ABSTRACT

In response to economic hurdles, several countries turn to devaluing their national currencies as a way to cope with economic difficulties. Such acts have a variety of effects on many industries, including real estate, which has led to multiple institutional and regulatory reformations aiming at minimising these effects. This paper uses a system thinking methodology that emphasises underpinning relationships among all entangled components to examine how such reforms affect minimising risks associated with currency devaluation on the real estate market.

This paper uses this methodology beyond linear cause-effect analyses to consider interactions and interconnectedness in order to give some insights to gain:

The impact of the currency devaluation on the real estate market based on Egyptian recent situation.

The unintended consequences of government reforms on real estate market variables

Solution leverage points where to intervene in the system.

Holistic understanding which enables decision makers to see a wider picture and factors.

Egypt has faced severe fluctuations in the economic climate, which has entailed a sharp devaluation of the currency three times between 2016 and 2023 (which could be considered a special aggressive case study between countries due to repetitiveness and effects).

The effects of this devaluation have extended to all sectors, and the most important of these effects was severe challenges that faced the real estate market performance. The Real Estate market (REM) recently in Egypt has faced huge recession of transactions of the market.

This research focuses on understanding the relations of reforms of the regulations which is designed to give a comprehensive overview of the government reforms of RE business, and how it has been interacting with the ramifications of those currency devaluation impacts.

Introduction

With rapid scanning on currency devaluation cases happened in different countries in different situation, the paper addresses general overview for the impact of those cases on real estate business. When it comes to currency devaluation, the real estate market may face different repercussions. Investigating the rise in housing supply prices as a result of rising import costs for building supplies and machinery as one example is worth pursuing.

Another instance is how a decline in the value of the currency would encourage more overseas investors to regard the acquisition of a foreign property as a bargain [Citation1], which would raise prices because of increased demand. Additionally, because interest rates ostensibly limit mortgage rates, they are not immune to the effects of devaluation of currencies [Citation2]. Aspiring buyers find it difficult to get mortgages due to the higher interest rates associated with these situations, which could lower activity rates overall [Citation3].

Additionally, when working with assets, inflation resistance tends to decline [Citation4]. Property value is included under this general phrase since it can be both somewhat susceptible to market fluctuations in demand for housing and judged less valuable during periods of depressed economic growth, which increases market speculation, affecting the risk of entry for investors. Generally, currency devaluation leads to economic uncertainty, and it can have a significant cascading repercussion in the real estate market in several ways, including four main aspects:

increasing property prices; when imports such as building materials or equipment get more expensive because of lower exchange rates, they drive up construction costs which inevitably causes property prices rise even further (IMF [Citation5]).

since purchasing power from other currencies increases for foreign investors while investing locally becomes cheaper, this leads them toward snapping up properties quickly causing a sudden surge in demand, a phenomenon that drives prices up further [Citation6].

a devaluation in currency can lead to an increase in interest rates, which can affect mortgage when interest rates go up alongside depreciated exchange rates [Citation7]. Which leads to buying property through mortgages being too expensive for most customers, causing a significant downward slope on the real estate industry movement.

inflation can diminish asset values by slowly eroding their worth over extended periods, leading buyers away from investing in depreciating assets altogether [Citation8].

Problem background

The impacts of devaluation cover an array of variables, while it is a fundamental method used by governments that would stabilize the economy through currency control, increasing cash flow from direct foreign investments and improving local consumption rates as export prices increase. However, without the proper government reforms, market entry risk is increased due to inadequate risk management agencies and a lack of solid hedge funding infrastructure. This is also exacerbated through increased investment speculation and regulatory disproportionate investment and development laws [Citation9].

Currency devaluation and the reforms implemented by governments can greatly impact the real estate market. Here are some important factors to take into account;

Devaluing a currency automatically raises the burden of taxes, inflation and interest rates on developers, investors and customers alike. When import prices increase due to devaluation, it affects construction materials and machinery, causing a decrease in supply. However, the decrease of demand from local demographics due to tightening expenditures as inflation increases equalizes the decrease of supply. Meanwhile, as affordability increases for foreigners, their increased demand nudges the market in a more favorable direction. The increased demand for loans can be utilized for better stability and profit if investment speculation is controlled [Citation7].

Safeguard against currency devaluation: Real estate can act as a safeguard against currency devaluation. When a currency experiences devaluation tangible assets like estate tend to perform often surpassing other markets during and after economic downturns. This is because real estate holds its value and offers stability and potential for investors when faced with economic conditions [Citation10].

The devaluation of currency like the US dollar can have an impact, on real estate prices and demand. When the dollar weakens it becomes more appealing for foreign investors to buy real estate as their buying power increases. This can potentially lead to prices in locations and popular markets. However, the impact of currency devaluation on estate can differ depending on the investors’ home country [Citation11].

Foreign investment: When a country’s currency loses value it can make real estate more affordable, for investors. This often leads to an increase in investment in the real estate market, which can drive up prices and create a boom in areas [Citation12].

Considerations for the market: It’s important to understand that the impact of currency devaluation on estate can vary between local and international investors. For investors specifically currency devaluation can be seen as a tax on real estate investments potentially resulting in negative effects on investment decisions [Citation12].

Investment strategy: To navigate the challenges posed by currency devaluation real estate investors should focus on securing passive income streams through renting or wholesaling properties. While currency devaluation may not have an impact on real estate prices, it can still have consequences, for investments. Therefore, it is crucial for investors to adapt their strategies accordingly [Citation12].

Depending on the severity of the issue and the unique circumstances of the market, governments may react to the effects of the currency devaluation on the real estate market in a variety of ways. The following are possible government responses: IMF [Citation5].

Monetary policy refers to various measures that central banks can take to stabilize the economy and currency. These measures may include adjusting interest rates as implementing quantitative easing. The real estate market can be indirectly impacted by monetary policy because changes in mortgage rates and housing demand can occur.

Fiscal policy. On the other hand is the use of government spending and tax incentives to stimulate economic activity. By increasing spending on infrastructure projects or encouraging homebuying through tax incentives governments can directly affect the real estate market by increasing demand for housing. To prevent foreign investment from driving up property prices and making housing less affordable for local residents and limiting purely yield movements. In the market governments frequently introduce regulations that limit investment in the real estate sector. These measures may involve imposing taxes on buyers or placing restrictions on the types of properties that non-citizens can buy.

Housing policies put forth by governments aim to tackle affordability issues in different ways such as providing subsidies for low-income households or increasing the supply of affordable housing.

Currency controls are a more extreme measure employed when necessary to limit capital flight by imposing restrictions on foreign capital inflow that could cause a significant impact on demand for housing in the real estate market.

Generally, several factors, including different externally influential ones like economy types and investment qualities, play a significant role in determining how deep-rooted the currency devaluation’s impact will be on real estate markets if it is implemented. These factors require a careful consideration when unraveling their full effects. In order to lessen these effects on many sectors, including the real estate market, governments frequently adopt several regulatory, legislative, institutional, and financial reforms.

In summary when there are repeated instances of currency devaluation and the subsequent reforms implemented by the government it can have an impact on the real estate market. This impact can influence aspects such as investment choices, prices and overall demand. Real estate can be an asset during times of currency devaluation; however, investors must diligently assess the consequences and adjust their strategies accordingly to effectively navigate through these challenges.

Research objectives

This paper discusses the risks of currency devaluation on the real estate market and how the governments can deal with those impacts throughout by investigating the four main objectives:

To address the impact of the currency devaluation on the real estate market based on the recent Egyptian recent situation.

To address the unintended consequences of government reforms on the real estate market variables.

To address the solution leverage points as to where to intervene in the system.

To give an insight on a holistic understanding which enables decision makers to see a wider picture and factors.

Essentially, the effect of those reforms is not instantaneous, and not yet float on surface of the real estate market. So, it is necessary to follow an approach that analyzes the complexity of relations and how they work to understand and analyze the dynamics of those relations. Also, it could be considered as beyond a linear cause-effect, not a causal loop system, which takes into account the complexities and interconnections in various systems. It represents an approach to comprehending the how and why of occurrences.

Systems thinking proves to be the approach in exploring and grasping these intricacies to understand the complexity of those relations, and as the fresh perspective that it would bring to our understanding, which could be promising solutions for international and future issues.

Local context

Why Egypt?

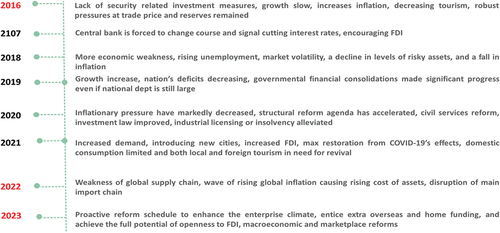

Egypt has had a tumultuous path in the last decade economically and fiscally, with consequences affecting every aspect of the country. Egypt has experienced three instances of currency devaluation in seven years (). Recent economic reports suggest that Egypt may soon face its fourth and potentially most severe wave of currency devaluation in addition to severe lack of foreign currency which affects all business sectors including the real estate market.

Figure 1. The exchange rate of Egyptian pounds against 1 USD against EGP June 2014 -June 2023.

Prior to 2016, Egypt had been enjoying a more stable economic outcome. However, reoccurring devaluations have increased the risk of real estate investment in Egypt. The three major devaluations in November 20 March 2016 22 and March 2023 have repercussions such as inflation, unclear brokerage activity laws, procedural delays/complications, fluctuating fees/taxes and mortgages that are not encompassing all the market’s demographics [Citation13] and incomplete framework of legislative procedures [Citation5].

Issues such as regulatory disproportionality, inadequate amount of risk management agencies and hedge funds in Egypt, and lack of security-related investment measures have all been exasperated by the ongoing economic instability. The devaluations have been used to revive the economy, increase the marketability for foreign investors and contain capital flight, as well as avoiding the domestic debt crisis while pursuing a shift from exports to consumption in the economy [Citation14].

It is concluded that central banks will likely be forced to change course and signal cutting interest rates, which should result in a sustained recovery of asset prices and subsequently the economy by the end of 2023 [Citation15]. More economic weakness, rising unemployment, market volatility, a decline in levels of risky assets, and a fall in the rapid inflation will occur. Due to these challenges, this paper will cover the 2016 and later devaluations to this point as they have shaped the real estate market.

Hence, Egypt could be considered as a rich case study to discuss recent currency devaluation issues for better understanding its consequences and the way for needed reforms to mitigate them.

Real estate market’s situation in Egypt from 2016 till 2023

The devaluation of the Egyptian pound on three occasions is the major factor that the country has needed to adapt to in the last five years, but inflation has also taken its toll on the economy as well. Initially, the first devaluation was done due to the commodity prices slump and the crude price slide that was ongoing in 2015/2016 [Citation16]; other major devaluations were done in 2022 and 2023 to unlock the IMF assistance [Citation17] and absorb the shock caused by the COVID-19 pandemic in the global ()

Figure 2. The timeline of Egyptian currency devaluation impacts and its effects on real estate market.

The devaluation of currency in Egypt can be attributed to interconnect many factors which can be summarized through main four aspects as follows:

Economic Imbalances: Egypt’s foreign exchange reserves have been strained by deficits and trade imbalances. The governments high spending and low revenue generation have resulted in budget gaps leading to increased reliance on borrowing and aid.

Inflationary Pressures: Inflation has risen in Egypt diminishing the purchasing power of the currency. This inflation can be attributed to factors such as population growth, reductions in subsidies and disruptions in the supply chain.

Political and Social unrest: Instances of instability and social unrest have discouraged investments and tourism which has had a significant impact on the inflow of foreign exchange.

External Shocks: Global economic factors such as fluctuations in oil prices and changes in interest rates can influence the value of a currency. Egypt’s dependence on oil imports and vulnerability to shocks have further strained its currency. The consequences of the coronavirus pandemic have also cast a shadow on the economic and social climate globally and on Egypt in particular.

Egypt’s real estate market had an influence of instability of economic situation by November 2016 but has a speedy recovery in the following years due to huge demand and the governmental influences during this period.

Egypt’s real estate market experienced strong demand in 2020, which led the nation to start introducing new cities with potential for significant real estate projects, including the New Administrative Capital, New Alamein City and New Mansoura City. Egypt offers enticing investment opportunities due to the continuing development and formation of 20 new cities, as well as the upgrading/developing of the 23 already existing new cities [Citation18]. Egypt received a huge amount of FDI in 2017 compared to all African countries and the Arab world, according to the UN’s World Investment Report. Egypt had positive growth story effectively became one of pent-up calls that were released through increased macroeconomic and political equilibrium between 2017 and pandemic [Citation19].

Egypt’s real estate market had been gradually recovering from challenging dynamics sparked by the EGP devaluation in November 2016. The devaluation increased construction costs significantly on the supply side, straining companies’ bank sheets. Demand was stifled by the quick devaluation of the local currency, which increased prices by more than 50% and turned away both potential purchasers looking for homes that were ready to move into and homeowners trying to sell their properties. The Central Bank of Egypt’s (CBE) severe monetary tightening measures, put in place to combat rising inflation, also attracted capital out of real estate and into bank-backed savings products with rates of 15% to 20%, modestly lowering demand for starter homes in 2017 [Citation20]. Throughout 2018, there was a gradual easing of price pressures, favoring developers. The Central Bank of Egypt (CBE) reduced interest rates by a combined 650 basis points (bps) in 2018 and 2019, encouraging investors to put their money back into real estate [Citation21].

Because of the pandemic, the government implemented partial lockdown measures and curfew hours between March and July, which had a substantial negative impact on the economy. Financial instability brought in a dramatic decline in purchasing activity across practically all industries, including real estate, as a result of widespread job losses, pay freezes, commodities shortages and the propensity for cash hoarding.

The market’s supply side was also severely impacted on a number of fronts. Construction input imports were held down, which delayed construction and delivery timelines due to global supply chain disruptions and decreased trade volume. Construction sites were temporarily shut down by the government to stop the spread of the virus, which caused delays in project timelines and increased overhead expenses for developers remaining on payroll [Citation22].

The Central Bank of Egypt’s mortgage finance effort, which undoubtedly changed the market in favor of lending to these clients, has continued to draw Class-C consumers into the mortgage market throughout 2020 [Citation22]. However, even though it is anticipated that home financing debt will increase in the future, the pandemic has negatively affected clients’ capacity to make payments, which has undoubtedly weighed on default rates. In order to offset these risks to asset quality, the Financial Regulatory Authority prolonged payment schedules by six months till September and instructed non-banking finance companies to reschedule loan payment; the risk in our portfolio is unquestionably higher, but it is believed it may come from class-A mortgages rather than low-income ones [Citation22]. The lower value of residential units and the assistance provided by the government to obtain these loans protect class-C mortgage contracts. Since the home they are purchasing is their only asset, they cannot afford to fail on their payments, so they have a fundamental need to keep the house they were given through the program. Conversely, homeowners with higher incomes may afford to have their assets seized in the event of a default [Citation22].

However, there is an aspect to this situation. We can see it in the performance of the real estate market, where local people are protecting their money by investing in property. This trend has caught the attention of developers who are competing through incentives flexible payment plans and extensive promotional campaigns. Additionally, the introduction of scale real estate projects suggests that the devaluation has attracted foreign interest in Egyptian ventures. Unfortunately, it seems that this momentum is slowing down due to tightening conditions and the recent interest rate hikes by the Central Bank of Egypt.

The impact of currency devaluation on real estate market variables

The real estate market showed resilience while other industries faced difficulties following the revolutions, in 2011 and 2013. One reason for the stability of the property market is that many Egyptians choose to convert their cash into assets like properties. The recent decrease in the value of the pound against the dollar has motivated Egyptians to exchange their currency and invest in housing units as they have confidence that real estate prices will not decline compared to other sectors but instead continue to rise. Both businesses and everyday Egyptians experience the effects of a currency and inflation in Egypt.

Real estate and infrastructure players in Egypt are facing challenges due to the increase in prices of materials and building supplies well as higher borrowing costs. The recent currency devaluation by the Central Bank of Egypt in March 2021 has further added to these cost increases. Notably steel prices serve as a benchmark because they have an impact on sectors. Additionally, contractors are finding it difficult to predict the direction of raw material prices, making it challenging for them to establish pricing strategies during this phase. The depreciation of the currency has resulted in a slowdown in sales and growth within the real estate market. As a result, average consumers have purchasing power and are becoming more selective in their buying decisions. Interestingly, despite this trend, there has been an increase in real estate sales. To mitigate risk additional measures are being taken to maintain cap rates [Citation23].

The problem of entry risk is further compounded by the absence of regulations. The lack of harmonized legislation does not affect institutions and their products but also impacts collateral and other guarantees associated with these products often tied to real estate assets. Consequently, any discrepancy between the assessed property value and its actual market value increases risks associated with real estate investments since prospective buyers may acquire titles, with values [Citation22].

We could address the relations of impact of currency devaluation variables to the real estate market (REM) which has affected:

Direct variables to Real Estate Market (REM) by:

Increasing Market entry risk due to inadequate amount of risk management agencies and hedge funds

Increasing appreciation/pricing while increasing import prices which raise construction cost.

Increasing the demand while increasing affordability in foreign investment.

Increasing cash flow based on increase of movement of outward cash flow while increasing inward cash flow from foreigners.

Increasing leverage/loan based on the increased need for loans due to decreased affordability.

Decreasing supply that is affected by decreasing construction machinery and materials.

Decreasing economic stability increases investment speculation and regulatory disproportionality.

Decreasing demographics affordability while increasing income polarity and household debt, tightening spending.

Indirect variables to the real estate market (REM) by:

Increasing interest rates

Increasing inflation

Increasing taxes

Lately there has been an observation by developers in Egypt that various factors, such as the status of projects, can significantly impact the outcome. The impact on firms tends to vary.

Developers who are facing instability need to sell properties in order to collect funds and then allocate them to contractors.

On the other hand developers with finances have the flexibility to both sell properties and award contracts simultaneously up to a certain extent.

However, it is crucial for developers to consider the average costs over years in order to assess how their profit margins might be affected. Taking a long-term perspective it is believed that cost increases will be absorbed so that overall profit margins won’t experience changes over an extended period of time. However, any potential limitations on price hikes could restrict how much developers can increase their prices within a year.

Government response 2016–2023

Governmental reforms for real estate market in 2016–2023

Throughout the devaluation period of Egyptian pound from 2016 till 2023, there were many other challenges affecting the real estate market in general, which the government has worked on to avoid their negative impacts, and as a way forward to enhance the performance of the real estate market Egypt’s government reforms have created proportionality, whether it is overseeing the inward cash flow from direct foreign investments or national debt levels as market entry risk increases due to lack of security-related investment measures [Citation24].

As seen above, currency controls are used to limit capital flight, impacting demand while controlling inflation. The Central Bank of Egypt’s (CBE) severe monetary tightening measures, put in place to combat rising inflation, also attracted capital out of Real Estate and into bank-backed savings products with better interest rates against home financing debt increases in the future. The pandemic has negatively affected clients capacity to make payments, which has undoubtedly weighed on default rates. In order to offset these risks to asset quality, the Financial Regulatory Authority prolongs payment schedules and instructed non-banking finance companies to reschedule loan payment, as the risk in Egypt’s portfolio is unquestionably higher, encouraging hedge buying home to help against inflation. Successful macroeconomic stabilization and marketplace reforms have triggered a surge in overseas traders, while limiting development is maintained to avoid oversupply. The Egyptian government has extended deadlines of existing projects by 20% and is now considering projects as complete once they have reached 85% of construction to balance the supply rates in the market.

Furthermore, Egypt has had many other governmental reforms that help a thriving real estate atmosphere with minimal risk during the second currency devaluation, which could be considered as fragmented reforms to tackle specific impacts of currency devaluation as follows:

From 2015 to 2020, the presidential decree 17/2015 authorized the authorities to offer land freed from charge, in certain areas only to investors meeting sure technical and monetary necessities; this has additionally facilitated the improvement of Egyptian real estate marketplace. To cater to overseas funding, partnerships and joint inventory businesses can also additionally personal desolate tract land inside those limits, although overseas companions or shareholders are concerned, furnishing that as a minimum 51 percent of the capital is owned through Egyptians [Citation25].

With the current regulation amendments that were implemented as of May 7, there have been significant changes made to the Ministry of Justice’s Real Estate registry system that have made it possible to simplify the steps for registering real estate inside the real estate registry.

The Central Bank of Egypt’s (CBE) Mortgage Finance Initiative has had a main impact as well, launching EGP 100bn loan finance initiative concentrated on low- and center-profits homebuyers with payment plans that may span as much as 30 years with a low interest price of no extra than 3 percent [Citation26]. The Central Bank of Egypt (CBE) additionally abolished the maximum net area unit requirement and expanded the maximum unit fee to EGP 2.5 million. Additionally, the Central Bank of Egypt (CBE) allowed banks to simply accept opportunity guarantees for finance if the unit cannot be registered [Citation27].

While the residential sector is currently highly impacted by the economic headwinds, we expect the situation to improve once the economy stabilizes. Earlier this year, we saw the government responding to the real estate developers’ demands of receiving state support to help alleviate some of the challenges they are facing. Among the various initiatives, the government has extended deadlines of existing projects by 20% and is now considering projects as complete once they have reached 85% of construction – down from 90% previously. This shall allow developers to complete the rest of their project at their own pace without risking getting fined.

Those reforms have had an effect on the long-term stability of the real estate market, making it more resistant to currency devaluation. However, in the term they have caused a scarcity of housing leading to increased prices.

Government reforms impacts on the consequences of real estate market variables

Massive foreign financial support has helped Egypt stabilize its tight economic spot over the years; however, it is common for governments globally to restrict unregulated direct/indirect foreign investments as a precautionary measure to maintain and increase economic stability.

However, the recent reforms implemented by the government have had effects and consequences on aspects of the real estate market. The following are some of the outcomes:

Foreign currency liquidity has been a worry for real estate developers and investors in Egypt. The lack of currency has made it challenging to import construction materials resulting in delays and higher costs. To address this issue the government has taken steps to enhance foreign exchange liquidity. The Central Bank of Egypt (CBE) has implemented policies to guarantee the availability of currency for imports, including construction materials. These measures have played a role, in alleviating liquidity concerns and minimizing construction delays within the real estate industry [Citation28].

Public account deficit: The Egyptian government acknowledges the significance of addressing the public account deficit in order to establish an environment. They have implemented reforms such, as practicing discipline and adopting austerity measures to decrease budget deficits. The objective is to improve management attract investors and boost investor confidence in the real estate market. A lower deficit can lead to decreased inflation and interest rates, thereby making real estate investments more appealing [Citation29].

Shaky investment atmosphere: The government has taken steps to tackle the problem of an investment climate. They have been focusing on making it easier to do business and simplifying procedures. Reforms such as cutting down on paperwork have been put in place to attract international investors to the real estate industry. These efforts by the government are already showing outcomes in creating a favorable environment, for investors [Citation30].

Increased market entry costs: The Egyptian government has implemented measures to tackle the issue of rising costs for entering the market. One of these steps involves reducing taxes and fees related to real estate transactions such as property registration and transfer taxes. Lowering these expenses makes it financially feasible for both individuals and businesses to participate in the real estate market. This in turn can boost demand and foster growth within the market [Citation31].

Decreased profit margin: Due to the decline in profit margins within the real estate market the government has taken measures to address this issue. Their focus has been on improving the infrastructure and logistics sector. By enhancing transportation and logistics they aim to lower construction costs, thereby increasing profit margins for real estate developers. Alongside these efforts the government has also encouraged partnerships between the private sectors in infrastructure projects with the goal of reducing development costs [Citation32].

Pricing speculation: Pricing speculation can cause fluctuations in the market and create problems with affordability. The government has been actively taking steps to tackle this issue by introducing regulations and promoting transparency. Through the provision of market data and the implementation of regulations to control speculation the Egyptian government aims to stabilize property prices and make sure they remain affordable for everyone [Citation33].

Impact analysis of the Egyptian case study

Adopting the proper government reforms is crucial to reduce the negative consequences of currency devaluation on the real estate markets, whose sustainability of the market has a strong relationship with macroeconomic factors, including fluctuations in exchange rates, to better gauge the effects. Therefore, this paper will give an insight of understating different relations between all those aspects and variables using the system thinking approach, Additionally, it will explore how regulatory reforms have impacts on those variables. For understanding of the real estate market system after and during devaluations, it is very important to understand the relations of that system addressing the government reforms on mitigating the risks associated with currency devaluation on real estate market. That will be based on the above understanding the relations of impact of currency devaluation of RE market variables and the governmental reforms and actions related to real-estate market during 2016–2023. Different kinds of relations will be discussed using those layers to address the impact analysis of how the governmental reforms have affected the dynamics of the real estate market.

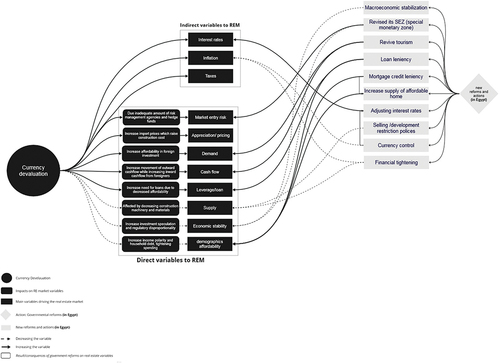

Understanding relations of the system (existing case)

When the value of exchanging the foreign currency decreases inflation tends to increase because the prices of goods and services go up. Throughout history real estate has proven to be a way to protect against inflation since property values typically rise alongside or surpass inflation rates. As inflation rises, rents increase well which boosts the value of our assets. Although building costs and interest rates have also gone up, the positive impact experiencing outweighs the effects (costs versus increased property value). While exchange rate of the foreign currency continues to increase, the Central Bank of Egypt (CBE) raise interest rates to stabilize the economy and counteract inflation. This could lead to mortgage rates in turn. Consequently, there might be a decrease in demand for estate causing a slowdown in real estate value growth or even a decline in property values depending on supply and demand dynamics at play. While term fixed rate mortgages offer protection against this uncertainty, most of our projects are financed with short-term debt that’s subject, to fluctuations.

Furthermore, the devaluation of currency has attracted investors who recognized an opportunity to enter or expand their presence in the real estate market at a lower cost. According to the Central Bank of Egypt [Citation34] there has been an increase in FDI in Egypt and this trend is expected to continue in 2022/23 with real estate being one of the main sectors attracting FDI attention. Many developers from Gulf countries have announced projects for primary and secondary residences over the past year.

By analyzing the below chart, we could conclude some main facts as follows: ()

Figure 3. Understanding relations of the system in Egypt (existing case).

Rising interest rates is one of the major effects to decrease affordability, and while currency control does decrease inflation and its effects, it also plays a key role in adjusting interest rates. Loan leniency for both developers and buyers increase affordability rates as well, and mortgage credit leniency creates a bigger pool of buyers that also increases demand and supply.

Financial tightening also plays a factor in decreasing supply, while supply is decreased due to these restrictive policies, and the effects from inflation rates on import of construction materials and transportation, as investors are less able to sell and develop new units. Nonetheless, Egypt’s government tends to have quantitative easing methods across the years for developers’ restrictions, as these are usually set up only temporarily.

Egyptian government has created developers’ relief which often subsequently increases the confidence in hedge buying to decrease prices and raise affordability, which is considered to decrease market entry risk alongside creating trustworthy project consultancy agency and revising the policies for special monetary zones.

Tighter financial conditions had a direct impact on commercial property prices by making it more expensive for investors to finance new deals or refinance existing loans, thereby lowering investment in the sector. They could also have an indirect impact on the sector by slowing economic activity, reducing demand for commercial property such as shops, restaurants, and industrial buildings.

In a recent analysis to what happened in the real estate market, the financial conditions are indeed an important driver of commercial real estate prices, and they help to explain the divergent performance of the sector across regions during the pandemic and currency devaluations.

Credit policies directly influenced real estate market dynamics in the sense that real estate assets form the collateral on which mortgages and loans are allocated. Competitive and affordable mortgage rates facilitate the purchase of real estate and have a direct influence on living standards. Competitive and affordable mortgage rates with easier repayment installments are increasingly an essential for both young couples and first-home family buyers. Competitive and affordable mortgages and loans to provide access to private ownership or partial ownership for a growing number of citizens would contribute to solving housing problems in the long run.

For discussion and comments: https://miro.com/welcomeonboard/a1lUZkp4RVpMWUN4UlE2WDA1eVVuYTJFOGdhQzJoclFFRVlWb1N0bk1sUnBEZmNuM2ZkUVhMckV5Mm51eUduTnwzNDU4NzY0NTYxNDA1MDk0MDQ3fDI=?share_link_id=271108111979

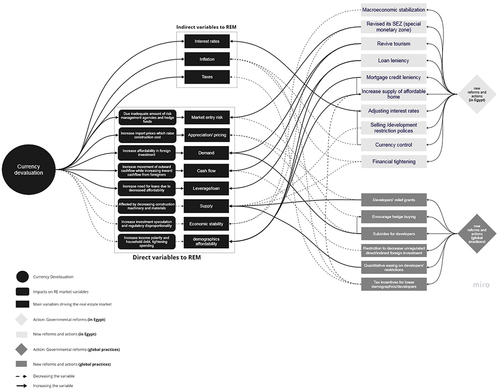

Enhancing the dynamics of the system: (proposed enhanced case)

Global practices of government reforms and actions

In order to enhance the dynamics of the system, it is crucial to explore a range of comprehensive global experiences set involving governmental reforms that aim to lessen the effects of currency devaluation on the real estate market by focusing on initiatives such as:

1. Developer support grants: Some countries facing challenges or currency volatility may offer grants or financial assistance, to real estate developers to help them navigate fluctuations in currencies.

The government of Hong Kong has implemented a subsidy program known as the ‘Anti Epidemic Fund’ in order to support real estate developers who are facing difficulties due to the COVID-19. The goal is to ensure the stability of the real estate market [Citation35].

2. Promotion of hedging practices: To mitigate risks associated with currency fluctuations many countries with real estate markets encourage the adoption of hedging practices. The United Arab Emirates and Singapore both experiencing investment in real estate actively promote these practices.

The real estate market in the United Arab Emirates (UAE) encourages the use of hedging strategies, which enable investors to secure exchange rates, for property transactions. This approach helps minimize the impact of currency fluctuations and boosts investor trust and assurance [Citation36].

3. Subsidies for developers: In various countries those prioritizing development are offered government subsidies and reduced interest rates to support real estate developers.

For instance, the government of India has implemented measures to encourage developers by offering subsidies and lowering interest rates on loans for affordable housing projects. This initiative aims to boost construction activities and enhance the feasibility of these projects [Citation37].

4. Regulation of foreign investment: Countries that attract foreign real estate investors often have regulations in place to ensure stability and alignment with their development goals. Australia serves as an example by implementing regulations on investment in real estate to maintain control over property prices and guarantee affordable housing, for its citizens.

The Australian government has rules when it comes to investment in the real estate sector. These rules are put in place to manage property prices make sure that domestic buyers can afford homes and align foreign investments with the country’s development objectives [Citation38].

5. Quantitative easing measures with developer restrictions: Central banks in countries like the United States, European nations and Japan have introduced measures of easing to inject liquidity into sectors, including real estate during times of economic downturn.

During the crisis the United States introduced measures known as quantitative easing to inject liquidity into the real estate sector. However, these measures were often accompanied by limitations imposed on developers in order to discourage activities [Citation39].

6. Tax incentives for lower demographics and developers: Countries grappling with housing affordability issues, such, as the United States and several European nations, may consider implementing tax incentives aimed at lower-income individuals and developers. Inflation is a major factor to maintain as it increases taxes, demographic’s affordability, cash flow, prices and demand. Therefore, globally, governments set up tax incentives for lower demographics and developers to decrease both inflation and taxes’ effects on affordability.

Germany provides tax incentives to developers who build housing units that are affordable. This helps encourage developers to focus on creating housing options for individuals with incomes making it easier for them to access and afford accommodations [Citation40].

Enhanced system including global practices of government reforms and actions

Based on we can predict a more enhanced system addressing the full aspects together; this could give insights on better performance for the system using more government reforms and providing more macroeconomic stability to the real estate market ().

Figure 4. Enhanced system including global practices of government reforms and actions.

For discussion and comments: https://miro.com/welcomeonboard/a1lUZkp4RVpMWUN4UlE2WDA1eVVuYTJFOGdhQzJoclFFRVlWb1N0bk1sUnBEZmNuM2ZkUVhMckV5Mm51eUduTnwzNDU4NzY0NTYxNDA1MDk0MDQ3fDI=?share_link_id=271108111979

Conclusion

To reply to the main objects of the research, and based on the analysis and enhanced system, we can assess impact of the currency devaluation on the real estate market and the government response as follows:

After currency devaluation waves, the dynamics of the system of real estate are quite challenging. The system had been affected by multitude of factors that had a great impact on the market variables, followed by some main emerging consequences on the health of the market.

This situation necessitates urgent responses in all sectors, through governmental reforms and both direct and indirect actions.

In order to predict the impacts of new enhanced system on main consequences of real estate market variables, as an attempt of reaching macroeconomic stabilization in Egypt we have to predict the impacts of new enhanced system on main consequences of real estate market variables, through getting foreign currency liquidity to acceptable levels, public account deficit narrowing and a slow increase of inflation rates.

In general, it can be quite challenging to determine specifically the impact of currency devaluation on the real estate market variables. This is because it is influenced by a multitude of factors. While external factors like the economy and government reforms do play a role, they are not the determinants of outcomes. Hence, the government reforms do not alone shape economies. It is crucial to understand these interconnections to develop policies that minimize losses caused by external triggers.

Egypt has adopted a strategy of gradual reducing the value of its currency and making small adjustments to prices. This approach is particularly beneficial for countries with foreign currency obligations, such as external debt or a large portion of imported goods in domestic consumption. These reforms have had long-term implications for the stability of the real estate market, making it more resistant to fluctuations in currency exchange rates. However, they have also affected the availability of housing resulting in prices.

Understanding how these aspects of the real estate market system including the impacts of currency devaluation and the government reforms are interconnected is crucial for comprehending how each element impacts the system. These relationships can be categorized into two groups: the direction of relations and the type of relations as follows ():

Figure 5. Directions of aspects’ relations of the real estate market’s system.

Directions of aspects’ relations of the real estate market’s system

To fully comprehend the interactions, within this system it is essential to analyze the interconnections in both directions; there are typically numerous direct and indirect influences, including the real estate market which is directly impacted by currency devaluation. When a currency’s value declines, it loses purchasing power, which reduces real estate investment and may lower market values.

How the impacts of currency devaluation are affected bygovernment reforms. Regulations that make it simpler for individuals to acquire funds and make real estate investments might lessen the effects of currency devaluations. Similarly, easing trade or tax barriers can also operate as a buffer against the effects of devaluation.

The link between currency devaluation and government reforms feedback loops. For instance, additional investment in the real estate market can result from a currency devaluation in reaction to regulatory reforms.

Sectors like the real estate markets (REMs) are directly impacted by the complex interactions between government reforms and currency devaluation. Currency depreciation and regulatory reforms are positively correlated, fostering sound real estate investments. Contrarily, a negative response to onerous rules may deter investors from making investments in some nations, which would reduce the rate of growth of currencies over time. The real estate market is harmed by this imbalance.

Types of aspects’ relations of the real estate market system

Understanding how various external factors can affect real estate markets and currency devaluation is crucial. Factors such as unrest or shifts in supply and demand have the potential to influence each market differently. It is important to monitor these factors and compare their impact with improvements.

The connection between reforms and the interconnectivity of real estate markets is significant. Depending on the effects of changes and currency devaluations some markets may be more vulnerable than others. The effectiveness of reforms can also be influenced by varying conditions across markets. To minimize the impact of currency devaluation on both the economy and the real estate market it is essential to have an understanding of this system. By understanding these interactions governments can implement reforms that mitigate effects.

The correlation between impact and capital flows is also noteworthy. Government reforms have the potential to either attract or deter capital flows, which subsequently affect real estate markets and currency devaluation. For example if regulations are overly strict, investors may be discouraged from investing in a country leading to decreased growth and increased currency devaluation. These factors can consequently decrease activity within the real estate market.

The relationship between events and their influence on the currency and real estate markets is quite intriguing. For instance when economic conditions shift, central banks worldwide tend to modify their strategies, resulting in fluctuations in currency values and adjustments in the real estate sector. Moreover policy measures such as taxes, subsidies and government spending can also play a role in impacting both currency devaluation and the real estate market. These interconnections between currency valuations, capital flows and policy tools all contribute to shaping the dynamics of the real estate market.

Finally, decision-makers should take into account additional policy tools in the context of interrelated economic variables existing in an economy, taxes, subsidies and government spending impacting monetary valuation and capital flows impacting the performance of real estate markets (REMs). Furthermore, addressing the root causes of currency devaluation such as inflation and a significant budget deficit should be a priority for the government. This will contribute to creating a environment for the real estate market in the future. And it is crucial for the government to maintain oversight of the impacts of these reforms and make modifications.

Disclosure statement

No potential conflict of interest was reported by the author(s).

References

- Nashashibi K. International monetary fund. Devaluation in developing countries: the difficult choices. 1983. Available from: https://www.Users/baher/Downloads/022-article-A004-en.pdf.

- Yrigoy I. Transforming non-performing loans into re-performing loans: hotel assets as a post-crisis rentier frontier in Spain. 2018. Available from: https://www.sciencedirect.com/science/article/abs/pii/S0016718518303312

- Howard M. Exchange rate devaluation and the demand for real money. Savings Dev. 2002;26(1):33–48. https://www.researchgate.net/publication/287442288_Exchange_rate_devaluation_and_the_demand_for_real_money_balances_in_Jamaica

- Diala A. Effects of exchange rate volatility on low income residential real estate investment returns. Res. J. Finance Account 2022;8(6):8–15. https://www.iiste.org/Journals/index.php/RJFA/article/viewFile/36295/37294

- IMF. How countries should respond to the strong dollar. 2022.

- Andrés Rosanovich S, Paula Di Giovambattista A, 2020. Exchange rate pass-through to house rental prices. Evidence from the buenos aires’ semi-dollarized market. Available from: https://www.scielo.cl/pdf/invi/v35n99/0718-8358-invi-35-99-130.pdf

- OECD. (2022 Nov 14). Revenue statistics Africa: key findings for Egypt. Available from: https://www.oecd.org/countries/egypt/

- Mariolis T, Ntemiroglou N. Matrix multipliers, demand composition and income distribution: post-Keynesian–Sraffian theory and evidence from the world’s ten largest economies. Metroeconomica. 2023;74(4):658–697.

- IMF. Devaluation in developing countries: the difficult choices. 1983.

- Realtor magazine. real estate as a hedge against currency devaluation. 2020. Available from: https://www.nar.realtor/magazine/broker-news/network/real-estate-as-a-hedge-against-currency-devaluation

- Wealth briefing. The Dollar’s Depreciation And Real Estate Impact. 2023. Available from: https://www.wealthbriefing.com/html/article.php?id=197894

- Reality times. 2020. How currency devaluation creates a real estate boom. Available from: https://realtytimes.com/headlines/item/1040231-how-currency-devaluation-creates-a-real-estate-boom

- Altunbaş Y, Kara A, Marqués-Ibáñez D. Large debt financing syndicated loans versus corporate bonds. Ecb.europa.eu. [updated 2009; cited 2022 Jul 24]. Available from: https://www.ecb.europa.eu/pub/pdf/scpwps/ecbwp1028.pdf

- Youssef H, Alnashar S, Erian J, et al. Egypt economic monitor : from floating to thriving – taking Egypt’s exports to new levels. World Bank. [cited 2019 July 1]. Available from: https://documents.worldbank.org/en/publication/documents-reports/documentdetail/260061563202299626/egypt-economic-monitor-from-floating-to-thriving-taking-egypts-exports-to-new-levels

- IMF. Transcript of press conference on the IMF program for Egypt. 2023. Available from: https://www.imf.org/en/News/Articles/2023/01/10/tr011023-transcript-of-egypt-press-briefing

- 7 reasons for Africa’s currency slide. World Economic Forum. [cited 2015 Aug 26]. Available from: https://www.weforum.org/agenda/2015/08/7-reasons-for-africas-currency-slide/

- Yap KLM, Goko C, Song Z. The devaluation run in emerging markets is just getting started. Bloomberg.Com. [cited 2023 Feb 13]. Available from: https://www.bloomberg.com/news/articles/2023-02-12/the-devaluation-run-in-emerging-markets-is-just-getting-started#xj4y7vzkg

- WorldBank. Egypt’s economic update — april 2022. 2022 Jul 7.

- GAIF. Invest in Egypt. 2020. Available from: https://www.investinegypt.gov.eg/English/pages/sector.aspx?SectorId=84

- CBE. Annual report 2016/2017 - البنك المركزي المصري. 2016. Available from: https://www.cbe.org.eg/-/media/project/cbe/listing/research/annual-report/annualreport2016-2017.pdf.

- OECD. Egypt continues to strengthen its institutional and legal framework for investment - OECD. Oecd.org. [updated 2009; cited 2022 Jul 5]. Available from: https://www.oecd.org/countries/egypt/egypt-continues-to-strengthen-its-institutional-and-legal-framework-for-investment.html

- AmCham E. Affordability Affairs. AmCham. [updated 2021; cited 2022 Jun 14]. Available from: https://www.amcham.org.eg/publications/industry-insight/issue/33/AFFORDABILITY-AFFAIRS.

- JLL. 2023 Global data center outlook. [cited 2023, April 8]. Available from: https://www.us.jll.com/en/trends-and-insights/research/data-center-outlook

- IMF. (2016). IMF executive board approves US$12 billion extended arrangement under the extended fund facility for Egypt. [cited 2022 Jun 21]. Available from: https://www.imf.org/en/News/Articles/2016/11/11/PR16501-Egypt-Executive-Board-Approves-12-billion-Extended-Arrangement

- Wagner E (2020). Egypt - United States department of state. United States Department of State. [cited 2022 Jul 20]. Available from: https://www.state.gov/reports/2020-investment-climate-statements/egypt/.

- CBE. Financial stability report 2020 - البنك المركزي المصري. 2020.

- USDS. (2020). 2020 investment climate statements: egypt. [cited 2022 Jun 13]. Available from: https://www.state.gov/reports/2020-investment-climate-statements/.

- Reuters. Egypt eases access to foreign currency for importers, factories. 2021.

- Daily News Egypt. Egypt’s 2021-2022 budget aims to reduce public debt. 2021.

- Egypt Today. Egypt launches 16 initiatives to improve business climate. 2021a.

- Egypt Today. Egypt’s real estate tax draft law to reduce financial burdens. Egypt Today. 2021b.

- Enterprise. 2021. Egypt approves PPP projects in healthcare, logistics, and infrastructure.

- Oxford Business Group. 2021. Egypt’s Real Estate Market: a Historical Perspective.

- CBE. Central bank of Egypt’s measures to offset the impact of covid-19. 2022. Available from: https://www.cbe.org.eg/-/media/project/cbe/file/long-context/central-bank-of-egypts-measures-to-offset-the-impact-of-covid19.pdf

- Global times. Support policies boosting recovery in China’s vital property sector new. 2023.

- Ball S. Hedge funds - jurisdictional comparisons. New. 2011.

- Godrej Properties. Affordable housing options in India: government initiatives and developer contributions. 2023.

- Parliament of Australia. regulation of foreign investment in residential property. 2013. Available from: https://www.aph.gov.au/-/media/02_Parliamentary_Business/24_Committees/243_Reps_Committees/Economics/44p/Real_Estate/Report/Chapter2.pdf?la=en&hash=D5F62C78C447794415520AEBB3FDE6B56BCD2585

- European Parliament. ECB quantitative Easing (QE): lessons drawn from QE experiences carried out by other major central banks - Monetary Dialogue. 2015. Available from: https://www.europarl.europa.eu/cmsdata/105460/IPOL_IDA(2015)587289_EN.pdf

- USAID. Effectiveness and economic impact of tax incentives in the SADC region. 2004. Available from: https://pdf.usaid.gov/pdf_docs/Pnacy929.pdf