?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Starting from document research, this paper analyzes the mechanism of the risk spillover effect from developed capital markets to the Chinese capital market. After that, this paper conducts an empirical study on the risk spillover effect of developed capital markets on the Chinese capital market by using the DCC-GARCH model. Then the impact degree of global major stock market fluctuations on the Chinese stock market is measured. The analysis shows that there exists a significant risk spillover effect of developed capital markets on the Chinese capital market, but the effect began to weaken after the financial crisis and the size of the spillover effect can be affected by macro factors such as geographical locations, foreign trade, and foreign investment.

1. Introduction

In recent years, under the trend of the integration of global economy, finance, and science and technology, the co-movement between capital markets of various countries has been increasing and the contagion trend of ‘rising and falling together’ has been presented, especially when some significant events like COVID-19 happen (Baber Citation2020; Zhang, Ding, and Shi Citation2022). Cross-border capital is playing an increasingly essential role in the global capital market (Alkan and Çiçek Citation2020), especially with the comprehensive promotion of financial markets in developing countries like the Chinese financial market opening to the outside world, Chinese financial system will be more closely linked with the world financial system, and cross-border capital will play an increasingly critical role in the Chinese capital market. However, since the spillover character of financial risks, the risk transmission mechanism between different capital markets, would transmit the fluctuation of one capital market to others, it means that the possibility of the Chinese capital market and other capital markets of developing countries being exposed to foreign market risks will become higher (Shen, Dai, and Luo Citation2014; He Citation2019). Therefore, for the sake of normal operation of the Chinese capital market and other capital markets in developing countries without abnormal fluctuation, under this background, it will be of great practical significance to study the spillover effect of foreign market risk on the Chinese capital market and design effective policies and methods to better prevent the spillover effect during the opening up of the Chinese financial market, which can also be a reference for capital markets in other developing countries.

When it comes to the spillover effect, it can be defined as the dependence of a given asset variance on the past covariance and variance of other assets from the micro perspective (Bonato, Caporin, and Ranaldo Citation2013), and can also be defined as the bilateral spillover level of risks when the market goes up and down from the macro perspective (Li et al. Citation2021). This effect would make negative events become more extensive and profound to investors’ expectations and transmit the fluctuation of the capital market to other stock markets through stock re-pricing and investor psychological expectations (Baruník and Křehlík Citation2018; Yu Citation2019). In order to prevent the negative effect it brings, the risk spillover effect should be measured through the Garch-Copula-Covar model and other models (He Citation2019), then the economic indicators of developed countries should be emphasized. Internal and external risk monitoring and early warning are necessary to be strengthened, and international cooperation in supervision is suggested to carry out (Yang Citation2015, Citation2020). It can be found that the existing literature on the spillover effect of foreign market risk has mainly paid attention to its definition, degree measurement, negative information impact on investors’ reaction frequency and expectations, and relevant countermeasures. Although there exists some studies that research the risk spillover effect of the foreign market on the Chinese capital market, most of them only researched the spillover effect of developed capital market in a single country or region on the Chinese capital market that lacked universality, existing the research gap that does not have analysis on the spillover effect transmission mechanism of foreign market risk on the Chinese capital market and further measurement on spillover effect degree, which limited the estimation of entire risk spillover effect on the Chinese capital market.

Based on the summary of the existing relevant research results, in order to fill the research gap mentioned before, this article makes an in-depth analysis and discussion on the main transmission mechanism of the risk spillover effect of foreign market risk to the Chinese capital market. Also, the DCC-GARCH model and constructed dynamic risk spillover index are used to measure the direction, degree, and trend of the risk spillover effect of global major stock market fluctuation on the Chinese stock market to contribute to answering the following questions in the research area: 1.) How does the spillover effect of foreign market risk transmit from developed countries or regions to the Chinese capital market? 2.) What are the direction and specific extent of the spillover effect? 3.) What is the impact of significant events like China’s accession to WTO and COVID-19 on the spillover effect? These would undoubtedly have important practical significance and theoretical value for maintaining the stable and healthy development of the Chinese capital market and other capital markets in developing countries, improving the level of foreign financial risk prevention level of each country, and enriching the spillover effect of foreign risks and other aspects of the study.

Compared with the existing literature, this study makes contributions with the findings below: First, the risk spillover effect can transmit from foreign capital markets to the Chinese capital market through foreign trade, investment, and market contagion channels. Second, from China’s accession to WTO in 2007, the openness of the Chinese capital market strengthened the risk spillover effect from the foreign capital market on the Chinese capital market gradually and the dynamic correlation between them also ascended, but the strengthening degree varied with different geographical locations. Third, the risk spillover effect began to weaken from 2007 to 2019 because of the increased maturity and independence of the Chinese capital market, it may even have a spillover effect on overseas markets in turn. Fourth, the risk spillover effect would have a certain degree rise when a global emergency like COVID-19 occurred in 2020. Fifth, the capital markets of regions or countries that have frequent trade and convenient capital exchange with China such as Hong Kong, Singapore, and Japan tend to have a more obvious spillover effect on the Chinese capital market than other developed capital markets, which agrees with the viewpoint of shock from trade perspective (Bastos Citation2020).

The above findings reveal that the Chinese capital market is becoming more mature and independent, and the risk spillover effect from the foreign capital market through foreign trade, investment, and market contagion on the Chinese capital market begins to weaken. But the capital markets of developed regions close to China still have an obvious spillover effect on the Chinese capital market, because they have frequent trade and convenient capital exchange with China. Based on these findings, investors would consider the transmission factors when investing to better assess the potential risk spillover effect from foreign markets, and market regulators can also design targeted policies to prevent and monitor the risk spillover effect, especially when a global emergency occurs.

The remaining parts of this study are as follow: Section 2 summarizes the relevant literature and points out the contribution of this study. Section 3 analyzes the transmission mechanism of the risk spillover effect from developed capital markets to the Chinese capital market. Section 4 conducts an empirical analysis of the spillover effect and measures the specific direction, degree, and trend of the spillover effect. In the end, section 5 concludes the findings and presents several targeted policy suggestions.

2. Literature review

Since the 1980s, with the increasing co-movement of the global capital market, the risk spillover effect of the capital market has been widely concerned and studied by foreign scholars. Compared with foreign scholars, Chinese scholars started their research later, starting around 2005. However, under the background of the Chinese capital market’s accelerated opening to the outside world, in recent years, domestic research on this aspect has gradually increased. Overview the existing literature, the experts and scholars of domestic and overseas have carried out in-depth studies on the risk spillover effect from the following perspectives:

2.1 Definition of concept of risk spillover effect

At present, there are still differences in the definition of the risk spillover effect in academic circles. From a narrow definition, Bonato, Caporin, and Ranaldo (Citation2013) defined risk spillover as the dependence of a given asset variance on the past covariance and variance of other assets. Shen, Dai, and Luo (Citation2014) extended it to a broader area and believed that the risk spillover effect refers to the risk transmission mechanism of risks among different capital markets. Zhou and Han (Citation2017) explained the risk spillover effect as when one party has a risk, the risk of the other party will significantly increase; He (Citation2019) called the risk spillover effect the fluctuation of return rate caused by asset price differences in different capital markets would be transmitted from the capital market of one country to the capital market of another country. Starting from macroeconomic factors, some scholars argued that the risk spillover effect means that when the capital market of a country fluctuates after a shock to a country, it will impact the capital markets of other countries with economic ties and the correlation between the two capital markets will be significantly strengthened (Forbes and Rigobon Citation2002; Li and Lin Citation2021), which also implies that the fluctuation of capital market in a country in the early stage will have an impact on its own capital market in the current period (Li Citation2020). Li et al. (Citation2021) put forward the concept of risk spillover in a broad sense, that is, the bilateral spillover level of risks when the market goes up and down.

2.2 Study on impact of risk spillover effect

Many scholars have proposed different views on the risk spillover effect of foreign capital markets on other foreign capital markets. Boako and Alagidede (Citation2018) studied the spillover effect of developed stock markets on African stock markets by constructing the Covar-Copula model and calculating the downward CoVaR and stated that the spillover effect was not obvious but there existed both unidirectional and bi-directional causality between some African and developed capital markets. He (Citation2019) measured the spillover effect of the US stock market on the stock markets of ASEAN countries and the time of mutation through the Garch-Copula-Covar model, noting that the effect of the US stock market on ASEAN countries markets is decreasing. Yang (Citation2020) simulated the co-movement of stock markets in countries along the Belt and Road Initiative by constructing a semi-variogram model under the Kriging method and found that there was a certain spillover effect. This effect would become more obvious under the circumstance of a high negative and positive return rate. Papadamou, Kyriazis, and Tzeremes (Citation2019); Li (Citation2020); Liu and Wang (Citation2021) proposed: the frequency of investors’ reactions to negative information is much higher than positive ones, and the impact of negative information on investors’ expectations will last for a long time, that is, the spread of negative events will be more extensive and profound (Baruník and Křehlík Citation2018; Du Citation2020).

When it comes to the research on the risk spillover effect of the overseas markets on the Chinese capital market, some scholars believed that overseas market risks have a great impact on the Chinese capital market and there are certain risk spillover effects, such as Zhao and Ai (Citation2010) analyzed and pointed out that European capital market has an obvious risk spillover effect on the Chinese capital market with the help of Copula-GARCH model; Hu (Citation2012) studied the diffusion of a risk spillover effect from the perspective of extreme risk spillover and found that American stock market had an obvious positive extreme risk spillover effect on the Chinese stock market; Zhao (Citation2020) made an empirical study by using the binary GARCH-BEKK (1,1) model and pointed out that the market of major developed countries would cause an obvious unilateral impact on the Chinese market (Yang Citation2015). On the contrary, some scholars believed that overseas market risks have a limited impact on the Chinese capital market and there is no risk spillover effect. For example, Shi (Citation2018) conducted an empirical test on the reaction of the capital market by collecting data from the S&P 500 index and the CSI 300 index and found that the sentiment of foreign capital markets had a limited impact on the mainland market, mainly because of the lag in the interpretation of information by investors (Li and Li Citation2019). Yu (Citation2019) used the DCC-GARCH model to explore the information transmission between the Chinese and American stock markets and believed that although foreign capital markets would have a certain impact on the Chinese capital markets in the short term through stock re-pricing and psychological expectations, it would have little impact in the long term. Also, some scholars pointed out that the Chinese capital market would have a spillover effect on foreign capital markets. Mata et al. (Citation2021) thought that the Chinese capital market would produce a spillover effect on emerging market economies and Asian economies (He Citation2019), but this effect weakened after COVID-19 occurred (Zhang and Li Citation2022). Zhang and Mao (Citation2022) found that there was an asymmetric spillover effect from the Chinese capital market to the American capital market through exchange rate and gold channels, and it became stronger during the COVID-19 period.

2.3 Research on countermeasures of risk spillover effect

For the impact of risk spillover, many experts put forward countermeasures from multiple perspectives. Yang (Citation2015) and Yang (Citation2020) suggested that relevant departments should pay constant attention to the economic indicators of developed countries, strengthen internal and external risk monitoring and early warning, and carry out international cooperation in supervision. At the same time, a sharing platform for regulatory information and a risk early warning system should be established (Wang Citation2018; Li, Liu, and Lu Citation2020; Wu, Liu, and Ye Citation2021), and departments should regularly issue warnings and take countermeasures to reduce the impact of foreign market risks on the Chinese capital market; Cheng (Citation2016) advised that financial institutions should enhance their ability to cope with risks by reducing leverage ratio and improving their capital use efficiency and risk management level. Qian and Wang (Citation2016), Guan (Citation2017), Zhao (Citation2020), and Sheng et al. (Citation2020) proposed that government departments should strengthen the construction of supervision mechanisms for the capital market through information data collection, monitoring analysis, and abnormal fluctuation management three aspects, orderly open domestic capital market to attract investors and improve its operational efficiency on the basis of effectively controlling market risks (Hu Citation2012; Yu Citation2019; Sobiech Citation2019; Li Citation2020).

Most of the studies above are based on the perspective of the single developed capital market when researching the risk spillover effect on the Chinese capital market that lacks universality, and insufficient attention has been given to the transmission channel of the risk spillover effect from the developed capital market to the Chinese capital market. Also, the specific direction, degree, and trend of risk spillover effect have not been measured when significant events happen like China’s accession to WTO, COVID-19, and so on. This study aims to find the risk spillover effect of representative developed capital markets around the world on the Chinese capital market. The novel point of this study is that it pays attention to questions that how does the risk spillover effect transmit from those developed capital markets to the Chinese capital market and the change of the direction, degree, and trend of the spillover effect before, during, and after China acceded to WTO, COVID-19, and other critical events. This study contributes to the existing literature on the risk spillover effect of developed capital markets on developing capital markets sufficiently.

3. Mechanism analysis of spillover effect of overseas market risks on the Chinese capital market

3.1 Generating spillover effects through foreign trade channels

The stock market is closely bound up with the development level of a country’s real economy and foreign trade (Mata et al. Citation2021). Under the background of increasingly frequent economic and trade exchanges among countries today, the stock market is more affected by foreign trade, thus producing spillover effects. Specifically, according to the supply-demand theory, first, on the demand side, the stock market of a country tends to do well when its economy is booming. At the same time, economic prosperity also means that the domestic demand exceeds the supply, which will facilitate the increase of import demand and foreign trade level, and further promote the economic development of other trading partner countries, promoting the stock market development of other countries (Bastos Citation2020), and thus to have a positive spillover influence on the trading partner country stock markets. On the contrary, when the economy of a country is in a downturn, its import demand would decline, and the level of foreign trade would decrease accordingly, which would have a negative spillover impact on the stock market of trading partners. Secondly, on the supply side, in the context of global economic integration, a country’s stock market would also be affected by commodity prices in foreign trade markets. A country depressed macroeconomic would reduce domestic consumer demand and lead to excess capacity, suppliers have to decrease the product price to attract customers, and under the influence of the market risk contagion effects, the global commodity market’s overall price level would drop corresponding, leading to other countries’ overall economic level fall, and produce negative spillover effects to the stock market of other countries (Liu Citation2022).

As far as China is concerned, since China joined WTO, the export volume has been on the rise every year. As can be seen from , Chinese import and export volume to main trading partners like ASEAN, EU, US, Japan, and South Korea, reached nearly 17 trillion yuan in 2020. This shows that China’s economy is largely dependent on the demand for imports from these economies. Therefore, China’s stock market is highly correlated to the economic development of these economies. Once these trading partners encounter economic difficulties and import demand declines, China’s overall economic development level would also be affected, producing an external impact on the Chinese stock market accordingly.

Table 1. Chinese import and export to major trading partners from 2015 to 2020(unit: 100 million yuan).

3.2 Generating spillover effects through investments abroad channels

Under the environment of global economic integration and financial market opening, a country’s stock market is also vulnerable to cross-border capital flows. In this context, international capital is easier to flow to other countries through direct or indirect investment, especially those countries with low capital movement restrictions (Gulzar et al. Citation2019). When a country’s economy is depressed, foreign investors especially speculators would withdraw funds due to the uncertainty of economic fluctuations, which will exacerbate the liquidity shortage and economic deterioration of the country, and thus directly affect the country’s stock market (Yan, Huang, and Su Citation2019). Especially when the major economies in the world face financial crises, both the scale of investment from other countries and its scale of investment to other economies would shrink. Conversely, prosperous countries attract inflows of foreign capital.

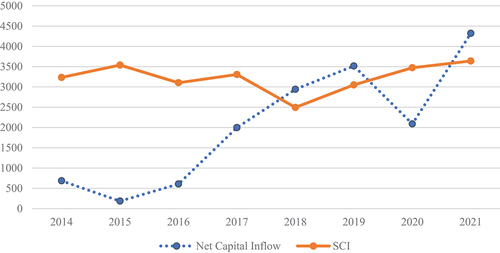

Since the reform and opening up, due to the rapid development of the economy in China, the Chinese capital market has attracted a great number of foreign investment capital, jointly promoting the development of the Chinese capital market. Since 2014, the Chinese capital market has settled the Shanghai-Hong Kong Stock Connect, Shenzhen-Hong Kong Stock Connect, and so on, opening the national capital market to other capital markets and encouraging cross-border capital to enter the Chinese capital market. Till 2021, the north capital, the net capital inflow from the Hong Kong stock market to the mainland market, has reached approximately 430 billion yuan. Both the capital flow and growth rate increased enormously, and the Shanghai Composite Index also showed a synchronous upward trend in the same period as a whole, although the north capital declined to 208 billion in 2020 because of the COVID-19 outbreak, it suddenly bounced back in the next year (see ).

Figure 1. Net capital inflow and stock index changes of shanghai connect from 2014 to 2021 (unit: 100 million yuan).

3.3 Spillover effects through market contagion channels

According to the market contagion theory of behavioral finance, in the case of information asymmetry, there is a convergence effect and herd effect in the market, and the price fluctuation of the stock market of one country will infect the stock market of other countries, especially those more sensitive capital markets. Therefore, when there is a crisis or early warning of a crisis in a country’s stock market, investors will follow other investors to withdraw their money based on panic and negative expectations of the stock market of this country (Baber Citation2020). At the same time, such panic will be transmitted to other countries stock markets through capital flows, resulting in a negative spillover effect, making the stock markets of other countries weaker. On the contrary, a positive spillover effect would exist and lead the stock market of other countries to be strong when the stock market does not face the crisis.

As the Chinese capital market continues to open up, the capital flows become more frequent, and the correlation between China’s economy and that of other countries becomes increasingly stronger, it also means that the spillover effect of major global stock markets such as the United States on the Chinese stock market will become larger and larger. When overseas markets face crises, panic among foreign stock investors is more likely to spread to Chinese investors and prompt them to sell shares, causing the Chinese market to fall. It is worth paying special attention to that, as most domestic investors are retail investors, their investment experiences are relatively insufficient, and they are not rational enough to analyze and process information, so their irrational investment behaviors are more likely to lead to herd effect. When major foreign stock markets have large fluctuations, under the impact of this influence, the spillover effect of foreign market risks on the Chinese stock market would be intensified.

4. Empirical analysis of spillover effect from foreign market risk to the Chinese capital market

4.1 Sample selection and data sources

4.1.1 Sample selection

In the following empirical analysis of the spillover effects of foreign market risks on the Chinese capital market, this paper will mainly select stock price indices in seven countries or regions as the research sample, which is influential in the worldwide market. They are the S&P 500 index (SPX), FTSE100 index (FTSE100), Frankfurt index (DAX), Nikkei 225 index (N225), Hang Seng index (HSI), Singapore Straits index (STI), and China’s Shanghai index (SCI).

4.1.2 Data sources

The data used in this study are all from Wind. In terms of time span, this paper takes the Shanghai Composite Index as the benchmark and selects the daily closing price data of the above seven countries or regions sample index from 19 December 1990, to 29 January 2021, with a period of 31 years. Among them, the data of some days are blank due to different holidays in each stock market. In this paper, the closing price of the previous day is taken as the data of the closing day. After data processing, 7,835 sets of data are obtained. In addition, because the period of sample data is too long, this paper takes China’s accession to WTO as the time node and divides this period into two cycles: before and after China’s accession to WTO. The software used for the empirical analysis is MATLAB.

4.2 Model construction and variable determination

4.2.1 Model selection

It is assumed that the conditional correlation coefficient between two financial time series is time-varying, which can accurately describe the fluctuation relationship between different markets. Compared with ARCH and GARCH models, the DCC-GARCH model has the advantages of less parameter estimation and clear economic significance analysis. The specific expression of this model is shown below:

In Formula 1, is the rate of return,

is the conditional mean, and

is the residuals that obey standard normal distribution. In Formula 2,

is a conditional covariance matrix,

is a diagonal matrix composed of conditional standard deviation (see Formula 3), and

is a matrix composed of dynamic correlation coefficients, where elements are all dynamic correlation coefficients. In Formula 4,

is a symmetric positive determined matrix, and

is the matrix obtained through removing the square root of the diagonal elements of

. In Formula 5,

and

are dynamic correlation coefficients,

>0 (i = 1,2 … p);

>0 (j = 1,2 … q). To be Specific,

is the lag term coefficient of the previous perturbation term, which represents the influence degree of residuals on the variance correlation coefficients of different sequences.

is the lag term coefficient of conditional variance, which represents the influence degree of past volatility correlation on the present volatility correlation. If

, the model is stable and the dynamic correlation is valid.

4.2.2 Variables determination and descriptive statistics

The variable selected in this paper is the return rate of the sample index of the above seven countries or regions. At the same time, to more accurately describe the changes in these stock index returns, this paper chooses the logarithmic sample data to make the data smoother and eliminate the possible heteroscedasticity. The specific formula for the logarithmic return rate is as follows:

In Formula 6, represents the logarithmic return rate of the stock index,

represents the daily closing price of the stock index at time t, and

represents the daily closing price of the previous day.

After the logarithmic processing of each stock price index, the statistical test results of each stock index are listed in below to make the data more intuitive. As can be seen from , first, according to the average logarithmic returns, the average returns of SCI and SPX Index are respectively 0.00045 and 0.00031, which are relatively high. The average return of N225 is 0.00001, which is a relatively low average. The average value of logarithmic stock index returns of the seven sample countries (or regions) is relatively small. Second, from the perspective of the fluctuation of logarithmic return, the rate of return standard deviation of SCI and HSI is larger, which is 0.0217 and 0.0152 respectively, indicating that the fluctuation of the rate of return is larger. While the standard deviation of SPX, FTSE100, and STI is smaller, which means that the volatility of the returns is smaller. Thirdly, from the perspective of skewness and kurtosis, the stock index return distribution of SPX, FTSE100, DAX, N225, and HSI is left-skewness (skewness <0) with negative skewness, while the stock index return distribution of SCI and STI is right-skewness (skewness >0) with positive skewness. Besides, the kurtoses of all index returns are greater than 3, which are generally high and show sharp peaks and thick tails. Finally, the Jarque-Bena statistic test is utilized to test whether the sample data obeys normal distribution. The result shows that the seven statistics are all far greater than the threshold value under the 5% significance level, so the null hypothesis is rejected. Therefore, the rate of return of stock indexes from seven countries (or regions) in the sample does not follow the normal distribution.

Table 2. Rate of return descriptive statistics of stock index from sample seven countries (or regions).

As the previous data does not conform to the normal distribution, it is necessary to normalize the data transformation. we use Box-Cox transformation to adjust the data and get the following conclusions, which can be seen in .

Table 3. Rate of return descriptive statistics of stock index from sample seven countries or regions (the result of the BOX – COX transformation).

4.3 Stationarity test and arch effect test

4.3.1 Stationarity test

Next, we implement the ADF test on the stability of the stock index return series in the sample seven countries (or regions), and the specific results can be seen in . It is notable that the null hypothesis is rejected by the ADF statistics of the stock index return series of all countries (or regions) under the 1% significance level. It indicates that the rate of return of all sample stock indexes is considered to be stable time series with no unit root, and it is possible to conduct subsequent analysis.

Table 4. ADF test results of sample seven countries (or regions) stock index return series.

4.3.2 ARCH effect test

To assure the data validity, the ARCH effect test of the sample logarithmic return series is continued in the following part of this paper. Ljung-Box Q test is used to perform sequence autocorrelation tests on the residual sequence after filtering, and it is found that the seven groups of sample sequence data have a certain degree of autocorrelation. Therefore, the ARCH test is utilized to continue the conditional heteroscedasticity test for the seven residual sequences. The results show that when each sequence lags 1–5 order, the corresponding P-values are extremely small, which indicates that conditional heteroscedasticity exists in all logarithmic return sequences, that is, the ARCH effect exists in all logarithmic return residual sequences. See for specific test results.

Table 5. ARCH effect test.

The above stationary test and ARCH effect test show that these variables can be estimated by the GARCH model and they all meet the requirements of the DCC-GARCH model. Then the DCC-GARCH model is tested, and the results are as follows: P value is 0, and the statistical value is 85.97, which indicates that the test has been passed.

4.4 Model estimation and result analysis

4.4.1 DCC coefficient estimation

In general, there are two steps to obtain DCC coefficients by using the DCC-GARCH model. First, the single variable GARCH(p,q) model is used to estimate the sample sequences and obtain the standardized residual sequence value. Second, the DCC coefficient is estimated by using the obtained standardized residual sequence value, and the dynamic correlation coefficient is obtained. In this article, GARCH(1,1) model, a model that is suitable for the financial time series study in a single variable GARCH(p,q) model, is selected for parameter estimation. After screening the model residuals from each return series, the residuals are standardized by the corresponding conditional standard deviation. They represent the basic independent identically distributed sequences with zero mean and unit variance. Then, DCC coefficients are estimated according to these standardized residual sequences, and the complete estimated results are listed in below.

Table 6. DCC-GARCH model estimation result.

From , it is clear that the parameter estimation results of stock index return from seven sample countries (or regions) are prominent, which are all in line with α+β<1. The general distribution of each index is similar, showing relatively small α and large β. It shows that the current fluctuation of stock index returns has little impact on the market, while the early fluctuation of stock index returns tends to have a greater impact on the market driven by market memory. At the same time, the values of each stock market return α+β are large and close to 1, reflecting that the volatility of the rate of return will last for a long time.

4.4.2 Dynamic correlation coefficient estimation

After estimating the DCC coefficient, the dynamic correlation coefficients among all sample stock index returns can be obtained. The specific results are listed in below.

Table 7. Dynamic correlation coefficient sequence between the return rate of six countries/regions and China’s Shanghai composite index.

It is found that the mean dynamic correlation coefficient between the stock index in China (SCI) and the index in the United States (SPX) is only 0.03, indicating a low correlation. Meanwhile, the mean dynamic correlation coefficient between SCI and FTSE100 and DAX index is 0.07 respectively, which is also relatively low. In addition, the average dynamic correlation coefficient between SCI and N225, and STI is 0.15 and 0.18 respectively, indicating a moderate degree of correlation. It also should be noted that the average dynamic correlation coefficient between HSI and SCI is the largest among the sample indexes, which reaches 0.27, indicating a high degree of correlation.

In order to more accurately describe the trend of the dynamic correlation coefficient between the Chinese stock index and other regional stock indexes, this paper divides the total period of sample data into two cycles: before and after China’s accession to the WTO (2001 year, see below). To begin with, before China acceded to the WTO, the mean dynamic correlation coefficients of the Chinese stock index with that of the United States, Britain, and Germany were nearly zero or negative, showing zero or negative correlation. While the mean dynamic correlation coefficients with Japan, Hong Kong, and Singapore stock indexes were positive, the mean was not big. After China entered into WTO, the mean dynamic correlation coefficient between the Chinese stock index and American, British, and German stock indexes changed from zero or negative to positive, and the mean dynamic correlation coefficients between the Chinese stock index and Japanese, Hong Kong and Singapore stock indexes also increased to a certain extent. This shows that before and after China’s accession to WTO, the dynamic correlations between the Chinese stock market and the stock markets in sample regions had a great change. Before China acceded to WTO, the dynamic correlations between the Chinese market and others were low. However, after China acceded to the WTO, the dynamic positive correlations between the Chinese stock market and the sample region stock markets were significantly enhanced, showing the characteristics of synchronous rise and fall.

Table 8. Comparison of dynamic correlation coefficients before and after China’s accession to WTO.

In general, there are dynamic correlations between the Chinese stock market and the stock markets in sample regions, showing a trend of gradual growth, but the degree of dynamic correlation is different with geographical location. To be specific, the dynamic correlations between the Chinese stock market and the stock markets of Japan, Hong Kong, Singapore, and other geographically close regions are significantly stronger than that of the stock markets in the United States, the United Kingdom, Germany, and other geographically distant regions.

4.4.3 Measurement of risk spillover index

After obtaining the dynamic correlation coefficient, in order to further measure the risk spillover degree of overseas market risks to the Chinese stock market, this article constructed the dynamic spillover index of stock markets in sample seven countries (or regions) by adopting the generalized variance decomposition method (Diebold and Yilmaz Citation2012) and using Matlab software to write relevant algorithms. The specific methods are shown below:

First, create an n-variable Var (p) model with stable covariance and a lag time of p.

In Formula 7, =(x1,t, … , XN,t)’,

is the N*N coefficient matrix, and

is the white noise. Since this model has a relatively stable covariance, Formula 7 can be converted to the form of a moving average:

Where A0 is the N*N unit matrix (when i < 0, ).

Next, Formula 10 is used to measure the impact of the jth variable part on the prediction error variance of the ith variable, and the generalized variance decomposition is got.

In Formula 10, is the impact of the jth variable on the ith variable,

is the standard error of the ith variable prediction error, and ej represents the N × 1 vector.

We use the dynamic risk spillover index constructed above to measure the direction and size of the risk spillover effect among the stock markets of sample seven countries (or regions), so as to obtain the risk spillover effect indices of the stock markets of China and other sample six countries (or regions), as shown in .

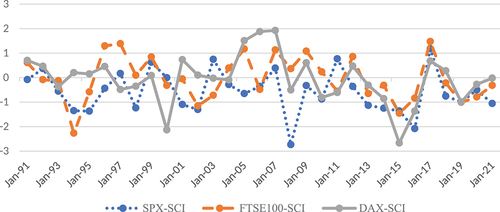

Figure 2. Risk spillover indices of US, Britain, and Germany stock markets to the Chinese stock market.

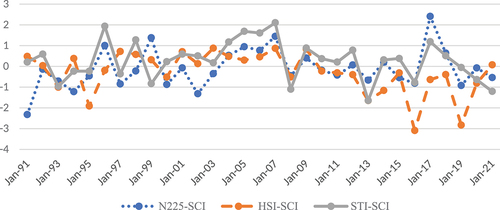

Figure 3. Risk spillover indices of Japan, Singapore, and Hong Kong Stock markets to the Chinese stock market.

First, we may see the risk spillover index of the U.S., U.K., and German stock markets to Chinese stock markets (see ). Before China acceded to the WTO, the average risk spillover index of these three markets on China’s stock market is negative, indicating that foreign market fluctuations have little influence on the Chinese stock market. But this phenomenon changed after China acceded to the WTO, and the impact of foreign stock market fluctuations on the Chinese stock market has significantly expanded. Of particular concern is that in the early years of China’s accession to the WTO (2001–2007), the risk spillover index average rose rapidly to 0.18. However, from 2007 to 2019, the period after the subprime crisis and before COVID-19, the influence of stock market fluctuations in major developed countries like the United States, United Kingdom, and Germany on the Chinese stock market began to weaken significantly, although the risk spillover index surged greatly in 2017 because of the launch of Shenzhen-Hong Kong Stock Connect, it continued to decrease later, indicating that the impact of market fluctuations in these countries on the Chinese capital market showed a significant downward trend. After the outbreak of COVID-19, the risk spillover index existed in certain recovery, but the average index is still negative, revealing the limited effect of the risk spillover effect from three countries on the Chinese capital market under the COVID-19 background. Secondly, we may see the risk spillover index of stock markets in Japan, Singapore, and Hong Kong to the Chinese stock market (see ). The impact of the three regions on the Chinese stock market is similar to that of the United States, United Kingdom, and Germany, just less volatile than the three regions. Especially from 2007 to 2019, the influence of all three regions on the Chinese stock market decreased but was still greater than the influence of the United States, United Kingdom, and Germany. After the COVID-19 outbreak, the influence also showed a certain recovering trend, but the average index is still negative.

4.4.4 Analysis of empirical results

The empirical analysis above shows that after China acceded to the WTO, the dynamic correlations between the Chinese stock market and major stock markets in the world have risen year by year, and individual countries show different trends, which are mainly affected by the influence of foreign trade and investment. First of all, from the perspective of foreign trade, the trade between a country and other countries would increase their economic relations, and the stock market, as a barometer of a country’s economy, will be greatly affected by the macro economy. Before China joined the WTO, its trade volume was relatively low due to the general frequency of trade exchanges with the United States, United Kingdom, Germany, Japan, Singapore, and other regions. Therefore, the dynamic correlations between the Chinese stock market and the foreign stock market during this period were correspondingly low. Nevertheless, this phenomenon changed greatly after China acceded to the WTO, the economic and trade exchanges between China and these regions rose sharply and showed a trend of gradual rapid growth, which enhanced the spillover effect of capital markets in these regions on the Chinese capital market. Among them, Hong Kong, Singapore, and Japan have the obvious spillover effect on the Chinese capital market, mainly because these regions are highly dependent on the Chinese economy and the economic and trade ties are relatively close, thus strengthening the linkage between the capital markets.

Secondly, from the perspective of foreign investment, the inflow of cross-border capital would increase the linkage between the capital market of a country and other capital markets. From the establishment of the Chinese stock market in the 1990s to the beginning of this century, the dynamic correlations between the Chinese stock market and the stock markets in developed countries were low due to the low openness of the Chinese capital market. With the increased size of the Chinese capital market and the improvement of relevant mechanisms, the opening-up of the Chinese capital market has been significantly strengthened in the past decade. The opening of the Shanghai-Hong Kong Stock Connect in 2014 and Shenzhen-Hong Kong Stock Connect in 2016 has further expanded the degree of opening-up of the Chinese capital market. The inflow of foreign capital has greatly enhanced the dynamic correlations and spillover effect of the capital markets in the U.S., U.K., Germany, Japan, Hong Kong, Singapore, and other regions on the Chinese capital market. In addition, the convenience of capital exchange will also strengthen the correlation between capital markets. Compared with the European and American capital markets, the capital flow in the capital markets of Japan, Singapore, and Hong Kong is more convenient to flow to the capital market of China. Therefore, the dynamic correlations between these three regions and the Chinese capital market are particularly strong.

At the same time, from the calculation results of the risk spillover effect index, the risk spillover effect of six sample regions on the Chinese mainland market experienced a process from weak to strong before and after China’s accession to the WTO, but it began to weaken gradually after 2007 to 2019. This is mainly a result of the increased correlation between the Chinese market and foreign markets after China acceded to the WTO. However, the economic growth in US, UK, Germany, and Japan has been slowing since 2007, due to the shock of the financial crisis. During this period, the macroeconomic environment of the Chinese market was better, and its securities market was developing very rapidly, the market regulation means of the Chinese government has become more mature too, so the market was relatively independent, and it may even have a spillover effect on foreign markets in turn. After the outbreak of COVID-19 in 2020, the risk spillover effect from capital markets of developed countries existed for certain recovery, mainly because the global pandemic emergency would strengthen the correlation between capital markets and increase the risk spillover effect, but the entire affecting degree is limited.

5. Conclusion and policy suggestions

5.1 Main conclusion

According to the above formation mechanism and empirical analysis of the risk spillover effect of the foreign market on the Chinese capital market, this article tries to draw the following basic conclusions:

First of all, before China acceded to WTO, the dynamic correlations between the Chinese stock market and the stock markets in developed regions were low, and the risk spillover effect of the capital markets in developed regions on the Chinese capital market was not obvious. However, after China acceded to WTO, the dynamic correlations between the Chinese stock market and the stock markets in developed regions have greatly improved, and the average dynamic correlation coefficients are greater than 0. It indicates that with the continuous improvement of the openness of capital markets in developing countries such as the Chinese capital market, the dynamic correlation between domestic and foreign markets is rising, and the risk spillover effect of foreign capital market on the Chinese capital market is also gradually increasing, but the strengthening degree varies with different geographical locations. Although the stock markets of developed regions close to China, like Singapore, Japan, and Hong Kong, are not the major output party of global market risk spillover effect as the stock markets in Europe and America, their spillover effect on the Chinese stock market is greater than that of developed regions stock market far from China.

Second, from the calculation results of the risk spillover effect index, the risk spillover effect of the six sample regions on the Chinese mainland market experienced a process from weak to strong before and after China’s accession to the WTO. But after 2007 to 2019, with the continuous improvement of the Chinese macro economy and the rapid growth of its capital market, the risk spillover effect of foreign markets on the Chinese capital market has gradually weakened. The risk spillover effect of the Chinese capital market to foreign markets is emerging and gradually increasing. This also reveals that the size of the risk spillover effect of the overseas market on domestic capital markets in developing countries is closely related to the development level of the domestic macroeconomy and the scale of the capital market. When a global emergency happened like the outbreak of COVID-19 in 2020, the correlation between capital markets would be strengthened and the risk spillover effect from developed capital markets would recover but the degree is limited.

Third, changes in macroeconomic factors such as foreign trade and investment would strengthen the relationship between the two regional capital markets’ correlation, leading to changes in the capital market risk spillover effect. Therefore, if the risk spillover effect cannot be effectively contained in time, it will react on the whole national economy and increase its impact on the whole society and economy in developing countries.

For capital market regulators and investors, the findings of this article are absolutely meaningful. For developing capital market regulators, knowing the way that the risk spillover effect transmits from foreign markets to the domestic capital market is beneficial to design targeted policies to monitor and prevent potential risk. For investors, when they invest, the understanding of the risk spillover effect transmission channel may help them to consider macro factors like foreign trade and investment to assess the potential risk spillover effect degree. However, there are several limitations that can be improved in future research. First, this study only researched capital markets of seven countries or regions, more developed capital markets in other countries or regions can be considered in future research. Second, in this study, the main research object is the Chinese capital market, other developing capital markets can also be researched and the clue of research on the spillover effect from the Chinese capital market to other developing capital markets is provided.

5.2 Policy recommendations

The above theoretical research and empirical analysis show that with the development of global economic and financial integration and greater openness of the Chinese capital market, cross-border capital impact on the Chinese capital market is also growing. Particularly, with the development of the Chinese financial market’s comprehensive opening to the outside world, the dynamic correlations between domestic and foreign markets will also increasingly significant. Therefore, it is overwhelmingly significant for the sustainable and healthy development of the Chinese capital market to timely and effectively control the risk spillover effect from foreign markets and minimize it as much as possible. On account of the empirical results, this paper puts forward the following suggestions from policymakers and investors:

To build a new pattern of development with both domestic and international circulation, and make the Chinese economy and capital market bigger and stronger. Given the risk spillover effect size of foreign market on the domestic capital market is closely related to the domestic macroeconomic development situation and the strength of the capital market, therefore, under the background of the comprehensive opening of the Chinese financial market to the outside world, China should actively change its economic development strategy, and make the Chinese economy and capital market bigger and stronger. After the tremendous influence of the financial crisis in 2007 and the COVID-19 pandemic in 2020, the current international political and economic situation has undergone great changes. Trade protectionism and anti-globalization have exacerbated the uncertainty of the global economy and the volatility of the capital market. In this context, it is necessary for China to get rid of the traditional great cycle mode of over-dependence on western countries’ foreign trade exports, shift from dependence on foreign trade development to a development strategy based on domestic demand and supplemented by foreign trade, and actively promote the transformation of its economy to a new domestic and international cycle mode to promote the sustained and stable development of Chinese economy. At the same time, the Chinese government should go ahead with expanding the scale of the Chinese capital market, improving the level of supervision over the capital market, and enhancing the market’s ability to resist risks.

Reasonably control the opening pace of the Chinese capital market and strengthen the monitoring of cross-border speculative capital. For the last few years, under the background of the rapid rise in the Chinese economy, the Chinese capital market has also gained rapid development. However, compared with the capital market of developed countries, the Chinese capital market is still an emerging market with immature development and the level of market supervision needs to be further improved. Therefore, while pursuing the speed of opening up, China also needs to keep a watchful eye on the potential risks, such as the introduction of short-term speculative capital would increase the volatility of the capital market and the malicious short-selling of the Chinese market by foreign capital. The Chinese government should strengthen the monitoring of the flow scale and channels of cross-border speculative capital, particularly strengthening the monitoring of cross-border funds such as Shanghai-Hong Kong Stock Connect and Shenzhen-Hong Kong Stock Connect, improve the construction of liquidity risk early warning systems of cross-border speculative capital, and further improve relevant laws and regulations.

Give priority to opening domestic financial institutions and encourage them to go global. Compared with mature foreign financial institutions, Chinese local financial institutions have some shortcomings such as a weak ability to resist risks and poor market competitiveness. After the opening of financial institutions such as securities and trust companies to the outside world, the entry of foreign head institutions will squeeze the market share and development space of local institutions to a certain extent. At the same time, the profit-seeking characteristics of foreign financial institutions will also aggravate the volatility of the domestic capital market, making the risk spillover effect more obvious. Therefore, domestic financial institutions should be given priority in opening up, so that they can explore and learn from the experience of mature foreign institutions in the overseas market, and quickly improve the anti-risk ability and comprehensive competitiveness of local financial institutions.

Improve the level of investors and effectively avoid risks. Due to a large number of retail investors in the Chinese capital market, these retail investors generally have disadvantages such as a lack of investment experience, poor understanding of investment concepts, and weak ability to resist risks. Against the backdrop of the increasing openness of the Chinese capital market and increasingly significant risk spillover effect, it is necessary for individual investors to cultivate correct investment concepts, rationally choose investment products, construct reasonable investment portfolios, and effectively disperse risks.

Acknowledgments

Except for four authors, this research received no contribution from any other individuals.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Correction Statement

This article has been corrected with minor changes. These changes do not impact the academic content of the article.

Additional information

Funding

Notes on contributors

Xinhui Zhou

Dr. Xinhui Zhou is an associate professor of Finance at the Shanghai Lixin College of Accounting and Finance. She received Ph.D. from Xi 'an Jiaotong University. Her research fields include capital markets and macroeconomic policy, private finance, and so on.

Yuzhe Li

Mr. Yuzhe Li is a student at the City University of Hong Kong. He received M.S. from the City University of Hong Kong and B.S. from Liaoning University. His research interests include trade economy and capital market.

Bing Chen

Dr. Bing Chen is a professor of Finance at the Shanghai Lixin College of Accounting and Finance. He received Ph.D. from Fudan University. His research interests include financial stability, financial management, and so on.

Huadong Jiang

Dr. Huadong Jiang is a professor of Finance at the Shanghai Lixin College of Accounting and Finance. He received Ph.D. from Nankai University. His research areas are law and corporate finance, and digital finance.

References

- Alkan, B., and S. Çiçek. 2020. “Spillover Effect in Financial Markets in Turkey.” Central Bank Review 20 (2): 53–64. doi:10.1016/j.cbrev.2020.02.003.

- Baber, H. 2020. “Spillover Effect of COVID-19 on the Global Economy.” Transnational Marketing Journal 8 (2): 177–196. doi:10.33182/tmj.v8i2.1067.

- Baruník, J., and T. Křehlík. 2018. “Measuring the Frequency Dynamics of Financial Connectedness and Systemic Risk.” Journal of Financial Econometrics 16 (2): 271–296. doi:10.1093/jjfinec/nby001.

- Bastos, P. 2020. “Exposure of Belt and Road Economies to China Trade Shocks.” Journal of Development Economics 145 (3): 1–14. doi:10.1016/j.jdeveco.2020.102474.

- Boako, G., and P. Alagidede. 2018. “Systemic Risks Spillovers and Interdependence Among Stock Markets: International Evidence with Covar-Copulas.” South African Journal of Economics 86 (1): 82–112. doi:10.1111/saje.12182.

- Bonato, M., M. Caporin, and A. Ranaldo. 2013. “Risk Spillovers in International Equity Portfolios.” Journal of Empirical Finance 24: 121–137. doi:10.1016/j.jempfin.2013.09.005.

- Cheng, B. 2016. “Research on the Spillover Effects of Chinese Listed Commercial Banks’ Systemic Risk—A Method Based on Copula-CoVaR.” Master Thesis, Hebei University.

- Diebold, F. X., and K. Yilmaz. 2012. “Better to Give Than to Receive: Predictive Directional Measurement of Volatility Spillovers.” International Journal of Forecasting 28 (1): 57–66. doi:10.1016/j.ijforecast.2011.02.006.

- Du, S. X. 2020. “Research on the Co-movement of Major International Stock Markets before and after the Stock Market Crash.” Master Thesis, Guilin University of Technology.

- Forbes, K. J., and R. Rigobon. 2002. “No Contagion, Only Interdependence: Measuring Stock Market Comovements.” The Journal of Finance 57 (5): 2223–2261. doi:10.1111/0022-1082.00494.

- Guan, T. Y. 2017. “The Study on Finance Firewall System of China in The Trend of Mixed-Operation.” Master Thesis, Hunan University.

- Gulzar, S., G. M. Kayani, H. Xiaofeng, U. Ayub, and A. Rafique. 2019. “Financial Cointegration and Spillover Effect of Global Financial Crisis: A Study of Emerging Asian Financial Markets.” Economic Research-Ekonomska Istraživanja 32 (1): 187–218. doi:10.1080/1331677X.2018.1550001.

- He, Z. Y. 2019. “A Comparative Study of the Spillover Effects of Sino-US Stock Markets on Stock Markets in ASEAN Countries.” Master Thesis, Zhejiang University of Finance and Economics.

- Hu, H. 2012. “A △Covar Measurement Method Based on Time-varying Parametric Copula.” Master Thesis, Zhejiang Gongshang University.

- Li, J. Y. 2020. “A Study on the Dynamic Spillover Effects of Stock Markets in Typical Countries along the Belt and Road.” Master Thesis, Jilin University.

- Li, Z. L., and L. Li. 2019. “Research on the Spillover Effect of the New Round of Monetary Policy Adjustment of the Federal Reserve on Chinese Capital Market.” New Finance 30 (5): 24–28.

- Li, Y. J., and X. R. Lin. 2021. “Risk Contagion Effect and Influencing Factors Between Shanghai Shenzhen 300 Shares Index Futures and Spot Market.” Journal of Financial Development Research 40 (1): 69–77. doi:10.19647/j.cnki.37-1462/f.2021.01.010.

- Li, Z. W., S. N. Liu, X. F. Li, and B. L. Wang. 2021. “Generalized Dynamic Risk Spillover Between Internet Finance and Traditional Finance—an Empirical Study Based on Copula-ARMA-GARCH-CoVar.” Systems Engineering 39 (1): 01–17.

- Li, Z., Q. Liu, and Y. C. Lu. 2020. “A Study of Sovereign Debt Risk Cross-Country Spillover: New Evidence from the Frequency Domain.” Journal of Financial Research 63 (9): 59–77.

- Liu, X. X. 2022. “Study on the Correlation of Gold Price Under Economic Cycle.” Gold 43 (6): 1–6. doi:10.11792/hj20220601.

- Liu, G. Y., and Q. M. Wang. 2021. “The Research on the Linkage of Stock Markets Along the Belt and Road Initiative.” Journal of Shandong Technology and Business University 35 (1): 68–78+102. doi:10.3969/j.issn.1672-5956.2021.01.009.

- Mata, M. N., M. N. Razali, S. R. Bentes, and I. Vieira. 2021. “Volatility Spillover Effect of Pan-Asia’s Property Portfolio Markets.” Mathematics 9 (6): 1–21. doi:10.3390/math9121418.

- Papadamou, S., N. A. Kyriazis, and P. G. Tzeremes. 2019. “Spillover Effects of US QE and QE Tapering on African and Middle Eastern Stock Indices.” Journal of Risk and Financial Management 12 (2): 57. doi:10.3390/jrfm12020057.

- Qian, X. X., and W. A. Wang. 2016. “Research on the Linkage Effect of RMB Exchange Rate Fluctuations, Short-Term International Capital Flows and Stock Price in the Process of Financial Liberalization.” International Economics and Trade Research 32 (12): 95–108. doi:10.13687/j.cnki.gjjmts.2016.12.007.

- Shen, Y., S. W. Dai, and X. Luo. 2014. “The Measure of Systematic Risk Spillover Effect in China’s Financial Sector—study Based on the GARCH-Copula-CoVar Model.” Modern Economic Science 36 (6): 30–38.

- Sheng, S. C., C. H. Zhang, W. S. Peng, X. J. Zhang, and L. Q. Zhang. 2020. “China’s Financial Situation and Risk Warning.” International economic review 28 (6): 9–21+4.

- Shi, Y. 2018. “The Transmission of Overreaction Effect among International Capital Market –A Research on Chinese Stock Index Market.” Master thesis, Capital University of Economics and Business.

- Sobiech, I. 2019. “Remittances, Finance and Growth: Does Financial Development Foster the Impact of Remittances on Economic Growth?” World Development 113 (C): 44–59. doi:10.1016/j.worlddev.2018.08.016.

- Wang, Q. 2018. “Research on Systematic Risk of Listed Financial Institutions in China – Based on the Angle of Relevance.” Master Thesis, Shandong University of Finance and Economics.

- Wu, S. J., X. G. Liu, and G. A. Ye. 2021. “A Comparative Study on Macro Prudential Management and Capital Control of Cross-Border Capital Flows.” South China Finance 42 (1): 68–79.

- Yan, J. J., Y. Huang, and Y. H. Su. 2019. “Research on Macro-Prudential Management of Cross-Border Flow of Speculative Funds.” Southwest Finance 40 (8): 3–10.

- Yang, Y. 2015. “Spillover Effect of Developed Capital Market on Chinese Stock Market: An Empirical Study Based on the Three-Factor AR-Egarch Model.” Financial Development Review 6 (2): 142–151.

- Yang, J. 2020. “Research on the Correlation of Stock Markets of ‘Belt and Road Initiatives’ Countries from the Perspective of Trade Spatial Network Correlation.” Master Thesis, Shanghai Normal University.

- Yu, S. 2019. “Research on the Linkage between China and the US Stock Market under the Stock Market Cycle.” Master Thesis, Capital University of Economics and Business.

- Zhang, Y. M., S. S. Ding, and H. L. Shi. 2022. “The Impact of COVID‐19 on the Interdependence Between US and Chinese Oil Futures Markets.” Journal of Future Markets 42 (4): 1–12. doi:10.1002/fut.22326.

- Zhang, K. Q., and Y. B. Li. 2022. “Global Spillover Effect of Economic Policy Uncertainty and Stock Market Volatility.” Finance & Economics 66 (7): 1–16.

- Zhang, Y. M., and J. Y. Mao. 2022. “COVID-19′s Impact on the Spillover Effect Across the Chinese and U.S. Stock Markets.” Finance Research Letters 47 (4): 1–11. doi:10.1016/j.frl.2022.102684.

- Zhao, J. N. 2020. “A Comparative Study on the Stock Market Linkage between China and Other Brics Countries and Major Developed Countries.” Master thesis, Jilin University.

- Zhao, X. L., and Y. F. Ai. 2010. “Copula-GARCH Based Financial Market Time-Varying Correlation Analysis.” Scientific Decision Making 17 (6): 58–63.

- Zhou, A. M., and F. Han. 2017. “Research on the Risk Spillovers Between Stock and Exchange Rate Markets – Based on the Garch-TVP Copula-Covar Model.” Financial Markets 34 (11): 54–64. doi:10.16475/j.cnki.1006-1029.2017.11.006.