?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

Focusing on Asian economies over the period 2006 to 2019, we find that while non-bank finance appears to complement rather than substitute credit provision by the traditional banking sector, weaker regulatory quality is an important driving factor. Moreover, while we find that central bank policy rates countercyclically affect credit provision by non-banks, impulse responses to monetary policy shocks with and without non-bank finance indicate that the effectiveness of monetary policy as a transmission channel to GDP growth, inflation, house prices, and traditional bank credit is weakened in the presence of non-bank finance. Our paper has implications for monetary policy implementation, potentially incorporating non-banks into central bank operations and liquidity provision, as well as for financial supervisors on mitigating regulatory arbitrage.

1. Introduction

“Today’s central banks typically affect asset prices through primary dealers, or big banks, to which they provide liquidity at fixed prices – so-called open-market operations. But if these banks were to become less relevant in the new financial world, and demand for central bank balances were to diminish, could monetary policy transmission remain effective?” – Christine Lagarde (Citation2018, 6)

This paper examines the impact of credit provision by non-banks (including fintech and big tech credit) on the transmission of monetary policy in Asia over the period 2006 to 2019.Footnote1 A panel structural VAR (PSVAR) approach is used to generate impulse responses of key macroeconomic and financial variables – GDP growth, inflation, house prices, private credit to GDP – to monetary policy shocks in empirical models without and with non-bank finance to gauge the effect of non-bank finance on the monetary policy transmission mechanism. A stronger response of policy target variables in the former set of models to monetary policy shocks would imply that non-bank finance weakens the effectiveness of monetary policy transmission. There is no consensus in the literature on the role of non-bank finance for monetary policy, either theoretically or empirically, with much of the empirical work focusing on the United States. This paper contributes to the empirical literature using a novel approach, with a focus on Asian economies, that enables a counterfactual analysis to be undertaken.

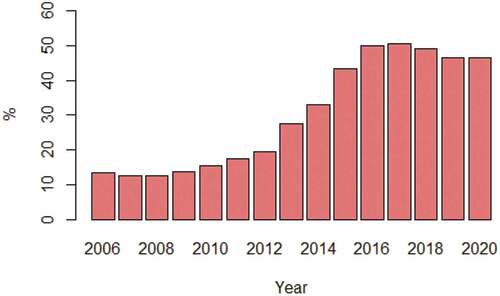

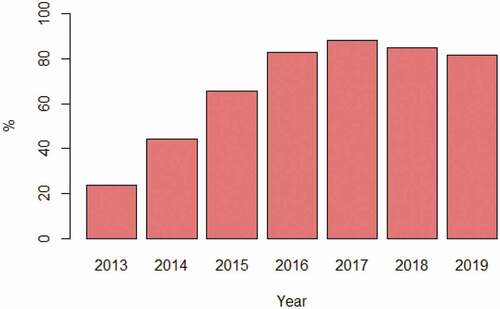

The focus on Asian economies is motivated by the significant growth of non-bank finance in the region over the past 15 years or so. The share of global non-bank credit held by Asian economies has risen from around 13% in 2006 to around 50% in 2019 (see ). Moreover, the increase in the share of global fintech and big tech credit held by Asian economies has been substantial, from less than 25% in 2013 to over 80% in 2019 (see ). McGuire et al. (Citation2021) make the point that non-banks in some Asian EMEs have grown to become significant creditors in global financial markets as opposed to comprising largely borrowers, also with implications for monetary policy transmission. Moreover, the rapidly changing nature of the credit intermediation landscape in Asia creates substantial challenges for effective monetary policy transmission. In addition, it is important to note that the relatively fragmented regional financial regulatory environment in Asia creates significant opportunities for regulatory arbitrage for non-banks in the region, with potential financial stability concerns (Acharya, Schnabl, and Suarez Citation2013; Aramonte, Schrimpf, and Shin Citation2021; BIS Citation2021).

Overall, this paper finds that while monetary policy has a statistically significant countercyclical effect on credit provision by non-banks in Asia, non-bank finance weakens the monetary policy transmission to GDP growth, inflation, house prices, and traditional bank credit. Our results may reflect frictions in the bank lending channel of monetary policy due to competitive pressures from non-banks. Our baseline results are robust to alternative estimation specifications and sub-samples of non-bank credit. The paper has implications for monetary policymakers in understanding the role of non-bank finance on monetary policy effectiveness. For example, our findings suggest a consideration for non-banks to be incorporated into central bank operations and liquidity provision. This is particularly important given the rapid growth of alternative forms of credit in the non-bank sector. There are also implications for financial stability and regulatory policy, as central banks seek to find the right balance in the monetary policy framework that both maximize the benefits of non-bank finance for monetary policy transmission while also minimizing the risks. In particular, excessive risk-taking by non-banks and regulatory arbitrage opportunities could expose systemic vulnerabilities in the financial sector, thereby pointing toward appropriately designed financial sector reforms and surveillance.

The rest of the paper is structured as follows: Section 2 discusses theoretical considerations and reviews the empirical literature. Section 3 presents the data and methodology employed in our analysis. Section 4 discusses our empirical results. Section 5 concludes.

2. Theoretical and Empirical Considerations

The research question in this paper is motivated by the increased importance of non-banks in credit provision in Asia in recent years which has stimulated debate about whether it enhances or worsens monetary policy transmission (e.g. Mohanty and Rishabh Citation2016). Related to this, the development of digital finance or fintech has continued strongly over the past decade or so, particularly in Asia, with implications for the transmission of monetary policy. From a theoretical perspective, with enhanced access to the financial system due to digitalization, via savings and credit channels, households, and firms can smoothen consumption over time (e.g. Mehrotra and Yetman Citation2014), which is particularly important in the face of a negative output shock. This implies that the central bank could affect inter-temporal consumption decisions of a larger proportion of the economy, thereby improving the effectiveness of monetary policy transmission, i.e. non-bank credit provision via fintech may improve the transmission of monetary policy through reducing financial frictions. There is also a counter-theoretical argument whereby the monetary policy transmission mechanism may be disrupted via regulatory arbitrage, with policy tightening by the central bank potentially leading to a loosening of credit conditions via the non-bank sector (e.g. Buchak et al. Citation2018; Hasan, Kwak, and Li Citation2020). In addition, as credit intermediation by non-banks would rise, this would have implications for the information content of monetary aggregates that form the basis of monetary policy formulation, and more broadly on how the economy responds to monetary policy (e.g. Bernoth, Gebauer, and Schäfer Citation2017).

This paper contributes to the growing literature on the implications of non-bank finance and fintech for the macroeconomic management of the economy through its effect on the monetary policy transmission mechanism. Early work by Cecchetti (Citation2002) noted that macroeconomic management becomes more complex in an environment of fintech given shifting trend productivity and difficulties in estimating potential output. The shift in financial intermediation away from traditional banks has implications for the transmission of traditional monetary policy, as large technology firms increasingly engage in the provision of financial services (Bernoth, Gebauer, and Schäfer Citation2017; Hasan et al., Citation2020; Mancini-Griffoli et al. Citation2018; Navaretti et al. Citation2017; Wong and Eng Citation2020). In addition, the involvement of so-called non-banks in liquidity transformation and leveraged lending creates financial vulnerabilities at the systemic level, and opportunities for regulatory arbitrage (Bank for International Settlements Citation2019). These vulnerabilities are amplified given the interconnectedness of non-banks with the traditional banking sector.

There is limited empirical research on the implications of fintech and the involvement of non-banks in lending on the effective transmission of monetary policy, and in particular how the traditional channels of monetary policy may be disrupted. One of the channels that may be affected by an increasing involvement of non-banks is the balance sheet channel, which is based on the premise that interest rate changes will affect the balance sheets of firms, thereby affecting the lending behavior of credit providers. Where there is a high or growing proportion of non-banks relative to traditional banks, the traditional balance sheet channel may be impaired as traditional banks compete with non-banks and therefore will have a greater incentive to insulate borrowers from monetary policy shocks (e.g. Bolton et al. Citation2016). Non-banks may also have implications for the bank lending channel of monetary policy. Monetary policy easing could facilitate higher leveraging of non-banks compared to traditional banks given that the latter may be constrained by prudential regulation. Capital requirements could also lead to a delayed response of traditional banks to interest rate changes (Van den Heuvel Citation2002). Therefore, non-banks could facilitate an amplified transmission of monetary policy in the presence of regulatory constraints on the traditional banking sector. There is no clarity, however, on extent of the effect of non-banks on the bank lending channel of monetary policy, given substantial differences in elasticities across non-banks to monetary policy shifts due to wide heterogeneity in firm size and access to capital markets, as well as variations in risk-taking preferences (IMF Citation2016). Some other empirical literature indicates that higher financial inclusion is associated with stronger monetary policy transmission to output in emerging Asia (e.g. Mehrotra and Nadhanael Citation2016).

On risk preferences, competition from the traditional banking sector for deposits and funding may lead to excessive risk-taking. Therefore, while the ongoing diffusion of digital finance into financial intermediation activity can spur economic activity and promote financial inclusion, there may be scope for rising financial fragility and systemic risk. The monetary policy risk-taking channel thus may be amplified due to an increasing presence of non-banks in the market as a result of differences in their business structures and operations compared to traditional banks, including through a higher reliance on short-term wholesale funding (Adrian and Shin Citation2011). The effectiveness of monetary policy can also be enhanced where fintech increases the sensitivity of asset prices to interest rate changes (e.g. Mylonas, Schich, and Wehinger Citation2000).

Overall, there is a lack of consensus in the theoretical and empirical literature on the extent and direction of the effect of non-banks on monetary policy transmission. The development of fintech and big tech credit over the past decade may improve the transmission of monetary policy via the reduction of financial frictions and enhancing financial inclusion (e.g. Rajan Citation2006). Monetary policy transmission could also be hindered due to regulatory arbitrage. In addition, as credit intermediation by non-banks would rise, this would have implications for the information content of monetary aggregates that form the basis of monetary policy formulation, and more broadly on how the economy responds to monetary policy. The lack of consensus in the literature is related to differences in studies on how to measure non-banks, differences in time periods and methodologies and differences across countries. Many US-based studies find that the balance sheet and bank lending channels of monetary policy are dampened due to fintech and non-bank lending, i.e. the effect of monetary policy shocks have the expected response in the traditional banking sector, but non-banks nullify this effect. For example, a monetary policy tightening may lead to constrained lending by traditional banks, with non-banks being less responsive to such shocks (Altunbas, Gambacorta, and Marques-Ibanez Citation2009). There lack a clear consensus, however, with other studies finding that the bank lending channel seems to be amplified due to non-banks, where non-bank responses to monetary policy shocks are found to be greater in magnitude than those of traditional banks (IMF Citation2016). Using data on regional-level adoption of fintech in the People’s Republic of China, Hasan et al. (Citation2020) find that fintech adoption mitigates monetary policy transmission to real GDP, consumer prices, and housing prices in the short term, and the growth of bank loans in the longer term, effects they attribute to regulatory arbitrage and competition between fintech and banks. Building on previous studies, with a focus on Asia, our paper uses a panel structural VAR approach to generate impulse responses of macroeconomic and financial variables to monetary policy shocks with and without non-bank finance, enabling a counterfactual assessment.

Some other previous work shows that fintech has a negative influence on the transmission mechanism of monetary policy, based on the premise that fintech encourages savings and investment outside traditional banking channels (Agarwal and Zhang Citation2020; Mumtaz and Smith Citation2020). In addition, digital finance in the form of currency has implications for monetary policy, although there remain some uncertainties on whether digital currency complement or substitute the prevailing monetary system (Brunnermeier, James, and Landau Citation2019). The emergence of private, decentralized cryptocurrencies erodes the ability of central banks to affect the money supply, thus negatively affecting monetary policy effectiveness (Fernández-Villaverde and Sanches Citation2019). This has led to discussions by central banks globally on whether they should issue their own digital currency (Auer, Cornelli, and Frost Citation2020; BIS Citation2018). While the scale of private cryptocurrencies is at the moment not at a level that would detrimentally affect macroeconomic stability and the conduct of monetary policy, there still remain questions as to how a central bank digital currency would affect traditional bank operations (particularly in times of financial crisis). That said, some academic research indicates that a central bank digital currency would enhance the effectiveness of monetary policy to the extent that these currencies bear interest (Bordo and Levin Citation2017).

Our paper is also related to the wider literature that considers the effect of non-banks and fintech on financial stability, the other core mandate of the central bank. In particular, challenges faced by policymakers in the regulation of non-traditional credit providers means that it may complicate the central bank’s mandate on safeguarding financial stability (Philippon Citation2017). However, like the case of monetary policy, there is no consensus in the empirical literature on whether fintech enhances or worsens financial stability (Fung et al. Citation2020). Kirilenko and Lo (Citation2013) find that financial stability risks may rise due to fintech as represented by algorithmic trading strategies that can exacerbate stock market contagion in crisis times. Other papers have pointed to the vulnerability of the peer-to-peer lending market where lenders are unable to appropriately price the risk of borrower default, thereby worsening the financial stability outlook (e.g. Mild, Waitz, and Wockl Citation2015). There also exists a range of studies that stress the benefits for financial stability due to fintech as a result of the greater efficiency of financial transactions and the diversification and risk-sharing features that it affords the financial system as a whole, as well as information transparency (e.g. Kosmidou et al. Citation2017). Other related literature includes work on the implications of fintech and digital technological advancement in the financial sector on the structure of the financial system as a whole, such as studies on effect of blockchain technology on central bank payment and clearing operations, which also have knock-on effects for the effective transmission of traditional monetary policy (e.g. Raskin and Yermack Citation2016).

3. Data and Methodology

For non-bank finance, data is attained for the period 2006Q1 to 2019Q4 for seven Asian economies (the People’s Republic of China (PRC); Hong Kong, China; India; Indonesia; Japan; Republic of Korea; Singapore). For fintech/big tech, data are available for 2013Q1 to 2019Q4 across ten Asian economies (the People’s Republic of China (PRC); Hong Kong, China; India; Indonesia; Republic of Korea; Malaysia; the Philippines; Singapore; Thailand; and Viet Nam). The countries selected as well as the data period were determined by the data availability. Additionally, the chosen sample period allows us to avoid possible structural breaks due to the COVID-19 pandemic. The first stage examines the determinants of non-bank finance and fintech credit, based on a set of banking sector variables, domestic fundamentals, and global factors. Drawing on the literature that examines the determinants of fintech credit, the banking sector variables include the banking credit/GDP, return on equity (ROE) of banks, and the Z-score of banks; domestic controls include GDP growth, GDP per capita, inflation rate, interest rate, and house prices, regulatory quality, plus risk indicators denoted by the VIX and a domestic financial stress index. These variables have been collected from Bloomberg, the BIS, the FSB, the IMF International Financial Statistics, and the World Bank. Regarding the fintech/big tech credit (relative to GDP), the data are taken from a new dataset constructed by Cornelli et al. (Citation2020), whereby fintech credit is defined as credit activity facilitated by electronic platforms that are not operated by commercial banks. Details of the variables, including their definitions, data sources, summary statistics as well as the plot of main variables are shown in the Appendix (see , and ).Footnote2 Underpinned by the earlier discussion of the theoretical and empirical consideration, our baseline equation to be estimated is as follows:

where yi,t represents non-bank finance, the narrow measure of non-bank financial intermediate lending, or fintech/big tech credit/GDP; xi,t represents a vector of banking sector–specific variables, including the banking credit/GDP, ROE of banks, and the z-score of banks; zi,t represents a set of domestic fundamentals; VIX is the Chicago Board Options Exchange (CBOE) Volatility Index, a measure of global risk aversion; δ1i are country-specific fixed effects; λ1t represents time fixed effects, a control for global shocks; and εi,t is the error term. The variables are lagged by one period to mitigate against endogeneity concerns.

Second, a panel structural vector autoregressive (PSVAR) model is used to examine (i) the response of non-bank sector credit provision to monetary policy shocks, and (ii) the response of GDP growth, inflation, house prices, and bank credit/GDP to shocks imposed on monetary policy where non-bank finance is an active market player compared to when it is excluded (i.e. switched off in the VAR).Footnote3 The PSVAR is implemented in a set-up across the same countries as in the fixed effects panel analysis. The PSVAR can be denoted as follows in its general specification, with structural shocks identified by a recursive restriction:

where is the matrix of the lag polynomial;

refers to the demeaned value of endogenous variables of country i to accommodate country-specific fixed effects; and

is a vector of structural disturbances. Crucially, monetary policy shocks are identified by assuming a Taylor-type rule for the monetary authority. Our identification strategy is based on a block recursive restriction (Christiano, Eichenbaum, and Evans Citation1999), which results in the following matrix

to fit a just-identified model:

The ordering of the variables imposed in the recursive form implies that the variables at the top (such as ) will not be affected by contemporaneous shocks to the lower variables (such as

,

), while the lower variables will be affected by contemporaneous shocks to the upper variables. Usually, it is preferable for slower-moving variables to be ordered before fast-moving variables (Bruno and Shin Citation2015). It follows therefore that we place the growth rate of GDP and inflation rate before the interest rate, reflecting a long-standing view that many macroeconomic variables are not affected instantaneously by monetary policy shocks (Christiano, Eichenbaum, and Evans Citation1999). Following the interest rate, we place house prices and banking sector variable – the bank credit to GDP ratio – in the ordering, which implies that these variables will only be affected by contemporaneous shocks to macroeconomic fundamentals and monetary policy. We place the non-bank credit variable in the last place in the ordering, which is not only based on the assumption that macroeconomic, monetary policy and banking variables will affect the development of non-bank finance, but also on the consideration of our first-stage empirical results that imply that these factors are driving non-bank finance. The lag selection of the panel SVAR model is based on the Akaike Information Criterion (AIC), which suggests that our model should have two lags.

4. Empirical Results

outlines the determinants of non-bank finance and fintech/big tech credit. In terms of monetary policy effectiveness, we find a negative and significant relationship between non-bank finance and the interest rate, indicating that the conduct of monetary policy is effective and countercyclical in nature. For fintech/big tech credit, however, we find no significant effect of the interest rate, indicating some friction in the transmission of monetary policy. Columns 1 and 2 report the results of our basic equation specification that examines the determinants of non-bank finance and fintech/big tech credit. The result shows that the development of non-bank finance and fintech/big tech credit is significantly affected by domestic traditional banking sector credit, GDP per capita, house prices, and global risk aversion.

Table 1. Determinants of non-bank finance and fintech/big tech credit: panel estimates.

We find that a higher level of GDP per capita leads to an increase in non-bank and fintech/big tech credit, indicating the importance of economic development as well as technological progress. On metrics from the traditional banking sector, overall, we find a positive relationship with non-bank finance and fintech/big tech credit.Footnote4 This indicates that the non-bank sector may act as a complement rather than substitute to the traditional banking sector. This is in alignment with the well-documented “credit rationing” to the private sector in EMEs compared to advanced economies, with domestic banks in EMEs historically more risk averse to lending to the private sector. Non-bank finance and alternative credit may help to fill that gap in EMEs. Interestingly, we find that a booming asset market (i.e., the housing market) negatively affects the non-bank finance and fintech/big tech credit, perhaps related to consumer preferences for lending from more traditional sources in the case of housing and mortgage loans. On risk, we find that non-bank finance (and fintech/big tech credit) is significantly affected the level of global risk aversion. Higher risk in the global financial system leads to an increase in non-bank finance, suggesting regulatory arbitrage may be at play. To add further weight to the regulatory arbitrage narrative, we find that lower regulatory quality boosts both non-bank finance-based lending and fintech/big tech lending. Finally, we also find that financial soundness negatively affects the development of non-bank finance.Footnote5

In an alternative specification, we also examine more closely the role of central bank independence on non-bank finance in Asia as well as interactions of regulatory quality with the domestic banking sector variables.Footnote6 Central bank independence (CBI) is an important factor that can influence the development of non-bank finance. Using the central bank transparency index of Dincer and Eichengreen (Citation2014) as a proxy CBI indicator, we find that a higher level of CBI leads to an increase in non-bank finance in Asia. This is in alignment with the finding that CBI may incentivize government authority to deregulate the financial market (Kern, Negre, and Aklin Citation2021). Concerning the potential effect of CBI on the effectiveness of the monetary policy, we examine this by including an interaction term that gauges the role of CBI in interest rate transmission. We find that the negative effect of the interest rate on non-bank finance becomes stronger if the level of CBI is higher, which is in line with the related literature on CBI and monetary policy effectiveness. We also interact regulatory quality with the domestic banking sector variables to examine the role of regulatory quality in the effect of the traditional banking sector’s development on non-bank finance. Our estimates indicate that a higher level of regulatory quality significantly dampens the positive relationship between the traditional banking sector and non-bank finance.

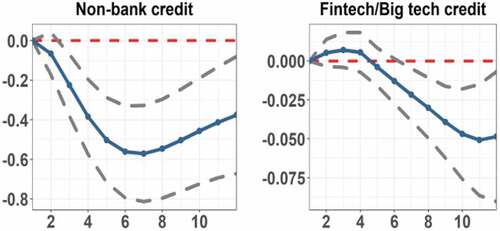

The regression analysis helps to provide empirical insights on main macroeconomic and financial factors that drive non-bank finance, including a separate analysis for fintech/big tech credit. Importantly, we find a significant relationship between non-bank finance and the interest rate, demonstrating a role for monetary policy on non-banks. To probe this relationship further, turning to the impulse response analysis, we first estimate the response of credit provision by non-banks and fintech providers to a monetary policy shock, as shown in .

Figure 1. Impulse responses to monetary policy shocks on credit provision by non-banks.

As can be seen in , the response of non-bank credit to a tightening in monetary policy is statistically significant and negative, in line with intuition. The significance of the reaction of non-bank finance is consistent with the earlier panel regression estimates, also affirming the countercyclicality of monetary policy. The response of fintech and big tech is also as expected, although its effect becomes significant only after some delay.

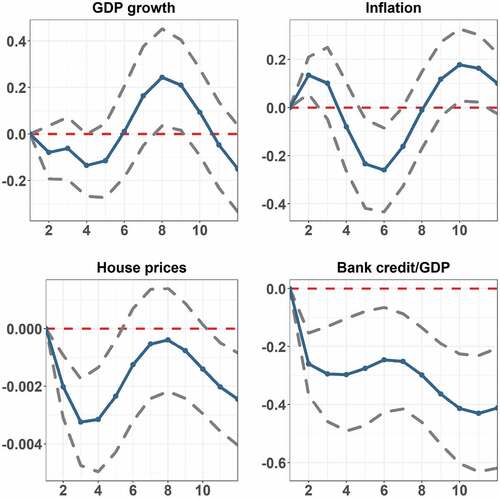

delve further into the role of non-bank finance in monetary policy transmission, presenting the impulse responses of a key monetary policy target variables to a tightening monetary policy shock, based on our estimated panel SVAR model.Footnote7 presents the results for a monetary policy transmission where non-bank finance is activated in the system, while in , non-bank finance is excluded. The monetary policy shock is defined as 25 basis points (bp) increase in the policy rate. The dashed lines in the figure report 95% confidence intervals.

Figure 2. Impulse responses to monetary policy shocks: with non-bank finance.

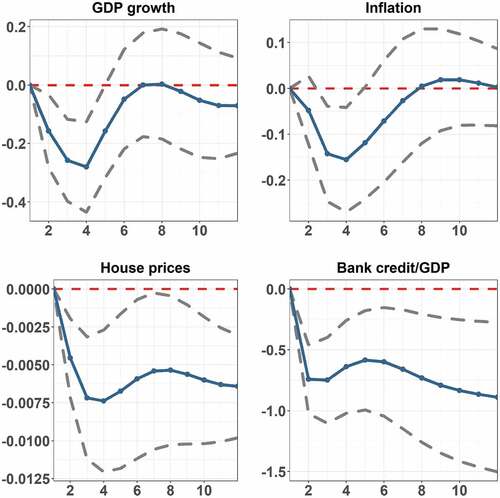

Figure 3. Impulse responses to monetary policy shocks: without non-bank finance.

From , we find that the negative response of inflation becomes statistically significant only after 5 quarters, and the effects are time-varying, while the response of GDP growth is not significant. For bank credit, this declines sharply on impact, and exhibits persistence and statistical significance over the full horizon due to the monetary policy tightening shock, with a peak effect of 0.42% points. In addition, house prices respond downward and significantly, at least in the short run. In order to examine the comparative role of non-bank finance on monetary policy transmission to key target variables, we also compute the monetary policy shocks where non-bank finance is excluded from the SVAR, as shown in .

shows that, in the absence of non-bank finance, GDP growth contracts significantly due to a monetary policy tightening, with a peak effect of 0.25% points after around four quarters. The transmission to GDP growth is therefore more effective than compared to the case with non-bank finance where no significant effect was found. In the model without non-bank finance, we also find that the response of inflation is less ambiguous than the model with non-bank finance, with monetary policy transmission demonstrating its expected effect. In particular, a 25 basis point rise in policy rate is associated with a drop in inflation of around 0.15% points at the peak after around 4 quarters. Moreover, house prices display a persistent negative decline after the tightening of monetary policy, which is in line with the previous literature that emphasizes the role of monetary policy in cooling down housing booms in support of financial stability (Williams Citation2016). The reaction of house prices is also more persistent and statistically significant where non-bank finance is switched off. In addition, the magnitude of the transmission to bank credit is are twice as large and more persistent in the scenario without non-bank finance, with a peak effect of 0.785% points. The evidence from the empirical work suggests therefore the presence of non-bank finance in the financial system detrimentally affects the transmission of monetary policy.

While some of the prevailing literature finds that non-bank finance, and in particular fintech credit, as well as the availability of financial services by fintech providers, can strengthen monetary policy transmission (Bolton et al. Citation2016; Buchak et al. Citation2018), we find the opposite. This may be related to disturbances to the bank lending channel of monetary policy caused by competition from non-banks. Closing the regulation gap between banks and non-banks may help to improve the overall effectiveness of monetary policy.

5. Conclusions

This paper empirically examines the effect of non-bank finance on the effectiveness of monetary policy transmission in Asian economies. Overall, we find that while non-bank finance appears to complement rather than substitute credit provision by the traditional banking sector, weaker regulatory quality is an important driving factor. Moreover, we find a negative relationship between central bank policy rates and non-bank finance, which affirms the countercyclicality of monetary policy. In addition, we find that the effectiveness of monetary policy as a transmission channel to GDP growth, inflation, house prices, and traditional bank credit is shown to be weaker in the presence of non-bank finance providers. Our paper has implications for monetary policy implementation, potentially incorporating non-banks into central bank operations and liquidity provision, as well as for financial supervisors on mitigating regulatory arbitrage through financial regulation reform. Policy makers need to ensure that non-bank finance is adequately taken on board in monetary policy decision-making, recognizing that a substantial share of credit intermediation is accounted for outside of the traditional banking sector. Excessive risk-taking by non-banks could lead to systemic risk vulnerabilities in economic downturns, with non-banks facing potential loss absorption difficulties, thereby further impairing effective monetary policy transmission. Research going forward is warranted on the balance sheet composition of non-banks and the related channels through which non-bank finance transmits through to the macroeconomy at different stages of the business cycle.

Disclaimer

The views expressed in this paper are the views of the authors and do not necessarily reflect the views or policies of ADBI, ADB, its Board of Directors, or the governments they represent.

Disclosure Statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

Notes

1. The countries include the People’s Republic of China (PRC); Hong Kong,China; India; Indonesia; Japan; Republic of Korea; Sinagpore; Malaysia; the Philippines; Thailand; Vietnam.

2. In terms of preliminary analysis (shown in in the Appendix), the fixed effects model is justified on the basis of results from a Hausman test. We use the quadratic interpolation procedure to convert the time series into a quarterly frequency. The interpolated variables include: fintech and big tech credit/GDP, ROE of banks, and the z-score of banks.

3. As regards the stationarity of the variables used in the PSVAR, panel unit root test results shown in in the Appendix indicate that the variables are stationary.

4. The data of banks’ ROE and z-score from the World Bank are only updated to 2017, and therefore are not available over the whole sample period.

5. Given the potential for exchange rate pass-through to prices, which would infer a significant role of the exchange rate in setting monetary policy, we carried out a robustness test incorporating the exchange rate. Overall it is found that the effect of monetary policy on non-bank finance does not depend on the exchange rate however. More specifically, the interaction term of the interest rate and exchange rate is not significant. Inclusion of the exchange rate therefore does not affect our baseline findings. These results are available from the authors upon request.

6. The additional specification of the empirical results is provided in in the Appendix.

7. For robustness, we also computed impulse responses based on PSVAR systems with and without fintech/big tech credit, the results of which are consistent with our baseline.

8. We exclude Argentina due to high inflation and Brazil due to potential measurement bias, as outlined by the Financial Stability Board (Citation2021).

9. Cornelli et al. (Citation2020) provide the detailed description of the sample of countries.

References

- Acharya, V., P. Schnabl, and G. Suarez. 2013. Securitization without risk transfer. Journal of Financial Economics 107 (3):515–36. doi:10.1016/j.jfineco.2012.09.004.

- Adrian, T., and H. S. Shin. 2011. Financial intermediaries and monetary economics. In Handbook of monetary economics, ed. B. M. Friedman and M. Woodford, Vol. 3, 601–50. Amsterdam: Elsevier.

- Agarwal, S., and J. Zhang. 2020. FinTech, lending and payment innovation: A review. Asia-Pacific Journal of Financial Studies 49 (3):353–67. doi:10.1111/ajfs.12294.

- Altunbas, Y., L. Gambacorta, and D. Marques-Ibanez. 2009. Securitisation and the bank lending channel. European Economic Review 53 (8):996–1009. doi:10.1016/j.euroecorev.2009.03.004.

- Aramonte, S., A. Schrimpf, and H. S. Shin. 2021. Non-bank financial intermediaries and financial stability. BIS Working Papers 972, Bank for International Settlements.

- Auer, R., G. Cornelli, and J. Frost. 2020. Rise of the central bank digital currencies: Drivers, approaches and technologies. BIS Working Paper No. 880, Bank for International Settlements, Basel.

- Bank for International Settlements. 2018. Central bank digital currencies. BIS committee on payments and market infrastructure, Bank for International Settlements, Basel, March.

- Bank for International Settlements. 2019. Big tech in finance: Risks and opportunities. BIS Annual Report 2019, 55–79.

- Bank for International Settlements. 2021. BIS quarterly review, Bank for International Settlements, Basel, December.

- Bernoth, K., S. Gebauer, and D. Schäfer. 2017. Monetary policy implications of financial innovation. DIW Discussion Paper, Deutsches Institut für Wirtschaftsforschung, Berlin.

- Bolton, P., X. Friexas, L. Gambacorta, and P. E. Mistrulli. 2016. Relationship and transaction lending in a crisis. The Review of Financial Studies 29 (10):2643–76. doi:10.1093/rfs/hhw041.

- Bordo, M. D., and A. T. Levin. 2017. Central bank digital currency and the future of monetary policy. NBER Working Paper No. 23711, National Bureau of Economic Research, Cambridge, MA.

- Brunnermeier, M. K., H. James, and J.-P. Landau. 2019. The digitalization of money. NBER Working Paper No. 26300, National Bureau of Economic Research, Cambridge, MA.

- Bruno, V., and H. S. Shin. 2015. Capital flows and the risk-taking channel of monetary policy. Journal of Monetary Economics 71 (C):119–32. doi:10.1016/j.jmoneco.2014.11.011.

- Buchak, G., G. Matvos, T. Piskorski, and A. Seru. 2018. FinTech, regulatory arbitrage, and the rise of shadow banks. Journal of Financial Economics 130 (3):453–83. doi:10.1016/j.jfineco.2018.03.011.

- Cecchetti, S. G. 2002. The new economy and the challenges for macroeconomic policy. National Bureau of Economic Research, NBER Working Paper No. 8935, National Bureau of Economic Research, Cambridge, MA.

- Christiano, L. J., M. Eichenbaum, and C. L. Evans. 1999. Monetary policy shocks: what have we learned and to what end? In Handbook of macroeconomics, ed. J. B. Taylor and M. Woodford, Vol. 1, 65–148. Amsterdam: Elsevier.

- Cornelli, G., J. Frost, L. Gambacorta, P. R. Rau, R. Wardrop, and T. Ziegler. 2020. Fintech and big tech credit: A new database. BIS Working Papers No. 887, Bank for International Settlements, Basel.

- Dincer, N. N., and B. Eichengreen. 2014. Central bank transparency and independence: Updates and new measures. International Journal of Central Banking 10 (1):189–259. doi:10.2139/ssrn.2579544.

- Fernández-Villaverde, F., and D. Sanches. 2019. Can currency competition work? Journal of Monetary Economics 106:1–15. doi:10.1016/j.jmoneco.2019.07.003.

- Financial Stability Board. 2021. Global monitoring report on non-bank financial intermediation. December.

- Fung, D. W. H., W. Y. Lee, J. J. H. Yeh, and F. L. Yuen. 2020. Friend or foe: The divergent effects of fintech on financial stability. Emerging Markets Review 45:100727. doi:10.1016/j.ememar.2020.100727.

- Hasan, I., B. Kwak, and X. Li. 2020. Financial technologies and the effectiveness of monetary policy transmission. IWH Discussion Paper No. 26/2020, Leibniz-Institut für Wirtschaftsforschung Halle, Halle.

- IMF. 2016. Monetary policy and the rise of nonbank finance. Global Financial Stability Report—Fostering Stability in a Low-Growth, Low-Rate Era, International Monetary Fund, Washington, DC.

- Kern, A., M. Negre, and M. Aklin. 2021. Does central bank independence increase inequality? Policy Research Working Paper No. 9522, World Bank, Washington, DC.

- Kirilenko, A. A., and A. W. Lo. 2013. Moore’s law versus Murphy’s law: Algorithmic trading and its discontents. Journal of Economic Perspectives 27 (2):51–72. doi:10.1257/jep.27.2.51.

- Kosmidou, K., D. Kousenidis, A. Ladas, and C. Negkakis. 2017. Determinants of risk in the banking sector during the european financial crisis. Journal of Financial Stability 33:285–96. doi:10.1016/j.jfs.2017.06.006.

- Lagarde, C. 2018. Central banking and fintech. A brave new world. Innovations 12 (1/2):4–8. doi:10.1162/inov_a_00262.

- Mancini-Griffoli, T., M. S. Martinez Peria, I. Agur, A. Ari, J. Kiff, A. Popescu, and C. Rochon. 2018. Casting Light on Central Bank Digital Currency. IMF Staff Discussion Note No. 08, International Monetary Fund, Washington, DC.

- McGuire, P., I. Shim, H. S. Shin, and V. Sushko. 2021. Outward portfolio investment and dollar funding in emerging Asia. BIS Quarterly Review, Bank for International Settlements, Basel, December.

- Mehrotra, A., and G. Nadhanael. 2016. Financial inclusion and monetary policy in emerging Asia financial inclusion in Asia. In Financial inclusion in Asia, ed. S. Gopalan and T. Kikuchi, 93–127. London: Palgrave.

- Mehrotra, A., and J. Yetman. 2014. Financial inclusion and optimal monetary policy. BIS Working Papers No. 476, Bank for International Settlements, Basel

- Mild, A., M. Waitz, and J. Wockl. 2015. How low can you go? — Overcoming the inability of lenders to set proper interest rates on unsecured peer-to-peer lending markets. Journal of Business Research 68 (6):1291–305. doi:10.1016/j.jbusres.2014.11.021.

- Mohanty, M. S., and K. Rishabh. 2016. Financial intermediation and monetary policy transmission in EMEs: What has changed since the 2008 crisis? In Monetary policy in India, ed. C. Ghate and K. Kletzer, 111–50. New Dehli: Springer.

- Mumtaz, M. Z., and Z. A. Smith. 2020. Empirical examination of the role of fintech in monetary policy. Pacific Economic Review 25 (5):620–40. doi:10.1111/1468-0106.12319.

- Mylonas, P., S. Schich, and G. Wehinger. 2000. A changing financial environment and the implications for monetary policy. OECD Economics Department Working Paper No. 243, Organisation for Economic Cooperation and Development, Paris.

- Navaretti, G. B., G. Calzolari, J. M. Mansilla-Fernandez, and A. F. Pozzolo. 2017. Fintech and banking. friends or foes? European Economy – Banks, Regulation, and the Real Sector 2:9–30. doi:10.2139/ssrn.3099337.

- Philippon, T. 2017. The fintech opportunity. BIS Working Paper No.s 655, Bank for International Settlements, Basel.

- Rajan, R. G. 2006. Has finance made the world riskier? European Financial Management 12 (4):499–533. doi:10.1111/j.1468-036X.2006.00330.x.

- Raskin, M., and D. Yermack. 2016. Digital currencies, decentralized ledgers, and the future of central banking. NBER Working Paper No. 22238, National Bureau of Economic Research, Cambridge, MA.

- Van den Heuvel, S. J. 2002. Does bank capital matter for monetary transmission? FRBNY Economic Policy Review 8 (1 A):259–65.

- Williams, J. C. 2016. Measuring the effects of monetary policy on house prices and the economy. BIS Papers No. 88, 7–16.

- Wong, C.-Y., and Y.-K. Eng. 2020. Implications of platform finance on monetary policy transmission. The Singapore Economic Review, forthcoming.

Appendix

Table A1. Overview of variables used in the empirical analysis.

Table A2. Summary statistics.

Table A3. Preliminary analysis.

Table A4. Determinants of non-bank finance and fintech/big tech credit: Alternative specifications.

Figure A1. Share of total global non-bank credit held by Asian economies.

Figure A2. Share of total global fintech/big tech credit held by Asian economies.

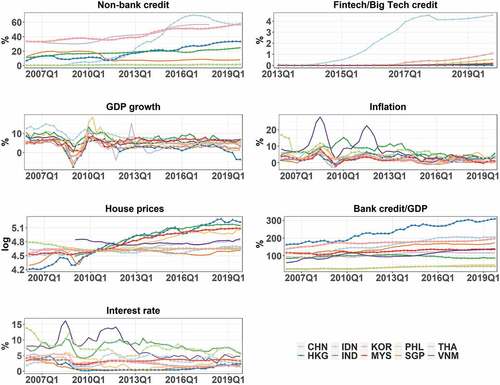

Figure A3. Time series of Main Variables Used in the Empirical Analysis.Notes: This figure plots the time series of the main variables used in this study, including non-bank credit to GDP ratio (%), fintech and big tech credit to GDP ratio (%), real GDP growth rate (%), inflation rate (%), real house prices (log), bank credit to GDP ratio (%), the interest rate (%). The indicators CHN, HKG, IND, IDN, KOR, MYS, PHL, SGP, THA, and VNM represent the People’s Republic of China (PRC), Hong Kong, India, Indonesia, the Republic of Korea, Malaysia, the Philippines, Singapore, Thailand, and Viet Nam, respectively.