?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.Abstract

This study examined whether firms’ external financing demands affect the impression management of carbon information disclosure; we also considered the moderating role of media attention in this relationship. The sample consisted of firms in eight energy-intensive industries included in the State Council of China’s “Notice on the Pilot Work of Carbon Emission Trading.” The findings are as follows: (1) A positive correlation existed between external financing demand and the impression management of carbon information disclosure; that is, compared to firms without external financing demand, those with external financing demand had greater impression management of carbon information disclosure. (2) Media attention partially weakened the effect of external financing demand on the impression management of carbon information disclosure. These findings are shown to be robust. Further test indicated that, compared to state-owned enterprises (SOEs), the effect of external financing demand on the impression management of carbon information disclosure was more pronounced in non-SOEs. Our findings enrich the literature on carbon information disclosure. They also provide ideas for governments to formulate carbon information disclosure standards, for investors to effectively identify firm’s impression management of carbon information disclosure, and for firms to better carry out carbon management.

Introduction

Rapid economic development has been accompanied by dramatic global climate change, which, in turn, is imposing constraints on the scope of economic activity. From the Kyoto Protocol in 1997 to the Global Climate Conference in Copenhagen in 2009, and then to the UN Climate Change Conference in Madrid in December 2019, carbon emissions have become an issue of global concern. In 2011, the State Council of China issued the “Notice on Pilot Carbon Emission Trading,” proposing to gradually introduce a carbon emission trading market that includes eight energy-intensive industries: petrochemicals, chemicals, building materials, steel, nonferrous metal, paper, electric power, and aviation. China’s carbon emission trading market was first implemented in the electric power industry on December 19, 2017. On November 3, 2020, the Central Committee of the Communist Party of China issued the proposal for formulating the 14th Five-Year Plan for National Economic and Social Development and the Vision Target for 2035, which noted that China should promote the market-based trading of carbon emission rights and formulate an action plan for peaking carbon emissions by 2030.

With this emphasis on carbon emission reduction, the demand for carbon information in China’s capital market is unprecedentedly high. Yet, the carbon information disclosure level of Chinese firms remains relatively low [Citation1–3]. Further, this disclosure status quo is obviously not conducive to helping investors to make relevant decisions. In addition, given the lack of strict regulations on carbon information disclosure in China, as a form of nonfinancial disclosure, carbon disclosures tend to have problems such as qualitative description, a lack of quantitative information, and a lack of independent third-party examination. As such, carbon information disclosure in China may have strong operability, giving rise to the phenomenon of impression management in the disclosure of carbon information. Previous studies have found that the carbon information disclosed in corporate social responsibility (CSR) reports tends to have impression management characteristics [Citation4–7]. Impression management in voluntary disclosures may lower the quality of reports and lead to the improper allocation of funds [Citation8]. There is a need, therefore, to enhance research on the impression management of carbon information disclosure in China.

Impression management is a management behavior in which firms intentionally or unintentionally attempt to control the impressions of the main audience for information [Citation9, Citation10]. As a concept in the field of psychology, impression management has been used to analyze the characteristics of firms’ information quality in management [Citation11] and has been applied to CSR research over the last 20 years [Citation12–16]. Recent studies have found that firm performance [Citation2], firm governance [Citation17], and female directors [Citation18] can influence impression management behavior in CSR reports. Studying the economic consequences of impression management in CSR reports, Ji and Dong [Citation19] found that impression management in CSR reports had a significant negative effect on the cost of equity capital.

The abovementioned studies on the impression management of nonfinancial information disclosure only focused in general on CSR reports without specifically considering carbon information disclosure as a subdivision of information disclosure. Talbot and Boiral [Citation4] examined the impression management technologies of 10 large Canadian carbon-emitting firms, establishing the precedent for research on the impression management of carbon information disclosure. They found that firms tend to manipulate or conceal certain carbon information elements, selectively disclose information, and actively manage impressions, all of which affects the quality of disclosure. Talbot and Boiral [Citation5] subsequently studied impression management strategies in the sustainability reports of 21 energy firms. With the exception of Talbot and Boiral [Citation4, Citation5], in general, existing studies have not specifically considered the impression management of carbon information disclosure. There is still a lack of large-sample empirical research on the driving factors of the impression management of carbon information disclosure. To fill this gap, this study aimed to empirically investigate the impression management of carbon information disclosure in eight energy-intensive industries.

China has been implementing green financial policies since 2003. This has included a series of regulations, such as the “Green Credit Guide” (2012) and “Green Investment Guidelines (trial)” (2018). Such regulations tie the financing of firms to their environmental performance; in this regard, the financing behavior of energy-intensive industries is even more constrained by environmental protection. Under such constraints, firms may win the favor of investors by taking concrete steps to reduce carbon emissions; alternatively, they may adopt impression management measures when disclosing carbon information to create a false impression of proenvironmental behavior. In light of this, the present study examined whether the external financing demands of eight energy-intensive industries affect the impression management of carbon information disclosure. We found that compared to firms without external financing demand, those with external financing demand were more inclined to “package” their carbon performance—that is, they were more inclined to conduct impression management in carbon information disclosure. Moreover, media attention had a significant negative moderating effect in the relationship between external financing demand and the impression management of carbon information disclosure. These findings can help promote the development of green financial policies in China while providing empirical evidence for standardizing carbon information disclosure.

This research makes several contributions. First, we established a measurement index system for the impression management of carbon information disclosure. Referring to the greenwashing measurement index system of Huang et al. [Citation20], the Global Reporting Initiative (GRI) on the quality requirements of nonfinancial reporting and the characteristics of carbon information disclosure, we constructed a measurement index system for the impression management of carbon information disclosure. This index system can directly measure the impression management degree of carbon information disclosure, which overcomes the deficiencies of indirect agency based on the residual value of the influencing factor model constructed by Huang and Yao [Citation2] and Zhang and Qiu [Citation17]. Further, it can more intuitively reflect the impression management performance of firms.

Second, we empirically study the impression management of carbon information disclosure. This study is the first to investigate the relationship between external financing demand and the impression management of carbon information disclosure. This expands research on the driving factors of impression management in nonfinancial information disclosure and enriches the literature on carbon information disclosure by combining national macrofinancial policy with microlevel firm behavior.

Finally, we examine the supervision and governance functions of media attention. Although external financing demand has a driving effect on the impression management behavior of carbon information disclosure, media attention, as an external supervision mechanism, can effectively regulate the relationship between them. This provides empirical evidence for the identification and governance of the impression management behavior of carbon information disclosure.

Literature review and hypothesis development

External financing demand and the impression management of carbon information disclosure

External financing demand refers to the need for firms to raise funds from the capital market through financial activities. China has implemented green financial policies. The “Implementation Report of China’s Monetary Policy (the Fourth Quarter of 2017),” released by the People’s Bank of China in 2018, includes green financing in macroprudential assessment, which accelerated the implementation of the green credit policy. On October 21, 2020, the General Office of the Ministry of Ecology and Environment issued the “Guidance on Promoting Investment and Financing for Addressing Climate Change.” According to the guideline, to achieve emission reduction targets, more funds need to be allocated for investment and financing in the domain of climate change, and eligible climate-friendly firms need to receive financing support through the capital market. Such regulations tie the carbon emission reduction performance of energy-intensive firms to their financing. Arguing that carbon credit is the future development trend of green credit, Gao [Citation21] proposed the concept of carbon credit based on the green credit system of commercial banks, linking low carbon with credit. Faced with increasingly stringent green credit regulations, if energy-intensive firms do not meet the requirements, their external financing can be limited to some extent. For example, in September 2017, Shanghai Securities News reported that Shangfeng Cement’s refinancing had been hampered by environmental concerns. As regulatory authorities pay increasing attention to environmental protection issues, firms’ financing is correspondingly affected by environmental performance. Although China’s emission trading system (ETS) has only been implemented in the electric power industry and not the other seven energy-intensive industries, carbon emission reduction performance undoubtedly places financial pressure on firms.

Capital is indispensable for firms’ development. If a firm cannot get timely financial support when it has external financing demand, it will have significant negative effects on operations and development. Therefore, the greater the external financing demand, the stronger the possible motivation for impression management. Sun [Citation10] noted that competition for scarce resources is a major motivator for firms to disclose information. CSR performance reflects firms’ contribution to society, which can enhance their competitiveness with regard to investment [Citation22, Citation23], loans [Citation24], and other scarce resources. Kleimeier and Viehs [Citation25] noted that firms that voluntarily disclose carbon emission information enjoy more favorable lending conditions than their nondisclosing counterparts. High-quality carbon disclosure can reduce the cost of debt financing by reducing the risk of default [Citation26]. From the creditor’s point of view, environmental violation will lead to more penalties or fines. Thus, when a firm relies on external funds, creditor supervision requires the firm to disclose more information [Citation27]. Therefore, in some respects, external financial investors hold a positive attitude toward high-quality carbon disclosure.

Under China’s strict environmental credit policy, the pressure for environmental legitimacy makes firms more likely to disclose carbon information [Citation28]. However, under the theoretical legitimacy framework, there is a negative relationship between carbon performance and carbon disclosure [Citation6]. A high carbon disclosure score might not necessarily reflect a firm’s underlying carbon-reduction performance [Citation7]. Indeed, some firms opt for evasive or symbolic disclosure when choosing a carbon disclosure strategy [Citation29, Citation30]. In this regard, firms may adopt impression management strategies in carbon disclosure to establish a good reputation and cater to investors to obtain financing.

According to information asymmetry theory, it is difficult for most stakeholders to have a direct understanding of the actual environmental performance and efforts of firms in their production processes [Citation31]. Firms’ carbon performance can only be measured by the carbon information they disclosed. That is, in the process of disclosure, there may be differences between the information firms provide and the information stakeholders need. Such asymmetry provides a space for firms to manage impressions of their carbon information disclosure. Studying the correlation between financing demand and CSR information disclosure, Zhai [Citation32] found a significant positive correlation between external financing demand and CSR information disclosure. With the depth study of information disclosure, Meng et al. [Citation33] noted that when judging the level of corporate disclosure, firms should consider whether to adopt a strategy of “substantive disclosure” or “symbolic disclosure.” Therefore, research on the relationship between external financing demand and environmental information disclosure can be extended to include external financing demand and the impression management of information disclosure.

According to signal transmission theory, to meet external financing demand, firms may adopt impression management strategies in their carbon information disclosure to present an environmentally friendly image to stakeholders. On the one hand, this can reduce the cost of regulatory violations caused by poor environmental performance; on the other hand, it can make it easier to obtain funding from financial institutions. Faced with the dilemma between legal threats and cost increases brought about by stringent green credit regulations, firms often respond symbolically to external pressure [Citation34] to obtain financial support. At the same time, since China’s carbon information disclosure standards remain imperfect, impression management is considered the most effective way to achieve financing objectives without modifying economic activities. Huang et al. [Citation20] found that, compared to firms without financing demand, firms with external financing demand showed a higher degree of greenwashing. Li and Guan [Citation35] noted that firms’ carbon emission reduction activities are conducive to obtaining bank loans; however, given the costs associated with reducing emissions, carbon emission reduction activities will reduce firms’ market value. So, for energy-intensive industries with external financing demand, rather than invest a lot of time, money, and resources in carbon emission reduction, they may be more inclined to selectively disclose information to investors to meet regulatory requirements and access financing. Thus, the first hypothesis is proposed:

H1: External financing demand is positively correlated with the impression management degree of carbon information disclosure.

Moderating role of media attention

Previous studies have mainly focused on the supervision and governance function of media reports. With regard to information, media can collect information to reduce information asymmetry [Citation36] and restrain management misconduct [Citation37]. Regarding financial reports, media not only effectively identify accounting fraud by firms [Citation38] but also provide risk warnings to auditors. The synergistic governance of media attention and independent auditing can significantly improve the transparency of accounting information [Citation39]. Qi et al. [Citation40] found that media reports played a positive role in the governance of earnings manipulation, which harms stakeholders’ interests. Similarly, for nonfinancial disclosures, media attention also plays a role of supervision and governance, making the environmental performance of firms more transparent and enabling stakeholders to obtain more facts beyond corporate reports. Chen et al. [Citation41] suggested that the more media attention a firm receives, the more likely it is that earnings manipulation will give rise to public alarm. On the one hand, when carbon emission reduction performance fails to meet requirements, if the firm creates a false impression of emission reduction through impression management, media supervision may cause impression management to fail. On the other hand, if media report that a firm had environmental violations, if the firm still adopts impression management, the likelihood of being “exposed” increases, which will affect the firm’s reputation. Therefore, the greater the media attention, the higher the risk and cost of impression management.

Given the existence of information asymmetry between firms and stakeholders, when firms adopt impression management, financial institutions and investors cannot judge the accuracy of the disclosed content. Since investors cannot grasp the true emission reduction performance of firms, they passively accept the information disclosed by firms and make investment decisions accordingly. However, media may help investors learn about a firm’s true environmental performance so they can make more informed investment decisions. Therefore, when firms have external financing demand, due to media supervision, they will be more cautious in their carbon information disclosure and reduce obvious impression management behaviors to avoid attracting regulatory attention and creating a dishonest impression. Thus, Hypothesis 2 is proposed:

H2: Compared to firms with low media attention, the effect of external financing demand on the impression management of carbon information disclosure is weaker for firms with high media attention.

Research design

Sample and data

In 2011, the State Council issued the “Notice on the Pilot Work of Carbon Emission Trading.” This proposed gradually promoting the carbon emission trading market, which would eventually include the eight major energy-intensive industries. Given the relatively mature conditions of the electric power industry, the national carbon ETS was first implemented in the electric power industry on December 19, 2017; the other seven industries will be gradually included. For the research sample, this study selected firms from the eight major energy-intensive industries that provided CSR reports from 2015 to 2018. Samples with missing key variables and ST (special treatment) firms were eliminated, and 522 effective samples were finally obtained. shows the distribution of the samples. To avoid interference from extreme values, all continuous variables were winsorized by 1%. We manually collected and calculated the impression management data of carbon information disclosure by reading the environmental performance content of the CSR reports. The CSR reports were downloaded from cninfo.com. Financial status and other firm governance data all came from the China Stock Market & Accounting Research Database (CSMAR). Data processing was performed using Stata 14.0.

Table 1. Sample distribution after elimination.

Variable definition

Impression management of carbon information disclosure (C_imp)

There is no unified measurement standard for the degree of the impression management of carbon information disclosure. Huang et al. [Citation20] proposed that impression management and greenwashing are two aspects of the same problem in environmental information disclosure and have a mutual cause–effect relationship. Likewise, we hold that greenwashing and the impression management of environmental information disclosure are different expressions with the same meaning and can be considered quantitatively equal. Therefore, we constructed a measurement index system for the impression management of carbon information disclosure from the five aspects of balance, comparability, accuracy, reliability, and integrity, referring to the greenwashing measurement index system constructed by Huang et al. [Citation20], the Global Reporting Initiative (GRI) on the quality requirements for nonfinancial reporting, the Carbon Disclosure Project (CDP), and carbon information content [Citation3, Citation42]. The specific disclosure items relatively completely contain the carbon information that firms should disclose in an ideal state. See for details.

Table 2. Measurement index system for the impression management of carbon information disclosure.

In the process of carbon information disclosure, firms have many ways to describe their performance. We carefully read the environmental disclosure portions of the CSR reports of the sample firms to judge whether the disclosure was for its own sake or referred to real action. That is, there are two types of corporate disclosure: symbolic disclosure and substantive disclosure. If a firm uses simple descriptions, general summaries, easy-to-imitate content, or difficult-to-verify content, then reliability is low, and it is considered a symbolic disclosure. The following is an example of symbolic content:

In recent years of construction and development, [we have] constantly increased investment in energy conservation and environmental protection.… The firm’s energy conservation and emission reduction effects are obvious.… Environmental emission targets continue to improve.… [We continue] to realize the unification of economic benefits, environmental benefits, and social benefits.

Meanwhile, if a firm discloses more verifiable information, such as factual statements, case descriptions, or quantitative descriptions, then its carbon information disclosure is considered substantive [Citation43–45]. The following is an example:

Through efficient use of water resources, clean hydropower generates 19.09 billion kilowatt-hours of electricity, which is equivalent to saving 60,894,200 tons of standard coal and reducing 156,315,500 tons of carbon dioxide, which is equivalent to planting 428,300 hectares of hardwood forests.… Every 100 million kWh of clean hydropower will save 31,900 tons of standard coal, equivalent to 81,900 tons of carbon dioxide emissions.… The economic benefit is about 50 million yuan.

In the process of obtaining impression management data, two raters read the information disclosed by firms using the content analysis method, and a third party reconciled any differences between them. If a firm disclosed an item, we judged whether it was symbolic or substantive. In the case of a symbolic disclosure, the value of symbolic disclosure is 1, and the value of substantive disclosure is 0. In the case of a substantive disclosure, the symbolic disclosure value is 0, and the substantive disclosure value is 1. If the item is not disclosed, both values are 0.

As mentioned previously, impression management and greenwashing have the same meaning. Therefore, we referred to the measurement method for greenwashing in Huang et al. [Citation20] to measure the degree of the impression management of carbon information disclosure from the two aspects of selective disclosure and expressive manipulation. Selective disclosure means a firm might not reveal specific information about its emission reduction performance if it has failed to meet requirements. Expressive manipulation is a symbolic disclosure that uses simple qualitative description. This study measured the degree of selective disclosure by the ratio of undisclosed items to the total number of disclosed items (12); expressive manipulation was measured by the ratio of symbolically disclosed items to the total number of disclosed items:

Finally, the degree of the impression management of carbon information disclosure (C_imp) was obtained through geometric averaging:

(1)

(1)

External financing demand (EFD)

Following Demirgüç-Kunt and Maksimovic [Citation46], Durnev and Kim [Citation47], Lu and Zhang [Citation48], Huang et al. [Citation20], and Yang and Guo [Citation49], this study reflected external financing demand based on the difference between firm growth and the endogenous growth firms can achieve. The specific formula is as follows:

(2)

(2)

where SIZE represents asset size and RETURN is return on equity. On this basis, EFD, which is greater than the annual industry average, is valued at 1; otherwise, it is 0.

Media attention (MEDIA)

There are two main ways to measure media attention. The first is to measure media attention by the number of reports in newspaper media, Internet media, and social media [Citation50]. The second is to measure the number of reports on firms from multiple representative newspapers in the Full-Text Database of Major Chinese Newspapers on cn.com [Citation51]. Given the excessive amount of news on Baidu search and other websites, most of it is repeated or reproduced news, with less authority than newspapers, as well as the possibility of “Internet Water Army” involvement. Thus, referring to Luo et al. [Citation51], we selected the second measurement method. Specifically, we chose eight authoritative, representative newspapers from the full-text database of major Chinese newspapers: Economic Observer, Securities Times, Shanghai Securities News, Securities Daily, China Business News, twenty first Century Business Herald, First Financial Daily, and China Securities Journal. The full names of the sample firms were searched, and reports related to those firms were selected and read in detail. When the name of the sample firm appeared throughout the whole report, the report was included in the total number of reports for the sample company; the total number of media reports for the sample firms was thus finally counted.

Control variables

Referring to Zhang and Qiu [Citation17], Huang et al. [Citation20], and Luo et al. [Citation51], we selected return on assets (ROA), asset-liability ratio (LEV), growth ability (GROW), firm scale (SIZE), first big shareholder stake (SHARE), market-to-book (MTB) value, executive compensation (PAY), and management shareholding (ExcuHldRt) as control variables. presents the specific variable definitions.

Table 3. Variable definitions.

Model construction

To test the influence of external financing demand on the impression management of carbon information disclosure (H1), the following model was established:

(3)

(3)

The explained variable (C_imp) is the degree of the impression management of carbon information disclosure, and the key explanatory variable (EFD) is firms’ external financing demand. According to the theoretical analysis (H1), if external financing demand stimulates management to undertake the impression management of carbon information disclosure, the coefficient of EFD in model (3) is expected to be significantly positive. That is, when a firm has external financing demand, it is motivated to undertake the impression management of carbon information disclosure.

To test the moderating effect of media attention on the relationship between external financing demand and the impression management of carbon information disclosure (H2), based on model (3), model (4) was established:

(4)

(4)

where MEDIA is media attention, and EFD*MEDIA is the cross multiplication of the two. According to our theoretical analysis (H2), media, as an external supervision mechanism, can inhibit the impression management of carbon information disclosure to meet external financing demand. Therefore, the coefficient of EFD*MEDIA is expected to be significantly negative.

Empirical results

Descriptive statistics

reports the descriptive statistics of the variables. The mean value of the impression management of carbon information disclosure (C_imp) is 60.293, indicating that the impression management of carbon information disclosure exists, its degree is relatively large, and the differences between firms are also relatively large (standard deviation: 30.754). The mean EFD value is 0.337, indicating that one-third of the firms had external financing demand. The mean value and standard deviation of MEDIA are 0.747 and 0.747, respectively, indicating that different firms received different media attention. The mean value of property right (STATE) is 0.693, indicating that non-SOEs (state-owned enterprises) accounted for about one-third of the sample. In addition, there are large differences among the samples in terms of ROA, LEV, and SHARE.

Table 4. Descriptive statistical analysis of variables.

Regression results

shows the multiple regression results for external financing demand on the impression management of carbon information disclosure. To test H1, regression analysis was conducted on model (3); the regression results are shown in column (1) of . The F-value of model (3) is 6.73, which is significant at the 1% level, indicating that the model is relatively stable. The EFD regression coefficient is 8.676 and significant at the 1% level. In addition, PAY, SHARE and ExcuHldRt, and ROA and MTB are significantly correlated with the impression management of carbon information disclosure at 10%, 5%, and 1%, respectively. This indicates that the above variables have a certain degree of influence on the impression management of carbon information disclosure among firms. In conclusion, the regression results of model (3) show that there is a significant positive correlation between external financing demand and the impression management of carbon information disclosure. That is, when firms have external financing demand, they have a stronger incentive to undertake the impression management of carbon information disclosure. This is consistent with the theoretical expectation of H1.

Table 5. Multiple regression results.

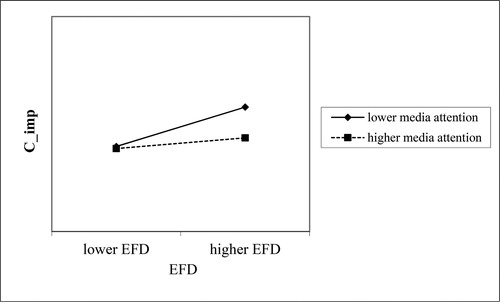

According to the above theoretical analysis, media increasingly play the role of external supervision, which can reduce information asymmetry between investors and firms, thus inhibiting opportunistic behavior by management. Therefore, according to H2, it is expected that a higher level of media attention will restrain the impression management of carbon information disclosure due to external financing demand. To test this hypothesis, model (4) was estimated, where the primary concern is the regression coefficient of EFD*MEDIA. Column (2) in shows the regression results. The F-value of this model is 6.77 and significant at 1%, indicating that the model is relatively stable. EFD*MEDIA has a regression coefficient of −7.633 and is significant at the 5% level. In addition, SHARE and PAY, ExcuHldRt, and ROA and MTB are significantly correlated with the impression management of carbon information disclosure at 10%, 5%, and 1%, respectively. In summary, the regression results of model (4) show that media attention has a significant negative moderating effect on the relationship between external financing demand and the impression management of carbon information disclosure. This is consistent with H2. For clarity, graphically illustrates the moderating effect of media attention (MEDIA) between external financing demand (EFD) and the impression management of carbon information disclosure (C_imp). It can be seen in the figure that, compared to firms with high media attention, the positive effect of external financing demand on the impression management of carbon information disclosure is stronger among firms with low media attention, which further supports H2.

Figure 1. Moderating effect of media attention.

Robustness test

To verify the reliability of the conclusions, robustness tests were conducted as described below.

(1) Logit model test. In the main test, the impression management of carbon information disclosure (C_imp) is a continuous variable, and the above regression is carried out using the least-squares model. For the robustness test, we redefined the explained variable RC_imp. It has a value of 1 if the degree of impression management of carbon information disclosure is greater than the industry average; otherwise, 0. A logit model with discrete dependent variables was established for the whole sample, and the test of model (3) was carried out again. Column (1) in shows the regression results. The EFD regression coefficient of the key explanatory variable, external financing demand (EFD), is 0.395 and significant at 10%, which is consistent with the OLS regression results.

Table 6. Regression results of robustness tests (1) and (2).

(2) Inspection of chemical and nonferrous metal industries. Firms in the chemical and nonferrous metal industries were selected as samples to test the robustness of model (3). There were 258 firms in total, accounting for about half of the total sample. Column (2) in shows the regression results. The EFD regression coefficient of the key explanatory variable, external financing demand (EFD), is 8.382 and significantly positive at the 5% level. This verifies the robustness of the empirical results.

(3) Replace the measurement of external financing demand. Firms’ financing behaviors include the issuance of stocks and bonds and the allotment of stocks. Referring to Song et al. [Citation52] and Li et al. [Citation53], we measured external financing demand by the issuance of stocks and bonds and the allotment of stocks. If a firm issues additional stocks or bonds or allots stocks during a given year, it is considered that the firm has external financing demand when it makes carbon information disclosures during the same year; otherwise, the firm has no intention of financing. EFD takes a value of 1 if there is financing behavior; otherwise, 0. At the same time, we changed the measurement method for some control variables. Referring to Huang and Yao [Citation2] and Zhang and Qiu [Citation17], we substituted CEO shareholding rate (CEOhave) for managerial shareholding (ExcuHldRt). shows the regression results. As shown in column (1), the EFD regression coefficient of the key explanatory variable, external financing demand (EFD), is 5.023 and significant at the 10% level. As shown in column (2), EFD*MEDIA has a regression coefficient of −6.296 and is significant at the 10% level, which verifies the robustness of our empirical results.

Table 7. Regression results of robustness test (3).

Further test

In China, SOEs can more easily obtain government subsidies or bank loans through government intervention than non-SOEs. Therefore, SOEs are relatively less worried about raising funds than non-SOEs. Li et al. [Citation54] found that in the negative relationship between corporate carbon information disclosure quality and bond financing costs, nonpublic firms are significantly stronger than public firms. Zhou et al. [Citation55] also found that carbon risk had a more significant effect on debt financing for private firms than for SOEs. Zhai [Citation32] concluded that compared to listed non-SOE firms, listed SOEs had weaker motivation to deal with external financing by disclosing social responsibility information. SOEs have a wider range of sources of capital than non-SOEs and have a closer relationship with the government. When SOEs have external financing demand, most do not need to worry about the source of funds; thus, they do not have strong motivation to obtain financing through the impression management of carbon information disclosure. Since non-SOEs lack government backing, banks are more cautious when granting loans and will pay more attention to carbon performance. Therefore, non-SOEs have a stronger motivation to undertake the impression management of carbon information disclosure to meet financing demand.

To test the difference between SOEs and non-SOEs in the relationship between external financing demand and the impression management of carbon information disclosure, we divided the whole sample into two subsamples: SOEs (STATE = 1) and non-SOEs (STATE = 0). They were tested based on model (3). shows the results.

Table 8. Regression results of SOEs and non-SOEs.

Columns (1) and (2) in list the regression results for the subsamples of SOEs and non-SOEs, respectively. For SOEs (STATE = 1), the EFD coefficient is still positive but not significant. For non-SOEs (STATE = 0), the EFD coefficient is 14.721 and significantly positive at 1%. These results indicate that the relationship between external financing demand and the impression management of carbon information disclosure is different between SOEs and non-SOEs.

Discussion and conclusion

Taking firms in eight energy-intensive industries from 2015 to 2018 as samples, this study examined the effect of external financing demand on the impression management of carbon information disclosure, as well as the moderating effect of media attention. The results showed that firms’ external financing demand was positively correlated with the impression management degree of carbon information disclosure. The results also showed that, compared to firms with low media attention, the effect of external financing demand on the impression management of carbon information disclosure was weaker among firms with high media attention. In other words, media attention can effectively constrain the positive relationship between firms’ external financing demand and the impression management of carbon information disclosure. Further test showed that the relationship between external financing demand and the impression management of carbon information disclosure was different under different property rights. The positive correlation between the external financing demand of non-SOEs and the impression management of carbon information disclosure was more significant.

Our findings have two academic implications. First, the impression management index system for carbon information disclosure provides a meaningful academic experiment to identify the impression management of carbon information disclosure. This has great significance for the identification of the impression management of carbon information. It introduces the theory of impression management from psychology into carbon information disclosure and identifies the problems existing in corporate carbon information disclosure. Also, our measurement index system can enrich research in the field of environmental accounting, promote research methods for investigating the impression management of carbon information disclosure, and provide theoretical significance for related research.

Second, this study contributes to the literature on the impression management of carbon information disclosure. Unlike the case studies of Talbot and Boiral [Citation4, Citation5], we conducted large-sample empirical research on the driving factors of the impression management of carbon information disclosure among China’s energy-intensive industries, which enriched the research on impression management of carbon information disclosure.

Our findings have positive practical implications for governments, investors, and firms. First, this study can help government departments to better understand the motives underlying firms’ impression management behaviors and provide a decision-making reference for promoting green corporate carbon management practices. Faced with regulatory requirements, energy-intensive industries with external financing demand will tend to greenwash their carbon performance. Debt financing obtained through impression management is a distortion of green policy; it is not conducive to the rational allocation of credit resources and can even negatively affect the carbon management of the whole society. Thus, it is necessary for governments to formulate standards to improve the quality of carbon information disclosure and reduce information asymmetry to meet the demand for “real” carbon information. This study also found that media regulation is conducive to improving the transparency and reliability of environmental information disclosure. The supervision and governance function of media attention provides empirical evidence for a multicentered governance model of the impression management of carbon information disclosure.

Second, it is noted that in the context of stricter green credit, investors need to strengthen their ability to identify impression management behavior in carbon information disclosure. We found that energy-intensive industries with huge external financing demand will adopt impression management strategies to greenwash their carbon performance. This study suggests that investors should pay more attention to the performance of our 12 index items when judging the true carbon performance of a firm. Investors should also evaluate whether a firm adopts an impression management strategy based on symbolic disclosure or expressive manipulation. In this way, investors will be better equipped to invest in firms with authentic carbon emission reduction performance. This can also provide a reference for investment in green projects to promote the further development of China’s green financial policies.

Third, we found that the higher the emission reduction performance of a firm, the more easily it will obtain financing. Thus, with higher levels of carbon information disclosure, the environmental risks posed by information opacity can be further reduced. In the context of increasingly strict environmental regulations, firms genuinely committed to environmental protection are more popular in the market. Therefore, the impression management of carbon information disclosure is only a short-term rather than long-term strategy. Thus, firms with a sustainable development philosophy should invest in “truly green” activities and thereby strengthen their carbon performance through real action.

This study nevertheless has some limitations. First, our impression management index system was constructed based on content analysis. Although content analysis has been widely used in carbon information disclosure research, it is still vulnerable to researcher subjectivity, among other shortcomings, which will affect the reliability of the index. Specifically, in this study, the classification of carbon information disclosed by sample firms was easily affected by subjective factors. Future studies can therefore improve the quantification of impression management and establish a more reliable measurement method. Second, the samples selected for this study came from eight energy-intensive industries, with a total sample size of 522. Since energy-intensive industries comprise a special class of industry, future research should examine whether our conclusions regarding the impression management of carbon disclosure are applicable to other types of industries.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- Jiang Y. Analysis on the construction of carbon information disclosure quality evaluation system—a case study of heavy pollution Industry. Commun Financ Account. 2019;(10):22–26.

- Huang YX, Yao Z. Corporate social responsibility report, impression management and corporate performance. Econ Manage. 2016;38(01):105–115.

- Chen H, Wang HY. Definition, measuring methods and status of carbon information disclosure in Chinese enterprises. Ecol Econ. 2015;11(4):393–400.

- Talbot D, Boiral O. Strategies for climate change and impression management: a case study among Canada’s large industrial emitters. J Bus Ethics. 2015;132(2):329–346. doi:10.1007/s10551-014-2322-5.

- Talbot D, Boiral O. GHG reporting and impression management: an assessment of sustainability reports from the energy sector. J Bus Ethics. 2018;147(2):367–383. doi:10.1007/s10551-015-2979-4.

- Luo L. The influence of institutional contexts on the relationship between voluntary carbon disclosure and carbon emission performance. Account Finance. 2019; 59(2):1235–1264. doi:10.1111/acfi.12267.

- Guo T, Zha G, Lee CL, et al. Does corporate green ranking reflect carbon-mitigation performance? J Cleaner Prod. 2020;277:1–13. https://doi.org/10.1016/j.jclepro.2020.123601

- Leung S, Parker L, Courtis J. Impression management through minimal narrative disclosure in annual reports. Br account Rev. 2015;47(3):275–289. doi:10.1016/j.bar.2015.04.002.

- Leary MR, Kowalski RM. Impression management: a literature and two component model. Psychol Bull. 1990;107(1):34–37. doi:10.1037/0033-2909.107.1.34.

- Sun ML. On impression management behavior in information disclosure of listed companies. Account Res. 2004;(03):40–45.

- Geely Feng LH, Wang HH. Influence of organizational impression management on quality characteristics of CSR report. Friends Account. 2010;(07):19–21.

- Kim MS, Kim DT, Kim JI. CSR for sustainable development: CSR beneficiary positioning and impression management motivation. Corp Soc Responsib Environ Mgmt. 2014; 21(1):14–27. doi:10.1002/csr.1300.

- Tata J, Prasad S. CSR communication: an impression management perspective. J Bus Ethics. 2015; 132(4):765–778. doi:10.1007/s10551-014-2328-z.

- Abernathy J, Stefaniak C, Wilkins A, et al. Literature review and research opportunities on credibility of corporate social responsibility reporting. AJB. 2017; 32(1):24–41. doi:10.1108/AJB-04-2016-0013.

- Diouf D, Boiral O. The quality of sustainability reports and impression management: a stakeholder perspective. AAAJ. 2017; 30(3):643–667. doi:10.1108/AAAJ-04-2015-2044.

- Lourenço IC, Oliveira J, Branco MC, et al. Are CSR leaders less prone to engage in impression management? XVIC, ongresso Internacional de Contabilidade e Auditoria. Ordem dos Contabilistas Certificados. 2017.

- Zhang ZY, Qiu JT. Accounting conservatism, corporate governance and social responsibility report impression management. Financ Theory Pract. 2017; 38(03):77–83.

- García-Sánchez IM, Suárez-Fernández O, Martínez-Ferrero J. Female directors and impression management in sustainability reporting. Int Bus Rev. 2019; 28(2):359–374. doi:10.1016/j.ibusrev.2018.10.007.

- Ji ML, Dong BY. The influence of impression management on equity capital cost in social responsibility report – based on the moderating effect of accounting conservatism. Financ Account Mon. 2019;(16):160–168.

- Huang RB, Chen W, Wang KH. External financing demand, impression management and enterprise greenwashing. Comp Econ Soc Syst. 2019;(03):81–93.

- Gao G. The new trend of green credit: the past life of carbon credit. Environ Protection. 2010;22:27–29.

- Dhaliwal DS, Li OZ, Tsang A, et al. Voluntary nonfinancial disclosure and the cost of equity capital: the initiations of corporate social responsibility reporting. Account Rev. 2011;86(1):59–100. doi:10.2308/accr.00000005.

- Ghoul S, Guedhami O, Kwok CCY, et al. Does corporate social responsibility affect the cost of capital? J Bank Financ. 2011; 35(9):2388–2406. doi:10.1016/j.jbankfin.2011.02.007.

- Goss A, Roberts G. The impact of corporate social responsibility on the cost of bank loan. J Bank Financ. 2011; 35(7):1794–1810. doi:10.1016/j.jbankfin.2010.12.002.

- Kleimeier S, Viehs M. Carbon disclosure, emission levels, and the cost of debt. SSRN Electron J. 2018. doi:10.2139/ssrn.2719665.

- Yang J, Zhang M, Liu YC. How does carbon information disclosure affect debt financing cost – a study on intermediation effect based on debt default risk? J Beijing Inst Technol. 2020;22(04):28–38.

- Shen H, Zheng S, Adams J, et al. The effect stakeholders have on voluntary carbon disclosure within Chinese business organizations. Carbon Manage. 2020; 11(5):455–472. doi:10.1080/17583004.2020.1805555.

- Mei XH, Ge Y, Zhu XN. Research on the influence mechanism of environmental legitimacy pressure on corporate Carbon information disclosure. Soft Sci. 2020;34(08):78–83.

- Hrasky S. Carbon footprints and legitimation strategies: symbolism or action? Acc Audit Account J. 2011; 25(1):174–198. doi:10.1108/09513571211191798.

- Herold DM, Lee KH. The influence of internal and external pressures on carbon management practices and disclosure strategies. Australas J Environ Manag. 2019; 26(1):63–81. doi:10.1080/14486563.2018.1522604.

- Lyon TP, Maxwell JW. Greenwash: corporate environmental disclosure under threat of audit. J Econ Manage Strategy. 2011; 20(1):3–41. doi:10.1111/j.1530-9134.2010.00282.x.

- Zhai HY. Influence of external financing demand on corporate Social Responsibility Disclosure under soft budget constraints. China Popul Resour Env. 2010; 20(09):107–113.

- Meng X, Zeng S, Xie X, et al. Beyond symbolic and substantive: strategic disclosure of corporate environmental information in China. Bus Strat Env. 2019; 28(2):403–417. doi:10.1002/bse.2257.

- Marquis C, Toffel MW, Zhou Y. Scrutiny, norms, and selective disclosure: a global study of greenwashing. Organ Sci. 2016; 27(2):483–504. doi:10.1287/orsc.2015.1039.

- Li Z, Guan F. Research on the economic consequences of carbon emission reduction by Chinese enterprises. J Zhongnan Univ Econ Law. 2015;(03):11–18.

- Fang L, Peress J. Media coverage and the cross-section of stock returns. J Financ. 2009;64(5):2023–2052. doi:10.1111/j.1540-6261.2009.01493.x.

- Dyck AN, Volchkova L, Zingales L. The corporate governance role of the media: evidence from Russia. J Financ. 2008;63(3):1093–1135. doi:10.1111/j.1540-6261.2008.01353.x.

- Miller GS. The press as a watchdog for accounting fraud. J Account Res. 2006; 44(5):1001–1033. doi:10.1111/j.1475-679X.2006.00224.x.

- Li XH, Yang K. Research on media attention, audit opinion and accounting information transparency. J Cent Univ Financ Econ. 2015;(10):52–60.

- Qi B, Yang R, Tian G. Can media deter management from manipulating earnings? Evidence from China. Rev Quant Finan Acc. 2014; 42(3):571–597. doi:10.1007/s11156-013-0353-0.

- Chen Y, Cheng CA, Li S, et al. The monitoring role of the media: evidence from earnings management. J Bus Finan Account. 2020. doi:10.2139/ssrn.2938955.

- Li HY, Fu SY, Wang RF. Construction of carbon information disclosure evaluation system. Stat Decis. 2015;(13):40–42.

- Clarkson PM, Li Y, Richardson GD, et al. Revisiting the relation between environmental performance and environmental disclosure: an empirical analysis. Account Organ Soc. 2008;33(4–5):303–327. doi:10.1016/j.aos.2007.05.003.

- Walker K, Wan F. The harm of symbolic actions and green -washing: corporate actions and communications on environmental performance and their financial implications. J Bus Ethics. 2012;109(2):227–242. doi:10.1007/s10551-011-1122-4.

- Qian W, Cai N. Institutional complexity and strategic choice of enterprise environment: an interpretation from the perspective of institutional logic. Comp Econ Soc Syst. 2015;(01):125–138.

- Demirgüç-Kunt A, Maksimovic V. Law, finance, and firm growth. J Financ. 1998; 53(6):2107–2137. doi:10.1111/0022-1082.00084.

- Durnev AA, Kim EH. To steal or not to steal: firm attributes, legal environment, and valuation. J Financ. 2005;60(3):1461–1493. doi:10.1111/j.1540-6261.2005.00767.x.

- Lu TP, Zhang DX. Financing demands, financing constraints and earnings management. Account Res. 2014;(01):35–41.

- Yang N, Guo SH. Financing demands, investor sentiment and earnings management. Wuhan Financ. 2020;(02):58–66.

- Meng Y. An empirical study on the influence of media attention on real earnings management. 6th International Conference on Humanities and Social Science Research (ICHSSR 2020). Atlantis Press, 2020:228–233. doi:10.2991/assehr.k.200428.050.

- Luo W, Guo X, Zhong S, et al. Environmental information disclosure quality, media attention and debt financing costs: evidence from Chinese heavy polluting listed companies. J Cleaner Prod. 2019;231:268–277. doi:10.1016/j.jclepro.2019.05.237.

- Song C, Tian YY, Chen Q. Internal control voluntary disclosure, disclosure cost and financing demand. J Shanxi Univ Financ Econ. 2014;36(01):91–102.

- Li H, Fu S, Chen Z, et al. The motivations of Chinese firms in response to the carbon disclosure project. Environ Sci Pollut Res Int. 2019;26(27):27792–27807. doi:10.1007/s11356-019-05975-5.

- Li L, Liu QQ, Tang DL. Carbon performance, carbon information disclosure quality and equity financing cost. Manag Rev. 2019;31(01):221–235.

- Zhou ZF, Wen K, Zeng HX. Carbon risk, media attention and debt financing cost – empirical evidence from listed enterprises in China’s A-share high-carbon industry. Mod Financ Econ. 2017;37(08):16–32.