Abstract

Knitwear producers in New Zealand are looking for ways to deal with the uncertainties that have arisen due to the COVID-19 pandemic. This research considers the impact of the pandemic and its effects on the development and long-term survival of the knitwear sector. An anonymous online survey was undertaken among New Zealand’s established knitwear manufacturers, with seven taking up the survey. The respondent companies accounted for around half of the total workforce employed in the country’s knitwear sector. The data were analysed using both quantitative and qualitative methods. A SWOT analysis was conducted to place the sector in a global context, identifying necessary measures for future strategic planning. The findings revealed that the supply chain has been disrupted, some businesses have stalled, and the cost of obtaining raw materials has skyrocketed. Due to the impact of the pandemic on the tourism industry, revenues have fallen. As COVID-19 is an ongoing challenge, knitwear manufacturers need to rearrange their supply chains to increase local suppliers and explore new and innovative ways to engage with domestic customers.

Introduction

The COVID-19 pandemic has created uncertainties, forcing New Zealand’s knitwear manufacturers to develop strategies to address the new economic context in order to survive. Manufacturing in general has been impacted, and there are indications that smaller manufacturers have been less able to withstand the consequences. Many are closing their operations. Between September and November, 2020, 16,234 enterprises in New Zealand permanently closed compared to 7154 during the same period in 2019, which is an increase of 127 percent (Edmunds Citation2021). Understanding the current state of the knitwear industry, how it is progressing, and sharing strategies for surviving this critical scenario are vital. This study is an initial attempt to gather current information and learnings from manufacturers’ experiences to help develop solutions and identify future opportunities.

Coronavirus 2 or COVID-19, a novel type of severe acute respiratory syndrome, struck the world in late 2019, affecting every country around the globe. Governments throughout the world struggled to formulate strategies to stop the spread of the virus. Many countries went into months-long lockdowns, limiting cross-border travel and trade, with COVID-19 containment measures directly impacting the global economy. In 2020-21, the global gross domestic product (GDP) loss from the pandemic was estimated to be over USD 9 trillion, with countries that relied on tourism, travel, hospitality and entertainment for their growth being the most heavily impacted (Gopinath Citation2020).

The COVID-19 pandemic has had a significant impact on textile and fashion industries. Globally, there was a marked fall in demand for apparel products, with some 86 percent of garment manufacturing businesses seeing a drop in orders (Sedex Citation2021). A Women's Wear Daily article, published December 24, 2020, reported that as people stayed at home and economies shut down, several well-known brands were severely hit by COVID-19. Many international brands and retailers delayed payments or cancelled orders for goods that had already been manufactured or were in the process of being made (OECD Citation2020). As a result, many enterprises had to shut down most or all their operations (Roberts-Islam Citation2020).

Following confirmation of a few local cases of COVID-19 in March, 2020, New Zealand was one of a few countries to lock its borders, impose strong travel restrictions, and issue strict stay-at-home orders to prevent the spread of the disease. While mortality rates remained low, the country’s economy was severely affected. Although the garment sector in New Zealand is well established, there has been little research or publication to date on the impact of the COVID-19 pandemic. This paper identifies the advancements that have been made in the country’s knitwear manufacturing businesses and provides an outline of the industry’s current situation in the aftermath of the pandemic.

Literature review

Many studies have recently reported the impact of the COVID-19 pandemic on global businesses, economies, and supply networks (Fairlie Citation2020; Maliszewska, Mattoo, and Van Der Mensbrugghe Citation2020; Xu et al. Citation2020). COVID-19-related publications have also begun to appear in the garment and textile industries. While some reports are there on its influence on the global textile and fashion supply chain (Chakraborty and Biswas Citation2020; Ahsan Citation2020), a few others have analysed its economic implications on countries with bigger apparel industries. Boudreau and Naeem (Citation2021), for example, examined the economic impact of the pandemic on Bangladesh’s ready-made garment factories, indicating significant revenue losses, order cancellations, and challenging times for smaller businesses. Other authors such as Wulandari and Darma (Citation2020) have searched for positive outcomes, researching tactics and innovative ways to improve textile sales, and Zhao and Kim (Citation2021) worked on a conceptual model that depicted the links between different value chain segments in the garment and textile sector. Studies that investigated the knitwear sector and the challenges faced by knit manufacturers were conducted in India (Mahajan and Bains Citation2020; Mehta and Kaur Citation2021), however, none has been conducted explicitly in New Zealand. The COVID-19 pandemic has had a significant impact on the industry globally; subsequently, it is important to understand both the positive and negative ways that local regions and economies have responded. As the pandemic’s far-reaching impacts will not be resolved anytime soon (Kissler et al. Citation2020), businesses will need to enhance their preparedness to adapt, recover quickly and avoid unplanned interruptions in future.

Knitwear Manufacturing in New Zealand

Knitting is one of the earliest methods of clothing production (Au Citation2011), predating the industrial revolution as a method of mass production (Black Citation2012). It was introduced to New Zealand in the nineteenth century together with wool. Colonists from Britain who settled in the country realised that the topography was comparable to home, making it appropriate for raising sheep. Settlers brought spinning, weaving and knitting tools and used the wool grown in New Zealand to manufacture clothing (Smith and Finn Citation2015). This allowed them to meet their families’ basic needs for woollen apparel, and to supplement their income by making and selling apparel products (De Pont Citation2018). Consequently, both wool and knitwear production found a home in the country.

During much of the twentieth century, wool and apparel enterprises were among the top industries and main contributors to the country’s economy. From the early 1950s through to the 1960s, wool and its products were the main export earners (Briggs Citation2003). A considerable number of people worked in the knitting industry, from winding yarns through to cutting, linking, stitching and steaming garments (De Pont Citation2018). During the late 1980s and early 1990s, trade liberalisation and economic restructuring severely impacted the manufacturing industry. The domestic economy was opened to global trade, tariffs on goods entering were reduced, and clothing imports increased (Dalziel Citation2016). Domestic output in the garment manufacturing industry halved between 1992 and 2001, while imported clothing grew from 20 to 60 percent of the market (Burleigh Evatt and NZIER, in Lewis, Larner, and Heron Citation2008). The remaining garment production shifted to value products, with items characterised by higher quality, brand name, improved performance, product innovation, or the ability to fit a specialised function being exported (MBIE Citation2018a). Exports became critical to business survival. Despite a drop in domestic sales of locally manufactured goods, garment exports increased. Between 1992 and 2001, the percentage of output exported increased to more than 25 percent (Lewis, Larner, and Heron Citation2008).

There was a significant fall in local textile and garment manufacturing in the last few decades of the twentieth century. However, the industry survived, with knitwear manufacturing proving to be the most important remaining area of textile production. The knitwear production process has advanced significantly over the last few decades. Modern technologies and automated processes that require less labour and enhance production allowed knitwear manufacturing to endure (Smith and Finn Citation2015). The invention of 3D seamless knitting technology reduced the number of post-knitting activities such as cutting and sewing, by knitting a whole garment on the machine (Underwood Citation2009). Shima Seiki and Stoll are the pioneers and leaders in this field, having invented Wholegarment® and Knit&Wear®, respectively (Ramsay Citation2013). Since the early 2000s, the country’s knitwear sector has been importing seamless knit technology, and its demand has continued to expand (Smith Citation2013).

Knitwear manufacturing represents a modest and medium-sized sector in New Zealand. Manufacturers produce high-end, knitted products for sale both domestically and internationally. In 2019, the gross export of knitted garments like jerseys, pullovers, cardigans, waistcoats and other related articles made of wool and fine animal hair was USD 6.4 million (WITS Citation2022). Auckland in the North Island and Canterbury in the South Island are major hubs for knit production. Other districts that support knitwear production include Palmerston North, Dunedin, the Bay of Plenty and Wanganui. There is currently a lack of accessible data on the exact size of the industry and the current number of garment manufacturers operating in the country, which this study aims to address.

Supply chain challenges

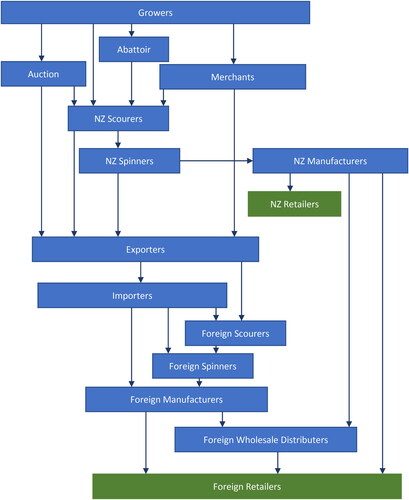

The knitwear supply chain starts with the production of fibres. Luxury fibres and blends are typically involved in New Zealand’s knitwear exports and follow a similar pattern to the country’s supply chain of strong wool. Conforte, Dunlop, and Garnevska (Citation2011) demonstrated the flow of wool across the country’s strong wool value chain, as shown in . Farmers sell the produce to brokers, who either export it to overseas processing facilities, or sell it to a limited number of locally based facilities. In a NZ Herald article, published August 13, 2020, Nigel Hales, chief executive of New Zealand Woolscouring, one of the country’s largest scouring factories, reports that there were 28 wool scourers in the early 1980s, but that has now been reduced to two. One is in Napier in the North Island and another in Timaru in the South Island.

Figure 1 Flow of wool through New Zealand’s strong wool value chain (Adapted from Conforte, Dunlop, and Garnevska Citation2011).

In the area of spinning, mule spinning is employed for finer fibres and blends like merino, possum and cashmere (Cottle and Wood Citation2012), which are specifically used in machine knitting. Woolyarns in Lower Hutt is the only mule spinning mill in the whole southern hemisphere (Khan Citation2020). Even though the country produces a substantial proportion of textile fibres, the supply chain engaged in yarn production is highly fragmented, which has a significant impact on the pricing of final goods. Today, New Zealand’s broader apparel manufacturing businesses consist of a small handful of niche, ethical or high-end designer labels (Tearfund Citation2019), who are heavily reliant on international suppliers for most of their production needs.

Given the knitwear sector’s reliance on local and foreign suppliers, as well as the unique circumstances of the COVID-19 pandemic, the authors believed it would be useful to understand how the industry has handled the crisis. There has been limited research into how New Zealand’s knitwear sector has been disrupted and what tactics have been used to successfully maintain its viability (Bezuidenhout et al. Citation2021). By reviewing specific industry reactions and producing a SWOT analysis, this study provides insights into potential strategies and new possibilities. We have also made some concrete suggestions to help the knitwear sector emerge from the pandemic and carve out a distinctive, more sustainable niche in the global market, based on indications identified in the data.

Methodology

An anonymous online survey was conducted in April, 2021. An initial online search identified approximately 45 apparel knitting companies operating within New Zealand. Companies that manufactured offshore and did not have an online presence such as an e-mail address, were excluded, which decreased the number of manufacturers to 20. The Textile Design Lab (TDL), a research laboratory at Auckland University of Technology that is engaged with the country’s textile industry, was consulted to collect e-mail addresses of companies that were legitimate and active in knitwear manufacturing.

The 20 manufacturers were approached through e-mail, to request their participation in the survey. Nine of the 20 business owners responded, with two stating that they were unable to participate due to unspecified reasons. Seven participants took up the survey, a valid return given the industry’s modest size. Because the survey was anonymous, limited information about the respondents could be gathered. The participants owned small and medium-sized knitwear manufacturing facilities that together employ over 330 employees, which is half of the total number of employees involved in knitwear production. A 2018 report from the Ministry of Business, Innovation, and Employment identified 660 persons employed in knitting production within New Zealand (MBIE Citation2018a). The survey used Qualtrics software to present open-ended and closed-ended questions concerning COVID-19’s impact on the supply chain, revenue and government support. Results were collected and the data analysed using both numerical and qualitative methods.

A SWOT (strengths, weaknesses, opportunities and threats) analysis was then carried out to synthesise the data about the current pandemic situation across the sector and to determine steps to be taken for future strategic planning. SWOT analysis is a method widely employed by businesses globally to examine an organisation’s internal and external environments (Ghazinoory, Abdi, and Azadegan-Mehr Citation2011). It has been utilised either alone or in combination with other analysis methods to help find solutions to complex problems. SWOT analysis was utilised to formulate development strategies for the textile and garment sector in Pakistan (Kanat et al. Citation2018); Uzbekistan (Kim and Park Citation2019); South Korea (Jo and Lee Citation2018); Sri Lanka (Wickramasinghe and Abdullah Citation2011); Iran (Atilgan, Derafshi, and Kanat Citation2011); China (Han et al. Citation2017); and the United Kingdom (Li et al. Citation2016). The SWOT analysis has provided growth strategies to individual businesses in the apparel manufacturing sector (Colovic Citation2014; Tuan Citation2012; Görener, Kerem, and Korkmaz Citation2012), and can assist industries in responding to the challenges of the COVID-19 pandemic. Rahman (Citation2020), for example, used SWOT analysis along with Porter’s Five Force Model to recommend measures for preventing the Bangladesh Garment Manufacturing and Exporters Association from suffering COVID-related losses. There is potential for a SWOT analysis of New Zealand’s knitwear industry to identify opportunities for its growth.

Scope and timing

This study did not look at the entire garment manufacturing business but focused specifically on knitted garment products. Other businesses supporting knitwear manufacturing such as fibre and yarn processing, dyeing and finishing, were omitted from this study. The research was conducted in April, 2021, following the first major lockdown in March-April, 2020, and prior to the second, extended lockdown in August-December, 2021. Although the COVID-19 outbreak was still affecting many regions globally at the time, New Zealand remained pandemic free, mostly due to its “COVID elimination” strategy and strict border restrictions (Baker, Kvalsvig, and Verrall Citation2020). At the time of writing, the COVID-19 vaccine was being rolled out to the public in a staged plan which commenced in April, 2021.

Results

New Zealand supports small businesses, with small and medium-sized enterprises (SMEs) representing over 97 percent of all businesses, employing 29 percent of the workforce and contributing 28 percent of the country’s GDP (MBIE Citation2018b). Small businesses in New Zealand have fewer than 20 employees, small-to-medium have between 20 to 49, medium have between 50 to 99, and large have more than 100 employees (MBIE Citation2014).

As the online survey was anonymous, the participants were given alphabetical identifiers ‘A’ through ‘G’. contains information about the participants and their businesses. The survey participants were New Zealand manufacturers who were owners of small and small-to-medium-sized enterprises; however, one participant owned a large business. All firms produced their own knitwear labels, and most of them produced for other apparel brands as well. Many of these manufacturers were also active in retailing, wholesaling and export activities. They were not involved in farming wool or yarn manufacturing.

Table 1. Participant information.

Supply chain management

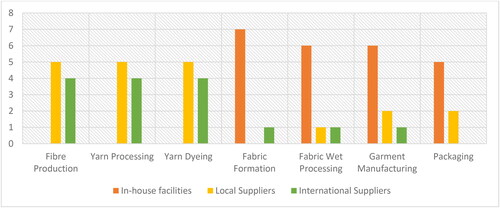

Participating companies depended heavily on external sources for fibre processing, yarn processing and yarn dyeing operations. The survey found that Companies B, D and G relied both on local and international suppliers for their yarn needs, whereas Company A depended solely on international suppliers. Companies C and E procured yarns from locally based suppliers, however, Company F made no mention of its yarn source. More developed in-house facilities were available for knitwear manufacturers across the latter stages of the supply chain. The survey reported that, other than Company F, all others had in-house fabric formation, wet processing and garment manufacturing capabilities. Packaging was done in-house by all except for Companies A and F, who relied on local vendors. shows the reliance of the participating firms throughout the knitted apparel supply chain.

Figure 2 Manufacturers’ reliance at various parts of the supply chain.

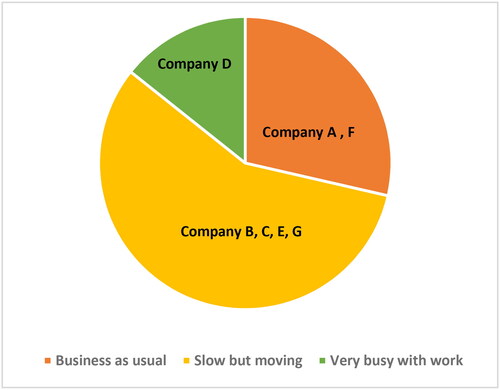

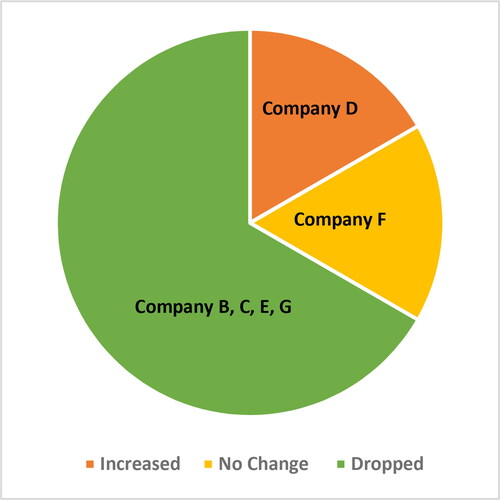

The COVID-19 pandemic created global supply-chain bottlenecks, causing many enterprises to stall (The Treasury Citation2021). Nearly half of the manufacturers that participated in this survey were reliant on international suppliers for the initial stages of the supply chain. Manufacturers who relied on local suppliers were also affected due to the countrywide lockdown in the initial months of the pandemic. Knitwear makers had to deal with the consequences of slower deliveries and higher shipping costs from overseas suppliers. depicts the impact of COVID-19 on the supply chain. Company D reported an increase in business, Companies A and F indicated normal business operations, while Companies B, C, E and G stated that business had slowed down but was still moving. This could be because supply chains that were dependent on domestic suppliers had fewer blockages, whereas businesses that relied on foreign suppliers suffered a greater slowdown. Although border restrictions were a disaster for some manufacturers, they were a windfall for others. When asked to comment on the effects of border restrictions on their business, some contradictory responses were noted, presented here as quotes in .

Figure 3 Impact on the supply chain.

Table 2. Selected quotes from survey participants on the impact of border restrictions.

Company D benefitted from border limitations and was able to increase production. As New Zealand was better able to control the spread of the virus than many other countries, a few of the country-based brands that were previously producing in China switched to domestic suppliers, keeping some manufacturers busier than normal. However, border restrictions hampered normal operations for Companies E and G.

Revenue generation

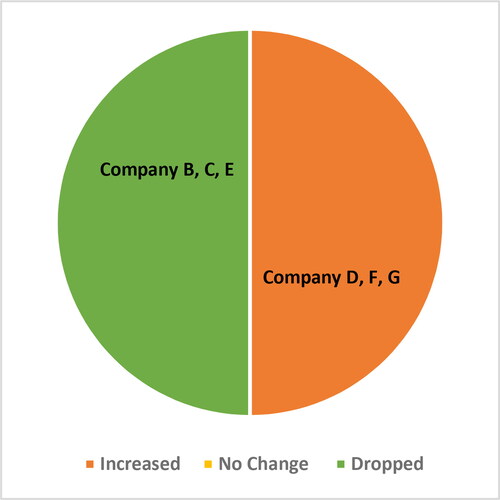

Revenues in the knitwear industry decreased, with the influence on commerce for domestic and foreign markets shown in and . Company A prefered not to answer questions related to revenue, but of the other six businesses, half reported a drop in domestic sales. They attributed this decrease to a drop in tourism as visitors were unable to enter the country due to the border restrictions. On the other hand, brands that catered to a wider range of consumers for domestic or online sales were less affected. Company B reported that: “We have two brands. On our wholesale-only brand which had a lot of retailers selling to tourists in New Zealand and Australia, the impact has been approximately 80 percent down. Our other brand that sold to a mix of domestic and tourists has been less affected.” Half of the businesses, though, experienced an overall increase in domestic sales, reporting a jump in online sales as a result of an online shopping boom. International sales fell, with most businesses reporting a drop. There was no change in revenue for Company F and Company D reported an increase in sales. A few enterprises planned to restructure their operations to focus on the domestic market because they were more optimistic that things would return to normal in Australasia sooner than in other parts of the world. Company E suggested it could “realign the business to a more domestic market”.

Figure 4 Impact on domestic sales.

Figure 5 Impact on international sales.

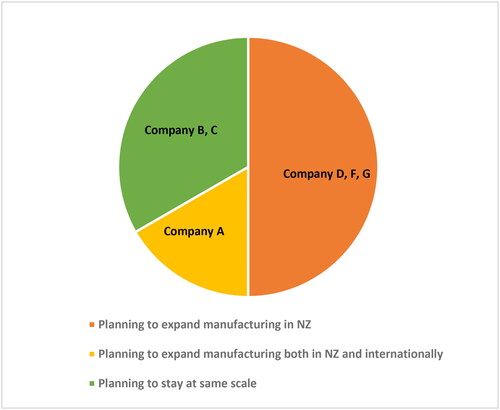

On being asked about the impact of the pandemic on their future business plans, the feedback was extremely positive. shows the future aspirations of the companies surveyed. Companies D, F and G expected to boost manufacturing locally, Company A planned to expand both in New Zealand and globally, while Companies B and C planned to stay on the same scale. Company E, however, did not mention any growth plans but did express its desire to realign business strategies to a more local economy. Although most businesses reported lower sales, there was hope and positivity expressed for things to get back to normal.

Figure 6 Future business plans.

Governmental intervention

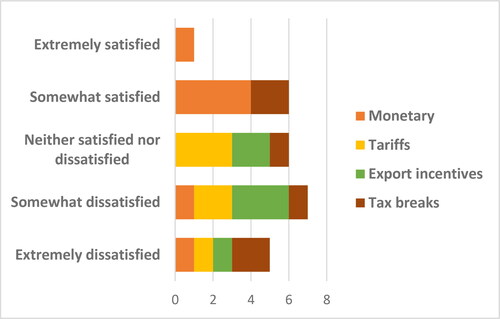

The government offered a variety of tax relief to businesses, including a COVID-19 wage subsidy to assist firms in keeping people employed and ensuring their long-term viability (BDO NZ Citation2020). This study investigated knitwear manufacturers’ satisfaction with the assistance and services provided by the government. depicts the participants’ satisfaction with the government’s monetary assistance, tariffs, export incentives and tax exemptions during the COVID-19 outbreak.

Figure 7 Review of government support.

Most manufacturers were very satisfied with the monetary support, but responses to the government’s tariff policies and export incentives ranged from neutral to dissatisfied. The survey revealed a mixed response to the evaluation of tax breaks, with responses ranging from moderately satisfied up to extremely dissatisfied. There was no special consideration given to knitwear manufacturers, and the aid granted to all sectors was equal. Manufacturers had to contend with a shortage of skilled labour, rising wages and compliance expenses on top of the supply chain bottlenecks and ongoing restrictions on foreign tourism. provides participant responses on additional help from the government. Manufacturers were looking for ways to save costs in order to retain their skilled workforce in times of falling revenue. Increasing labour and regulatory costs were sources of concern for small businesses such as companies F and G.

Table 3. Some direct quotes from participants on additional help sought from the government.

SWOT Analysis of New Zealand’s Knitwear Manufacturing Sector

A comprehensive understanding of the business environment is required for strategic planning and is one of the key factors for facilitating this SWOT analysis (Hill and Westbrook Citation1997; Ying Citation2010). In a Business News Daily article updated October 19, 2022, the strengths and weaknesses of an industry are reported to include internal factors such as human resources, physical and financial resources, while opportunities and threats focus on external factors such as market trends, economic forces and political regulations. The analysis reveals how strengths can be leveraged to create new opportunities, as well as ways to exploit growth avenues by addressing weaknesses. The authors carried out a SWOT analysis on New Zealand’s knitwear manufacturing sector, based on the literature discussed in this paper and findings from the survey. The SWOT analysis is presented in .

Table 4. SWOT analysis of New Zealand’s knitwear manufacturing sector.

Proposed strategies for knitwear manufacturers

Looking at the influence of the COVID-19 pandemic and the SWOT analysis, the following strategies are put forward to assist in reshaping operations for knitwear manufacturing in New Zealand:

Maintaining a flexible supply chain and bringing in more local players will help lessen the dependency on foreign suppliers. Partnerships with local businesses including joint ventures, would help the industry and other ancillary sectors thrive (Wulandari and Darma Citation2020).

Due to rising consumer interest and a genuine need to address social and environmental concerns, prioritising sustainability when sourcing products and processes would be beneficial (Berg et al. Citation2019).

Using locally produced material would reduce the risk of supply shortage, promising good availability of resources at all times. It would also improve the niche and point of difference for New Zealand’s knitwear manufacturing (Smith and Finn Citation2015).

Businesses should constantly strive to improve their supply chain and product innovation to increase their sales potential (Wangsa and Kristianti 2018).

Digitising operations need to be scaled to support innovation across the entire fashion value chain. This should include design (3D design, AI planning), merchandising (virtual sampling, video sign-offs), sales (digital sell-in, virtual showrooms), consumer engagement (virtual shows, social selling), sourcing and the supply chain (nearshoring and vendor integration) (Berg et al. Citation2020).

Pursuing diversified markets through e-commerce to reach out to new customers (Wulandari and Darma Citation2020).

Training a locally available workforce to operate knitwear machinery, reducing the reliance on foreign talent.

Discussion

The seven enterprises surveyed for this study were small and medium-sized businesses that play a vital role in knitwear manufacturing. Although the response rate appears to be small, the size of the knitwear sector in New Zealand is relative to its population size and thus smaller than in more populous nations. The companies that participated represented a good portion of the sector, employing half of the employees working in knitwear production (MBIE Citation2018a).

Supply chain disruptions

The scope and magnitude of damage from COVID-19 is vastly different from prior catastrophes such as China’s SARS outbreak in 2003, or Indonesia’s tsunami in 2004 (Xu et al. Citation2020). COVID-19 not only disrupted local supply chains but had a significant impact on global supply chains at every stage, from raw materials to end consumers. It is likely the pandemic will fundamentally change the makeup of global textile, clothing, leather and footwear supply chains, accelerating the reshoring or nearshoring of manufacturing (ILO Citation2020).

New Zealand’s manufacturers transfer their goods and raw materials across multiple countries due to the globalised nature of the garment industry. Depending on size and delivery time, these commodities are moved by a combination of land, sea and air freight. Multiple national and international lockdowns have disrupted manufacturing by slowing or halting the movement of goods. The costs to procure raw materials from overseas suppliers have increased significantly. Items and services needed for garment construction such as yarn, fabric, stitching threads, buttons, trims and other components, were often sourced from offshore companies. While raw material is produced in-country, it is often sent offshore for processing. For example, New Zealand-grown merino wool is sent to China or Vietnam for scouring, spinning and dyeing processes and later imported back to be knitted into apparel products.

Lockdowns around the world have drawn attention to the risks of high supply-chain interconnectedness and the problems associated with global trade. Interruptions, lockdowns and border closures on a national and worldwide scale impacted the movement of products. The cost of buying raw materials soared, and operations stalled. Cost increase, caused by a lack of availability of certain supplies as many countries imposed extreme lockdown measures, hampered routine production and deliveries. A global shortage of shipping containers and New Zealand’s severe COVID-19 regulations for ships and sailors added to the shortages and costs (Walters Citation2020). Additional compliance and expense caused many shipping companies to abandon their journeys (Walters Citation2020). This resulted in yarn and supply shortages, which increased costs further. Knitwear makers that relied on overseas suppliers for goods also saw a slowdown in manufacturing. Businesses had little choice but to wait for their goods as fewer aeroplanes delivered freight and long delays were reported at the ports (Du Plessis and Drive Citation2020). Manufacturers who relied on home suppliers were found to be less affected. This study suggests that if manufacturers want to economise on raw material imports and avoid future disruptions they should seek to reduce their dependency on overseas suppliers and enhance their domestic supply chains.

Suppressed consumer demand

The garment industry has suffered a significant drop in demand globally. Consumer demand for clothes was suppressed by quarantine measures, retail store closures, loss of income, and a fear of spending money during a time of economic uncertainty (Xu et al. Citation2020). Major brands such as Adidas, Ralph Lauren, Gap and Inditex were forced to close stores in several countries in the first few months of COVID-19-related restrictions (ILO Citation2020). According to global statistics, 50 percent of factories and their supplier plants were not operating at full capacity in 2020, and 15 percent of all manufacturers produced less than half of their capacity (RBA Citation2020). The countries with the most trade integration and where tourism trade played a significant role in the economy suffered the greatest losses (Maliszewska, Mattoo, and Van Der Mensbrugghe Citation2020). As this study shows, New Zealand businesses that were reliant on the tourist market were heavily impacted. Globally, travel had come to a halt as of mid-March, 2020, and as of May, 2022, travel had yet to fully resume in New Zealand, with a gradual relaxing of border restrictions planned over the coming months.

Knitwear makers in New Zealand faced a significant economic impact because of the COVID-19 pandemic. Both local and international markets saw a drop in revenue. Brands that relied heavily on tourism for domestic sales were severely hurt but there was an increase in domestic sales. People had limited access to foreign marketplaces as travel was prohibited and shipping was delayed, shifting them towards local markets to meet their requirements. There was also a widespread drive to buy local and support domestic industries. During the early days of the pandemic, people were encouraged to buy locally made goods, not only to aid the economy and save employment, but also to ensure timely deliveries. The ‘Buy New Zealand Made’ campaign was launched as a long-term strategy to assist local manufacturers in competing with global suppliers (Jennings Citation2020).

International sales were also down during the pandemic, consistent with a reported drop in demand for garment products around the world. Social gatherings were rare, and people were primarily confined to their homes, preventing them from purchasing new clothing through normal retail channels. The pandemic also impacted transportation connectivity. A Mallory Alexander International Logistics news article, published May 7, 2020, reported that shipping services reduced the number of port calls due to declining demand and cargo imbalances, generating uncertainty for knitwear exporters. However, a few participants reported an increase in international sales, with a huge acceleration reported on online channels. A surge in online sales for both local and international markets was evident. New Zealand Post data indicates that there was a 105 percent increase in online buying when the country moved into lockdown (NZ Post Citation2020). A similar trend was observed around the world, which may have aided local exporters in gaining revenue from digital sales. This might be viewed as a silver lining and a growing opportunity for the sector moving forward.

Government responses and their effects

Government intervention was needed to contain the virus, with economic support measures necessary to offset the socio-economic effects. Monetary aid, bailouts, nationalisation and stimulus programmes were used by governments around the world to handle the tremendous economic consequences of halting business activity during the pandemic (OECD Citation2020). New Zealand unveiled an NZD 12.1 billion package, the world’s largest per capita package, which included wage subsidies, healthcare reform, money for low-income families, and reforms to business taxation (Graham-McLay Citation2020).

Lockdown closures in garment manufacturing impacted both businesses and workers, therefore government assistance was vital. Companies benefitted from a short-term government scheme designed to subsidise wages and keep people employed during the lockdown. This survey found that while several respondents were content with the government’s financial assistance, many were dissatisfied with its policies on tariffs, export incentives and tax breaks. During the pandemic’s initial phase, manufacturers sought more help in the form of business subsidies and export incentives. Suggestions made by participants of this survey included involving more domestic companies in government procurement and considering compliance costs for local manufacturers. Knitwear producers would like to see more government support in developing a skilled workforce as there is currently a shortage of workers with specialised skills. Issues with the supply chain are also set to continue, with shipping delays contributing to the rising costs of trade. Subsequently, it is critical to be thinking long term, and consider how to support and protect local manufacturing. By assisting local producers, the government would not only address supply-chain difficulties but also contribute to the growth of the local economy.

Knitwear manufacturers in the country have experienced numerous obstacles since tariffs were removed in the late 1980s, and the industry today is much smaller due to increased international competition. Knitwear items make up a small but unique part of the country’s manufacturing economy, and government support for the industry could be enhanced by initiatives tailored toward growing local manufacturing resilience and capability.

Reshaping business for the future

Despite the vulnerability of the supply chain and a significant drop in revenue, knitwear producers remained optimistic about future opportunities. They were unsure whether it was commercially feasible to produce clothing in the country prior to the pandemic. This scepticism was dispelled during the pandemic as it was discovered that procuring locally was more advantageous than relying on international suppliers and trade. While one participating company proposed to expand internationally, there was a clear indication that manufacturers anticipated growing locally, or staying at the same scale for a while. None of the businesses that replied to the survey planned to cut or close their operations. However, this may not be consistent across the industry, as companies planning to shut down may not have participated in the survey.

The overall impact of the COVID-19 pandemic on the country’s knitwear manufacturing sector has been mixed. Sales are projected to stay low for the foreseeable future, since cross-border travel will take time to bounce back and foreign exchange earnings will be difficult to achieve. Continual disruptions in the supply of goods and services are likely to continue occurring around the world. For the manufacturing industry to recover and regenerate quickly, it is critical that all segments of the supply chain collaborate to develop sustainable and innovative business models. It is a moment to reassess and re-evaluate the industry’s strengths and weaknesses, and to take advantage of the opportunities that the pandemic has brought. The SWOT analysis provided in this paper sees opportunities for increased global demand for quality knitted products, online sales, and consumer awareness of sustainable products, and suggests manufacturers work towards this. While staying ahead on digital platforms and supporting the sector, the government must assess the long-term consequences of the pandemic on manufacturing. The crisis provides a chance to increase the value of “New Zealand-made”.

Conclusion

As a major wool producer, with some remaining domestic processing capacity and a growing interest in developing the value of the wool sector, the knitwear industry offers both technical and manufacturing capabilities that could be better utilised. Manufacturing was impacted by the global consequences of the COVID-19 pandemic in 2020. Lockdowns in New Zealand and other parts of the world have had immediate ramifications for local and international supply networks. Local providers, particularly in areas of fibre processing, yarn manufacturing and dyeing, require reinforcement. The supply chain has become more vulnerable and returning to normal will be difficult. Supporting local suppliers would help to remove the risk of over-reliance on international suppliers and mitigate the threat of rising freight rates and delivery delays. Prioritising sustainability when sourcing items and processes would be advantageous and employing locally produced material would lessen the danger of supply shortages, ensuring constant access to resources. It would also support the growth of knitwear products, a niche in the global market.

On the revenue side, the curtailment of the tourist trade has had a significant impact on domestic sales. With the country revising its approach to mass tourism (Withers Citation2021), it will be difficult for manufacturers to return to business-as-usual in tourism-related sales. Finding new methods for redirecting domestic markets needs to be a key focus. Internet sales should be prioritised in order to attract new international clients. Along with digitising all business operations, enterprises should seek to enhance their supply chains and product innovation to increase their sales potential. While the government’s short-term wage subsidy was appreciated, further government assistance is critical. To take businesses forward, more skilled workers are needed, and manufacturers are seeking government assistance in educating new talent from within the community.

While the immediate priority of the knitwear apparel sector is to navigate through the crisis brought on by the COVID-19 pandemic, this is a suitable time to implement improvements that will have a long-term impact. There are potential strategies for change based on the industry’s strengths, weaknesses, opportunities and threats that can benefit local knitwear enterprises and other small and medium-sized enterprises in other parts of the world in the design of longer-term, more sustainable industries.

Limitations and future studies

While doing an online survey amid a pandemic was convenient, it had several drawbacks. Given the uncertainty around the changing nature of the pandemic and its impact on the future, approaching individuals and asking them to share their experiences was difficult. The seven business owners who replied represent a small but useful sample size, but do not represent the entire industry. This issue could be addressed in future by conducting an online or telephone interview with a bigger set of companies. The SWOT analysis in the report is also a limited appraisal of the knitwear sector’s performance and attributes identified by the authors, and there are opportunities for industry insiders to expand it further.

A follow-up study could corroborate the conditions described in this report over a longer period, and investigate further measures to rehabilitate and expand the knitwear industry. As several manufacturers declined to participate in this survey, it would be useful to find out how they have fared once the borders open and the supply chains are restored. Furthermore, it may be useful to compare the effects of the pandemic on the knitwear manufacturing industries of other countries to highlight global impacts and local responses.

Acknowledgements

We would like to thank our colleague, Mr Peter Heslop (Manager, Textile Design Lab, AUT), for his assistance in developing the survey. We would also like to thank all the knitwear manufacturers who took part in the survey. Thank you to the reviewers of this work who offered helpful and insightful feedback which improved this article.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Notes on contributors

Mitali Nautiyal

Mitali Nautiyal is a PhD candidate at Auckland University of Technology, School of Art & Design, New Zealand. Her doctoral research focuses on the environmental impact of the textile industry, with the aim to develop a design tool that can be used to evaluate environmental sustainability of apparel products. [email protected]

Frances Joseph

Frances Joseph is Professor of Material Futures in the School of Future Environments and Director of the Textile and Design Lab at Auckland University of Technology, New Zealand. Her research focus on materiality and textility includes areas of intra-active textiles, bio-based materials, local production systems and material ecologies. [email protected]

Amabel Hunting

Amabel Hunting is Senior Lecturer at Auckland University of Technology, New Zealand. Her expertise is in the intersect of design and business, with her research focused on design thinking, collaborative practices and sustainable design. [email protected]

Donna Cleveland

Donna Cleveland is an Associate Professor and the Deputy Dean of School, School of Communication and Design, Royal Melbourne Institute of Technology, Vietnam. Her research in the field of sustainable design, articulates fashion and textiles thinking and systems. Her practice is engaged with issues of materiality, making and resilience across areas of art, design and creative technology. [email protected]

References

- Ahsan, Mohammad F. 2020. Textile and Apparel Supply Chain during COVID 19: A Perspective from Bangladesh. University of Rhode Island, Kingston, U.S.A. https://digitalcommons.uri.edu/tmd_major_papers/10/.

- Atilgan, Turan, Morjon Haddad Derafshi, and Seher Kanat. 2011. “Analysis of Textile and Clothing Sector: Iran Case.” Journal of Textile & Apparel/Tekstil ve Konfeksiyon 21 (3): 280–284. https://avesis.ege.edu.tr/yayin/7d4f5cbf-8856-450d-a030-be19baae61e3/analysis-of-textile-and-clothing-sector-iran-case.

- Au, Kin-Fan, ed. 2011. Advances in Knitting Technology. Oxford, Cambridge, Philadelphia and New Delhi: Woodhead Publishing Series in Textiles: Number 89.

- Baker, Michael G., Amanda Kvalsvig, and Ayesha J. Verrall. 2020. “New Zealand’s COVID-19 Elimination Strategy.” The Medical Journal of Australia 213 (5): 198–200. doi:10.5694/mja2.50735.

- BDO NZ 2020. “Relief Packages for the Agribusiness Sector.” April 15. https://www.bdo.nz/en-nz/covid-19/agribusiness-relief-packages

- Berg, Achim, Lara Haug, Saskia Hedrich, and Karl-Hendrik Magnus. 2020. “Time for Change.” McKinsey & Company, Europe. http://dln.jaipuria.ac.in:8080/jspui/bitstream/123456789/11031/1/Time-for-change-How-to-use-the-crisis-to-make-fashion-sourcing-more-agile-and-sustainable.pdf.

- Berg, Achim, Saskia Hedrich, Patricio Ibanez, Sara Kappelmark, Karl-Hendrik Magnus, and Marie Seeger. 2019. “Fashion’s New Must-Have: Sustainable Sourcing at Scale.” McKinsey & Company, Europe. https://www.mckinsey.com/∼/media/mckinsey/industries/retail/our%20insights/fashions%20new%20must%20have%20sustainable%20sourcing%20at%20scale/fashions-new-must-have-sustainable-sourcing-at-scale-vf.ashx.

- Bezuidenhout, Carel N., Daniel Passos de Oliveira, Anthony Black, Teresa Murrell, Chelsea Dela Cruz, Bhavin Vaghela, Logan P. Kirk, Rahul Dilip Kathara, and Noah Sun. 2021. A Scholarly Review of Supply Chain Integration within the New Zealand Wool Industry. Operations and Engineering Innovation, Massey University, Manawatu Campus, Palmerston North, New Zealand. https://mro.massey.ac.nz/handle/10179/16790.

- Black, Sandy. 2012. Knitting: Fashion, Industry, Craft. London: V&A Publishing.

- Boudreau, Lara, and Farria Naeem. 2021. “The Economic Effects of COVID-19 on Ready-made Garment Factories in Bangladesh.” C-19 Note Private Enterprise Development in Low-Income Countries (PEDL), ERG 7849. https://pedl.cepr.org/publications/economic-effects-covid-19-ready-made-garment-factories-bangladesh

- Briggs, Phil, New Zealand Institute of Economic Research. 2003. and Looking at the Numbers: A View of New Zealand’s Economic History. NZ Institute of Economic Research. Wellington, New Zealand. https://nla.gov.au/nla.cat-vn1033647.

- Chakraborty, Samit, and Manik Chandra Biswas. 2020. “Impact of COVID-19 on the Textile, Apparel and Fashion Manufacturing Industry Supply Chain: Case Study on a Ready-Made Garment Manufacturing Industry.” SSRN Electronic Journal 3 (2): 181–199. doi:10.2139/ssrn.3762220.

- Colovic, Gordana. 2014. “The Garment Manufacturers Risk Assessment-Swot Analysis.” Journal of Textile Science & Engineering 04 (06): 1. doi:10.4172/2165-8064.1000173.

- Conforte, Daniel, Samuel Dunlop, and Elena Garnevska. 2011. “New Zealand Wool inside: A Discussion Case Study.” International Food and Agribusiness Management Review 14 (1030-2016-82797): 147–178. https://www.ifama.org/resources/Documents/v14i3/Case-Conforte-Dunlop-Garnevska.pdf.

- Cottle, David, and Errol Wood. 2012. “Overview of Early Stage Wool Processing.” The Australian Wool Education Trust Licensee for Educational Activities University of New England, 1–22. https://www.woolwise.com/wp-content/uploads/2017/07/WOOL-482-582-12-T-01.pdf

- Dalziel, Paul. 2016. “Spending in the Economy - Economic Reform from 1984.” Te Ara - the Encyclopedia of New Zealand. https://teara.govt.nz/en/spending-in-the-economy/page-3

- De Pont, Doris. 2018. “Manawatu Knitting Mills 1889-.” New Zealand Fashion Museum. https://nzfashionmuseum.org.nz/manawatu-knitting-mills/

- Du Plessis, Heather, and Allan Drive. 2020. “Covid-induced Delays Causing Massive Problems for the Supply Chain.” Newstalk ZB, November 20. https://www.newstalkzb.co.nz/on-air/heather-du-plessis-allan-drive/audio/chris-carr-covid-induced-delays-causing-massive-problems-for-the-supply-chain/

- Edmunds, Susan. 2021. “Covid Reality Bites: Business Closures Spike 130pc.” Stuff (Business) News, March 4. https://www.stuff.co.nz/business/300243922/covid-reality-bites-business-closures-spike-130pc

- Fairlie, Robert. 2020. “The Impact of COVID‐19 on Small Business Owners: Evidence from the First Three Months after Widespread Social‐Distancing Restrictions.” Journal of Economics & Management Strategy 29 (4): 727–740. doi:10.1111/jems.12400.

- Ghazinoory, Sepehr, Mansoureh Abdi, and Mandana Azadegan-Mehr. 2011. “SWOT Methodology: A State-of-the-Art Review for the Past, a Framework for the Future.” Journal of Business Economics and Management 12 (1): 24–48. doi:10.3846/16111699.2011.555358.

- Gopinath, Gita. 2020. “The Great Lockdown: Worst Economic Downturn Since the Great Depression.” IMF Blog, April 14. https://blogs.imf.org/2020/04/14/the-great-lockdown-worst-economic-downturn-since-the-great-depression/

- Görener, Ali., Kerem Toker, and Korkmaz Ulucay. 2012. “Application of Combined SWOT and AHP: A Case Study for a Manufacturing Firm.” Procedia - Social and Behavioral Sciences 58: 1525–1534. doi:10.1016/j.sbspro.2012.09.1139.

- Graham-McLay, Charlotte. 2020. New Zealand Launches Massive Spending Package to Combat COVID-19. The Guardian, International Edition, March 17. https://www.theguardian.com/world/2020/mar/17/new-zealand-launches-massive-spending-package-to-combat-covid-19

- Han, Hui-Hui, Li-Ying Mi, Tao Yang, and Xin Luo. 2017. “Research on Countermeasures for the Upgrade and Transformation of Garment Industry in China.” In 3rd Annual 2017 International Conference on Management Science and Engineering (MSE 2017), 29–33. Atlantis Press. doi:10.2991/mse-17.2017.8.

- Hill, Terry, and Roy Westbrook. 1997. “SWOT Analysis: It’s Time for a Product Recall.” Long Range Planning 30 (1): 46–52. doi:10.1016/S0024-6301(96)00095-7.

- ILO 2020. “COVID-19 and the Textiles, Clothing, Leather and Footwear Industries.” International Labour Organisation, Sectoral Brief on pandemic, April 8. https://www.ilo.org/wcmsp5/groups/public/–-ed_dialogue/–-sector/documents/briefingnote/wcms_741344.pdf

- Jennings, Mark. 2020. “Buy Local and Save the Economy.” Newsroom. June 30. https://www.newsroom.co.nz/buy-local-and-save-the-economy

- Jo, Myoung Rae, and Min Jung Lee. 2018. “A Study on Development Strategy of South Korea Textile Industry in Indonesia Using SWOT Analysis.” In Proceedings of the Korean Society of Computer Information Conference, 530–531. Korean Society of Computer Information. https://www.koreascience.kr/article/CFKO201831342441009.page.

- Kanat, Seher, Sadaf Aftab Abbasi, Mazhar Hussain Peerzada, and Turan Atilgan. 2018. “SWOT Analysis of Pakistan’s Textile and Clothing Industry.” Industria Textila 69 (06): 502–510. doi:10.35530/IT.069.06.1488.

- Khan, Jimad. 2020. “Woolyarns- Making it New Zealand” -Episode 56. April 28. YouTube. https://www.youtube.com/watch?v=K_P-Bgrg4A4

- Kim, Yong-Jeong, and Jaehun Park. 2019. “A Sustainable Development Strategy for the Uzbekistan Textile Industry: The Results of a SWOT-AHP Analysis.” Sustainability 11 (17): 4613. doi:10.3390/su11174613.

- Kissler, Stephen M., Christine Tedijanto, Edward Goldstein, Yonatan H. Grad, and Marc Lipsitch. 2020. “Projecting the Transmission Dynamics of SARS-CoV-2 through the Postpandemic Period.” Science (New York, N.Y.) 368 (6493): 860–868. doi:10.1126/science.abb5793.

- Lewis, Nick, Wendy Larner, and Richard Le Heron. 2008. “The New Zealand Designer Fashion Industry: Making Industries and co‐Constituting Political Projects.” Transactions of the Institute of British Geographers 33 (1): 42–59. https://www.jstor.org/stable/30131207?seq=1. doi:10.1111/j.1475-5661.2007.00274.x.

- Li, Si-Nuo, Y. Li, Ming-Liang Cao, and R. Padhye. 2016. “Current Status of the UK Textile Industry and Its Sustainable Development.” In Textile Bioengineering and Informatics Symposium Proceedings, 1. 756–764.

- Mahajan, Surabhi, and Sandeep Bains. 2020. “Impact of Lockdown Due to COVID-19 on Apparel and Knitwear Industries of Ludhiana.” Indian Journals- Journal of Community Mobilisation and Sustainable Development 15 (2): 347–351. doi:10.5958/2231-6736.2020.00009.

- Maliszewska, Maryla, Aaditya Mattoo, and Dominique Van Der Mensbrugghe. 2020. “The Potential Impact of COVID-19 on GDP and Trade: A Preliminary Assessment.” World Bank Policy Research Working Paper 9211, 1–24. http://hdl.handle.net/10986/33605.

- MBIE 2014. “The Small Business Sector Report.” Ministry of Business, Innovation, and Employment, New Zealand. https://www.mbie.govt.nz/dmsdocument/3951-small-business-sector-report-2014

- MBIE 2018a. “Beyond Commodities: Manufacturing into the Future.” Ministry of Business, Innovation, and Employment, New Zealand. https://www.mbie.govt.nz/dmsdocument/3938-beyond-commodities-manufacturing-into-the-future

- MBIE 2018b. “New Zealand’s Support for Small Business.” Ministry of Business, Innovation, and Employment, New Zealand. https://www.mbie.govt.nz/dmsdocument/2925-new-zealands-support-for-small-business-pdf

- MBIE 2020. “Manufacturing Fact Sheet: The Sector in the Lead up to COVID-19.” Ministry of Business, Innovation, and Employment, New Zealand. https://www.mbie.govt.nz/dmsdocument/11427-manufacturing-factsheet

- Mehta, Swati, and Manpreet Kaur. 2021. “COVID-19 and Ludhiana’s Woolen Knitwear Industry: Way Forward.” Research Journal of Textile and Apparel 25 (3): 209–225. doi:10.1108/RJTA-07-2020-0082.

- NZ Post. 2020. “Covid-19 has Forever Changed the Way Kiwis Shop.” NZ Post. Post & Parcel News, August 10. https://postandparcel.info/125073/news/new-research-from-nz-post-has-indicated-that-online-shopping-increased-105-when-new-zealand-moved-into-alert-level-3-as-a-result-of-the-covid-19-pandemic-and-the-experience-may-have-changed-t/

- OECD. 2020. “COVID-19 and Responsible Business Conduct.” policy responses to Coronavirus (COVID-19). https://www.oecd.org/coronavirus/policy-responses/covid-19-and-responsible-business-conduct-02150b06/

- Rahman, Md Mufidur. 2020. “Suggested Strategy for Bangladesh Garment Manufacturers and Exporters Association (BGMEA) during and Post Covid-19 to Protect the Industry from Massive Loss.” Global Journal of Management and Business Research 20 (9): 1–10. https://globaljournals.org/GJMBR_Volume20/5-Suggested-Strategy-for-Bangladesh.pdf

- Ramsay, Kathryn. 2013. “Exploring the Opportunities for Moving from Craft to Design with the Emergence of High Technologies in a New Zealand Context.” PhD diss., Auckland University of Technology. http://hdl.handle.net/10292/5557.

- RBA 2020. “COVID-19 Impact at a Glance.” Responsible Business Alliance Brief (19.3. 2020). https://www.responsiblebusiness.org/media/docs/COVID19Survey.pdf

- Roberts-Islam, Brooke. 2020. “The True Cost of Brands not Paying for Orders During the COVID-19 Crisis.” Forbes. March 30. https://www.forbes.com/sites/brookerobertsislam/2020/03/30/the-true-cost-of-brands-not-paying-for-orders-during-the-covid-19-crisis/?sh=2b99584f5ccc

- Sedex 2021. “The Impact of Covid-19 on Suppliers.” Sedex. https://www.sedex.com/wp-content/uploads/2021/01/Sedex-Impact-of-COVID-19-on-Supply-Chains-FINAL.pdf

- Smith, Amanda Elizabeth. 2013. “Seamless Knitwear: Singularities in Design.” PhD diss., Auckland University of Technology. http://hdl.handle.net/10292/5761.

- Smith, Amanda, and Angela Finn. 2015. “Built for Niche: Rethinking the Role of Manufacturing in Developing Designer Fashion in New Zealand.” International Journal of Fashion Studies 2 (1): 29–42. doi:10.1386/infs.2.1.29_1.

- Tearfund 2019. “The 2019 Ethical Fashion Report, the Truth Behind the Barcode.” https://www.tearfund.org.nz/getmedia/a3d9fc5f-54a1-46c1-b85f-c004da975620/FashionReport_2019_10-April-19_NZ.pdf.aspx

- The Treasury 2021. “WEU Special Topic-The Economic Impacts of Global Supply Chain Disruption.” New Zealand Government. https://www.treasury.govt.nz/publications/research-and-commentary/rangitaki-blog/weu-special-topic-economic-impacts-global-supply-chain-disruption

- Tuan, Luu Trong. 2012. “Development Strategy for a Textile Firm.” Journal of Management and Sustainability 2 (2): 136. doi:10.5539/jms.v2n2p136.

- Underwood, Jenny. 2009. “The Design of 3D Shape Knitted Preforms.” PhD diss., RMIT University. https://researchrepository.rmit.edu.au/esploro/outputs/9921861597201341.

- Walters, L. 2020. Why our ships haven’t come in. Newsroom report, December 23. https://www.newsroom.co.nz/why-our-ships-havent-come-in

- Wangsa, Patrick, and Rina Adi Kristianti. 2019. “Pengaruh Usaha Koordinasi, Integrasi Strategis, Orientasi Pasar, Dan Inovasi Produk Terhadap Kinerja Pemasaran Pada Toko Bombay Textile Indonesia.” Jurnal Manajemen Bisnis Dan Kewirausahaan 3 (2): 70–77. doi:10.24912/jmbk.v3i2.4962.

- Wickramasinghe, G. L. D, and N. Abdullah. 2011. Analysis of Strategic Factors for the Sri Lankan Textile and Apparel Industry.” University of Moratuwa, Sri Lanka. http://dl.lib.mrt.ac.lk/handle/123/8044.

- Withers, Tracy. 2021. “New Zealand Mulls Limiting Mass Tourism to Preserve Green Image.” Bloomberg News, March 19. https://www.bloomberg.com/news/articles/2021-03-18/new-zealand-considers-tourism-change-to-counter-negative-impacts

- WITS 2022. “New Zealand Jerseys, Pullovers, Cardigans, Waistcoats and Similar Articles; of Wool or Fine Animal Hair, Knitted or Crocheted Exports by Country in 2019.” World Integrated Trade Solution. https://wits.worldbank.org/trade/comtrade/en/country/NZL/year/2019/tradeflow/Exports/partner/ALL/product/611010

- Wulandari, Ni Luh Putu Tary, and Gede Sri Darma. 2020. “Textile Industry Issue in Pandemic of COVID-19.” PalArch’s Journal of Archaeology of Egypt/Egyptology 17 (7): 8064–8074. https://archives.palarch.nl/index.php/jae/article/view/3526.

- Xu, Zhitao, Adel Elomri, Laoucine Kerbache, and Abdelfatteh El Omri. 2020. “Impacts of COVID-19 on Global Supply Chains: Facts and Perspectives.” IEEE Engineering Management Review 48 (3): 153–166. doi:10.1109/EMR.2020.3018420.

- Ying, Yang. 2010. “SWOT-TOPSIS Integration Method for Strategic Decision.” In 2010 International Conference on E-Business and E-Government, pp. 1575–1578. doi.org/ doi:10.1109/ICEE.2010.399.

- Zhao, Li., and Kihyung Kim. 2021. “Responding to the COVID-19 Pandemic: Practices and Strategies of the Global Clothing and Textile Value Chain.” Clothing and Textiles Research Journal 39 (2): 157–172. doi:10.1177/0887302X21994207.