?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This paper provides novel evidence on commodity market exposure, i.e., the impacts of commodity price and terms of trade fluctuations on macro performance amongst 46 emerging and developing countries (EMDCs) in Africa, Asia and the Latin American and Caribbean (LAC) region. We estimate the exposure of six macroeconomic variables to the commodity prices and terms of trade. Our results indicate that in overall terms, there is a strong and statistically significant long-run relationship between the vector of analyzed world trade prices and macro variables in all EMDCs. However, based on the short-term reactions, only about 10% of the macroeconomic variation amongst the EMDCs is due to commodity market-related exposures. Our results also indicate that the commodity market exposure is not unanimous across countries, amongst regions, or especially between measures of exposure.

1. Introduction

Primary commodities are of special importance for most emerging and developing countries (EMDCs). In some of these countries, commodities are imported inputs, whereas the other EMDCs are suppliers of those commodities. Both types of EMDCs are exposed to the commodity market price changes. For exporters, an increase in commodity prices channels an improvement in export revenues, hence, boosting the economy. In contrast, for the commodity importers, an increase in commodity prices has negative effects on economic performance. Standard open economy macro theory proposes that exogenous commodity price shocks have large impacts on commodity exporters and importers at macroeconomic level (see Fernández, Schmitt-Grohé, and Uribe Citation2017; Kose Citation2002; Schmitt-Grohé and Uribe Citation2018). However, the previous empirical studies are unable to provide a unanimous inference about the size of the impacts on different countries or on groups of countries, or on how to measure these shocks (based on commodity prices, or terms-of-trade values), what groups of commodities produce these shocks especially, or what econometric methods should be used in estimating the exposure. This is particularly an empirical question of high economic priority. Hence, there is an extensive demand for further results about the size and dynamics of commodity market exposure in different countries, especially among the ones that are most exposed to these shocks.

Previous inference about the significance of the commodity and standard terms of trade exposures is very heterogenous. Theoretical real business cycle models, which calibrate the impacts of standard and/or commodity terms of trade shocks on the macro variables propose that the commodity terms of trade shocks are the major source of economic fluctuations among the emerging and developing countries (see Aguiar and Gopinath Citation2007; Bidarkota and Crucini Citation2000; Broda Citation2004; Drechsel and Tenreyro Citation2018; Fernández, Schmitt-Grohé, and Uribe Citation2017; Fornero, Kirchner, and Yany Citation2016; Kose Citation2002; Mendoza Citation1997; Roch Citation2019; Schmitt-Grohé and Uribe Citation2018; Shousha Citation2016). In general, the results seem to be method dependent: For example, Schmitt-Grohé and Uribe (Citation2018) have indicated that although the results may vary across countries, the terms of trade shocks would constitute only 10% of the macroeconomic fluctuations in the developing economics. This result is further supported by Fernández, Schmitt-Grohé, and Uribe (Citation2017). On the other hand, Ben-Zeev, Pappa, and Vicondoa (Citation2017) propose that the commodity terms of trade shocks could constitute almost half of the output fluctuations in Latin American economies. Sizable impact has also been reported in Roch (Citation2019) estimates using heterogenous panel model show that the commodity price shocks can explain even 30% of the movements in output among the Latin American countries.

Furthermore, regarding the rivalry between the two main important international trade variables supposed to have macroeconomic effects in emerging and developing markets, i.e,, the standard terms of trade (tot) and the commodity terms of trade (ctot), there is a long list of studies that have previously focused on the role of especially the terms of trade effects on macro fluctuations (Agenor and Aizenman Citation2004; Raddatz Citation2007), starting from Harberger (Citation1950) and Laursen and Metzler (Citation1950). In their seminal studies, they showed that a negative shock to the terms-of-trade would worsen the current account. Later, Ostry and Reinhart (Citation1992) found that the terms of trade shocks have a strong effect on real exchange rates and the current account. Another early study, which relates to ours is, e.g. Bidarkota and Crucini (Citation2000), who combined national terms of trade data for developing countries with world prices of internationally traded primary commodities and found that the variation in the world prices of three or fewer key exported commodities may even account for 50% or more of the annual variation in the terms of trade of a typical developing country. They concluded that the commodity price fluctuations should be central features of studies of business cycle transmission across developing and industrialized nations.

In support, our evidence suggests that the EMDCs cannot be regarded as a homogenous group of countries with respect to the commodity market exposures. There are strong numerical differences in the exposures amongst countries, regions and commodity groups, but they all share the common feature that the commodity prices have a significant impact on the macroeconomic variables. The inference on the commodity price exposure seems to be depended on the variable used as a measure for commodity exposure. E.g. Harberger (Citation1950) and Laursen and Metzler (Citation1950), Ostry and Reinhart (Citation1992) Bidarkota and Crucini (Citation2000), Roch (Citation2019), Lopez-Martin, Leal, and Fritscher (Citation2017) all indicate that the inference on commodity price exposure depends on whether the standard terms of trade (tot) or the commodity terms of trade (ctot) is being used as an exposure variable. This disparity calls for further research. In order to make a firm conclusion about the phenomenon, we examined the exposure of 46 commodity dependent EMDCs to the world trade price changes, especially focusing on the effects of ctot, tot, and global commodity price indices (gcp). We use the Gruss and Kebhaj (Citation2019) commodity price data, which plays an integral part in our study. This new dataset is completely different e.g. compared to Bidarkota and Crucini (Citation2000) since it focuses both on imports and exports prices and quantities.Footnote1

Our main contributions regarding the role of commodity market exposure are the following. First, individual macroeconomic variables in EMDC are somewhat differently exposed to the tot, ctot, and gcp shocks. However, there seems to be a common long-run, stationary relationship between all the individual cyclical macro variable series and the three price measures in our data set. This relationship has a statistically significant error-correction parameter in almost all country groupings and for all the macroeconomic variables of interest in our analysis. This is a new, strong finding in the EMDC data. It emphasizes the strong price effects of global markets, and hence, output, consumption, investment, trade balance, inflation and exchange rate exposure to commodity and price shocks. Second, based on the short-run shock effect analyses the standard terms of trade exposure also transmits the non-commodity market price effects, which are essentially influenced by the non-commodity exports and imports compositions (e.g. services). Third, many developing countries have specialized in only one or a few commodities in their exports or imports. In effect, based on our results the individual commodity price indices, e.g. for minerals, energy or agricultural products’ prices for all the countries, may not adequately capture the country-specific shocks.Footnote2 Moreover, the global commodity markets are strongly correlated in terms of the market prices (see Byrne, Fazio, and Fiess Citation2013). Therefore, the use of a global (aggregate) commodity market index series as one alternative price series in our analyses captures this phenomenon.

We also shed new light on the idea that some of the macroeconomic variables in EMDCs may possibly be more exposed to the world trade market prices than others. This follows the assumption of the small open economy real business cycle (RBC) theory, which suggests that different sectors/variables of the macroeconomy (aggregate output, private consumption, private investments, international trade, general price level and real effective exchange rate) respond differently to different exogenous price shocks across countries. Hence, using multiple world trade price series in this study also controls for the heterogeneity in individual/group exposures in this respect. For example, we use the country-specific commodity terms of trade index to account for the differences in the country’s commodity market trade (imports and exports) weighted by the country’s output. We expect that this variable better captures the effects of commodity price fluctuations on different group/country performance, compared with the standard terms of the trade index. Finally, in all our analyses we acknowledge the concerns raised by Hamilton (Citation2018) about the use of Hodrick and Prescott Citation1997 filtering in macro econometric modeling. Therefore, we end up using the Hamilton (Citation2018) filtering for the cyclical components in our analysis. This is also a novel application among the studies of commodity exposure which typically employs HP filtering if needed.Footnote3

Our findings can be summarized as follows. First, the results show that the newly constructed commodity terms of trade dataset from the International Monetary Fund (IMF), described in Gruss and Kebhaj (Citation2019), has a strong potential to be used when analyzing the aggregate macroeconomic fluctuations among the EMDCs. The estimates from the Pooled Mean Group (PMG) estimator of Pesaran, Shin, and Smith (Citation1997, Citation1999) propose a remarkably strong symmetry in terms of long run adjustment of macro variables, ca. −0.50, (output, consumption, investment trade balance, consumer price index and exchange rate) toward the long-run equilibrium after a common commodity price shock (standard terms of trade, commodity terms of trade and global commodity price index) across the group of countries analyzed. The PMG estimates verified further the significant role of the global commodity price index especially when the long run effects are concerned. It had significant effect in 58% of cases across the macro variables among our 6 groups of countries. The significance of the short run exposures of macro variables were more alike. The number of significant impacts varied between 8 (for the commodity terms of trade and global commodity price index) and 5 (for the commodity terms of trade). PMG estimates also pointed out that the consumer prices are especially significantly exposed to the global commodity price index.

In addition, the short-run shocks (impulse responses) reveal that many of the real economic sectors in the Other (Latin American and Caribbean [LAC] and Asia) group of economies are more exposed to price changes compared to for example the African economies. This part of our results lends support to other related studies (e.g. Céspedes and Velasco Citation2012; Collier and Goderis Citation2012; Deaton and Miller Citation1996). Also, the non-commodity exporting economies are severely exposed to the world trade price movements compared to the reactions amongst the commodity-dependent economies. Overall, the findings on average, suggest that these shocks account for less than 10% of the variation in the macroeconomic variables. This corroborates with e.g. Schmitt-Grohé and Uribe (Citation2018) findings. In particular, the impulse responses reveal how real aggregate output and private investments improve because of favorable price changes, which strongly supports the evidence in Roch (Citation2019). Most importantly, we find that a favorable commodity price shock appreciates the real exchange rate, which makes these economies competitively cheaper in terms of foreign goods, but the downside effect is a rise in the prices of consumer goods (inflationary effects) and a prominent contraction in private consumption. Our findings concerning the standard terms of trade also confirm the results of Schmitt-Grohé and Uribe (Citation2018), who used similar terms of trade series in the empirical analysis.

The rest of the paper is structured as follows. Section 2 presents our empirical approach. Section 3 describes the data. The empirical results and discussions are presented in Section 4. Section 5 concludes with policy recommendations. The online appendix presents the theoretical RBC model motivating our empirical analyses. The appendix displays also the additional empirical results.

2. Econometric Model

The theoretical motivation of our empirical approach is based on a small, open economy RBC macro model described in Online Appendix A, which follows the previous analyses such as those of Mendoza (Citation1995, Citation1991), Schmitt-Grohé and Uribe (Citation2018) and Wickens (Citation2008). The empirical form of the model is analyzed using the Structural Vector Autoregression (SVAR) approach, as previously utilized, for example, in Fernández, Schmitt-Grohé, and Uribe (Citation2017), Schmitt-Grohé and Uribe (Citation2018), and Shousha (Citation2016). The SVAR modeling starts with a reduced form VAR that takes the form:

where is a vector of dependent variables,

is n x n matrix of the parameters on lagged variables,

denotes a vector of the lagged dependent variables, and

is a set of errors that have zero expected values and a variance-covariance matrix

. Hannan-Quinn (HQIC) information criterion choose

to be the number of optimal lags. The order of variables in the VAR model is given as:

where denotes the exogenous price variable vector, and

denotes the endogenous macro variables in our analysis. Based on the small, open economy structure of our theoretical model described in Appendix A, we identified the commodity terms of trade (ctot), the standard terms of trade (tot) and the global commodity price (gcp) as the alternative exogenous price variables affecting macroeconomic variables: the aggregate output (y), consumption (c), investments (inv), trade balance (tb), consumer price index (cpi) and real effective exchange rate (er) fluctuations. Therefore, to scrutinize the impacts of the exogenous price shocks on the macro variables, we formulate a SVAR model that takes the form:

Because the errors ( in the reduced form VAR (EquationEquation (1)

(1)

(1) ) are correlated, we had to formulate EquationEquation (3)

(3)

(3) so that the error term

becomes a linear combination of the structural shocks

Here,

and

are n x n matrices of parameters, and

is a diagonal matrix of variances and covariances indicating that the errors are now independent of each other. For the identification of exogenous structural shock effects, we ordered the variables in the

matrix based on a Cholesky decomposition (lower triangular matrix), similar to Fernández, Schmitt-Grohé, and Uribe (Citation2017) and Shousha (Citation2016). This is to ensure that the vector of endogenous (macro) variables does not have any contemporaneous impact on the vector of exogenous world trade prices by the assumption of small, open economy model described in Appendix A. The ordering of variables in

is important because it enables us to uniquely identify the shocks from the exogenous prices, ceteris paribus. Hence, if we assume

is a non-singular n x n matrix, that is invertible, then we can rewrite EquationEquation (4)

(4)

(4) in a reduced form as:

where represents the mutually uncorrelated reduced form innovations. This form normalizes the covariance matrix

of the structural errors, so that the reduced-form error covariance matrix is

. Now, the elements in

are the short-run contemporaneous parameter values for the variables

captures the dynamics in the system, and

becomes a structural multiplier that serves as the weights. Following the approaches of Drechsel and Tenreyro (Citation2018) and Schmitt-Grohé and Uribe (Citation2018), we choose

so that the structural shocks are given by one standard deviation (SD), which can be interpreted as a group unit shock. This enables us to simulate the impulse response functions (IRFs) and forecast error variance decomposition (FEVD) from the structural model with our interest in the exogenous prices giving the impulses and endogenous variables as responding to them.

In addition to utilizing the structural VAR approach, that is based on the assumption of stationarity of the analyzed vector of time series variables in a panel form, we also analyze specifically whether our main macroeconomic variables have a long-run steady state relationship with the world trade prices i.e., ctot, tot, and the gcp using a Vector Error Correction Model (VECM) representation of autoregressive distributed lag (ARDL) model.Footnote4 However, considering the dimensions of our panel data, both the cross-sectional (N = 46 EMDC’s) and time-series (T = 37 years) dimensions are fairly large. Hence, we use the Blackburne and Frank (Citation2007) approach, to account for the fact that the asymptotics of large N and large T dynamic panels (with prominent non-stationarity) are different from the asymptotics of traditional large N and small T dynamic panels. We estimate the VECM representation of our panel data separately for each macroeconomic (y) variable and the vector of price (x) variables in the formFootnote5

where ,

,

, and

The parameter is the error-correcting speed of adjustment term, and if it is zero, then there would be no evidence for a long-run relationship. This parameter is expected to be significantly negative under the prior assumption that the (levels) relationships between the variables of our interest show a return path to a long-run equilibrium. Of particular importance is the vector

, which contains the long-run relationships between the variables. We estimated the model using the Pooled Mean Group estimator introduced by Pesaran, Shin, and Smith (Citation1997, Citation1999). It allows both the heterogeneous short-run dynamics and common long-run elasticities. Our specification includes the (cyclical components of) macro variable of interest and the set of price variables (ctot, tot, and gcp) in each case. Often only the long-run parameters are of primary interest, and the results of the pmg option in Stata include the long-run parameter estimates and the averaged short-run parameter estimates.

3. Data

We collected annual observations on the country-specific commodity terms of trade, the standard terms of trade and six country-specific macroeconomic variables covering the period from 1980 to 2017 for 46 EMDCs. In addition, we used the global commodity price index data covering the period from 1980 to 2016. The sources of the data were the World Bank, IMF, UNCTADStat, and the paper by Gruss and Kebhaj (Citation2019). We categorized our variables into two main blocs as follows: (a) The exogenous price bloc: the commodity terms of trade (ctot), the standard terms of trade (tot) and the global commodity price (gcp); and (b) The endogenous (macroeconomic) variable bloc: aggregate output (y), private consumption (con), private investments (inv), trade balance (tb), consumer price index (cpi) and real effective exchange rate (er).

For the construction of our set of exogenous world trade price series, we used various measures to identify the exposure. First, we used the World Development Indicators (WDIs) trade-weighted export to import unit value index as the measure of the standard terms of trade (see Schmitt-Grohé and Uribe Citation2018). Second, we used the newly introduced GDP-weighted commodity export to import price series as the measure of commodity terms of trade (see Gruss and Kebhaj Citation2019) and the commodity market price (all group) index from the World Bank pink sheet (Citation2019).Footnote6 Based on the theoretical model given in the online Appendix A, our set of endogenous variables consisted of similar variables to that of Schmitt-Grohé and Uribe (Citation2018), and we retrieved it from the World Bank WDI database.Footnote7 Eligibility criteria for choosing a specific EMDC to be included in our panel of countries required that an individual country had to satisfy the following criteria: 1; The country must be considered a commodity export dependent country in one of the three commodity export sectors (agricultural products, minerals or energy commodities) by UNCTAD,Footnote8 2; It must be considered as an emerging or developing country/market by IMF, UNCTAD or Morgan Stanley Capital International (MSCI) classification, and 3; It must have at least 30 years of consecutive annual on all the variables available in WDI or IMF databases.

Ultimately, 46 countries satisfied the screening criteria to be included in this study. Thereafter, we categorized the countries first into three regions: 22 African countries, 10 Asian countries and 14 LAC countries. The second grouping was based on the commodity sector dependence by UNCTAD (Citation2019); it consisted of 15 agriculture export dependent countries, 9 minerals dependent, 7 energy dependent and 15 non-commodity export dependent countries and their exchange rate regimes (see Table B.1).Footnote9 Considering that our theoretical model was set up to examine fluctuations (cycles) in macroeconomic variables, we had to transform our data series by taking log values and detrending them using the Hamilton (Citation2018) filter to obtain the cyclical components of the data.

After the transformation, we performed panel unit root tests on the raw data and the cyclical component using the Levin, Lin, and Chu (Citation2002) test for a common unit root in the panel, and the Im, Pesaran, and Shin (Citation2003) test for individual unit roots in the panel. The panel unit root test results (cf. Table D.1) show that some of the variables in the raw data, i.e. the commodity terms of trade, global commodity prices, and output and consumer price indexes, are I(1), whilst the other variables are I(0). As expected, the cyclical component of the Hamilton filtered data for all the variables was stationary, i.e. I(0) at levels. Fig. B.1 plots the cyclical data of the macroeconomic variables and the world trade prices for some selected economies. See also Tables B.2. and B.3 for the key descriptive statistics on the analyzed macroeconomic variables for the groupings.

4. Empirical Results and Discussion

4.1. Long-run and Short-run Dynamic Relationships

This section presents and discusses the main empirical results in the following order. Because our panel unit root tests indicated that the cyclical components of e.g. the macro variables seem to be stationary processes, the natural starting point would be directly the SVAR-based analysis. However, considering the high first order autocorrelation coefficients for some of the variables analyzed (cf. Tables B.2 and B.3), we have reasons to believe that focusing only on the SVAR-based results might yield biased results in some cases. Because of this, and the obvious possibility that due to having both large cross-sectional (N) and large time-series (T) dimensions in our data, the assumption of stationarity and homogeneity of slope parameters might be inappropriate, we start our reporting and discussion of results from the VECM representation given in EquationEquation (5)(5)

(5) above. report the long-run cointegration relationship (denoted LR) which is normalized for the macro-variable in question, and the vector of world trade prices, i.e, ctot, tot, and gcp, and also the short-run dynamics (denoted SR)

Table 1. ARDL-VECM estimates for output, private consumption and investment

Table 2. ARDL-VECM estimates for trade balance, consumer price index and real exchange rate

As we see from the results in , the ARDL-based panel cointegration procedure allowing for heterogenous effects amongst the cross-sectional units reveals that there indeed are some interesting long-run relationships between the variables. The most striking result is that in all the cases, the error correction term (ECT) is statistically significant even at 1% risk level and it also has an economically appealing interpretation. The size of the economically relevant negative error correction coefficient varies from −0.11 (for aggregate output in the group of 24 ‘Other Countries’ to −0.67 for the aggregate output in the ‘Energy’-dependent countries. This finding is really striking, since it reveals the extreme importance of the equilibrium relationships between the local macro variables and global commodity prices, and the country-specific commodity-terms of trade (ctot) and standard terms of trade (tot) series. The implication is that the commodity market behavior really has a strong role in determining the macroeconomic equilibrium conditions in the countries analyzed.

Furthermore, the long-run relationship (LR) between each individual macro variable and the three price variables seems to vary a lot between the various country groupings, and it varies much more than the role of the ECT-term. For example, exchange rate and investments are the variables that react often and statistically most significantly to the ctot, tot and gcp changes. In addition, aggregate consumption in the energy, and agricultural production dependent countries reacts negatively in the long-run relationship to the rising ctot values. Moreover, the reaction is clearly stronger in both these (individual coefficients in the LR-relationship are −0.51 and −0.49, respectively) compared to the non-commodity dependent countries (with coefficient −0.33). On the other hand, the exchange rate reactions are very strong in the LR-relationship for both the agricultural dependent countries and African countries (of which many are actually dependent on agricultural production), and in these cases all the ctot, tot, and gcp series have a statistically significant parameter estimate in the long-run equilibrium relationship. Similar conclusions cannot be drawn so strongly for any of the other groupings or macro variables.

In overall terms, the results reported in suggest that the degree of variation in both the long-run (LR) and short-run (SR) dependencies amongst the three price variables and the individual macro indicators is very strong. However, the utilized VECM-representation of our data set revealed also very strongly, that the analyzed price variables (ctot, tot, and global commodity price index) are indeed extremely important for all the macro variables and for all the groupings of our country-level data. The mean value of the ECT-term coefficient is −0.525, and the standard deviation is 0.015, so it seems that in these data, in average terms about half of the error in the long-run relationships between the price variables and the macro situation (irrespective of the macro indicator used) is corrected every year, and this is indeed a strong error-correction mechanism also in economic meaning. However, because the short-term results are much more heterogenous already based on this first stage of our empirical analyses, the next step of our analysis is based on focusing on the relationships between the variables in SVAR representations of our data.

4.2. Shock Reactions

This section presents the impulse responses (IRFs) and forecast error variance decomposition (FEVD) results obtained from the SVAR representations given in EquationEquations (1)(1)

(1) –(Equation4

(4)

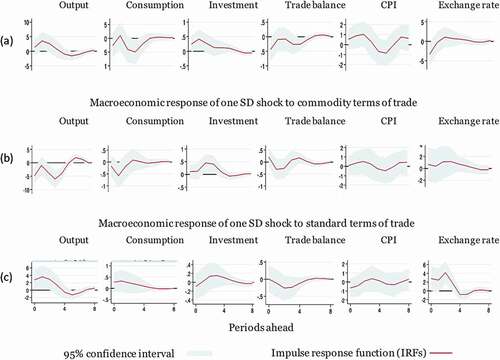

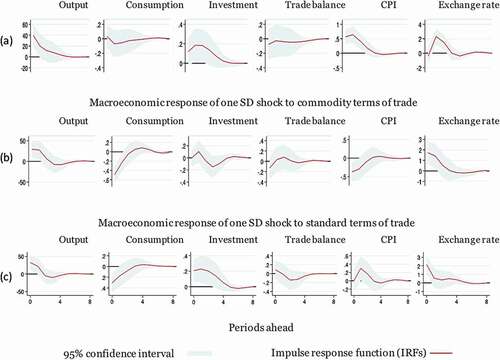

(4) ) above. present the IRFs obtained from one standard deviation shock to the world trade prices in rows (a)–(c) for the African and Other economies groups.Footnote10 We chose this specific setup to be reported and discussed in more details, because this enables us to compare our results directly with some previous studies, such as Ben-Zeev, Pappa, and Vicondoa (Citation2017), Fernández, Gonzalez, and Rodriguez (Citation2018), Schmitt-Grohé and Uribe (Citation2018), Shousha (Citation2016) and Mendoza (Citation1995), who also found that the commodity terms of trade, standard terms of trade and global commodity price shocks have varying effects on different macroeconomic variables (aggregate output, private consumption, private investments, trade balance, consumer price index and real effective exchange rate) amongst the EMDCs. Row (b) in shows the macroeconomic variables’ response to one standard deviation shock from the commodity terms of trade index. The reactions suggest that when a favorable commodity terms of trade shock hits the African economies, real economic activities such as the aggregate output will contract immediately, and private consumption as well, a year after the shock, whilst private investment improves 2 years after the shock. These impacts are statistically significant within a 95% confidence margin. In comparison with row (c), a similar characteristic can be seen that a favorable standard terms of trade shock causes aggregate output to expand for almost two years. This also causes the real effective exchange rate to appreciate within two years after the shock. The African economies’ exposure to the global commodity price shocks suggests that the aggregate output and private investments expand a year after a favorable price shock. However, the region may experience depreciation in the real effective exchange rate immediately due to the shock (see row a).

Figure 1. Impulse responses for the African economies.

Figure 2. Impulse responses for the Other economies.

Notably, the aggregate output reacts unfavorably to commodity terms of trade shock, which was unexpected. The reason for this is not obvious. A possible explanation for the reaction of the output is that the African economies export primary commodities and then import the value-added ones. Assuming a rise in commodity prices directly translates to a rise in the cost of imported products as inputs, this may adversely affect the output amongst the African economies. presents the reactions of the macroeconomic variables in the Other group of economies to one standard deviation shock in the world trade prices. Here, the significant reactions are much stronger compared to the African economies. It’s obvious from row (a) that a favorable shock in the global commodity price index causes an expansion in the aggregate output, private investments and consumer price index immediately after the shock. Furthermore, the real effective exchange rate will appreciate one year after the shock. These reactions are statistically significant within the 95% confidence margins. Similarly, the responses shown in row (b) indicate that a favorable commodity terms of trade shock causes output to rise immediately, whilst the real effective exchange rate appreciates after a year (see also Roch Citation2019). However, private consumption and consumer price inflation seem to contract immediately after the shock. These findings are in line with those of Ben-Zeev, Pappa, and Vicondoa (Citation2017).

row (c) shows that the standard terms of trade shock expands real economic activities such as aggregate output and private investments and appreciates the real exchange rate. Private consumption seems to be contracting immediately, which also confirms the findings of Schmitt-Grohé and Uribe (Citation2018). Most importantly, we find that unlike for the data on African economies, the results presented in rows (a–c) suggest that within a 95% confidence margin, a favorable shock in the world trade prices causes aggregate output to expand, and the prices of foreign goods become cheaper as a result of the appreciation in the real exchange rate amongst the Other group of economies. Together, these results indicate that when a shock hits African or the group of Other economies, the effects on their macroeconomic performance persist for at least two to 4 years before they converge to zero. As an implication from this finding, we highlight the extent of exposure in these economies to the world trade price shocks and the chain of events on how these impacts favorably or adversely influence and persist in these economies. These results are in general consistent with that of e.g. Drechsel and Tenreyro (Citation2018), Mendoza (Citation1992, Citation1995), Kose (Citation2002) and Schmitt-Grohé and Uribe (Citation2018). Furthermore, a robustness check based on using alternatively computed cyclical observations for the analyzed variables from Hodrick and Prescott (Citation1997, HP) filtering procedure reveals the consistency of our results, too.Footnote11

Figs. C.1 – C.4 report the responses of macroeconomic variables to a one standard deviation shock to the world trade price for the commodity dependent groups of economies. In general, results show both favorable and unfavorable reactions to the world trade price shocks for different commodity dependent groups. These reactions are statistically significant in many cases. We find this as further implications on how the EMDC’s are ex-ante exposed to the world trade prices irrespective of their production structure. In addition, the strong and significant reactions of the macro variables in many cases confirms the long-run relationship between the macro variables and the commodity market behavior which, as was witnessed based on our ARDL-VECM analyses, indeed has a strong role in determining the macroeconomic equilibrium conditions in the analyzed countries.

The theoretical framework (see Online Appendix A) of this study assumes that the groups of economies analyzed are small open economies. They have minimal or no control over the global commodity import/export markets as well as in other goods market price movement. This makes their economies vulnerable to any unanticipated price movements in the world market. Our results have revealed some important dynamics in their economic activities responding to exogenous shocks. We also detect that some economies have benefited from the global commodity price booms in the form of improvement in aggregate output and investment. We also observe that appreciation in the real exchange rates is common, which makes those economies competitively cheaper in terms of foreign goods, but the downside of this is the subsequent rise in the price of consumer goods (inflationary effects) and the declining private consumption. Overall, many of these exposures are consistent with the other related studies cited earlier, e.g. see Schmitt-Grohé and Uribe (Citation2018).

However, in order to understand more profoundly the importance of these shocks affecting the country groups, we examined how much of the fluctuation in the economic activities can be explained by the world trade price shocks using forecast-error variance decomposition (FEVD). For this purpose, we decomposed the variance in the macroeconomic variables for each shock and projected it five years ahead. Tables C.1 and C.2 display the FEVD in Africa with respect to Other group of economies. Overall, the results show that less than 10% of the variations in aggregate output, private consumption, private investment, trade balance, consumer price index and real effective exchange can be explained by the world trade prices. The results suggest that the commodity terms of trade and global commodity market price shocks may account for a greater proportion compared to the standard terms of trade index shocks.

5. Conclusions

This study assessed the macroeconomic exposures of different types of commodity market dependent Emerging and Developing Countries (EMDC) on the recent fluctuations in global commodity prices and the terms of trade. For this purpose, we first constructed a theoretical model that identifies the main exogenous shocks affecting some key macroeconomic variables in 46 emerging and developing, small open economy countries. Based on this theoretical framework, we then analyzed the long- and short-run relationships between three world trade price series and six key macroeconomic indicators.

Our main results can be summarized as follows. First of all, our Pooled Mean Group ARDL-VECM modeling approach of the long-run relationships between commodity terms of trade, standard terms of trade and global commodity market index series and the analyzed six macroeconomic variables reveals that there is a very strong long-run relationship amongst the EMDC data. This result is very consistent in all the country groupings, and it can be given as an error correction representation amongst the variables suggesting quite rapid adjustment of the macroeconomy to the deviations from the long-run equilibrium relationship due to shocks in commodity prices. Furthermore, from the short-run analyses we find that many of the real economic sectors in the Other (LAC and Asia) group of economies are more exposed to the world trade price changes compared to the group of African economies. For the economies grouped according to their production structure, the results reveal that the non-commodity export-dependent EMDC economies are even more sensitive to the world trade price fluctuations compared to the commodity-dependent sector economies, such as agricultural products and minerals.

Finally, our short-run, shock effect findings reveal that, on average, less than 10% of the variance in the key macroeconomic variable fluctuations can be explained by the world trade price shocks in all the groups. Nevertheless, our results show in general that all the commodity-dependent countries in Africa, Asia, Latin America, and the Caribbean are strongly exposed to the world commodity trade price fluctuations. Hence, this study suggests that the future policies and decision-making should carefully acknowledge the impact of these world trade price shocks, especially for Africa and Latin American regions, which are most exposed to these shocks. In addition, we propose that the policy makers especially in African countries should pay attention to mitigating the unfavorable commodity terms of trade shocks.

Supplemental Material

Download PDF (1.3 MB)Supplemental Material

Download MS Word (2.9 MB)Acknowledgments

The authors are most grateful to the Editor, Subject Editor and two anonymous reviewers for their comments that greatly improved the quality of this paper. Comments and suggestions from the participants of JSBE summer seminar 2019 are also appreciated.

Supplementary material

Supplemental data for this article can be accessed on the publisher’s website.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1. In Bidarkota and Crucini (Citation2000), the quantity of exports of each commodity item was assumed to be constant because they did not have access to the time series on trade quantities at the fine level of detail of the commodity price data series. In contrast to that, we exploit a dataset which is constructed utilizing the country-level, detailed commodity terms of trade series, based on both the exports and imports quantities, as well as the individual, global commodity market price series.

2. Hence, we argue that using only the standard terms of trade series or the individual commodity price indices to examine the unanticipated effects of world trade prices on the aggregate economies may not provide the best possible information on the effects of world trade prices on the macroeconomic performance of these countries (see also Fernández, Schmitt-Grohé, and Uribe Citation2017).

3. We also tested the models with the HP filtered data. In general, the HP filtered data provided a little higher but consistent value of exposure than the Hamilton procedure.

4. We are grateful to an anonymous referee for this suggestion.

5. Blackburne and Frank (Citation2007) start the derivation of EquationEquation (5)(5)

(5) from the standard autoregressive distributed lag (ARDL) specification in the form

where the number of groups is

the number of periods is

is a

vector of explanatory variables;

are the

coefficient vectors;

are scalars, and

is the group specific effect. If the variables in the ARDL model are, for example, I(1) and cointegrated, then the error term is an I(0) process for all i. As stated by Blackburne and Frank (Citation2007), too, a principal feature of cointegrated variables is their responsiveness to any deviation from long-run equilibrium. This feature implies an error correction model in which the short-run dynamics of the variables in the system are influenced by the deviation from equilibrium. Hence, it is common to re-parameterize the ARDL model to the one given here in EquationEquation (5)

(5)

(5) .

6. Available at https://www.worldbank.org/en/research/commodity-markets.

7. See Online Appendix D for a detailed description of the variables.

8. The United Nations Conference on Trade and Development (UNCTAD Citation2019) state of commodity dependence report categorizes a country as commodity dependent if more than 60% of its total merchandise exports constitute of commodities during the period 2013–2017.

9. The groupings are reported in Online Appendix B. Henceforth Tables B.1, C.1, etc. and Figures B.1, C.1, etc. denote the results reported in the Online Appendix B, C, etc., respectively.

10. See the results for all the other country groupings and setups reported in the Online Appendix C.

11. We performed a robustness check using the standard HP filtering approach for all our analyses. However, we only report the results based on the Hamilton (Citation2018) filtering approach. The results based on the HP filtering data are available upon request.

References

- Agenor, P. R., and J. Aizenman. 2004. Savings and the terms of trade under borrowing constraints. Journal of International Economics 63:321–40. doi:https://doi.org/10.1016/S0022-1996(03)00069-2.

- Aguiar, M., and G. Gopinath. 2007. Emerging market business cycles: The cycle is the trend. Journal of Political Economy 115:69–102. doi:https://doi.org/10.1086/511283.

- Ben-Zeev, N., E. Pappa, and A. Vicondoa. 2017. Emerging economies business cycles: The role of commodity terms of trade news. Journal of International Economics 108:368–76. doi:https://doi.org/10.1111/iere.12263.

- Bidarkota, P., and M. J. Crucini. 2000. Commodity Prices and the Terms of Trade. Review of International Economics 8 (4):647–66. doi:https://doi.org/10.1111/1467-9396.00248.

- Blackburne, E. F., III, and M. W. Frank. 2007. Estimation of nonstationary heterogenous panels. Stata Journal 7 (2):197–208. doi:https://doi.org/10.1177/1536867X0700700204.

- Broda, C. 2004. Terms of trade and exchange rate regimes in developing countries. Journal of International Economics 63 (1):31–58. doi:https://doi.org/10.1016/S0022-1996(03)00043-6.

- Byrne, J. P., G. Fazio, and N. Fiess. 2013. Primary commodity prices: Co-movements, common factors and fundamentals. Journal of Development Economics 101:16–26. doi:https://doi.org/10.1016/j.jdeveco.2012.09.002.

- Céspedes, L. F., and A. Velasco. 2012. Macroeconomic performance during commodity price booms and busts. IMF Economic Review 60 (4):570–99. doi:https://doi.org/10.1057/imfer.2012.22.

- Collier, P., and B. Goderis. 2012. Commodity prices and growth: An empirical investigation. European Economic Review 56:1241–60. doi:https://doi.org/10.1016/j.euroecorev.2012.04.002.

- Deaton, A., and R. Miller. 1996. International commodity prices, macroeconomic performance and politics in sub-Saharan Africa. Journal of African Economics 5:99–191.

- Drechsel, T., and S. Tenreyro. 2018. Commodity booms and busts in emerging economies. Journal of International Economics 112:200–18. doi:https://doi.org/10.1016/j.jinteco.2017.12.009.

- Fernández, A., A. Gonzalez, and D. Rodriguez. 2018. Sharing a ride on the commodities roller coaster: Common factors in business cycles of emerging economies. Journal of International Economics 111:99–121. doi:https://doi.org/10.1016/j.jinteco.2017.11.008.

- Fernández, A., S. Schmitt-Grohé, and M. Uribe. 2017. World shocks, world prices, and business cycles: An empirical investigation. Journal of International Economics 108:2–14. doi:https://doi.org/10.1016/j.jinteco.2017.01.001.

- Fornero, J., M. Kirchner, and A. Yany 2016. Terms of trade shocks and investment commodity-exporting economies. Working Papers Central Bank of Chile 773.

- Gruss, B., and S. Kebhaj 2019. Commodity terms of trade: A new database. International Monetary Fund Working Paper 19/21.

- Hamilton, J. D. 2018. Why you should never use the Hodrick-Prescott filter. The Review of Economics and Statistics 100 (5):831–43. doi:https://doi.org/10.1162/rest_a_00706.

- Harberger, A. C. 1950. Currency depreciation, income, and the balance of trade. Journal of Political Economy 58 (1):47–60. doi:https://doi.org/10.1086/256897.

- Hodrick, R. J., and E. C. Prescott. 1997. Postwar U.S. business cycles: An empirical investigation. Journal of Money, Credit and Banking 29 (1):1–16. doi:https://doi.org/10.2307/2953682.

- Ilzetzki, E., C. M. Reinhart, and K. S. Rogoff. 2019. Exchange arrangements entering the 21st century: Which anchor will hold? Quarterly Journal of Economics 134 (2):599–646. doi:https://doi.org/10.1093/qje/qjy033.

- Im, K. S., M. H. Pesaran, and Y. Shin. 2003. Testing for unit roots in heterogeneous panels. Journal of Econometrics 115 (1):53–74. doi:https://doi.org/10.1016/S0304-4076(03)00092-7.

- IMF. 2018. Annual report on exchange arrangements and restrictions. Washington, DC: International Monetary Fund.

- Kose, M. A. 2002. Explaining business cycles in small open economies: How much do world prices matter? Journal of International Economics 56:299–327. doi:https://doi.org/10.1016/S0022-1996(01)00120-9.

- Kose, M. A., and R. Riezman. 2001. Trade shocks and macroeconomic fluctuations in Africa. Journal of Development Economics 65:55–80. doi:https://doi.org/10.1016/S0304-3878(01)00127-4.

- Laursen, S., and L. Metzler. 1950. Flexible exchange rates and the theory of employment. Review of Economics and Statistics 32 (4):281–99. doi:https://doi.org/10.2307/1925577.

- Levin, A., C. F. Lin, and C. Chu. 2002. Unit root tests in panel data: Asymptotic and finite-sample properties. Journal of Econometrics 108 (1):1–24. doi:https://doi.org/10.1016/S0304-4076(01)00098-7.

- Lopez-Martin, B., J. Leal, and A. M. Fritscher. 2017. Commodity price risk management and fiscal policy in a sovereign default model. Journal of International Money and Finance 96:304–23. doi:https://doi.org/10.1016/j.jimonfin.2017.07.006.

- Mendoza, E. G. 1991. Real business cycles in a small open economy. American Economic Review 81:797–889.

- Mendoza, E. G. 1992. The terms of trade and economic fluctuations. International Monetary Fund (IMF) Working Paper 92/98.

- Mendoza, E. G. 1995. The terms of trade, the real exchange rate, and economic fluctuations. International Economic Review 36:101–37. doi:https://doi.org/10.2307/2527429.

- Mendoza, E. G. 1997. Terms of trade uncertainty and economic growth. Journal of Development Economics 54:323–56. doi:https://doi.org/10.1016/S0304-3878(97)00046-1.

- Ostry, J., and C. Reinhart. 1992. Private savings and terms of trade. IMF Staff Papers 32:495–517. doi:https://doi.org/10.2307/3867471.

- Pesaran, M. H., Y. Shin, and R. P. Smith 1997. Estimating long-run relationships in dynamic heterogeneous panels. DAE Working Papers Amalgamated Series 9721.

- Pesaran, M. H., Y. Shin, and R. P. Smith. 1999. Pooled mean group estimation of dynamic heterogeneous panels. Journal of the American Statistical Association 94:621–34. doi:https://doi.org/10.1080/01621459.1999.10474156.

- Raddatz, C. September 2007. Are external shocks responsible for the instability of output in low-income countries? Journal of Development Economics 84(1):155–87. doi: https://doi.org/10.1016/j.jdeveco.2006.11.001.

- Roch, F. 2019. The adjustment to commodity price shocks. Journal of Applied Economics 22:1:437–67. doi:https://doi.org/10.1080/15140326.2019.1665316.

- Schmitt-Grohé, S., and M. Uribe. 2003. Closing small open economy models. Journal of International Economics 61:163–85. doi:https://doi.org/10.1016/S0022-1996(02)00056-9.

- Schmitt-Grohé, S., and M. Uribe. 2018. How important are terms-of-trade shocks? International Economic Review 59 (1):85–111.

- Shousha, S. 2016. Macroeconomic effects of commodity booms and busts: The role of financial frictions. mimeo. Columbia University.

- UNCTAD. 2019. The state of commodity dependence. International Trade and Commodities. Geneva, Switzerland: UNCTAD.

- Wickens, M. 2008. Macroeconomic theory: A dynamic general equilibrium approach. Princeton, NJ: Princeton University Press.