ABSTRACT

Green bonds are one of the most prominent innovations in the area of sustainable finance over the past decade. However, to date there have only been a few academic studies on green bonds, and these have tended to focus on what impact green labels have on bond yields. Our analysis is one of the first empirical studies designed to address the broader questions of what attracts investors and issuers to the green bond market, the role of green bonds in shifting capital to more sustainable economic activity, and how green bonds impact the way organisations work with sustainability. Using Sweden as a case study, this paper provides insights into the rapid growth of the green bond market and how green bonds affect market participants’ engagement with sustainability that are easily missed if one focuses only on how green bonds are marketed.

Introduction

One of the most prominent financial innovations in the area of sustainable finance over the past ten years has been the development of green bonds and the growth of the green bond and other ‘labelled bonds’ markets (e.g. sustainability and social bonds). Green bonds tend to be structured in the same way as conventional investment grade bonds, with the exception that that the bond has a ‘use of proceeds’ clause that states that the financing will be used for green investments. This means that unlike ‘vanilla’ bonds that finance the general working capital of the issuer, green bonds should be used for financing or re-financing only green projects or assets. At the same time, the buyer of a green bond will usually have recourse to the issuer’s entire balance sheet, meaning that the investor is not exposed directly to the financial risks of the specific projects the green bond finances (Climate Bonds Initiative Citationn.d.).Footnote1

The World Bank, in cooperation with the Swedish bank SEB, issued the first green bond in 2008 (World Bank Citation2019). Since then the global green bond market has grown from 11 billion USD issued in 2013 and 36 billion USD issued in 2014 (OECD Citation2016) to 167 billion USD issued in 2018 (Climate Bonds Initiative Citation2019). Cumulative issuances up to 2018 are 521 billion USD (Climate Bonds Initiative Citation2019), while the total green bond market is just over one percent of the global bond market (Chasan Citation2019). The green bond market is thus small but growing rapidly. Yet, despite significant growth there has to date been very little academic research on green bonds.

In the finance literature there has been some work examining if the green label makes a difference to bond yields/pricing of green bonds (Ehlers and Packer Citation2017; Baker et al. Citation2018; Zerbib Citation2019). This is a central question but there remain a number of other important questions that need to be addressed if we are to better understand the role of this financial innovation in helping to make our economies more sustainable. What attracts investors and issuers to the green bond market? To what extent is it financial, business-case, or legitimacy/institutional-oriented incentives that explain engagement with the green bonds market? Do participants in the green bond market view green bonds as an important tool for shifting capital from less sustainable to more sustainable investments? What do investors’ and issuers’ reported experience tell us about the role of green bonds in advancing sustainability in practice?

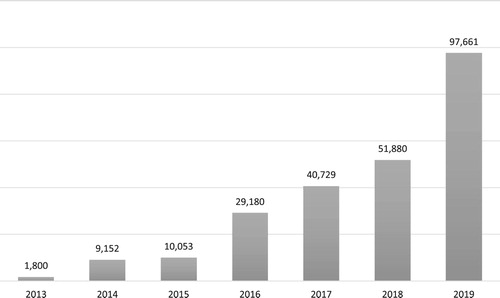

This paper is one of the first empirical academic studies based in interview data to take a broader look at the role of green bonds as an instrument for ‘greening’ the financial sector in pursuit of greener economies. Sweden is selected as a case study because it is widely considered to be a frontrunner in sustainable finance and in the green bond market. In 2018 green bonds accounted for 10% of the total SEK bond market (Danske Bank Citation2019). shows the rapid growth of the green bond market in Sweden since 2013.

Figure 1. Green Bonds Issued in Sweden (million SEK). Source: Graph based on data from Environmental Finance Bond Database (accessed January 28, 2020). https://www.bonddata.org/.

Given similarities in the structure of financial markets, particularly within Europe and North America, there should be an expectation of similar incentive structures driving the growth of green bonds in a number of markets. However, Sweden does represent an interesting case given that it is a recognised leader in the green bond market and given that the level of green bond issuances compared to total issuances is moving green bonds out of a niche asset class and into the mainstream. Sweden thus represents a comparatively mature green bond market and analysing the benefits and limitations of green bonds in the Swedish market can provide insights into the role green bonds may play in regions with still emerging labelled bond markets.

Finance as a site for driving sustainability

The finance sector is increasingly seen as vital for accelerating the transition to sustainability and climate neutrality. One reason is the need to mobilise large amounts of private capital in order to meet the investments needs for achieving the climate targets of the Paris Agreement and the UN Sustainable Development Goals (SDGs) (UNEP Citation2015; Bielenberg et al. Citation2016; IEA Citation2017). Another reason is because of the finance sector’s role in allocating capital efficiently. This makes the finance sector a key arena for impacting what happens in economies broadly all over the world (Hourcade and Shukla Citation2013; Grubb Citation2014).

There are a number of pathways through which finance can be a catalyst for advancing sustainability. These include fiscal and monetary policy, investor concerns about unsustainable business practices leading to stranded assets (McGlade and Ekins Citation2015; Material Economics and SEI Citation2018), investor concerns about climate policy and climate impact risks (Bloomberg et al. Citation2017), better transparency on who is financing unsustainable economic activity (Global Canopy Programme Citation2016; Galaz et al. Citation2018; Folke et al. Citation2019; Gardner et al. Citation2019), and better understanding of how so called environmental social and governance (ESG) dimensions impact the financial performance of assets (Busch, Bauer, and Orlitzky Citation2016).

There are now many active initiatives with the purpose of ensuring that the finance sector does contribute to achieving sustainability, such as the United Nation’s Principles for Responsible Investment and the Financial Stability Board’s Task Force on Climate-related Financial Disclosures. The European Commission’s ongoing Action Plan on Sustainable Finance involves the development of legislative proposals designed to facilitate the movement of capital into sustainable investments. Two key elements of the plan are the development of a taxonomy of sustainable economic activity and the establishment of standards for sustainable financial products including a new voluntary EU green bonds standard based on the taxonomy (European Commission Citation2018, Citation2019).

Green bonds

Green bonds are an important development because they are a financial innovation designed to facilitate sustainable investing for institutional investors such a pension funds, insurance companies, mutual funds, and sovereign wealth funds. For example, green bonds are sometimes highlighted as an innovation that can help increase sustainable infrastructure investments from institutional investors by improving the liquidity of infrastructure assets (Merk et al. Citation2012; Della Croce and Yermo Citation2013; Bhattacharya, Oppenheim, and Stern Citation2015; OECD Citation2016).

With the exceptions of green bonds issued in China and India, what makes a bond green has to date not tended to be regulated. Instead, a common practice for establishing the ‘greeness’ of a bond has been alignment of the bond’s use of proceeds clause with the Green Bond Principles (GBPs), or other similar voluntary standards. The GBPs have been developed and endorsed by financial actors through the International Capital Markets Association (ICMA). The GBPs list renewable energy, energy and resource efficiency, pollution reduction, water and waste management, conservation, and climate adaptation as the types of projects that can be financed with a green bond (ICMA Citation2018).

Over 90% of green bonds are investment grade issuances (Tiftik, Mahmood, and Nozema Citation2019), meaning that they have high to medium credit quality ratings (i.e. AAA & AA or A & BBB ratings). A recent study of green bonds issued between 2013 and 2017 finds that the yields of green bonds are on average two basis points (bps) lower than those of comparable conventional bonds (Zerbib Citation2019). One common explanation for this yield difference is the high demand for and limited supply of green bonds. However, the presence of any pricing difference and its level is still debated in empirical studies (e.g. Larcker and Watts Citation2019). Irrespective of this debate, what is clear is that the vast majority of green bonds could have been issued as conventional bonds with little difference to the issuers’ ability to raise capital at favourable rates.

The structure of the green bond market todays raises several questions. If green bonds are nearly identical to regular investment grade bonds in terms of financial performance why are issuers making the extra effort to go through the green bond labelling, verification, and reporting process? Similarly, if the financial characteristics of green bonds do not differ significantly from conventional bonds, what explains the high demand for green bonds among investors? What value are green bonds delivering to issuers and investors, and what difference do they make to the way issuers and investors interact with each other? Understanding the motivations of actors participating in the green bond market is central to understanding what role green bonds can play in directing investment towards sustainable development and how we should understand green bonds as a new financial innovation.

Theory

To date there has been very little theorisation of the growth of the green bond market in the academic literature. For this study we use the literature on corporate social responsibility (CSR) and socially responsible investing (SRI), and in particular the different strands of organisational theory that underpins this literature, to demarcate motivations for engagement with the green bond market (Aguilera et al. Citation2007; Campbell Citation2007; Bengtsson Citation2008; Kurucz, Colbert, and Wheeler Citation2008; Matten and Moon Citation2008; Weber Citation2008; Van der Laan Citation2009; Greenwood et al. Citation2011; Brammer, Jackson, and Matten Citation2012; Scholtens and Sievänen Citation2013; Fernando and Lawrence Citation2014; Jansson and Biel Citation2014; Pedersen and Gwozdz Citation2014; Hockerts Citation2015; Strand, Edward Freeman, and Hockerts Citation2015; Majoch, Hoepner, and Hebb Citation2017). The CSR and SRI literature is directly relevant to understanding the bottom up growth of the green bond market because it provides us with an extensive body of theoretical and empirical work that examines why organisations engage in sustainability and social responsibility practices beyond what is legally mandated and regulated.

Importantly, we do not conceptualise participation in the green bond market as equivalent to SRI and even less so as a form of CSR. The phenomena may be related, but we use work on CSR and SRI for the purpose of developing a theoretical framework that distinguishes between three categories of motivations or drivers for engagement with sustainability practices: direct financial benefits, business case benefits, and legitimacy and institutionally-oriented incentives.

Direct financial incentives

The potential financial incentives for investing in green bonds are straightforward to identify as they are no different than for any other asset class. For an investor there is a direct financial incentive to invest in a green bond if this bond provides lower risk, and/or better returns, and/or better diversification benefits than other comparable non-labelled bonds or other assets they could invest in. For issuers, there is a direct financial incentive to issue a green bond as opposed to a non-labelled bond if the green bond reduces their cost of capital and/or improves their access to capital, i.e. reduces capital availability risks.

Note that another potential financial incentive for investors is associated with the size of the institutional investors. It is sometimes argued that because large institutional investors are exposed to the economy very broadly, they have financial incentives to ensure the long-term sustainability of the economy and the correction of market failures and negative externalities that undermine long-term economic efficiency (Hawley and Williams Citation2002). On this view universal investor incentives for engaging with various forms of sustainable finance could be part of a strategy to shift investment towards assets considered to be consistent with long-term sustainability and away from ‘brown’ assets with negative externalities that are expected to undermine long-run economic sustainability.

Business case

The business case for investing or issuing green bonds refers to incentives related to the economic performance of the investor or issuer that is not directly related to the financial performance of the green bond for the respective parties. Following from Hockerts (Citation2015) we highlight four types of non-financial business case incentives; branding, operational efficiency, creating new markets, and reducing risk.

The business case for the branding benefits of engaging in sustainable finance could be to attract and retain customers and clients or to charge premium prices for products and services (Menon and Menon Citation1997; Du, Bhattacharya, and Sen Citation2007; Belz and Schmidt-Riediger Citation2010; Dangelico and Vocalelli Citation2017). Operational efficiency may be enhanced by, for example, attracting high quality employees, impacting the productivity of employees motivated by sustainability commitments of the organisation, or identifying new operational efficiency gains (Branco and Rodrigues Citation2006; Morsing Citation2006; Sen, Bhattacharya, and Korschun Citation2006; Grolleau, Mzoughi, and Thomas Citation2007; Henriques and Sadorsky Citation2007; Ali et al. Citation2010).

Creating new markets could entail developing new investment products for customers interested in sustainable investing and/or attracting new classes of customers to existing and new product offerings (Renneboog, Horst, and Zhang Citation2011; Jansson and Biel Citation2014; Riedl and Smeets Citation2017). There could also be incentives associate with reducing risk that are not directly related to financial risks. For example, reputational risks and risks associate with potential future regulation related to sustainability (Davis Citation1973; Banerjee Citation2008; Barnett and Hoffman Citation2008; Gond and Piani Citation2013; Haufler Citation2013).

Legitimacy and institutional-oriented drivers

The academic literature on corporate engagement with sustainability identifies a number of incentives and pressures that are not narrowly based in specific business strategies but instead in broader forces relating to the legitimacy of the organisation and its so called ‘license to operate’ at a societal level (Gray, Kouhy, and Lavers Citation1995; Bansal and Roth Citation2000; Moir Citation2001; Deegan Citation2002; Sharfman, Shaft, and Tihanyi Citation2004; De Villiers and Van Staden Citation2006; Campbell Citation2007; Bolton, Kim, and O’Gorman Citation2011; Brammer, Jackson, and Matten Citation2012). Prominent theoretical perspectives adopted to understand these types of drivers are institutional theory (Meyer and Rowan Citation1977; DiMaggio and Powell Citation1983; Oliver Citation1991; Campbell Citation2007; Scott Citation2008), stakeholder theory (Roberts Citation1992; Freeman Citation1994; Donaldson and Preston Citation1995; Mitchell, Agle, and Wood Citation1997; Harrison and Edward Freeman Citation1999; Freeman Citation2001), and legitimacy theory (Deegan Citation2002; Deephouse and Carter Citation2005; Deegan Citation2019).

In our theoretical framework we follow Fernando and Lawrence (Citation2014) in grouping legitimacy, stakeholder, and institutional theory together as a set of theories that either predict similar motivations for engaging with sustainability and social responsibility or that make predictions that are largely complimentary. Common to legitimacy, stakeholder, and institutional theory is the idea that organisations face incentives to conform to norms and expectations that are imposed on the organisation by pressures that are external to the organisation’s primary mandate (although pressures can come from both external and internal stakeholders). These pressures can come from institutions, stakeholders, and social conditions/norms (Fernando and Lawrence Citation2014). Following from this understanding, engagement with sustainable finance could be explained by an organisation’s efforts to:

secure legitimacy in the face of societal level pressures to demonstrate sustainable business practices,

demonstrate accountability to identifiable stakeholders with sustainability demands on the organisation,

conform to the sustainability practices of other like-organisations that are facing the same institutional level pressures to engage with sustainability.

Especially institutional theory predicts that organisations facing similar institutional conditions will tend to adopt similar policies and procedures (isomorphism). This can be because organisations have to respond to the same types of stakeholders (Deegan Citation2009), because they face competitive reasons to adopt new trends other organisations are engaging with (e.g. for efficiency, management of uncertainty, and legitimacy reasons) (DiMaggio and Powell Citation1983; Unerman and Bennett Citation2004), or because actors in these types of organisations aim to adopt emerging professional expectations within a specific sector (DiMaggio and Powell Citation1983; Deegan Citation2009).

The theoretical predictions of institutional, stakeholder and legitimisation theory all relate in one way or another to securing or bolstering the survival and success of the organisation and its employees. As such it is difficult to make a sharp distinction between legitimacy and institutionally oriented theories of actor motivations and the business case for engaging with sustainability and social responsibility activities. However, there is a useful distinction to be made between reasons for engagement based (i) a business strategy where investments in sustainability activities are expected to directly improve the financial performance of the organisation over the short to medium term versus (ii) a more general goal of maintaining the status of the company or organisation as viable and successful at a broader sectoral or societal-level.

summarises the theoretical framework adopted to understand the motivations of issuers and investors in the Swedish green bond market and to design our interview protocol.

Table 1. Three categories of motivation for engagement in the green bond market.

Materials and methods

The aims of this study are to better understand what attracts investors and issuers to the green bond market, to assess the role of green bonds in shifting capital from less to more sustainable economic activity, and to provide insight on how green bonds in practice impact the way organisations work with sustainability. To address these questions, we conducted twenty-two in-depth interviews with actors in the Swedish green bond market over the fall of 2017 and spring of 2018. We interviewed nine issuers of green bonds from both the public and private sectors that have issued green bonds in Swedish Kronor (SEK). Three of the issuers interviewed have also issued green bonds in other currencies. We interviewed nine Swedish investors in green bonds, including public pension funds, private pension & investment funds, and insurance companies. We also interviewed two Swedish banks that underwrite green bonds in the Swedish green bond market, one exchange, and an expert in the Government of Sweden’s recent inquiry on green bonds. Interviews were sought from issuers and investors until well-grounded patterns in the data were found to be repeated (Bowen Citation2008).

We developed interview protocols structured to provide answers to three research questions:

What are the incentives of investors and issuers to engage in the GB market? To what extent is it financial, business-case, or legitimacy/institutional-oriented incentives that explain engagement with the green bonds market?

Do participants in the green bond market view green bonds as an important tool for shifting capital from less sustainable to more sustainable investments?

What difference do green bonds make to the ways in which issuers and investors work with sustainability? What do investors’ and issuers’ reported experience tell us about how we should understand the role of green bonds in advancing sustainability?

Interviews followed two semi-structured protocols that were similar but modified to reflect the differing perspectives of bond issuers and bond investors. For the two banks, questions from the issuer and investor protocols were used but some questions were modified to reflect the bank’s role as an intermediary or dropped due to not being relevant. For the exchange, service provider, financial regulator, and the member of the Government of Sweden’s green bond inquiry the interview protocols were used as a thematic guide, but the interview questions were less structured and developed organically during the interviews.

The interview protocol for issuers and investors included (i) an introductory section with general questions on the importance of sustainability for the finance sector, the tools used by investors to advance sustainability, and assessments of the effectiveness of these tools, (ii) a section specifically on the incentives for engaging in sustainable finance – delineating financial, business case, and non-business case incentives, (iii) a section on the incentives for either issuing green bonds or investing in them – again delineating between financial, business case, and non-business case incentives, (iv) a section on the perceived impacts of green bonds on shifting capital towards sustainable investments and on the operations of organisations, (v) a section on the barriers to scaling up green bonds and sustainable finance more generally.

Informants were offered anonymity and interviews were recorded with handwritten notes and transcribed to digital form according to the structure of the interview guide directly after each interview. The majority of interviewees were willing to be quoted for this study, sometimes with and sometimes without needing to give explicit consent to individual recorded statements. However, some respondents were less willing to be directly quoted, and given some perceived caution among our respondents in the first interviews, the decision was made to anonymize the reporting of results in order to create a trusting and open interview exchange.

Data was assessed by analysing the most grounded patterns in interview data using open coding (Coffey and Atkinson Citation1996). The set of overarching code categories were; (a) the incentive structure, (b) the impact of green bonds, and (c) the accelerators and barriers to growth of the market. Under incentives (a) we coded for (i) financial, (ii) business case, and (iii) non-business case incentives. Under impacts (b) we coded for (i) increasing sustainable investment, (ii) greening business models, and (iii) operational/organisational improvements. Under accelerators & barriers (c) we coded for (i) project supply, (ii) risks and bankability, (iii) policies and standards.

Results

Incentives to invest in green bonds

All respondents in our sample expressed that the clearest advantage to investing in green bonds is that one can invest in specific green projects or assets that are independently verified as green without taking on any meaningful additional risk. As one respondent put it, being able to make a certified green investment at the same risk as the other bonds we might invest in is a ‘no brainer’. In addition to the ease of investing in green bonds, respondents also highlighted that having a specified use of proceeds makes it very easy to communicate to clients and stakeholders how investments are contributing to sustainability. This makes green bonds a good first step into green investing and a strong signalling tool.

Respondents largely frame their incentives for investing in green bonds in terms of the non-financial business case rather than financial incentives. Green bonds are a way of attracting customers to the company and investors often referenced increasing demand among their customers either for specific sustainable investments vehicles or for demonstrating how the company is contributing to sustainability. Thus, we see incentives grounded in both branding (Menon and Menon Citation1997) and offering new premium products to customers (Jansson and Biel Citation2014; Riedl and Smeets Citation2017).

Respondents did not tend to ascribe any financial advantage associate with investing in green bonds, but rather described green bonds as on par with other relevant fixed income investments. Some respondents did suggest that because those companies that issue green bonds are high performers in terms of sustainability there should be some risk reduction advantages of investing in a green bond versus regular bonds. These perceptions are similar to perceptions ESG investors express on the benefits of integrating ESG factors into investment decisions (Duuren, Plantinga, and Scholtens Citation2016).

There was a consensus among respondents that the yields for green bonds were slightly lower than for other comparable bonds due to high demand for these investments. Although respondents did not give specific quantifications for this yield difference, estimates offered ranged from 2 to 6 basis points. At the same time, respondents were consistent in indicating that they were not able to accept lower returns from green bonds. Thus, there was some inconsistency in responses on this point. Only one respondent suggested that investing in green bonds was potentially inconsistent with their investing mandate due to the lower comparative yields green bonds are able to secure (i.e. the so-called ‘greenium’).

With respect to the non-financial business case for investing in green bonds, respondents consistently pointed to benefits such as attracting not only customers but also staff and skilled competence (Sen, Bhattacharya, and Korschun Citation2006). Importantly, all of our investor respondents have well established sustainability agendas within their organisations. As such, green bonds are part of a larger profile of work on sustainability. Interestingly, some respondents thought and wished that customer demand would be stronger, indicating that the organisation was moving ahead of customer demand to some extent with respect to sustainability work. This response was particularly prevalent among asset managers adopting a strategy to offer customers new sustainable investment vehicles.

Another major benefit consistently noted by our respondents was the improved dialogue on sustainability with issuers and internally within the organisation. Green bonds provide an opportunity for investors to learn about what counts as good sustainability performance and to use that knowledge in dialogue with organisations they invest in going forward. Respondents also indicated that green bonds helped to further integrate a sustainability perspective throughout the organisation (Ali et al. Citation2010).

None of our respondents explicitly framed investing in green bonds as motivated by legitimacy seeking or institutional pressures. For example, none of the investors indicated that they faced significant pressure from NGOs to engage with sustainable finance. However, investors all agreed that engagement with sustainability within the financial sector has increased significantly over the past five years, and that in Sweden most major financial actors are strengthening their sustainable finance profiles.

Investors cite a large number of sector initiatives related to sustainable finance, and a level of activity that can make it difficult engage everywhere. These responses combined with the evidence above that investors’ have some willingness to accept weaker returns in order to invest in green bonds suggests that there may be legitimacy seeking and institutional incentives for investing. Based on our interview responses it does appear that for large investors in the Swedish context their good standing within the sector and among stakeholders requires that they engage with sustainable finance. This provides support to theories that point to institutional and legitimacy oriented explanations for why organisations tend to adopt similar practices (DiMaggio and Powell Citation1983)

Incentives to issue green bonds

For issuers, it is the banks underwriting their bond programmes that typically initiate the idea of issuing a green bond. The three most widely held incentives to issue green bonds among our issuer interviewees were: broadening the investor base, lower capital costs, and meeting investor demand for sustainable investment products. Here, we see that financial incentives are more prominent amongst issuers compared to investors. This is not surprising of course given that it is the issuers that benefit financially from the high demand for green bonds and the lower interest rates they can secure. However, even if the financial incentives among issuers are stronger than for investors, we still judge the financial drivers to be weak among issuers.

Although nearly all our responding issuers say that the rebate they receive by issuing green bonds more than covers the added cost of green certification and reporting, the cost of capital benefits still appear to be small. Only one issuer suggested that the difference in the cost of capital between a green versus regular bond could make an investment in a green project viable when it would not otherwise be financially viable. The example given was about the level of green certification of a new building and not whether or not the building would be constructed. In general, however, issuers concluded that the rebate associated with issuing a green bond made no significant difference to the issuing company’s overall investment decisions. Still, the effect is large enough for some issuers that they indicated that good financial practice calls for issuing ‘green’ when possible. Issuers did not expect that preferential yield rates could increase much beyond current levels.

Securing access to capital was actually the most often cited financial benefit among issuers. At the same time, the large majority of respondents indicated that they did not currently have challenges with regard to access to capital. Instead, issuers argued that access to capital will increasingly be contingent on demonstrating green credentials and that for this reason there are first mover advantages to engaging with sustainable finance. This expectation that access to financing will increasingly be dependent on the sustainability of borrowers was shared among the large majority of our respondents.

Given that the issuers we interviewed indicted that access to capital is not currently a challenge, it is to some extent surprising that this was the dominant response for the advantage of issuing green bonds. However, we argue that these responses should be interpreted in the context in which our issuers typically first issued green bonds. It is on the advice of a bank or a funding agency that has expertise on issuing green bonds and that sees the demand for green bonds among investors that issuers tend to first enter into this market. Thus, although access to capital is not judged to be a challenge, issuers are receiving signals from their main stakeholders in the finance sector on the desire to have access to sustainable investment opportunities. This supports the theory that when organisations face expectations from stakeholders they are dependent on, e.g. economically, this will impact their willingness to engage in sustainability practices (Roberts Citation1992).

Other incentives for issuing green bonds focused on the non-financial business case. Issuers tended to argue that the work they already do on sustainability and sustainability reporting makes issuing a green bond relatively unproblematic. Issuing a green bond can thus help to consolidate internally the sustainability work the company is already doing. In a similar way, issuing a green bond is also viewed as a good means to communicate this work externally. Being able to issue a green bond is also perceived as a stamp of quality for the organisation. Such perceptions support theories that companies seek out and can secure customer demand and loyalty by demonstrating the integration of sustainability into their business practices (Du, Bhattacharya, and Sen Citation2007). Thus, we see clear branding incentives among issuers. Yet, a difference here is that the target of this branding is not clearly directed towards the customers of issuers.

For example, a real estate company may market its rental spaces as environmentally friendly to its customers but the fact that the building has been financed (or more likely re-financed) by a green bond is not information that looks to be important from the renter’s perspective. Rather, it is green building rating and certification systems that the real estate company’s customers can relate to. Green financing is added on to the building once it is complete, and this labelling or branding is satisfying the interests of the company’s lenders (i.e. institutional investors or banks).

Many issuers, especially companies that are not ‘pure play’ issuers, cite the further mainstreaming of their sustainability work into the overall operations of the organisation as a benefit of issuing a green bond. For example, by linking the sustainability and financial management functions of the organisation. Issuing a green bond is also viewed as one means to further consolidate the investments in sustainability already made by the company and to further incorporate sustainability into the strategic decisions of the company’s leadership.

Investor perspectives on green bonds and shifting capital

In the beginning of our interviews we asked investors to identify and rank the most important tools they employ to move the sustainability agenda forward and to realise more green investments. Most often mentioned were integrating ESG criteria into investment decisions and active ownership, particularly in collaboration with other owners that share sustainability objectives. Other tools often mentioned were positive and negative screening and longer-term investment strategies. Green bonds were rarely ranked as one of the most impactful tools. Issuers, for their part, did not claim that green bonds made the projects they finance viable when they otherwise would not be. As a financial instrument, green bonds are not judged by our respondent to play a large role in shifting capital from unstainable to sustainable investments, a result that confirms results from earlier assessments of the market (Shishlov, Morel, and Cochran Citation2016).

Importantly our results should not be interpreted as showing green bonds to be judged negatively or ineffective by our respondents. We find that the large majority of interviewees are highly positive to green bonds, with only one investor indicating that lower yields from green bonds were bringing into question their ability to invest in this asset class. Investors in general find that green bonds are impactful because they incentivise bond issuers to shift to greener business models. The growth of the green bond market is also viewed as the first steps to raising sustainability demands broadly in capital markets. Investors also find that green bonds are an important tool for creating awareness among their customers and the public on the links between sustainability and finance.

Issuer perspectives on green bonds and shifting capital

Issuers make similar arguments and see issuing green bonds as a catalyser for raising the ‘green ambitions’ of specific projects and the company as whole. Thus, even if issuers do not indicate that green bonds affect their cost of capital in a way that can impact their overall investment strategies, they do indicate that green bonds can lead to more investment into the environmental performance of the projects they do decide to invest in. This is an interesting finding in light of recent empirical evidence that green bonds are correlated with overall better comparative environmental footprints for issuing companies (Flammer Citation2020).

Many of the interviewed issuers argue that green bonds help to ‘make the case’ for the sustainability work the company is already doing, further consolidating the sustainability profile of the company. An important governance impact is that the reputation of green bond issuers becomes dependent on ensuring that any assets financed by a green bond remain within certification. Finally, issuers see green bonds as serving an important signalling function, highlighting that other comparable investments are not green and that there is investor demand for green investments.

Throughout our interviews, both investors and issuers highlighted the ability to link investment to a specific and verified project as the crucial advantage of green bonds. Reporting impact to investors on metrics such as avoided emissions or improved water efficiency allows the investor to demonstrate to its customers and stakeholders how capital is being put to work for sustainability. However, a key finding of our study is that when market actors reflect on the impact of green bonds on moving economies towards sustainability, they tend not to highlight the actualisation of green projects and investments. Instead, respondents point to indirect impacts on the internal operations of both investors and issuers, elevated sustainability ambition levels, raising the status of sustainability work within their organisations, and broader signalling effects as the central benefits of green bonds.

Discussion

What explains the growth of the green bond market in Sweden?

Based on our responses on the incentives for engaging in the green bond market we can identify a number of key drivers for the growth of the green bond market in Sweden. We see that there are weak financial incentives, but stronger financial incentives for issuers compared to investors. We see that non-financial business case advantages are most cited, but more so for investors while issuers are more balanced in citing financial and business-case advantages. We see clearly that green bonds represent a familiar and low risk financial instrument for both investors and issuers. This leads to a strong matching between issuer and investor incentives. Issuers in our study hold green assets that are appropriate for bond financing while green bonds are designed to fit into to existing capital markets with little additional investment analysis required from investors. This means that investors and issuers are able to contribute to sustainability mandates they already have and to respond to their stakeholders’ sustainability interests at relatively low cost.

This strong matching of investor and issuer incentives explains both the rapid growth of the green bond market and limits to its growth. Our respondents all argue that there is no lack of demand for green bonds among Swedish investors, but rather a lack of good green projects/assets appropriate for bond financing. The demand for green bonds has incentivised public and private actors that borrow on capital markets and that have green assets/projects to meet investor demand. But all respondents cited the need to improve the pipeline of bankable green projects in order grow the market for green bonds.

Although we do not perform a comparative analysis in this study, most of the results with respect to issuer and investor incentives look like they could easily be generalised to similar financial markets, especially in Europe. However, our interview subjects did emphasise the extent to which having a strong sustainability profile has become a norm in Sweden linked to the reputation and standing of financial actors. The broad internalisation of this agenda may explain why Sweden has a comparatively high share of green bonds within its domestic bond market and is an interesting research question for future comparative work.

Another interesting result for this study was the extent to which both investors and issuers called for more leadership, long-term planning, and stronger climate policy from the state as the most important factors in increasing the availability of bankable green investments. Issuing of sovereign green bonds is another avenue for increasing the asset class, and Sweden appears ready to follow France and others in issuing a state green bond (Regeringskansliet Citation2019). However, at the time of our study there was no clear pattern among respondents on this policy. Some respondents viewed the issuance of a Swedish sovereign bond as important while others were sceptical or unaware of the issue.

How does engagement in the green bond market advance sustainability?

Given that green bonds tend to finance or re-finance projects that would have happened without this financial instrument, there has been a large debate on what ‘additionality’ or added value green bonds deliver. This debate is understandable given that green bonds are for the most part structured as typical investment grade municipal and corporate bonds, while the ‘use of proceeds’ innovation does not appear to lead to significant changes in how capital is allocated. Are green bonds an important innovation for sustainability or just the status-quo in new green packaging?

Based on our analysis we find that it is a legitimate concern that green bonds falsely give the impression that they are more impactful that they actually are. Although actors in the Swedish market are careful to note that green bonds are not very different as financial instruments than other bonds, they also market green bonds in terms of the projects they fund and the environmental impacts they have. This can create the impression that investments in green bonds are moving capital into novel investments, while in practice our respondents have largely shifted capital from state bonds to investment grade municipal and corporate bonds. At the same time, our evidence shows the investors and issuers are actually changing the way they interact in capital markets and that these changes have positive impacts for sustainability at the operational level within organisations.

It is the ‘use of proceeds’ clause that is the most significant innovation in labelled bonds markets, and it has created a system for standardising and scaling the environmental engagement of investors on capital markets. Green bonds have created a new infrastructure within capital markets consisting of: guidelines for what counts as a green investment, the development of company frameworks providing transparency on how proceeds will be used, external validation of the credibility of issuers’ green bond frameworks, and reporting back to investors on the use of proceeds and their environmental impacts (Alfsen et al. Citation2018).

Our analysis shows that there are many similarities between active ownership and the way green bond markets are structure that are easily missed if one focuses only on the way green bonds are marketed to external stakeholders. Although buyers of bonds do not have the voting rights they have when they invest in equity, all of our respondents have highlighted that engaging with the green bond market leads to dialogue on sustainability expectations between investors and issuers that would not have occurred without green bonds. Of course, green bonds only represent a small fraction of the bond market, but there does appear to be opportunities to expand ‘use of proceeds’ thinking more broadly in capital markets and in other parts of the financial system. This is important because investors already indicate that active ownership is one of the most impactful instruments they have to bring about changes in the real economy (Amel-Zadeh and Serafeim Citation2018).

A relatively new trend is for fixed-income institutional investors to engage with companies on ESG factors (Hanson et al. Citation2017), at least to the extent that these have not be addressed by traditional credit ratings. Green bonds are part of this trend, a trend which could arguably be more impactful than equity ESG investing. If capital markets and banks raise demands on borrowers to demonstrate improved sustainability performance this could lead to more significant impacts on the cost of and access to capital.

Conclusions

In this study we find that the incentives for engagement with the green bond market in Sweden are dominated by business-case incentives rather than financial incentives. There are some direct financial incentives, especially for issuers who highlight small reductions in the cost of capital and better access to capital. However, respondents are more consistent in pointing to benefits such as attracting customers and staff, mainstreaming sustainability into internal operations, and broader signalling effects.

Within the context of a Swedish financial sector in which engagement with sustainability has become a clear norm, we also see evidence of legitimacy seeking, stakeholder, and institutional incentives for engagement in the green bond market. Among investors this is reflected in their willingness to accept weaker returns from green bonds than those they expect from comparable non-labelled bonds. Among issuers these types of incentives are reflected in their willingness to do the extra work needed to issue green bonds despite very good access to capital.

Overall, we find that the bottom up growth of the green bond market is due to the strong matching of incentives between issuers and investors. Green bonds are designed to be a familiar and low risk financial instrument that allows both investors and issuers to contribute to sustainability mandates at relatively low cost. Our respondents do not judge green bonds to play a large role in shifting capital from unstainable to sustainable investments. Green bonds are however perceived to provide incentives to issuers to raise the ‘green ambitions’ of specific projects and their organisations.

Overall, when market actors reflect on the impact of green bonds in practice, they tend not to highlight the actualisation of green projects. Instead, they emphasise the mainstreaming of sustainability consideration into the ways investors and issuers interact with each other and internally within their organisations. However, because green bonds are marketed in terms of metrics such as renewable energy generated, emissions avoided, or waste managed we find that green bonds do risk giving market outsiders the impression that they are more impactful that they actually are in terms of shifting capital. Our analysis shows that as a financial tool green bonds are a quite conservative innovation. They do not appear to be unlocking new sources of capital for green investment or making green investments financially viable when they otherwise would not be.

Our analysis shows that there are many similarities between active ownership and the way green bond markets are structure that are easily missed if one focuses only on the way green bonds are marketed. The green bond market has evolved into a new infrastructure within capital markets consisting of green guidelines, use of proceeds commitments, external validation, and reporting. This new infrastructure is changing the way actors interact on capital markets, raising expectations with regards to ESG performance.

Acknowledgments

This research was support by the Marianne & Marcus Wallenberg Foundation under Grant MMW 2016.0045. The authors would like to thank Emma Sjöström and Asbjørn Torvanger for their helpful comments on earlier drafts of this paper. We would also like to thank Luca de Lorenzo and Måns Nilsson for their input on the design of this study, and Gregor Vulturius for assisting in compiling data on green bond issuances in Sweden. Finally, we would like to thank the participants at two workshops in 2019, one in Stockholm and one in Oslo, for their feedback on the results of this research.

Disclosure statement

No potential conflict of interest was reported by the author(s).

Additional information

Funding

Notes

1 Some green bond issuers, such as renewable energy producers, consider their entire business model to be green and issue green bonds as ‘pure play’, meaning that the use of proceeds is for general corporate purposes.

References

- Aguilera, Ruth V., Deborah E. Rupp, Cynthia A. Williams, and Jyoti Ganapathi. 2007. “Putting the S Back in Corporate Social Responsibility: A Multilevel Theory of Social Change in Organizations.” Academy of Management Review 32 (3): 836–863. doi: 10.5465/amr.2007.25275678

- Alfsen, Knut H., Kristina Alnes, Alexander O. Berg, Christa Clapp, Sophie Dejonckheere, Harald Francke Lund, Bernhard Schiessl, and Asbjørn Torvanger. 2018. “CICERO MILESTONES 2018. A Practitioner’s Perpective on the Green Bond Market.” 16, September. https://pub.cicero.oslo.no/cicero-xmlui/handle/11250/2561603.

- Ali, Imran, Kashif Ur Rehman, Syed Irshad Ali, Jamil Yousaf, and Maria Zia. 2010. “Corporate Social Responsibility Influences, Employee Commitment and Organizational Performance.” African Journal of Business Management 4 (13): 2796–2801.

- Amel-Zadeh, Amir, and George Serafeim. 2018. “Why and How Investors Use ESG Information: Evidence From a Global Survey.” Financial Analysts Journal 74 (3): 87–103. doi: 10.2469/faj.v74.n3.2

- Baker, Malcolm, Daniel Bergstresser, George Serafeim, and Jeffrey Wurgler. 2018. “Financing the Response to Climate Change: The Pricing and Ownership of US Green Bonds.” National Bureau of Economic Research Working paper 25194: 1–40. doi:10.3386/w25194.

- Banerjee, Subhabrata Bobby. 2008. “Corporate Social Responsibility: The Good, the Bad and the Ugly.” Critical Sociology 34 (1): 51–79. doi: 10.1177/0896920507084623

- Bansal, Pratima, and Kendall Roth. 2000. “Why Companies Go Green: A Model of Ecological Responsiveness.” Academy of Management Journal 43 (4): 717–736.

- Barnett, Michael L., and Andrew J. Hoffman. 2008. “Beyond Corporate Reputation: Managing Reputational Interdependence.” Corporate Reputation Review 11 (1): 1–9. doi: 10.1057/crr.2008.2

- Belz, Frank-Martin, and Birte Schmidt-Riediger. 2010. “Marketing Strategies in the Age of Sustainable Development: Evidence from the Food Industry.” Business Strategy and the Environment 19 (7): 401–416.

- Bengtsson, Elias. 2008. “Socially Responsible Investing in Scandinavia–a Comparative Analysis.” Sustainable Development 16 (3): 155–168. doi: 10.1002/sd.360

- Bhattacharya, Amar, Jeremy Oppenheim, and Nicholas Stern. 2015. “Driving Sustainable Development through Better Infrastructure: Key Elements of a Transformation Program.” Brookings Global Working Paper Series.

- Bielenberg, Aaron, Mike Kerlin, Jeremy Oppenheim, and Melissa Roberts. 2016. “Financing Change: How to Mobilize Private-Sector Financing for Sustainable Infrastructure.” McKinsey Center for Business and Environment. http://newclimateeconomy.report/2015/wp-content/uploads/sites/3/2016/01/Financing_change_How_to_mobilize_private-sector_financing_for_sustainable-_infrastructure.pdf.

- Bloomberg, M. R., D. Pavarina, G. Pitkethly, C. Thimann, and Y. L. Sim. 2017. Final Report: Recommendations of the Task Force on Climate-Related Financial Disclosures. Task Force on Climate-Related Financial Disclosures. Switerzland.

- Bolton, Sharon C., Rebecca Chung-hee Kim, and Kevin D. O’Gorman. 2011. “Corporate Social Responsibility as a Dynamic Internal Organizational Process: A Case Study.” Journal of Business Ethics 101 (1): 61–74. doi: 10.1007/s10551-010-0709-5

- Bowen, Glenn A. 2008. “Naturalistic Inquiry and the Saturation Concept: A Research Note.” Qualitative Research 8 (1): 137–152. doi:10.1177/1468794107085301.

- Brammer, Stephen, Gregory Jackson, and Dirk Matten. 2012. “Corporate Social Responsibility and Institutional Theory: New Perspectives on Private Governance.” Socio-Economic Review 10 (1): 3–28. doi: 10.1093/ser/mwr030

- Branco, Manuel Castelo, and Lúcia Lima Rodrigues. 2006. “Corporate Social Responsibility and Resource-Based Perspectives.” Journal of Business Ethics 69 (2): 111–132. doi: 10.1007/s10551-006-9071-z

- Busch, Timo, Rob Bauer, and Marc Orlitzky. 2016. “Sustainable Development and Financial Markets: Old Paths and New Avenues.” Business & Society 55 (3): 303–329. doi: 10.1177/0007650315570701

- Campbell, John L. 2007. “Why Would Corporations Behave in Socially Responsible Ways? An Institutional Theory of Corporate Social Responsibility.” Academy of Management Review 32 (3): 946–967. doi: 10.5465/amr.2007.25275684

- Chasan, Emily. 2019. “Bonds to Save the Planet - Bloomberg.” April 23, 2019. https://www.bloomberg.com/news/articles/2019-04-23/bonds-to-save-the-planet.

- Climate Bonds Initiative. 2019. Green Bonds: The State of the Market 2018. London: Climate Bonds Initiative. file:///Users/aaron.maltais/Downloads/cbi_gbm_final_032019_web%20(2).pdf.

- Climate Bonds Initiative. n.d. “Understanding Climate Bonds.” Accessed October 14, 2019. https://www.climatebonds.net/resources/understanding.

- Coffey, Amanda, and Paul Atkinson. 1996. Making Sense of Qualitative Data: Complementary Research Strategies. Thousand Oaks: Sage Publications.

- Dangelico, Rosa Maria, and Daniele Vocalelli. 2017. “‘Green Marketing’: An Analysis of Definitions, Strategy Steps, and Tools through a Systematic Review of the Literature.” Journal of Cleaner Production 165: 1263–1279. doi: 10.1016/j.jclepro.2017.07.184

- Danske Bank. 2019. “From 38 to 70bn SEK Green Bonds Are on the Rise in Sweden.” January 22, 2019. https://danskeci.com/ci/financial-markets/solutions/sustainable-finance/from-38-to-70bn-sek-green-bonds-are-on-the-rise-in-sweden.

- Davis, Keith. 1973. “The Case for and against Business Assumption of Social Responsibilities.” Academy of Management Journal 16 (2): 312–322.

- Deegan, Craig. 2002. “Introduction: The Legitimising Effect of Social and Environmental Disclosures–a Theoretical Foundation.” Accounting, Auditing & Accountability Journal 15 (3): 282–311. doi: 10.1108/09513570210435852

- Deegan, Craig. 2009. Financial Accounting Theory. North Ryde, NSW: McGraw Hill.

- Deegan, Craig Michael. 2019. “Legitimacy Theory.” Accounting, Auditing & Accountability Journal 32 (8): 2307–2329. doi:10.1108/AAAJ-08-2018-3638.

- Deephouse, David L., and Suzanne M. Carter. 2005. “An Examination of Differences between Organizational Legitimacy and Organizational Reputation.” Journal of Management Studies 42 (2): 329–360. doi: 10.1111/j.1467-6486.2005.00499.x

- Della Croce, Raffaele, and Juan Yermo. 2013. “Institutional Investors and Infrastructure Financing.”.

- De Villiers, Charl, and Chris J. Van Staden. 2006. “Can Less Environmental Disclosure Have a Legitimising Effect? Evidence from Africa.” Accounting, Organizations and Society 31 (8): 763–781. doi: 10.1016/j.aos.2006.03.001

- DiMaggio, Paul J., and Walter W. Powell. 1983. “The Iron Cage Revisited: Institutional Isomorphism and Collective Rationality in Organizational Fields.” American Sociological Review 48: 147–160. doi: 10.2307/2095101

- Donaldson, Thomas, and Lee E. Preston. 1995. “The Stakeholder Theory of the Corporation: Concepts, Evidence, and Implications.” Academy of Management Review 20 (1): 65–91. doi: 10.5465/amr.1995.9503271992

- Du, Shuili, Chitrabhan B. Bhattacharya, and Sankar Sen. 2007. “Reaping Relational Rewards from Corporate Social Responsibility: The Role of Competitive Positioning.” International Journal of Research in Marketing 24 (3): 224–241. doi: 10.1016/j.ijresmar.2007.01.001

- Duuren, Emiel van, Auke Plantinga, and Bert Scholtens. 2016. “ESG Integration and the Investment Management Process: Fundamental Investing Reinvented.” Journal of Business Ethics 138 (3): 525–533. doi:10.1007/s10551-015-2610-8.

- Ehlers, Torsten, and Frank Packer. 2017. “Green Bond Finance and Certification.” BIS Quarterly Review September.

- European Commission. 2018. “Commission Action Plan on Financing Sustainable Growth.” Text. European Commission - European Commission. March 8, 2018. https://ec.europa.eu/info/publications/180308-action-plan-sustainable-growth_en.

- European Commission. 2019. “EU Green Bond Standard.” Text. European Commission - European Commission. June 18, 2019. https://ec.europa.eu/info/publications/sustainable-finance-teg-green-bond-standard_en.

- Fernando, Susith, and Stewart Lawrence. 2014. “A Theoretical Framework for CSR Practices: Integrating Legitimacy Theory, Stakeholder Theory and Institutional Theory.” Journal of Theoretical Accounting Research 10 (1): 149–178.

- Flammer, Caroline. 2020. “Green Bonds: Effectiveness and Implications for Public Policy.” Environmental and Energy Policy and the Economy 1 (1): 95–128. doi:10.1086/706794.

- Folke, Carl, Henrik Österblom, Jean-Baptiste Jouffray, Eric F. Lambin, W. Neil Adger, Marten Scheffer, Beatrice I. Crona, Magnus Nyström, Simon A. Levin, and Stephen R. Carpenter. 2019. “Transnational Corporations and the Challenge of Biosphere Stewardship.” Nature Ecology & Evolution 3: 1396–1403. doi:10.1038/s41559-019-0978-z.

- Freeman, R. Edward. 1994. “The Politics of Stakeholder Theory: Some Future Directions.” Business Ethics Quarterly 4: 409–421. doi: 10.2307/3857340

- Freeman, R. Edward. 2001. “A Stakeholder Theory of the Modern Corporation.” Perspectives in Business Ethics Sie 3: 144.

- Galaz, Victor, Beatrice Crona, Alice Dauriach, Bert Scholtens, and Will Steffen. 2018. “Finance and the Earth System–Exploring the Links between Financial Actors and Non-Linear Changes in the Climate System.” Global Environmental Change 53: 296–302. doi: 10.1016/j.gloenvcha.2018.09.008

- Gardner, T. A., M. Benzie, J. Börner, E. Dawkins, S. Fick, R. Garrett, J. Godar, et al. 2019. “Transparency and Sustainability in Global Commodity Supply Chains.” World Development 121 (September): 163–177. doi: 10.1016/j.worlddev.2018.05.025

- Global Canopy Programme. 2016. Sleeping Giants of Deforestation: The Companies, Countries and Financial Institutions with the Power to Save Forests. Oxford, UK: Global Canopy Programme. https://www.globalcanopy.org/sites/default/files/documents/resources/sleeping_giants_of_deforestation_-_2016_forest_500_results.pdf.

- Gond, Jean-Pascal, and Valeria Piani. 2013. “Enabling Institutional Investors’ Collective Action: The Role of the Principles for Responsible Investment Initiative.” Business & Society 52 (1): 64–104. doi: 10.1177/0007650312460012

- Gray, Rob, Reza Kouhy, and Simon Lavers. 1995. “Corporate Social and Environmental Reporting: A Review of the Literature and a Longitudinal Study of UK Disclosure.” Accounting, Auditing & Accountability Journal 8 (2): 47–77. doi: 10.1108/09513579510146996

- Greenwood, Royston, Mia Raynard, Farah Kodeih, Evelyn R. Micelotta, and Michael Lounsbury. 2011. “Institutional Complexity and Organizational Responses.” Academy of Management Annals 5 (1): 317–371. doi: 10.5465/19416520.2011.590299

- Grolleau, Gilles, Naoufel Mzoughi, and Alban Thomas. 2007. “What Drives Agrifood Firms to Register for an Environmental Management System?” European Review of Agricultural Economics 34 (2): 233–255. doi: 10.1093/erae/jbm012

- Grubb, Michael. 2014. Planetary Economics: Energy, Climate Change and the Three Domains of Sustainable Development. Oxford: Routledge.

- Hanson, Dan, Tom Lyons, Jennifer Bender, Bruno Bertocci, and Bobby Lamy. 2017. “Analysts’ Roundtable on Integrating ESG into Investment Decision-Making.” Journal of Applied Corporate Finance 29 (2): 44–55. doi:10.1111/jacf.12232.

- Harrison, Jeffrey S., and R. Edward Freeman. 1999. “Stakeholders, Social Responsibility, and Performance: Empirical Evidence and Theoretical Perspectives.” Academy of Management Journal 42 (5): 479–485.

- Haufler, Virginia. 2013. A Public Role for the Private Sector: Industry Self-Regulation in a Global Economy. Washington, DC: Carnegie Endowment for International Peace.

- Hawley, James P., and Andrew T. Williams. 2002. “The Universal Owner’s Role in Sustainable Economic Development.” Corporate Environmental Strategy 9 (3): 284–291. doi:10.1016/S1066-7938(02)00056-8.

- Henriques, Irene, and Perry Sadorsky. 2007. “Environmental Management Systems and Practices: An International Perspective.” In Corporate Behaviour and Environmental Policy, edited by Nick Johnstone, 34–70. Cheltenham: Edward Elgar in association with OECD.

- Hockerts, Kai. 2015. “A Cognitive Perspective on the Business Case for Corporate Sustainability.” Business Strategy and the Environment 24 (2): 102–122. doi: 10.1002/bse.1813

- Hourcade, Jean-Charles, and Priyadarshi Shukla. 2013. “Triggering the Low-Carbon Transition in the Aftermath of the Global Financial Crisis.” Climate Policy 13 (sup01): 22–35. doi: 10.1080/14693062.2012.751687

- ICMA. 2018. “Green Bond Principles: Voluntary Process Guidelines for Issuing Green Bonds.” ICMA. https://www.icmagroup.org/assets/documents/Regulatory/Green-Bonds/June-2018/Green-Bond-Principles—June-2018-140618-WEB.pdf.

- IEA & IRENA. 2017. Perspectives for the Energy Transition: Investment Needs for a Low-Carbon Energy System. Paris: IEA.

- Jansson, Magnus, and Anders Biel. 2014. “Investment Institutions’ Beliefs about and Attitudes toward Socially Responsible Investment (SRI): A Comparison between SRI and Non-SRI Management.” Sustainable Development 22 (1): 33–41. doi: 10.1002/sd.523

- Kurucz, Elizabeth C., Barry A. Colbert, and David Wheeler. 2008. “The Business Case for Corporate Social Responsibility.” In The Oxford Handbook of Corporate Social Responsibility, edited by Andrew Crane, Abagail McWilliams, Dirk Matten, Jeremy Moon, and Donald S. Siegel, 83–112. Oxford: Oxford University Press.

- Larcker, David F., and Edward M. Watts. 2019. “Where’s the Greenium?” ID 3333847. Stanford: Rock Center for Corporate Governance at Stanford University. https://www.gsb.stanford.edu/gsb-cmis/gsb-cmis-download-auth/474556.

- Majoch, Arleta AA, Andreas GF Hoepner, and Tessa Hebb. 2017. “Sources of Stakeholder Salience in the Responsible Investment Movement: Why Do Investors Sign the Principles for Responsible Investment?” Journal of Business Ethics 140 (4): 723–741. doi: 10.1007/s10551-016-3057-2

- Material Economics, and SEI. 2018. Framing Stranded Asset Risks in an Age of Disruption. Stockholm Sweden: Material Economics & The Stockholm Environment Institute. https://www.sei.org/wp-content/uploads/2018/03/stranded-assets-age-disruption.pdf.

- Matten, Dirk, and Jeremy Moon. 2008. “‘Implicit’ and ‘Explicit’ CSR: A Conceptual Framework for a Comparative Understanding of Corporate Social Responsibility.” Academy of Management Review 33 (2): 404–424. doi: 10.5465/amr.2008.31193458

- McGlade, Christophe, and Paul Ekins. 2015. “The Geographical Distribution of Fossil Fuels Unused When Limiting Global Warming to 2 C.” Nature 517 (7533): 187–190. doi: 10.1038/nature14016

- Menon, Ajay, and Anil Menon. 1997. “Enviropreneurial Marketing Strategy: The Emergence of Corporate Environmentalism as Market Strategy.” Journal of Marketing 61 (1): 51–67. doi: 10.1177/002224299706100105

- Merk, Olaf, Stéphane Saussier, Carine Staropoli, Enid Slack, and Jay-Hyung Kim. 2012. “Financing Green Urban Infrastructure.”.

- Meyer, John W., and Brian Rowan. 1977. “Institutionalized Organizations: Formal Structure as Myth and Ceremony.” American Journal of Sociology 83 (2): 340–363. doi: 10.1086/226550

- Mitchell, Ronald K., Bradley R. Agle, and Donna J. Wood. 1997. “Toward a Theory of Stakeholder Identification and Salience: Defining the Principle of Who and What Really Counts.” Academy of Management Review 22 (4): 853–886. doi: 10.5465/amr.1997.9711022105

- Moir, Lance. 2001. “What Do We Mean by Corporate Social Responsibility?” Corporate Governance: The International Journal of Business in Society 1 (2): 16–22. doi: 10.1108/EUM0000000005486

- Morsing, Mette. 2006. “Corporate Moral Branding: Limits to Aligning Employees.” Corporate Communications: An International Journal 11 (2): 97–108. doi: 10.1108/13563280610661642

- OECD. 2016. Green Bonds: Mobilising the Debt Capital Markets for a Low Carbon Transition. Paris: OECD Publishing. https://www.oecd.org/environment/cc/Green%20bonds%20PP%20%5Bf3%5D%20%5Blr%5D.pdf.

- Oliver, Christine. 1991. “Strategic Responses to Institutional Processes.” Academy of Management Review 16 (1): 145–179. doi: 10.5465/amr.1991.4279002

- Pedersen, Esben Rahbek Gjerdrum, and Wencke Gwozdz. 2014. “From Resistance to Opportunity-Seeking: Strategic Responses to Institutional Pressures for Corporate Social Responsibility in the Nordic Fashion Industry.” Journal of Business Ethics 119 (2): 245–264. doi: 10.1007/s10551-013-1630-5

- Regeringskansliet, Regeringen och. 2019. “Staten ska ge ut gröna obligationer senast 2020.” Text. Regeringskansliet. July 18, 2019. https://www.regeringen.se/pressmeddelanden/2019/07/staten-ska-ge-ut-grona-obligationer-senast-2020/.

- Renneboog, Luc, Jenke Ter Horst, and Chendi Zhang. 2011. “Is Ethical Money Financially Smart? Nonfinancial Attributes and Money Flows of Socially Responsible Investment Funds.” Journal of Financial Intermediation 20 (4): 562–588. doi: 10.1016/j.jfi.2010.12.003

- Riedl, Arno, and Paul Smeets. 2017. “Why Do Investors Hold Socially Responsible Mutual Funds?” The Journal of Finance 72 (6): 2505–2550. doi: 10.1111/jofi.12547

- Roberts, Robin W. 1992. “Determinants of Corporate Social Responsibility Disclosure: An Application of Stakeholder Theory.” Accounting, Organizations and Society 17 (6): 595–612. doi: 10.1016/0361-3682(92)90015-K

- Scholtens, Bert, and Riikka Sievänen. 2013. “Drivers of Socially Responsible Investing: A Case Study of Four Nordic Countries.” Journal of Business Ethics 115 (3): 605–616. doi: 10.1007/s10551-012-1410-7

- Scott, W. Richard. 2008. “Approaching Adulthood: The Maturing of Institutional Theory.” Theory and Society 37 (5): 427–442. doi: 10.1007/s11186-008-9067-z

- Sen, Sankar, Chitra Bhanu Bhattacharya, and Daniel Korschun. 2006. “The Role of Corporate Social Responsibility in Strengthening Multiple Stakeholder Relationships: A Field Experiment.” Journal of the Academy of Marketing Science 34 (2): 158–166. doi: 10.1177/0092070305284978

- Sharfman, Mark P., Teresa M. Shaft, and Laszlo Tihanyi. 2004. “A Model of the Global and Institutional Antecedents of High-Level Corporate Environmental Performance.” Business & Society 43 (1): 6–36. doi: 10.1177/0007650304262962

- Shishlov, Igor, Romain Morel, and Ian Cochran. 2016. Beyond Transparency: Unlocking the Full Potential of Green Bonds.” Institute for Climate Economics Report, https://www.I4ce.Org/Download/Unlocking-the-Potential-of-Green-Bonds/ (Erişim Tarihi: 20.08. 2017).

- Strand, Robert, R. Edward Freeman, and Kai Hockerts. 2015. “Corporate Social Responsibility and Sustainability in Scandinavia: An Overview.” Journal of Business Ethics 127 (1): 1–15. doi: 10.1007/s10551-014-2224-6

- Tiftik, Emre, Khadija Mahmood, and Celso Nozema. 2019. Sustainable Finance in Focus: Green Bonds Take Root. Instittute of International Finance. https://www.iif.com/Portals/0/Files/SF_green_bond_issuance%20vf.pdf.

- UNEP. 2015. The Financial System We Need: Aligning the Financial System with Sustainable Development. Nairobi: United Nations Environment Programme. http://unepinquiry.org/wp-content/uploads/2015/11/The_Financial_System_We_Need_EN.pdf.

- Unerman, Jeffrey, and Mark Bennett. 2004. “Increased Stakeholder Dialogue and the Internet: Towards Greater Corporate Accountability or Reinforcing Capitalist Hegemony?” Accounting, Organizations and Society 29 (7): 685–707. doi:10.1016/j.aos.2003.10.009.

- Van der Laan, Sandra. 2009. “The Role of Theory in Explaining Motivation for Corporate Social Disclosures: Voluntary Disclosures vs ‘Solicited’Disclosures.” Australasian Accounting, Business and Finance Journal 3 (4): 2.

- Weber, Manuela. 2008. “The Business Case for Corporate Social Responsibility: A Company-Level Measurement Approach for CSR.” European Management Journal 26 (4): 247–261. doi: 10.1016/j.emj.2008.01.006

- World Bank. 2019. “10 Years of Green Bonds: Creating the Blueprint for Sustainability Across Capital Markets.” World Bank. March 18, 2019. https://www.worldbank.org/en/news/immersive-story/2019/03/18/10-years-of-green-bonds-creating-the-blueprint-for-sustainability-across-capital-markets.

- Zerbib, Olivier David. 2019. “The Effect of Pro-Environmental Preferences on Bond Prices: Evidence from Green Bonds.” Journal of Banking & Finance 98: 39–60. doi: 10.1016/j.jbankfin.2018.10.012