?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This study investigates the pass-through of exchange rate shocks to different aggregate prices in China. The baseline analysis is carried out with vector autoregressive models incorporating a distribution chain of pricing, and various modifications are examined for robustness. The central results show an appreciation of the local currency tends to suppress domestic inflation at the early production stages, although the pass-through effect only amounts to a moderate degree for consumer prices. As the contribution of external factors to the persistently low inflation environment mostly has been modest, the paper suggests that the monetary authority can contribute to the permanent component of low exchange rate pass-through to domestic inflation, by continually conducting a credible and efficient stable-inflation policy.

1. Introduction

The effect of exchange rate fluctuations on domestic prices can be referred to as the exchange rate pass-through relationship, which has generated extensive research interests in international economics. The degree of exchange rate pass-through may affect inflation dynamics and the transmission mechanism of monetary policy in general.

Table 1. Variable description and data source

Table 2. Summary statistics of variables

The aim of this study is to provide empirical evidence on the degree of the aggregate pass-through to different prices in China. We exploit the information in the time series to investigate the macroeconomic pass-through of exchange rates to domestic inflation by the integrated framework and test the robustness of the results with respect to model specifications. The estimated outcome may be of direct relevance for policy design.

Exchange rate fluctuations can affect consumer prices directly, as the prices of imported finished goods for final consumption will generally increase after a reduction in the purchasing power of the underlying national currency. The consumer prices may also be indirectly affected by exchange rate shocks, due to upward pressure on the prices of commodity products, imposing by the higher imported input costs and producer’s efforts to retain the markup. Over the decades, Chinese imports of primary commodities have grown dramatically and are having major influence on the respective supplies and demands for many of these commodities.

It is therefore reasonable to consider the intermediate goods that undergo non-traded production and distribution processes prior to final consumption in the transmission mechanism. It may be interesting to see the extent to which these production or distribution channels may dampen the impact of exchange rate shocks on consumer prices. Lower degree of pass-through may be caused by market participant’s lower perceived persistence of cost fluctuations.

Nonetheless, the dynamics of the overall exchange rate pass-through depends on a variety of factors, including the share of imports in the consumption basket, the bargaining power of suppliers, the cost of price adjustments, and the perceptions of the duration or stickiness of the currency revaluation. The prices of service products tend to be less affected by the direct pass-through effects, given that these products are mostly produced domestically.

Another potential transmission channel in which exchange rate fluctuations can influence domestic prices is through changes in the demand composition and aggregate demand levels at each stage of the distribution chain. For instance, a decrease in the value of the yuan will increase both the domestic and foreign demand for goods produced in China. The depreciation will inevitably lead to the expenditure switching effect, when imported goods become more expensive from the perspective of domestic consumers, this will increase their preference for domestically produced substitutes. Moreover, foreign demand for export goods from China will increase, as they appear to be less expensive from the perspective of foreign buyers. Higher domestic and foreign demands for these goods produced in China may then reinforce the global competitiveness of relevant industries.

Nevertheless, the degree of exchange rate pass-through may be limited by the firms’ high tolerance to costs variance and inability to pass on cost increases downstream in a globally integrating economy characterized by a high-competition environment.

The empirical study on the effects of exchange rate pass-through to aggregate prices at various distribution stages may have important macroeconomic implications. Based on the estimation outcome, the direct impact of exchange rate pass-through on domestic consumer inflation tends to be modest, and evidently less than the degree of pass-through to input inflation and producer inflation. The robustness of the central results to model specification is high in general, and the sensitivity analysis provides further evidence that the exchange rate pass-through to consumer prices is far from complete.

By pinning down the size of pass-through to the price variables, this study contributes to the evaluation of domestic macroeconomic effects of exchange rate fluctuations and may help improve the countercyclical policy design (i.e., enabling more efficiently designed expansionary policies or stimulus measures against economic disturbances or uncertainties surrounding external factors). This paper may also contribute to further investigation on the effectiveness of monetary policy at stabilizing growth and domestic inflation. The evidence supports the hypothesis that low and stable inflation environment can be reinforced by a highly credible and efficient monetary policy, which tend to have a dampening impact on the firm’s inclination to pass on cost fluctuations.

2. Background & literature

Studies regarding the exchange rate pass-through in the literature of international economics have already become extensive. From an industrial organization perspective, the early work of Dornbusch (Citation1987) stated that an incomplete pass-through to prices results from producers’ partial adjustment of their own profit margins in response to an exchange rate shock in an imperfect competition framework.

According to such theoretical basis, market and industry structure, the degree of competition, and the pricing behavior of producers are the main factors affecting the responsiveness of aggregate price adjustments. Many other researchers have then attempted to explain the incomplete pass-through by investigating firms’ response to changes in input costs in oligopolistic markets (Atkeson & Burstein, Citation2008; Bergin & Feenstra, Citation2001).

Indeed, pass-through to consumer prices should be imperfect considering the production or distribution processes. In the case where imports serve as production inputs, imported goods account for only a partial cost of the final product sold to consumers, and the rest of the production may integrate many non-tradable factors, such as marketing, retailing, and distribution services. In addition, many factors associated with the trading and production processes can attenuate the influence of exchange rate fluctuations on domestic prices, including trade distortions, transportation and distribution costs, cross-border production strategy by multinational companies and the use of currency hedging may also play a role.

A strand in the literature has taken into consideration the impact of exchange rate fluctuations on the prices of intermediate goods in the production or distribution processes before arriving at the end consumers (McCarthy, Citation2007; Stulz, Citation2007). They provide consistent evidence that the impact of exchange rate shocks on consumer prices is dampened along the production or distribution channels.

Nevertheless, the measurement of the exchange rate pass-through could be a critical parameter for monitoring and forecasting the real output growth and domestic inflation in emerging economies which tend to severely affect by external shocks (Devereux, Lane, & Xu, Citation2006).

The investigation on exchange rate pass-through in China has generated some research interests over the years due to the country’s continuous integration to the global economy and the series of reforms of the exchange rate system. To begin with, a managed float system was first introduced for evaluating domestic currency against a basket of major trading currencies in 2005. A strong pass-through effect on the prices of agriculture products imported from the United States to China is found in the early application by Ju and Yang (Citation2010); this study advocated the need for government trade policy intervention to support domestic agriculture industries when the local currency appreciates.

Based on an autoregressive distributed lag model, Zhu and Liu (Citation2012) confirms negative relationship between yuan appreciation and domestic inflation. Jiang and Kim (Citation2013) capture a higher degree of exchange rate pass-through to producer price than to retail price in China by a structural vector autoregression, price indexes respond rather quickly to exchange rate fluctuations in their model. At the industry level, Hong and Zhang (Citation2016) estimated the exchange rate pass-through to import prices of raw materials, their results revealed significant divergence, in which higher degree of pass-through tends to be found for basic metal and chemical products than to the textiles and non-metallic mineral products, so the average transmission to import prices for industries must be incomplete.

Over the years, the central bank of China has been investing efforts to integrate the local currency into the global monetary and financial system by gradually moving towards a more flexible and market-based currency regime. In the fall of 2015, the International Monetary Fund (IMF) included the yuan in the special drawing rights (SDR) basket in addition to the US dollar, the euro, the Japanese yen, and the British pound. The reserve currency status of the yuan reflects substantial progress behind the exchange rate system reforms and recognizes the currency’s rising international credibility. The openness and continuous integration of China’s financial market then becomes increasingly crucial and relevant to policy authorities and other market participants around the globe.

Under the current managed float regime, the People’s Bank of China (PBC) takes the previous day’s closing price of CNY/USD as a starting point, and it evaluates yuan’s movements against some major currencies set by the China Foreign Exchange Rate Trade SystemFootnote1 (CFETS) since the previous fixing, and subsequently determine the current day’s fixing. In addition, the exchange rate is only allowed to free float within a band of 2% on either side of a fix reference rate.

Besides the aforementioned mechanism, the PBC has reportedly employing a “countercyclical factor” for the fixing management. In such setting, commercial banks and other institutional currency trading participants in a panel submit quotes that the CFETS adopts to set the central parity, which effectively constitutes an additional factor for CNY/USD fixing. According to the monetary authority, the rationale for the additional measure as a countercyclical management is that severe exchange rate fluctuations during a day shall not be validated in the next fixing, when the underlying economic fundamentals do not warrant it (PBC, Citation2017).

The impossible trinity argues that exchange rate stability, domestic monetary policy independence, and free capital movements cannot be achieved simultaneously in an open economy. China’s transformation into a market-based economy is associated with the development of a modernized monetary policy framework. Financial liberalization and greater exchange rate flexibility over the years impose challenges on the policy authority for efficiently maintaining price stability. This empirical study aims to deepen our understanding of the transmission mechanism of exchange rate pass-through and may contribute to the policy operations.

3. Model and methodology

A model of pricing along a distribution chain is developed to examine the pass-through of the exchange rate movements to domestic inflation at various distribution stages.Footnote2 The chain structure is of research interest as China’s economy has a large and complete manufacturing sector that intakes substantial imported raw materials.

The empirical model features a mechanism in which exchange rate shocks can be transmitted to input prices, thereby affecting the cost of production and consumer prices in turn. In addition to the influence from the exchange rate dynamics, inflation at each stage of the distribution chain is affected by shocks from the domestic economic activity and monetary policy. The baseline case involves a vector of six variables consisting of output (y), money supply (m), nominal effective exchange rate (ex), and the price indexes along the distribution chain, namely input prices (ipi), producer prices (ppi) and consumer prices (cpi).

Price variation at each stage in period t is assumed to be affected by several macroeconomic factors, other than its own shock. The first component is the expected price level at that stage based on the information available at the end of period t-1. The second is the output shock at that stage to control for the domestic economic activity. The third factor affecting each stage of production is the monetary policy shock, which also affects exchange rate and domestic inflation. The fourth component involves price shocks from each of the previous production stages of the chain. The final factor is the exchange rate shock. The macroeconomic effects of exchange rate shock on price indexes form the central theme of this empirical analysis.

The own price shocks at each stage capture a portion of a stage’s price variation that cannot be explained by available information from period t-1, in addition to contemporaneous information regarding domestic activity, money supply, exchange rate, and price shocks at all previous stages of the distribution cycle. These own price shocks represent changes in the pricing power and markups of firms at each production stage.

The model contains two features from the pricing stage. First, the input price shocks in the model can affect the domestic consumer inflation both directly and indirectly through their effects on producer cost and inflation. Second, the pricing chain does not allow contemporaneous feedback. The price indexes along the distribution chain in period t can be presented as follows:

where ,

,

are shocks of output, monetary policy, and exchange rate respectively;

,

,

are shocks of input prices, producer prices, and consumer prices; and

is the expectation of a current period variable x based on available information set at the end of period t-1. We assume that these conditional expectations can be projected by the lag variables in the system.

EquationEquation (1)(1)

(1) to (3) imply a recursive vector autoregressive framework. To complete the empirical model, we incorporate additional assumptions to identify shocks from the aggregate output, money supply, and exchange rate. Specifically, we assume that real activity has a one-period delay response to price and financial signals, such as money supply and exchange rate movements, while the exchange rate, as a financial asset price, responds immediately to real and monetary innovations.

As Taylor (Citation1995) suggested long ago, short-term fluctuations of the exchange rates mostly cannot be explained by macroeconomic fundamentals, such that a simple model can be sufficient to identify shocks from the exchange rate. The identifying assumption for the exchange rate pass-through is that price indexes are affected by exchange rate shocks in the contemporaneous period. As such, the price indexes are ordered last in the system, this is not simply an ordering issue, but an identification condition that is essential to isolate the pass-through effects.

Assume that firms are less likely to change their output decisions in response to unexpected changes in financial signals within a relatively short time interval due to adjustment cost and planning inertia. Further assume the monetary authority has a discretionary control over its policy instruments and that pricing information are unobservable in the current period. Therefore, the policy reaction is based on available information in period t-1. These aspects of the model can be represented in the following manner:

Generally, the recursive scheme implies that the identified shocks contemporaneously affect their corresponding variables and those variables that are ordered at those later stages, but they have no contemporaneous impact on variables that are ordered before. The standard reduced form representation of the VAR(p) model can be expressed as follows:

where contains k endogenous variables for the sample period t, and p is the number of lags in the system of equations.

denotes the matrix capturing all deterministic variables, such as the intercepts and the exogenous policy dummy variables. In the baseline model,

reduces to a standard vector of constants. The

are k by k coefficient matrices and

is a k-dimensional vector containing the error terms. The primitive system of the baseline model is presented as follows:

A, B, and represent square coefficient matrices of the order k.

is the k variable vector of constants. The structural disturbance

can be composed to obtain the reduced form error terms:

Identification of the system can be achieved with knowledge of the k by k matrices A and B. An exact identification requires the number of restrictions on the A and B matrices to be equal to . The cross-sectionally uncorrelated pure structural shocks have zero covariances. Thus, matrix B is diagonal, yielding

restrictions. Diagonal elements of matrix A are equal to 1, representing the coefficients of dependent variables in Equationequation (8)

(8)

(8) .

Together with the analysis presented in Equationequations (1)(1)

(1) to (6), matrix A is lower triangular with diagonal elements set to 1, leading to several restrictions equal to

. The total number of retractions of the two matrices is

, thus the necessary condition for exact identification is satisfied. The restrictions can be imposed following a Cholesky decomposition scheme as follows:

To incorporate the information of the long-run relationship regarding the inherent non-stationarity of the variables in the simultaneous framework, the empirical analysis can be further extended to apply a VECM. The reduced form representation in Equationequation (7)(7)

(7) can evolve to the vector error correction system of equations in the first-differenced term as follows:

where and

. Information on both long-run and short-run relationships can be extracted from this system. The coefficient estimates in

captures short-run transitory information due to previous shocks in the variables, and long-run information is retained in the coefficient estimates of

which can be decomposed as

. The cointegrating vectors are presented by

, capturing the long-run equilibrium relationships among the different levels of variables. The loading matrix

measures the variables’ adjustment to restore the system or the average speed of convergence from deviation towards equilibrium in the long run.

4. Data

The data set comprises monthly observations from January 2011 to September 2021. Using observations of monthly frequency appears to be appropriate for this empirical study, as this frequency better accounts for real-world price stickiness, and the short-term dynamics of the pass-through mechanism can be particularly informative to the monetary authority when developing inflation forecasts.

This study aims to provide insight on the transmission of exchange rate (EX) fluctuations to the domestic prices (IPI, PPI, CPI) at the input, producer, and consumer stages, respectively. These price variables are thus at the center of the empirical analysis. Assuming prices are set along the production channel, exchange rate shocks that are initially passed to the costs of imported materials can lead to reactions at all stages of a distribution chain of pricing.

To complete the model framework, there exist two additional portions. Industrial production index (Y) is included as a proxy to control for the aggregate economic activity. The impact of monetary policy is captured by a key interest rate variable (M).

Financial liberalization and greater exchange rate flexibility requires a modern, market-based monetary policy framework to efficiently achieve price stability. Over the years, the People’s Bank of China has evidently de-emphasized the importance of the historical quantity-based policy tools (IMF, Citation2016). Alongside the market-oriented interest rate reform and rapid development in the financial markets, monetary policy stance has been conveyed through the interest rate channel, and the seven-day pledged repo rate appears to have become the targeted short-term money market rate, which can serve as the policy proxy.

To better capture exchange rate movements and their impact, the exchange rate variable is taken as the monthly average of the nominal effective exchange rate index versus 60 economies (2010 = 100) calculated by the Bank for International Settlements (BIS). An increase indicates an appreciation of the country’s currency against the broad basket of currencies. The effective exchange rate index has time-varying weights to take into consideration of China’s growing significance represented by trade flow, and adjustments has been made by the BIS to account for the mainland’s indirect trade with the rest of the world via Hong Kong.

As an alteration to the model specification, the oil price variable appears in the sensitivity analysis as a proxy variable for the imported input prices. This creates the alternative VEC model. The series were drawn from the Federal Reserve Economic Data (FRED) and were extracted originally as monthly global price of the WTI Crude, USD per Barrel. Since we are interested in the effect of imported input prices, oil price data are translated into the local currency of the underlying economy, as in work of Beirne and Bijsterbosch (Citation2011) for their empirical estimation focused on the European Union’s member countries.

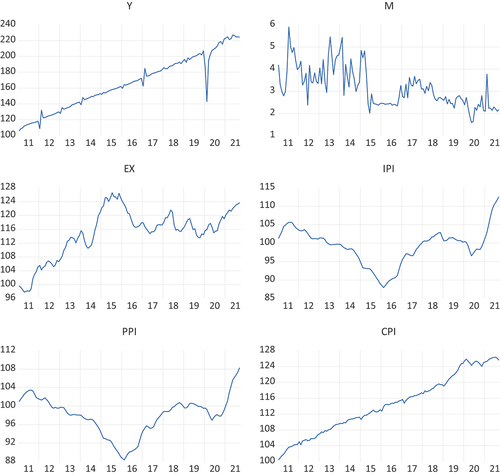

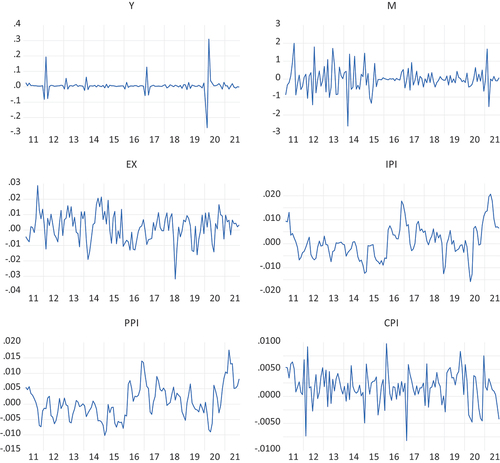

present the descriptive overview and statistical behavior of the series, while the level and log-difference plots of all the endogenous variables in the baseline model are shown in , respectively. All series, excluding the nominal effective exchange rate and the short-term policy rate, are seasonally adjusted by means of the Census X-13 procedure.

Figure 1. Variables in levels.

Figure 2. Variables in log-difference.

Output tends to grow at a relatively stable pace over the years, until the COVID-19 pandemic emerged around the end of 2019. The deep recession quickly recedes however, leaving a sharp “V” in the level plot. The output growth after the pandemic shock appears to be more volatile, which may be caused by increased uncertainty arising from some macro-level factors.

The benchmark interest rate exhibits a generally downward trend. This is expected as monetary policy has remained supportive to partially offset the impact of deleveraging efforts over the years, especially in financial-sector regulation and supervision, housing policies, and local government financing.

After a series of reforms toward a market-based system, the strength in yuan exchange rate now better reflects the diverging economic situations between home and abroad. Related disturbances in the balance of payments and global FX markets also play important role in its valuation. A trend has emerged that the yuan appreciating against the basket of foreign currencies, as the nominal effective exchange rate continual to surge after the pandemic shock. The yuan is climbing to its strongest levels in six years against the currencies of the country’s trading partners. Over the years though, the nominal effective exchange rate of yuan moved in both directions and had two-way volatility, while generally remained stable.

China is a major importer of industrial inputs with a large and complete manufacturing sector. As such, a strong yuan may help suppress production prices due to the lower costs of imported materials. Under the highly uncertain global economic environment, the price indexes at the input and the producer stages are both growing at the fastest pace over the decades, adding to the global pressure. The jump in imported raw material prices, especially in some energy-intensive products lead to a surge in the domestic producer prices. Nonetheless, there is little evidence yet that the upstream sectors can pass on rising costs to the downstream, the relatively stable inflation regime for the final consumption goods warrants further investigation.

Despite the various patterns found in the time series plots, the Augmented Dickey–Fuller (ADF) test results presented in suggest that all endogenous variables are stationary after log-differenced.

Table 3. ADF unit root test results

For the optimal lag length, displays the estimated results of the likelihood ratio (LR) tests along with various information criteria on the model specifications. Since information criteria are essentially indications of the goodness of fit of the alternatives, we consider them as complements to the LR test. Therefore, the number of lags is set at three according to the LR indicator for both baseline and alternative models.

Table 4. Lag order selection criteria

Based on the results of the Johansen cointegration tests in , at least one cointegrating relationship can be detected for all model specifications. Consequently, a VEC model can be employed to incorporate the long-run information contained in the data of interests.

Table 5. Johansen co-integration test results

5. Baseline results

5.1. VAR

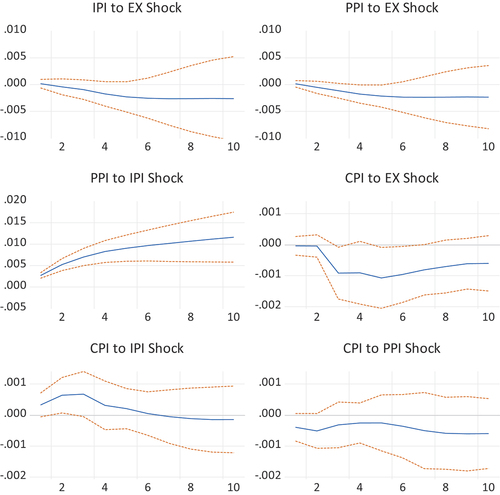

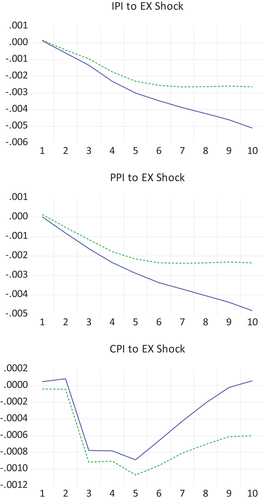

The estimation exercise begins by submitting the baseline variables to the vector autoregression model to evaluate the short-run dynamics of the pass-through effect. The reduced form residuals from the VAR are orthogonalized using a Cholesky decomposition to identify the structural shocks. To account for the non-stationarity in the data and to facilitate the interpretation of results, all series enter the model as log differences. tracks some accumulated impulse response functions with two standard error confidence bands for the price indexes.

Figure 3. Accumulated impulse responses (VAR).

In vector autoregressive estimation, the degree of pass-through is quantified by means of impulse response functions. As the system is shocked by a structural innovation of exchange rate, the estimated pass-through of this shock to prices can be observed. The impulses of the log-differenced variables are normalized, and the accumulated responses approximate percentage changes in the underlying variable following a one standard deviation shock in a foreign variable. The accumulated responses of relevant price indexes to exchange rate shocks may be interpreted as the pass-through value.

For instance, the pass-through of the exchange rate appreciation shock amounts to an approximately 0.25% drop for both input prices and producer prices. The responses at these stages appear to be borderline significant and gradually increasing till the sixth month, and insignificantly different from zero thereafter. These price variables tend to have a quick reaction to exchange rate shocks.

For the pass-through of exchange rate to consumer prices, the effect takes place at an even faster pace, although the degree of the response tends to be relatively moderate. After 5 months, the pass-through amounts to about 0.11%. The estimated response functions of the price variables appear to follow the inverse hump-shaped pattern, as the increments were mainly concentrated in the first six months. Nonetheless, relatively strong pass-through effects can be found for the prices at the production stages compare to that at the final consumption stage.

It is worth noting that the prices at producer and consumer stages have an immediate positive response to a shock from input prices. This presents an indirect transmission channel, in which an appreciation of domestic currency reduces input costs, suppressing producer and consumer inflation downstream. The results show modest response of consumer prices to the shocks from prior stages, implying high levels of costs absorption along the pricing chain. The response of consumer prices to a shock at the producer stage has the wrong sign, although the estimates are not significantly different from zero. This anomaly in the outcome disappears when a VEC model is applied, as further describe below.

5.2. VECM

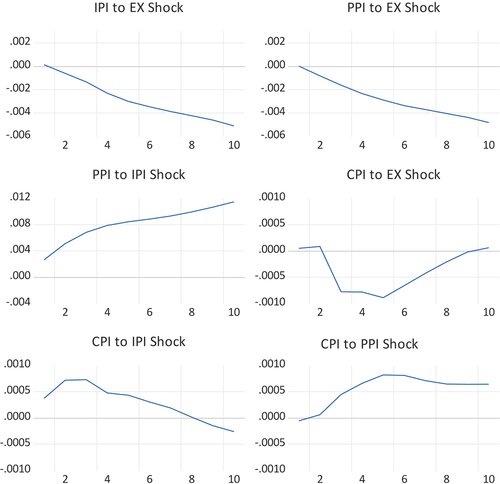

Since all the baseline endogenous variables are stationary as log differences and a cointegration relationship can be established, our analysis is extended by submitting the log-transformed series into the vector error correction model. Concerning the equilibrium relationship, the augmented error correcting term incorporates long-run information contained in the underlying data set.

The estimated results are presented in , showing that all price indexes respond negatively to an appreciation shock in the exchange rate as expected. Furthermore, the response of consumer prices to the producer price shock now has the correct (positive) sign, in line with common perceptions concerning pricing behavior along a distribution chain.

Figure 4. Impulse responses (baseline VECM).

Compared to the VAR case however, the pass-through effect to the price indexes at the input and producer stages evidently becomes stronger. This can be clearly seen also in , which combines the impulse response functions to facilitate comparison. Nevertheless, the exchange rate pass-through to consumer prices appears to be only temporary, as the effect gradually vanished over longer horizons, implying some sort of self-correcting mechanism inherent in consumer pricing to the soared costs of imported consumption goods. The correction in consumer pricing may stem from the substitution effect from competing domestic suppliers of similar goods.

Figure 5. Comparison of the impulse responses (dotted line: VAR and solid line: baseline VEC).

Overall, a standardized appreciation shock tends to produce a stronger pass-through effect for input prices and producer prices and a weaker effect for consumer prices comparing to that of the vector autoregressive estimation. The divergence in the accumulated responses appear to be concentrated over the longer horizons after the 5th months, as the momentum of the pass-through effect on input and producer prices continues. Specifically, at the ending horizon, the pass-through effects of exchange rate to input prices and producer prices approximate to 0.5%, which is almost twice as large when compared with the VAR case.

A relatively weak yuan increases production costs of domestic producers who, seeking to sustain certain level of profit margins, may allocate the burden to consumers to some extent by raising prices of the final commodities. This indirect transmission of exchange rate shocks to the final consumer prices continues to work, since prices at the later stages are found to respond positively to shocks from earlier stages, and that currency depreciation lifts the costs on input material and intermediate goods. Although the response of consumer prices to producer shock appears to be persistent, the pass-through of input price to CPI is temporary and even turn negative at the later horizon, pointing towards the existence of offsetting forces. The estimation outcome generally suggests that the cost absorption level along the distribution chain remains high.

The unrestricted cointegrating coefficients () and the adjustment coefficients (

) are presented in . The VEC model has the cointegration vector built into the specification so that it restricts the long-run behavior of the endogenous variables to converge to their cointegrating relationships while allowing for adjustment dynamics in the short term. The loading matrix measures the average speed of convergence towards long-run equilibrium. These coefficients show the variables’ reaction to disequilibrium in the spread. In particular, the last three rows of the loading matrix show the amount needed to restore the system to equilibrium for the price variables at each stage.

Table 6. Bai-Perron multiple breakpoint tests results

Table 7. Comparison of the impulse responses (results multiplied by 100 to show percentage changes)

Table 8. Granger causality/block exogeneity wald tests results

Table 9. Unresticted long-run and loading matrix

6. Sensitivity analysis

Empirically estimated results may be sensitive to the specification of the underlying model. By submitting the baseline model to several modifications, we can examine the robustness of the estimated pass-through effects. First, the input price variable (ipi) in the baseline model is substituted by the oil price (op) as a proxy for the imported input price, to form an alternative model. Second, the matrix of deterministic variables, namely from Equationequation (7)

(7)

(7) , include both the intercepts and an exogenous policy dummy variable (pfxr), to incorporate the effects of potential policy intervention in the FX market.

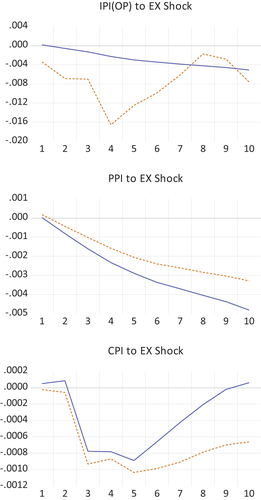

The first scenario is initiated by substituting the input price index by the oil price to control for the costs of imported inputs. The lag length for the alternative model is set equal to 3, following the LR test results in (b). In the Johansen cointegration rank tests, both trace and max eigenvalue test statistics point to the existence of one cointegrating relationship of the endogenous variables.

The estimated results of exchange rate pass-through for the alternative model are distinguishable to that of the baseline model by an inspection of . Obviously, the estimated response for imported input goods is fast and strong compared with the response for the price index of general input goods. Nevertheless, the difference appears to be temporary and mostly concentrated within the early horizons, as the degree of pass-through exceeds 1.6% at the 4th month, and gradually falls back down afterwards.

Figure 6. Comparison of the impulse responses (dotted line: oil price VEC and solid line: baseline VEC).

For the producer prices, the degree of pass-through tends to be stronger than that in the VAR case but less than that in the baseline VEC case. The degree of pass-through to consumer prices is comparable to the baseline VEC version in the early horizons. However, the effect tends to be more persistent and remains at the higher level after the 5th horizon, resembling that in the VAR case.

In the second scenario, the policy intervention dummy (pfxr) is introduced to control for the monetary authority’s temporary intervention over the market value of yuan, and such policy actions may be captured by the dramatic changes in the national foreign exchange reserve series. The policy dummy variable is set equal to one for the periods in which a break is detected by the Bai-Perron multiple break point tests, and it is set to zero for all other periods. The policy dummy is augmented to the baseline estimation as an exogenous variable. provides a summary of the periods for which a break occurs as detected in the foreign exchange reserve data.

Based on the test results, policy interventions seem to be concentrated in the early years of the sample prior to the end of 2016. Here may provide evidence that the series of reforms toward a market-based exchange rate system has shifted monetary authority’s behavior, enabling the exchange rate to better reflect the economic fundamentals and facilitate external adjustment. This may also imply that exchange rate enters a relatively stable regime, and less intervention is needed to reduce the degree of uncertainty in the economy.

To see how sensitive the baseline results are under the presence of policy intervention, a comparison of the impulse responses between the baseline VEC model and the counterpart that is augmented by the exogenous policy dummy variable can be reviewed in . Overall, the impact brought by the exogenous policy dummy to our baseline model estimates are modest for the most part. This sensitivity exercise may also contribute to the confirmation of the central results and the robustness of the study, as the degree of exchange rate pass-through to the price variable at each stage are rather similar across the horizons.

presents a summary of the results for the block exogeneity Wald tests performed on the baseline version of the VAR and VEC models. These results revealed some statistically significant unidirectional relations, favoring the idea that the underlying exchange rate pass-through mechanism describes the behavior of the segment price indexes, and thus the distribution chain structure is a reasonable consideration in the model setup.

The price indexes proved to be endogenous, as they were caused, in the Granger sense, by the exchange rate at the significance level of 10% for both the VAR and VEC estimates in the baseline case. They were also being caused by the combined effect of the remaining variables at the 1% significant level. These results led to the conclusion that exchange rate plays the driving role of the price indexes, as the information contained in the series helps to explain pricing movements along the distribution chain.

7. Discussion

This section aims to shed more light on the economic and practical implications of the empirical results. The study found some key features of the pass-through mechanisms in the integrated framework and examined the robustness of the results with respect to model specifications. This may provide useful information to policy authorities and other market participants, especially in the global economic environment hit by heightened uncertainty. In general, the results suggest that a local currency appreciation help suppressing domestic inflation at all distribution stages, especially for input prices and producer prices over the longer horizons. Nonetheless, the pass-through effect on consumer prices tends to be weak and transitory.

Aided by low labor costs, technically skilled workforce, good infrastructure and a vast domestic market, the underlying economy has become the world’s manufacturing powerhouse in recent decades. Set aside any effects generating from competing domestic goods, if exchange rate fluctuations were to pass down the distribution chain, the direct effect on the consumer prices would be bounded by the ratio of final consumption expenditures on import goods in the private sector, as the consumer price index is weighted by expenditures.

The establishment of a large and complete manufacturing sector with comparably high international competitiveness may limit the proportion of domestic private sector’s total expenditure on the imported final goods. Indeed, the estimated response of the consumer prices to the exchange rate shock tends to be much smaller than that of the prices at the earlier stages.

Please recall the shocks at each stage are that portion of a stage’s inflation that cannot be explained based on information with a period lag alongside contemporaneous information about domestic aggregate output, monetary policy stance, exchange rates, and inflation at previous stages of the distribution cycle. These shocks can therefore be considered as changes in the pricing strategy or markups of firms at these stages, and the estimated results show moderate response of consumer inflation to costs fluctuations at the previous stages.

The presence of increasing global competition and a large domestic manufacturing sector may also suggest that firms operate in a highly competitive business environment. This implies continuous downward pressure on makeups and higher aggregate multifactor productivity, due to marginal exits of low-productivity firms. Facing this kind of high-level competition, the firms’ ability to pass on cost surges downstream is limited. Moreover, by striving to achieve cost efficiency, productivity advancements may enhance the capacity of firms to absorb cost fluctuations related to exchange rate volatility.

The high level of commitment of the monetary authority to keep inflation low may also lead to the weak and transitory pass-through to consumer prices. In the prolonged low inflation environment, firms become less likely to pass on price shocks to the downstream markets, due to the expectation of countervailing monetary policy interventions and other potential inflation stabilizing efforts by the government. We may implicitly assume that the persistence of aggregate inflation is a driving factor for the perceived persistence of cost changes.

The nominal effective exchange rate of the yuan has surged after the pandemic shock. In particular, the yuan has strengthened to three-year highs against the U.S. dollar, generating concerns about the competitiveness of the export sector, which remains a major contributor to aggregate economic growth. Severe external shocks can make planning difficult for manufacturers that routinely make large, long-term capital expenditures whose returns are crucial determinants of financial performance.

To overcome the heightened uncertainties in global economic environment, the policymakers in China give high priority to balance efforts to lower financial stability risks with economic growth. Under the ongoing deleveraging strategy which keeps macroprudential, fiscal, and housing policies tight at the national level, it may be sensible to maintain an accommodative monetary policy stance to prevent an overtightening of financial conditions.

The robustness of our central results is high to different model specifications. Based on the estimation, the contribution of external factors to the persistently low inflation environment mostly has been modest. Hence, the moderate degree of pass-through to consumer inflation may have come from presumably more permanent factors, implying that the monetary authority has been successful in stabilizing inflation expectations.

The key implication that may concerned the policy authority is that the fluctuations in exchange rates and commodity prices resulting from possible continued turmoil related to the pandemic, especially in emerging markets, will have modest effects on domestic consumer inflation given that macroeconomic policies stay on the right track.

8. Conclusion

This paper has examined the pass-through of exchange rate shocks to domestic inflation at different stages of the distribution cycle. Moving towards further financial liberalization and greater exchange rate flexibility, the modern, market-based monetary policy framework should prioritize the maintenance of domestic price stability. The transmission mechanism of external factors can evolve to take a substantive role in the determination of both real activity and inflation and will become increasingly informative for policy design.

Based on our results, an appreciation shock of the yuan is estimated to suppress domestic inflation. Nevertheless, the impulse response of consumer prices to exchange rate shock tends to be modest and transitory, while relatively high degree of pass-through can be found at the earlier stages of the distribution chain. This is reinforced by the incorporation of long-run information using the error correction estimation methodology. The sensitivity analysis confirms the central findings, as the baseline results hold qualitatively and quantitatively for the most part in the various robustness exercises.

As observations at monthly frequency can better account for price stickiness in the real world, the results uncover short-term pass-through dynamics that can be of interests to policy authorities and other market participants. There is an indication that the production or distribution processes exert a dampening effect on consumer inflation associated with production cost fluctuations. This may imply that the firms tend to have strong tolerance for cost absorption and low bargaining power when striving to maintain global competitiveness.

The underlying economy has a large and complete manufacturing sector that may have reduced the import share of final goods in the total private sector expenditure, and the related competitive business environment tends to increase the stickiness of pricing in reaction to fluctuations in the costs of imported input materials. The analysis further implies that the monetary authority can contribute to the permanent component of low exchange rate pass-through to domestic inflation, by continually conducting a credible and efficient stable-inflation policy.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Jia Ji

Dr. Ji holds a PhD from the Graduate Center, City University of New York; and a BCom from the Sauder School of Business, University of British Columbia. His research interests cover financial economics, international finance, and fiscal-monetary policy coordination.

Notes

1 This is an affiliate of the People’s Bank of China.

2 The chain structure of the model is similar to that of McCarthy (Citation2007).

References

- Atkeson, A., & Burstein, A. (2008). Pricing-to-market, trade costs, and international relative prices. American Economic Review, 98(5), 1998–2031.

- Beirne, J., & Bijsterbosch, M. (2011). Exchange rate pass-through in central and Eastern European EU member states. Journal of Policy Modeling, 33(2), 241–254.

- Bergin, P. R., & Feenstra, R. C. (2001). Pricing-to-market, staggered contracts, and real exchange rate persistence. Journal of International Economics, 54(2), 333–359.

- Devereux, M. B., Lane, P. R., & Xu, J. (2006). Exchange rates and monetary policy in emerging market economies. Economic Journal, 116(511), 478–506.

- Dornbusch, R. (1987). Exchange rates and prices. American Economic Review, 77, 93-–106.

- Hong, P., & Zhang, F. (2016). Exchange rate pass-through into china’s import prices: An empirical analysis based on ARDL model. Open Journal of Social Sciences, 4(4), 13–22.

- IMF. (2016). The people’s Republic of China: Selected issues. International Monetary Fund Country Report, 16(271), 12–15.

- Jiang, J., & Kim, D. (2013). Exchange rate pass-through to inflation in China. Economic Modelling, 33, 900–912.

- Ju, R., & Yang, R. (2010). Risk of exchange rate pass-through and adaptive strategies of land-intensive products in China: Taking import products from U.S. as an example. Agriculture & Agricultural Science Procedia, 1, 170–178.

- McCarthy, J. (2007). Pass-through of exchange rates and import prices to domestic inflation in some industrialized economies. Eastern Economic Journal, 33(4), 511–537.

- PBC. (2017). “The ‘countercyclical factor’ introduced into the RMB exchange-rate regime by the foreign-exchange self-disciplinary mechanism.” Monetary Policy Report Quarter, 23–26

- Stulz, J. (2007). Exchange rate Pass-through in Switzerland: Evidence from vector autoregressions. Swiss National Bank Economic Studies, 4, 1–32.

- Taylor, M. P. (1995). The economics of exchange rates. Journal of Economic Literature, 33, 13–47.

- Zhu, J., & Liu, L. (2012). RMB exchange rate, domestic aggregate demand and inflation—Based on the exchange rate transmission theory. Economic Theory and Business Management, 3, 80–89.