?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This paper builds a new dataset on bank ownership and finds no evidence of a negative correlation between state-ownership of banks and economic growth. Banking crises predict increases in state-ownership but that there is no evidence that high state-ownership predicts banking crises. Contrary to past literature, the paper also shows that recent data show no difference between the profitability of private and public banks located in emerging and developing economies. The paper corroborates the existing literature which shows that in emerging and developing economies lending by state-owned banks is less procyclical than private bank lending.

1 Introduction

The presence of the state in the financial system through direct ownership of banks has decreased rapidly since the late 1980s. In the mid-1970s, the government owned more than 40% of bank assets in advanced economies and about two-thirds of bank assets in developing and emerging economies. By the early 1990s, state ownership of banks had dropped to about 25% in advanced economies and to less than 50% in emerging and developing economies (Levy Yeyati et al., Citation2007). Privatization continued through the 1990s and the first years of the new millennium. Immediately before the global financial crisis, the government controlled about 18% of bank assets in advanced economies and 30% of bank assets in emerging and developing economies.Footnote1

State-ownership of banks is often justified by market failures and development goals. The social view emphasizes how public interventions can address market imperfections that lead to underinvestment in projects with high social returns (Stiglitz Citation1994; Levy-Yeyati, Micco, and Panizza Citation2007). The development view highlights the necessity of state-owned banks in countries where institutional failures prevent the development of a financial sector that can meet a country’s development needs (Lewis Citation1950; Gerschenkron Citation1962).

The privatization wave that started in the 1980s was linked to a sea change in the consensus view on the role of the state in finance. The perception that political failures dominate market failures led to the view that government intervention often makes things worse. State-ownership became associated with the idea that state-owned enterprises only exist to provide rents to the policymakers that control them (Kornai Citation1979, Shleifer and Vishny Citation1994). This political view of state-ownership (La Porta, Rafael, and Shleifer Citation2002) was crystallized by an influential World Bank report which concluded that: “Whatever its original objectives, state ownership tends to stunt financial sector development, thereby contributing to slower growth” (World Bank Citation2001, 123).

The global financial crisis led a resurgence of interest in state-ownership of banks (World Bank Citation2012, Inter-American Development, Citation2014; International Monetary Fund Citation2020, European Bank for Reconstruction and Development Citation2020) and to a view that state-owned banks are not necessarily good or bad per se but dynamic institutions that, under certain conditions, can evolve and contribute to addressing society’s most pressing problems (Marois Citation2021). It is also worth mentioning that there are several types of banking institutions which are somewhere in between traditional private banks and state-owned banks. Butzbach and von Mettenheim (Citation2015) call these institutions which have missions that include social and public policy goals and stakeholder-oriented governance “Alternative Banks” and suggest that alternative banks have several advantages with respect to traditional private banks.

This paper contributes to the discussion by building a new dataset which is longer and more detailed than what has been used in the existing literature and by using these new data to reassess the links between state-ownership of banks and each of financial depth, economic growth, financial stability, bank performance, and lending cyclicality. Two things that the paper does not do are to explicitly focus on the role of public banks as a tool to respond to the Covid 19 pandemic and to address climate change. McDonald, Marois, and Barrowclough (Citation2020) focus on the first issue and Marois (Citation2022) on the second.

Besides using more recent and longer data, this paper differs from previous work by focusing on commercial banks, instead of combining commercial and development banks. Commercial and development banks have different missions and modes of operations. Many development banks have an explicit development mandate which, in some cases, is narrowly defined (lending to the agricultural sector, lending to SMEs, lending to the export industry). State-owned commercial banks, instead, tend to have broader mandates. Moreover, while most commercial banks operate as first-tier institutions (i.e., they interact directly with the final borrower), a substantial number of development banks are second-tier institutions (see Fernandez-Arias, Hausmann, and Panizza Citation2020) with a completely different business model and cost structure. Hence, it does not make much sense to compare the performance and roles of these different types of financial institutions.

The influential work by La Porta, Rafael, and Shleifer (Citation2002) shows that state ownership of banks in the 1970s is associated with lower future financial depth and GDP growth. However, the cross-sectional nature of their analysis does not allow controlling for unobservable factors which could be jointly correlated with state ownership of banks and the outcomes of interest. The presence of such unobservable factors makes the negative relationship between state-ownership and growth observed in cross-country studies consistent with both the political and the social and development views described above.

The dataset assembled for this paper allows using panel data to estimate the short- and medium-term relationship between state-ownership and financial depth and to show that there is no robust correlation between these two variables. State-ownership of banks is not significantly correlated with current and future financial depth, and financial depth is not significantly correlated with current and future state-ownership of banks. I also find no robust correlation between state-ownership of banks and successive growth, measured using both 5-year and 10-year growth spells (if anything, the relationship is positive but rarely statistically significant).

Taken together, these results do not provide strong support for either the development or the political view. The lack of a positive correlation between the presence of state-owned banks and financial depth or GDP growth could be driven by the fact that this correlation is affected by the presence of unobservable variables which have a causal effect on both economic growth and the presence of state-owned banks. This is the endogeneity problems highlighted by Rodrik (Citation2012).

I use bank-level data to study the relationship between ownership and performance. Note that one should be careful in interpreting these results. The fact that state-owned banks have lower profitability and higher NPL than private banks does not necessarily mean that state-owned banks are poorly managed. State-owned banks with a social mandate do not maximize profits and could be efficient even if they realize losses and have large non-performing loans. Comparing the profitability of private and state-owned banks is, however, useful in order to establish whether there are opportunity costs linked to having state-owned banks.

Past research found that state-owned banks located in emerging and developing economies are less profitable than private banks (Micco, Panizza, and Yanez Citation2007; Cull, Soledad Martínez Pería, and Verrier Citation2018). Results based on data for the period 1995–2009 are consistent with these findings. However, recent data paint a more nuanced picture and suggest no difference between the profitability of private and public banks located in emerging and developing economies. With respect to non-performing loans, results based on recent data are consistent with previous work indicating that state-owned banks in both advanced and developing economies have higher levels of non-performing loans than private banks.

As procyclical lending by private banks may reduce the effectiveness of macroeconomic policies, countercyclical lending by state-owned banks could be useful in smoothing the business cycle (for a discussion of the potential role of public banks in macroeconomic policy, see Marshall and Rochon Citation2019). Micco and Panizza (Citation2006) used bank-level data to test this hypothesis and showed that lending by state-owned banks is less procyclical than private bank lending and that this difference in lending cyclicality is especially important in developing and emerging economies. Several follow-up studies found similar results (World Bank Citation2012; Brei and Schclarek Citation2013; Cull and Martinez-Peria, Citation2013; Coleman and Feler Citation2015; Bertay, Demirgüç-Kunt, and Huizinga Citation2015, De Haas et al. Citation2015; Duprey Citation2015). Section 6 corroborates the existing evidence of countercyclical lending by state-owned banks located in developing and emerging market economies and also shows that there is no difference between the pre and post GFC period.

2 Data

This paper uses four main types of data: (i) bank-level data from Fitch Connect; (ii) macroeconomic data from the IMF-WEO database and from the World Bank World Development Indicators; (iii) firm survey data from the World Bank Enterprise Survey; and (iv) industry-level data from UNIDO.Footnote2

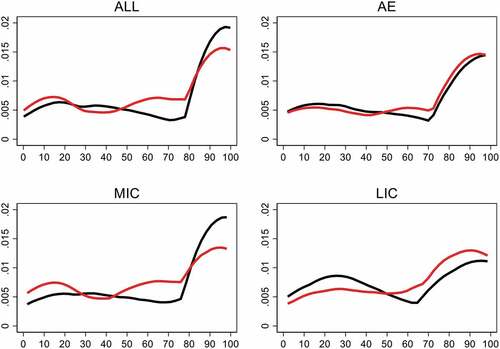

The bank-level dataset consists of an unbalanced panel covering 7,150 banks in 180 countries over the period 1995–2018 and a total of over 100,000 observations. plots the non-parametric distribution of the share of state-ownership for banks with positive state-ownership (the black lines are for 2010 and the red lines for 2018). In advanced and middle-income economies, the distribution is concentrated towards high shares (above 80%) of state ownership (even though in middle-income economies the 2018 distribution is flatter than the 2010 distribution). In low-income economies, instead, there are two peaks, one at 20% and one at 90%. In this group of countries, the distribution of state-ownership shares is flatter than advanced and middle-income economies.

Figure 1. Distribution of state-ownership shares.This figure plots the non-parametric distribution (Epanechnikov Kernel) of state ownership for all banks in which state ownership is at least 1%. The top left panel includes all the banks included in the dataset used in this paper, the top right panel only uses data for banks based in advanced economies, and the bottom panels use data for banks based in middle-income (MIC) and low-income (LIC) economies.

I build two country-year level measures of state ownership. The first measure is the number of state-owned banks over the total number of banks. Formally:

where is a dummy variable which takes value one if bank

(located in country

) in year

is state owned (with state-ownership defined using the 20% threshold) and zero if it is private and

is the number of commercial banks that operate in country

in year

.Footnote3

The second measure is the share of state ownership weighted by bank assets. Formally:

where are the assets of bank

(located in country

) in year

, and all other variables are defined as in EquationEquation (1)

(1)

(1) . Throughout the paper, I will use

to indicate a country-level continuous measure of state-ownership and

as a bank-level dummy that takes value one if the bank is state-owned (using the 20% threshold).

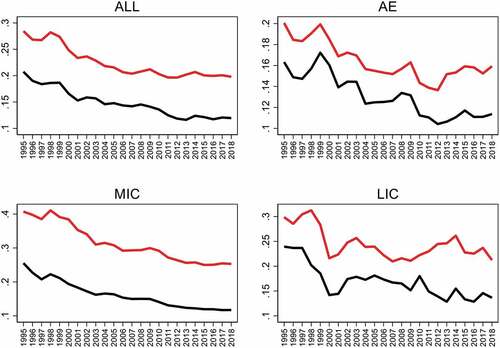

plots the evolution of state-ownership over 1995–2018. The black lines show the simple average ( and the red lines show the weighted average (

). As state-owned banks tend to be large, the weighted average is higher than the simple average. The top left panel of shows that the share of commercial bank assets controlled by the state dropped from nearly 30% in 1994 to about 20% in 2018. In advanced economies, the share of bank assets controlled by the government went from 20% in 1995 to about 15% in 2009 and then increased to about 17% in the aftermath of the global financial crisis (top right panel of ). In middle-income countries, instead, state ownership decreased from about 40% in 1995 to 28% in 2018. In low-income economies, the share of assets controlled by the state started at 30% in 1995, bottomed out to about 22% in 2008, increased to 25% over 2008–14, and dropped again over 2014–18.

Figure 2. Share of state-owned banks.

3 Country-level evidence

This section uses country-level panel data to assess the relationship between state-ownership of banks and each of financial depth (proxied by credit to the private sector over GDP), economic growth, and financial stability. Before looking at the regressions’ results, it is worth noting that one should be careful in interpreting cross-country regressions which relate state-ownership of banks with outcomes such as financial depth or GDP growth. The observed correlation between the presence of state-owned banks and outcomes such as financial depth or economic growth could be driven by unobserved variables which are jointly correlated with bank ownership and the outcome variables we are interested in.

If the observed cross-country variation in state-ownership of banks is not random, a negative correlation between the endogenously chosen level of state-ownership and each of financial and economic growth could either be driven by the presence of market failures (as postulated by the development and social views of state-owned banks), by the presence of political failures (as postulated by the political view), or by the joint presence of these different types of failures. This endogeneity problem can be illustrated with a simplified version of the model described in Rodrik (Citation2012).

Assume a situation in which: (i) a certain market failure has a negative effect on a policy objective

(financial depth or economic growth, in our case); (ii) the government can mitigate this market failure by establishing a state-owned bank of size

; and (iii) there are agency costs

associated with the operations of the state-owned bank, where

is a shift parameter associated with policy effectiveness (lower values of

are associated with more efficient policymaking), and with

, and

, and

. Given these assumptions, the socially optimal size of the state-owned banks is obtained from the following maximization problems:

and the socially optimal value of is implicitly defined by the first-order condition

.Footnote4

If is chosen by self-interest policymakers who, besides caring about social welfare (with weight

, also obtain private rents

(with

and

) from the state-owned banks, the equilibrium level of

is obtained from the following maximization problem:

The value of chosen by self-interested politicians is implicitly defined by

. If

, politicians provide more state-owned banking than it is socially optimal. In other words, there is a political motive to state-owned banks.

Rodrik (Citation2012) points out that the presence of political motives does not necessarily mean that setting is preferable to the suboptimal level of state-owned banks chosen by self-interested politicians. This would only be the case if

, where

is the size of state-owned banking that solves the self-interested policymakers’ problem. In other words, the fact that political imperfections lead to too much state-ownership does not necessarily imply that the optimal level of state-ownership is zero. This first consideration suggests that the ample evidence in favor of political motives does not necessarily mean that zero state-ownership would be a preferable option.

Second, and more important, the simple model derived by Rodrik provides an illustration of the endogeneity problem as it can yield a cross-country negative correlation between and

even in a situation in which policymakers are both benevolent (

is close to one) and efficient (

is small). To show that this is the case, consider a group of countries with different levels of distortions

and verify that the equilibrium level of state-ownership

is increasing in

and the policy objective

is decreasing in

:

Therefore, if is unobservable and cannot be controlled for, a cross-country regression of

over

will show that state ownership is negatively correlated with

. And this is so even if policymakers choose the level of

that maximizes

. This is a classic endogeneity problem: as market imperfections increase, benevolent policymakers will increase state-ownership, but since

, the optimal level of state-ownership will not fully eliminate the effect of the distortion (i.e.,

). This generates a negative correlation between

and

. Hence,

when we observe a negative correlation between interventions and performance, we cannot distinguish between two diametrically opposed views of the world ―one in which governments are driven by desirable economic motives and one in which they are driven by economically harmful, political motives (Rodrik Citation2012, 146)

In the regressions of this section, I will try to address this issue by augment the models with a rich set of controls, with country fixed effects (which capture the time-invariant component of ), and by also looking at whether state-ownership predicts financial depth or the other way around. However, none of these strategies can fully solve the endogeneity problem described above.

3.1 State-owned banks and financial depth

Given the intertemporal nature of the typical financial contract, the presence of asymmetric information and weak contract enforcement are key sources of financial market imperfections which reduce private banks’ incentives to lend to small and informationally opaque borrowers. The presence of these market failures is the most commonly used rationale for state interventions in financial markets and for the presence of state-owned banks.

This is the theory, but what do the data say? explores the contemporaneous correlation between state-ownership and financial depth in an unbalanced panel of up to 171 countries over the period 1995–2018. The different models are estimated using both pooled OLS and fixed effects regressions. Fixed effects regressions have the advantage of attenuating omitted-variable problems as they implicitly control for institutional characteristics which can be jointly associated with small financial sectors and the presence of state-ownership ( in Rodrik’s model). However, in the presence of variables with limited within-country variation, fixed effects models can also lead to multicollinearity and amplify problems associated with measurement error.

Table 1. State-owned banks and financial depth (dep. var: credit to the private sector).

Column 1 of shows that the correlation between state-ownership and financial depth is negative: countries with more state-owned banks have smaller financial sectors. The bottom panel of the table shows that this negative correlation is robust to including country fixed effects. However, there could be time-variant country characteristics which are jointly correlated with market failure and state ownership. These variables include creditors’ rights, macroeconomic stability (which can be proxied by inflation), and an overall measure of economic development (proxied by GDP per capita). Columns 2–8 show that in most cases the correlation between state-ownership and financial depth is no longer statistically significant once I control for these variables (the correlation remains marginally significant at the 10% confidence level in the fixed effects regression for the sample of emerging and developing economies). I probe further and test whether state ownership of banks predicts financial depth over a five-year period. I find no robust evidence of a negative correlation between state-ownership and future levels of financial depth (full results are available in Panizza Citation2021). I also conduct the opposite experiment and test whether financial depth predicts changes in state-ownership or in the level of state ownership. Regression results suggest that higher financial depth is associated with higher levels of state-ownership five-year later. However, the coefficients are rarely statistically significant (full results are available in Panizza Citation2021).

Summing up, while previous work which used older data and focused on the cross-sectional correlation between state ownership and financial depth found a strong negative correlation between state-ownership of banks and financial depth, the more recent data and a panel set-up that allows controlling for a richer set of covariates show no strong correlation between state ownership of banks and financial depth (a result already present in Levy Yeyati et al., Citation2007). Most of these findings are in contrast with both the view that state ownership stunts financial-sector development (World Bank Citation2001) and with the development and social views suggesting that state-owned banks have a positive catalytic effect and should be especially active in countries with poorly working financial sectors.

3.2 State-owned banks and GDP growth

There are at least two channels through which state-ownership of banks could affect growth. On the positive side, state-owned banks could contribute to financing projects with high social returns but lower private returns. On the negative side, political lending may lead to resource misallocation and thus reduce economic growth.

Existing work yields mixed results. While, in a pure cross-country set-up, La Porta, Rafael, and Shleifer (Citation2002) found a strong negative correlation between state-ownership and economic growth, Levy Yeyati et al. (Citation2007) showed that these results are somewhat sensitive to the sample and time period used in the analysis.

provides a new set of estimates that use more recent data and a panel framework.Footnote5 In , I focus on 5-year growth spells and in Table 13 on 10-year growth spells. In all regressions, I use the same set of controls as in Beck and Levine (Citation2004). As in Tables 6–9, I use overlapping growth periods and correct for the presence of a moving average component in the error term.

Table 2. State-owned banks and GDP growth (dep. var: per capita GDP growth, 5-year average).

There is a positive correlation between state ownership and subsequent growth in the full sample of countries (column 1, ) and in the subsamples of emerging and developing economies (column 3) and middle-income countries (column 4). These results, however, are not robust to controlling for country fixed effects (columns 6–10). Taken together, these results suggest that there is a weak and rarely statistically significant positive correlation between state-ownership of banks and subsequent growth. There is no evidence in line with the negative correlation found in purely cross-sectional studies that use older data.

3.3 State-owned banks and banking crises

There is limited and mixed evidence on the link between state-ownership of banks and the incidence of banking crises (Cull, Soledad Martínez Pería, and Verrier Citation2018). Caprio and Martinez Peria (Citation2004) found that state-ownership of banks is positively associated with the prevalence of banking crises. La Porta, Rafael, and Shleifer (Citation2002), instead, find no statistically significant correlation between state ownership and the incidence of banking crises over 1970–1990, and Barth, Caprio, and Levine (Citation2004) found a positive univariate correlation between state-ownership of banks and the incidence of banking crises which, however, is not robust to controlling for other variables.

Reverse causality is an especially complicated issue because banking crises often lead to nationalization episodes (Laeven and Valencia, Citation2018) and studies which do not carefully control for the timing of the event may reach wrong conclusions. The dataset assembled for this paper is especially suitable to address this issue as it allows to carefully control for state-ownership before and after banking crises. With this objective in mind, I use a multivariate logit model to estimate the following specification:

where is a dummy variable that takes value one in the first year of a banking crisis (I drop from the sample all the crisis years after the first, the data are from Leaven and Valencia, Citation2018),

,

, and

are the lagged, contemporaneous, and future values of government ownership of banks, MIC and LIC are dummy variables that take value one for middle income- and low-income countries, respectively (high-income is the excluded group), GFC is a dummy that takes value one for the years of the global financial crisis (2008 and 2009), and

is a matrix of country-year level controls.

I start by estimating EquationEquation (7)(7)

(7) by only including state ownership (i.e., I set

). Column 1 of indicates that a higher level of state ownership at time

is negatively and significantly associated with the probability of observing a banking crisis at time

. It also shows that there is no significant contemporaneous correlation between state ownership and the likelihood of observing a banking crisis and that the share of state-ownership increases after the crisis. These findings are consistent with the idea that banking crises cause state-ownership, rather than the other way around. They are also consistent with Laeven and Valencia’s (Citation2018) data which show that a large number of banking crises are followed by nationalization episodes.

Table 3. State-owned banks and banking crises and logit model (dep. var: banking crisis dummy).

Column 2 shows that the results are robust to controlling for the middle-income and low-income dummies. These dummies show a higher incidence of banking crises in middle-income countries (low-income countries are not significantly different from high-income countries). Column 3 shows that, as expected, the incidence of banking crises increased during the global financial crisis. However, controlling for the GFC dummy does not alter the previous results. Finally, column 4 augments the model with the set of controls used by Demirgüç-Kunt and Detragiache (Citation2005). As expected, I find that banking crises are positively associated with currency depreciations, inflation, and credit growth. Controlling for these variables, I find that the coefficient associated with remains negative and statistically significant, while the coefficient of

remains positive but no longer significant.

Taken together, the results of suggest that there is no evidence that higher levels of state-ownership of banks predict banking crises over the period 1995–2018. There is some evidence that banking crises lead to an increase in state-ownership of banks.

4 Bank-ownership and performance

This section uses bank-level data to study the relationship between ownership and different measures of bank performance and activity. I start by looking at profitability, net interest margins (and separately at interest income and expenditure), and non-performing loans, I then check if state-owned banks are more likely to hold government bonds, and I conclude by studying the relationship between state-ownership and liquidity creation.

4.1 Profitability, interest margins and non-performing loans

I estimate, several versions of the following model:

where is a performance indicator for bank i, in country c, in year t,

is a dummy that takes value one for state-owned banks,

is a matrix of bank-level controls, and

and

are country-year and bank type fixed effects.Footnote6 Errors are clustered at the bank level. Note that even though

is time-varying, EquationEquation (8)

(8)

(8) does not include bank fixed effects because ownership changes are rare and the inclusion of fixed effects would only allow estimating the effect of ownership for the relatively small number of banks that changed ownership.

I consider the following performance indicators: (i) Returns on Assets (ROA); (ii) Net Interest Margin (NIM); and (iii) Non-Performing Loans/Loans. I use the following set of controls: (i) Log(assets); (ii) non-interest income/assets; (iii) customer deposits/assets; (iii) Loan/assets; and (iv) non-interest expenditure over assets.

I estimate EquationEquation (8)(8)

(8) separately for the sub-sample of advanced economies, middle-income economies, low-income economies, East-Asia and Pacific, East Europe and Central Asia, Latin America and the Caribbean, the Middle East and North Africa, South Asia, and sub-Saharan Africa. I also estimate models for the whole period, and for 1995–2009 and 2010–2018 separately. Given the large number of estimations involved in these exercises, I do not report tables with full regression results, but a set of graphs with the point estimates of

and the confidence intervals of these estimates. I also report results for a set of regressions that do not include bank type fixed effects.

Returns on assets

When I estimate the model for the full period (1995–2018), I tend to find a negative correlation between state-ownership and bank profitability (the exception is East Asia and Pacific). However, the correlation is only statistically significant at the 95% confidence level in emerging and developing economies (the coefficient is precisely estimated in middle-income countries) and in East Europe and Central Asia (top left panel of ). The results are essentially identical if I do not include bank specialization fixed effects (top right panel of ).

The bottom panel of shows substantial time heterogeneity. There is evidence that before 2010 state-owned banks located in developing and emerging markets had lower profitability than their private counterparts. The gap was particularly large in East Europe and Central Asia and in Latin America and the Caribbean. Instead, there was no differential between private and state-owned bank profitability in advanced economies. In the second part of the sample, instead, there is no statistically significant difference in profitability between private and public banks located in developing and emerging economies. However, a gap opened in advanced economies, with state-owned banks having profitability levels which are significantly lower than those of private banks.

Net interest margin

Data for the full period show that state-owned banks tend to have higher net interest margins than their private counterparts and that the difference between the two groups is statistically significant in middle-income economies, East Asia and Pacific, and Latin America and the Caribbean (top left panel of ).

As in the case of profitability, the relationship between state ownership and net interest margins changed over time (bottom panels of ). The higher net interest margins enjoyed by state-owned banks in Latin America are mostly driven by the pre-2010 period and those of East Asia are driven by the post-2009 period. Moreover, state-owned banks in East Europe had higher interest margins before 2010 and lower after 2010 (with the difference being statistically significant in the latter period).

Non-performing loans

The top left panel of shows that state-owned banks tend to have higher non-performing loans than their private counterparts in both advanced economies and emerging and developing economies. The difference is especially high in low-income economies and in South Asia and Latin America. The bottom panels of show again substantial over-time heterogeneity and indicate smaller differences in non-performing loans in the post-2009 period (the difference in non-performing loans is no longer statistically significant in both Latin America and sub-Saharan Africa).

4.2 Lending to the government

Large holdings of government bonds on bank balance sheets may amplify financial vulnerabilities through the bank-sovereign doom loop. IMF (Citation2020) documents that during the European sovereign debt crisis there was a substantial increase in holdings of government paper by state-owned banks and that in emerging and developing economies with high levels of public debt, state-owned banks hold more government bonds than private banks.

The top left panel of shows that holdings of government bonds by state-owned banks are significantly larger than holdings of government bonds by private banks in advanced economies, low-income economies, in Eastern Europe and Central Asia, and in Latin America and the Caribbean. Looking at sub-periods, we observe opposite trends for advanced economies and middle-income economies (bottom panels of ). While the relative share of government bonds held by state-owned banks increased rapidly in advanced economies after the European sovereign debt crisis of 2011–12, the opposite happened in middle-income economies.

Panizza (Citation2021) checks if state-owned banks hold more government bonds when public debt is high. In the full sample, there is evidence that in countries with high debt levels state-owned banks hold more public debt than their private counterparts. This finding is driven by the behavior of middle-income economies.

5 Cyclicality

One possible rationale for state-ownership of banks is that procyclical lending of private banks may reduce the effectiveness of countercyclical macroeconomic policies (Levy Yeyati et al., Citation2007). If this is the case, countercyclical lending by state-owned banks could be useful in smoothing the business cycle, especially during deep recessions.

To the best of my knowledge, Micco and Panizza (Citation2006) were the first to use bank-level data to show that lending by state-owned banks in emerging and developing economies is less procyclical than private bank lending. Several follow-up studies corroborated this result using both cross-country data and by focusing on individual countries (Önder and Özyıldırım Citation2013, Bonomo, Brito, and Martins Citation2015). A recent study by Ture (Citation2021) also finds that lending by state-owned banks is less procyclical than private bank lending, but that this is not the case in developing economies with high levels of public debt.

In this section, I update the analysis of Micco and Panizza (Citation2006) and also explore the role of heterogeneity, building on the work of Ture (Citation2021). I start by estimating the following model:

where is the growth rate of net loans (measured in USD) of bank

located in country

,

is real GDP growth in country

, year

, and all other variables are defined as above. In the set-up of Equationequation (10)

(10)

(10) ,

indicates that state-owned banks are less procyclical (or more countercyclical) than their private counterparts (the main effect of

is absorbed by the country-year fixed effects).

Column 1 of estimates EquationEquation (10)(10)

(10) by setting

. As in Micco and Panizza (Citation2006), I find that

is negative and statistically significant, consistent with the idea that state-owned banks contribute to macroeconomic stabilization. Columns 2 and 3 show that this result is robust to relaxing the assumption that

. In columns 4 and 5, I estimate separate models for advanced economies and emerging and developing economies and corroborate Micco and Panizza’s (Citation2006) finding that the countercyclical role of state-owned banks is only present in emerging and developing economies. Columns 6–11 of show that the results are also robust to running separate regressions for the pre and post-2009 period.

Table 4. Bank ownership and lending cyclicality (dep. var: growth of net loans).

I also check if the countercyclical role of state-owned banks reduces their profitability around the business cycle. I find no evidence in this direction. However, I do find some evidence that lending countercyclicality affects the cyclicality of non-performing loans.

explores the role of fiscal fundamentals. In columns 1–3, I allow for separate coefficients for high and low public debt country-years. High debt is defined as having a debt-to-GDP ratio above 100% for advanced economies and above 60% for developing and emerging economies. Contrary to what found by Ture (Citation2021), I do not find any difference in countercyclicality between high and low debt countries. If anything, countercyclicality seems higher in high debt countries (but the difference is not statistically significant). There are four key differences between my analysis and that of Ture (Citation2021): (i) a larger and longer sample (my sample of emerging and developing countries includes 29,800 observations, that of Ture about 3,000 observations); (ii) different coverage (my sample only includes commercial banks); (iii) I measure cyclicality using real GDP growth instead of using a deviation from trend growthFootnote7; and (iv) I include country-year fixed effects instead of macroeconomic controls. In future analyses, it would be interesting to explore which of these differences drives the different results.Footnote8

Table 5. Bank ownership, lending cyclicality, and fiscal fundamentals (dep. var: growth of net loans).

In the last three columns of , I use sovereign ratings as an encompassing measure of fiscal fundamentals. I allow for different coefficients for investment grade and non-investment grade country-years and find that countercyclicality is higher in non-investment grade countries.

6 Conclusions

There are opposing views on the role of state-owned banks. While the social and development views suggest that state-ownership of banks can address important market failures and promote financial deepening, the political view maintains that state-owned banks only exist to provide rents to the policymakers that control them and that state-owned banks have a negative effect on financial sector development and economic growth.

This paper uses new data on state-owned commercial banks and does not find strong evidence in support of either view of state-owned banks. At the macro-level, there is no evidence that state-ownership of banks predicts financial depth or economic growth. This could be due to the fact that state owned banks have no effect on these variables or to the endogeneity problem highlighted by Rodrik (Citation2012) and discussed in Section 3 of the paper. There is also no evidence that state-ownership increases the likelihood of financial crises.

At the micro-level, I find that recent data show decreasing profitability gaps between state-owned and private banks but indicate that state-owned banks tend to have more non-performing loans than private banks. Given that state-owned banks do not maximize profits, the presence of a profitability gap does not necessarily indicate that state-owned banks are inefficient. The lack of such a gap, however, suggests that there are no large opportunity costs linked to the presence of state-owned banks.

I also find that state-owned bank may contribute to macroeconomic stabilization. Specifically, I find that lending by state-owned banks is either countercyclical or less procyclical than lending by private banks. I also find that this stabilization role of state-owned banks does not lead to lower profitability and that countercyclical lending by state-owned banks is not mitigated by high public debt or by weak fiscal fundamentals as captured by sovereign credit ratings.

One key takeaway from my analysis is that there is substantial heterogeneity both across countries and across time and institutions within a country. Future research should focus on understanding the drivers of this heterogeneity.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Notes

1. These shares include state-owned development banks. State-ownership shares of commercial banks are 4–6 percentage points lower (see , below).

Bank ownership and lending to the government (dep. var government bond holding over assets). The spikes are 95% (in black) and 99% (in grey) confidence intervals.

Bank ownership and lending to the government (dep. var government bond holding over assets). The spikes are 95% (in black) and 99% (in grey) confidence intervals.

2. Besides these four main sources of data, the paper also uses information on banking crisis from Laeven and Valencia (Citation2018) and sovereign credit rating data from Fitch, Moody’s, and Standard & Poor’s. Details on the construction of the bank-level dataset are provided in Panizza (Citation2021).

3. The 20% threshold is standard in the literature because, as mentioned by La Porta, Rafael, and Shleifer (Citation2002), 20% ownership is typically sufficient for control. Ture (Citation2021) Frigerio and Vandone (Citation2018) and Cornett et al. (Citation2009). The results of this paper are robust to using a higher threshold for the state-ownership dummy.

4. I assume , because with

, the social planner problem yields the corner solution

.

5. Table 12 uses 5-year growth spells. I obtain similar results if I use 10-year growth spells

6. Bank types are: Bank holding company, Commercial bank, Credit union, Cooperative bank, Investment bank, Private bank, Savings bank.

7. I adopt this strategy because in emerging and developing countries trend growth is not well-defined (Aguiar and Gopinath Citation2007).

8. Another possible difference has to do with the role of global crises. Specifically, Ture (Citation2021) finds that high public debt in developing economies matters for cyclicality when she excludes the Global Financial Crisis from the sample.

References

- Aguiar, M., and G. Gopinath. 2007. “Emerging Market Business Cycles: The Cycle Is the Trend.” Journal of Political Economy 115 (1): 69–102. doi:10.1086/511283.

- Barth, J., G. Caprio, and R. Levine. 2004. “Bank Regulation and Supervision: What Works Best?” Journal of Financial Intermediation 13 (2): 205–248. doi:10.1016/j.jfi.2003.06.002.

- Beck, T., and R. Levine. 2004. “Stock Markets, Banks, and Growth: Panel Evidence.” Journal of Banking & Finance 28 (3): 423–442.

- Bertay, A. C., A. Demirgüç-Kunt, and H. Huizinga. 2015. “Bank Ownership and Credit over the Business Cycle: Is Lending by State Banks Less Procyclical?” Journal of Banking and Finance 50: 326–339. doi:10.1016/j.jbankfin.2014.03.012.

- Bonomo, M., R. Brito, and B. Martins. 2015. “The After-Crisis Government-Driven Credit Expansion in Brazil: A Firm-Level Analysis.” Journal of International Money and Finance 55: 111–134. doi:10.1016/j.jimonfin.2015.02.017.

- Brei, M., and A. Schclarek. 2013. “Public Bank Lending in Times of Crisis.” Journal of Financial Stability 9 (4): 820–830. doi:10.1016/j.jfs.2013.01.002.

- Butzbach, O., and K. von Mettenheim. 2015. “Alternative Banking and Theory.” Accounting, Economics, and Law: A Convivium 5 (2): 105–171.

- Coleman, N., and L. Feler. 2015. “Bank Ownership, Lending, and Local Economic Performance during the 2008–09 Financial Crisis.” Journal of Monetary Economics 71: 50–66. doi:10.1016/j.jmoneco.2014.11.001.

- Cornett, M., L. Guo, S. Khaksari, and H. Tehranian. 2009. “The Impact of State Ownership on Performance Differences in Privately-Owned versus State-Owned Banks: An International Comparison.” Journal of Financial Intermediation 19 (1): 74–94. doi:10.1016/j.jfi.2008.09.005.

- Cull, R., M. Soledad Martínez Pería, and J. Verrier. 2018. “Bank Ownership: Trends and Implications” WB Research Working Paper 8297

- Demirgüç-Kunt, Asli, and Enrica Detragiache. 2005. “Cross-Country Empirical Studies of Systemic Bank Distress: A Survey.” National Institute Economic Review 192 (1): 68–83.

- Duprey, T. 2015. “Do Publicly Owned Banks Lend against the Wind?” International Journal of Central Banking 11 (2): 65–112.

- European Bank for Reconstruction and Development. 2020. Transition Report, European Bank for Reconstruction and Development, London

- Fernandez-Arias, E., R. Hausmann, and U. Panizza. 2020. “Smart Development Banks.” Journal of Industry, Competition and Trade 20 (2): 395–420. doi:10.1007/s10842-019-00328-x.

- Frigerio, M., and D. Vandone. 2018.“Bank Ownership and Firm-Level Performance: An Empirical Assessment of State-Owned Development Banks”.Contemporary Issues in Banking,edited byM. García-Olalla,Clifton. 197–219. London: Palgrave Macmillan.

- Gerschenkron, A. 1962. Economic Backwardness in Historical Perspective. Cambridge, MA: Harvard University Press.

- Haas, D., Y. K. Ralph, A. Pivovarsky, and T. Tsankova. 2015. “Taming the Herd? Foreign Banks, the Vienna Initiative and Crisis Transmission.” Journal of Financial Intermediation 24 (3): 325–355. doi:10.1016/j.jfi.2014.05.003.

- Inter-American Development Bank. 2014. Rethinking Productive Development. Washington DC: Inter-American Development Bank.

- International Monetary Fund. 2020. Fiscal Monitor: April, International Monetary Fund. Washington DC.

- Kornai, J. 1979. “Resource-constrained versus Demand-constrained Systems.” Econometrica 47 (4): 801–819. doi:10.2307/1914132.

- Laeven, L., and F. Valencia. 2018. “Systemic Banking Crises Revisited.” In IMF Working Papers 18/206. Washinton DC: International Monetary Fund.

- Levy-Yeyati, E., A. Micco, and U. Panizza. 2007. “A Reappraisal of State-Owned Banks.” Economia 20: 209–259.

- Lewis, W. A. 1950. The Principles of Economic Planning. London: G. Allen & Unwin.

- Marois, T. 2021. “A Dynamic Theory of Public Banks (And Why It Matters).” Review of Political Economy 34: 356–371 Forthcoming.

- Marois, T. 2022. Public Banks: Decarbonisation, Definancialisation, and Democratisation. Cambridge: Cambridge University Press.

- Marshall, W., and L.-P. Rochon. 2019. “Public Banking and Post-Keynesian Economic Theory.” International Journal of Political Economy 48: 1, 60–75. doi:10.1080/08911916.2018.1550947.

- McDonald, D., T. Marois, and D. Barrowclough. 2020. Public Banks and COVID-19: Combatting the Pandemic with Public Finance. Geneva: UNCTAD.

- Micco, A., and U. Panizza. 2006. “Bank Ownership and Lending Behavior.” Economics Letters 93 (2): 248–254. doi:10.1016/j.econlet.2006.05.009.

- Micco, A., U. Panizza, and M. Yanez. 2007. “Bank Ownership and Performance. Does Politics Matter?” Journal of Banking & Finance 31 (1): 219–241. doi:10.1016/j.jbankfin.2006.02.007.

- Önder, Z., and S. Özyıldırım. 2013. “Role of Bank Credit on Local Growth: Do Politics and Crisis Matter?” Journal of Financial Stability 9 (1): 13–25. doi:10.1016/j.jfs.2012.12.002.

- Panizza, U. 2021. “State Owned Commercial Banks,” CEPR Discussion Papers 16259

- Porta, L., F. L.-D.-S. Rafael, and A. Shleifer. 2002. “Government Ownership of Banks.” Journal of Finance 57 (1): 265–301. doi:10.1111/1540-6261.00422.

- Rodrik, D. 2012. “Why We Learn Nothing from Regressing Economic Growth on Policies.” Seoul Journal of Economics 25: 137–151.

- Shleifer, A., and R. Vishny. 1994. “Politicians and Firms.” Quarterly Journal of Economics 109 (4): 995–1025. doi:10.2307/2118354.

- Stiglitz, J. 1994. “The Role of the State in Financial Markets.” Proceedings of the World Bank Annual Conference on Economic Development 1993. Washington: World Bank.

- Ture, E. 2021. Revisiting the Stabilization Role of Public Banks: Public Debt Matters. Washinton DC: International Monetary Fund WP.

- World Bank. 2001. Finance for Growth: Policy Choices in a Volatile World. Washington DC: World Bank.

- World Bank. 2012. “Global Financial Development Report 2013: Rethinking the Role of the State in Finance.” World Bank, Washington DC.