?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Both transformational and problematic platforms, corresponding to moderate and severe scam conditions, are considered abnormal in Chinese marketplace lending. This paper examines the impact of scams in marketplace lending on investor confidence and attention. We find that as the abnormal platform ratio increases, lenders are more likely to lose confidence and withdraw investments. They also become more concerned about the risks associated with marketplace lending and the entire industry. These effects are primarily driven by severe scam conditions. Additionally, the effects of severe scam conditions on investment withdrawals and industry-related news searches are contemporaneous, while there is a lag in the effects on searching for risk-related news. Furthermore, we also find that regulatory policies enhance individual sensitivity to severe scams, and severe scams result in greater capital outflows in first-tier regions and more significant levels of panic in other regions.

1. Introduction

Marketplace lending, also known as online lending or peer-to-peer lending (Tian & Wu, Citation2023; Vallee & Zeng, Citation2019), acts as an information intermediary between lenders and borrowers (Kowalewski et al., Citation2022), bridging the information gap. However, some platforms may engage in Ponzi schemes or face moral and liquidity risks. This can result in management fleeing, business model changes, or business closures. Consequently, borrowers may be unable to apply for new loans, and lenders may struggle to withdraw the principal and interest. A notable example is the Ezubao scam, one of the biggest online lending scam, which led to losses exceeding CNY 50 billion (US$ 7.6 billion) from 900 thousand lenders (Zhao et al., Citation2018).

The level of trust within marketplace lending significantly influences investment willingness (Qian & Lin, Citation2020). Scams can have a detrimental impact on the entire online lending market, particularly in the short term, as they erode lender confidence. Baidu’s aggregate search frequency, which is similar to the Google search trends, serves as a direct measure of individual attention in China (Chen et al., Citation2016). Consequently, individuals, particularly stakeholders, are undoubtedly paying attention to the peer-to-peer lending scams. However, the extent to which scam conditions can influence investor confidence and attention remains a relatively underexplored area.

This paper aims to address the questions mentioned above. We collect the trading data for the entire online lending market from the prominent marketplace lending portal, WDZJ, and collect the aggregate Baidu search trends for keywords related to marketplace lending risk and marketplace lending industry in the Chinese context. WDZJ classifies abnormal platforms into two categories: transformational platforms and problematic platforms. The transformational ratio corresponds to a moderate scam condition, while problematic ratio corresponds to a severe scam condition.Footnote1 We use the net capital inflow as a measure of investor confidence and Baidu search trends to measure investor attention.

Our findings indicate that as the abnormal platform ratio increases, lenders are more likely to lose confidence and withdraw investments. They also become more concerned about the risks associated with marketplace lending and the entire industry. These effects are predominantly driven by severe scam conditions. Additionally, the effects of severe scam conditions on investment withdrawals and industry-related news searches are contemporaneous, while there is a lag in the effects on searching for risk-related news. Furthermore, we also find that regulatory policies enhance individual sensitivity to severe scams, and severe scams result in greater capital outflows in first-tier regions and more significant levels of panic in other regions.

Our contribution to the literature is threefold. First, we demonstrate that severe scam conditions significantly erode investor confidence and induce higher levels of panic. It adds to the literature on the failure of the marketplace lending in China (Gao et al., Citation2021; He & Li, Citation2021; Liu et al., Citation2019), and offers valuable insights for future supervision and development of new financial formats. Second, while existing literature examines the impact of investor attention on capital market reactions (Chen et al., Citation2016; Zhang & Wang, Citation2015; Zhang et al., Citation2013), we focus on the effects of scam conditions on investor attention, shedding light on future research concerning adverse events in the financial market. Lastly, our study concentrates on investment withdrawals and investor attention as well as the dynamic effects of scam conditions, complementing existing research on lender size and trading volume (Chen et al., Citation2021).

The remainder of this paper is organized as follows. Section 2 reviews the related literature. Section 3 provides an overview of institutional background in our setting. Section 4 presents the details of our data as well as the summary statistics. Section 5 outlines our empirical methodology. Section 6 reports the baseline results, explores dynamic effects, analyses heterogeneous results, and conducts robustness tests. Finally, we conclude our paper in Section 7.

2. Literature review

Investor confidence and trust are significantly influenced by the financial and credit status of peer-to-peer lending platforms and their affiliations (Jiang et al., Citation2021; Yan et al., Citation2018). Platforms can enhance investor confidence by taking actions that accurately reflect real risks and effectively address information asymmetry (Caldieraro et al., Citation2018). The lenders will have increased confident and a higher likelihood of investment when borrowers provide more detailed financial information (Larrimore et al., Citation2011). Trust in both borrowers and platforms influences lenders’ willingness to lend. However, trust in borrowers has a more direct and effective impact (Chen et al., Citation2014). In the shock of peer-to-peer lending scams, lenders may lose confidence and become anxious. Chen et al. (Citation2021) find the platform absconding can significantly reduce the number of lenders and trading volume.

Individuals have limited attention, and attention is a scarce cognitive resource (Kahneman, Citation1973). Attention can be measured directly and indirectly. Indirect proxies for investor attention include trading volume (Gervais et al., Citation2001), front-page news events (Barber & Odean, Citation2008; Yuan, Citation2015), and specific events (Seasholes & Wu, Citation2007). In the digital age, people often use search engines to collect information, and their attention is palpable when they conduct searches (Da et al., Citation2011). Aggregate search frequency data from Google (Da et al., Citation2011) or Baidu (Zhang et al., Citation2013) provides a direct and unambiguous measure of investor attention. A growing body of literature explores the impact of Baidu search trends on abnormal stock returns and trading volumes (Zhang et al., Citation2013), future stock prices (Zhang & Wang, Citation2015), a firm’s future crash risk (Wen et al., Citation2019), market responses to macroeconomic events (Chen et al., Citation2016), and the effects on the trading volume and interest rates in the marketplace lending (Chen et al., Citation2020; He et al., Citation2021).

A burgeoning literature delves into the role of various factors on funding probability, default risk, and financing costs in marketplace lending. These factors encompass loan descriptions (Dorfleitner et al., Citation2016; Herzenstein et al., Citation2011), loan maturity (Croux et al., Citation2020), borrower appearance (Duarte et al., Citation2012; Jenq et al., Citation2015), social capital (Freedman & Jin, Citation2017; Jiang et al., Citation2020), network centrality (Chen et al., Citation2022), homophilous intensity (Li et al., Citation2023), race (Pope & Sydnor, Citation2011), gender (Chen et al., Citation2020; Li et al., Citation2020), education (Xu et al., Citation2020), debt-to-income ratios (Emekter et al., Citation2015), inflation (Nigmonov et al., Citation2022), and location (Chong & Wei, Citation2023; Wang et al., Citation2021). Additionally, a significant body of literature focuses on building models for predicting marketplace lending risk. Non-financial factors may hold greater importance than financial ones in determining investment decisions in the FinTech-based sector (Kou et al., Citation2021). Some clustering algorithms have proven effective in analyzing financial risks, such as fraud detection and credit rating (Kou et al., Citation2014; Li et al., Citation2021). Credit risk models based on similarity networks offer both high predictive accuracy and explainability (Giudici et al., Citation2020). The use of cost-sensitive multi-class classifiers for credit rating can reduce the total cost for peer-to-peer platforms (Wang et al., Citation2021). Moreover, machine learning models are increasingly employed for predicting bankruptcy, default rates, and credit scores (Bracke et al., Citation2019; Figini & Giudici, Citation2011; Giudici, Citation2001; Kou et al., Citation2021; Liu et al., Citation2022).

Overall, previous studies have primarily focused on the factors influencing investor confidence, the measurement of investor attention and its role in financial markets, as well as predictive models and determinants in marketplace lending. However, there remains a gap in the literature about the impact of scam conditions on investor confidence and attention. This gap serves as the motivation for our research, where we aim to investigate the effects of scam conditions on investment withdrawals and risk- and industry-related searches in the context of marketplace lending.

3. Institutional background

The first peer-to-peer lending platform, Zopa, was established in England in 2005. Subsequently, the emerging lending marketplaces are located worldwide, such as LendingClub and Prosper in the United States, Auxmoney and Smava in Germany, Renrendai and Ppdai in China. The online marketplace lending has exhibited exponential growth in developed economies such as the USA, now serving as an essential credit supplier to consumers (Tang, Citation2019). The market share of U.S. mortgage loans issued by FinTech lenders who offer a completely online application process increased from 2% to 8% from 2010 to 2016 (Fuster et al., Citation2019).

In China, the first peer-to-peer lending platform was established in 2007. By December 2019, the total volume of the Chinese online credit market amounted to approximately CNY 8863 billion (equivalent to US$ 1291 billion based on an exchange rate of 6.865). The total number of lenders and borrowers reached 180 million and 132 million, respectively, which accounts for equivalent to 12.79% and 9.43% of China’s population.Footnote2 The Chinese online lending market maintains an average interest rate of 12%, similar to the credit card’s installment rate. The maximum and minimum interest rates are 21.63% and 9.21%, respectively. The average loan duration is nearly 10 months, indicating that borrowers often seek short-term loans through online lending platforms. Notably, the online lending market in China was one of the largest globally (Nemoto et al., Citation2019). As of December 2018, the total lending volume amounted to approximately 20% of consumption loans provided to households provided by the traditional banking sector (Braggion et al., Citation2018). During the peak of the Chinese online peer-to-peer lending market, there were 3608 operating online lending platforms across all 31 provinces and municipalities of mainland China. The monthly turnover reached CNY 254 billion (equivalent to US$ 37 billion based on an exchange rate of 6.865).

However, Ezubao was established in July 2014, operating as a peer-to-peer lending-based Ponzi scheme, and it ceased trading in December 2015, ultimately closing down in February 2016. The Ezubao scam attracted about US$ 7.6 billion from 900 thousand lenders (Zhao et al., Citation2018). While Ezubao was not the first peer-to-peer lending scam in China, but it appeared to be the largest. In the short run, the downfall of Ezubao was likely to hurt the lenders’ confidence in peer-to-peer lending. In the long run, the Chinese regulators aimed to exert control over the peer-to-peer lending industry and introduce new regulations. The first public policy draft for regulating the peer-to-peer lending industry was issued by the China Banking Regulatory Commission in December 2015,Footnote3 marking the industry’s transition into an era of standardized development.

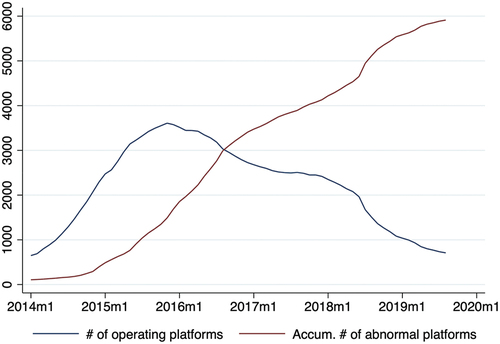

shows the peak in the number of operating platforms was observed in November 2015. Subsequently, the number of operating platforms steadily declined month by month following the Ezubao scam, and the accumulative number of abnormal platforms increased notably after the implementation of regulated policies. By August 2019, only 709 lending platforms were still providing intermediary services. The accumulative number of abnormal platforms reached 5912, including 3062 transformational platforms and 2850 problematic platforms. These classifications were based on WDZJ criteria. Transformational platforms transform their business, stop doing business, or stop applying for new loans, which tend to be problematic. Problematic platforms are runaway, difficulty in payment, closed their company, or intervened with economic investigation.

Figure 1. The number of marketplace lending platforms.

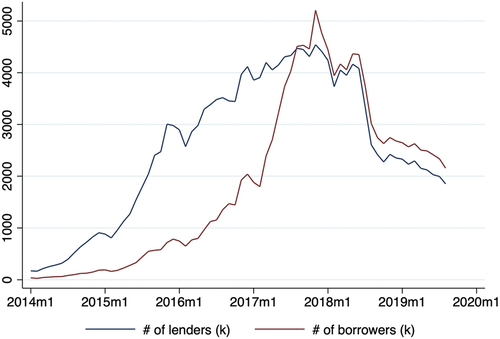

shows the number of monthly active lenders and borrowers in the Chinese peer-to-peer lending market. Following the emergence of the Ezubao scam and other abnormal events in the short run, there was a decline in the number of active lenders and borrowers. With the introduction of prudential supervision, the trends for the number of operating platforms, active lenders, and borrowers display an inverted U-shaped pattern.

Figure 2. The number of active lenders and borrowers.

4. Data

WDZJ.com is founded in October 2011 and focuses on disclosing information about the peer-to-peer lending industry. It serves as a powerful peer-to-peer portal website. Peer-to-peer lending platforms share their transaction data with WDZJ. After collecting transaction data at the platform level, WDZJ processes the data and publishes monthly industry records. Through this portal website, we can obtain monthly data from January 2014 to August 2019, which includes monthly trading volume, balance, the number of operating platforms, the number of transformational platforms, the number of problematic platforms, interest rates, duration, the number of active lenders, and the number of active borrowers.

The net capital inflow, calculated as the difference between the monthly balance and its lagged term, serves as an indicator of the capital flow within the peer-to-peer lending market, reflecting lenders’ confidence in this industry. Lenders exhibit greater confidence when capital flows into the peer-to-peer lending market. Conversely, when lenders withdraw investment, it indicates a lack of confidence among lenders in the peer-to-peer lending market. The ratio of abnormal platforms to the total platforms can be used to assess the prevalence of scams, with a higher ratio suggesting a higher incidence of fraudulent activities. We also calculate the ratios of transformational platforms and problematic platforms to assess various scam conditions.

Baidu index is a website that provides the aggregate search frequency by the Baidu search engine, covering various customers and regions in China.Footnote4 It’s similar to Google Trends. We can obtain the daily Baidu search trends for specific keywords. These daily search trends offer insights into the concerns of the customers. We gather search trends for “peer-to-peer collapse” and “peer-to-peer runaway” to measure monthly apprehensions related to market risk.Footnote5 Additionally, we collect the search trends for “peer-to-peer financing”, “peer-to-peer lending”, “WDZJ”, and “P2Peye” to measure monthly concerns within the industry.Footnote6 The mentioned keywords are relevant to the peer-to-peer lending risk and the peer-to-peer lending industry in the Chinese context. The higher the search trends for these keywords, the greater the level of concern.

reports the summary statistics for our final sample. The average net capital inflow in the peer-to-peer lending market is CNY 8.89 billion (equivalent to US$ 1.29 billion based on an exchange rate of 6.865). The highest monthly capital inflow recorded is CNY 57.75 billion, while the maximum monthly capital outflow is CNY 66.72 billion. Overall, approximately 3.80% of lending platforms show abnormalities in a given month, with the highest abnormal ratio reaching 14.99%. More specifically, the average transformational ratio stands at 1.95%, and the average problematic ratio is 1.85%. At the market level, the average interest rate is 12.16%, and loans have an average maturity of 9.35 months. The average number of active lenders per month is approximately 2.56 million, while the average number of active borrowers per month is 1.86 million.

Table 1. Summary statistics.

Panel B of provides summary statistics for the daily search trends of the mentioned keywords. The average daily search trends for the risk-related keywords, “peer-to-peer collapse” and “peer-to-peer runaway”, are 806 and 1197, respectively. The average daily search trends for the industry-related keywords, “peer-to-peer financing”, “peer-to-peer lending”, “WDZJ”, and “P2Peye”, are 6817, 7913, 10298, and 6422, respectively.

Panel C reports the monthly search trends related to the peer-to-peer lending risk and peer-to-peer lending industry. On average, the monthly search trends for peer-to-peer lending risk are 60.92 thousand, while the monthly search trends for the peer-to-peer lending industry are 956.94 thousand. Overall, it is evident that consumers are more focused on the peer-to-peer lending industry compared to their concerns about peer-to-peer lending risk.

5. Empirical strategy

Our empirical strategy relies on the OLS regressions, with control variables related to the peer-to-peer lending market. To examine the effects of the scam conditions on the lenders’ confidence, we estimate the following model,

where is the difference between the monthly balance and its lagged term, reflecting increased confidence when capital flows into the market and decreased confidence when capital flows out of the market.

is the peer-to-peer lending scam condition, which can be the abnormal ratio, transformational ratio, or problematic ratio.

is a vector of market-related variables, including interest rate, duration, number of active lenders, and number of active borrowers.

is a vector of year fixed effects, helping absorb the unobservable and confounding macroeconomic shocks. The observations span from January 2014 to August 2019. Therefore, we add year dummy variables for the years 2015 to 2019 to our model. For a comprehensive list of variables, please refer to the data section.

To estimate the effects of scam conditions on lenders’ concerns related to peer-to-peer lending risk, we employ the following model,

where is the monthly search trends for “peer-to-peer collapse” and “peer-to-peer runaway”, which are related to the peer-to-peer lending risk within the Chinese context. Increased search trends indicate heightened concerns. The rest of the variables are the same as in the model (1).

To estimate the effects of scam conditions on the lenders’ concerns regarding the peer-to-peer lending industry, we employ the following model,

where is the monthly search trends for “peer-to-peer financing”, “peer-to-peer lending”, “WDZJ”, and “P2Peye”, which are related to the peer-to-peer lending industry within the Chinese context. The rest of the variables are the same as in the model (1). Additionally, we investigate the dynamic pattern of the effect by incorporating lag terms for the scam conditions into the models (1) to (3).

Peer-to-peer lending scams have garnered the attention of Chinese regulators. In December 2015, regulators released the first public policy draft with the aim of exerting control over the peer-to-peer lending industry. The impact of scams on lenders’ confidence and concerns may vary in the pre-policy and post-policy periods. To estimate the heterogeneous effects across different policy stages, we re-estimate the regressions using pre-policy and post-policy subsamples.

As of the end of 2019, there were a total of 6606 peer-to-peer lending platforms located across all 31 provinces and municipalities in mainland China. More than 41% of these platforms were located in the first-tier regions, Guangdong, Beijing, and Shanghai. It’s important to note that the scale effects of peer-to-peer lending may differ between first-tier regions and other areas, and consumer literacy may also be different between these regions. Consequently, we re-estimate the regressions separately for first-tier regions and the other areas to examine the effects of scams in these distinct geographical regions.

6. Results

6.1. Baseline results

reports the estimates of the model (1), showing the effects of scams on the net capital inflow. In Columns (1) and (2), we examine the impact of abnormal ratio on the net capital inflow. The coefficients associated with the abnormal ratio are negative and highly significant at the 1% level, indicating that lenders tend to lose confidence and withdraw capital when confronted with scam conditions. These effects are economically significant, even after accounting for all control variables. Specifically, a one-standard-deviation increase in the abnormal ratio is associated with a substantial outflow of CNY 11.02 ( = 2.474 × 4.453) billion from the online lending market.

Table 2. Scams and net capital inflow.

Abnormal platforms can be categorized into two groups: transformational and problematic, corresponding to moderate and severe scam conditions. We also examine the effects of these specific scam conditions on the net capital inflow using the model (1). In Columns (3) and (4), we find that the coefficients of transformational ratio are negative but non-significant, while the coefficients of problematic ratio are negative and highly significant. This suggest that transformational conditions, such as transforming their business model, discontinuing operations, and ceasing to accept new loan applications, have non-significant effects on capital flow. In contrast, problematic conditions, such as running away, facing difficulties in making payments, closing their company entirely, and becoming subject to economic investigations, discourage lenders and result in capital outflows from the lending market. A one-standard-deviation increase in the problematic ratio is associated with a substantial outflow of CNY 9.78 ( = 1.569 × 6.234) billion. Consequently, the adverse effects of scams on investor confidence are primarily driven by severe scam conditions.

presents the estimates from the model (2), showing the effects of scam conditions on lenders’ concerns regarding marketplace lending risk. Columns (1) and (2) show the coefficients for the abnormal ratio are positive and highly significant at the 1% level. This suggests that lenders tend to become more concerned about the risk associated with marketplace lending when confronted with scam conditions. Notably, a one-standard-deviation increase in the abnormal ratio leads to a notable increase of 52 ( = 2.474 × 21.021) thousand search queries, which is equivalent to 85% of the sample average. Columns (3) and (4) show the effects of two specific scam conditions on risk-related concerns. The coefficients of transformational ratio are positive but non-significant, indicating that the moderate scam conditions have a limited impact on risk-related concerns. Conversely, the coefficients of problematic ratio are positive and highly significant. A one-standard-deviation increase in the problematic ratio results in a substantial increase of 46 ( = 1.569 × 29.382) thousand search queries, equivalent to 76% of the sample average. Therefore, the impact of scams on risk concerns is mainly driven by severe scam conditions.

Table 3. Scams and concerns of risk.

To further investigate the impact of scam conditions on lenders’ concerns, we examine their effects on lenders’ concerns of the marketplace lending industry. shows the estimates of the model (3). The coefficients of abnormal ratio are significantly positive at the 1% level, indicating that an increase in abnormal platforms leads to lenders paying more attention to the marketplace lending industry. Columns (3) and (4) show that severe scam conditions mainly drive the effects on industry concerns. A one-standard-deviation increase in the problematic ratio results in a substantial increase of 142 ( = 1.569 × 90.595) thousand search queries, equivalent to 15% of the sample average. Relative to the transformational platforms, problematic platforms have a more significant impact on consumers and society. Therefore, the effects of marketplace lending scams on the lenders’ confidence and concerns are primarily driven by severe scam conditions.

Table 4. Scams and concerns of industry.

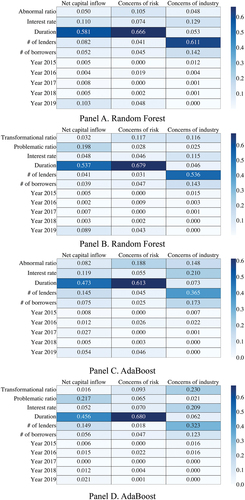

Random forest and adaptive boosting (AdaBoost) are commonly used machine learning models in various financial prediction tasks, including stock market prediction (Breitung, Citation2023; Khaidem et al., Citation2016; Park et al., Citation2022), bankruptcy prediction (Alfaro et al., Citation2008; Zhou & Lai, Citation2017), credit spread prediction (Mercadier & Lardy, Citation2019), credit risk measurement (Rao et al., Citation2020; Tang et al., Citation2019), and financial distress prediction (Sun et al., Citation2020). In this study, we employ random forest and AdaBoost regression models to estimate feature importance. We split half of the observations into the test set, ensuring that the number of out-of-sample observations are the same with the in-sample observations. Panels A and B in show the feature importance using random forest regression models, while Panels C and D use AdaBoost regression models. The results reveal that the feature importance associated with the abnormal ratio, transformational ratio, and problematic ratio are not the smallest, suggesting that these features can, to some extent, predict investor confidence and attention.

Figure 3. Heatmaps of the feature importance.

6.2. Dynamic estimate

In the analysis of dynamic effects, it’s important to consider the timing of lenders’ responses to marketplace lending scams. Typically, the withdrawal of investments or the search for related news is expected to occur after the realizing scams on certain marketplace lending platforms, at a daily level. However, our marketplace lending data is available at the monthly level. The contemporaneous or lagged effects of scam conditions at this level are still unexplored.

To better understand the dynamic pattern of these effects, we add lag terms for the transformational ratio and problematic ratio in the baseline models (1) to (3), and shows the dynamic estimate. Columns (1) and (2) reveal no contemporaneous or lag effects of the transformational ratio on investment withdrawals. There are only contemporaneous effects of the problematic ratio on investment withdrawals, without lagged effects. Columns (3) to (6) show that there are no lag effects of the transformational ratio on concerns related to marketplace risks or the entire market. However, there is a one-term lag effect of the problematic ratio on concerns related to risks but contemporaneous effects on concerns about the marketplace lending industry. Therefore, the effects of severe scam conditions on investor confidence and concerns are mainly contemporaneous, with lag effects only observed in concerns related to risks.

Table 5. Scams and investor confidence and attention: dynamic estimate.

6.3. Heterogeneity

In the context of marketplace lending regulation, it’s worth considering the impact of regulatory changes and the publication of policy drafts by Chinese regulators. In December 2015, the first policy draft was introduced to regulate marketplace lending. The marketplace lending platforms should be intermediary institutions and cannot enhance the borrowers’ credit line or create the capital pool in the prudential supervision stage. These regulatory signals can influence consumer behavior. To sharpen our analyses, we investigate the effects of scam conditions across different supervision stages. shows the estimates according to models (1) to (3).

Table 6. Scams and investor confidence and attention: heterogeneity across supervision stages.

Before the policy was introduced, we find that an increase in the transformational ratio results in capital outflows from the online lending market. It also leads to lenders paying more attention to risk-related search queries. However, the severe scam conditions can hardly affect the investment withdrawals (shown in the second column), lenders’ concerns about marketplace lending risk (shown in the fourth column), and concerns about the marketplace lending industry (shown in the sixth column) before the regulatory policy.

During the prudential supervision stage, lenders focus on the severe scam conditions rather than moderate ones. An increase in the problematic ratio leads to capital outflows from online lending market (shown in the first column), an increase in lenders’ attention to marketplace lending risk (shown in the third column) and marketplace lending industry (shown in the fifth column). Furthermore, the effects of moderate scams after the policy are statistically similar to these before the policy. However, the effects of severe scams on investor confidence and attention after the policy are significantly more prominent than those before the policy. It means that severe scams have a substantial impact on the market and cause enormous anxiety during the prudential supervision stage.

Guangdong, Beijing, and Shanghai are classified as first-tier regions, hosting over 41% of the marketplace lending platforms. The impact of scam-related shocks on the marketplace lending may vary between these first-tier regions and other regions. Additionally, consumer literacy and search trends may be different across these regions. We investigate the effects of scams across different areas according to models (1) to (3) and show the estimates in .

Table 7. Scams and investor confidence and attention: heterogeneity across regions.

The results reveal that the transformational ratio has a limited impact on the investor confidence and attention in both first-tier regions and other regions. Furthermore, the effects of transformational ratio on first-tier regions and other regions are statistically similar. Conversely, the problematic ratio is significantly and negatively associated with the investment withdrawals, and positively associated with concerns related to the risk and industry in both first-tier regions and other regions. However, the effects of the problematic ratio on capital outflows in first-tier regions are statistically more substantial than in other regions. The effects of the problematic ratio on the concerns related to risk and the marketplace lending industry in first-tier regions are statistically less than in other regions. This suggests that severe scams have a significant impact on investment withdrawals in first-tier regions and cause more substantial panic in other regions.

6.4. Robustness

In the robustness test section, we would like to re-estimate our results using alternative measurements for scam conditions. The abnormal platforms to operating platforms (ATO) ratio measures the total scam condition. The transformational platforms to operating platforms (TTO) ratio measures the moderate scam condition. Additionally, the problematic platforms to operating platforms (PTO) ratio measures the severe scam condition.

shows the effects on investor confidence and attention using alternative scam conditions. We observe a significant negative correlation between the ATO ratio and net capital inflow, and a positive association with lenders’ concerns of the risk and the industry. It means that as the scam ratio increases, lenders are more likely to withdraw their investments and become more attentive to risk and industry conditions. Notably, these effects are primarily driven by the PTO ratio, an alternative measure of the severe scam condition.

Table 8. Robustness tests: baseline results.

shows the dynamic effects of alternative scam conditions. The alternative moderate scam condition exhibits no lag or contemporaneous impact on investor confidence and attention concerning risks and the industry. In contrast, the alternative severe scam condition shows contemporaneous effects on investment withdrawal and the search for industry-related news, while it has both contemporaneous and lag effects on searching risk-related news.

Table 9. Robustness tests: dynamic estimate.

provides insights into the impacts of alternative scam conditions at different supervision stages. Before the policy implementation, the alternative moderate scam condition increases the capital outflows and leads to an increase in risk-related search queries. In contrast, the alternative severe scam condition has limited effects on the net capital inflows and concerns of the risk and the industry during this pre-policy period. However, during the prudential supervision stage, the influence of the alternative severe scam condition becomes highly significant. Lenders start to withdraw their investments and conduct more searches related to marketplace lending risk and marketplace lending industry. The impact of alternative severe scam conditions on the post-policy group is even more pronounced than before the policy was implemented.

Table 10. Robustness tests: heterogeneity across supervision stages.

shows the impacts of alternative scam conditions across different regions. The alternative moderate scam condition, as represented by the TTO ratio, shows limited effects on net capital inflow and search trends related to the risk and the industry in both first-tier regions and other regions. Conversely, the alternative severe scam condition, denoted by the PTO ratio, leads to the capital outflows from the market and an increase in risk- and industry-related search queries in both first-tier regions and other regions. However, it’s worth noting that scam events result in more significant capital outflows in the first-tier regions and trigger greater panic in the other regions.

Table 11. Robustness tests: heterogeneity across regions.

7. Conclusion

Marketplace lending, which acts as an intermediary between lenders and borrowers, serves as an essential supplier of credit to the consumers (Braggion et al., Citation2018; Jiang et al., Citation2021; Tang, Citation2019). Notably, China’s emerging peer-to-peer lending (marketplace lending) is the most extensive worldwide (Nemoto et al., Citation2019). However, nationwide marketplace lending scams, such as the Ezubao Ponzi scheme, have eroded lenders’ confidence in the emerging marketplace lending, leading to panic among investors.

Transformational platforms undergo changes in their business operations, typically a symptom of becoming problematic platforms. However, the problematic platforms experience more severe issues. Both the two types, corresponding to moderate and severe scam conditions, respectively, are considered abnormal. This paper uses the abnormal platform ratio, transformational platform ratio, and problematic platform ratio at the market level to gauge the prevalence of scam conditions. Drawing from data obtained from WDZJ and Baidu index, we investigate how these scam conditions impact lenders’ confidence and concerns about both the risk and industry.

As the abnormal platform ratio increases, lenders are more likely to lose confidence in marketplace lending and withdraw their investments. Simultaneously, they become more attentive to the risks associated with marketplace lending and the emerging marketplace lending industry. We find that the problematic platform ratio (indicative of severe scam conditions) predominantly drives our results. Furthermore, the effects of severe scam conditions on the withdrawing investment and searching industry-related news are contemporaneous, but there’s a lag in the effects on the searching for risk-related news.

As for the heterogeneous results, it’s challenging for severe scam conditions to affect lenders’ confidence and concerns before regulatory policies are in place. However, after the introduction of regulations, lenders’ responses are more pronounced in the presence of severe scam conditions. Moreover, severe scams result in capital outflows and increased searches about the risk of marketplace lending and marketplace lending industry in both first-tier regions and other regions. Nevertheless, severe scams result in greater capital outflows in the first-tier regions and induce more significant levels of panic in the other regions.

Given the observed impact of severe scam conditions on lenders’ confidence and attention, there is a clear need for strengthened regulatory oversight. Regulatory authorities should enhance their monitoring mechanisms to identify and address potential scams promptly, such as continuous assessment of platform operations. Policymakers should prioritize the timely implementation of regulatory measures to reduce the adverse effects of scams on the emerging marketplace. Considering the variation in the impact across regions, policymakers should provide additional support to lenders in regions more susceptible to panic, helping stabilize the market environment and reducing panic-induced reactions.

Acknowledgments

We would like to thank Inmaculada Martínez Zarzoso (the editor), the associate editor, two anonymous referees, and seminar participants at Shandong University for their helpful suggestions. Any remaining errors are our responsibility.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Jianwen Li

Jianwen Li earned his Ph.D. in Economics from Shandong University in 2020. Presently, he serves a research associate professor at the School of Economics, Shandong University, China. His research focuses on FinTech. Email: [email protected]

Yang Zhou

Yang Zhou is currently a Ph.D. candidate at the School of Economics, Shandong University, China. His research interests are digital finance and financial inclusion.

Jinyan Hu

Jinyan Hu obtained his Ph.D. in Economics from Shandong University in 2002. He currently holds the position of professor at both the School of Economics, Shandong University, China and the School of Economics, Qingdao University, China. His research focuses on informal finance, online lending, capital market and monetary policy.

Notes

1 Transformational platforms undergo changes in their business operations, either by transforming their business model, discontinuing operations, or ceasing to accept new loan applications. These changes are typically a response to problematic situations. Problematic platforms, on the other hand, experience more severe issues, which can include running away, facing difficulties in making payments, closing their company entirely, or becoming subject to economic investigations.

2 Data is from the WDZJ, one leading peer-to-peer industry information provider in China.

3 The China Banking Regulatory Commission published the initial public policy draft titled “Interim Measures for the Management of Business Activities of Online Lending Information Intermediary Institutions”.

4 As of October 2020, Baidu, with a dominant market share of 76.33%, stood as the most popular search engine in China, accounting for the majority of search queries conducted. (Source: StatCounter, https://gs.statcounter.com/search-engine-market-share/all/china/2020)

5 In the Chinese context, peer-to-peer collapse means “P2P爆雷”, and peer-to-peer runaway means “P2P跑路”.

6 In the Chinese context, peer-to-peer financing means “P2P理财”. Peer-to-peer lending means “网络借贷” or “网贷”. WDZJ means “网贷之家” and P2Peye means “网贷天眼”.

References

- Alfaro, E., García, N., Gámez, M., & Elizondo, D. (2008). Bankruptcy forecasting: An empirical comparison of AdaBoost and neural networks. Decision Support Systems, 45(1), 110–23. https://doi.org/10.1016/j.dss.2007.12.002

- Barber, B. M., & Odean, T. (2008). All that glitters: The effect of attention and news on the buying behavior of individual and institutional investors. The Review of Financial Studies, 21(2), 785–818. https://doi.org/10.1093/rfs/hhm079

- Bracke, P., Datta, A., Jung, C., & Sen, S. (2019). Machine learning explainability in finance: An application to default risk analysis. Working Paper.

- Braggion, F., Manconi, A., & Zhu, H. (2018). Can technology undermine macroprudential regulation? Evidence from peer-to-peer credit in China. Working Paper.

- Breitung, C. (2023). Automated stock picking using random forests. Journal of Empirical Finance, 72, 532–556. https://doi.org/10.1016/j.jempfin.2023.05.001

- Caldieraro, F., Zhang, J. Z., Cunha, M., Jr., & Shulman, J. D. (2018). Strategic information transmission in peer-to-peer lending markets. Journal of Marketing, 82(2), 42–63. https://doi.org/10.1509/jm.16.0113

- Chen, X., Chong, Z., Giudici, P., & Huang, B. (2022). Network centrality effects in peer to peer lending. Physica A: Statistical Mechanics and Its Applications, 600, 127546. https://doi.org/10.1016/j.physa.2022.127546

- Chen, X., Huang, B., & Ye, D. (2020). Gender gap in peer-to-peer lending: Evidence from China. Journal of Banking and Finance, 112, 105633. https://doi.org/10.1016/j.jbankfin.2019.105633

- Chen, X., Hu, X., & Ben, S. (2021). How individual investors react to negative events in the FinTech era? Evidence from China’s peer-to-peer lending market. Journal of Theoretical & Applied Electronic Commerce Research, 16(1), 52–70. https://doi.org/10.4067/S0718-18762021000100105

- Chen, D., Lai, F., & Lin, Z. (2014). A trust model for online peer-to-peer lending: A lender’s perspective. Information Technology and Management, 15(4), 239–254. https://doi.org/10.1007/s10799-014-0187-z

- Chen, J., Liu, Y. J., Lu, L., & Tang, Y. (2016). Investor attention and macroeconomic news announcements: Evidence from stock index futures. Journal of Futures Markets, 36(3), 240–266. https://doi.org/10.1002/fut.21727

- Chen, R., Qian, Q., Jin, C., Xu, M., & Song, Q. (2020). Investor attention on internet financial markets. Finance Research Letters, 36, 101421. https://doi.org/10.1016/j.frl.2019.101421

- Chong, Z., & Wei, X. (2023). Exploring the spatial linkage network of peer-to-peer lending in China. Physica A: Statistical Mechanics and Its Applications, 630, 129279. https://doi.org/10.1016/j.physa.2023.129279

- Croux, C., Jagtiani, J., Korivi, T., & Vulanovic, M. (2020). Important factors determining Fintech loan default: Evidence from a lendingclub consumer platform. Journal of Economic Behavior and Organization, 173, 270–296. https://doi.org/10.1016/j.jebo.2020.03.016

- Da, Z., Engelberg, J., & Gao, P. (2011). In search of attention. The Journal of Finance, 66(5), 1461–1499. https://doi.org/10.1111/j.1540-6261.2011.01679.x

- Dorfleitner, G., Priberny, C., Schuster, S., Stoiber, J., Weber, M., de Castro, I., & Kammler, J. (2016). Description-text related soft information in peer-to-peer lending–evidence from two leading European platforms. Journal of Banking and Finance, 64, 169–187. https://doi.org/10.1016/j.jbankfin.2015.11.009

- Duarte, J., Siegel, S., & Young, L. (2012). Trust and credit: The role of appearance in peer-to-peer lending. The Review of Financial Studies, 25(8), 2455–2484. https://doi.org/10.1093/rfs/hhs071

- Emekter, R., Tu, Y., Jirasakuldech, B., & Lu, M. (2015). Evaluating credit risk and loan performance in online peer-to-peer (P2P) lending. Applied Economics, 47(1), 54–70. https://doi.org/10.1080/00036846.2014.962222

- Figini, S., & Giudici, P. (2011). Statistical merging of rating models. Journal of the Operational Research Society, 62(6), 1067–1074. https://doi.org/10.1057/jors.2010.41

- Freedman, S., & Jin, G. Z. (2017). The information value of online social networks: Lessons from peer-to-peer lending. International Journal of Industrial Organization, 51, 185–222. https://doi.org/10.1016/j.ijindorg.2016.09.002

- Fuster, A., Plosser, M., Schnabl, P., & Vickery, J. (2019). The role of technology in mortgage lending. The Review of Financial Studies, 32(5), 1854–1899. https://doi.org/10.1093/rfs/hhz018

- Gao, M., Yen, J., & Liu, M. (2021). Determinants of defaults on P2P lending platforms in China. International Review of Economics & Finance, 72, 334–348. https://doi.org/10.1016/j.iref.2020.11.012

- Gervais, S., Kaniel, R., & Mingelgrin, D. H. (2001). The high‐volume return premium. The Journal of Finance, 56(3), 877–919. https://doi.org/10.1111/0022-1082.00349

- Giudici, P. (2001). Bayesian data mining, with application to benchmarking and credit scoring. Applied Stochastic Models in Business and Industry, 17(1), 69–81. https://doi.org/10.1002/asmb.425

- Giudici, P., Hadji-Misheva, B., & Spelta, A. (2020). Network based credit risk models. Quality Engineering, 32(2), 199–211. https://doi.org/10.1080/08982112.2019.1655159

- He, Q., & Li, X. (2021). The failure of Chinese peer-to-peer lending platforms: Finance and politics. Journal of Corporate Finance, 66, 101852. https://doi.org/10.1016/j.jcorpfin.2020.101852

- He, F., Qin, S., & Zhang, X. (2021). Investor attention and platform interest rate in Chinese peer-to-peer lending market. Finance Research Letters, 39, 101559. https://doi.org/10.1016/j.frl.2020.101559

- Herzenstein, M., Sonenshein, S., & Dholakia, U. M. (2011). Tell me a good story and I may lend you money: The role of narratives in peer-to-peer lending decisions. Journal of Marketing Research, 48(SPL), S138–S149. https://doi.org/10.1509/jmkr.48.SPL.S138

- Jenq, C., Pan, J., & Theseira, W. (2015). Beauty, weight, and skin color in charitable giving. Journal of Economic Behavior and Organization, 119, 234–253. https://doi.org/10.1016/j.jebo.2015.06.004

- Jiang, J., Liao, L., Wang, Z., & Zhang, X. (2021). Government affiliation and peer-to-peer lending platforms in China. Journal of Empirical Finance, 62, 87–106. https://doi.org/10.1016/j.jempfin.2021.02.004

- Jiang, J., Liu, Y. J., & Lu, R. (2020). Social heterogeneity and local bias in peer-to-peer lending–evidence from China. Journal of Comparative Economics, 48(2), 302–324. https://doi.org/10.1016/j.jce.2019.11.001

- Kahneman, D. (1973). Attention and effort. Prentice-Hall.

- Khaidem, L., Saha, S., & Dey, S. R. (2016). Predicting the direction of stock market prices using random forest. arXiv preprint arXiv:1605.00003.

- Kou, G., Olgu Akdeniz, Ö., Dinçer, H., & Yüksel, S. (2021). Fintech investments in European banks: A hybrid IT2 fuzzy multidimensional decision-making approach. Financial Innovation, 7(1), 39. https://doi.org/10.1186/s40854-021-00256-y

- Kou, G., Peng, Y., & Wang, G. (2014). Evaluation of clustering algorithms for financial risk analysis using MCDM methods. Information Sciences, 275, 1–12. https://doi.org/10.1016/j.ins.2014.02.137

- Kou, G., Xu, Y., Peng, Y., Shen, F., Chen, Y., Chang, K., & Kou, S. (2021). Bankruptcy prediction for SMEs using transactional data and two-stage multiobjective feature selection. Decision Support Systems, 140, 113429. https://doi.org/10.1016/j.dss.2020.113429

- Kowalewski, O., Pisany, P., & Ślązak, E. (2022). Digitalization and data, institutional quality and culture as drivers of technology-based credit providers. Journal of Economics and Business, 121, 106069. https://doi.org/10.1016/j.jeconbus.2022.106069

- Larrimore, L., Jiang, L., Larrimore, J., Markowitz, D., & Gorski, S. (2011). Peer to peer lending: The relationship between language features, trustworthiness, and persuasion success. Journal of Applied Communication Research, 39(1), 19–37. https://doi.org/10.1080/00909882.2010.536844

- Li, X., Deng, Y., & Li, S. (2020). Gender differences in self-risk evaluation: Evidence from the renrendai online lending platform. Journal of Applied Economics, 23(1), 485–496. https://doi.org/10.1080/15140326.2020.1797338

- Li, T., Kou, G., Peng, Y., & Philip, S. Y. (2021). An integrated cluster detection, optimization, and interpretation approach for financial data. IEEE Transactions on Cybernetics, 52(12), 13848–13861. https://doi.org/10.1109/TCYB.2021.3109066

- Liu, Y., Yang, M., Wang, Y., Li, Y., Xiong, T., & Li, A. (2022). Applying machine learning algorithms to predict default probability in the online credit market: Evidence from China. International Review of Financial Analysis, 79, 101971. https://doi.org/10.1016/j.irfa.2021.101971

- Liu, Q., Zou, L., Yang, X., & Tang, J. (2019). Survival or die: A survival analysis on peer‐to‐peer lending platforms in China. Accounting & Finance, 59(S2), 2105–2131. https://doi.org/10.1111/acfi.12513

- Li, J., Zhang, B., Jiang, M., & Hu, J. (2023). Homophilous intensity in the online lending market: Bidding behavior and economic effects. Journal of Banking & Finance, 152, 106876. https://doi.org/10.1016/j.jbankfin.2023.106876

- Mercadier, M., & Lardy, J. P. (2019). Credit spread approximation and improvement using random forest regression. European Journal of Operational Research, 277(1), 351–365. https://doi.org/10.1016/j.ejor.2019.02.005

- Nemoto, N., Storey, D. J., & Huang, B. (2019). Optimal regulation of P2P lending for small and medium-sized enterprises. ADBI Working Paper Series.

- Nigmonov, A., Shams, S., & Alam, K. (2022). Macroeconomic determinants of loan defaults: Evidence from the US peer-to-peer lending market. Research in International Business and Finance, 59, 101516. https://doi.org/10.1016/j.ribaf.2021.101516

- Park, H. J., Kim, Y., & Kim, H. Y. (2022). Stock market forecasting using a multi-task approach integrating long short-term memory and the random forest framework. Applied Soft Computing, 114, 108106. https://doi.org/10.1016/j.asoc.2021.108106

- Pope, D. G., & Sydnor, J. R. (2011). What’s in a picture? Evidence of discrimination from prosper.com. Journal of Human Resources, 46(1), 53–92. https://doi.org/10.1353/jhr.2011.0025

- Qian, Y., & Lin, X. (2020). The research on the influencing factors of trust in online P2P lending: Based on platform. In 2020 IEEE 4th Information Technology, Networking, Electronic and Automation Control Conference (ITNEC), Chongqing, China (Vol. 1, pp. 2626–2632). IEEE.

- Rao, C., Liu, M., Goh, M., & Wen, J. (2020). 2-stage modified random forest model for credit risk assessment of P2P network lending to “three rurals” borrowers. Applied Soft Computing, 95, 106570. https://doi.org/10.1016/j.asoc.2020.106570

- Seasholes, M. S., & Wu, G. (2007). Predictable behavior, profits, and attention. Journal of Empirical Finance, 14(5), 590–610. https://doi.org/10.1016/j.jempfin.2007.03.002

- Sun, J., Li, H., Fujita, H., Fu, B., & Ai, W. (2020). Class-imbalanced dynamic financial distress prediction based on adaboost-SVM ensemble combined with SMOTE and time weighting. Information Fusion, 54, 128–144. https://doi.org/10.1016/j.inffus.2019.07.006

- Tang, H. (2019). Peer-to-peer lenders versus banks: Substitutes or complements? The Review of Financial Studies, 32(5), 1900–1938. https://doi.org/10.1093/rfs/hhy137

- Tang, L., Cai, F., & Ouyang, Y. (2019). Applying a nonparametric random forest algorithm to assess the credit risk of the energy industry in China. Technological Forecasting and Social Change, 144, 563–572. https://doi.org/10.1016/j.techfore.2018.03.007

- Tian, G., & Wu, W. (2023). Big data pricing in marketplace lending and price discrimination against repeat borrowers: Evidence from China. China Economic Review, 78, 101944. https://doi.org/10.1016/j.chieco.2023.101944

- Vallee, B., & Zeng, Y. (2019). Marketplace lending: A new banking paradigm? The Review of Financial Studies, 32(5), 1939–1982. https://doi.org/10.1093/rfs/hhy100

- Wang, H., Kou, G., & Peng, Y. (2021). Multi-class misclassification cost matrix for credit ratings in peer-to-peer lending. Journal of the Operational Research Society, 72(4), 923–934. https://doi.org/10.1080/01605682.2019.1705193

- Wang, T., Zhao, S., & Shen, X. (2021). Why does regional information matter? evidence from peer-to-peer lending. European Journal of Finance, 27(4–5), 346–366. https://doi.org/10.1080/1351847X.2020.1720262

- Wen, F., Xu, L., Ouyang, G., & Kou, G. (2019). Retail investor attention and stock price crash risk: Evidence from China. International Review of Financial Analysis, 65, 101376. https://doi.org/10.1016/j.irfa.2019.101376

- Xu, J., Hilliard, J., & Barth, J. R. (2020). On education level and terms in obtaining P2P funding: New evidence from China. International Review of Finance, 20(4), 801–826. https://doi.org/10.1111/irfi.12242

- Yan, Y., Lv, Z., & Hu, B. (2018). Building investor trust in the P2P lending platform with a focus on Chinese P2P lending platforms. Electronic Commerce Research, 18(2), 203–224. https://doi.org/10.1007/s10660-017-9255-x

- Yuan, Y. (2015). Market-wide attention, trading, and stock returns. Journal of Financial Economics, 116(3), 548–564. https://doi.org/10.1016/j.jfineco.2015.03.006

- Zhang, W., Shen, D., Zhang, Y., & Xiong, X. (2013). Open source information, investor attention, and asset pricing. Economic Modelling, 33, 613–619. https://doi.org/10.1016/j.econmod.2013.03.018

- Zhang, B., & Wang, Y. (2015). Limited attention of individual investors and stock performance: Evidence from the ChiNext market. Economic Modelling, 50, 94–104. https://doi.org/10.1016/j.econmod.2015.06.009

- Zhao, Y., Kou, G., Peng, Y., & Chen, Y. (2018). Understanding influence power of opinion leaders in e-commerce networks: An opinion dynamics theory perspective. Information Sciences, 426, 131–147. https://doi.org/10.1016/j.ins.2017.10.031

- Zhou, L., & Lai, K. K. (2017). AdaBoost models for corporate bankruptcy prediction with missing data. Computational Economics, 50(1), 69–94. https://doi.org/10.1007/s10614-016-9581-4