and reporting obligations imply a role for a registry, or alternatively, the obligations could be integrated into an expanded corporate financial reporting regime.Footnote10 The service providers and other existing infrastructure for measuring, reporting and auditing CO2 emissions would need to be scaled up to ensure capacity for a significantly expanded role. Apart from reporting standards, accreditation of reporting and verification services providers would improve outcomes.

Recognizing that a parallel operation of conventional carbon pricing and the CRO framework would be possible during a transition phase, as discussed in section 2 in the Supplementary Information, here we follow the approach that once the RC carbon budget for Paris Agreement alignment is exhausted, then:

emissions = carbon debt;

one metric tonne CO2/CO2e emissions = one CRO.

By defining carbon debt as a financial debt, corporate and financial market regulators also would have roles in addition to central and commercial banks and these are roles they are assuming already (IFRS, Citation2023). In relation to a mechanism for CRO allocation, accounting, auditing and related management, commercial banks would set up CRO accounts for their emitter-customers (based on the last annual reported emissions) just as they might normally set up deposit accounts for those emitter-customers if they were borrowing money.

The central bank would require each commercial bank to hold a ‘reserve’ account facility with it on which it would charge a CRO Base Premium (interest at a base rate). The mechanism through which the CRO Base Premium, or ‘cost’ of the carbon debt, is charged to commercial banks, would be determined by the central bank. By way of illustration, for instance, a commercial bank's CRO reserve account facility with the central bank might be charged Base Premium interest to reflect the amount of CROs issued by that commercial bank to its emitter-customers. Thus, it would reflect pricing of the risk to the central bank of the commercial bank failing to acquire the equivalent amount of removal units that would be required to discharge the issued CROs. For example, calculation of the CRO Base Premium – in addition to the modelling aspects discussed in section 2.1 – might be based on the spot contract for removal units, or even a forward contract (e.g. 3-month futures contract) with daily reconciliation.

For their customer-emitter entities, the CRO Commercial Premium would be determined by the CRO issuer bank, based on normal credit risk evaluations. A possible mechanism for issuing CROs is shown diagrammatically in Figure S2 in the Supplementary Information.

Emitters with CROs on their balance sheet for which they must pay a CRO Premium would need, in accordance with their obligations to repay the carbon debt, to acquire units generated by projects that remove CO2 from the atmosphere.Footnote11 Thus, the need to repay carbon debt, in accordance with the conditions of the CROs on the emitter entity's balance sheet, will drive demand for removal units and hence, funding for development of CDR projects to generate the removal units. Recognizing the demand, it is anticipated that banks and other financiers will fund CDR projects that generate removal units for purchase by holders of CROs.

3.2.2. Supply side

Minimum technical, assurance, governance and management requirements would be introduced by a standard for CDR projects, with the aim not only to ensure integrity and quality of outcomes, but also to foster a role for a class of professional managers, who would be tasked to ensure CDR projects continued to satisfy those requirements.Footnote12 The requirements would address technical characteristics such as delivery risk and quality/integrity risk (e.g. permanence; saturation risk; timing of removals; leakage risk; long-term management requirements; co-benefits; as well as a number of other characteristics).Footnote13

In addition to legal governance of CDR delivery and quality/integrity risk, requirements might also include the standard of project management to be maintained; and accounting and cost coverage requirements (see Table S4, Supplementary Information). These elements could generate disclosure and transparency requirements, with the entities managing the projects obliged to provide information on project performance and risk issues, project structure and response mechanisms for any risks, thus further encouraging development of the professional standard of management.

Standard-based removal units would facilitate a smoother running, more efficient physical market for purchasers by reducing transaction costs for emitter entities needing to satisfy and remove CROs from their balance sheet. The removal units could be transacted more readily using a Master Agreement with transaction specific matters (parties, volume, price) dealt with in a term sheet, thereby reducing the legal complexity and transaction costs.Footnote14 A more efficiently operating market might be expected to encourage greater participation, facilitating more competitive cost reductions and a more rapid scaling up of the CDR project sector.

CDR projects generate removal units, minimum requirements for which could be prescribed by regulation (applying the national, or an international standard: see the Supplementary Information). The removal units, notwithstanding meeting the commitments set out in the standard and regulation, would nevertheless demonstrate different characteristics, depending on the method applied by the project (e.g. delivery risk based on permanence, and saturation risk; tonnage removal units per annum; scheduling of delivery). Importantly, elements such as co-benefits (including features that may not avail themselves to being priced directly, but nevertheless add to the value of the project and removal units generated by it, e.g. environmental improvement, biodiversity enhancement) would be taken into account. Thus, not only would different methods generate removal units with price differences in the market, but any co-benefits would also give projects differing profiles and so be factored into the removal unit pricing according to the preferences of the various market actors.

3.3. Interaction of public and private sector actors

It will be critical that an established marketplace is functioning robustly well before CROs are required to be included in emitting entities’ financial accounts. For this to occur, there needs to be significant scaling up of CDR projects; and an initial learning-by-doing period of CDR market operation. These two aspects are complementary and could be part of the transitional measures governments put in place to foster development of the CDR market. Putting in place the necessary legal instruments that give rise to binding financial commitments would be an integral initial part of this process.

Thus, the primary initiative to implement the CRO policy framework will need to come from government. All the same, the process of implementation could generate significant engagement with the private sector, in particular with private finance facilitating rapid scaling up of the CDR sector, as well as generating substantial revenue for hedging future risk (through CRO Premium payments on carbon debt being set aside for that purpose).Footnote15

In relation to the finance sector, for example, if commercial banks have the role envisaged by the Proposals, by ‘extending CRO credit’ to their emitter-customers, a new financial market would be created, including potential for subsequent securitization of portfolios of CROs to free up capital.Footnote16 Similarly, to the extent that the banks and lenders extend debt finance to the project owners/developers, another financial market would be generated, again including potential for the initial lenders to securitize loan portfolios to free up capital.

The opportunities for these secondary markets suggest potential private sector interest. Equally, developments such as these could promote greater transparency, since performance reporting, delivery, quality/integrity and other matters would need to be defined in commercial documents (for example, prospectuses, regulated by corporate law) in relation to any secondary markets, providing an additional layer of governance screening. Development of a class of management professionals could encourage growth and governance in the CDR sector.

The public sector and private sector roles, and how they might interact, are illustrated in Table S2, in the Supplementary Information.

3.4. Legal implementation of the CRO policy framework

Clearly, implementation of the CRO policy framework needs to be initiated by government. While other sectors, particularly the private financial sector, will have important roles, as a first step, adoption of policies and legislative action are needed to set the course for and incentivize such fundamental changes.

All the same, as outlined here, the legislative actions required could be relatively straightforward. Subject to resolution of some preliminary elements, the legal framework envisaged could be implemented by a package of three instruments:

an enactment of primary legislation;

development of a national (or international) standard; and

secondary legislation (a regulation) to adopt the standard and implement the primary legislation.

For these purposes, it is herein contemplated that the jurisdiction where the framework is being implemented is the United Kingdom. All the same, the three instruments could be adapted to fit the lawmaking arrangements of other jurisdictions. Details of the three instruments for implementation of the legal framework envisaged by the CRO policy framework are illustrated in text and related Tables S3, S4 and S5, in the Supplementary Information.

The preliminary elements to be resolved would be first, the specific temperature increase target: e.g. 1.5, 1.7, 2.0°C or another; second, the global RC carbon budget to stay within that target given a specific likelihood; third, when the global RC carbon budget will be expended, based on the rate of emissions; and consequently, agreement on the date when emissions = carbon debt (or on TDI carbon budget and parallel operation of the CRO framework, as discussed in section 2 in the Supplementary Information).

Notwithstanding the usual free rider and leakage problems, while there is no reason why an individual government could not make a determination of these elements for its own policy purposes, it would clearly be better for there to be regional or, ideally, multilateral or broad international determinations on a consistent basis. All the same, apart from the first, which involves a specific choice (although, to some extent, already resolved by commitments of governments to align with the Paris Agreement target), these elements would resolve themselves with the passage of time.

4. Discussion and conclusion

The CRO policy framework sets out mechanisms by which substantially more ambitious near-term decarbonization complemented by earlier deployment of CO2 removal technologies might be achieved. This mechanism is innovative not only in its intention to place the climate change mitigation pricing levers in the hands of the traditional managers of financial and price stability, namely central banks; more so, it is innovative for the corollary of integrating climate change mitigation response management far more into the economic mainstream, treating carbon debt as financial debt, hence accounting for the externality of carbon emissions as part of core economic and financial management. In so doing, it begins to address a fundamental challenge of climate change policy, namely the question of intergenerational equity, by the application of the PPP. The legal basis of the PPP will be further extended as climate targets become legally binding in many countries (Black et al., Citation2021). In line with this principle, the implementation of the CRO policy framework requires relatively straight-forward legislative measures to adjust existing legal structures.

The proposed CRO policy framework implies that conventional carbon pricing through ETSs or carbon taxes will become obsolete in the near-term as the RC carbon budget becomes depleted. Rather than seeking to integrate CDR into ETSs (Rickels et al., Citation2020; UK Government, Citation2022), which is associated with several technical difficulties (Burke & Gambhir, Citation2022), policymakers should strive for intertemporal mechanisms such as the CRO framework. The implied potential for separate price levels for CDR and ERs might entail efficiency gains if endogenous technological change is considered.

We have illustrated that CRO pricing fully builds on existing modelling practices, which need to be further improved to get a better understanding of joint Earth system, socio-economic and technological risks. Details remain to be further elaborated and teased out, including additional attribution mechanisms for overshoot risks, as well as the integration of non-CO2 GHGs. Moreover, the degree of public involvement in a framework that builds on markets and privately held removal obligations needs to be further investigated.

In this article, Section 3 adds substance by offering the outline of one possible pathway for implementation. The proposed CRO policy framework sets out a demand side (carbon debt) and a supply side (CO2 removal units), thus intimating the creation of a CDR market. In so doing, it points to a way in which the CDR sector can be scaled up to the degree necessary if the limits on global warming targeted by Paris Agreement Parties are to be achieved. The primary initiative must come from government putting in place policies and legal instruments to generate confidence that a robust CDR market is in place before carbon debt and removal obligations take effect. While inter-jurisdictional collaboration and consistency (for instance, in the case of the Standard, being under the aegis of the International Organization for Standardization) always holds out the possibility for better outcomes, the framework, instruments and mechanisms outlined here could be applied initially on a jurisdiction-by-jurisdiction basis, without detriment to the potential for development of a global CDR market in the longer term.

We conclude that the CRO policy framework characterizes feasible and necessary mechanisms to respond to the increasing evidence and warnings, in particular from the IPCC, of the need to drawdown CO2 emissions and scale up removals, if average global surface temperature is to be stabilized within the targets envisaged by the Paris Agreement.

Supplemental Material

Download MS Word (277.8 KB)Disclosure statement

No potential conflict of interest was reported by the author(s).

Correction Statement

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes

1 The remaining cumulative (RC) carbon budget represents the cumulative net emissions quantity until 2100 compatible with a specific warming threshold, such as 1.5°C.

2 Emission reductions compared to a baseline scenario might include carbon capture and storage (CCS) but do not include any atmospheric carbon removals.

3 In this manuscript, we equate gross emissions to carbon debt, essentially positing an RC carbon budget of zero. Thus, we consider the CRO framework's initiation to align with the RC carbon budget's exhaustion (refer to b). Nonetheless, there exist compelling arguments for initializing the CRO framework before this depletion, as detailed in the Supplementary Information.

4 Compare the two scenarios in for an illustration of that effect.

5 This is in some ways similar to the mechanism described in Rickels et al. (Citation2021).

6 For instance, the funds might be targeted at reducing future climate change risks, as hypothesized in Bednar et al. (Citation2021); or for addressing welfare distributional issues associated with carbon pricing.

7 Dikau and Volz (Citation2021), section 2. The authors made detailed analysis of 135 central bank mandates and compared them to arrangements and responsibilities adopted by the central banks in practice.

8 The Proposal and the framework for implementation in this paper advocate this via introduction of carbon debt and the CDR market.

9 While reference is to the Bank of England, the principle could be extrapolated to other central banks and their mandates. Additionally, there is scope for broader consensus through bodies such as the Financial Stability Board (FSB), Bank for International Settlements (BIS), and the Network for Greening the Financial System (NGFS).

10 There are increasing public policy developments in this respect taking place already, for instance: (1) the International Sustainability Standards Board (ISSB), established at COP26 to develop a comprehensive global baseline of sustainability disclosures for the capital markets, launched a consultation on its first two proposed standards. One sets out general sustainability-related disclosure requirements (Exposure Draft IFRS S1) and the other specifies climate-related disclosure requirements (Exposure Draft IFRS S2), see IFRS (Citation2023); (2) The U.S. Securities and Exchange Commission announced proposed rules to require disclosures about a company's governance, risk management, and strategy with respect to climate-related risks. Moreover, the proposal would require disclosure of any targets or commitments made by a company, as well as its plan to achieve those targets and its transition plan, if it has them (US SEC, Citation2023).

11 For simplicity, referred to here as CDR projects generating removal units.

12 In terms of the length of this project management commitment, there is a clear parallel with the role performed by pension fund managers.

13 The aim would be that each project would generate removal units equal to or better than a minimum regulatory requirement, which would be based on a national standard or, ideally, an international standard for such.

14 Similar approach to that of the International Swaps and Derivatives Association (ISDA) Master Agreement.

15 There are parallels in the financing of nuclear waste management, for example see: World Nuclear Association, National Policies and Funding (WNA, Citation2023); and OECD Nuclear Energy Agency(NEA, Citation2021); and also the building of sovereign wealth funds. On the other hand, historic failures in many jurisdictions to provide for mine site rehabilitation provide examples of cost legacies left for future generations of taxpayers.

16 As a matter of policy, governments may be reluctant to have commercial banks move the responsibility for the CROs held by their customers off the bank balance sheets by securitizing, unless certain elements of obligation remain with the bank or are adequately provided for through parallel mechanisms.

References

- Bateman, W., & Allen, J. (2022). The Law of Central Bank reserve creation. The Modern Law Review, 85(2), 401–434. https://doi.org/10.1111/1468-2230.12688

- Bednar, J., Baklanov, A., & Macinante, J. (2023, January). The carbon removal obligation: Updated analytical model and scenario analysis. IIASA Working Paper WP-23-001. https://pure.iiasa.ac.at/id/eprint/18572/

- Bednar, J., Obersteiner, M., Baklanov, A., Thomson, M., Wagner, F., Geden, O., Allen, M., & Hall, J. W. (2021). Operationalizing the net-negative carbon economy. Nature, 596(7872), 377–383. https://doi.org/10.1038/s41586-021-03723-9

- Bednar, J., Obersteiner, M., & Wagner, F. (2019). On the financial viability of negative emissions. Nature Communications, 10(1), https://doi.org/10.1038/s41467-019-09782-x

- Black, R., Cullen, K., Fay, B., Hale, T., Lang, J., Mahmood, S., & Smith, S. (2021). Taking stock: A global assessment of net zero targets. Energy & Climate Intelligence Unit and Oxford Net Zero. https://eciu. net/analysis/reports/2021/taking-stock-assessment-net-zero-targets

- Burke, J., & Gambhir, A. (2022, December). Policy incentives for greenhouse gas removal techniques: The risks of premature inclusion in carbon markets and the need for a multi-pronged policy framework. Energy and Climate Change, 3, 100074. https://doi.org/10.1016/j.egycc.2022.100074

- Canadell, J. G., Monteiro, P. M. S., Costa, M. H., Cotrim da Cunha, L., Cox, P. M., Eliseev, A. V., Henson, S., Ishii, M., Jaccard, S., Koven, C., Lohila, A., Patra, P.K., Piao, S., Rogelj, J., Syampungani, S., Zaehle, S., & Zickfeld, K. (2021). Global carbon and other biogeochemical cycles and feedbacks. In V. Masson-Delmotte, P. Zhai, A. Pirani, S. L. Connors, C. Péan, S. Berger, N. Caud, Y. Chen, L. Goldfarb, M. I. Gomis, M. Huang, K. Leitzell, E. Lonnoy, J. B. R. Matthews, T. K. Maycock, T. Waterfield, O. Yelekçi, R. Yu, & B. Zhou (Eds.), Climate change 2021: The physical science basis. Contribution of working group I to the sixth assessment report of the intergovernmental panel on climate change (Ch. 5, pp. 673–816). Cambridge University Press. https://doi.org/10.1017/9781009157896.007

- Dikau, S., & Volz, U. (2021, June). Central bank mandates, sustainability objectives and the promotion of green finance. Ecological Economics, 184, 107022. https://doi.org/10.1016/j.ecolecon.2021.107022

- Fankhauser, S., & Hepburn, C. (2010). Designing carbon markets. Part I: Carbon markets in time. Energy Policy, 38(8), 4363–4370. https://doi.org/10.1016/j.enpol.2010.03.064

- Friedlingstein, P., O’Sullivan, M., Jones, M. W., Andrew, R. M., Gregor, L., Hauck, J., Le Quéré, C., Luijkx, I. T., Olsen, A., Peters, G. P., Peters, W., Pongratz, J., Schwingshackl, C., Sitch, S., Canadell, J. G., Ciais, P., Jackson, R. B., Alin, S. R., Alkama, R., et al. (2022). Global carbon budget 2022. Earth System Science Data, 14(11), 4811–4900. https://doi.org/10.5194/essd-14-4811-2022

- Fuglestvedt, J., Rogelj, J., Millar, R. J., Allen, M., Boucher, O., Cain, M., Forster, P. M., Kriegler, E., & Shindell, D. (2018). Implications of possible interpretations of ‘greenhouse gas balance’ in the Paris agreement. Philosophical Transactions of the Royal Society A: Mathematical, Physical and Engineering Sciences, 376(2119), 20160445. https://doi.org/10.1098/rsta.2016.0445

- Fuss, S., Lamb, W. F., Callaghan, M. W., Hilaire, J., Creutzig, F., Amann, T., Beringer, T., de Oliveira Garcia, W., Hartmann, J., Khanna, T., Luderer, G., Nemet, G. F, Rogelj, J., Smith, P., Vicente, J. L. V., Wilcox, J., del Mar Zamora Dominguez, M., & Minx, J. C. (2018). Negative emissions—part 2: Costs, potentials and side effects. Environmental Research Letters, 13(6), 063002. https://doi.org/10.1088/1748-9326/aabf9f

- Gasser, T., Guivarch, C., Tachiiri, K., Jones, C. D., & Ciais, P. (2015). Negative emissions physically needed to keep global warming below 2°C. Nature Communications, 6(1), 7958. https://doi.org/10.1038/ncomms8958

- Gasser, T., Kechiar, M., Ciais, P., Burke, E. J., Kleinen, T., Zhu, D., Huang, Y., Ekici, A., & Obersteiner, M. (2018, September). Path-dependent reductions in CO2 emission budgets caused by permafrost carbon release. Nature Geoscience, 11(11), 830–835. https://doi.org/10.1038/s41561-018-0227-0

- Geden, O., Peters, G. P., & Scott, V. (2019). Targeting carbon dioxide removal in the European union. Climate Policy, 19(4), 487–494. https://doi.org/10.1080/14693062.2018.1536600

- Geden, O., & Schenuit, F. (2020). Unconventional mitigation: Carbon dioxide removal as a new approach in EU climate policy. SWP Research Paper 2020/RP08. German Institute for International and Security Affairs. https://www.swp-berlin.org/10.184492020RP08/

- Grubler, A., Wilson, C., Bento, N., Boza-Kiss, B., Krey, V., McCollum, D. L., Rao, N. D., Riahi, K., Rogelj, J., De Stercke, S., Cullen, J., Frank, S., Fricko, O., Guo, F., Gidden, M., Havlík, P., Huppmann, D., Kiesewetter, G., Rafaj, P., et al. (2018). A low energy demand scenario for meeting the 1.5°C target and sustainable development goals without negative emission technologies. Nature Energy, 3(6), 515–527. https://doi.org/10.1038/s41560-018-0172-6

- Honegger, M., & Reiner, D. (2018). The political economy of negative emissions technologies: Consequences for international policy design. Climate Policy, 18(3), 306–321. https://doi.org/10.1080/14693062.2017.1413322

- IFRS. (2023). IFRS - ISSB delivers proposals that create comprehensive global baseline of sustainability disclosures. https://www.ifrs.org/news-and-events/news/2022/03/issb-delivers-proposals-that-create-comprehensive-global-baseline-of-sustainability-disclosures/

- Lamboll, R. D., Nicholls, Z. R. J., Smith, C. J., Kikstra, J. S., Byers, E., & Rogelj, J. (2023). Assessing the size and uncertainty of remaining carbon budgets. Nature Climate Change. https://doi.org/10.1038/s41558-023-01848-5

- Lando, D. (2004). Credit risk modeling: Theory and applications. Princeton series in finance. Princeton University Press.

- Lawrence, M. G., Schäfer, S., Muri, H., Scott, V., Oschlies, A., Vaughan, N. E., Boucher, O., Schmidt, H., Haywood, J., & Scheffran, J. (2018). Evaluating climate geoengineering proposals in the context of the Paris agreement temperature goals. Nature Communications, 9(1). https://doi.org/10.1038/s41467-018-05938-3

- Luderer, G., Vrontisi, Z., Bertram, C., Edelenbosch, O. Y., Pietzcker, R. C., Rogelj, J., De Boer, H. S., Drouet, L., Emmerling, J., Fricko, O., Fujimori, S., Havlík, P., Iyer, G., Keramidas, K., Kitous, A., Pehl, M., Krey, V., Riahi, K., Saveyn, B., et al. (2018). Residual fossil CO2 emissions in 1.5–2 °C pathways. Nature Climate Change, 8(7), 626–633. https://doi.org/10.1038/s41558-018-0198-6

- Macinante, J., & Singh Ghaleigh, N. (2022). Regulating removals: Bundling to achieve fungibility in GGR removal units. Carbon & Climate Law Review, 16(1), 3–17. https://doi.org/10.21552/cclr/2022/1/4

- McKay, A., David, I., Staal, A., Abrams, J. F., Winkelmann, R., Sakschewski, B., Loriani, S., Fetzer, I., Cornell, S. E., Rockström, J., & Lenton, T. M. (2022). Exceeding 1.5°C global warming could trigger multiple climate tipping points. Science, 377(6611), eabn7950. https://doi.org/10.1126/science.abn7950

- McLaren, D. P., Tyfield, D. P., Willis, R., Szerszynski, B., & Markusson, N. O. (2019, August). Beyond ‘Net-zero’: A case for separate targets for emissions reduction and negative emissions. Frontiers in Climate, 1, 4. https://doi.org/10.3389/fclim.2019.00004

- McLeay, M., Radia, A., & Thomas, R. (2014). Money creation in the modern economy. Bank of England Quarterly Bulletin, 54(1), 14–27. https://www.bankofengland.co.uk/-/media/boe/files/quarterly-bulletin/2014/money-creation-in-the-modern-economy.pdf?la = en&hash = 9A8788FD44A62D8BB927123544205CE476E01654

- NEA. 2021. Ensuring the adequacy of funding for decommissioning and radioactive waste management (Vol. 7549). OECD Publishing.

- Obersteiner, M., Bednar, J., Wagner, F., Gasser, T., Ciais, P., Forsell, N., Frank, S., Havlik, P., Valin, H., Janssens, I. A., Peñuelas, J., & Schmidt-Traub, G. (2018). How to spend a dwindling greenhouse Gas budget. Nature Climate Change, 8(1), 7–10. https://doi.org/10.1038/s41558-017-0045-1

- Riahi, K., Schaeffer, R., Arango, J., Calvin, K., Guivarch, C., Hasegawa, T., Jiang, K., Kriegler, E., Matthews, R., Peters, G. P., Rao, A., Robertson, S., Sebbit, A. M., Steinberger, J., Tavoni, M., & van Vuuren, D. P. (2022). Mitigation pathways compatible with long-term goals. In P. R. Shukla, J. Skea, R. Slade, A. Al Khourdajie, R. van Diemen, D. McCollum, & M. Pathak, S. Some, P. Vyas, R. Fradera, M. Belkacemi, A. Hasija, G. Lisboa, S. Luz, & J. Malley (Eds.), IPCC, 2022: Climate change 2022: Mitigation of climate change. Contribution of working group III to the sixth assessment report of the intergovernmental panel on climate change. Cambridge University Press. https://doi.org/10.1017/9781009157926.005

- Rickels, W., Proelß, A., Geden, O., Burhenne, J., & Fridahl, M. (2020). The future of (negative) emissions trading in the European Union. Kiel Working Paper. Kiel Institute for the World Economy.

- Rickels, W., Proelß, A., Geden, O., Burhenne, J., & Fridahl, M. (2021). Integrating carbon dioxide removal into European emissions trading. Frontiers in Climate, 3, 62. https://doi.org/10.3389/fclim.2021.690023

- Rogelj, J., Geden, O., Cowie, A., & Reisinger, A. (2021). Three ways to improve net-zero emissions targets. Nature, 591(7850), 365–368. https://doi.org/10.1038/d41586-021-00662-3

- Rogelj, J., Huppmann, D., Krey, V., Riahi, K., Clarke, L., Gidden, M., Nicholls, Z., & Meinshausen, M. (2019). A new scenario logic for the Paris agreement long-term temperature goal. Nature, 573(7774), 357–363. https://doi.org/10.1038/s41586-019-1541-4

- Stainforth, D. A. (2021). ‘Polluter pays’ policy could speed up emission reductions and removal of atmospheric CO2. Nature, 596(7872), 346–347. https://doi.org/10.1038/d41586-021-02192-4

- UK Government. (2022). Developing the UK Emissions Trading Scheme (UK ETS). GOV.UK. 2022. https://www.gov.uk/government/consultations/developing-the-uk-emissions-trading-scheme-uk-ets

- US SEC. (2023). SEC.Gov | statement on proposed mandatory climate risk disclosures. https://www.sec.gov/news/statement/gensler-climate-disclosure-20220321

- WNA. (2023). National policies: Radioactive Waste Management - Appendix 3 - World Nuclear Association. https://www.world-nuclear.org/information-library/nuclear-fuel-cycle/nuclear-wastes/appendices/radioactive-waste-management-appendix-2-national-p.aspx#:~:text = The%20nuclear%20utilities%20make%20payments,company%2C%20and%20also%20cover%20decommissioning