ABSTRACT

Risks are a central part of life for households in low-income countries and health shocks in particular are associated with poverty. Formal mechanisms protecting households against the financial consequences of shocks are largely absent, especially among poor rural households. Our aim is to identify the relative importance of health shocks and to explore factors associated with coping behaviour and foregone care. We use a cross-sectional survey among 1226 randomly selected agricultural households in Kenya. In our sample, illness and injury shocks dominate all other shocks in prevalence. Almost 2% of households incurred catastrophic health expenditure in the last year. Using a probit model we identified the main coping strategies associated with facing a health shock: (1) use savings, (2) sell assets and (3) ask for gifts or loans. One in five households forewent necessary care in the last 12 months. We conclude that health shocks pose a significant risk to households. Implementing pre-payment or saving mechanisms might help protect households against the financial consequences of ill health. Such mechanisms, however, should take into account the competing shocks that agricultural households face, making it almost impossible to reserve a share of their limited resources for the protection against health shocks only.

Introduction

Risks are a central part of life for most households in low-income countries (LICs) (Banerjee & Duflo, Citation2011). Understanding these risks and the associated coping strategies is of critical importance to policy makers. This is reflected in the World Development Report 2014 entitled Risk and Opportunity (World Bank, Citation2014), investigating how households can become more resilient to the wide range of risks they face. These risks can translate into a range of different ‘shocks’, defined as adverse events that are costly to individuals and households in terms of lost income, reduced consumption or the sale of assets (Dercon, Hoddinott, & Woldehanna, Citation2005).

Formal mechanisms to protect households against the financial consequences of shocks are largely absent in sub-Saharan Africa (SSA), especially among poor rural households working in the informal sector (European report on development, Citation2010). The majority of these households rely on agriculture for their livelihoods, that is, 61% of total employment in Kenya is in the agricultural sector (World Bank, Citation2005). These agricultural households are often affected by limited access to resources, low agricultural productivity and repeated exposure to risks, making them more susceptible to shocks (Tirivayi, Knowles, & Davis, Citation2013). The literature on risk and vulnerability in LICs has established that shocks from many sources occur frequently and can have a severe impact, leading to among others loss of assets (Heltberg, Oviedo, & Talukdar, Citation2013). However, evidence about the relative importance of health shocks compared to other adverse events and associated copings mechanisms in Kenya specifically is very limited. This paper adds to the existing literature by comparing health shocks to other adverse events, by exploring the factors associated with coping behaviour and foregoing necessary care among Kenyan households facing illness in the absence of widespread formal insurance schemes.

Illness is among the most important shocks associated with poverty in LICs (Leive & Xu, Citation2008). About 100 million people fall into poverty each year because of health-care costs (World Bank, Citation2014). Health shocks can place a double financial burden on households, not only having to bear the costs of medical treatment but also the income loss from inability to work (Leive & Xu, Citation2008). Since the bulk of healthcare in LICs is financed through out-of-pocket (OOP) payments at the time of use, many households suffer financial catastrophe as a result of seeking care or forego necessary healthcare all together (Van Doorslaer et al., Citation2006; Xu et al., Citation2003). The combination of catastrophic health-care expenditures and foregone earnings can cause households to slide below the poverty line or even deeper into poverty (Wagstaff, Citation2008), the so called ‘medical poverty trap’ (Whitehead, Dahlgren, & Evans, Citation2001). Notwithstanding these considerable financial consequences, coverage by formal insurance against health shocks remains limited (De Allegri, Sauerborn, Kouyaté, & Flessa, Citation2009; Grimm, Citation2010), especially among agricultural households (Mathauer, Schmidt, & Wenyaa, Citation2008), who are also more susceptible to health shocks (Tirivayi et al., Citation2013).

The aim of this paper is to identify the relative importance of health shocks compared to other shocks and to explore the factors associated with coping behaviour and foregoing necessary care among agricultural households facing illness in the absence of widespread formal insurance schemes. We study households in the agricultural sector in Kenya where the need for increasing protection against health shocks is particularly high (Health Insurance Fund, Citation2011; International Labour Organization, Citation2013; PharmAccess Foundation, Citation2014). The 2014 World Development Report, for example, showed that Kenya's risk preparation (based on a composite index of human capital, physical and financial assets, social support and state support) is low compared to neighbouring countries Ethiopia and Tanzania (World Bank, Citation2014).

Protecting Kenyans against health shocks and their consequences is indeed high on the policy agenda. Several parties have recently rolled out health insurance schemes in Kenya, including the Kenyan government and the Dutch Health Insurance Fund (HIF). The Kenyan government introduced the National Hospital Insurance Fund (NHIF) (Government of the Republic of Kenya, Citation2007) and the Dutch HIF cooperates with PharmAccess and the Africa Air Rescue Health Insurance Ltd. to offer low-cost health insurance to selected target groups in Kenya (Health Insurance Fund, Citation2015). The first group that became eligible for this insurance from the HIF were the members of the Tanykina Dairy Plant Ltd. (Van der Gaag et al., Citation2011) and members of Lelbren Dairies Ltd. were expected to become eligible at a later stage. Both Tanykina and Lelbren are farmer cooperatives, collecting milk from individual farmers that is subsequently sold in bulk to factories. This benefits members of the cooperatives, because the price per litre milk is higher for bulked milk than for smaller amounts provided by individual farmers (Lelbren Dairies Limited, Citation2011). The study presented here was conducted among farmers of both cooperatives, before the health insurance was introduced.

Over the last decade, the literature on shocks in general and health shocks specifically, in low- and middle-income countries (LMIC), has grown. A study by Wagstaff and Lindelow (Citation2010) compared different shocks in Laos, showing that health shocks are more common than most other shocks and concentrated among the poor. Health shocks not only occur relatively frequently, but also, as evidence from rural Cambodia shows, cause more serious economic damage to households than crop failure (Kenjiro, Citation2005). The importance of health shocks is confirmed by most studies in LICs on this topic (Asfaw & von Braun, Citation2004; Gertler & Gruber, Citation2002; Lindelow & Wagstaff, Citation2005) and in detail by Heltberg and Lund (Citation2009), who found that health shocks dominate in frequency, costliness and adversity in Pakistan. However, Yilma et al. (Citation2014) found that, in rural Ethiopia, health shocks do not dominate in terms of frequency, but natural shocks do. Pitt and Rosenzweig (Citation1984) also found only small effects of illness on farm profits in Indonesia. Households made up for reductions in labour within the family by hiring outside help, thereby maintaining previous consumption levels. A more recent paper also investigated economic risks of ill health in Indonesia, but differentiated findings across socio-economic groups (Sparrow et al., Citation2014). Sparrow et al. (Citation2014) found that consumption smoothing following ill health was indeed successful but only for the wealthier half of the population. For rural and poor households, consumption smoothing was imperfect and non-food expenditure was affected. The main coping strategy for the poor was borrowing, implying potential long-term effects through incurred debt. They also conclude that health shocks might affect future income by depleting buffers such as assets and savings for consumption smoothing and financing healthcare (Sparrow et al., Citation2014).

When measuring financial protection against illness related expenditures, coping strategies provide important information on how households respond to health shocks (for a detailed description of coping strategies see e.g. Morduch, Citation1995). A literature review by McIntyre, Thiede, Dahlgren, and Whitehead (Citation2006) showed that health shocks trigger one or several coping strategies, including reduction of (food) consumption, sale of assets or livestock, taking out formal and informal loans, diversification of labour activities and intra-household labour substitution. Leive and Xu (Citation2008) show, in a study of 15 African countries, that in case of OOP health payments, 23% of households in Zambia and up to 68% in Burkina Faso borrow and sell assets. They also find that differences in coping strategies across socio-economic groups are considerable: among Kenyan households in the lowest wealth quintile, 45% of households affected by a health shocks sold assets or borrowed, while this percentage was 22% in the richest quintile. Chuma, Gilson, and Molyneux (Citation2007) compared rural and urban households in Coastal Kenya and found higher levels of reported ill health in the rural setting while differences in treatment-seeking patterns across socio-economic groups were specifically present in the urban setting. Urban households with a higher ability to pay used more care. They also indicated that households often opted for cheaper alternatives of healthcare to reduce potential costs.

Although coping strategies may help households to ensure coverage of their basic needs in the short run, the long-term consequences can be substantial (Flores, Krishnakumar, O'Donnell, & van Doorslaer, Citation2008). Assets or livestock often form an integral resource of a household's livelihood and selling may be the start of a vicious cycle of increased economic vulnerability. Children can be pulled out of school to enter the labour force and therefore fail to advance in school which can lead to long-term negative outcomes such as low educational attainment and lower future earnings (Duryea, Lam, & Levison, Citation2007). Borrowing from family and friends can have severe effects because households often remain in debt for a considerable time after the health shock (Damme, Leemput, Por, Hardeman, & Meessen, Citation2004). Apart from lending, family and friends also assist affected households through donations, as is especially common in SSA countries where strong sharing obligations exist. Though these donations may prevent the affected household from having to revert to coping strategies with a long-term economic impact, the effects on the donating family member(s) can be considerable. Grimm, Hartwig, and Lay (Citation2011) applied a theoretical model on a sample of small entrepreneurs in Burkina Faso, showing that donations to the (extended) family, in particular for health-related expenditures, can require foregoing profitable investments and hence inhibits long-term growth of the enterprise of the donor.

In addition to these coping strategies to deal with the economic consequences of ill health, some households have to revert to forego necessary healthcare. The effects of foregoing necessary care on health status and future health-care costs can be considerable, but most studies ignore foregone treatment (Grimm, Citation2010). As far as we know, only one study has specifically quantified the extent of foregone care in LICs. This study by Abiola, Gonzales, Blendon, and Benson (Citation2011) in 20 SSA countries showed that 35% (Ghana) up to 82% (Zimbabwe) of the families went without medicine or medical treatment in the previous year. Mebratie et al. (Citation2015) found, using clinical vignettes which avoid the problem of reporting bias due to the unperceived need for healthcare, that underutilisation of healthcare in rural Ethiopia is not driven by the inability to recognise health problems nor due to a low perceived need for modern care.

While these studies provide important insights necessary to understand health shocks and the associated coping strategies, households in different contexts cope with health shocks differently (Leive & Xu, Citation2008; Townsend, Citation1995). The existing evidence from agricultural households in Kenya is very limited. This study tries to fill that gap using cross-sectional data on household characteristics, self-reported health shocks and associated coping mechanisms and on foregone care. Clearly these data allow us to identify correlations but do not allow us to estimate causal effects due to a lack of control for reverse causality between income and shock occurrence.

In the following sections of this paper, we present the data collected and the methodology used. Subsequently we discuss the relative importance of health shocks, the average number of times households were affected by different shocks, that is, the shock prevalence, the socio-economic inequality in shock occurrence and the self-reported impact of these shocks. Then we discuss coping strategies and indicate which factors drive the use of these different strategies by estimating a multivariate probit model. The relative importance of different aspects of OOP health expenditure is assessed and we calculate whether a household incurred catastrophic health expenditure. This is followed by the estimation of a probit model to identify the factors associated with foregoing necessary care. We conclude with policy implications informing decision-making on the protection of agricultural populations in SSA against the financial consequences of illness.

Setting

Kenya is a low-income country in East Africa, with a population of 40 million people. Gross national income per capita is 790$ (all $ amounts are in US dollars) and 46% of the population lives below the poverty line (World Bank, Citation2010). 77% of children are fully immunised but under-five mortality (U5M) remains high at 73 per 1000 live births. This is still far from Millennium Development Goal 4 aiming to reduce U5M to 33 per 1000 by 2015 in Kenya (United Nations, Citation2013).

Our study took place in West Kenya where an estimated 70% of the population is involved in dairy farming (Lelbren Dairies Limited, Citation2011); this is slightly higher than the overall average of 61% in Kenya (World Bank, Citation2005). This suggests that the region is broadly representative for Kenya in terms of agricultural activity. A modal agricultural household has a total expenditure of 2600 $/year and owns 4 cows and 10 chickens. Most farmers also own sheep, goats or donkeys and have a plot of land to grow crops. The remaining 30% of the population generates income through the cultivation of tea crops or as day labourer at dairy or tea farms (Lelbren Dairies Limited, Citation2011). The remaining 30% of the population is not involved in dairy farming, for example because of formal employment or because they do not own any cattle, and is not represented in this study.

Data

We collected data from a random sample of 1226 agricultural households (7599 individuals) in 2011. Based on a list of all households in the study area supplying milk to the dairy farming cooperatives operating in this area – Tanykina Dairies Ltd. and Lelbren Dairies Ltd – 1315 households were selected through simple randomisation for an interview and no weights were applied. The necessary sample size was calculated (StataCorp LP, Citation2013) for another study on health-care visits in this population, which is slightly different from the health shocks studied here, though still related to the health status of the studied population. These calculations (power = 80%, α = 0.05) showed that a minimum of 1200 households was required to pick up a 10% increase in the number of health-care visits. To ensure that data from at least 1200 households would be available, a total of 1315 households were randomly selected. Of the selected households, 6.8% could not be interviewed because no consent was given, the household had moved recently out of the study area or the household could not be found, resulting in the study sample of 1226 households.

Interviewers and data-entrants received a two-week training from a multidisciplinary team of survey experts, researchers, data managers, a lab technician and a medical doctor. Focus group discussions with farmers were organised to check that all questions were understandable and the survey was piloted among 162 households (Van der Gaag et al., Citation2011). The interviewers worked in teams consisting of one socioeconomic and one biomedical interviewer. The questions used in this study were administered to the most knowledgeable person on behalf of all household members. In most cases this was the household head or the mother of the children.

The survey contained questions on household characteristics including age, gender, education, employment, consumption, assets, livestock, shocks and coping strategies for those who incurred a health shock and foregone care. There is also information about current enrolment of households in a health insurance scheme. When this survey took place the only health insurance scheme readily available in the study area was the NHIF, the primary provider of health insurance in Kenya (National Hospital Insurance Fund, Citation2014). Their coverage of the informal sector is limited and the benefit package contains only inpatient care in specific hospitals (Joint Learning Network for universal health coverage, Citation2014). In addition data were collected to develop a binary variable indicating whether the household diversified its income sources: only dairy farming (0) or also other income generating activities (1). Another binary variable indicates differentiation in the crops households are growing: more than one different types of crops (1) or not (0). The relevant sections of the survey are available upon request.

Ethical approval for this study was obtained from the Institutional Research and Ethics Committee from the Moi Teaching and Referral Hospital in Eldoret, Kenya under number 000603. Written informed consent was obtained from respondents through signing a letter that explained the details of the study.

Methodology

Relative importance of health shocks

We begin by identifying the relative importance of health shocks compared to other shocks, using a so-called ‘shocks section’ from our survey, which is based on a shocks section developed by Quintussi, Van de Poel, Panda, and Rutten (Citation2015) for rural India. Following two half-day focus group discussions with local farmers consisting of both women and men, we adapted this shocks section to better fit the Kenyan context and our study aim. This resulted in a shocks section which is a condensed version of the shock section in the World Bank's Living Standards Measurement Study - Integrated Surveys on Agriculture (World Bank, Citation2009). In our shock section, households were asked how many times in the past 12 months they experienced health shocks (illness and injury in the household, death in the household), natural and biological shocks (natural disaster, storage, crop or livestock disease), economic shocks (job loss, drop in sale prices of agricultural products and increase in agricultural input prices) and socio-political shocks (political, religious, tribal conflict and theft). We calculate the percentage of households which were affected once, twice or more than twice for each type of shock, as well as the average number of times households were affected by these different shocks, we call the latter the ‘shock prevalence’.

Socio-economic inequality in shocks

We measure socio-economic inequalities, that is, between the poor and the better off, in the occurrence of the different shocks by means of a concentration index (cf. e.g. Wagstaff & Van Doorslaer, Citation2000). Since the outcome measure is binary – shock occurred (1) or not (0), we use the corrected version of the concentration index as suggested by Erreygers (Citation2009). The corrected concentration index (CCI) is calculated as follows:(1)

where yi indicates whether household i experienced the specific shock or not and Ri represents the households’ fractional rank in the socio-economic distribution. Positive values of the CCI indicate a disproportionate concentration of y among the rich and vice versa.

To measure socio-economic status, we use detailed information on household consumption from both purchased and self-produced goods. The yearly household consumption is based on a context specific list of 57 items of weekly food consumption, 33 items of non-food consumption such as housing, transport and personal care as well as 50 annual non-food items such as clothing, furniture, health and education. We assume that the weekly and monthly consumption, as collected in the months February and March, is representative for the rest of the year and is therefore multiplied to obtain consumption information at yearly level.

Self-reported impact and value lost

For those households incurring a specific type of shock, the self-reported impact of this shock was collected on a five point Likert scale running from 1 very small to 5 very large. Respondents were subsequently asked to report the ‘value lost’, the actual monetary impact of these shocks including not only expenditures but also income, asset and land losses associated with the specific shock. Because this was included in one single question, we cannot differentiate between the direct and indirect costs. Monetary values were reported in the local currency and converted to US dollars in 2011 (1 Kenyan shilling = 0.0119$). We compare the value lost to the food consumption of the affected household and calculate the value lost as percentage of food expenditure. Both the value lost and the food expenditure are calculated per capita to correct for household size. Food expenditure is based on the 57 items of food consumption. We also calculate the average expected value lost, taking into account frequency and financial impact of these shocks for the population on average.

Coping strategies

Households were asked to indicate for each coping mechanism whether they used it (1) or not (0) in case of a health shock. Twelve coping strategies were included: do nothing, use savings, use insurance, sell animals/farm land/assets, work more hours, send children to relatives or friends, ask for gifts/assistance/loans from relatives and friends, borrow money from money lenders, borrow money from bank, seek religious/spiritual help, get help from a Non-Governmental Organisation (NGO) and other. Up to three different coping strategies could be indicated per shock. We explore the coping strategies triggered by health shocks, and analyse the factors associated with the use of specific coping strategies for the shock where the probability of occurrence in the past 12 months was larger than .05.

Most households used more than one coping mechanism and we expect the choice for these mechanisms to be correlated. Given that the dependent variables in a set of otherwise independent equations are potentially interdependent, we apply a multivariate probit regression model (Cappellari & Jenkins, Citation2003) on the subsample of households reporting a health shock, as shown below:(2)

with y*hc a latent variable which is 1 if household h adopted one of the c coping strategies in case of a health shock. In this study the equation counter c ranges from 1 to 4 representing the four coping strategies with a probability of occurrence larger than .05 (do nothing, use savings, sell animals/farm land/assets and ask for gifts/assistance/loans from relatives and friends). This threshold is used because the regression models for coping mechanisms with a lower probability of occurrence did not converge when applied to the subsample of households reporting a health shock. Xh are household characteristics (proportion of children in household (hh), proportion of elderly in hh, poor household, middle income household and household has health insurance), Bh are household head characteristics (age hh head, Christian hh head, primary educ. hh head, sec. or higher educ. hh head) Dh and are variables indicating whether the household diversified its income sources and crops (hh has income from source other than dairy, hh has income from diverse crops). The error terms (ϵhc) are drawn from a multivariate normal distribution. We report coefficients of the multivariate probit model for all outcomes and explanatory variables. Standard errors are calculated for each equation using the STATA user-written command – mvprobit. To calculate the average marginal effect, we use the simulation procedure proposed by Cappellari and Jenkins (Cappellari & Jenkins, Citation2003) for a multivariate probit model and perform 50 random draws to increase accuracy (Jones, Rice, Bago d`Uva, & Balia, Citation2007).

OOP health expenditures and catastrophic expenditure

We use total household health expenditure in the last 12 months for 9 expenditure categories (drugs, outpatient care, laboratory tests, inpatient care, transport to and from medical facility, traditional medical services, therapeutic appliances, health insurance premium and other). Based on total household health expenditure and total non-food expenditure, we calculate whether a household incurred ‘catastrophic’ expenditure (Xu et al., Citation2003). When health-care expenditures are large relative to the resources available to the household, the associated disruption to living standards is considered catastrophic. The catastrophic payment headcount is calculated as follows (ÒDonnell, Van Doorslaer, Wagstaff, & Lindelow, Citation2008):(3)

where N is the sample size and Eh is 1 if the share of health-care expenditure over total non-food expenditure is larger than a threshold z and 0 otherwise for household h. As proposed by Xu et al. (Citation2003) we place the threshold z at 40% of non-food expenditure.

Foregone care

Instead of spending on health shocks, households can also decide not to use necessary healthcare which limits costs, at the risk of experiencing a worse health status and higher health expenditures at a later stage. Every individual household member was asked whether he/she needed care in the last 12 months but could not get it, and subsequently had to indicate for which of the following reason(s): medical fees too expensive, no drugs available, could not afford medication, quality of care too low, could not take time off work, travel costs, no medical facility in the area, waiting times, unfriendly staff and other. The type of care foregone was also asked: care for acute illness, medication, care for chronic disease, therapeutic appliances, preventive care, maternity care, hospitalisation and other. We identify the types of households more likely to forego care using a probit model similar to equation (2) but with a single equation, that is, c = 1. We report coefficients of the single probit model for all explanatory variables. Standard errors are calculated using the STATA command – probit. To calculate the average marginal effect we subsequently use the – margins command. All analyses were performed in STATA 12.

Results

Relative importance of health shocks

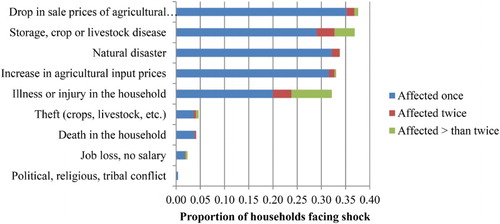

provides descriptive statistics. Kenyan households face a broad range of shocks; shows that the largest share of households (0.38) is faced with a drop in sale prices of agricultural products at least once. We also find that many households are affected at least once by storage, crop or livestock disease (0.37), natural disasters (0.34), increase in the agricultural input prices (0.33) and illness or injury in the household (0.32). Other shocks, related to theft, death and job loss occur only sporadically.

Figure 1. Proportion of households facing shocks.

Table 1. Descriptive statistics.

also shows that illness and injury affects households often more than once, while most other types of shocks hit only one time over the past 12 months. To take this frequency into account, we calculated the shock prevalence. This results in (first column ) illness and injury being the most prevalent shock, with an average of 0.644 times per year. Followed by storage, crop or livestock disease (shock prevalence of 0.551 times per year), drop in sale prices of agricultural products (0.435), natural disaster (0.359) and increase in agricultural input prices (0.352).

Table 2. Shock characteristics.

Socio-economic inequality in shocks

All shocks, apart from the very sporadic political conflict, have a positive CCI (see ), implying that these shocks are more prevalent among the better off. Drops in sale prices of agricultural products are most disproportionally distributed towards the rich, followed by storage, crop or livestock disease. Health shocks are less unequally distributed across socio-economic groups.

Self-reported impact and value lost

shows the self-reported impact by type of shock (1 very small to 5 very large), showing that even though illness or injury is the most prevalent shock, the average impact is relatively low (3.2 out of 5.0) while death in the household has the largest reported impact on households (4.3 out of 5.0).

Health as well as other shocks can have considerable financial implications. shows the average value lost for households that incurred a specific shock, both in US dollars and as percentage of household food expenditure per capita. These costs include not only direct expenditures but also the indirect costs of foregone earnings and sold assets and land. Death in the household (175$ per capita) is by far the most expensive shock, followed by job loss (98$ per capita) and natural disasters (70$ per capita). When we compare these costs to the yearly expenditure on food, we find that death in affected household takes up 72% of the total expenditure on food, which will probably have catastrophic effects. When we also take into account shock prevalence ( second column), the expected costs of illness or injury are high with 11% of yearly food expenditure and on par with sale price shocks and natural and biological shocks (all 10% of food expenditure).

Coping strategies

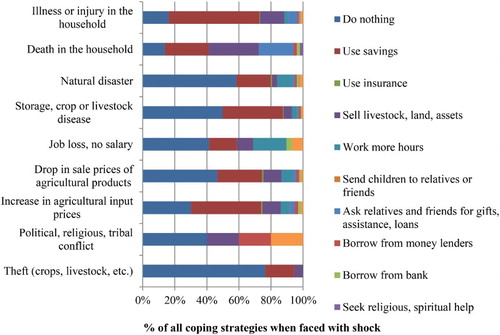

shows the dominant coping strategy associated with different types of shocks. Illness or injury costs are mostly covered by savings (56%), followed by selling livestock, land and assets (15%). There is also a considerable share of households indicating that they did nothing (16%) when illness or injury occurred. Death in the household leads to much larger reliance on relatives and friends for gifts, assistance and loans than any other shock. More formal arrangements, such as borrowing from a bank, are used only sporadically. Help from an NGO is not frequently sought in this population, nor is much spiritual or religious help for the financial consequences of shocks used.

Figure 2. Coping strategies when faced with shock.

shows the association between a limited number of factors and the four most used coping strategies in case of a health shock. The multivariate probit results suggest interdependence across the equations (the estimated correlation coefficients ρ21, ρ32 and ρ42 are significant), implying that the multivariate probit model is indeed the preferred model over individual probit models for each coping strategy separately. Of the coping strategies that were tested, the probability that a household does nothing in case of a health shock is significantly higher among the poor (11 percentage points (pp)) while this probability is significantly lower for households with income from a source other than dairy (9 pp). The probability to use savings is significantly lower among the poor (23 pp). The strategy to sell animals/farm land/assets is significantly more likely to be used in households where the head has a secondary or higher education (16 pp), by households who have income sources other than dairy (7 pp) and diversified their crops (8 pp), while the probability is lower among households who have a health insurance (10 pp). There is also a small but significant increase in the probability of using this coping strategy when the age of the household head is higher (0.01 pp). Finally, there is a negative association between asking for gifts/assistance/loans and the proportion of children in the household (24 pp) and also a negative association between this coping strategy and the household head having a secondary or higher education (11 pp). To confirm robustness of these findings (see Appendix Tables A1–A3, see Supplemental data): (1) an alternative model specification was tested which included additional interaction terms for the explanatory variables with a strong correlation (Cohen, Citation1988), (2) the original model was estimated on a sample excluding the top and bottom 10% of observations based on income and (3) the original model was estimated for a binary outcome variable reflecting whether any coping strategy was used or not. These robustness checks led to similar conclusions about the association between the factors tested and the coping strategies used in case of a health shock.

Table 3. Multivariate probit: Factors associated with coping strategies in case of a health shock.

OOP health expenditures and catastrophic expenditure

shows that drugs contribute with 6% of food expenditure by far the most to OOP health expenditures, followed by inpatient and outpatient care expenditures. The burden of laboratory tests, transport, traditional medical services and the health insurance premium is considerably lower. Reported expenditures on therapeutic appliances are typically almost zero. On average 1.88% of households incurred catastrophic expenditure, this percentage is higher for those which reported at least one health shock (3.04) though those without a health shock also incurred catastrophic expenditure (1.32%). Catastrophic expenditures are slightly lower among the poorest tertile of households (1.69%) compared to the better off (1.97%).

Table 4. Health-care expenditure as percentage of food expenditure.

Foregone care

So far we studied ex-post coping strategies and health-care expenditure, but households can also decide to forego necessary care. A considerable 21% of households report that at least one family member needed care in the past 12 months but could not get it. Often households which forego care, do this more than once. There is a clear socio-economic gradient in foregoing care, the CCI is negative (−0.083) and the tertile of poorest households reporting an average of 0.49 foregone health-care contacts compared to 0.34 among the richest households. This is an indication that foregoing necessary care relates to some extent to the available financial resources in a household. shows individual level data for the type of foregone healthcare. 52% of all cases of self-reported foregone care related to care for an acute illness, another 28% was for medication and 12% reported foregoing care for a chronic disease. Preventive care, maternity care and hospitalisation were less frequently reported to be foregone. shows the reported factors associated with foregoing necessary care. We find that 38% forewent care because the medical fees were too expensive and 20% because they could not afford the medication. Another considerable share (24%) of foregone care was associated with unavailability of drugs, while 6% forewent care because they perceived the quality of care to be too low. Only 2% forewent care because of travel costs or because of inability to take time off work, suggesting that direct costs of healthcare are more problematic than indirect costs.

Table 5. Reported type of foregone medical care.

Table 6. Reported reason for foregoing care.

shows the factors collected in this study that can be associated with foregoing care. These results confirm an association between poor households and foregoing care: the probability that a member from a poor household foregoes care is 7 pp higher. However, household where the head has at least primary education are less likely to forego care. To confirm robustness of these findings (see Appendix Tables A4 and A5, see Supplemental data): (1) an alternative model specification was tested which included additional interaction terms for the explanatory variables with a strong correlation (Cohen, Citation1988) and (2) the original model was estimated on a sample excluding the top and bottom 10% of observations based on income. These robustness checks led in most cases to similar conclusions about the association between the factors tested and foregone care.

Table 7. Probit: Factors associated with foregone care.

Conclusions and policy implications

This study shows that agricultural households in Kenya, like in most other LICs, are confronted with a wide range of uninsured shocks. We find that, among agricultural households, the most prevalent shock is illness or injury but these households are also frequently confronted with shocks that are specifically relevant for households in agriculture, that is, storage, crop or livestock disease, drop in sale prices of agricultural products, natural disaster and increase in agricultural input prices. This is in line with findings by Heltberg et al. (Citation2013) who found that in Maldives, Mexico and Nigeria, health shocks are the most commonly reported shock and these are second only to natural disaster in rural India, Peru and Uganda and second to asset loss in rural China. The study by Quintussi et al. (Citation2015), also on rural India, confirmed that health-related adverse events were the second most common adverse event, after natural disasters. While crop and livestock disease also occurred in about 8% of the Indian households, all other shocks were infrequent. Changes in agricultural prices were important adverse events in Kenya, but rural Indian households did not report to be frequently hit by these. This might be explained by more diverse sources of income generation, also outside of agriculture, assisted by self-help groups with informal micro-credit systems in which these Indian households participated.

In our sample, agriculture-related shocks are more prevalent among the better off. This pro-rich concentration might relate to the fact that only households that actually have agricultural products for sale, and not only for self-consumption, can be affected by these shocks. Health shocks are less unequally distributed and although costs associated with illness or injury are relatively, total expected costs are the highest because of the frequency of these shocks. These costs are mainly driven by OOP expenditures on drugs, inpatient and outpatient care. Expenditures on therapeutic appliances are typically almost zero. This might be due to limited access and limited usefulness of appliances like crutches and wheelchairs in rural environments with little paving.

Direct and indirect health costs can place a considerable burden on households: almost 2% of households incurred catastrophic expenditure in the past 12 months which would translate to approximately 80,000 affected household members across Kenya. Several mechanisms were identified at the household level to cope with the costs associated with the health shock. The main coping strategies were to (1) use savings, (2) sell animals/farm land/assets and (3) ask for gifts/assistance/loans. The probability that the first strategy is used is lower among the poor, while the second is more likely to be used by households with an educated head and diversified sources of income. This might relate to households with a lower socio-economic status having less savings, animals, farm land and assets. Further, there is a negative association between having health insurance and selling animals/farm land/assets in case of a health shock. This suggests that the financial protection provided by the health insurance prevents households from selling off their assets, though more research is necessary to verify this. Households with a higher proportion of children and with an educated household head are less associated with gifts/assistance/loans. It could be the case that educated household heads prefer selling their assets as opposed to asking for gifts, which might take away some of their experienced autonomy. All three of these strategies can have long-term negative economic consequence for households, as they may limit the ability to generate future income. Formal arrangements, such as borrowing from a bank and other assistance mechanisms including help from NGOs or religious institutions, are used only sporadically; this is probably due to low availability of these services. The estimated probability to use savings is significantly higher among the poor. Heltberg et al. (Citation2013) also show that the use of savings is a common coping strategy, as is the sale of productive assets, which often reduces future income earnings for agricultural households. They further find that rural households generally report a higher reliance on sales of non-productive assets such as furniture, basic appliances and durable items than urban households do, which was especially the case in Bangladesh and Uganda where the rural reporting rate is four times as high as with urban households. Yilma et al. (Citation2014) compared coping strategies for health and non-health shocks and report findings along the same line: health shocks are more likely to trigger borrowing and selling of assets compared to non-health shocks.

One in five households reported foregoing necessary care in the last 12 months and poor households were found to be more likely to forego care. Households with an educated head were less likely to forego care. This is in line with findings from Nikoloski and Ajwad (Citation2013) showing that in Russia, households with low educational attainment of the household head and with a high number of elderly people that suffered an income shock, tended to decrease expenditures on the use of health services. In more than half of the cases, foregone care was related to affordability of medical fees or medication and households with a lower educated head were more associated with foregoing care. This fuels concerns about the ability of the Kenyan health-care system to cater for the lowest socio-economic groups. Another third of the cases of foregone care were reported to be associated with low quality of care and unavailability of drugs. This suggests that problems persist in the health-care system, not only on the demand side (access and financial protection) but also on the supply side (availability and quality of care). Since only 2% of foregone care was associated with travel costs or inability to take time off work, it seems that the direct costs of healthcare are more problematic than indirect costs for agricultural households. Most cases of foregone care were for acute and chronic conditions, while only very few households reported to have foregone preventive or maternity care. Given the sharply rising prevalence of chronic diseases in LMIC (de-Graft Aikins et al., Citation2010), the expenditures for these conditions will add to the current burden of costs associated with infectious diseases, creating further challenges for households to obtain necessary care.

Our study confirms findings of Leive and Xu (Citation2008) that coping strategies with potential long-term negative impact such as using savings and selling assets to finance healthcare are widely used in Kenya. More importantly, our study shows that in addition to these problematic coping strategies, many households still frequently have to forego necessary care, especially the poorer, lower educated households. Our analysis suggests that the direct costs of healthcare utilisation mostly limit the access to care and that the indirect costs stemming from travel and taking time off work are considerably less problematic for agricultural households.

Generally, in most African countries, the health financing system is too weak to protect households from health shocks (Leive & Xu, Citation2008). Having health insurance can facilitate medical treatment and recovery, while reducing OOP expenses, when a family member falls ill (World Bank, Citation2014). Health insurance has indeed emerged as a frequently used instrument in current health financing reforms in LICs aimed at achieving universal coverage (Chomi, Mujinja, Enemark, Hansen, & Kiwara, Citation2014). Such pre-payment mechanisms could provide an important avenue for policy makers to complement efforts to reduce poverty with programmes to limit vulnerability of agricultural households. The Government of Kenya is making plans to implement a social health insurance programme by transforming the NHIF into a universal health coverage programme (Kimani, Ettarh, Warren, & Bellows, Citation2014). In March 2014 the NHIF announced an extension of insurance cover to cater for Kenyans working in the informal sector (Meso, Citation2014). However, the effectiveness of health insurance mechanisms is heavily debated (Gustafsson-Wright, Janssens, & van der Gaag, Citation2011), the enrolment rates for health insurance schemes differ widely across SSA (Garrett, Chowdhury, & Pablos-Mendez, Citation2009) and operational difficulties in the introduction of health insurance schemes in many LICs hamper their successful development (De Allegri et al., Citation2009). Even for the often heavily subsidised schemes, enrolment rates remain low (Banerjee & Duflo, Citation2011); for community based health insurance schemes the literature consequently reports rates between 1% and 10% (De Allegri et al., Citation2009). While 89% of the respondents in our study area who claim to know what health insurance is confirm that health insurance would be useful for their family, the enrolment rate among dairy farmers in this area three years after introduction of the health insurance scheme from the Dutch HIF remains low at 11.5% (Langedijk-Wilms & Teuling den, Citation2014) (for more information on the scheme see Van der Gaag et al., Citation2011).

One of the potential explanations for the limited health insurance enrolment lies in the multitude of shocks that these agricultural households face. Even though illness and injury proved to be on average the most prevalent shock, households were also frequently confronted with a range of other shocks. For a household with limited resources it might therefore be impossible to reserve a share of their limited resources to the protection of health shocks through premium payments for a health insurance. When the health insurance premium is relatively high, paying these costs implies that these resources can no longer be used to protect consumption in case of occurrence of other shocks like crop diseases or increases in agricultural input prices. In other words households need more flexible risk management devices that need to work for several types of risk simultaneously.

Other explanations for the limited enrolment could lie in a miscalculation of the return from the health insurance or liquidity constraints when households are requested to pay an annual premium upfront. In addition to these demand side challenges, respondents also perceived supply side shortcomings in the Kenyan health-care sector as apparent from the one third of foregone care cases attributed to low quality of care and unavailability of drugs. These shortcomings on the health-care supply side could also make investment in a health insurance less attractive.

The question that remains now is whether there are policy options other than health insurance schemes to protect agricultural households against the financial consequences of ill health. Given the multitude of shocks that these agricultural households face, savings through formal or informal mechanisms not tied to specific shocks, might be an important avenue to protect consumption in case of competing adverse events. Gertler, Levine, and Moretti (Citation2009) showed that, in Indonesia, access to microfinance and lending programmes helps households self-insure their consumption in case of unexpected illness. Indonesian families faced with a health shock who lived far from a financial institution suffered greater losses in consumption than families living nearer the institutions. Other more general financial safety net mechanisms preventing households from depleting important income generating assets can also play an important role in protecting households against the consequences of ill health. Policies could also aim to reduce the riskiness of the environment, for example through improving preventive care, regulating prices of agriculture products or introducing risk-reducing technologies in agriculture (e.g. vaccination of livestock and irrigation systems).

Limitations and further research

In interpreting the results it is important to recognise the limitations of this study. First, the inability to estimate causal effects derives from the lack of control for reverse causality between income and occurrence of shocks. We try to overcome this problem by using consumption instead of assets ownership as a measure of income since selling assets is often used as coping strategy. However, this is not likely to completely solve the problem because reducing consumption is also known to be an important coping mechanism. Second, there is a possible socio-economic reporting bias in self-reported information about the frequency and impact of specific shocks. Such heterogeneity across socio-economic groups has been documented in health status reporting: given the same objective health, respondents with different socio-economic backgrounds tend to report differently on their health because they have less information, lower health expectations and possibly different frames of reference (Bago d`Uva, Van Doorslaer, Lindeboom, & ÒDonnell, Citation2008; Bonfrer, van de Poel, Grimm, & Van Doorslaer, Citation2014; Lindeboom & Van Doorslaer, Citation2004; Salomon et al., Citation2003). Little is known about reporting bias related to specific shocks but it is possible that a similar underreporting by the poor is present in our study. This implies that we might underestimate the impact of shocks on poorer households.

Notwithstanding these limitations, our study suggests that health shocks are an important risk to households and that effective pre-payment mechanisms are needed to protect households against the financial consequences of ill health. However, such mechanisms have to take into account the competing risks that agricultural households face, which make it difficult to reserve a share of their limited resources to the protection of health shocks through premium payments for a health insurance.

The findings from this study also have relevance for other SSA countries with similarly limited formal insurance and considerable reliance on agriculture as income generating source. Further research is necessary to establish whether the most effective protection against the consequences of ill health can be provided through health insurance, saving mechanisms or more general financial safety net mechanisms, and how these can best be implemented.

Disclosure statement

No potential conflict of interest was reported by the authors.

Supplemental file

Download PDF (106.4 KB)Additional information

Funding

Related Research Data

References

- Abiola, S. E., Gonzales, R., Blendon, R. J., & Benson, J. (2011). Survey in sub-Saharan Africa shows substantial support for government efforts to improve health services. Health Affairs, 30(8), 1478–1487. doi:10.1377/hlthaff.2010.1055

- Asfaw, A., & von Braun, J. (2004). Is consumption insured against illness? Evidence on vulnerability of households to health shocks in rural Ethiopia. Economic Development and Cultural Change, 53(1), 115–129.

- Bago d`Uva, T., Van Doorslaer, E., Lindeboom, M., & ÒDonnell, O. (2008). Does reporting heterogeneity bias the measurement of health disparities? Health Economics, 17, 351–375.

- Banerjee, A., & Duflo, E. (2011). Poor economics. New York: PublicAffairs.

- Bonfrer, I., van de Poel, E., Grimm, M., & Van Doorslaer, E. (2014). Does the distribution of healthcare utilization match needs in Africa? Health Policy and Planning, 29(7), 921–937. doi:10.1093/heapol/czt074

- Cappellari, L., & Jenkins, S. (2003). Multivariate probit regression using simulated maximum likelihood. The Stata Journal, 3(3), 278–294.

- Chomi, E. N., Mujinja, P. G., Enemark, U., Hansen, K., & Kiwara, A. D. (2014). Health care seeking behaviour and utilisation in a multiple health insurance system: Does insurance affiliation matter? International Journal for Equity in Health, 13, 25-9276-13-25. doi:10.1186/1475-9276-13-25

- Chuma, J., Gilson, L., & Molyneux, C. (2007). Treatment-seeking behaviour, cost burdens and coping strategies among rural and urban households in Coastal Kenya: An equity analysis. Tropical Medicine and International Health, 12(5), 673–686. doi:10.1111/j.1365.3156.2007.01825.x

- Cohen, J. (1988). Statistical power analysis for the behavioral sciences (2nd ed.). Hillsdale, NJ: Lawrence Erlbaum Associates.

- Damme, W. V., Leemput, L. V., Por, I., Hardeman, W., & Meessen, B. (2004). Out-of-pocket health expenditure and debt in poor households: Evidence from Cambodia. Tropical Medicine & International Health, 9(2), 273–280. doi:10.1046/j.1365-3156.2003.01194.x

- De Allegri, M., Sauerborn, R., Kouyaté, B., & Flessa, S. (2009). Community health insurance in sub-Saharan Africa: What operational difficulties hamper its successful development? Tropical Medicine & International Health, 14(5), 586–596. doi:10.1111/j.1365-3156.2009.02262.x

- de-Graft Aikins, A., Unwin, N., Agyemang, C., Allotey, P., Campbell, C., & Arhinful, D. (2010). Tackling Africa's chronic disease burden: From the local to the global. Globalization and Health, 6(5), 1–7.

- Dercon, S., Hoddinott, J., & Woldehanna, T. (2005). Consumption and shocks in 15 Ethiopian villages, 1999–2004. Journal of African Economies, 14, 559–585.

- Duryea, S., Lam, D., & Levison, D. (2007). Effects of economic shocks on children's employment and schooling in Brazil. Journal of Development Economics, 84(1), 188–214. doi:10.1016/j.jdeveco.2006.11.004

- Erreygers, G. (2009). Correcting the concentration index. Journal of Health Economics, 28(2), 504–515.

- European report on development. (2010). Social protection for inclusive development. Brussels: European Communities.

- Flores, G., Krishnakumar, J., O'Donnell, O., & van Doorslaer, E. (2008). Coping with health-care costs: Implications for the measurement of catastrophic expenditures and poverty. Health Economics, 17(12), 1393–1412. doi:10.1002/hec.1338

- Garrett, L., Chowdhury, A. M. R., & Pablos-Mendez, A. (2009). All for universal health coverage. Lancet, 374(9697), 1294–1299. doi:10.1016/S0140-6736(09)61503-8

- Gertler, P., & Gruber, J. (2002). Insuring consumption against illness. American Economic Review, 92(1), 51–70.

- Gertler, P., Levine, D. I., & Moretti, E. (2009). Do microfinance programs help families insure consumption against illness? Health Economics, 18(3), 257–273. doi:10.1002/hec.1372

- Government of the Republic of Kenya. (2007). Kenya vision 2030 the popular version. Nairobi: Government of Kenya.

- Grimm, M. (2010). Mortality shocks and survivors’ consumption growth. Oxford Bulletin of Economics and Statistics, 72(2), 146–171. doi:10.1111/j.1468-0084.2009.00566.x

- Grimm, M., Hartwig, R., & Lay, J. (2011). Investment decisions of small entrepreneurs in a context of strong sharing norms. Conference University of Twente. Retrieved from https://www.utwente.nl/igs/research/conferences/2012/microinsurance/Full%20papers%20and%20presentations/Full%20papers%201B/Grimm_full%20paper%20Session_1b.pdf

- Gustafsson-Wright, E., Janssens, W., & van der Gaag, J. (2011). The inequitable impact of health shocks on the uninsured in Namibia. Health Policy and Planning, 26(2), 142–156. doi:10.1093/heapol/czq029

- Health Insurance Fund. (2011). Launch of the Tanykina community healthcare plan in Kenya. Retrieved from http://hifund.org/index.php?mact=News,cntnt01,detail,0&cntnt01articleid=92&cntnt01returnid=94

- Health Insurance Fund. (2015). About us. Retrieved from http://hifund.org/index.php?page=about-us

- Heltberg, R., & Lund, N. (2009). Shocks, coping, and outcomes for Pakistan's poor: Health risks predominate. Journal of Development Studies, 45(6), 889–910. doi:10.1080/00220380902802214

- Heltberg, R., Oviedo, A. M., & Talukdar, F. (2013). What are the sources of risk and how do people cope? Insights from household surveys in 16 countries. World Development Report Background Paper. The World Bank.

- International Labour Organization. (2013). Health microinsurance schemes, Kenya. Retrieved from http://www.ilo.org/dyn/ilossi/ssimain.viewScheme?p_lang=en&p_scheme_id=3126&p_geoaid=404

- Joint Learning Network for universal health coverage. (2014). Kenya: National Hospital Insurance Fund (NHIF). Retrieved from http://www.jointlearningnetwork.org/content/national-hospital-insurance-fund-nhif

- Jones, A., Rice, N., Bago d`Uva, T., & Balia, S. (2007). Applied health economics. London: Routledge Taylor & Francis group.

- Kenjiro, Y. (2005). Why illness causes more serious economic damage than crop failure in rural Cambodia. Development and Change, 36(4), 759–783. doi:10.1111/j.0012-155X.2005.00433.x

- Kimani, J. K., Ettarh, R., Warren, C., & Bellows, B. (2014). Determinants of health insurance ownership among women in Kenya: Evidence from the 2008–09 Kenya demographic and health survey. International Journal for Equity in Health, 13(1), 27-9276-13-27. doi:10.1186/1475-9276-13-27

- Langedijk-Wilms, A., & Teuling den, J. (2014). Personal communication by Bonfrer, I. with PharmAccess about current enrollment rates in the Tanykina community healthcare plan. Amsterdam: PharmAccess.

- Leive, A., & Xu, K. (2008). Coping with out-of-pocket health payments: Empirical evidence from 15 African countries. Bulletin of the World Health Organization, 86(11), 849–856.

- Lelbren Dairies Limited. (2011). Personal communication by Bonfrer, I. with Lelbren dairies management board. Lessos: Kenya.

- Lindeboom, M., & Van Doorslaer, E. (2004). Cut-point shift and index shift in self-reported health. Journal of Health Economics, 23, 1083–1099.

- Lindelow, M., & Wagstaff, A. (2005). Health shocks in china: Are the poor and uninsured less protected? World Bank Policy Research Working Paper, 3740, 1–25.

- Mathauer, I., Schmidt, J., & Wenyaa, M. (2008). Extending social health insurance to the informal sector in Kenya. An assessment of factors affecting demand. International Journal of Health Planning and Management, 23(1), 51–68. doi:10.1002/hpm.914

- McIntyre, D., Thiede, M., Dahlgren, G., & Whitehead, M. (2006). What are the economic consequences for households of illness and of paying for health care in low- and middle-income country contexts? Social Science & Medicine, 62(4), 858–865. doi:10.1016/j.socscimed.2005.07.001

- Mebratie, A., Van de Poel, E., Yilma, Z., Abebaw, D., Alemu, A., & Bedi, A. (2015). Healthcare-seeking behaviour in rural Ethiopia: Evidence from clinical vignettes. BMJ Open, 4, 1–12.

- Meso, I. (2014, March 18). NHIF launches health cover for informal sector. The Standard Digital News, pp. 1–1.

- Morduch, J. (1995). Income smoothing and consumption smoothing. Journal of Economic Perspectives, 9(3), 103–114.

- National Hospital Insurance Fund. (2014). NHIF. Retrieved from http://www.nhif.or.ke/healthinsurance/

- Nikoloski, Z. & Ajwad, M. I. (2013). Do economic crises lead to health and nutrition behavior responses? (Working Paper No. 6538). World Bank: Washington, DC.

- ÒDonnell, O., Van Doorslaer, E., Wagstaff, A., & Lindelow, M. (2008). Analyzing health equity using household survey data: A guide to techniques and their implementation. Washington, D.C.: The World Bank.

- PharmAccess Foundation. (2014). Health plan for Koisagat tea estate. Retrieved from http://www.pharmaccess.org/RunScript.asp?Page=413&p=ASP\Pg413.asp

- Pitt, M., & Rosenzweig, M. (1984). Agricultural prices, food consumption and the health and productivity of farmers. (No. 84). Minnesota: Economic Development Center University of Minnesota.

- Quintussi, M., Van de Poel, E., Panda, P., Rutten, F. (2015). Economic consequences of ill-health for households in northern rural India. BMC Health Services Research, 15(179), 1–11. doi 10.1186/212913-015-0833-0

- Salomon, J., Mathers, C., Chatterji, S., Sadana, R., Üstün, T., & Murray, C. (2003). Quantifying individual levels of health: Definitions, concepts, and measurement issues. In C. Murray, & D. Evans (Eds.), Health systems performance assessment: Debates, methods and empiricism (pp. 1–6). Geneva: World Health Organization.

- Sparrow, R., Van de Poel, E., Hadiwidjaja, G., Yumna, A., Warda, N., & Suryahadi, A. (2014). Coping with the economic consequences of ill health in Indonesia. Health Economics, 23(16), 719–728. doi:10.1002/hec.2945

- StataCorp LP. (2013). Stata power and sample-size reference manual. Texas: Stata Press.

- The World Bank. (2010). The world bank dataset Kenya. Retrieved from http://data.worldbank.org/country/kenya

- Tirivayi, N., Knowles, M., & Davis, B. (2013). The interaction between social protection and agriculture. Rome: Food and agriculture organization of the United Nations.

- Townsend, R. (1995). Consumption insurance: An evaluation of risk-bearing systems in low-income economies. The Journal of Economic Perspectives, 9, 83–102.

- United Nations. (2013). The millenium development goals report 2013. New York: United Nations.

- Van der Gaag, J., Lange, J., Schultsz, C., Heidenrijk, M., Gustafsson-Wright, E., Hendriks, M., … Duynhouwer, A. (2011). HIF supported health insurance projects in Kenya: Baseline report. Amsterdam: Amsterdam Institute for International Development.

- Van Doorslaer, E., O'Donnell, O., Rannan-Eliya, R. P., Somanathan, A., Adhikari, S. R., Garg, C. C., … Zhao, Y. (2006). Effect of payments for health care on poverty estimates in 11 countries in asia: An analysis of household survey data. The Lancet, 368(9544), 1357–1364.

- Wagstaff, A. (2008). Measuring financial protection in health. Policy Research Working Paper, 4554, 1–34.

- Wagstaff, A., & Lindelow, M. (2010). Are health shocks different? Evidence from a multi-shock survey in Laos. World Bank Policy Research Working Paper, 5335, 1–38.

- Wagstaff, A., & Van Doorslaer, E. (2000). Measuring and testing for inequity in the delivery of health care. The Journal of Human Resources, 35(4), 716–733.

- Whitehead, M., Dahlgren, G., & Evans, T. (2001). Equity and health sector reforms: Can low-income countries escape the medical poverty trap? [Abstract]. The Lancet, 358(9284), 833–836.

- World Bank. (2009). LSMS-ISA Survey for Uganda. Retrieved from http://siteresources.worldbank.org/INTLSMS/Resources/3358986-1181743055198/3877319-1328111100912/UNPS_HH.pdf

- World Bank. (2005). World development indicators. The World Bank.

- World Bank. (2014). World development report 2014: Risk and opportunity – Managing risk for development. Washington, DC: World Bank.

- Xu, K., Evans, D., Kawabata, K., Zeramdini, R., Klavus, J., & Murray, C. (2003). Household catastrophic health expenditure: A multicountry analysis. The Lancet, 362, 111–117.

- Yilma, Z., Mebratie, A., Sparrow, R., Abebaw, D., Dekker, M., Alemu, G., & Bedi, A. (2014). Coping with shocks in rural Ethiopia. The Journal of Development Studies, 50(7), 1009–1024.