?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This paper examines whether financial constraints of firms influence their pricing behavior. To do so, a product-level dataset is used from Iranian-listed manufacturing companies. This study employs the imposition of international sanctions against Iran in 2012 as an exogenous shock to identify the effect of financial constraints. According to the results financially restricted firms keep their prices lower than their counterparts to increase their internal financial resources. The results show the difference between output prices of constrained and unconstrained firms rising after the imposition of sanctions. In addition, this relationship is affected by the degree of export-orientation of firms, and only exporter firms that experienced the negative demand shock after the sanctions, set their price lower to reduce the financial pressures. Also, the degree of dependency on imported input does not play a significant role in the relationship and ownership structure of firms has a significant impact on the relationship.

1. Introduction

How do financial frictions affect the price-setting behavior of firms? The dynamics of price adjustments play a critical role in the transmission mechanisms of economic policies. So it is essential to know which factors influence pricing behavior. In this regard, the puzzling behavior of price changes after the 2007–2008 financial crisis (mentioned in studies like Gilchrist, Schoenle, Sim, and Zakrajšek (Citation2017), Duca et al. (Citation2017), and Kim (Citation2021)) has motivated studies to examine the effect of financial markets frictions on price-setting behavior of firms. This paper investigates how firm’s financial constraints (resulted from financial frictions) affect the pricing behavior. This issue helps to understand how financial market imperfections affect the dynamics of price changes and how financial shocks affect the real sector.

According to the studies, the presence of financial constraints can impact the deviation between the actual and desired price of firms (Balleer, Hristov, & Menno, Citation2020). The main question is how firms manage their output price to mitigate the consequences of financial constraints. Brander and Lewis (Citation1986), Glazer (Citation1994), and Phillips (Citation1995) were the first studies to examine the effect of a financial position index on pricing behavior. One of the main challenges in the literature is contradictory results: some papers find that when more constrained, firms raise prices, while other studies find firms lower prices (Ge, Citation2020). Some studies like Erol (Citation2003), Kim (Citation2021), and Ge (Citation2020) try to explain this heterogeneity in the effect of financial constraints on pricing behavior. However, further analysis of the relationships is helpful for better understanding the impact of financial conditions on output pricing among firms. So, this paper aims to explore the relationship between financial constraints and pricing behavior. Specifically, this study examines the hypothesis that financially constrained firms lower their output prices to mitigate the problem of limited access to external financial resources.

In the examination of the relationship between price adjustments and credit market conditions, the identification problem is a critical challenge. Despite a strong correlation between the price changes and financial market conditions in aggregate data, identifying the true relationship between these two factors needs to capture the impact of other influential variables that is difficult to obtain with aggregate data (Kim, Citation2021). Therefore, it is necessary to design an identification strategy that takes advantage of micro-level data to identify the relationship. To do so, I use a unique dataset that combines 2285 product prices with corresponding financial indicators of 301 Iranian manufacturing firms. In this paper, the imposition of international sanctions against Iran in 2012 is used as a potential source to identify the effect of financial constraints on pricing behavior. The sanctions affect the costs and margins of Iranian firms through various channels. So adjustment of output prices as a consequence of the sanctions is inevitable. However, severe exchange rate depreciation caused by the imposition of sanctions generally raised domestic prices in terms of local currency. Note that the price changes were not the same and different features of markets, products, and firms have caused differences in the prices growth. So, I expect that the financial position of firms explains part of the difference in their pricing behavior and firms with financial constraints raise their prices less than their counterparts after a jump in prices.

The main contributions of the paper are three-fold. First, it exploits the imposition of international sanctions as an exogenous shock and investigates the effect of financial constraints on the pricing behavior of firms after the imposition of the sanctions. The imposition of sanctions acts as a trigger for an adverse demand shock as well as an adverse supply shock. It causes a negative demand shock for exporters and a negative supply shock for input importers. Using the case of sanctions as an identification source and micro-level data makes it possible to test the relationship between financial constraint and price-setting among firms after both demand and supply shocks. So for a deeper understanding of the relationship, price changes due to the demand shock are distinguished from price changes caused by the supply shock.

Second, this study examines the effect of financial constraints on pricing when prices generally are rising. Most of the studies in the issue analyzed the pricing behavior of firms after recessions in which the price trends were decreasing. Since the asymmetric price adjustment has been confirmed by many studies like Ball and Mankiw (Citation1994), extending the relationship between financial constraint and price setting to when the prices have an upward trend needs to be tested statistically. This paper fills the gap and considers the relationship between price-setting and financial constraints during an increasing price trend.

Third, this paper provides evidence regarding the relationship between pricing and financial conditions in a country with underdeveloped financial markets. The studiesFootnote1 widely address the influence of firms’ financial restrictions on pricing behavior in developed financial markets. This paper investigates whether the relationship remains stable in financial markets with higher financial frictions.Footnote2

The estimation results indicate firms with tighter financial constraints keep their output prices down. Also, according to the findings, financial constraints led to lower output prices after the sanctions only among the exporter firms that deal with a negative demand shock. Moreover, the link between financial constraints and pricing behavior is influenced by the ownership structure of price setters.

The rest of the paper is organized as follows. Section 2 contains the literature review. Section 3 describes the imposed sanctions against Iran and depicts their effects on economic variables. Section 4 presents the dataset used in this paper and also explains the methodology. Section 5 reports estimation results and discusses their interpretations. The last section concludes.

2. Literature review

In recent decades, some research has addressed the effect of financial constraints on output pricing behavior. The studies on this topic have reached widely varying, even contradictory results that create a challenging debate. Brander and Lewis (Citation1986) regarded a pioneering study, concludes that high debt firms to survive in bankrupt states and raise their profit in good conditions, choose a more aggressive strategy on the product market (or lower output prices). Some studies have supported the finding that firms under financial pressure reduce output prices to boost their income and increase their internal financial resource in the current period. Borenstein and Rose (Citation1995) and Busse (Citation2002) use data on the US airline industry and find that airlines in financial distress drop their price to increase their income by boosting the demand. Also, Zingales (Citation1998) indicates that highly leveraged firms affect survival by curtailing investments and reducing the output price. Baker, Sun, and Yannelis (Citation2020) show that significant effects of corporate taxes on prices are weaker for high-leverage firms. More recently, Kim (Citation2021) explains how a credit crunch affects the output price dynamics. He shows that the firms that faced a negative credit supply shock decreased their output prices by liquidating inventory and dumping their products to generate extra cash flow from the product market.

Some other studies have provided theoretical foundations and empirical evidence that is contradicted by the results of Brander and Lewis (Citation1986). In this approach, a decrease in output prices is deemed as an investment in market share that leads to rising future profits but does not increase internal sources of liquidity at the same time. So, firms cover liquidity shortfalls by increasing their price. This is contrary to the finding of Brander and Lewis (Citation1986). More precisely, in the adjustments of the output price and markup, the trade-off between the current and future profits is considered by firms. Some studies theoretically and empirically supported this hypothesis. Chevalier and Scharfstein (Citation1996) indicate output price and markup in financially constrained firms are countercyclical. In a recession, financially constrained firms to increase the current profits raise their output prices which also cuts their investments in the market share. In a boom, liquidity-constrained firms keep their prices down to invest in the market share. One of the pivotal works in this area is Gilchrist et al. (Citation2017) which investigates the effect of liquidity constraints on the pricing behavior of US firms during the financial crisis of 2008. The results indicate liquidity constrained firms charge higher prices in response to adverse financial or demand shocks to preserve internal liquidity, while their unconstrained counterparts cut prices. They conclude financial distress motivates financially constrained firms to increase output prices in recessions and leads to countercyclical behavior of markups and output prices. Also, Dasgupta and Titman (Citation1998), Kimura (Citation2013), Montero (2017), Khanna and Tice (Citation2005), and Secchi, Tamagni, and Tomasi (Citation2016) confirm that financially-constrained firms charging higher prices on average and the impact of financial constraints on prices is countercyclical.

So, while some studies suggest that financially constrained firms charge lower output prices to increase internal liquidity through boosting their output demand, other studies emphasize that lowering prices can only increase the market share and future profits. Therefore firms with limited access to external financial resources charge higher output prices to boost their current income and internal liquidity. To reconcile this contradictory finding, some articles show that the difference in the impact of financial constraints on prices can be attributed to other influential factors. Erol (Citation2003) states that the link between the leverage (as a proxy of financial position) and output price depends on the types of competition, uncertainties, and debt maturity. Phillips (Citation1995) finds that the sign of the relationship between debt ratio and output price varies across the industries, and leverage of rival firms, ease of expansion, and entry into an industry are factors that change the sign of the relationship. Some studies like Erol (Citation2003), Glazer (Citation1994), and Pichler, Stomper, and Zulehner (Citation2008) show debt maturity is an influential factor in the relationship between the level of debt and output pricing in a way that short-term and long-term debt have different effects on pricing behavior. Erol (Citation2003, Citation2005) confirms a higher level of short-term debt can cause an increase in output prices while long-term debt has the opposite effect. Showalter (Citation1995) provides evidence about the role of competition conditions in the debt–output pricing relationship and shows an increase in debt can lead to higher prices when competition is based on the price instead of quantity. Furthermore, Ge (Citation2020) uses micro data on insurance companies and finds the direction of financial constraints effect on a product price changes depending on how the product price changes impact the firm’s access to short-term financial resources. Duca, Montero, Riggi, and Zizza (Citation2017) confirm markup counter-cyclicality among financially constrained firms but introduce two factors that change the counter-cyclicality. The first is the degree of persistence in demand shocks. The Higher probability of the negative demand shocks persistence reduces the expected profit of investing in future market share by lowering the output prices. The second is the procyclicality of demand elasticity. When the elasticity of demand decreases during recessions, the expected gain from a given price cut becomes smaller. Also, Kimura (Citation2013) finds only output pricing in large firms is affected by financial restrictions and Kim (Citation2021) shows the size of reduction in product prices in response to a negative credit shock depends on products demand elasticity, issuing bonds, loans maturity, number of lenders and the size of firms.

Moreover, studies show that differences in proxies for the financial position of firms and various drivers of change in prices also can be sources of the result contradiction of the studies. Kim (Citation2021) notices this factor and finds the underlying reason for the difference in results of his paper and Gilchrist et al. (Citation2017) is the difference in the measure of financial constraints, which is the “weak liquidity position” in Gilchrist et al. (Citation2017). He concludes the liquidity ratio (used by Gilchrist et al. (Citation2017)) does not correctly represent the concept of financial constraints.

Overall, the studies have shown that financial pressures can affect the pricing behavior of firms, but there is no consensus on the sign of the relationship. While some papers conclude that firms reduce their output prices to mitigate the effects of financial restrictions, others come to the opposite conclusion and show that firms deal with the financial constraint problems by raising their output prices. However, some studies have attributed these conflicting results to other variables, such as demand elasticity, proxies for financial constraints, firm size, and debt maturities. Therefore, this study examines whether the intrinsic characteristics of firms, such as the degree of export-oriented, the import dependency, and the ownership structure can affect the relationship between financial constraints and prices. The existing studies in the literature explore the relationship between financial constraints and price changes after a decrease in prices that was generally due to recessions. This study examines whether the financial constraints distort the pricing behavior of firms after a positive shock to prices. It is expected limited access to finance affects firms’ pricing decision-making. Since the imposition of sanctions against Iran led to a sharp increase in prices, I exploit the sanctions as a source of identification of the effect. The study tests whether the relationship between output pricing and financial constraint depends on how firms get involved in foreign trade and firms’ ownership structure.

3. Economic sanctions against Iran

While there is no consensus on the effectiveness of sanctions policies to achieve policy objectives (Eaton & Engers, Citation1999; Giumelli & Ivan, Citation2013; Lam, Citation1990; Levy, Citation1999; Shin, Choi, & Luo, Citation2016; Smeets, Citation2018), numerous studies have confirmed the negative consequences of sanctions on the real sectors of targeted countries.Footnote3 Sanctions also influence on monetary and financial sectors.Footnote4 Moreover, according to Ghorbani Dastgerdi, Yusof, and Shahbaz (Citation2018), economic sanctions lead to higher inflation by decreasing the degree of openness, restricting investment inflows, and increasing inflation expectations. While the average annual inflation was 18.2 percent in 2010 and 2011 (two years before the sanction), in the two years after the imposition of sanctions (2012 and 2013) the average annual inflation reached 32 percent.

Rising tension over Iran’s nuclear programFootnote5 prompted international sanctions against Iran in 2012.Footnote6 In January 2012, the EU Foreign Affairs Council decided to impose an embargo on Iranian crude oil and petrochemical products, which took effect in July 2012. It was accompanied by, among other things, an insurance ban for oil shipments and a freeze on assets of the central bank of Iran (Borszik, Citation2016). This sanction severely cut off Iranian crude oil production and export in 2012 and 2013 (Panel (C) of ). Also, in March 2012, the Belgium-based Society for Worldwide International Financial Transfers (SWIFT) excluded Iranian banks from its network and, thereby, effectively prevented any foreign transactions with them through SWIFT, the world’s hub of electronic financial transactions (International Crisis Group, Citation2013, pp. 13–14). The financial sanction adversely affect Iran’s financial system and financial resources provided to the private sector by banks dropped after the imposition of international sanctions in 2012 (see Panel (E) of ). Oil sanctions combined with international financial, banking, and insurance sanctions have amplified the destructive effects of sanctions on the Iranian economy (Farzanegan, Mohammadikhabbazan, & Sadeghi, Citation2015). Panel (D) of shows that Iran’s foreign trade was directly influenced by the imposed sanctions in 2012. As depicted in Panel (A) of , because of the restrictions of sanctions on the import of raw materials and intermediate goods and also export products, production growth in the manufacturing sector became negative for eight consecutive quarters in 2012 and 2013. Dizaji and Van Bergeijk (Citation2013), Felbermayr, Syropoulos, Yalcin, and Yotov (Citation2019), and Farzanegan et al. (Citation2015) also confirm that the international sanctions imposed in 2012 negatively impact Iran’s real sectors. Gholipour (Citation2020) shows that the sanctions reduce investment in manufacturing sectors.

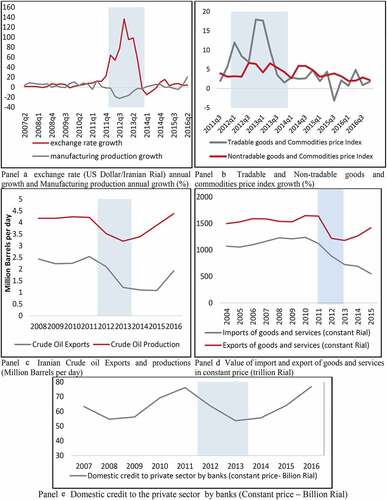

Figure 1. Macroeconomic and financial indicators during the sanctions.

A sharp increase in prices level was one of the consequences of the imposition of international sanctions. Restricted access to foreign exchange reserves and reduction of Foreign exchange earnings led to a jump in the exchange rates. As shown in Panel (A) of , the local currency (Iranian Rial) severely depreciated in 2012–2013. The annual growth of the US dollar/Iranian Rial exchange rate exceeded 100 percent in some quarters. This jump in the exchange rate caused a considerable increase in tradable goods and commodities prices (see Panel B of ). Ghorbani Dastgerdi et al. (Citation2018) illustrate that heavy sanctions created instability in the Iranian foreign exchange market and as a result increase inflation.

According to data presented in , the significant effects of the international sanction on Iranian economic variables lasted until 8 quarters after the imposition of sanctions. Dizaji and Van Bergeijk (Citation2013) find similar results and show the adverse effects of sanctions on Iranian macroeconomic variables are only significant in the first two years. This finding is also consistent with Hufbauer, Schott, and Elliott (Citation2008) finding. Accordingly, in this paper, eight quarters after the imposition of sanctions (2012q1-2013q4) are considered an effective period of the sanctions (hereafter the sanctions period). Thus, to quantify the effect of financial constraints on output pricing behavior, this paper focuses on price changes during the sanctions period (8 quarters after the imposition of sanctions in 2012q1).

In general, the imposition of international sanctions in 2012 generated a mixture of shocks that directly influenced domestic prices (in terms of local currency) in Iran. The severe exchange rate depreciation led to the jump in all tradable goods prices. Since other factors induce price changes, the increases in prices were not equal across the products and firms. In this paper, I examine whether financial constraints explain differences in price changes among the firms. Also, the role of some characteristics of firms is explored by statistical methods.

4. Data and methodology

The empirical analysis of this paper is based on a micro-level dataset consisting of data on prices and sales at the product-firm level and the inventory changes, and financial data at the firm level. The dataset is collected from the information of two main quarterly published reports of Iranian listed manufacturing companies: first, sale and production reports that include volumes and values of production and sale at the product level. Second, the financial statement reports.Footnote7 The final unbalanced dataset contains quarterly data on 2285 product-firm from 301 companies during the period 2007q3-2018q1. The sample period is selected in such a way that it covers before and after the imposition of sanctions in 2012 and their effective period (2012q1-2013q4).

reports the descriptive statistics (including mean, standard deviation, and median) of the relevant variables during the sample period. The statistics of price growth is reported in the first row of the table. Where

is the value of unit (as a proxy for price) good i in firm j at quarter t and

is annual sales growth that

is sale volume of good i in firm j at quarter t. Note that

and

are the only variables at the product-firm level and other variables are at the firm level.

Table 1. Descriptive statistics of the variables during the period 2007q3-2018q1.

This paper follows the approach introduced by Whited and Wu (Citation2006) for measuring the financial constraints of firms (). To calculate Whited and Wu index (WW index henceforth), I use the coefficients of WW index for Iranian companies that are estimated by Mahmoudzadeh, Nili, and Nili (Citation2016). However, the main results of the estimations are robust to the choice of different financial constraint proxies (see section 5.4).

To estimate the effect of financial constraints on price changes and to consider the change in this relationship during the sanctions period, following Gilchrist et al. (Citation2017) and Kim (Citation2021), I design the below equation:

Where is the financial constraint index for firm j in time t. In the baseline regressions, WW index is used as a proxy for financial constraints (

). To identify how the financial constraints affect the price growth during the sanctions period, the interaction of the financial constraint index (

) and the sanctions period dummy variable (

which equals 1 between 2012q1-2013q4 and 0 otherwise) is added to the regression. The sales growth (

) captures the cyclical changes in demand. In addition,

is the vector of corresponding firm-level control variables that include inventory change to sale ratio

, market share

, and industry-level price growth corresponding to firm j

(where

belongs to k and k is 4 digit ISIC Rev.4 industry). The inventory change ratio captures precautionary liquidity demand that may arise from the need to finance inventories during a downturn (Gilchrist et al., Citation2017). In addition, Market share (

) controls for firm’s market power and price inflation at the industry level (

) control any industry-level factors that influence costs and prices of firm j. As proposed by Reed (Citation2015) and Bellemare, Masaki, and Pepinsky (Citation2017), all explanatory variables in Equationequation (1)

(1)

(1) are lagged by one period to mitigate the endogeneity problem. Also, time and firm fixed effects (

,

) are introduced in the regression.

The coefficient of the financial constraint index () in Equationequation (1)

(1)

(1) shows the average effect of financial constraints on the pricing behavior of firms during the sample period. Also, the coefficient of the interaction variable between the sanction dummy variable and the financial constraint index (

) identifies the differential effect of financial constraints of firms during the sanctions period. Since the output prices dramatically and sharply changed after the imposition of sanctions, this period can be used as a source of identification of the financial constraint effect on the pricing behavior of firms. So the interaction term’s coefficient more accurately captures the effect of financial constraints.

5. Estimation result

5.1. Main results

The Weighted fixed effect regression is used in estimating Equationequation (1)(1)

(1) , where the weight is the real value of sales. All the estimations include time and firm-fixed effects, and standard errors are clustered at the product level.Footnote8 reports the results of the estimations in which the financial constraint index (

) is WW index. Column 1 presents the estimation results of Equationequation (1)

(1)

(1) with control variables. The results confirm that more financially restricted firms set their output prices significantly lower than their counterparts and this relationship between financial constraint and pricing behavior becomes stronger in the sanctions period. According to the estimated coefficients, a one standard deviation increase in WW financial constraint index implies a decrease in output price equal to %2 (29.88*0.07) and this reduction of prices is larger during the sanctions period and raises to %4 (29.88*(0.07 + 0.063)). In other words, more financially restricted firms set their output prices lower than their counterparts. The price differences prices created by financial constraints are larger during the sanctions period. Note that all prices increased on average due to the currency depreciation in the sanctions period. But, financially constrained firms rose their price significantly less than other firms in that period.

Table 2. Financial constraint effect on firms’ price setting behavior during the imposition of sanctions.

To capture the effect of change in firms’ productivity, total factor productivity (TFP) growth is introduced to the estimation as a control variable.Footnote9 The result reported in column (2) shows that the findings remain unchanged. Also, column (3) presents the estimation results with the sanction dummy variable (Sanc) as an independent variable instead of time fixed effect variables (since Sanc is a time dummy variable, collinearity between Sanc and time fixed effects omits one of them). The results indicate that the identified effect of financial constraint on pricing after the sanction is not sensitive to variation in control variables. Furthermore, the estimation results of Equationequation (1)(1)

(1) without control variables (shown in Column (4)) confirm that findings are robust to the exclusion of the control variables. Column (5) presents the results from estimating Equationequation (1)

(1)

(1) using annual data instead of quarterly data. Since coefficients of the financial constraint index and FCj,t-1*Sanc are significant and negative, it concludes that the main result is robust to changing the data frequency.

To address the potential endogeneity of firms’ financial constraints as the sanctions imposed, column (6) presents the results from estimating Equationequation (1)(1)

(1) using firms’ pre-sanctions financial constraints indexFootnote10 (FCj,2011q4 considered the index in 2011q4 before the sanctions were imposed). The coefficient of FCj, 2011q4*Sanc is negative and significant that showing the restrictions on access to external financial resources during the imposition of sanctions force firms to set their output price lower than others to boost their internal financial resource by increasing the sales.

Overall, it can be concluded that the financial constraints of firms have a significant effect on price-setting behavior, and financially constrained firms keep their prices down to increase their sales income. This aggressive strategy made a larger difference between the prices of financially constrained and unconstrained firms after imposing the shocks like imposition of sanctions.

5.2. Which restrictions of sanction were effective on pricing behavior?

The economy is affected by the sanctions through different channels such as restrictions on export, import, and investment. The intensity of each channel’s effect on firms is related to their various characteristics. So categorizing the firms based on their features allows investigating the effect of main channels separately and answering this question: Which aspect of the sanctions makes financially constrained firms set the lower prices?

To answer the question, the effects of restrictions on exports and imports are separately estimated in this section. The sanctions restricted firms’ access to export markets and therefore acted as a negative demand shock for export-oriented firms. Also, the sanctions acted as a negative supply shock for import-dependent firms that their access to the imported inputs is restricted. For determining which restrictions force financially constrained firms to set their price lower than their counterparts, I split the firm sample into four sub-samples based on firms’ export intensity index EXPi,t (ratio of export income to total income), and import dependency index IMPi,t (ratio of imported input to cost of goods sold) before the sanctions period. The estimation results of Equationequation (1)(1)

(1) in these subsamples are shown in the first four columns of . The estimation of columns (1) and (2) include firms with positive export income before the sanctions (Expj,2011q4 > 0), and the estimation of columns (3) and (4) include firms with no export income before the sanctions (Expj,2011q4 = 0). Also, estimation samples in columns (1) and (3) include firms without direct import dependency (Impj,2011q4 = 0), and columns (2) and (4) estimate the equation among firms with positive import dependency (Impj,2011q4 > 0). The estimated coefficients of the interaction term (FCj,t-1 *Sanc) are negative and significant only in the first two estimations that include only exporter firms, and changing the import dependency across the sub-samples does not significantly affect the result. So, the effect of financial constraints depends on whether firms are an exporter or not, and the import dependency index is not the relevant variable in this relationship. To support this finding, the export intensity index EXPi,t and import dependency index IMPi,t and their interactions with FCj,t-1*Sanc (as triple interactions) are introduced in the regression and the results are reported in column (5). The results show the triple interaction of export intensity has a significant and negative effect on output price while the coefficient of triple interaction of import dependency index is not significant. So, Financial constraints lead to lower prices only in exporter firms, and the degree of import dependency does not have a significant role in this relationship. So, only exporter firms that experienced a negative demand shock after the sanction set their price lower to reduce the financial pressures. Also, the degree of dependency on imported inputs does not play a significant role in the relationship, and the supply shock of the sanctions that affected import-dependent firms did not impact on pricing behavior of financially constrained firms. Indeed, the export intensity index and import dependency index are two proxies for the degree of exposure of firms to international sanctions. The results show that when being exposed to the sanctions is measured by the export intensity index, the degree of exposure of firms to international sanctions has affected the relationship between financial constraints and output pricing.

Table 3. Role of export orientation and import dependency after the sanction imposition.

In general, the driver of price change plays a critical role in the relationship between financial constraints and prices. So, financially constrained firms keep their output price lower (relative to their counterparts) only after a negative demand shock but not after a supply shock.

5.3. Does ownership structure matter?

Some studies such as Thomadsen (Citation2005), Emmons and Prager (Citation1997), McAndrews and Rob (Citation1996), and Zhao, Savage, and Chen (Citation2008) show that ownership structure influence on pricing behavior of firms. Emmons and Prager (Citation1997) find that ownership status affects price changes, and non-private ownership is associated with lower prices. In this section, I test whether the ownership structure of firms impacts the pricing behavior of the constrained firms after the imposition of the sanctions. To do so, the firm sample is split based on whether the government partially owned firms or not. The results from estimating Equationequation (1)(1)

(1) among firms that are partially and directly owned by the government, reported in column (1) of , show that the estimated coefficient of FCj,t-1*Sanc is negative and significant. Moreover, this coefficient is insignificant for firms not owned directly by the government (the result presented in column (2)). The result remains valid when besides direct ownership, indirect ownershipFootnote11 is considered as a benchmark for splitting the sample (column 3 of ). So having ownership relationships with the government is a determinant factor for output pricing of financially constrained firms.

Table 4. Ownership structure and pricing behavior after the sanction imposition.

5.4. Robustness check

In this section, several tests are carried out to ascertain the robustness of the findings. First, I evaluate the sensitivity of the results to alternative measures of financial constraint. So far, I have used Whited and Wu index (WW index) for measuring financial constraints at the firm level. Another measure that has been proposed in the literature to assess financial constraints is the Dividend payout ratio (the total amount of dividends paid out to shareholders relative to the net income). Column (1) of indicates the results of estimation using the Dividend payout ratio as the financial constraint index (a higher dividend payout ratio indicates less financial constraint). The result confirms that after the imposition of sanctions, firms with lower dividend payout ratios (financially constrained firms) set their prices lower to increase their internal cash flows. The financial constraint index in column (2) is defined based on Nickell and Nicolitsas’s (Citation1999) study. They introduced the borrowing rate ratio (ratio of interest payments to cash flow) as a measure of financial pressure. The negative relationship between output prices and the degree of financial restriction after the imposition of the sanctions remains significant with using Nickell and Nicolitsas (Citation1999) index as a proxy for financial constraint. In the third column of , I use deciles of Whited and Wu index (WW index) as a categorical index of financial constraint. So firms are divided into ten groups based on the degree of financial constraint. Since the estimated coefficient of the interaction term (FCj,t-1*Sanc) is negative and significant it can be concluded that the finding remains robust. Moreover, To show that the results are robust to different estimation methods, the instrumental variable regression method is used to estimate Equationequation (1)(1)

(1) . In these estimations, three measures of financial constraints (which are directly used as a proxy of financial constraint index in Columns (1) to (3)) are applied as an instrument variable of financial constraint (FCj,t). The reported results in Columns (4) to (6) confirm that the effect of the financial constraint index after the sanction is negative and significant. Generally, the link between financial position and pricing behavior of firms is not sensitive to the definition of financial constraint.

Table 5. Different proxies for financial constraint measure.

Second, I check the robustness of the results by changing the estimation period and the definition of the sanction dummy variable. So far, the estimations period has been 2011q1 to 2018q1, and the sanction dummy variable (Sanc) has been equal to 1 between 2012q1-2013q4 and zero otherwise. The results from estimating Equationequation (1)(1)

(1) using different estimation periods are reported in columns (1) and (2) of (change to 2011q1- 2015q1 and 2007q3-2018q1 respectively). Also, the definition of the sanction dummy variable is changed in column (3) (equal to 1 between 2012q2-2014q1 and zero otherwise). The estimated coefficients of the interaction variable FCj,t-1*Sanc are negative and significant in all three estimations. So, the result is robust to change in the estimation period and definition of the sanction dummy variables.

Table 6. Estimation results with different estimation periods and the sanction dummy variable.

Third, the reported results in previous sections are based on an unbalanced dataset. For ensuring that the imbalance of the dataset does not distort the main findings, the relationship is estimated by using semi-balanced and balanced datasets. Column (1) (Column (2)) in reports the results from estimating the relationship using a dataset that includes units (at product-firm level) with at least 10 observations (20 observations) during the estimation period. Moreover, estimation results based on a fully balanced dataset are reported in column (3). The coefficients of the interaction term remain negative and significant. So despite the reduction of observations in these cases, the main results do not change, and it is concluded that the imbalance of the panel data did not significantly change the main results.

Table 7. Considering the imbalance of the panel data in the estimations.

According to the literature and data analysis (see ) the effects of the sanctions on Iranian economic variables lasted until 8 quarters after the imposition. One approach to consider the effect of financial constraints on the pricing behavior of firms during these 8 quarters is to compare output prices before and after the sanctions period. So the definition of the dependent variable changed to =

. It means that I measure the effect of the explanatory variables on the cumulative change of output price during the eight quarters. The estimation results are presented in . The observations of four quarters after the sanction 2014q1 to 2014q4 are used in these estimations. Estimations (1) and (3) use FCj,t-8 as a proxy for financial constraint, and estimations (2) and (4) use the financial constraint index for the last quarter before the imposition of sanctions (2011q4). All reported coefficients of the financial constraint index in are negative and strongly significant. Thus, using this approach indicates that the estimated effect of financial constraints on the pricing of firms during the sanctions period is robust and does not distort by changing the methods.

Table 8. Cumulative effect on output price after the sanction imposition.

6. Conclusion

Financial constraints caused by the financial market frictions and incompleteness are one of the main channels that the financial sector influences the real sector. According to the literature, the firm’s performance measures such as production growth, sale growth, investment, and return on assets are affected by the presence of financial constraints. This study examines whether financial constraints impact the pricing of firms. The hypothesis in this paper is that financially constrained firms set their prices lower than other firms to reduce the pressures of liquidity shortages. This hypothesis is tested by using product-firm level data on Iranian firms (including 2208 products from 301 firms) during the period 2007q3-2018q1.

According to the estimation results, during the whole sample period, financial constraints force firms to set their outputs prices about 2 percent lower than their competitors and this difference in the prices rises to 4 percent after the imposition of the sanctions. So the financial constraints cause a difference in price adjustments across the firms after a sharp increase in the prices (due to the exchange rate shock). Hence, the relationship between the degree of financial constraints and price changes remains valid when prices are rising.

Also, to understand which restrictions of the sanctions make financially constrained firms set the lower prices, the relationship is estimated in subsamples split based on the firm’s dependency on output exports and input imports. The results show financial constraints lead to lower prices only in export-oriented firms and the degree of import dependency is not a relevant variable in the relationship between output pricing and financial constraint. In other words, only exporter firms that experienced a negative demand shock after the sanction set their price lower to solve the problem of restrictions on access to external financing. The supply shock of the sanctions that affected import-dependent firms did not significantly impact on pricing behavior of financially constrained firms. Thus, drivers of price changes play a critical role in the relationship between financial constraints and prices. Furthermore, the estimation results indicate that the effect of financial constraints on pricing depends on the ownership structure of firms in such a way that only firms that are directly and indirectly owned by the government, reduce their output price. The present study supports policy intervention to strengthen the financial infrastructure to promote the development of the financial sector to reduce price dispersion. The dataset used in this study includes information on listed companies and the lack of data on unlisted companies can be a primary limitation to the generalization of these results. Future research could investigate the relationship between firms’ financial situation among cross‐country data to consider the effect of environmental and institutional factors. Also, studying the influence of financial factors on the frequency of price changes will improve our understanding of the influential factor in the pricing decision-making process.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Notes on contributors

Sajad Ebrahimi

Sajad Ebrahimi is a senior researcher and faculty member at the Monetary and Research Institute (affiliated with the Central Bank of Iran). He graduated in Economics from the University of Tehran in 2015. His research and publication interests include financial economics and analysis of foreign currency and other financial markets. He published more than 20 papers in these areas. He earned the best paper award in finance studies from the 25th annual conference of Economic Research Forum in 2019.

Notes

1 See Brander and Lewis (Citation1986), Zingales (Citation1998), Busse (Citation2002), Kimura (Citation2013), Gilchrist et al. (Citation2017), Kim (Citation2021).

2 According to studies, financial development changes the market and firms’ structures and enhances the probability an individual starts his own business, favors entry, increases competition, and promotes growth of firms (Guiso, Sapienza, & Zingales, Citation2004). Arellano, Bai, and Zhang (Citation2012) and Gagliardi (Citation2009) show financial development change firm growth pattern and financial structures. Love and Zicchino (Citation2006) and Lerskullawat (Citation2019) find that development of the financial sector impact on firm’s investment decision-making. Firms’ decision-making of exporting and entry to export markets are also affected by the degree of financial development (Kumarasamy & Singh, Citation2018). Moreover, the severity of financing constraints is significantly larger in countries with less developed financial systems (Love & Zicchino, Citation2006). So, the relationship between firms’ decision-making and financial constraints can be influenced by the degree of financial development.

3 Studies have documented that the economic sanctions have direct adverse effects on trade (Afesorgbor, Citation2019; Caruso, Citation2003; Hufbauer et al., Citation2008; Yang, Askari, Forrer, & Teegen, Citation2004) and negatively influence macroeconomic variables. Some studies have illustrated that economic sanctions contract real sectors and reduce economic growth (Evenett, Citation2002; Hufbauer et al., Citation2008; Neuenkirch & Neumeier, Citation2015).

4 Sanctions increase net capital outflows of targeted states by rising political risks and leading to currency depreciation. Peksen and Son (Citation2015) show that economic sanctions are likely to trigger currency collapses and instigate currency crises. Also, Hatipoglu and Peksen (Citation2018) demonstrate that sanctions are likely to raise the probability of banking crises.

5 Iran’s nuclear program is a scientific effort by Iran to research and develops nuclear technology that is inherently multipurpose. Iran has declared that its nuclear program is exclusively for peaceful purposes. US and European countries were concerned about the possible use of nuclear technology for weapons manufacturing in case of Iran and imposed sanctions to compel Iran to restrict its nuclear program.

6 Iran’s economy has been plagued by various US sanctions since 1979 which have had much less impact than the international sanctions.

7 Data are obtained from Mabna (Rahavard) which collects data on companies listed on the Tehran Stock exchange (TSE) from their Published financial statements and other information in www.codal.ir (website belongs to the Securities and Exchange Organization of Iran (SEO)). Since there are disclosure obligations, all listed companies are included in the sample.

8 In both finance and asset pricing empirical work, researchers are often confronted with panel data. In these data sets, the residuals may be correlated across firms or across time, and OLS standard errors can be biased (Petersen, Citation2009). Using clustered standard errors is one solution to this bias problem which suggested by studies (such as Williams (Citation2000), Rogers (Citation1994) Angrist and Pischke (Citation2009), and Arellano (Citation1987)).

9 Total Factor Productivity (TFP) is estimated with using Tian and Twite (Citation2011) approach in which the Solow residual method applied to measure TFP in panel data framework.

10 As described by studies like Antonakis, Bendahan, Jacquart, and Lalive (Citation2014) applying the difference in differences (DID) approach can solve the endogeneity problem and make identification of causal relationship possible. However, some conditions must be met to use this technique. In this method, the occurrence of the event (sanction here) should not affect the benchmark variable (financial constraints here) that defines the control and treatment groups. Roberts and Whited (Citation2013) stated that to identify the causal effect in DID approach, the variables should be unaffected by the event. Using a pre-sanction period for FC help to ensure that the grouping of companies based on financial constraints is not affected by the imposition of sanction event.

11 Indirect ownership means the firms partially owned by large holding that connected to the government (including holding companies related to Iran’s social security agent, Bonyad Mostazafan Holding, Astan Ghods Razavi Holding and the Execution of Imam Khomeini’s Order (EIKO).

References

- Afesorgbor, S. K. (2019). The impact of economic sanctions on international trade: How do threatened sanctions compare with imposed sanctions? European Journal of Political Economy, 56, 11–26.

- Angrist, J. D., & Pischke, J. S. (2009). Mostly harmless econometrics: An empiricist’s companion. Princeton: Princeton university press.

- Antonakis, J., Bendahan, S., Jacquart, P., & Lalive, R. (2014). Causality and endogeneity: Problems and solutions. The Oxford Handbook of Leadership and Organizations, 1, 93–117.

- Arellano, M. (1987). Computing robust standard errors for within-groups estimators. Oxford Bulletin of Economics and Statistics, 49(4), 431–434.

- Arellano, C., Bai, Y., & Zhang, J. (2012). Firm dynamics and financial development. Journal of Monetary Economics, 59(6), 533–549.

- Baker, S. R., Sun, S. T., & Yannelis, C. (2020). Corporate taxes and retail prices (No. w27058). Stanford, Calif.: National Bureau of Economic Research.

- Balleer, A., Hristov, N., & Menno, D. (2020). Menu costs, the price gap distribution and monetary non-neutrality: The role of financial constraints. Centre for Economic Policy Research, Discussion Paper DP11790.

- Ball, L., & Mankiw, N. G. (1994). Asymmetric price adjustment and economic fluctuations. The Economic Journal, 104(423), 247–261.

- Bellemare, M. F., Masaki, T., & Pepinsky, T. B. (2017). Lagged explanatory variables and the estimation of causal effect. The Journal of Politics, 79(3), 949–963.

- Borenstein, S., & Rose, N. L. (1995). Bankruptcy and pricing behavior in US airline markets. The American Economic Review, 85(2), 397–402.

- Borszik, O. (2016). International sanctions against Iran and Tehran’s responses: Political effects on the targeted regime. Contemporary Politics, 22(1), 20–39.

- Brander, J. A., & Lewis, T. R. (1986). Oligopoly and financial structure: The limited liability effect. The American Economic Review 76 (5) , 956–970.

- Busse, M. (2002). Firm financial condition and airline price wars. RAND Journal of Economics, 33(2), 298–318.

- Caruso, R. (2003). The impact of international economic sanctions on trade: An empirical analysis. Peace Economics, Peace Science, and Public Policy 9 (2), , 1–29.

- Chevalier, J. A., & Scharfstein, D. S. (1996). Capital-market imperfections and countercyclical markups: Theory and evidence. American Economic Review, 86(4), 703–725.

- Dasgupta, S., & Titman, S. (1998). Pricing strategy and financial policy. The Review of Financial Studies, 11(4), 705–737.

- Dizaji, S. F., & Van Bergeijk, P. A. (2013). Potential early phase success and ultimate failure of economic sanctions: A VAR approach with an application to Iran. Journal of Peace Research, 50(6), 721–736.

- Duca, I., Montero, J. M., Riggi, M., & Zizza, R. (2017). I will survive. Pricing strategies of financially distressed firms. Pricing strategies of financially distressed firms (March 28, 2017). Bank of Italy Temi di Discussione (Working Paper) No, 1106.

- Eaton, J., & Engers, M. (1999). Sanctions: Some simple analytics. American Economic Review, 89(2), 409–414.

- Emmons, W. M., III, & Prager, R. A. (1997). The effects of market structure and ownership on prices and service offerings in the US cable television industry. The Rand journal of economics, 732–750.

- Erol, T. (2003). Capital structure and output pricing in a developing country. Economics Letters, 78(1), 109–115.

- Erol, T. (2005). Corporate debt and output pricing in developing countries: Industry-level evidence from Turkey. Journal of Development Economics, 76(2), 503–520.

- Evenett, S. J. (2002). The impact of economic sanctions on South African exports. Scottish Journal of Political Economy, 49(5), 557–573.

- Farzanegan, M. R., Mohammadikhabbazan, M., & Sadeghi, H. (2015). Effect of oil sanctions on the macroeconomic and household welfare in Iran: New evidence from a CGE model (No. 07-2015). MAGKS Joint Discussion Paper Series in Economics.

- Felbermayr, G., Syropoulos, C., Yalcin, E., & Yotov, Y. V. (2019). On the effects of sanctions on trade and welfare: New evidence based on structural gravity and a new database (No. 2131). Kiel Working Paper.

- Gagliardi, F. (2009). Financial development and the growth of cooperative firms. Small Business Economics, 32(4), 439–464.

- Ge, S. (2020). How do financial constraints affect product pricing? Evidence from weather and life insurance premiums. Fisher College of Business Working Paper, (2017-03), 27.

- Gholipour, H. F. (2020). Urban house prices and investments in small and medium-sized industrial firms: Evidence from provinces of Iran. Urban Studies, 57(16), 3347–3362.

- Ghorbani Dastgerdi, H., Yusof, Z. B., & Shahbaz, M. (2018). Nexus between economic sanctions and inflation: A case study in Iran. Applied Economics, 50(49), 5316–5334.

- Gilchrist, S., Schoenle, R., Sim, J., & Zakrajšek, E. (2017). Inflation dynamics during the financial crisis. American Economic Review, 107(3), 785–823.

- Giumelli, F., & Ivan, P. (2013). The effectiveness of EU sanctions. EPC Issue Paper, 76, 1–43.

- Glazer, J. (1994). The strategic effects of long-term debt in imperfect competition. Journal of Economic Theory, 62(2), 428–443.

- Guiso, L., Sapienza, P., & Zingales, L. (2004). Does local financial development matter? The Quarterly Journal of Economics, 119(3), 929–969.

- Hatipoglu, E., & Peksen, D. (2018). Economic sanctions and banking crises in target economies. Defense and Peace Economics, 29(2), 171–189.

- Hufbauer, G. C., Schott, J. J., & Elliott, K. A. (2008). Economic Sanctions Reconsidered. 3rd (hardcover+ CD). Washington, D.C.: Peterson Institute Press: All Books.

- International Crisis Group (2013). Spider web: The making and unmaking of Iran sanctions crisis group middle east report N°138.

- Khanna, N., & Tice, S. (2005). Pricing, exit, and location decisions of firms: Evidence on the role of debt and operating efficiency. Journal of Financial Economics, 75(2), 397–427.

- Kim, R. (2021). The effect of the credit crunch on output price dynamics: The corporate inventory and liquidity management channel. The Quarterly Journal of Economics, 136(1), 563–619.

- Kimura, T. (2013). Why do prices remain stable in the bubble and bust period? International Economic Journal, 27(2), 157–177.

- Kumarasamy, D., & Singh, P. (2018). Access to finance, financial development and firm ability to export: Experience from Asia–Pacific countries. Asian Economic Journal, 32(1), 15–38.

- Lam, S. L. (1990). Economic sanctions and the success of foreign policy goals: A critical evaluation. Japan and the World Economy, 2(3), 239–248.

- Lerskullawat, A. (2019). Financial development, financial constraint, and firm investment: Evidence from Thailand. Kasetsart Journal of Social Sciences, 40(1), 55–66.

- Levy, P. I. (1999). Sanctions on South Africa: What did they do? American Economic Review, 89(2), 415–420.

- Love, I., & Zicchino, L. (2006). Financial development and dynamic investment behavior: Evidence from panel VAR. The Quarterly Review of Economics and Finance, 46(2), 190–210.

- Mahmoudzadeh, A., Nili, F., & Nili, M. (2016). Cash conversion cycle and credit constraint: A theoretical/empirical synthesis. The Journal of Economic Studies and Policies, 3(1), 75–100.

- McAndrews, J. J., & Rob, R. (1996). Shared ownership and pricing in a network switch. International Journal of Industrial Organization, 14(6), 727–745.

- Neuenkirch, M., & Neumeier, F. (2015). The impact of UN and US economic sanctions on GDP growth. European Journal of Political Economy, 40, 110–125.

- Nickell, S., & Nicolitsas, D. (1999). How does financial pressure affect firms? European Economic Review, 43(8), 1435–1456.

- Peksen, D., & Son, B. (2015). Economic coercion and currency crises in target countries. Journal of Peace Research, 52(4), 448–462.

- Petersen, M. A. (2009). Estimating standard errors in finance panel data sets: Comparing approaches. The Review of Financial Studies, 22(1), 435–480.

- Phillips, G. M. (1995). Increased debt and industry product markets an empirical analysis. Journal of Financial Economics, 37(2), 189–238.

- Pichler, P., Stomper, A., & Zulehner, C. (2008). Why leverage affects pricing. The Review of Financial Studies, 21(4), 1733–1765.

- Reed, W. R. (2015). On the practice of lagging variables to avoid simultaneity. Oxford bulletin of economics and statistics, 77(6), 897–905. doi:10.1111/obes.12088

- Roberts, M. R., & Whited, T. M. (2013). Endogeneity in empirical corporate finance1 Constantinides, M., Stuz, R. In Handbook of the economics of finance (Vol. 2, pp. 493–572). North Holland, Amsterdam: Elsevier.

- Rogers, W. (1994). Regression standard errors in clustered samples. Stata Technical Bulletin, 3((13), 19–23).

- Secchi, A., Tamagni, F., & Tomasi, C. (2016). Export price adjustments under financial constraints. Canadian Journal of Economics/Revue Canadienne D’économique, 49(3), 1057–1085.

- Shin, G., Choi, S. W., & Luo, S. (2016). Do economic sanctions impair target economies? International Political Science Review, 37(4), 485–499.

- Showalter, D. M. (1995). Oligopoly and financial structure: Comment. The American Economic Review, 85(3), 647–653.

- Smeets, M. (2018). Can economic sanctions be effective? WTO Staff Working Papers, (ERSD-2018-03).

- Thomadsen, R. (2005). The effect of ownership structure on prices in geographically differentiated industries. RAND Journal of Economics 36 (4) , 908–929.

- Tian, G. Y., & Twite, G. (2011). Corporate governance, external market discipline and firm productivity. Journal of Corporate Finance, 17(3), 403–417.

- Whited, T. M., & Wu, G. (2006). Financial constraints risk. The review of financial studies, 19(2), 531–559. doi:10.1093/rfs/hhj012

- Williams, R. L. (2000). A note on robust variance estimation for cluster‐correlated data. Biometrics, 56(2), 645–646.

- Yang, J., Askari, H., Forrer, J., & Teegen, H. (2004). US economic sanctions: An empirical study. The International Trade Journal, 18(1), 23–62.

- Zhao, D., Savage, S. J., & Chen, Y. (2008). Ownership, location, and prices in Chinese electronic commerce markets. Information Economics and Policy, 20(2), 192–207.

- Zingales, L. (1998). Survival of the Fittest or the fattest? Exit and financing in the trucking industry. The Journal of Finance, 53(3), 905–938.