Abstract

Drawing on secondary data, we examine the transposition of the Accounting Directive 2013 into UK GAAP with a specific focus on references to IFRS. The process involved consultation and regulatory impact assessment on the options in the Accounting Directive and proposed changes to accounting standards for non-publicly accountable entities. This led to an IFRS-based approach from 2016 with three tiers: EU-adopted IFRS for group listed companies and other publicly accountable entities, an adaptation of IFRS for SMEs for non-publicly accountable entities, and a simplified version for micro-entities incorporating the requirements of the Accounting Directive. This outcome is not surprising since the UK was one of the founding members of the original International Accounting Standards Committee and a strong proponent of little GAAP. Indeed, the UK’s former Financial Reporting Standard for Smaller Entities provided a model for the IFRS for SMEs. In the past, there were few references to IFRS by the UK’s enforcement and interpretation bodies. Today, guidance is taken from IFRS Interpretations Committee. We contribute to the literature by describing the main processes involved in implementing the Accounting Directive and the move to an IFRS-based approach in UK GAAP. Our analysis should be of interest to researchers and policymakers alike.

JEL Code:

1. Introduction

The purpose of our study is to provide an overview of the role and current status of IFRS in the regulatory framework for financial reporting in the UK as a result of the implementation of the Accounting Directive (2013/34/EU) in 2013. This updates and consolidates previous Directives for statutory annual accounts and reports into a single Accounting Directive that applies to all members of the European Union (EU). The context for the study is that, EU-adopted IFRS have been required for the consolidated financial statements of all European companies whose debt or equity securities trade in a regulated market since 2005. However, the European Commission’s Impact Assessment concluded that introducing the IFRS for SMES (first issued in 2009) would not appropriately serve the objectives of simplification and reduction of administrative burdens for non-publicly accountable entities. Therefore, it has not been adopted by the EU. Drawing on secondary data, we examine the main processes and procedures involved in the transposition of the Accounting Directive in UK GAAP, with a specific focus on references to IFRS.

2. Documents Internalising the Accounting Directive (Directive 2013/34/EU)

The regulatory framework for financial reporting by private companies in the UK contains two main elements: company law and accounting standards. Company law sets the general legal framework, while accounting standards provide detailed guidance. The UK’s Financial Reporting Council (FRC) is responsible for setting standards for financial reporting, auditing, and actuarial practice.

Company law is embodied in the Companies Act 2006 (CA 2006), which is updated via Statutory Instruments (SI). CA 2006 incorporates the requirements of the relevant Directives issued by the European Parliament and Council. It includes the requirement that reporting entities make their accounts available at a registry. The UK’s official Registrar of Companies operates under the name of Companies House, an executive agency of the Department for Business, Energy & Industrial Strategy (BEIS).Footnote1 Companies House has responsibility for incorporating and dissolving limited companies, examining and storing company information delivered under company law, and making that information available to the public.

The Accounting Directive introduces greater harmonisation of the small company regime across the EU and increased simplification, with the aim of reducing burdens on small companies and increasing comparability and consistency of financial reporting. It also includes options that allow Member States to adapt it in accordance with national accounting frameworks and traditions. Implementation was required by July 2015. This was achieved in the UK by The Companies, Partnerships and Groups (Accounts and Reports) Regulations 2015 (SI 2015/980), which amends the following components of UK company law:

CA 2006

The Small Companies and Groups (Accounts and Directors’ Report) Regulations 2008 (SI 2008/409)

The Large- and Medium-sized Companies and Groups (Accounts and Reports) Regulations 2008 (SI 2008/410)

3. The Legislative System: How the Accounting Directive Is Internalised in National Regulations

The process for internalising the Accounting Directive in UK regulations started in 2011 with the discussion paper, Simpler Reporting for the Smallest Businesses (BIS/FRC, Citation2011), which sought views from a wide range of stakeholders over a 12-week period. Building on this, a government consultation was launched entitled Simpler Financial Reporting for Micro-entities: The UK’s Proposal to Implement the ‘Micros Directive’ (BIS, Citation2013). In particular, small companies, limited liability partnerships, qualifying partnerships preparing their accounts in accordance with the Partnerships (Accounts) Regulations 2008, preparers, auditors, and users of statutory accounts, professional accountancy bodies, and intermediaries representing business organisations were encouraged to give their views. Responses were required within three weeks. The final consultation, UK Implementation of the EU Accounting Directive (BIS, Citation2014) took place over an eight-week period in 2014. The consultation document drew attention to changes that were mandatory and the proposed approach for new or established options. In January 2015, a response to the consultation was published (BIS, Citation2015a) followed by an impact assessment of the changes (BIS, Citation2015b).

The Companies, Partnerships and Groups (Accounts and Reports) Regulations 2015 (SI 2015/980) came into force on 6 April 2015 and is applicable for financial years commencing on or after 1 January 2016.Footnote2 According to Deloitte (Citation2015, p. 2), the main changes to UK legal requirements for accounts and audit were the following:

the option to file full disclosures of related undertakings, such as subsidiaries and other significant investments, in the annual return was abolished for accounts approved by directors on or after 1 July 2015, and all required disclosures must now be in the accounts;

disclosures for large and medium-sized companies about their subsidiaries and other significant investments are expanded to include the address of the registered office of all such entities, whether inside or outside the UK (small companies are exempt from any such disclosure);

auditors have new reporting responsibilities in relation to the directors’ report and strategic report;

the maximum useful life of goodwill and intangible assets in exceptional cases, where no reliable estimate of life is possible, is set at ten years;

small company accounting size limits are raised substantially. The new limits also apply to audit exemption (although early adoption is not permitted for this purpose);

the scope of small company exemptions is widened, meaning that some companies that were previously ineligible will become entitled to exemptions;

small company accounts disclosure requirements are simplified significantly;

abbreviated accounts are abolished, although small companies will be able to prepare ‘abridged’ accountsFootnote3 for shareholders and for filing at Companies House.Footnote4

Although most of the above changes relate to filing and disclosure requirements, it was necessary to amend the UK and Republic of Ireland accounting standards to ensure continued consistency between company law and the financial reporting framework. The FRC used this opportunity to reconsider the most appropriate way that accounting standards could support the new micro-entities regime (FRC, Citation2015). All previous national accounting standards were withdrawn, and since 1 January 2016, UK accounting standards have been based on EU-adopted IFRS or adapted from the IFRS for SMEs:

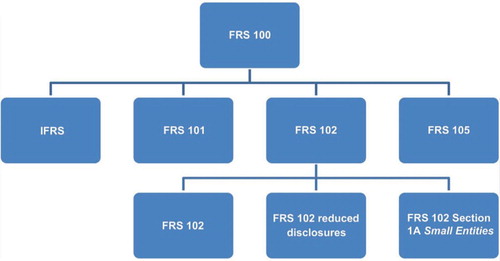

FRS 100, Application of Financial Reporting Requirements (2012) determines which reporting framework applies to which entities. Publicly listed group entities have been required to use EU-adopted IFRS since 2005, but may choose between IFRS and FRS 102 for the preparation of their individual parent accounts.

FRS 101, Reduced Disclosure Framework (2012) allows subsidiaries in a listed group to apply the same accounting as in the group accounts, but with fewer disclosures.

FRS 102, The Financial Reporting Standard Applicable in the UK and Republic of Ireland (2013) is based on the IFRS for SMEs with modifications. It has just over 300 pages and replaced over 70 accounting standards and UITF Abstracts spanning more than 2400 pages. FRS 102 can be used by any non-publicly accountable entity. Small entities may use Section 1A of FRS 102.

FRS 105, The Financial Reporting Standard applicable to the Micro-Entities Regime (2015) applies to micro-entities (as defined by CA 2006) that choose to apply the micro-entities regime introduced in UK company law in November 2013. The recognition and measurement requirements are based on FRS 102 with a number of significant simplifications, which are discussed in Section 7 of this paper. Micro-entities need only provide the minimum disclosures required by law.

It is important to emphasise that reporting entities can choose a higher level if they wish. summarises the effects of incorporating EU Directives in UK company law and the influence of IFRS since 1998.

Table 1. Key features of UK GAAP 1998–2016.

provides an overview of the new UK GAAP.

Figure 1. Overview of FRS 100, application of financial reporting requirements. Source: FRC (Citation2015, p. 4).

There are a number of advantages to the UK’s tiered approach (Collis, Holt, & Hussey, Citation2017). The main advantage is that the burden of compliance is reduced by applying the principle of proportionality. In addition, the IFRS-based approach throughout the tiers should aid transition for entities moving between categories. Entities in the lower tiers can use the regime for a higher tier if they wish (for example, if they are close to the threshold or planning an IPO). As all three tiers are IFRS-based, the approach also provides a high level of consistency for preparers, auditors, and users. However, one disadvantage is that international comparability is slightly impaired in respect of entities using FRS 102 and FRS 105.

Since 2004, the UK has contributed to EU harmonisation by adopting the EU maximum thresholds to determine the size of private companies in CA 2006, including the raised thresholds in the Accounting Directive 2013. From 1 January 2016, unless the entity is excluded for reasons of public interest,Footnote5 it will generally qualify for a particular size category in the UK if it meets two or more of three criteria shown in its first year. In a subsequent financial year, the entity must qualify or satisfy the size tests in that year and the preceding year.

Table 2. Size thresholds for accounting and auditing in the UK from 2016.

4. References to IFRS in UK Legislators’ Remarks to Draft Bill

Although UK accounting standards are now based on EU-adopted IFRS or adaptations of the IFRS for SMEs, there is no reference to any specific IFRS in The Companies, Partnerships and Groups (Accounts and Reports) Regulations 2015 (SI 2015/980).

Accounting and auditing standards provide detailed guidance to preparers, auditors, and users of the financial statements, but the general requirements for accounting and auditing stem from company law. The true and fair principle is an overriding requirement of UK and EU law. Section 393 of CA 2006 requires that the directors of a company must not approve accounts unless they are satisfied they give a true and fair view of the assets, liabilities, financial position, and profit or loss of the entity.

In the vast majority of cases a true and fair view will be achieved by compliance with accounting standards and by additional disclosure to fully explain an issue. However, where compliance with an accounting standard would result in accounts being so misleading that they would conflict with the objectives of financial statements, the standard should be overridden. (FRC, Citation2014, p. 1)

Disagreement with a particular standard does not provide grounds for departure. ‘Almost all true and fair overrides in the past were of law rather than of a standard’ (FRC, Citation2011, p. 3).

The micro-entities regime under FRS 105 requires very limited disclosure. Nevertheless, micro-entity accounts that comply with the minimal legal requirements are presumed to give a true and fair view, and there is no requirement for directors to consider what additional information may be needed in order for the accounts to give a true and fair view (FRC, Citation2015).

5. References to IFRS by Enforcement and Interpretation Bodies

In addition to its standard-setting responsibilities, the FRC is the independent disciplinary body for the accountancy and actuarial professions. It is also the competent authority for audit in the UK under new legislation which came into force following the EU Audit Regulation and Directive. The FRC’s Conduct Committee has oversight over the operation of the disciplinary arrangements and is supported by the Monitoring and the Case Management committees together with the Financial Reporting Review Panel and Tribunals. The responsibilities of the Conduct Committee include investigating cases that raise or appear to raise important issues affecting the public interest in the UK, and bringing disciplinary proceedings against those whose conduct appears to have fallen short of the standard reasonably expected of individual or firm members of the relevant professional body. All other cases of potential misconduct continue to be dealt with by the professional bodies.

A disciplinary investigation can be started in two ways. The professional bodies can refer cases to the FRC or the FRC may decide to investigate a matter of its own accord. There are 12 disciplinary tribunal reports on the FRC website.Footnote6 Four of them (Cattles, Emerging Business Trust, iSoft, and Torex) have some connection to accounting standards. However, the issues were not about whether a particular treatment was appropriate, but about whether sufficient evidence had been gathered by the auditor and/or whether the measurements and/or disclosures were fraudulent. Only one case (Cattles) mentions IFRS. It is not surprising that FRC tribunals rarely mention IFRS because they are more concerned with fraud and unprofessional conduct.

Another way in which IFRS could influence UK accounting standards is through the work of the former Urgent Issues Task Force (UITF), which attempted to resolve reporting issues arising from the divergent interpretations of accounting standards. UITF consensuses were published in the form of Abstracts, with the first being issued in 1991. UITF Abstracts 1–38 were issued prior to 2005 and Abstracts 39–48 were issued during the period 2005–2012. Compliance with UITF Abstracts was deemed necessary (other than in exceptional circumstances) in accounts that claim to give a true and fair view. The extent to which UITF Abstracts referred to IFRS is summarised in .

Table 3. Analysis of UITF abstracts.

There are two key aspects to the analysis in . First, 17 of the UITF Abstracts refer to IFRS or are associated with the IFRS Interpretations Committee. These include six Abstracts that were issued prior to 2005 (the date when IFRS became compulsory for UK listed companies). Second, three of the early Abstracts refer to US standards with no reference to IFRS. The table indicates that the UK’s UITF was at the cutting edge of reporting issues: often outward looking and taking guidance from good practice elsewhere.

In 2012, the UITF was disbanded as a result of FRC reforms. Since then, guidance on widespread accounting issues that have arisen from IFRS has been provided by the IFRS Interpretations Committee (IFRIC). IFRIC interpretations are subject to approval by the International Accounting Standards Board (IASB) and have the same authority as a standard issued by the IASB.

6. Stakeholders’ Positions on IFRS

Following the final consultation on UK Implementation of the EU Accounting Directive (BIS, Citation2014), 33 comment letters or emails were received (see https://www.gov.uk/government/consultations/eu-accounting-directive-smaller-companies-reporting). In addition to written comments, the policy was informed by discussions with an expert working group comprising senior representatives from the accountancy and audit sector. There is only one paragraph in the government’s response to the consultation (BIS, Citation2015a) that mentions IFRS. As the following extract shows, it relates to the formats for the financial statements.

Amongst those who expressed an opinion there was strong majority support for increased flexibility in the customisation of the profit and loss account and balance sheet. However, some expressed reservations saying that departures from the specific formats should be delegated to the Financial Reporting Council to approve to control diversity. There was also concern about whether this option would fully permit the use of IFRS formats. To quote one respondent, “We consider that the Government should work towards a solution that allows companies applying FRS 101 to prepare accounts with the same formats as used under EU-adopted IFRS in order to alleviate potential incomparability. The status quo is currently unsatisfactory as format and measurement changes are required from EU-adopted IFRS used for group reporting to the UK GAAP compatible Companies Act formats and measurements when presenting single entity financial statements under FRS 101”. Another respondent stressed the importance of making comparisons between different sets of accounts. (BIS, Citation2015a, p. 21)

7. Differences Between IFRS and UK Accounting Standards

Group entities with a listing on the London Stock Exchange have been required to prepare their consolidated accounts using EU-adopted IFRS since 2005, and these IFRS are permitted for single entity listed companies and private companies (IFRS Foundation, Citation2016). In 2009, when the IFRS for SMEs was issued, the FRC published a consultation paper on the Future of UK GAAP (ASB, Citation2009), which proposed that it would form the basis for UK GAAP for private companies. A total of 155 responses were received by February 2010. There was then a delay while UK regulators waited for the new Accounting Directive to be finalised. The following analysis by the European Financial Reporting Advisory Group identifies where the IFRS for SMEs is incompatible with the Accounting Directive (EFRAG, Citation2010, p. 2):

The prohibition to present or describe any items of income and expense as “extraordinary items” in the statement of comprehensive income (or in the income statement, if presented) or in the notes (IFRS for SMEs par. 5.10) (see Appendix par. 3–6).

The requirement to measure financial instruments within the scope of section 12 of the IFRS for SMEs (non-basic financial instruments) at fair value (IFRS for SMEs par. 12.7 and 12.8) (see Appendix par. 7–16). (Par. 11.2 IFRS for SMEs includes an option for entities to choose to apply the recognition and measurement provisions of IAS 39 Financial Instruments: Recognition and Measurement. As the option does not refer to a specific version of IAS 39, EFRAG has not been able to assess whether this option would be compatible with the EU Accounting Directives or not. Accordingly, EFRAG has disregarded the option when assessing whether or not the requirements of the IFRS for SMEs regarding financial instruments are compatible with the EU Accounting Directives or not).

The requirement to measure associates for which there is a published price quotation using the fair value model (IFRS for SMEs par. 14.7 and 14.10) (see Appendix par. 17–29).

The requirement to measure investments in jointly controlled entities for which there is a published price quotation using the fair value model (IFRS for SMEs par. 15.12 and 15.15) (see Appendix par. 17–29).

The requirement to presume the useful life of goodwill to be ten years if an entity is unable to make a reliable estimate of the useful life (IFRS for SMEs par. 19.23) (see Appendix par. 30–34).Footnote7

The requirement to recognise immediately in profit or loss any negative goodwill (IFRS for SMEs par. 19.24) (see Appendix par. 35–37).Footnote8

The prohibition to reverse an impairment loss recognised for goodwill (IFRS for SMEs par. 27.28) (see Appendix par. 38–42).

Added an option to Section 17 to revalue property, plant and equipment and, similarly, to Section 18 to revalue certain intangible assets.

Added an option to Section 18 to capitalise development costs when specified criteria are met.

Changed the presumption in Section 18 of a ten-year useful life for amortisable intangible assets, including goodwill, when a reliable estimate cannot be made to amortisation over not more than five years.

Added an option in Section to capitalise borrowing costs on qualifying assets.

Require merger accounting (pooling) for combinations of entities under common control.

Non-cash distributions to owners do not have to be measured at fair value.

Added an accrual accounting option for government grants.

Require a timing difference approach to deferred income taxes, rather than a temporary difference approach.

Permit the historical cost model for all biological assets.

Made numerous other changes to permit accounting treatments that exist in FRS at the transition date that align with IFRS Standard as adopted by the EU.

summarises the main differences between old UK GAAP and FRS 102 as amended in 2015, and between EU-adopted IFRS (the highest of the three tiers of UK GAAP) and FRS 102 as amended in 2015.

Table 4. Key differences between FRS 102 and FRS 105.

summarises the main differences between FRS 102 and FRS 105 (the lowest of the three tiers in UK GAAP).

Table 5. Key differences between old UK GAAP and FRS 102, and between EU-adopted IFRS and FRS 102.

8. Conclusions

Drawing on secondary data, we have examined the main processes and procedures involved in the transposition of the Accounting Directive 2013 in UK GAAP with a specific focus on references to IFRS. The challenge faced by policymakers in the UK has been how best to implement the Accounting Directive and reduce regulatory burdens whilst maintaining confidence in the integrity of the UK’s established financial reporting frameworks. A number of national consultations were conducted on the options in the Accounting Directive and the proposed changes to UK accounting standards applicable to non-publicly accountable entities, followed by regulatory impact assessment. This led to an IFRS-based approach in the UK from 2016 with three tiers: EU-adopted IFRS for group listed companies and other publicly accountable entities (with FRS 101 offering reduced disclosure for subsidiaries of group listed companies); an adaptation of the IFRS for SMEs for non-publicly accountable entities (FRS 102); and a simplified version of FRS 102 for micro-entities incorporating the requirements of the Accounting Directive (FRS 105). Entities are at liberty to choose a higher tier if they wish.

In the past, there were few references to IFRS by the UK’s former enforcement and interpretation bodies. However, it is of interest that the former UITF was influenced by IFRS even before 2005, and there is also evidence of the influence of US standards. Today, the UK takes guidance from IFRIC on widespread accounting issues arising from IFRS.

It is no surprise that the UK has adopted an IFRS-based approach, as the UK was one of the founding members of the International Accounting Standards Committee (IASC), which was established in London in 1973 through an agreement made by professional accountancy bodies from Australia, Canada, France, Germany, Japan, Mexico, the Netherlands, the UK and Ireland, and the USA. The UK continued its involvement when the IASC was replaced by the IASB in 2001, which was set up with an independent oversight organisation now known as the IFRS Foundation. The UK has also been a strong proponent of little GAAP, as evidenced by the adoption of the maxima EU size thresholds since 2004 and the development of the Financial Reporting Standard for Smaller Entities (FRSSE), which was in use from 1998 to 2015. The FRSSE provided a model for the IASB when designing the IFRS for SMEs in 2009 and both have contributed to FRS 102 and FRS 105 in the UK.

Acknowledgements

The authors are grateful to the anonymous reviewers for their helpful comments.

Disclosure Statement

No potential conflict of interest was reported by the author(s).

Notes

1 Formerly, the Department for Business, Innovation and Skills (BIS).

2 Earlier voluntary adoption was also permitted.

3 This is the term used in the legislation for the new shortened form of accounts for small companies.

4 If agreed by the shareholders, single entity small companies can prepare an abridged profit and loss account or an abridged balance sheet, or both.

5 Under the Companies Act 2006, ‘an entity is excluded from the small companies regime if it is a public company, a company that is an authorised insurance company, a banking company, an e-money issuer, an ISD investment firm or a UCITS management company, or carries on insurance market activity, or is a member of an ineligible group’ (c. 46, Part 15, Chapter 1, p. 178).

7 The Accounting Directive presumes a life of five years under these circumstances.

8 This is prohibited by the Accounting Directive.

References

- Accountancy. (2015). FRS 105 rules for micros. November, p. 67.

- ASB. (2009). The Future of UK GAAP, Accounting Standards Board. Retrieved January 9, 2017, from https://www.frc.org.uk/Our-Work/Publications/ASB/Consultation-Paper-Policy-Proposal-The-Future-of-U-File.pdf

- BIS. (2013). Simpler Financial Reporting for Micro-Entities: The UK’s Proposal to Implement the ‘Micros Directive’. Consultation Document, February. Retrieved August 28, 2016, from https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/237045/bis-13-1124-simpler-financial-reporting-for-micro-entities.pdf

- BIS. (2014). UK implementation of the EU Accounting Directive. Consultation Document, August. Retrieved August 28, 2016, from https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/350864/bis-14-1025-implemention-of-eu-accounting-directive-chapters-1-to-9-consultation.pdf

- BIS. (2015a). UK implementation of chapters 1–9 of the EU Accounting Directive. January. Retrieved August 28, 2016, from https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/398885/bis-15-36-uk-implementation-of-chapters-1-9-of-the-eu-accounting-directive-government-response-to-the-consultation2-final.pdf

- BIS. (2015b). UK implementation of the EU Accounting Directive: Chapters 1-9: Annual financial statements, consolidated financial statements, related reports of certain types of undertakings and general requirements for audit. Impact Assessment No. BISBE113. Retrieved August 28, 2016, from https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/446443/bis-15-279-eu-accounting-directive-chapters-1-to-9-final-stage-impact-assessment.pdf

- BIS/FRC. (2011). Simpler Reporting for the Smallest Businesses (Discussion Paper), August. Retrieved August 28, 2016, from https://www.gov.uk/government/uploads/system/uploads/attachment_data/file/31701/11-1100x-simpler-reporting-for-smallest-businesses-discussion-paper.pdf

- Collis, J., Holt, A., and Hussey, R. (2017). Business accounting (3rd ed.). London: Palgrave Macmillan.

- Companies House. (2016) Changes to accounting standards and regulations, 29 February. Retrieved June 30, 2016, from https://companieshouse.blog.gov.uk/2016/02/29/changes-to-accounting-standards-and-regulations/

- Deloitte. (2015). A closer look – UK Implementation of the EU Accounting Directive. Retrieved August 28, 2016, from http://www.iasplus.com/en-gb/publications/uk/closer-look/a-closer-look-uk-implementation-of-the-eu-accounting-directive

- EFRAG. (2010). Advice on compatibility of the IFRS for SMEs and the EU Accounting Directives. Draft letter to the European Commission. Retrieved August 28, 2016, from http://www.efrag.org/Assets/Download?assetUrl=%2Fsites%2Fwebpublishing%2FProject%20Documents%2F172%2FDraft%20letter%20to%20European%20Commission.pdf

- FRC. (n.d.). UITF and FRC Abstracts. Retrieved December 14, 2016, from https://www.frc.org.uk/About-the-FRC/FRC-structure/Corporate-Reporting-Council/Committees-and-work-streams/Urgent-Issues-Task-Force/UITF-UITF-and-FRC-abstracts.aspx

- FRC. (2011). True and Fair, July. Retrieved January 1, 2017, from https://www.frc.org.uk/FRC-Documents/FRC/Paper-True-and-Fair.aspx

- FRC. (2014). FRC publishes ‘True and Fair’ statement. PN 33/14, 4 June. Retrieved August 28, 2016, from https://www.frc.org.uk/News-and-Events/FRC-Press/Press/2014/June/FRC-publishes-%E2%80%98True-and-Fair%E2%80%99-statement.aspx

- FRC. (2015). Overview of the financial reporting framework, July, London: Financial Reporting Council. Retrieved January 9, 2017, from https://www.frc.org.uk/Our-Work/Publications/Accounting-and-Reporting-Policy/Overview-of-the-financial-reporting-framework.pdf

- IFRS Foundation. (2016). IFRS Application Around the World, Jurisdictional Profile: United Kingdom. Retrieved January 9, 2017, from http://www.ifrs.org/Use-around-the-world/Documents/Jurisdiction-profiles/United-Kingdom-IFRS-Profile.pdf

- PWC. (2015). Summary of key differences between old UK GAAP, new UK GAAP (FRS 102) and IFRS, 16 October. Retrieved January 1, 2017, from https://inform.pwc.com/inform2/show?action=informContent&id=1317233404103278