?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This research finds empirical evidence for the role of earnings quality as a mediator between good corporate governance (GCG) mechanisms and firm performance. The sample is 570 data manufacturing companies listed on the Indonesia Stock Exchange from 2015 to 2019. This research used multiple regression analysis. GCG mechanisms in this study measured by the proportion of independent board of commissioners, audit committee expertise, and frequency of audit committee meetings. The result shows that the proportion of independent board of commissioners and audit committee expertise does not affect earnings quality. On the other hand, institutional ownership and frequency of audit committee meetings affect earnings quality. However, the proportion of independent board of commissioners affects company performance. Institutional ownership, the frequency of audit committee meetings, audit committee expertise in accounting, and earnings quality do not affect company performance. This study provides a basis for investors to see the quality of GCG implementation which is a determinant of earnings quality as an investment consideration.

1. Introduction

Financial information cannot reflect all the changes in the operating activities of a business (Lev & Zarowin, Citation1999). Thus, companies should be more concerned about the importance of managing non-financial information to external parties (Faysal, Salehiet, and Moradi Citation2021). Non-financial information includes complementary information and other reporting tools, such as good corporate governance (GCG) implementation (Istianingsih, Citation2020; Istianingsih, Trireksani, & Manurung, Citation2020). This information is available in the annual reports of companies selling their shares on the Indonesia Stock Exchange (IDX).

Information about the activities of companies listed on the IDX must be presented in their annual reports. The obligation to present these financial reports is a requirement set by the competent institution in Indonesia – the OJK (Financial Services Authority). Business actors, such as management or financial accountants, might feel obliged to present reports with good company performance even if the performance is otherwise because management’s performance can be seen from the financial statements. One of the parameters used to measure performance is profit (Derbali Citation2021).

The agency theory implies an information asymmetry between the manager as an agent and the principal as the owner (Jensen & Meckling, Citation1976). Since managers have more information about a company’s internal condition and business prospects than investors, management should present accurate reports about the company’s condition to investors. However, the information provided may not reflect the real condition of the company (Sisaye Citation2021). This is due to differences in the interests of the agent and the principal (Scott, Citation2015). With this conflict of interest, incomplete information (asymmetry) may be presented in the financial statements, thereby making the financial statements misleading. Information asymmetry can decrease the quality of earnings.

When examining the problem of business investment in Indonesia, we need to take a look at the uniqueness of the GCG problem in Indonesia. The first problem relates to the role of independent commissioners who recently became the target of several political elites to enter this area. Is it true that they are able to properly oversee the direction of public company policies and are able to become a bastion for investors’ representatives in Indonesia? Another problem regarding GCG in Indonesia is the ownership structure of a public company. One of the ownership that is expected to be able to mediate the GCG conflict is the institutional owner. The hope is that this type of owner will be able to dampen management’s desire to tamper with profits so that the quality of financial reports also improves. In addition, we can see the results of the ACGA assessment that although it is still below the regional average score, the auditor’s score ranking and auditor regulation have a high enough score. But whether the quality of the regulator’s audit, for example the audit committee, is sufficient to reduce earnings management incentives that are detrimental to investors also needs to be examined more deeply.

This study analyzes the effect of GCG on earnings quality and the impact of earnings quality on the performance of companies in Indonesia, especially manufacturing companies listed on the IDX. We chose manufacturing companies listed on the IDX as the sample of this study because of the government’s policy to strengthen investment in the 2015–2019 RPJMN (National Medium Term Development Plan). The policy will be pursued by improving the investment and business climates to enhance the efficiency of the business licensing process. It promotes inclusive investment, especially by encouraging domestic investors to play a more significant role (Bappenas, Citation2015).

The study period is from 2015 to 2019 due to the global economic crisis that occurred in 2008, which was quite challenging for the Indonesian economy. After the crisis, the government implemented various policies to maintain economic stability. Indonesia economy started recovering before 2015, so 2014 ended with more robust macroeconomic stability performance and a process of economic adjustment towards a healthier direction (World-Bank, Citation2014).

The virtue of this research lies in tracing the role of GCG which is specifically highlighted as a basis for investors in public companies in Indonesia. Institutional ownership and the characteristics of the audit committee will be discussed in terms of effectiveness in meetings and expertise in accounting issues so that it can be seen that it is related to efforts to improve earnings quality, which is the spotlight of many parties for the assessment of the performance of public company management.

This paper is structured as follows: With the first section being an introduction, the remainder of the paper is divided into six sections. Section 2 argues the background of this research, Section 3 presents a theoretical literature review, Section 4 shows an empirical literature review and hypothesis development. Section 5 shows the research design consisting of methodology, measurement of variables and research model, Section 6 presents descriptive analysis, results of hypothesis testing, and interpretation. Section 7 presents the study’s summary and conclusions, limitations and scope for further research.

2. Background

One of the factors that is most likely to influence company performance is GCG (Man & Wong, Citation2013). GCG makes a company’s management more efficient. One way to achieve management efficiency is the application of an ‘actionless governance’ policy. Chen and Peng (Citation2020) stated that an ‘actionless governance’ policy is the best choice for all stakeholders to achieve long-term sustainable development. To support the issue of sustainable development, there are many important activities that management can do, for example choosing the right supplier in the company’s global supply chain activities (Shalke, Paydar, & Hajiaghaei-Keshteli, Citation2018). This ‘actionless governance’ can be attached to the proposition ‘to govern through non-interference’ to make it applicable in modern management. Thus, GCG’s contribution to corporate value creation is getting higher.

The concept of GCG aims to achieve transparency in corporate management for all users of financial statements and protect the interests of shareholders and creditors. Financial reports are essential in making investors’ economic decisions because company performance can be reflected in the resulting financial reports (Istianingsih, Citation2020). Company performance is an essential factor because it is an input for investors to make investment decisions. Implementing GCG also increases a company’s profitability so that the company’s survival will be more secure.

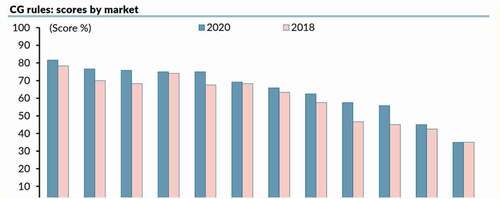

A survey conducted by the Asian Corporate Governance Association (ACGA) in Asian countries shows that Indonesia is in the last position in implementing GCG. The assessment covers five important aspects, including shareholder rights, fair treatment of shareholders, the role of stakeholders, disclosure and transparency as well as the responsibility of the board of commissioners.

The survey shows that the implementation of GCG in Indonesian was only 34% as against a target of 80%. This result has been used as an international standard. Indonesia has a long way to go to reach the 80% target; therefore, the phenomenon of GCG requires the support of the government. Evidence of the government’s concern can be seen from the issuance of various regulations governing GCG; one of them is the Minister of Finance Regulation Number: 88/PMK.06/2015 of 2015, which is about the implementation of GCG in companies under the guidance and supervision of the Minister of Finance.

shows that the condition in 2018 did not change for the better in 2020. Indonesia only scored 34% for market valuation and ranks twelfth out of twelve countries surveyed by Asian Corporate Governance Association (AGGA). While many believe that GCG reform will increase competitive advantage (Alazemi and Al Omari Citation2020). Then what about the investment prospects and seen from the performance of companies in Indonesia which are merely a complement to sufferers in the assessment of the implementation of GCG in ASIA.

Figure 1. Indonesia CG rules scores by market average (2018) and (2020)

The hope that GCG is able to reduce information asymmetry between stakeholders and improve the quality of earnings on which investors’ appraisals are based is certainly worth reviewing. The performance of companies in Indonesia, which is one of the benchmarks for investment, then needs to be questioned again.

When examining the problem of business investment in Indonesia, we need to take a look at the uniqueness of the GCG problem in Indonesia. The first problem relates to the role of independent commissioners who recently became the target of several political elites to enter this area. Is it true that they are able to properly oversee the direction of public company policies and are able to become a bastion for investors’ representatives in Indonesia? Another problem regarding GCG in Indonesia is the ownership structure of a public company. One of the ownership that is expected to be able to mediate the GCG conflict is the institutional owner. The hope is that this type of owner will be able to dampen management’s desire to tamper with profits so that the quality of financial reports also improves. In addition, we can see the results of the ACGA assessment that although it is still below the regional average score, the auditor’s score ranking and auditor regulation have a high enough score. But whether the quality of the regulator’s audit, for example the audit committee, is sufficient to reduce earnings management incentives that are detrimental to investors also needs to be examined more deeply.

The impact of implementing GCG can be directly observed in increasing business value. But indirectly, it can also be seen through the quality of the profits generated (Kwong, Mohamad, and Keong Citation2020). When the implementation of GCG in a company is exemplary, the supervisory function, which is the essence of GCG towards management, goes well (Alazemi and Al Omari Citation2020). The quality of financial reporting increases.

The quality of this report is seen from the quality of reported earnings. So what will be seen from this research is the mediating role of earnings quality on the relationship between GCG implementation and the business value of a company.

Most of the previous studies have tested the impact of GCG on earnings quality on business value. However, I consider the missing bridge to see the direct effect of implementing GCG on business value. The implementation of GCG is mainly to reduce agency problems, namely information asymmetry. This information asymmetry can be reduced by the transparency of the company’s management towards stakeholders. We know that one of the principles of GCG that must be met is transparency. Thus, information asymmetry can be reduced by implementing a monitoring mechanism through the implementation of GCG. When the monitoring role is good, the direct impact is on improving the quality of earnings reported by management.

Earnings number is a catchy number that investors always glance at. So that when the quality of reported earnings increases, it will increase stakeholder confidence in the company’s management. This trust will increase the value of the business in the eyes of investors. Thus, the implementation of GCG can be seen as impacting the value of this business directly and through the quality of earnings reported by management.

For example, the practical side of this research is from the observations and results of previous research on the role of auditors and commissioners. The appointment of commissioners in Indonesia is often based on the fact that they are former high-ranking officials but sometimes do not understand financial statements.

When the implementation of GCG has been imitated, it should reduce earnings management so that the quality of financial reports increases. This increase in earnings quality will serve as a bridge connecting the impact of GCG implementation on company value in the eyes of investors. This paper is different from Elzahaby (Citation2021), which tested the role of FP as a mediating relationship between GCG and EM with a sample of Egyptian listed firms during 2011–2017 using SEM. They found that FP significantly mediated the relationship between GCG and EM. Thus, the main idea of this paper is the role of earnings quality as a mediator of the relationship between GCG and business value.

3. Theoretical literature review

According to Scott (Citation2015), agency theory explains the contractual relationship between the principal and the agent. As an agent, a manager is responsible for maximizing the principal’s profit, and in return, the agent will be given a fee, as stipulated in the contract. As principal, shareholders are assumed to have only an interest in improving financial performance or their investment in a company (Gómez, Lagos, and Gómez-Betancourt Citation2017). Conversely, the agent is assumed to receive financial compensation. This difference in interests underlies the efforts of each party to increase their profits (Kyere and Ausloos Citation2021). The existence of information asymmetry is a source of problems in this relationship because the principal does not have sufficient information about the agent’s performance. But on the other hand, agents have more information about their capacities, work environment, companies and opportunities. This information gap is an opportunity for opportunistic profit engineering for management. One way to overcome information asymmetry is through the implementation of GCG. With the principles of transparency, accountability, responsibility, independence and fairness, it is hoped that GCG is able to improve the quality of earnings which is the reference for investment.

4. Empirical literature review and hypotheses development

4.1. Proportion of independent commissioners and earnings quality

The GCG mechanism is divided into two types – internal and external mechanisms (Istianingsih & Mukti, Citation2017). The internal mechanism is controlling a company by using its internal structures and processes, such as the general meeting of shareholders (GMS), the composition of board of directors and board of commissioners, managerial ownership, and meetings with the board of directors (Hamdan Citation2018). By contrast, the external mechanism is controlling a company by using external structures, such as control by the market. Other external mechanisms that also influence the company’s control, such as the government. Research (Mousavi, Hafezalkotob, Makui, & Sayadi, Citation2021) finds that the government intervenes in determining optimal hotel prices in competitive situations. GCG mechanisms that are often used to determine the quality of earnings are the composition of an independent board of commissioners.

Lin, Li, and Yang (Citation2006) stated that the audit committee’s role in ensuring the quality of the company’s financial reporting is significant. They examined the relationship between size, independence, financial expertise, activity, stock ownership, and earnings management. They show no evidence of a negative relationship between committee characteristics and earnings quality.

Alrayyes and Al Khaldy (Citation2019) analyzed the impact of GCG rules on earnings management in 13 public companies on the Palestine Exchange. They use GCG proxies in the form of a board of directors size, CEO duality, independence of the board of directors, property rights, number of board of directors meetings. Research by Alrayyes and Al Khaldy (Citation2019) found a negative effect between the size of the board of directors and CEO duality and between earnings management. However, they show a positive impact on the board of directors’ independence and earnings management. There is no relationship between the board of directors meetings and internal ownership with earnings management.

Nasiri and Ramakrishnan (Citation2020) stated that the proportion of independent commissioners does not affect a company’s earnings quality. However Fama and Jensen (Citation1983) stated that non-executive directors (independent commissioners) can act as mediators in disputes between internal managers and resolve management policies and advise management. Independent commissioners are in the best position to carry out the monitoring function to create an excellent CG company. Nasr and Ntim (Citation2018) findings show that board independence is positively related to accounting conservatism. The existence of independent commissioners who are not affiliated with owners and managers is a hope for the supervisory mechanism in order to reduce opportunistic profit manipulation opportunities. The higher the proportion of independent commissioners, the lower the chance for earnings management to increase the quality of earnings. Therefore, the following hypothesis is proposed:

Hypothesis 1 (H1): The proportion of independent commissioners affects earnings quality.

4.2. Institutional ownership and earnings quality

Institutional investors usually have better skills in financial reporting. They are smart investors in analyzing financial statements. Institutional owners play a role in monitoring company performance and preventing fraud in financial statements. Nasiri and Ramakrishnan (Citation2020) found that companies’ institutional ownership can affect the quality of reported earnings. The higher the institutional ownership, the lower the opportunity for opportunistic earnings management. The higher the institutional ownership, the better the quality of the reported earnings will be. Therefore, the following hypothesis is proposed:

Hypothesis 2 (H2): Institutional ownership affects earnings quality.

4.3. Frequency of audit committee meetings and earnings quality

The audit committee oversees the financial reporting process of a company. The effectiveness of the audit committee is reflected in their activities in attending meetings with the board of directors and providing input to management. It is assumed that an audit committee’s effectiveness in a company will minimize the possibility of manipulating reported earnings. Hamdan (Citation2020a) examined the impact of audit committee diligence/meetings on earnings quality in 23 industrial companies from the Gulf Cooperation Council (GCC) financial market during the 2014–2018 period. Hamdan (Citation2020b) reveals that audit committee persistence/meeting has no impact on earnings quality. On the other hand, Wasan and Mulchandani (Citation2019) showed that the frequency of audit committee meetings affects earnings quality. The more active they participate in meetings, the more effective the complaint committee is and the better the quality of earnings reported by management. Therefore, the following hypothesis is proposed:

Hypothesis 3 (H3): The frequency of audit committee meetings affects earnings quality.

4.4. Audit committee expertise in accounting and earnings quality

Kwong, Mohamad, and Keong (Citation2020) mentioned that one of the key determinants of an audit committee’s effectiveness is its finance expertise. Fraud and restatement of earnings are more prevalent when the members of the audit committee are not competent in finance. Elghuweel, Ntim, Opong, and Avison (Citation2017) examined the impact of the GCG mechanism on the earnings management behavior of 116 companies in Oman. They found that the GCG mechanism had an impact on EM. However, they found no evidence that board size, audit firm size, and a CG committee affect EM. Albedal, Hamdan, and Zureigat (Citation2020). found a relationship between audit committees and earnings quality of 40 companies listed on the Bahrain Stock Exchange during 2013–2017. Nasiri and Ramakrishnan (Citation2020) found a negative relationship between audit committee expertise in accounting and finance and earnings quality. Therefore, the following hypothesis is proposed:

Hypothesis 4 (H4): Audit committee expertise in accounting affects earnings quality.

4.5. Institutional ownership and company performance

Institutional ownership is one of the tools used as a supervisory mechanism for managerial shareholders to influence company performance. Nasiri and Ramakrishnan (Citation2020) and Koji, Adhikary, and Tram (Citation2020) studied the relationship between institutional ownership and company performance. They found that institutional ownership affects company performance. Therefore, the following hypothesis is proposed:

Hypothesis (H5): Institutional ownership affects company performance.

4.6. The proportion of independent commissioners and company performance

The board of commissioners in a company focuses more on the monitoring function of the implications of directors’ policies. The commissioners’ role is expected to minimize agency problems that may arise between the board of directors and shareholders. Boshnak’s (Citation2021) show that board size and independence, audit committee, and meeting frequency negatively impact firm performance However, Man and Wong (Citation2013) and Nasiri and Ramakrishnan (Citation2020) stated that an independent board of commissioners significantly affects firm value. The existence of an independent board of commissioners is a useful control tool of company performance. Therefore, the following hypothesis is proposed:

Hypothesis (H6): The proportion of independent commissioners affects company performance.

4.7. Audit committee expertise in accounting and company performance

Audit committee members who have expertise in finance help shareholders to read reports that have been presented by management. Moreover, they can help shareholders to measure company performance. Bhutta et al. (Citation2021) empirically examine the effect of managerial ability on firm performance. Using a sample of 246 companies listed on the Pakistan Stock Exchange from 2009 to 2017, this study finds that more capable managers significantly improve company performance while less qualified managers significantly reduce company performance. Wasan and Mulchandani (Citation2019) found that audit committee expertise in accounting has a significant effect on company performance. Therefore, the following hypothesis is proposed:

Hypothesis 7 (H7): Audit committee expertise in accounting affects company performance.

4.8. The frequency of audit committee meetings and company performance

As required by the Financial Services Authority, in carrying out its functions, duties, and responsibilities, the audit committee may hold periodic meetings. During audit committee meetings, the committee reviews the company’s current year’s performance and offer recommendations. Boshnak (Citation2021) examined the impact of GCG mechanisms, including board size, independence, meeting frequency, audit committee size and meeting frequency, CEO duality, and ownership concentration on Saudi listed companies’ operational, financial, and market performance. They show that board size and independence, audit committee, and meeting frequency have a negative impact on company performance. In addition, they also prove that performance increases with the frequency of board meetings and concentration of ownership. Therefore, the frequency of audit committee meetings can have a positive impact on company performance. Wasan and Mulchandani (Citation2019) proved that the frequency of audit committee meetings affects company performance. Therefore, the following hypothesis is proposed:

Hypothesis 8 (H8): The frequency of audit committee meetings affects company performance.

4.9. Earnings quality and company performance

Earnings quality is a profit that accurately describes a company’s profitability. Good quality earnings will lead to more informed investment decisions (Istianingsih, Citation2020; Istianingsih et al., Citation2020). The earnings quality of a company is related to the quality of management’s decision-making process, which has an impact on company performance. Istianingsih and Mukti (Citation2017) and Wasan and Mulchandani (Citation2019) studied the effect of earnings quality on company performance and found that earnings quality significantly affects company performance. Therefore, the following hypothesis is proposed:

Hypothesis 9 (H9): Earnings quality affects company performance.

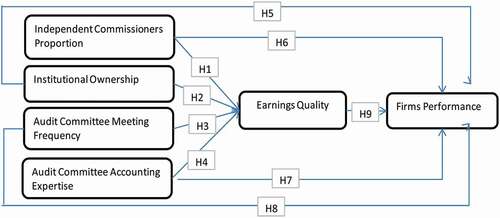

The relationships between the variables and indicators of each variable are depicted in .

Figure 2. Research model

5. Research design

5.1. Population and sample

All the sampled companies are manufacturing companies listed on the IDX. The research observation period is from 2015 to 2019. The companies were selected based on specific criteria (purposive sampling). The criteria are manufacturing companies listed on the IDX from 2015 to 2019; companies that did not make acquisitions or mergers during the research period; those that published annual and audited financial reports during the research year (in rupiah); companies with data on the variables under consideration.

5.2. Types and sources of data

The secondary data used in this study – the financial statements of manufacturing companies listed on the IDX from 2015 to 2019 – is from the website of IDX.

5.3. Definition and measurement of variables

The proportion of independent commissioners is measured by dividing the number of commissioners from outside the company (independent) by the total number of the company’s board of commissioners. Information about the number of independent commissioners is from each company’s annual reports, the Indonesian Capital Market Directory, and the IDX.

Institutional ownership is company shares owned by an institution or institutions. The indicator used to measure institutional ownership is the percentage of the total shares of a company owned by institutional parties.

An audit committee is a committee formed by the board of commissioners to assist the board of commissioners to fulfill its supervisory responsibilities. Their job includes reviewing audited annual and financial reports, reviewing the financial reporting process and internal control system, and overseeing the audit process. OJK requires the audit committee to conduct regular meetings, at least once in three months. Data on the frequency of audit committee meetings are found in the company’s published annual report.

Apart from being required to hold regular meetings, at least once in three months, the audit committee must have at least one member with an educational background and expertise in accounting and finance. Information about the expertise of audit committee members is presented in the company’s annual report.

In this study, earnings quality is measured by the proxy for discretionary accruals in the modified Jones Model (Dechow, Sloan, & Sweeney, Citation1995) which was also used in Zalata, Ntim, & Choudhry (Citation2019b). The model is written as follows

The total accrual value (TA), which is estimated with the ordinary least square (OLS) regression equation, is as follows:

By using the regression coefficient above the value of non-discretionary accruals can be calculated with the following formula:

Furthermore, the discretionary accruals (DA) can be calculated as follows:

The variables used in the equations above are defined below:

DACCit = Discretionary accruals of company i in period t

NDAit = Non-discretionary accruals of company i in period t

TACCit = Total accruals of company i in period t

Nit = Net income of company i in period t

CFOit = Cash flows from operating activities of company i in period t

Ait-1 = Total assets of company i in period t-1

ΔREVit = Change in company’s revenue in period t

PPEit = Fixed assets of company i in period t

ΔRecit = Change in receivables of company i in period t

e = error term

If the total accruals are the same as non-discretionary accruals (TACCit = NDAit), or DACCit = 0, it implies that the company does not carry out earnings management. If the value of discretionary accruals is further away from 0, it indicates that the company has a low earnings quality.

In this study, return on assets is used as a proxy of company performance and is defined as follows:

5.4. Analysis technique

Descriptive statistical analysis methods, data normality test, classical assumption test, and hypothesis test are used in this study. Based on the influence of CG and leverage on earnings quality, the first regression equation is as follows

The variables in EquationEquation (1)(1)

(1) are defined below:

DACCit = Discretionary accrual as a measurement of earnings quality

β0 = Constant

β1 – β6 = Regression coefficient

ICPit = Proportion of independent commissioners of company i in period t

INSTOWNERit = Institutional ownership of company i in period t

MEETINGit = Frequency of the company i’s audit committee meetings of company i in period t

EXPERTISEit = Audit committee members accounting expertise of company i in period t

e = error term

A second regression equation is used to test the hypothesis about the effect of CG and earnings quality on company performance as follows:

The variables in EquationEquation (2)(2)

(2) are defined below:

PERFORMit = Firm performance of company i in period t

β0 = Constant

β1 – β6 = Regression coefficient

DACCit = Earnings quality of company i in period t

ICPit = Proportion of independent commissioners of company i in period t

INSTOWNERit = Institutional ownership of company i in period t

MEETINGit = Frequency of the company i’s audit committee meetings of company i in period t

EXPERTISEit = Audit committee members accounting expertise of company i in period t

e = error term

6. Empirical results and discussion

6.1. Empirical results

6.1.1. Descriptive object of research

We obtained 141 manufacturing companies from the IDX website (www.IDX.co.id). After -employing a purposive sampling method based on predetermined criteria, a sample of 114 companies was obtained. The study period is five years, so the total years of observation 570.

6.1.2. Descriptive statistic

Descriptive statistical analysis was used to determine the trend of each research variable.

shows that PT Tiga Pilar Sejahtera Food Tbk had the lowest ICP value (0.200) in 2016. The company with the highest ICP value (0.600) from 2015 to 2019 is PT Suparma Tbk. The average value of PDKI is 0.40006, indicating that, on average, the proportion of independent board of commissioners is 40%.

Table 1. Market category scores of good corporate governance in Asia

shows the frequency of audit committees meetings ranges from 2 to 13 times a year with an average value of six times. PT Lion Metal Works Tbk had the lowest (twice) frequency of audit committee meeting. PT Surya Toto Indonesia Tbk had the highest frequency of audit committee meeting (13). The mean of the frequency of audit committee meeting indicates that, on average, the manufacturing companies held approximately six meetings a year. This number meets the requirement of the Financial Services Authority Regulation No. 55/POJK.04/2015 which states that an audit committee is required to hold regular meetings at least once in three months or four times a year.

Table 2. Description of research variables

The number of audit committee members with expertise in accounting ranges from 0 to 3 with an average of 1.8. The mean value is 1.8, indicating that, from 2015 to 2019, on average, approximately two members of the audit committees of the manufacturing companies had expertise in accounting. This number meets the requirement of the Financial Services Authority Regulation No.55/POJK.04/2015 about the Establishment and Guidelines for Audit Committee Work Implementation Chapter II article 7 (e). It states that “audit committee members must have at least 1 (one) member with educational background and expertise in accounting and finance

The values of earnings quality range from 0.0002 to 0.2100, with an average value of 0.052939. The lower the discretionary accruals value, the higher the earnings quality. The value of company performance has average value of 0.0477. Company performance measures a company’s ability to generate profits at a certain level of income, assets, and share capital.

6.1.3. Hypothesis test

shows that the R Square’s value is 0.161; this means that 16.1% of the variation in earnings quality can be explained by the proportion of independent commissioners (ICP), institutional ownership (INSTOWNER), frequency of audit committee meetings (MEETING), and audit committee expertise in accounting (EXPERTISE). Moreover, the remaining 83.9% is explained by other factors outside the regression model.

Table 3. Determination coefficient test (1)

shows the significance value of 0.001 is smaller than the threshold of 0.05, which means that the model is good and can be used to predict the hypothesis.

Table 4. Model test

6.1.4. Regression test for Model 1

shows the regression coefficient of ICP is −0.087, implying that a 1% increase in ICP reduces discretionary accruals by 0.087, assuming that earnings quality increases as the other independent variables remain constant. The results of the hypothesis test indicate that ICP has a significance value of 0.059. H1 is rejected. Therefore, the proportion of independent commissioners does not affect earnings quality.

Table 5. T-test result for Model 1

INSTOWNER has coefficient 0.062, and significant so H2 is accepted. Therefore, institutional ownership has a significant effect on earnings quality.

The MEETINGS coefficients −0.003, and significant. H3 is accepted. Therefore, the frequency of audit committee meeting has a significant effect on earnings quality.

The variable of EXPERTISE is −0.003, implying that a 1% increase in EXPERTISE reduces discretionary accrual by 0.003. EXPERTISE has a significance value so H4 is rejected. Therefore, audit committee expertise in accounting does not affect earnings quality.

show that the R Square’s value is 0.344, implying that ICP, KI, KA, meeting frequency, KA membership expertise, leverage, and earnings quality (DACC) explain 34.4% of the variation in company performance. Thus, other factors outside the regression model explain 65.6% of the variation.

Table 6. Coefficient determination model summary

show the significance value of 0.000 is less than 0.05 so Model 2 is good to predict the hypothesis.

Table 7. Model 2 test

show the regression coefficient of ICP is significant and implies the proportion of independent commissioner affects company performance. The regression coefficient of INSTOWNER has a significance value so institutional ownership proofed affects company performance.

Table 8. T-test for Model 2

The MEETINGS variable has a significance value greater than 0.05, implying that the result is not significant. While the EXPERTISE value is not significance. The audit committee expertise in accounting does not affect company performance. The coefficient of DACC is greater than 0.05, implying that earnings quality does not affect company performance.

6.2. Discussion

6.2.1. The effect of the proportion of independent board of commissioners on earnings quality

H1 predicts that the proportion of independent commissioners affected the quality of earnings in manufacturing companies listed on the IDX from 2015 to 2019 (0.059 > 0.05). However, this study finds that the proportion of independent commissioners does not affect earnings quality, so H1 is rejected.

This result is consistent with those in the studies of Wasan and Mulchandani (Citation2019) and Al-Absy and Ntim (Citation2020) who found that the proportion of independent commissioners does not affect earnings quality. This result is due to the weak competence and integrity of the independent board of commissioners. Al-Absy and Ntim (Citation2020) revealed that, generally, a company’s independent commissioners are only a formality to meet regulatory requirements since the majority shareholder still plays an important role. The intermediate portion of a company’s independent board of commissioners is only 40%, and this value is not enough enough to provide adequate control over management performance. Although, in theory, the presence of independent commissioners increases management’s independence, if they are the minority, it does not maximize the independent board of commissioners’ right to function. The proportion of independent commissioners is not a significant factor in the effectiveness of supervising a company’s management.

6.2.2. The effect of institutional ownership on earnings quality

H2 predicts that institutional ownership affected the earnings quality of manufacturing companies listed on the IDX from 2012 to 2016. After testing the hypothesis, the significance probability value (0.008) is less than 0.05 (0.008 < 0, 05). Therefore, institutional ownership affects earnings quality, so H2 is accepted.

This result is inconsistent with those in the studies of Istianingsih and Mukti (Citation2017), Nasiri and Ramakrishnan (Citation2020) and Tehranian (Citation2006), which state that institutional ownership does not affect earnings quality. This study supports research conducted by Kwong et al. (Citation2020) which stated that institutional ownership affects earnings quality. The results of this study show that, on average, 74% of the shares of the manufacturing companies listed on the IDX is owned by institutions. In carrying out supervisory function, institutional ownership can influence financial reports prepared by management. However, management is more likely to report good company performance according to shareholders’ expectations; this is due to investors who do not consider the numbers in financial statements; their only concern is the profits generated by the company.

6.2.3. The effect of the frequency of audit committee meetings on earnings quality

H3 predicts that the frequency of audit committee meetings affected the earnings quality of manufacturing companies listed on the IDX from 2015 to 2019. Therefore, the frequency of audit committee meeting affects earnings quality, so H3 is accepted.

This result is consistent with the hypothesis formulated and does not support the research conducted by Hajawiyah, Wahyudin, Kiswanto, and Pahala (Citation2020) which concluded that the frequency of audit committee meetings does not guarantee that the audit committee can monitor financial reports to detect inaccuracies. This study supports the studies of Kwong et al. (Citation2020) and Koji et al. (Citation2020) which stated that the frequency of audit committee meetings affects earnings quality. The descriptive statistics show that, on average, each company conducts approximately 6 (six) meetings in a year, indicating that the audit committee’s role has been carried out optimally. Audit committee meetings are held not only to comply with the provisions of the Financial Services Authority No. 55/POJK.04/2015 about the Establishment and Guidelines for the Work Implementation of the Audit Committee, which requires the audit committee to hold regular meetings, at least once in three months but also audit committee meetings are conducted to effectively to provide oversight of earnings quality.

6.2.4. The effect of the audit committee expertise in accounting on earnings quality

H4 predicts that audit committee accounting expertise affected the earnings quality of manufacturing companies listed on the IDX from 2015 to 2019. After testing the hypothesis, the significance probability value (0.481) is greater than the threshold of 0.05 (0.481 > 0.05). Therefore, audit committee expertise in accounting does not affect earnings quality, so H4 is rejected.

This result is not consistent with the hypothesis formulated and supports the research conducted by Hajawiyah (2020) which stated that audit committee members’ education level does not influence earnings quality. The obligation of the audit committee to have audit members who have expertise in accounting and finance is only necessary to comply with regulatory requirements stipulated in the provisions of the Financial Services Authority about the Establishment and Guidelines for the Work Implementation of the Audit Committee. This regulation requires an audit committee to have at least one member with an educational background and expertise in accounting and finance. Audit committee members who have an educational background in accounting cannot necessarily adopt accounting standards and play an active role in controlling and supervision to improve earnings quality. As seen from the average value in the descriptive statistics, which shows a mean of 1.8, the earnings quality is also due to the low number of corporate audit committees with expertise in accounting.

6.2.5. The effect of institutional ownership on company performance

H5 predicts that institutional ownership affected the performance of manufacturing companies listed on the IDX from 2015 to 2019. After testing the hypothesis, the significance probability value of 0.014 is less than the threshold of 0.05 (0.014 < 0, 05). Therefore, institutional ownership affects company performance, so H5 is accepted.

This result is consistent with the hypothesis formulated and support the research conducted by Koji et al. (Citation2020) in Japan, which stated that institutional ownership has a significant effect on company performance. The average institutional ownership in this study is 73.6%, representing majority ownership and implying that institutional ownership provides more oversight of company performance.

6.2.6. The effect of the proportion of independent board of commissioners on company performance

H6 predicts that the proportion of independent commissioners affected the performance of manufacturing companies listed on the IDX from 2015 to 2019. After testing the hypothesis, the significance probability value (0.030) is less than 0.05 (0.030 < 0.05). Therefore, the proportion of independent commissioners affects company performance, so H6 is accepted.

This result is inconsistent with the hypothesis formulated and supports the research conducted by Koji et al. (Citation2020) but following Laporšek, Dolenc, Grum, and Stubelj (Citation2021). Independent commissioners who are not related to the company through family relationships, management, and share ownership will be more objective and not interfere with decision making and company performance.

The result of the mediation test shows that t-count = 1.0333, which is less than t-table (1.98), with a significance level of 0.05. Therefore, there is no mediating effect of earnings quality on the relationship between the proportion of independent commissioners and company performance.

The mediation test results show that t-count = 1.2613, which is smaller than t-table (1.98), with a significance level of 0.05. Therefore, there is no mediating effect of earnings quality on the relationship between institutional ownership and company performance.

6.2.7. The effect of the audit committee expertise in accounting on company performance

H7 predicts that audit committee expertise in accounting affected the performance of manufacturing companies listed on the IDX from 2015 to 2019. After testing the hypothesis, the significance probability value of 0.795 is greater than 0.05. (0.795 > 0.05). Therefore, audit committee expertise in accounting does not affect company performance, so H7 is rejected.

This result is not consistent with the hypothesis formulated and does not support the research conducted by Wasan and Mulchandani (Citation2019) which stated that audit committee expertise in accounting significantly affects company performance. This study’s result supports the research conducted by Wasan and Mulchandani (Citation2019) which stated that audit committee expertise in accounting does not affect company performance. On average, the sampled companies had two members who have expertise in accounting and finance, which is relatively low. Audit committee members who have expertise in accounting only fulfill existing regulatory requirements since the audit committee members may not necessarily influence company performance.

The results of the mediation test results show that t-count = 1.316, with a significance level of 0.05. The result indicates that there is no mediating effect of earnings quality on the relationship between an audit committee expertise in accounting and company performance.

6.2.8. The effect of audit committee meeting frequency on company performance

H8 predicts that the frequency of audit committee meetings affected the performance of manufacturing companies listed on the IDX from 2015 to 2019. After testing the hypothesis, the significance probability value of 0.771 is greater than 0.05 (0.771 > 0.05). Therefore, the frequency of audit committee meeting does not affect company performance, so H8 is rejected.

This result is not consistent with the hypothesis formulated and does not support the research conducted by Kwong et al. (Citation2020) and Tehranian, Cornett, Marcus, and Saunders (Citation2006). This study supports the research of Wasan and Mulchandani (Citation2019) which stated that the frequency of audit committee meetings does not affect company performance. This study indicates that an increase in company performance is not related to frequent audit committee meetings. The average number of the frequency of audit committee meetings is six times a year. However, these meetings are not necessarily held to discuss the company’s performance in the current year to improve the company’s future performance.

The mediation test results show that t-count = 1.375, which is smaller than t-table (1.98), with a significance level of 0.05, so it can be concluded that there was no mediating effect of earnings quality on the relationship between the frequency of audit committee meetings and company performance.

6.2.9. Effect of earnings quality on company performance

H9 predicts that earnings quality affected firm performance. After testing the hypothesis, the significance probability value is greater than the standard. Therefore, earnings quality does not affect company performance. H9 is rejected.

This result is not consistent with the hypothesis formulated and does not support the research conducted by Febrilyantri and Istianingsih (Citation2018) which stated that earnings quality affects company performance. This study supports the research conducted by Gaio and Raposo (Citation2011) which stated that the quality of earnings reported by management does not improve company performance. Thus, earnings quality is not one of the factors considered by investors when deciding to invest in companies because earnings quality cannot be used as a guide in decision making since management can act optimistically when reporting company profits.

7. Summary and conclusion

Based on the research results, the following conclusions are drawn. The proportion of independent commissioners does not affect earnings quality. Institutional ownership has a negative effect on earnings quality. The frequency of audit committee meetings has a positive influence on earnings quality. Audit committee expertise in accounting does not affect earnings quality. The proportion of independent commissioners has a negative effect on company performance. Institutional ownership has a negative effect on company performance. The frequency of audit committee meetings does not affect company performance. Audit committee expertise in accounting does not affect company performance. Earnings quality does not affect company performance.

This study’s results can be used by stakeholders, especially investors, to consider using CG to control those involved in managing a company to reduce the occurrence of agency problems. Following Muhamad et al. (Citation2021) stated that the GCG mechanism plays an essential role in ensuring that stakeholders receive reliable and relevant financial information regarding the company’s performance.

Companies are expected to implement GCG since, as shown by the survey results from the ACGA, the rate of the implementation of CG in Indonesia is low. The ACGA report indicates that the implementation of CG in Indonesian has only reached 36% of the 80% target, which is used as international standards. Thus, management will show an excellent financial performance of a company to increase lenders’ trustworthiness. This paper agrees with Salehi and Moghadam (Citation2019), which focuses on managerial characteristics and company performance. The results of this study may be beneficial for investors to assess the company’s performance. They can estimate the value of their investment by looking at the implementation of GCG and the quality of earnings reported by the company (Hasheda and Almaqtarib Citation2021. Earnings management practices will likely increase, so the reported earnings will be of less quality.

This study has several limitations that may affect the research results. These limitations are (1) the sample used was only 570 firm-year data, so it is possible to affect the generalization of the research results. (2) This research is limited to manufacturing companies listed on the IDX. The results of this study are expected to be used as a reference by academics who want to learn more about the influence of the proportion of independent board of commissioners, institutional ownership, frequency of audit committee meetings, audit committee expertise in accounting, and leverage on earnings quality of manufacturing companies while controlling for firm size. Further research can measure the intervention variables with real earnings management models. Substitute following Zang (Citation2011) that there is a trade-off between accrual earnings management and earnings management through real activities. In addition, we convey that further research needs to choose one method such as the Fixed or Random Effect Regression method.

A company’s management is expected to continue to increase the value of the company by reporting the company’s actual financial performance to provide relevant and useful information through published annual financial reports so that the earnings reported by management will be of high quality. Companies should also consider implementing GCG because a well-managed company can attract potential investors to the company.

Investors and potential investors should be careful when making business decisions; they should focus on both earnings and non-financial information, such as the existence of an internal company mechanism. The results of this study provide helpful information for the accounting profession, regulators, and potential investors about the effectiveness of audit committee practices in Indonesia. Future research can develop a more accurate profit management model, such as by industry. By developing a model at the industry level, researchers can identify different patterns of earnings management in each industry. Moreover, future research can use more samples from the IDX, extend the research period, and add other variables that can improve earnings quality and company performance.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

References

- Al-Absy, M. S., & Ntim, C. G. (2020). The board chairman’s characteristics and financial stability of Malaysian-listed firms. Cogent Business & Management, 7(1), 1.

- Alazemi, M., & Al Omari, A. M. (2020). The application level of institutional governance in Islamic institutions and banks in Kuwait. International Journal of Business Ethics and Governance, 3(3), 85–101.

- Albedal, F., Hamdan, A. M., & Zureigat, Q. (2020). Audit committee characteristics and earnings quality: Evidence from Bahrain Bourse. In Corporate governance models and applications in developing economies (pp. 23–49). Published in the United States of America by IGI Global. DOI:https://doi.org/10.4018/978-1-5225-9607-3.ch002

- Alrayyes, Y., & Al Khaldy, N. (2019). The impact of governance rules on earnings management: Applied study on industrial and service companies listed on Palestine stock exchange. International Journal of Business Ethics and Governance, 2(3), 104–138.

- Jamie Allen, 2020. Asian Corporate Governance Association (ACGA) special report 2020.

- Bappenas. (2015). Laporan Akhir: Penyusunan Konsep Rancangan RPJMN (Rencana Pembangunan Jangka Menengah Nasional (2015–2019)): Pembangunan Berkelanjutan.

- Bhutta, A. I., Sheikh, M. F., Munir, A., Naz, A., Saif, I., & Ntim, C. G ( Reviewing editor). (2021). Managerial ability and firm performance: Evidence from an emerging market. Cogent Business & Management, 8, 1.

- Boshnak, H. A. (2021). Corporate governance mechanisms and firm performance in Saudi Arabia. International Journal of Financial Research, 12(3), 446.

- Chen, Z., & Peng, J. (2020). Competition strategy and governance policy for the dual international supply chains under trade war. International Journal of Management Science and Engineering Management, 15(3), 196–212.

- Dechow, P., Sloan, R., & Sweeney, A. (1995). Detecting earnings management. Accounting Review, 70(2), 193–225.

- Derbali, A. (2021). Determinants of the performance of Moroccan banks. Journal of Business and Socio-economic Development, 1(1), 102–117.

- Elghuweel, M. I., Ntim, C. G., Opong, K. K., & Avison, L. (2017). Corporate governance, Islamic governance and earnings management in Oman: A new empirical insights from a behavioural theoretical framework. Journal of Accounting in Emerging Economies, 7(2), 190–224.

- Elzahaby, M. A. (2021). How firms’ performance mediates the relationship between corporate governance quality and earnings quality? Journal of Accounting in Emerging Economies, 11(2), 278–311.

- Fama, E. F., & Jensen, M. C. (1983). Agency problems and residual claims. The Journal of Law & Economics, 26(2), 2.

- Faysal, S., Salehi, M., & Moradi, M. (2021). Impact of corporate governance mechanisms on the cost of equity capital in emerging markets. Journal of Public Affairs, 21(2), e2166.

- Febrilyantri, C., & Istianingsih. (2018). The influence of intellectual capital and good corporate governance on earnings response coefficient (Case study on banks listed on IDX 2013–2015). International Journal of Science and Research (IJSR), 7(9), 69–76.

- Gaio, C., & Raposo, C. (2011). Earnings quality and firm valuation: International evidence. Accounting and Finance, 51(2), 467–499.

- Gómez, J. M., Lagos, D., & Gómez-Betancourt, G. (2017). Effect of the board of directors on firm performance. International Journal of Economic Research, 14(6), 349–361.

- Hajawiyah, A., Wahyudin, A., Kiswanto, S., & Pahala, I. (2020). The effect of good corporate governance mechanisms on accounting conservatism with leverage as a moderating variable. Cogent Business & Management, 7(1), 1–12.

- Hamdan, A. (2018). Board interlocking and firm performance: The role of foreign ownership in Saudi Arabia. International Journal of Managerial Finance, 14(3), 266–281.

- Hamdan, A. (2020a). The role of the audit committee in improving earnings quality: The case of industrial companies in GCC. Journal of International Studies, 13(2), 127–138.

- Hamdan, A. M. M. (2020b). Audit committee characteristics and earnings conservatism in banking sector: Empirical study from GCC. Afro-Asian Journal of Finance and Accounting, 10(1), 1–23.

- Hasheda, A. A., & Almaqtarib, F. A. (2021). The impact of corporate governance mechanisms and IFRS on earning management in Saudi Arabia. Accounting, 207–224. doi:https://doi.org/10.5267/j.ac.2020.9.015

- Istianingsih. (2020). The effect of corporate social responsibility and good corporate governance on pharmaceutical company tax avoidation in Indonesia. Systematic Reviews in Pharmacy, 11(12), 977–983.

- Istianingsih, & Mukti, A. H. (2017). Does corporate governance as a moderating variable influence the relationship between asymmetry information and earning management? International Business Management, 11(4), 859–864.

- Istianingsih, Trireksani, T., & Manurung, D. T. (2020). The impact of corporate social responsibility. Disclosure on the future earnings response coefficient (ASEAN banking analysis). Sustainability, 11, 1–16.

- Jensen, M. C., & Meckling, W. H. (1976). Theory of the firm: Managerial behavior agency costs and ownership structure. Journal of Financial Economics, 3(4), 305–360.

- Koji, K., Adhikary, B. K., & Tram, L. (2020). Corporate governance and firm performance: A comparative analysis between listed family and non-family firms in Japan. Journal of Risk and Financial Management, 13(215), 1–20.

- Kwong, G. W., Mohamad, S., & Keong, O. C. (2020). Corporate governance and earnings management: Evidence from listed Malaysian firms. International Journal of Psychosocial Rehabilitation, 24(4).

- Kyere, M., & Ausloos, M. (2021). Corporate governance and firms financial performance in the United Kingdom. International Journal of Finance & Economics, 26(2), 1871–1885.

- Laporšek, S., Dolenc, P., Grum, A., & Stubelj, I. (2021). Ownership structure and firm performance – The case of Slovenia. Economic Research-Ekonomska Istraživanja, 1–23. doi:https://doi.org/10.1080/1331677X.2020.1865827

- Lev, B., & Zarowin, P. (1999). The boundaries of financial reporting and how to extend them. Journal of Accounting Research, 37(2), 353–385.

- Lin, J. W., Li, J. F., & Yang, J. S. (2006). The effect of audit committee performance on earnings quality. Managerial Auditing Journal, 21(9), 921–933.

- Man, C. K., & Wong, B. (2013). Corporate governance and earnings management: A survey literature. Journal of Applied Business Research, 29(2), 391–418.

- Mousavi, E. S., Hafezalkotob, A., Makui, A., & Sayadi, M. K. (2021). Hotel pricing decision in a competitive market under government intervention: A game theory approach. International Journal of Management Science and Engineering Management, 16(2), 83–93.

- Muhamad, S. F., Muhamad, F. H., Rahman, A. H. A., Muhammad, M. Z., Samad, N. S. A., & Bahari, N. (2021). Published in: The importance of new technologies and entrepreneurship in business development. In The context of economic diversity in developing countries. Springer International Publishing. Editors: Alareeni, Bahaaeddin, Hamdan, Allam, Elgedawy, Islam (Eds.)

- Nasiri, M., & Ramakrishnan, S. (2020). Earnings management, corporate governance and corporate performance among Malaysian listed companies. Journal of Environmental Treatment Techniques, 8(3), 1124–1131.

- Nasr, M. A., & Ntim, C. G. (2018). Corporate governance mechanisms and accounting conservatism: Evidence from Egypt. Corporate Governance, 18(3), 386–407.

- Ramli, R., & Erna, S. (2021). Comparative analysis of good corporate governance implementation based on ASEAN corporate governance scorecard from the indonesian banking industry. Jurnal Keuangan Dan Perbankan, 25(1), 117–131.

- Salehi, M., & Moghadam, S. M. (2019). The relationship between management characteristics and firm performance. Competitiveness Review, 29(4), 440–461.

- Scott, W. R. (2015). Financial accounting theory (7th ed.). Toronto: Pearson Canada Inc.

- Shalke, P. N., Paydar, M. M., & Hajiaghaei-Keshteli, M. (2018). Sustainable supplier selection and order allocation through quantity discounts. International Journal of Management Science and Engineering Management, 13(1), 20–32.

- Sisaye, S. (2021). The influence of non-governmental organizations (NGOs) on the development of voluntary sustainability accounting reporting rules. Journal of Business and Socio-Economic Development, 1(1), 5–23.

- Tehranian, H., Cornett, M. M., Marcus, A. J., & Saunders, A. (2006). Earnings management, corporate governance, and true financial performance. SSRN Electronic Journal. doi:https://doi.org/10.2139/ssrn.886142

- Wasan, P., & Mulchandani, K. (2019). Corporate governance factors as predictors of earnings management. Journal of General Management, 45(2), 71–92.

- World-Bank. (2014, March). Indonesia economic quarterly investment in flux. www.worldbank.org/id.

- Zalata, A. M., Ntim, C., Aboud, A., & Gyapong, E. (2019). Female CEOs and core earnings quality: New evidence on the ethics versus risk-aversion puzzle. Journal of Business Ethics, 160(2), 515–534.

- Zang, A. (2011). Evidence on the trade-off between real activities manipulation and accrual-based earnings management. The Accounting Review, 87, 675–703.

- Zalata, A. M., Ntim, C. G., Choudhry, T., Hassanein, A., & Elzahar, H. (2019b). Female directors and managerial opportunism: Monitoring versus advisory female directors. The Leadership Quarterly, 30(5), 101309.