?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Capital controls may adversely affect international trade. This study aims to demonstrate the usefulness of capital controls for reducing macroeconomic volatilities and then mitigating their negative effects on international trade. Using quarterly data, we applied a dynamic panel approach to a sample of 26 countries over the period 2010–2020. By diversifying the estimation techniques and using different capital control indexes, our results show that a capital control policy supports international trade and reduces exchange rate and interest differentials volatilities. The impact of capital controls is asymmetric when considering the role of financial development, the cyclical behavior of capital controls, and the simultaneous use of macroprudential policies. This study raises some policy implications, particularly, the necessary coordination and adjustment of the macroeconomic policies and the importance of targeting long-lasting controls when applying a restrictive policy.

1. Introduction

The international exchange of goods and services becomes easier with more capital account liberalization and engenders transnational financial flows. However, capital flow restrictions have been frequently employed to secure countries from grave financial panics and disrupt capital flow movements. Capital controls have important implications for international trade as a main tool of the restrictive policy (Lai, Citation2021). This study examines these implications and highlights the role of some channels through which capital controls affect trade.

Few studies have dealt with the relationship between capital controls and international trade. Giovannini and Park (Citation1989, Citation1992) were among the first to study this relationship. They examined the economic consequences of the prohibition of households holding foreign currencies and the limitation on the amount of money enterprises require to finance their international trade transactions. Tamirisa (Citation1998) used a gravity model to analyze the impact of capital and foreign exchange controls; their results show an adverse effect of these controls on bilateral exports. Wei and Zhang (Citation2007) examined how capital controls, especially foreign exchange controls, directly affect international trade. They found a tariff increase of about 11%–14%, implying a reduction in international trade due to these controls. Manova (Citation2008) focused on the differences in the industry financial vulnerability and found that equity market liberalization asymmetrically supports the exports of the most financially vulnerable industries. Lai, Wang, and Xu (Citation2021) found that the effect of capital controls on trade depends on the level of external financing and the tangibility of traded assets.

Feldstein (Citation1985) notes that “the world of commerce is complex.” International trade is affected by several interrelated determinants, which have complicated linkages. Recent debates on capital controls have raised the fact that these restrictions can potentially reduce capital flows to the countries that impose them, but can also have consequences on international trade, outside the economy in which they are imposed. Studies dealing with this issue are rare, if not nonexistent, making it difficult to identify the main channels through which capital controls affect trade.

Our investigation identified three distinct channels that could potentially mitigate or aggravate the effects of capital control actions on international trade.Footnote1 First, the exchange rate is a key variable in international trade and affects both imports and exports (Cushman, Citation1983; Viaene & De Vries, Citation1992). Certainly, any change in the value of currencies will stimulate or constrain commercial and financial transactions of goods and services by affecting relative prices (Houck, Citation1979). To reach exchange rate targets and avoid systemic risk, policymakers use capital controls (Magud, Reinhart, & Rogoff, Citation2011). These controls are also employed to prevent or limit the overheating of the economy and an increased appreciation of the exchange rate caused by massive capital inflows (Ostry et al., Citation2011; Pandey, Pasricha, Patnaik, & Shah, Citation2021). Second, the exchange rate policy is closely related to the monetary policy, which uses the interest rate as its essential instrument. Indeed, the differential of domestic and foreign interest rates is often used in international economics literature as the main determinant of international capital flows (Corsetti & Pesenti, Citation2005; Gong, Wang, & Zou, Citation2017). Capital controls may affect the monetary policy. According to Edwards (Citation1999), after implementing capital controls, interest rate differentials are reduced and tend to disappear gradually, more so than following capital account liberalization events.

Furthermore, the interest rate differentials affect the cost of capital borrowed from abroad, which raises the cost of international transactions (Soto, Citation1997). Third, both the exchange rate and monetary policies have often been used to deal with unwanted inflation (Bianchi, Melosi, & Rottner, Citation2019; Mankiw & Reis, Citation2003). General inflation has a close relationship within the exchange rates, through which it can affect international trade. Trade policy and cross-border trade are difficult to understand even with low inflation rates; economic principles become more complex with high and chronic inflation. Indeed, high inflation reflects increased changes in the level and allocation of real income domestically and internationally. Likewise, exchange rates, as well as international balance of payments accounts, are often modified due to variations in inflation (Dexter, Levi, & Nault, Citation2005; Stockman, Citation1985). The literature on the impact of globalization on prices suggests that Asian exports are favored due to their low costs, which gives them a significant advantage compared to advanced countries (Auer, Degen, & Fischer, Citation2013). Some studies highlight the harmful effect of capital controls on international trade through inflation volatility. For instance, Grilli and Milesi-Ferretti (Citation1995) suggest that capital controls generate a high inflation rate and tend to lower real interest rates. However, Romer (Citation1993) and Rodrik (Citation1998), among others, disagree with the evidence presented by Grilli and Milesi-Ferretti (Citation1995). Still, there is no consensus about the obvious impact of capital controls on inflation volatility.

Drawing on the above literature, capital controls may operate through exchange rate, interest rate differentials, and inflation rate to affect international trade and contribute to imports and exports. This study hypothesizes that these channels are relevant conduits for capital controls to affect international trade.Footnote2 This indirect impact of capital controls has never been tested empirically. This lack of empirical assessment is surprising, given the important implications these transmission channels have for designing a suitable macroeconomic policy supporting international trade. It has been argued that capital controls stringency has a direct detrimental effect on international trade (Edwards & Ostry, Citation1992; Lai et al., Citation2021). A consequence and relevant area of inquiry is whether these restrictions on capital flows also indirectly affect international trade in addition to their direct effect. This study predicts that the indirect impact of capital controls may be different based on whether the exchange rate, interest rate differentials, and inflation volatilities are mitigated.

The present study contributes to the literature in multiple ways. First, the existing literature on the impact of capital controls on international trade is scant and deals particularly with the direct effect (Lai et al., Citation2021). Our study differs in that we focus on both direct and indirect effects of capital controls, to evaluate how capital control policies mitigate or aggravate the impact of transmission channels on international trade. Second, we extend the existing literature by employing a broader scope data on capital controls, international trade, and related channels that affect international trade. Our data reflect capital control stringency across 26 countries from 2010 to 2020. Unlike most previous studies that consider broad-based measures of capital controls and apply inflow and outflow restrictions indicators on all types of flows, we adopt a new kind of capital controls index. The relevant Financial Accounts Restrictiveness Index is compiled by the IMF’s Monetary and Capital Markets Department, relying on source data of the IMF’s Annual Report on Exchange Arrangements and Exchange Restrictions (AREAER). The widely used indicators, including the Fernández, Klein, Rebucci, Schindler, and Uribe (Citation2016) and Chinn-Ito (Citation2008) indexes, are used for robustness check. Third, the literature has focused mainly on the effects of capital control on exporting countries (Eichengreen, Gullapalli, & Panizza, Citation2011). However, the international trade value is measured for both exports and imports of goods and services. In this study, the bilateral trade flows are considered; we analyze these effects for both exporting and importing countries. Fourth, our paper extends the analysis to some capital control related issues. For instance, during large inflows, policymakers tighten restrictions on capital inflows and reduce them for outflows, and vice versa during tightening periods (Fernández et al., Citation2016). The cyclical behavior of capital controls highlights multiple impacts on international trade according to the type of controls applied, and affects exporters and importers asymmetrically. Furthermore, macroprudential policies aiming for financial system stability can be introduced concurrently with capital controls, and the effects of the two policy tools may therefore be conflated (Bergant, Grigoli, Hansen, & Sandri, Citation2020; Lai et al., Citation2021). We provide evidence of a useful combination between capital controls and macroprudential policies. Finally, we compare the effect of capital controls in countries with developed and less developed financial systems, in accordance with previous findings that show that developed financial systems support capital control actions, which reduce macroeconomic volatility and benefit international trade in those countries (Cooper, Tarullo, & Williamson, Citation1999; Forbes, Citation2007).

The empirical analysis uses a dynamic panel framework to investigate the impact of capital controls on international trade. This study analyzes the behavior of capital controls in economies that vigorously alter these constraints over time. Our empirical approach entails two estimation phases, as in Forbes, Fratzscher, and Straub (Citation2015) and Glick, Guo, and Hutchison (Citation2006). Based on a quarterly dataset of 26 countries covering the period 2010–2020, we regressed two models according to the length of time capital controls were in place.Footnote3 We carried out the baseline model’s estimation with multiple techniques commonly recommended for dynamic panel models. We employed four estimators: the first two estimators of the Generalized Method of Moments (GMM), the difference, and the system GMM. We regressed our models using fixed-effects and random-effects maximum likelihood estimators (MLE). These estimators are based on transforming the likelihood function (Hsiao, Pesaran, & Tahmiscioglu, Citation2002). Our empirical approach considers the abovementioned capital control related issues. We performed multiple panels assessing the cyclical behavior of capital controls and the role of financial development, and we introduced macroprudential policies as a simultaneous restriction policy supporting capital control actions. A common challenge faced in the literature on the impacts of capital controls is the problem of endogeneity, more specifically, that of potential reverse causality (Alam et al., Citation2019; Galati & Moessner, Citation2018). We mitigated the risk of biased estimates due to endogeneity in multiple ways.

The empirical results show a significant negative impact of capital controls on international trade. This finding is consistent with the empirical literature suggesting a direct detrimental effect on international trade. Strangely, the direct effect of capital controls on international trade is different from the indirect effect inferred through interaction terms. The results prove that long-lasting capital controls mitigate the adverse effects of exchange rate and interest rate differential volatilities on international trade. This result is interesting, as while the direct effect of capital controls harms international trade, we provide evidence that such controls can also benefit international trade by mitigating the adverse effects of the three channels.

Furthermore, we found that capital controls affect exporting and importing countries asymmetrically. The findings support an intensification of capital control actions for more developed financial systems. Finally, the results show that the macroprudential policy lessens the extent to which fluctuations of the channels affect international trade. We ensured the results of this study are robust through further conventional indexes of capital controls – those of Fernández et al. (Citation2016) and Chinn-Ito (2008).

The findings of this study point to at least two policy implications. One is that targeted long-lasting capital controls, compared to episodic controls, can have sizeable gains in reducing the adverse effects linked to the volatility of our channel variables. A second policy implication concerns the necessary coordination of policies, domestically and internationally, affecting international trade. Capital controls as a restrictive policy should be appropriately joined by a policy mix (exchange rate and monetary policies) to support international trade (Bhattarai, Mallick, & Yang, Citation2021).

This paper is structured as follows. Section 2 presents the literature review. Section 3 outlines the empirical framework and data used. Section 4 reports our main findings and the interpretation of the results. Section 5 extends the analysis to capital controls related issues and robustness checks. The final section provides the conclusion.

2. Literature review

Capital controls remain a widely discussed issue in macroeconomic policies. Yet, the abundant studies on the effectiveness of capital controls and their impacts on international trade are less debated. Capital controls may act through multiple channels to affect international trade.

One main potential channel is the exchange rate. The theoretical literature has developed multiple evidence of a close causal relationship between changes in exchange rates and international trade. The evidence shows that higher exchange rate volatility leads to an increase in revenue uncertainty, which adversely impacts bilateral trade. Risk aversion and irrecoverable investment in productive capital seem to be the motivators of this increased uncertainty (Cushman, Citation1983; Hooper & Kohlhagen, Citation1978). Due to investors’ risk aversion, a negative correlation between exchange rate volatility and international trade can be assumed (Asteriou, Masatci, & Pılbeam, Citation2016). In contrast, McKenzie (Citation1999), among others, showed a positive impact of exchange rate fluctuations on international trade. Nonetheless, there is no consensus regarding this relationship. The consequences of exchange rate volatility for international trade remain undetermined, and the corresponding literature is mostly inconclusive. The global evidence characterizes the results of this relationship as heterogeneous since findings are dependent on the sample studied, empirical specifications, the proxies for exchange rate and international trade used, and the period of analysis (Steinbach, Citation2021).

A second potential channel of impact is through the interest rate differentials. Many empirical studies examining the surge in capital inflows to emerging economies found that the interest rate differentials is the basic determinant of these flows (Chakraborty, Citation2006; De Gregorio, Edwards, & Valdés, Citation2000; Frankel & Okongwu, Citation1996). Both capital inflows and outflows are seen as an obvious result of trade globalizationFootnote4 (Davis & Van Wincoop, Citation2018). The interest rate differentials may be considered a key variable for developing international trade through its role in the surge of capital flows. This role is also implied by the sticky price assumption of exchange rate determination, as the highest interest rate attracts capital inflows under a floating exchange rate regime (Meese, Citation1984; Obstfeld & Rogoff, Citation1995). Capital control actions may impact international trade via the interest rate differentials (Grilli & Milesi-Ferretti, Citation1995). Forbes (Citation2007) showed that capital flow restrictions increase cost (i.e., a rise in interest rate as a proxy for capital cost) and reduce international commercial transactions. The countries with the least access to international financial markets and which do not benefit from preferential rates would be most affected by these controls. Feldstein (Citation1985) suggested that to balance the supply and demand of funds, an increase in the interest rate can be achieved through private investment reduction and prioritizing capital inflows.

Inflation volatility may affect international trade and is proposed as our third channel. Stockman (Citation1985) suggests that slight changes in the inflation rate cause adverse impact on the direction of trade, and this impact becomes stronger with large shifts in the inflation rate. Capital controls exacerbate the adverse effect of inflation volatility, as they increase the cost of trade by creating additional frictions (Lai et al., Citation2021). Bilateral commercial transactions take a long time to conclude; the extent of these transactions will undoubtedly increase capital costs in surrounding exports and imports. The availability of this capital is still questioned with capital control policies. Likewise, additional costs may be incurred by governments applying administrative charges surrounding the delivery of goods and services, thus increasing the cost of international trade (Chor & Manova, Citation2012). These frictions will increase international trade costs. Grilli and Milesi-Ferretti (Citation1995) showed that capital controls act on the interest rate elasticity of money demand and consequently increase the optimal inflation rate; this effect on the inflation is unrelated to the exchange rate regime pursued – floating or fixed. The authors found that capital controls were correlated with minor real interest rates and increased inflation. Similarly, Romer (Citation1993) suggested that liberalization leads to lower inflation rates. Similarly, Gruben and McLeod (Citation2002) showed that inflation tends to decline in more liberalized economies. Rodrik (Citation1998) overlooked the evidence provided by the abovementioned studies. He suggested that large inflows weaken governments’ attempts to restrain inflation, and there is no evidence that inflation is reduced with more capital account liberalization. Mathieson and McKinnon (Citation1981) considered the role of financial development and endorsed the use of capital controls in less financially developed countries to control inflation.

Finally, our paper relates to a growing body of literature investigating capital control-related issues. For instance, studies searching for optimal capital controls show that controls must be procyclical for inflows and countercyclical for outflows (Benigno, Converse, & Fornaro, Citation2015; Bianchi, Citation2011). Consequently, to ensure more macroeconomic stability, these controls should discourage capital inflows during expansions and encourage them during contractions (Erten, Korinek, & Ocampo, Citation2021; Fernández et al., Citation2016). Capital controls’ cyclical and counter-cyclical behavior should produce asymmetric impacts on exporting and importing countries. A second related topic is the role of financial development in supporting capital control actions (Bush, Citation2019; Binici, Hutchison, & Schindler, Citation2010; Lane and Milesi-Ferretti, Citation2008). For instance, Bush (Citation2019) provides evidence that the level of financial development influences the impact of capital controls. He found that a high level of financial development supports the impact of the restrictive policy; therefore, policymakers need to choose between more financial liberalization or restricted capital account and act through targeted controls. Other studies looked at capital account liberalization instead of capital controls (Chinn & Ito, Citation2008; Eichengreen et al., Citation2011). These studies have highlighted the role of a more developed financial system in the success of the financial liberalization process. Another relevant matter concerns the joint use of macroprudential policies and capital controls. With data available for more than a decade since the 2008 global financial crisis, several recent studies examined the efficiency of restrictive policies in retrospect through a panel data analysis (Frost, Ito, & Van Stralen, Citation2020; Nier et al., Citation2020; Zehri, Citation2022). Many countries, particularly emerging economies, have used capital controls as an effective tool against the surge of capital flows. Those countries have also employed macroprudential policies to target major disequilibrium affecting the global macroeconomic and financial spheres. For instance, Qureshi, Ostry, Ghosh, and Chamon (Citation2011) examined a joint effect of macroprudential policies and capital controls to counter massive inflows and ensure more stability of the financial system. The authors found some overlap between macroprudential policies and capital controls.

The “financial trilemma” – that open capital markets and pegged exchange rates mean a loss of monetary autonomy – is the central focus of the current study. The exchange rate regimes, monetary/macroprudential policy regimes, and capital control policy interact each other and are qualified as the “impossible trinity”. The empirical literature highlights the difficulty of distinguishing the pure effects of capital controls from exchange rate and monetary policy regimes. Besides, some studies found that currency and banking crises have severely affected international trade and should be considered to assess the impact of capital controls. For instance, Nakatani (Citation2018) found that countries with de facto floating exchange rate regimes tend to have a higher probability of a severe currency crisis when they experience an interest rate differential shock. Esaka (Citation2010) found that floating exchange rate regimes significantly increase the probability of a currency crisis compared with pegged ones under capital controls. In addition, the conventional view is that pegged regimes under liberalized capital accounts increase the risk of currency crises (Radelet, Sachs, Cooper, & Bosworth, Citation1998). Recently, Nakatani (Citation2020) found that the effectiveness of macroprudential policy differs significantly across countries with different monetary policy frameworks, exchange rate policies, and capital flow measures. For example, macroprudential policy effectively changes the probability of a banking crisis in countries without capital controls, while it is not so in countries with capital controls. These previous studies have used dummy variables to alleviate the concerns related to monetary/exchange rate/capital controls policy interactions and the impact of crises.

3. Empirical framework and data

3.1. Data and variables

We constructed a quarterly dataset for 26 countries. The sample is composed mostly of emerging economies.Footnote5 These countries were chosen for two main reasons: first, they have floating exchange rate regimes that allow considering the exchange rate volatility; second, they have taken frequent capital control actions (e.g., Chile, Brazil, and Russia) that actively change over time, and such changes enable to highlight the cyclical behavior of capital controls. We take into account the differences in the level of financial development and the adoption of macroprudential policies in these countries; such partition will be useful in the empirical analysis. The analysis period is considered significant for this study, as it follows the 2008 financial crisis, which led to a rapid return to capital controls. Likewise, this period exhibits considerable fluctuations in international trade values (Lai et al., Citation2021).

3.1.1. Capital controls and international trade

The literature on capital controls recognizes multiple limits to finding accurate measures for the stringency of these controls. Previous works have employed de facto, de jure, and mixed indexes (Quinn, Schindler, & Toyoda, Citation2011; Fernández et al., Citation2016; Chinn-Ito, 2008). Unlike most previous studies that considered broad-based measures of capital controls and applied inflow and outflow restrictions indicators on all types of flows, we used an index of controls – denoted CC – developed in 2011 by the Fund’s Monetary and Capital Markets Department of the IMF. The relevant Financial Accounts Restrictiveness Index is based on source data from the IMF’s AREAER. The Financial Account Restrictiveness Index is a broad index obtained by averaging binary (i.e., “open” or “closed”) indexes of barriers in 62 groups of capital account transactions in the AREAERFootnote6 (Nier, Olafsson, Rollinson, & Gelos, Citation2020). The dependent variable of our empirical models (denoted trade) is the value of international trade calculated by the total of exports and imports of goods and services (Amiti & Wakelin, Citation2003). reports the description of all variables used in the empirical specifications.

Table 1. Country sample

Table 2. Description of variables

represents an association between capital control periods and the international trade value (% GDP). The figure corresponds to eight countries in our sample that have significant capital controls experience: Singapore, Egypt, Philippines, Iceland, Brazil, Chile, Thailand, and Turkey. The periods marked in gray correspond to capital control events. These periods are identified by monitoring restrictions to international trade applied by each country, relying on the information in the IMF’s AREAER. We note a reduction in international trade volume during capital control periods for the eight countries. The results in align with the literature showing that capital control actions harm international trade (Giovannini & Park, Citation1989; Tamirisa, Citation1998; Wei & Zhang, Citation2007).

Figure 1. Capital control periods and international trade.

3.1.2. Channels of capital controls

The empirical literature points to the difficulty of identifying the effects of capital controls. On the one hand, these controls do not vary much over time, reducing the power of standard fixed-effects regressions. On the other hand, their level could be correlated with several country-specific factors, exposing a random-effects regression to potential omitted variables. Cerdeiro and Komaromi (Citation2019) argue in favor of identifying the effects of capital controls through interaction effects, by showing in a simple model that capital controls not only affect the unconditional mean of flows, but importantly also the sensitivity of capital to numerous pull and push determinants. This point is usually not exploited in regression models that neglect to consider interactions and assume a cumulative linear impact of capital controls on the degree of capital movements. Following Cerdeiro and Komaromi (Citation2019), we controlled for time-invariant omitted variables at the country level as tightly as possible. In addition, and in order to identify the effects of policies, we included interaction terms to analyze how capital controls interact with macroeconomic fundamentals (channel variables) in affecting international trade.

The literature on the interaction between macroeconomic and restriction policies is relatively vast, and mostly proposes composite indexes for an association between macroeconomics aggregates and financial shocks (Bergant et al., Citation2020; Lai et al., Citation2021; Nier et al., Citation2020; Obstfeld, Ostry, & Qureshi, Citation2019; Zehri Citation2020). We draw on these studies by using three interaction terms between the capital control index and the volatility of some channel variables affecting international trade. Our first channel is the exchange rate volatility (XC); we used the real exchange rate standard deviation, which captures the effective relative price of goods and services. We controlled for the interest rates differentials (RATE) – our second channel – computed as the difference between domestic and international interest rates (Bacchetta, Davenport, & van Wincoop, Citation2021).Footnote7 We also controlled for inflation volatility (INF) – our third channel – calculated as the standard deviation of the Consumer Price Index.

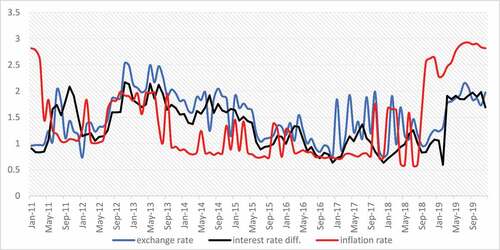

displays the fluctuations of the channel variables during the analysis period.Footnote8 It shows some correlation between exchange rate and interest rate differentials volatilities.Footnote9 In specific periods, the exchange rate and interest rate differentials show a similar pattern, while in others, the movements are in opposite directions. For instance, a distinct pattern can be seen at the end of the period, corresponding to the COVID-19 shock that affected the entire world. Those multiple associations confirm the diversity of correlations found by theoretical and empirical studies on the exchange rate volatility and interest rate differentials linkage. Numerous studies highlight the difficulty of coordinating between the two policies (i.e., policy mix, exchange rate, and monetary policy) to deal with concerning macroeconomic issues. Regarding the inflation rate volatility, shows an increase during the start and end periods. This may be attributed to two international shocks affecting the entire world – the start period following the 2008 global financial crisis, and the end period coinciding with the COVID-19 pandemic.

Figure 2. Channel variables volatilities.

3.1.3. Control variables and instruments

Our empirical models include important control variables that are expected to impact international trade profoundly. The first control variable is the real GDP, a proxy for the country’s economic power. We included the consensus forecast of future GDP growth (FGDP) as a control variable since it mitigates a potential simultaneity problem when “good news” about the economy leads to an appreciation of the exchange rate and affects the exchange rate trade. Wei and Zhang (Citation2007) showed that capital control stringency causes a considerable drop in bilateral trade transactions, similar to a rise in tariffs of about 11% to 14%. We controlled for trade barriers effects by including a simple average of tariff rates (TAR).

Since capital controls are potentially endogenous to other economic policies, we used instrumental variables estimation to isolate exogenous changes in capital controls and their implications for international trade. Relying on the empirical literature, and as suggested by Edwards (Citation2007), the following instruments were used: the current account deficit (CA), the percentage change in terms of trade (TERMS), foreign direct investment relative to the GDP (FDI), and international reserves (IR).

reports descriptive statistics of the model’s variables. The main finding is that capital restrictions change little throughout analysis; the capital controls index CC shows slight changes over time, with a standard deviation of 0.16. High volatilities are the main characteristic of the analysis period. Besides, the dominant aspect that stands out is the large variations of the channel variables and international trade. For the sample countries, on average, the standard deviation of the channel variables is roughly 31.45. The results of confirm the high volatility of the channels displayed in .

Table 3. Summary of statistics

3.2. Baseline setup and methodology

To formally study the links between capital controls and trade, the estimation equation underlying the baseline estimates was adopted from previous studies (e.g., Lai et al., Citation2021; Manova, Citation2013). As in Klein (Citation2012) and Bacchetta et al. (Citation2021), we distinguished between “wall” and “gate” controls.

The empirical analysis used a dynamic panel framework to investigate the effects of capital controls on international trade through the channel variables. Our baseline setup, in which we expand on some capital controls related issues, relates the dependent variable (trade) to exchange rate volatility (XC), interest rate differentials (RATE), inflation volatility (INF), capital control actions (CC), and their interactions. We denote TC the vector of transmission channel variables; TC : {XC; RATE; INF}. Our regressions are based on the two equations for long-lasting controls and episodic controls outlined below:

Long-lasting controls, the “walls” effect of capital controls (levels, CC)

Short-standing controls, the “gates” effect of capital controls (1-quarter change, ΔCC)

Where log (tradei;t) is the dependent variable measured by the total of imports and exports of goods and services in country i at time t. “CC” is the level of capital control index. “Z” denotes the vector of control variables and instruments previously described.

A key focus of our analysis is the interaction between capital controls (i.e., the “walls” and the “gates”) and the channel variables: Do such controls reduce the extent to which the channels stimulate or dampen international trade? If capital control actions effectively mitigate an adverse impact of our channels on international trade, we expect a rise in . The parameters

and

reflect capital controls’ direct and indirect effects, respectively.

We performed the estimation of EquationEquations (1)(1)

(1) and (Equation2

(2)

(2) ) with various estimation techniques commonly recommended for dynamic panel models and which provide robust estimators. For our study, these estimators fit better with a moderate number of countries and a short period. We used two Generalized Method of Moments (GMM) estimators – the difference and the system GMM. Some studies have concluded that system GMM is more efficient than difference GMM (Blundell & Bond, Citation1998); the preference for the system GMM estimators is motivated by their robustness despite the heteroskedasticity aberrations in a linear regression specification containing a narrow time series.Footnote10 Alternatively, dynamic panel data analysis can use two commonly used estimators – the fixed effects and random effects maximum likelihood estimators (MLE) (Hsiao et al., Citation2002). The two types of estimation – GMM and MLE – have different advantages, particularly the weakly endogenous explanatory variables.

Table 4. Capital control related-issues – System GMM estimates

Table 5. Robustness check – The “Walls” effect of capital controls

A common challenge faced by the research on the impacts of capital controls is the problem of endogeneity – more specifically that of potential reverse causality (Alam et al., Citation2019; Galati & Moessner, Citation2018). Capital control actions do not occur in a vacuum; they may be taken in response to macroeconomic and financial developments, which may be the same variables used to assess their effects. We mitigated the risk of biased estimates due to endogeneity in four ways (the first two being commonly applied in the literature – e.g., Cerutti, Claessens, & Laeven, Citation2017; Claessens, Ghosh, & Mihet, Citation2013):

In our baseline setup, we lagged the capital controls index and control variables by one-quarter and include the lagged dependent variableFootnote11;

Among our estimators, we used the Arellano-Bond GMM methodology, which is suitable for independent variables that are not strictly exogenous;

We focused on the interaction term of

. This should suffer less from an endogeneity bias, based on the assumption that changes in the transmission channels are not commonly considered when designing a capital control policy. The change in the transmission channel then functions as an exogenous shifter of the effect of prior capital control action, reducing the potential endogeneity problem;

We included the control and instrumental variables described earlier.

We examine potential simultaneity one step further by accounting more fully for economic fundamentals that may be driving both capital controls and international trade simultaneously.

The regression equations include dummy variables for currency crisis (D1), banking crisis (D2), de facto exchange rate regimes (D3), and inflation targeting regimes (D4).Footnote12 As detailed in section 2, the famous trilemma is behind this exercise. The exchange rate regimes, monetary/macroprudential policy regimes, and capital control policy interact and raise the difficulty of isolating the pure effects of capital controls. Otherwise, it is to distinguish the pure effects of capital controls from exchange rate regimes and monetary policy regimes. Dummy variables for currency and banking crises are also important factors to control in the regressions as financial crises severely affect international trade.

4. Results and interpretation

4.1. Baseline results

Estimation results of the baseline regression for the “walls” and “gates” effects of capital controls (i.e., EquationEquations (1)(1)

(1) and (Equation2

(2)

(2) )) are presented in .Footnote13 Panels (1) and (2) report the estimates using GMM estimators – difference and system, respectively. Panels (3) and (4) report the findings using MLE estimators – fixed and random effects, respectively. Similarly, we regressed panels (5) to (8) for EquationEquation (2)

(2)

(2) .Footnote14

Table 6. Baseline model

The different estimation methods – GMM and MLE – match the signs and levels of the coefficients. There is higher statistical significance with the MLE estimators. The validity of the instruments is accepted for the GMM regressions, following the Hansen test for over-identifying restrictions. The p-values for first- and second-order autocorrelated disturbances are displayed for AR(1) and AR(2). The results show the absence of autocorrelation for the second-order, however there is a significant first-order autocorrelation. According to the Hausman Test, the fixed effects MLE are preferred to random effects. The Wald test statistics are highly significant for all estimation methods, showing that the models’ variables lead to statistically significant improvement in their fit. In sum, our diagnostic tests corroborate the correct model specifications.

The findings show very similar coefficients generated by the different estimation techniques. Our results clearly show significant adverse effects of capital controls on international trade. This result is consistent with the empirical literature showing a direct detrimental effect of capital controls on international trade (Giovannini & Park, Citation1989, Citation1992; Tamirisa, Citation1998; Wei & Zhang, Citation2007). For the channels without interaction with the capital controls index, the estimated exchange rate volatility ranges from −0.091 to −0.132, showing an adverse effect on international trade. Similarly, a harmful impact is displayed by the estimates of interest rate differentials, which range from −0.095 to −0.136. These results are expected given the specific relationship between monetary and exchange rate policies in developing economies due to persistent boom-and-bust capital flows (Guzman, Ocampo, & Stiglitz, Citation2018). Globally, macroeconomic instability and excess volatility are often a source of weak economic performance and fragility (Kose, Prasad, & Terrones, Citation2003). The impact of inflation fluctuations is stronger; its coefficient is about −0.192 to −0.236, indicating that around the fifth to the fourth decrease in international commerce is caused by inflation volatility. Usually, inflation volatility reflects a climate of uncertainty that discourages international trade transactions.

Considering the indirect impact, the exchange rate interaction term has a significant coefficient of −0.095, which has interesting economic significance implying that 9.5% of international trade changes are transmitted through exchange rate changes (with the different estimation methods). When capital controls are permanent (comparison between coefficients of “walls” and “gates”), the exchange rate becomes less volatile and reduces the adverse effect on trade.

The interaction term coefficients of the interest rate differentials are similar to the exchange rate interaction term. However, compared to the direct effect, there is a significant decrease in the interaction term coefficient of the interest rate differentials (for the “walls” effect). For example, in column (1) the coefficient decreases from −0.127 to −0.094. Furthermore, the results show that permanent capital controls are more effective in mitigating the adverse effect of interest rate differentials than episodic controls. Indeed, the coefficients of the interaction term increase from “gates” to “walls”.

The exception in these results is the inflation rate volatility; capital controls seem to worsen the unwanted effect of inflation. The comparison between the coefficients of INF and CCxINF shows that the adverse impact of inflation on international trade was aggravated following the application of capital controls. This result is different from that found with the exchange rate and the interest rate differentials, for which capital controls mitigate the adverse effects of their volatility. This result of the inflation effect is not surprising; as detailed in the literature review, there is no clear consensus regarding the relationship between capital controls and inflation. Our results are similar to the those of the studies suggesting that capital controls are correlated with higher inflation (Grilli & Milesi-Ferretti, Citation1995; Romer, Citation1993).

Overall, the results provide strong evidence that more capital control stringency mitigates the adverse effects of exchange rate and interest rate differentials volatilities on international trade. This result is interesting since while the coefficients displaying the direct impact of capital controls on international trade are negative, we found that these controls can benefit trade by limiting the adverse effects of these channels. Thus, our study reveals that the direct effect of capital controls on international trade is – unexpectedly – different from the indirect effect inferred through interaction terms. The result of inflation volatility is more debatable since capital controls amplify the detrimental effects of inflation volatility on trade. Comparing “walls” with “gates” estimates, we found that the coefficients are stronger for “walls”, showing that long-lasting capital controls have a stronger impact on international trade. Targeted controls should be effectively implemented in a precautionary manner, ahead of a surge of trade flows. This suggests that long-lasting targeted controls indeed reduce the volatility of our channels and thereby support international trade.

The different results for the exchange rate and interest rate differentials, on the one hand, and inflation, on the other hand, raise the necessity of coordination between the various economic policies affecting these variables. Exchange rate and monetary policies have often been used as a policy mix to target inflation. Capital controls may be joined to the policy mix to support international trade as a restrictive policy. A careful mix of these various policies is necessary to achieve optimal results (Bhattarai et al., Citation2021).

5. Capital controls related issues and robustness check

Here we extend the analysis for further consideration and examine issues related to the use of capital controls. First, previous studies have been particularly interested in the countercyclical behavior of capital controls and distinct controls on inflows and outflows. Second, a debate has been raised about the role of financial development in supporting capital control actions. Third, macroprudential policies – as closely related restrictive policies – may be implemented concurrently or separately from capital controls.

reports the estimates of capital controls related issues. For EquationEquation (1)(1)

(1) , panels (1) and (2) report the findings on the cyclical behavior of capital controls, and distinguish between capital control actions on exporters (controls on inflows) and importers (controls on outflows), respectively. Panels (3) and (4) consider the role of financial development and display the results for financially developed and less developed countries, respectively. Finally, Panel (5) reports the findings following the introduction of macroprudential policies. Similarly, we regressed panels (6) to (10) for EquationEquation (2)

(2)

(2) .

5.1. Countercyclical capital control policy

There are specific circumstances when countercyclical capital controls are desirable. Policymakers are advised to impose stringent controls on inflows during expansions and ease controls on outflows during contractions and vice versa. Thus, there should be negative correlations between capital controls and the two types of flows during expansions and contractions. The cyclical behavior of capital controls highlights multiple impacts on international trade according to the type of controls applied (controls on inflows or outflows). For the present examination, we hypothesized that (1) exports are related to capital controls on inflows, and (2) imports are associated with capital controls on outflows (Lai et al., Citation2021). The results of this exercise are reported in . Panels (1) and (6) present the estimates for controls on inflows (exporting countries), and panels (2) and (7) present the controls on outflows (importing countries).

Overall, the results suggest that exporting countries are the least affected by the adverse effect of capital controls. In “walls” regressions, the capital controls index has statistically significant coefficients of around −0.078 and −0.102 for exporting and importing countries. This result shows that the adverse effect of capital controls on international trade is stronger for importing countries. Similarly, the adverse effects of the channels are diminished with the interaction terms. This improvement in the impact on trade is more sizeable in the exporting countries than the importing countries. The coefficients of these channels are −0.091, −0.094, and −0.207 for exporting countries, and lower for importing countries (−0.107, −0.112, and −0.245), showing a stronger adverse impact on international trade in importing countries.

Exporting countries have the privilege of accessing foreign exchange earnings and can hedge against the effects of capital controls more effectively than importing countries. Likewise, capital controls increase currency depreciation events and grow foreign exchange reserves of exporting countries (Alfaro, Cunat, Fadinger, & Liu, Citation2018). After the 2008 financial crisis, emerging economies have accumulated substantial foreign exchange reserves (Pina, Citation2015). Capital controls can isolate these countries from international capital markets and thus deprive them of owning foreign currencies. International reserve holdings have allowed several emerging markets to mitigate the adverse impact of capital controls on international trade. This increased accumulation of international reserves enables the country to obtain extra liquidity and constitutes a solution to such a situation (Aizenman and Lee, Citation2007; Obstfeld et al., Citation2008).

5.2. Level of financial development

The effect of capital controls is not isolated from the macroeconomic and domestic financial circumstances. A close link exists between the development of the financial system and the quality of financial institutions (Eichengreen & Rose, Citation2014). Bush (Citation2019) found that capital control actions are amplified in a more developed financial system through enforcing targeted controls to alter international trade. Several papers examine the linkage between financial development and trade. Globally, financial development has a positive effect on trade (Beck, Citation2002; Eichengreen et al., Citation2011; Forbes, Citation2007; Manova, Citation2013; Rajan & Zingales, Citation1998). We investigated whether the impact of capital controls is different based on the level of financial development. We divided our sample into financially developed and financially repressed economies. The data on financial development were borrowed from Svirydzenka (Citation2016), who established a classification of 180 economies according to their level of financial development (noted FD). In , panels (3), (8), (4), and (9) report the findings for financially developed and less developed economies, respectively.

The findings support an intensification of capital control actions in more developed financial systems. Considering the direct impact, the capital controls index coefficients are lower (with a negative sign) in the financially developed countries, which shows a mitigation of the adverse effects of capital controls on international trade. This mitigation effect is even stronger for long-lasting controls (“walls”) compared to episodic controls (“gates”). Regarding the indirect effects through the channel variables, the results of the interaction terms show that financial development also helps sustain the impact of capital controls. Indeed, the coefficients of these interaction terms are negative and statistically significant and are higher in financially developed countries than in less developed ones. Financial development facilitates the effectiveness of capital control actions in reducing the volatility of channel variables, thereby improving international trade.

5.3. Macro-Prudential policies

We examined whether macroprudential measures to protect the financial system can support or hinder capital control actions. When macroprudential policies and capital controls are introduced concurrently, the effects of the two policies may be conflated. Panels (5) and (10) display the results of jointly applying macroprudential policies with capital controls.Footnote15 The data source for macroprudential policy actions is the IMF’s iMaPP database (Alam et al., Citation2019),Footnote16 the most comprehensive macroprudential policies to date (noted MP).

Previous studies have shown that macroprudential and capital control policies, introduced countercyclically to capital inflows, support the financial system’s stability and maintain macroeconomic equilibrium (Eichengreen & Rose, Citation2014; Forbes, Fratzscher, & Straub, Citation2013). Moreover, both policies should “put sand in the wheels” of bilateral financial transactions and are more active in times of inflows surges and relaxed during recessions (Klein, Mariano, & Özmucur, Citation2007).

Our results show that a macroprudential policy lessens the extent to which the volatility of the channel variables affects international trade. Comparing the coefficients of the interaction terms in , for the “walls” regressions, we found that exchange rate, interest rate differentials, and inflation coefficients increase from −0.095, −0.081, and −0.306 to −0.041, −0.047, and −0.146, respectively. These findings show that controlling for the macroprudential policies does not reduce the impact of capital controls; contrarily, this impact is strengthened. For a given appreciation of the real exchange rate, the subsequent adverse effect of the exchange rate channel is weaker when macroprudential policies had been tightened in the previous quarter. The results also show an increase in the coefficient of interest rate differentials and inflation volatility, indicating that the adverse effect on international trade was mitigated following macroprudential policies. Comparing the findings of “walls” and “gates” in , macroprudential policies fit better with long-lasting capital controls and tend to reinforce the preceding impact exerted by capital controls of reducing the volatilities. Also here, policy coordination between macroprudential regulations and capital controls is necessary. An optimal adjustment of both policies is required to control the risks threatening the financial system’s stability and reduce the volatility of the transmission channels to support international trade.

5.4. Robustness check

In our robustness test, we considered two alternative capital control indexes: the Fernández et al. (Citation2016) and the Chinn-Ito (2008) indexes.Footnote17 For the present investigation, both indexes are well-suited for cross-country comparisons of the level of openness and can differentiate between controls on inflows and on outflows and between “walls” and “gates” controls. The study has assumed that all quarterly values within one year are the same for these capital control indexes that are only available on an annual basis.

The dataset of Fernández et al. (Citation2016) reports the restrictions applied by 99 economies from 1995 to 2015. Each index takes the value one if a restriction exists and 0 otherwise. This binary index is based on a narrative reading of IMF’s AREAER. Fernández et al. (Citation2016) analyzed the restrictions on 10 asset categories. The present study used the overall index, noted “ka”. Furthermore, we used the “kaopen” index from Chinn-Ito (2008). This index is widely used as a de jure proxy of financial liberalization. Its construction is also based on a narrative description of the restrictions provided by the IMF’s AREAER. It proxies the extent of liberalization measures for various international transactions likely to be subject to capital controls. “kaopen” ranges from −1.80 to 2.54, was applied to 181 countries, and covers the period 1970–2019. Higher values correspond with more openness of cross-border trade transactions. Like the Fernández et al. (Citation2016) index, “kaopen” has the merit of measuring capital controls’ stringency on inflows and outflows.

reports the findings of the robustness test. Globally, our results were not altered following alternative capital control indexes. In particular, the interaction term coefficients remain statistically significant and have the same signs as in . The estimates in align with our previous findings and indicate that capital controls mitigate the adverse effect on international trade through their impact on the channel variables.

To accurately estimate whether capital controls affect international trade, the least-squares dummy variable method (LSDV) in the pooled ordinary least squares (OLS) and fixed effects estimation method was used as a robustness check for estimation. The last column of reports the results of the LSDV estimations.

The results are widely in line with the findings of the GMM system estimator. However, the interaction term of the inflation rate becomes insignificant, and the interaction terms of the interest rate differentials and the exchange rate turns less statistically significant. Oppositely, the capital control index is now associated with a negative and more significant impact on international trade, consistent with a direct adverse effect of capital controls.

As a further robustness check, we applied our panel data to a VAR model to obtain the impulse response function and confidence intervals. We included two lags of each variable in the model. We assumed that exogenous transmission channels estimated in EquationEquations 1(1)

(1) and Equation2

(2)

(2) are now endogenous and affected by shocks to CC indicators since the specification of the VAR model removes the previously instrumental variables used in the baseline model.

shows the responses of the exchange rate, interest rate differentials, inflation rate, and international trade volatilities to a change of one standard deviation of the capital controls indexes.

Figure 3. Impulse responses to a capital controls shock.

The first column in plots the impulse response of the volatilities corresponding to a random shock of long-lasting capital controls. This column shows a negative impact of the shock on all three macroeconomic volatilities. These plots mirror the role of capital controls in mitigating the adverse effects of the channel variables’ volatilities. Besides, there is a positive impact on international trade, showing a supporting role of capital controls. The second column in plots the impulse response of episodic capital controls shock. We observe a close trend like in the first column; however, the magnitude of the impact is lower, and the effect of the shock dies out relatively quickly (after eight quarters). The impulse response analysis confirms the empirical results discussed previously and highlights that “walls” controls are more effective in reducing volatilities and supporting international trade.

6. Conclusion

This paper presents an empirical investigation of the channels through which capital controls impact international trade. The findings of this study cast doubt on the prevailing view on the adverse effect of capital controls on international trade. We found that capital controls are useful and mitigate the harmful effects of the volatility of the exchange rate and interest rate differentials. The moderation of these volatilities supports international trade. Conversely, capital controls aggravate the unwanted effect of inflation volatility on international trade.

The results of this study raise some policy implications. First, targeted long-lasting “walls” capital controls can have a sizeable impact of reducing the adverse effects of the volatility of the channel variables. Policymakers need to choose the right time to introduce capital controls. When these controls are applied early, they are more effective and respond better to macroeconomic imbalances. Second, The complexity of the players in international trade calls for the use of monetary and exchange rate policies in tandem with capital controls. The combination of these policies turns out to be quite delicate. This combination requires close coordination domestically and internationally, which can eventually redress the unwanted effect found for inflation volatility.

The decisions to control inflows or outflows are concerning since the analysis on the countercyclical behavior of capital controls revealed that exporting countries are the least affected by the adverse impact of these controls. This study highlights the useful role of macroprudential policies, which support capital control actions in reducing macroeconomic fluctuations. The role of financial development is also emphasized; more developed financial systems support capital control actions in mitigating the volatilities of the channel variables, thus promoting international trade transactions.

Our results are compatible with the current literature. The impact of capital controls varies according to different considerations, particularly the level of financial development, targeting inflows vs. outflows, and the concurrent use of macroprudential policies. Our findings remain robust across specifications, specifically the use of alternative capital control indexes.

Data availability statement

Data available on request due to privacy/ethical restrictions.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Chokri Zehri

Chokri Zehri is associate professor of economics at Prince Sattam bin Abdulaziz University in Saudi Arabia. A Tunisian citizen, he taught at Gabes University and al-baha international college of sciences before coming to Prince Sattam University in 2019. Zehri received his B.Ec. from the Institute of Higher Commercial Studies of Carthage-Tunis in 2001 and completed his master and Ph.D. in Economics at Aix-Marseille II University – France in 2007. Zehri’s research interests include the macroeconomics policies; financial crises; capital account liberalization, capital controls; external debts; and econometric methods for program and policy evaluation. He published many papers in these areas and got several awards for outstanding publications.

Notes

1 Additional channels can be considered and may impact international trade; however, we are satisfied with these three channels which we consider to be the most relevant to affect international trade.

2 Throughout the remainder of the paper, we refer to exchange rate, interest rate differentials, and inflation rate as the channels of capital controls. We refer to indirect effect when the impact of capital controls operates through these channels (i.e., within interaction terms).

3 We use the distinction between “walls” and “gates” effects of capital controls defined in Klein (Citation2012) and later employed by Bacchetta et al. (Citation2021).

4 (Davis and Van Wincoop Citation2018) compared between financial globalization and trade globalization. They found that neither financial nor trade globalization affected the volatility of gross capital flows. However, trade integration increased the volatility of net flows, while financial integration decreased the volatility of net flows.

5 The sample is restricted to 26 countries due to data limitation.

6 The index is useful for our empirical examination since it differentiates between controls on inflows and on outflows.

7 The international interest rate is measured by real U.S. 10-year treasuries rate. Movements in this interest rate are the global benchmark for markets and dominate the world’s real interest rate.

8 The data is aggregated for all sample countries.

9 It is useful to test conditional volatility behavior through ARCH or GARCH elements. However, our study uses quarterly economic data, which does not allow this test.

10 This motivated our choice to regress our models with the system GMM for the analysis of capital controls related issues and robustness check of , respectively.

11 One quarter lag was chosen according to the AIC information criteria and sequential testing for the significance of coefficients on lag.

12 The dummy variables take the value of one if a crisis occurs (similarly de facto exchange rate regimes or inflation targeting regimes are used) and zero if not.

13 The results focus more on capital controls index coefficients, channels, and interaction terms. Control variables, instruments, dummy variables and the lagged dependent variable are inserted in all panel regressions, but not reported in the estimates results to avoid content overload.

14 Columns (1) to (4) present the estimates from EquationEquation (1)(1)

(1) – long-lasting controls, and columns (5) to (8) report the estimates of EquationEquation (2)

(2)

(2) – episodic controls.

15 We obtained from Ahnert et al. (Citation2021) indexes of macroprudential FX regulations (MP) – i.e., prudential regulations targeting the financial sector .

16 The database covers 17 instruments for a total of 138 counties over the period 1999–2016 at a monthly frequency.

17 See Batini and Durand (Citation2020) for a survey on capital control indexes.

References

- Ahnert, T., Forbes, K., Friedrich, C., & Reinhardt, D. (2021). Macroprudential FX regulations: Shifting the snowbanks of FX vulnerability? Journal of Financial Economics, 140(1), 145–174.

- Aizenman, J., & Lee, J. (2007). International reserves: Precautionary versus mercantilist views, theory and evidence. Open Economies Review, 18(2), 191–214.

- Alam, Z., Alter, M. A., Eiseman, J., Gelos, M. R., Kang, M. H., Narita, M. M., …Wang, N. (2019). Digging deeper–Evidence on the effects of macroprudential policies from a new database. Washington: DC: International Monetary Fund.

- Alfaro, L., Cunat, A., Fadinger, H., & Liu, Y. (2018). The real exchange rate, innovation and productivity: heterogeneity, asymmetries and hysteresis (No. w24633). National Bureau of Economic Research.

- Amiti, M., & Wakelin, K. (2003). Investment liberalization and international trade. Journal of International Economics, 61(1), 101–126.

- Asteriou, D., Masatci, K., & Pılbeam, K. (2016). Exchange rate volatility and international trade: International evidence from the MINT countries. Economic Modelling, 58, 133–140.

- Auer, R. A., Degen, K., & Fischer, A. M. (2013). Low-wage import competition, inflationary pressure, and industry dynamics in Europe. European Economic Review, 59, 141–166.

- Bacchetta, P., Davenport, M., & van Wincoop, E. (2021). Can sticky Portfolios explain international capital flows and asset prices? Cambridge, MA: NBER Chapters.

- Batini, N., & Durand, L. (2020). Analysis and advice on capital account developments: Flows, restrictions, and policy toolkits. IEO Background Paper BP/20-02/03 for IEO evaluation of “IMF Advice on Capital Flows”. Washington: International Monetary Fund.

- Beck, T. (2002). Financial development and international trade: Is there a link? Journal of International Economics, 57(1), 107–131.

- Benigno, G., Converse, N., & Fornaro, L. (2015). Large capital inflows, sectoral allocation, and economic performance. Journal of International Money and Finance. 55, 60–87.

- Bergant, K., Grigoli, M. F., Hansen, M. N. J. H., & Sandri, M. D. (2020). Dampening global financial shocks: Can macroprudential regulation help (more than capital controls)? Washington, DC: International Monetary Fund.

- Bhattarai, K., Mallick, S. K., & Yang, B. (2021). Are global spillovers complementary or competitive? Need for international policy coordination. Journal of International Money and Finance, 110, 102291.

- Bianchi, J. (2011). Overborrowing and systemic externalities in the business cycle. American Economic Review, 101(7), 3400–3426.

- Bianchi, F., Melosi, L., & Rottner, M. (2019). Hitting the elusive inflation target (No. w26279). National Bureau of Economic Research.

- Binici, M., Hutchison, M., & Schindler, M. (2010). Controlling capital? Legal restrictions and the asset composition of international financial flows. Journal of International Money and Finance, 29(4), 666–684.

- Blundell, R., & Bond, S. (1998). Initial conditions and moment restrictions in dynamic panel data models. Journal of Econometrics, 87(1), 115–143.

- Bush, G. (2019). Financial development and the effects of capital controls. Open Economies Review, 30(3), 559–592.

- Cerdeiro, D. A., & Komaromi, A. (2019). Financial openness and capital inflows to emerging markets. In Search of robust evidence. International Monetary Fund.

- Cerutti, E., Claessens, S., & Laeven, L. (2017). The use and effectiveness of macroprudential policies: New evidence. Journal of Financial Stability, 28, 203–224.

- Chakraborty, I. (2006). Capital inflows during the post-liberalisation period. Economic and Political Weekly 41 (2) , 143–150.

- Chinn, M. D., & Ito, H. (2008). A new measure of financial openness. Journal of Comparative Policy Analysis, 10(3), 309–322.

- Chinn, M. D., & Ito, H. (2008). A new measure of financial openness. Journal of Comparative Policy Analysis, 10(3), 309–322.

- Chor, D., & Manova, K. (2012). Off the cliff and back? Credit conditions and international trade during the global financial crisis. Journal of International Economics, 87(1), 117–133.

- Claessens, S., Ghosh, S. R., & Mihet, R. (2013). Macro-prudential policies to mitigate financial system vulnerabilities. Journal of International Money and Finance, 39, 153–185.

- Cooper, R. N., Tarullo, D. K., & Williamson, J. (1999). Should capital controls be banished? Brookings Papers on Economic Activity, 1999(1), 89–141.

- Corsetti, G., & Pesenti, P. (2005). International dimensions of optimal monetary policy. Journal of Monetary Economics, 52(2), 281–305.

- Cushman, D. O. (1983). The effects of real exchange rate risk on international trade. Journal of International Economics, 15(1–2), 45–63.

- Davis, J. S., & Van Wincoop, E. (2018). Globalization and the increasing correlation between capital inflows and outflows. Journal of Monetary Economics, 100, 83–100.

- De Gregorio, J., Edwards, S., & Valdés, R. O. (2000). Controls on capital inflows: Do they work? Journal of Development Economics, 63(1), 59–83.

- Dexter, A. S., Levi, M. D., & Nault, B. R. (2005). International trade and the connection between excess demand and inflation. Review of International Economics, 13(4), 699–708.

- Edwards, S. (1999). How effective are capital controls? Journal of Economic Perspectives, 13(4), 65–84.

- Edwards, S. (2007). Introduction to” capital controls and capital flows in emerging economies: Policies, practices and consequences. In Capital controls and capital flows in emerging economies: Policies, practices, and consequences (pp. 1–18). Chicago, IL:: University of Chicago Press.

- Edwards, S., & Ostry, J. D. (1992). Terms of trade disturbances, real exchange rates, and welfare: The role of capital controls and labor market distortions. Oxford Economic Papers, 44(1), 20–34.

- Eichengreen, B., Gullapalli, R., & Panizza, U. (2011). Capital account liberalization, financial development and industry growth: A synthetic view. Journal of International Money and Finance, 30(6), 1090–1106.

- Eichengreen, B., & Rose, A. (2014). Capital controls in the 21st century. Journal of International Money and Finance, 48, 1–16.

- Erten, B., Korinek, A., & Ocampo, J. A. (2021). Capital controls: Theory and evidence. Journal of Economic Literature, 59(1), 45–89.

- Esaka, T. (2010). De facto exchange rate regimes and currency crises: Are pegged regimes with capital account liberalization really more prone to speculative attacks? Journal of Banking & Finance, 34(6), 1109–1128.

- Feldstein, M. (1985). International trade, budget deficits, and the interest rate. The Journal of Economic Education, 16(3), 189–193.

- Fernández, A., Klein, M. W., Rebucci, A., Schindler, M., & Uribe, M. (2016). Capital control measures: A new dataset. IMF Economic Review, 64(3), 548–574.

- Fernández, A., Klein, M. W., Rebucci, A., Schindler, M., & Uribe, M. (2016). Capital control measures: A new dataset. IMF Economic Review, 64(3), 548–574.

- Forbes, K. J. (2007). One cost of the Chilean capital controls: Increased financial constraints for smaller traded firms. Journal of International Economics, 71(2), 294–323.

- Forbes, K. J., Fratzscher, M., & Straub, R. (2013). Capital controls and macroprudential measures: What are they good for? SSRN Electronic Journal. doi:10.2139/ssrn.2364486

- Forbes, K., Fratzscher, M., & Straub, R. (2015). Capital-flow management measures: What are they good for? Journal of International Economics, 96, S76–S97.

- Frankel, J. A., & Okongwu, C. (1996). Liberalized portfolio capital inflows in emerging markets: Sterilization, expectations, and the incompleteness of interest rate convergence. International Journal of Finance & Economics, 1(1), 1–23.

- Frost, J., Ito, H., & Van Stralen, R. (2020). The effectiveness of macroprudential policies and capital controls against volatile capital inflows. SSRN Electronic Journal. doi:10.2139/ssrn.3623036

- Galati, G., & Moessner, R. (2018). What do we know about the effects of macroprudential policy? Economica, 85(340), 735–770.

- Giovannini, A., & Park, J. W. (1989). Capital controls and international trade finance. Cambridge, MA:: National Bureau of Economic Research. doi:10.3386/W3112

- Giovannini, A., & Park, J. W. (1992). Capital controls and international trade finance. Journal of International Economics, 33(3–4), 285–304.

- Glick, R., Guo, X., & Hutchison, M. (2006). Currency crises, capital-account liberalization, and selection bias. The Review of Economics and Statistics, 88(4), 698–714.

- Gong, L., Wang, C., & Zou, H. F. (2017). Optimal exchange-rate policy in a model of local-currency pricing with vertical production and trade. Open Economies Review, 28(1), 125–147.

- Grilli, V., & Milesi-Ferretti, G. M. (1995). Economic effects and structural determinants of capital controls. Staff Papers - International Monetary Fund, 42(3), 517–551.

- Gruben, W. C., & McLeod, D. (2002). Capital account liberalization and inflation. Economics Letters, 77(2), 221–225.

- Guzman, M., Ocampo, J. A., & Stiglitz, J. E. (2018). Real exchange rate policies for economic development. World Development, 110, 51–62.

- Hooper, P., & Kohlhagen, S. W. (1978). The effect of exchange rate uncertainty on the prices and volume of international trade. Journal of International Economics, 8(4), 483–511.

- Houck, J. P. (1979). Inflation and international trade (No. 784-2016-52048), pp. 57–63.

- Hsiao, C., Pesaran, M. H., & Tahmiscioglu, A. K. (2002). Maximum likelihood estimation of fixed effects dynamic panel data models covering short time periods. Journal of Econometrics, 109(1), 107–150.

- Klein, M. W. (2012). Capital controls: Gates versus walls (No. w18526). National Bureau of Economic Research.

- Klein, L. R., Mariano, R. S., & Özmucur, S. (2007). Capital controls, financial crises and cures: Simulations with an econometric model for Malaysia. Recent Financial Crises: Analysis, Challenges and Implications, 134–147 .

- Kose, M. A., Prasad, E. S., & Terrones, M. E. (2003). Financial integration and macroeconomic volatility. IMF Staff Papers, 50(1), 119–142.

- Lai, K., Wang, T., & Xu, D. (2021). Capital controls and international trade: An industry financial vulnerability perspective. Journal of International Money and Finance, 116, 102399.

- Lai, K., Wang, T., & Xu, D. (2021). Capital controls and international trade: An industry financial vulnerability perspective. Journal of International Money and Finance, 116(C), 102399.

- Lane, P. R., & Milesi-Ferretti, G. M. (2008). The Drivers of Financial Globalization. The American economic review, 98(2), 327–332.

- Magud, N. E., Reinhart, C. M., & Rogoff, K. S. (2011). Capital controls: myth and reality-a portfolio balance approach (No. w16805). National Bureau of Economic Research.

- Mankiw, N. G., & Reis, R. (2003). What measure of inflation should a central bank target? Journal of the European Economic Association, 1(5), 1058–1086.

- Manova, K. (2008). Credit constraints, equity market liberalizations and international trade. Journal of International Economics, 76(1), 33–47.

- Manova, K. (2013). Credit constraints, heterogeneous firms, and international trade. Review of Economic Studies, 80(2), 711–744.

- Mathieson, D. J., & McKinnon, R. (1981). How to manage a repressed economy. Princeton Essays in International Finance, 145, 1–26.

- McKenzie, M. D. (1999). The impact of exchange rate volatility on international trade flows. Journal of Economic Surveys, 13(1), 71–106.

- Meese, R. A. (1984). Is the sticky price assumption reasonable for exchange rate models? Journal of International Money and Finance, 3(2), 131–139.

- Nakatani, R. (2018). Real and financial shocks, exchange rate regimes and the probability of a currency crisis. Journal of Policy Modeling, 40(1), 60–73.

- Nakatani, R. (2020). “Macroprudential policy and the probability of a banking crisis. Journal of Policy Modeling, 42(6), 1169–1186.

- Nier, E. W., Olafsson, T. T., Rollinson, Y. G., & Gelos, G. (2020). Exchange rates and domestic credit-can macroprudential policy reduce the link? IMF Working Papers, 2020(187 1–25).

- Nier, E. W., Olafsson, T. T., Rollinson, Y. G., & Gelos, G. (2020). Exchange Rates and Domestic Credit-Can Macroprudential Policy Reduce the Link? International Monetary Fund Working Paper No. 20/187.

- Obstfeld, M., Ostry, J. D., & Qureshi, M. S. (2019). A tie that binds: Revisiting the trilemma in emerging market economies. Review of Economics and Statistics, 101(2), 279–293.

- Obstfeld, M., & Rogoff, K. (1995). Exchange rate dynamics redux. Journal of Political Economy, 103(3), 624–660.

- Obstfeld, M., Shambaugh, J. C., & Taylor, A. M. (2008). Financial Stability, the Trilemma, and International Reserves. National Bureau of Economic Research Working Paper

- Ostry, M. J. D., Ghosh, M. A. R., Habermeier, M. K. F., Laeven, M. L., Chamon, M. M., Qureshi, M., & Kokenyne, A. (2011). Managing capital inflows: What tools to use? Washington, DC:: International Monetary Fund.

- Pandey, R., Pasricha, G. K., Patnaik, I., & Shah, A. (2021). Motivations for capital controls and their effectiveness. International Journal of Finance & Economics, 26(1), 391–415.

- Pina, G. (2015). The recent growth of international reserves in developing economies: A monetary perspective. Journal of International Money and Finance, 58, 172–190.

- Quinn, D., Schindler, M., & Toyoda, A. M. (2011). Assessing measures of financial openness and integration. IMF Economic Review, 59(3), 488–522.

- Qureshi, M. S., Ostry, J. D., Ghosh, A. R., & Chamon, M. (2011). Managing capital inflows: The role of capital controls and prudential policies. NBER Working Paper No. 17363.

- Radelet, S., Sachs, J. D., Cooper, R. N., & Bosworth, B. P. (1998). The East Asian financial crisis: Diagnosis, remedies, prospects. Brookings Papers on Economic Activity, 29(1), 1–74.

- Rajan, R., & Zingales, L. (1998). Financial development and growth. American Economic Review, 88(3), 559–586.

- Rodrik, D. (1998). Why do more open economies have bigger governments? Journal of Political Economy, 106(5), 997–1032.