Abstract

Trading in energy derivatives is subjected to a fragmented regulatory framework which is largely designed for capital markets. Since 2011, a tailor made regime for the energy sector is in place; REMIT. Market participants need to find their way in this diverse set of obligations and prohibitions. This article describes the regulatory paradigm to which market participants need to adhere and the practical impact on trading in energy derivatives. Data reporting obligations, position limits and the prohibition on insider trading, market manipulation and the disclosure of inside information are discussed in more detail. The article concludes that REMIT fills in a regulatory gap, but its existence is not necessarily inevitable to capture energy derivative trading under a supervisory regime which is adapted to the specifics of energy markets.

Introduction

Background

In 2021, the regulation on wholesale energy market integrity and transparency (“REMIT”) celebrates its 10th anniversary.Footnote1 Time to look back and reflect on the necessity of this regulatory instrument which aimed to bridge a gap between financial regulations and the energy market. This article provides an oversight of the regulatory framework which applies to energy companies who trade in derivatives which have a value based on an energy product, hereinafter further defined as “Energy Trading”.Footnote2 Next to REMIT, Energy Trading is captured by financial regulations, such as the market abuse directive, the corresponding market abuse regulation (“MAD”/“MAR”),Footnote3 the European Market Infrastructure Regulation (“EMIR”)Footnote4 and the Markets in Financial Instruments Directive (“MiFID II”).Footnote5 These regulations are interlinked and overlap at some stages. For market participants active in Energy Trading – including energy companies – it’s not always clear how to adhere to such an extensive set of legal obligations.

The purpose of this article is twofold: firstly, to expose the regulatory paradigm which applies to Energy Trading including its obligations, boundaries and challenges for energy companies. Secondly, this article will answer the question whether a specific regulatory framework which REMIT introduced is crucial when compared to the existing regulations. The first section explains how Energy Trading works in practice with a focus on markets, products and risks. The second section gives an overview of the legal framework focusing on the intersection between financial regulations and the specific framework for Energy Trading. It appears that energy companies are more and more active in Energy Trading, which implies that financial- and energy markets are becoming more and more intertwined.Footnote6 This article notes that REMIT’s prohibition on insider trading and market abuse, fills in a gap which was previously not addressed by other financial regulations such as MAD/MAR and MiFID II. Finally, in the third section the article explores how the theoretical scope of the regulation and the framework it provides for impacts market participants active in Energy Trading. This article does not focus on the explanations of definitions of financial instruments, insider trading or market abuse. Nor does it enter into a normative discussion on whether its effects on the market or market participants are desirable from a – for example – social, economic or even psychological point of view. Instead, it aims to take a step back and focus the question whether the current set of rules – and especially REMIT – reflect the initial goal of establishing a specific framework for the energy market and whether the imposed rules are fit to meet this goal. Only then, the central question if REMIT is indispensable can be answered. This article concludes that the rationale behind the reasons to establish REMIT are not necessarily convincing, since it lacks a holistic approach of the functioning of the market on which energy derivatives are traded and settled financially and the specific risks relating thereto.

Section 1

1. ENERGY TRADING IN PRACTICE

1.1. Derivative trading

Most energy companies are active in the production and sale of electricity and gas. Electricity may be generated through gas- or coal fired power plants or renewable sources such as wind turbines or solar panels, but can also be purchased from another producer. The purpose of trading in commodities such as gas, coal or electricity, is usually to meet an underlying demand to run a power plant or to deliver an agreed volume to a purchaser. In addition to the trade in physical commodities, a large number of energy companies trade in financial instruments. In case the value of such financial instrument depends on – or is derived from – the value of an underlying variable such as the price of a traded assets asset, it is called a derivative.Footnote7 A derivative can be described as an agreement between two parties to sell and purchase a financial security for a certain price. The fact that derivatives are financial instruments, means that – usually – no physical delivery of the underlying product will take place and that they are mostly settled financially. Commodity derivatives are financial instruments whose price is based on the price of commodities. As mentioned in the introduction, the term Energy Trading is used to describe the trade in derivatives which have a value based on an energy product. Derivatives can exist in all types of shapes, but is not a defined term or grasps a fixed set of financial instruments.Footnote8 Since no clear definition exists, new financial instruments may be invented which could qualify as a derivative. As a consequence, a comprehensive regulatory regime is difficult to establish, which contributes to derivatives’ intangible character and bad reputation. One of the characteristics of commodity derivatives is that they hardly ever lead to delivery of the underlying physical contract, because traders choose to close out their positions prior to the delivery period specified in the contract, which in its turn contributes to the level of liquidity.Footnote9

Why do energy companies engage in Energy Trading while their core business is the production of energy?Footnote10 Energy Trading can have multiple functions: (i) it transforms uncertainty about fluctuating energy prices into a calculable risk; and (ii) it transfers this risk to a counterparty that has a comparative advantage in bearing it because of an open position or a different risk appetite.Footnote11

1.2. Hedging

Energy companies do not know the price level of power and gas in the future, they can try to mitigate this fluctuating energy price risk by trading in financial instruments. The risk mitigating function can also be defined as a hedge function. How does this work? Hedging is done by concluding a transaction – either on an exchange or at a bilateral over the counter (“OTC”) levelFootnote12 – for the purchase or sale of a financial instrument with a different counterparty at the same time and in that way mitigating – hedging – the fluctuating energy price risk against the parallel financial trade.

But how does hedging work in practice? Let’s use the example of an energy company owning a coal fired power plant. In order to produce electricity, large amounts of steam coal are needed to fuel the power plant. The price of coal to run this plant may form a large part of the costs of an energy company and fluctuations in the price of coal can have a large impact on its financial position. When the company estimates that a certain volume coal is needed on a date in the future, for example 1 July 2022, it can go into the derivative market to hedge its exposure to future price fluctuations by locking in a price for a derivative with the delivery date on 1 July 2022. This is done by purchasing physically settled futures, swaps or forwards equaling the amount metric tonnes of coal needed on 1 July 2022. If only financially settled derivatives are available, then the energy company would have to find a seller of physical coal between now and 1 July 2022 and, once found, sell the financial derivative. Should the energy company choose to not hedge and leave the exposure open, then they run the risk of coal prices running up from the current future/swap/forward price. Conversely, if prices fall compared to today’s price, they would hedge at a better level. In either case, the energy company can time their hedges based on their view of future price of coal and be flexible to purchase or sell their hedges as a result of changing market prices or conditions, such as Brexit uncertainty, changes in interest rates, wars or a pandemic.

The concept of hedging is important in the assessment to which extent MiFID II and EMIR apply to Energy Trading (see also paragraph 2.2). Hedging can be considered as a form of insurance against price fluctuations of a commodity. It plays an important role in Energy Trading because prices are volatile with large price fluctuations and therefore high price risks. Even though hedging could minimize or control a price risk, there is no guarantee that the overall profitability of a market participant’s activities will increase. Because hedging entails entering into multiple transactions at the same time, the risk that a counterparty defaults by not paying the price for the derivative agreed between parties increases. It is not always clear to distinguish hedging from other reasons for trading, such as speculationFootnote13 or arbitrationFootnote14 as reasons for trading.Footnote15 Cheng and Xiong reflect that the classification of market participants into the categories of “speculators” and “hedgers” very poorly aligns with the economically relevant distinction; reducing versus increasing risk. They state that many “hedgers” appear to take bets on prices that are insensitive to their current exposure.Footnote16 This draws the conclusion that risk-mitigating measures are not always the reason for hedging and that regulation in order to minimize risks imposed by derivative trading should maybe focus on the identity of a market participant instead of its activities. Cheng and Xiong conclude that disregarding the identity of the trader as a factor of classifying trades, and instead emphasize on the motive of a trade, may be difficult to ascertain. This conclusion is underlined by Duffie, who also points out the distinction in trading motives is already difficult for regulators to distinguish in a bilateral trade environment, and would be much harder to implement in an anonymous market in which orders may be split by algorithms and allocated to a wide range of counterparties.Footnote17 Since the distinction between the three reasons for trading in derivatives is not always clear, it could be discussed whether such distinction is the right consideration to ground regulation on. The qualification of market participants, their risk appetite and market position could also be taken into account when determining the impact of Energy Trading on the real economy and therefore imposing a systemic risk.Footnote18 In addition, the fact that Energy Trading by energy companies is backed by physical assets and that it can be conducted in order to mitigate exposure which results of physical trading, can be considered an indication that hedging activities are more likely to occur than speculative ones. A market participant trading in (heavily) subsidized renewable products where margins and risks are lower than for the old and grey commodities, are less likely to enter into risky derivative trades and is less likely to qualify as a speculator.

Section 2

2. APPLICABLE LEGAL FRAMEWORK

Prior to the implementation of REMIT in 2011, Energy Trading was captured under MiFID II, MAD/MAR and EMIR, all originally designed to monitor capital markets. The paragraphs below give an overview of the reasons and circumstances which led to the implementation of REMIT after which specific obligations for Energy Trading companies will be further explained.

2.1. History

A EU wide policy in the field of Energy Trading was lacking for a long time.Footnote19 One of the results of the 2007 capital market crisis was that serious deficiencies in global financial markets law became visible.Footnote20 A report of the Larosière group pointed out that the supervisory system during the crisis failed, mainly due to a lack of adequate regulation.Footnote21 It appeared that several structural problems existed on capital markets and expert opinions on recommended solutions to these problems emphasized the importance of integrating national securities markets, harmonizing the access to the European capital marketFootnote22 and establishing a supervisory agency at community level.Footnote23 Also, the financial crisis revealed deficiencies in the markets for OTC derivatives.Footnote24 The European Commission (“EC”) introduced a number of regulatory measures impacting both exchange- and OTC traded energy derivatives, aiming to recognize and prevent systematic risks for Europe’s entire financial system as well as measures to improve the supervision of individual financial service providers and capital market participants.Footnote25 Since the core regulations of European capital markets law was already in place, the question came up whether sector specific rules for the energy market were necessary.Footnote26 Studies concluded that the current capital markets framework did not properly address market integrity issues in the electricity- and gas markets and suggested that proposals for a basic, tailor-made market abuse framework in the energy sector legislation for all electricity and gas products should be considered.Footnote27 An alternative to such new framework was to increase the scope of MAR, but it was not considered appropriate to include “behavior that does not involve financial instruments, for example, to trading in spot commodity contracts that only affects the spot market”.Footnote28 As a result, regulatory packages with specific rules for commodity trading sector were presented. Regulations established by the First, Second and Third Energy Packages were used to create an internal electricity market based on three pillars: competition, energy security and environment.Footnote29 The Third Package could be used as a starting point to reform the energy sector and to justify the need for sector specific rules relating to transparency and market abuse.Footnote30 This package introduced the revision of current regulations,Footnote31 the initiative to reform MiFID II,Footnote32 introduction of REMIT and new regulators: the European Securities and markets Authority (“ESMA”)Footnote33 with a supervisory role within the scope of MiFID II, EMIR and MAD/MAR and – specifically for the energy sector and REMIT – the Agency for the Cooperation of Energy Regulators (“ACER”).Footnote34 The objective of REMIT is to increase integrity and transparency in the wholesale energy market to foster competition for the benefit of final consumers of energy. The aim of EMIR is to reduce systemic risk by increasing market transparency and to mitigate counterparty risk by introducing a clearing obligation for OTC derivatives. MiFID II aims to make financial markets more transparent and to increase the level of protection for investors. MAD/MAR aims to increase public confidence and integrity of financial markets.

2.2. Energy trading subjected to regulation

One of the obligations with the most far-reaching consequences for Energy Trading companies, is the licensing requirement under MiFID II for financial- and certain non-financial entities.Footnote35 There is an exemption to this licensing scheme, in case Energy Trading qualifies as “ancillary” to regular business activity.Footnote36 The qualification as “ancillary” – or traded for hedging purposes – is thus crucial for energy companies who would want to avoid the license obligation imposed by MiFID II.Footnote37 This exemption is still subject to discussion between regulators and industry players.Footnote38 Next to MiFID’s far-reaching license obligation,Footnote39 other regulatory obligations include reporting obligations, position limits, prohibitions of insider trading and market manipulation.

2.2.1. Data reporting obligation

Obligations to report details of commodity derivative transactions and fundamental data relating thereto, find their regulatory basis in EMIRFootnote40 and REMITFootnote41 and MiFID II.Footnote42 Such details include information on parties, price, venue of execution, quantity, delivery type, interest rates maturity date and details on clearing obligations. Under EMIR, market participantsFootnote43 have the obligation to report these details to a trade repository, which in its turn reports to ESMA.Footnote44 Under REMIT, information is reported to ACER directly. The reporting obligations under REMIT focus on the prevention of market abuse,Footnote45 whilst MiFID II and EMIR refer to systemic risk.Footnote46 There is an overlap between REMIT and EMIR regarding reporting obligations, even though REMIT provides for an exemption for trades which have been reported under EMIR already.Footnote47 The two reporting streams trigger questions on effectiveness of reporting obligations and supervisory activities.Footnote48 In practice, it appears that transaction reporting has not been flawless since EMIR entered into force. Not only did ESMA fail to provide clear and consistent guidance regarding which type of transactions should be reported by whom, also it has been unclear what the regulators would actually do with the information flow. In addition, market participants and industry groups regularly point out the administrative burden of data reporting obligations.

2.2.2. Position limits

MiFID II imposes a position limit regime, which means that national regulatory authorities (“NRA’s”) should establish limits on the positions an undertaking holds under a derivative contract in relation to a commodity in order to prevent market abuse.Footnote49 This means that the amount of commodity derivatives a market participants has in its portfolio cannot exceed a threshold set by an NRA. Such limits should promote integrity of the market for the derivative and the underlying commodity. For non-financial counterparties as defined under EMIR, there is an exemption to the position limit regime. The thresholds do not apply to positions which are objectively measurable as reducing risks which directly relate to their primary commercial activities. In practice, this means that market participants have an incentive to include their trading activities under the hedging exemption. Most Energy Trading companies are able to apply for this exemption as their trades are backed by the assets they own.

2.2.3. Disclosure of inside information

MAD/MAR aim to increase the integrity of financial markets through the prohibition of market abuse, by requiring market participants to disclose price sensitive information and to prohibit insider dealing and market manipulation. On the prohibition of insider trading, both MAD/MARFootnote50 and REMITFootnote51 prohibit the use of inside information for acquiring or disposing financial instruments or wholesale energy products they relate to. Differences can be found in the definition of inside information; all information regarding commodity derivatives falls under the scope of MAD/MAR including a specific reference to emission allowances, but not all inside information as defined in MAR equals that of the definition of inside information of REMIT, which merely relates to wholesale products.Footnote52 Another overlap is the obligation to publicly disclose inside information.Footnote53 Again, the definition of inside information differs between the two regimes. For MAD/MAR, the obligation has a focus on all inside information concerning the issuer of a financial instrument, where REMIT points out that inside information should relates to information relevant to the capacity and use of facilities. Even though REMIT includes information relating to commodity derivatives, the disclosure requirement is much broader than under MAD/MAR. Information which is specific enough to assume that it may influence related financial instruments is considered as inside information. For energy companies, this could mean the key terms of commodity derivative contracts, but also information relating to maintenance work and outages of a facility qualify as inside information under REMIT and should be disclosed in a timely manner.Footnote54 In addition, MAD/MAR and REMIT coincide on the obligation to notify suspicious transactions to the NRA.Footnote55 Like the prohibition of market manipulation, this obligation is similar under MAD/MAR and REMIT, with an equal carve out for wholesale energy markets. Explanations of the obligations under MAD/MAR remain high level which provoked market initiatives to develop standards for reporting in absence of a clear guidance.Footnote56

2.2.4. Market manipulation

REMIT provides for a sector specific prohibition on insider trading and market manipulation, which was previously captured by MAD/MAR and MiFID II. As a result, both MAD/MAR and REMIT prohibit the engagement in, or an attempt to manipulate the market.Footnote57 Market abuse is a concept that covers unlawful behavior in the financial markets and consists of insider dealing, unlawful disclosure of inside information and market manipulation. The concept of market abuse and market manipulation as defined in REMIT is not similar to the concept of market abuse to which article 102 of the Treaty on the Functioning of the European Union refers to, namely any abuse by one or more undertakings of a dominant position within the internal market or in a substantial part of it shall be prohibited as incompatible with the internal market in so far as it may affect trade between Member State. As a consequence, the market abuse prohibition under REMIT applies to all market participants, even those which are non-dominant. Also, competition law has a focus on the impact of competition on a market, whilst REMIT increases its scope to integrity and transparency. ACER provides examples of market manipulation, such as wash trades, placing orders with no intention of executing them, cross market manipulation and spreading false information through the media.Footnote58 In November 2015, the Spanish NRA imposed a EUR 25 million fine on Iberdrola Géneración for manipulating the Spanish wholesale electricity market.Footnote59 Where market manipulation in the energy landscape previously could only be challenged through competition law and the abuse of a dominant position, this case was the first where an NRA successfully imposed the prohibition of REMIT. Since then, NRA’s have taken a total of 13 sanction decisions, which were all based on breaches of on breaches of the prohibition of market manipulation under article 5 REMIT. Fines range from EUR 1,500 for traders individuallyFootnote60 up to EUR 42,5 million in the most recent decision.Footnote61 None of these cases focus on Energy Trading, but rather on trade in gas- and electricity markets with a physical delivery.

Section 3

3. ANALYSIS

3.1. Intersection financial regulations and energy regulation

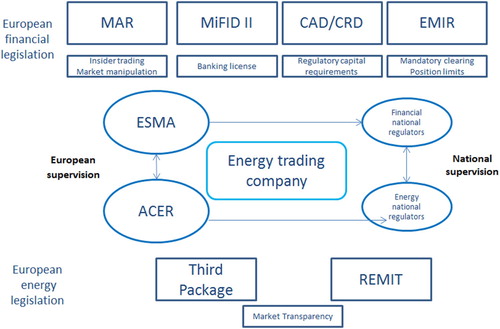

As seen above, Energy Trading finds itself in between financial- and energy regulation. The European Parliament reflected on the interaction between financial regulations and REMIT.Footnote62 It states that the prohibitions on trading on inside information and market manipulation are formulated in such a way that they are consistent with the MAD/MAR and do not apply to financial instruments which are already covered by that directive. In that way, REMIT has filled in a gap by making the prohibition on market abuse and market manipulation, disclosure of inside information and the reporting of suspicious transactions much more concrete for the energy sector. The activities of Energy Trading companies are captured in the intersection of both regulatory frameworks – which show similarities as well as differences – and they supervised by both ESMA and ACER ().Footnote63

Figure 1. Position Energy Trading companies in European financial- and energy legal frameworks.

Differences between the two regulatory frameworks are the result of the structure and characteristics of the products which are traded.Footnote64 For example, physical settlement in energy markets requires a physical infrastructure in facilitating the settlement, whilst financial settlement doesn’t.Footnote65 Also, gas and electricity as commodities and the specific features of related derivatives played a role.Footnote66 Similarities between the regulatory regimes for the energy- and financial markets are derived from an overarching background: the monitoring of the market and the corresponding authorization and license requirements.

The objectives envisaged during the design of REMIT provide a guideline to analyze whether the obligations on market participants address the initial goals. The EC stated that wholesale energy markets are crucial to the well-being of citizens, competitiveness of business and the success of the EU energy policy. It emphasized the importance that citizens, businesses and NRA’s should have confidence in the integrity of the market.Footnote67 REMIT aimed to create a framework to ensure that these markets function properly, i.e. their outcomes are not distorted by abusive market behavior, but truly reflect market fundamentals.Footnote68 This means that the regulation should appropriately govern the behavior of market participants and that rules therein are complete, consistent, adapted to the specifics of energy markets and designed to effectively detect market misconduct.Footnote69 The EC concluded that the lack and the divergence of the current set of rules was insufficient to ensure the stable and orderly functioning of the energy markets. This view was also supported by market-participants.Footnote70 The EC furthermore stated that as long as the necessary information is not available to NRA’s, abusive behavior will remain difficult to detect. While drafting REMIT, several options to enforce rules were analyzed, which ranged from self-regulation of markets, to extension of MAD/MAR and MiFID II and rules defined at EU level, where monitoring and enforcement could be executed by ACER, another unique EU agency or member-states themselves.Footnote71 The different options were set against the impact on market stability, price, administrative costs, job creation and environmental costs. The most preferable solution was the one where rules were defined at EU level and monitoring and enforcement was shared between ACER and NRA’s. It has not been made clear by the legislator, however, why the current financial regulatory framework could not have been extended by widening the scope to commodity derivatives, especially since REMIT reflects so much overlap with existing regulation.Footnote72 Was the establishment of entirely new framework necessary and – if so – proportionate? Do the implemented rules meet the standards that were envisaged and do they effectively manage the risk in energy markets or could such rules have been implemented in the current regulatory framework?Footnote73

3.2. Was REMIT inevitable?

3.2.1. Existing regulation

REMIT introduced prohibitions of insider trading and market abuse for Energy Trading which was not previously addressed by other financial regulations. It is however not clear how these prohibitions add to REMIT’s goals, such as a higher level of transparency.Footnote74 Transparency does not automatically lead to a better functioning market. Nor does implementing a regulation which imposes obligations which are also reflected in other types of regulations. Looking at the scope of REMIT, it might seem tempting for a regulator to draft comprehensive regulations to capture all possible financial instruments and market participants. When doing so, not only supervision and enforcement might be put under pressure, but also a negative effect on market and its liquidity might come into effect. Ford and Kay state that the conclusion that systemic risk justifies extended regulation on banks, is not persuasive in itself and might lead to regulation of any activity which competes with any activity undertaken by a regulated firm.Footnote75 To prevent over-regulating, the regulator should assess which exact instruments and market participants add to the risk which is to be prevented by the regulation. This analysis is not reflected in REMIT or its preparatory documents. At least, the regulator did not show a reasoning why certain instruments may have an effect on the market which could lead to a more stable financial market with transparent prices and increased competition. Also, imposing obligations derived from competition law on market participants without a dominant position does not align with a desire to prevent systemic risk to occur. After all, without a dominant position it is a challenge to impose a systemic risk to the real economy. Hence, a causal connection between regulatory obligations and risks imposed on companies active in Energy Trading is not evident. As a result, the regulator has imposed a pressure not only on itself by having the obligation to process enormous amounts of reported data, but also on the market participants. The same effect could have been established by amending the current regulatory framework, for example by increasing the scope of EMIR regarding reporting obligations and including energy derivatives under the prohibition of insider trading and the disclosure of inside information under MAD/MAR. It is not said that the merger of the different sets of obligations is necessarily more effective or the only option, but looking at the impact of a diversified portfolio of regulations and supervisory tools applicable to Energy Trading, it would have been logical to question its viability. As REMIT does not Such research is not reflected in REMIT or its preparatory documents and it is therefore not necessarily evident that the goals of REMIT could not have been obtained by enhancing the scope of existing regulation, such as MAD/MAR and EMIR.

3.2.2. Market characteristics

The effect of REMIT on energy companies is large, especially in the field of data reporting and disclosure of inside information.Footnote76 As seen in Section 2, obligations and prohibitions in the field of reporting obligations, the prohibition of insider trading, market manipulation and disclosure of inside information overlap in some ways. Different regulatory models covering similar topics and addressing similar actors. This leads to confusion amongst market participants. The exact scope of obligations has to be distilled from a diverse set of regulations and may lead to a lack of clarity on which activities are subjected to regulation. Not only does such confusion on how to comply with which rules lead to a high workload for compliance departments of impacted market participants and high costs for engaging external counsels, it also increases the risk for market participants not to comply with the rules simply because they are too confusing.Footnote77 In view of the overarching principle of a desire to increase transparency in the market, this regulatory paradox imposes an unclear burden of obligations on market participants.

REMIT does not address specific risks related to Energy Trading, such as market-, credit- and operational risk or specific risks relating to the identity of market participants. The EC has taken the position that regulation should be focused on the character of financial instruments which are being traded in the first place and not on the identity of financial institutions or energy companies.Footnote78 There are several arguments to support the position that Energy Trading should be subjected to a different regulatory scope than capital markets. Energy companies state that their Energy Trading activities are backed by assets and are there therefore less risky.Footnote79 The EC seems to implicitly underline this argument by including a “hedging” carve out in MiFID II. Secondly, energy companies do not cause the same systemic risks as other financial market participants do, which view is also supported by regulators.Footnote80 Energy companies do not have access to central back liquidity to meet liquidity requirements and do not take deposits from private clients.Footnote81 Therefore, they should not be exposed to financial regulations to the same level as other financial players. At the same time, energy companies’ role as producers of crucial commodities for society, is systemic in itself. Also, the physical product relating to the financial instruments traded by energy companies are meant to be consumed by individuals, who are strongly dependent of the end product and – indirectly – affected by fluctuations and movements on the market. These arguments all relate to specific characteristics of the energy sector. Preparatory documents for REMIT could have addressed that even though energy companies do not hold deposits and in that sense are quite different than banks, they do have significant market power because they are the dominant actors in determining ultimate consumer prices. This is a different argument than that market abuse in one member state does not only affect wholesale prices across national borders, but also retail prices for consumers.Footnote82 Moreover, economic studies on the effects of transparency on the market, its level of liquidity and costs of risk management for energy trading companies and the real economy could have been taken into account.Footnote83 This has not been done and a holistic approach of the functioning of Energy Trading, its risks and markets is not apparent.Footnote84 Research on the psychological effects on market participants, trading patterns and economic behavior of subjecting Energy Trading to a regulated regime and a heavily supervised environment could have had consequences for ideas on effectiveness of transparency in a market. It seems that REMIT does not address the link between the implications of REMIT on the risks in the market for energy derivatives. This position is understandable from a legal perspective, since the internal legal reasoning behind legislation is a legal justification in itself. However, a regulator should not only use the point of view from a legal scholar in addressing legislation which has an (economic) effect on a market, but should apply a more balanced approach by taking into account a more normative study on the social, political and economic effects of regulation. One can make a comparison to markets where agricultural derivatives are being traded. After the crisis in 2007, criticism regarding these types of derivatives followed the same patterns as for energy derivatives.Footnote85 The regulatory framework for agricultural derivatives consists of MiFID II, EMIR and MAD/MAR, but a specific – agriculture focused – framework like REMIT is missing.

4. Conclusions

The focus of this research is to expose the regulatory model which applies to energy companies involved in Energy Trading and to investigate the boundaries and obligations on their activities imposed by this model and on the other to analyze if REMIT is indispensable looking back now that REMIT’s 10th anniversary is approaching. Section 1 reflects the reasons why energy companies conduct Energy Trading and the risks relating thereto. The regulatory framework in Section 2 shows that there is an overlap between REMIT and financial regulatory frameworks such as MAD/MAR, MiFID II and EMIR in the field of reporting obligations, prohibitions of insider trading and market manipulation and the disclosure of inside information. It appears that REMIT filled in a regulatory gap which was left open in current financial regulation. When focusing on a purely internal legal assessment, it can be concluded that the introduction of obligations of transaction reporting and the prohibition of market abuse, insider trading and market manipulation could contribute to a properly functioning energy market in the sense that it´s outcome is not distorted by the behavior which REMIT prohibits. Section 3 addresses the background and rationale of both REMIT and financial regulations and concludes that REMIT has imposed a large set of regulatory obligations on both market participants and regulatory authorities. Paragraph 3.2.1 concludes that preparatory documents do not reflect the full scope of the current existing framework and the pros and cons of amending them to meet REMIT’s aims and goals, whilst a more normative analysis on the affected market, its liquidity and other economic effects could have led to a different outcome. Not only did the EC failed to assess these effects and specific market characteristics whilst drafting REMIT, it does not give signs that it takes the economic scope of REMIT into account going forward, like the systemic risk imposed by energy companies as reflected on in paragraph 3.2.2. Often the argument is simply that some rule is “necessary on investor protection grounds”. The administrative costs of regulation or long term economic effects do not always receive the attention they deserve. The more important regulatory burden is the effect and costs on market participants, on their innovative behavior and on competitive response.Footnote86 And as a result thereof, ultimately on the effect on consumers and the price they have to pay for energy products. Given the number of sanctions imposed under REMIT, it appeared that the regulation has matured over the last years. But one should have no envy for regulators: the scope of financial regulation is increased and workload generated by the obligations laid down in the regulations is bigger than ever. The question is whether regulators and market participants are ready to face market developments within the boundaries that REMIT impose.

***

Additional information

Notes on contributors

Liebrich M. Hiemstra

Liebrich M. Hiemstra, PhD student, Tilburg Law and Economics Center, University of Tilburg, the Netherlands Senior Legal Counsel Vattenfall N.V., Amsterdam, the Netherlands.

Notes

1 Regulation (EU) No 1227/2011 of the European Parliament and of the Council of 25 October 2011 on wholesale energy market integrity and transparency entered into force on 28 December 2011. The regulatory core of REMIT consists of prohibitions of market abuse, inside trading and market manipulation and obligations in relation to the publication and reporting of information relating to products traded in wholesale energy markets. Subjected to REMIT are contracts for the supply of electricity or natural gas where delivery takes place in the European Union, contracts relating to the transportation thereof and derivatives relating to such transportation or the production, trading or delivery of electricity and natural gas. Both OTC and derivatives traded on regulated markets are in scope.

2 Derived from: (i) Directives 2009/72 EC of the European Parliament and of the Council of 13 July 2009 concerning common rules for the internal market in electricity and repealing Directive 2003/54/EC; and (ii) Directive 2009/73/EC of the European Parliament and of the Council of 13 July 2009 concerning common rules for the internal market in natural gas and repealing Directive 2003/55/EC, I use the term energy companies for entities which are active in the productions of energy, but also in transmission, distribution and delivery of electricity, gas without being end users.

3 Directive 2003/6/EC of the European Parliament and of the Council of 28 January 2003 on insider dealing and market manipulation (market abuse) and Commission Directive 2004/72/EC of 29 April 2004 implementing Directive 2003/6/EC of the European Parliament and of the Council as regards accepted market practices, the definition of inside information in relation to directives on commodities, the drawing up of list of insiders, the notification of managers’ transactions and the notification of suspicious transactions, replaced by Regulation (EU) No 596/2014 of the European Parliament and of the Council of 16 April 2014 on market abuse (market abuse regulation) and Directive 2003/6/EC of the European Parliament and of the Council and Commission Directives 2003/124/EC, 2003/125/EC and 2004/72/EC and corresponding Directive 2014/57/EU of the European Parliament and of the Council o 16 April 2014 on criminal sanctions for market abuse (market abuse directive).

4 Regulation (EU) No 648/2012 Of The European Parliament and of The Council of 4 July 2012 on OTC derivatives, central counterparties and trade repositories and Regulation (EU) 2019/834 of the European Parliament and of the Council of 20 May 2019 amending Regulation (EU) No 648/2012 as regards the clearing obligation, the suspension of the clearing obligation, the reporting requirements, the risk-mitigation techniques for OTC derivative contracts not cleared by a central counterparty, the registration and supervision of trade repositories and the requirements for trade repositories (EMIR Refit).

5 Directive 2014/65/EU of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Directive 2002/92/EC and Directive 2011/61/EU and Regulation (EU) No 600/2014 of the European Parliament and of the Council of 15 May 2014 on markets in financial instruments and amending Regulation (EU) No 648/2012. The large volatility in commodity markets formed one of the key reasons to revise MiFID II and increase regulatory oversight. By adopting MiFID II, the EC introduced a market structure which aimed to close loopholes and ensure that trading, wherever appropriate, takes place on regulated markets. See, L Nijman, “The Impact of the New Wave of Financial Regulation for European Energy Markets” (2012) 47 Energy Policy 468–77. (MAD/MAR) and EMIR which refer to financial instruments are updated by way of general repeal in Art. 94 MiFID II and therefore as of 3 January 2018 have to be applied to the wider scope of derivatives and financial instruments as defined in MiFID II.

6 S Pront-van Bommel, “The Development of the European Electricity Market in a Juridical No Man’s Land” in A Dorsman (ed), Financial Aspects in Energy. A European Perspective (Springer, 2011).

7 JC Hull, Options, Futures and Other Derivatives (Essex: Pearson Education Limited, 2012), 1 and J Biggins, “‘Targeted Touchdown’ and ‘Partial Liftoff’: Post crisis Dispute Resolution in the OTC derivatives Markets and the Challenge or ISDA” (2012) 13(12) German Law Journal 1299.

8 Biggins, supra n 7, p. 1300.

9 Hull, supra n 7, p. 23. Liquidity describes the degree to which an asset or security can be quickly bought or sold in the market without affecting the asset’s price. The importance of liquidity as a prerequisite to market functioning is a basic assumption in the development of financial regulations.

10 When defining a regulatory framework to address trading in derivatives, several questions arise: Which risks do firms hedge? How much do they hedge? How far ahead do they hedge? What determines corporate hedging policy? Should firms hedge at all? “as straightforward as it might appear, these questions are still largely unresolved”, see S Moeller and P MacKay, “The Value of Corporate Risk Management” (2006) SSRN Electronic Journal and “academic guidance is still lacking”, see G Poitras, Commodity Risk Management (Routledge, 2013), 48.

11 JR Macey, “Derivative Instruments; Lessons for the Regulatory State” (1996) 21 Journal of Corporation Law 69–93, https://digitalcommons.law.yale.edu/cgi/viewcontent.cgi?article=2441&context=fss_papers.

12 Examples of exchanges where derivatives are traded include Nordpool, Powernext, the Intercontinental Exchange and the New York Mercantile Exchange. A majority of traded derivatives is conducted by an intermediate party; a broker. A broker usually lays off much or all of the risk of its client-initiated derivatives positions by running a “matched book,” that is, by aiming for offsetting trades, profiting on the differences between bid and offer terms. See also D Duffie, “The Failure Mechanics of Dealer Banks” (2010) 24(1) Journal of Economic Perspectives 51–72.

13 According to Hull, supra n 7, p. 15: Speculation is the activity where a market player takes a position in order to make profit, whilst hedgers want to avoid exposure to adverse market movements in the price of an asset. Speculation is therefore the opposite of hedging: taking upon a risk in order to make profit instead of mitigating a risk with the objective to avoid a loss. Speculation can be a business in itself and the return for speculators is not guaranteed. The in-house professional execution of speculative trading is proprietary trading. The objective of these (in-house) departments is to make money and in planning to do so, they use their working capital.

14 According to Hull, supra n 7, p. 16: Arbitrage is a process whereby market participants profit from price discrepancies. This is done by simultaneously entering into transactions relating to a similar product in two or more markets. Since one trade stands in for the other, arbitrage can be risk free. The possibility to arbitrage only exists if a product is priced differently on different market or if this difference is the result of the difference in currency rates or other variables. Interesting in the process of arbitrage is that there is a short window of opportunity for market participants, since the forces of supply and demand will eventually create a balance between the different markets.

15 Functions may overlap or intertwine. An illustrative example can be found in the decline of Enron, being an energy company transformed into a derivative trader. According to Partnoy, supra n 15, Enron shifted its business model from being an energy company to a derivative trader. It’s decline was based on – amongst others – the risks imposed to the company as a result of derivative trading, such as the use of “prudency” reserves in order to smooth out profits and losses over time and the mismarking of forward curves to hide losses and for traders to receive higher bonuses, see F Partnoy, “Testimony in the Hearings Before the US Senate Committee on Governmental Affairs”, 24 January 2002, https://www.gpo.gov/fdsys/pkg/CHRG-107shrg78614/html/CHRG-107shrg78614.htm.

16 IH Cheng and W Xiong, “Why Do Hedges Trade So Much”, Working Paper Dartmouth College Hanover New Hampshire, Hanover, 2013.

17 D Duffie, “Challenges to a Policy Treatment of Speculative Trading Motivated by Differences in Beliefs” (June 2014) 43(2) Journal of Legal Studies.

18 C Staritz and K Küblböck, “Re-regulation of Commodity Derivative Markets: Critical Assessment of Current Reform Proposals in the EU and the US”, Working Paper, Austrian Foundation for Development Research (ÖFSE), No. 45, 2013 and D Lautier and F Raynaud, “Systemic Risk in Energy Derivative Markets: A Graph-Theory Analysis” (2012) 33(3) The Energy Journal.

19 SE Eisma (red.), Leerboek Effectenrecht (Ars Aequi Libri, 2002), 11. Also, the energy sector in the European Community was nationally segregated and energy itself was regarded as being too bound with national sovereignty and national survival. Talus explains that the system of energy monopolies, which played a role in rebuilding European economies after WWII, had lost its purpose and its political legitimacy (K Talus, EU Energy Law and Policy. A critical Account (Oxford University Press, 2013). Daintith and Hancher stated that: In this Respect that There is No Indication in the Treaty of the European Union that the Basic Range of Rules Should Not be Applicable in the Energy Sector as in All Others Covered by the Treaty. T Daintith and L Hancher, “The Management of Diversity: Community Law as an Instrument of Energy and Other Sectoral Policies” (1984) 4(1) Yearbook of European Law 123–67.

20 As a result of a sector inquiry in the energy market in 2007, the EC concluded that in many consumers’ views, the lack of trust in the functioning of wholesale markets, price formation and wholesale trading mechanisms and market manipulation were the reason for past price increases. (See: European Commission, “DG Competition Report on Energy Sector Inquiry”, Brussels, 10 January 2007, https://ec.europa.eu/competition/sectors/energy/inquiry/index.html). The choice for specific rules for the energy market regarding transparency and market abuse is largely derived from recommendations from regulatory bodies based on consultation documents reflecting opinions of market participants, including exchanges and energy companies (See for example: Committee of European Securities Regulators (“CESR”) and the European Regulators’ Group for Electricity and Gas (“ERGEG”) advice to the European Commission in the context of the Third Energy Package Response to Question F.20 – Market Abuse, CESR 08/739).

21 CF de Larosière, The High Level Group on Financial Supervision in the EU (Report, 2009).

22 R Veil, European Capital Markets Law (Hart Publishing, 2013), 2.

23 C Segré, “The Development of a European Capital Market. Report of a Group of Experts Appointed by the EEC Commission”, November 1966, https://aei.pitt.edu/id/eprint/31823, p. 235: An agency at Community level, to be competent for issues floated within the territory of the Community and to be endowed with powers similar to those of the Securities and Exchange Commission in the United States, the Banking Commission in Belgium or the Bank Control Commissariat in Luxembourg. The Segré report was the basis for a legislative process to remodel capital markets regulation in five phases which took over 50 years to be accomplished. Moloney describes different phases in the European capital legislation (See: N Moloney, EC Securities Regulation (Oxford University Press, 2013), 11.

24 Even though the financial crisis did not start as a result of an increasing trade in derivatives, but as a result of the mortgage crisis and macroeconomic events, government policies, the relaxation of lending standards by financial institutions and failure of regulations, the crisis did provoke an increase in the attention to the deficiencies in the markets where OTC derivatives were traded. Gorton states that the crisis was caused by information problems related to declining house prices, which prevent subprime mortgages from being refinanced (see G Gorton, The Panic of 2007 (NBER, 2020) [online], https://www.nber.org/papers/w14358 [Accessed 2 July 2020]). Because subprime mortgages are financed through a chain of securities and structures, investors could not easily determine the location and extent of the risk. This led to a panic reaction from investors and depositors to withdraw cash according to M Roe, “The Derivatives Market’s Payment Priorities as Financial Crisis Accelerator” (2011) SSRN Electronic Journal. Also, the general opinion that only exchange traded financial instruments were to be regulated was amended and the focus on regulating OTC derivative trading was increased. Carruthers states that the general claim market participants active in foreign exchange transactions in the OTC market were large, sophisticated institutions that knew what they were doing. Yet, several events in the market underscored that OTC derivatives involved considerable risk, even for experts. See B Carruthers, “Diverging d“erivatives: Law, Governance and Modern Financial Markets” (2013) 41(2) Journal of Comparative Economics 386–400. On the increased attention on markets for OTC derivatives, see Hull, supra n 7 and M Kerste, M Gerritsen, J Weda, and B Tieben, “Systemic Risk in the Energy Sector – is There a Need for Financial Regulation?” (2015) 78(C) Energy Policy 22–30.

25 CV Communication of the Commission on European financial supervision, 27 may 2009, COM(2009) 252 final.

26 The core of European capital markets law consists of MAD, EMIR, MiFID II.

27 CESR and ERGEG advice to the European Commission in the context of the Third Energy Package Response to Question F.20 – Market Abuse, CESR 08/739, p. 4. Also, CESR and ERGEG concluded that market integrity was not sufficiently ensured through the current set of rules derived from competition law, general business contract law and certain financial law rules. See also K Talus, EU Energy Law and Policy Issues (Intersentia, 2014), 309.

28 Regulation 596/2014 (MAR), recital 20.

29 M Sokolowski, Regulation in the European Electricity Sector (Routledge, 2016). The First Package on common rules for the internal market in electricity and natural gas introduces measures aimed at opening up the market and shifted the focus from a state oriented to a liberalized market (See also K Talus, Research Handbook on International Energy Law (Edward Elgar Publishing Limited, 2014). First Package: Directive 96/92/EC of the European Parliament and of the Council of 19 December 1996 concerning common rules for the internal market in electricity and Directive 98/30/EC of the European Parliament and of the Council of 22 June 1998 concerning common rules for the internal market in natural gas. The Second Package focused on competition by opening the electricity and gas markets by improving the third party access regime. Second Package: Directive 2003/54/EC of the European Parliament and of the Council of 26 June 2003 concerning common rules for the internal market in electricity and repealing Directive 96/92/EC – Statements made with regard to decommissioning and waste management activities; Directive 2003/55/EC of the European Parliament and of the Council of 26 June 2003 concerning common rules for the internal market in natural gas and repealing Directive 98/30/EC; Regulation (EC) No 1228/2003 of the European Parliament and of the Council of 26 June 2003 on conditions for access to the network for cross-border exchanges in electricity; and Regulation (EC) No 1775/2005 of the European Parliament and of the Council of 28 September 2005 on conditions for access to the natural gas transmission networks.

30 The Third Package Directive 2009/72/EC concerning common rules for the internal market in electricity and repealing Directive 2003/54/EC; Directive 2009/73/EC concerning common rules for the internal market in natural gas and repealing Directive 2003/55/EC; Regulation (EC) 713/2009 of the European Parliament and of the Council of 13 July 2009 establishing an Agency for the Cooperation of Energy Regulators; Regulation (EC) 714/2009 on conditions for access to the network for cross-border exchanges in electricity and repealing Regulation (EC) 1228/2003; and the Regulation (EC) 715/2009 on conditions for access to the natural gas transmission networks and repealing Regulation (EC) 1775/2005. The package was based on the following assumptions: (i) unbundling of network operators from supply or production companies; (ii) strengthening the power and independence of national regulators by granting them the right to use certain regulatory tools; (iii) cooperation between transmission system operators and the creation of a European network for transmission system operators; and (iv) increased power of consumers by providing national regulators with increased powers to enable more transparency.

31 The prospectus directive: Directive 2003/71/EC of the European Parliament and the Council of 4 November 2003 on the prospectus to be published when securities are offered to the public or admitted to trading and amending (Directive 2001/34/EC, OJ L345, 31 December 2003) and the transparency directive (Directive 2004/109/EC of the European Parliament and of the Council of 15 December 2004 on the harmonization of transparency requirements in relation to information about issuers whose securities are admitted to trading on a regulated market and amending Directive 2001/34/EC, OJ L390, 31 December 2004 were revised and MAD was replaced by the Regulation on insider dealing and market manipulation (market abuse) (Proposal for a Regulation of the European Parliament and of the Council on Insider Dealing and Market Manipulation (market Abuse) of 20 October 2011, COM(2011) 651 final).

32 According to Cameron and Heffron, the justification of this revision was twofold; the financial crisis revealed weaknesses regarding the regulation of derivatives and the increasing complexity of financial instruments required an increased investor protection (see P Cameron and R Heffron, Legal Aspects Of EU Energy Regulation (Oxford University Press, 2016), 19. Also, financial regulators saw the commodity markets as being part of the systemic risk which is faced by banks and similar institutions that trade derivatives and that they therefore seek to bring commodity derivatives within the scope of financial regulation. The EC claimed that reforms were necessary due to market- and technological developments which caused several provisions in MiFID to be outdated and plans for MiFID II emerged.

33 COM(2009) 503 final, art. 3(1).

34 An overlap in supervisory activities of ESMA and ACER exists in several areas, including reporting obligations of derivative transactions.

35 The licensing obligation is far reaching not only because it triggers obligations based on MiFID II, but the license obligation also triggers requirements based on the capital requirements directive which are triggered by a license obligation: Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms, amending Directive 2002/87/EC and repealing Directives 2006/48/EC and 2006/49/EC and Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012 Text with EEA relevance.

36 The technical criteria to when an activity is ancillary is also specified in regulatory technical standard 20 (https://ec.europa.eu/transparency/regdoc/rep/3/2016/EN/C-2016-7643-F1-EN-MAIN.PDF). Art 2 sub (1)j MiFID II. The calculation methods for establishing when an activity is to be considered ancillary to the main business of a group is specified in regulatory technical standards (Commission Delegated Regulation 2017/592 on the criteria for the ancillary activity exemption (RTS 20)), supplemented by a guidance document from ESMA (ESMA Questions & Answers on MiFID/MiFIR Commodity Derivatives Topics: https://www.esma.europa.eu/sites/default/files/library/esma70-872942901-28_cdtf_qas.pdf) Those calculation methods take into consideration that ancillary activities must constitute a minority of the activities at group level and the size of their trading activity compared to the overall market trading activity in a certain asset class must also be limited. The calculation of the size of the trading activities and capital is based on a simple average of the daily trading activities or estimated capital allocated to such trading activities, during three annual calculation periods that precede the date of calculations.

Another effect on energy companies is the exemption from MiFID II of CO2 emission rights (under Annex 1, part C (6) and (11)) and the so-called “REMIT carve-out”, under which physically settled contracts that are traded on a venue are financial instruments are exempted from the definition of financial instruments: power and gas contracts with delivery in the EU that are traded on an OTF and which must be physically settled (i.e. parties must have “proportionate arrangements” in place to make or take delivery of the underlying commodity, with “unconditional, unrestricted, enforceable obligations” to make or take delivery) are not considered as financial instrument. Replacement of physical delivery with cash settlement in this case is not allowed.

37 B De Bruijne and LM Hiemstra, “MiFID II: sombere vooruitzichten voor energiebedrijven” (2015)Nederlands Tijdschrift voor Energierecht.

38 See for example: Joint Industry Group advocacy paper on the commodity market exemption: Future EU 27 Commodity Markets Exemption under the MiFID II Review, d.d. 12 May 2020, https://www.dai.de/files/dai_usercontent/dokumente/positionspapiere/Future%20Commodity%20Markets%20Exemption_12052020_final_sent.pdf.

39 Such as the requirements based on the capital requirements directive which are triggered by a license obligation: Directive 2013/36/EU of the European Parliament and of the Council of 26 June 2013 on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms, amending Directive 2002/87/EC and repealing Directives 2006/48/EC and 2006/49/EC and Regulation (EU) No 575/2013 of the European Parliament and of the Council of 26 June 2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012 Text with EEA relevance

40 Article 9 EMIR.

41 Article 7 and 8 REMIT. Under REMIT, a list of types of transactions is provided that have to be reported to ACER and, in addition, a list of contracts which have to be reported upon request. Specific details of transactions subject to the reporting obligation include price, quantity, parties and beneficiaries (source: Commission Implementing Regulation (EU) No 1348/2014 of 17 December 2014 on data reporting implementing Article 8 (2) and Article 8 (6) of Regulation (EU) No 1227/2011 of the European Parliament and of the Council on wholesale energy market integrity and transparency). Under REMIT, a list of types of transactions is provided that have to be reported to ACER and, in addition, a list of contracts which have to be reported upon request. Specific details of transactions subject to the reporting obligation include price, quantity, parties and beneficiaries (source: Commission Implementing Regulation (EU) No 1348/2014 of 17 December 2014 on data reporting implementing Article 8 (2) and Article 8 (6) of Regulation (EU) No 1227/2011 of the European Parliament and of the Council on wholesale energy market integrity and transparency).

42 Article 8 and 10 MiFIR.

43 EMIR introduces several categories of counterparties with different obligations: financial counterparties (“FC”) as defined under MiFID II, small financial counterparties who belong to a group whose aggregate positions in OTC derivatives are EUR 8 billion or below (“SFC”), non-financial counterparties above the clearing threshold (“NFC+”) and non-financial counterparties under the clearing threshold (“NFC−”).

44 Art 9 EMIR. According to Title VII of EMIR, a trade repository is defined as a legal person that centrally collects and maintains the records of derivatives and EMIR provides for a separate section on requirements for trade repositories regarding organizational arrangements and operational reliability.

45 Market abuse under REMIT is not defined in the same way as in article 102 Treaty on the Functioning of the European Union (see paragraph 2.2.4).

46 The obligation under MiFID II to report transactions and related transparency requirements fall into two categories: (i) general transparency requirements regarding pre- and post-trade disclosure of transaction details; and (ii) transaction reporting obligations relating to a notification obligation of a market participants position to regulators.

47 Article 8 (3) REMIT.

48 LM Hiemstra, “Energy Trading and Its Multiplicity of Supervisors. Effectiveness of Fragmented Supervision and Information Sharing in View of Reporting Obligations for Energy Trading Companies”, TARN Working Paper 4/2020.

49 Article 57 MiFID II.

50 Article 2 MAR.

51 Article 3 REMIT.

52 ESMA Final Report MAR PDF, p. 48, https://www.esma.europa.eu/sites/default/files/library/2015/11/2015-esma-1455_-_final_report_mar_ts.pdf.

53 Article 17 MAR and article 4 REMIT.

54 In November 2015, the Estonian transmission system operator Elering was fined by the Estonian competition authority for a failure to disclose information on maintenance work to a subsea electricity cable in a timely manner. The maintenance work caused an outage and both the maintenance works and the outage itself qualified as “inside information” according to the authority. On 4 April 2016, a regional first instance court in Tallinn declared however that the Estonian TSO did not breach article 4 (1) of REMIT. Even though the court acknowledged that the outage of the maintenance works to the subsea cable qualified as “inside information” according to REMIT, but that Elering did not breach the obligation to disclose this information in a timely manner and that the court takes into consideration that information has been published within 60 min. This case shows that the qualification of information as inside information may depend on details and that energy companies should be ready to act resolute in case of any event such as an outage. The Estonian Competition Authority decision isn’t publicly available for reasons of confidentiality. However, the Estonian Competition Authority did publish a press release on the decision: https://www.konkurentsiamet.ee/index.php?id=27831. The decision of the Harju County Court of 4 April 2016 with number 4-15-10109/10 is only available in Estonian: https://www.riigiteataja.ee/kohtulahendid/detailid.html?id=179359134.

55 Article 16 sub 2 MAR and article 15 REMIT.

56 The European Federation for Energy Traders introduced an electronic trade monitoring system which was launched in September 2017. This system aims to provide market participants with a tool to centrally collect data for EMIR and REMIT and the reuse thereof for MAD/MAR purposes. https://www.efetnet.org/Media/News/Detail/EFETnet-s-plans-for-Market-Abuse-Regulation-MAR-.

57 Article 15 MAR and article 5 REMIT.

58 ACER Guidance on the application of REMIT, last version 17 June 2016, https://www.acer.europa.eu/Official_documents/Other%20documents/4th%20Edition%20ACER%20Guidance%20REMIT.pdf.

59 Spanish Comisión Nacional de los Mercados y la Competencia – Resolución del Consejo – Multa : SNC/DE/0046/14 – Iberdrola Generación SAU d.d. 24 November 2015: https://www.cnmc.es/sites/default/files/757366_10.pdf. The regulator found proven that Iberdrola Generación deliberately increased market prices by reducing electricity supply from hydroelectric plants in a 23 d period. Reference is made to the “Guidance on the application of the definitions set out in Article 2 of Regulation (EU) No 127/2011 of the European Parliament and of the Council of 25 October 2011 on wholesale energy market integrity and transparency”, p. 18 where ACER explains types of practices which could constitute market manipulation as follows: Actions undertaken by persons that artificially cause prices to be at a level not justified by market forces of supply and demand, including actual availability of production, storage or transportation capacity, and demand (“physical withholding”): This is for example the practice where a market participant decides not to offer on the market all the available production, storage or transportation capacity, without justification and with the intention to shift the market price to higher levels, e.g. not offering on the market, without justification, a power plant whose marginal cost is lower than the spot prices, misusing infrastructure, transmission capacities, etc., that would result in abnormal high prices.

60 On 20 February 209, Bundesnetzagentur imposed fines of EUR 150,000 on Uniper Global Commodities SE and of EUR 1,500 and EUR 2,000 on two traders in response to a case of gas market manipulation: https://www.bundesnetzagentur.de/SharedDocs/Pressemitteilungen/EN/2019/20190220_Marktmanipulation.html.

61 On 15 April 2020, OFGEM imposed a fine of £37 million on InterGen (UK) Ltd on energy market abuse: https://www.ofgem.gov.uk/publications-and-updates/finding-intergen-has-breached-article-5-prohibition-market-manipulation-regulation-eu-no-12272011-european-parliament-and-council-25-october-2011-wholesale-energy-market-integrity-and-transparency-remit.

62 Proposal for a Regulation of the European Parliament and of the Council on energy market integrity and transparency, COM/2010/0726_8 December 2010, paragraph 4.3.1.

63 P Mäntysaari, EU Electricity Trade Law. The Legal Tools for Electricity Producers in the Internal Electricity Market (Springer, 2015).

64 More information on the rationale behind financial regulations can be found in objectives of regulation based on pro-cyclicality or counter-cyclical measures as reflected on in the report of the International Center for Monetary and Banking Studies, “The Fundamental Principles of Financial Regulation. Geneva Reports on the World Economy”, June 2009, p. 31, https://www.icmb.ch/ICMB/Publications_files/Geneva%2011.pdf.

65 Rules for network access not only increase the entry level for potential interested parties, they also entail a geographical limit. Such entry barrier may prevent entities of conducting physical trading activities and related financial trading for hedging purposes. However, such limit does not apply to financial markets and the barrier in itself does not prevent parties from being active in trading in commodity derivatives. Another difference between the regulatory frameworks is that financial markets are not bound to borders and are increasingly global, whilst energy markets may have a strong national or regional focus. This could be a consequence of the limited possibilities for physical settlement, which could be bound to specific regions. Lastly, Energy Trading is strongly influenced by environmental concerns.

66 Different commodities may have different price characteristics. For example, electricity cannot be stored on an industrial scale, whilst demand is continuous, but subject to seasonal changes and this results in a high connectivity between market prices and availability, characterized by large but predictable price differences. Natural gas is possible to store, but quite costly. Moreover, both gas and electricity prices are interlinked. Another characteristic is that there is a strong correlation between prices in neighboring countries, since production and consumption are not limited by national boundaries. For the seasonal effects on demand and supply of commodities see also: Hull, supra, n 7, p. 749.

67 Impact Assessment d.d. 8 December 2010, p. 6.

68 Ibid, 20.

69 Ibid, 20.

70 Response of the European Federation of Energy Traders to Public Consultation by the Directorate General for Energy on measures to ensure transparency and integrity of wholesale markets in electricity and gas of 31 May 2010: […] a sub-optimal oversight of energy wholesale markets exists, which hinders further market development. The current regulatory situation does, in particular, not take into account the factual situation that energy wholesale markets are increasingly characterized by a wide range of actors […], cross-border trade, important derivatives markets around markets in underlying energy products and increasing liquidity in energy wholesale trading activities. https://www.efet.org/Cms_Data/Contents/EFET/Media/Documents/Public%20-%20Position%20Papers/EFET_response_to_DG_Energy_Consultation_23072010_final_sent_clean.pdf.

71 Impact Assessment d.d. 8 December 2010.

72 According to Impact Assessment d.d. 8 December 2010 p. 28: “Extension of financial market legislation to cover all relevant energy markets would bring these markets within the financial regulatory framework. This framework, in particular MAD, is designed to establish a genuine single market for financial services. Notwithstanding, the close links between energy markets and some financial markets, the requirements of financial market supervision differ in important ways from energy market oversight. Explicitly extending MAD to cover all energy markets would undermine the focus and effectiveness of MAD. […] It the light of the strong advice from financial and energy regulators, and the distinct scope of MAD, this option was not considered in detail.”

73 When taking these questions one step further, one could dispute about the reasons trading venues should be regulated and the importance of protection of investors against market abuse, promotion of market integrity and protection against systemic risk. See AM Whittaker, “Tackling Systemic Risk on Markets: Barings and Beyond” in F Oditah (ed), The Future for the Global Securities Market. Legal and Regulatory Aspects (Clarendon Press, 1996), 259.

74 Ibid.

75 C Ford and J Kay, “Why Regulate Financial Services” in F Oditah (ed), The Future For The Global Securities Market. Legal and Regulatory Aspects (Clarendon Press, 1996), 154, 148.

76 REMIT has an impact on physical forward contracts for electricity and gas, which fall outside the scope of MiFID II and the calculations for exemptions and – consequently – related rules from EMIR and related capital requirements based on Directive 2013/36 EU and regulation EU 575/2013 on access to the activity of credit institutions and the prudential supervision of credit institutions and investment firms, amending Directive 2002/87/EC and repealing Directive 2006/48 EC and 2006/49/EC and regulation EU 575/2013 on prudential requirements for credit institutions and investment firms and amending Regulation (EU) No 648/2012. Based on article 498 sub (1) of the regulation, commodity traders are exempted. For FC’s and large NFC’s (with a position taken in speculative OTC derivative contracts which exceeds a threshold of EUR 3 billion), heavier duties regarding, for example, clearing are imposed. Most energy companies stay below this threshold.

77 On 16 February 2017, ACER issued an open letter to market participants indicating its initiative to start an assessment of completeness, accuracy and timely submission of the data received under REMIT. It emphasized that there are many data quality issues regarding reporting. https://www.acer-remit.eu/portal/public-documentation.

78 EMIR, recital 29; MiFID II recital 12.

79 EFET response to EC call for evidence on EU regulatory framework for financial services, 31 January 2016, p. 5, https://www.efet.org/Home/search?key=EFET_response_EC_31012016.

80 See Council of European Energy Regulators response to ESMA Consultation Paper on the Impact of Position Limits and Position Management and on Weekly Position Reports, 20 December 2019, p. 3, https://www.ceer.eu/documents/104400/6509669/C19-MIT-84-003_ESMA+CP_CEER+response_for+publication/12c5d37f-7b46-bfd4-60be-739d68b6aeff.

81 Joint Energy Associations Group response to ESMA Consultation Paper MiFID II review report on position limits and position management of 19 December 2019: https://cdn.eurelectric.org/media/4142/jeag_response_mifid_ii_cp_remit_191220219_final_clean-2019-030-0761-01-e-h-3B13975A.pdf.

82 REMIT, recital 4.

83 A Gentzoglanis, 2013, Derivative regulation and its impact on energy and utility firms, European Energy market 2013 10th conference paper.

84 Interesting in this respect is the view of Garicano and Van Reenen who state that the real problem with market participants is the systemic risk they impose and that proposals to improve transparency and corporate governance are useless. See L Garicano and J Van Reenen, “LSE Centre for Economic Performance: Financial Regulation – Can We Avoid Another Great Recession?” (21 Apr 2010) British Politics and Policy at LSE, Blog Entry: https://eprints.lse.ac.uk/41365/.

85 European Parliament, DG for Internal Policies, “Regulating Agricultural Derivatives Markets”, November 2013, https://www.europarl.europa.eu/RegData/etudes/divers/join/2013/513989/IPOL-AGRI_DV%282013%29513989_EN.pdf.

86 Ford and Kay, supra n 75, p. 54.