Abstract

Developers of urban parking decks—either stand-alone or ancillary to other uses like office, retail or housing—will soon face a decision brought on by the advent of driverless vehicles (DV): maximize short term cash flow and risk that these structures’ useful life will be cut short, or build sustainably and make them convertible to other land uses, thus extending useful life. Sustainable investment often involves higher up-front costs to preserve building life and therefore residual value in the long run. It may also require higher maintenance costs and lower cash flows to achieve the same goals. Thus any sustainable benefits from building reuse are essentially eliminated in present value terms, potentially leading to wasteful investment. With driverless cars and decreased parking demand as a frame of reference, this paper uses financial simulation modeling to look at the issue in the context of sustainable parking garages, and explores ways to predict the who, when, and where of upcoming investment parking structure decisions. Alternative paradigms for decision making (mini-max as opposed to purely profit maximization) are also explored. We find that under likely future market conditions for parking, developers will be hard pressed to make their required investment returns on new parking structures for holding periods of longer than 10 years on convertible structures, likely leaving the field to the public sector.

Parking in commercial parking structures and surface lots (serving retail, office, multifamily residential, or in stand-alone structures) is a prevalent land use. In a study of 15 major U.S. metro areas (in the top 45 by population), these four sectors reflect over 18.5 million parking spaces, or 32% of the total number of parking spaces. Of these, retail is the second biggest provider of off-street parking (behind residential spaces in private homes), followed by office, institutional space, multifamily, and stand-alone parking structures (Simons, Citation2020, Appendix 12-A).

Developers and property owners have certainly heard about driverless vehicles (DVs) coming. How soon is this expected? What if demand for parking dries up within the next decade or two? Consider the investment decision to build a new parking deck within the next few years, either stand-alone or part of a residential or commercial project. Government-mandated parking minimums are becoming less common, although the market and lenders may demand more than the minimum parking ratio. Should a developer go for maximizing short term cash flow and risk being left with an underutilized single-use building, or spend extra money to allow for the parking structure to be converted to another use, assuring it can viably continue to be a productive asset? Parking is not a very glamorous real estate sector, but it consumes an enormous amount of land use and a proportionately large percentage of the construction budget. Sustainable development means we do not build functionally obsolescent buildings.

Sustainable real estate investments may have cash flows that are below average, and may cost more to build. On the upside, they may have a residual value long into the future. Sustainable investment often involves higher up-front costs, to preserve building life and therefore residual value in the long run. It may also require higher maintenance costs and lower cash flows to achieve the same goals. Thus, the holding period and discount rate are hugely influential in determining sustainable design compared to a more short-term utilitarian project.

The present value of the property residual on sale is a prime determining factor. Assumptions on market appreciation may also change: Building a structure into a market of falling demand would mean present value would be only a function of cash flows, to exclude changes in terminal asset value (in its current use), which could not be expected to appreciate and could even drop. Thus, the terminal values for long hold periods of over 20 years, and higher interest rates are punishing: At a 4% interest rate a dollar in 20 years is worth only 46 cents today. For rates higher than 8%, the residual is 10 cents on the dollar, falling to less than 5 cents for hold periods of 30 years or longer. Thus any sustainable benefits from building reuse are essentially eliminated in the discounted cash flow (DCF) model, potentially leading to wasteful investment in physical resources dictated by market forces made solely on net present value (NPV). Thus, some worthy parking infrastructure investments will likely never be made by the private sector because the opportunity cost of capital (discount rate) is too high. The question is: Does “worthy” include externalities, like social benefit (e.g., the triple bottom line)? Are public entities, with lower discount rates, more likely to be early adopters of sustainable investments like convertible parking structures?

While this paper analyzes stand-alone parking structures as the unit of investment, the logic can also be extended to those parking decks that charge hourly parking fees as part of their operating model. Parking structures operated for “free” (e.g., most shopping malls) are outside the scope of this analysis.

This paper uses financial simulation modeling to focus on sustainable parking garage decisions, in the context of the upcoming advent of driverless cars and decreased parking demand. It explores ways to predict the who, what, when, where and why of upcoming investment parking structure decisions. Alternative paradigms for decision making (mini-max vs. maximizing) are also addressed. The results have implications for private developers and their future investment decisions. The analysis is generally conducted on a before-tax cash flow basis, and ignores potential public spin-off benefits from economic development, increasing the property tax base. For private investors, we ignore investment tax credits and common cash flow write-offs of depreciation and interest deductibility, although these are briefly addressed in the policy section.

Research Questions

The main premise of this study is to determine conditions under which market players would find it profitable to invest in convertible parking structures. Assumptions are made about the demand for parking, discount rates, holding periods, construction budgets, and operating cash flows. There are implicit assumptions regarding the appreciation of the parking asset in its current use.

Who? Are returns high enough to attract investment from a private sector developer, or a public investment entity with a low discount rate?

What? A parking structure facing a potentially large change in market demand.

When? At what time would the investment be made? Times (such as now) with sustained lower interest rates overall?

Where? Will the holding period and discount rate affect where the investments are made (areas with compressed cap rates)?

Why? What is the objective function of the decision maker on this sustainable investment? Is it purely profit maximization, or are other decision rules possible?

What are the expectations for the asset to appreciate in its current use, or to have terminal value only for the shell of the structure for conversion to another land use such as housing or office space?

Parking Garages: The Investment Problem

Consider parking garages. For the last 50 years or so, they were built fairly cheaply with sloped floors and low ceiling heights to keep construction costs down and to maximize the number of spaces that could be accommodated. This utilitarian approach worked well for generating cash flow, but if parking demand were to decrease substantially the structure would become redundant. Then it becomes essentially a single-use building, and can’t be repurposed. This is not sustainable.

On the other hand, the advent of driverless cars is on the horizon. This revolution in transit is likely to incorporate a restructuring of car ownership such that new robo-fleet operators will be formed, first partially, then substantially replacing private car ownership. These new firms are likely to be a partnership between a vehicle manufacturer (e.g., Ford, GM or BMW), a tech company (like Waymo or Mobileye) and a service operator (such as Uber or Lyft). These entities would seek to provide inexpensive transit based on much lower operating costs, to include removal of the driver and vehicle electrification to reduce fuel and maintenance costs. The service would attract riders by competing on low costs and certain other services, and would be app-driven.

Thus, it is likely that in 10 to 20 years the demand for downtown parking will be substantially diminished in many U.S. urban markets. Simons, Feltman, and Malkin (Citation2018), and Simons (2020, Chapter 9) project that the market demand for urban parking could decrease by 10% and by as much as 30% by 2030 (see the Appendix for a summary table of modal choices supporting these conclusions). The market penetration of trips in single user DVs or multiple rider DVs total 19% for this middle DV adoption scenario. The same table shows a 30% penetration by 2035. In metro areas with stable or declining populations (e.g., many Midwestern cities), underlying population growth would not mitigate the decline in parking demand. In growth areas, population growth could offset declining parking demand, depending where development is located.

Thus, if a new stand-alone parking structure (or fee-charging parking structure attached to another commercial building) is contemplated, or if a new building needs an associated new parking facility for the medium term, it does not make sense to build a sloped parking structure that will cease to be in demand and will need to be torn down within 10 to 20 years, even if it is more cash-flow efficient in the short run. The extra construction costs to create flat floors of sufficient height to allow conversion are about 15-30% over baseline costs. At some point, these costs become sustainable in order to generate a higher terminal value of a recyclable parking structure shell. When is that point, and what type of developer would be likely to act this way?

Apparently the convertible parking structure concept is early: Very few have been built to date. Indeed, only two are known: an existing office building in Cincinnati, and another office building under construction in Los Angeles. A few others are planned in Seattle and Grand Rapids, Michigan. Also, four known parking garage rehabs have been completed: a residential project in Wichita; an office incubator in London, UK; a hotel in Cincinnati; and a university student space facility in Chicago (Simons, Citation2020, Chapter 18).

Part of the reason the convertible parking structure concept has not been widely implemented is that there is not yet a clear picture on the risks to the parking industry from driverless car fleets and their impact on private vehicle ownership. The second factor, the focus of this paper, is the role that the discount rate and holding period play in the investment decision.

This research uses 48 discounted cash flow (DCF) simulations to determine likely timing for the switch-over from short-term sloped parking structures to longer term convertible ones, over a range of interest rates, loan terms, and various lending assumptions.

Literature Review

The convertible parking garage is a type of sustainable real estate investment. Sustainable investment has been studied relative to countries, sustainable real estate social returns, and intergenerational equity. The discount rate is identified as a key factor, but the unit of analysis is not property investment. Much of the literature is from the late 1980s onward. There is limited literature focusing solely on parking structures, and what exists places them in the realm of public infrastructure.

General Sustainability Literature

Goodland and Ledec (Citation1987), in an early classic economics tome, examine development strategies to provide an adequate, sustainable living standard for, essentially, the entire population of a nation. They address the desirability of using positive discount rates for short-run private transactions, and how it may affect outcomes.

Solow (Citation1993), in an invited lecture for Resources for the Future, was an early adopter of the term sustainability, applying it in the context of economic growth and environmental preservation. Solow’s work led to the concept of the “triple bottom line” where social benefit is in the decision matrix along with financial return.

Arrow et al. (Citation2010) examine overall sustainability in economic growth in five large countries with different patterns. They look at financial, social, and health capital, and the role these play in wealth creation and investment, using theoretical economic models to model sustainable outcomes over time. Natural capital, minerals, and renewables like forests are analyzed using descriptive statistics. The discount rate does not receive much attention in their models, and holding periods are not really addressed.

In a widely cited seminal piece, Beckerman (Citation1994) argues that sustainable development has been defined as morally unacceptable and totally impractical. Sustainability is addressed in the context of societal welfare maximization. This research generally uses the nation as the unit of analysis, and the variables are the environment and economic development/GDP. As part of the study, Beckman compares the present values of two income streams, and considers discounting future incomes at a varying rate using a form of benefit analysis.

A recent book by Pearce, Barbier, and Markandya (Citation2013), Sustainable Development in the Third World, focuses on economics and the environment. They cover numerous economic principles, but use third world countries as the unit of analysis. In sum, the general sustainability literature cited here does not help much in guiding the current research.

Parking Structure Literature

There is a limited amount of peer-reviewed literature on parking structures on the engineering and infrastructure investment and management side. For example, de Neufville, Scholtes, and Wang (Citation2006) use spreadshseet modeling in a real-options context to evaluate the flexibility in engineering systems in a case study of parking structures. Schenk (Citation2008) looks at decision making about public investments, including parking structures, under conditions of uncertainty, which could include future land use flexibility: one method included discounted cash flow. Finally, de Haan (Citation2011) considers the issue of flexible infrastructures under conditions of uncertainty in the context of Poland.

Real Estate Sustainability Literature

There is some more recent literature specific to sustainable real estate investment on returns from LEED and green building features, although they do not focus on parking structures or the discount rate and holding period per se. The articles are presented from least to most relevant to the research at hand.

Addae-Dapaah et al. (Citation2009) look at sustainable investment in commercial buildings in Singapore. They find that the investors studied were aware of and approved of the general benefits of green buildings, but were nevertheless somewhat apathetic. Beneficial financial factors (i.e., cost savings, attractiveness of the building to tenants, cleaner air in the building) did positively influence the investors’ interest in green buildings. Tax incentives were also positively viewed. All the factors considered in this study pertain to ongoing cash flows. However, the asset sale price and discount rate, which are in play well off into the future, are not explicitly addressed.

De Francesco and Levy (Citation2008) examine key real estate sustainable drivers affecting property investment decisions in Australia and how these drivers affect the investment product landscape and management of existing property investments. The study was conducted to demonstrate how sustainability principles may form part of the wider agenda of corporate property investment strategy and social responsibility. They find that the impact of sustainability on property investment can only be assessed by adopting a holistic approach, including the behavioral effects of economic, social, ecological, policy, and regulative environments.

Babawale and Oyalowo (Citation2011) study real estate valuers’ (appraisers’) perceptions of sustainability in real estate valuation in Nigeria. They survey 160 surveyors and valuers to determine the significance of a range of sustainability features, based on the social, economic, and environmental features that constitute the triple bottom line of sustainability. They show there is a growing awareness of the need to mainstream sustainability into real estate valuation practice, although respondents tended to define real estate sustainability in terms of its social, rather than economic or environmental features. Some of the literature they refer to does address rates of return. Although DCF is mentioned as a conventional method, it was apparently considered familiar and is not featured in their survey.

Jackson (Citation2009) studies sustainable real estate options in new construction. The research uses Monte Carlo simulations to determine the expected returns from LEED and Energy Star buildings. Increased construction costs and altered operating costs are examined. The study models time with a fixed holding period of 25 years and uses a discount rate; however, it is revealed in the form of an IRR, rather than set to determine NPV compared with the “non-sustainable” scenario. Thus the terms (discount rate and holding period) of the current research are employed, but not featured, in Jackson’s research.

In a report for the Royal Institution of Chartered Surveyors (RICS), Sayce, Sundberg, and Clements (Citation2010) present an extensive literature review on sustainable real estate investment, determining that this field in real estate dates from around 2000, with little empirical work before 2008. Nearly all scholars acknowledge additional up-front costs, sometimes with operating benefits such as reduced energy costs and increased occupancy due to “green” status. Only about 10% of the work is based on transactional data, with the balance composed of literature reviews, theory, and surveys of attitudes toward sustainability. Of the green attributes researched or abstracted, only longevity tangentially addresses our concern here (connected to holding period), and discount rate is not found (see Sayce et al., Citation2010, Figure 10, p. 21). Duration to sell and lower risk are mentioned (Sayce et al., Citation2010, Figure 14, p. 28), as potential contributions to value, although they appear to be of modest concern. The transactional studies cited do not unpack the discount rate, but appear to only report on sales price premiums associated with green labels in the U.S. office markets. Sayce et al. remark:

Several authors have demonstrated that it is possible to reflect sustainability in the methods used by valuers. Sayce et al. (2007), Boyd (2005) and De Francesco (2008) all explore the use of DCF techniques to reflect sustainability features. These studies serve to demonstrate that it is possible to reflect sustainability in property valuation and appraisal using known methods, as pointed out by Boyd (2005); however there is a noted lack of data for producing the cash flow (2010, p. 37).

Nowhere in their review of the 125 articles, reports, and papers do they explicitly mention the effect of holding periods or discount rates on residual value as a factor in sustainable investing.

The connection of the peer-reviewed literature to DCF and the low present value (PV) of the residual/terminal value problem is tenuous. Thus, we use simulated cash flows to make a point, and illustrate the effects of holding period and required rates of return on the parking structure investment decision. We can then infer which type of market player (public or private) would tolerate minimum investment returns at various levels.

Simulations

We consider two competing design styles for investment in to-be-built new parking garages. The assumptions were vetted by a parking professional.Footnote1 Both are assumed to be four-story, above-ground structures that can park 200 cars. One (with sloped floors) is not able to be repurposed, but is utilitarian and efficient for parking cars. The other project is also fine for parking cars, but can be reused, and costs more to build. First we introduce the two parking structure scenarios, then set forth the variable terms of the analysis.

Sloped Scenario

One has a sloped floorplate scheme (the Sloped scenario). which is cheaper to build and can accommodate cars parked on the ramps, but is unsuitable for adaptive reuse of any kind. It has a clear height of seven feet between floors, which is fine for parking but again, unsuitable for adaptive reuse because the ceilings are too low. This sloped parking project has a $5 million initial cost ($25,000 per space). It would be eligible for a loan at a 0.7 loan to value (LTV) ratio, and would produce before tax cash flows (BTCF) of $200,000 a year. The structure has sloped ramps and is not convertible to other land uses. Thus, assuming a net decrease in demand for parking, the end value in its existing use has been greatly diminished, and the project has a residual value of only $1 million (land less demolition), or 20% of its initial cost. All figures shown are in today’s dollar values with inflation going forward at 3%.

Convertible Parking Structure Scenario

The second scenario has a flat floorplate scheme and is designed to be convertible to other future uses like housing or office space (the Convertible scenario). At $6.5 million, it is more expensive to build ($30,000 per space or 30% more) and cannot accommodate parking on the ramps because they are external or otherwise unavailable. However, this configuration allows for a height of 12 feet between floorplates and is suitable for a few likely types of adaptive reuse. This convertible parking project would also be eligible for a loan at a 0.7 LTV ratio, and would produce BTCF of $170,000 a year. The lower cash flows may be attributable to having to maintain the external ramps, having to acquire a slightly larger piece of land, and the need to preserve future utility infrastructure more carefully. We make the same assumptions about net decreased demand for parking and negligible demand for the structure in its existing land use, but because the structure has flat floorplates, it has a higher residual value of $3 million (land, plus a portion of the shell), or 46% of its initial cost. Again, all figures shown are in today’s dollars with inflation going forward at 3%.

Financial Assumptions and Baseline Results

The cash flows are modeled in four sets of discount rates (4%, 8%, 12%, and 16%) and for four time periods (10, 20, 30, and 40 years out). This yields 16 scenarios for each set of sloped and convertible scenarios (32 total). We also set minimum rates of return for all scenarios, (both for unleveraged and leveraged returns), although only leverage returns are modeled. An initial caveat: Debt service is kept constant for all scenarios, implying a 10-year reset on financing (i.e., a 10-year balloon/call on all debt). A second caveat: This analysis is at the before tax cash flow level, and ignores tax benefits such as depreciation, interest deductibility, and any benefits from programs like Opportunity Zones or New Market Tax Credits.

and show the main building blocks of the 32 different simulations. The Sloped parking structure scenario for 10 years at a 4% interest rate is shown to have an NPV (after consideration of the project’s initial investment) of $1.22 million, while the Convertible parking structure scenario’s NPV is $2.26 million.

Table 1. 10-year, 4% Sloped parking structure cash flows.

Table 2. 10-year, 4% Convertible parking structure cash flows.

The analysis in is replicated 32 times. shows all the results, presented by holding period. As can be readily seen, for any holding period, higher interest rates substantially lower the NPV, although not to the same extent (i.e., a harsher discount for longer holding periods is evident). The “cents on $ at end” column (identical for both Sloped and Convertible sets of data), shows in part why this is the case: The residual values at the end of the holding period are progressively smaller, and for 30+ year holds, are less than 10 cents on the present value dollar, except for the lower (likely public) discount rate of 4%. This means that the present value of the future residual value of the improvements (the reward for sustainable investment) is devalued to the point of triviality.

Table 3. 32 baseline NPV summaries for both Sloped and Convertible scenarios.

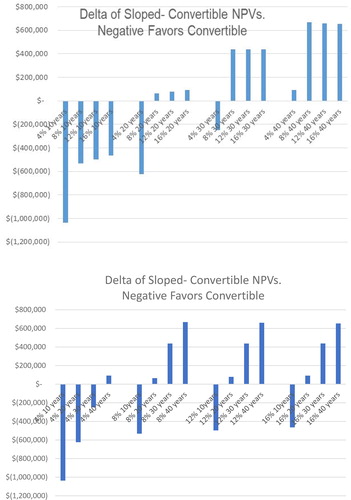

For the next step, in order to simplify the analysis, the difference in the NPVs between the two different parking structure construction types, but otherwise identical financial scenarios (e.g., same interest rate and holding period) is calculated, yielding the DIFFERENCE (delta) between the NPVs. For example, the NPV difference between the 4% 10-year Sloped and 4% 10-year Convertible is $1.22 million-$2.26 million = $1.04 million. This is shown as the first result of 16 matched pairs in , which shows the results in graph format, first sorted by increasing interest rates over a fixed holding period, then (same results) by interest rate, with the holding term varying.

Figure 1. Graphs of NPV deltas sorted by holding term (Top) and interest rate (Bottom).

Some general conclusions from the results are that the shorter the holding term, the more it favors the convertible parking structure. Regardless of interest rate, expected holding periods of 10 years all favor the convertible structure, and at 20 years the results are financially indistinguishable. All holding periods of 30 years or longer favor the sloped structure (except for the 4% scenario for 30 years). These observations do not consider market demand for parking.

Similarly, looking at the same data through the interest rate lens, all 4% loans favor the convertible structure, except for 40 years, where the results are financially equivalent. Due in part to the decay of the PV contribution of the residual value of the parking structure, and importance of early cash flows, the results for the 8%, 12%, and 16% deltas are almost identical: 10 years favors the convertible structure, at 20 years the financial results are equivalent, and longer terms favor the sloped version. That’s how steep the discounts are (operationalizing the “cents on $” column above).

These observations are purely numerical, before considering the market plausibility of the scenarios. For example, interest rates (now between 4-7%), and when the driverless cars are expected to substantially impact the market for parking (softness within 10 to 20 years) are of prime relevance. When these factors or added to the mix, shows the same results as above (sorted like the top graph) with the favored scenario and a comment on plausibility.

Table 4. Difference of NPV between paired Sloped and Convertible scenarios.

For private market players contemplating building parking structures at interest rates of 8% and above (reasonable for speculative new construction development deals), any deals longer than 20 years would favor the sloped structure. There’s just one large problem: A hold longer than 20 years would likely result in a substantial decay in the demand for parking, so it’s unrealistic to assume this scenario would be correct in the future marketplace. Further, it is rare that a private investor would consider a 30- or 40-year hold period for an asset.

On the other hand, the financial results of a 10-year hold period clearly favor the convertible parking structure, but it’s likely a bit early for the effects of driverless cars to negatively impact demand enough within 10 years. The likely time range where demand would substantially decrease is in the 10- to 20-year time frame, with 15 years as a reasonable inflection point. The financial results show indifference, or favoring convertible structures at lower (public) interest rates. Thus, we could conclude that over the operative time frame, new parking structures (either stand-alone or as an integral part of a new development project) would likely be built by public entities, and perhaps private entities in markets with extremely low cap rates would build convertible parking structures first. In other words, under most of these initial scenarios, the private sector would not build a convertible structure purely on a rate of return basis within the next few years.

Sensitivity Analysis

Since construction and market adjustments can vary considerably, we have assumed some enhancements to the convertible scenario, while keeping the sloped scenario the same. The differences for the baseline case yield 16 additional simulations for the sensitivity analysis, which can again be compared as above.

Sloped Parking Structure Scenario

Use the same sloped scenario as above.

Convertible Parking Structure Scenario

The second scenario still has a flat floorplate scheme, and is designed to be convertible to other future uses like housing or office space. We again assume the same $6.5 million cost to build, 12 feet between floorplates, and that this configuration is suitable for a few likely types of adaptive reuse. This enhanced convertible parking structure scenario assumes that lending markets reward convertibility as a risk-reducing strategy, so we increase the LTV to 0.8 (from 0.7) We also assume somewhat higher before tax cash flows ($190,000 a year), although they are assumed to still be below the Sloped scenario cash flows. This could be achieved through technological management, or smaller car size, or both, in that strategies can be found to better manage any additional maintenance costs, as managing convertible parking structures becomes more common. Finally, we assume that the demand for the structure in use as a parking structure, in the face of declining demand for parking, is less than the residual value of conversion in another land use. Thus, the project’s convertible design at end of the structure’s useful life is good enough to allow 55% of its value to be retained toward the next use ($3.6 million). This is mostly for better design of utility connections and roof structure, ability to add floors, etc. All other assumptions remain the same.

shows the results of these 16 additional runs, and the 16 matched comparisons. For all cases, the convertible scenario stochastically dominates the sloped scenario for NPV, and would appear to be the better investment/design choice.

Table 5. Summary difference of NPV results between paired Sloped and Convertible scenarios: Sensitivity analysis with improved convertible assumptions.

Conclusions

We are likely at the predawn of the driverless car era in the United States, where the rise of robo-fleets is likely to cause urban parking demand to dwindle substantially in 10 to 20 years. Although the reduction in demand for parking is likely to be most pronounced in metro areas with flat population growth, the same principles would still apply (perhaps to a lesser degree) to growing metro areas, depending where the household growth is located. In this study, we intertwine this vehicular trend with the notion of sustainable investment, and investigate whether convertible parking structures—those that meet current or near-term parking demand and still provide an avenue for future use by recycling the building shell—are becoming a realistic investment option for private sector developers. These conclusions focus on stand-alone parking decks, but could be extended to decks attached to other commercial uses that that charge user fees.

The cash flow simulations show that low discount rate scenarios (4%) of less than 10 to 20 years generally favor a convertible parking structure, while longer holds and higher discount rates favor investing in a sloped structure that disposes of an asset before the end of its useful physical life. Since it is likely that the parking market will dry up substantially in about 15 years (the midpoint of the 10- to 20-year range), longer holds assuming continued parking revenue growth are unrealistic. On the other hand, conversion would not be needed under a short holding period of 10 years. The “sweet spot” is about 15 years out, where parking demand is likely to have pivoted.

Thus, we conclude:

Who? Low discount rate entities such as public agencies and not-for-profits would be the first to do these convertible parking structure projects. Private developers would be a player in the parking conversion game starting in about five years.

What? Build convertible parking structures, designed to have a useful shell for the next land use cycle, in about 15 to 20 years, rather than sloped parking garages with a disposable end use.

When? The projects should be built within approximately 10 years of the decay in parking demand, starting soon, but not longer than five years from now. Times (such as now) with sustained lower interest rates overall could accelerate this investment trend;

Where? Convertible parking structures would appear first in areas with compressed cap rates, like big coastal cities, and in these investment climates, private sector developers might be interested on convertible parking structures earlier.

Why? To make money and maximize profits, of course, but also to preserve the garage’s physical structure and avoid owning an embarrassing asset that did not reach the end of its useful life. This represents another objective function outside maximizing financial return: minimax—avoid maximum loss—which in this case is looking foolish. As of now, we have not needed to assert that these types of long-term innovative investments are a public good to be plausible, (e.g., the need of the public to park near vibrant retail areas). Time will tell.

Lenders and bond-buyers are in the mix and have control of the loan terms (loan to value ratios, balloon payments, callable bonds); they could always refuse to buy or lend on parking-secured assets. Much of the risk can be mitigated by the lender by having the note be callable after 10 years. This phenomenon has not quite appeared yet; it is early in the cycle and only a few convertible parking structures, cited above, have been built at this time.

Also, public parking structures are sometimes employed as an economic development tool, and serve as a place-making “loss leader” to encourage a key jobs-laden company to locate in a strategic location, or to retain them in place if they threaten to relocate.Footnote2

The simplified before-tax analysis in this study has not addressed potential income tax benefits (or liabilities) to a private developer, including depreciation and interest, or any capital gains tax. In reality, some public and private parking structures are funded with (property) tax increment financing (TIF), as well as other tools including New Market Tax Credits, and more recently, an Opportunity Zone deal structure, which allows investors to defer capital gains tax for a number of years. Finally, a sale-leaseback strategy could be used to convert public parking structures to private ownership so certain income benefits can be obtained. Then, once the project is fully amortized, it could revert back to public sector ownership in 20 to 30 years. Determining which entity retains the land development rights is also an issue to be negotiated.

In sum, we believe that investment in convertible parking structures is likely to be a growing trend. The financial incentives appear to be most beneficial to the public sector, either as a loss leader, or for conventional financial benefit-cost analysis, or to set an example for sustainable investing. One other motivation to build convertible structures may be the mini-max objective function: Public leaders could look foolish tearing down a parking deck (say after 15 years) before its useful life has been consumed. Future research could track these trends, and identify adoption of similar sustainable investments.

Additional information

Funding

Notes

1 Thanks to Lee Shorts for reviewing the cost assumptions.

2 I include this interesting case, provided by one of the peer-reviewers for this article. “For example, Columbia, SC built a ∼350 space convertible deck in the early 1990s to allow an empty former Belk's store to be converted into the HQ for Carolina First Bank. The deck is leased to the owner for $1 per year until 2026, when the lease increases to $30 per space per month. At that point the building owners can elect to purchase the deck for an appraised value. The math is simple: 350 spaces at $360 per year is $126,000. Subtract 5% for operating costs and the NOI is $119,700. At a 7% cap rate, the value is $1,710,000-or-$4,885 per space. That's a $25,000 per space ($8,750,000 total) loss for Columbia, SC based on the report's estimated cost (adjusted for inflation) of $30,000 per space for a convertible deck.”

References

- Addae-Dapaah, K, Hiang, L.K & Shi, S. (2009). Sustainability of sustainable real property development. Journal of Sustainable Real Estate, 1, 203–225.

- Arrow, K., Dasgupta, P., Goulder, L.H., Mumford, K.J., & Oleson, K. (2010). Sustainability and the measurement of wealth (NBER Working paper #16599). National Bureau of Economic Research.

- Babawale, G.K., & Oyalowo, B. (2011). Incorporating sustainability into real estate valuation: The perception of Nigerian valuers. Journal of Sustainable Development, 4(4), 236–248.

- Beckerman, W. (1994). 'Sustainable development': Is it a useful concept? Environmental Values, 3, 191–209.

- De Francesco, A., & Levy, D. (2008). The impact of sustainability on the investment environment, Journal of European Real Estate Research, 1(1), 72–87.

- de Haan, J. (2011). Flexible infrastructures for uncertain futures. Futures 43(9), 921–922.

- de Neufville, R., Scholtes, S., & Wang, T. (2006). Real options by spreadsheet: Parking garage case example. Journal of Infrastructure Systems, 12(2), 107–111.

- Goodland, R., & Ledec, G. (1987). Neoclassical economics and principles of sustainable development. Elsevier Press.

- Jackson, J. (2009). How risky are sustainable real estate projects? An evaluation of LEED and Energy Star development options. Journal of Sustainable Real Estate, 1, 91–106.

- Pearce, D., Barbier, E., & Markandya, A. (2013). Sustainable development: Economics and environment in the Third World. Routledge Press.

- Sayce, S., Sundberg, A., & Clements, B. (2010). Is sustainability reflected in commercial property prices: An analysis of the evidence base. Royal Institute of Chartered Surveyors (RICS).

- Schenk, S. (2008). Valuation of flexibility for public investments. First international conference on infrastructure systems and services: Building networks for a brighter future (INFRA), Rotterdam, Netherlands. IEEE.

- Simons, R., Feltman, D., & Malkin, A. (2018). When would driverless vehicles make downtown parking unsustainable, and where would the driverless car fleet rest during the day? Journal of Sustainable Real Estate, 10, 3–32.

- Simons, R. (2020). Driverless cars, urban parking and land use. Routledge Press.

- Solow, R. (1993). An almost practical step toward sustainability. Resources Policy, 19(3), 162–172.

Appendix

Appendix of DV adoption, middle scenario.