?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.

?Mathematical formulae have been encoded as MathML and are displayed in this HTML version using MathJax in order to improve their display. Uncheck the box to turn MathJax off. This feature requires Javascript. Click on a formula to zoom.ABSTRACT

This paper investigates the development of domestic and international demand for Indonesian palm oil, in line with national biofuel mandates and established export markets. Domestic demand for palm oil for (i) achieving biodiesel targets and (ii) meeting food and industrial uses will reach 20 million tonnes by 2025, equivalent to 61% of Indonesian production in 2014. Thus, it is possible for Indonesia to be self-sufficient, reaching the biodiesel targets without increasing plantation areas. However, to meet both domestic and international demand, a total 51 million tonnes of crude palm oil will be needed in 2025. This requires additional land of up to 6 million hectares with current yields. The expansion of oil palm plantations in Indonesia has led to debates related to deforestation, threatened biodiversity, and greenhouse gas emissions. We show that increasing agricultural yields could serve the purpose, benefiting biodiesel production while reducing the need for new land. Therefore, we recommend that the ambitious Indonesian biodiesel mandates are pursued in combination with a strategy for increased productivity in palm oil production, utilization of degraded land to contain greenhouse gas emissions, and use of palm oil biomass residues for energy production.

Introduction

Palm oil has become one of the most important crops for food, energy, and international trade in Indonesia [Citation1,Citation2]. With major efforts to reduce fossil fuel dependency and new targets for introduction of biodiesel blends [Citation2,Citation3], the domestic demand for palm oil is bound to increase rapidly in the coming decade. Likewise, demand for vegetable oils continues to increase globally [Citation4]. While this offers the opportunity for continued development of the palm oil industry, it requires a significant expansion of palm oil production which, left unchecked, may lead to negative impacts such as land pressure and increase of greenhouse gas (GHG) emissions, among others [Citation5,Citation6]. In fact, previous expansion of palm oil production in Indonesia has been pointed out as a major cause of deforestation and GHG emissions [Citation6–8]. Thus, how can Indonesia take advantage of the expanding markets for palm oil without compromising on sustainability?

Indonesia became an importer of fossil oil after 2003 due to declining domestic production and increasing oil consumption [Citation9]. The country is now aiming at reducing energy dependency and GHG emissions, as well as diversifying energy sources [Citation10,Citation11]. An important policy in this direction is the promotion of biofuels such as biodiesel. In this context, Indonesia has adopted an ambitious biofuel policy with increased but differentiated targets by fuel and sector [Citation3,Citation12]. The target for biodiesel was set at 20% blend by 2016 for the transport and industry sector, and 30% in the power generation sector [Citation3]. Targets expand to 30% blending in 2025, comprising transport, industry, and power generation (Indonesia Regulation 12/2015). Indonesia produced 3.3 billion liters (bL) of biodiesel in 2014, of which 1.6 bL were used as transport fuel, and the rest exported [Citation3]. In spite of government efforts, biodiesel blending contributed only 6% of the total diesel consumption in 2014.

The main feedstock for biodiesel production in Indonesia is crude palm oil (CPO), which is also increasingly used for domestic food production and industrial applications. In addition, CPO exports are very important for the country's economy. Nevertheless, since 2015, palm oil products are subject to an export levy intended to divert production from export markets, and support the development of domestic biodiesel production [Citation12]. The tax revenue collected on exported CPO and CPO derivatives is used to promote biodiesel production and the domestic biofuel market. The traditional strategy used to meet increased CPO demand in Indonesia has been to expand the plantation area. As of 2006, the country is the largest producer of CPO in the world, a result of decades of favorable governmental incentives to expand production [Citation13]. In 2014, Indonesia used 10.6 million hectares (Mha) of land for palm oil production [Citation14] compared to 5.3 Mha in 2003, thus doubling the planted area in a decade. Indonesia had 92.4 Mha of forest area and 57 Mha of agricultural area in 2013 [Citation15]. Oil palm occupied around 18% of the agricultural land. Forest land has decreased by an average of 1.1% annually since 1990, while the oil palm area has increased by more than 10%. The expansion of oil palm plantations has been highly criticized, and identified as a major cause of land conversion, deforestation and loss of biodiversity [Citation16–18]. In fact, a major part of the GHG emissions in the country result from land-use change (LUC) [Citation5]. Already another 6–7 Mha of additional land has recently been allocated to the palm oil industry [Citation19]. With blending mandates aimed at reducing GHG emissions, the overall benefits of the policy will be jeopardized if increased domestic demand for biodiesel were to cause additional deforestation and LUC.

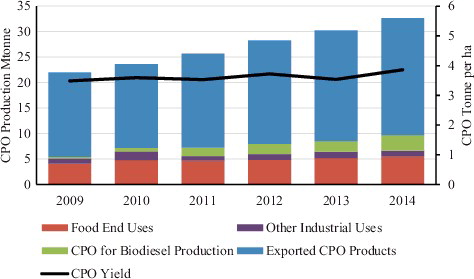

Therefore, alternative options to meet palm oil demand have to be considered, such as increasing agricultural yields. Yields achieved between 2009 and 2014 are shown in . Notably, the yields of Indonesian plantations have reached 3.8 tonnes CPO per hectare. This is significantly lower than those obtained in Malaysia, which reported an average of 4.5 tonne per ha in 2013 [Citation20,Citation21]. Therefore, it is worth exploring the role that yield improvements can play in meeting the demand for CPO in a context of increasing climate policy stringency. The latter refers particularly to the need to reduce emissions from LUC.

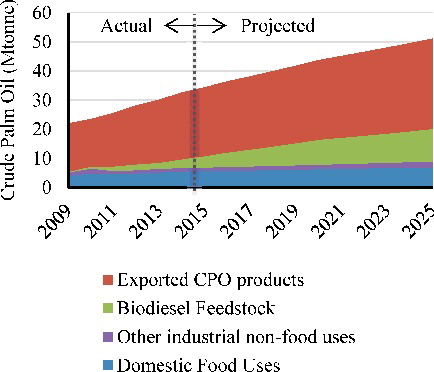

Figure 1. Volume of crude palm oil (CPO) feedstock for export, biodiesel production, food use and other industrial domestic uses in Mtonne (left axis), and CPO yield development in tonne per ha (right axis) in Indonesia, 2009–2014.

Many studies have investigated the role of oil palm in LUC dynamics and deforestation [Citation22–25], the impact of biofuels on food and LUC [Citation26], and the effect of biofuel mandates [Citation27–30]. Recently, different scenarios for simulating alternative options for meeting sugar self-sufficiency and bioethanol blending mandates in Indonesia were investigated [Citation31]. However, the conditions for CPO feedstock supply, and land area needed to meet the biodiesel mandates, in Indonesia have not been specifically addressed in previous studies. Both are important as biodiesel production will require an increasing amount of CPO to meet the blending targets. This study investigates the impact of biofuel mandates on future CPO demand, and whether increasing CPO demand can be met in Indonesia with improved productivity of feedstock supply.

Our intention is to determine (i) the amount of feedstock required to meet both domestic and export CPO demand, and (ii) the plantation area needed to produce that feedstock. We particularly explore variations in yield in the timeframe between 2015 and 2025 to verify whether plantation expansion can be halted without harm to the targets envisaged. The analysis contributes to improve understanding about the role that the agriculture sector can play in bioenergy development in Indonesia and other agrarian economies. The scope of the study is limited to the demand for CPO to meet fuel, food, and industrial demand within a relatively short term. Hence, the paper does not consider other vegetable oils or second-generation biodiesel (2G, e.g. waste-based biodiesel production) which are likely to become more important if increased penetration of biodiesel is aimed for in the longer run.

In the first scenario, we analyze the development of the domestic demand for CPO in Indonesia following from the introduction of the biodiesel blending policy. This scenario is used to give an indication of how much can be achieved if domestic markets are prioritized, and how far one could go beyond present biodiesel targets if all CPO were used domestically. The second scenario analyzes what will be required to meet both the domestic and export demand. Considering the global importance of palm oil for food, and the role of palm oil exports for Indonesia, this is a more likely scenario.

Following this introduction, the evolution of palm oil production and markets for CPO are evaluated in the second section, along with an analysis of the role that Indonesia plays as global supplier of palm oil for food, fuel, and industrial use. The methodological approach, data sources, and conditions for production expansion are presented in the third section. Results of the analysis are shown in the fourth section. Key issues and concerns regarding sustainable palm oil for biodiesel production are also discussed. Finally, the fifth section provides concluding remarks on the study.

Evolution of palm oil production chain and markets in Indonesia

Palm oil is one of the most important agricultural products in Indonesia. Following from a rapid agricultural development in the second half of the last century, palm oil has become an important source of both food and raw materials. Palm oil is also a significant commodity worldwide, comprising one third of all vegetable oil used for food [Citation32]. Today, Indonesia is the largest exporter of CPO in the world, sharing global market dominance with Malaysia.

Palm oil is an important commodity for Indonesia both domestically and internationally. The national CPO production has grown by 8% annually in the last years [Citation32], increasing from 22 million tonnes (Mtonne) in 2009 to 33 Mtonne in 2014 (see ). In 2014, the domestic market absorbed 30% of the CPO production within three main categories of use: food, biodiesel production and other industrial non-food uses [Citation14]. Palm oil is the most important vegetable oil used for food in Indonesia; it is used twice as much as soybean and 4 times more than peanut oil [Citation14]. The domestic use of palm oil for food has increased by 20% since 2011, and reached 5.5 Mtonne in 2014 [Citation14,Citation33]. The demand of palm oil for food is expected to continue increasing, together with population and gross domestic product (GDP) growth in Indonesia [Citation34].

After food, the largest domestic use of CPO is for biodiesel production. shows the distribution of CPO uses in Indonesia and exports from 2009 to 2014. In 2014, 3.0 Mtonne of CPO were used for biodiesel production compared to 1.2 Mtonne for other industrial uses. A total of 3.3 bL biodiesel were produced in Indonesia in 2014, 1.6 bL of which were used domestically, particularly in transport (95%) [Citation3]. Biofuels are internationally traded [Citation35–38] and the market has evolved according to the logics of resource potential and availability, and comparative production costs [Citation39]. Despite international debate around the risks of biofuel expansion, and imposed restrictions to address sustainability requirements, these markets continue growing.

From 2004 to 2014, the production of palm oil doubled in the world, in parallel with increasing population and food consumption. In 2014, one third of all vegetable oil used for food originated from palm oil [Citation32]. Food and Agriculture Organization of the United Nations (FAO) and The Organisation for Economic Co-operation and Development (OECD) estimate that the demand for vegetable oil for food will increase by 25% globally until 2024 [Citation34]. Of the total global export of CPO, 79% is used for food. Many countries are completely dependent on these imports for their supply of vegetable oil. India, for example, the largest importer of palm oil, has no domestic production, and uses over 95% of the imported volume (9 Mtonne) for food purposes [Citation32]. Indonesia exported 70% of its production of CPO in 2014, and thus the country plays an important role in the global market for vegetable oil, palm oil in particular. shows the supply chain of the current CPO and biodiesel production system, including information on CPO demand and land requirements.

Figure 2. Crude palm oil (CPO) and biodiesel production system with domestic uses and export. Numbers in parentheses refer to the production and use in 2014.

Given the above context, we evaluate how much CPO is needed for Indonesia to meet the domestic demand for biodiesel, food, and other industrial uses, while also continuing to play a role in the global market. We examine the total CPO consumption that can be expected until 2025, and the corresponding amount of land required to meet the demand.

Methodology and data sources

To analyze the impact of biofuel mandates on future CPO demand, and explore how CPO demand can be met in Indonesia, we evaluate future domestic use and export of Indonesian palm oil. CPO demand for producing biodiesel is derived from projections of fuel use and conversion rates for palm oil biodiesel. We make a projection of diesel demand until 2025, using historical data and expected demand growth. Biodiesel demand is derived from volumetric blending according to biofuel mandates as defined by Indonesia Regulation 12/2015. In addition to the demand for biodiesel to meet blending targets, we include the development of domestic demand for Indonesian CPO for food and other industrial purposes. We also elaborate on the development of exports until 2025. Based on a demand analysis, the total amount of CPO feedstock required is calculated and, subsequently, the area required for oil palm plantations.

We provide details on the projections for future CPO demand resulting from increasing biodiesel production, and CPO supply for domestic demand and international export markets. The CPO feedstock for biodiesel is aggregated with the demand for other uses (food, industrial, and export). We then derive the plantation area needed to cover the total expected demand. The study linearly extrapolates the projection of palm oil needed for meeting the blending targets, food production and industrial uses. We assume that no major changes will take place until 2025 when it comes to demand development, which justifies this linear extrapolation. The potential interactions with alternative crops for vegetable oils for food and fuel production, and potential price conflicts, are outside the scope of the study.

Projections for CPO demand

The study particularly considers the impact that Indonesian biodiesel policies may have on the demand for CPO, thus also affecting demand for land to accommodate oil palm plantations. Therefore, we first project the domestic demand for CPO in Indonesia following from the introduction of the biodiesel blending policy. Limiting the amount of land to the area used in 2014 (10.6 Mha), we evaluate whether the current plantation area is sufficient to cover domestic demand in the first place, without requiring further plantation expansion. This is done to provide a reference scenario, and as a way of better contextualizing the challenge being faced at the national level.

Given that the domestic use of palm oil amounted to 30% of the total production in 2014 (see ), focusing solely on domestic demand would be a drastic change of course for the palm oil industry. Thus, we proceed to verify what will be required for Indonesia to be able to meet both the domestic and export demand for CPO until 2025 in a context of improved sustainability in the sector. For the purpose of the analysis, improved sustainability is correlated with limitation in the expansion of plantations to avoid deforestation. Notice that the export of biodiesel is excluded. Although Indonesia exported more than half of its biodiesel production in 2014, we consider that this was mainly due to short-term discrepancies in the process of introducing biodiesel blends in the internal market. We assume that this will not be the case once diesel subsidies are eliminated and appropriate incentives are created for promoting biodiesel blending and mandatory targets.

Domestic biodiesel demand projection

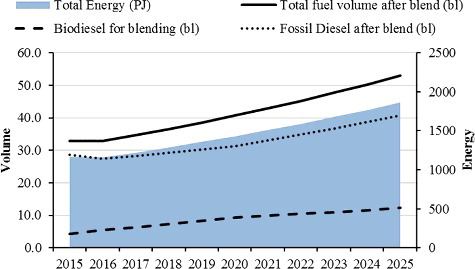

The biodiesel policy targets aim at reducing fossil fuel imports, diversifying energy sources and reducing GHG emissions. Indonesia has biodiesel blending targets for transport and industrial sectors set at 15% in 2015, 20% in 2016 and 30% from 2020 to 2025. To achieve these targets, Indonesia will need more biodiesel than the country currently produces. Transport and industrial sectors stood for a combined 99% of diesel consumption in 2014, transport alone using over 95% of the diesel [Citation3]. Note that the analysis does not consider biodiesel consumption in power generation. The government of Indonesia is reducing its reliance on diesel fuel-based power production through a favorable policy for coal- and natural gas-based power plants [Citation12]. Fossil diesel for the total electricity generation is estimated to be only 1% by 2025.

Blending targets are specified by volume of fuel. The basis for the estimation of future fuel demand is the diesel energy demand which can be covered by both fossil diesel and biodiesel. Demand for diesel in the transportation and industrial sectors is expected to rise by 5.4% annually. This value is derived from an average from projections by the United States Department of Agriculture (USDA) and the Agency for the Assessment and Application of Technology (BPPT: Badan Pengkajian dan Penerapan Teknologi in Bahasa) [Citation3,Citation40]. The biodiesel share is based on the fuel blending targets and blending by fuel volume. Our projections for future demand for biodiesel can be seen in , which shows the biodiesel and fossil diesel needed to meet blending targets and the projected energy demand in 2025.

Figure 3. Projected diesel demand in Indonesia, expressed in volume of the energy carrier (left axis) and total energy (right axis).

Land needed to meet palm oil biodiesel feedstock requirements is estimated using historical average yields in Indonesia, and displayed along with volume of biodiesel and CPO feedstock required for the blending targets (see ). Details on fuel conversion to CPO feedstock and results of other projections can be found in Section (Calculations for CPO demand and plantation area requirements) and in the Appendix ( and ).

Table 1. Fuel volume, feedstock mass and area requirements for achieving Indonesian biodiesel blending targets according to Indonesia Regulation 12/2015.

Palm oil demand for domestic food and industrial uses

Data and assumptions used in projections of domestic palm oil demand for food and industrial uses were gathered from three external sources. The growth in domestic palm oil use for food and the export of palm oil is based on the OECD-FAO Agricultural Outlook 2015 [Citation34]. The OECD-FAO report provides projections until 2024, and we chose to linearly extrapolate the value for an additional year to include 2025. We chose 2014 as the starting year for our projections. The values for domestic food demand, industrial use and export are gathered from the USDA report on Indonesia oilseeds and products [Citation14]. Population estimates and projections as well as GDP data are collected from the World Bank database [Citation41].

Palm oil has an important role in food diets in Indonesia. Increase in palm oil demand for food originates from both population growth and higher vegetable oil consumption due to dietary changes related to growing GDP per capita [Citation34]. The population is projected to grow from 254 million inhabitants in 2014 to 285 million in 2025, based on World Bank forecasts [Citation41]. We assume that food demand will grow by 1.1% per capita in Indonesia [Citation34].

We anticipate that the domestic industrial demand will have an important role to play in the demand for palm oil. Industrial domestic non-food uses in Indonesia include a plethora of oleo-chemical products such as pharmaceuticals, cosmetics and industrial chemicals. To calculate the future demand in this sector, some generalization was made. The Asia-Pacific region dominates the oleo-chemical market, and demand in this region is expected to increase 5.1% annually [Citation42]. Therefore, we assume that the annual CPO demand from the domestic non-food industry will also increase by 5.1% annually until 2025.

Development of palm oil exports

In 2015, 30 bL biodiesel was produced globally [Citation43] of which 80% came from vegetable oil [Citation4]. Vegetable oil will remain the main feedstock for biodiesel production until 2025 to meet an expected world demand of 41.4 bL [Citation4]. Waste-based biodiesel will only contribute 20% of the total projected biodiesel demand. Around 12% of the global vegetable oils are used for biodiesel production, with palm oil standing for one third of the total. Thus, in order to meet the growing demand for vegetable oil for food (i.e. edible oil), biofuel, and industrial uses, more CPO will be needed.

CPO is the only vegetable oil exported from Indonesia [Citation14]. The export of palm oil is very important for Indonesian producers as the market is well established and growing. The Indonesian export of palm oil grew from 3.4 billion USD to 17.5 billion USD between 2004 and 2014 – that is, from 5% to 10% of the total export value in 10 years [Citation44]. The development of the vegetable oil market could have a significant impact on future CPO demand. The global demand for vegetable oil is projected to increase by an average of 1.6% per year [Citation34]. In 2024, it is estimated that Indonesia will be supplying 37% of all vegetable oil exports in the world [Citation34]. We use the OCED-FAO demand projections for 2024 and Indonesia's share of export to calculate future exports of CPO from Indonesia. We interpolate from the export volumes reported for Indonesia in 2014 [Citation14] to 37% of the projected vegetable oil demand in 2024 [Citation34]. We linearly extrapolate this in order to include 2025. A summary of these CPO demand projections until 2025 is shown in .

Table 2. Projections of future demand for Indonesian crude palm oil (CPO, Mtonne).

Calculations for CPO demand and plantation area requirements

This section shows how we calculate the requirements for achieving domestic and international CPO demand. We consider the palm oil supply chain system as shown in with domestic food and industrial uses and exports, excluding biodiesel export. Our intention is to determine (i) the amount of feedstock required to meet CPO demand and (ii) the plantation area needed to produce that feedstock. We use a straightforward two-step method for this purpose. First, we convert the volume of biodiesel needed to meet the blending targets into an equivalent amount of CPO feedstock. The feedstock for biodiesel is then aggregated with the demand for other uses (food, industrial and export) – see EquationEquation (1)(1)

(1) .

(1)

(1) From the aggregation of CPO uses, we are able to derive a total amount of CPO needed each year. We then elaborate on yields (tonne CPO per ha) to determine the land use requirements to produce this feedstock – see EquationEquation (2)

(2)

(2) .

(2)

(2) EquationEquation (1)

(1)

(1) determines the total CPO needed for different end uses, in line with the system shown in . Biodiesel demand is gathered from our projections in section above Projections for CPO demand (also, see and ). The CPO-to-biodiesel conversion ratio used is an average based on three previous studies [Citation45–47]. Fuel conversion and fuel data can be found in and .

We do not consider any improvements in biodiesel conversion during the time period analyzed, or the use of other biodiesel feedstock or 2G biodiesel. Neither do we consider industrial limitations in conversion capacity. As Indonesia has clearly stated its ambition to reduce GHG emissions, increase energy security and diversify energy sources, we consider that blending targets will be met and that all future biodiesel production will be used domestically to achieve those targets. This is under the assumption that bottlenecks preventing implementation of Indonesian domestic biodiesel blending policies are removed.

Total plantation area is the product of the total CPO feedstock demand and agricultural yield for palm oil, calculated as per EquationEquation (2)(2)

(2) . Not all plantation area is harvested every year; some parts undergo planting or replanting, or have not yet matured. Therefore, the ratio of 0.8 harvested area to total plantation area is used. This ratio has been observed historically in Indonesia [Citation14] and used in projections for oil palm production by Wicke [Citation22].

In the face of the low average yields observed in Indonesia today, and potential improvements, a one-way one-parameter sensitivity analysis is performed on the Yieldi, j parameter, where j is the yield in the i:th year between 2015 and 2025. This is done to highlight the impact that yield may have on the plantation area required for palm oil production, and the potential benefits of promoting higher yields. We consider future agricultural yields that are realistic within the short term or best cases for Indonesian oil palm plantations. The first case considers the present average yield of 3.8 tonne/ha, implying no improvements. The second case implies medium improvements or 22% better yields (that is, 4.4 tonne/ha) by 2025. This is in line with past trends (2006–2014) [Citation48] and results from 3% improvement per year [Citation49]. The last case implies reaching high yields, up to 6.0 tonne/ha in 2025, in line with the potential yield indicated in various studies [Citation13,Citation22,Citation50–52]. A summary of yields and parameters used in the sensitivity analysis is shown in .

Table 3. Palm oil yields for analysis of land requirements (tonne/ha).

Results and discussion

To meet the 30% biodiesel blending target in 2025, 12.2 bL of biodiesel is needed. This requires 11.2 Mtonne of crude palm oil (), equivalent to one third of the total CPO production in 2014, and 370% of the amount of CPO used for biodiesel production in 2014. It should be kept in mind that the biodiesel production in the projection is devoted solely to meeting the Indonesian blending targets, and thus there is no room for export of biodiesel in this case.

Feedstock and land demand is evaluated to analyze the impact of the introduction of the biodiesel blending policy and verify whether the increasing demand can be met without further pressure on forest land for plantation expansion. The results of the analysis are visualized in and for the domestic demand alone, and and for both domestic and international demand.

Figure 4. Crude palm oil (CPO) required for domestic uses only.

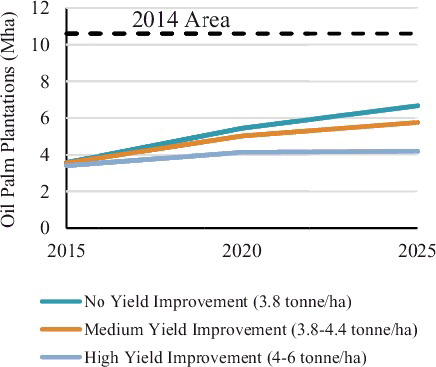

Figure 5. Plantation area needed to supply domestic crude palm oil (CPO) demand.

Figure 6. Crude palm oil (CPO) required for domestic and export demand.

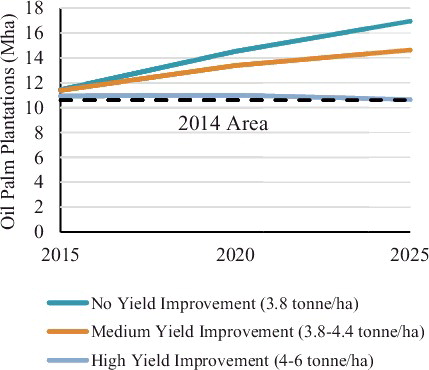

Figure 7. Plantation area needed for domestic and export crude palm oil (CPO) demand.

Meeting domestic demand by 2025

Indonesia's use of CPO is projected to double and reach 20.1 Mtonne by 2025, compared to 10 Mtonne in 2014. shows details of the changes in demand for food, biodiesel production and other industrial uses. A majority of the increase will be from biodiesel production which will require 11.2 Mtonne of CPO in 2025, up from 3 Mtonne in 2014. The CPO demand for food will increase from 5.5 Mtonne in 2014 to 6.9 Mtonne in 2025. The other industrial non-food uses increase by over 70% to 2.0 Mtonne in 2025.

The land required for supporting the domestic demand and reaching the target blends (i.e. 30% by 2025) amount to 6.7 Mha with no yield improvements. This is equivalent to 64% of the total oil palm plantation area in 2014. If yields are improved to 6 tonne/ha, only 40% of current cultivated area is required for domestic demand. Thus limiting production to 10.6 Mha as present will leave a surplus of 12 to 31 Mtonne CPO for exports or other applications after domestic uses are met, all depending on the yields achieved (see ).

In 2014 only 30% of total production was used to meet the domestic demand; thus, the new demand implies a doubling of domestic demand by 2025. Biodiesel production to meet the set targets will be responsible for four fifths of the domestic increase in CPO demand. Thus, the implementation of blending targets will have a great impact on the availability of CPO feedstock for uses other than biodiesel. If not properly managed, this could lead to continued pressure to expand oil palm plantations. Certainly, if export is disregarded, Indonesia will have no problem realizing the blending targets and meeting other domestic demands without expanding plantations or improving palm oil yields. In fact, if all CPO is used in the country, 40–69% of the domestic fossil fuel (i.e. diesel) demand could be substituted by biodiesel in 2025 (depending on yields achieved). However, in face of the established exports and growing markets for CPO, the high export value of the CPO commodity, aligned interests along the export markets, and the large costs that curtailing exports would impose on the national economy, a focus on domestic demand only is not a realistic option.

Meeting domestic and export demand by 2025

To remain a major supplier of CPO both internally and at the global level, Indonesia will have to expand CPO production significantly. The total CPO production will have to reach 51.1 Mtonne in 2025. This implies an absolute increase of 18.1 Mtonne CPO compared to 2014. Export and biodiesel production are responsible for 44% and 45% of the increase in demand, respectively. shows the feedstock required for meeting both domestic uses and exports. Exports will still require the majority of the CPO reaching 31.0 Mtonne in 2025, equivalent to a 33% increase from the 23.0 Mtonne exported in 2014. This means that exports would account for 61% of the total demand in 2025, compared to 70% in 2014.

Notably, despite the growth of CPO production required to meet increasing demand until 2025, the annual growth rate is only half (4%) of what has been seen between 2009 and 2014 (8%). The increase in demand occurs at a higher rate in the first 5 years until 2020 because of the targeted blend, which goes from 20% in 2016 to 30% in 2020. From 2020 to 2025, the blending rates remain at 30% and additional biodiesel demand comes from an increase in total diesel demand instead of increased blending mandates, unless new policies are put in place.

shows the amount of land required, evaluating sensitivity to different yield levels (see ). If yields remain at 3.8 tonne per ha, a total of 16.9 Mha will be needed to meet CPO demand by 2025. This implies 6.3 Mha in addition to the 10.6 Mha occupied by palm oil plantations in 2014. Achieving medium yield improvements (3.8 to 4.4 tonne per ha) will reduce land needs to 14.6 Mha, which is still 4.0 Mha more than the area occupied today. However, if the potential yield of 6 tonne per ha is achieved, less than 0.5 Mha additional land is required until 2025. Notice that yields are calculated for mature productive land, which amounts to 80% of the total planted area.

Development prospects in the palm oil industry

The analysis in this paper shows that, with improved resource efficiency, it is possible to achieve the targets set by the Indonesian government when it comes to biodiesel production from palm oil. Improved yields of oil palm plantations are fully possible in Indonesia [Citation13,Citation51,Citation52,Citation54]. Yields in Indonesian oil palm plantations are currently lower than those observed in the neighboring country Malaysia, the second largest CPO producer in the world, where the yield reaches 4.5 tonne per ha in 2013 [Citation20]. The highest performing province in Indonesia, Central Kalimantan, also reported 4.5 tonne per ha 2014 [Citation48].

A more intensive use of the land, in line with the potential indicated in former studies and the performance observed in Malaysian plantations, will result in improved resource efficiency and enhanced production. This is an important observation as several studies have addressed sustainability concerns related to the expansion of palm oil production [Citation22–25,Citation55]. In addition, a recent study evaluating the role of land in the implementation of sectoral policies in Indonesia, viz. biofuel, agricultural, forest and climate policies, indicated the need for increased coherence in land classification and transparency on land allocation and use as a way to improve sustainability in sectoral policies of Indonesia [Citation56]. The possibility to continue developing the palm oil industry without further pressure on land is a promising signal for the industry.

Increasing yields could bring multiple positive effects, including reduced pressure on land, protection of forests and biodiversity, reduction of emissions and improved output from the land. Increased productivity has previously been recommended by other authors when introducing biofuels [Citation28,Citation57,Citation58]. Increased yields can help secure biomass supply for biofuel production [Citation57,Citation58] and possibly reduce the total cost of biodiesel production [Citation59]. Some yield improvement may come naturally as the oil palms in Indonesian plantations mature and reach peak yield, occurring at age 10 to 20 [Citation60]. Yield gaps exist also among different types of producers. In estate plantations, the yield of CPO is 0.5 tonne higher per ha than in smallholdings [Citation48,Citation61]. This disparity may be mainly due to a lack of leadership in smallholders’ cooperatives and management practices, but unclear land tenure may also play a role [Citation62]. Closing the yield gap would help secure enough biomass for food, fuel and exports.

A higher yield can help lower production costs for biodiesel, making the implementation of blending targets more cost-efficient. However, at present, Indonesia lacks a clear national strategy for promoting improved yields in palm oil production. Such a strategy has, for instance, been developed in neighboring Malaysia to boost palm oil production as part of a larger national development program. Having a political strategy for sustainable intensification of feedstock production has been recommended as a way of addressing the complexity of land dynamics for biofuel purposes [Citation63]. Our study shows that such a strategy will improve resource efficiency, an important step also toward improved sustainability in the sector.

Yield improvement can be achieved through best management practices in cultivation and harvesting, complying with certification sustainability criteria, and improving quality of fresh fruit bunches (FFB) [Citation52]. Palm oil standards and certification schemes, namely the Roundtable on Sustainable Palm Oil (RSPO) and Indonesia Sustainable Palm Oil (ISPO), are in place, but it is important to harmonize sustainability criteria and standards, including definitions, unified and coherent methodologies, and verification and monitoring procedures.

In spite of the ongoing debates, palm oil will remain the main feedstock for biodiesel production in the near future [Citation4,Citation64]. Best management practices considering environmentally friendly approaches such as zero burning, conservation of wildlife and habitat, integrated pest management, and waste minimization and utilization are some of the best strategies for improving the supply chain efficiency [Citation64]. Best management practices not only contribute to increase yield but also help maintain soil quality and health [Citation65]. Empty fruit bunches (EFB, a waste product) at the CPO mills can be composted and used as fertilizer for nutrient cycling, and for maintaining soil quality. Biomass residues such as fiber and shells can be efficiently utilized in combined heat and power (CHP) plants to produce surplus electricity for sale to the grid. Moreover, waste streams – the palm oil milling effluent (POME) – can be used to produce biogas for electricity generation in Indonesia. In spite of technological advancements in the 2G biodiesel production [Citation66], there are still concerns in the supply chains of waste cooking oil (WCO) such as scattered production points (restaurants, hotels, households) [Citation67] and recycling modes [Citation68]. WCO available for biodiesel production is estimated by multiplying the recovery ratio (i.e. 20–45% of vegetable oil consumption) and percentage (%) of the country's population in metropolitan area [Citation69]. It should be noted that the entire metropolitan area has a population of over 30 million in Indonesia (in 2014) [Citation70], i.e. equal to around 12% of the total population. At present, due to the lower WCO collection efficiency, the study does not consider the 2G biodiesel production from waste cooking oil in the projection of biodiesel production in Indonesia. However, there are prospects for increased biodiesel production from WCO if the collection of palm oil WCO is promoted. For example, the potential of biodiesel from WCO (waste derived from edible palm oil) is between 12 and 27 PJ, which represents between 8 and 19% of the total biodiesel blending requirements in 2015 in Indonesia. Here, WCO is estimated based on a vegetable oil used recovery ratio of 20%−45% [Citation69] and 30% population in the metropolitan area.

GHG emissions from LUC and biodiesel production

The expansion of oil palm plantations in the past few decades has been subject to significant criticism due to deforestation, loss of biodiversity, and increase in GHG emissions. GHG from direct LUC occur when carbon stocks in soil and vegetation are altered due to the expansion of oil palm plantation into forest or pasture land. Emissions from indirect land use change (iLUC) occur when agricultural land (for food and feed production) and forest land (for fiber and timber production) are displaced due to the cultivation of oil palm for biofuel production. Additionally, if agricultural crops are diverted for biofuels production instead of producing food, feed, fiber and industrial products, there might be iLUC. This does not occur necessarily at a local level, though. Land usually needs to be converted elsewhere for meeting food, feed and fiber demand.

Thus, direct and indirect land use (LUC and iLUC) emissions may affect GHG emissions significantly [Citation71,Citation72]. If biofuels are produced from grassland or forest land, GHG emissions might actually increase, leading to a ‘biofuel carbon debt’ with a long payback period [Citation71]. In spite of increasing concerns about iLUC emissions, there are no agreed international standards or procedures for accounting GHG emissions related to iLUC emissions [Citation73]. Land quality and management practices also affect bioenergy feedstock yields and related GHG emissions [Citation74]. In any case, the potential increase in yields, and their capacity to help meet increasing demand for palm oil, as shown in the analysis, offers an opportunity to contain further LUC in the near future.

Emissions from palm oil biodiesel production mainly come from the cultivation of oil palm (including LUC) and processing operations, i.e. palm oil milling and biodiesel conversion phases. There are several studies to estimate GHG emissions using a life-cycle assessment (LCA) approach. The emissions sources include: land clearing and cultivation, fertilization use and application, fossil fuel use, and methane produced from POME and EFB disposal, while GHG fixation and carbon credits are considered from CO2 fixed by oil-plant trees and GHG avoided by selling main and co-products in palm oil milling and refining operations [Citation75,Citation76].

Palm oil milling biomass residues (EFB, palm kernel shells, and fiber) and waste streams (POME) can be used for energy production since they have a high energy content. Biogas recovery in POME-based anaerobic digestion plants and its use to substitute for fossil energy can result in significant reductions of GHG emissions in comparison with traditional open-pond treatment facilities [Citation75,Citation77]. It should be noted that GHG emissions from palm oil production are lower than those from other vegetable oils, due to the high yields per hectare. Better management practices, higher yields and use of organic fertilizers can further reduce emissions in the cultivation stage. Biofuels produced from waste biomass or perennial feedstock grown on degraded and abandoned agricultural lands may offer net GHG savings [Citation71]. Additionally, palm oil expansion on degraded land for biodiesel production can avoid GHG emissions [Citation22,Citation78], simultaneously maintaining the rich biodiversity and ecosystem services of forests.

Food and fuel security: enhancing resource efficiency in the palm oil industry

The analysis above has indicated how much land is required to meet the projected demand for palm oil in Indonesia, considering both domestic and international demand for biodiesel, food and industrial use. When agricultural land is used to produce both food and biofuel, competition is likely to occur. In this study, we do not consider the price interactions that can lead to such competition. We have used a linear extrapolation method based on the past trend and future projections for estimating demand for palm oil in the time frame between 2015 and 2025. This is a first step, comprising an evaluation of the physical conditions for the implementation of present biodiesel policies in regards to land use, agricultural productivity, plant efficiency for energy conversion, and demand for palm oil products. The advancement of 2G biofuels is likely to further affect the potential resource efficiency of the palm oil industry, reducing the risks for competition with food. However, this is not a realistic option in the short time frame examined in this study.

Increased use of vegetable oils for biodiesel production may cause food price fluctuations and affect food security. The interaction of food and biofuel systems is complex when it comes to expansion of land for palm oil feedstock production, prices for palm oil and derived products (i.e. fuel and food). Thus, caution is needed when designing economic and policy instruments to promote the development of the industry. Once the biofuel blending targets become mandatory, the demand for biodiesel will be determined by policies rather than by market forces. This could lead to an increase in food prices if unchecked. Economic models are developed to analyze the effect of the biofuel expansion, land use allocation, and biofuel–food price interactions [Citation79–85]. These models are also used to address uncertainties related to iLUC emissions [Citation86,Citation87].

The analysis in this study helped identify unique measures that could improve resource efficiency in the palm oil sector of Indonesia in the short term, including best agricultural practices for improved yield and energy generation from biomass wastes and industrial effluents. Further analysis is needed to explore interlinkages between biofuel and food systems, aiming at optimal conditions for palm oil utilization, in terms of allocation of land, feedstock price, biofuel and food prices, along with fuel subsidies, blend mandates, use of alternative vegetable oils and technological innovation. Such analysis will be needed as Indonesia aims for more ambitious targets in this industry, in terms of both value creation and sustainability.

Conclusions

The results of this study indicate that the palm oil industry in Indonesia can develop both nationally and internationally without expansion of oil palm plantations. In fact, Indonesia can meet its domestic demand for CPO until 2025 using the equivalent of 63% of the oil palm planted area in 2014, while keeping the same average yield. However, this would curtail exports and the option to profit from the development of global palm oil markets. Today, Indonesia holds a leading position in the international palm oil market, and palm oil exports are important for the country's economy. In addition, reducing exports from Indonesia may affect food security in countries relying on large palm oil quantities for food, such as India, China, Pakistan and Bangladesh.

Yield improvements are fully possible and bring multiple benefits in addition to the possibility to meet both domestic and international demand for CPO. Focusing on yield improvements is a promising option as it allows the country to pursue other objectives such as reduction of encroachment on forest land, threats to biodiversity, and mitigation of GHG emissions related to LUC. In addition, yield improvements can help increase the total economy of the palm oil industry, bringing improved rents from the land and more income to smallholders. Ultimately, this will also affect the costs of implementing the biodiesel targets, in a positive way. A national strategy to promote improvement in yields is highly recommended and should address the varying conditions in oil palm production found in different types of production units in the country. Although not analyzed in this study, the utilization of palm oil residues for electricity and 2G biofuel production can further improve the energy and climate gains of palm oil biodiesel production systems, though this will require integrated strategies, and will take longer to implement.

Acknowledgements

This work was funded by the Swedish Energy Agency (Energimyndigheten) and conducted under the Indonesian Swedish Initiative for Sustainable Energy Solutions (INSISTS). The study has been carried out independently.

Disclosure statement

No potential conflict of interest was reported by the authors.

Additional information

Funding

References

- OECD/FAO. OECD-FAO agricultural outlook 2015. Paris: OECD Publishing; 2015. https://doi.org/10.1787/agr_outlook-2015-en.

- Putrasari Y. Praptijanto A, Santoso WB, et al. 2016; Resources, policy, and research activities of biofuel in Indonesia: A review. Energy Reports.2:237–245..

- Global Agriculture Information Network (GAIN) - USDA Foreign Agricultural Service. Indonesia biofuels annual 2015, United States Department of Agriculture (USDA). 2015.

- OECD/FAO. OECD-FAO agricultural outlook. Paris: OECD Publishing; 2016. https://doi.org/10.1787/agr_outlook-2016-en.

- Uusitalo V, Väisänen S, Havukainen J, et al. Carbon footprint of renewable diesel from palm oil, jatropha oil and rapeseed oil. Renew Energy. 2014;69:103–113. DOI:10.1016/j.renene.2014.03.020.

- Ramdani F, Hino M. Land Use Changes and GHG Emissions from Tropical Forest Conversion by Oil Palm Plantations in Riau Province, Indonesia. PLoS One. 2013;8(7):e70323. DOI:10.1371/journal.pone.0070323.

- Gaveau DLA, Sheil D, Husnayaen, Salim MA, et al. Rapid conversions and avoided deforestation: examining four decades of industrial plantation expansion in Borneo. Sci Rep. 2016;6:32017. DOI:10.1038/srep32017.

- Susanti A, Maryudi A. Development narratives, notions of forest crisis, and boom of oil palm plantations in Indonesia. Forest Policy Econ. 2016;73:130–139..

- >BP Statistical Review of World Energy. 2016. Available at: http://www.bp.com/statisticalreview (Accessed 10 August 2017).

- Mujiyanto S, Tiess G. Secure energy supply in 2025: Indonesia's need for an energy policy strategy. Energy Policy. 2013;61:31–41. DOI:10.1016/j.enpol.2013.05.119.

- Kumar S, Shrestha P, Salam PA. A review of biofuel policies in the major biofuel producing countries of ASEAN: Production, targets, policy drivers and impacts. Renewable Sustainable Energy Rev. 2013;26:822–836. DOI:10.1016/j.rser.2013.06.007.

- Global Agriculture Information Network (GAIN) - USDA Foreign Agricultural Service. Indonesia biofuels annual 2016, United States Department of Agriculture (USDA). 2016.

- Corley RHV, Tinker PB. The Oil Palm. Fifth Edition ed. Oxford: John Wiley & Sons, Ltd; 2016. DOI:10.1002/9781118953297.

- Global Agriculture Information Network (GAIN) - USDA Foreign Agricultural Service. Indonesia: oilseeds and products annual 2015, United States Department of Agriculture (USDA). 2015.

- FAO. Food and agriculture organization of the United Nations, statistics division, (FAO-STAT), Available from: http://www.fao.org/faostat/en/#home. 2015.

- Koh LP, Wilcove DS. Is oil palm agriculture really destroying tropical biodiversity ? Conserv Lett. 2008;1:60–64. DOI:10.1111/j.1755-263X.2008.00011.x.

- Butler RA, Koh LP, Ghazoul J. REDD in the red: palm oil could undermine carbon payment schemes. Conserv Lett. 2009;2:67–73. DOI:10.1111/j.1755-263X.2009.00047.x.

- Fitzherbert EB, Struebig, MJ, Morel A, et al. How will oil palm expansion affect biodiversity ? Trends Ecol Evol. 2008;23:538–545. DOI:10.1016/j.tree.2008.06.012.

- USDA, FAS -. United States Department of Agriculture, Foreign Agricultural Service. Commodity intelligence report. Indonesia: Palm Oil Expansion Unaffected by Forest Moratorium; 2013. Available at http://www.pecad.fas.usda.gov/highlights/2013/06/indonesia/ (accessed 24 August 2017).

- Global Agriculture Information Network (GAIN) - USDA Foreign Agricultural Service. Malaysia: Palm Oil PSD Revisions (Oilseeds and Products), United States Department of Agriculture (USDA). 2015.

- USDA, FAS -. United States Department of Agriculture, Foreign Agricultural Service. Commodity intelligence report. Southeast Asia: Post-2020 Palm Oil Outlook Questionable; 2014. Available at https://pecad.fas.usda.gov/highlights/2014/09/SEAsia/index.htm (accessed 20 December, 2016).

- Wicke B, Sikkema R, Dornburg V, et al. Exploring land use changes and the role of palm oil production in Indonesia and Malaysia. Land Use Policy. 2011;28:193–206. DOI:10.1016/j.landusepol.2010.06.001.

- Koh LP, Miettinen J, Liew SC, et al. Remotely sensed evidence of tropical peatland conversion to oil palm. Proc Natl Acad Sci USA. 2011;108:5127–5132. DOI:10.1073/pnas.1018776108.

- Sayer J, Ghazoul J, Nelson P, et al. Oil palm expansion transforms tropical landscapes and livelihoods. Glob Food Sec. 2012;1:114–119. DOI:10.1016/j.gfs.2012.10.003.

- Gatto M, Wollni M, Qaim M. Oil palm boom and land-use dynamics in Indonesia: The role of policies and socioeconomic factors. Land Use Policy. 2015;46:292–303. DOI:10.1016/j.landusepol.2015.03.001.

- Lam MK, Tan KT, Lee KT, et al. Malaysian palm oil: Surviving the food versus fuel dispute for a sustainable future. Renew Sustain Energy Rev. 2009;13:1456–1464. DOI:10.1016/j.rser.2008.09.009.

- Havlík P, Schneider UA, Schmid E, et al. Global land-use implications of first and second generation biofuel targets. Energy Policy. 2011;39:5690–5702. DOI:10.1016/j.enpol.2010.03.030..

- Mosnier A, Havlík P, Valin H, et al. Alternative U.S. biofuel mandates and global GHG emissions: The role of land use change, crop management and yield growth. Energy Policy. 2013;57:602–614. DOI:10.1016/j.enpol.2013.02.035.

- Ravindranath NH, Lakshmi CS, Manuvie R, et al. Biofuel production and implications for land use, food production and environment in India. Energy Policy. 2011;39:5737–5745. DOI:10.1016/j.enpol.2010.07.044.

- Wise M, Dooley J, Luckow P, et al. Agriculture, land use, energy and carbon emission impacts of global biofuel mandates to mid-century. Appl Energy. 2014;114:763–773. DOI:10.1016/j.apenergy.2013.08.042.

- Khatiwada D, Silveira S. Scenarios for bioethanol production in Indonesia: How can we meet mandatory blending targets ? Energy. 2017;119:351–361. DOI:10.1016/j.energy.2016.12.073.

- USDA, FAS - United States Department of Agriculture, Foreign Agricultural Service. Oilseeds: world markets and trade. 2015. Available at http://www.fas.usda.gov/data/oilseeds-world-markets-and-trade (accessed 15 June 2016).

- Global Agriculture Information Network (GAIN) - USDA Foreign Agricultural Service. Indonesia: oilseeds and products annual 2013, United States Department of Agriculture (USDA). 2013.

- OECD/FAO. OECD-FAO Agricultural Outlook 2015. Paris: OECD Publishing; 2015. DOI: https://doi.org/10.1787/agr_outlook-2015-en.

- Johnston M, Holloway T. A global comparison of national biodiesel production potentials. Environ Sci Technol. 2007;41:7967–7973. http://pubs.acs.org/doi/abs/10.1021/es062459k (accessed 24 August 2016).

- Mathews JA. Biofuels: What a Biopact between North and South could achieve. Energy Policy. 2007;35:3550–3570. DOI:10.1016/j.enpol.2007.02.011.

- Thamsiriroj T, Murphy JD. Is it better to import palm oil from Thailand to produce biodiesel in Ireland than to produce biodiesel from indigenous Irish rape seed ? Appl Energy. 2009;86:595–604. DOI:10.1016/j.apenergy.2008.07.010.

- Lamers P, Hamelinck C, Junginger M, et al. International bioenergy trade—A review of past developments in the liquid biofuel market. Renew Sustain Energy Rev. 2011;15:2655–2676. DOI:10.1016/j.rser.2011.01.022.

- Junginger M, Bolkesjø T, Bradley D, et al. Developments in international bioenergy trade. Biomass Bioenergy. 2008;32:717–729. DOI:10.1016/j.biombioe.2008.01.019.

- BPPT - Badan Pengkajian dan Penerapan Teknologi (Agency for the Assessment and Application of Technology). Indonesia energy outlook 2014. 2014. Available at https://www.bppt.go.id/outlook-energi (accessed 15 June 2016).

- World Bank. Health Nutrition and Population Statistics: Population Estimates and Projections. Popul Estim Proj. 2015; Available at http://data.worldbank.org/data-catalog/population-projection-tables (accessed 24 August 2016).

- Elsevier. Rising demand in cosmetics applications drives oleochemicals market, Focus Surfactants 2, Available from: https://www.sciencedirect.com/journal/focus-on-surfactants/vol/2015/issue/4, Amsterdam, The Netherlands, Elsevier Ltd; 2015.

- REN21 - Renewable Energy Policy Network for the 21st Century. Renewable global status report. 2016.

- DESA/UNSD. United Nations Comtrade database, 2016. 2016. http://comtrade.un.org/data/ (accessed 19 April 2017).

- Papong S, Chom-In T, Noksa-nga S, et al. Life cycle energy efficiency and potentials of biodiesel production from palm oil in Thailand. Energy Policy. 2010;38:226–233. DOI:10.1016/j.enpol.2009.09.009.

- Rincón LE, Valencia MJ, Hernández V, et al. Optimization of the Colombian biodiesel supply chain from oil palm crop based on techno-economical and environmental criteria. Energy Econ. 2015;47:154–167. DOI:10.1016/j.eneco.2014.10.018.

- Queiroz AG, França L, Ponte MX. The life cycle assessment of biodiesel from palm oil (“dendê”) in the Amazon. Biomass Bioenergy. 2012;36:50–59. DOI:10.1016/j.biombioe.2011.10.007.

- Ministry of Agriculture. Statistik Perkebunan Indonesia - Tree crop estate statistics of Indonesia, 2012-2014 KELAPA SAWIT. Jakarta: Palm Oil; 2013.

- Dros JM, Aidenvironment, Accommodating growth: two scenarios for Oil Palm production growth. Amsterdam, The Netherlands: 2003. Available from: http://assets.panda.org/downloads/accommodatinggrowth.pdf .

- Afriyanti D, Kroeze C, Saad A. Indonesia palm oil production without deforestation and peat conversion by 2050. Sci Total Environ. 2016;557-558:562–570. DOI:10.1016/j.scitotenv.2016.03.032.

- Hoffmann MP, Castaneda Vera A, van Wijk MT, et al. Simulating potential growth and yield of oil palm (Elaeis guineensis) with PALMSIM: Model description, evaluation and application. Agric Syst. 2014;131:1–10. DOI:10.1016/j.agsy.2014.07.006.

- Donough C, Witt C, Fairhurst T. Yield Intensification in Oil Palm Plantations. Better Crop. 2009;93:12–14.

- Global Agriculture Information Network (GAIN) - USDA Foreign Agricultural Service. Indonesia: oilseeds and products annual 2014, United States Department of Agriculture (USDA). 2014.

- Fairhurst T, Griffiths W, Donough C, et al. Identification and elimination of yield gaps in oil palm plantations in Indonesia. In: Agro 2010 XIth ESA Congr. Montpellier, France: 2010. pp. 343–344. http://edepot.wur.nl/171498 (accessed 10 October 2016).

- Keson J, Wongsai S. Is Oil Palm agriculture expansion really restricted to pre-existing Cropland? 33rd Asian Conf. Remote Sens. 2012; http://a-a-r-s.org/acrs/index.php/acrs/acrs-overview/proceedings-1?view=publication&task=show&id=441 (accessed 24 August 2016).

- Harahap F, Silveira S, Khatiwada D. Land allocation to meet sectoral goals in Indonesia—An analysis of policy coherence. Land Use Policy. 2017;61:451–465.

- Witcover J, Yeh S, Sperling D. Policy options to address global land use change from biofuels. Energy Policy. 2013;56:63–74. DOI:10.1016/j.enpol.2012.08.030.

- Lewandowski I. Securing a sustainable biomass supply in a growing bioeconomy. Glob Food Sec. 2015;6:34–42. DOI:10.1016/j.gfs.2015.10.001.

- Padula AD, Santos MS, Ferreira L, et al. The emergence of the biodiesel industry in Brazil: Current figures and future prospects. Energy Policy. 2012;44:395–405. DOI:10.1016/j.enpol.2012.02.003.

- USDA, FAS - United States Department of Agriculture, Foreign Agricultural Service. Commodity intelligence report. Malaysia: Stagnating Palm Oil Yields Impede Growth; December 2012. Available at http://www.pecad.fas.usda.gov/highlights/2012/12/Malaysia/ (accessed 24 August 2016).

- International Finance Corporation. Diagnostic Study on Indonesian Oil Palm Smallholders. 2013. Available at http://www.aidenvironment.org/media/uploads/documents/201309_IFC2013_Diagnostic_Study_on_Indonesian_Palm_Oil_Smallholders.pdf (accessed 20 December 2016).

- Feintrenie L, Chong WK, Levang P. Why do Farmers Prefer Oil Palm ? Lessons Learnt Bungo District, Indonesia, Small-Scale For. 2010;9:379–396. DOI:10.1007/s11842-010-9122-2.

- Harvey M, Pilgrim S. The new competition for land: Food, energy, and climate change. Food Policy. 2011;36:S40–S51. DOI:10.1016/j.foodpol.2010.11.009.

- Tan KT, Lee KT, Mohamed AR, et al. Palm oil: Addressing issues and towards sustainable development. Renewable Sustainable Energy Rev. 2009;13:420–427. DOI:10.1016/j.rser.2007.10.001.

- Pauli N, Donough T, Oberthür T, et al. Changes in soil quality indicators under oil palm plantations following application of ‘best management practices’ in a four-year field trial. Agriculture, Ecosyst Environ. 2014;195:98–111. https://doi.org/10.1016/j.agee.2014.05.005.

- de Araújo CDM, de Andrade CC, Silva ES, et al. Biodiesel production from used cooking oil: A review. Renewable Sustainable Energy Rev. 2013;27:445–452.

- Jiang Y, Zhang Y. Supply chain optimization of biodiesel produced from waste cooking oil. Transport Res Procedia. 2016;12:938–949.

- Zhang H, Ozturk UA, Wang Q, et al. Biodiesel produced by waste cooking oil: Review of recycling modes in China, the US and Japan. Renewable Sustainable Energy Rev. 2014;38:677–685.

- Sheinbaum-Pardo C, Caldero´n-Irazoque A, Ramı´rez-Sua´rez R. Potential of biodiesel from waste cooking oil in Mexico. Biomass Bioenergy. 2013;56:230–238.

- World Population Review. 2018. Available at: http://worldpopulationreview.com/countries/indonesia-population/ (Accessed 1 March 2018).

- Fargione J, Hill J, Tilman D, et al. Land clearing and the biofuel carbon debt. Science. 2008;319:1235–1238.

- Searchinger T, et al. Use of U.S. croplands for biofuels increases greenhouse gases through emissions from land-use change. Science. 2008;319:1238–1240.

- Finkbeiner M. Indirect land use change – Help beyond the hype ? Biomass Bioenergy. 2014;62:218–221. https://doi.org/10.1016/j.biombioe.2014.01.024.

- Wightman JL, Duxbury JM, Woodbury, PB. Land quality and management practices strongly affect greenhouse gas emissions of bioenergy feedstocks. Bioenergy Research. 2015;8:1681–1690. DOI 10.1007/s12155-015-9620-3.

- Bessou C, Chase LDC, Henson IE, et al. Pilot application of PalmGHG, the Roundtable on Sustainable Palm Oil greenhouse gas calculator for oil palm products. J Cleaner Prod. 2014;73:136–145. https://doi.org/10.1016/j.jclepro.2013.12.008.

- Saswattecha K, Kroeze C, Jawjit W, et al. Assessing the environmental impact of palm oil produced in Thailand. J Cleaner Prod. 2015;100:150–169. https://doi.org/10.1016/j.jclepro.2015.03.037.

- Silalertruksa T, Gheewala SH. Environmental sustainability assessment of palm biodiesel production in Thailand. Energy. 2012;43:306–314. DOI:10.1016/j.energy.2012.04.025.

- de Carvalho CM. Palm oil expansion on degraded land for biodiesel production: a case study in Pará state, Brazil. Biofuels. 2013;4(5):485–492.

- Johansson DJA, Azar C. A scenario based analysis of land competition between food and bioenergy production in the US. Clim Change. 2007;82:267–291. DOI 10.1007/s10584-006-9208-1.

- Oladosu G, Msangi S. Biofuel-food market interactions: a review of modeling approaches and findings. Agriculture. 2013;3:53–71. DOI:10.3390/agriculture3010053.

- Drabik D, Just DR, Timilsina GR. The economics of Brazil's Ethanol-Sugar markets, mandates, and tax exemptions. Am J Agricultural Econ. 2014;97:1433–1450. DOI: 10.1093/ajae/aau109.

- Das S, Priess JA, Schweitzer C. Modelling regional scale biofuel scenarios – a case study for India. GCB Bioenergy. 2012;4:176–192. DOI: 10.1111/j.1757-1707.2011.01114.x.

- Chakravorty U, Hubert MH, Moreaux M. Land allocation between food and energy. Front Econ China. 2014;9:52–69. DOI: 10.3868/s060-003-014-0004-8.

- Chen X, Huang H, Khanna M, et al., Meeting the mandate for biofuels: implications for land use, food, and fuel prices. Chicago, USA: The Intended and Unintended Effects of U.S. Agricultural and Biotechnology Policies. University of Chicago Press; 2012.

- To H, Grafton RQ. Oil prices, biofuels production and food security: past trends and future challenges. Food Sec. 2015;7:323–336. DOI 10.1007/s12571-015-0438-9.

- Plevin RJ, O'Hare M, Jones AD, et al. Greenhouse gas emissions from biofuels’ indirect land use change are uncertain but may be much greater than previously estimated environ. Sci Technol. 2010;44:8015–8021. DOI: 10.1021/es101946t.

- Khanna M, Crago CL, Black M. Can biofuels be a solution to climate change? The implications of land use change-related emissions for policy. Interface Focus. 2011;1:233–247. DOI:10.1098/rsfs.2010.0016.

Appendix

Table A1. Future projections of Indonesian total diesel-type energy demand, expressed in billion liters of fossil diesel energy equivalents.

Table A2. Data used for calculation of energy demand and crude palm oil (CPO) conversion into palm oil biodiesel.