?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

The Photovoltaic industry promotes the transformation of China’s energy structure to green and low-carbon, which is of great significance to achieve the goal of “Carbon Peaking and Carbon Neutrality.” At present, the industry is mainly faced with problems such as the drastic reduction of government subsidies and the difficulty of financing. From the perspective of independent auditing, our paper takes 54 A-share listed photovoltaic companies in China from 2011 to 2020 as the research object to study the impact of audit quality on financing efficiency, and the role of agency costs in the relationship between audit quality and financing efficiency.The results show that audit quality is positively related to financing efficiency. For every 1% increase in audit quality, the financing efficiency will increase by 13%. In addition, agency cost plays an intermediary role between audit quality and financing efficiency. For every 1% increase in audit quality, agency cost can be reduced by 34% and financing efficiency can be increased by 25%.

1. Introduction

As China’s energy consumption has depended on fossil and other scarce resources for a long time, it may lead to problems such as unreasonable energy structure or environmental pollution. In September 2020, at the 75th Session of the United Nations General Assembly, China explicitly set the goals of “Carbon Emissions” by 2030 and “Carbon Neutrality” by 2060. To achieve the purpose of “Dual Carbon,” China continues to promote the adjustment of energy structure and vigorously develop renewable energy. Solar energy is valued for its unique advantages. Firstly, as a renewable energy source, solar energy can be used freely without geographical or spatial restrictions. Secondly, as one clean energy, solar energy can reduce greenhouse gas emissions and alleviate air pollution. Finally, because of its universality, solar energy will not be monopolized and cause an energy crisis. Qi and Zhang (Citation2017) also put forward the technological advantages of solar energy: pollution-free production, no energy consumption, no regional restrictions, and saving land resources. Liang Xu et al. (Citation2018) studied the environmental cost and economic benefit of China’s photovoltaic enterprises from 2011 to 2016 by using the life cycle assessment method. Although the ecological price is higher than the financial benefit, the financial benefit increases with the rapid growth of the photovoltaic market industry.

At present, China’s photovoltaic enterprises rank among the top globally in terms of manufacturing scale, industrial technology level, application market expansion, and industrial system construction. The rapid development of photovoltaic enterprises in the early stage is due to financial subsidies. Government subsidies improve the operating performance of photovoltaic enterprises (An and Wang Citation2018), innovation performance (Lin and Luan Citation2020), and technological innovation (Jiang et al. Citation2021). Meanwhile, the photovoltaic enterprises have entered the mature stage, with further expansion of capital demand and a series of inefficiency problems caused by fiscal subsidies. Cai et al. (Citation2019) used data enveloping analysis to measure the efficiency of China’s photovoltaic enterprises. They found that the overall efficiency of the photovoltaic power generation industry is at a low level. In addition, Yang, Lin, and Chen (Citation2017) analyzed that due to the poor competitiveness of photovoltaic products, excessive reliance on technology introduction, low level, repetitive production, and low entry threshold of the industry, the photovoltaic enterprises have excess capacity. On May 31, 2018, the National Development and Reform Commission, the Ministry of Finance, and the National Energy Administration issued a notice on photovoltaic power generation in 2018, limiting the scale of distributed power stations and significantly reducing subsidies for centralized and distributed power stations per kilowatt-hour. This policy reduces financial donations, resulting in the need for capital market support for photovoltaic enterprises. Different from traditional industries and high-tech industries, photovoltaic enterprises are typical capital-intensive enterprises. On the one hand, it has a significant demand for capital, a long investment cycle, a considerable risk of use, and the need for money runs through the entire industrial process. On the other hand, direct financing and indirect financing in the securities market provide limited support to photovoltaic enterprises. The funding of photovoltaic enterprises is a severe problem (Zhang et al. Citation2018). Studies have shown that after the “countervail” policy, many enterprises went bankrupt, and banks blocked some photovoltaic enterprises, resulting in higher financing costs (Li Xu et al. Citation2020). In addition to financing difficulties, photovoltaic enterprises have a significant problem of “Light Abandonment and Power Limitation.” In 2018, with the decline of China’s demand, the capacity utilization rate of small and medium-sized enterprises decreased to less than 50%, and the efficiency of capital use was not high. Despite the continuous reduction of subsidies in photovoltaic enterprises, the distributed photovoltaic power station project still has a high internal rate of return (Zhao and Wang Citation2019). Therefore, studying the financing efficiency of listed companies in photovoltaic enterprises is helpful to solve their financing problems, speeding up their development process, and reducing the environmental pollution. Based on the above financing situation of the photovoltaic enterprises, our paper studies the financing efficiency of photovoltaic enterprises.

So far, researches on the financing efficiency of photovoltaic enterprises mostly start from the perspective of financing difficulty. Eichhammer, Ragwitz, and Schlomann (Citation2013) proposed that the funds for renewable energy mainly come from the public budget with low efficiency. New sources of financing are therefore required in addition to national budgets. Barkatullah and Ahmad (Citation2017) mentioned financing challenges based on analyzing the significant capital demand, high construction risk, and protracted cycle of the new energy industry, and new energy project funds come from the public sector, so it is necessary to seek new financing channels to relieve the pressure of government departments. Kabir et al. (Citation2018) pointed out that the development of solar technology is an essential solution to the growth of energy demand and discussed many problems faced by the solar industry. In addition to technological uncertainty and low energy efficiency, high investment costs and a lack of financing mechanisms restrict the development of the solar industry. Wu et al. (Citation2021) point out that the financing scale of photovoltaic power generation in Cameroon is insufficient. The financing structure is single, and the financing gap is large, which seriously hinders the development of photovoltaic power generation. Photovoltaic enterprises are also constantly seeking solutions. Feldman, Jones-Albertus, and Margolis (Citation2020) verified the impact of R&D activities on the financing cost of the solar industry and concluded that R&D contributes to the reduction of financing cost of the solar industry, that is, R&D affects the financing efficiency of the solar industry.

The financing efficiency of photovoltaic enterprises has some problems. Ma, Xu, and Yu (Citation2017) used the DEA method to measure the financing efficiency of photovoltaic enterprises from 2013 to 2015 and concluded that the financing efficiency of photovoltaic enterprises is at a low level. Lyu and Shi (Citation2018) evaluated the financing efficiency of different parts of the global renewable energy industry and other financing methods, and comprehensively concluded that all new energy industries are in a state of low efficiency, and compared with the photovoltaic enterprises, the wind power industry is more efficient. Due to the unique nature of the photovoltaic enterprises, part of the technical knowledge needs to be kept secret, which further exacerbates investors’ lack of understanding of photovoltaic enterprises. Due to information asymmetry, photovoltaic investors have high risks investing in power station projects (Tan, Tan, and Rong Citation2018). Studies have proved that due to the opaque information of SMEs, banks find it difficult to distinguish between risky and non-risky enterprises, resulting in financing difficulties (Palazuelos, Crespo, and Corte Citation2017). As a third-party regulator, an audit plays a vital role in information transmission and increases the credibility of corporate information disclosure (Wardhani and Zhou Citation2019). To a certain extent, audit quality represents the authenticity of accounting information released by enterprises to the outside. In addition, a high-quality audit is conducive to investors’ understanding and investment in photovoltaic enterprises, and studies have shown that independent audit plays a governance role in some companies (Chen et al. Citation2011), which has a particular impact on the internal organizational structure, investment decisions and capital use of enterprises. Our paper studies the impact of audit quality on financing efficiency based on the special industrial background of the photovoltaic industry.

In terms of influencing factors, because audit quality cannot be directly observed, previous scholars mainly focused on auditor independence (Olivia Furiady and Kurnia Citation2015), abnormal audit fees (Jung, Kim, and Chung Citation2016), audit fees (Martinez and Moraes Citation2017), firm size (Kim et al. Citation2017), auditor Professionalism (Salehi, Fakhri Mahmoudi, and Daemi Gah Citation2019), auditor experience (Haeridistia and Agustin Fadjarenie Citation2019), auditor motivation and objectivity (Zahmatkesh and Rezazadeh Citation2017), corporate transparency (Johl et al. Citation2021) and the level of internal governance of listed companies (Aiqadasi and Abidin Citation2018). In terms of economic consequences, some scholars study the impact of high-quality audits on listed companies. Boubaker et al. (Citation2018) studied the economic consequences of audit quality and its impact on enterprise investment efficiency. Beisland, Mersland, and Str?m (Citation2015) studied that high-quality audit is conducive to the improvement of the internal governance level of listed companies. Lin, Wan, and Chen (Citation2019) confirmed that external audits can be used as an alternative means of internal control to inhibit the earnings management of marine enterprises, and the audit quality is significantly negatively correlated with earnings management. Shubita (Citation2021) studied the impact of audit quality on the market value of listed companies and confirmed that the size of the firm, audit fees, and audit tenure are not necessarily related to the market value. The research on the relationship between audit quality and financing mainly focuses on the impact of audit quality on enterprise value Taqi (Citation2013) and debt financing cost (Coffie, Bedi, and Amidu Citation2018), while the research on the financing efficiency of external governance mechanisms is relatively few. A summary of related studies is shown in .

Table 1. Summary of audit quality research status.

To sum up, as shown in , the research status at home and abroad mainly focuses on audit quality, the current situation of photovoltaic enterprise financing, and the relationship between audit quality and financing issues.

Table 2. Analysis table of research status in China and other countries.

Based on the signal transmission theory and principal-agent theory, this paper studies the impact of audit quality on financing efficiency, expanding the research on the influencing factors of financing efficiency and enriching the research on the economic consequences of audit quality. In addition, the development of photovoltaic enterprises plays a vital role in protecting the environment and realizing the upgrading of energy structure. Therefore, studying the financing efficiency of Chinese photovoltaic enterprises will help solve their current development problems and promote their rapid development.

The remainder of the paper is organized as follows. The theoretical basis and hypothesis building will be presented in Section 2. To verify the hypothesis proposed in the article, our paper established a multiple linear regression model concerning the selection of indicators by Fang and Wu (Citation2015), Wang and Wang (Citation2016) and other predecessors, and used the mediation test method proposed by Wen (Wen et al. Citation2004) to test the mediating variable will be introduced in Section 3. Section 4 contains empirical results, followed by the discussion in Section 5. Finally, the conclusion will be offered in Section 6.

2. Hypothesis formulation

According to financing efficiency, financing behavior is divided into two stages: the fund-raising stage and the fund allocation stage (Li and Wu Citation2016). For the financing stage of the photovoltaic enterprises, the delayed issuance of government subsidies (Tan, Tan, and Rong Citation2018) and the policy of decreasing government subsidies have aggravated the financing difficulty. Swarnalakshmi and Seth (Citation2015) also mentioned that renewable energy has met India’s energy demand and alleviated environmental pressure, and developed rapidly. Still, financing has become a massive obstacle to its development, and financial support is needed. Luo et al. (Citation2016) also pointed out the problems faced by distributed photovoltaic power generation: financing difficulties, unclear definition of housing property rights, risks in photovoltaic power generation policies, risks in access to the power grid, and uncertainties in profitability. The photovoltaic enterprises need to turn to capital markets for funding. For banks or individual investors, due to the limitation of professional ability, it is impossible to deeply understand photovoltaic enterprises, which leads to financing difficulties in photovoltaic enterprises. Even sector investors, faced with financing needs, have to invest time and cost to understand the photovoltaic sector, resulting in higher financing costs for the photovoltaic enterprises. When conducting audit services, auditors, as professionals, can employ external experts to better complete audit services for professional problems in photovoltaic enterprises on the premise of following audit standards. Independent audit effectively reduces internal and external information asymmetry. Kontokosta, Spiegel-Feld, and Papadopoulos (Citation2020) demonstrated that mandatory energy audits minimize energy consumption in residential buildings and office buildings by increasing access to information disclosure. In addition, the hiring of auditors itself is also a signal of good management. Aobdia, Lin, and Petacchi (Citation2015) confirmed that high-quality hiring auditors send a positive sign to the market, on the one hand, enhancing the credibility of financial reports, on the other hand, reducing the cost of debt, and enterprises obtain a more significant amount of credit without requiring collateral. In addition to enhancing external investors’ trust in photovoltaic enterprises, a high-quality audit also provides a guarantee for investors. An audit is an authentication service that provides reasonable assurance, and the reasonable assurance provided by an audit plays an actual value. The loan interest rate of audited enterprises is lower (Blackwell et al. Citation1998). Cole-Baker and Bowyer (Citation1998) proposed that independent audit plays a significant role in companies that need to raise funds, and going concern audit helps enterprises obtain funds. Hou et al. (Citation2019) proved that auditors with overseas experience could significantly reduce the financing costs of enterprises. Based on the above influence of audit quality on financing activities of the photovoltaic enterprises, the following hypotheses are proposed in our paper:

Hypothesis 1.

Audit quality has a significant positive impact on the fund-raising efficiency of photovoltaic enterprises.

For photovoltaic enterprises, fund allocation efficiency refers to how photovoltaic enterprises use capital. The silicon raw material link upstream of the photovoltaic enterprises has high technical barriers, and the technology of producing mono-crystalline silicon and poly-silicon is not mature, resulting in low production capacity and low capital utilization efficiency. Low capital and technical barriers in the battery manufacturing process in the middle reaches. Faced with a large amount of foreign demand, enterprises overproduce and repeat production, which eventually leading excess capacity. The biggest problem of downstream power plants in photovoltaic enterprises is light abandonment. Solar power plants cost money to build, and the electricity they produce cannot be connected to power plants due to storage problems, leading to the pain of “light abandonment.” The reason is the construction and technical problems of the power station. Therefore, the issue of excess capacity and “light abandonment” in photovoltaic enterprises seriously affects the use efficiency of capital. Based on the principal-agent theory, the creditor will make a contract when providing funds to the enterprise. Creditors generally stipulate the use of funds in the contract and limit the use of funds by shareholders. However, creditors cannot fully know the use of funds. In real life, shareholders often violate the spirit of the contract, illegally use the funds obtained from financing, damage the interests of creditors, and cause agency problems. Although the accounting firm is a third-party service organization entrusted by the company’s shareholders, the audit opinions and audit reports issued by the auditors are public, so the attestation services provided by the certified public accountants can also be regarded as the supervision of shareholders’ behavior. According to the principal-agent theory and the governance role of audit, audits can supervise management activities, reduce agency problems, and ultimately affect the efficiency of capital allocation. The independent third-party independent audit can supervise the daily operation and management activities of the photovoltaic enterprises, promote correct project investment, and further improve the efficiency of capital allocation. Studies have shown that the Big Four firms are better than the non-Big Four firms in preventing management from encroaching on shareholders’ economic interests through cash and other liquid assets (Huang et al. Citation2019). Internal auditors can help institutions improve their governance (Beisland, Mersland, and Str?m Citation2015). As a governance mechanism of enterprises, independent audit inhibits the earnings management behaviors of enterprises (Kouaib and Jarboui Citation2014). A high-quality audit improves the corporate governance system and improves corporate performance (Favalli, Gori Maia, and da Silveira Citation2020). Based on the above analysis, our paper proposes the second hypothesis:

Hypothesis 2.

Audit quality has a positive impact on the fund allocation efficiency of photovoltaic enterprises.

Scholars have studied the impact of independent audits on financing costs from its reputation mechanism and the governance role. Sattar, Javeed, and Latief (Citation2020) proposed that audit quality could help improve the financial performance of enterprises based on the manufacturing data of Pakistan from 2008 to 2017. Based on the case study of audit failure, Hakim and Omri (Citation2010) confirmed that the value of accounting information is positively correlated with the reputation, professionalism, and experience of auditors through the analysis of Tunisian capital market auditors. Chen, Saffar, and Srinidhi (Citation2017) found that high audit quality is related to a high proportion of public debt and a correspondingly low proportion of bank debt in corporate debt financing through an extensive sample survey of American companies. In companies with high information asymmetry and poor governance, the impact of audit quality on debt structure is more significant. High audit quality improves corporate transparency and assuages lenders’ fears, thus enabling companies to borrow more information-sensitive debt. Cheng et al. (Citation2020) believe that audit partners are considered subordinate partners if their clients are subject to sanctions due to financial disclosure, and research finds that equity financing will be reduced without changing inferior partners. Bostan et al. (Citation2021) confirmed that government audit institutions minimize the government deficit and total government debt, ensure the sustainability of public finance and improve government efficiency through their organizational structure, nature of activities, and professionalism. According to the signal transmission theory, in the research on the relationship between audit quality and financing efficiency, creditors are at an information disadvantage and maintain a cautious attitude toward the financing needs of enterprises, which increases the difficulty for enterprises to obtain funds. At this time, the high-quality audit can act as a guarantor to send a signal to creditors, play a role in increasing credit, and improve creditors’ trust in the enterprise. The higher the audit quality, the more authentic the signal is. Generally, investors in the capital market recognize the enterprises audited by the four major firms and believe that such enterprises operate well, which makes it easier to invest funds in such enterprises, resulting in the reduction of financing costs of enterprises, thus affecting the financing efficiency. Based on the principal-agent theory, creditors will make contracts when providing funds to enterprises. Creditors will generally specify the purpose of funds in the contract and restrict the use of funds by shareholders. However, creditors cannot fully know the purpose of the use of funds. In real life, shareholders often use the funds obtained by financing in violation of the spirit of the contract, damaging the interests of creditors and causing agency problems. Although the accounting firm is a third-party service institution entrusted by the company’s shareholders, the audit opinions and audit reports issued by auditors are public, so the assurance services provided by certified public accountants can also be regarded as the supervision of shareholders’ behavior. According to the principal-agent theory and the governance role of audit, the audit can supervise the activities of management, reduce agency problems, and ultimately affect the efficiency of fund allocation. Based on the above analysis of audit quality on fund-raising efficiency and fund allocation efficiency of the photovoltaic enterprises, the paper believes that audit quality has a significant impact on fund-raising efficiency and fund allocation efficiency of the photovoltaic enterprises. On the basis that the financing efficiency of the photovoltaic enterprises includes fund-raising efficiency and fund allocation efficiency, our paper puts forward the third hypothesis:

Hypothesis 3.

Audit quality has a positive impact on the financing efficiency of photovoltaic enterprises.

The existence of enterprise agency problems may not only increase the difficulty of fund-raising, but also reduce the efficiency of fund use. Firstly, in the fund-raising stage, shareholders tend to operate with high liabilities, while creditors are difficult to provide high funds to ensure funds’ safety. The inconsistency of interests between them leads to the difficulty of fund-raising and agency problems. Equity financing is the same. Due to the existence of agency problems, investors cannot trust enterprises, which also increases the difficulty of fund-raising in the capital market and reduces the efficiency of fund-raising. Secondly, in the stage of capital allocation, the common agency problems between management and shareholders will also affect the efficiency of capital allocation. High consumption of management, illegal use of funds, and short-term behavior will affect the efficiency of fund allocation and reduce the effectiveness of fund allocation.

In essence, the agency problem originates from information asymmetry. In the process of financing, the information asymmetry between the financing parties leads to financing difficulties and increases transaction costs. Stnic (Citation2016) pointed out that information asymmetry makes financial market participants unable to use enough information to take action and obtain the optimal decision, which may lead to wrong transactions and losses. Doukas, Kim, and Pantzalis (Citation2008) confirmed that the reports of securities analysts could increase the transparency of enterprises, make investors understand and trust enterprises, and increase the external financing of enterprises. Chod et al. (Citation2017) found that block-chain can enhance the transparency of business processes and make information transmission more effective, that is, block-chain technology provides the ability to obtain favorable financing terms at a lower information cost. Therefore, the key to solving the financing problem is to increase the degree of information transparency and reduce the information asymmetry between the financing parties.

A high-quality audit can increase the reliability, authenticity and transparency of information disclosed by enterprises, reduce the information asymmetry between financing parties, reduce agency problems in the stage of fund-raising, and improve the success rate of financing. At the same time, the supervisory role of a high-quality audit can replace creditors to supervise the use of funds by financing enterprises, avoid risky projects, reduce agency problems and reduce the difficulty of financing. In the midstream battery manufacturing link, photovoltaic enterprises are more likely to pursue production capacity excessively and ignore market demand, resulting in overcapacity. Auditors can reduce managers’ short-term investment behavior and inefficient investment behavior effectively through supervision, and prevent managers from using funds for high-risk investment and over-investment. Based on the impact of audit quality on the agency problem in the fundraising and allocation stages above, our paper puts forward the following assumptions:

Hypothesis 4.

Audit quality affects the financing efficiency of photovoltaic enterprises by reducing agency costs positively.

3. Materials and method

3.1. Samples and data sources

Our paper takes photovoltaic enterprises as the research object and selects 257 photovoltaic concept stocks on https://www.eastmoney.com/. Due to the extensive range of photovoltaic concept stocks, 68 listed companies mainly engaged in photovoltaic business are chosen based on photovoltaic concept stocks. Considering that the development of the photovoltaic enterprises is greatly affected by the “anti-subsidy” and “anti-dumping” policies in 2012 and the policies of reducing subsidies in 2018, the ten-year data from 2011 to 2020 are selected for research. After deleting samples lacking data and sample companies listed after 2011, 54 listed companies mainly engaged in photovoltaic business were selected.

The input-output indicators and related data used to measure financing efficiency in our paper are all from the CSMAR database and the RESSET database. When data is lacking, 540 sample data are obtained through the annual reports of sample companies. STATA14 software was used to test the relationship between audit quality and financing efficiency of the photovoltaic enterprises. Fund-raising efficiency and fund allocation efficiency are measured by DEAP2.1 software.

3.2. Empirical model

In our paper, model 1 is constructed to verify the impact of audit quality on the fund-raising efficiency of photovoltaic enterprises. Model 2 is built to demonstrate the effect of audit quality on the fund allocation efficiency of photovoltaic enterprises. Construct model 3 to ascertain the effect of audit quality on the financing efficiency of the photovoltaic enterprises; Model 4 and Model 5 were constructed to test the mediating effect of agency cost.

Model 1:

Model 2:

Model 3:

Model 4:

Model 5:

Wherein is fund-raising efficiency;

is fund allocation efficiency;

is financing efficiency;

is audit quality,

is the intercept term,

is the regression coefficient of corresponding variables, and

is a random error term. All variables in models (1)、(2)、 (3)、 (4) and (5) are defined in detail in Appendix A.

Fund-raising efficiency (): Our paper uses data envelopment analysis (DEA) to measure the efficiency of fund-raising in photovoltaic enterprises. In our paper, debt capital cost, equity capital cost, and equity ratio are selected as the input indexes of fund-raising efficiency. In contrast, debt growth rate, owner equity growth rate, and capital availability rate are chosen as the output indexes of fund-raising efficiency.

Fund allocation efficiency (): Our paper uses data envelopment analysis to measure the Fund allocation efficiency of photovoltaic enterprises. Capital allocation involves the use of capital after raising capital. Our paper takes the output index of capital raising efficiency as the input index of Fund allocation efficiency. Therefore, the input indexes of Fund allocation efficiency in our paper are debt growth rate, equity growth rate, capital availability rate, and the output indexes of Fund allocation efficiency are total asset turnover rate, asset return rate, operating income growth rate, and earnings per share.

Financing efficiency (): Financing efficiency includes two links, capital raising and capital allocation, and its value is the arithmetic average of fund-raising efficiency value and fund allocation efficiency value.

Audit quality (): the Jones model is the most representative measure of earnings quality. The model considers that the net profit of an enterprise is composed of the accrued profit (

) under the accrual basis and the net cash flow from operating activities in the cash flow statement. The accrued profit is divided into maneuverability and non-maneuverability according to its nature, and only the non-maneuverable accrued profit reflects the true profitability of the enterprise. The following formula is used to calculate the absolute value of the manipulated profit in the audited financial statements, which represents the audit quality. Combining the relationship between the accrued profit of maneuverability and audit quality, we take the

value as an absolute value

Where represents the total accrued profit of listed company

in the year

, equal to the net profit of the listed company in the year

minus the net cash flow generated by operating activities;

represents the total assets of the listed company

in the year;

represents the incremental operating revenue of the listed company

in year

.

represents the original value of fixed assets of the listed company

in the t year.

is the residual term.

、

、

are the parameters. The manipulative accruals calculated by the above formula represent audit quality. The larger the manipulative accruals are, the more pronounced the profit manipulation of the listed company is, and the worse the audit quality is.

4. Results

4.1. Descriptive statistics

shows the results of the statistical analysis of each variable. Among them, the average value of fund-raising efficiency() is 0.37797, and the fund-raising efficiency is low. The minimum value of fund-raising efficiency is 0, the maximum value is 1, and the standard deviation is 0.354853. Therefore, it can be seen that the fund-raising efficiency of listed photovoltaic companies varies greatly, and the fund-raising efficiency of the photovoltaic enterprises needs to be further improved. The average value of

is 0.57139, which is better than the efficiency of fund-raising. The minimum value of Fund allocation efficiency is 0, and the maximum value is 1. There is a significant gap in fund allocation efficiency among photovoltaic enterprises. The average financing efficiency (

) of the photovoltaic enterprises is 0.47468, which is still at a low level. The average value of audit quality (

) of the photovoltaic enterprises is −0.07699, and the minimum value is −0.66534, indicating that the audit quality of some photovoltaic industries is low. At present, the audit quality of photovoltaic enterprises is not at a high level; that is, a high-quality audit has not fully played the role of supervision and management in photovoltaic enterprises. The average management expense ratio (

) is 0.08858, indicating high agency costs in current photovoltaic enterprises.

Table 3. Descriptive statistical results.

The average value of the capital structure () of listed companies in the photovoltaic enterprises is 0.49402, and the asset-liability ratio of general enterprises is 0.45–0.65, indicating that the capital structure of most enterprises in the photovoltaic enterprises is reasonable. However, the maximum value of the capital structure is 2.86104, and some photovoltaic enterprises have a high debt level and face significant financial risks, while the minimum value is only 0.05159, which shows a low debt level, and does not give full play to the role of financial leverage. The capital structure of the photovoltaic enterprises needs to be further improved, and a reasonable capital structure is also conducive to improving the financing efficiency of the photovoltaic enterprises. It is worth noting that the mean value of operating income growth rate (

) is 0.34914, while the standard deviation is 3.05891, indicating that the growth of listed companies in photovoltaic enterprises varies greatly.

4.2. Correlation analysis

shows the correlation analysis results of variables such as fund-raising efficiency, fund allocation efficiency, financing efficiency, and audit quality of listed photovoltaic companies. The correlation coefficient between audit quality () and fund-raising efficiency (

) is 0.1109 and is positively correlated at a 1% level, which preliminary verifies Hypothesis 1. The correlation coefficient between audit quality (

) and fund allocation efficiency (

) is −0.104 and is significantly correlated at the level of 5%, indicating that audit quality and fund allocation efficiency are significantly correlated, which preliminary verifies Hypothesis 2. In the correlation analysis results of audit quality and financing efficiency of the photovoltaic enterprises, the correlation coefficient of audit quality (

) and financing efficiency (

) is 0.0875, and there is a significant positive correlation at the level of 5%, which preliminary verifies Hypothesis 3.

Figure 1. Correlation coefficients.

4.3. Regression analysis

4.3.1. Regression analysis of audit quality and photovoltaic enterprises’ fund-raising efficiency

shows the regression results of audit quality () and fund-raising efficiency (

) of listed companies in the photovoltaic enterprises. As shown in , the adjusted

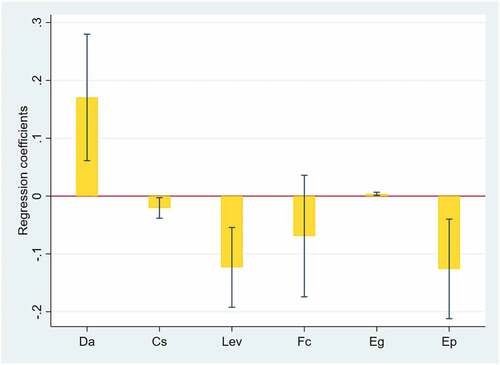

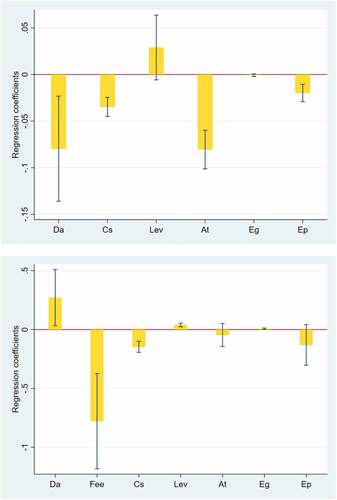

is 0.1897, that is, all variables selected in model 1 explain capital raising efficiency to 18.97%. Due to the diversity of influencing factors, our study cannot account for all of them, which may make the interpretation somewhat flawed. The goodness of fit of the regression model is acceptable, that is, the regression model of audit quality and fund-raising efficiency of the photovoltaic enterprises is acceptable. The table shows that the regression coefficient of audit quality and fund-raising efficiency of the photovoltaic enterprises is 0.17487, and there is a significant positive correlation at the level of 5%. That is, audit quality can significantly positively affect the fund-raising efficiency of the photovoltaic enterprises, which verifies Hypothesis 1. Among the control variables selected in our paper, the regression coefficient of company size and photovoltaic enterprises’ fund-raising efficiency is −0.04386 which is significantly correlated at 1%. Regression result shows that the company size, the greater the photovoltaic enterprises to raise the efficiency of funds is smaller, from the theoretical analysis of the company size, the greater the help boost investor confidence in companies, contribute to fund-raising, more significant. Still, the company needs to raise more funds, fund-raising is challenging to meet the raise of the advance amount, and fund-raising costs are large fund-raising efficiency is low.

Figure 2. Regression results of audit quality and photovoltaic enterprises’ fund-raising efficiency.

Table 4. Regression results of audit quality and photovoltaic enterprises’ fund-raising efficiency.

4.3.2. Regression analysis of audit quality and photovoltaic enterprises’ fund allocation efficiency

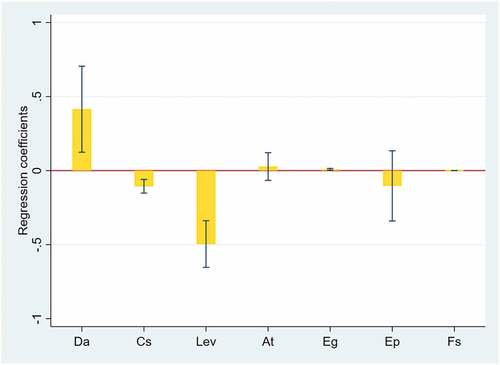

shows audit quality () and photovoltaic enterprises’ fund allocation efficiency (

). In , the adjusted

is 0.2846, that is, all variables selected in model 2 explain the capital raising efficiency to 28.46%. Our paper cannot exhaust all factors, which may make the explanation slightly weak. The goodness of fit of the regression model is acceptable; that is, the regression model of audit quality and fund allocation efficiency of the photovoltaic enterprises is good. The regression coefficient of audit quality and fund allocation efficiency of the photovoltaic enterprises is 0.45471, and it is significantly positively correlated at the level of 5%, proving Hypothesis 2. That is, audit quality can dramatically improve the efficiency of capital allocation in photovoltaic enterprises. The regression coefficient of company size and fund allocation efficiency of the photovoltaic enterprises is −0.06759, and it is significantly correlated at the level of 1%. The regression coefficient of capital structure and fund allocation efficiency of the photovoltaic enterprises is 0.030339, and it is significantly positively correlated at the level of 1%. Although the high debt level limits the capital raising behavior, it improves the fund allocation efficiency of the photovoltaic enterprises. For the photovoltaic enterprises, for some time, regardless of the actual application of the photovoltaic enterprises, a large number of photovoltaic equipment production, construction of photovoltaic power stations, resulting in photovoltaic power generation cannot match the production power and domestic power, resulting in the phenomenon of light abandonment. The phenomenon of abandoning light sharply reduces the allocation efficiency of capital. However, when the debt level of the photovoltaic enterprises is high, creditors will strictly limit the use of funds to avoid illegal use of funds and improve the allocation efficiency of funds. The regression coefficient of capital utilization capacity and fund allocation efficiency of the photovoltaic enterprises is 0.150311, which is significantly positively correlated at the level of 1%.

Figure 3. Regression results of audit quality and photovoltaic enterprises’ fund allocation efficiency.

Table 5. Regression results of audit quality and photovoltaic enterprises’ fund allocation efficiency.

4.3.3. Regression analysis of audit quality and financing efficiency of the photovoltaic enterprises

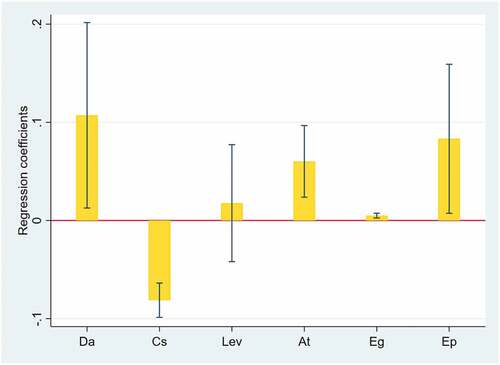

The regression result of audit quality () and financing efficiency of the photovoltaic enterprises (

) is shown in . The adjusted

is 0.5835, that is, all variables selected in model 3 explain the financing efficiency of the photovoltaic enterprises to 58.35%. Our paper cannot exhaust all the factors that affect the financing efficiency of photovoltaic enterprises, which may make the explanation somewhat flawed. But the goodness of fit of the regression model is acceptable and statistically significant. That is, the regression model of audit quality and financing efficiency of the photovoltaic enterprises is acceptable. The regression coefficient of audit quality and financing efficiency of the photovoltaic enterprises is 0.1317, and it is significantly positively correlated at a 5% level, which verifies Hypothesis 3. Improving audit quality helps improve the financing efficiency of photovoltaic enterprises. The regression coefficient of company size and financing efficiency of the photovoltaic enterprises is −0.08769, and it is significantly negatively correlated at the level of 1%. Based on the above relationship between company size, fund-raising efficiency, and fund allocation efficiency of the photovoltaic enterprises, it can be seen that company size is significantly negatively correlated with fund allocation efficiency and fund-raising efficiency of the photovoltaic enterprises. Under the joint influence of the efficiency of capital raising, and capital allocation of the photovoltaic enterprises, the company size reduces the financing efficiency of the photovoltaic enterprises. The regression coefficient of capital structure and financing efficiency of the photovoltaic enterprises is 0.003877, which is a significant positive correlation at a 1% level. That is, the more debt, the higher the financing efficiency of the photovoltaic enterprises. Because debt is more, fund-raising efficiency is lower; fund allocation efficiency is higher. The influence of total liabilities on fund-raising efficiency and fund allocation efficiency will eventually lead to the effect of financing efficiency.

Figure 4. Regression results of audit quality and financing efficiency of the photovoltaic enterprises.

4.3.4. Testing the mediating effect of agency cost

Our paper uses the mediation effect test method to examine the mediation effect of agency cost on audit quality and financing efficiency.

According to the mediation effect testing steps, the first step is to verify the relationship between audit quality and financing efficiency of the photovoltaic enterprises, as shown in . The regression results show that audit quality can significantly improve the financing efficiency of photovoltaic enterprises. The second step is to examine the relationship between audit quality and agency cost, as shown in .

Table 6. Regression results of audit quality and financing efficiency of the photovoltaic enterprises.

Table 7. Test results of the intermediary effect of agency cost.

According to the regression results in , in the regression relationship between audit quality () and agency cost (

), the adjusted

−0.0796, which is significantly correlated at the level of 1%. In other words, audit quality has a significant negative correlation with agency cost. The higher the audit quality, the less agency cost is, which also verifies the supervision role of a high-quality audit. Moreover, the regression coefficient of capital structure and agency cost is 0.028903, showing a positive relationship, that is, the enterprise with more debt can reduce agency costs.

As shown in , the third step of the agency cost intermediary effect test is to test the joint regression results of audit quality (), agency cost (

), and financing efficiency (

) of the photovoltaic enterprises. The results are shown in . Among them, the regression coefficient of audit quality and financing efficiency of the photovoltaic enterprises is 0.249191, and there is a significant positive correlation at a 5% level. The regression coefficient of agency cost and financing efficiency is −0.34356, which is significantly correlated at 5%. Therefore, in the test of the intermediary effect, the intermediary product of agency cost is significant, which plays a partial intermediary role and verifies Hypothesis 4.

Figure 5. Test results of the intermediary effect of agency cost.

4.4. Robustness test

To prove the credibility of the above empirical results, the robustness test is carried out by using the substitution variable method. The audit quality is represented by the audit fee borne by photovoltaic enterprises. The higher the audit fee is, the more time, cost, and energy the independent auditors pay, thus, the quality of audit results is more elevated.

respectively show the regression analysis of audit quality on photovoltaic enterprises’ fund-raising efficiency, photovoltaic enterprises’ fund allocation efficiency, and photovoltaic enterprises financing efficiency. The results are consistent with the above empirical results, thus proving the stability of the above results. shows the robustness test of the analysis on the influence mechanism of audit quality on the financing efficiency of the photovoltaic enterprises. The regression analysis of audit quality on agency cost shows no significant results. Our paper further uses Bootstrap to verify the results of the intermediary effect. Bootstrap test evidence in our paper also proves that agency cost plays a partial intermediary role in the impact of audit quality on the financing efficiency of photovoltaic enterprises. The robustness test verified the reliability and credibility of the above results.

Table 8. Robust regression results of audit quality and photovoltaic enterprises’ fund-raising efficiency.

Table 9. Robust regression results of audit quality and photovoltaic enterprises’ fund allocation efficiency.

Table 10. Robust regression results of audit quality and financing efficiency of the photovoltaic enterprises.

Table 11. Robustness test results of the intermediary effect of agency cost (a).

5. Discussion

Based on the financing status of Listed Companies in the photovoltaic industry, this paper studies the relationship between audit quality and financing efficiency. Through research, we find that audit quality can significantly improve the efficiency of fundraising and fund allocation, and on this basis, it is positively related to financing efficiency. Further research shows that audit quality can affect financing efficiency through agency cost.

From the external point of view, the research on the influence factors of the audit quality included in the financing efficiency is conducive to playing the role of an independent audit as an external governance mechanism. A high-quality audit not only has the function of signal transmission, but also plays an important role in supervising and managing listed companies. The research of this paper also helps enterprises to pay attention to the role of high-quality audits in reducing the information asymmetry between enterprises and information users.

This paper has some limitations in studying the relationship between audit quality and financing efficiency of photovoltaic enterprises. On the one hand, our paper chooses the Jones model to calculate audit quality. Compared with other models, this model removes the effect of accounts receivable when calculating non-manipulative profit, which may lead to different results. On the other hand, when using data envelopment analysis to measure the financing efficiency, the selected indicators are limited, which cannot ensure the stability of the efficiency calculation results.

6. Conclusions and policy implications

Starting from the definition of financing efficiency of the photovoltaic enterprises, our paper divides financing behavior into two stages: fund-raising and fund allocation. Data envelopment analysis is used to measure the efficiency of capital raising, capital allocation, and financing in photovoltaic enterprises. Taking 54 listed companies in China’s A-share photovoltaic enterprises from 2011 to 2020 as the research object, our paper studies the impact of audit quality on the fund-raising efficiency, fund allocation efficiency, and financing efficiency of the photovoltaic enterprises. Further study of the influence mechanism of audit quality on the financing efficiency of the photovoltaic enterprises.

The research conclusions are as follows: 1% improvement in audit quality will improve the efficiency of fundraising by 18.49%, the efficiency of fund allocation by 45.47%, and the efficiency of financing by 13.17%. In addition, agency cost plays an intermediary role between audit quality and financing efficiency of photovoltaic enterprises. In other words, improving the audit quality by 1% can reduce the agency cost of photovoltaic enterprises by 34.36%, thus improving the financing efficiency of photovoltaic enterprises by 24.92%.

Therefore, photovoltaic enterprises should not only pay attention to the cost of capital raising, but also pay attention to the standard of capital used to improve the financing efficiency. To improve the financing efficiency of photovoltaic enterprises, in addition to improving the internal situation of enterprises, we should pay attention to the role of the independent audit. Improving audit quality also helps improve financing efficiency.

For the scope of future research, firstly, in the empirical research, there may be data errors in the robustness test using the discretionary accruals to represent the audit quality and using the surrogate variable method to represent the audit quality. Future research should further improve the measurement method of audit quality and improve the accuracy of measurement. Second, financing behavior involves many factors. Future research should continue to explore factors affecting financing efficiency. Finally, when examining the mechanism of audit quality on financing efficiency, it only verifies the role of agency cost in the relationship between audit quality and financing efficiency, and other factors need to be further enriched.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Aiqadasi, A., and S. Abidin. 2018. The effectiveness of internal corporate governance and audit quality: The role of ownership concentration - Malaysian evidence. Corporate Governance International Journal of Business in Society 18 (2):233–21. doi:10.1108/CG-02-2017-0043.

- An, G., and H. Wang. 2018. Evaluation of fiscal policy effect of china’s photovoltaic industry. Light & Engineering Retrieved from ://WOS:000454568400013. 26 (4):111–16. doi:10.33383/2018-123.

- Aobdia, D., C. J. Lin, and R. Petacchi. 2015. Capital market consequences of audit partner quality. Accounting Review 90 (6):2143–76. doi:10.2308/accr-51054.

- Barkatullah, N., and A. Ahmad. 2017. Current status and emerging trends in financing nuclear power projects. Energy Strategy Reviews 18:127–40. doi:10.1016/j.esr.2017.09.015.

- Beisland, L. A., R. Mersland, and R. Str?m. 2015. Audit quality and corporate governance: evidence from the microfinance industry. International Journal of Auditing 19 (3):218–37. doi:10.1111/ijau.12041.

- Blackwell, D. W., Noland, D. B. N T R, and T. R. Noland. 1998. The value of auditor assurance: Evidence from loan pricing. Journal of Accounting Research 36 (1):57–70. https://doi.org/10.2307/2491320.

- Bostan, I., M. B. Tudose, R. I. Clipa, I. C. Chersan, and F. Clipa. 2021. Supreme audit institutions and sustainability of public finance. Links and evidence along the economic cycles. Sustainability 13 (17). doi: 10.3390/su13179757.

- Boubaker, S., A. Houcine, Z. Ftiti, and H. Masri. 2018. Does audit quality affect firms’ investment efficiency? The Journal of the Operational Research Society 69 (10):1688–99. doi:10.1080/01605682.2018.1489357.

- Cai, H., L. Liang, J. Tang, Q. Wang, L. Wei, and J. Xie. 2019. An empirical study on the efficiency and influencing factors of the photovoltaic industry in China and an analysis of its influencing factors. Sustainability 11 (23):6693. doi:10.3390/su11236693.

- Chen, H., J. Z. Chen, G. J. Lobo, and Y. Wang. 2011. Effects of audit quality on earnings management and cost of equity capital: Evidence from China*. Contemporary Accounting Research 28 (3):28. doi:10.1111/j.1911-3846.2011.01088.x.

- Cheng, C., K. Wang, Y. Xu, and N. Zhang. 2020. The impact of revealing auditor partner quality: Evidence from a long panel. Review of Accounting Studies 6 (4):1475–506. doi:10.1007/s11142-020-09537-w.

- Chen, Y., W. Saffar, and B. Srinidhi. 2017. Does audit quality affect firms’ debt financing choices?. Social Science Electronic Publishing. doi:10.2139/ssrn.3047517.

- Chod, J., N. Trichakis, G. Tsoukalas, H. Aspegren, and M. Weber. 2017. On the financing benefits of supply chain transparency and blockchain adoption. Social Science Electronic Publishing. doi:10.1287/mnsc.2019.3434.

- Coffie, W., I. Bedi, and M. Amidu. 2018. The effects of audit quality on the costs of capital of firms in Ghana. Journal of Financial Reporting and Accounting (4):639–59. doi:10.1108/JFRA-03-2017-0018.

- Cole-Baker, J. R., and G. J. Bowyer. 1998. The role of the independent technical audit in raising finance. Journal- South African Institute of Mining and Metallurgy 98 (7):317–26.

- Doukas, J. A., C. Kim, and C. Pantzalis. 2008. Do analysts influence corporate financing and investment? Financial Management 37 (2):303–39. doi:10.1111/j.1755-053X.2008.00014.x.

- Eichhammer, W., M. Ragwitz, and B. Schlomann. 2013. Introduction to the special issue: Financing instruments to promote energy efficiency and renewables in times of tight public budgets. Energy & Environment 24 (1–2):1–26. doi:10.1260/0958-305X.24.1-2.1.

- Fang, X., and Y. Wu. 2015. Research on financing efficiency of small and medium-sized enterprises in the new third board market. Economic Management 37 (10):42–51. doi:10.19616/j.cnki.bmj.2015.10.007.

- Favalli, R. T., A. Gori Maia, and J. M. F. J. da Silveira. 2020. Governance and financial efficiency of Brazilian credit unions. RAUSP Management Journal 55 (3):355–73. doi:10.1108/rausp-02-2019-0018.

- Feldman, D., R. Jones-Albertus, and R. Margolis. 2020. Quantifying the impact of R&D on PV project financing costs. Energy Policy 142:111525. doi:10.1016/j.enpol.2020.111525.

- Haeridistia, N., and Agustin, F. 2019. The effect of independence, professional ethics & auditor experience on audit quality. International Journal of Scientific & Technology Research 8 (2):24–27.

- Hakim, F., and M. A. Omri. 2010. Quality of the external auditor, information asymmetry, and bid-ask spread: Case of the listed Tunisian firms. International Journal of Accounting & Information Management 18 (1):5–18. doi:10.1108/18347641011023243.

- Hou, F., F. Liao, J. Liu, and H. Xiong. 2019. Signing auditors’ foreign experience and debt financing costs: Evidence for sustainability of Chinese listed companies. Sustainability 11 (23):11. doi:10.3390/su11236615.

- Huang, P., Y. C. Wen, Y. Zhang, R. Financeaccounting, and C. F. Lee. 2019. Does the monitoring effect of Big 4 audit firms really prevail? Evidence from managerial expropriation of cash assets. 55 (2):739–68. doi:10.1007/s11156-019-00858-9.

- Jiang, C., D. Liu, Q. Zhu, and L. Wang. 2021.Government subsidies and enterprise innovation: Evidence from China’s photovoltaic industry. Discrete Dynamics in Nature and Society 2021: 1–9.doi: 10.1155/2021/5548809

- Johl, S., M. B. Muttakin, D. G. Mihret, S. Cheung, and N. Gioffre. 2021. Audit firm transparency disclosures and audit quality. International Journal of Auditing 25 (2):508–33. doi:10.1111/ijau.12230.

- Jung, S. J., B. J. Kim, and J. R. Chung. 2016. The association between abnormal audit fees and audit quality after IFRS adoption. International Journal of Accounting and Information Management 24 (3):252–71. doi:10.1108/IJAIM-07-2015-0044.

- Kabir, E., P. Kumar, S. Kumar, A. A. Adelodun, and K. H. Kim. 2018. Solar energy: Potential and future prospects. Renewable & Sustainable Energy Reviews 82:894–900. doi:10.1016/j.rser.2017.09.094.

- Kim, P. N., D. H. Nguyen, P. T. Quang, and H. Thuy. 2017. Audit firm size, audit fee, audit reputation and audit quality: The case of listed companies in vietnam. Asian Journal of Finance & Accounting 9 (1):429. doi:10.5296/ajfa.v9i1.10074.

- Kontokosta, C. E., D. Spiegel-Feld, and S. Papadopoulos. 2020. The impact of mandatory energy audits on building energy use. Nature Energy 5 (4):1–8. doi:10.1038/s41560-020-0589-6.

- Kouaib, A., and A. Jarboui. 2014. External audit quality and ownership structure: Interaction and impact on earnings management of industrial and commercial Tunisian sectors. Journal of Economics Finance & Administrative Science 19 (37):78–89. doi:10.1016/j.jefas.2014.10.001.

- Lin, B., and R. Luan. 2020. Do government subsidies promote efficiency in technological innovation of China’s photovoltaic enterprises? Journal of Cleaner Production 254. doi:10.1016/j.jclepro.2020.120108.

- Lin, C., X. Wan, and Y. Chen. 2019. Impact of external audit quality on earnings management in marine enterprises. Journal of Coastal Research 98 (sp1):100. doi:10.2112/SI98-025.1.

- Li, H., and L. Wu. 2016. Analysis of financial support efficiency for China’s wind power industry. Energy Sources Part B Economics Planning & Policy 11 (7–12):1035–41. doi:10.1080/15567249.2016.1185480.

- Luo, G. L., C. F. Long, X. Wei, and W. J. Tang. 2016. Financing risks involved in distributed PV power generation in China and analysis of countermeasures. Renewable and Sustainable Energy Reviews 63:93–101. doi:10.1016/j.rser.2016.05.026.

- Luo, J., Y. Peng, and Y. Chen. 2020. Annual report length and the company’s equity financing cost. Manage Reviews 32 (1):11. CNKI:SUN:ZWGD.0.2020-01-136.

- Lyu, X., and A. Shi. 2018. Research on the Renewable Energy Industry Financing Efficiency Assessment and Mode Selection. Sustainability 10:222. doi:10.3390/su10010222.

- Martinez, A. L., and A. D. J. Moraes. 2017. Relationship between auditors’ fees and earnings management. Revista de Administração de Empresas 2 (2):148–57. doi:10.1590/S0034-759020170204.

- Ma, L., F. Xu, and Y. Yu. 2017. Evaluation of financing efficiency of listed companies in photovoltaic industry based on DEA model. Light and Engineering 25 (3):71–78.

- Olivia Furiady, R. K., and R. Kurnia. 2015. The effect of work experiences, competency, motivation, accountability and objectivity towards audit quality. Procedia - Social and Behavioral Sciences 211:328–35. doi:10.1016/j.sbspro.2015.11.042.

- Palazuelos, E., N. H. Crespo, and J. Corte. 2017. Accounting information quality and trust as determinants of credit granting to SMEs: The role of external audit. Small Business Economics 51 (2):1–17 doi:10.1007/s11187-017-9966-3.

- Qi, L., and Y. Zhang. 2017. Effects of solar photovoltaic technology on the environment in China. Environmental Science and Pollution Research 24 (28):22133–42. doi:10.1007/s11356-017-9987-0.

- Salehi, M., M. R. Fakhri Mahmoudi, and A. Daemi Gah. 2019. A meta-analysis approach for determinants of effective factors on audit quality : Evidence from emerging market. Journal of Accounting in Emerging Economies 9 (2):287–312. doi:10.1108/JAEE-03-2018-0025.

- Sattar, U., S. A. Javeed, and R. Latief. 2020. How audit quality affects the firm performance with the moderating role of the product market competition: Empirical evidence from Pakistani manufacturing firms. Sustainability 12 (10):12. doi:10.3390/su12104153.

- Shubita, M. 2021. The impact of audit quality on Tobin’s Q: Evidence from Jordan*. Journal of Asian Finance Economics and Business 8 (7):517–23. doi:10.13106/jafeb.2021.vol8.no7.0517.

- Stnic, F. A. 2016. The cost of capital under information asymmetry’s constraint. Theoretical and Applied Economics xxiii:96–103. http://store.ectap.ro/suplimente/International_Finance_and_Banking_Conference_FIBA_2016_XIV.pdf

- Swarnalakshmi, U., and R. Seth. 2015. Financing large scale wind and solar projects—a review of emerging experiences in the Indian context. Renewable & Sustainable Energy Reviews.

- Tan, Z., Q. Tan, and M. Rong. 2018. Analysis on the financing status of PV industry in China and the ways of improvement. Renewable and Sustainable Energy Reviews 93:409–20. (OCT.). doi:10.1016/j.rser.2018.05.036.

- Taqi, M. 2013. Consequences of audit quality in signaling theory perspective. GSTF Journal on Business Review (GBR) 2 (4):133–36. doi:10.5176/2010-4804_2.4.262.

- Wang, C., and Z. Wang. 2016. Analysis on financing efficiency of enterprises listed on “new third board”. Shanghai finance 11:70–75. doi:10.13910/j.cnki.shjr.2016.11.010.

- Wardhani, R., and D. H. Zhou. 2019. The role of audit quality on market consequences of voluntary disclosure: Evidence from East Asia. Asian Review of Accounting 27 (3):373–400. doi:10.1108/ARA-03-2018-0083.

- Wen, Z. L., L. Chang, K. T. Hau, and H. Y. Liu. 2004. Testing and application of the mediating effects. Acta Psychologica Sinica 36 (5):614–20.

- Wu, Z., M. L. Njoke, G. Tian, and J. Feng. 2021. Challenges of investment and financing for developing photovoltaic power generation in Cameroon, and the countermeasures. Journal of Cleaner Production 7:126910. doi:10.1016/j.jclepro.2021.126910.

- Xu, L., Q. Zhang, K. Wang, and X. Shi. 2020.Subsidies, loans, and companies’ performance: Evidence from China’s photovoltaic industry. Applied Energy 260: 260.doi: 10.1016/j.apenergy.2019.114280

- Xu, L., S. Zhang, M. Yang, W. Li, and J. Xu. 2018. Environmental effects of China’s solar photovoltaic industry during 2011-2016: A life cycle assessment approach. Journal of Cleaner Production 170:310–29. doi:10.1016/j.jclepro.2017.09.129.

- Yang, B., C. Lin, and W. Chen. 2017. Governance mechanism of the excess capacity of the photovoltaic enterprises from the perspective of technological innovation. Light & Engineering 25 (3):44–50. Retrieved from ://WOS:000411849700006.

- Zahmatkesh, S., and J. Rezazadeh. 2017. The effect of auditor features on audit quality. Tékhne 15 (2):S1645991117300105. doi:10.1016/j.tekhne.2017.09.003.

- Zhang, S., M. Yang, W. Li, and J. Xu. 2018. Environmental effects of China’s solar photovoltaic industry during 2011–2016: A life cycle assessment approach. Journal of Cleaner Production 170:310–329. doi:10.1016/j.jclepro.2017.09.129.

- Zhao, X.-G., and Z. Wang. 2019. Technology, cost, economic performance of distributed photovoltaic industry in China. Renewable & Sustainable Energy Reviews 110:53–64. doi:10.1016/j.rser.2019.04.061.

- Zijl, M. N. H. K. A. T. V., K. Ahmed, and T. van Zijl. 2017. Audit quality, earnings management, and cost of equity capital: Evidence from India. International Journal of Auditing 21 (2):177–89. doi:10.1111/ijau.12087.