ABSTRACT

The thesis of this paper is that the role of debt and its relationship with equity in the firm, due to recent significant developments in the corporate finance markets after the global financial crisis of 2007-2008, has been transformed. The relatively new, but already very experienced private credit funds, are competing with banks in a dynamic market which is full of unforeseen and large-scale risks. The paper examines private credit funds and compares their business model to bank financing from a corporate governance perspective. The paper shows that modern debt providers (i) are interested in the firm's profit maximisation, (ii) are dynamically involved in the governance of the firm also outside financial distress, and that (iii) corporate loan financing agreements are often expected to be renegotiated (repriced). The paper argues that outside financial distress, debt and equity have become even more overlapping and intertwined than they used to be.

1. A renaissance in corporate finance

Over the past 25 years the corporate finance landscape and, especially the corporate debt finance environment, has changed significantly.Footnote1 The rise in innovative trends and techniques in corporate finance enhanced the essential role of debt in the firm.Footnote2 Fuelled by the post-GFC banking regulation,Footnote3 there has been an increased competition among the traditional finance providers, such as banks, and the non-traditional finance providers,Footnote4 in particular, private credit funds.Footnote5 This competition has been one of the main factors shaping the global debt financing markets in the past years.Footnote6 More recently, the competition has become more intense, as sophisticated institutional investors (e.g. sovereign wealth funds) started to compete with banks and private credit funds by directly providing financing to companies.Footnote7

With the development of the primary and secondary markets for corporate loans, debtholders found innovative ways to minimise their risk exposure. Innovative legal tools to diversify risk, and to price it adequately and on a dynamic basis incentivise debtholders to think of alternative strategies and financing options for engaging with their borrowers. The growing interconnectedness of financial risks also influenced the development of debt markets and the incentives of debtholders.Footnote8 The changes driven by the urgent need for sustainable finance further enhanced the essential role of debt in the firm’s life cycle.Footnote9 Other factors, influencing and reshaping the role of debt in the firm, include the advancement of digital lending and FinTech lending,Footnote10 as well as the blurring lines between private and public capital markets.Footnote11

Lately, inflation has caused a surge in the interest rates worldwide.Footnote12 Higher interest rates result in a lower demand in risky leveraged loans, which might negatively affect firms’ refinancing chances.Footnote13 On top of that, the global corporate indebtedness reached unprecedented levels caused by the COVID-19-crisis.Footnote14 In this period, the debt of private non-financial sector reached its all-time high (approximately 170% of world GDP).Footnote15 In 2022/2023, the global corporate debt has reached its new record peak with $456 billions of net new corporate debt incurred.Footnote16 Finally, the 2023 collapse of several banks in the United States and Europe – providers of $ billions of debt capital – is a strong reminder of debt’s prominent role in supporting economic activity and of its significant role in the firm.Footnote17

These developments in corporate finance are very important also for corporate governance: a firm’s capital structure influences its governance framework. Unlike equity, debt has not yet been in the spotlight of corporate governance. The notion of ‘debt governance’ is an emerging and evolving one. The earlier influential literature highlighted the role of debt in interactive corporate governanceFootnote18 and stressed that debt is the ‘missing lever’Footnote19 of corporate governance. It also examined, to a certain extent, the increasing potential of debt to influence the firm’s performance.Footnote20

Recently, there have also been several important contributions advocating for the significance of debt in corporate governance. Examples include investigating the role of debt stewardship in the context of ESG and The UK Stewardship Code,Footnote21 examining debt governance effects of material adverse change/effect clauses in corporate debt financing agreements,Footnote22 studying the role of negative debt covenants in credit agreements,Footnote23 analysing the governance role of debt in the U.S.-based dual class ownership structures,Footnote24 and proposing a theory of governance in the context of credit derivatives trading.Footnote25

Yet, the role of debt in corporate governanceFootnote26 has predominantly been addressed in the context of debt covenantsFootnote27 and, in the majority of cases, with respect to the traditional bank financing.Footnote28 The earlier scholarship has not addressed the increasing significance of private credit funds and of the modern debt governance mechanisms, including the debtholder control tools requested by the private credit market.

These developments have important implications for the firm, as they materially impact the dynamics between the different corporate constituencies (e.g. directors, debtholders, shareholders), giving debtholders more control mechanisms to influence the firm also outside financial distress: to cope with the dynamic nature of corporate debt markets, which are full of unforeseen and large-scale risks.Footnote29

In these areas of corporate finance and corporate governance foundational legal questions require re-examination. The urgency of addressing these issues is reinforced by the important changes in corporate finance markets over the past twenty-five years, including the increasing popularity of the private capital industry, specifically of private credit (that has recently been outperforming even the high-yield bonds and the syndicated loan markets),Footnote30 and by the need to better understand the dynamic role of debt in the firm and its modern-day relationship with equity.

In light of this, the focus of this paper is the evolution of the role of corporate debt finance outside financial distress: how debt investment has influenced and could influence the firm in this timeframe.Footnote31

The paper proposes a modern conceptualisation of debt governance (‘modern debt governance’). It does so by developing a taxonomy of modern debt governance, comparing the influence of banks and private credit funds when investing debt capital in a firm.Footnote32 The term ‘debt governance’ in this paper denotes (i) the influence of debtholders on the firm outside financial distress (e.g. cost of finance, directors’ incentives, decisions of the board, the firm’s flexibility to operate, relationship between debtholders and shareholders) (‘the domain of debt influence’), and (ii) how debtholders through their decisions influence the firm (‘the mechanisms of debt influence’), and (iii) the impact that such debt governance decisions have also beyond the firm (i.e. externalities) (e.g. the society, other market participants, general availability of funding) (‘the boundaries of debt influence’).Footnote33

Due to market changes, debt finance has come to play an important role in the firm also outside financial distress: the mechanisms of debt governance are and will be evolving, and the impact of debt on the firm’s performance is of a dynamic nature. Both traditional, but also more modern mechanisms of debt governance are a result of a market driven approach that aims to address the evolving nature of debt finance.

Private credit funds invest on a long-term basis and operate in an illiquid market, charging an illiquidity premium for this. Such a long-term and typically illiquid investment that is usually carried out on a bilateral basis (i.e. between a single debt investor and a borrower) lays a foundation for more cooperation and trust building between the firm and its debt investors. Relational finance is back!

Floating price in private credit (i.e. floating interest re-priced every 30–90 days), as opposed to relying only on debt covenants, is a modern form of debtholders’ influence. It also drives the debtholders’ control of the firm, enabling them (i) to influence and engage with the firm on an ongoing basis and prior to its financial distress, (ii) to have a dynamic view of the firm’s valuation (which often corresponds to the interest rates), and (iii) consequently, to develop an evergreen financing structure. As interest rates go up (as has been the case lately), the servicing of debt becomes more difficult for the borrower-firms (i.e. cost of debt servicing is becoming high). This modern form of debt governance has significant implications on the incentives of the firm’s directors to take into account the interests of debtholders also outside financial distress.Footnote34 In modern markets, debtholders are increasingly interested in ex-ante accurately pricing and ex-post dynamically repricing their investments, as opposed to focusing only on their ex-post credit ranking. In a bank-originated debt market, repricing is also driven by the liquidity in the secondary loan markets.

The strong reliance of private credit funds on contractual creditor protection through bespoke debt covenants, in particular, financial maintenance covenants, as opposed to incurrence-based covenants, that have been predominant in bank lending (covenant-lite trend), provides private credit funds with more scope for control and intervention. Such a control is, moreover, of a long-lasting and relational nature.

By seeking board representation and getting access to the borrower-firm’s management team, private credit funds have a dynamic view on the firm’s valuation and influence the firm. Board representation also helps private credit funds to achieve their investment strategy. This management aspect speaks directly to the corporate governance role of debt.

They also bargain for an equity upside and are often lead investors in the deal. These debt investors are interested in ‘non-default governance’ issues (i.e. governance outside financial distress) because their investment is like equity. More recently, debt investment also generates higher returns than equity, because of the rise in the interest rates. While this type of investment is akin to equity, debt investors are still repaid ahead of equity.

The modern debt governance approach of repricing debt has further implications on the understanding of the nature of loan financing. It challenges the traditional position that loan financing deals are not expected to be renegotiated: they are expected to be continued and not ended. Yet, sometimes, they are expected to be ex-post repriced due to the dynamic nature of debt finance.

The contractual return provisions in the private credit market, entitling debt providers to a minimum return (akin to quasi-equity) and carried interest on their debt investment, directly challenge the traditional conception of debt in corporate finance and corporate governance.Footnote35 The conventional approach is that debt providers are interested in value-maintaining activities of the firm, whereas shareholders are interested in value-maximisation. Private creditors invest for a long-term. These investors are interested in the firm’s success and its capital growth in order to be paid back not only the main debt sum, the interest rate, but also a return on their debt investment and participate in profit sharing on the fund level.

Private credit funds, as they continue to compete with banks, are likely to play a key role in the evolving nature of corporate finance – reshaping and revolutionising private debt markets, by filling in the gaps in financing needs and helping to stabilise financial markets.

In the modern market environment of sophisticated debtholders, outside financial distress, equity and debt have become even more intertwined than they used to be. This paper does not claim that debt governance is always in the interests of equity. Instead, it argues that the significant changes to debt markets affect modern-day debt capital’s relationship with equity, making the two more interconnected and overlapping, even more so in private firms.Footnote36 Modern-day debt investors are interested in the success of their investments also outside the firm’s financial distress, for instance, to generate high return on their debt investment and to achieve the investment strategy (for private credit funds), or to be able to successfully market debt to the secondary loan market (for banks).Footnote37 Effective debt governance not only within, but also outside financial distress further minimises ‘the firm’s total competence and conflict costs’.Footnote38

This paper also aims to show that often debtholders through these modern debt governance mechanisms of private ordering (contractual bargaining) achieve and could achieve a degree of control also outside financial distress. By addressing this, the paper aims to show how the reliance of private credit funds on private bargaining can also improve the economic efficiency (i.e. the link between contractual bargaining (private law) and economic efficiency.)Footnote39

The remainder of this paper is organised as follows: Section 2 studies the important changes in corporate finance markets with respect to private debt. It further presents a taxonomy of the key features of private debt (loan) financing deals, comparing banks with private credit funds (). Section 3 considers the implications of the market changes, discussed in Section 2, from a debt governance perspective. It develops a taxonomy of modern debt governance mechanisms, analysing and contrasting bank financing and private credit financing (). Section 4 then examines the connection between ‘equity’ and ‘debt’ in the firm in the world of sophisticated debtholders. It examines the general benefits of the interlinked equity-debt governance system outside financial distress, and also the advantages of symbiotic equity-debt governance for the firms with private credit financing. Section 5 concludes.

Table 1. Taxonomy of private debt (loan) financing based on the type of the debtholder.

Table 2. Taxonomy of Modern Debt Governance based on the type of the debtholder.

2. Modern private debt: how did we get here?

This section addresses the first theme of this paper: the evolution of corporate finance, in particular, of corporate debt finance. It examines the significant patterns of change in the corporate debt finance markets over the past twenty-five years with respect to private debt. In doing so, this section also investigates the key features of modern debt: dynamic, parallel, adaptable, and market driven.Footnote40

The proceeding analysis establishes the framework on which Sections 3 and 4 rely on (i) to analyse and, where relevant, also to propose modern mechanisms of debt governance, and (ii) to investigate how debtholders influence or could influence the firm outside financial distress. Before doing this, sub-section ‘A’ offers an overview of the origins of the role of ‘debt’ in corporate governance.

A. ‘Debt’ in corporate governance

The term ‘debt governance’ has not often been used in the corporate governance literature, or in the general corporate law scholarship.Footnote41 In their seminal corporate governance paper, Shleifer and Vishny argued that large debtholders have incentives to improve the firm’s performance because similarly to large shareholders, ‘[…] they want to see the returns on their investments to materialize’.Footnote42 It was the influential works by Triantis and Daniels (1995), and Baird and Rasmussen (2006), followed by later studies by Tung (2009), Whitehead (2009), Choi and Triantis (2013), Yadav (2014) that revolutionised the role of debt in the firm and highlighted the role of debt in corporate governance, exploring its significance in the context of the firm.Footnote43

This earlier scholarship made very important contributions in advocating that debt has been a ‘missing lever’Footnote44 of corporate governance, as argued by Baird and Rasmussen, and that debtholders are in a position to monitor and detect managerial shirking, as advocated by Triantis and Daniels.Footnote45 Choi and Triantis further demonstrated how the debtholders’ certain decisions via signal-exchange and collaboration on penalising management have beneficial effects for the firm and its other stakeholders.Footnote46 Economists Nini, Smith, and Sufi showed that efficient debtholder control can promote equity-focused corporate governance or even replace it.Footnote47

Later, Gullifer and Payne argued that one should also consider the governance power given to the debtholders when they waive a breach or default by the borrower-firm.Footnote48 Gullifer and Penn examined the role of negative covenants in credit agreements and their potential role in aligning the interests of directors with that of the firm.Footnote49 More recently, Gomtsian offered a framework for understanding how debt holders can contribute to stewardship outside distress, exploring the role of debtholders in promoting responsible business practices through the stewardship of borrowers.Footnote50 In the context of U.S. uptier transactions, Schloessmann proposed to treat debtholder control over debt covenants similar to the control that controlling shareholders have over corporations by imposing a waivable fiduciary duty of loyalty on controlling debtholders.Footnote51

Nevertheless, the role of debt in the firm for a long time has traditionally been limited to when the firm becomes insolvent or is bordering insolvency.Footnote52 Besides, by virtue of the times when the studies were made, many of them predominantly examined the role of debt covenants and mostly with respect to the traditional bank financing model. The times were different, so were the nature, complexity, and sophistication level of debt markets and of their participants. The times have changed: the firm no longer has to be insolvent for its debtholders to have a significant impact on the firm, and their influence mechanisms do not have to be limited to debt covenants (as discussed in Sections 3 and 4).

B. Two markets for private debt

The important developments in corporate finance markets over the past twenty-five years, and especially post-GFC, resulted in two markets for private debt (i.e. markets where a firm can obtain private debt financing): the traditional bank market and the private credit market. How did we get here? As the proceeding discussion explains, in these two markets, there is a difference not only in the nature and identity of the providers of debt capital, but also in the incentives and the rights that they request to influence and control the firm.Footnote53

The reason for such a divergence is that in a modern market (i.e. post-GFC) banks have been mostly operating within the funding model of ‘originate-to-distribute’Footnote54 to the secondary liquid loan market. The term ‘originate-to-distribute’ means that debt is originated and later sold to the secondary loan market. This model is also known in the finance community as the ‘moving business’.

By contrast, private credit funds have largely focused on the funding model of ‘originate-to-suit-and-fit’ the portfolio of the market that they operate in. The term ‘originate-to-suit-and-fit’ means that debt is originated and kept until its maturity or repayment. This financing framework is also called the ‘storage business’.

The distinction between these two funding models can additionally be described as ‘trading the risk’ for banks vs ‘owning the risk’ for private credit funds. The following sub-sections ‘i’–‘iv’ explore these two funding models (including their interconnectedness), the business nature of private credit funds and their future in debt markets, and the obstacles facing the banks post-GFC, preventing them from using the same business operational strategy as the private credit funds.

i. How and why did this happen?

The corporate debt financing markets were slow developing markets with a strong relational finance element attached to them: banks relied on their relationship with firms to originate and manage their portfolios.Footnote55 In the loan markets, the banks simply knew the firms that they were dealing with: there was less information asymmetry between the providers and receivers of debt finance. As a result, there was not an urgent need to look into loan covenant packages to address borrower-opportunism and to facilitate information sharing regime, and the contractual framework (including debtholder protection provisions) was less detailed. Similarly, for the bond markets, there were covenants included in bond agreements; those, however, were a lot thinner than the covenants requested by banks in loan financing agreements.

From 1970s, when the syndicated loan market started to gather speed, not only the debtholders, but also the corporate borrowers became more sophisticated.Footnote56 Prior to the GFC and, especially, in its aftermath, there has been a further important change in the nature of debt finance and of its providers. The traditional bank-financed debt market has withered away. In this market, there has been a gradual shift from relationship finance to a state where relational finance has become much less common.

This change happened following the various economic scandals during the GFCFootnote57 that involved several of the global financial players, such as the Lehman Brothers, the Royal Bank of Scotland and others, causing the financial regulators worldwide to introduce stricter rules for the banks.Footnote58 Gorton and Metrick suggest that the rise of nonbank lenders was facilitated by ‘regulatory and legal changes that gave advantages to three main institutions: money-market mutual funds (MMMFs) to capture retail deposits from traditional banks, securitization to move assets of traditional banks off their balance sheets, and repurchase agreements (repos) that facilitated the use of securitized bonds as money’.Footnote59 The shift from the traditional banking model into what is commonly known as market-based financeFootnote60 could also be attributed to developments in financing engineering, as well as the globalisation of funding and capital markets.Footnote61

Driven by these changes, markets moved on. There is still the architecture for loans, but banks are often selling or are aiming to sell loans soon after the origination to the secondary loan market.Footnote62 Banks also no longer retain monopolistic position of financing large-scale leveraged buyouts.Footnote63 These developments in debt markets created a raft of opportunities for private credit funds,Footnote64 changing the historic perception of private credit ‘from dinosaur to dynamic funding model’.Footnote65 Private credit funds have come to fill in the gaps in the market where the banks could no longer contribute. Characterised as the ‘money market funding of capital market lending’,Footnote66 private credit funds are financial intermediaries ‘[…] conduct[ing] maturity, credit, and liquidity transformation without explicit access to central bank liquidity or public sector credit guarantees’.Footnote67

During the course of the past fifteen years and, especially, since the start of the COVID-19-crisis, the private credit market has flourished.Footnote68 The number of private credit funds has increased dramatically, so did their power and investment appetite.Footnote69 The private credit market includes asset manager giants, such as Apollo, Ares, Blackstone, KKR, and Oaktree Capital. Over the period of 2003–2020, the market for corporate private debt has grown four times.Footnote70 The private credit market, specifically, expanded from $250 billion in 2010, to $1.5 trillion as of 3rd quarter of 2023,Footnote71 making it a larger market than the venture capital market (which was estimated to grow to $251.54 billion in 2023).Footnote72 In comparison, in 2023, the high-yield bond market has reached $1.4 trillion, the leveraged loan market $1.4 trillion, the Eurozone bank loans $5.0 trillion, the US bank loans $5.4 trillion, and the market for investment-grade bonds $8.1 trillion.Footnote73 As of March 2024, the private credit market is estimated to have reached $1.8 trillion.Footnote74

ii. Private credit – a revived and nearly new phenomenon

Described as the ‘new force in finance’,Footnote75 private credit is becoming one of the key sources of modern debt finance. As an asset class, it existed even before the GFC. Yet, private credit is a revived and a nearly new paradigm because of its significant growth over the past years. In the past fifteen years, private credit funds thrived and are no longer seen as finance providers to only short-term, small sum, non-investment grade firms, which used to be the traditional perception of private credit.Footnote76 Private credit is active not only in the leveraged loan market and provides enough ‘liquidity to fund larger and larger transactions, but also the flexibility to provide an array of financing structures – including unitranche and floating-rate notes’.Footnote77

Such an advancement in the private credit market is evidenced, for instance, by the provision of $4.8 billion financing for FinastraFootnote78 and €4.5 billion financing for Adevinta ASA: the two largest private credit deals on record at the timing of writing this paper. This trend also attests to the willingness of the private credit funds to cooperate amongst each other to finance larger (club) deals.Footnote79

Additionally, private credit has become even more relevant in helping banks to push their liquidity, especially given the 2023 banking turmoil. A notable example of this trend is Ares Management’s acquisition of $3.5 billion lender finance portfolio from Pacific Western Bank, where this portfolio consists of high quality, senior secured, asset-backed loans.Footnote80 Private credit’s commitment to green finance has also become more substantial. For instance, Blackstone raised $7.1 billion (The Blackstone Green Private Credit Fund III) to finance clean-energy companies.Footnote81 Another interesting development with regards to the involvement of private credit – which has traditionally been seen as a finance source for private firms – is the provision of large amounts of private credit financing to multinational public firms. An example of this is chipmaker Wolfspeed Inc. raising $1.25 billion secured note financing from private credit providers, such as Apollo and others.Footnote82

From the investors’ side, a 2023 survey by Goldman Sachs shows that institutional family offices are also interested in investing in private credit.Footnote83

From offering multi-billion dollar unitranche club financing to the provision of net-asset-value (NAV) loans and payment-in-kind (PIK) loans, the more experienced private credit funds, such as Ares, Apollo, Blackstone, and Oaktree Capital, have arguably led to what I describe as a quantum leap in corporate finance.Footnote84

This dramatic rise of private credit has been described as a ‘parallel to the “privatisation” of equity markets’.Footnote85 The data provider Preqin projects a growth for private credit between 2021 and 2027 to reach an all-time high in 2027 by reaching $2.3 trillion.Footnote86 By contrast, the projections for bank financing are less optimistic. For instance, according to the latest EY European Bank Lending Economic Forecast, growth in bank lending to businesses across the Eurozone area is estimated to slow down with growth of only 3% in 2023 and 0.9% in 2024.Footnote87

The ongoing competition between banks and private credit funds directly impacts borrower-firms.Footnote88 This competition especially increased as leveraged loans and other sources of traditional capital have dried up, and buyout firms started to seek finance from private credit funds.Footnote89 An important question, however, is whether the boom behind credit is here to stay. In the context of European deals,Footnote90 on the one hand, in contrast to 2020, during 2021 there was an 89% increase in deals by alternative (nonbank) lenders.Footnote91 By contrast, in Q3 2022, the number of European private debt deals fell by 15.7% in comparison to the same period in 2021.Footnote92 On the other hand, according to the data provider Preqin, in the second quarter of 2023 alone private credit funds raised $71.2 billion globally, which is more than twice the amount compared to the first quarter of 2023, with a fundraising increase in Europe ($33.8 billion raised in Europe out of $71.2 billion globally) and with direct lending being the most dominant private credit strategy.Footnote93

Besides, the surge in the interest rates to combat inflation has its costs and benefits for the providers of private credit. This is because some firms will struggle accessing public markets for finance, helping private credit providers to gain further clientele. It has been suggested that such a development may be advantageous for private credit funds, as it gives them a stronger position to bargain for more protection and favourable conditions.Footnote94 Rising interest rates, however, also entail problems for the borrower-firms that have already incurred a lot of private debt: they now will be facing debt repayments with a higher rate and will need to continue honouring their financial obligations.Footnote95

Despite the ongoing macroeconomic conditions, there is strong demand for private credit, ‘[…] even as dealmaking wanes’.Footnote96 This is because private credit provides attractive returns. It could also help with hedging against rising inflation and diversifying borrowing portfolio of the firms.Footnote97 Moody’s 2023 study on private credit and associated risks highlights that ‘[…] when managed within a robust risk framework, [it] provides opportunity for growth and can improve the portfolio’s overall risk-adjusted return’.Footnote98

As economic conditions globally deteriorate, the private credit model is in a good position to attract even more share of a market from commercial banks, as private credit funds are experienced in operating in an illiquid market: that is their business model.Footnote99 Finally, as mentioned earlier, while the private credit market originated as a finance provider for small and medium-sized companies, in the past years (especially post-COVID-19), the private credit industry has provided multi-billion $ finance also to investment grade private companies, and recently also public companies – a substantial improvement in the landscape of corporate borrowers which rely on private credit. Given the current strains on bank financing, the question arises whether the corporate borrowers that are unable to obtain private credit are self-screening themselves.

iii. Private credit and its business model

The magnetic success behind private credit could be attributed to its different business model from that of banks. This paper developed a taxonomy of private debt financing () below, which aims to demonstrate the important characteristics of loan financing deals based on the type of the debtholder: bank vs private credit.

As shown in , there are several important differences in the business models of the providers of private debt. In the originate-to-distribute (bank-dominated) market, debt is being traded, and the two most important questions for the original debt investor are (i) who is going to hold these rights at a later stage, and (ii) whether it will be in a position to predictably sell the loan in the near future (e.g. three months).

For private credit funds, on the other hand, the main interest is not to originate debt in order to later distribute it; they are predominantly interested in suiting-and-fitting the portfolio of the market that they operate in and often self-originate loans by keeping them until their maturity.Footnote100 Institutional and retail investors in this market invest in loans and provide capital normally to small and medium-sized companies, where capital is essentially the provision of support to the firm by investing in it.Footnote101 In terms of public counterparts for private credit, it has been suggested that ‘[for] private direct lending market, its public counterparts are the syndicated bank loan market and the high yield market’.Footnote102

Unlike commercial banks, private credit funds do not have traditional depositors whose funds are covered by insurance. Instead, they raise short-term funds in the money markets,Footnote103 including from commercial banks, relying on this type of financing to purchase assets that have a longer-term maturity.Footnote104 Also differently from banks, private credit funds typically provide high-risk loans which are not liquid.Footnote105 The driver for them is a long-term relationship with their borrower-firms. This leads to flexibility between the relationship of debt providers and the borrower-firm and the returns that private credit funds negotiate to satisfy their investment model: risk-adjusted returns in addition to the traditional interest charged on debt. In other words, private credit aims to provide better absolute returns to its investors in a form of a regular income (return premium and performance premium).Footnote106

Compared to banks, private credit funds provide firms with access to non-amortising, bullet structures and typically offer more flexibility.Footnote107 They also offer (i) a faster way of obtaining finance due to the due diligence and underwriting process being shorter than the one conducted by banks, (ii) larger hold sizes for leveraged loans, and (iii) more creative solutions to finance the growth of the firm.Footnote108 Yet, private credit funds request a higher cost of credit and are not in a position to provide clearing facilities and ancillaries.Footnote109 During the past years, the protective debt covenant package in bank provided financing has typically been covenant-lite, as opposed to the covenant protection package included in the direct lending deals originated by the private credit funds.Footnote110 The latter bargain for a stronger protection (e.g. the inclusion of financial maintenance covenants).Footnote111

In terms of the seniority of private credit in capital structure, according to Deloitte’s 2023 Spring Private Debt Deal Tracker, from Q4 of 2021 to Q4 of 2022, from 4,290 total European deals completed by 76 private debt lenders that participated in Deloitte’s survey,Footnote112 83% of the private credit deals were first lien structuredFootnote113 (senior unitranche/stretched senior, super senior RCF,Footnote114 super senior TLFootnote115). Unitranche financingFootnote116 in this period has been the most common structure for private debt deals, with 57% of the UK deals and 48% of the European deals structured this way.Footnote117 In comparison, subordinate structures represent only 17%.Footnote118 In sum, in the private credit market the trade-off for the firm is a higher price and more control on its business decisions by the debtholders, but more scope for relational finance with the debtholder, and innovation, creativity, and growth for the borrower-firm.

Despite their increasing numbers and growing significance, there has been little scholarly research carried out specifically on private credit funds. Notable exceptions from economics and finance are mentioned below. Buchner et al., using proprietary deal data (for the period of 1982–2015) of private-debt funds from the Centre for Private Equity Research, among other things, find that private credit deals without venture capital and private equity sponsors generate premium, and that this sponsorless premium compensates debt investors for higher risk and costs of risks mitigation.Footnote119 Jang uses a proprietary dataset of credit agreements to study the US market of nonbank direct lending to private equity middle market buyouts.Footnote120 Jang’s study shows that similarly to banks, direct lenders actively rely on covenants for monitoring the borrower-firm; by contrast to bank financing, direct lending is more expensive, because private credit funds bargain for higher interest rates and request tighter debt covenants; compared to bank financing they also provide finance more against cash flow to smaller firms, offer more flexibility in ex-post distress situations, and require more involvement from private equity (‘PE’) sponsors.Footnote121 A study by Block et al., surveys the US and European investors, primarily direct lending funds, with private debt assets under management of over $300 billion.Footnote122 Among other things, the authors find that the US and European funds share many similarities, but that the European private credit funds are less dependent on PE sponsors and are more in a competition with banks.Footnote123 Earlier, Böni and ManigartFootnote124 collected data on 448 private debt funds (1986–2018) and examined their net-of-fees internal rate of return (‘IRR’) (private debt fund performance), finding that on average the net-of-fees IRR was 9.19% and highlighting that private credit funds offer attractive returns to their investors.Footnote125

iv. It is a trade-off story

The costs and benefits of the nonbank financing system have been a subject of great debate. The empirical evidence suggests that nonbank financing creates value by ‘[…] provid[ing] commercial banks with sources for increased loanable funds and assumes some of the risks associated with loan origination’.Footnote126 Chernenko et al. – who analysed hand-collected credit agreements (filed with The US Securities and Exchange Commission) for a random sample of 750 publicly traded US-based middle-market firms that appear in Compustat financial dataset at least once for the time period between 2010–2015 – find that one-third of all loans are provided by nonbank financial intermediaries.Footnote127 This is especially true when there is less competition between the banks and nonbanks, as the latter see this as an opportunity to charge a higher interest rate.Footnote128 Chernenko et al., also show that ‘nonbanks improve access to capital for firms that are observably risky and that are unable to borrow from banks because of bank regulations’.Footnote129 A study by Davydiuk et al., finds that borrower-firms’ access to direct lending, in particular, funding by business development companies, stimulated economic growth and innovation.Footnote130

According to The UK Financial Conduct Authority, this non-traditional finance model ‘offers the prospect of significant welfare gains for society – if we monitor it carefully’.Footnote131 Similarly, a study by The World Bank highlights the benefits for firms of obtaining new finance from non-traditional sources, specifically, the advantages with respect to diversification of their financing sources and improvement of resilience to financial crises.Footnote132 At the same time, nonbank lenders are also an important source for obtaining syndicated financing for non-financial firms.Footnote133 Ivashina and Valée show that ‘a larger non-bank funding for the loan, and a smaller skin in the game of the arranging bank, are […] associated with more complex contractual terms’.Footnote134

On the other hand, the increasing shift from the bank-dominated model to private credit has raised concerns over the transparency of the firms that are being financed by private credit funds and of their debt. The EU adopted new rules on the amount of borrowed money that private debt funds can invest.Footnote135

C. Interconnectedness of two markets

The flourishing of private credit creates more competition in debt financing markets; competition in itself is a positive phenomenon. Although, as the previous sub-section explained, there are two markets for firms to obtain private finance (i.e. from private credit funds and from banks), the private credit model is not entirely separate from the rest of the private debt market (i.e. bank-originated debt). Why? There is an economic link between these two markets because of various intercreditor issues which often arise as banks and private credit funds both borrow from and lend to each other and generally do business with each other, including, for instance, by participating in syndicated financing.Footnote136 This sub-section highlights the interconnectedness of risks in these two markets.Footnote137

On the one hand, since typically the private credit capital is ‘locked in’, it is less susceptible to fluctuations in the market and, therefore, less likely to cause a systemic crisis by itself.Footnote138 On the other hand, as private credit funds also often borrow money from banks for their business and the availability of bank capital has been limited since especially the banking turmoil of 2023,Footnote139 such a development may also affect private credit funds. Moreover, if the borrower-firms cannot repay due to rising interest rates, this may also negatively impact the private credit industry. This is not only a problem for those lending and doing business with the providers of private credit, but also for those firms which, as a result, may not be able to borrow from them.

These propositions are in line with the Bank of England’s (‘BoE’) Financial Stability Report, highlighting that ‘Any crystallisation of risks in [private credit] markets could spill over to the UK given the role of risker credit markets in financing UK businesses, and through UK financial institutions’ exposures to affected global counterparties, including foreign banks’.Footnote140

On the other hand, the same BoE report also mentions that

Private credit exposures of UK banks are limited. The closed-ended nature of funds investing in private credit, their low leverage, and extended lifespan, may help to limit fire sale risks. The [US] Federal Reserve has therefore noted that risks to US financial stability from private credit funds appear low. Nonetheless, parts of the US market use riskier fund structures with greater leverage to boost returns compared to the UK.Footnote141

The web of interconnected risks in these two parallel markets for private debt may, nevertheless, present systemic risks for the global economy.Footnote142 This type of risk interconnection is in addition to more general correlation of financial risks as a result of the COVID-19-crisis.Footnote143 While this paper does not aim to discuss the macroeconomic implications of these interconnected risks, it is important to flag that the debtholder controls rights in each market have been different over the past years (covenant-lite or more aggressive).Footnote144 In covenant-lite packages, the control rights inserted vary in their nature from those in non-leveraged finance.Footnote145

The empirical results also confirm that in modern debt markets there is an ever-growing interconnectedness between these different typesFootnote146 of debtholders and the capital that they provide.Footnote147 At the same time, their incentives are different. For instance, compared to bank lenders, nonbank syndicate participants have a higher likelihood of exiting the syndicate than agreeing to renegotiate the syndicated deal.Footnote148

The changes in debt markets, resulting in two competitive markets for private debt, have important consequences for the relationship of debtholders and their borrower-firms. Modern-day debtholders have more mechanisms, experience, and more diverse interests to control their investments on a continuous basis, including prior to the firm’s financial distress. The implications of these changes from the perspective of the corporate governance role of debt form the discussion of Section 3.

3. Modern debt governance – why should we care?

This section addresses the second theme of this paper: the implications of the changes in debt financing markets for modern debt governance. presents a developed taxonomy of modern debt governance mechanisms, categorising them based on the type of the debtholder (banks vs private credit funds). The taxonomy also shows how changes in private debt finance markets have shaped modern debt governance.

This section also demonstrates that these debt governance mechanisms (i) reflect the parallel nature (i.e. banks vs private credit funds) of the market reality in which debtholders and firms operate in, (ii) are driven by the competition between the providers of debt capital, (iii) and are adaptable – directed by the need to keep pace with the dynamic nature of modern debt finance. This section further explains why debtholders are interested in the governance of the firm when the firm is solvent.

A. Mechanisms

This sub-section develops a modern taxonomy – shaped by the modern market practices – which provides a summary of the modern debt governance mechanisms forming the basis of the discussion in sub-sections B–G.

B. Relational finance is back

Due to the typically bilateral and illiquid nature of private credit financing, there is more scope in private credit for relational finance. ‘Relational finance concentrates specifically on the essence of the debtor–creditor relationship. It incentivises the creditor to ensure beneficial financial coordination and control, with derived gains accumulating to all stakeholders’.Footnote149

For borrower-firms the relational nature of finance has both its advantages and disadvantages. It is beneficial as relational debtholder has a better knowledge of the specifics and objectives of the borrower business and is, arguably, in a better position to help the borrower to achieve them. It also helps both borrowers and debtholders to address information asymmetry problems, minimising the social costs that are connected to financial distress.Footnote150

On the other hand, the costs of relational finance for the borrower are the information monopoly obtained by its debtholder. This is especially the case with the private credit financing, where the debt investment is long-term and where the nature of financing is private. In the longer-term, this might result in a hold-up problem for the borrower.

As mentioned in Section 2, for banks relational finance has mostly withered away due to increased banking regulation.Footnote151 The increased competition – as a result of change to the landscape of debt providers and predominantly driven by banking regulation, which creates a capitally inefficient framework for banks – continues to impact banks’ ability to provide long-term relational finance and above a certain size.Footnote152

C. Board representation – dynamic view of valuation

In addition to the relational nature of private credit financing, private credit funds also make nominations for their representatives to sit on the board of directors of their portfolio companies.Footnote153 This management aspect (representation on the board) speaks directly to the corporate governance role of debt. It also helps to establish a more informed relationship between the debtholders and the firm, giving debtholders a dynamic view of the firm’s valuation.

Debtholders’ involvement on the borrower-firm’s board in this way adds value to the firm, contributes and helps private credit funds to achieve their investment strategy.Footnote154 It is also beneficial for the firm in terms of knowing and trusting who owns the risk of its debt. Debtholders in this way also have enhanced information rights.Footnote155 These debt investors have formal and informal meetings with the board of their portfolio (i.e. borrower) firms.

Driven by the relational nature of finance provided in this market, private creditors participate in the running of the firm and provide sophisticated monitoring. They get access to the management team, scrutinising what the managers of the borrower-firm do. Such access also helps to establish relational finance. This type of involvement channels a continuous flow of information, enabling private credit funds to do firm valuations on a dynamic basis – valuations that reflect the true value of the firm at the time.

This development has lately been studied empirically. An empirical study on private credit funds by Block et al., surveys the degree of board representation when private credit funds sit on the board of their borrower-firms.Footnote156 The survey finds that outside financial distress, private credit funds do seek board representation both in the US and in Europe, where only 41% and 22% participants of their survey responded to remaining as passive participants.Footnote157 The authors also find that during financial distress, there is more active participation on the borrower-firm’s board.Footnote158 Their results are in line with the empirical findings by Jang (2022),Footnote159 suggesting, among other things, that private credit funds have a strong influence on the board (actively seeking board observation rights) during renegotiation process post-covenant violation.Footnote160 As shown in , compared to private credit, in modern-day bank financing, there is less opportunity for relational finance, the debtholders have less enhanced information, and there is less scope for dynamic valuation of the firm.

D. Equity upside, being lead investor, participation in capital growth

One of the interesting features of loan financing provided by private credit funds is the direct participation of debt investors in capital growth of the private credit funds in which they inject debt capital.Footnote161 Such a participation in capital growth and profit sharing is achieved through a contractual mechanism stipulating for an internal rate of return (‘IRR’).Footnote162

The return consists of two components. The first one known as ‘“preferred return” (also hurdle rate) [is] a minimum annual return that the limited partners are entitled to claim before the fund manager starts receiving carried interest’.Footnote163 In this regard, compared to private equity, where investors should not expect a return on capital or distributions for typically several years, in private credit, investors are entitled to receive this part of their income quickly. The second one ‘“carried interest” [is] the amount (profits) which is above the preferred return rate that the fund manager receives as compensation which is based on the performance of the investment’.Footnote164

It is a contractual entitlement to a return on their debt investment: return not in the form of a traditional interest rate, as it is in bank financing, but in addition to this. Depending on the private credit strategy (senior debt, subordinated capital, credit opportunities/distressed debt, specialty finance) the IRR is different, with senior debt having the lowest (but still a higher IRR than investment grade bonds or higher yield bonds) and distressed debt having the highest IRR.Footnote165

This development shows that private credit challenges the traditional conception of debt investment in corporate finance and corporate governance. The established position is that debt providers are interested in value-maintaining activities of the firm, whereas shareholders are interested in value-maximisation. The conventional approach for loan finance (as opposed to, for instance, convertible debt) is that there is no capital growth for debt providers.Footnote166 Yet, in private credit, debt investors’ participation in profit (i.e. through a return on their debt investment) disqualifies the orthodox position.

In private credit, debt investment is typically for a long-term (these debt investors, are locked in a relationship for a long time), and the investors in this market are interested in the firm’s successful performance: to be paid back not only the main sum, the interest, but also a return on their investment.

In addition to participation in profit sharing via return on debt investment on a fund level, as discussed above, private credit investors participate in control and upside risk through equity stakes and warrants. When they do so, they benefit in their capacity as shareholders and not debtholders, but it is their bargaining for these rights contractually as debtholders that later allows this level of control.

In this regard, Buchner et al., find that

the average deal in [their] sample [deals between 1982–2015] comprises an equity stake (Direct Equity) of almost 7% upon conclusion of the deal. Through their exercise of warrants included in the deal, debt investors acquire a further equity stake, averaging 4% upon warrant exercise. ([…] Postdeal Equity).Footnote167

E. Bespoke debt covenants

Unlike in bank financing, where the design of debt covenants is often ex-ante informed by the later chance and cost of syndication of the loan, in private credit, including for unitranche loan facilities,Footnote169 debt covenants can be more bespoke. Private credit funds also bargain for stricter financial maintenance covenants. Examples of maintenance covenants are a borrower maintaining a (i) maximum leverage ratio (specified ratio of debt to EBITDA,Footnote170 or some other cash flow measure), or maximum interest coverage ratio (specified ratio of EBITDA or some other cash flow measure to interest expense), or minimum fixed charge coverage ratio (specified ratio of EBITDA, or some other measure).

These leverage covenants are key and will require the borrower to deleverage over time. Especially for senior debt facilities, breach of a financial covenant will be an Event of Default under the financing agreement, allowing the debtholder to accelerate the debt. In bank financing, since 2017–2018 onwards there has been the trend of covenant-lite financing. By contrast to financial maintenance covenants, incurrence covenants that are more common in high-yield bonds and covenant-lite loans ‘[…] only require compliance with a financial ratio if the borrower does a particular action (for example, issues more debt or takes on a further loan)’.Footnote171 In addition, to more bespoke financial covenants, private credit funds also bargain for heavy information rights to monitor the borrower.

Unlike bank financing, where standardised (e.g. LMA-based)Footnote172 documentation is very common and serves as a basis for negotiations, for private credit financing, because of its nature, often the loan documentation specifically reflects the objectives of the borrower–lender relationship and is bilaterally negotiated between the parties. This also gives debtholders more scope for ex-ante bargaining for control and monitoring rights.

Finally, it is important to note that there is a difference between debt governance via debt covenants (covenant-lite) in bank financing and debt governance via bespoke debt (including financial maintenance) covenants in a relational finance environment on a long-term basis that is provided by private credit funds.

F. Dynamic control through floating pricing

This sub-section focuses on the repricing trend in private credit. Floating price phenomenon in private credit is a way of debtholder influence – driving debtholders’ control of the firm. This type of control enables debtholders to have a significant impact on the firm: to influence the firm not only in a more traditional sense, when the firm is in financial distress, but also beyond this timeframe. It is also different from more traditional debt governance through debt covenants.Footnote173

i. Pricing and barriers to accurate pricing

This sub-section explores the important aspects to an accurate calculation of credit risk and pricing of debt, and the typical barriers to their accurate completion. Many notions, including that of credit risk and pricing of debt, are a response to imperfect markets and market failures.Footnote174

From the debtholders’ perspective, credit risk has been defined as ‘the possibility of losing money due to the inability, unwillingness, or nontimeliness of a counterparty to honor a financial obligation’.Footnote175 It has been suggested that main issues with respect to risk are the non-guaranteed nature that the event will materialise, the latter’s impact on the firm’s value, and that there are both positive and negative implications that could be caused by the materialisation of the event.Footnote176

Debtholders price risk in different ways, such as through interest rate, contractual creditor protection, and through proprietary creditor protection. When pricing risk, they also rely on borrower’s past financial statements. Financial statements, however, rely on historical data, and, therefore, their usefulness is limited to a certain extent. Contractual representations and warranties are also not useful in the longer term. This is due to the fact that except for a few repeating (evergreen) representations,Footnote177 the majority of contractual representations and warranties in loan financing are given by the firm at the time of entering into the agreement. Risk is also priced by relying on various risk-diversification (debt decoupling) mechanisms (e.g. loan transfers). Risk exposure becomes a bigger concern for debtholders when the provided finance is medium or long-term. This is especially the case in private credit, where in addition to the long-term nature of financing the market is illiquid.Footnote178 There are several reasons for debtholders’ concern in long-term financings.

First, the longer the time-period of exposure, the higher the chances that the borrower-firm might not be able or willing to pay. In other words, time is a risk.Footnote179 Debt investors look for optimal mechanisms to quantify types of risks, including credit risk. Yet, quantification of credit risk is a complicated and not an exact science. Relying heavily on a single number or a fixed criterion might not necessarily be useful. Several barometers of risks have been suggested in the literature, such as the credit exposure, the probability of default, the recovery rate in case of default, and the tenor of the provided loan.Footnote180

Second, the predictability or precise calculation based on one or only several figures (e.g. by relying on financial covenants: debt/equity ratio, EBITDA,Footnote181 etc.) is often impractical. This is because specifically quantified numbers mainly account for borrower-opportunism (e.g. endogenous events/idiosyncratic risks), whereas external events (e.g. exogenous risks/risk externalities, such as inflation, market crash, or COVID-19) can also significantly influence a borrower-firm’s behaviour.

Third, an exact quantification of the debtholder’s exposure is typically calculated at ‘Day 1’. This is one of the main issues for bank-originated loan financing (e.g. term loans, revolving loans, syndicated loans) and is also true for bonds. When the firm enters into the agreement with the debtholder, the firm makes representations and warranties about its business. Except for very few repeating representations, however, the rest of representation and warranties are typically made at ‘Day 1’ of entering into the transaction. Setting the price at ‘Day 1’ typically does not reflect what might happen, for instance, in a year. Such a quantification of risk is thus often not up to date; it does not necessarily consider the long-term nature of finance and unpredictable future.Footnote182 There are also other types of risks relevant for credit pricing, such as liquidity risk, market risk, operation risk, that should ultimately be reflected in the pricing of corporate debt. In private credit, these issues are addressed through a floating interest, which is repriced every 30–90 days.

In the past years, another new debt pricing component has been the factoring of ESG requirements in the price of corporate debt (e.g. sustainability-linked loans, social loans, green loans).Footnote183 The inclusion of ESG-based criteria in sustainability-linked loans, green loans, social loans, is an example of the ex-post incentive alignment (reward) legal strategy.Footnote184 In the private credit market, this is achieved through ESG-linked margin ratchets.Footnote185 The loan interest margins are reduced when the borrower-firm achieves certain predefined sustainability targets.

In the context of the calculation of credit price, a firm’s credit rating often provides certain guidance to its debt investors. In the private credit market, however, borrower-firms used to be and many of them still are typically unrated firms. In bank financing, a firm’s credit rating is determined by credit rating agencies based on historical data, and it is often the borrower-firm that initiates a dialogue with a credit rating agency to appraise its credit rating. At times a part of the undetected risk could be attributed to the willingness of credit rating agencies to ‘over-rate’ borrower-firms. It has been argued that this was the case during the 2008 sub-prime crisis.Footnote186 One explanation for this could be that there is not enough competition among the credit rating agencies. This sub-section will not discuss the credit rating issue further. For the purposes of the following analysis, it is sufficient to note that credit rating in private credit is not a requirement and in bank financing it represents a backwards-looking approach that does not necessarily and accurately reflect what will happen to the firm. This is especially concerning for long-term revolving loans. This position is in line with the proposition that ‘the probability of default with the potential for credit ratings to migrate over time adds a dynamic element to credit risk estimation’.Footnote187

Credit risk is further influenced by the decisions of the firm’s directors. Directors, as fiduciaries of the company,Footnote188 are the ones to make most decisions. Their decisions also impact the firm’s debt financing decisions and its credit risk profile. According to Merton, three variables plus a discount factor are used to determine the likelihood of default. Those are ‘the time to maturity (lessens the likelihood), the volatility of the company’s operations (increases the likelihood), and the existing distance between the assets and debt (lessens the likelihood)’.Footnote189

The empirical evidence in the context of bank financing suggests that renegotiated debt agreements following a violation of covenants have interesting pricing implications. For instance, Nini et al., find that such debt agreements ‘provide less fundings, have a shorter maturity, and carry a higher interest rate spread compared with the contracts prior to the violation’.Footnote190 Roberts shows that the typical loan provided by a commercial bank reprices corporate loans five times or every nine months.Footnote191 Gârleanu and Zweibel find that the median covenant violation occurs one year from the inception of the loan.Footnote192 Repricing of corporate debt is sometimes caused not necessarily by a violation of the terms by the borrower-firm, but as a consequence of an exogenous risk affecting the financial relationship or because the firm wishes to have more flexibility in its operations.

ii. Dynamic element to pricing

This sub-section argues that floating pricing in private credit is a form of debt governance, directly impacting the firm and addressing the dynamic nature of debt. Often pricing and repricing of debt has nothing to do with the low quality of the borrower-firm. Rather, it is driven by the firm’s wishes to be more flexible in its day-to-day operations, especially in the context of bigger deals.

As the following discussion explains, the capital providers in the private credit market are not looking to a control in the traditional sense, and they still acquire information often because of the relational nature of finance. These debt investors charge a floating rate spread above the reference rate. The floating interest provides private credit investors with the opportunity to reflect the current market cost of lending in their long-term relationship with the firm.

In the past twenty-five years, there has been a shift in the corporate debt market from escalating and exiting a financial relationship to ex-post repricing it. For banks, it is important for their debt investment to reflect the current cost of lending and the up-to-date position of the borrower-firm: to be able to sell this debt to the liquid secondary loan market. Unlike banks, private credit funds typically operate in an illiquid market: they price their illiquidity, including by charging an illiquidity premium.Footnote193 Dynamic pricing has become an essential part of private credit financing, as it allows private credit funds to price their illiquidity more adequately and to keep up with the market changes (e.g. the rise in the interest rates to combat inflation) affecting the cost of finance.

Firms are normally provided with financing based on debtholders’ ex-ante calculation of (i) the profitability of the project and (ii) the overall credit risk of the borrower-firm.Footnote194 Consequently, pricing is the flipside of the expected profit from the loan. Debtholders typically calculate the risk of a firm’s default in advance and price debt accordingly. Such a pricing strategy is beneficial for them as it allows to offset the risk of potential default on the part of the firm. Generally, they are also careful about terminating financing because a wrongful acceleration might result in payment of a substantial amount of damages and might also negatively affect their business reputation.

Pricing/repricing debt is useful not only for countering the renowned information asymmetry problem and the inter-connected ‘market for lemons’Footnote195 issue embedded in debt financing markets; arguably, it is equally important for addressing the problem of lending to the borrower-firm when the debtholders have made a ‘pricing mistake’. In this context, the term ‘pricing mistake’ means that the price (i.e. the margin) does not reflect the risk or the market cost of lending. In other words, it is no longer profitable for the lender to lend to the firm on such price as agreed previously. The COVID-19-crisis is a practical example of such a situation where debtholders were forced to reconsider the price of corporate debt. This proposition is in line with the earlier empirical evidence, which suggests that many long-term debt contracts are renegotiated prior to their stated maturity.Footnote196

From the borrower-firms perspective there are two main reasons why the borrowers agree on floating interest rate. First, in the context of private credit lending, the borrower is looking for specialised lenders who can help the company to achieve its business strategy, and, in return, the borrower agrees on floating interest rate. Second, in the past years since the beginning of 2023, there were serious liquidity issues, affecting significantly syndicate loan markets. This meant that borrowers did not have many alternatives, but many of companies needed urgent financing.

Repricing results in changes to the amount, maturity and other terms of financing, and sometimes these changes are caused not necessarily by financial distress of the firm.Footnote197 This allows debtholders to directly and significantly influence the firm and is a new form of debt governance, which is different from the traditional influence of debtholders via breach of debt covenants. It drives the debtholders’ control of the firm. Floating price enables debtholder to influence and engage with the firm on an ongoing basis and to be in a good position to dynamically value the firm. As interest rates go up, the servicing of debt becomes more difficult for the borrower-firms (i.e. cost of debt servicing is becoming high). This new form of debt governance has significant implications on the incentives of the firm’s directors and puts pressure on them to consider the interests of the debtholders also outside financial distress.

G. Liquidity affecting governance

Since the GFC, there has been a further development in the secondary loan markets. There is more liquidity in the secondary loan market, and banks no longer hold on to loans until their maturity. This sub-section focuses on the changes in the secondary markets for corporate loans, and the impact of the liquidity in the secondary loan markets on debt investors’ incentives to divest and transfer risk. It argues that such a change has its implications on their behaviour and engagement with borrower-firms from a debt governance perspective.

i. Evolution, but revolution?

When making financing decisions, debt investors provisionally calculate the riskiness of the firm in their cost of finance. These investors that are interested in minimising their risk exposure from the default of an individual borrower-firm might look for techniques to transfer their loans and diversify their risk. This is especially typical for syndicated loans.Footnote198

There are different reasons for loan transfers, which include, but are not limited to risk diversification, subsequent syndication, and the defaulting nature of the loan. For banks, this could also be the result of capital adequacy rules imposed by banking regulation.Footnote199 When banks offset risk because there is a problem with the borrower-firm, they may write down a loan or transfer it, or enter into a credit default swap, or a repo transaction.

In debt finance, there used to be a distinction between a tradable debt and other type of debt.Footnote200 However, these other types of debts that used to be non-tradable, for instance, syndicated loans, have now come to be transferred on a frequent basis. This creates liquidity for the secondary markets for loans. The buyers used to be banks, but nowadays the buyers of transferred loans can also be specialised distressed debt traders and vulture funds. For loans that are not syndicated, the interest in a loan can also be sold to the secondary market. Alternative means of creating liquidity also involve collateralised loan obligations and credit default swaps. As a result, there is a shift from ‘assets that are held to creation of assets that are tradable similar to securities’.Footnote201 The strict distinction between these two classes of debt is no longer as important as it used to be.

Although this paper focuses on private debt, it is worth mentioning that, in relation to the bond markets, bondholders also used to hold on to debt until the maturity of the bonds, relying on payments on the principal amount and interest. In the past years, bondholders typically sell their bonds prior to their maturity.Footnote202 Schwarcz argues that this makes bondholders similar to equity investors, as they are now more interested in pricing their debt as opposed to securing a priority in the creditor rank.Footnote203

For bank financing, historically banks sold their participations in loans, but that they also kept most of their loans until maturity and, by negotiating a loan, used to protect their assets.Footnote204 Nowadays, banks typically originate loans to sale those to the secondary loan market, and they buy and sell credit risk in order to manage their risk exposure more efficiently.Footnote205 In this regard, the maturity of loan has been argued to also affect corporate governance.Footnote206

The secondary market for loans consists of the primary (syndicated) loan market, where portions of a loan are placed with several banks, and the secondary category for the seasoned or secondary loans, where it is a single bank selling off an existing loan or a part of it.Footnote207 These secondary loan markets have grown in their size and act as an important channel for managing credit risk.Footnote208 As a result, there is more liquidity not only in the context of public, but also private debt markets. Such a development in secondary trading has been argued to possibly even overtake the important role of debt covenants, including financial covenants, and monitoring in corporate governance.Footnote209

At the same time, in the past years corporate borrowers started to restrict the use of sub-participation for lenders, and this development has had an immediate impact on the liquidity in the secondary loan market.Footnote210 Penn argues that the reason for this is because borrowers no longer view sub-participation as a mechanism of transferring economic risk. Rather, they see it as a ‘[…] method of transfer which potentially impacts rights and obligations under the underlying loan and also its relationship with the [l]ender’.Footnote211

ii. Liquidity and transferred debt

The liquidity in the secondary loan market, some might argue, weakens the incentives of the original debt investors to actively monitor the firm. Along these lines, some argue that the traditional mechanisms of engaging with the firm (e.g. debt covenants), thus, might be less relevant.Footnote212 This sub-section argues that since in the past years there has been a lot of competition in the secondary loan markets, it is in the original debt investors’ interests to monitor the original loan package and invest in the relationship with the firm. Otherwise, the original debt investor (typically a commercial bank) might not be able to successfully market this debt to the secondary loan market or be able to market it but only with a substantial discount to its original price, meaning that it will incur losses.Footnote213

Despite the changes in the market from originate-to-hold to originate-to-distribute,Footnote214 first, the original banks will not be in a strong position to distribute the debt if it does not reflect the true position of the borrower-firm at the time.

Second, the lead arranger/manager in syndicated facilities often hold on to debt, even if the other members of the consortium market it to the secondary debt market. On the one hand, an information asymmetry exists between the original and the new debtholder. On the other hand, these new investors can benefit from the involvement of the original banks and the information that they hold on the firm.

Third, the borrowers sometimes successfully manage to restrict some types of transfer, for instance, sub-participation.Footnote215 Moreover, the empirical evidence in the context of bank loan financing suggests that there are negative stock returns for the firm on the loan sale announcement.Footnote216

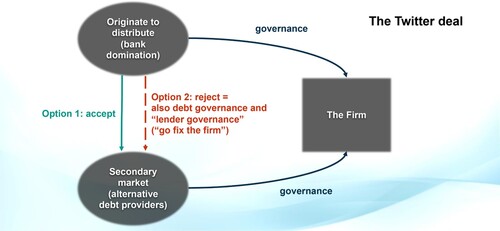

The liquidity in the secondary loan markets, and the option to market the debt to the secondary market is also profitable for the firm. This is because, especially in times of recession and as shown by the Twitter deal, the investors in the secondary market will not be willing to buy an overpriced debt, or will buy it, but at a huge discount to the original price. By making either decision, the secondary debt investors, also contribute to debt governance (‘lender governance’).Footnote217 Moreover, the longer the original debt investors are forced to hold their debt and are not able to sell it, the longer the loan market will be frozen, causing further negative externalities. At the time of submitting this paper, the banks were not yet able to offload or refinance Twitter debt.Footnote218

Such a risk diversification strategy could affect debtholders’ incentives and the extent of their involvement in monitoring the borrower.Footnote219 This additionally raises the question of socially optimal renegotiation of the financing agreement and the debt investor’s incentives to transfer the loan. It also touches upon an important tension between ‘the right of the borrower to prevent or limit the transfer of the debt and the right of a lender to alienate its own property, namely the debt or the proceeds’.Footnote220

It is also possible for debt investors to provide finance to firms, with an option for the former to transfer the loan at any point in time.Footnote221 This typically happens especially with high-risk (non-investment grade) firms. Depending on the type of a loan transfer (e.g. novation, assignment, sub-participation),Footnote222 the original debt investor will either cease its relationship with the firm or will continue to be involved in a limited way. While one might argue that the liquidity in the secondary loan markets might dis-incentivise debt investors, including syndicate lenders, to monitor and enforce the firm’s compliance,Footnote223 the empirical evidence suggests the contrary.Footnote224 Additionally, the original debt investors will be concerned about the restrictiveness of the initial financing terms. This is because they may otherwise be concerned that they will not be able, for instance, to transfer the loans in the secondary loan market without appropriate debtholder protection mechanisms.Footnote225

4. The equity-debt story in a world of sophisticated debtholders

This section addresses the third theme of this paper: the implications of the evolution of corporate debt finance for the modern-day relationship between equity and debt. What happens to the equity-debt story in a world of sophisticated debtholders? Due to the changes in corporate finance markets and the increased importance of the role of debt financing, equity and debt governance have become even more intertwined and overlapping than they used to be.Footnote226 This section does not claim that debt governance is always in the interests of equity. Instead, it argues that the significant changes to debt markets affect modern-day debt capital’s relationship with equity, making the two more interconnected and overlapping.

i. Why should there be more interest?

The preceding discussion showed the evolution of the role of debt in the firm. The way that debt operates today implies that the firm’s directors are often incentivised and influenced to take into account the debtholders’ interests also outside financial distress. Depending on the type of debt financing (bank or private credit), the influence mechanisms may differ (). Before exploring the benefits of symbiotic equity-debt governance, one should consider why there should be more interest in the relationship between modern-day equity and debt. Three inter-connected justifications are presented below.