ABSTRACT

This paper presents a literature review on models for assessing corporate sustainability. The review encompasses 68 papers that were published in indexed peer-reviewed journals from 1990 to 2019, which were available on Web of ScienceTM in May 2020. The goal of this study is to evaluate how corporate sustainability is being evaluated in different sectors. We concluded that there is still no consensus among researchers from different areas regarding what corporate sustainability means and different indicators have been used to assess it. The biggest problem is that in various cases the sustainability tripod is not considered. Our study recommends a set of relevant indicators to be adopted for assessing corporate sustainability considering a four-dimensional perspective. The recommendation is based on the number of times these indicators were applied in the reviewed models, and it can be useful for different types of organisations and/or sectors. For future work, we suggest improving this review to include other databases and consequently other relevant publications, to analyse the operators used to aggregate the uni-dimensional information, and then to propose a general four-dimensional index for corporate sustainability assessment, based on a non-compensatory aggregation operator, which can be applied to evaluate different types of companies.

1. INTRODUCTION

Every year, we observe an increasing number of sustainable consumers who incorporate sustainability issues in their buying decisions. Moreover, these new class of consumers desire that besides shareholders’ gains, the value generated by organisations should have a positive impact for the environment and society. As a consequence of this new consumer behaviour, investors are looking for corporations that have been adopting sustainability practices in their processes and policies. Corporate sustainability involves applying systematic efforts in the organisation’s strategy aiming to reduce negative environmental and social impacts resulting from its processes (Hepper et al. Citation2017). It includes to meet the needs of its stakeholders (shareholders, employees, customers, pressure groups, communities, others) without compromising its ability to meet the needs of future generation. For this, companies need to maintain their economic, social and environmental capital base, actively contributing to sustainability in the political domain (Dyllick and Hockerts Citation2002).

Models for evaluating corporate sustainability have become necessary. In the last years, different non-profit organisations worldwide have been applied efforts to evaluate sustainability of companies in different segments and regions. One of the most important initiative is the Global Reporting Initiative (GRI) (Garcia et al. Citation2016) that is produced by an independent international organisation, aiming to create a global common language for organisations to report their impacts. Other important initiative is the Dow Jones Sustainability Index (DJSI) that aims to evaluate various publicly traded companies. A similar model named Corporate Sustainability Index was developed to evaluate companies listed in the São Paulo Stock Exchange (BM&FBOVESPA). In Brazil, there are also the indicators proposed by Ethos Institute, which is a civil society organisation, whose goal is to support private companies to manage their businesses adopting sustainability principles.

Organizations can measure corporate sustainability using models proposed by specialised agencies (GRI, DJSI, etc.) or they can develop their own models (Antolín-López, Delgado-Ceballos, and Montiel Citation2016). As a consequence, many models for assessing corporate sustainability have been proposed in the specialised literature (scientific papers and books). Most of them are based on the Triple Bottom Line (TBL) concept. The TBL is a business concept, proposed by Elkington (Citation1999) that establishes that business performance should be founded on three pillars: economic (organisation’s financial success and resilience), environmental (environmental health), and social (social well-being). This concept expands the knowledge of company’s stakeholders, showing them, beyond traditional and financial aspects, the impact of the business in the world around it (Arowoshegbe and Emmanuel Citation2016). Some examples of models that consider the TBL concept are: Kubule and Blumberga (Citation2019); Liern and Pérez-Gladish (Citation2018); Vivas et al. (Citation2019); Wang and Lin (Citation2007). However, there are models in which the meaning of sustainability is wider, while in others is more restrict, in some cases considering only one perspective. Antolín-López, Delgado-Ceballos, and Montiel (Citation2016) pointed out that studies are necessary to investigate which aspects are relevant to assess and to disclose impacts of corporate sustainability activities.

Feil, de Quevedo, and Schreiber (Citation2015) affirm that models for assessing corporate sustainability have aroused notable interest from academics and business managers. The investigation of these models contributes to improve the quality of indicators, aiming to provide more appropriate answers to society’s desires (Silva, Freire, and Silva Citation2014). Morioka et al. (Citation2018) add that there is a demand for studies on the development, implementation and improvement of tools that integrate the logic of sustainability and business management. Some researches aim to analyse and compare these models: A. Feil et al. (Citation2019); Feil and Schreiber (Citation2017); Morioka et al. (Citation2018); Silva, Freire, and Silva (Citation2014).

We observe that the concept sustainability can have different meanings according to the context in which it is being used; in this sense, we believe that, according to the semantic value that is being considered, a same company can have different level of performance in terms of corporate sustainability. Consequently, a sustainability index might not reflect what actually happens in practice; and, in some cases, the misinformation can be used to mislead society and investors. We need to understand what is behind a corporate sustainability index and how reliable this information seems to be. In this sense, the goal of this paper is to perform a literature review on models for assessing corporate sustainability that were published in peer-reviewed indexed journals in the last two decades, aiming to identify dimensions and main indicators used for assessing corporate sustainability, the sources of information used for evaluation of companies, and the sectors for which this type of evaluation have been applied. The paper is organised into four sections: Section 2 presents the methodological procedures; Section 3 shows the analysis of the papers; Section 4 presents the discussion of the results; and Section 5 presents the conclusions.

2. RESEARCH METHODOLOGY

This paper presents a literature review on models for assessing corporate sustainability. The review encompasses 68 articles that were published in peer-reviewed journals between 2002 and 2019. The review follows the four-step iterative process described in Seuring and Müller (Citation2008): (i) material collection, which includes the definition and delimitation of the materials to be analysed; (ii) descriptive analysis, which presents the distribution of papers over the years, journals with the highest number of publications, and main authors on this topic; (iii) category selection, in which we identified the structural dimensions and analytical categories to evaluate the papers; and (iv) material analysis based on the proposed evaluation framework. shows the review process.

Figure 1. The flowchart of the review process

2.1. Material Collection

The material collection starts with the definition of keywords and other search parameters (languages, period, type of document, etc.). Creswell and Creswell (Citation2017) recommend starting the search on peer-reviewed journals available in computerised databases. We used the Web of ScienceTM Core Collection because it is the world’s leading scientific research and analytical information platform (Li, Rollins, and Yan Li, et al., Citation2018); it offers multidisciplinary services and has a common navigation environment, data structure and search language (Birkle et al. Citation2020). The review was performed in May 2020 using the Web of ScienceTM Core Collection database. shows the parameters used in the search.

Table 1. Parameters of the search in the Web of Science™

The search returned 1,239 papers that were submitted to a preliminary analysis, by reading the title, keywords, and abstract. After that, 844 papers were removed resulting in 395 articles that were read in full. Then, we established a set of criteria for inclusion or exclusion of papers: they should present a new model for assessing corporate sustainability or apply an existing model; assessing corporate sustainability means measuring the performance of organisations and/or the performance of sustainable production practices or processes. Three hundred and twenty-seven papers that did not meet the set of criteria were removed from the base, resulting in 68 papers.

2.2. Category selection

This step includes the definition of structural dimensions and analytical categories used to evaluate the papers. Structural dimensions are the main topics of analysis and they are composed by analytical categories Seuring and Müller (Citation2008).

For supporting this step, we used the software NVivo. As we read the papers papers, dimensions and their respective analytical categories were identified. Then, NVivo was used to encode and organise these categories into a hierarchy structure. For each encoded fragment of text, NVivo creates a nod (or a hierarchy of nodes) that is a structure to store information gathered from the papers. The meaning of the nodes depends on the methodological approach used (Lage Citation2010). In our study, we used the content analysis approach and the hierarchy of nodes represents categories of information, that is, the dimensions (1st level) and their respective categories (2nd level). This tree node structure is the framework used to analyse the papers (). This framework allows us to identify the dimensions and main indicators used in the models for assessing sustainability, the sources used for assessing the indicators, the sectors for which the indicators are being proposed/applied. As the papers we read, NVivo addressed each segment of the text to the proper category in the framework.

Table 2. Category analysis

3. ANALYSIS

The goal of the analysis is to understand the strengths and weaknesses of the research, and also to identify research gaps that deserve more attention (Leonidou et al. Citation2020). In the descriptive analysis step, we extract characteristics of interest from each study: distribution of papers over the years, the main journals in which they were published and the more productive authors. In the qualitative analysis, we tried to identify relationships among the papers.

3.1. Distribution of the papers per year, journals and authors

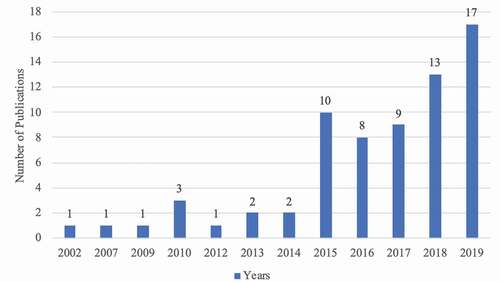

Although our review encompasses the period 1990–2019, the first paper was published in 2002 and it proposes a model for measuring the progress of institutions based on Agenda 21 (Spangenberg Citation2002). presents the evolution of the papers over the years, from 2002 to 2019.

Figure 2. Distribution of the papers per year

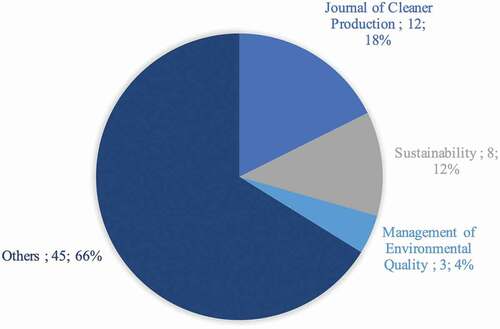

In 2015, the world confirmed its commitment to the 2030 Agenda for Sustainable Development, which is an action programmefor people, the planet and prosperity with the aim of improving the quality of life (Hristov and Chirico Citation2019). This can explain the increasing in the number of publications in the last 5 years: ~70% of the publications are concentrated between 2015 and 2019 (average of 9,6 articles per year). The papers were distributed into 34 different journals. Only 3 journals have more than 2 publications on this topic: Journal of Cleaner Production (12 papers, ~18%), the Sustainability Journal (8 papers, ~12%), and the Management of Environmental Quality (3 papers, ~4%). presents the journals with the highest volume of publications.

Figure 3. Distribution of the papers per journals

In 2015, the world confirmed its commitment to the 2030 Agenda for Sustainable Development, which is an action programme for people, the planet and prosperity with the aim of improving the quality of life (Hristov and Chirico Citation2019). This can explain the increasing number of publications in the last 5 years – ~70% of the publications are concentrated between 2015 and 2019 (average of 9,6 articles per year).

The papers were distributed into 34 different journals. Only 3 journals have more than 2 publications on this topic (): Journal of Cleaner Production (12 papers, ~18%), the Sustainability Journal (8 papers, ~12%), and the Management of Environmental Quality (3 papers, ~4%).

The sample contains 205 different authors: 95% (194 authors) published only one paper; 3% (7 authors) published two papers; 2% (4 authors) published more than three. Based on the number of publications, the main authors are as follows: Goran Svensson from Norway; Carmen Padin from Spain; Beverly Wagner from Scotland; and Lu Wang from Beijing/China, who investigates metal-organic structures. Goran Svensson’s main interest topics are corporate sustainability, ethics, marketing, supply chain, and service management. In his six papers, which are produced in collaboration with other authors, including Carmen Padin and Beverly Wagner, the authors explore sustainable business practices based on the TBL concept (Dos Santos, Svensson, and Padin (Citation2013); Høgevold et al. (Citation2015); Høgevold et al. (Citation2019); Laurell et al. (Citation2019); Svensson et al. (Citation2016); Svensson and Wagner (Citation2015). Lu Wang’s research area is metal-organic structures, but he also has research on models for assessing corporate sustainability considering the TBL concept (Wang, Wang, and Dai (Citation2018); Wang and Lin (Citation2007); Wang et al. (Citation2018).

3.2. Sustainability dimensions

In 66% of the cases (45 papers), corporate sustainability is evaluated considering the TBL concepts, that is, economic, environmental, and social dimensions simultaneously. Madan Shankar, Kannan, and Udhaya Kumar (Citation2017) considered the TBL, but the social dimension was modelled adopting a perspective that is focused on healthy and safety of individuals. Instead of using the term social, they named the third dimension as employee safety, encompassing issues such as training and education programmes, use of personal protective equipment, etc. Hussain, Alameeri, and Ajmal (Citation2017) extend the focus on healthy and safety to corporate’s customers.

In addition to TBL, some studies consider an extra dimension that encompasses issues on ethics, strategies, business policies, relationship with stakeholders: Aras et al. (Citation2017); Schrippe and Ribeiro (Citation2019); Wang, Wang, and Dai (Citation2018). This fourth dimension has been called by its authors governance, corporate governance, corporate sustainability. K. E., V. S., and Gurumurthy (Citation2018) added a dimension called business, for dealing with conflict management and organisation image. And Loor Alcívar et al. (Citation2020) added a fourth dimension named corporate identity, which focuses on the company’s vision and mission. Despite the different nomenclature the dimensions also evaluate one or more aspects of governance, which encompasses every sphere of management. Governance was also considered in the study by Bonsón and Bednárová (Citation2015) and Muñoz-Torres et al. (Citation2019). However, in the former, the environmental dimension was suppressed, and only economic and social aspects were considered in combination with governance issues. While in the second study, the authors suppressed the economic dimension, remaining environmental, social and governance dimensions.

Some studies considered only environmental and social dimensions simultaneously: Amor-Esteban, Galindo-Villardón, and García-Sánchez (Citation2019); Cowper-Smith and de Grosbois (Citation2011); Esteban, Villardón, and Sánchez (Citation2017); Nikolaou, Tsalis, and Evangelinos (Citation2019). Others studies evaluated sustainability considering a single perspective: Regarding the environmental dimensions, we identified the following studies: Cubilla-Montilla et al. (Citation2020); Nallusamy et al. (Citation2015); Silva, Freire, and Silva (Citation2014). As for social dimension, we identified the following studies: Ajmal et al. (Citation2018); Hutchins et al. (Citation2019); Paredes-Gazquez, Rodriguez-Fernandez, and de La Cuesta-gonzalez (Citation2016). Staniškienė and Stankevičiūtė (Citation2018) evaluated the social dimension over a perspective of relationship with employees, including employee participation, cooperation, equal opportunities, employee development, health and safety, and partnership. Spangenberg (Citation2002) evaluated corporate sustainability considering a governance perspective, based on the idea that organisations have a structure guided by implicit and explicit internal rules. Deng et al. (Citation2018) and Lu et al. (Citation2016) proposed an evaluation of corporate sustainability considering the perspective focused on governance aspects (learning and growth, internal processes, customers and finance) without care about what happens beyond its boundaries; the indicators focus on maintaining and increasing economic performance; some of the criteria are as follows: employee productivity, increasing management efficiency, corporate image, etc.

Roca and Searcy (Citation2012) and Rowley, Geschke, and Lenzen (Citation2015) did not present the dimensions that they use for evaluation of corporate sustainability.

3.2.1. Input sources

In 43% of the cases (29 papers), sustainability indicators adopted in these studies were obtained from the specialised literature. In 29% (20 papers), authors used indicators obtained from corporate sustainability reports published by companies and specialised agencies, such as Global Reporting Initiative (GRI), Dow Jones Sustainability Index (DJSI), Corporate Sustainability Index from BM&FBOVESPA, etc. Most of them (~74%) adopted GRI indicators. The following studies adopted exclusively GRI indicators: Ahmad, Wong, and Rajoo (Citation2019); Ajmal et al. (Citation2018); Baumgartner and Ebner (Citation2010); Cubilla-Montilla et al. (Citation2020); de Campos and Simon (Citation2019); Garcia et al. (Citation2016); Gómez-Navarro et al. (Citation2018); Infante et al. (Citation2013); Lenort et al. (Citation2017); Rai (Citation2015); Silva, Freire, and Silva (Citation2014). Beyond GRI, Cowper-Smith and de Grosbois (Citation2011) adopted indicators provided by the United Nations Environmental Program and the World Tourism Organization, which is an agency associated with the United Nations that seeks to promote sustainable tourism. Amoako, Lord, and Dixon (Citation2017) adopted GRI and reports from the United Nations Division of Sustainable Development (UNDSD). Finally, Roca and Searcy (Citation2012) adopted GRI and sustainability reports from Canadian companies. Alternatively to the GRI, Bonsón and Bednárová (Citation2015) adopted a set of non-financial indicators provided by AECA (acronym in Spanish to Asociación Española de Contabilidad y Administración de Empresas) for evaluation of Eurozone’s companies. The AECA’s non-financial (NI) indicators aim to reduce the lack of balance between the indicators evidenced by other structures, such as the GRI, which focuses on governance guidelines. Still in the European ambit, Escamilla-Solano (Citation2019) adopted reports from different companies and indicators provides by the European Commission, which is a European institution for promoting economic, political, and social cooperation and integration.

Indicators provided by two Brazilian organisations were also applied: Schrippe and Ribeiro (Citation2019) adopted the Corporate Sustainability Index proposed by the São Paulo Stock Exchange (BM&FBOVESPA); and Sarango-Lalangui, Álvarez-García, and Del Río-rama (Citation2018) adopted Indicators of the Ethos Institute. Ocampo, Clark, and Promentilla (Citation2016) were based on the Sustainable Manufacturing Indicator Repository (SMIR) which provides different databases and indicators categorised by topics to measure their sustainability performance. Dos Dos Santos, Svensson, and Padin (Citation2013) evaluated the sustainability of a retail chain and adopted indicators collected from annual reports produced by the company itself. In some cases (9% of the papers), authors used studies published in the specialised literature combined with corporate sustainability reports: GRI, United Nations Environment Program Financial Initiative (UNEP-FI), and Association of Chartered Certified Accountants (ACCA) (Aras et al. Citation2017); and GRI (Hourneaux, Gabriel, and Gallardo-Vázquez Citation2018; Hubbard Citation2009; Reis, Jacomossi, and Casagrande Citation2015; Wang et al. Citation2015).

In 10% of the cases (7 papers), sustainability indicators were proposed based on judgement of specialists (academics, managers and other employees qualified and/or experienced in a particular area of knowledge) collected through interviews, workshop, questionnaire, etc.: Buys et al. (Citation2014); Da Silva Batista and de Francisco (Citation2018); Hutchins et al. (Citation2019); Kolk, Hong, and van Dolen (Citation2008); Laurell et al. (Citation2019); Nara et al. (Citation2019); Staniškienė and Stankevičiūtė (Citation2018). Some studies (4% of the cases) adopted judgement of specialists combined with corporate sustainability reports (Muñoz-Torres et al. Citation2019; Rowley, Geschke, and Lenzen Citation2015; Wang and Lin Citation2007). Other studies (3%) adopted judgement of specialists combined with specialised literature sources (Deng et al. Citation2018; Lucato, Da Silva Santos, and Tadeu Pacchini Citation2017). Antolín-López, Delgado-Ceballos, and Montiel (Citation2016) and Oliveira, Zanella, and Camanho (Citation2019) were based on specialised literature, corporate sustainability reports (GRI, DJSI, etc.), and international standards (ISO 26000), which deals with social responsibility and aims to help organisations to incorporate social and environmental practices.

3.2.2. Sustainability indicators

Five hundred and eighty-three indicators were identified and grouped into four analytical categories: economic, social, environmental, and other. Secondly, we combined indicators that evaluate the same aspect, even when they have different nomenclatures. Then, we selected relevant aspects and provided a description for them; each description encompasses all indicators that were aggregated in it. The criterion used to determine the relevance of aspects is the number of times they were applied in the reviewed papers.

The economic dimension of TBL is focused on the economic value generated by the company and on the organisation’s contribution to the economy (Elkington Citation1999). This dimension comprises 93 sub-indicators and the most relevant isare as follows: Profit, Cost, Revenue, Expense, Economy, Investment, and other economic values. shows these criteria.

Table 3. Indicators based on the economic dimension of the Triple Bottom Line

The social dimension of TBL includes conducting beneficial and fair practices for employees, human capital and the community (Elkington Citation1999). This dimension grouped 174 sub-indicators and the most relevants are as follows: Employees, Community, Health and safety, Human capital, Human rights, and Diversity and social equity. shows these criteria.

Table 4. Indicators based on the social dimension of the Triple Bottom Line

The environmental dimension of TBL involves efficient use of administrative resources not to compromise future generations (Elkington Citation1999). This category gathered 113 sub-indicators and the most relevant are as follows: Biodiversity, Environmental management system, Emissions, Water, Energy, and Waste. shows these criteria.

Table 5. Indicators based on the environmental dimension of the Triple Bottom Line

The governance dimension encompasses every sphere of management, from company’s objectives, to action plans and internal controls, performance measurement, corporate disclosure, and relationship with its various stakeholders (shareholders, employees, customers, suppliers, financiers, the government, and the community). This group comprises 203 sub-indicators and the most relevant are: Governance, Internal process, Customer, Compliance with legislation, Ethics and anti-corruption, Communication, Policy, Strategy, Supply chain, Company and Product. shows these criteria.

Table 6. Governance dimension indicators

3.2.3. Sector

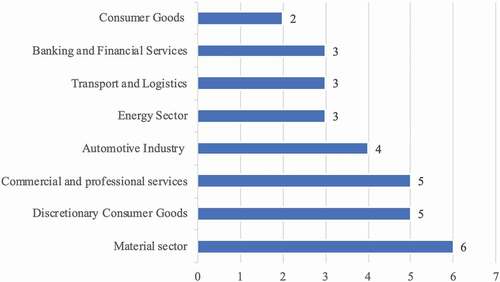

In 46% of cases (31 papers), the studies were intended to only one sector: Materials Sector (Ahmad, Wong, and Rajoo Citation2019; Amoako, Lord, and Dixon Citation2017; Braccini and Margherita Citation2018; Lenort et al. Citation2017; Ocampo, Clark, and Promentilla Citation2016; Oliveira, Zanella, and Camanho Citation2019); Energy Sector (Garcia et al. Citation2016; Infante et al. Citation2013; Paredes-Gazquez, Rodriguez-Fernandez, and de La Cuesta-gonzalez Citation2016); Energy Sector (Cowper-Smith and de Grosbois Citation2011; Karaman and Akman Citation2018; Thabrew et al. Citation2018); Transport and Logistics (Hilsdorf, de Mattos, and de Campos Maciel Citation2017; Hussain, Alameeri, and Ajmal Citation2017; Nallusamy et al. Citation2015; Wang et al. Citation2015); Discretionary Consumer Goods (Charmondusit, Phatarachaisakul, and Prasertpong Citation2014; Feil, de Quevedo, and Schreiber Citation2015; Huang and Badurdeen Citation2017; Lu et al. Citation2016; Madan Shankar, Kannan, and Udhaya Kumar Citation2017); Consumer Goods (Buys et al. Citation2014; Nara et al. Citation2019); Banking and Financial Services (Aras et al. Citation2017; Escamilla-Solano Citation2019; Rai Citation2015); Commercial and Professional Services (Deng et al. Citation2018; Gómez-Navarro et al. Citation2018; Muñoz-Torres et al. Citation2019; Wang, Wang, and Dai Citation2018; Zahid and Ghazali Citation2015). shows the distribution of studies in this group based on the sectors evaluated.

Figure 4. Distribution of studies based on the sectors evaluated

Other studies (16% or 11 papers) were concerned with evaluation of sustainability of companies from different sectors: Energy Sector and Materials Sector (Silva, Freire, and Silva Citation2014); Banking and Financial Services, Healthcare, Energy Sector, etc. (Amor-Esteban, Galindo-Villardón, and García-Sánchez Citation2019); Materials Sector and Discretionary Consumer Goods (Froehlich and Bitencourt Citation2016); Banking and Financial Services, Energy Sector, Materials sector, etc. (Reis, Jacomossi, and Casagrande Citation2015); Healthcare, Consumer Goods, Materials Sector, among others (Rowley, Geschke, and Lenzen Citation2015); Commercial and Professional Services and Consumer Goods (Oginni and Omojowo Citation2016); Automotive Industry, Banking and Financial Services, Consumer Goods, Healthcare, Materials Sector, Commercial and Professional Services, etc. (Bonsón and Bednárová Citation2015); Materials Sector, Energy Sector, Banking and Financial Services, Capital Goods, etc. (Roca and Searcy Citation2012); Energy Sector, Transport and Logistics, etc. (Schrippe and Ribeiro Citation2019); Discretionary Consumer Good, Consumer Goods, Commercial and Professional Services, etc. (Svensson and Wagner Citation2015); Commercial and Professional Services, Capital Goods, etc. (Svensson et al. Citation2016).

The rest of the studies, 38% of the sample (26 papers) do not show the sector.

3.2.4. Category analysis

presents a summary of the category analysis.

Table 7. Summary of the category analysis

4. DISCUSSION

Since 2015, Assessing corporate sustainability has gained increasing attention from academics. We believe that this is a consequence of the 2030 Agenda for Sustainable Development that was launched in 2015: around 70% of publications concentrated in the last 5 years. These papers are widely distributed in 34 peer review journals that encompasses issues on Operations Research Management Science, Business Economics, Engineering, Environmental Science Ecology, Scientific Technology, Development Studies, Biodiversity Conservation, and other topics, indicating that the topic is being addressed over different perspectives.

Nonetheless, this research topic is still incipient and as well as the concept corporate sustainability. In the reviewed papers, we observed that the semantic meaning of corporate sustainability were constructed in different ways; in most of cases, this concept is founded on the tripod economic-social-environmental. However, in almost 10% of cases, sustainability concept does not consider the sustainability tripod, and in some cases only one dimension was considered, which means the meaning of sustainability is completely misunderstood. Moreover, various studies define corporate sustainability considering aspects of governance, adopting a perspective that observes issues like company’s goals, strategies and action plans, internal controls, ethics, performance measurement, supply chain, relationship with stakeholders, etc. We believe this four-dimensional perspective (economic, social, environmental, and governance) is essential to provide a proper meaning to corporate sustainability.

Different types of information are being used to construct the perspective of each dimension: we identified 583 indicators. Depending on indicators that were adopted to assess the level of corporate sustainability, a same company can have different performance indexes, and both might not reflect what actually happens in practice. it is necessary to calibrate instruments used to assess corporate sustainability, establishing which indicators are relevant to evaluates aspects of sustainability in each dimension, considering also the particularities of sector/segment organisations are inserted to. Moreover, the quality of information used to assess these indicators it is very important to ensure the accuracy of these instruments. Aiming to contribute with this calibration, we suggest a set of indicators that can be used to assess sustainability according to each dimension; the criteria used for selected the indicators was number of times they were applied in the reviewed papers.

Other aspect that important, is the way in which the indicators are aggregated to construct the four-dimensional information that will represent the index of corporate sustainability. It is important to avoid the effect of compensation that some aggregation operators provoke; that is, we should avoid that a poor performance in a given dimension (for example, environmental) can be compensated by for a very good performance in other (for example, economic). This type of trade-off is not acceptable when we are looking for sustainable development. This is a critical issue because most of models for assessing sustainability are based on the additive model, which is a compensatory operator. We encourage for the used of non-compensatory aggregation operators, such as the outranking multi-criteria methods, to ensure a strong concept of sustainability.

Finally, we observed that some studies lacks from foundation on the specialist literature on sustainability. The Bellagio Principles highlight the need to use models with targeted objectives, to adopt a holistic view, to use a simple structure capable of adapting to contingencies, to enable clear and comprehensive communication to support the decision-making of actors – key, etc. (Malheiros, Coutinho, and Philippi Júnior Citation2012). However, in various of the reviewed models, the instruments/metrics for evaluation of indicators are not provided.

5. CONCLUSIONS

This paper presents a literature review on models for assessing corporate sustainability. We searched for papers that were published in indexed peer-reviewed journals from 1990 to 2019, which were available on Web of ScienceTM Core Collection database in May 2020. A total of 68 papers were reviewed in depth according to a set of analytical categories that were organised into four structural dimensions: sustainability dimensions, input sources, sector/areas, sustainability indicators. The first paper was published in 2002, but around 70% of studies were published from 2015 onward, possibly influenced by the United Nations General Assembly that occurred in 2015 and established the 2030 Agenda. The publication are spread across 34 journals that publishes contributions on different areas, indicating that corporate sustainability assesses have been addressed in the literature by academics from different research areas. However, 95% of these authors has only one publication, indicating that the issue is still in a beginning phase.

Indeed, in the qualitative analysis, we observed that there is still no consensus among these researchers regarding what corporate sustainability means. Different indicators have been applied to construct the corporate sustainability concept. These indicators were organised into four dimensions: economic, social, environmental, and governance, which is a dimension that encompasses aspects of management. Most of the models are based on the sustainability tripod, but in various case the Triple Bottom Line was not considered and in some critical case only one dimension was considered to evaluate sustainability. One consequence of this is that a corporate sustainability index associated with a given organisation might not reflect what this organisation does in practice.

It is not possible to assess sustainability without concern with economic, social and environmental aspects, simultaneously. But in case of corporate sustainability the Triple Bottom Line is not enough and aspects of governance should be observers, making the corporate sustainability a four-dimensional concept. Our study recommends a set of relevant indicators to be adopted for assessing corporate sustainability considering a four-dimensional perspective. The recommendation is based on the number of times these indicators were applied in the reviewed models, and it can be useful for different types of organisations and/or sectors.

Besides the information used to construct the corporate sustainability concept, other critical aspect is the way in which this information is aggregated. We should ensure that the used aggregation operator avoid or at least reduce trade off among dimensions. This aspect was not observed in our reviews and it represents the main limitation of our work. Another limitation of this study refers to the use of only one database and some important studies might not be included in our review. For future work, we suggest improving this review to include other databases and consequently other relevant publications, to analyse the operators used to aggregate the uni-dimensional information, and then to propose a general four-dimensional index for corporate sustainability assessment, based on a non-compensatory aggregation operator, which can be applied to evaluate different types of companies.

Acknowledgments

This study was financed in part by the Coordenação de Aperfeiçoamento de Pessoal de Nível Superior – Brasil (CAPES) – Finance Code 001.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes on contributors

Paloma R. S. Bezerra

Paloma: Master in Administration (Federal University of Campina Grande, Brazil). Member of the research groups: DeSiDeS (Development of Support Systems for Sustainable Decisions from Federal University of Campina Grande), and Knowledge Management and Sustainability from the State University of Paraíba, Brazil. Current research interests include: Organizational Studies; Entrepreneurship; and Sustainable development.

Fernando Schramm

Fernando: Associate Professor at Federal University of Campina Grande, Brazil, Head of DeSiDeS (Development of Systems for Supporting Sustainable Decisions). Current research interests include: problem structuring methods; multi-criteria decision making; group decision; negotiation and conflict resolution; data science; and artificial neural networks.

Vanessa B. Schramm

Vanessa: Associate Professor at Federal University of Campina Grande, Brazil, IEEE Senior Member. Head of DeSiDeS (Development of Systems for Supporting Sustainable Decisions). Current research interests include: problem structuring methods; multi-criteria decision making; group decision; negotiation and conflict resolution.

References

- Ahmad, S., K. Y. Wong, and S. Rajoo. 2019. “Sustainability Indicators for Manufacturing Sectors.” Journal of Manufacturing Technology Management 30 (2): 312–334. doi:https://doi.org/10.1108/JMTM-03-2018-0091.

- Ajmal, M. M., M. Khan, M. Hussain, and P. Helo. 2018. “Conceptualizing and Incorporating Social Sustainability in the Business World.” International Journal of Sustainable Development & World Ecology 25 (4): 327–339. doi:https://doi.org/10.1080/13504509.2017.1408714.

- Amoako, K. O., B. R. Lord, and K. Dixon. 2017. “Sustainability Reporting.” Meditari Accountancy Research 25 (2): 186–215. doi:https://doi.org/10.1108/MEDAR-02-2016-0020.

- Amor-Esteban, V., M.-P. Galindo-Villardón, and I.-M. García-Sánchez. 2019. “A Multivariate Proposal for A National Corporate Social Responsibility Practices Index (NCSRPI) for International Settings.” Social Indicators Research 143 (2): 525–560. doi:https://doi.org/10.1007/s11205-018-1997-x.

- Antolín-López, R., J. Delgado-Ceballos, and I. Montiel. 2016. “Deconstructing Corporate Sustainability: A Comparison of Differ- Ent Stakeholder Metrics.” Journal of Cleaner Production 136 (A,SI): 5–17. doi:https://doi.org/10.1016/j.jclepro.2016.01.111.

- Aras, G., N. Tezcan, O. Kutlu Furtuna, and E. Hacioglu Kazak. 2017. “Corporate Sustainability Measurement Based on Entropy Weight and TOPSIS.” Meditari Accountancy Research 25 (3): 391–413. doi:https://doi.org/10.1108/MEDAR-11-2016-0100.

- Arowoshegbe, A. O., and U. Emmanuel. 2016 aug. “Sustainability and Triple Bottom Line: An Overview of Two Interrelated Concepts.” Igbinedion University Journal of Accounting 2:126. Retrieved from https://iuokada.edu.ng/journals/ 9F2F7F6B56B433D.pdf.

- Baumgartner, R. J., and D. Ebner. 2010. “Corporate Sustainability Strategies: Sustainability Profiles and Maturity Levels.” Sustainable Development 18 (2): 76–89. doi:https://doi.org/10.1002/sd.447.

- Birkle, C., D. A. Pendlebury, J. Schnell, and J. Adams. 2020 feb. “Web of Science as a Data Source for Research on Scientific and Scholarly Activity.” Quantitative Science Studies 1 (1): 363–376. doi:https://doi.org/10.1162/qss_a_00018.

- Bonsón, E., and M. Bednárová. 2015. “CSR Reporting Practices of Eurozone Companies.” Revista de Contabilidad 18 (2): 182–193. doi:https://doi.org/10.1016/j.rcsar.2014.06.002.

- Braccini, A., and E. Margherita. 2018. “Exploring Organizational Sustainability of Industry 4.0 Under the Triple Bottom Line: The Case of a Manufacturing Company.” Sustainability 11 (1): 36. doi:https://doi.org/10.3390/su11010036.

- Buys, L., K. Mengersen, S. Johnson, N. van Buuren, and A. Chauvin. 2014. “Creating a Sustainability Scorecard as a Predictive Tool for Measuring the Complex Social, Economic and Environmental Impacts of Industries, a Case Study: Assessing the Viability and Sustainability of the Dairy Industry.” Journal of Environmental Management 133: 184–192. doi:https://doi.org/10.1016/j.jenvman.2013.12.013.

- Charmondusit, K., S. Phatarachaisakul, and P. Prasertpong. 2014. “The Quantitative Eco-efficiency Measurement for Small and Medium Enterprise: A Case Study of Wooden Toy Industry.” Clean Technologies and Environmental Policy 16 (5): 935–945. doi:https://doi.org/10.1007/s10098-013-0693-4.

- Cowper-Smith, A., and D. de Grosbois. 2011. “The Adoption of Corporate Social Responsibility Practices in the Airline Industry.” Journal of Sustainable Tourism 19 (1): 59–77. doi:https://doi.org/10.1080/09669582.2010.498918.

- Creswell, J. W., and J. D. Creswell. 2017. Research Design: Qualitative, Quantitative, and Mixed Methods Approaches (5th ed.). Thousand Oaks, CA: SAGE Publications, Inc. Retrieved from https://us.sagepub.com/en-us/nam/research-design/book255675.

- Cubilla-Montilla, M. I., P. Galindo-Villardón, A. B. Nieto-Librero, M. P. Vicente Galindo, and I. M. García-Sánchez. 2020. “What Companies Do Not Disclose about Their Environmental Policy and What Institutional Pressures May Do to Respect.” Corporate Social Responsibility and Environmental Management 27 (3): 1181–1197. doi:https://doi.org/10.1002/csr.1874.

- Da Silva Batista, A. A., and A. C. de Francisco. 2018. “Organizational Sustainability Practices: A Study of the Firms Listed by the Corporate Sustainability Index.” Sustainability 10 (1): 226. doi:https://doi.org/10.3390/su10010226.

- de Campos, R. S., and A. T. Simon. 2019. “Insertion of Sustainability Concepts in the Maintenance Strategies to Achieve Sustainable Manufacturing.” Independent Journal of Management & Production 10 (6): 1908–1931. doi:https://doi.org/10.14807/ijmp.v10i6.939.

- Deng, D., S. Wen, F.-H. Chen, and S.-L. Lin. 2018. “A Hybrid Multiple Criteria Decision Making Model of Sustainability Performance Evaluation for Taiwanese Certified Public Accountant Firms.” Journal of Cleaner Production 180: 603–616. doi:https://doi.org/10.1016/j.jclepro.2018.01.107.

- Dos Santos, M. A., G. Svensson, and C. Padin. 2013. “Indicators of Sustainable Business Practices: Woolworths in South Africa.” Supply Chain Management: An International Journal 18 (1): 104–108. doi:https://doi.org/10.1108/13598541311293212.

- Dyllick, T., and K. Hockerts. 2002 mar. “Beyond the Business Case for Corporate Sustainability.” Business Strategy and the Environment 11 (2): 130–141. doi:https://doi.org/10.1002/bse.323.

- Elkington, J. 1999. Cannibals with Forks: The Triple Bottom Line of 21st Century Business. Hoboken, NJ: John Wiley and Sons Ltd. 424 978-1841120843. Retrieved from https://www.wiley.com/en-vu/Cannibals+with+Forks%3A+The+Triple+Bottom+Line+of+21st+Century+Business-p-9781841120843

- Escamilla-Solano, F.-P., Paule-Vianez, Plaza-Casado. 2019. “Effect of the Disclosure of Corporate Social Responsibility on Business Profitability. A Dimensional Analysis in the Spanish Stock Market.” Sustainability 11(23):6732. doi:https://doi.org/10.3390/su11236732.

- Esteban, V. A., M. P. G. Villardón, and I. M. G. Sánchez. 2017. “Cultural Values on CSR Patterns and Evolution: A Study from the Biplot Representation.” Ecological Indicators 81: 18–29. doi:https://doi.org/10.1016/j.ecolind.2017.05.051.

- Feil, A. A., D. M. de Quevedo, and D. Schreiber. 2015. “Selection and Identification of the Indicators for Quickly Measuring Sustainability in Micro and Small Furniture Industries.” Sustainable Production and Consumption 3 (September): 34–44. doi:https://doi.org/10.1016/j.spc.2015.08.006.

- Feil, A. A., and D. Schreiber. 2017. “Análise Da Estrutura E Dos Critérios Na Elaboração Do Índice de Sustentabilidade.” Sustentabilidade Em Debate 8 (2): 30–43. doi:https://doi.org/10.18472/SustDeb.v8n2.2017.21516.

- Feil, A., D. Schreiber, C. Haetinger, V. Strasburg, and C. Barkert. 2019. “Sustainability Indicators for Industrial Organizations: Systematic Review of Literature.” Sustainability 11 (3): 854. doi:https://doi.org/10.3390/su11030854.

- Froehlich, C., and C. C. Bitencourt. 2016. “Sustentabilidade Empresarial: Um Estudo de Caso Na Empresa Artecola.” Revista de Gestão Ambiental E Sustentabilidade 5 (3): 55–71. doi:https://doi.org/10.5585/geas.v5i3.332.

- Garcia, S., Y. Cintra, R. D. C. S. Torres, and F. G. Lima. 2016. “Corporate Sustainability Management: A Proposed Multi-criteria Model to Support Balanced Decision-making.” Journal of Cleaner Production 136 (A,SI): 181–196. doi:https://doi.org/10.1016/j.jclepro.2016.01.110.

- Gómez-Navarro, T., M. García-Melón, F. Guijarro, and M. Preuss. 2018. “Methodology to Assess the Market Value of Companies according to Their Financial and Social Responsibility Aspects: An AHP Approach.” Journal of the Operational Research Society 69 (10): 1599–1608. doi:https://doi.org/10.1057/s41274-017-0222-7.

- Hepper, E. L., O. T. de Souza, M. D. C. Petrini, and C. E. L. E. Silva. 2017 jan. “Proposing a Maturity Model for Corporate Sustainability.” Acta Scientiarum. Human and Social Sciences 39 (1): 43–53. doi:https://doi.org/10.4025/actascihumansoc.v39i1.33127.

- Hilsdorf, W. D. C., C. A. de Mattos, and L. O. de Campos Maciel. 2017. “Principles of Sustainability and Practices in the Heavy-duty Vehicle Industry: A Study of Multiple Cases.” Journal of Cleaner Production 141: 1231–1239. doi:https://doi.org/10.1016/j.jclepro.2016.09.186.

- Høgevold, N. M., G. Svensson, H. Klopper, B. Wagner, J. C. S. Valera, C. Padin, and D. Petzer. 2015. “A Triple Bottom Line Construct and Reasons for Implementing Sustainable Business Practices in Companies and Their Business Networks.” Corporate Governance: The International Journal of Business in Society 15 (4): 427–443. doi:https://doi.org/10.1108/CG-11-2014-0134.

- Høgevold, N. M., G. Svensson, R. Rodriguez, and D. Eriksson. 2019. “Relative Importance and Priority of TBL Elements on the Corporate Performance.” Management of Environmental Quality: An International Journal 30 (3): 609–623. doi:https://doi.org/10.1108/MEQ-04-2018-0069.

- Hourneaux, F., Jr, M. L. D. S. Gabriel, and D. A. Gallardo-Vázquez. 2018. “Triple Bottom Line and Sustainable Performance Measurement in Industrial Companies.” Revista de Gestão 25 (4): 413–429. doi:https://doi.org/10.1108/REGE-04-2018-0065.

- Hristov, I., and A. Chirico. 2019. “The Role of Sustainability Key Performance Indicators (Kpis) in Implementing Sustainable Strategies.” Sustainability 11 (20): 5742. doi:https://doi.org/10.3390/su11205742.

- Huang, A., and F. Badurdeen. 2017. “Sustainable Manufacturing Performance Evaluation at the Enterprise Level: Index- and Value-Based Methods.” Smart and Sustainable Manufacturing Systems 1 (1): 20170004. doi:https://doi.org/10.1520/SSMS20170004.

- Hubbard, G. 2009. “Measuring Organizational Performance: Beyond the Triple Bottom Line.” Business Strategy and the Environment 18 (3): 177–191. doi:https://doi.org/10.1002/bse.564.

- Hussain, M., A. Alameeri, and M. M. Ajmal. 2017. “Prioritizing Sustainable Practices of Service Organizations.” International Journal of Information Systems in the Service Sector 9 (1): 22–36. doi:https://doi.org/10.4018/IJISSS.2017010102.

- Hutchins, M. J., J. S. Richter, M. L. Henry, and J. W. Sutherland. 2019. “Development of Indicators for the Social Dimension of Sustainability in a U.S. Business Context.” Journal of Cleaner Production 212: 687–697. doi:https://doi.org/10.1016/j.jclepro.2018.11.199.

- Infante, C. E. D. D. C., F. M. de Mendonça, P. M. Purcidonio, and R. Valle. 2013. “Triple Bottom Line Analysis of Oil and Gas Industry with Multicriteria Decision Making.” Journal of Cleaner Production 52: 289–300. doi:https://doi.org/10.1016/j.jclepro.2013.02.037.

- K. E., K., V. V. S., and A. Gurumurthy. 2018. “Modelling and Analysis of Sustainable Manufacturing System Using a Digraph-based Approach.” International Journal of Sustainable Engineering 11 (6): 397–411. doi:https://doi.org/10.1080/19397038.2017.1420108.

- Karaman, A. S., and E. Akman. 2018. “Taking-off Corporate Social Responsibility Programs: An AHP Application in Airline Industry.” Journal of Air Transport Management 68: 187–197. doi:https://doi.org/10.1016/j.jairtraman.2017.06.012.

- Kolk, A., P. Hong, and W. van Dolen. 2008. “Corporate Social Responsibility in China: An Analysis of Domestic and Foreign Retailers’ Sustainability Dimensions.” Business Strategy and the Environment 19 (5): n/a–n/a. doi:https://doi.org/10.1002/bse.630.

- Kubule, A., and D. Blumberga. 2019. “Sustainability Analysis of Manufacturing Industry.” Environmental and Climate Technologies 23 (3): 159–169. doi:https://doi.org/10.2478/rtuect-2019-0086.

- Lage, M. C. 2010. “Utilização Do Software NVivo Em Pesquisa Qualitativa: Uma Experiência Em EaD.” ETD - Educação Temática Digital 12: 198. doi:https://doi.org/10.20396/etd.v12i0.1210.

- Laurell, H., N. P. Karlsson, J. Lindgren, S. Andersson, and G. Svensson. 2019. “Re-testing and Validating a Triple Bottom Line Dominant Logic for Business Sustainability.” Management of Environmental Quality: An International Journal 30 (3): 518–537. doi:https://doi.org/10.1108/MEQ-02-2018-0024.

- Lenort, R., D. Staš, P. Wicher, D. Holman, and K. Ignatowicz. 2017 . Comparative Study of Sustainable Key Performance Indicators in Metallurgical Industry. Rocznik Ochrona Srodowiska 19: 36–51 . Retrieved from http://ros.edu.pl/index.php?option=com_content&view=article&id=526:studium-porownawcze-wskaznikow-zrownowazonego-rozwoju-w-przemysle-metalurgicznym&catid=45&lang=pl&Itemid=205

- Leonidou, E., M. Christofi, D. Vrontis, and A. Thrassou. 2020. “An Integrative Framework of Stakeholder Engagement for Innovation Management and Entrepreneurship Development.” Journal of Business Research 119: 245–258. doi:https://doi.org/10.1016/J.JBUSRES.2018.11.054. oct.

- Li, K., J. Rollins, and E. Yan. 2018. Web of Science Use in Published Research and Review Papers 1997–2017: A Selective, Dynamic, Cross-domain, Content-based Analysis. Scientometrics 115 (1): 1–20. doi:https://doi.org/10.1007/s11192-017-2622-5

- Liern, V., and B. Pérez-Gladish. 2018. “Ranking Corporate Sustainability: A Flexible Multidimensional Approach Based on Linguistic Variables.” International Transactions in Operational Research 25 (3): 1081–1100. doi:https://doi.org/10.1111/itor.12469.

- Loor Alcívar, M. I., F. González Santa Cruz, N. Y. Moreira Mero, and A. Hidalgo Fernández. 2020. “Analysis of the Relationships between Corporate Social Responsibility and Corporate Sustainability: Empirical Study of Co-operativism in Ecuador.” International Journal of Sustainable Development & World Ecology 27 (4): 322–333. doi:https://doi.org/10.1080/13504509.2019.1706661.

- Lu, I.-Y., T. Kuo, T.-S. Lin, G.-H. Tzeng, and S.-L. Huang. 2016. “Multicriteria Decision Analysis to Develop Effective Sustainable Development Strategies for Enhancing Competitive Advantages: Case of the TFT-LCD Industry in Taiwan.” Sustainability 8 (7): 646. doi:https://doi.org/10.3390/su8070646.

- Lucato, W. C., J. C. Da Silva Santos, and A. P. Tadeu Pacchini. 2017. “Measuring the Sustainability of A Manufacturing Process: A Conceptual Framework.” Sustainability 10 (1): 81. doi:https://doi.org/10.3390/su10010081.

- Madan Shankar, K., D. Kannan, and P. Udhaya Kumar. 2017. “Analyzing Sustainable Manufacturing Practices – A Case Study in Indian Context [Article].” Journal of Cleaner Production 164: 1332–1343. doi:https://doi.org/10.1016/j.jclepro.2017.05.097.

- Malheiros, T. F., S. M. V. Coutinho, and A. Philippi Júnior. 2012. “Indicadores de Sustentabilidade E Gestão Ambiental.” In Indicadores de Sustentabilidade E Gestão Ambiental. Barueri: Manoele.

- Morioka, S. N., D. R. Iritani, A. R. Ometto, and M. M. de Carvalho. 2018. “Revisão Sistemática Da Literatura Sobre Medição de Desempenho de Sustentabilidade Corporativa: Uma Discussão Sobre Contribuições E Lacunas.” Gestão & Produção 25 (2): 284–303. doi:https://doi.org/10.1590/0104-530x2720-18.

- Muñoz-Torres, M. J., M. Á. Fernández-Izquierdo, J. M. Rivera-Lirio, and E. Escrig-Olmedo. 2019. “Can Environmental, Social, and Governance Rating Agencies Favor Business Models that Promote a More Sustainable Development?” Corporate Social Responsibility and Environmental Management 26 (2): 439–452. doi:https://doi.org/10.1002/csr.1695.

- Nallusamy, S., M. Ganesan, K. Balakannan, and C. Shankar. 2015. “Environmental Sustainability Evaluation for an Automobile Manufacturing Industry Using Multi-Grade Fuzzy Approach.” International Journal of Engineering Research in Africa 19: 123–129. doi:https://doi.org/10.4028/JERA.19.123.

- Nara, E. O. B., C. Gelain, J. A. R. Moraes, L. B. Benitez, J. L. Schaefer, and I. C. Baierle. 2019. “Analysis of the Sustainability Reports from Multinationals Tobacco Companies in Southern Brazil.” Journal of Cleaner Production 232: 1093–1102. doi:https://doi.org/10.1016/j.jclepro.2019.05.399.

- Nikolaou, I. E., T. A. Tsalis, and K. I. Evangelinos. 2019. “A Framework to Measure Corporate Sustainability Performance: A Strong Sustainability-based View of Firm.” Sustainable Production and Consumption 18: 1–18. doi:https://doi.org/10.1016/j.spc.2018.10.004.

- Ocampo, L. A., E. E. Clark, and M. A. B. Promentilla. 2016. “Computing Sustainable Manufacturing Index with Fuzzy Analytic Hierarchy Process.” International Journal of Sustainable Engineering 9 (5): 1–10. doi:https://doi.org/10.1080/19397038.2016.1144828.

- Oginni, O., and A. Omojowo. 2016. “Sustainable Development and Corporate Social Responsibility in Sub-Saharan Africa: Evidence from Industries in Cameroon.” Economies 4 (4): 10. doi:https://doi.org/10.3390/economies4020010.

- Oliveira, R., A. Zanella, and A. S. Camanho. 2019. “The Assessment of Corporate Social Responsibility: The Construction of an Industry Ranking and Identification of Potential for Improvement.” European Journal of Operational Research 278 (2): 498–513. doi:https://doi.org/10.1016/j.ejor.2018.11.042.

- Paredes-Gazquez, J. D., J. M. Rodriguez-Fernandez, and M. de La Cuesta-gonzalez. 2016. “Measuring Corporate Social Responsibility Using Composite Indices: Mission Impossible? the Case of the Electricity Utility Industry.” Revista de Contabilidad 19 (1): 142–153. doi:https://doi.org/10.1016/j.rcsar.2015.10.001.

- Rai, A. 2015. “Sustainability Reporting-A Recent Trend and Future Prospects in India.” Pacinc Business Review Internationa 7(8):90–99. Retrieved from http://www.pbr.co.in/2015/2015{_}month/February/12.pdf.

- Reis, L., F. Jacomossi, and R. Casagrande. 2015. “O Isomorfismo Nos Relatórios de Sustentabilidade: Uma Análise Das Empresas Brasileiras Que Compõem O Dow Jones Sustainability INDEX.” Revista de Gestão Ambiental E Sustentabilidade 4 (2): 49–64. doi:https://doi.org/10.5585/geas.v4i2.176.

- Roca, L. C., and C. Searcy. 2012. “An Analysis of Indicators Disclosed in Corporate Sustainability Reports.” Journal of Cleaner Production 20 (1): 103–118. doi:https://doi.org/10.1016/j.jclepro.2011.08.002.

- Rowley, H. V., A. Geschke, and M. Lenzen. 2015. “A Practical Approach for Estimating Weights of Interacting Criteria from Profile Sets.” Fuzzy Sets and Systems 272: 70–88. doi:https://doi.org/10.1016/j.fss.2015.01.011.

- Sarango-Lalangui, P., J. Álvarez-García, and M. Del Río-rama. 2018. “Sustainable Practices in Small and Medium-Sized Enterprises in Ecuador.” Sustainability 10 (6): 2105. doi:https://doi.org/10.3390/su10062105.

- Schrippe, P., and J. L. D. Ribeiro. 2019. “Preponderant Criteria for the Definition of Corporate Sustainability Based on Brazilian Sustainable Companies.” Journal of Cleaner Production 209: 10–19. doi:https://doi.org/10.1016/j.jclepro.2018.10.001.

- Seuring, S., and M. Müller. 2008. “From a Literature Review to a Conceptual Framework for Sustainable Supply Chain Management.” Journal of Cleaner Production 16 (15): 1699–1710. doi:https://doi.org/10.1016/j.jclepro.2008.04.020.

- Silva, E., O. Freire, and F. Silva. 2014. “Indicadores de Sustentabilidade Como Instrumentos de Gestão: Uma Análise Da GRI, Ethos E ISE.” Revista de Gestão Ambiental E Sustentabilidade 3 (2): 130–148. doi:https://doi.org/10.5585/geas.v3i2.130.

- Spangenberg, J. H. 2002. “Institutional Sustainability Indicators: An Analysis of the Institutions in Agenda 21 and a Draft Set of Indicators for Monitoring Their Effectivity.” Sustainable Development 10 (2): 103–115. doi:https://doi.org/10.1002/sd.184.

- Staniškienė, E., and Ž. Stankevičiūtė. 2018. “Social Sustainability Measurement Framework: The Case of Employee Perspective in a CSR-committed Organisation.” Journal of Cleaner Production 188: 708–719. doi:https://doi.org/10.1016/j.jclepro.2018.03.269.

- Svensson, G., and B. Wagner. 2015. “Implementing and Managing Economic, Social and Environmental Efforts of Business Sustainability.” Management of Environmental Quality: An International Journal 26 (2): 195–213. doi:https://doi.org/10.1108/MEQ-09-2013-0099.

- Svensson, G., N. Høgevold, C. Ferro, J. C. S. Varela, C. Padin, and B. Wagner. 2016. “A Triple Bottom Line Dominant Logic for Business Sustainability: Framework and Empirical Findings.” Journal of Business-to-Business Marketing 23 (2): 153–188. doi:https://doi.org/10.1080/1051712X.2016.1169119.

- Thabrew, L., D. Perrone, A. Ewing, M. Abkowitz, and G. Hornberger. 2018. “Using Triple Bottom Line Metrics and Multi- Criteria Methodology in Corporate Settings.” Journal of Environmental Planning and Management 61 (1): 49–63. doi:https://doi.org/10.1080/09640568.2017.1289900.

- Vivas, R., Â. Sant’anna, K. Esquerre, and F. Freires. 2019. “Measuring Sustainability Performance with Multi Criteria Model: A Case Study.” Sustainability 11 (21): 6113. doi:https://doi.org/10.3390/su11216113.

- Wang, C., L. Wang, and S. Dai. 2018. “An Indicator Approach to Industrial Sustainability Assessment: The Case of China’s Capital Economic Circle.” Journal of Cleaner Production 194: 473–482. doi:https://doi.org/10.1016/j.jclepro.2018.05.125.

- Wang, L., and L. Lin. 2007. “A Methodological Framework for the Triple Bottom Line Accounting and Management of Industry Enterprises [Article].” International Journal of Production Research 45 (5): 1063–1088. doi:https://doi.org/10.1080/00207540600635136.

- Wang, L., L. Ma, K.-J. Wu, A. S. Chiu, and S. Nathaphan. 2018. “Applying Fuzzy Interpretive Structural Modeling to Evaluate Responsible Consumption and Production under Uncertainty.” Industrial Management & Data Systems 118 (2): 432–462. doi:https://doi.org/10.1108/IMDS-03-2017-0109.

- Wang, Z., N. Subramanian, A. Gunasekaran, M. D. Abdulrahman, and C. Liu. 2015. “Composite Sustainable Manufacturing Practice and Performance Framework: Chinese Auto-parts Suppliers’ Perspective.” International Journal of Production Economics 170 (A): 219–233. doi:https://doi.org/10.1016/j.ijpe.2015.09.035.

- Zahid, M., and Z. Ghazali. 2015. “Corporate Sustainability Practices among Malaysian REITs and Property Listed Companies.” World Journal of Science, Technology and Sustainable Development 12 (2): 100–118. doi:https://doi.org/10.1108/WJSTSD-02-2015-0008.