ABSTRACT

This study investigates whether country-level institutions related to the labor market affect firms’ disclosure of information about their directors. Our findings, based on a sample of public companies domiciled in 46 countries, show that the level of disclosure of directors’ information, particularly information on their remuneration, is lower for firms in countries with better developed labor markets. We further find that in countries with more stringent labor regulations, firms are less likely to disclose both directors’ remuneration and biographical information. Firms in countries with better labor systems (e.g. greater mobility in the labor market and more effective social dialogue) make more such disclosures. Overall, our findings suggest that better developed country-level institutions related to the labor market disincentivize firms from disclosing information about directors. However, different types of country-level institutions have different impacts on firms’ incentives to make such disclosures. Our study provides valuable insights into how labor market development affects the alignment of boards’ incentives with those of stakeholders such as employees and how external pressure from employees affects a firm’s strategic actions regarding disclosing directors’ information.

JEL:

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Supplemental data

Supplemental data for this article can be accessed online at https://doi.org/10.1080/1540496X.2023.2203810

Notes

1. See Appendix C for detailed definitions of each country-level institutional variable associated with labor market development.

2. One indicator of the role directors’ information plays in both the capital and labor markets is the Dodd-Frank Act, which requires publicly owned companies to report the so-called “CEO pay ratio” to reveal how wide the gap is between the compensation earned by average workers and their CEOs.

3. Choi, Frosy, and Meek (2002) define countries with heavy central government intervention, in addition, have been closed to foreign investment and international competition are countries with closed information system.

4. Fama and Jensen (1983) suggest that self-interested directors are more likely to engage in window dressing and induce firms to offer higher compensation.

5. Sustainalytics assigns a value of 50 to firms whose disclosure levels are broadly in line with market practice or for which data are not yet available, and thus does not distinguish between these two reasons. Therefore, in our tests, we delete all firm-month observations with a score of 50. However, including all observations with a score of 50 in our sample does not change the conclusions of our study.

6. A country’s labor market development on its own (i.e., separate from institutional or cultural factors) may cause changes in directors’ information disclosure levels. As a result, endogeneity could be an issue if there are one or more confounding variables that are correlated with both the main independent variable (a country’s labor market development) and the dependent variable (disclosure of directors’ information). In addition, simultaneity bias could be an issue if labor market development measures depend to a degree on firms’ disclosure levels. In this study, we use the lagged independent variables to reduce concerns about endogeneity and simultaneous causality.

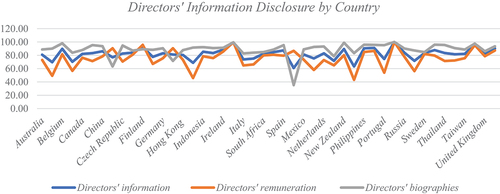

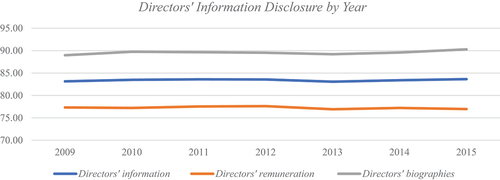

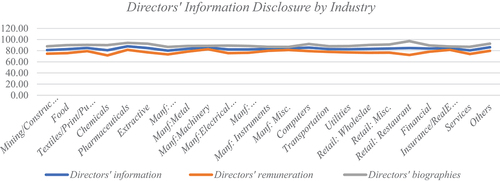

7. For ease of observation, present the average values of Directors’ Information across countries, years, and industries, respectively.

Figure 1. Average disclosure level of directors’ information by country.

Figure 2. Average disclosure level of directors’ information by year.

Figure 3. Average disclosure level of directors’ information by industry.

8. The drop in observations is because the use of one-year lagged independent variables in the regression model.

9. In the first-stage, we use a firm’s number of employees as the instruments for a country’s labor market development, and regress a country’s labor market development (Labor Market) on the firm’s disclosure information (Directors’ Information) and a set of control variables (i.e., a country’s GDP (GDP), whether a country mandates ESG disclosure (Mandatory), whether a country implements corporate governance reform (Reform), a country’s legal origin (Legal Origin), and a country fixed effect). Research shows that all of these control variables can affect a country’s labor market development (Ashenfelter and Card 1999; Freeman 2007). Then, we estimate our EquationEquation (1)(1)

(1) by including the predicted values from the first-stage regression model; Since studies (Dhaliwal et al. 2012; Ramanna 2013) suggest that a firm’s number of employees affects the firm’s transparency only through a country’s labor market, we expect firms with more employees to be more likely to disclose directors’ information. Therefore, the firm’s number of employees could be a good instrument for a country’s labor market. We also run the Hansen – Sargan over-identification test and the Stock and Yogo weak instrument test (Stock and Yogo 2005) to investigate the validity of our instrument. Based on the results from the Hansen – Sargan test (J-statistic = 3.87, p = .29) and weak instrument test (critical value=16.85, using 5% bias, is less than the F-statistic (30.09)), we conclude that our instrument is appropriate to use when the dependent variable is Directors’ Information.

10. Number of observations is dropped due to a further merge of ASSET 4 dataset with our current dataset.

11. The CBR Leximetric data sets provide data on labor laws in 117 countries for the period between 1970 and 2013. As our sample period (2009–2015) extends beyond 2013, we use a country’s average LRI score for 2005–2013 to represent its scores in the remaining years of our period of analysis, i.e., 2014–2015. This approach appears justifiable, as a country’s LRI tends to remain stable or change very slowly over time.

12. Because both Labor System and Labor Regulation are a function of Labor Market, these two independent variables are correlated and there is a possibility that this correlation could result in high levels of multicollinearity (Lennox, Francis, and Wang 2012). However, the results of a variance inflation factor (VIF) test yield VIF values of 3.63 and 3.14 for Labor System and Labor Regulation, respectively, and a mean VIF value of 2.62 for the regression model, suggesting that any multicollinearity between Labor System, Labor Regulation, and the independent variables in the regression model is not severe (Green 2008).

13. If a country’s Labor System (Labor Regulation) is ranked in the upper (lower) 25% of Labor System (Labor Regulation) in our sample countries in year t, we denote these countries as having high (low) levels of Labor System (Labor Regulation).

14. We include the same set of control variables as in EquationEquation (1)(1)

(1) , as research shows that these country-level institutional factors and firm attributes have an impact on firms’ performance (Saona and Martin 2018; Sharma, Sharma, and Litt 2018; Younge and Marx 2012).