ABSTRACT

Alternative performance measures (APMs) may increase uncertainty and perceived risks concerning the audit, and rouse the auditor’s professional skepticism (PS), for example in case the APMs and official reporting diverge (e.g. one shows a profit and the other a loss). In this paper, using a survey of Finnish certified public auditors (N = 220), we study how auditors perceive relationships between audit work, PS, and APMs. When examining PS, we use both personal ‘trait skepticism’ and case-specific ‘state skepticism’. Our results show that state skepticism related to APMs can explain skeptical behavior and that it is a separate component from trait skepticism. Both state skepticism and considerations of the usefulness of APMs are helpful in assessing audit evidence and accounting figures. Further, we find that auditors hold various views of APMs and that ‘search for knowledge’ and ‘questioning mind’ are key dimensions of PS in coping with APMs.

1. Introduction

The Conceptual Framework for Financial Reporting (IASB, Citation2018, p. 1.6) states that in addition to the financial statements, investors, and lenders need other information to make economic decisions. Such information may include considerations of economic conditions and company outlooks, and alternative performance measures (APMs). There are several alternative reporting practices, such as ‘non-IFRS’ or ‘non-GAAP’ profit and loss statements, ‘pro forma’ performance measures, and financial ratios that are calculated in an alternative way. At the same time, IFRS financial statements should deliver relevant, comparable, verifiable, timely, and understandable information (IASB, Citation2018). Consequently, reporting ‘non-IFRS’ metrics or APMs in general might contradict these aims and may call for additional attention or skepticism from the auditor (see, e.g. Becker et al., Citation1998; ISA Citation200, Citation2009; Nelson, Citation2009).

While companies have been using APMs in investor communications for a long time (Herr et al., Citation2022), their value in financial reporting is debated. Whereas APMs can improve the representation of the firm’s core performance (Black et al., Citation2021), the increasing use of alternative performance measures also poses challenges for users of financial statements (Ciesielski & Henry, Citation2017). Multiple APMs, or ‘alternative truths’, may increase uncertainty over what is a ‘true and fair view’ of the company performance.

APMs are a challenge to auditors because their task is to ensure that financial statements provide a true and fair view of the company (Healy & Palepu, Citation2001). While reporting APMs may be an effective way to give more information about a company to markets (Deloitte, Citation2016), their information can also be misleading. This is because alternative ways of representing financial information and performance indicators may include subjectivity and pose a threat to the true and fair view conveyed by the financial statements. Potentially worrying issues emerge if APMs influence the market actors too much (see Andersson & Hellman, Citation2007) and if investors rely too much on pro forma information (Allee et al., Citation2007).

In the global perspective, national accounting standards vary in their relationship between APMs and auditing: sometimes APMs are audited and sometimes they are not. In the US, for example, APMs are not usually audited, because they are traditionally reported outside financial statements (Black & Christensen, Citation2018). However, auditors are still responsible for APMs because audited statements should be in line with other financial information that is disclosed (Black & Christensen, Citation2018). In Germany, on the other hand, the management report is audited and APMs are usually presented in it (Jana & McMeeking, Citation2021).

Given the incongruous regulatory approaches to the auditing of alternative reporting, research into auditors’ reactions to APMs in audit work is relatively scarce. Chen et al. (Citation2012) find that compared with GAAP reporting, optimistic pro forma measures increase audit fees and the probability of resignation. APMs suggest therefore additional work or risks from the perspective of the auditor. Moreover, alternative performance reporting can lower audit quality (Hallman et al., Citation2022), but high-quality auditors are associated with higher quality alternative reporting (Entwistle et al., Citation2012; Feng et al., Citation2023). The empirical evidence on how auditors respond to APMs relies however on archival data and thus there is little insight into how they perceive APMs in practice. Consequently, our first research question (RQ1) is: How do auditors perceive alternative performance measures in financial reporting?

When carrying out the audit, the auditor is expected to exercise professional skepticism (PS) when assessing financial statements (e.g. ISA Citation200, Citation2009; Nelson, Citation2009). PS manifests itself as auditor-specific trait skepticism, which involves sub-dimensions such as ‘questioning mind’ or ‘search for knowledge’, and as auditing task-specific state skepticism (see Hurtt, Citation2010; Nelson, Citation2009; Robinson et al., Citation2018). Trait skepticism is regarded as an antecedent of state skepticism which then may moderate skeptical action (Hurtt, Citation2010). In the auditing literature, a bulk of research into PS has focused on trait skepticism, whereas state skepticism has received less scholarly attention (Khan & Oczkowski, Citation2021). While the auditor’s traits and social characteristics could create a skeptical mindset (see Hurtt, Citation2010) available, PS requires situational assessment (Nolder & Kadous, Citation2018). Alternative financial information can be argued to form a situation in which appropriate skepticism is recommended (Ciesielski & Henry, Citation2017). Consequently, we develop a novel instrument to measure state skepticism and in a particular case of analyzing – and trusting – APM information. It has been noted however that situations can emerge where the auditor exercises trust which is not a part of PS (Glover & Prawitt, Citation2014), as the auditor encounters APMs. For this reason, we also devise an instrument that measures the auditor’s trust in APMs. Thus, our second research question (RQ2) is: How does professional skepticism explain skeptical behavior and trust related to APMs?

While both trait and state skepticism are recognized as components of PS, the relationship between the two is not clear. A review of the auditing literature suggests that there is no statistically significant correlation between state and trait skepticism (Khan & Oczkowski, Citation2021). Further, there is no research into how the two relate to each other in the case of APMs. As a result, our third research question (RQ3) asks: How is trait skepticism related to state skepticism in the case of APMs?

To answer our research questions, we examine a nation-wide survey of Finnish certified public auditors (N = 220). A survey-based methodology is a way to glean descriptive data from practitioner insights into previously unhypothesized relationships (Bloomfield et al., Citation2016). With our survey answers we expect to capture auditors’ views of APMs in a specific situation, i.e. in a case of showing a loss according to IFRS but a profit according to APMs, which can be a potential red flag relating to earnings management (see Becker et al., Citation1998). Thus, our study complements archival and experimental studies concerning APMs. Considering audit research methods, we develop a survey instrument to measure state skepticism, for which to date (to the best of our knowledge) there has not been an instrument offering insight into the auditor’s work. The data were analyzed with factor analyzes and structural equation modeling (SEM). Focusing on a single EU country with relatively homogenous auditor educational requirements (accounting education, see Sundgren, Citation1998) controls for cross-sectional variation between different institutional settings (see Hope et al., Citation2012; Jahn & Loy, Citation2023).

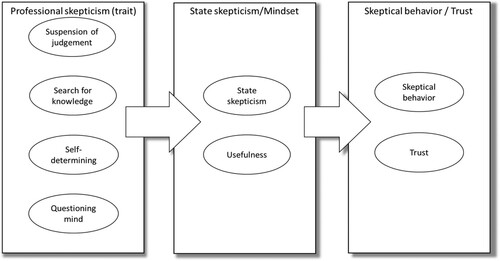

In order to analyze professional skepticism relating to APMs, we use the multidimensional measurement scale and the model of PS introduced by Hurtt (Citation2010). The Hurtt scale of PS is the predominant method for measuring and operationalizing professional trait skepticism (Khan & Oczkowski, Citation2021). The Hurtt (Citation2010) model proposes the idea that trait skepticism leads to state skepticism and to skeptical behavior (see our adaptation of the model in in Section 3.2). While the original Hurtt scale includes six dimensions, we follow Blix et al. (Citation2021) and use four subscales of PS: questioning mind, self-determining, search for knowledge, and suspension of judgement. Questioning mind and self-determining mean being critical and making up one’s own mind, whereas search for knowledge means being curious and wanting to learn new things, and finally suspension of judgment can be seen as applying careful consideration (see also in Section 4).

Figure 1. The conceptual model.

Table 1. Descriptive statistics and factor loadings for the professional (trait) skepticism.

This study makes several contributions to various streams of literature. First, we contribute theoretically to the auditing literature (Cohen et al., Citation2017; Hurtt, Citation2010; Robinson et al., Citation2018) by showing that state skepticism is a separate component of PS. Second, in comparison to the archival studies on APMs which rely on empirical proxies of auditors’ actions and judgements (e.g. Chen et al., Citation2012; Hallman et al., Citation2022), our paper uses a survey-based approach to examine how auditors perceive the use of APMs in a case situation and in relation to audit work. Third, this study contributes to the literature on PS (e.g. Hurtt, Citation2010; Nelson, Citation2009) by showing how trait and state skepticism relate to the auditor’s perceptions of APMs. Finally, we also add to this literature by including a novel instrument to measure state skepticism in the APM context.

This paper proceeds as follows. In Section 2, we discuss the conceptual background of professional skepticism research. In Section 3, we introduce the data and methodology. Section 4 reports the results and Section 5 the conclusions.

2. Background

The European Securities Markets Authority (ESMA) defines an APM as a financial measure of historical or future financial performance, financial position, or cash flows, other than a financial measure defined or specified in the applicable financial reporting framework (ESMA, Citation2015). ESMA (Citation2015, Citation2021) offers guidelines concerning the presentation of APMs. In addition, IOSCO (Citation2016) has published guidelines for non-GAAP measures. Since ESMA seeks to enhance investor protection and orderly financial markets, it emphasizes that guidelines should be taken seriously for enforcement purposes (ESMA, Citation2021). This suggests that alternative or adjusted presentations may be vulnerable to manipulative practices. Further, FRC (Citation2021) examined the quality of APM reporting in the UK and noted that high levels of APM usage may obscure relevant GAAP information. In their sample, 19 out of 20 companies reported more favorable adjusted results than GAAP results.

Some companies refer to APMs as ‘non-IFRS reporting’ or ‘adjusted reporting’ but these alternative ways of reporting may include subjective and asymmetrical information elements, potentially jeopardizing the classic accounting considerations of conservatism in reporting (e.g. Basu, Citation1997) and a fair presentation or the true and fair view (Evans, Citation2003; Hamilton & Ohogartaigh, Citation2009; Rautiainen et al., Citation2022; Walton, Citation1993). Yet offering both an official and an alternative view may be seen as providing additional information. Hence, while APMs may not be perceived as manipulation, the reader of the financial statement might be confused by them.

For a skeptical person, blurring the true and fair view can resemble manipulative practices and suggest problems in corporate governance or internal control, making the work of auditors more difficult – and risky (e.g. Bedard & Johnstone, Citation2004). Auditors often exhibit skepticism in their work, i.e. a ‘questioning mindset’, critical judgment, and search for knowledge (Cohen et al., Citation2017, p. 4), or an ‘attitude preceding skeptical behavior’, related to personal, task, and situational factors (Robinson et al., Citation2018, p. 215). There can be skepticism however stemming from the traits of the auditor (trait skepticism) and situational skepticism emerging from the state of affairs in the company and in the external environment referred to as ‘state skepticism’ (Cohen et al., Citation2017; Hurtt, Citation2010; Robinson et al., Citation2018).Footnote1

How APMs are presented may accentuate risks of auditing and forms of skepticism. For instance, in a situation where official figures indicate a decline in performance, managers could be tempted to remove some items and highlight APMs that show higher performance. Further, skepticism and risk perceptions may also affect auditors’ career outcomes (Cohen et al., Citation2017). As an example, auditors in Texas who assumed (presumptive doubt) that there was managerial dishonesty were less likely to remain within the auditing profession (Cohen et al., Citation2017).

Considering various alternative or optional reporting practices, pro forma statements present historical information adjusted as if transactions had occurred at a different time or under a different organizational structure. Bhattacharya et al. (Citation2003) regard reporting earnings figures on pro forma basis as a controversial practice. Further, Bhattacharya et al. (Citation2003) note that pro forma earnings exclude income statement items that managers have deemed to be nonrecurring or nonrepresentative, and so ‘pro forma announcers’ tend to be relatively young firms e.g. in the tech sector, and that they are ‘significantly less profitable, more liquid, and have higher debt levels’ than many other firms in their industries (p. 285). Bhattacharya et al. (Citation2003) also argue that firms exclude expenses in their pro forma earnings, but they usually do not exclude the same items in the next pro forma announcement (p. 285). This supports the view that pro forma statements are often motivated by a managerial desire to meet or beat analysts’ expectations. Alternative ways of reporting, such as the full ‘non-IFRS’ profit and loss statement presentation, may affect comparability and investor perceptions. For instance, management tends to place a greater emphasis on non-GAAP figures in earnings calls when those numbers show a higher performance or beat benchmarks (Henry et al., Citation2020). Here non-IFRS is not only pro forma or alternative indicator reporting but presents, for example, the whole profit and loss statement according to the company’s own accounting view of excluding extraordinary items and costs from organizational restructuration.

Additional presentation, such as subtotals of the profit and loss statement, may give better information about the company’s performance to investors, especially considering that the IFRS board too has planned alternative ways of presentation (IFRS ED, Citation2019). These alternative statements are not always clearly regulated or audited, however, and may thus pose a threat to conveying a true and fair view to investors in the possible case where the views provided by non-IFRS and IFRS reporting do not align. This practice suggests a possibility for incoherent presentations, and non-comparability and questions being raised about management’s motivation or governance (Ciesielski & Henry, Citation2017). Therefore, PS is needed to see through alternative numbers and analyze the information properly (ibid.), but it is not known how trait and state skepticism components of PS affect skeptical behavior and trust in APMs or if they are separate components among certified auditors.

The auditor is an important part of the control of a company and corporate governance with the role of ensuring accounting quality and protecting shareholders and investors (Cohen et al., Citation2002).Footnote2 Yet accountants, managers, and even auditors may need to balance the different views of stakeholders, as there are several possibly applicable financial reporting frameworks (national accounting standards, IFRS, US GAAP, etc.) and presentation styles with visualizations and segment reports for global companies. Hence it is not always clear what a true or fair view is, allowing room for managerial discretion or biases in auditor decision-making (Chang & Luo, Citation2021). There is earlier evidence that auditors are critical toward issues suggesting managerial bias, or earnings management, related to financial information (Becker et al., Citation1998).

PS is an element of audit quality and influences the audit process (Hurtt et al., Citation2013). The International Standard of Auditing 200 (ISA Citation200, Citation2009) defines the use of PS as follows: The auditor shall plan and perform an audit with PS recognizing that circumstances may exist that cause the financial statements to be materially misstated (ISA 200, p. 15). FRC (Citation2019) points out that high-risk audits involve PS, especially when there are questions relating to management judgements and estimates, suggesting state skepticism, i.e. skepticism related to certain conditions or a case situation (Cohen et al., Citation2017; Hurtt, Citation2010; Robinson et al., Citation2018). There is little evidence, however, on trait skepticism. For example, Rose (Citation2007) found in an experiment involving 125 auditors that auditors who rely less on other people pay more attention to the evidence of aggressive financial reporting. These auditors also suspect more often that a misstatement has been intentional. In addition, auditors who have experience of frauds tend to think more often that misstatements are intentional. Therefore, the auditor’s professional skepticism could predict how auditors perceive the presentation of APMs.

3. Data and methods

3.1. Data and the survey instrument

A survey of Finnish certified public auditors (CPAs) was conducted in September 2021. The list of all CPAs in Finland was obtained from the Finnish Patent and Registration Office. Finland is an EU country with detailed requirements for auditors’ education, including courses in accounting, auditing, and law as well as requirements for practical work experience. There are two main types of certified auditors in the country, called KHT and HT.Footnote3 KHT is the highest level of auditor certification, whereas the lower-tier HT certification usually precedes KHT. Both auditor types were included in our survey. We sent an e-mail message to 1271 recipients containing a link to an online survey, with a reminder message sent after one week. We received 220 answers, corresponding to a response rate of 17.3%. All 220 respondents worked as auditors and 119 of them had the higher Finnish (‘KHT’) auditor certification status.

We used two techniques to identify whether the nonresponse bias and the common method bias are present in our survey data. The nonresponse bias was assessed by comparing different waves of respondents. We constructed four groups: the respondents who participated in the survey on the same day they received the survey e-mail (n = 126), those who responded to the survey after the first day but before a reminder message was sent to the respondents (n = 35), those who responded to the survey on the same day they received the remainder message (n = 48), and the remaining respondents (n = 12). No discernible differences between the groups were found based on one-way analysis of variance. The existence of common method bias was assessed using Harman’s one-factor method. Since the variance explained by a one-factor solution is 21%, we conclude that the risk of common method bias being present in our survey responses is small.

The survey instrument (see Appendix 1) contained several statements relating to alternative performance measures and professional skepticism. The survey instrument contained 17 items concerning APMs. In Finland, the financial statements of listed companies follow IFRS but also often include APMs which, according to our pre-interviews and discussions with Finnish auditors, are not necessarily audited with the same diligence as the ‘official numbers’. APMs are usually presented as additional information to the official financial statements in management reports. We probed the respondent’s views of APMs using statements that were measured on the five-point Likert scale (1 = disagree, … , 5 = agree). A survey-based methodology can offer practitioner insights (Bloomfield et al., Citation2016), and in our case, we expect to capture the views of auditors regarding APMs in a specific situation.

To measure state skepticism, we developed a survey instrument investigating the auditor’s skepticism in a situation (or case) that might be regarded as a ‘red flag’, i.e. if the client company makes losses according to GAAP but profit according to alternative measures. The interest and initial construct definition was based on earlier literature and discussions with practitioners and scholars. Hurtt (Citation2010; see also Becker et al., Citation1998; Black et al., Citation2018) suggested that alternative reporting might in some cases be misleading. Then, noticing a lack of a measurement instrument for state skepticism for survey studies in the APM context, we discussed the topic with scholars and experts in the field (resembling the expert agreement and pre-interviews suggested by Rossiter (Citation2002)) to refine the construct definition (wording) and to form a measurement scale. Consequently, our measure included three novel statements about audit risk, financial statement manipulation, and skepticism. We also surveyed the auditors’ perceptions of the usefulness of APMs. Furthermore, our instrument included statements which measured skeptical and trusting attitudes toward management behavior in financial reporting, including alternative performance metrics.

As a measure of professional (trait) skepticism, we used a ten-item version of the professional skepticism scale (Blix et al., Citation2021), drawn from the 30-item multidimensional professional skepticism survey instrument by Hurtt (Citation2010). The Hurtt scale has been shown to be a reliable measure of trait skepticism (Khan & Oczkowski, Citation2021). Following Blix et al. (Citation2021), we also use a scale that allows for a neutral answer (=3 in our case), which is different from the original Hurtt (Citation2010) six-point scale. The abbreviated scale consists of four subscales: questioning mind, search for knowledge, suspension of judgement, and self-determining. As argued by Hurtt (Citation2010), the first three subscales ‘relate to the way an auditor examines evidence’ (p. 152). The subscale of self-determining measures autonomy, which relates to the level of evidence the auditor requires before passing a judgment (Hurtt, Citation2010). We thus use these established subscales now in the context of APMs.

The omitted dimensions are interpersonal understanding (with e.g. statement of interest in other people’s behavior) and self-confidence (with statements such as ‘I have confidence in myself’, see Hurtt, Citation2010), which we regard as relatively personal and less related to the assessment of differing IFRS/APM information presented in our case. We also included two items to probe the respondent’s job satisfaction and career intentions because the impact of skepticism on these is not fully clear (see Cohen et al., Citation2017), particularly if we consider that doubts, e.g. about managerial honesty might relate both to the traits of the auditor or to the case situation. In addition, we followed Cohen et al. (Citation2017) in questions relating to the auditor’s background, such as auditing experience and position in the firm, with some country-specific questions relating to auditor qualifications.

3.2. Methods and the empirical model

Since this study is exploratory, we use exploratory factor analysis (EFA) to examine how auditors perceive APMs. The constructs derived from EFA were used as dependent variables in a structural equation model (SEM). We also use factor analysis to extract the subscales of PS. We report analyzes including checks for correlation, consistency and model fit, and a bootstrapping analysis for mediation effects (see Hair et al., Citation2009; Zhao et al., Citation2010).

Control variables in the model were age, auditing experience, gender, Big4, KHT certification, domain-specific experience in auditing listed companies, senior position, office size, and a long-term intention of staying within the audit profession. These variables were consistent with the antecedents of professional skepticism, such as knowledge, auditor’s quality (Big4), auditing experience and incentives (Hurtt, Citation2010; Hurtt et al., Citation2013; Nelson, Citation2009). Variable operationalizations are described in . We analyzed the data using Stata 15 software.

Our empirical model is based on Hurtt (Citation2010), proposing basically that PS as trait skepticism (the left side of ), together with state skepticism, leads to skeptical behavior. We also consider some additional elements related to the concept of ‘skeptical mindset’ used (but not very clearly defined) by Hurtt (Citation2010). In our view, a skeptical mindset may relate to the perceived usefulness of alternative performance figures in auditing and then affect the trust in alternative performance figures, or again, in the auditor’s skeptical behavior (the right side of , see also and ). We explore these relationships in our conceptual model (), in which the four sub-dimensions (or subscales) of professional trait skepticism on the left lead to state skepticism or to a perception of usefulness of APM. We consider that trait skepticism and state skepticism are not necessarily similar. The auditor may generally appreciate aspects of practical usefulness of APMs as opposed to the state skepticism relating to APMs because Hurtt’s PS is a construct of neutral trait skepticism as opposed to presumptive doubt, which assumes suspicion by default (Nelson, Citation2009). State skepticism and usefulness, in turn, may manifest themselves as skeptical behavior (particularly in a special case or state) or as trust or trusting behavior in relation to APMs (generally).

Table 2. Descriptive statistics and factor loadings for the APM survey instrument.

4. Results

4.1. Descriptive statistics regarding PS

The descriptive statistics for the subscales of PS are reported in . All items exhibit statistically significant t-values, suggesting that the respondents had opinions either for or against the statements. Consistent with Hurtt’s (Citation2010) original version of the survey instrument, the factor solution yields four distinct dimensions for professional skepticism (PS), what we consider as trait skepticism. The Cronbach’s Alphas for the dimensions range from 0.62 (questioning mind) to 0.89 (suspension of judgement), which suggests that they can be used as measures of the dimensions of PS. These are consistent with the ones reported by Hurtt (Citation2010) whose alpha values range from 0.67 (questioning mind) to 0.89 (search for knowledge) for the same four dimensions. It should be noted that Blix et al. (Citation2021) did not use or assess the validity of the abbreviated scale as a multidimensional construct. Thus, the abbreviated scale appears to capture reasonably well the multidimensional characteristics of PS.

Second, reports the descriptive statistics and the loadings of EFA for the survey instrument that probed Finnish public auditors’ perceptions of APMs. The t-test statistics indicate that the respondents on average had a clear opinion, i.e. they agreed or disagreed with the statements in most cases. Our exploratory factor analysis yielded four distinct factors, with two items dropped from the solution. It is noteworthy that APMs in general were not perceived as related to potential financial statement manipulation risk, even if in our case or state situation this risk was recognized (see ). We labeled the factors as Usefulness, Trust, Skeptical behavior, and State skepticism (see also the right-hand side of ). The usefulness factor (Useful for short) reflects a positive perception of the usefulness of APMs. The Trust factor relates to a trusting attitude toward companies’ compliance with the guidance concerning APMs. The Skeptical behavior and thinking factor (Skeptical for short) captures auditors’ critical views on how management uses APMs. The State skepticism factor (State for short) is a novel construct of state skepticism with respect to APMs when compared to a differing view portrayed by the IFRS. Useful and State exhibit a very good internal consistency, as indicated by the high Cronbach’s Alpha values of their constructs. Instead, Trust and State exhibit a lower degree of internal consistency, with alphas slightly above 0.60. These values are acceptable however in exploratory work (Hair et al., Citation2009).

reports the descriptive statistics for the sample. The measures for the subscales of trait skepticism, proposed mediators and dependent variables are standardized (mean = 0, standard deviation (SD) = 1). Regarding control variables, the average auditor was a 51-year-old male (a quarter of the sample were female), with over twenty years of auditing experience. Fifty-four percent of the respondents held the higher-tier (KHT) public auditor certification. Sixty-nine percent of the sample reported holding a senior position. Approximately a quarter of the respondents worked with Big 4 companies. Forty-six percent of the respondents had audited listed companies. Most respondents were committed to staying in the industry long-term.

Table 3. Descriptive statistics.

Additionally, Appendix 2 shows a correlations matrix for the variables used in the empirical model. Most variables exhibit moderate correlations with each other, which suggests that multicollinearity may not pose a serious problem. Further, high correlations are rather obvious: Age correlates with experience and the KHT certification; Big 4 firms tend to hire KHT auditors and carry out listed company audits; the respondent’s age is negatively linked with how long he or she plans to stay in business. Appendix 2 shows that the suspension of judgement factor (with variables like ‘I take my time when making decisions’) is highlighted among female auditors and seems to positively correlate with longer careers in auditing. Appendix 2 also shows that that Skeptical behavior and Trust do not correlate; instead, the State skepticism and Trust factors are negatively correlated.

4.2. Structural equation model

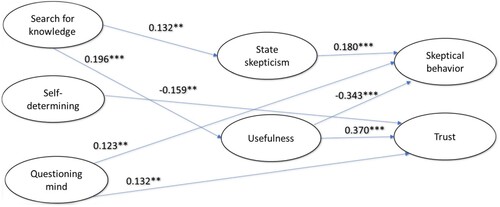

Next, and report the SEM results. shows only the estimated coefficients for paths involving the dimensions of PS and dependent variables. In , the model’s fit statistics are indicative of a good fit, with the overall coefficient of determination (R-squared) over 30%. The results show that Search for knowledge predicts State and Useful. This could be regarded as consistent with trait skepticism exhibiting a neutral version of PS. That is, the auditor who scores high on the subscale has a neutral view of APMs and collects evidence before forming any opinion.

Figure 2. Structural equation model.

Table 4. Structural equation model results.

In the second part of the mediation model (see ), state skepticism is a positive predictor of skeptical behavior and thinking, whereas usefulness is a negative predictor. For state skepticism and usefulness, only usefulness predicts trust. These results suggest that state skepticism is correlated with skeptical behavior, whereas usefulness is linked with trust. An examination of direct paths shows that questioning mind is positively associated with both skeptical behavior and trust as a direct predictor. Self-determining is negatively associated with trust (−0.159) and search for knowledge precedes and plausibly helps forming any opinion.

Several studies (e.g. Zhao et al., Citation2010) suggest that the existence of ‘mediation effects’ should be assessed by bootstrapped bias-corrected percentile confidence intervals. Only two such effects can be established, as indicated by non-zero bias-corrected 95% confidence intervals in . The usefulness factor mediates the path between search for knowledge and skeptical behavior and trust with a negative and positive coefficient with a comparable magnitude for the former and latter, respectively.

Table 5. Significant mediation effects.

Direct effects and coefficient estimates for control variables are reported in Appendix 3. Regarding direct effects, questioning mind is a positive predictor of skeptical and trust, whereas self-determining is a negative predictor of trust. The estimated coefficients suggest that a long-term intention to stay within the auditing profession is negatively associated with state skepticism. Otherwise, other general auditor characteristics, such as gender, age, experience, the auditor’s quality or senior position are not clearly associated with state skepticism. Moreover, experience in auditing listed companies is positively associated with skeptical behavior. All in all, we find that state skepticism is a largely separate component of professional skepticism. In addition, search for knowledge is a key aspect of PS in predicting trust or skeptical behavior in auditing.

5. Conclusions

5.1. Discussion

This paper investigated how auditors’ views of alternative performance measures in financial statements in the European context are related to professional skepticism, as measured by state and trait skepticism. Relating to the first research question, RQ1, ‘How do auditors perceive alternative performance measures in financial reporting?’ our results indicated that in general Finnish auditors hold positive views of APMs. Regarding RQ2 ‘Does professional skepticism explain skeptical behavior and trust related to APMs?’ our analyzes suggest that trust in APMs is related to search for knowledge, and that after a careful analysis the auditor can assess alternative forms of reporting, i.e. the auditor can see through the alternative truths. Finally, as an answer to RQ3, ‘How is trait skepticism related to state skepticism in the case of APMs?’, we found that state skepticism is largely separate from trait skepticism.

Our findings contribute to the auditing literature by demonstrating the effect of state skepticism, as a separate element of PS in audit work, on the skeptical behavior of auditors in relation to APMs in a European context. Further, state skepticism appears to be unrelated to auditor characteristics, such as experience, the auditor’s quality, or senior position, which have been proposed to be antecedents of PS (e.g. Nelson, Citation2009). We also contribute to earlier findings on professional skepticism (Cohen et al., Citation2017; Hurtt, Citation2010; Robinson et al., Citation2018) by showing that there are aspects of both trait and state skepticism related to APMs. Further, we provide a detailed view (through structural equation modeling in ) on how these link to the auditor’s trust in accounting figures. Our findings suggest that professional skepticism or its effects are not straightforward and that there are several linkages and effects (see ), and that questioning mind is a positive predictor of skeptical behavior and trust, suggesting that reflecting on data facilitates the auditor’s work. Further, again emphasizing the importance of considering both the usefulness of data and the specific case situation, we found that search for knowledge is an important element in audit work and related to both trust and skeptical behavior. In addition, we found that the self-determining component of PS (see ) indicates less trust, which we see as a specific contribution to earlier literature on professional skepticism in auditing context (e.g. Hurtt, Citation2010).

Methodologically, our novel state skepticism measurement instrument aims to contribute to survey studies concerning the analysis of trait and state skepticism in auditing (elaborating e.g. Robinson et al., Citation2018). Besides understanding potential biases in auditor decision-making generally (Chang & Luo, Citation2021), it is important to know the case company, understand the state of affairs, and the messages conveyed both with APMs and with other accounting figures in audit work.

5.2. Managerial and practical implications

As a practical and managerial implication, interest in searching knowledge and being able to notice special case situations seem to be important practical skills for auditors. It would be advisable to emphasize professional skepticism in university education and auditor training. Furthermore, since there are studies that suggest a potentially obfuscating role of APM reporting, but auditors in our sample hold a generally positive view of APMs, auditor education could address this and emphasize both the interpretation and the need of a skeptical approach to APMs, at least in special cases where APMs and official numbers diverge. Furthermore, concerning researchers, our study offers insights into measuring PS and case-specific situations which could be useful in survey studies.

5.3. Limitations and future research

This paper has some limitations. First, our focus was on a single EU country, so evidence from other countries with other requirements for auditors might yield different results. The single-country focus may also limit the generalizability of our findings. Second, the sample size was small, reducing the statistical power of empirical tests. Finally, our work is based on a survey of auditor perceptions of APMs, and these perceptions may not be congruent with how auditors behave in actual audits.

As a direction for future studies, we call for further research into professional skepticism in various contexts and cases as well as into the possibilities for auditors to detect other manipulative states of affairs in the current turbulent times. We also recommend similar research in other times and jurisdictions. Further research might thus bring greater understanding of trait and state skepticism and their measurement, and test our state skepticism measurement instrument in other contexts. For instance, experiments that address relationships between trait and state skepticism in the case of APMs could shed light on the results reported in this paper.

Acknowledgements

The authors would like to thank the anonymous reviewer and the editors for their valuable support and comments. Further, we thank the survey respondents for their answers, and we are grateful for the comments received in EUFIN 2022 Lisbon and in EAA 2022 Bergen.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1 In addition, attitudes or feelings of auditors have been regarded as potential components of skepticism (Nolder & Kadous, Citation2018), but personal feelings or emotions are largely beyond the scope of this research.

2 According to Jensen (Citation1993), four control forces affect corporations: the capital markets, the legal/political/regulatory system, the product and factor markets, and the internal control system headed by the board of directors. There are risks and problems however in control systems, such as asymmetry of information (ibid.). Auditing obviously relates to capital markets and to the regulatory systems, but stakeholder views are not necessarily coherent and may include alternative viewpoints. Alternative viewpoints may also relate e.g. to the various forms of sustainability and tax reporting and auditing such reports (see e.g. Klimczak et al., Citation2023; Mura, Citation2023).

3 Additionally, in Finland, there is a specialization degree, JHT (previously called JHTT), for public sector auditors but this survey did not focus on the auditing of public sector or nonprofit organizations.

References

- Allee, K. D., Bhattacharya, N., Black, E. L., & Christensen, T. E. (2007). Pro forma disclosure and investor sophistication: External validation of experimental evidence using archival data. Accounting, Organizations and Society, 32(3), 201–222. https://doi.org/10.1016/j.aos.2006.09.012

- Andersson, P., & Hellman, N. (2007). Does pro forma reporting bias analyst forecasts? European Accounting Review, 16(2), 277–298. https://doi.org/10.1080/09638180701390966

- Basu, S. (1997). The conservatism principle and the asymmetric timeliness of earnings. Journal of Accounting and Economics, 24(1), 3–37. https://doi.org/10.1016/S0165-4101(97)00014-1

- Becker, O. L., Defond, M., Jiambalvo, J., & Subramanyam, K. R. (1998). The effect of audit quality on earnings management. Contemporary Accounting Research, 15(1), 1–24. https://doi.org/10.1111/j.1911-3846.1998.tb00547.x

- Bedard, J. C., & Johnstone, K. M. (2004). Earnings manipulation risk, corporate governance risk, and auditors’ planning and pricing decisions. The Accounting Review, 79(2), 277–304. https://doi.org/10.2308/accr.2004.79.2.277

- Bhattacharya, N., Black, E. L., Christensen, T. E., & Larson, C. R. (2003). Assessing the relative informativeness and permanence of pro forma earnings and GAAP operating earnings. Journal of Accounting and Economics, 36(1–3), 285–319. https://doi.org/10.1016/j.jacceco.2003.06.001

- Black, D. E., & Christensen, T. E. (2018). Policy implications of research on non-GAAP reporting. Research in Accounting Regulation, 30(1), 1–7. https://doi.org/10.1016/j.racreg.2018.03.001

- Black, D. E., Christensen, T. E., Ciesielski, J., & Whipple, B. (2018). Non-GAAP reporting: Evidence from academia and current practice. Journal of Business Finance & Accounting, 45(3–4), 259–294. https://doi.org/10.1111/jbfa.12298

- Black, D. E., Christensen, T. E., Ciesielski, J., & Whipple, B. (2021). Non-GAAP earnings: A consistency and comparability crisis? Contemporary Accounting Research, 38(3), 1712–1747. https://doi.org/10.1111/1911-3846.12671

- Blix, L. H., Chui, L. C., Pike, B. J., & Robinson, S. N. (2021). Improving auditor performance evaluations: The impact on self-esteem, professional skepticism, and audit quality. Journal of Corporate Accounting & Finance, 32(4), 84–98. https://doi.org/10.1002/jcaf.22512

- Bloomfield, R., Nelson, M. W., & Soltes, E. (2016). Gathering data for archival, field, survey, and experimental accounting research. Journal of Accounting Research, 54(2), 341–395. https://doi.org/10.1111/1475-679X.12104

- Chang, C. J., & Luo, Y. (2021). Data visualization and cognitive biases in audits. Managerial Auditing Journal, 36(1), 1–16. https://doi.org/10.1108/MAJ-08-2017-1637

- Chen, L., Krishnan, G., & Pevznera, M. (2012). Pro forma disclosures, audit fees, and auditor resignations. Journal of Accounting and Public Policy, 31(3), 237–257. https://doi.org/10.1016/j.jaccpubpol.2011.10.008

- Ciesielski, J. T., & Henry, E. (2017). Accounting’s tower of Babel: Key considerations in assessing non-GAAP earnings. Financial Analysts Journal, 73(2), 34–50. https://doi.org/10.2469/faj.v73.n2.5

- Cohen, J., Dalton, D. W., & Harp, N. L. (2017). Neutral and presumptive doubt perspectives of professional skepticism and auditor job outcomes. Accounting, Organizations and Society, 62, 1–20. https://doi.org/10.1016/j.aos.2017.08.003

- Cohen, J., Krishnamoorthy, G., & Wright, A. M. (2002). Corporate governance and the audit process. Contemporary Accounting Research, 19(4), 573–594. https://doi.org/10.1506/983M-EPXG-4Y0R-J9YK

- Deloitte. (2016). Alternative performance measures. IFRS in focus – A practical guide. Retrieved July 2016, from https://www2.deloitte.com/content/dam/Deloitte/ru/Documents/audit/IFRS_news/july-27-2016.pdf

- Entwistle, G. M., Feltham, G. D., & Mbagwu, C. (2012). Credibility attributes and investor perceptions of non-GAAP earnings exclusions. Accounting Perspectives, 11(4), 229–257. https://doi.org/10.1111/1911-3838.12000

- ESMA. (2015). ESMA guidelines on alternative performance measures. 05/10/2015| ESMA/2015/1415en

- ESMA. (2021). ESMA proposes improvements to transparency directive after wirecard case. https://www.esma.europa.eu/sites/default/files/library/esma32-51-818_letter_to_the_ec_on_next_steps_following_wirecard.pdf

- Evans, L. (2003). The true and fair view and the ‘fair presentation’ override of IAS 1. Accounting and Business Research, 33(4), 311–325. https://doi.org/10.1080/00014788.2003.9729656

- Feng, Z., Francis, J. R., Shan, Y., & Taylor, S. (2023). Do high-quality auditors improve non-GAAP reporting? The Accounting Review, 98(1), 215–250. https://doi.org/10.2308/TAR-2019-0592

- FRC. (2019). Achieving high quality audits consistently. Financial Reporting Council. A letter by David Rule, FRC executive director of supervision, to audit firms. Retrieved November 8, 2019 from https://www.frc.org.uk/getattachment/a40f77f6-9542-47be-b1c5-e15ece70415a/Achieving-high-quality-audits-letter-(sent-to-firms-08-11-19).pdf

- FRC. (2021). Thematic review: Alternative performance measures. Financial Reporting Council. Retrieved October 2021, from https://www.frc.org.uk/getattachment/74ed739d-2237-4d3e-a543-af8ada9b0e42/FRC-Thematic-Review-on-APMs-October-2021.pdf

- Glover, S. M., & Prawitt, D. F. (2014). Enhancing auditor professional scepticism: The professional scepticism continuum. Current Issues in Auditing, 8(2), P1–P10. https://doi.org/10.2308/ciia-50895

- Hair, J. F., Black, B., Babin, B. J., & Anderson, R. E. (2009). Multivariate data analysis (7th ed.). Pearson.

- Hallman, N. J., Schmidt, J. J., & Thompson, A. M. (2022). Audit implications of non-GAAP reporting. Journal of Accounting Research, 60(5), 1947–1989. https://doi.org/10.1111/1475-679X.12433

- Hamilton, G., & Ohogartaigh, C. (2009). The third policeman: ‘The true and fair view’, language and the habitus of accounting. Critical Perspectives on Accounting, 20(8), 910–920. https://doi.org/10.1016/j.cpa.2009.02.003

- Healy, P., & Palepu, K. (2001). Information asymmetry, corporate disclosure, and the capital markets: A review of the empirical disclosure literature. Journal of Accounting and Economics, 31(1–3), 405–440. https://doi.org/10.1016/S0165-4101(01)00018-0

- Henry, E., Hu, N., & Jiang, X. (2020). Relative emphasis on non-GAAP earnings in conference calls: Determinants and market reaction. European Accounting Review, 29(1), 169–197. https://doi.org/10.1080/09638180.2019.1664312

- Herr, S. B., Lorson, P., & Pilhofer, J. (2022). Alternative performance measures: A structured literature review of research in academic and professional journals. Schmalenbach Journal of Business Research, 74, 389–451. https://doi.org/10.1007/s41471-022-00138-8

- Hope, O.-K., Langli, J. C., & Thomas, W. B. (2012). Agency conflicts and auditing in private firms. Accounting, Organizations and Society, 37(7), 500–517. https://doi.org/10.1016/j.aos.2012.06.002

- Hurtt, R. K. (2010). Development of a scale to measure professional skepticism. Auditing: A Journal of Practice & Theory, 29(1), 149–171. https://doi.org/10.2308/aud.2010.29.1.149

- Hurtt, R. K., Brown-Liburd, H., Earley, C., & Krishnamoorthy, G. (2013). Research on auditor professional skepticism: Literature synthesis and opportunities for future research. Auditing: A Journal of Practice & Theory, 32(Suppl. 1), 45–97. https://doi.org/10.2308/ajpt-50361

- IASB Conceptual Framework. (2018). IASB, IFRS Foundation.

- IFRS ED. (2019). IFRS exposure draft, ED/2019/7. General presentation and disclosures. December 2019. Published for comments only by the International Accounting Standards Board.

- IOSCO. (2016). Statement on NON-GAAP financial measures, final report. https://www.iosco.org/library/pubdocs/pdf/IOSCOPD532.pdf

- ISA 200. (2009). International Standard on Auditing 200. Overall objectives of the independent auditor and the conduct of an audit in accordance with international standards on auditing. Retrieved December 15, 2009.

- Jahn, P., & Loy, T. (2023). Audit in Europe – A comparison of access requirements into the audit profession across the European Union. Accounting in Europe, 20(2), 244–271. https://doi.org/10.1080/17449480.2023.2205867

- Jana, S., & McMeeking, K. (2021). Alternative performance measures: Determinants of disclosure quality – Evidence from Germany. Accounting in Europe, 18(1), 102–142. https://doi.org/10.1080/17449480.2020.1829655

- Jensen, M. C. (1993). The modern industrial revolution, exit, and the failure of internal control systems. Journal of Finance, 48(3), 831–880. https://doi.org/10.1111/j.1540-6261.1993.tb04022.x

- Khan, M. J., & Oczkowski, E. (2021). The link between trait and state professional skepticism: A review of the literature and a meta-regression analysis. International Journal of Auditing, 25(2), 558–581. https://doi.org/10.1111/ijau.12232

- Klimczak, K., Hadro, D., & Meyer, M. (2023). Executive communication with stakeholders on sustainability: The case of Poland. Accounting in Europe, 1–23. https://doi.org/10.1080/17449480.2023.2213242

- Mura, A. (2023). Reconciling competing reporting objectives through deferred tax accounts: Evidence on private Italian firms. Accounting in Europe, 1–35. https://doi.org/10.1080/17449480.2023.2213249

- Nelson, M. W. (2009). A model and literature review of professional skepticism in auditing. Auditing: A Journal of Practice and Theory, 28(2), 1–34. https://doi.org/10.2308/aud.2009.28.2.1

- Nolder, C. J., & Kadous, K. (2018). Grounding the professional skepticism construct in mindset and attitude theory: A way forward. Accounting, Organizations and Society, 67, 1–14. https://doi.org/10.1016/j.aos.2018.03.010

- Rautiainen, A., Järvenpää, M., & Mättö, T. (2022). Non-IFRS and changes in accounting institutions – Lessons from Nokia. Accounting History, 27(4), 524–548. https://doi.org/10.1177/10323732221094033

- Robinson, S. N., Curtis, M. B., & Robertson, J. C. (2018). Disentangling the trait and state components of professional skepticism: Specifying a process for state scale development. Auditing: A Journal of Practice & Theory, 37(1), 215–235. https://doi.org/10.2308/ajpt-51738

- Rose, J. M. (2007). Attention to evidence of aggressive financial reporting and intentional misstatement judgments: Effects of experience and trust. Behavioral Research in Accounting, 19(1), 215–229. https://doi.org/10.2308/bria.2007.19.1.215

- Rossiter, J. R. (2002). The C-OAR-SE procedure for scale development in marketing. International Journal of Research in Marketing, 19(4), 305–335. https://doi.org/10.1016/S0167-8116(02)00097-6

- Sundgren, S. (1998). Auditor choices and auditor reporting practices: Evidence from Finnish small firms. European Accounting Review, 7(3), 441–465. https://doi.org/10.1080/096381898336376

- Walton, P. (1993). Introduction: The true and fair view in British accounting. European Accounting Review, 2(1), 49–58. https://doi.org/10.1080/09638189300000003

- Zhao, X., Lynch, J. G., & Chen, Q. (2010). Reconsidering Baron and Kenny: Myths and truths about mediation analysis. Journal of Consumer Research, 37(2), 197–206. https://doi.org/10.1086/651257

Appendices

Appendix 1. The survey instrument

General items/background selections:

Sex; Age; How many years have you worked as an auditor?

Are you working as an auditor at the moment?

Do you have experience on auditing stock exchange listed companies?

Do you work at a Big-4 company (Deloitte, EY, KPMG, PwC)?

Do you have a senior/leading position?

What is the size of your workplace?

Do you have a KHT (Finnish higher auditing) degree?

(1) I trust the information provided by the alternative performance measures.

(2) It is good to eliminate one-off events from the financial statement figures and present alternative performance measures.

(3) Alternative performance measures provide useful information for investors about the company’s financial results.

(4) Using alternative performance measures provides useful information for auditing.

(5) Alternative performance measures are misleading to financial statement users (R).

(6) Presenting alternative performance measures means increased auditing risks.

(7) Reporting alternative performance measures is useful in auditing.

(8) Finnish companies know how to follow the alternative performance measures related guidance from the European Securities and Market Authority, ESMA.

(9) Presenting alternative performance measures increases the risk of financial statement manipulation.

(10) Presenting alternative performance measures facilitates forming a true and fair view on the financial statements.

(11) I am usually skeptical regarding what management tells me.

(12) When presenting alternative performance measures companies typically embellish the image of the company.

(13) Companies tend to maximize their stock value by presenting alternative performance measures.

(14) Alternative performance measures give useful information about the formation of the company results.

(15) Companies know how to operate correctly when reporting alternative performance measures.

(16) If a company reports losses according to IFRS but profit according to alternative performance measures, it is a sign of an increased audit risk.

(17) If a company reports losses according to IFRS but profit according to alternative performance measures, it is a sign of an increased risk for financial statement manipulation.

(18) If a company reports losses according to IFRS but profit according to alternative performance measures, I am more skeptical in my audit.

(19) I am satisfied with my work.

(20) I intend to stay in my profession for a long time.

(21) I think that learning is exciting.

(22) I take my time when making decisions.

(23) I relish learning.

(24) I dislike having to make decisions quickly.

(25) I don’t like to decide until I’ve looked at all the readily available information.

(26) My friends tell me that I often question things that I see or hear.

(27) I frequently question things that I see or hear.

(28) I tend to immediately accept what other people tell me.

(29) I often accept other people’s explanations without further thought.

(30) I usually accept things I see, read or hear at face value.

Note: Items 16, 17, and 18 represent our novel state skepticism instrument.

Appendix 2. Correlation matrix